Submitted:

19 September 2023

Posted:

19 September 2023

You are already at the latest version

Abstract

This study investigates the relationship between energy metals and precious metals to assess their suitability as safe haven assets in clean energy investment portfolios. It focuses on the impact of events in 2020 and 2022, characterized by substantial investments in clean energy. The research reveals that, except for Nickel Futures (NICKELc1), energy metals are positively linked with clean energy indexes. This suggests that they can serve as a secure investment option for green investors looking to diversify their portfolios. As a result, the study dismisses the initial question, indicating that energy metals can indeed be considered safe havens within the context of clean energy investments. Additionally, the research reinforces prior findings that precious metals like gold, silver, and platinum possess safe haven characteristics in relation to specific clean energy stock indexes. These results have significant implications, particularly given the increasing investments in clean energy stocks and the recurring uncertainties in the market. In summary, this study supports the idea that both energy metals and precious metals can play valuable roles in clean energy portfolios, providing stability during turbulent times in the market.

Keywords:

Clean Energy Stocks

; Energy Metals

; Gold

; Silver

; Platina

; Safe Haven

1. Introduction

The acknowledgment of climate change as a pressing global concern has prompted the implementation of several laws and programs with the objective of mitigating greenhouse gas emissions (GHGs) and facilitating the shift towards cleaner sources of energy. Consequently, there has been a notable surge in investments in clean energy technology, including solar energy, wind power, electric vehicles, and energy efficiency solutions. Consequently, the clean energy sector has witnessed significant expansion, emerging as a prominent business in its own right. This phenomenon has garnered the interest of not only environmentalists and policymakers but also individuals involved in the financial market, such as investors, traders, and analysts. The discernible environmental and social advantages linked to clean energy have become increasingly apparent, resulting in an amplified desire for investment opportunities that prioritize sustainability. There is a rising concern among investors over the sustainable prospects of conventional sectors reliant on fossil fuels, prompting them to seek potential avenues within the clean energy industry. In addition, the decreasing costs of clean energy technologies have caused a shift in the energy landscape, rendering them more comparable to traditional energy sources. This development has not only enhanced the economic feasibility of clean energy but has also generated prospects for investment with the possibility of favorable returns. Consequently, both institutional and individual investors have been committing substantial financial resources towards clean energy initiatives, thereby fostering the emergence of specialist funds and investment mechanisms that specifically target renewable energy endeavors [1,2,3].

Furthermore, the integration of clean energy into financial markets has been accelerated by the advancement of innovative financial instruments and mechanisms. The popularity of green bonds, which are explicitly allocated to fund environmentally sustainable initiatives, has increased. These bonds give investors the chance to contribute to clean energy initiatives while simultaneously yielding financial gains. The interplay between financial markets and the clean energy sector has a complex and diverse nature. The expansion of the clean energy industry is subject to the effects exerted by financial market dynamics. The availability and cost of funding for clean energy projects can be influenced by various factors, including investor sentiments, access to cash, and regulatory systems. The ratings of clean energy companies and the general impression of the sector's appeal can also be influenced by financial market developments and investor behavior. Conversely, the field of clean energy possesses the potential to impact the financial markets. The adoption of cleaner energy sources has the potential to hinder the growth of traditional energy markets, causing shifts in the assessment of fossil fuel corporations and their associated assets. Moreover, the growing incorporation of clean energy technology across diverse sectors has the ability to provide new investment opportunities and reshape market dynamics [4,5,6].

The expansion of the clean energy sector is accompanied by a corresponding increase in the demand for raw materials necessary for the production of clean energy solutions. Metals play a crucial role as essential raw materials in the production of clean energy solutions, hence rendering them exposed to significant increased demand owing to the widespread adoption of clean energy technology. Based on this fact, it is anticipated that the prices and broader market dynamics of energy metals could experience substantial transformations, influencing the interplay between these metals and the clean energy markets. Investors with substantial capital investments in the clean energy markets exhibit a keen interest in understanding the relationship between clean energy companies and energy metals. A precise understanding of this connection proves beneficial in mitigating the risk associated with clean energy assets. The significance of this matter arises from the fact that clean energy stocks are perceived as a very new asset class, resulting in heightened market volatility [7,8]. Therefore, it is essential to understand the strategies employed by environmentally conscious investors in order to effectively diversify their portfolios and mitigate the inherent risks connected with clean energy indexes. The above analyses are important for policymakers because they can use the results of our research to come up with good coverage measures to reduce the risk of contagion that could come from how volatile commodity markets are.

There is a limited body of research on hedge strategies pertaining to investors that possess assets in clean energy markets. Previous research has overlooked the evaluation of energy metal coverage performance and the potential risks entailed by portfolios incorporating clean energy assets. While there exists an expanding corpus of scholarly works pertaining to material flows, supply limitations, and the significance of metals in the context of the energy transition, the investigation into the relationship between clean energy assets and metals remains relatively limited in the existing literature. Furthermore, it is important to note that these studies often overlook energy metals and clean energy markets, despite the substantial use of metals as primary resources in clean energy technology. This knowledge gap highlights the need for more research to better understand and address risk management strategies for investors in clean energy markets [9]. The study [10] and [11] have conducted noteworthy studies examining the relationship between clean energy stock prices and metal prices. However, it is important to note that their investigations are constrained by their focus on particular linkages and metals. In [10] study, the GARCH-jump method was used to figure out how the uncertainty in the silver market, as shown by the silver volatility index (VXSLV), affected solar stock indexes around the world. The author suggests that there is a detrimental impact of VXSLV on the stock indexes that are being examined. The findings show that an upward trend in the volatility of the silver market could potentially disrupt the operations of the solar energy industry. Furthermore, [11] conducted an analysis on the interdependence and causal relationship between cross-quantiles of non-ferrous metals and clean energy indexes. Their findings revealed that the conditional dependence among these assets is time-varying and exhibits asymmetry in terms of tail dependence potential. Given the preceding discourse and the existing research gap pertaining to the link between clean energy stock indexes and energy metals, this study aims to examine if energy metals serve as safe havens for clean energy stocks. To the best of our knowledge, this study is the first attempt to examine the relationship between clean energy stock returns and the prices of energy metals that are sensitive to the growing demand for clean energy solutions. In addition, we evaluate the extent to which precious metals can be regarded as secure investment options for environmentally conscious investors that incorporate clean energy indexes into their investment portfolios.

Our research falls within the domain of safe haven properties, specifically focusing on gold [12,13,14] and silver [15,16,17]. However, our study distinguishes itself by employing long-term relationship models, specifically the [18], to examine a particularly tumultuous period in the global economy. This methodology is robust in extremely volatile financial markets since the authors modify the typical tests by assuming that the co-integration vector changes at an unknown date. The main findings show that, with the exception of Nickel Futures (NICKELc1), precious metals have a positive relationship with clean energy stock indexes, indicating that precious metals are a safe haven for green investors looking to rebalance their portfolios during extreme market events such as the 2020 global pandemic and the Russian invasion of Ukraine in 2022.

The present study is structured into 6 distinct sections. Section 2 provides an overview of the existing body of literature pertaining to clean energy stocks, the characteristics of metals as secure haven assets, and the linkage between clean energy stocks and metals. The data and method are outlined in Section 3. Section 4 provides a comprehensive overview and critical examination of the research outcomes. In this section, we will engage in a comprehensive discussion. Section 6 presents its final analysis. Finally, Section 7 discusses the practical implications.

2. Literature Review

In recent decades, the shift to a carbon-resilient economy has piqued the interest of academics, investors, and financial institutions alike. This transition entails shifting away from traditional carbon-intensive forms of energy like coal and oil and toward cleaner, more sustainable energy sources like solar and wind energy. The Paris climate accord, reached in 2015, was a major driver of this transformation since it set a goal of keeping global warming to less than 2 degrees Celsius above pre-industrial levels, with the goal of reducing warming to 1.5 degrees. This target cannot be met unless greenhouse gas emissions are significantly reduced, particularly in the energy sector. The United Nations Climate Change Conference (COP26), held in November 2021, marked a watershed point in the worldwide struggle to combat climate change. One of the most difficult aspects of this transition is balancing the immediate economic benefits of old energy sources with their long-term environmental implications. Many businesses and investors are beginning to recognize the hazards of investing in carbon-intensive industries, as the costs of carbon emissions are expected to rise with time, making these investments less appealing. Simultaneously, the transition to clean energy creates huge prospects for investors, particularly in renewable energy, energy efficiency, and low-carbon transportation [19,20,21,22,23].

2.1. Prices Of Renewable And Conventional Energy Stocks

Green investors are concerned about the environmental and long-term consequences of increasing dirty energy usage. Investors must monitor the performance of their clean and dirty energy stock indexes in order to measure the impact of their investments and understand the offsets between clean and dirty energy. Clean energy indexes contain corporations that use renewable energy and sustainable technology, whereas dirty energy indexes include companies that use fossil fuels and contribute to environmental deterioration. Investors can match their portfolios with sustainability goals, make informed financial decisions, anticipate legislative changes, and grab emerging opportunities in the growing energy sector by analyzing these trade-offs. Investors can examine the environmental impact of their investments by examining financial performance, policy and regulatory situations, and navigating the energy transition. This overview establishes the groundwork for a more in-depth examination of these asset classes and their implications for investors in the evolving financial and clean energy markets [24,25,26,27].

The study [28,29,30,31] investigated the impact of oil and technology shares on clean energy stock indexes. According to [28], high oil prices favor clean energy companies due to replacement. In addition to the price of oil, the authors incorporate interest rates and the price of technology stocks. Surprisingly, the data shows that oil prices have no impact on clean energy stock prices; however, shocks in technology company prices have an impact on clean energy stock prices. Furthermore, [29] stated that raising conventional energy prices and/or imposing a carbon tax would boost investment in clean energy companies. The authors contend that the prices of oil and technology shares have different effects on the stock prices of clean energy companies. While [32] investigated the risk factors of renewable energy companies using a variable beta model. Empirical evidence suggests that increased corporate sales have a negative influence on company risk, whereas rising oil prices have a favorable impact on company risk. When oil price returns are positive and moderate, sales growth can offset the impact of the oil price return, resulting in decreased systematic risk. According to the author, the high price of oil raises the systematic risk for clean energy companies. The authors [31] analyzed the relationships between oil prices, clean energy stock prices, and technology stock prices. The findings reveal that there was a fundamental change at the end of 2007, during which time the price of oil rose significantly. Unlike earlier research, the authors find a positive link between oil prices and clean energy prices following structural crashes. There appears to be a resemblance in market reaction between clean energy company prices and technology stock prices.

The research [33,34,35], and [36] focused on the long-term and short-term shocks between clean energy stock indexes and "dirty" energy stock indexes. The work [33] analyzed the long-term relationship between alternative energy company stock values and oil prices. They employed threshold co-integration tests to accomplish this, which endogenously integrate potential regime changes in the long-term relationship of the underlying variables. The presence of co-integration of variables with two endogenous structural breaks is indicated by the authors. This study indicates that neglecting structural breaks in long time series data can result in spores. In terms of causality, while the prices of alternative energy company’s stocks are affected by the prices of technology shares, oil prices, and short-term interest rates, there is no long-term causality between the prices of alternative energy shares. The study [34] discovered that the oil and renewable energy markets are not inextricably linked, implying that the development of renewables companies is less affected by oil price shocks. From March 2010 to February 2020, [37] investigated the volatility transmission between SPGCE (S&P Global Clean Energy), SPGO (S&P Global Oil), two non-renewable energy commodities (natural gas and crude oil), and three crude petroleum distillation products (heating oil, petrol, and propane). The empirical findings show a great deal of variation in overflow patterns of returns, volatility, and shocks. The authors emphasize the benefits of dynamic diversification of energy commodities, particularly heating oil, to energy-related stock markets. They also discovered that the SPGCE and SPGO stocks had the highest average ideal weight and coverage effectiveness, implying that the positive performance of the SPGSE stocks significantly compensates for the negative performance of the SPGO stocks. [38] examined energy stock and price indexes such as the S&P Global Clean Energy Index (GCE), the WilderHill Clean Energy Index (ECO), the S&P/TSX Renewable Energy and Clean Technology Index (TXCT), the S&P 500, WTI crude oil, and natural gas prices Henry Hub (HH). The findings reveal that the correlations between WTI, GCE, ECO, and natural gas (HH) prices are positive and expanding as a function of the respective energy prices. It appears logical since the values of renewable energy, which sells electricity on the spot market, are valued by rising energy costs, given that electricity spot prices rise in lockstep with energy prices.

Recently, the authors [39,40], and [41] examined the long- and short-term shocks between clean energy stock indexes and assets classified as dirty. The study by [39] investigated the co-movements between clean and dirty energy indexes before and during the COVID-19 pandemic. The study examines the interdependence of the underlying markets by employing a large sample of dirty energies such as crude oil, heating oil, diesel, gasoline, and natural gas, while the clean energy market is represented by the S&P Global Clean Energy index and the WilderHill Clean Energy index. The findings reveal that while there are few instances of strong co-movements between dirty and clean energy markets in the short term, there are a few instances of high co-movements between dirty and clean energy markets in the long term. In the same vein, [40] evaluated the movements of the clean and dirty energy markets, indicating considerable shocks between the analyzed energy indexes and thus testing the possibility of portfolio diversification. Furthermore, [41] investigated whether the eventual increase in correlation caused by the events of 2020 and 2022 causes volatility between clean energy indexes and cryptocurrencies classified as "dirty" due to their energy-intensive extraction and transaction procedures. According to the empirical findings, clean energy stock indexes can provide a sustainable safe haven for dirty energy cryptocurrencies. However, the precise associations vary depending on the digital coin under consideration. The implications of the study's findings for investment strategies are important, and this knowledge can inform decision-making processes and encourage the adoption of sustainable investment practices. Investors and policymakers can acquire better knowledge of how clean energy investments interact with the cryptocurrency market.

2.2. Precious Metals as Hedge for Stocks

The authors, [42], conducted a study to establish testable definitions for gold as a hedge, diversifier, and safe port asset. These definitions were used to see if gold served as a safe haven for stocks and commodities. The authors defined a hedge in their study as an asset that is not or is adversely associated with another asset on average. A diversifier, on the other hand, is described as an asset that is favorably associated with another asset on average but not perfectly. Finally, during market shocks, a safe haven was defined as an asset that was not correlated or negatively correlated with another asset. The study's findings demonstrated that gold acts as an effective safe haven for stocks, but only for about 15 working days after a substantial negative shock in the stock markets of the United States, the United Kingdom, and Germany. Furthermore, the findings revealed that gold operates as a hedge for American and British markets but not for German stocks. Furthermore, the analysis discovered that gold is a more effective hedge during low markets than it is during strong markets in the three stock markets. Overall, [42] research provides empirical evidence that gold can be used as a shelter asset and a hedge for stocks, with its usefulness altering depending on market conditions and geographical setting.

The authors publications, [43,44], and [45], all use gold's features as a safe haven asset for international stock markets. The authors explored the extent to which gold provides financial stability and its association with stock markets. The work [43] add to our understanding of gold as a safe haven by investigating its level of stock protection. The study examines 53 international stock exchanges and distinguishes between weak and strong safe havens. According to the findings, gold serves as a robust safe haven for the majority of established stock markets studied. However, the findings indicate that gold tends to follow stock markets amid extreme shocks in global financial markets, implying that it is just a marginal safe haven for stock market risk. The author [46] used a smooth transition regression model to build on the work of [43]. This method allows them to evaluate gold as a hedge as well as a safe haven, separating the regression model into two regimes. The authors examine data from 18 developed-country markets and 5 regional indexes. The authors conclude that gold is a weak hedge and a safe haven in most circumstances, noting that the usefulness of gold as a hedge or safe haven is dependent on the current economic environment. The study [47] analyze the association between gold and US aggregate stocks, as well as US energy stocks, in keeping with earlier research. His findings reinforce the assumption that gold serves as a safe haven asset for the US equity market as a whole. During financial crises, the authors demonstrate the presence of a negative association between gold and US stocks. The findings also show that the return correlations between commodities and stock markets vary significantly over time. Specifically, the negative association between gold and US stocks appears to have been stronger during the Dot-Com bubble than after the US real estate bubble. Overall, these studies provide useful information about gold's role as a safe haven asset for international stock markets.

The study [48] investigated gold's hedge and safe haven characteristics with respect to Dow Jones stock industry indexes. The sample period was divided into two subperiods for this reason, and the results demonstrate that gold's hedge and safe port features are changeable. Gold has not been a hedge for oil and gas, commodities, or utilities for the entire period (1980–2017); gold has been a safe haven for practically all markets except technology. During subperiod I (1980–1995), gold was a safe haven for all industries rather than a hedge for oil and gas. Gold is not a hedge for oil and gas, commodities, and utilities in Subperiod II (1996–2017), nor is it a safe haven for oil and gas. Furthermore, [49] attempted to examine if gold protects investors in Pakistan from the risks associated with exchange rates, oil shocks, and stock returns by assessing the hedging and safe haven characteristics of gold returns from August 1997 to May 2016. The key findings show that gold only acts as a hedge against foreign exchange risk while also acting as a safe haven in terms of the risks associated with oil shocks, exchange rates, and the stock market, implying that investors can potentially invest in gold to protect themselves against exchange-rate losses.

The development of clean energy-related stock indexes in recent years has transformed the way investors track and evaluate the performance of open-source enterprises in the clean energy sector. These indexes have developed into useful portfolio management tools, providing insight into the growth and potential of clean energy investments [50,51,52]. The authors, [52], investigated whether gold and crude oil can be considered safe harbor assets in relation to the clean energy stock indexes, S&P Global Clean Energy and WilderHill Clean Energy, and concluded that both raw oil and gold are weak safe harbor assets for clean energy indexes. The study by [50] investigated the possibility of mixing clean energy stock and emission allowance indexes in a portfolio with dirty energy assets to lessen the risk of a drop. The authors demonstrate that investing in clean energy companies is beneficial not just to a sustainable energy transition to renewable sources but also to their financial appeal. The authors [53] findings provided insight on the dynamic nature of asset connections. In their investigation, Bitcoin, gold, exchanges, and natural gas appear as volatility transmitters, showing their influence on market volatility transmission. Crude oil and stock markets, on the other hand, operate as shock sensors, indicating their vulnerability to exogenous shocks and volatility. Understanding the relationship between clean energy stock indexes, cryptocurrencies, and other assets can provide useful information for investors looking to diversify their portfolios and capitalize on new opportunities.

Recently, the authors [54] explored if gold, USD, and Bitcoin are hedging assets and safe havens for stocks and whether they are effective in risk diversification when international stock markets fail. According to the study's findings, the USD is the most valuable hedging and safe-haven asset, followed closely by gold, and Bitcoin is the least valuable. It should also be emphasized that the proposed combined method outperforms in terms of decreasing the risk of portfolio declines. Furthermore, [55] investigated if gold serves as a hedge or safe haven for the key stock markets in the Middle East and North Africa region. The findings demonstrate a high correlation between gold and stock performance. When both the gold and MENA stock markets are rising, there is a positive link. Given the risk of spillover between gold and stock markets, MENA investors should exercise caution when using gold as a safe haven since its efficiency as a hedge varies between MENA stock markets. In addition, [56] investigated the hedge, safe haven, and diversification properties of Islamic indexes, Bitcoin, and gold, as well as in ten of the coronavirus-affected countries: the United States, Brazil, the United Kingdom, Italy, Spain, Germany, France, Russia, China, and Malaysia. In all nations analyzed throughout the COVID-19 pandemic crisis period, empirical results show that Islamic indexes are not regarded as hedge assets for the mainstream market. Gold, on the other hand, serves as a powerful hedge in all countries except Brazil and Malaysia. Bitcoin is a good hedge in the United States, as well as a strong hedge and safe harbor in China. Furthermore, [57] investigated FAANA shares (Facebook, Apple, Amazon, Netflix, and Alphabet) and found that they delivered positive returns with extraordinary durability during the pandemic period, indicating a shift in their investment risk. In this paper, we depart from previous research by examining the hedging, diversification, and safe harbor features of FAANA stocks against four alternative assets: gold, US Treasury securities, Bitcoin, and the USD/CHF. Throughout the sample period, the majority of FAANA shares served as a weak or strong safe haven against gold, Treasury bonds, Bitcoin, and the USD/CHF. Furthermore, during the epidemic, FAANA shares served as safe havens against the US Treasury and the USD/CHF. According to the authors, FAANA, which was originally deemed a risky high-tech action, matured, and became a safe haven throughout the recent stormy period.

3. Materials and Methods

3.1. Materials

The inclusion of energy metals such as aluminum, copper, and nickel is appropriate because they are commodities with transparent price systems that are widely traded. Furthermore, the anticipated shock in the hunt for clean energy solutions helps to support the inclusion of these metals in the study. Aluminum, copper, and nickel play critical roles in a wide range of sustainable energy technologies, including electric vehicles (EVs), wind turbines, solar panels, and energy storage devices. The study includes gold, silver, and platinum for comparison purposes because their covering and safe port features are well known. In the purpose of this study, clean energy is used as a generic term to describe companies that potentially gain significantly from a shift in society toward reducing emissions and pollution caused by energy consumption.

Table 1.

The article's indexes for dirty and clean energy stocks.

| Indexes | Definitions | |

|---|---|---|

| WilderHill Clean Energy | ECO | The purpose of this index is to represent the success of clean energy enterprises in the United States. |

| S&P Global Clean Energy | SPGTCLEN | This index, which is part of the S&P 500 and Dow Jones Indexes, measures the performance of global clean energy companies. |

| Nasdaq Clean Edge Green Energy | CEXX | It is an index that tracks the performance of green energy companies listed on the NASDAQ market. |

| Gold | XAU | The international symbol for gold in financial markets is the XAU. Gold is a precious metal that is traded in international troy ounce commodities markets (31.1035 grams) and is commonly utilized as a hedge asset and safe haven. |

| Silver | XAG | The chemical symbol XAG is used to represent silver in financial markets and price quotations around the world. Silver's price, like gold's, is stated in international commodities markets and is measured per troy ounce (31.1035 grams). Silver, like gold, is seen as a safe haven in times of economic uncertainty and financial market instability. |

| Platinum | XPT | The XPT is both the chemical symbol and the symbol used to symbolize platinum in financial markets around the world. Platinum, like gold and silver, is a precious metal that may be utilized in a range of industrial applications. Its price is measured in troy ounces (31,1035 grams). |

| Aluminum | MAL3 | Aluminum is a metal that is utilized in a variety of industrial and consumer purposes, but its primary market commercialization happens through futures and options in the primary material markets. |

| Nickel Futures | NICKELc1 | Nickel is a metal that is used in a range of industrial applications, including the production of stainless steel and batteries, and its price is affected by a variety of factors, including industrial demand, supply, and worldwide demand. |

| Copper Futures | HGU3 | Copper futures are traded on commodities exchanges and are denoted by unique symbols such as "HGU3." The symbol "HG" stands for copper, while "U3" stands for the month and year in which the futures contract expires. In this scenario, "U3" could indicate a copper futures contract with a maturity date of September 2023, but it is important to double-check the specific maturity date because these contracts have multiple maturities throughout the year. |

Source: Own elaboration

The data used for the study was obtained from the Thomson Reuters Eikon database and spans the period from July 13, 2018, to July 11, 2023. To eliminate currency distortions and ensure a consistent comparison of the various assets and indexes, all prices in the study are quoted in US dollars. The sample was separated into two subperiods: Tranquil, which includes the years from July 2018 to December 2019, and Stress, which includes the years from January 2020 to July 2023, as well as the COVID-19 pandemic and the Russian invasion of Ukraine in 2022.

The study by [58] suggests employing return series rather than price series to examine the behavior of financial markets, because investors are primarily interested in the returns of an asset or asset portfolio. In complementarity, the returns series have statistical features that facilitate the analytical approach, especially stationarity, which is not typically present in price series. For the reasons stated above, the series of price indexes have been adjusted in terms of growth rates or differences in the Neperian logarithms of current and past returns, of logarithmic, instantaneous, or continuously constructed returns using the following expression:

where is the profit rate on day and and are the series closing prices at days and , respectively.

3.2. Methods

The present study will be conducted in multiple phases. For the initial phase of sample characterization, we will employ fundamental descriptive statistical measures. Additionally, we will use the [59] adhesion test, which assumes the normality of the time series, as well as the [60] test for autocorrelation of the residuals. In order to ascertain the stability of the residues, we will employ the CUSUM tests proposed by [61] for estimation purposes. To assess the validity of the stationarity assumption in the time series, we will employ the summary table that includes the methodologies proposed by [62,63], and [64]. Additionally, we will validate the results using the tests developed by [65] and [66], incorporating the Fisher Chi-square transformation and [67] approach. The test statistic in question follows a chi-square distribution, and its significance level is employed to ascertain the presence of a unit root. In contrast, the Choi Z-stat variant of the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) tests presents an alternate methodology wherein the test statistics are estimated using the maximum likelihood estimation of the autoregressive model. In order to ensure the accuracy and reliability of our econometric functions, we will conduct a stability analysis to prevent misleading projections. To accomplish this, we will adopt the methodology proposed by [61], which involves using the CUSUM test to examine any changes in the variance of the normal distribution. This test specifically evaluates the persistence of coefficients within the regression model. The methodology employed for the validation of long-term relationships will be the one proposed by [18], as it is suitable for analyzing a particularly turbulent period in the global economy. The methodology proposed by [18] demonstrates resilience in highly turbulent financial market conditions due to the author's use of a generalized approach to co-integration testing. This approach accounts for the possibility of a change in the co-integration vector at an unknown point in time. The authors investigated four models. The first template includes a level shift (Level):

In where is a , dimensional vector, is , is the independent term before the break, is the independent term change after the break, and Dt is a dummy variable. A time trend is included in the second model (Trend):

In this model, represents the independent term prior to the structure change, and represents the change in the separate term following the break. In comparison to the preceding model, this one includes a regime transition (Regime):

A hypothetical structural change implies that the inclination vector will also change. As a result, the balance ratio moves in synchrony with the level. The authors refer to the third model as the regime transition model.

Finally, the authors provide the fourth model, which appears to complement the previous ones; they add the option of changing structure in a model with segmented time trend (Regime and Trend):

In this scenario, and are the same terms that were presented in the preceding models. The denotes the co-integration of the inclination coefficients, and the denotes a change in the inclination of the coefficients.

4. Results

4.1. Descriptive Statistics

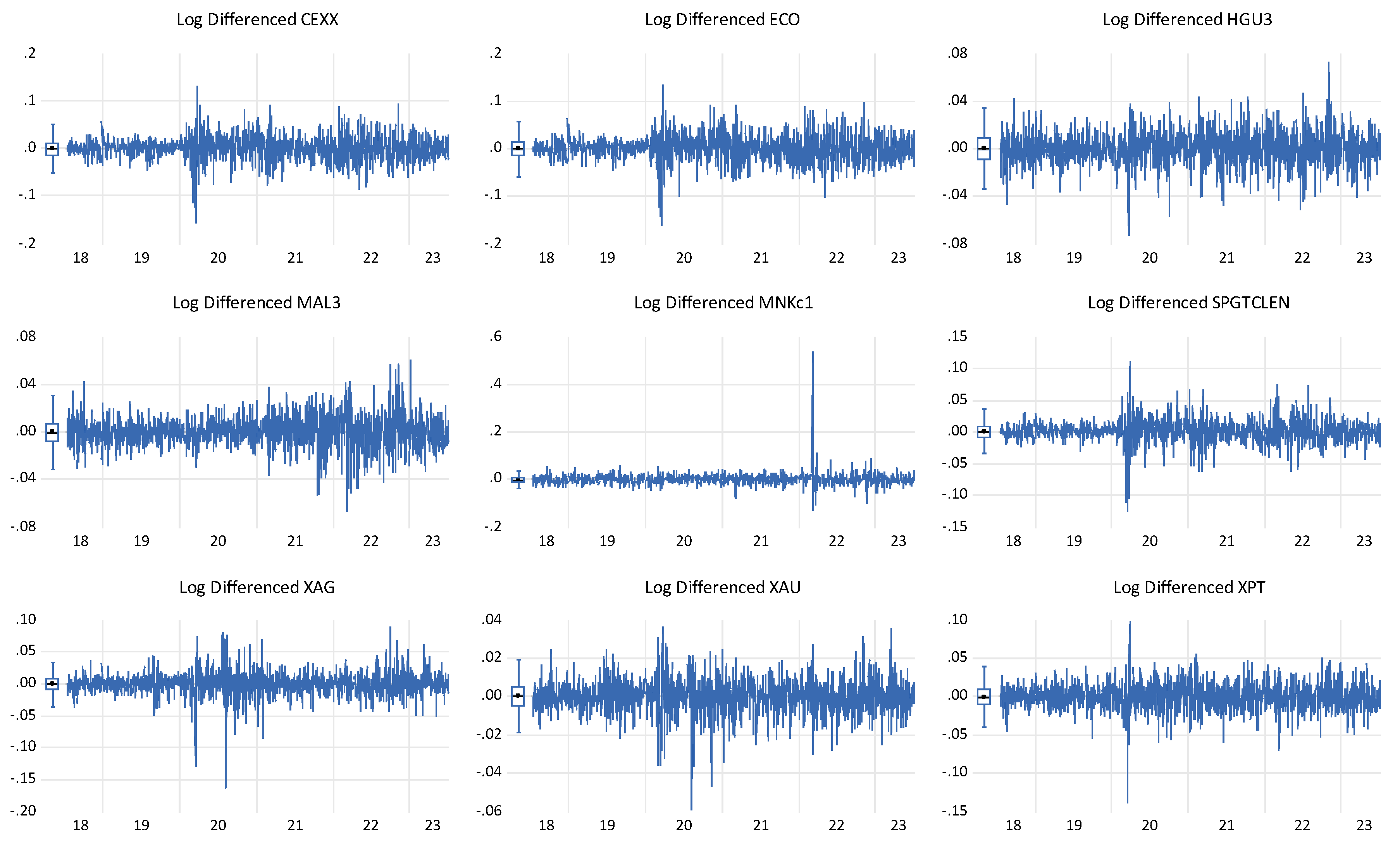

Figure 1 shows the return evolution of energy metals such as Aluminum (MAL3), Nickel Futures (NICKELc1), Copper Futures (HGU3), precious metals such as Gold (XAU), Silver (XAG), Platinum (XPT), and clean energy stock indexes such as the S&P Global Clean Energy Index (SPGTCLEN), Nasdaq Clean Edge Green Energy (CEXX), and WilderHill Clean Energy index (ECO) from February 16, 2018, to February 15, 2023. The indicators examined clearly show significant structural breaks, indicating the volatility to which these markets have been subjected, particularly in the first months of 2020, which coincides with the first wave of the COVID-19 pandemic and the oil price war between Russia and Saudi Arabia. Already in 2022, primarily in the first and second quarters of the year, fluctuations in the time series can be observed, indicating structural breaks, a situation that occurs as a result of the Russian invasion of Ukraine and the resulting concerns about rising associated inflation. The international market findings presented in this study are supported by the research conducted by [24] and [68].

Table 2 presents a summary of the main descriptive statistics, in returns, for various time series, specifically the Aluminum (MAL3), Nickel Futures (NICKELc1), Copper Futures (HGU3), Gold (XAU), Silver (XAG), Platinum (XPT), S&P Global Clean Energy Index (SPGTCLEN), Nasdaq Clean Edge Green Energy (CEXX), and WilderHill Clean Energy Index (ECO). The data covers the period from 16 February 2018 to 15 February 2023. When examining the mean returns, it is evident that the markets exhibit positive values. However, when considering the standard deviation, it becomes apparent that the WilderHill Clean Energy Index (ECO) stock index displays the greatest value (0.027667), indicating a greater level of dispersion in contrast to the mean. To determine if we were dealing with a normal distribution, we assessed the skewness and kurtosis. We observed that the skewness had non-zero values, indicating asymmetry, while the kurtosis had values different from 3, indicating deviation from normality. Specifically, the skewness values were not equal to 0, while the kurtosis values were not equal to 3. To establish validity, we conducted the [59] adherence test and observed that the null hypothesis was rejected at a significance level of 1%.

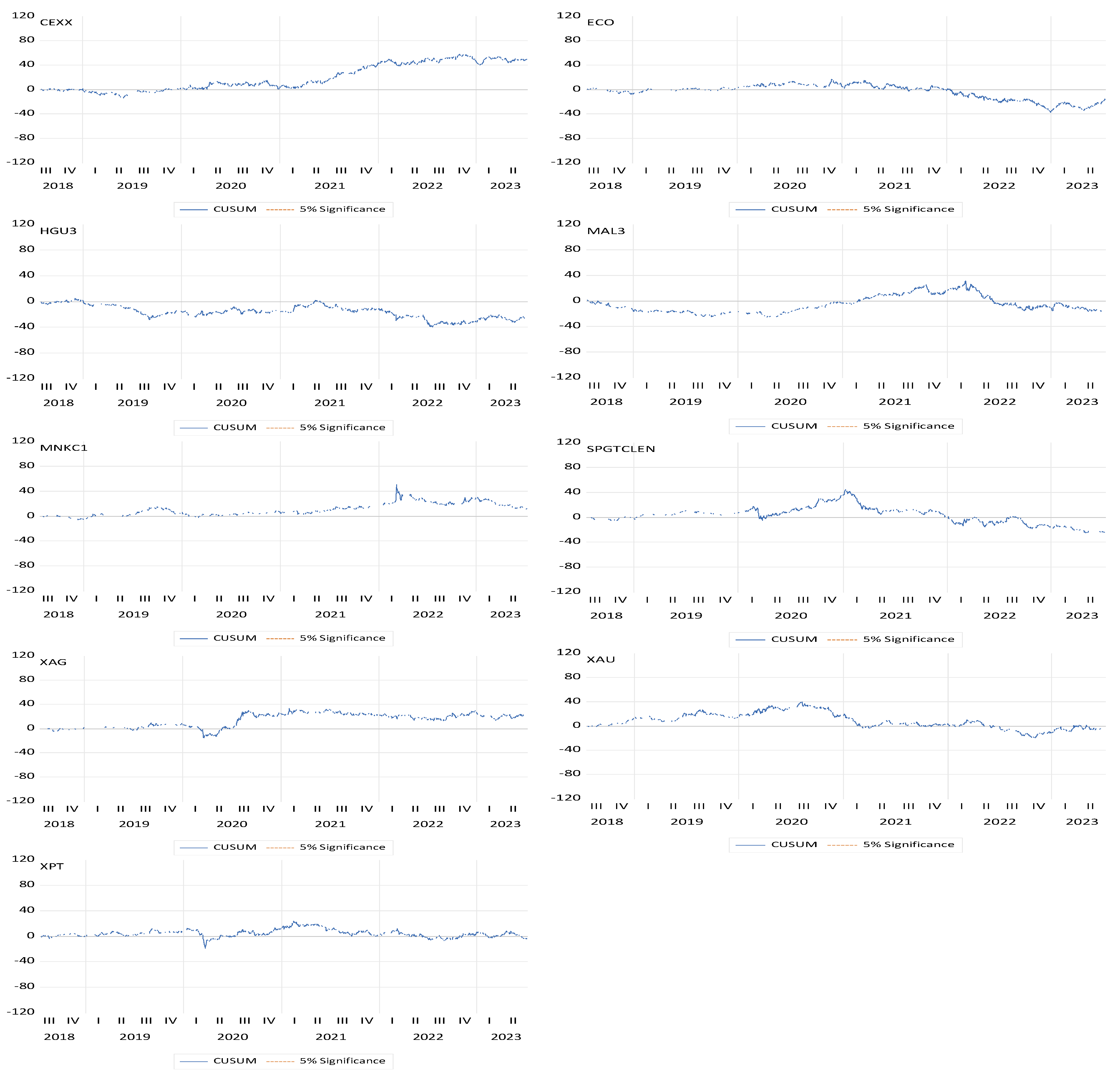

Figure 2 shows the graphical representations of [61] CUSUM method, which is a statistical tool for finding changes in a distribution's variability. The provided dataset consists of the time series for various commodities and indexes, namely Aluminum (MAL3), Nickel Futures (NICKELc1), Copper Futures (HGU3), Gold (XAU), Silver (XAG), Platinum (XPT), S&P Global Clean Energy Index (SPGTCLEN), Nasdaq Clean Edge Green Energy (CEXX), and WilderHill Clean Energy index (ECO). The data spans from February 16, 2018, to February 15, 2023. Upon examining the graphs, it becomes evident that the distribution of returns in the analyzed time series exhibits leptokurtosis and asymmetry, indicating a lack of precise alignment of the data points along the line. Considering the limitations of our ability to determine the precise distribution of the time series being examined, it is possible to make an inference about an essentially normal distribution based on the Central Limit Theorem (CLT). This inference is supported by the fact that the time series was composed of a sufficiently large number of observations.

4.2. Diagnostic

4.2.1. Time Series Stationarity

To assess the validity of the stationarity assumptions in the time series, we conducted panel unit root tests. Specifically, we employed the [62] test, Levin, [63], and [64] to validate the presence of unit roots. Additionally, we used [65] and [69] with the Fisher Chi-square transformation to complete the validation. The time series under consideration includes the price index of Aluminum (MAL3), Nickel Futures (NICKELc1), Copper Futures (HGU3), Gold (XAU), Silver (XAG), Platinum (XPT), S&P Global Clean Energy Index (SPGTCLEN), Nasdaq Clean Edge Green Energy (CEXX), and the WilderHill Clean Energy index (ECO). To ensure stationarity, the original data is transformed into first-order logarithmic differences. The stationarity is then confirmed by rejecting the null hypothesis, at a significance level of 1%, as indicated in Table 3.

4.3. Methodological Results

To answer the research question, we conduct an analysis to determine the suitability of energy metals, including Aluminum (MAL3), Nickel Futures (NICKELc1), Copper Futures (HGU3), and precious metals such as Gold (XAU), Silver (XAG), Platinum (XPT), as safe haven assets for green investors. These investors incorporate clean energy stock indexes, specifically the S&P Global Clean Energy Index (SPGTCLEN), Nasdaq Clean Edge Green Energy (CEXX), and WilderHill Clear Energy Index (ECO), within their investment portfolios.

Table 4 presents a summary of long-term shocks observed during a period of perceived stability. The analysis reveals that the metal Aluminum (MAL3) exhibits 8 significant shocks in the pricing formation of other assets, indicating the full occurrence of all possible shocks. Conversely, MAL3 does not possess the characteristics of a safe haven asset. The Copper Futures (HGU3) energy metal exhibits complementarity by producing 4 shocks, rendering it a safe investment option for the S&P Global Clean Energy Index (SPGTCLEN). However, it does not offer the same level of security as the Gold (XAU), Silver (XAG), WilderHill Clear Energy Index (ECO), and Nasdaq Clean Edge Green Energy (CEXX). Platinum (XPT), a highly valued precious metal, exhibits a notable influence on the fluctuations observed in the prices of aluminum and copper. This phenomenon highlights the inherent stability and reliability of platinum as a safe haven option within the context of clean energy indexes. The CEXX is positioned as a significant contributor to the MAL3 and HGU3. The interaction between XAU and MAL3 confirms the coverage properties with regard to other assets and sustainable energy indexes. The indexes for Nickel Futures (NICKELc1), XAG, and clean energy, namely ECO and SPGTCLEN, do not exhibit any significant impact on the price formation of other assets under consideration. This suggests that these indexes possess safe haven characteristics for green investors seeking to diversify their portfolio risks and optimize their returns.

In the Tranquil subperiod, it is estimated that there were 17 long-term shocks out of a total of 72 probable shocks. The findings of this study show that despite the perceived stability in the global financial markets, there are opportunities for portfolio diversification. Specifically, there are assets that do not significantly impact clean energy indexes. It is observed that the majority of these assets possess the attributes of a safe haven, with the exception of MAL3.

Table 5 shows the findings pertaining to the subperiod of Stress, namely the events occurring in 2020 and 2022. The analysis reveals the occurrence of 18 long-term shocks. Nickel Futures (NICKELc1) can be considered a risky asset in several markets as it has been observed to cause long-term shocks in all of its pairs (8 out of 8 possibilities). However, during the Tranquil period, this asset exhibited the characteristics of a safe haven. Copper Futures (HGU3) present shocks with NICKELc1, Gold (XAU), and Platinum (XPT), which act as a safe investment option for green investors. XPT induces shocks in HGU3 and Silver (XAG). XAU exerts an influence on the formation of copper prices, whereas Aluminum (MAL3) has an impact on the price of NICKELc1. The influence of XAG on the price formation of any asset is negligible, indicating its safe haven characteristics during moments of economic uncertainty in the global economy. Furthermore, it is important to acknowledge that the stock indexes related to clean energy exhibit shock-emitting characteristics. Specifically, the S&P Global Clean Energy Index (SPGTCLEN) impacts the prices of HGU3, NICKELc1, and WilderHill Clean Energy Index (ECO). Similarly, the ECO influences the price of NICKELc1. However, it is worth noting that the Nasdaq Clean Edge Green Energy (CEXX) index does not have any influence on the rates of any assets.

Overall, there was a slight increase in long-term shocks from 17 to 18 between the subperiods. This suggests that the events of 2020 and 2022 do not significantly impact the safe haven characteristics of these markets. However, it is important to note that the energy metal Nickel Futures (NICKELc1) has deviated from these properties during this period of uncertainty in the global economy. Given the mentioned findings, the research question regarding the impact of the events in 2020 and 2022 on the long-term shocks between energy metals, precious metals, and clean energy indexes cannot be validated.

5. Discussion

Table 6 presents a summary table that provides a comparison between two distinct subperiods, namely Tranquil and Stress. Upon comparing the two subperiods, it is evident that the uncertainty resulting from the global pandemic of 2020 and the Russian invasion of Ukraine in 2022 did not exacerbate the long-term shocks. During the Tranquil phase, Aluminum (MAL3) did not exhibit the properties of a safe haven. However, in the subsequent Stress period, it acquired these characteristics. During the Tranquil period, Copper Futures (HGU3) did not act as a safe investment choice for the clean energy indexes WilderHill Clean Energy Index (ECO) and Nasdaq Clean Edge Green Energy (CEXX). This period of uncertainty revealed specific coverage characteristics for the green indexes. Nickel Futures (NICKELc1) exhibited characteristics of a hedging asset throughout the Tranquil period. However, upon analysis during the Stress period, it became evident that it had lost these attributes of being a safe haven. During both periods, precious metals like Gold (XAU), Silver (XAG), and Platinum (XPT) exhibited the characteristics of safe haven assets, as anticipated due to their inherent security. Furthermore, we also ascertain the shock-emitting nature of clean energy stock indexes through the analysis of certain assets. It is observed that, in periods of market stability, the S&P Global Clean Energy Index (SPGTCLEN) and the ECO do not exert any influence on the price formation of any asset. However, the CEXX does have an impact on the prices of Aluminum (MAL3) and HGU3. During the subperiod characterized by Stress, it is observed that the ECO index exerts an influence on the nickel market. Additionally, the SPGTCLEN was found to induce shocks in the prices of HGU3, Nickel Futures (NICKELc1), and the ECO stock index. Conversely, it is noted that the CEXX index does not have any significant impact on any of the aforementioned markets. In conclusion, based on the information derived from the events that transpired in 2020 and 2022, it can be inferred that portfolio diversity continues to be a resilient and efficacious approach to mitigating risk and attaining enduring financial objectives. While it is impossible to totally eradicate market volatility, the implementation of a diversified portfolio can effectively mitigate the consequences of unfavorable occurrences, providing investors with a sense of security and assurance, even during challenging periods. Authors [43,46], and [47] provide evidence of these findings, showing that gold has safe-haven characteristics as compared to some financial markets.

6. Conclusion

This study examined the impacts of significant global events, such as the worldwide pandemic in 2020 and the Russian conflict with Ukraine in 2022, on various assets and indexes. The findings revealed specific assets, namely gold (XAU), silver (XAG), and platinum (XPT), to be classified as "safe haven" assets. These assets have demonstrated their ability to maintain their sheltering properties even in times of stress, aligning with their established reputation for providing security during periods of turbulence. The behavior of specific assets exhibited volatility in response to varying market conditions. As an example, it was observed that Aluminum (MAL3) demonstrated safe haven properties during the period of stress, whereas Copper Futures (HGU3) and Nickel Futures (NICKELc1) displayed distinct characteristics in both calm and stressful periods. The study also examined the impact of clean energy stock indexes, such as the S&P Global Clean Energy Index (SPGTCLEN) and the Nasdaq Clean Edge Green Energy index (CEXX), on various assets. The study revealed that these indexes exert an influence on the prices of certain assets under varying market situations. While it is impossible to entirely eradicate market volatility, the results indicate that a diversified portfolio can offer stability and instill confidence in investors, especially during challenging periods. This suggests that the practice of diversifying investments across several asset classes can effectively reduce risk and enhance the likelihood of achieving long-term financial prosperity. In summary, the analysis highlights the significance of diversification as a strategy for managing risk and indicates its continued efficacy in navigating the unpredictable nature of financial markets. This is supported by the observed behavior of various assets and indexes in different market conditions throughout the years 2020 and 2022. The findings of the study have indicated that portfolio diversification is a very efficacious technique. During periods of market tensions, it is seen that different assets and indexes exhibit varying reactions. It is widely acknowledged that maintaining a well-diversified portfolio can serve as a mitigating strategy to minimize the impact of unfavorable occurrences.

7. Practical Implications

The study emphasizes the ongoing significance of diversifying investment portfolios. The allocation of investments across several asset classes can serve to manage risk and minimize vulnerability to the unique swings of individual assets, thus offering protection against market uncertainty. Furthermore, it acknowledges the significance of safe haven valuables such as Gold, Silver, and Platinum. These assets have the ability to act as a safe haven against market crises and retain their protective characteristics even in times of strain within global financial markets. Investors with an interest in clean energy stocks should prioritize the diligent tracking of clean energy stock indexes, such as the S&P Global Clean Energy Index (SPGTCLEN) and the Nasdaq Clean Edge Green Energy Index (CEXX). These indexes possess the potential to exert an influence on the prices of specific assets, necessitating investors to take these interrelationships into account when constructing their investment portfolios. Although diversification is a proven strategy for mitigating risk, it is important to note that it is unable to entirely eradicate market volatility. Investors need to adopt a long-term outlook, anticipate market volatility, and acknowledge the inherent presence of risk in investment decisions. A portfolio that is diversified across many asset classes can offer stability and instill confidence in investors, particularly in times of market volatility and uncertainty. Due to the intricate nature of financial markets and the imperative of strategic asset allocation, a considerable number of investors can benefit from the pursuit of expert financial counsel. Financial consultants play a crucial role in tailoring investment plans to align with the unique risk profiles and aspirations of individuals, all while staying informed of the latest market events. In summary, the preceding practical consequences underscore the significance of diversification, the evaluation of safe haven assets, and the importance of a meticulously crafted investment strategy that can effectively adjust to varying market situations. By using this acquired knowledge, investors may improve their ability to effectively mitigate risk and strategically pursue their long-term financial objectives.

Author Contributions

The four authors, R.D., M.C., N.T., P.A. and P.H., contributed equally to this work. All authors have read and agreed to the published version of the manuscript.

Funding

This paper is financed by the Center for Advanced Studies in Management and Economics, University of Évora, 7004-516 Évora, Portugal.

Data Availability Statement

The authors confirm that the data supporting the findings of this study are available within the article.

Acknowledgments

Rui Dias is pleased to acknowledge the financial support from Fundação para a Ciência e a Tecnologia (Grant UIDB/04007/2020).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Ahmad, W. On the Dynamic Dependence and Investment Performance of Crude Oil and Clean Energy Stocks. Res Int Bus Finance 2017, 42. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Ugolini, A. The Impact of Energy Prices on Clean Energy Stock Prices. A Multivariate Quantile Dependence Approach. Energy Econ 2018, 76, 136–152. [Google Scholar] [CrossRef]

- Dawar, I.; Dutta, A.; Bouri, E.; Saeed, T. Crude Oil Prices and Clean Energy Stock Indices: Lagged and Asymmetric Effects with Quantile Regression. Renew Energy 2021, 163, 288–299. [Google Scholar] [CrossRef]

- Ritchie, J.; Dowlatabadi, H. Divest from the Carbon Bubble ? Reviewing the Implications and Limitations of Fossil Fuel Divestment for Institutional Investors. Review of Economics & Finance 2015, 5. [Google Scholar]

- Henriques, I.; Sadorsky, P. Investor Implications of Divesting from Fossil Fuels. Global Finance Journal 2018, 38. [Google Scholar] [CrossRef]

- Blitz, D. Betting Against Oil: The Implications of Divesting from Fossil Fuel Stocks. SSRN Electronic Journal 2021. [Google Scholar] [CrossRef]

- Ahmad, W.; Rais, S. Time-Varying Spillover and the Portfolio Diversification Implications of Clean Energy Equity with Commodities and Financial Assets. Emerging Markets Finance and Trade 2018, 54. [Google Scholar] [CrossRef]

- Aslam, F.; Aziz, S.; Nguyen, D.K.; Mughal, K.S.; Khan, M. On the Efficiency of Foreign Exchange Markets in Times of the COVID-19 Pandemic. Technol Forecast Soc Change 2020, 161, 120261. [Google Scholar] [CrossRef]

- Alves Dias, P.; Blagoeva, D.; Pavel, C.; Arvanitidis, N. Cobalt: Demand-Supply Balances in the Transition to Electric Mobility; 2018. [Google Scholar]

- Dutta, A. Impact of Silver Price Uncertainty on Solar Energy Firms. J Clean Prod 2019, 225, 1044–1051. [Google Scholar] [CrossRef]

- Yahya, M.; Ghosh, S.; Kanjilal, K.; Dutta, A.; Uddin, G.S. Evaluation of Cross-Quantile Dependence and Causality between Non-Ferrous Metals and Clean Energy Indexes. Energy 2020, 202. [Google Scholar] [CrossRef]

- Baur, D.G.; McDermott, T.K. Is Gold a Safe Haven? International Evidence. J Bank Financ 2010, 34, 1886–1898. [Google Scholar] [CrossRef]

- Bulut, L.; Rizvanoghlu, I. Is Gold a Safe Haven? The International Evidence Revisited. Acta Oeconomica 2020, 70. [Google Scholar] [CrossRef]

- Chemkha, R.; BenSaïda, A.; Ghorbel, A.; Tayachi, T. Hedge and Safe Haven Properties during COVID-19: Evidence from Bitcoin and Gold. Quarterly Review of Economics and Finance 2021, 82. [Google Scholar] [CrossRef]

- Caporale, G.M.; Gil-Alana, L.A. Gold and Silver as Safe Havens: A Fractional Integration and Cointegration Analysis. PLoS ONE 2023, 18. [Google Scholar] [CrossRef] [PubMed]

- Azimli, A. Degree and Structure of Return Dependence among Commodities, Energy Stocks and International Equity Markets during the Post-COVID-19 Period. Resources Policy 2022, 77. [Google Scholar] [CrossRef]

- Hasan, M.B.; Hassan, M.K.; Rashid, M.M.; Alhenawi, Y. Are Safe Haven Assets Really Safe during the 2008 Global Financial Crisis and COVID-19 Pandemic? Global Finance Journal 2021, 50. [Google Scholar] [CrossRef]

- Gregory, A.W.; Hansen, B.E. Residual-Based Tests for Cointegration in Models with Regime Shifts. J Econom 1996, 70, 99–126. [Google Scholar] [CrossRef]

- Wang, Y.; Liu, Y.; Gu, B. COP26: Progress, Challenges, and Outlook. Adv Atmos Sci 2022, 39. [Google Scholar] [CrossRef]

- Arora, N.K.; Mishra, I. COP26: More Challenges than Achievements. Environmental Sustainability 2021, 4. [Google Scholar] [CrossRef]

- Lennan, M.; Morgera, E. The Glasgow Climate Conference (COP26). International Journal of Marine and Coastal Law 2022, 37. [Google Scholar] [CrossRef]

- Jacobs, M. Reflections on COP26: International Diplomacy, Global Justice and the Greening of Capitalism. Political Quarterly 2022, 93. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Hughes, L.; Kar, A.K.; Baabdullah, A.M.; Grover, P.; Abbas, R.; Andreini, D.; Abumoghli, I.; Barlette, Y.; Bunker, D.; et al. Climate Change and COP26: Are Digital Technologies and Information Management Part of the Problem or the Solution? An Editorial Reflection and Call to Action. Int J Inf Manage 2022, 63. [Google Scholar] [CrossRef]

- Dias, R.; Horta, N.; Chambino, M. Clean Energy Action Index Efficiency: An Analysis in Global Uncertainty Contexts. Energies 2023, 16, 18. [Google Scholar] [CrossRef]

- Dias, R.; Teixeira, N.; Alexandre, P.; Chambino, M. Exploring the Connection between Clean and Dirty Energy: Implications for the Transition to a Carbon-Resilient Economy. Energies (Basel) 2023, 16, 4982. [Google Scholar] [CrossRef]

- Dias, R.; Alexandre, P.; Teixeira, N.; Chambino, M. Clean Energy Stocks : Resilient Safe Havens in the Volatility of Dirty Cryptocurrencies. 2023.

- Santana, T.P.; Horta, N.; Revez, C.; Dias, R.M.T.S.; Zebende, G.F. Effects of Interdependence and Contagion on Crude Oil and Precious Metals According to ΡDCCA: A COVID-19 Case Study. Sustainability (Switzerland) 2023, 15. [Google Scholar] [CrossRef]

- Henriques, I.; Sadorsky, P. Oil Prices and the Stock Prices of Alternative Energy Companies. Energy Econ 2008, 30. [Google Scholar] [CrossRef]

- Kumar, S.; Managi, S.; Matsuda, A. Stock Prices of Clean Energy Firms, Oil and Carbon Markets: A Vector Autoregressive Analysis. Energy Econ 2012, 34. [Google Scholar] [CrossRef]

- Sadorsky, P. Modeling Renewable Energy Company Risk. Energy Policy 2012, 40. [Google Scholar] [CrossRef]

- Managi, S.; Okimoto, T. Does the Price of Oil Interact with Clean Energy Prices in the Stock Market? Japan World Econ 2013, 27. [Google Scholar] [CrossRef]

- Sadorsky, P. Modeling Renewable Energy Company Risk. Energy Policy 2012, 40. [Google Scholar] [CrossRef]

- Bondia, R.; Ghosh, S.; Kanjilal, K. International Crude Oil Prices and the Stock Prices of Clean Energy and Technology Companies: Evidence from Non-Linear Cointegration Tests with Unknown Structural Breaks. Energy 2016, 101. [Google Scholar] [CrossRef]

- Vrînceanu, G.; Horobeț, A.; Popescu, C.; Belaşcu, L. The Influence of Oil Price on Renewable Energy Stock Prices: An Analysis for Entrepreneurs. Studia Universitatis „Vasile Goldis” Arad – Economics Series 2020, 30. [Google Scholar] [CrossRef]

- Asl, M.G.; Canarella, G.; Miller, S.M. Dynamic Asymmetric Optimal Portfolio Allocation between Energy Stocks and Energy Commodities: Evidence from Clean Energy and Oil and Gas Companies. Resources Policy 2021, 71. [Google Scholar] [CrossRef]

- Kanamura, T. A Model of Price Correlations between Clean Energy Indices and Energy Commodities. Journal of Sustainable Finance and Investment 2022, 12. [Google Scholar] [CrossRef]

- Asl, M.G.; Canarella, G.; Miller, S.M. Dynamic Asymmetric Optimal Portfolio Allocation between Energy Stocks and Energy Commodities: Evidence from Clean Energy and Oil and Gas Companies. Resources Policy 2021, 71. [Google Scholar] [CrossRef]

- Kanamura, T. A Model of Price Correlations between Clean Energy Indices and Energy Commodities. Journal of Sustainable Finance and Investment 2022, 12. [Google Scholar] [CrossRef]

- Farid, S.; Karim, S.; Naeem, M.A.; Nepal, R.; Jamasb, T. Co-Movement between Dirty and Clean Energy: A Time-Frequency Perspective. Energy Econ 2023, 119. [Google Scholar] [CrossRef]

- Dias, R.; Teixeira, N.; Alexandre, P.; Chambino, M. Exploring the Connection between Clean and Dirty Energy: Implications for the Transition to a Carbon-Resilient Economy. Energies (Basel) 2023, 16, 4982. [Google Scholar] [CrossRef]

- Dias, R.; Alexandre, P.; Teixeira, N.; Chambino, M. Clean Energy Stocks : Resilient Safe Havens in the Volatility of Dirty Cryptocurrencies. 2023.

- Baur, D.G.; Lucey, B.M. Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold. Financial Review 2010, 45. [Google Scholar] [CrossRef]

- Baur, D.G.; McDermott, T.K. Is Gold a Safe Haven? International Evidence. J Bank Financ 2010, 34, 1886–1898. [Google Scholar] [CrossRef]

- Beckmann, J.; Berger, T.; Czudaj, R. Does Gold Act as a Hedge or a Safe Haven for Stocks? A Smooth Transition Approach. Econ Model 2015, 48. [Google Scholar] [CrossRef]

- Junttila, J.-P.; Pesonen, J.M.; Raatikainen, J. Commodity Market Based Hedging against Stock Market Risk in Times of Financial Crisis: The Case of Crude Oil and Gold. SSRN Electronic Journal 2017. [Google Scholar] [CrossRef]

- Beckmann, J.; Berger, T.; Czudaj, R. Does Gold Act as a Hedge or a Safe Haven for Stocks? A Smooth Transition Approach. Econ Model 2015, 48. [Google Scholar] [CrossRef]

- Junttila, J.-P.; Pesonen, J.M.; Raatikainen, J. Commodity Market Based Hedging against Stock Market Risk in Times of Financial Crisis: The Case of Crude Oil and Gold. SSRN Electronic Journal 2017. [Google Scholar] [CrossRef]

- Chen, K.; Wang, M. Is Gold a Hedge and Safe Haven for Stock Market? Appl Econ Lett 2019, 26. [Google Scholar] [CrossRef]

- Chang, B.H.; Rajput, S.K.O.; Ahmed, P.; Hayat, Z. Does Gold Act as a Hedge or a Safe Haven? Evidence from Pakistan. Pak Dev Rev 2020, 59. [Google Scholar] [CrossRef]

- Gargallo, P.; Lample, L.; Miguel, J.A.; Salvador, M. Dynamic Risk Management in European Energy Portfolios: Evolution of the Role of Clean and Carbon Markets. Energy Reports 2022, 8. [Google Scholar] [CrossRef]

- Ozdurak, C.; Umut, A.; Ozay, T. The Interaction of Major Crypto-Assets, Clean Energy, and Technology Indices in Diversified Portfolios. International Journal of Energy Economics and Policy 2022, 12. [Google Scholar] [CrossRef]

- Elie, B.; Naji, J.; Dutta, A.; Uddin, G.S. Gold and Crude Oil as Safe-Haven Assets for Clean Energy Stock Indices: Blended Copulas Approach. Energy 2019, 178. [Google Scholar] [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Wang, S.; Wei, Y. Volatility Communicator or Receiver? Investigating Volatility Spillover Mechanisms among Bitcoin and Other Financial Markets. Res Int Bus Finance 2022, 59. [Google Scholar] [CrossRef]

- Sharma, U.; Karmakar, M. Are Gold, USD, and Bitcoin Hedge or Safe Haven against Stock? The Implication for Risk Management. Review of Financial Economics 2023, 41. [Google Scholar] [CrossRef]

- Mensi, W.; Maitra, D.; Selmi, R.; Vo, X.V. Extreme Dependencies and Spillovers between Gold and Stock Markets: Evidence from MENA Countries. Financial Innovation 2023, 9. [Google Scholar] [CrossRef] [PubMed]

- Bahloul, S.; Mroua, M.; Naifar, N. Re-Evaluating the Hedge and Safe-Haven Properties of Islamic Indexes, Gold and Bitcoin: Evidence from DCC–GARCH and Quantile Models. Journal of Islamic Accounting and Business Research 2023. [Google Scholar] [CrossRef]

- Yousaf, I.; Plakandaras, V.; Bouri, E.; Gupta, R. Hedge and Safe-Haven Properties of FAANA against Gold, US Treasury, Bitcoin, and US Dollar/CHF during the Pandemic Period. North American Journal of Economics and Finance 2023, 64. [Google Scholar] [CrossRef]

- Tsay, R.S. Analysis of Financial Time Series; 2002. [Google Scholar]

- Jarque, C.M.; Bera, A.K. Efficient Tests for Normality, Homoscedasticity and Serial Independence of Regression Residuals. Econ Lett 1980, 6. [Google Scholar] [CrossRef]

- Ljung, G.M.; Box, G.E.P. On a Measure of Lack of Fit in Time Series Models. Biometrika 1978, 65. [Google Scholar] [CrossRef]

- Inclán, C.; Tiao, G.C. Use of Cumulative Sums of Squares for Retrospective Detection of Changes of Variance. J Am Stat Assoc 1994, 89. [Google Scholar] [CrossRef]

- Breitung, J. The Local Power of Some Unit Root Tests for Panel Data. Advances in Econometrics 2000, 15. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.F.; Chu, C.S.J. Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties. J Econom 2002, 108. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for Unit Roots in Heterogeneous Panels. J Econom 2003. [Google Scholar] [CrossRef]

- Dickey, D.; Fuller, W. Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root. Econometrica 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Perron, P.; Phillips, P.C.B. Testing for a Unit Root in a Time Series Regression. Biometrika 1988, 2, 335–346. [Google Scholar] [CrossRef]

- Choi, I. Unit Root Tests for Panel Data. J Int Money Finance 2001, 20, 249–272. [Google Scholar] [CrossRef]

- Santana, T.P.; Horta, N.; Revez, C.; Dias, R.M.T.S.; Zebende, G.F. Effects of Interdependence and Contagion on Crude Oil and Precious Metals According to ΡDCCA: A COVID-19 Case Study. Sustainability (Switzerland) 2023, 15. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Perron, P. Testing for a Unit Root in Time Series Regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

Figure 1.

Evolution, in returns, of the financial markets under review, from February 16, 2018, to February 15, 2023.

Figure 1.

Evolution, in returns, of the financial markets under review, from February 16, 2018, to February 15, 2023.

Figure 2.

CUSUM charts created for the residues of the markets under consideration, from July 13, 2018, to July 11, 2023.

Figure 2.

CUSUM charts created for the residues of the markets under consideration, from July 13, 2018, to July 11, 2023.

Table 2.

Summary table of descriptive statistics in returns for the markets under consideration from July 13, 2018, to July 11, 2023.

Table 2.

Summary table of descriptive statistics in returns for the markets under consideration from July 13, 2018, to July 11, 2023.

| Mean | Std. Dev. | Skewness | Kurtosis | JB | Probability | Observations | |

|---|---|---|---|---|---|---|---|

| CEXX | 0.000818 | 0.025233 | -0.344916 | 6.583154 | 699.0304 | 0.000000 | 1260 |

| ECO | 0.000412 | 0.027667 | -0.303020 | 5.930867 | 470.2566 | 0.000000 | 1260 |

| HGU3 | 0.000242 | 0.014330 | -0.182271 | 4.602964 | 141.8751 | 0.000000 | 1260 |

| MAL3 | 5.46E-05 | 0.013571 | -0.042690 | 5.078401 | 227.1697 | 0.000000 | 1260 |

| MNKC1 | 0.000491 | 0.024283 | 8.135917 | 185.9311 | 1770749. | 0.000000 | 1260 |

| SPGTCLEN | 0.000639 | 0.018158 | -0.439446 | 9.671195 | 2377.058 | 0.000000 | 1260 |

| XAG | 0.000303 | 0.018690 | -0.582112 | 11.71614 | 4059.640 | 0.000000 | 1260 |

| XAU | 0.000351 | 0.009164 | -0.430383 | 6.273462 | 601.4647 | 0.000000 | 1260 |

| XPT | 8.94E-05 | 0.018104 | -0.570660 | 8.079954 | 1423.198 | 0.000000 | 1260 |

Source: Own elaboration (Software Eviews12)

Table 3.

Summary table of panel unit roots tests, in returns, from 13 July 2018 to 11 July 2023.

| Group unit root test: Summary | ||||

|---|---|---|---|---|

| Method | Statistic | Prob* | Cross- sections |

Obs. |

| Null: Unit root (assumes common unit root process) | ||||

| Levin, Lin & Chu t | -184.570 | 0.0000 | 9 | 11319 |

| Breitung t-stat | -90.1528 | 0.0000 | 9 | 11310 |

| Null: Unit root (assumes individual unit root process) | ||||

| Im, Pesaran and Shin W-stat | -118.841 | 0.0000 | 9 | 11319 |

| ADF - Fisher Chi-square | 2370.52 | 0.0000 | 9 | 11319 |

| PP - Fisher Chi-square | 2370.52 | 0.0000 | 9 | 11322 |

Source: Own elaboration. Note: *Probabilities for Fisher tests are computed using an asymptotic Chi square distribution. All other tests assume asymptotic normality.

Table 4.

Summary table of the long-term shocks between the analyzed financial markets between July 13, 2018, and December 31, 2019.

Table 4.

Summary table of the long-term shocks between the analyzed financial markets between July 13, 2018, and December 31, 2019.

| Markets | Test | Stat. | Method | Lags | Break Date | Results |

|---|---|---|---|---|---|---|

| MAL3 | HGU3 | Zt | -5.91*** | Trend | 2 | 25/10/2028 | Shocks |

| MAL3 | NICKELc1 | ADF | -5.57*** | Trend | 2 | 02/11/2018 | Shocks |

| MAL3 | XAU | ADF | -5.76*** | Trend | 2 | 02/11/2018 | Shocks |

| MAL3 | XPT | Za | -57.86*** | Trend | 0 | 24/10/2018 | Shocks |

| MAL3 | XAG | ADF | -5.60*** | Trend | 2 | 02/11/2018 | Shocks |

| MAL3 | ECO | Zt | -5.71*** | Trend | 0 | 02/01/2019 | Shocks |

| MAL3 | SPGTCLEN | ADF | -5.59*** | Trend | 2 | 23/10/2018 | Shocks |

| MAL3 | CEXX | Zt | -6.21*** | Trend | 0 | 02/01/2019 | Shocks |

| HGU3 | MAL3 | Zt | -3.97 | Trend | 0 | Non-existent | |

| HGU3 | NICKELc1 | Zt | -4.20 | Trend | 0 | Non-existent | |

| HGU3 | XAU | ADF | -4.93* | Trend | 0 | 01/05/2019 | Shocks |

| HGU3 | XPT | ADF | -4.27 | Trend | 0 | Non-existent | |

| HGU3 | XAG | ADF | -4.94* | Trend | 0 | 01/05/2019 | Shocks |

| HGU3 | ECO | ADF | -5.05** | Trend | 0 | 22/05/2019 | Shocks |

| HGU3 | SPGTCLEN | ADF | -4.70 | Trend | 0 | Non-existent | |

| HGU3 | CEXX | ADF | -4.72* | Trend | 1 | 02/10/2018 | Shocks |

| NICKELc1 | MAL3 | Zt | -3.29 | Trend | 2 | Non-existent | |

| NICKELc1 | HGU3 | Za | -19.65 | Trend | 3 | Non-existent | |

| NICKELc1 | XAU | Za | -24.67 | Trend | 1 | Non-existent | |

| NICKELc1 | XPT | Zt | -3.14 | Trend | 0 | Non-existent | |

| NICKELc1 | XAG | Zt | -4.17 | Trend | 0 | Non-existent | |

| NICKELc1 | ECO | Zt | -3.48 | Trend | 2 | Non-existent | |

| NICKELc1 | SPGTCLEN | Zt | -3.72 | Trend | 2 | Non-existent | |

| NICKELc1 | CEXX | Zt | -3.23 | Trend | 2 | Non-existent | |

| XAU | MAL3 | Zt | -5.71*** | Regime | 2 | 27/06/2019 | Shocks |

| XAU | HGU3 | Zt | -3.47 | Regime | 0 | Non-existent | |

| XAU | NICKELc1 | ADF | -3.36 | Regime | 1 | Non-existent | |

| XAU | XPT | Zt | -3.26 | Regime | 0 | Non-existent | |

| XAU | XAG | Zt | -3.64 | Regime | 5 | Non-existent | |

| XAU | ECO | Zt | -3.49 | Regime | 0 | Non-existent | |

| XAU | SPGTCLEN | Zt | -4.02 | Regime | 0 | Non-existent | |

| XAU | CEXX | Zt | -3.38 | Trend | 1 | Non-existent | |

| XPT | MAL3 | Zt | -4.77* | Regime | 1 | 22/08/2019 | Shocks |

| XPT | HGU3 | ADF | -4.95** | Regime | 3 | 08/08/2019 | Shocks |

| XPT | NICKELc1 | ADF | -3.85 | Regime | 0 | Non-existent | |

| XPT | XAU | Zt | -4.00 | Regime | 0 | Non-existent | |

| XPT | XAU | ADF | -3.78 | Regime | 0 | Non-existent | |

| XPT | ECO | Zt | -4.30 | Regime | 0 | Non-existent | |

| XPT | SPGTCLEN | Zt | -4.42 | Regime | 0 | Non-existent | |

| XPT | CEXX | Zt | -4.29 | Regime | 5 | Non-existent | |

| XAG | MAL3 | Zt | -4.69 | Regime | 1 | Non-existent | |

| XAG | HGU3 | ADF | -4.35 | Regime | 1 | Non-existent | |

| XAG | NICKELc1 | Zt | -4.66 | Regime | 0 | Non-existent | |

| XAG | XAU | ADF | -4.40 | Regime | 5 | Non-existent | |

| XAG | XPT | Zt | -3.77 | Regime | 0 | Non-existent | |

| XAG | ECO | Zt | -4.44 | Regime | 1 | Non-existent | |

| XAG | SPGTCLEN | Zt | -4.47 | Regime | 1 | Non-existent | |

| XAG | CEXX | Zt | -4.39 | Regime | 1 | Non-existent | |

| ECO | MAL3 | Zt | -4.68 | Trend | 0 | Non-existent | |

| ECO | HGU3 | Zt | -4.30 | Trend | 1 | Non-existent | |

| ECO | NICKELc1 | Zt | -3.95 | Trend | 1 | Non-existent | |

| ECO | XAU | Zt | -3.83 | Trend | 1 | Non-existent | |

| ECO | XPT | Zt | -3.66 | Trend | 1 | Non-existent | |

| ECO | XAU | Zt | -4.03 | Trend | 1 | Non-existent | |

| ECO | SPGTCLEN | ADF | -3.41 | Trend | 0 | Non-existent | |

| ECO | CEXX | Zt | -3.65 | Trend | 0 | Non-existent | |

| SPGTCLEN | MAL3 | Zt | -3.76 | Trend | 0 | Non-existent | |

| SPGTCLEN | HGU3 | Zt | -3.67 | Trend | 1 | Non-existent | |

| SPGTCLEN | NICKELc1 | Zt | -3.69 | Trend | 1 | Non-existent | |

| SPGTCLEN | XAU | Zt | -3.83 | Trend | 1 | Non-existent | |

| SPGTCLEN | XPT | Zt | -3.39 | Trend | 1 | Non-existent | |

| SPGTCLEN | XAU | Zt | -3.59 | Trend | 1 | Non-existent | |

| SPGTCLEN | ECO | Zt | -3.82 | Trend | 0 | Non-existent | |

| SPGTCLEN | CEXX | Za | -4.28 | Trend | 2 | Non-existent | |

| CEXX | MAL3 | ADF | -5.01** | Trend | 0 | 04/02/2019 | Shocks |

| CEXX | HGU3 | ADF | -5.12** | Trend | 0 | 03/10/2019 | Shocks |

| CEXX | NICKELc1 | Zt | -3.97 | Trend | 1 | Non-existent | |

| CEXX | XAU | Zt | -3.95 | Trend | 1 | Non-existent | |

| CEXX | XPT | Zt | -3.93 | Trend | 1 | Non-existent | |

| CEXX | XAU | Zt | -3.89 | Trend | 1 | Non-existent | |

| CEXX | ECO | ADF | -3.93 | Trend | 0 | Non-existent | |

| CEXX | SPGTCLEN | ADF | -3.72 | Trend | 0 | Non-existent |

Source: Own elaboration (Software Stata). Note: The critical values are found in Gregory and Hansen (1996). The critical values for the ADF and Zt parameters are: −5,45 (1%); −4,99 (5%); −4,72 (10%). For the Za parameter, the critical values are: −57,28 (1%); −47,96 (5%); −43,22 (10%). The asterisks ***, **, * indicate statistical significance at 1%, 5% and 10%, respectively.

Table 5.

Summary table of the long-term shocks between the analyzed financial markets between January 2, 2020, and July 11, 2023.

Table 5.

Summary table of the long-term shocks between the analyzed financial markets between January 2, 2020, and July 11, 2023.

| Markets | Test | Stat. | Method | Lags | Break Date | Results |

|---|---|---|---|---|---|---|

| MAL3 | HGU3 | ADF | -3.84 | Regime | 0 | Non-existent | |

| MAL3 | NICKELc1 | Zt | -6.66*** | Trend | 5 | 02/03/2022 | Shocks |

| MAL3 | XAU | Zt | -4.19 | Trend | 5 | Non-existent | |

| MAL3 | XPT | Za | -27.73 | Trend | 0 | Non-existent | |

| MAL3 | XAG | Zt | -3.78 | Trend | 1 | Non-existent | |

| MAL3 | ECO | Zt | -3.58 | Trend | 1 | Non-existent | |

| MAL3 | SPGTCLEN | ADF | -3.49 | Trend | 1 | Non-existent | |

| MAL3 | CEXX | Zt | -3.51 | Trend | 1 | Non-existent | |

| HGU3 | MAL3 | Zt | -4.32 | Regime | 0 | Non-existent | |

| HGU3 | NICKELc1 | Zt | -5.61*** | Trend | 0 | 01/03/2022 | Shocks |

| HGU3 | XAU | Zt | -4.77* | Trend | 0 | 05/02/2021 | Shocks |

| HGU3 | XPT | ADF | -5.04** | Trend | 0 | 20/06/2022 | Shocks |

| HGU3 | XAG | Za | -39.08 | Trend | 0 | Non-existent | |

| HGU3 | ECO | Zt | -4.61 | Trend | 0 | Non-existent | |

| HGU3 | SPGTCLEN | Zt | -4.63 | Trend | 0 | Non-existent | |

| HGU3 | CEXX | Zt | -4.57 | Trend | 1 | Non-existent | |

| NICKELc1 | MAL3 | Zt | -8.14*** | Trend | 0 | 02/03/2022 | Shocks |

| NICKELc1 | HGU3 | Za | -7.04*** | Trend | 0 | 28/02/2022 | Shocks |

| NICKELc1 | XAU | Za | -44.38* | Trend | 0 | 21/01/2022 | Shocks |

| NICKELc1 | XPT | Za | -48.32** | Trend | 0 | 21/01/2022 | Shocks |

| NICKELc1 | XAG | ADF | -5.10** | Trend | 0 | 21/01/2022 | Shocks |

| NICKELc1 | ECO | Zt | -5.19** | Trend | 0 | 21/01/2022 | Shocks |

| NICKELc1 | SPGTCLEN | Zt | -5.23** | Trend | 0 | 21/01/2022 | Shocks |

| NICKELc1 | CEXX | Zt | -5.40** | Trend | 0 | 21/01/2022 | Shocks |

| XAU | MAL3 | Zt | -4.04 | Trend | 1 | Non-existent | |

| XAU | HGU3 | Zt | -5.01** | Trend | 1 | 05/02/2021 | Shocks |

| XAU | NICKELc1 | Zt | -3.55 | Trend | 0 | Non-existent | |

| XAU | XPT | Zt | -3.56 | Trend | 0 | Non-existent | |

| XAU | XAG | Zt | -4.03 | Trend | 0 | Non-existent | |

| XAU | ECO | Zt | -3.95 | Trend | 1 | Non-existent | |

| XAU | SPGTCLEN | Zt | -3.97 | Trend | 1 | Non-existent | |

| XAU | CEXX | Zt | -4.35 | Trend | 1 | Non-existent | |

| XPT | MAL3 | Zt | -4.36 | Trend | 2 | Non-existent | |

| XPT | HGU3 | Zt | -4.75* | Trend | 0 | 13/07/2021 | Shocks |

| XPT | NICKELc1 | ADF | -4.15 | Trend | 1 | Non-existent | |

| XPT | XAU | Zt | -4.31 | Trend | 2 | Non-existent | |

| XPT | XAG | ADF | -4.83 | Regime | 2 | 22/12/2020 | Shocks |

| XPT | ECO | Zt | -4.32 | Trend | 0 | Non-existent | |

| XPT | SPGTCLEN | Zt | -3.90 | Regime | 0 | Non-existent | |

| XPT | CEXX | Zt | -4.35 | Trend | 0 | Non-existent | |

| XAG | MAL3 | Zt | -3.61 | Regime | 0 | Non-existent | |

| XAG | HGU3 | ADF | -4.41 | Regime | 0 | Non-existent | |

| XAG | NICKELc1 | Zt | -4.42 | Trend | 0 | Non-existent | |

| XAG | XAU | Zt | -4.28 | Trend | 0 | Non-existent | |

| XAG | XPT | Zt | -4.51 | Trend | 0 | Non-existent | |

| XAG | ECO | Zt | -4.28 | Trend | 0 | Non-existent | |

| XAG | SPGTCLEN | Zt | -4.21 | Trend | 0 | Non-existent | |

| XAG | CEXX | Zt | -4.40 | Trend | 0 | Non-existent | |

| ECO | MAL3 | Zt | -4.21 | Trend | 2 | Non-existent | |

| ECO | HGU3 | Zt | -3.83 | Trend | 2 | Non-existent | |

| ECO | NICKELc1 | Zt | -4.77* | Regime | 0 | 23/02/2021 | Shocks |

| ECO | XAU | Zt | -4.37 | Trend | 2 | Non-existent | |

| ECO | XPT | Zt | -4.16 | Trend | 2 | Non-existent | |

| ECO | XAG | Zt | -4.61 | Trend | 2 | Non-existent | |

| ECO | SPGTCLEN | Zt | -4.33 | Trend | 4 | Non-existent | |

| ECO | CEXX | Zt | -4.39 | Trend | 0 | Non-existent | |

| SPGTCLEN | MAL3 | Zt | -4.60 | Trend | 2 | Non-existent | |

| SPGTCLEN | HGU3 | Zt | -5.91*** | Regime | 5 | 25/02/2021 | Shocks |

| SPGTCLEN | NICKELc1 | Zt | -6.20*** | Regime | 2 | 24/02/2021 | Shocks |

| SPGTCLEN | XAU | Zt | -3.50 | Regime | 1 | Non-existent | |

| SPGTCLEN | XPT | Zt | -4.66 | Regime | 2 | Non-existent | |

| SPGTCLEN | XAG | Zt | -3.64 | Regime | 2 | Non-existent | |

| SPGTCLEN | ECO | Zt | -5.86*** | Regime | 1 | 11/02/2021 | Shocks |

| SPGTCLEN | CEXX | Za | -41.10 | Regime | 0 | Non-existent | |

| CEXX | MAL3 | Zt | -4.10 | Trend | 3 | Non-existent | |

| CEXX | HGU3 | Zt | -3.94 | Trend | 0 | Non-existent | |

| CEXX | NICKELc1 | Zt | -4.21 | Trend | 0 | Non-existent | |

| CEXX | XAU | Zt | -4.20 | Trend | 0 | Non-existent | |

| CEXX | XPT | Zt | -4.03 | Trend | 0 | Non-existent | |

| CEXX | XAG | Zt | -4.26 | Trend | 0 | Non-existent | |

| CEXX | ECO | Zt | -4.45 | Trend | 0 | Non-existent |

Source: Own elaboration (Software Stata). Note: The critical values are found in Gregory and Hansen (1996). The critical values for the ADF and Zt parameters are: −5,45 (1%); −4,99 (5%); −4,72 (10%). For the Za parameter, the critical values are: −57,28 (1%); −47,96 (5%); −43,22 (10%). The asterisks ***, **, * indicate statistical significance at 1%, 5% and 10%, respectively.

Table 6.