Submitted:

23 September 2023

Posted:

26 September 2023

You are already at the latest version

Abstract

Nigeria's upstream oil and gas sector is extensively contributing to the economic growth of the country, but the sector is plagued with challenges around corporate social responsibility (CSR) and taxation practices. Petroleum Industry Act (PIA) is introduced to tackle these challenges towards promoting sustainable development in Nigeria. The aim of this study is to explore the PIA’s provisions on CSR and taxation, identify the Act’s implementation challenges and improvement opportunities, propose an integrated framework for monitoring and evaluating the PIA’s impact on CSR and taxation over time, and recommend measures for enhancing PIA’s impact on CSR and taxation support for sustainable development in Nigeria's upstream oil and gas sector. This study adopts the qualitative desk review method to analyze existent literature, reports, and documents regarding PIA’s provisions on CSR and taxation. Findings reveal that the PIA’s provisions greatly emphasize CSR initiatives and taxation transparency in improving responsible ethical business behaviour. An integrated framework for monitoring and evaluating PIA’s impact over time is developed. This study concludes that the PIA's provisions can balance CSR and taxation practices for sustainable development. The study’s recommendations include using the integrated framework as a structured strategy for monitoring and evaluating the PIA’s impact. This study contributes to the discussion on the imperatives of ethical business practices and regulatory frameworks for sustainable development drive in the oil and gas sector.

Keywords:

corporate social responsibility

; taxation

; petroleum industry act

; sustainable development

; upstream oil and gas sector

; integrated framework

; Nigeria

1. Introduction

Nigeria is one of Africa’s leading oil and gas producing countries that is heavily depending on its upstream oil and gas sector for revenues; for example, the petroleum profits tax significantly contribute to the country’s gross domestic product and sustainable development financing [1]. However, the oil and gas producing region in Nigeria is plagued with environmental, economic, and social concerns caused by the operations of the oil companies impacting on societies. Prior to the legislation of the Petroleum Industry Act (PIA) that was signed on August 16, 2021 [2], many stakeholders have expressed concerns on how the upstream sector oil and gas companies appear to neglect the development of the oil and gas host communities. While the PIA is a great effort initiated to support transparency, accountability, and sustainable practices; also, it repeals the Petroleum Profits Tax Act (PPTA) for directing the activities of the upstream sector oil and gas companies in Nigeria [3-5]. Thus, it is hoped that the PIA can inspire a responsible social behaviour of the companies towards corporate social responsibility (CSR) and taxation to drive sustainable development in Nigeria. CSR helps companies to think beyond maximizing profits only, displaying commitment to economic, environmental, and social concerns caused by their operations in society [6]. The government should ensure effective and fair taxation of activities of the oil and gas companies since taxation transparency is intensified by the PIA [2] to obtain revenue for financing sustainable development. Whereas some provisions in the PIA are related to CSR and taxation with likely social, economic, and environmental impact, there is a lack of information and research on how the Act may affect the practices of both the CSR and taxation in Nigeria’s upstream oil and gas sector. In this context, taxation on the profits from the sale of crude oil collected by the Federal Inland Revenue Service (FIRS) is considered in this study and not royalty or other payments by the upstream oil and gas companies. Also, CSR has the potentials to reduce tax revenue collection by the FIRS in reality.

This study explores relevant provisions of the PIA linked to CSR and taxation to provide useful insights into the legislation’s intent and likely implications for the upstream sector oil and gas companies operating in Nigeria. The study hopes to propose a framework for use in monitoring the PIA’s impact over time to ensure transparency and accountability in CSR and tax practices in the Nigerian upstream oil and gas sector. While this study will bridge the gaps in knowledge about the impact of PIA on CSR and taxation within the upstream oil and gas sector in Nigeria, it will contribute to a better understanding of the PIA’s effectiveness in sustainable development drive in Nigeria's upstream sector. The study’s findings will be of great significance to industry stakeholders, policymakers, and general public in reinforcing decision-making for encouraging a sustainable development path towards a future inclusive growth and prosperity of the oil and gas sector in Nigeria. Thus, the PIA is introduced as a vital policy document to reshape Nigeria's upstream oil and gas sector with the aim of addressing the issues of CSR and taxation practices. This study focuses on the provisions of the PIA explicitly linked to CSR and taxation to provide better insights into the real impact, challenges and opportunities, and propose a framework for its monitoring in driving sustainable development in the upstream oil and gas sector in Nigeria.

The rest of this paper is structured including the statement of the problem followed by the aim and objectives of the study and research questions. Literature review section includes overview of Nigeria’s upstream oil and gas sector, previous studies on CSR and taxation related to Nigeria’s oil and gas sector, and gaps in existing literature. Also, the theoretical framework and conceptual clarifications underpinning the study analysis. The section on research methodology covers qualitative desk review study method detailing how the research problem is addressed. The results section comprise the analysis of the provisions of the PIA on CSR and taxation, implementation challenges and improvement opportunities concerning PIA’s provisions, proposed integrated framework for monitoring and evaluating the PIA's impact, and recommendations for addressing the implementation challenges and using the improvement opportunities identified to enhance the PIA’s impact. The section on discussion focuses on the study’s findings discussed in alignment with research questions. The conclusion section covers the study’s key findings, limitations and future research directions and final closing remark.

1.1. Statement of the problem

In Nigeria, the upstream oil and gas sector has an important role to play in revenue generation and significantly contributing to the economic growth of the country. But the sector is plagued with challenges comprising community hostility and environmental concerns around CSR and taxation practices, affecting sustainable development in the sector and the oil producing areas. Whereas these challenges emanated since the 1950s when crude oil exploration and production activities began in the oil producing Niger Delta region, intervention agencies such as the Niger Delta Development Commission was created to promote economic development of the region. Recently, the PIA is introduced in Nigeria as a reflection of a robust legislation mandating CSR by establishing the host communities development trust and emphasizing taxation transparency for the sustainable development of Nigeria’s upstream oil and gas sector [3,7]. Nevertheless, the regulations governing oil and gas sector are ineffective since the discovery of crude oil in the 1950s as prior legal frameworks lack transparency and accountability to drive sustainable development in Nigeria’s oil and gas sector in line with international best practice [5]. Whereas the PIA is considered a win-win approach for addressing the oil and gas sector challenges and inspiring cooperative relationship and sustainable development in Nigeria [3,5,8], but it is not clear how the PIA’s provisions on CSR and taxation may impact sustainable development path within the sector. Yet, prior studies ignore the implications of the PIA for CSR and taxation regarding sustainable development. Thus, there is a need to understand the real impact of the PIA on CSR and taxation in Nigeria’s upstream oil and gas sector. Now, there is deficient knowledge concerning the provisions of the PIA specifically linked to CSR and taxation. Also, lack of a framework for monitoring and evaluating the PIA’s impact effectiveness in promoting CSR practice and enabling tax compliance behaviour in Nigeria’s upstream oil and gas sector. This study seeks to bridge these gaps by critically exploring and assessing the PIA's provisions on CSR and taxation, identifying implementation challenges and improvement opportunities of the Act, proposing an integrated framework for monitoring and evaluating the PIA’s impact, and proffering recommendations for the PIA’s impact effective performance. By this effort, the study intents to encourage stakeholder involvement, inform policymaking, and promote a more socially responsible ethical behaviour and sustainable development path for Nigeria's upstream oil and gas sector.

1.2. The aim and objectives of the study

The aim of this study is to explore the PIA’s provisions on CSR and taxation, identify the Act’s implementation challenges and improvement opportunities, propose an integrated framework for monitoring and evaluating the PIA’s impact on CSR and taxation over time, and recommend measures for enhancing PIA’s impact on CSR and taxation support for sustainable development in Nigeria's upstream oil and gas sector.

The specific objectives of the study are to:

- Explore the PIA’s provisions linked to CSR and taxation in Nigeria's upstream oil and gas sector support for sustainable development.

- Identify the implementation challenges and improvement opportunities concerning the PIA’s provisions on CSR and taxation in Nigeria's upstream oil and gas sector.

- Propose an integrated framework for monitoring and evaluating the PIA’s impact on CSR and taxation in Nigeria's upstream oil and gas sector over time.

- Proffer recommendations for addressing the implementation challenges and using the improvement opportunities identified to enhance the PIA's impact on CSR and taxation support for sustainable development in Nigeria’s upstream oil and sector.

1.3. Research questions

- How do the PIA’s provisions link to CSR and taxation in Nigeria's upstream oil and gas sector support for sustainable development?

- What are the implementation challenges and improvement opportunities concerning the PIA’s provisions on CSR and taxation in Nigeria's upstream oil and gas sector?

- What is the proposed integrated framework for monitoring and evaluating the PIA’s impact on CSR and taxation in Nigeria's upstream oil and gas sector over time?

- What recommendations can be proffered for addressing the implementation challenges and using the improvement opportunities identified to enhance the PIA's impact on CSR and taxation support for sustainable development in Nigeria’s upstream oil and sector?

2. Literature review

The literature review is structured in important themes providing better insights into the current position of knowledge and identifying the gaps which this study seeks to address.

2.1. Overview of Nigeria's upstream oil and gas sector

The upstream oil and gas sector in Nigeria comprises activities linked to crude oil exploration, drilling and production. It includes the processes that happen before the extraction of crude oil such as the detection oil and gas reserve, exploratory well drilling, and reservoir management. While the sector continues to play a key role in the general value chain of petroleum operations, it is affected by the provisions of the PIA mainly on CSR and taxation. However, the origin of the oil and gas industry dates back to August 27, 1859, when Edwin Drake found crude oil in the region of Pennsylvania, USA. In Nigeria, crude oil exploration commenced in 1908 during the colonial administration but it was disrupted by the World Wars in 1914 and 1939. In 1947, exploration returned, and commercial oil quantity was first found in January 1956 with first supply in February 1958, by the Shell Business Group [1]. While Nigeria’s upstream sector has over 70 (international and local) upstream oil and gas companies [9]; again, their activities are linked to economic, environmental, and social issues against expected sustainable development solutions by governments and societies in the oil and gas producing countries such as Nigeria [10]. While the oil and gas sector transactions yield large economic rents with corruption antics; also, the quantity of oil and gas reserves and production activities in the sector might have changed Nigeria from an agrarian economy to one dependent on crude oil for revenues [1]. But this success is with several challenges comprising environmental degradation and tax non-compliance which the PIA is expected to address [2,3,8], in meeting the expectations of society such as the oil host communities in Nigeria [5].

2.2. Previous studies on CSR and taxation related to Nigeria's oil and gas sector

In recent years, the concepts of CSR and taxation have received huge interest in the oil and gas sector in Nigeria. For example, CSR is linked to the abilities of companies to manage the social, economic, and environmental impacts of their operations in society [6]. While CSR is relevant in Nigeria’s oil and gas sector, maybe, because the sector seems to be dominating the country’s economy with its activities having great implications for the environment, local communities, and general society [9,10]. Previous studies have examined the link between CSR and taxation in many jurisdictions including Nigeria. While such studies explored the extent that companies participate in CSR activities; equally, the motivations for such activities, and the impact of CSR initiatives on taxation applicable to the oil and gas sector. For example, one study emphasized the importance of CSR in extractive industries due to their impact on the communities, though the roles of government agencies in CSR are unknown. As public administrators in Nigeria can impact CSR in extractive industries to help community projects. This study implies that public bureaucracies in Nigeria impact on CSR performance [6]. This suggests that CSR and taxation practices by companies in Nigeria’s oil and gas sector may pose challenges that a legislation is needed to regulate their performance.

Also, the important roles of CSR activities in the form of community development by extractive multinational companies in both developed and developing countries were studied, with focus on the impact of CSR on community development for sustainable development in the extractive mining sector in Africa. Findings reveal that CSR efforts are in health, education, employment, sanitation, water, and skills in improving community interactions [11]. This implies that CSR helps business and community relationships for harmonious coexistence. Also, the COVID-19 pandemic asked the governments and mining companies to prioritize CSR needs bordering on environmental and human rights issues [12]. While COVID-19 has hugely affected companies in the extractive sector in developing countries; the pandemic has caused global economic and social suffering, that CSR prompted questions on morality regarding community and employee welfare priorities [13]. Whereas environmental and investment concerns spark debates on CSR in the extractive industry; a study reported that mines’ closure have adverse effects including environmental and job damage. This affects local communities, initiating insecurity and termed challenges of CSR in the extractive industry [14]. When responsible leadership was explored regarding sustainable development of a community, extractive industries’ CSR effectiveness was emphasized although little attention is given to the antecedents of CSR plans in developing countries. That responsible leadership plays a key role in CSR implementation for sustainable development [15].

Lately, climate change and global warming imply environmental concerns mainly in extractive industries including oil, gas, and mining. These industries greatly contribute to environmental degradation, resource depletion, and pollution; but CSR seeks safeguarding the environment. While technological adoption: 4IR namely AI, IoT, machine learning, and robotics can reduce environmental impact, integrating technologies by 4IR in the extractive industry can promote CSR and sustainable development [16]. Like Nigeria, also, in Kenya, the extractive companies engage in CSR to gain social legitimacy to develop the community, with legislations including the Petroleum Act 2019, Mining Act 2016, and Mining Policy 2016 enacted to provide support for CSR implementation [17]. Another study considered CSR practice in Nigeria’s oil and gas sector and focused on maladministration and violence. While oil companies adopt voluntary CSR activities in addressing these issues, mandatory CSR by definite CSR rule is requested to help a framework for CSR implementation. The government and nongovernment organizations are asked to work together to reduce negative environmental impacts such as in the Niger Delta region of Nigeria [18]. Weak government regulations and multinational companies’ challenges including human rights abuses, environmental degradation, and weak transparency complicate development strategies in the Niger Delta. Thus, a whistleblowing system should be reinforced to promote accountability and transparency help for eliciting corporate responsible behaviour by reporting and reducing corruption and other malpractices in the Nigerian oil and gas sector [19]. A study revealed poverty and environmental ruin in the oil producing communities are propelled by corruption in the Nigerian oil sector, despite the interventions by governments and companies. While CSR is to bridge developmental gaps mainly in the oil host communities, corruption antics weaken CSR strategic efforts [20]. As corruption and CSR are contested in the Niger Delta of Nigeria, institutional corruption is linked to faulty CSR framework in the oil and gas sector with global implications too [21].

The resource control demands mainly by the oil and gas host communities relate to insufficient revenue derivation and environmental damage due to oil and gas mining activities in Nigeria. So, oil host communities always hold the oil companies responsible for increased CSR towards satisfying their needs for sustainable development. With agitations argued to be genuine, there is a call for institutionalizing and formalizing it by governments and companies through CSR improved investment for actually addressing concerns of the oil communities [22]. Perhaps, due to the prevalence of insufficient CSR projects driving conflicts in the oil and gas host communities such as in the Niger Delta region of Nigeria [23]. Nevertheless, the upstream oil and gas companies fulfil various CSR initiatives in addressing the economic, social, and environmental concerns due to their operations in the Niger Delta region of Nigeria. It is claimed that such CSR projects are ineffective thereby, not contributing to the development needs of the oil host communities, despite environmental degradation, insecurity and poverty persist to seemingly prompt violence in the oil producing region [24]. But a study revealed two views about CSR projects in the oil host communities. First, companies believe they provide adequate infrastructure and scholarship, for example, to address the socio-economic development of the Niger Delta area. Second, oil host communities prefer receiving revenue share against CSR projects implementation. Thus, it was suggested that a threshold of a minimum uniform CSR investment based on percentage of revenue should be set and reported yearly to ensure transparency and socio-economic growth in oil communities [25].

Besides, some studies have linked CSR to taxation based on data from the stock exchange that include various companies like the oil and gas companies. For example, one study explored the relationship between corporate governance, tax avoidance, and CSR disclosure in developing markets (Nigeria) and a frontier market (Pakistan). Findings disclose that in Nigeria, CSR is positively significant and linked to tax avoidance. In Pakistan, CSR and tax avoidance link is positive but insignificant. The impact of board characteristics on CSR vary with a mixture of positively insignificant relationships in Nigeria, and negatively insignificant relationships in Pakistan. But the study highlights the implication of CSR for companies and governments [26]. A study used stock exchange secondary data and revealed when CSR is based on environmental remedy, corporate tax complements are positively complementary, but substitutive for poverty relief and promoting education depending on a company’s size. Whereas complementary CSR should be encouraged, aggressive tax planning must be controlled because tax allowances and incentives are provided to improve CSR participation [27]. Another study has examined CSR execution impact on tax aggressiveness using companies’ data (2007-2013) in Nigeria. While company performance and size are reported to influence tax aggressiveness, a negative relationship between CSR performance and tax aggressiveness is reported, and tax authorities are advised to address it [28]. Besides, a study showed that CSR and tax planning are negatively related for companies with complementary and substitutive orientations [29]. Contrary to the negative findings above, a study reported a significant relationship between CSR (community and environment) components and tax aggressiveness. Companies are encouraged to align their CSR initiatives and tax compliance to promote sustainable development [30].

2.3. Gaps in existing literature

From previous studies reviewed, there are research gaps. Firstly, most studies: for example, have focused on the link between CSR and agitation or violence in oil communities [22-24], community and environmental development [6,11-14,16], or responsible leadership [15]. But the specific provisions of regulatory laws such as the petroleum profit tax act or the PIA appear not to be probed, concerning the oil and gas sector for the companies to participate in CSR and taxation practices towards sustainable development. Secondly, previous studies underline the requirements for making regulations to improve CSR performance [17,18,25], whistleblowing [19] or corruption [20,21]. CSR is linked to tax avoidance [26] or tax planning [27,29] or tax aggressiveness [28,30], and tax authorities are asked to monitor CSR against tax aggressiveness [28]. But there is yet a framework for use in monitoring and evaluating the effectiveness of a regulation’s provisions on CSR and taxation over time support for sustainable development. Thirdly, previous studies have explored the aspects of CSR and taxation independently. Few studies have researched into their connection and implications for sustainable development under the PIA since its enactment in 2021. This study focuses on the combined impact of the PIA on both CSR and taxation in Nigeria's upstream oil and gas sector. Because the PIA's provisions may result in unintended effects as strict CSR obligations and improved taxation can have potential influence on the behaviour of companies in many ways. These unexpected effects may be difficult to predict requiring monitoring and evaluation on a continuous basis. In this current study, attempt is made towards addressing the above research gaps for a better understanding of the PIA’s impact on CSR and taxation in driving sustainable development in the Nigerian upstream oil and gas sector context.

2.4. Theoretical framework

The theoretical framework for this study comprises two theories namely the legitimacy theory and stakeholder theory. These theories provide the basis for the understanding of CSR practice and taxation compliance concerning the PIA in Nigeria’s upstream oil and gas sector.

2.4.1. Legitimacy theory

The legitimacy theory emphasizes the actions of companies in justifying their operations. This is critical because companies can align their actions with the expectations and norms of society to obtain legitimacy and acceptance to access societal resources [31]. The PIA has introduced new requirements, the oil and gas companies in Nigeria may sought the need for adopting CSR plans and complying with taxation rules to uphold their legitimacy and fame. In this study, the provisions of the PIA can influence companies' views of legitimacy and their reactions about CSR and taxation practices. So, the legitimacy theory provides an understanding to explore and evaluate the voluntary and planned implementation aspects of CSR and taxation mainly in the normative sense [31] for improving sustainable development in Nigeria’s oil and gas sector.

2.4.2. Stakeholder theory

The stakeholder theory emphasizes the relationship of third parties besides the shareholders on the performance of companies [32]. This is critical as companies interact in different ways with various stakeholders influencing their decision-making and corporate behaviour. In this study, the provisions of PIA on CSR and taxation are liable to impact different stakeholders including government agencies, investors, local communities, and environmental groups. Understanding these interactions and their dynamics will help in identifying the extent that the implementation of the PIA can affect CSR and taxation practices in Nigeria's oil and gas sector. The stakeholder theory gives a framework for the analysis of the stakeholders’ expectations, interests, and needs [32] to guide the evaluation of the effectiveness of PIA in promoting sustainable development and the engagement of stakeholders in Nigeria’s oil and gas sector.

2.5. Conceptual clarification

Conceptual clarifications are required to understand the important terms relevant in this study. The clarifications of the terms involve Petroleum Industry Act (PIA) as the legislation initiated to regulate oil and gas operations in Nigeria’s upstream oil and gas sector; CSR as the abilities of the companies to manage economic, social, and environmental concerns of their operations; . Tax compliance relates to voluntarily upholding tax duties, crucial in generating tax revenue. Transparent accountability mechanisms are vital in supporting public confidence and effective governance. These terms are interconnected and influence the tax revenue yield and can discredit an efficient tax system such as in Nigeria

2.5.1. Petroleum industry act (PIA)

The Petroleum Industry Act (PIA) is a detailed legal framework for the regulation of oil and gas operations: exploration, production, management, and utilization of oil and gas resources in Nigeria’s upstream sector petroleum activities. the framework has outlined the discharge of corporate governance mechanisms, community involvement and development, environmental preservation, taxation, and revenue resource management in the sector. For example, the PIA has instituted a detailed framework mandating the oil and gas companies to meaningfully engage in CSR projects. While it realizes the oil and gas sector’s major impact on local communities, social welfare, and environment, the upstream oil and gas companies are required to set aside a percentage of their operational budgets annually for CSR projects. The projects should foster sustainable development and enhance host communities’ welfare. CSR plans should align with identifiable requirements and objectives of the host communities, which underscores fostering cooperation, negotiation, and true commitment on the parts of the companies and communities. Also, PIA asks that companies should report their CSR projects transparently and accountably as evidence of a responsible behaviour within the Nigerian upstream oil and gas sector [33].

About taxation, the PIA has introduced strong tax regulations towards enhancing transparency, compliance, and tax revenue management in Nigeria's oil and gas sector. While the regulations are essential in optimizing government tax revenue collection, this is to foster equity but block practices of illicit financial flows. For example, the PIA has established a strong framework for determining and collecting royalties, tax revenue and other financial payments from the oil and gas companies. Also, financial records must be accurately and regularly reported to appropriate regulatory agencies. Whereas the PIA underscores the need for accessible accounting, this is to ensure that companies transparently provide their financial activities breakdown. Furthermore, a fund for oil and gas revenue management is created specifically to finance projects improving environmental preservation and sustainable development. The PIA is imposing strict penalties such as for tax evasion issues and non-compliance behaviour when compared to its provisions [33]. The ideal is to optimize voluntary tax compliance while improving tax revenue collection for financing sustainable development from Nigeria’s upstream oil and gas sector.

2.5.2. Corporate social responsibility (CSR)

Corporate social responsibility (CSR) is the will of the companies to voluntarily contribute to the environment and society through developmental initiatives beyond the profit maximization objective. CSR is described in terms of Carroll’s four vital responsibilities: economic, ethical, legal, and philanthropy [34]. Many activities can be achieved as an integral part of CSR including tax payment, community and environmental development; yet the relevance of ethics cut across the Caroll’s pyramid of responsibilities in economic relations [34]. This study focuses on how companies can align the provisions of CSR within the PIA towards contributing to sustainable development of the local oil and gas communities and larger society in Nigeria.

2.5.3. Taxation

Taxation is the process of collecting tax revenue. Taxation compliance relates to the oil and gas companies’ adherence to the provisions on taxation in the PIA. This covers accurately reporting tax financial information, discharging tax responsibilities, and complying with the tax laws for ensuring legality and transparency in tax revenue collection and remittance to government. As the role of enforcement in driving tax compliance cannot be over-emphasized [35]. While the main aspect of the objective of the PIA is to improve taxation compliance, there is implied need for proper management of tax revenue in driving sustainable development within the Nigerian upstream oil and gas sector. This suggests that taxation in Nigeria’s upstream oil and gas sector is based on the law [36], although tax evasion is disrupting tax revenue collection in developing countries such as Nigeria with tax administration challenges [35].

2.5.4. Sustainable development

Sustainable development is linked to a balanced method in seeking to accomplished economic growth, environmental protection, social inclusion though ensuring the welfare of the present generation not compromising that of future generation. Sustainable development goals provide action plans for sustainable development [37]. In this study, sustainable development includes the assessment of how the impact of the PIA on CSR and taxation can align with the community welfare, environmental preservation, and economic feasibility principles. Towards ensuring that oil and gas companies’ activities positively contribute to a long-term economic, social, and environmental benefits to society in Nigeria. because principles of sustainable development are advised for integration into aspects of policymaking for societal long-term benefits [37].

3. Research methodology

Research methodology relates to the approach utilized in conducting this study comprising data selection and analysis method, and whole process of research design [38,39]. The methodology guides measures taken to achieve the research objectives; also, ensures reliability of the study. In this study, the methodology helps in data gathering, analyzing, and interpreting, contributing to the credibility and validity of its findings [40]. Based on research objectives and the nature of data collected, phenomenology qualitative research methodology is utilized in this study to explore and gain insights into the impact of the PIA provisions on CSR and taxation [38-40].

3.1. Research design

The qualitative desk review methodology is utilized in this study to analyze existent literature, documents, and reports related to the PIA’s impact on CSR and taxation in Nigeria's upstream oil and gas sector. The qualitative desk review is mainly appropriate to synthesize information, identify patterns, and generate meaningful insights from different sources without necessarily using the primary data such as from interviews and questionnaires. Based on systematic review and analysis of the literature sources relevant in this study, conclusions are drawn regarding the research objectives [41-47].

3.2. Data sources and criteria for selection

The main sources of data for this study comprise academic journals, government publications, reports, industry reports, policy documents, and other credible sources appropriate to the topic. The sources are classed as secondary data. The criteria for selection include data relevance and related to the PIA, CSR, and taxation in Nigeria's upstream oil and gas sector. Keywords were used in the data search with defined exclusion and inclusion criteria. Thus, literature sources were critically evaluated for credibility, quality, and relevance as core features of the qualitative desk review method. Data reliability was ensured by the assessment of methodology, author’s biases and credentials, and materials’ publication dates [43,46,47].

3.3. Data extraction procedure

The procedure for data extraction includes the logical detection and collection of the relevant information, opinions including disagreements and agreements, and findings from the selected sources regarding the topical research area. This comparative analysis helped in understanding the development of views and ideas over time [41,45-47]. Data extraction is guided by certain predetermined themes such as PIA’s provisions linked to CSR and taxation, CSR, taxation compliance, and sustainable development. The data extracted were organized to enable the use of thematic analysis with gaps in the literature being identified for more study based on intense academic demand [42,44,45,47].

3.4. Thematic analysis

The thematic analysis method is used to detect patterns and insights based on the data extracted. This implies classifying the data into repeating themes linked to the PIA's impact on CSR and taxation. Themes were refined and revised to describe nuances and differences in the literature. By the thematic analysis procedure, the research objectives were explored in detail [41-45].

3.5. Ethical considerations

This study is based on secondary data and relied entirely on existing literature and documents; thus, the ethical considerations linked to human objects and data secrecy do not apply.

4. Results

The analysis in this study is guided by the theoretical framework combining legitimacy theory and stakeholder theory. These theories help in interpreting the data to understand the dynamics in practicing CSR and taxation regarding the PIA in Nigeria’s upstream oil and gas sector.

4.1. Provisions of the PIA on corporate social responsibility (CSR) and taxation

In line with the first objective of this study, the analysis of PIA’s provisions on CSR and taxation in Nigeria's oil and gas sector may reveal remarkable shifts as the PIA supports improved CSR execution by environmental protection and community development. Also, taxation provisions appear to drive tax revenue management, tax transparency and compliance. While these shifts mirror a firm drive for balanced practices, this may creäte and sustain a mutual industry-society correlation that is expected to reshape and forge a path towards sustainable development. Thus, the analysis of the PIA provisions on CSR and taxation in Nigeria's upstream oil and gas sector will provide insights into the Act’s intent and sustainable development implications as follows.

4.1.1. PIA’s provisions linked to corporate social responsibility (CSR)

The upstream sector oil and gas companies in Nigeria partake in oil exploration and production activities. While there is no clear provisions on CSR to benefit the oil host communities in the Petroleum Profits Tax Act (PPTA) 2004, but provisions for CSR seem to exist in the PIA for host communities to benefit social, economic, and environmental projects [33]. For example, the PIA’s Chapter 3 focuses on host communities development with main objectives in Section 234(1)(a-d) to promote the sustainable development of the oil host communities. To ensure that the host communities through petroleum activities reap economic and social benefits directly. This is to promote harmonious and peaceful coexistence between the oil license companies and host communities, creating a framework for the host communities’ development. In Section 235(1), the host communities development trust is to be incorporated for the host communities’ benefits. While companies can only implement projects based on the needs assessment of host communities, such projects should translate into real community development plan in Section 235(7). The timeframe of 12 months is recommended for incorporation of the host communities development trust effective from the date of existing oil mining leases provided in Section 236. If created, Section 237 has attached the obligations of the host communities development trust to transfer of a company’s interest and obligations to another party. Further, host communities’ interests are secure in Section 238 with provision for penalties such as revocation of applicable license in case of failure to comply with the provisions in Chapter 3 of the Act. While this is to enhance the development of the host communities [33]; also, CSR commitments link the host communities to the oil companies [8] for promoting sustainable development in Nigeria [7].

Moreover, the PIA’s Section 239 provides the objectives of the host communities development trust detailed in Sub-Section 3 towards the sustainable growth of the oil host communities. The funding sources for host communities development trust comprise one or more accounts termed host communities development trust fund in Section 240(1) and its Sub-Sections. Also, Section 240(2) provides that on an annual basis, companies should contribute into the host communities development trust fund a sum equivalent to 3% of actual operating expenditures of the previous financial year in the upstream petroleum activities affecting the host communities [33]. Despite the 3% is opposed as being small [2], but this amount may be higher than that of the Niger-Delta Development Commission. It is important to be more concerned with the management of the trust. Who allocates the trust’s funds? Section 244 enables the Board of Trustees to share the trust’s funds on a yearly basis under Section 240. The funds to be allocated: capital projects (75%), reserve (20%), and administrative expenses (5%). A community can forfeit the cost of repairs in events of vandalism, sabotage and civil unrest causing damage to petroleum facilities or disruption of production activities. The host communities assessment of needs to be done in line with the Act’s provisions in Section 251 and its Sub-Sections, subsequent to the granting and issuance of any lease or license under the PIA. Findings of an assessment should inform the companies’ development plan for the host communities towards promoting sustainable development. Section 256 exempts host communities development trust funds from taxation. In Section 257, the expenses incurred by the companies under Section 240(2) are tax deductible for both hydrocarbon tax and company income tax purposes. But Section 257(2) provides that except for natural and technical causes, disruptions to operations or damage to petroleum and its facilities by sabotage or vandalism or civil unrest, will make the host communities to forfeit their entitlements equal to the repair costs of the damage incurred and emphasized in Section 257(3) of the Act [33]. Thus, the PIA’s host communities development trust is a good-bet strategy for supporting sustainable development in Nigeria’s oil and gas sector [1,4,5,7,8].

Given the various PIA’s provisions on CSR, it becomes obvious that the Act seeks promoting CSR activities of the companies as a basis for the exploitation of resources in a more transparent and accountable manner. Such CSR activities cover expenditures on education, environmental protection, community development, healthcare, and charity. Whereas the creation and funding of the host communities development trust is a milestone achievement, proper use of the trust’s funds should be closely monitored. This underscores the necessity for a specified CSR planned budget indicating commitment to uphold positive development impact in the host communities. Also, the PIA emphasizes that companies should transparently report CSR activities executed, by presenting details of the scopes, types, and outcomes of such activities on the environment, social, and economic conditions of the host communities. Thus, promoting accountability and transparency which can enable the stakeholders to assess the companies’ efforts and efficiency of their CSR initiatives towards sustainable development in Nigeria.

4.1.2. PIA’s provisions linked to taxation

The PIA has introduced hydrocarbon tax to replace the petroleum profit tax in the PPTA [33]. The hydrocarbon tax is levied on the upstream oil and gas companies for obtaining a fair share of revenue due to exploitation of oil and gas resources. Taxation in Nigeria’s upstream oil and gas sector is based on the PPTA [36], but currently replaced with the PIA in 2021 [3,5,33]. For example, the PIA’s Chapter 4 is on petroleum industry fiscal framework. Section 258(a-e) of the Act provides a fiscal framework that is progressive to balance business risk and rewards in generating revenue to the Nigerian government. The fiscal framework is based on the principles of dynamism, clarity, and generally applicable fiscal rules; thus, it should ensure fair investors’ returns while expanding government’s revenue base. As the framework is intended to simplify petroleum tax administration and uphold transparency and equity within the petroleum sector fiscal regime in Nigeria. In Section 259(a)(i-ii), Federal Inland Revenue Service (FIRS) is responsible for the assessment and collection of the government’s oil and gas tax revenue. The FIRS will collect 30% of profits for each of hydrocarbon tax and company income tax based on the sale of crude oil, and 2% for tertiary education tax. Therefore, the PIA is improved over PPTA since company income tax is introduced and tertiary education tax is no longer tax deductible for the upstream companies. While the PIA has repealed some laws related to petroleum operations, Section 260 provides hydrocarbon tax for upstream companies related to onshore, shallow water operations, and deep offshore petroleum operations. In Section 263 and its Sub-Sections, allowable deductions for tax purposes are provided to encourage participation in CSR activities. Deductions not allowed for tax purposes are provided in Section 264 for calculations to obtain the adjusted profit of an oil company in an accounting year [33].

Also, the losses and profits of the upstream oil and gas companies should be assessed consistent with the PIA’s provisions in Section 265 and its Sub-Sections. Estimation of assessable profits in Section 265 provides the basis for deciding the chargeable profits and allowances in Section 266(1). Chargeable profits are termed as the assessable profits amount after handling allowable deductions in line with the Act’s provisions in an accounting year. In Section 267(a-b), the Act provides how chargeable tax is ascertained. Chargeable tax is a given percentage of chargeable profits for an aggregated period. To tackle situations where the chargeable tax may be less than an amount to be realized based on crude oil barrel at measurement point and per barrel oil fiscal price, the payment of additional chargeable tax is provided in Section 268 and its Sub-Sections. The aspects of artificial transactions likely to promote tax avoidance are tackled since the FIRS is mandated to reverse or disregard such transactions that can reduce chargeable profits for tax purposes in Section 269. Besides, the PIA upholds tax accountability and transparency because Section 277 mandates the upstream companies to prepare their accounts and deliver same with other relevant particulars for hydrocarbon tax purposes. In Section 282, the FIRS can assess and collect tax payable when the time for a company to deliver its self-assessment tax returns has elapsed. The timeframe for tax payment for the upstream companies is provided in Section 291 and its Sub-Sections. The tax is payable in 13 instalments with normally 12 monthly equal instalments and a final instalment in the 13th month for reconciliations. Obviously, the penalty for tax non-compliance and its enforcement when the timeframe for tax payment has passed is provided in Section 292. Further offences and penalties are provided in Sections 297-301 which cover aspects such as tax default and false reporting of information. Section 302 and its Sub-Sections cover company income tax for companies into upstream petroleum operations [33]. So, the PIA is to overhaul the upstream oil and gas sector as a win-win approach for improving sustainable development in Nigeria [5,8] and taxation transparency is intensified [2]. However, leadership is necessary for successful implementation of sustainable development drive [15].

Given the PIA’s provisions on taxation, it becomes clear that the Act seeks to encourage taxation transparency of the companies as a basis for the exploitation of resources in a more accountable way. Because the PIA provisions on taxation have introduced a structured strategy for ensuring a more fair and equitable taxation to optimize tax revenue collection from oil and gas mining operations. The upstream oil operators, mainly the local and international oil companies, should pay a percentage of their profits from the sale of crude oil to the government. This emphasizes the need for a taxation framework for the companies to pay their fair share of taxes indicating commitment to support positive development impact in Nigeria. While the upstream companies are directed to keep proper records of all their financial transactions regarding the sale of crude oil and CSR activities for tax purposes, this will ensure that transparent records are preserved to improve tax avoidance and evasion. So, the PIA underscores the promotion of taxation equity and transparency for the government to optimize oil and gas tax revenue collection to financing sustainable development in Nigeria.

4.1.3. Provisions of the PIA on CSR and taxation: Implications for sustainable development

The analysis of CSR and taxation provisions in the PIA framework reveals intense implications for sustainable development in Nigeria's upstream oil and gas sector. Whereas the PIA leads an era of change by driving effective practices of CSR, such practices should be aligned with the companies’ environmental preservation and community benefits [8]. Also, strict taxation rules may ensure that tax transparency, tax revenue management and compliance are prioritized [2]. As the larger impact of the PIA’s provisions is beyond matters of fiscal and corporate behaviour. For example, the PIA emphasizes responsible ethical corporate practices consistent with United Nations Sustainable Development Goals and global sustainable development policy. Thus, the PIA's provisions on CSR and taxation may reshape the role of the upstream oil and gas sector in Nigeria's sustainable development drive. So, the sector will reconcile economic returns with societal promises underlining advent of a path towards sustainable development with economic growth, environmental protection and social welfare advocating stakeholders’ involvements in CSR initiatives in Nigeria [6]. Economic growth links to an investor’s confidence that the PIA’s provisions on CSR and taxation can be built and sustained. For when the Nigeria’s upstream oil and gas sector is transparently driven and socially liable, it can attract domestic and foreign direct investments support for economic growth. Community development may be improved as CSR projects can result in an improved infrastructure and living conditions for cooperative relationship, benefiting the local communities directly for wider economic growth [11,12].

Environmental protection: This relates to environmental resource protection through which the PIA’s provisions integrate environmental concerns into CSR practices to protect the natural resources from hazard and depletion. Whereas protection measures may reduce environmental damage for community benefits [30], this can add to long-term feasibility of Nigeria’s upstream oil and gas sector. While taxation transparency can ensure that tax revenues are well managed to aid investments in efforts to protect the environment by mitigating negative environmental impacts; yet insecurity issues revolve around environmental damage [14]. Social benefits link to community emancipation supported by the PIA’s provisions on CSR practices prioritizing community benefits. Thus, initiatives comprising healthcare, education, and skilled-vocational development improve social welfare, and contribute to the alleviation of poverty and improving the living conditions of society. CSR performances must address oil communities’ development needs [22] as conflicts in such communities may be triggered by faulty CSR projects [23,24], saying that CSR is key for governments and companies [26] in decreasing local communities’ driven conflicts and inspiring balanced relationships between companies and society support for sustainable development [23,24]. Importantly, CSR performance should reflect morality in prioritizing community and employee welfare [13].

Based on the exploration of the PIA’s provisions on CSR and taxation in Nigeria’s upstream oil and gas sector, this study’s findings disclosed that the PIA is a robust regulatory framework introduced in the sector. The Act requires the upstream oil and gas companies to contribute to sustainable development by allotting a percentage of their business incomes for CSR initiatives, to improve economic, environmental, and social impacts on the oil and gas host communities. Also, the PIA’s provisions on taxation imply clear approaches support for taxation transparency in tackling tax avoidance and evasion to foster revenue generation. Thus, the PIA’s provisions on CSR and taxation can substantially contribute to promote sustainable development through a beneficial responsible ethical business practice for improving community relationships.

4.2. Implementation challenges and improvement opportunities concerning PIA’s provisions

There are certain challenges and improvement opportunities implementing the PIA’s provisions on CSR and taxation in Nigeria. The challenges and improvement opportunities are reflections of the complications in the country’s regulatory, economic and socio-political contexts. The oil and gas companies experience track-finding difficulties in balancing their potential negative impacts on society with sustainable development in the Nigerian upstream oil and gas sector.

4.2.1. Implementation challenges concerning the PIA’s provisions on CSR and taxation

The challenges implementing the PIA’s provisions on CSR and taxation have negative impact on the realization of sustainable development in Nigeria’s upstream oil and gas sector. Certain implementation challenges identified include:

- Regulatory and standardization complexities: The PIA is a fiscal regulatory framework to govern the oil and gas sector operations, which its provisions are complex and subject to misinterpretations and confusions in many ways as the language of the Act appears imprecise and ambiguous [4]. Stakeholders may otherwise understand and interpret the PIA’s provisions on CSR and taxation; thus, implementation inconsistencies may occur. This is complicated by standardization inadequacies about implementation guidelines to clearly provide governments’ expectations and what the companies need to do towards simplifying compliance. The lack of PIA’s transparency and accountability can affect sustainable development drive in Nigeria’s upstream oil and gas sector regarding international best practices [5,8], as the Act’s implementation will be problematic [48].

- Awareness inadequacy: The upstream oil and gas companies may initially face the lack of awareness adequacy of the provisions of the PIA that has offered regulatory changes, likely to stimulate certain understanding, interpretation, and implementation challenges without extensive awareness across the sector [5]. An awareness inadequacy may make companies to find it difficult to satisfy the requirements for CSR and taxation practices and compliance. Since proper information disclosures may affect the efficiency of their operations, considering that such information have a timeframe for disclosures.

- Monitoring and strategic enforcement: The implementation of the PIA’s provisions on CSR and taxation requires adequate routine monitoring and strategic enforcement for deep stakeholders’ compliance to be attained. While tax allowances and incentives can promote CSR participation, if no mechanisms for monitoring and enforcement are put in place, then noncompliance with the provisions may be evitable [27].

- Limitations in investment resources: While companies need resources mainly finance to invest; the PIA has mandated CSR and taxation practices imposing the allocation of resources [2,25], that possibly can affect investment and business plans and operations. The companies if not big sizes, are likely to face limitations in resources to train experts, which may affect the implementation of the provisions of the PIA on CSR and taxation.

- Change resistance: There seems to be long period of industrial norms such as crude oil inaccurate measurement, not theft that is being practiced by the upstream companies in Nigeria’s upstream oil and gas sector. The PIA is introducing changes which can oppose some industrial norms, and this may affect adequate compliance with the Act. Because of the lack of political will, commitment, and problem-solving leadership [2,15].

- Community involvement: The PIA has mandated implementing CSR initiatives which entails effective community involvement that can pose likely challenges to companies: owing to the communities’ communication and language barriers, historical antecedents and cultural issues. Also, different expectations of the different people in Nigeria, which may be hard to understand and address, likely to affect the implementation of the PIA. Despite communities’ stakeholders should be involved in CSR projects for promoting cooperative existence [6,11,12,18] and implementation of the PIA [8].

- Short-term disruptions: The implementation of the PIA’s provisions concerning CSR and taxation may have a transition impact from its initiation to maturity period, likely to affect the financial positions of the companies. This may generate business disruptions in the short-term that strategic plans by added costs may be necessary to mitigate such disruptions. Complying with the PIA may pose challenges at the period.

- Government commitment and capacity: The upstream oil and gas sector is regulated by government in Nigeria. So, the government’s important role in monitoring the sector to ensure adequate compliance with the PIA cannot be overemphasized. Yet, government’s commitment and human capacity of its agencies [2,48] may be limited by the resources budgeted for monitoring [28], as training and retraining of employees are recommended to ensure that the PIA’s provisions are properly implemented [8].

- Taxation complexity: The PIA has presented changes in taxation provisions which may appear complex in view of the international nature of the transactions of the upstream oil and gas companies. When the changes in taxation provisions are not well understood and correctly applied, there are chances for noncompliance and many errors to occur.

- Collecting and reporting CSR data: CSR initiatives being implemented by the upstream oil and gas companies other than those achieved by the host communities development trust fund should be properly reported. So, data should be collected regarding such CSR projects for reporting purposes due to their tax effects. This may require the companies to fix systems robust enough to collect data accurately and reporting same timely [16].

The above challenges can be addressed through a long-term strategic effort comprising mutual cooperative relationships between the oil and gas sector stakeholders such as the governments, companies, and civil society organizations in utilizing the recommendations provided ahead.

4.2.2. Improvement opportunities concerning the PIA’s provisions on CSR and taxation

The PIA’s provisions on CSR and taxation offer huge improvement opportunities in Nigeria’s upstream oil and gas sector. Essentially, the opportunities have roots in the challenges identified above including:

- Technological solution drive: The implementation of the PIA provisions can encourage innovative and technological solutions that may improve environmental protection and efficiency in operations. Using technological solutions to collect data, enable reporting, ensure monitoring and enforcement in real-time can foster compliance with the PIA to enhance accountability and transparency in Nigeria’s upstream oil and gas sector [16].

- Stakeholders’ collaborative commitment: The PIA provisions can enable the industry actors, civil society organizations, and government officials to collaborate for relevant opportunities to align mutual objectives and benefits as smoothly and committedly as possible. This can improve sharing of ideas and understanding of the PIA’s provisions for a consistent and effective implementation of the Act in Nigeria’s oil and gas sector in the spirit of stakeholders cooperative relationship [6,11,12,18].

- Stakeholders’ reputation and consultation: The implementation of the PIA’s provisions on CSR and taxation can enhance the reputation of companies for gaining access and legitimacy to societal resources. Also, effective community involvement and taxation practices can lift citizens’ trust for sustainable development. Equally, the involvement of stakeholders such as the oil host communities during consultations in designing CSR initiatives can help in evaluating and determining the effectiveness of such initiatives in addressing the needs of the oil host communities [11,17,18].

- Building capacity: The PIA has introduced changes in the fiscal framework of the oil and gas sector. This needs the building of capacity of the stakeholders through training and retraining sessions for fostering compliance with the Act and its successful impact. Regulatory bodies, oil companies, oil host communities, and civil society organizations can be trained to understand the PIA’s implementation regarding CSR and taxation [8,48].

- Incentive drive and recognition: The PIA provisions ask companies to behave socially responsible to attract potential investors support for sustainable development drive. So, incentives such tax allowances and tax breaks can be introduced to trigger compliance with the Act but to be monitored [27]. Besides, the companies that have exceptionally exhibit CSR efforts may be motivated to even do more through recognition events for excellent practices, that may persuade others to participate in doing CSR activities too.

- Long-term projects: The PIA provisions underline sustainable development consistent with the long-term objectives and interests of both the communities and companies. So, investment in sustainable development projects can well contribute to environmental preservation, social inclusion, and economic improvement benefits to all and sundry [11,14,30].

- Measurable performance indicators: There is the need to clearly define CSR initiatives for measurable performance indicators that can help the companies to monitor progress, and evaluating impact to improve accountability, trust, transparency, and integrity [19].

- Simplicity and popularization: The PIA's provisions may gain from simplicity since the Act has repealed many laws regarding the oil and gas sector operations in one document for stakeholders to use. While this is expected to lower legal issues for companies with financial constraints to seek the PIA’s interpretation fostering some compliance level, but CSR and tax avoidance negative relationship [29] may call for intensive monitoring.

- Regulatory adaptability: The PIA's provisions can be revisited and further improved to be more adaptable for implementation given the diverse contexts which the upstream oil and gas companies operation in Nigeria. This can improve the Act’s impreciseness [4] to support sustainable development drive in Nigeria’s upstream oil and gas industry.

The above improvement opportunities can be used by a long-term strategic effort comprising mutual cooperative relationships between oil and gas sector stakeholders such as governments, companies, and civil society organizations in utilizing the recommendations provided ahead.

Based on the examination of the PIA’s provisions on CSR and taxation in Nigeria’s upstream oil and gas sector, this study’s findings disclosed that there are some implementation challenges and improvement opportunities associated with the Act. By this study, the PIA implementation challenges identified comprise the regulatory and standardization complexities, monitoring and strategic enforcement, community involvement, government commitment and capacity, and collecting and reporting CSR data. However, improvement opportunities identified comprise technological solution drive, stakeholders’ collaborative commitment, stakeholders’ reputation and consultation, building capacity, and incentive drive and recognition. These improvement opportunities are valuable towards addressing the implementation challenges for improving the effectiveness of the PIA’s provisions.

4.3. Proposed integrated framework for monitoring and evaluating the PIA’s impact

The proposed integrated framework for monitoring and evaluating the impact of the PIA on CSR and taxation in Nigeria's upstream oil and gas sector is intended to assess the effectiveness of PIA provisions. This framework includes key indicators to assess the societal impact of CSR and taxation. It enriches the alignment between sustainable development and accountability by tracking environmental protective measures, tax revenue management, financial contributions, and community development efforts. The framework will promote flexible management while improving CSR and taxation practices to better understand the PIA’s potentials in addressing economic, environmental, and social concerns support for sustainable development in Nigeria. Consistent with the second objective of this study, an integrated framework for monitoring and evaluating the impact of the PIA on CSR and taxation in Nigeria's upstream oil and gas sector is hereby proposed. The framework links key performance indicators (KPIs) as the criteria for evaluating CSR and taxation, and a plan for assessing the effectiveness of the PIA's over time.

4.3.1. Key indicators for monitoring and evaluating CSR using the PIA

The key indicators for evaluating CSR in Nigeria's upstream oil and gas sector through the PIA are notable yardsticks providing better insights into CSR initiatives’ impact and effectiveness. The indicators are drawn from the various literature reviewed and observation provide support in evaluating CSR practices alignment with the PIA’s provisions and sustainable development objectives and outcomes. Basically, tracking the indicators can help the industry stakeholders, policymakers, and local and general communities to assess how the practices of CSR contribute to sustainable development. Some key CSR indicators comprise:

- Community development projects: This measures the projects’ number, extent, impact, and role in uplifting the living conditions of communities. Target projects must improve healthcare, infrastructure, education, etc. Number of recipients or beneficiaries and the length that benefits being provided can last must be evaluated. While the PIA underlines community participation; thus, this indicator is critical for evaluating real benefits.

- Conflict mitigation: This examines CSR effectiveness in addressing conflicts between the oil host communities and oil companies. Indicator include measuring the reductions in disputes or disruptions or protest incidents.

- Environmental protection: This assesses the extent to which the initiatives on CSR address environmental concerns due to the oil and gas operations by the companies. Indicators cover superior waste disposal practices, green-friendly technology adoptions, pollution reductions, reforestation projects, and habitation restorations.

- Human rights: This assesses the observance of human rights policies and standards such as labour rights including forced labour prevention or child labour. By this indicator, CSR policies and initiatives will uphold business ethical practices.

- Local content utilization: This assesses the extent that the local workers and companies benefit from the oil and gas sector activities. Indicators include workforce composition, local suppliers proportion, and skills and vocational development plans for example, to address unemployment and poverty for sustainable development drive.

- Long-term impact: This evaluates the extent to which CSR initiatives are durable and their long-term but not short-term impact as real commitment on environmental protection, social and community development.

- Social investment: This quantifies the financial contributions companies make to social programmes and projects such as in education (scholarships), healthcare (clinics), etc., mainly in the oil and gas host communities.

- Stakeholder engagement: This assesses inclusiveness, rate, effectiveness and quality of stakeholder engagement such as with regulatory bodies, civil society organizations, and local communities involvement and representation in the process of decision-making. Strong stakeholders’ engagements ensure CSR-based initiatives will address their true concerns and needs towards sustainable development.

4.3.2. Key indicators for monitoring and evaluating taxation using the PIA

The key indicators for evaluating taxation in Nigeria's upstream oil and gas sector through the PIA are important yardsticks providing better insights into taxation compliance, transparency, and tax revenue management. The indicators are drawn from the various literature reviewed and observation support for evaluating taxation practices alignment with the PIA’s provisions and sustainable development objectives and outcomes. Basically, tracking the indicators can help the government to optimize tax revenue collection for financing sustainable development. Some key taxation indicators comprise:

- Anti-avoidance measures: This examines the adoption of anti-tax avoidance practice to mitigate tax revenue leakage consistent with the aim of the PIA's taxation transparency.

- Local content development levy: This measures the local content development fund and its funding as a commitment to building local capacity and sector’s development.

- Revenue utilization: This evaluates the application of tax revenues for the provision of sustainable development projects for infrastructure and community development.

- Royalty payments: This evaluates the adherence to the obligations to pay royalty in the PIA. This should be consistently monitoring for improved revenue generation.

- Tax compliance rate and reporting: This assesses the extent to which tax regulations and reporting accuracy are being complied with as provided in the PIA. Indicators comprise timely filing of tax return, accurate tax payment, proper business income reporting, and correct tax registration.

- Tax contribution to government revenue: This quantifies tax contributions of the sector to government revenue collection. Indicator evaluates how taxation may align with the sector’s economic importance and the tax revenue maximization objectives of the PIA.

- Tax incentives utilization: This examines how tax incentives as provided in the PIA are being used. It assesses whether or not the companies benefit from incentives for the growth of the sector and not compromising the revenue payable to the government.

- Tax revenue transparency: This assesses transparency levels of tax revenue disclosures and reporting based on what the oil and gas companies may have generated. Indicator is to ensure availability of information that can be truly accurate and often accessible.

- Transfer pricing: This assesses the intra-group transactions and mechanisms for pricing transparency. Proper controls should be set to mitigate tax avoidance and evasion risks for more revenue generation to finance sustainable development.

4.3.3. Integrated framework for monitoring and evaluating PIA’s impact in Nigeria

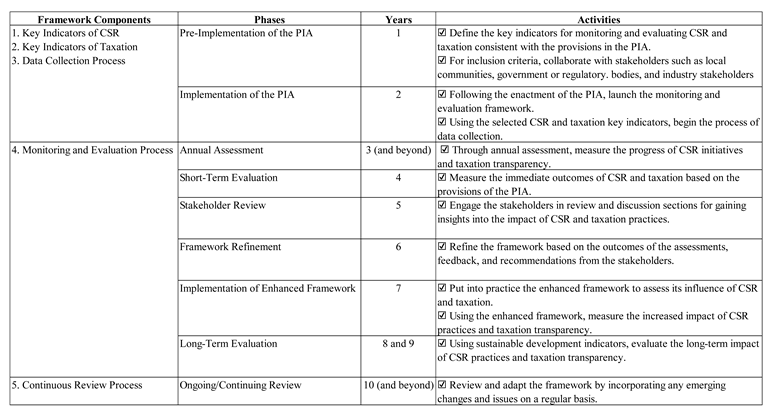

The integrated framework for monitoring and evaluating the PIA’s impact in Nigeria's upstream oil and gas sector presents a broad but detailed approach for determining the outcomes of CSR and taxation practices. The framework in Table 1 below has important components and various phases. The framework is necessary since tax incentives inspire companies’ CSR performance but should be monitored for the effective implementation of the PIA [27]. Based on feedback mechanisms and flexibility, the framework will be responsive to the needs and dynamism of the oil and gas sector in Nigeria. By integrating CSR and taxation main features, the framework will help in assessing aspects of social, economic, and environmental concerns consistent with the principles of sustainable development. This can provide a detailed understanding of the PIA's impact in contributing to the sustainable development of Nigeria’s oil and gas sector. Also, the timeframe (in phases) and milestones (in years) are provided in the integrated framework for monitoring and evaluating PIA’s impact of CSR and taxation over time (Table 1 below). While the integrated framework is consistent with the objective of PIA in ensuring transparency, accountability, and sustainable development in Nigeria; it combines the key indicators for CSR and taxation practices, which gives an organized strategy to evaluate the impact of the PIA on Nigeria's upstream oil and gas sector over a duration of ten years.

Table 1.

Integrated framework for monitoring and evaluating PIA’s impact.

|

Source: Author.

The framework flexibility and adaptation involved the ability of the monitoring and evaluation integrated framework to counter emerging priorities and challenges and changing situations in the Nigerian oil and gas sector. Because the sector’s stakeholders’ expectations, regulatory and business environments may over time change, the framework is thus adaptable and flexible to support future refinements or adjustments depending on evolving needs and information. While framework flexibility supports the framework's various assessment techniques, indicators, and components to be adapted, this ensures that the evolving insights and issues are accommodated. For example, if further CSR and/or taxation practices and laws are introduced, the framework can integrate such changes towards ensuring its significance. However, adaptation is connected to the ability of the framework to accommodate changing priorities and unexpected challenges. For example, if CSR initiatives and/or taxation transparency are impacted by external factors, the framework is adjustable to effectively address such challenges. Consequently, by flexibility and adaptation, the integrated framework for monitoring and evaluating the impact of the PIA provisions on CSR and taxation practices will remain effective and responsive to contribute to the sustainable development of Nigeria’s upstream oil and gas sector in practice. Moreover, the framework flexibility and adaptation advantages comprise:

- Allowing for greater sensitivity of the sector’s changes and dynamisms.

- Ensuring that the framework continues to be effective and relevant over time.

- Allowing the integration of additional and new indicators, best practices, and data.

- Enriching ability of the framework in making contributions to sustainable development.

Whereas the framework flexibility and adaptation clearly provide the details of the criteria and process how changes can be made to the integrated framework, its primary components are consistent and cannot be altered. Framework flexibility and adaptation constitute the guidelines for adjusting the integrated framework yet keeping its integrity including:

- Identification of events or trigger points that may explicitly prompt potential adjustment or review to the framework. Triggers may comprise industry trends, regulatory changes, stakeholders’ feedback, or major alterations in priorities of sustainable development.

- Having identified the trigger points, then a detailed assessment should be done to decide the need for the framework’s adaptation. Additional and new challenges, opportunities, and information should justify the necessity for the changes that may have occurred.

- Engagement of the stakeholders in the process of decision-making is necessary for their input. So, relevant stakeholders including the civil society organizations, government bodies, and industry professionals should be consulted for perspectives and insights on the framework’s likely adaptations.

- After stakeholders’ engagements, then specific changes to the framework are proposed with a plan of alignment of such changes with the initial objectives towards enhancing the effectiveness of the framework in adopting evolving issues.

- Proposed changes should be internally reviewed and the approval of the relevant bodies or authorities governing the implementation of the framework should be sought.

- Updated framework based on its adaptation should be properly communicated to the stakeholders including clear plans for implementation, rationale, and expected impacts.

Based on the critical analysis of the PIA’s provisions on CSR and taxation in Nigeria’s upstream oil and gas sector, this study’s findings reinforced the development of an integrated framework for monitoring and evaluating PIA’s impact on CSR and taxation over time. Components of the integrated framework are the key indicators of CSR, key indicators of taxation, data collection process, monitoring and evaluation process, and continuous review process. These components comprise phases with their activities: pre-implementation, implementation, annual assessment, short-term evaluation, stakeholder review, framework refinement, implementation of enhanced framework, long-term evaluation, and ongoing review (Table 1 above). The framework is a structured strategy for stakeholders to utilize in evaluating the impact of the PIA on CSR and taxation over time regarding sustainable development in Nigeria’s upstream oil and gas sector.

4.4. Recommendations for addressing the implementation challenges and using the improvement opportunities identified to enhance the PIA's impact

The analysis of the impact of the PIA provisions on CSR and taxation in Nigeria's upstream oil and gas sector discloses various challenges and improvement opportunities. Recommendations for improving the Act’s effectiveness for promoting sustainable development of the sector are:

4.4.1. Recommendations for addressing the implementation challenges of the PIA

The recommendations below can be collectively, properly, and effectively adopted to address the implementation challenges of the provisions of the PIA on CSR and taxation for promoting sustainable development in Nigeria’s upstream oil and gas sector [2] including:

- Simplification and regulatory standardization: The provisions of the PIA's should be further simplified and made clear while controlling for industry terminologies that can facilitate understanding and application of the Act. Thus, stakeholders in the oil and gas sector should be consulted to standardize the PIA’s application and interpretation. PIA’s vagueness and compliance can be improved by providing clear and succinct guidelines in it, defining specific CSR initiatives and taxation duties for the companies.

- Awareness promotion: Large-scale awareness should be promoted towards educating the oil and gas sector’s stakeholders mainly on the requirements of the PIA concerning CSR and taxation. Such awareness should emphasize the relevance of ethical business practices and the impact of CSR and taxation on oil host communities for sustainable development in Nigeria.

- Monitoring and strategic enforcement: A robust monitoring and strategic enforcement system should be created that can help in tracking CSR and taxation practices of the companies. Using technological solutions can support transparency in data collection, analysis, reporting, verification, sharing, and rapid remedial actions against differences in real-time. Thus, PIA’s help for establishing strong monitoring mechanisms to monitor CSR activities and taxation compliance should be sustained to ensure the timely double-checking of transactions on a daily basis.