Submitted:

22 September 2023

Posted:

26 September 2023

You are already at the latest version

Preprints on COVID-19 and SARS-CoV-2

Abstract

The current global financial sector is dedicated to providing customers with more advanced and strategic services. With channels like internet banking, mobile phone banking, and telephone banking, the industry delivers multi-channel banking services to satisfy its clients. The COVID-19 pandemic has directly impacted the global economy, as well as the financial sector, with the banking sector facing lockdown initiatives to curb the virus's spread. As a result, mobile payment methods have been favored by people over physical money for transactions. This study analyzes the factors that influenced mobile banking usage during the pandemic in Sri Lanka.. Convenience sampling was used, comprising of 200 online questionnaires conducted among customers in Sri Lanka. The collected data was analyzed using descriptive analysis, exploratory factor analysis, and multiple linear regression through IBM SPSS 25. Research findings revealed that trust and risk were significant factors affecting mobile banking usage in Sri Lanka. Trust had a positive effect while Risk negatively effects to the mobile banking usage. Ease of use and Usefulness were irrelevant factors during the COVID-19 pandemic in Sri Lanka.

Keywords:

mobile banking

; COVID-19

; usefulness

; ease of use

; risk and trust

1.Introduction

Mobile banking is a convenient way to access banking and financial services on mobile telecommunication devices such as smartphones or tablets. Unlike internet banking, mobile banking uses a software, commonly known as an app to provide these services. Its primary aim is to make customers happy by enabling them to carry out transactions anywhere and at any time without the need to wait in queues (Jegatheesparan & Rajeshwaran, 2020; Kumari, 2015). According to Ayoobkhan (2018), mobile banking is an extension of internet banking. Initially, mobile banking was implemented in New York, USA, during the early 1980s, and the Bank of Scotland provided mobile banking services for the customers of Nottingham Building Society in the United Kingdom simultaneously (Jegatheesparan & Rajeshwaran, 2020). Notably, the history of mobile banking indicates that it was first developed and spread in developed countries such as the United Kingdom, the United States, Australia, and some European nations. The process evolution of mobile banking, as per Rahmani et al. (2012), is as follows:

- Introduction of GPRS technology - Late 1999 and in 2000

- Introduction of Personal Office Mobile Services

- Introduction of mobile money - in 2000

- Introduction of Third Generation Mobile - in late 2001

The inception and growth of mobile banking can be traced through various generations, starting with its first generation that provided customers with information via SMS. The second generation, known as internet banking, allowed customers to access banking services via the mobile browser. The current third generation, popularly known as the smartphone era, has brought about mobile banking applications that offer a wide range of services such as bill payments, fund transfers, account balance checks, and statement printing(Barati & Mohammadi, 2009). Mobile banking has evolved to include more advanced features like stock exchange transactions, buy and sell orders, and portfolio updates, offering a comprehensive electronic banking platform. Furthermore, self-banking or self-service banking technology has made transactions more efficient and manageable for customers. In summary, mobile banking has transformed the way customers interact with financial institutions by providing a convenient, flexible, and comprehensive platform (Manel & Dias, 2022)..

1.1. Mobile banking usage during the COVID 19 Pandemic

The existence of the world has been subject to several obstacles throughout history. Although mankind has managed to overcome various challenges, environmental pandemics caused by invisible viruses still pose a threat. An example of such a pandemic is Covid-19, caused by a strain of the SARS species known as SARS-CoV-2. The virus was initially detected in Wuhan, China, in December 2019. Despite the Chinese government's imposition of a lockdown to control the spread of the virus, it quickly spread to other regions within China and gradually to all parts of the world. Covid-19 continues to be an ongoing challenge, causing devastating effects on human health, lives, and livelihoods around the world. While vaccines and other measures have been developed to counter the pandemic, the virus continues to be a threat to global health and economic stability.

COVID-19 pandemic has being directly affecting to the global economy and financial sector. Banking is the one of key industry to achieve the performance of financial sector. The pandemic has caused uncountable issues for the worldwide people. It has led to a dramatic loss of human life and presented unprecedented challenges to global public health. As a precaution of this issue, the world practiced social distancing as the World Health Organization’s recommendations (Tang et al., 2020; WHO, 2021). Many governments lock downed their economy to minimize the spread of the virus. The banking sector is also are facing the strict lockdown initiatives implemented to decreasing the coronavirus spread. People faced liquidity and financial problems in the pandemic period as they stopped their businesses and do the transactions with the bank accounts. To help customers in lack of liquidity, many countries used the government guarantees on bank credits. On the other hand, usage of the paper and coins are declined as they considered as the major way to transform the Coronavirus in the pandemic period and people used the online payment methods instead of physical money usage for the transactions (Trong and Tran, 2021). As the results, COVID- 19 pandemic effects on banking sector aggravate use of internet based payments and digital channels. This banking feature to customers for maximizing the advantages for clients during the pandemic period. Figure 1 present the customer’s use digital applications for their transactions in 2021 and it is a progress compared to the percentage.

As people continue to practice social distancing and avoid physical contact, there has been a significant increase in the usage of internet-based payments and digital channels. To adapt to this changing landscape, banks have expanded their online services, enabling customers to access banking facilities easily. Additionally, governments have introduced initiatives to support their citizens by providing government guarantees on bank credits, aimed at helping those who have been adversely affected by the pandemic. Despite the challenges presented by the Covid-19 pandemic, the banking sector has shown remarkable resilience and adaptability by providing better and more efficient banking services to customers. As the world continues to battle the pandemic, reliance on digital banking is likely to continue to grow as it offers both customers and financial institutions a safe, convenient, and cost-effective way of conducting financial transactions. Table 1 illustrates the growing trend of using digital applications for transactions in the year 2021.

According to Table 1, there has been significant progress in the adoption of digital applications for financial transactions, with 64.1% of the population using digital payments in 2021, compared to 55% in 2017. Interestingly, the percentage of the population making digital payments was higher than the percentage receiving them. This demonstrates a growing preference among consumers for online payment platforms. Another noteworthy finding is that 27% of people made digital utility payments during the Covid-19 pandemic, suggesting a greater willingness to use digital platforms during times of crisis. As customers continue to rely on digital banking, financial institutions must continue to innovate and improve their services to meet customer demands. Ultimately, the pandemic has highlighted the importance of digital banking and has accelerated its adoption, providing a safer and more efficient way of conducting financial transactions.

1.2. Usage of mobile banking in Sri Lanka during the COVID 19

In Sri Lanka, the Covid-19 pandemic has had a significant impact on the banking sector, causing disruptions to customers' interactions with banks due to movements restrictions and lockdowns. To adapt to these challenges, many banks and customers in Sri Lanka have embraced digitalization procedures to improve their services. Mobile banking applications have become increasingly important during the pandemic, with banks actively encouraging their clients to use digital platforms for their banking activities to ensure social distancing practices and minimize the risk of infection (Yapabandara & Nagendrakumar, 2022). As a result, the usage of mobile banking in Sri Lanka has increased significantly, offering an alternative to in-person visits to the bank and making banking services more accessible to customers, even during times of crisis. This increased adoption of digital banking is likely to continue beyond the pandemic, with mobile banking becoming an essential tool for banking services in Sri Lanka.

Table 2 shows that the usage of digital payment applications varies by income groups, with 38.3% of people in the lower-middle-income category using digital payment applications in 2021. However, an encouraging sign is that a significant proportion of Sri Lankans have started using digital payment applications for the first time during the pandemic, particularly for utility payments. 20.3% of the population made utility payments digitally for the first time during the pandemic, higher than the population who usually make digital utility payments. Similarly, 7.1% of people in the lower-middle-income category in Sri Lanka also made utility payments using digital platforms during the pandemic, showing an expanded reach of digital payments among low-income households. This highlights that Sri Lankan people are increasingly aware of the convenience and safety of using digital payment applications.

Overall, the adoption of digital payments in Sri Lanka has increased significantly during the Covid-19 pandemic, and the trend is expected to continue. As more and more people seek to conduct their financial transactions remotely, banks need to continue to improve their digital offerings and make mobile banking more accessible and user-friendly, especially for the low-income category.

Despite the growing popularity of mobile banking, previous research indicates that a considerable proportion of Sri Lankans still rely on traditional banking methods, even though they have internet access and are aware of mobile banking platforms. According to Hettiarachchi (n.d.), most Sri Lankans do not utilize mobile banking, including educated individuals, who remain hesitant and prefer traditional methods such as visiting the bank branch for transactions. The research by Manel and Dias (2022) found that ATM is the most popular self-banking platform in Sri Lanka, with less than 1% of customers typically using mobile banking or other payment gateways. This suggests a continued preference for traditional methods, even though Sri Lanka has high levels of technological literacy. Despite being among the most technologically literate populations globally, Sri Lankan people's behavioral intention to use mobile banking remains in the primitive stage. Therefore, identifying the factors that hinder mobile banking adoption in Sri Lanka is crucial. Banks are increasingly offering mobile banking services accessible on mobile telephones, but its adoption remains limited due to various reasons.

Given that a substantial proportion of the Sri Lankan population still relies on traditional banking methods, it is crucial to identify the factors influencing low adoption of mobile banking, including barriers such as lack of awareness, concerns over security, and lack of trust in mobile banking. Addressing these barriers would be crucial to increasing mobile banking adoption in Sri Lanka. Increasing education and awareness about the benefits of mobile banking and offering incentives or rewards for using mobile banking platforms are among the strategies that financial institutions can adopt to encourage more Sri Lankans to adopt mobile banking.

Previous research has highlighted that there are challenges that hinder the wider adoption of mobile banking in Sri Lanka (Ferando, K. A., & Kumari, J. P. (2022). This includes the fact that the mobile banking market remains relatively small when compared to the overall banking customer base and traditional banking transactions. As a result, both supply and demand for mobile banking services have not been fully realized. Furthermore, there is a lack of research that specifically explores the factors that influence mobile banking usage during the Covid-19 pandemic in Sri Lanka. Thus, this study aims to fill this research gap by investigating the factors that affect mobile banking adoption during the pandemic within Sri Lanka. The study's findings can shed new light on the challenges that inhibit wider mobile banking adoption and can guide financial institutions and policymakers in developing more effective strategies for promoting mobile banking. The study aimed to identify;

- The factors that affect the mobile banking usage during the Covid – 19 pandemic in Sri Lanka.

- The nature and impact of these factors on the mobile banking usage in Sri Lanka during the Covid -19 pandemic.

2. Theoretical background of the study

The banking industry's performance has seen significant growth with the increased usage of technology in recent years. It is one of the most innovative industries, consistently adopting new technologies to provide efficient and advanced services to customers. Extensive literature explores the innovation of the banking industry and the advantages and opportunities it presents, with many researchers using models to identify customer behavior and technological acceptance. Among the most cited models are the Theory of Planned Behavior (TPB), Technology Acceptance Model (TAM), and Unified Theory of Acceptance and Use of Technology (UTAUT), which are often used to explain how customers adopt IT-based services in the banking industry. These models have demonstrated the industry's ability to stay ahead in an ever-changing digital landscape and will continue to shape customer behavior and banking services in the future.

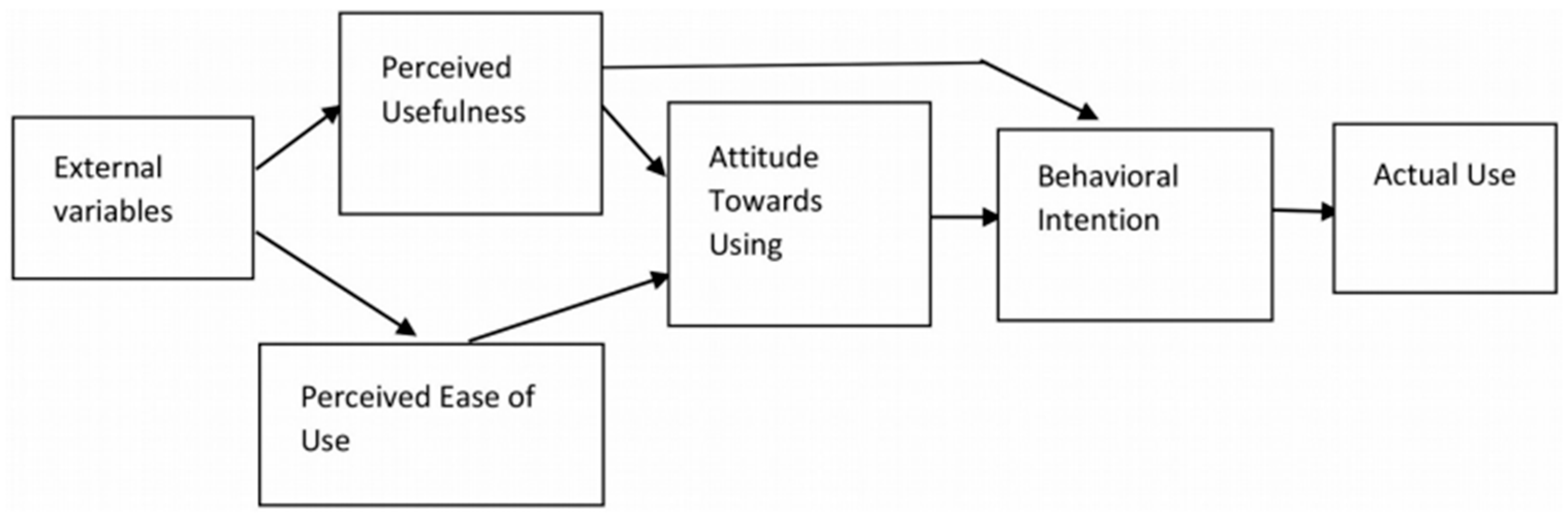

2.1. Technology Acceptance Model (TAM)

Technology Acceptance Model (TAM), it is one of the most widely-used models to examine the acceptance of technology in different IT-based services worldwide. TAM explains two primary factors that affect an individual's intention to use technological innovations: perceived ease of use and perceived usefulness. TAM aims to establish a relationship between users and a product and how users are influenced by it. It has been used extensively when considering the behavioral intention to use mobile banking applications. TAM explains why users may accept or reject information technology and provides insights into customer adoption behavior. Perceived ease of use, trust, and perceived usefulness beliefs are the two sets of TAM that determine behavioral intention to use technology, as reported by Jegatheesparan and Rajeshwaran, 2020. These factors have been recognized as important elements that explain technology acceptance, especially in the banking industry.

In summary, the Technology Acceptance Model has been valuable in identifying essential factors that influence technology adoption and has contributed to the understanding of customer behavior. As the banking industry continues to evolve and innovate with technology, models like TAM will play a critical role in shaping customer behavior and banking services in the future.

Figure 1.

Technology Acceptance Model (TAM). Source: Amadu, Muhammad, Mohammed, Owusu & Lukman (2018).

Figure 1.

Technology Acceptance Model (TAM). Source: Amadu, Muhammad, Mohammed, Owusu & Lukman (2018).

TAM is based on the idea that people's perceptions of the usefulness and ease of use of a technology, as well as their perceptions of the trustworthiness and riskiness of the technology, influence their intention to use the technology. The model includes the following components:

- Perceived usefulness: the degree to which a person believes that using a technology will enhance their job performance or make their lives easier.

- Perceived ease of use: the degree to which a person believes that using a technology will be effortless and straightforward.

- Attitude towards using: the degree to which a person has a positive or negative evaluation of using the technology.

- Behavioral intention: the degree to which a person intends or plans to use the technology.

- Actual use: the degree to which a person uses the technology in practice.

TAM also includes the concepts of perceived risk and trust, which can influence the adoption of a technology. Perceived risk refers to the degree to which a person believes that using a technology may have negative consequences, such as financial loss or damage to reputation. Trust refers to the degree to which a person believes that the technology provider or developer is honest, reliable, and competent. Overall, TAM is a model that acknowledges the importance of trust and risk perceptions in shaping people's adoption behavior towards technology.

2.2. Empirical review of the study

According to the research done by Lakshika and Sajeewanie in 2019, they focused on examining the factors influencing customers' behavioral intention to use mobile banking applications in Sri Lanka. They investigated four antecedents, namely perceived risk, trust, convenience, and relative advantage to identify why most consumers do not use this innovative service. The study found that perceived risk, trust, convenience, and relative advantage all have a positive relationship with users' behavioral intention to use mobile banking applications. Users who perceive mobile banking as more convenient and advantageous are more likely to adopt it. Furthermore, users who perceive the mobile banking application as trustworthy and having less perceived risk related to security and privacy concerns are more likely to use it. In conclusion, their research emphasized that banks should focus on eliminating potential risks related to security and privacy, creating trust among customers, and making mobile banking applications more user-friendly and convenient. By doing so, banks can increase the acceptance and usage of mobile banking applications, ultimately leading to more satisfied customers and an increase in market share.

Moving on to the research done by Perera and Gunaratna , 2020, they investigated the impact of five service quality dimensions, namely tangibility, reliability, responsiveness, assurance, and empathy, on customer satisfaction with mobile banking. They used customer loyalty as the dependent variable, and customer satisfaction on mobile banking as the independent variable. The study employed several statistical techniques such as frequency statistics, descriptive statistics, Pearson correlation, regression model, and ANOVA to analyze the collected data. The results showed that all the mobile banking service quality attributes positively relate to customer satisfaction. Meaning, the better the service quality dimensions are in mobile banking, the more satisfied the customers will be, and the more likely they will remain loyal to their bank. Their research highlights the importance of ensuring high levels of service quality, including tangibility, reliability, responsiveness, assurance, and empathy to increase customer satisfaction and loyalty towards mobile banking. By improving service quality, banks can provide a desirable mobile banking experience to their customers, ultimately leading to better business growth in the long term.

In the research study of Ayoobkhan in 2018, the author aimed to examine the factors influencing mobile banking adoption in the context of Sri Lanka. Self-administered questionnaires were distributed among respondents of Sampath banks in Ampara district, and data were analyzed using descriptive analysis, correlation analysis, and regression analysis.

The study found that perceived usefulness, perceived ease of use, cost, trust, and perceived risk are significant factors influencing the adoption of mobile banking. The study revealed that respondents perceive mobile banking as more useful and easy to use, leading to increased adoption. Additionally, the lower the perceived cost and perceived risk, and the higher the trust in mobile banking, the more likely the customers will adopt it.

The findings of this study provide important insights for banks to promote the adoption of mobile banking in Sri Lanka. By enhancing the usefulness and ease of use of mobile banking applications, providing affordable and secure mobile banking services, and building trust among customers, banks can facilitate the adoption of mobile banking and improve their customer base. Ultimately, the adoption of mobile banking will lead to better customer service, increased efficiency, and sustainable growth for the banks.

Harshana and Wanniarachchige (2022) investigated the effect of the Covid-19 pandemic on the performance of Sri Lankan banks. The study included 18 licensed commercial banks, and data were collected for the year 2020. The authors used various statistical techniques, including correlation analysis, regression analysis, and t-tests to analyze the data. The results indicated that the Covid-19 pandemic has had a statistically significant adverse effect on bank performance in Sri Lanka. The financial performance of banks was negatively affected due to the economic slowdown caused by the pandemic. Moreover, the study found that the net interest margin, return on assets, and return on equity of banks were adversely impacted due to the pandemic. The research highlights the importance of banks being resilient during times of crisis. Banks need to adopt proactive measures to mitigate the impacts of external shocks like the Covid-19 pandemic on their performance. The study provides insights for banks to adopt appropriate risk management strategies, enhance their digital capabilities, and improve their funding structure to minimize the impact of crises on their operations. By doing so, banks can maintain their financial stability and meet the changing needs of their customers during uncertain times.

Yapabandara and Nagendrakumar (2022) have conducted a study to determine the impact of the Covid-19 pandemic on the adoption of mobile banking in Sri Lanka. Using a stratified random sample from three districts, the study found that computer and internet literacy, perceived usefulness, and awareness were the most significant factors influencing online banking adoption. The results highlight the importance of improving digital literacy among customers and creating awareness of the benefits of mobile banking.

Jayarathne et al., (2022) examined the motives behind mobile payment adoption among customers and retailers in Sri Lanka during the pandemic. Their findings indicate that Performance expectancy and facilitating conditions are common motives, while Hedonic motivation and perceived technology security differ across urban and rural areas. The study underscores the need for banks to understand the unique needs of customers in different regions and tailor their offerings accordingly.

In conclusion, these studies shed light on various aspects of banking in Sri Lanka, including the adoption of mobile banking, factors influencing adoption, and the impact of the Covid-19 pandemic on bank performance

2.3. Variables for the Study

- Ease of use

Ease of use is a very important factor, a customer considering when he purchase a product. A product should be easy to use to enhance the customer satisfaction. Ease of use is the most important factor for accept electronic banking (Upadhyay et al., 2017). And it will affect to attract the demand of the customers. Perceived ease of use refers that the degree in which a customer believes that using a particular system would be free of charge (Lakshika & Sanjeewanie, 2019). There are several determinants of the perceived ease of use as computer anxiety, perceived enjoyment, perception of external control and computer self-efficacy (Manel & Dias, 2022). In mobile banking ease of use directly affects to the acceptance of an information system. When compare the mobile banking with ATM transactions, mobile banking can easily use to do transactions and banking activities. Kahandawa and Wijenayake (2014) suggested that, there will be a positive impact and increase the satisfaction of the user, when he/she finds that the system is easy to use.

- 2.

- Usefulness

Usefulness means the degree which a person believes that the using of particular system or technology increase his job performance (Wijesooriya & Sritharan, 2018). In their study Ravichandran and Madana (2016) also have proved it by mentioning that perceived usefulness is strongly connected with productivity. Because, in a workplace when employers use computers, it cause to improve their job performance, increase job effectiveness. There are several determinants of the perceived usefulness as image, output quality, job relevance and subjective norm (Manel & Dias, 2022). Moreover usefulness is a vital factor in Technology Acceptance Model (TAM) (Jagatheesparan & Rajeshwaran, 2020; Ayoobkhan, 2018; Wijesooriya & Sritharan, 2018; Ravichandran & Madana, 2016). If mobile banking is useful for someone he will motivate to use mobile banking very frequently and at the same time his satisfaction level also will increase.

- 3.

- Risk

When a customer tries a new product the risk is always combined with it. On the service providers or suppliers side they also take a higher risk by offering the product or service as they deal with the customer’s satisfaction. 73.5% of mobile banking users expressed their concerns about the security of the mobile banking (Huili & Chunfang, 2011). As emphasized by Lakshika and Sanjeewanie (2019) perceived risk can be classified into five categories as security risk, performance risk, social risk, financial risk and time risk. Security risk refers the all the losses happen due to the frauds or hackers activities. When it comes to the mobile banking, security is a more concerning factor (Jegatheesparan & Rajeshwaran, 2020). Performance risk will arise due to the malfunctions of the mobile banking platforms. All the losses arise when using the mobile banking include in social risk. Financial risk arise due to the misuse of bank account and transaction errors. Time risk indicates the all the losses of time.

- 4.

- Trust

The base for the success of a system is the customers’ trust. As mentioned by Ayoobkhan (2018) studies which investigate about the factors which affect to adopt and accept technology based services have identified trust as a key factor. Trust can be defined as the perception of the degree to which an exchange partner fulfil the consumer’s transactional obligations in the situations which are characterized as risk or uncertainty (Wijesooriya & Sritharan, 2018). Customer trust in mobile banking can be operationalized as the accumulation of customer beliefs about integrity, kindness, and ability, which can improve the customer's willingness to rely on mobile banking to obtain financial transactions (Alalwan et al., 2017).

3. Research Methodology

This study adopted a quantitative approach to analyze and draw insights. Quantitative techniques provide a systematic means for making data-driven decisions and conducting powerful analyses. Both primary and secondary data were used in the study. A questionnaire was designed using Google Docs and distributed via email using convenience sampling. The questionnaire consisted of Likert Scale items with anchors ranging from 1 to 5 for each variable. The study examined the measurement model to test reliability and validity. Descriptive and correlation analyses were conducted, followed by multiple linear regression analysis to test the research hypotheses and model. The collected data were analyzed using the IBM SPSS 25 software.

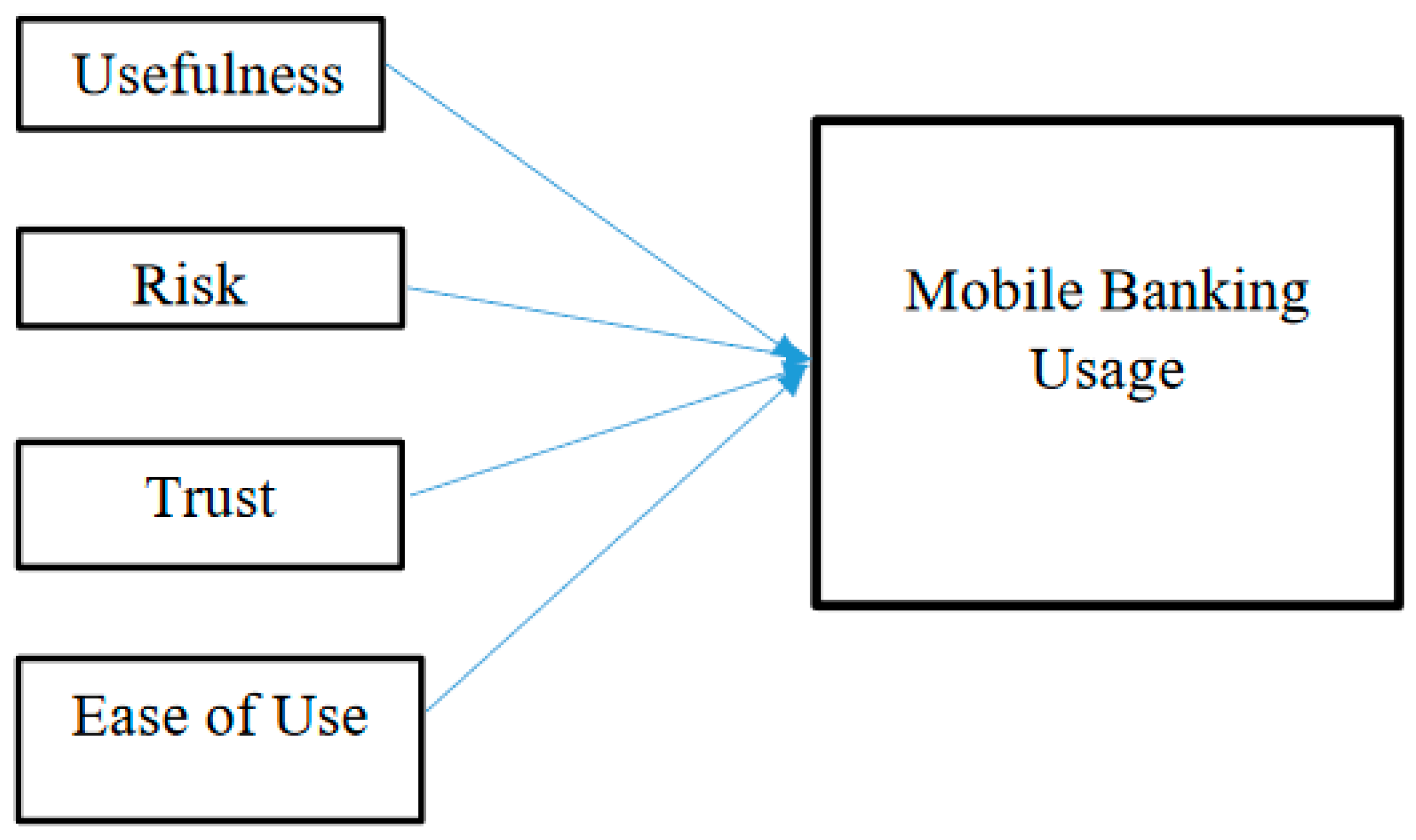

3.1. Conceptual Framework and research hypothesis of the Study

The conceptual framework for this research is grounded in the Technology Acceptance Model (TAM). The main independent variables in the study are perceived usefulness, perceived risk, trust, and ease of use. While ease of use and perceived usefulness are precursors of TAM, perceived risk and trust have been taken from the attitudes which degree to which a person has a positive or negative evaluation of using the technology.. The dependent variable in this study is mobile banking usage, and it is hypothesized to have a direct effect on it. The study proposes four hypotheses to further examine this relationship and provide valuable insights that can help improve the adoption and use of mobile banking in Sri Lanka. This study provides a comprehensive view of the factors that influence mobile banking usage in the country.

Figure 2.

Conceptual Framework of the Study. Source: Research data, 2023.

Hypothesis one (H1):

One of the critical variables in this study is perceived usefulness, which refers to the extent to which a person believes that using a particular system or technology increases job performance (Wijesooriya & Sritharan, 2018). If customers perceive mobile banking as useful, they will be motivated to use it, ultimately leading to an increase in mobile banking usage. Therefore, it is hypothesized that perceived usefulness has a positive and significant effect on mobile banking usage. By identifying the factors that affect users' perceptions of mobile banking's usefulness, banks can develop appropriate strategies to enhance customer perceptions and motivate them to adopt mobile banking services.

H1: A usefulness of mobile banking platforms could have a positive impact on the mobile banking usage.

Hypothesis two (H2):

Security concerns associated with mobile banking have become a major obstacle to its adoption in Sri Lanka (Jegatheesparan & Rajeshwaran, 2020). With the increasing number of cybercrimes and online frauds, customers are hesitant to use mobile banking services, fearing that their personal and financial information could be compromised. Therefore, it is hypothesized that perceived risk has a negative and significant effect on mobile banking usage. By identifying the factors that contribute to customers' risk perceptions, banks can take appropriate measures to mitigate these risks and enhance customers' trust in mobile banking services. This could lead to increased adoption and usage of mobile banking services in Sri Lanka while addressing the security concerns of customers

H2: A higher level of risk in mobile banking platforms could have a negative impact on the mobile banking usage.

Hypothesis Three (H3):

It can be defined as the degree to which a customer has confidence and reliance on their mobile banking service provider (Wijesooriya & Sritharan, 2018). As mobile banking involves personal and sensitive information, customers highly prioritize security and data protection. Hence, it can be hypothesized that building trust has a positive and significant effect on mobile banking usage. Providing secure and reliable services, respecting customers' privacy, and establishing a positive reputation can help financial institutions gain customers' trust. By doing so, mobile banking services can become more widely adopted, thus providing financial inclusion and furthering Sri Lanka's digital transformation.

H3: trust of mobile banking will make a positive impact on the mobile banking usage.

Hypothesis four (H4):

Ease of use is a critical component of mobile banking services that financial institutions must prioritize. Research indicates that the degree to which customers believe that using a particular system is free of charge significantly influences their willingness to accept electronic banking. Studies have also suggested that there is a positive impact on user satisfaction when a system is easy to use. Therefore, it can be hypothesized that creating user-friendly and intuitive mobile banking applications can significantly influence the success of mobile banking services in Sri Lanka. Financial institutions must continually strive to enhance the ease of accessibility and convenience of their mobile banking services to attract more customers and drive adoption in Sri Lanka's increasingly digitized economy.

H4: ease of use in the mobile banking will make a positive impact on the mobile banking usage.

3.2. Demographic profile of the respondents

This section gives an overview of demographic characteristics and personal information of the respondents.

Table 3.

Demographic profile of the respondents.

| Description | Frequency | Percentage |

|---|---|---|

| Gender | ||

| Male | 93 | 54% |

| Female | 107 | 46% |

| Age | ||

| Below 20 | 8 | 4% |

| 21 – 30 | 150 | 75% |

| 31 – 40 | 28 | 14% |

| 41 – 50 | 8 | 4% |

| 51 – 60 | 6 | 3% |

| Education Level | ||

| G.C.E Ordinary Level | 7 | 3% |

| G.C.E. Advanced Level | 60 | 30% |

| Higher Diploma | 21 | 11% |

| Undergraduate Degree | 98 | 49% |

| Master’s Degree | 12 | 6% |

| PHD or higher | 2 | 1% |

Figure 7 – Source: Survey data (2023).

The study surveyed 200 respondents, out of which 54% were female and 46% were male. Although both genders were represented, a higher percentage of females were included in the sample. The majority of the respondents (75%) were between the ages of 21-30, with only 3% of respondents being 51-60 years old. This implies that people above 50 years may be less inclined to use mobile banking for their day-to-day financial activities. In terms of education, 49% of respondents held an undergraduate degree, while 30% had only completed their Advanced Levels. Only 6% of the respondents had a Master's degree, while a mere 1% held a PhD or higher. These findings suggest that financial institutions could target younger customers who are more tech-savvy, while also ensuring that the mobile banking app is easy to use for customers with lower levels of education and digital literacy.

4. Data analysis and Discussion

4.1. Reliability Analysis

In terms of data analysis, the reliability of data is an essential aspect that determines the accuracy and usefulness of findings. Although the Cronbach's alpha coefficients were used to assess the internal consistency of the scale scores, the reliability analysis was unable to determine the consistency of the total scores for each scale. This underscores the importance of ensuring the reliability of collected data through rigorous testing procedures. Typically, a Cronbach's alpha value of 0.7 is considered standard for reliability, and higher scores indicate greater consistency. Notably, all the dimensions displayed high reliability scores of greater than 0.7, indicating consistency among participants' responses to the questionnaire. In conclusion, the high reliability of collected data suggests that the findings of this study are reliable and can be used effectively for further analysis

Table 4.

Reliability analysis.

| Variable | Cronbach’s Alpha | No. of Items |

|---|---|---|

| Usefulness | 0.939 | 4 |

| Ease of Use | 0.927 | 4 |

| Trust | 0.832 | 3 |

| Risk | 0.962 | 4 |

| Mobile Banking Usage | 0.889 | 4 |

Source: Survey data, 2023.

4.2. Factor Analysis

Factor analysis is a useful statistical technique that can be used to identify the most critical factors affecting the use of mobile banking. To determine the suitability of factor analysis, the Kaiser-Meyer-Olkin value (KMO) and Bartlett’s test are considered. The KMO measures the sampling adequacy for the analysis, with values ranging from 0 to 1. According to research by Islam et al. (2019), a KMO value of 0.7 or above is considered good, while values between 0.5 and 0.7 are considered mediocre. Additionally, Kweyu and Ngare (2013) reported that KMO values above 0.9 are considered excellent. Therefore, a high KMO value indicates that the sample is suitable for factor analysis, and the results obtained are trustworthy and accurate. By using factor analysis in this study, we can identify the key factors that impact the use of mobile banking services in Sri Lanka. Table 5 present the factor analysis of the study.

The results of the KMO and Bartlett’s test presented in Table 5 indicate that all five variables, including the independent variables of usefulness, ease of use, trust, risk, and the dependent variable of mobile banking usage, are suitable for factor analysis. Specifically, all KMO values are higher than 0.6, which is considered adequate for the analysis. This suggests that the sample size is sufficiently large, and the selected variables are suitable for factor analysis. Additionally, the Bartlett’s test results indicate significant interrelationships between all five variables with a p-value of 0.000, which is below the alpha value of 0.05. The high internal validity of the variables indicates that they are related and can be analyzed effectively using factor analysis. Therefore, we can conclude that the collected data is suitable for factor analysis, and the results obtained can be used to inform decision-making in the banking industry in Sri Lanka.

4.3. Regression Analysis

In this study, multiple regression analysis was conducted to test the proposed hypotheses and identify the factors that significantly affect mobile banking usage. The regression analysis examines the relationships between the dependent variable, mobile banking usage, and the independent variables, including usefulness, ease of use, trust, and risk. The analysis involves finding the best-fit line that explains how the independent variables affect the dependent variable.. The results of the analysis identify the factors with the strongest impact on mobile banking usage, which can guide decision-making in the banking industry towards improving customer adoption and satisfaction with mobile banking services.

Table 6 indicates that the p-value of usefulness is higher than the accepted significant level of 0.05, and the coefficient value is -0.172. These findings suggest that usefulness does not significantly impact mobile banking usage in the Sri Lanka during Covid-19. In other words, mobile banking usage does not depend on its perceived usefulness, and therefore there is an insignificant relationship between usefulness and mobile banking usage. Consequently, usefulness is not identified as one of the significant factors contributing to the adoption and usage of mobile banking services in Sri Lanka during Covid-19. However, further research is needed to explore factors that may impact mobile banking usage in this context.

The p-value of Risk is lower than the 0.05 significant level, and the coefficient value is -0.220, indicating a significant and negative correlation between Risk and Mobile Banking Usage. This suggests that mobile banking users in Sri Lanka are aware that the level of risk associated with mobile banking platforms could impact their usage. However, it is also worth noting that these users do not consider transactions through mobile banking platforms to be risky. Overall, these findings emphasize the importance of addressing risk and security concerns to further promote the adoption of mobile banking services in the region..

In addition, the p-value of Trust is lower than the 0.05 significant level, and the coefficient value is 0.332, indicating a significant and positive correlation between Trust and Mobile Banking Usage. This implies that mobile banking users in Sri Lanka perceive their service providers as trustworthy, and this factor is one of the main drivers that attract them to use mobile banking services. Therefore, financial institutions should focus on building trust with their customers by providing transparent and reliable services to further promote the uptake and usage of mobile banking services. By doing so, financial institutions can improve customer loyalty and satisfaction while also expanding their customer base.

Regarding Ease of Use, it is worth noting that the p-value is higher than 0.05 significant level, and the coefficient value is -0.049, which suggests that Ease of Use does not have a significant impact on Mobile Banking Usage in the context of Sri Lanka . Mobile banking users do not consider the ease of use as a critical factor in their decision-making process when it comes to using mobile banking services. Although convenience is always a desirable factor, it seems that other factors such as trust and security play a more critical role in this scenario. Hence, it is imperative to focus more on improving these factors to increase the adoption and usage of mobile banking in the region.

4.5. Multiple Regression Analysis to Explain the Model Fitting

Table 7 presents the model fitting of the study, indicating that the Correlation (R) coefficient value is 0.645, indicating a positive relationship between the dependent variable (Mobile Banking Usage) and the independent variables (Usefulness, Ease of Use, Trust, and Risk). The Coefficient of Determination (R2) is 0.416, meaning that 41% of the variation in Mobile Banking Usage is explained by the independent variables. However, the remaining 59% of the variation in Mobile Banking Usage is due to other factors that are not covered in this study. Therefore, the model is not entirely accurate, and researchers should conduct further investigations to identify other variables that have an impact on Mobile Banking Usage. Overall, the study provides valuable insights into the factors influencing the adoption and usage of mobile banking services in Sri Lanka.

4.6. ANOVA in Multiple Regression Analysis

Table 8 provides an overall assessment of the conceptual model used in the study. The F-value of 32.548 indicates that the model is significant, and at least one of the independent variables can be used to predict Mobile Banking Usage in Sri Lanka. The p-value of 0.000 is less than the significance level of 0.05, providing further evidence that the model is accurate and reliable in predicting Mobile Banking Usage. As a result, financial institutions and other stakeholders can use these findings to understand and address the factors affecting Mobile Banking Usage in the region. By addressing these factors, institutions can improve adoption rates, promote financial inclusion, and support a shift towards a cashless society. Therefore, these results are of great importance and highlight the need for continued research and analysis of mobile banking services to support financial growth and development in the region.

4.7. Discussion

The study had a main objective of determining the factors influencing Mobile Banking Usage in Sri Lanka during the Covid-19 pandemic. The findings of the study revealed that both Risk and Trust factors are significant in influencing Mobile Banking Usage in Sri Lanka. Trust had a strong influence on the usage of Mobile Banking, as demonstrated by the p-value of less than 0.05, which indicated a significant relationship between trust and Mobile Banking Usage. Similarly, the p-value of Risk was also less than 0.05, indicating a strong relationship between the two variables. These findings indicate that financial institutions need to prioritize building trust and reducing risk when promoting mobile banking services to their customers. By doing so, they can improve the adoption of Mobile Banking services and optimize the benefits of digital financial services. Overall, these results provide valuable insights into the factors that influence the adoption of Mobile Banking services in Sri Lanka

Moreover, the findings of this study are consistent with other studies conducted in Sri Lanka on Mobile Banking adoption. Ayoobkhan (2018) study on Mobile Banking adoption in Sri Lanka concluded that Trust is a critical factor in the adoption and use of Mobile Banking services, further corroborating this study's results. Likewise, Wijesooriya and Sritharan, (2018) study found that Trust was an essential factor in influencing the adoption of financial technology systems like Mobile Banking. Additionally, the study conducted by Ravichandran and Madana (2016) on factors influencing mobile banking adoption in the Kurunegala district found that Risk had a negative impact on mobile banking adoption rates. Finally, Kahandawa and Wijenayake, (2014) study on the impact of mobile banking services on customer satisfaction in Sri Lankan State Commercial Banks revealed that customers' perceptions of risk negatively affect satisfaction with mobile banking services. Taken together, these studies' results suggest that Trust and Risk are essential factors that influence the adoption and usage of Mobile Banking services in Sri Lanka and highlight the importance of addressing these factors to enhance the appeal and effectiveness of mobile banking services.

However, the study's findings also indicate that Ease of Use and Usefulness were not significant factors influencing the usage of mobile banking in Sri Lanka. These findings contrast with previous research studies, where Ease of Use and Usefulness were found to be essential factors in determining mobile banking usage. The reason for this discrepancy could be attributed to the fact that the significant values were higher than the 0.05 significant level. Nonetheless, these results align with the findings of other studies in Saudi Arabia, where Jabri (2015) reported that perceived usefulness did not affect the intention to use Mobile Banking services. Nevertheless, the respondents had difficulty evaluating the usefulness of Mobile Banking, perceiving it as no different from other channels like ATMs, telephone banking, or internet banking. These results are also consistent with the findings of Sumargo et al, (2021) study, which reported a negative and insignificant correlation between the perceived Ease of Use and the intention to use mobile banking services. Overall, these results underscore the complex nature of digital financial services adoption, calling for more research and analysis to identify and address the factors that influence their adoption and usage.

Furthermore, the study's findings imply that financial institutions in Sri Lanka must prioritize building consumer trust in Mobile Banking platforms as a strategy to increase its usage. Trust was identified as the most critical variable influencing mobile banking usage among consumers during the Covid-19 pandemic. Moreover, the study suggests that financial institutions can increase customers' trust by offering specific guarantees such as ensuring the security of technological infrastructure, confidentiality, and maintaining a good reputation. These factors are essential to building and maintaining customer confidence in Mobile Banking services. These findings are consistent with Alalwan et al, (2017) study, which found that trust had a significant positive impact on mobile banking adoption among Jordanian bank customers. Hence, building consumer trust in Mobile Banking platforms is critical to increase its usage and achieve the benefits of digital financial services.

On the other hand, Risk was identified as a significant factor that can discourage Mobile Banking usage in Sri Lanka. The multiple regression analysis revealed a negative relationship between Risk and Mobile Banking usage during the Covid-19 period. This implies that the risks associated with Mobile Banking platforms could raise users' insecurities and have a detrimental impact on its usage. Therefore, addressing users' concerns regarding the potential risks of using Mobile Banking platforms is necessary to encourage their adoption. Financial institutions can combat this issue by implementing robust measures to protect users' data and transactions and providing clear and concise information regarding the risk management practices utilized in their mobile banking platforms. In conclusion, addressing the issue of risk in Mobile Banking services is crucial to increase users' trust and adoption, and financial institutions must prioritize this factor to promote their digital financial services effectively.

The study's findings may also suggest that respondents have a high level of familiarity with traditional electronic banking services such as ATMs and CDMs, resulting in their perception of these services as more useful and easier to use than Mobile Banking services. Despite the convenience that Mobile Banking services can provide, respondents may feel more comfortable with ATMs, CDMs, and face-to-face banking activities due to their long-standing usage. Addressing this perception requires financial institutions to educate their customers on the benefits of using Mobile Banking services, emphasizing its unique advantages for modern financial transactions. By doing so, customers can gain a more comprehensive understanding of Mobile Banking's capabilities and contribute to increasing its acceptance and adoption rates. These results highlight the need for banks to continuously monitor the market and adjust their strategies to stay ahead of the competition and meet consumers' changing expectations.

5. Implications of the study

The results of this study hold significant importance for commercial banks that offer mobile banking services. Key decision-makers such as bank managers, directors, IT solution providers, web developers, software engineers and marketing managers can gain valuable insights into the best practices for implementing online banking services. They can also leverage the findings to design effective mobile banking apps and websites that cater to their customers' needs. The study sheds light on the most significant factors that impact the adoption of mobile banking, highlighting Trust and Risk as critical factors that need to be considered while developing and upgrading mobile banking applications. This study thus offers valuable guidance that can help banking systems improve their mobile banking services and deliver an optimal customer experience.

The survey results revealed that respondents found difficulties in using mobile banking platforms and did not consider them easy to use. One of the reasons for this could be the language barrier and technological barriers. In this context, service providers can introduce local languages on mobile banking applications and also introduce voice-based service support. These solutions would be effective in boosting the usage and usefulness of mobile banking. To increase the relative advantage of mobile banking applications compared to conventional platforms, banks should focus on making their mobile banking applications more user-friendly. Therefore, banks must strive to improve the user interface of their mobile banking applications to make them more intuitive and straightforward, enhancing customer experience and satisfaction. By heeding these suggestions, banks can improve their mobile banking services and increase customer trust and loyalty.

The study has identified that risk and trust play a significant role in determining the adoption of mobile banking services. Therefore, service providers should prioritize enhancing the security of their mobile banking applications. They can do this by introducing verification codes and high-security passwords, which will help to build customer trust and confidence. Additionally, app developers and web developers should create mobile banking apps with minimal risk and optimal performance, ensuring that customers have a seamless experience while using the service. To attract more customers, especially those from rural areas and the elder population, perfect marketing campaigns should be launched, highlighting the benefits and convenience of mobile banking services. By implementing these strategies, the service providers can increase customer confidence in their mobile banking applications, leading to a significant increase in usage and adoption rates.

6. Conclusions

The results of the study have shown that Trust and Risk are the most influential factors in determining the adoption of mobile banking services. A positive relationship was found between Trust and the usage of mobile banking, while a negative relationship was observed between Risk and the usage of mobile banking. Interestingly, Usefulness and Ease of Use were found to be less significant factors in determining the adoption of mobile banking services. The main objectives of the study were thus achieved. These findings indicate that in the unprecedented times of the Covid-19 pandemic, people placed paramount importance on the security of their transactions. The financial woes faced by many people during this period placed a higher emphasis on the need for trust in mobile banking applications, rather than their ease of use or usefulness. Thus, service providers need to focus more on improving the security features of their mobile banking applications to increase their acceptance rates amongst users.

References

- Alalwan, A., Dwivedi, Y. K., & Rana, N. P. (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, 37(3), 99–110. [CrossRef]

- Amadu, L., Muhammad, S. S., Mohammed, A. S., Owusu, G., & Lukman, S. (2018). Using technology acceptance model to measure the use of social media for collaborative learning in Gahana. Journal of Technology and Science Education, 8(4), 321–336. [CrossRef]

- Ayoobkhan, A. (2018). Factors contributing to the adoption of mobile banking in Sri Lanka: Special reference to Sampath Bank in Ampara District. International Journal of Latest Engineering and Management Research, 3(8), 47–57.

- Barati, S., & Mohammadi, S. (2009). An efficient model to improve customer acceptance of mobile banking. World Congress on Engineering and Computer Science.

- Fernando, K. A., & Kumari, J. P. (2022). Customer satisfaction on usage of mobile banking services in Sri lanka. Asian journal of advances in research, 234-248.

- Harshana, K. R. K., & Wanniarachchige, M. K. (2022). Effect of Covid-19 pandemic on the performance of the Sri Lankan banks. International Journal of Accounting & Business Finance , 8(2), 135–156. [CrossRef]

- Hettiarachchi, H. A. H. (2013). Factors affecting to customer adoption of internet banking.

- Huili, Y., & Chunfang, Z. (2009). The analysis of influencing factors and promotion strategy for the use of mobile banking. Canadian Social Science, 7(2), 60–63.

- Jabri, l.M. (2015). The intention to use mobile banking: Further evidence from Saudi Arabia. S.Afr.J.Bus.Manage, 46(1), 23–34. [CrossRef]

- Jayarathne, P. G. S. A., Chathuranga, B. T. K., Dewasiri, N. J., & Rana, S. (2022). Motives of mobile payment adoption during COVID-19 pandemic in Sri Lanka: a holistic approach of both customers’ and retailers’ perspectives. South Asian Journal of Marketing, 4(1), 51–73. [CrossRef]

- Jegatheesparan, K., & Rajeshwaran, N. (2020). Factors influencing on customer usage of online banking: From the perspective of technology acceptance and theory of reasoned action models. SEUSL Journal of Marketing, 5(2), 57–69.

- Kahandawa, K., & Wijayanayake, J. (2014). Impact of mobile banking services on customer satisfaction: A Study on Sri Lankan state commercial bank. International Journal of Computer and Information Technology, 3(3), 546–552.

- Kumari, J. P. (2016). Conceptual Framework: Factors Affecting for usage of Online Banking in Sri Lanka. International Journal, 25.

- Kumari, P. (2015). Customer adoption and attitudes in mobile banking in Sri Lanka. International Journal of Economics and Management Engineering. 2016c, 9(12), 4355-4359.

- Kweyu, M., & Ngare, P. (2013). Factor analysis of customers perception of mobile banking services in Kenya. Journal of Emerging Trends in Economics and Management Sciences , 5(1), 1–8.

- Madumanthi, I., & Nawaz, S. S. (2016). Undergraduates’ adoption of online banking in Sri Lanka. Journal of Information Systems & Information Technology, 1(1), 10–17.

- Manel, D. P. K. (2022). Determinants of the adoption of technology based self-banking system - Evidence from Sri Lanka. Sri Lankan Journal of Business Economics, 11(1), 1–21.

- Mokongoro, G. (2014). Factors influencing customer adoption of mobile banking services in Tanzania. 1–66.

- Nayanajith, D. A., Dissanayake, D. M. R., Wanninayake, W. M. C. B., & Damunupola, K. A. (2021). Acceptance of mobile banking application services offered by Sri Lankan commercial banks. Sri Lanka Journal of Technology, 11–17.

- Perera, A. L. D., & Gunaratna, A. G. D. L. K. (2020). Interrelations between mobile banking service quality attributes, customer satisfaction and customer loyalty in domestic commercial banks in Sr Lanka. International Conference on Business Research, 112–129.

- Rahmani, Z., Tahvildari, A., Honarmand, H., Yousefi, H., & Daghighi, M. S. (2012). Mobile banking and its benefits. Arabian Journal of Business and Management Review, 2(5), 37–40.

- Ravichandran, D., & Madana, M. H. B. A. H. (2016). Factors influencing mobile banking adoption in Kurunegala district. Journal of Information Systems & Information Technology, 1(1), 24–32.

- Roshana, M. R., Kaldeen, M., & Banu, R. (2020). Impact of Covid 19 outbreak on Sri Lankan economy. Journal of Critical Reviews, 7(14), 2024–2133.

- Sajeewanie, L. A. C., & Lakshika, A.A.H. (2019). Factors influence on customers’ behavioral intention to use mobile banking application Sri Lanka. Interdisciplinary Conference of Management Researchers .

- Technology Acceptance Model (TAM) and the Theory of Planned Behavior (TPB) together along with (1) a moderator between the two models, (2) perceived risk, and (3) trust.

- Upadhyay, H. J., Rajani, P., & Surani, S. (2017). Determining association between age, occupation and usage of online banking services among customers. Parikalpana - KIIT Journal of Management, 13(2), 37–46. [CrossRef]

- Wani, T. A., & Ali, S. W. (2015). Innovation Difusion heory. Journal of General Management Research, 3(2), 101–118.

- Wijesooriya, W. M. I. P., & Sritharan, S. (2018). Exploring the determinants of users’ satisfaction in mobile commerce. The Journal of Business Studies, 2(1), 1–13.

- World Bank. (2021). The Global Findex Database. Worldbank.org. https://www.worldbank.org/en/publication/globalfindex.

- Yapabandara, A., & Nagendrakumar, N. (2022). Did the effects of the pandemic affect online/digital banking adoption in Sri Lanka? Int. J. Electronic Banking, 3(3), 238–262. [CrossRef]

Table 1.

Digital Banking in World.

| Made of received digital payments in 2021 as the percentage (% age 15+) | |

|---|---|

| All adults, 2021 | 64.1 |

| All adults, 2017 | 52.1 |

| Women | 60.6 |

| Adults in the poorest 40% of households | 57.4 |

| Received a digital payment | 42.6 |

| Made a digital payment in to an account | 58.8 |

| Received a government payment using an account | 20.5 |

| Received a private sector wage in to a account | 20,9 |

Source: World Bank (2021).

Table 2.

Digital banking usage in Sri Lanka.

| Country Data | South Asia | Lower Middle Income | |

|---|---|---|---|

| Made or received payment in the past year (% age 15+) | |||

| All adults, 2021 | 55.1 | 33.7 | 38.3 |

| All adults, 2017 | 47.2 | 27.8 | 30.8 |

| Women | 47.5 | 26.5 | 32.3 |

| Adults n the poorest 40% of households | 48.8 | 26.1 | 30.0 |

| Received a digital payment | 29.7 | 18.7 | 23.3 |

| Made a digital Ppayment | 43.5 | 24.9 | 30.4 |

| Received a government payment into an account | 13.8 | 10.0 | 11.9 |

| Received a private sector wage into an account | 12.3 | 5.4 | 6.6 |

| Sent or received a domestic remittance payment using an account | 10.1 | 9.2 | 13.8 |

| Made a digital utility payment | 20.3 | 10.7 | 12.3 |

| Made first digital utility payment during COVID- 19 | 16.9 | 7.7 | 7.1 |

| Made a digital merchant payment | 18.1 | 9.7 | 11.9 |

| Made first digital merchant payment during COVID-19 | 9.6 | 6.3 | 6.5 |

Source: World Bank (2021).

Table 5.

Factor analysis.

| Factors | Kaiser-Meyer-Olkin Test (KMO Test) | Bartlett’s test (Sig.) |

|---|---|---|

| U | 0.851 | 0.000 |

| EU | 0.854 | 0.000 |

| T | 0.705 | 0.000 |

| R | 0.824 | 0.000 |

| MBU | 0.691 | 0.000 |

Source: Survey data.

Table 6.

Regression analysis.

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

|---|---|---|---|---|---|---|

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 4.621 | .445 | 10.385 | .000 | |

| Usefulness | -.172 | .092 | -.146 | -1.855 | .065 | |

| EU | -.049 | .086 | -.068 | -.561 | .575 | |

| Trust | .332 | .080 | .508 | 4.167 | .000 | |

| Risk | -.220 | .053 | -.339 | -4.156 | .000 | |

| a. Dependent Variable: MBU | ||||||

Source: Survey data.

Table 7.

Model Summary.

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

|---|---|---|---|---|

| 1 | .645a | .416 | .403 | .24432 |

| a. Predictors: (Constant), Risk, Usefulness, EU, Trust | ||||

Source: Survey Data (2023).

Table 8.

ANOVA test.

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 7.772 | 4 | 1.943 | 32.548 | .000b |

| Residual | 10.924 | 183 | .060 | |||

| Total | 18.695 | 187 | ||||

| a. Dependent Variable: MBU | ||||||

| b. Predictors: (Constant), Risk, Usefulness, EU, Trust | ||||||

Source: Survey Data (2023).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.