Submitted:

12 July 2023

Posted:

14 July 2023

You are already at the latest version

Abstract

Load forecasting is an important component of power system and resource planning for electrical grids. The adoption of electric vehicles (EVs), behind-the-meter (BTM) solar, and heat pumps will significant change the amount and variability of loads. Electrification adoption and load forecasting in arctic regions and Alaska is limited. This paper provides the first load and electrification adoption forecast for the Alaska Railbelt transmission system, including yearly adoption rates of EVs, BTM solar, and heat pumps and hourly load data. Adoption rates are based on available historical data and compared to other regional and national trends. Two forecasts are created: 1) a moderate adoption forecast based on projections from current adoption rates and comparisons to other projections, and 2) an aggressive forecast, which provides a bookend comparison at the high adoption rate of 90% for all technologies. The results of these forecasts demonstrate a significant increase in both energy, 80% and 116% for moderate and aggressive, respectively and peak load demand, 113% and 219% for moderate and aggressive, respectively. Additionally, the results indicate a maximum hourly load change of 260% and 381% for the moderate and aggressive forecasts, respectively. These findings highlight a need for resource planning, which accounts for increases in demand and suggests that significant demand management is needed to smooth and control the load fluctuations as a result of the adoption of EVs, BTM solar, and heat pumps.

Keywords:

load forecast

; electrification

; heat pumps

; electric vehicles

; solar

; Alaska

; Railbelt

1. Introduction

Forecasting of load and behind-the-meter (BTM) resource adoption is important for utility resource planning and balancing supply and demand. As utilities plan for grid modernization, electricity consumption must be forecast over many years. As the energy system evolves and electrifies, we will see increasing electricity consumption from technologies like heat pumps and electric vehicles (EVs) as well as higher BTM generation from technologies like rooftop photovoltaic (PV) solar systems. The literature is limited on the effect that cold temperatures have on BTM solar PV generation, heat pump consumption profiles, and EV charging, specifically in arctic regions. Many electrification and load forecasting studies [1] only include the contiguous US and data on Alaska is limited. This paper provides a load and electrification adoption forecast for heat pumps, EVs, and BTM solar to 2050 for Alaska’s Railbelt electric grid.

The Railbelt is the largest regional electric grid in Alaska, spanning about 700 miles from Fairbanks to Homer. This Railbelt serves about 70% of Alaska’s population and about 75% of Alaska’s electrical load. Currently, about 80% of the Railbelt’s electricity generation comes from fossil fuels and 20% comes from renewable sources, mainly hydro. The unique electricity landscape of the Railbelt and Alaska’s winter-peaking load contribute to many challenges to achieving a high penetration of renewables.

Decarbonization and the potential electrification of heating and transportation have significant implications for the amounts and types of new generation necessary to serve demand. Nationwide, an all-electric approach to decarbonized space heating could require a 70% increase in electricity capacity [2]. Load forecasting studies for the US often omit Alaska and data on Alaska is limited. However, regions that see low winter temperatures face unique challenges to electrification and adoption of technologies such as heat pumps. Some studies find that the single largest limitation to electrification of heating is very cold temperatures in the winter that cause both higher heating demand and lower heat pump efficiency [2]. In addition, the adoption of heat pumps may have a significant impact on the shape and time of peak electricity demand [1]. In Alaska, despite the lower heat pump efficiencies due to cold temperatures, the high cost of heating means that heat pumps can reduce energy costs overall [3,4].

Electrification of the transportation sector could cause a significant increase in electricity demand. Transportation currently accounts for less than 1% of US electricity demand but accounts for 30% of primary energy consumption [1]. Forecasting electricity demand from EVs in cold climates can be complicated due to the significant impact of cold temperatures on the performance/efficiency of EVs and electricity consumption when EVs are parked to keep the battery at an optimal temperature for performance and health. Cold temperatures seen in Alaska can decrease EV range by up to 50% and colder temperatures can increase the time required to charge EV batteries [5,6].

There were 1,250 EVs registered in Alaska as of December 2021 [5]. The State of Alaska Electric Vehicle Infrastructure Implementation Plan predicts that in 2026, 1.01% of all registered vehicles in Alaska will be EVs, up from 0.20% EV penetration in 2021 for light-duty vehicles [5]. In comparison, as of 2021, the New England Independent System Operator (ISO-NE) had an EV penetration rate of 0.59%, projected to be 14% by 2031 [7].

Forecasting solar output from BTM PV is important for grid operators since it reduces demand on the grid. The output from solar depends on weather conditions and can be especially variable in the winter due to snow, cloud cover, and fewer hours of daylight. In regions like the Railbelt that face extreme weather in winter months and very few hours of daylight, solar installations have low capacity factors (7-15%) [8]. In grids with winter-peaking demand, solar does not reduce system peak demand since solar only reduces demand during the middle of sunny days without significant snow cover on the PV panels. Furthermore, BTM PV adoption rates are influenced by various policy drivers such as feed-in-tariffs, net energy metering (NEM), and the federal investment tax credit (ITC).

While many load-forecasting studies exist for the lower 48 states, studies on forecasting load, output from BTM solar, electrification with heat pumps, and adoption and charging profiles of EVs are understudied for arctic regions including Alaska. This study provides the first Railbelt region wide load and electrification adoption forecast for the Alaska Railbelt transmission system. The load forecasts produced include yearly adoption rates of EVs, BTM solar, and heat pumps. The forecasts are useful for energy planning for the region.

This paper is organized into the following sections: Section 2 provides general information relevant to the forecasts. Section 3 provides the methods, data, and resulting yearly forecasts for the adoption of EVs, heat pumps, and BTM solar. Section 4 provides the methods, data, and resulting hourly load data for EVs, heat pumps, BTM solar, and the total load. Section 6 concludes with a summary of the key findings and implications of the forecasts.

2. Electrification and BTM Solar Baseline Information

This section outlines the data and methods used to estimate the baseline information necessary to create electrification adoption forecasts. This data includes 1) the number of buildings, which is needed for estimating the residential solar and heat pump adoption, and 2) the number of vehicles, which is needed for estimating EV adoption. The data was collected by borough or governmental area.

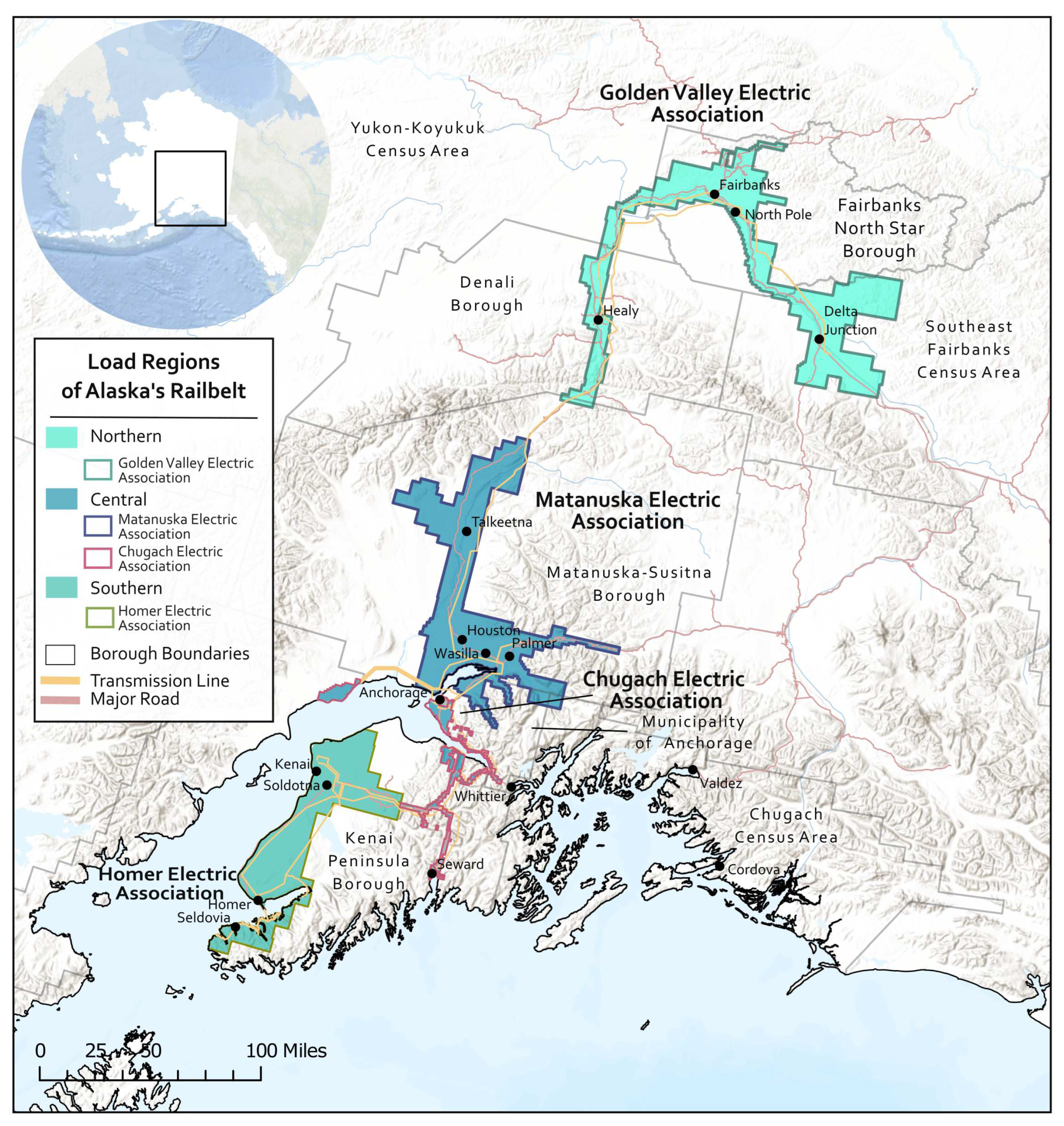

The collected data is also categorized by electric utility and general load area. There are four electric cooperatives in the Railbelt: Golden Valley Electric Association, Matanuska Electric Association, Chugach Electric Association, and Homer Electric Association. There are three general load areas in the Railbelt, which are connected vertically with a single transmission line, called Northern, Central, and Southern. These boroughs, utility service areas, and load areas are illustrated in Figure 1.

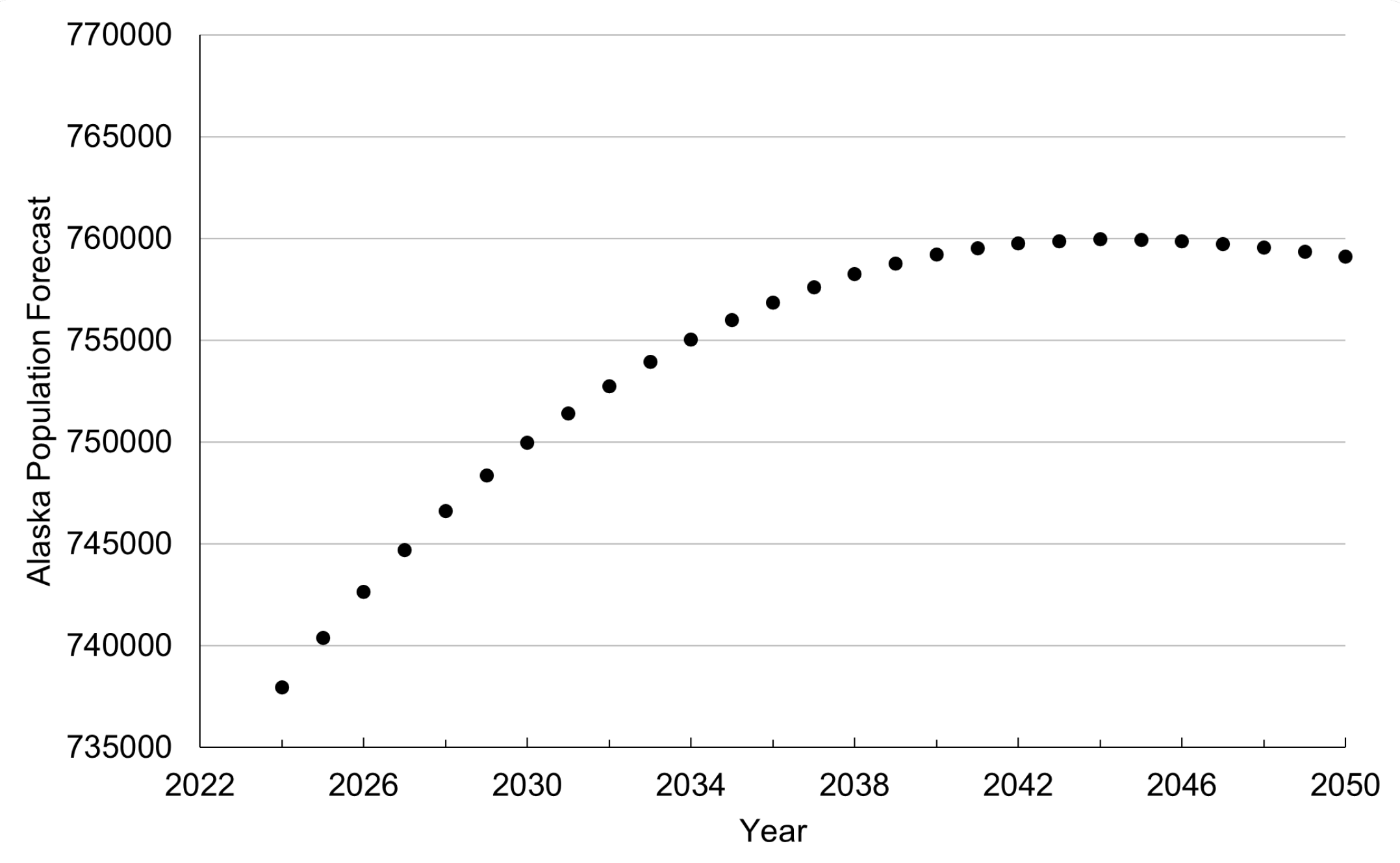

Alaska’s population has declined from 742,874 in 2015 to 734,323 in 2020 [9]. Research and analysis of Alaska’s population by the Alaska Department of Labor and Workforce project an increase in population from 2021 to 2040 in the Railbelt region until 2040 when the rate of change becomes relatively stable until 2050, as illustrated in Figure 2 [9].

The forecasted population growth from 2023 to 2050 is approximately 3%. Due to the negligible forecasted population change in Alaska, it is estimated that net number of buildings and vehicles calculated in the sections below will remain constant through 2050. Therefore, no increases in the number of buildings or vehicles are included in the forecasts.

2.1. Number of Buildings

The number of buildings receiving electricity from the Railbelt transmission system was calculated from public records requests for property information to the Fairbanks NorthStar Borough, Kenai Peninsula Borough, Matanuska-Sustina Borough, and the Municipality of Anchorage.

The property information collected from the boroughs and the Municipality of Anchorage included address, year built, and primary use of property. This information was used to determine the number of residential, commercial, and non-residential or non-commercial buildings in these boroughs and municipality. Industrial buildings are not evaluated as part of this study.

The Denali Borough, the City of Nenana, and the City of Delta are also located along the Railbelt, however there are no property taxes in these places or a property database. Denali Borough includes the towns or cities of Anderson, Healy, Cantwell, and Denali Park. In absence of property information from these locations, census data from the 2018 American Community Survey for Physical Housing Characteristics for Occupied Housing Units [10] was collected. The number of occupied housing units from the census data was used as the number of residential buildings for these locations. The number of commercial buildings was estimated by using the ratio of residential to commercial buildings from FNSB for the locations with more commercial activity (Denali Park) and MSB for the locations with less commercial activity (Nenana, Delta Junction, Anderson, Cantwell, Healy).

The number of commercial and residential building receiving electricity from the Railbelt transmission system are outlined in Table 1.

The total number of buildings, including commercial and residential, considered in this study as potentially installing residential solar or a heat pump categorized by load region are Northern: 45,223, Central: 153,102, and Southern: 48,487. The total number of commercial and residential buildings in the Railbelt used in this study is 292,035.

2.2. Number of Vehicles

The number of vehicles in use by residences that receive electricity from the Railbelt transmission system was determined by the number of registered vehicles in 2022 as listed by the Department of Motor Vehicles (DMV) for Fairbanks North Star Borough, Delta Junction, Matanuska-Susitna Borough, Kenai Peninsula Borough, City of Delta Junction, City of Nenana, and the Municipality of Anchorage [11]. The types of vehicles for which DMV reports data include passenger, motorcycle, commercial trailer, trailer, commercial truck, pickup, bus, and snowmobile. This study considered the electrification of the following vehicle types: car (DMV "passenger" type), truck (DMV "pickup" type), box truck (DMV "commercial truck" type), and bus. The number of vehicles by type and by area are outlined in Table 2. There is some overlap between the DMV regions and the utility service areas, which makes the number of vehicle counts not an exact match to DMV regions. However, for the purpose of this study, the utility service areas assigned to each DMV region are also outlined in Table 2.

The total vehicles for this study considered to be potentially electrified categorized by electric utility are GVEA: 94,234, MEA: 76,600, CEA: 268,481, and HEA: 59,548.

3. Yearly Forecasts

The forecasts generated as a part of this study included projections for the existing load base, EVs, BTM PV, and heat pumps. Local and global trends were used to project growth rates and generate an estimate for the amount of load through 2050.

Two load forecasts were generated to represent two trajectories for the adoption of electrification and residential solar generation. These forecasts are called the moderate and aggressive forecasts. The moderate forecast was determined by following current adoption of technologies and forecasts generated by other Alaskan entities. The aggressive forecast was set to assume 90% of buildings (residential and commercial) adopt heat pumps and residential solar, and 90% of vehicles are electric vehicles in 2050. Therefore the aggressive forecast provides a comparison of current trends and near total adoption of these technologies. The inputs, assumptions, and methods used to generate these forecasts are outlined below along with the resulting projections.

3.1. Electric Vehicles

Number of Electric Vehicles

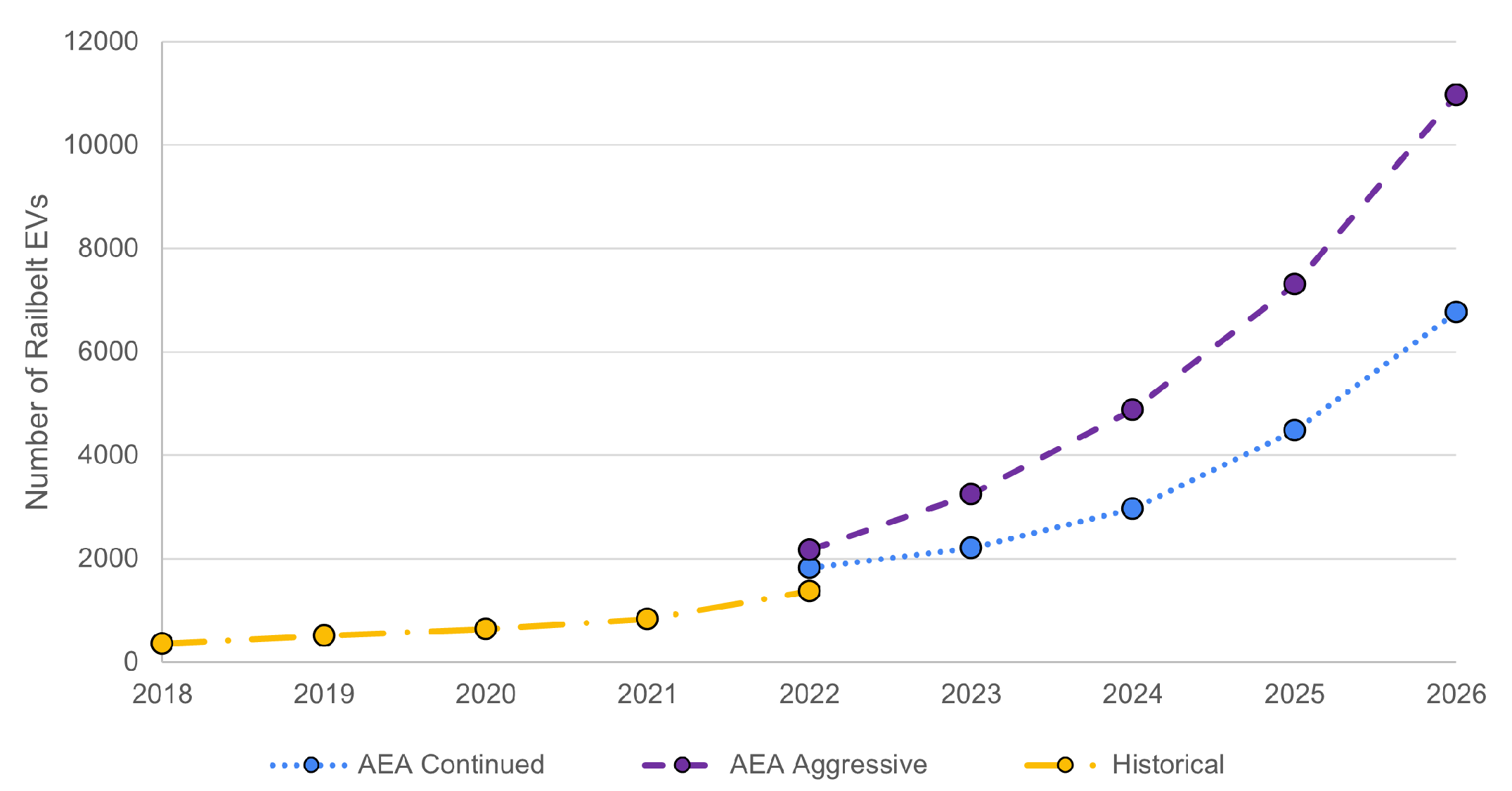

The Alaska Energy Authority (AEA) produced two EV growth forecasts through 2026, continued and aggressive, for the state of Alaska as part of their Electrical Vehicle Infrastructure Implementation Plan [5]. The forecasts were scaled from all of Alaska to just the Railbelt by assuming 76% of vehicles in the AEA Alaska forecasts were on the Railbelt, which was based on the number of registered vehicles in the state versus in communities along the Railbelt. The historical growth rates for electric vehicles in Anchorage were obtained from CEA’s electric vehicle information [12]. The AEA forecasts and the historical numbers of EVs on the Railbelt can be seen in Figure 3.

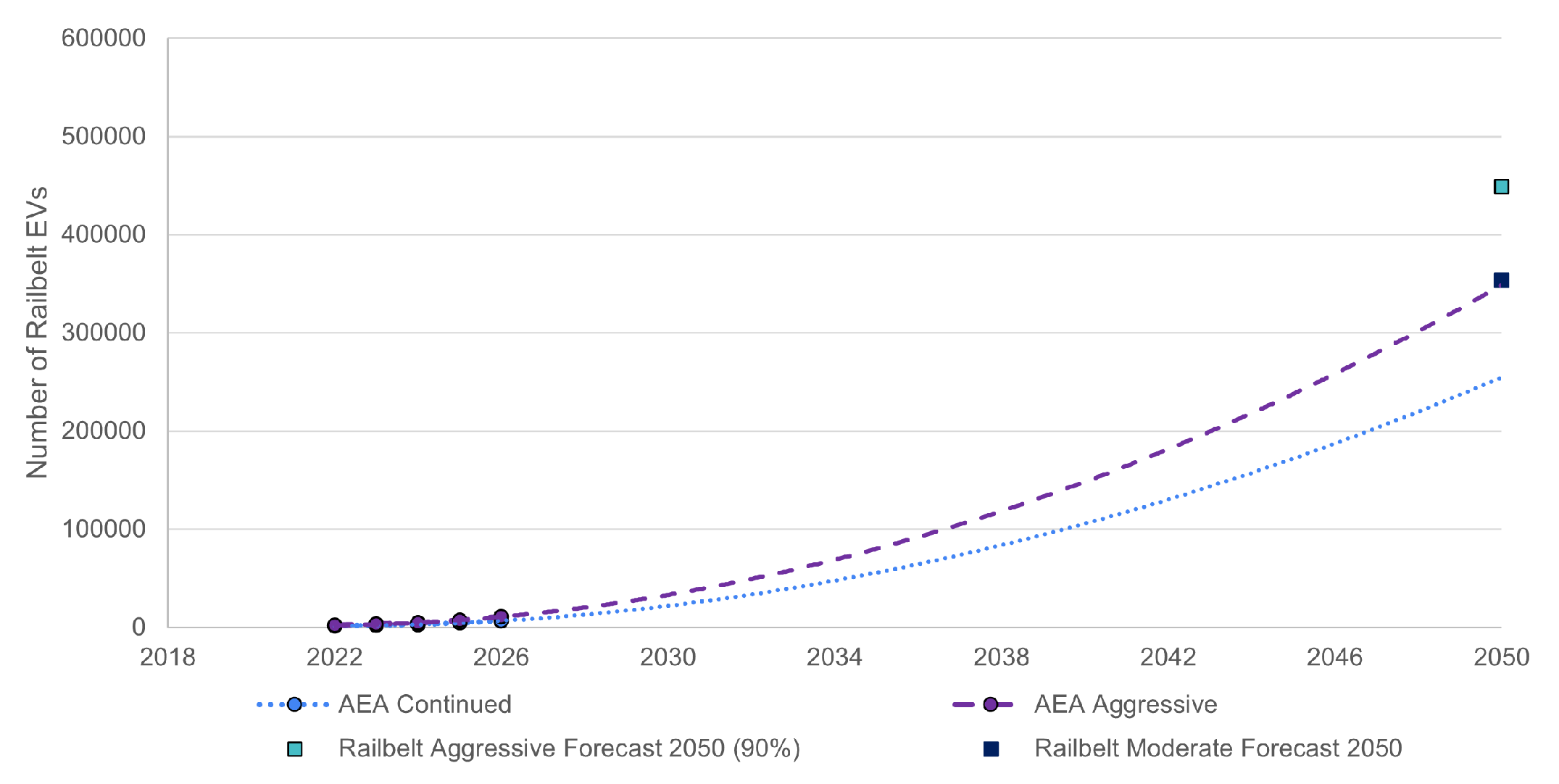

The AEA forecasts were then extended to 2050 based on an assumed continuation of 2nd degree polynomial growth. The moderate forecast of EV adoption in this study is assumed to be the result of the extended AEA aggressive forecast. In 2050, the number of EVs on the Railbelt for the moderate forecast is 353,381 which equates to 71% of vehicles based on 2022 Alaska DMV number of registered vehicles in the Railbelt. The aggressive forecast for this study assumes 90% of vehicles will be EVs, which equates to 449,000 vehicles. These forecasts are illustrated in Figure 4.

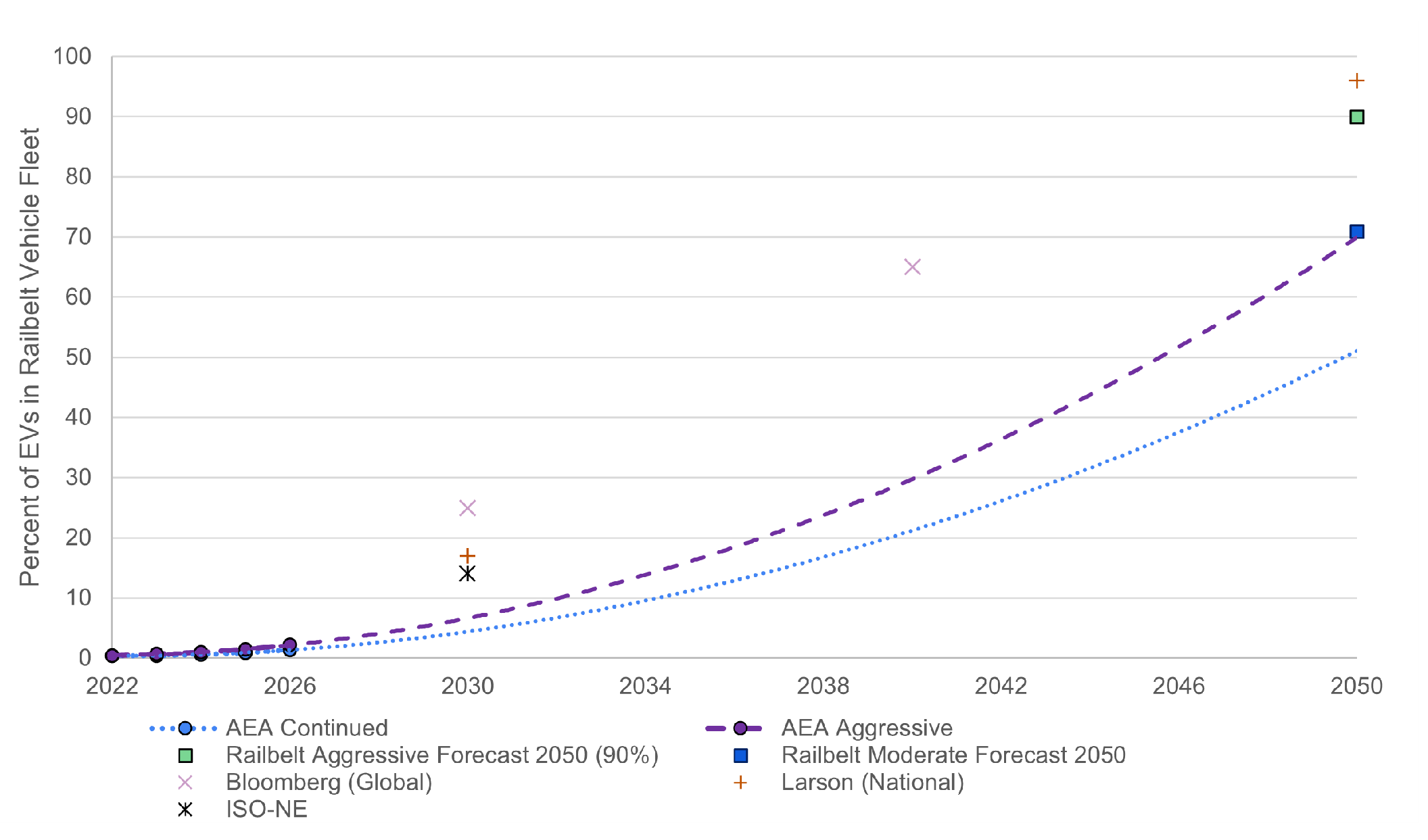

To compare these EV adoption forecasts to other regional, national, and global forecasts, the number of EVs used in Figure 5 was converted to the percent of vehicles in the Railbelt in Figure 5. The Bloomberg Electric Vehicle Outlook for Electric Vehicles [13] for leading markets is shown as comparison, as the United States is considered a leading market. The ISO-NE EV forecasts [7] are shown as a comparison to another cold region in the United States, as EV performance degrades in cold weather. Additionally, the national EV adoption forecasts from [14] is also illustrated in Figure 5.

The Railbelt EV adoption forecast is slightly lower than ISO-NE, the United States, and global leading market adoption forecasts as seen in Figure 5. The Railbelt adoption rate in 2030 is approximately 10% compared to 15-25% adoption for the other regions. This lower adoption rate is reasonable and is expected for the Railbelt in Alaska due to the increased energy use both while parked and while driving in cold-climate as outlined in [15].

3.2. Behind-the-Meter Solar

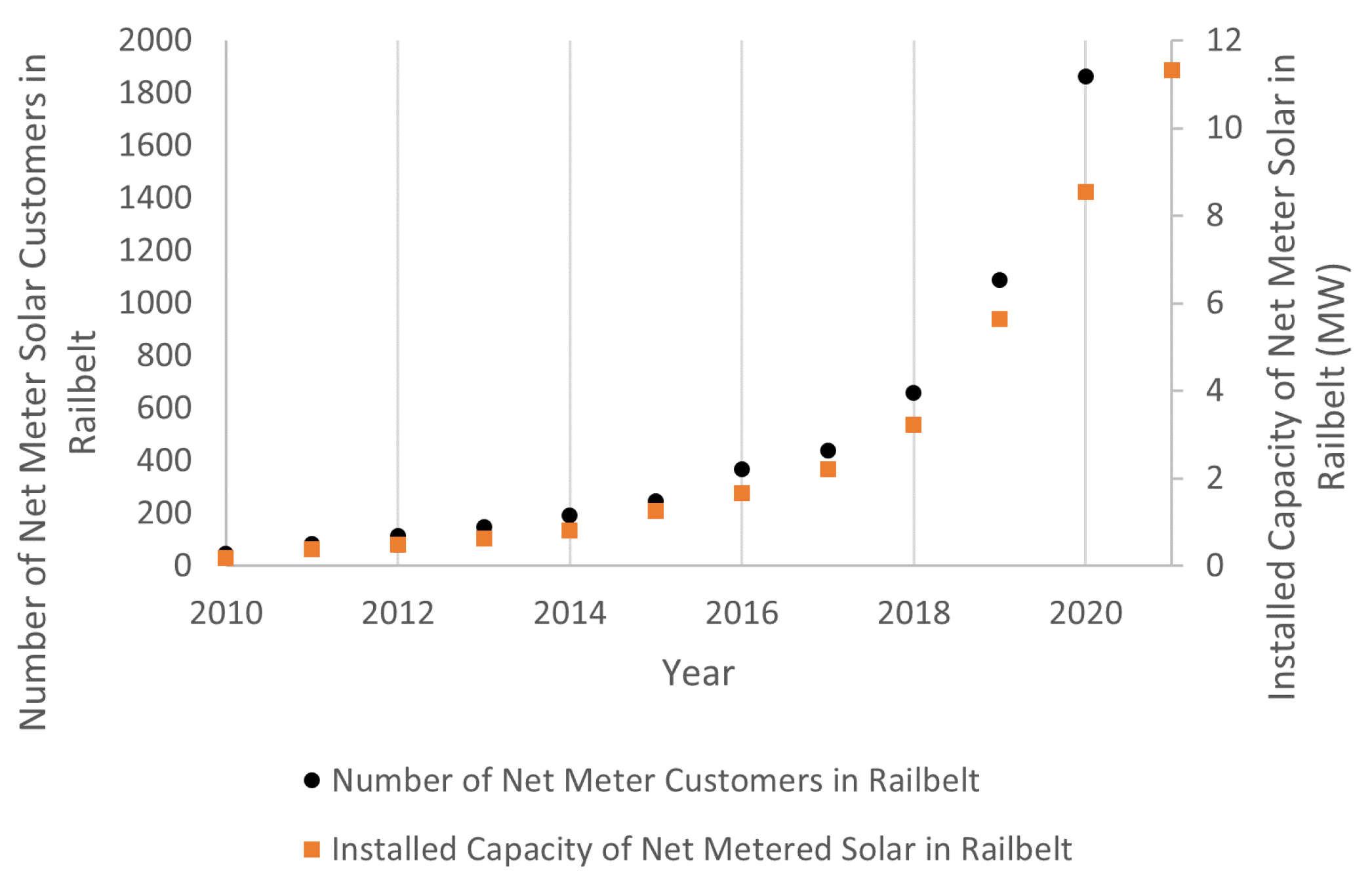

The primary constraints for solar PV adoption in Alaska are the lack of state incentives and a renewable portfolio standard (RPS), and the ITC’s effective years. Alaska currently has no RPS, although an Alaskan senate bill had been introduced to enforce one but it was not passed in the 2023 state legislative session. BTM solar incentives available to Alaska include the federal solar ITC and local solarize programs where discounts are available for community-wide solar installations. The ITC provides a 30% discount for solar PV installation between 2022 and 2032, decreasing to 26% in 2033, and 22% in 2034 [16]. Despite the lack of state incentives or mandates for clean energy generation, the Railbelt has experienced exponential growth of the BTM capacity of BTM solar PV, which is illustrated in Figure 6 [17].

The BTM solar forecast generated in this work used several factors to determine growth rates, including:

- ITC expiration date

- Projected electricity prices

- Projected solar costs

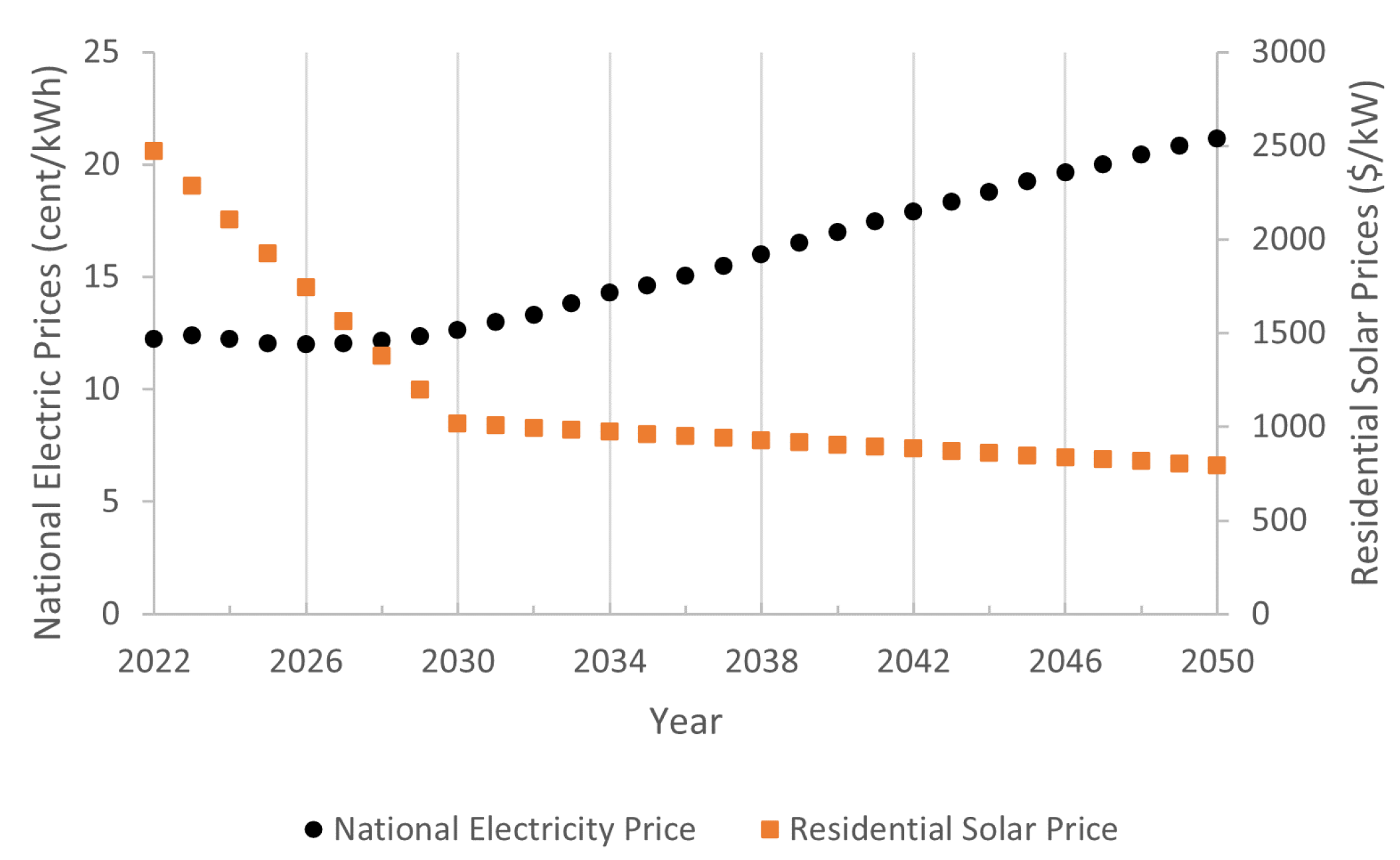

The Energy Information Administration’s (EIA) energy outlook predicts national electricity rates to increase linearly beginning around 2027 [18]. The National Renewable Energy Laboratory’s (NREL) Annual Technology Baseline (ATB) for residential and commercial PV costs (levelized cost of energy (LCOE), operations and maintanence (O&M), capital expenditures (CAPEX)) shows decreasing costs for both the moderate and advanced scenarios until 2030, then decreases at a lower rate after 2030 [19]. These electricity and solar costs forecasts are illustrated in Figure 7.

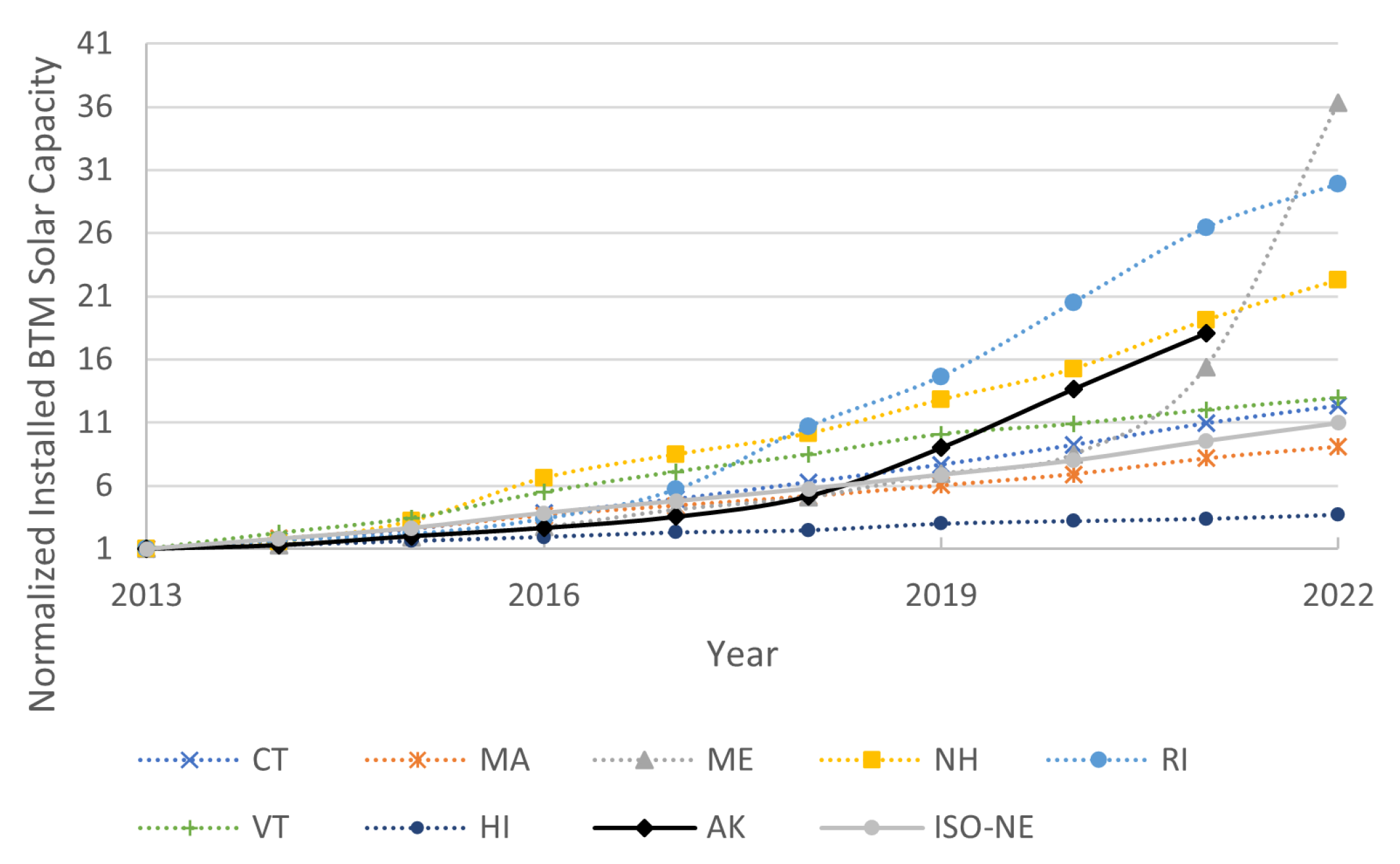

The historical Railbelt BTM solar capacity was compared to other BTM solar forecasts across the United States including the states within ISO-NE’s territory (Maine, Massachusetts, Vermont, New Hampshire, Connecticut, and Rhode Island) [20], representing a cold region and Hawai’i [21], representing a region with very high BTM solar installations rates. The Hawai’i installed capacity is from the Hawaiian Electric, Hawai’i Electric Light, and Maui Electric covering the islands of Maui, Lana‘i, and Moloka‘i. For equal comparison between regions, the installed capacity forecasts are normalized by the 2013 amount of installed BTM solar capacity.

Figure 8.

Historical Behind-the-Meter solar installations in the Railbelt, in ISO-NE, and Hawai’i normalized by 2013 installed capacity by region [20,21].

For perspective, the historical BTM solar installed capacity as a percentage of peak load is 0.5% in ISO-NE (2022 net peak load in ISO-NE was 24,780 MW [22]), 74.7% in Hawai’i (2020 net peak load in HECO was 1,496 MW: Hawai’i was 183 MW [23], O‘ahu was 1,116 MW [24], Moloka‘i was 5.8 MW, Lana‘i was 6.14 MW, Maui was 185.3 MW [25]), and 1.5% in the Railbelt (2021 net peak load in Railbelt was 765.3 MW). Note that the Hawai’i and ISO-NE are summer peaking systems, and therefore, BTM solar will impact the peak load in those regions. In the Railbelt, the peak load occurs in winter, and therefore, BTM solar will have the most impact during the lowest load period in the summer, which was 381 MW in 2021. Therefore, the 2021 Railbelt BTM solar capacity as a percentage of the minimum summer load is 4.8%. A better comparison of BTM solar impact to the system would be a energy generation comparision. However, that information was unavailable. ISO-NE and Hawai’i will have a greater amount of energy generation per installed capacity due to high capacity factors in those regions with lower latitudes compared to the Railbelt. Therefore, even though the percentage of BTM solar by installed capacity to peak load and minimum load is larger in the Railbelt compared to ISO-NE, ISO-NE will experience a greater impact from BTM solar in terms of total energy generation.

A significant finding is that the Railbelt in Alaska is experiencing a similar growth rate (not total amount) in BTM solar to ISO-NE compared to peak load and as normalized by 2013 installed capacity. This growth rate is similar despite lower capacity factors in the Railbelt and a lack of state incentives for BTM solar in Alaska. The growth rate as normalized by 2013 installed capacity amounts in Hawai’i is lower compared to ISO-NE and the Railbelt. Hawai’i’s lower growth rate is likely due to reaching hosting capacity limits of the distribution and transmission system in Hawai’i due to high percentage as compared to peak load (74.7%). Therefore, it is reasonable to expect continued BTM solar growth rates in the Railbelt similar to those which are currently seen.

This work predicts continued exponential growth based on the number of installations or number of buildings with solar, based on the exponential growth shown in Figure 6, until 2027 which is halfway through the duration of the ITC which ends in 2032.

After the four year period of exponential growth from 2023 through 2027, it is assumed that solar installations will continue to increase linearly. The linear growth rate was based on the rate of change from 2025 to 2027, which equates to approximately 3,318 customers per year. This rate of change was applied from 2028 to 2033, a year after the 30% ITC discount ends. This is to reflect possible construction delays.

From 2034 to 2040, estimated electric costs are increasing, estimated solar installation costs have a small rate of decline, and the ITC discount is decreased to 26% and 22% for systems installed by 2033 and 2034, respectively. Therefore for this time period, it was assumed that installations will continue to increase, but at half of the previous rate, about 1,659 customers per year.

It is expected that the percentage of households that can afford to install solar PV that haven’t already done so will also decrease over time, which is predicted to negatively impact solar adoption in the absence of solar incentive programs for low and middle income households. For the period from 2040 through 2050 the growth rate is halved again to 829 customers per year to reflect this impact. By the end of 2050, the projected number of residential and commercial buildings with solar is 53,386. Given that the number of residential and commercial buildings in the Railbelt is 292,035 this means that 18% of residential and commercial buildings in the Railbelt will have installed BTM solar according to this forecast.

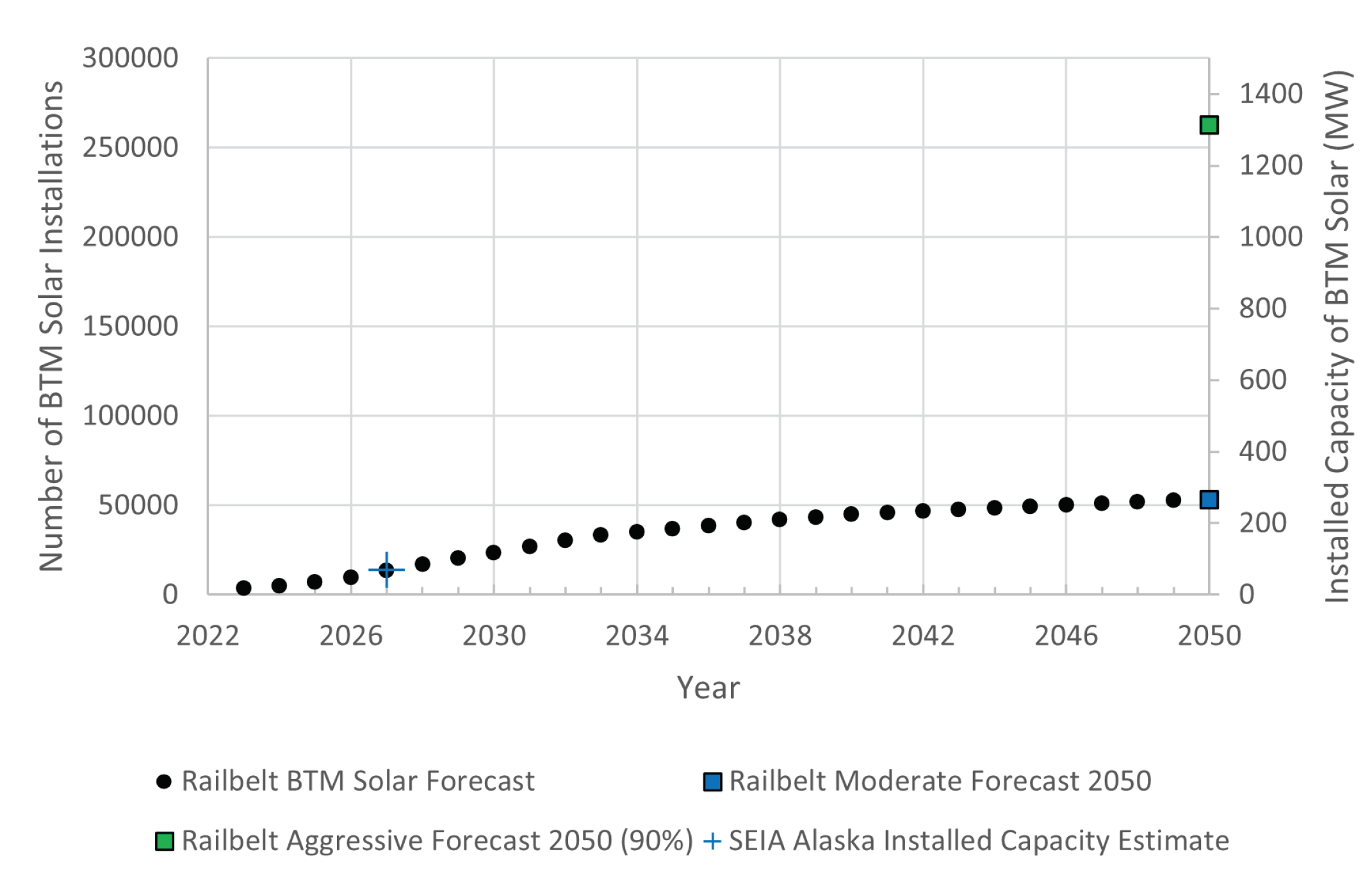

Using the current typical BTM solar installation size of 5 kW per install, the installed BTM solar capacity is calculated. The BTM solar forecast by number of installations and by capacity is shown in Figure 9. For comparison, the Solar Energy Industries Association’s (SEIA) five year growth projection for Alaska was also included in Figure 9 at a total of 69 MW by 2027. This is very similar to the introduced Railbelt BTM solar forecast.

The aggressive solar forecast introduced in this study assumes a 90% of residential and commercial buildings will install BTM solar by 2050. This equates to 262,832 houses, and a total installed capacity of 1,314 MW based on a 5 kW typical installation size per building.

3.3. Heat Pumps

The heat pump adoption rate assumes a new installation of a heat pump. This does not assume the full replacement of heating systems, since, for most of the Railbelt, temperatures routinely fall below the efficient operating range of heat pumps when a back up heat source would be necessary. The purpose of this heat pump adoption forecast is to predict the impact heat pump installations would have to load and not to transition all heating sources to electricity.

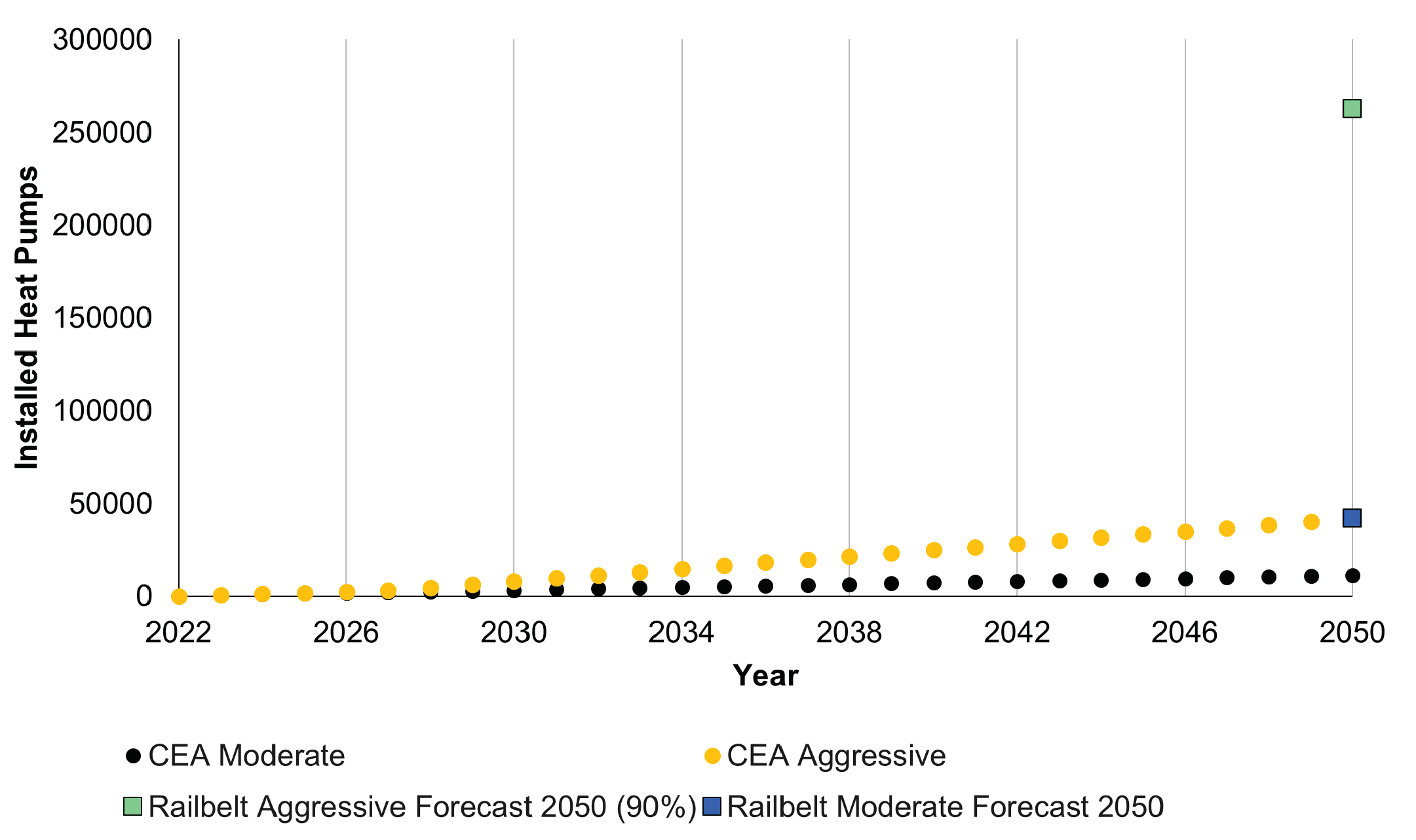

CEA generated a heat pump forecast for the CEA service territory [26]. This heat pump forecast was expanded to include all of the Railbelt and extrapolated to 2050. The CEA moderate and aggressive forecasts were continued at the same growth rate from the original forecast of 2032 out to the target of 2050 for this study. The forecast was also increased by 97% to expand to the entire Railbelt at an equal rate of adoption. The forecasts are shown in terms of number of installations and by the installed capacity assuming a 3.2 kW rating per heat pump. The CEA moderate and aggressive based forecasts are illustrated in Figure 10.

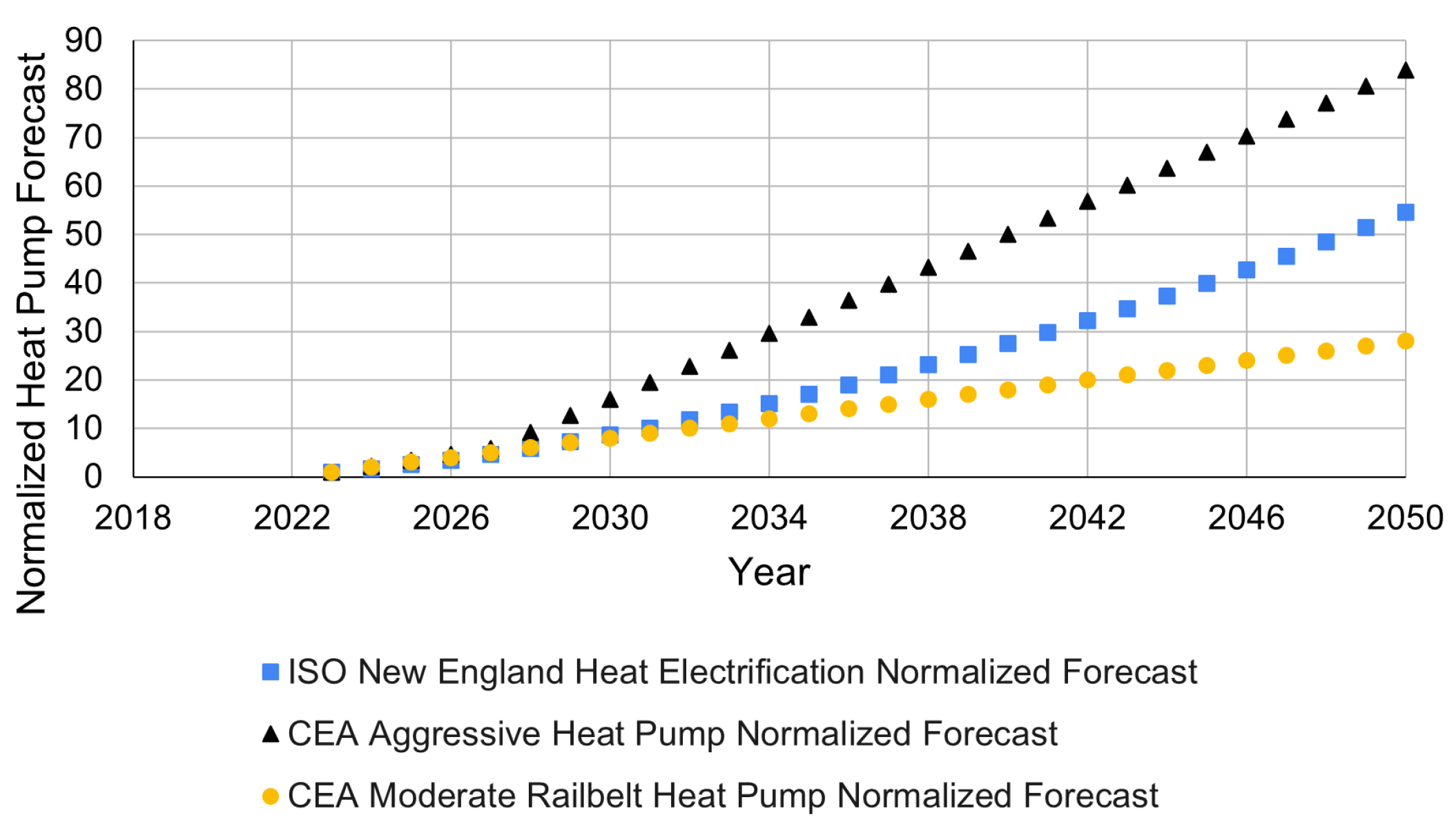

The ISO-NE’s 2022 Heating Electrification Forecast was use to provide comparison to the Railbelt heat pump forecasts as extrapolated from CEA’s forecasts. The forecasts were normalized by the 2022 number of installations to provide more equal comparison of the forecasted growth rates. These normalized heat pump growth forecasts are shown in Figure 11.

The heat pump forecasts for 2023 from ISO-NE and from CEA are also compared by percent of total occupied housing. The 2023 ISO-NE heat electrification forecasts estimates 63,700 heat pump installations in 2023, out of approximately 6 million occupied housing units, equates to 2.2% of households. The CEA moderate and aggressive forecast estimates 200 and 250 installed heat pumps respectively for the moderate and aggressive forecast in 2023 in CEA’s territory. This extrapolates to 400 and 500 installed heat pumps for the moderate and aggressive forecasts for the Railbelt, which equates to 0.2% and 0.25% of occupied housing units. In comparison to ISO-NE, the number of heat pumps forecasted to be installed in the Railbelt in 2023 is 10 times less than ISO-NE. Therefore, ISO-NE is much farther along in adoption of heat pumps than the Railbelt, and it is feasible that adoption of heat pumps in the Railbelt may exceed that in ISO-NE on a per household basis due to its low 2023 forecasted adoption rate.

ISO-NE is primarily heated with natural gas [27], which has a price of $16.60/MMBtu [28]. In the Railbelt, the central region is primarily heated by natural gas as well but at a slightly lower price of $14.46/MMBtu. The northern and southern regions have a greater mix of heat energy sources, including #1 heating oil with a current price of $29.84/MMBtu. In the Fairbanks North Star borough in the northern load region where heating oil is common, U.S. Environmental Protection Agency’s air quality standards are in violation. As a result of those violations proposed actions include the use of ultra-low sulfur diesel to replace use of heating oil and additional measures to reduce PM and SO emissions from coal power plants [29]. Both of these proposed measures would increase the cost of residential heating and electricity, which will impact the value of heat pumps in the region.

Additionally, affordable natural gas availability in Alaska is uncertain according to statements from the operator of the Cook Inlet natural gas wells, Hilcorp [30]. Since natural gas is the primary fuel used to generate electricity on the Railbelt, an increase in the price of natural gas resulting from a reduced supply will impact the price of electricity, which is used to operate a heat pump. Regional variation in climate, electricity prices, heating fuel prices, and heating fuel availability will play a role in the adoption rate of heat pumps. Heat pumps provide an additional value beyond heating in New England as they can also provide air conditioning whose need in this region has increased over the years. In comparison, there less but not negligible need for air conditioning in the Railbelt.

Taking into account the tradeoffs between the cost of heating fuels, value of air conditioning, normalized forecasts, percent adoption of heat pumps comparison, and affordable natural gas availability risk in the Railbelt, it is estimated that the Railbelt will have a higher adoption rate than ISO-NE. Therefore, the aggressive heat pump forecast proposed in this study follows the extrapolated CEA moderate forecast. This equates to 41,916 heat pump installations in commercial and residential buildings by 2050, which is 14.4% of all commercial and residential buildings. This would result in a potential maximum additional load of 160 MW from heat pumps, though it is unlikely that all heat pumps would be consuming electricity at the same time. It is noted that this forecast will change and should be updated in the event of unavailability of affordable natural gas.

The aggressive heat pump forecast introduced in this study assumes that 90% of residential and commercial buildings will install a heat pump by 2050. This equates to 262,832 houses, and a potential maximum additional load of 841 MW based on a 3.2 kW typical installation size per building.

3.4. Base Load

The current load profile, referred to here as baseline load, from 2021 was increased by 12% for 2040 as was done in the NREL Alaska RPS report [31]. This rate of growth was continued to 2050, resulting in approximately 18% load growth from 2021 to 2050 of the current load profile. The hourly total load and load characteristics are provided in following sections.

4. Hourly Load Data

4.1. Electric Vehicle Hourly Load Profile

The hourly load from EVs was created using collected Alaskan EV efficiency data, temperature versus efficiency data, and load shapes derived from the ISO-NE EV forecasts. The steps taken are outlined below, and the detailed methodology is provided in Appendix A.

- Calculate total vehicle type counts per each load region.

- Calculate electricity use per mile while driving.

- Determine driving profiles (miles traveled per day).

- Calculate energy use while parked.

- Calculate daily EV load by load area.

- Calculate hourly loads by load area using load shapes.

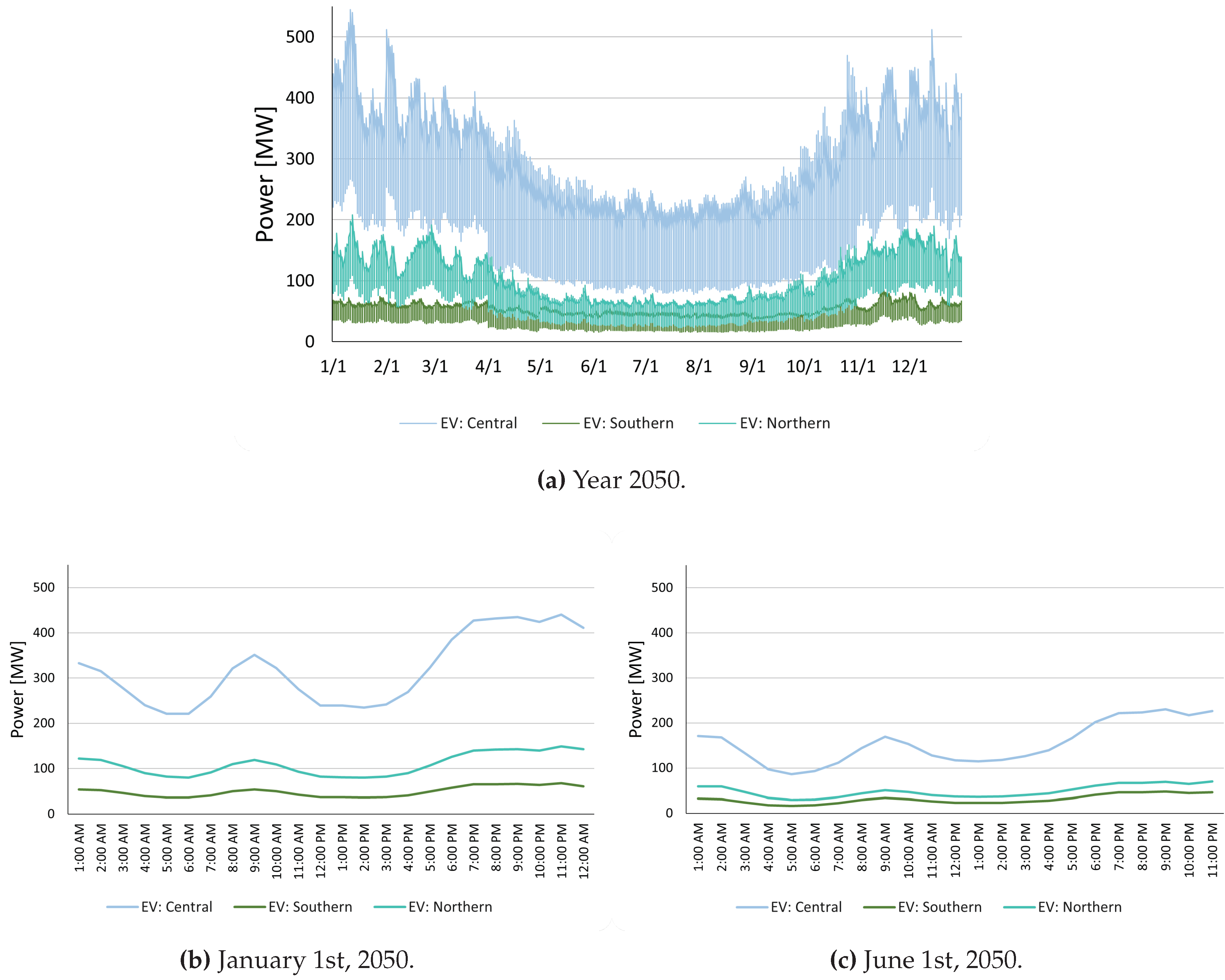

The hourly load demand from EVs for the moderate forecast are shown in Figure 12 showing results for the year 2050, January 1st 2050, and June 1st 2050.

In the aggressive forecast it was assumed that 20% of the EV load can function as a flexible load. Since 20% of the EV load is assumed flexible, the load shapes, which reflect smoothing due to aggregation of many vehicles, would apply to 80% of the EV load. The 20% flexible load is served during hours chosen each day to minimize electricity production cost. For both of these reasons, no smoothing was applied to the flexible EV loads.

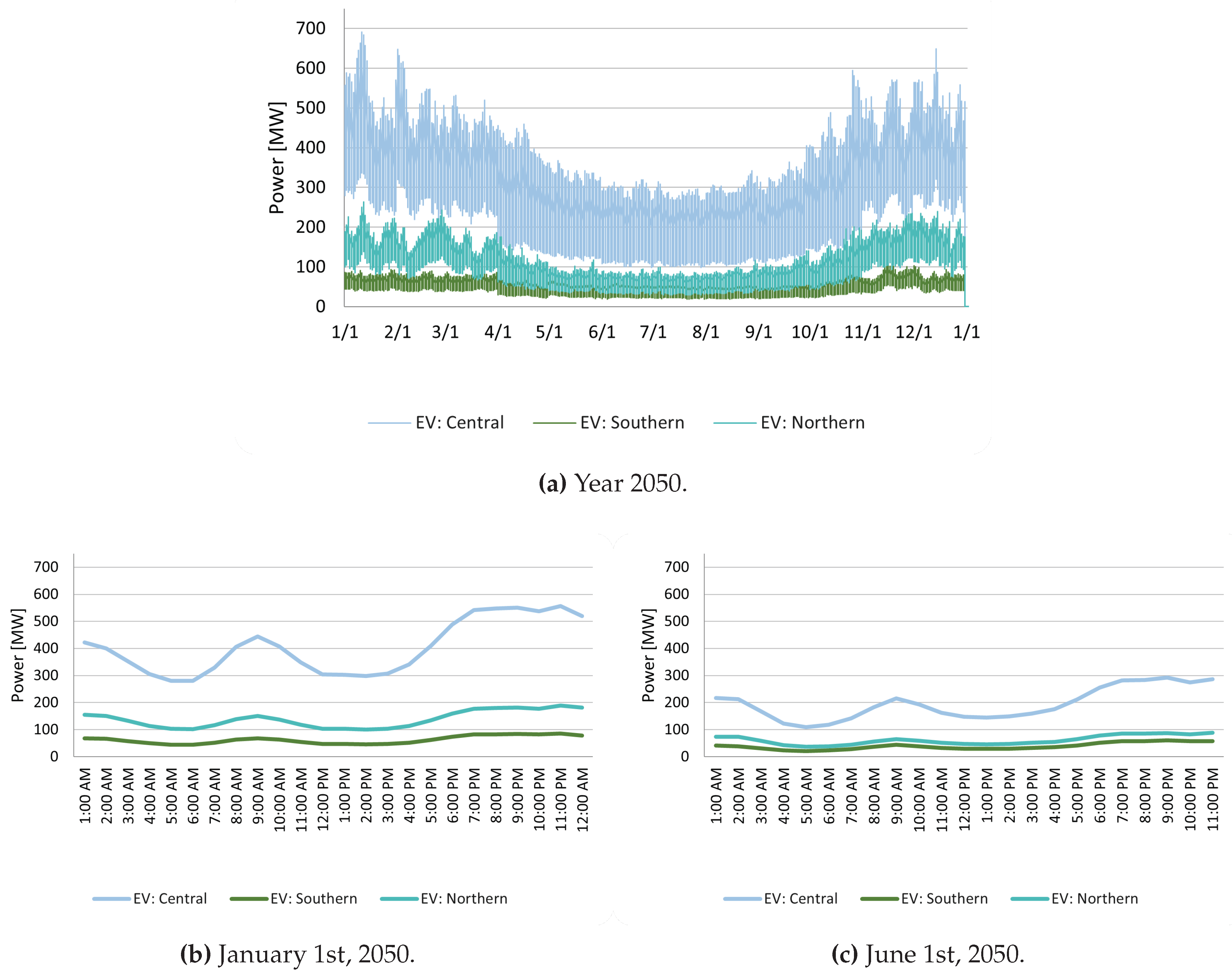

The hourly load demand from EVs for the aggressive forecast are shown in Figure 13 showing results for the year 2050, January 1st 2050, and June 1st 2050.

4.2. Behind-the-Meter Solar

NREL’s System Advisor Model (SAM) [32] was used to create the hourly generation profiles using typical meterological year (TMY) irradiance data for three representative locations: Anchorage (Central), Soldotna (Southern), and Fairbanks (Northern). A PVWatts [33] photovoltaic model with no financial model was used in the SAM simulation. Most of the default settings applied except for the following changes in the system design:

- the DC nameplate capacity was set to the allocated solar for each region

- 45° tilt

- 180 Azimuth

- ground coverage ratio of 0.3

- bifacial module

- albedo of 0.5

The individual hourly BTM solar generation data was multiplied by the number of commercial and residential buildings with BTM PV installations as estimated by the moderate and aggressive forecasts for BTM PV adoption in the Railbelt. Gaussian noise was then added to the BTM solar generation for the moderate forecast to account for geographical diversity of the residential solar behavior beyond the three selected locations. The BTM solar generation for the aggressive forecast also had gaussian noise added. Additionally, a 9-hour average moving filter was applied to incorporate control by DERMS through household batteries to make the daily load fluctuations from residential solar more manageable by other generation resources.

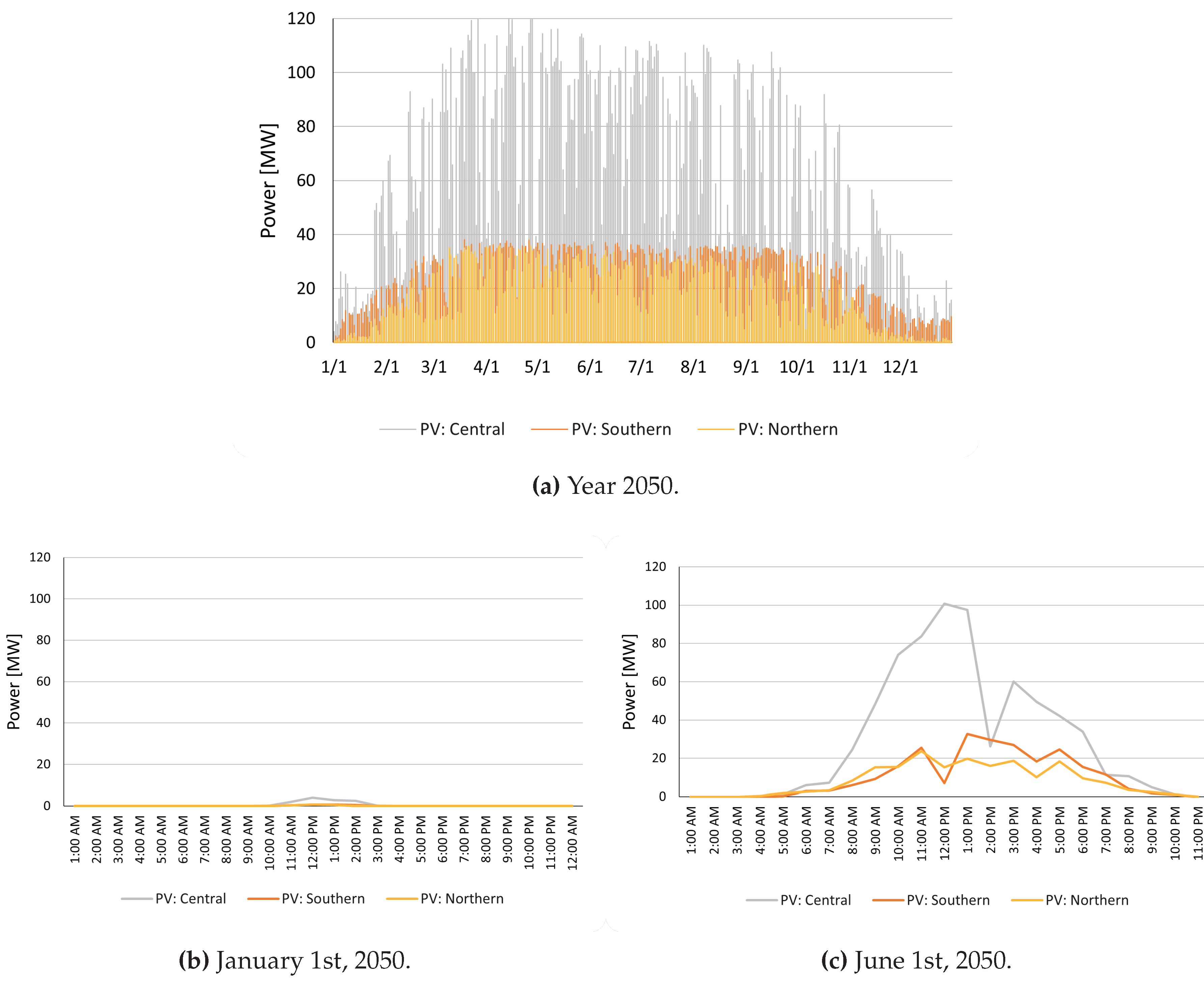

The hourly generation from BTM solar for the moderate forecast is shown in Figure 14, which shows results for the year 2050, January 1st 2050, and June 1st 2050.

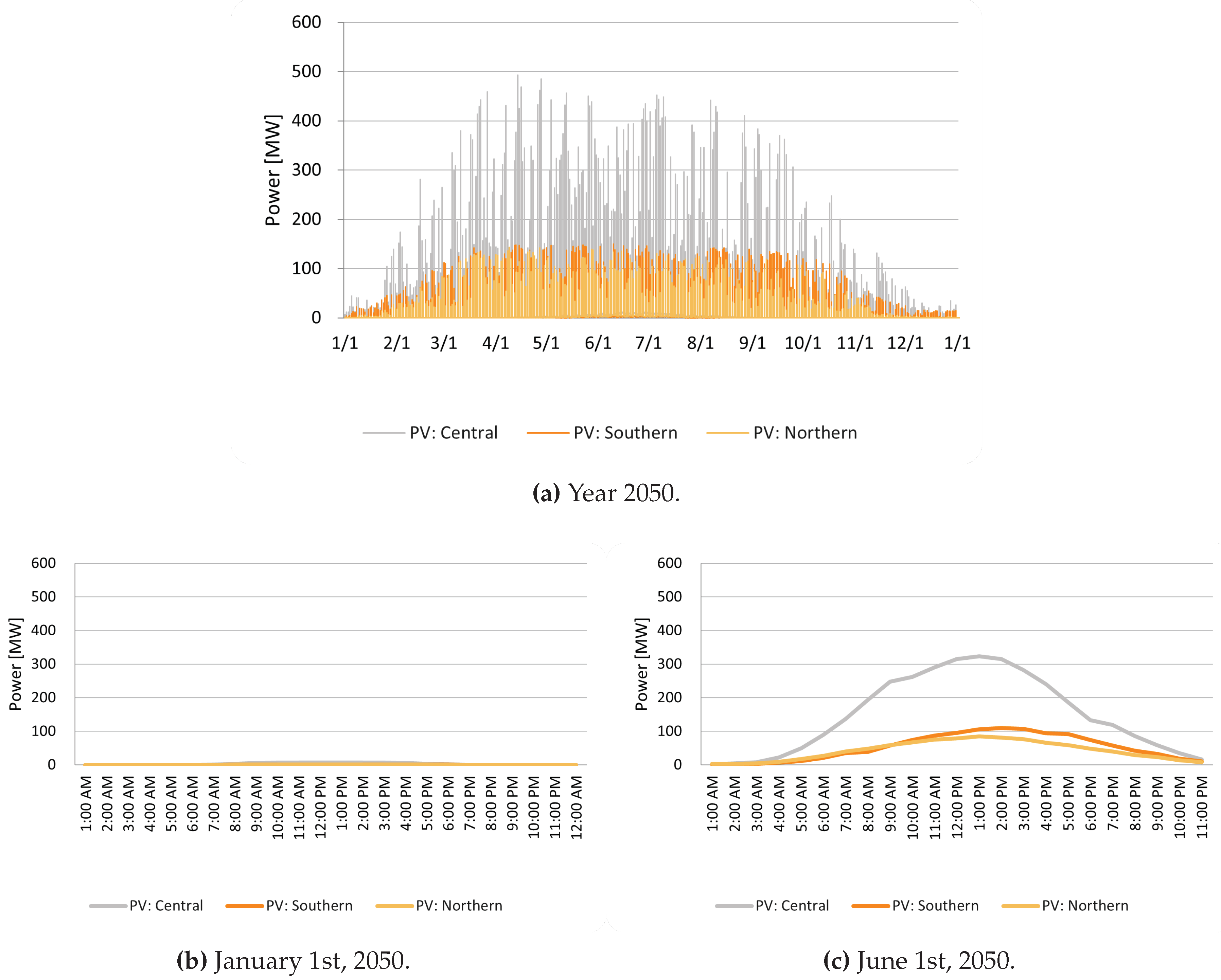

The hourly generation from BTM solar for the aggressive forecast is shown in Figure 15, which shows results for the year 2050, January 1st 2050, and June 1st 2050.

4.2.1. Heat Pumps

Hourly electricity consumption from heat pumps was based on three individual representative heat pumps located in Anchorage (Central), Soldotna (Southern), and Fairbanks (Northern) to represent the three load regions. The electrical rating of the heat pump is assumed to be 3.2 kW. The Alaska Mini-Split Heat Pump Calculator [34] was used to generate the hourly electrical consumption rates for each representative heat pump in each location using TMY weather data. The individual hourly heat pump data was multiplied by the number of commercial and residential buildings with installed heat pump as estimated by the moderate and aggressive forecasts for heat pump adoption in the Railbelt. Gaussian noise was then added to the heat pump load for the moderate and aggressive forecasts to account for geographical diversity of the heat pump behavior beyond the three selected locations.

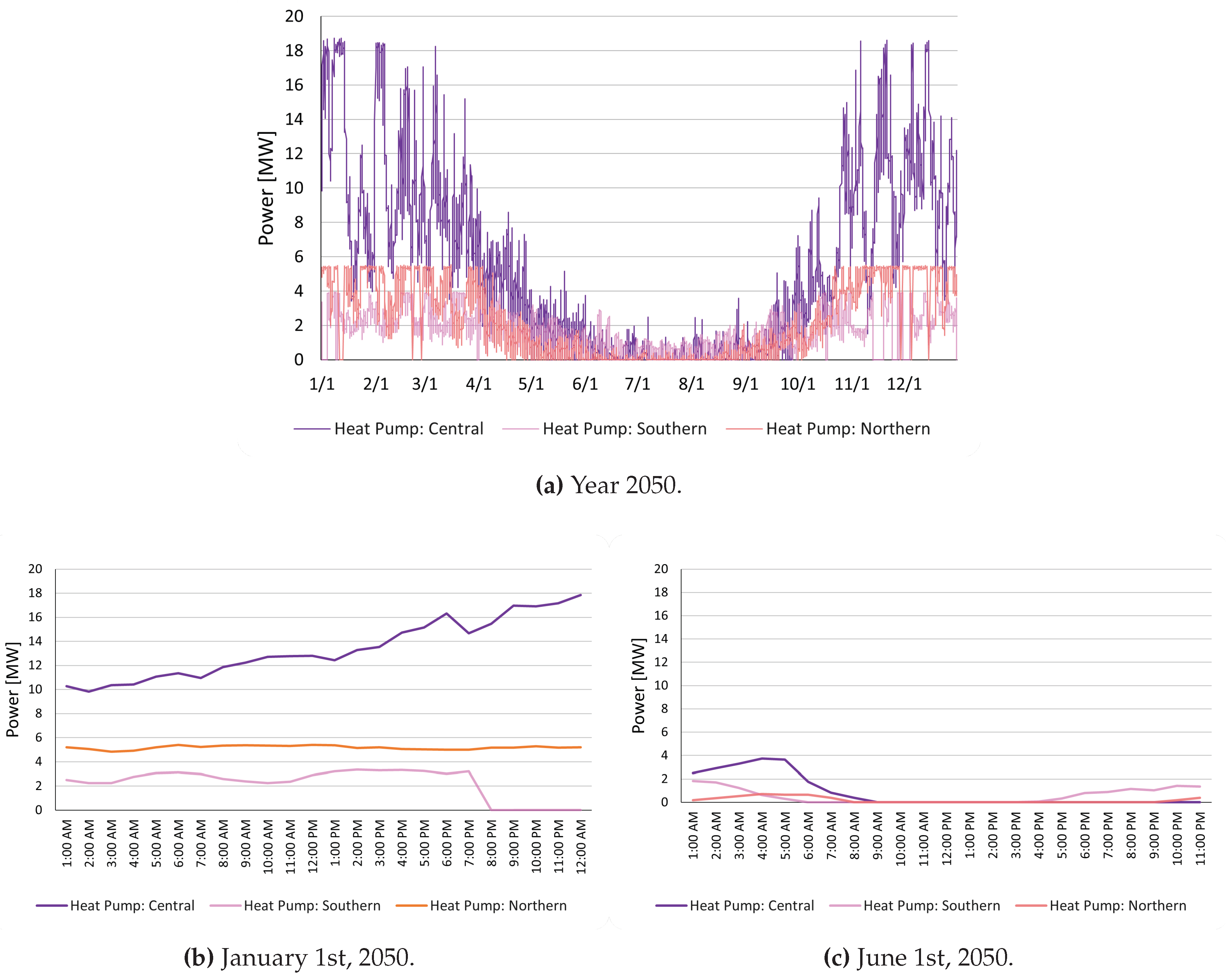

The hourly load demand from heat pumps for the moderate forecast is shown in Figure 16, which shows results for the year 2050, January 1st 2050, and June 1st 2050.

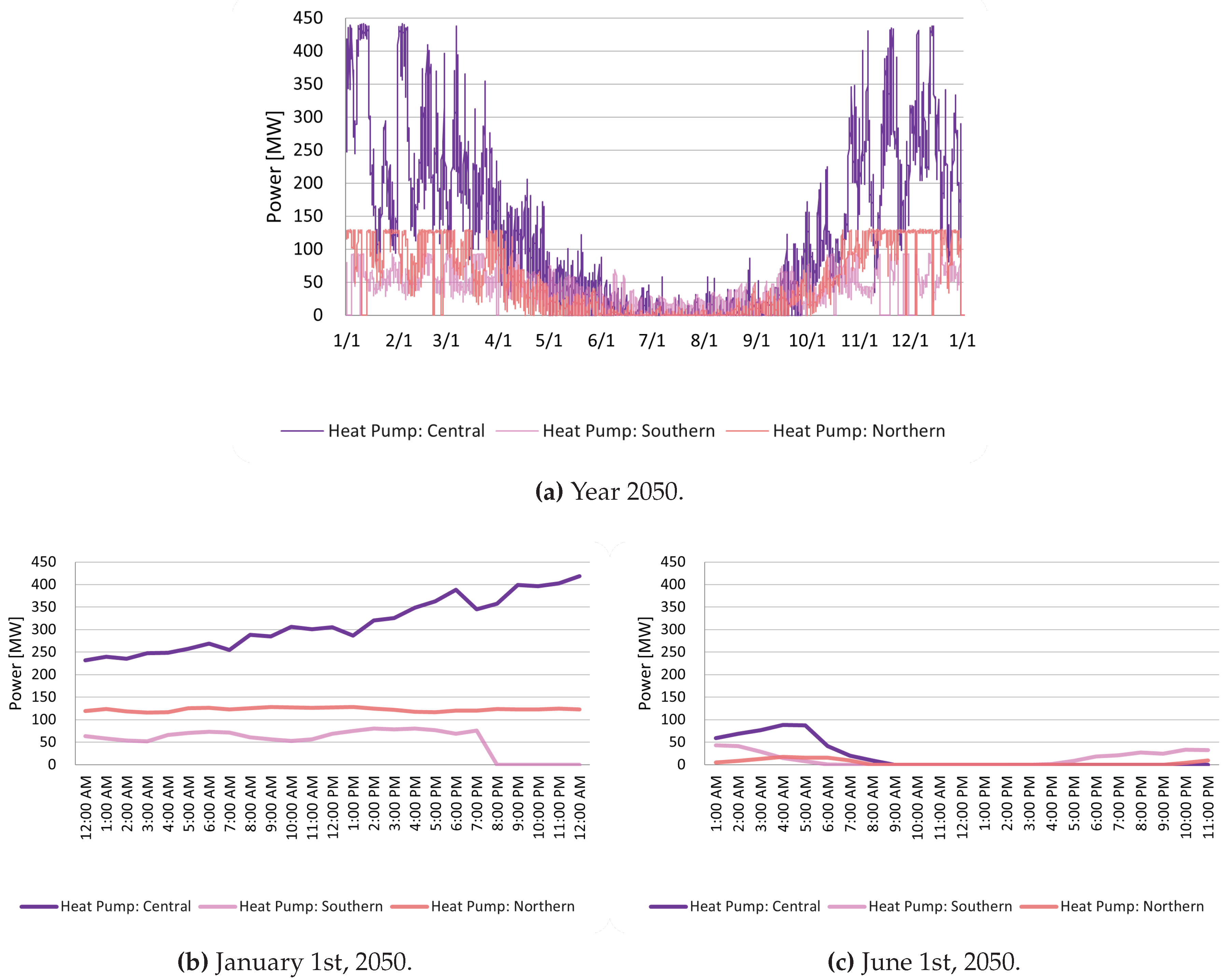

The hourly load demand from heat pumps for the aggressive forecast is shown in Figure 17, which shows results for the year 2050, January 1st 2050, and June 1st 2050.

5. Total Load Characteristics

Load characteristics from the current 2021 load and the 2050 aggressive and moderate load forecasts are presented in Table 3.

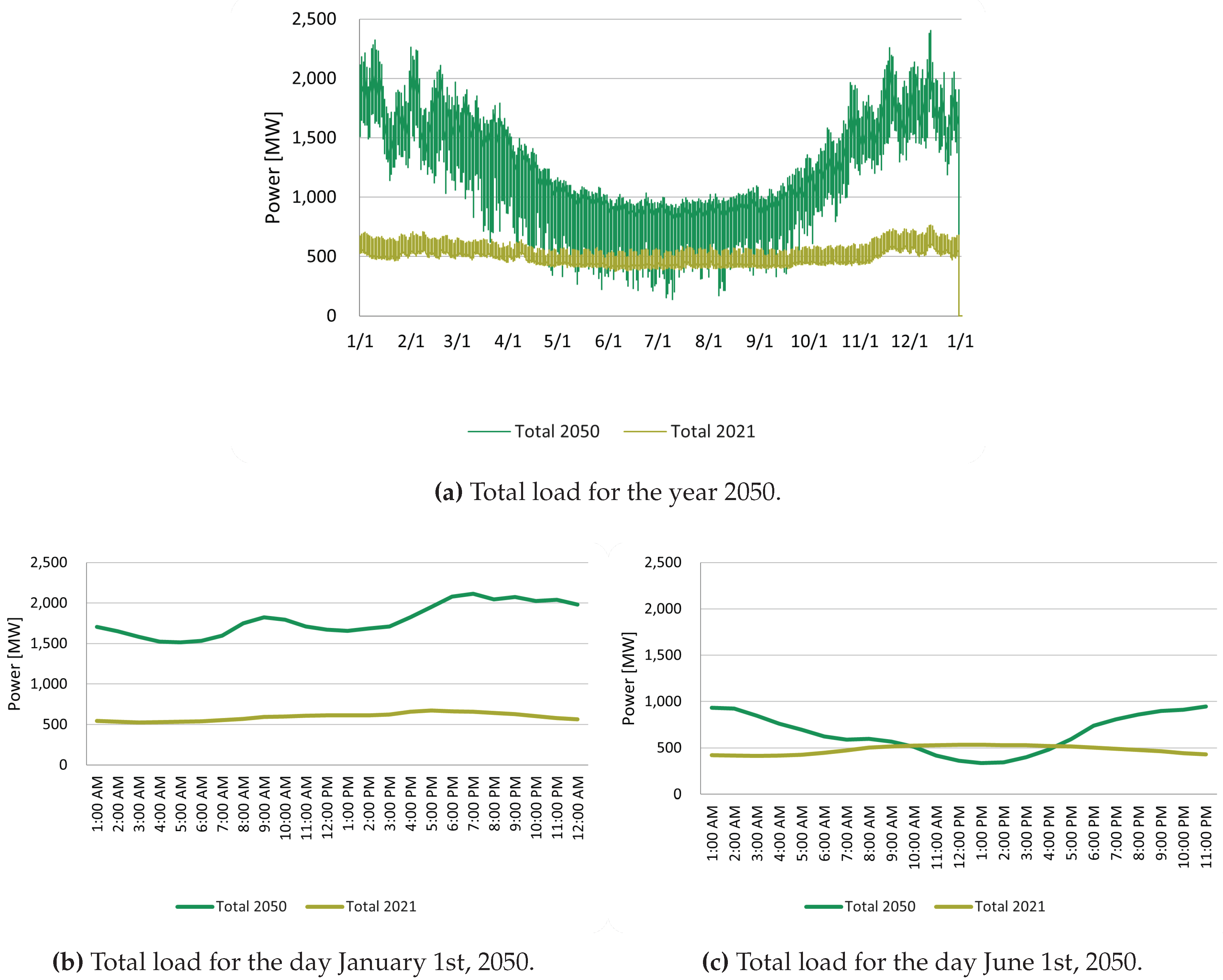

The hourly total load demand, including the base load, heat pumps, electric vehicles, and generation from residential solar for the moderate forecast are shown in Figure 18 showing results for the year 2050, January 1st 2050, and June 1st 2050.

The total hourly load demand for the aggressive forecast are shown in Figure 19 showing results for the year 2050, January 1st 2050, and June 1st 2050.

This moderate adoption 2050 load forecast results in a 80% increase in the total energy and a 113% increase in the peak load. The minimum load in the system is increased by 53%. The hourly demand change increased by 260% which is significantly higher than the increases in total energy and peak load. This suggests that DERMS would be beneficial to control and smooth the load fluctuations.

This aggressive adoption 2050 load forecast results in a 116% increase in the total energy and a 219% increase in the peak load. In addition, due to the increase in residential solar there is a reduction in the minimum load, which occurs in the summer when solar production is high. The minimum load is decreased by 62%. The hourly demand change increased by 381% , which is also significantly higher than the increases in total energy and peak load. Additional action may be needed through demand management and DERMS to manage load fluctuations.

These shifts result in a more heavily winter peaking system with relatively lower minimum summer loads. This will result in a higher emphasis of utility-scale wind generation in decarbonization scenarios than utility-scale solar. Care will be taken to study summer low load periods of time when system inertia may be low due to solar output, and frequency stability will be a concern.

6. Conclusion

This load and electrification adoption forecast for the Alaska Railbelt transmission system is the first Railbelt region-wide forecast proposed for this region. Adoption rates for BTM solar, EVs, and heat pumps are proposed for a moderate adoption forecast based on projections from current adoption rates and comparisons to other projections from local Railbelt utilities and states in ISO-NE’s territory. The proposed aggressive forecast provides a bookend comparison at the high adoption rate of 90% for all technologies.

The results of these forecasts demonstrate a significant increase in both energy and peak load demand for both the moderate and aggressive forecasts. The moderate forecast results in a 80% increase in total energy and 113% increase in peak load. The aggressive forecast results in a 116% increase in total energy and 219% in peak load. Notably, there are even greater increases in the maximum hourly load change at 260% and 381% for the moderate and aggressive forecasts, respectively. This suggests that significant demand management is needed to smooth and control the load fluctuations as a results of the adoption of BTM solar, EVs, and heat pumps.

These load forecasts were based on current trends and status of available energy resources, such as natural gas. As adoption trends and availability of energy resources change, these load forecasts should be updated to reflect those changes. The forecasts are useful for energy planning for the region, most pertinently the significant increase in load due to electrification despite BTM solar adoption.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “Conceptualization, P.C., A.F, J.V., S.C.; methodology, P.C., A.F., M.W., C.P., S.C.; formal analysis, P.C., A.F., M.W., S.C.; writing—original draft preparation, P.C., A.F., C.M., M.W., S.C.; writing—review and editing, P.C., J.V., S.C., D.P.; visualization, N.H.; supervision, P.C.; project administration, P.C.; funding acquisition, P.C., S.C. All authors have read and agreed to the published version of the manuscript.

Funding

This project is part of the Arctic Regional Collaboration for Technology Innovation and Commercialization (ARCTIC) 2 Program - Innovation Network, an initiative supported by the Office of Naval Research (ONR) Award #N00014-22-1-2049. This project is funded by the state of Alaska FY23 economic development capital funding.

Data Availability Statement

The hourly solar, heat pump, and electric vehicle load and generaiton data presented in this study are openly available in Zenodo at 10.5281/zenodo.8140771 [35].

Acknowledgments

Special thank you to the following organizations for providing staff expertise to comment and provide input on this work: Golden Valley Electric Association, Chugach Electric Association, Larry Jorgensen and David Thomas at Homer Electric Association, Matanuska Electric Association, Brian Hickey at Railbelt Regional Coordination, and Bryan Carey at Alaska Energy Authority. Special thank you to Alan Mitchell for providing heat pump load data.

Abbreviations

The following abbreviations are used in this manuscript:

| AEA | Alaska Energy Authority |

| ATB | Annual Technology Baseline |

| BTM | Behind the Meter |

| CAPEX | Capital Expenditures |

| CEA | Chugach Electric Association |

| DERMs | Distributed Energy Resource Management Systems |

| DMV | (Alaska) Department of Motor Vehicles |

| EV | Electric Vehicles |

| GVEA | Golden Valley Electric Association |

| HEA | Homer Electric Association |

| HECO | Hawaiian Electric Company |

| HVDC | High Voltage Direct Current |

| IPP | Independent Power Producer |

| ISO-NE | Independent System Operator - New England |

| IRA | Inflation Reduction Act |

| ITC | Investment Tax Credit |

| kW | kilowatt |

| kWh | kilowatt-hour |

| LCOE | levelized cost of energy |

| MEA | Matanuska-Susitna Electric Association |

| MW | megawatt |

| MWh | megawatt-hour |

| NEM | net energy metering |

| NERC | North American Electric Reliability Corporation |

| NREL | National Renewable Energy Laboratory |

| O&M | Operations and Maintanence |

| PV | Photovoltaics |

| RPS | Renewable Portfolio Standard |

| SAM | System Advisor Model |

| SEIA | Solar Energy Industries Association |

| TMY | Typical Meteorological Year |

Appendix A. Electric Vehicle Hourly Load Data Calculations

Appendix A.1. Step 1. Total vehicle type counts

The number of vehicles as provided through registered vehicle information from the DMV are outlined in Table 2. Each DMV region was assigned a weather city in order to use TMY hourly temperatures to model electricity use. The DMV regions were also assigned a load region. The weather city and load region associated with each DMV region are outlined in Table A1.

Table A1.

Utility, load region, and weather city for each DMV region.

| Area | Electric Utility | Load Region | Weather City |

|---|---|---|---|

| Fairbanks NorthStar Borough | GVEA | Northern | Fairbanks |

| City of Nenana | GVEA | Northern | Fairbanks |

| City of Delta Junction | GVEA | Northern | Delta Junction |

| Matanuska-Susitna Borough | MEA | Central | Wasilla |

| Municipality of Anchorage | CEA | Central | Anchorage |

| Kenai Peninsula Borough | HEA | Southern | Kenai |

Appendix A.2. Step 2. Electricity use per mile while driving

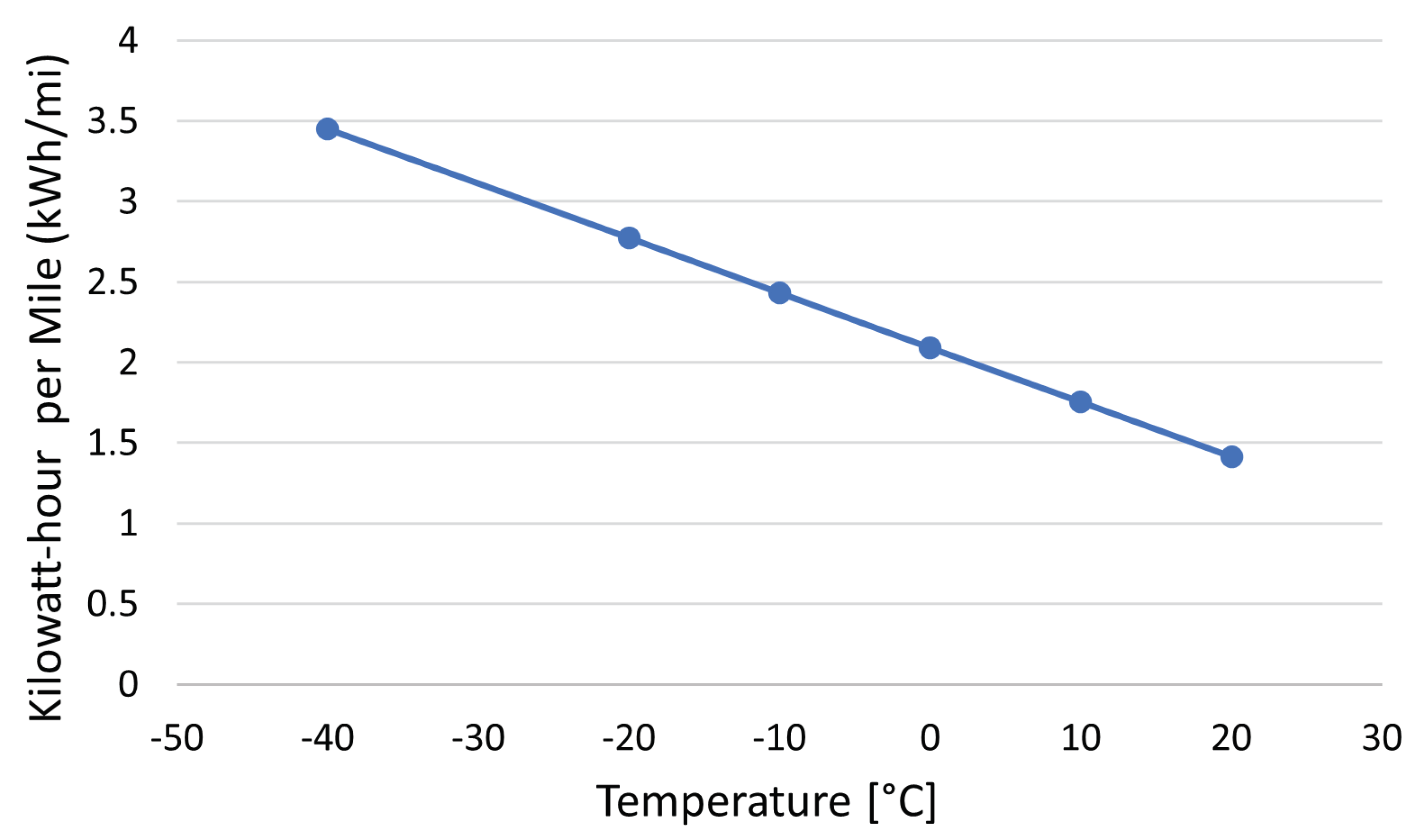

For vehicle types “car” and “truck,” the calculation of kWh per mile while driving is based on a fitted equation that relates kWh per mile to hourly temperature in degrees C. There are two building blocks to these energy per mile equations.

The first building block is the assumed maximum efficiency, which occurs at temperatures ranging from 20 ℃ to 25℃. It is assumed that the maximum efficiency for a car is 0.22 kWh/mile and for a “truck” is 0.43 kWh per mile. The 0.22 kWh per mile value for cars comes from crowdsourced data collected by Michelle Wilber of ACEP for several Alaska vehicles. The temperature associated with this efficiency is 25℃.

The 0.43 kWh/mile value for vehicle type “truck” (i.e., pickup trucks) comes from the 0.5 kWh/mile rated efficiency for the Ford F150 Lightning [36]. A 1.15x range improvement factor was applied to this value, which equates to a reduction in kWh per mile from 0.5 kWh per mile to 0.43 kWh per mile (0.43 = 0.5/1.15).

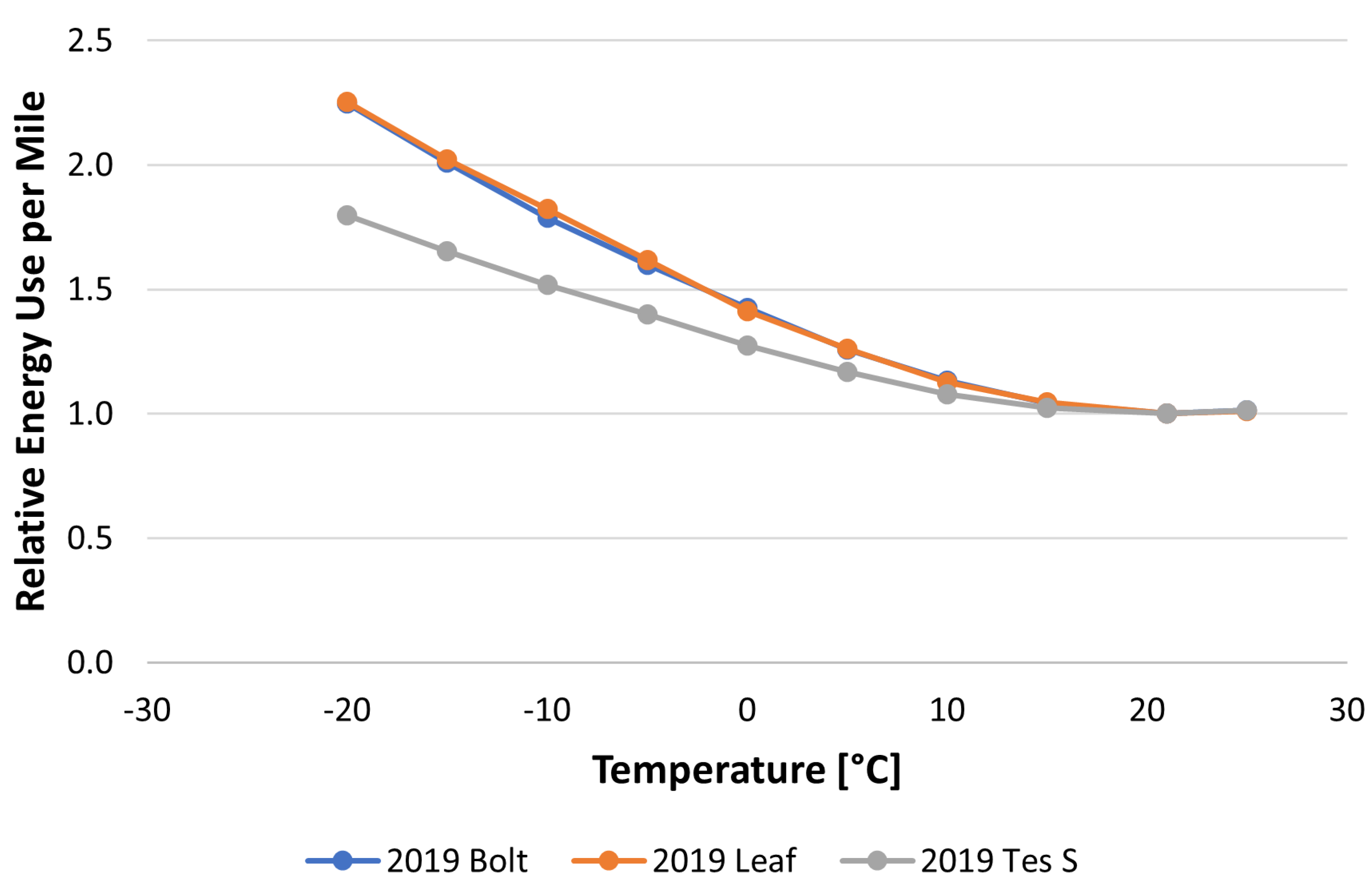

The second building block is an equation for relative energy consumption versus temperature. Relative energy consumption is inversely proportional to relative range, and therefore, can be directly calculated from reported data on range levels, or range reductions, vs. temperature. The following example illustrates the procedure. Data on range versus temperature compiled by Geotab Inc. [37] shows that the optimal range is achieved at 21℃ (about 70 F) and is 1.15 times the “rated range” reported by manufacturers. The Geotab range data are summarized in Table A2.

Table A2.

Geotab data on range vs temperature.

| Range, km | |||

|---|---|---|---|

| Temp [℃] | 2019 Bolt | 2019 Leaf | 2019 Tes S |

| 25 | 414 | 254 | 349 |

| 21 | 420 | 257 | 354 |

| 15 | 403 | 246 | 346 |

| 10 | 371 | 228 | 328 |

| 5 | 334 | 204 | 303 |

| 0 | 295 | 182 | 278 |

| -5 | 263 | 159 | 253 |

| -10 | 235 | 141 | 233 |

| -15 | 209 | 127 | 214 |

| -20 | 187 | 114 | 197 |

For a given vehicle, the relative energy use is inversely proportional to relative range. For example, using the 2019 Bolt data and taking the 21℃ range as the “base”: The relative range at 0℃ versus the range at 21℃ is equal to 295 divided by 420 which is 0.702. Therefore, the relative energy use is 1 divided by 0.702 which equals 1.42 = range at 21 / range at 0 = 420/295.

Converting the Geotab data into relative kWh per distance traveled yields the following plot shown in Figure A1, showing the basic relationship between kWh per distance traveled and temperature.

Figure A1.

Relative EV energy use at varying temperatures, from Geotabs range data.

The above Geotab data illustrate the basic efficiency versus temperature relationship.

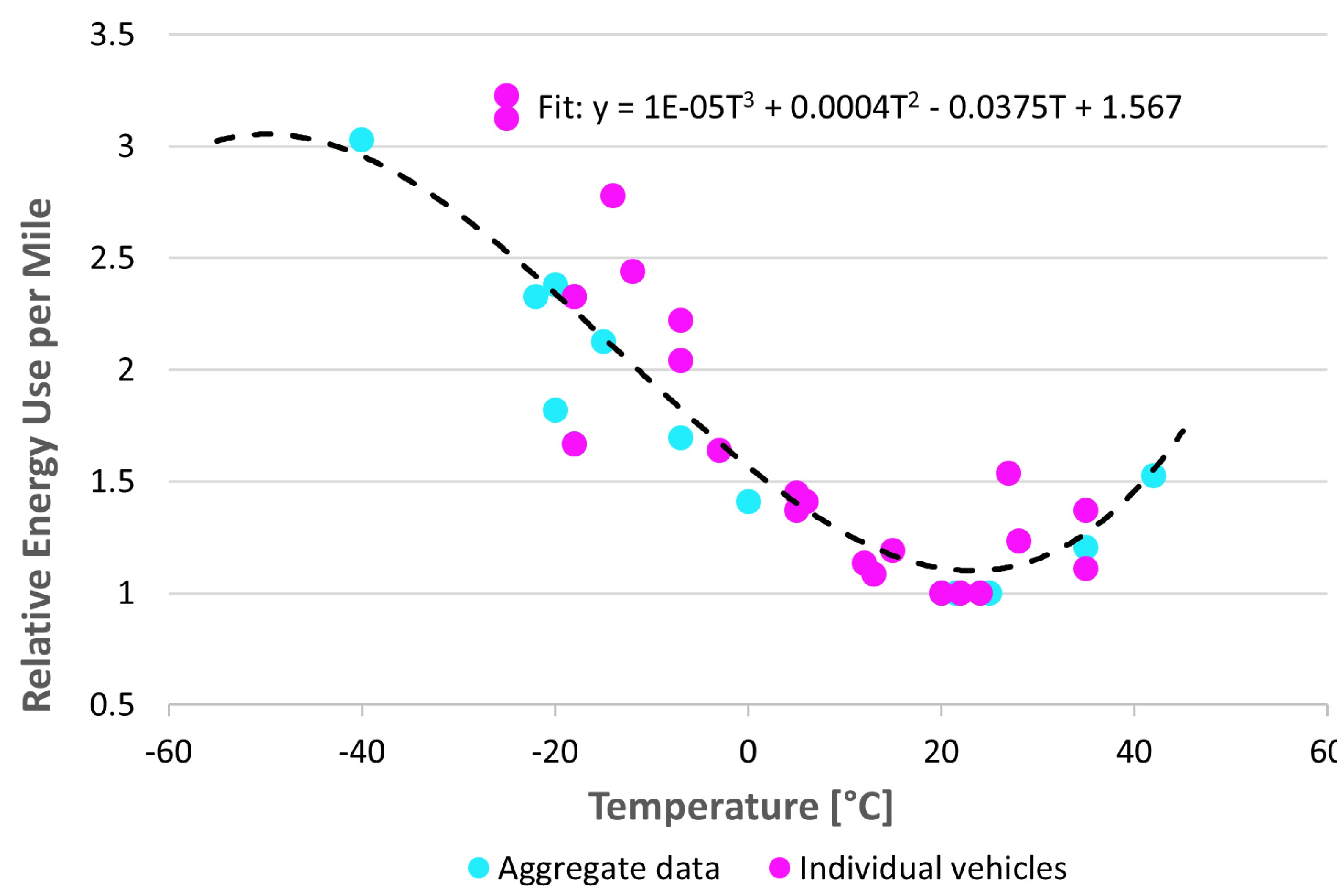

For the load projections for vehicle type “car” and “truck,” aggregated Geotab data was used with 5 other sources on relative range vs temperature [15]. Three data points from Geotab data were generated [37]. The data points derived were range reductions of 29%, 57%, and 34.5% at temperatures 0°C, -22°C and +42°C respectively. Range reductions were converted to relative kWh per mile and fitted with a cubic polynomial to the data. The resulting equation is:

where:

relative kWh/mile = 1.00 at temp yielding maximum range

T is temperature in degrees C

Figure A2 shows the relative energy use per mile and temperature relationship. The blue dots represent aggregated data and therefore have less noise. The pink dots are from individual vehicles.

Figure A2.

Fitted relative EV energy use per mile vs. temperature for light duty vehicles (car and truck). Blue dots are aggregated from multiple vehicles; pink dots are from individual vehicles.

Figure A2.

Fitted relative EV energy use per mile vs. temperature for light duty vehicles (car and truck). Blue dots are aggregated from multiple vehicles; pink dots are from individual vehicles.

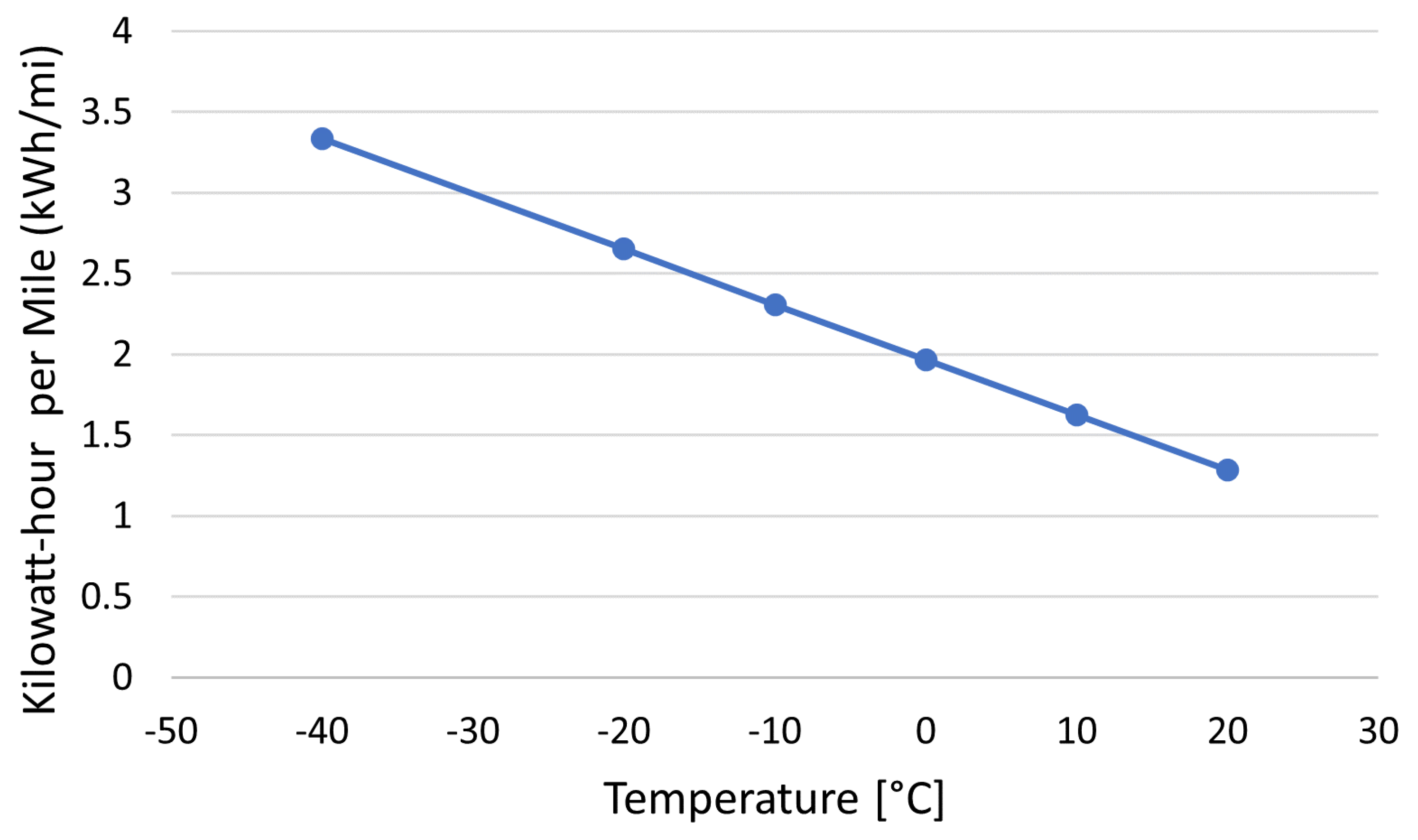

For the vehicle type “boxtruck,” which was equated to the DMV’s “commercial truck” category, the fitted equation is for absolute kWh per mile and is based on data from the Municipality of Anchorage electric box truck, a Peterbilt 220. The fitted equation is written below and shown in Figure A3.

Figure A3.

Fitted kWh per mile vs temperature for type “boxtruck”.

For vehicle type “bus”, the fitted equation is from data for the an electric school bus operated in Tok, Alaska:

Figure A4.

Fitted kWh per mile vs temperature for vehicle type “bus”.

Appendix A.3. Step 3. Driving profiles

Simplified driving profiles were assumed as follows:

- Car and Truck: 30 miles per day; 15 miles at 8:30 am and 15 miles at 5:30 pm

- Boxtruck and Bus: 60 miles per day; 30 miles at 8:30 am and 30 miles at 3:30 pm

Appendix A.4. Step 4. Energy use while parked

For all vehicle types, garages were not assumed and the parked energy equation, based on limited Alaska data, is:

To give a sense of magnitudes, this equation yields 1,351 kWh per year for parked energy use with Anchorage weather. Electric vehicles may use energy while parked for various purposes including accessories and communication, but the available Alaska data show a strong temperature effect, indicating that an important and primary use is in keeping the battery at an optimal temperature for performance and health.

Appendix A.5. Step 5. Daily loads by load area

With the above building blocks in place, the kWh per hour used by each vehicle type for each hour of the year was tabulated using the hourly temperature data for Anchorage, Wasilla, Delta Junction, Fairbanks, and Kenai. These numbers are from the energy discharged from the batteries and used by the vehicle. The hourly vehicle usage was aggregated to daily energy requirements that need to be met by charging. Table A3 shows the estimated daily kWh of each vehicle type for the five cities. An intermediate output of interest is the kWh per day used by each vehicle type.

Table A3.

Estimated kWh per day for each vehicle type, averaged over quarters of the year.

| Jan-Mar | Apr-Jun | Jul-Sept | Oct-Nov | ||

|---|---|---|---|---|---|

| Anchorage | A_car | 18.3 | 10.6 | 8.8 | 17.0 |

| A_truck | 29.8 | 18.6 | 16.2 | 27.9 | |

| A_boxtruck | 136.4 | 99.3 | 89.8 | 130.7 | |

| A_bus | 143.9 | 107.0 | 97.5 | 138.2 | |

| Delta Junction | D_car | 21.6 | 10.5 | 9.5 | 20.9 |

| D_truck | 34.7 | 18.6 | 17.1 | 33.7 | |

| D_boxtruck | 150.8 | 95.8 | 91.5 | 148.0 | |

| D_bus | 158.2 | 103.5 | 99.2 | 155.5 | |

| Fairbanks | F_car | 22.5 | 10.6 | 9.3 | 22.0 |

| F_truck | 36.0 | 18.6 | 16.8 | 35.3 | |

| F_boxtruck | 154.1 | 97.1 | 90.1 | 152.5 | |

| F_bus | 161.5 | 104.8 | 97.8 | 159.9 | |

| Kenai | K_car | 14.3 | 12.7 | 10.4 | 13.3 |

| K_truck | 26.1 | 19.5 | 17.1 | 27.4 | |

| K_boxtruck | 125.3 | 102.2 | 93.1 | 128.7 | |

| K_bus | 132.8 | 109.9 | 100.8 | 136.2 | |

| Wasilla | W_car | 16.8 | 10.5 | 9.4 | 15.5 |

| W_truck | 27.7 | 18.5 | 17.0 | 25.9 | |

| W_boxtruck | 130.0 | 98.7 | 93.4 | 124.6 | |

| W_bus | 137.5 | 106.4 | 101.1 | 132.1 | |

As a reality check, the calculated daily kWh per vehicle for cars was compared to, and found to be within 2 percent of, output from the EVI-Pro Lite tool [38].

To get daily loads by load area, daily kWh per vehicle was aggregated across vehicle types using the numbers of each type in each region.

Appendix A.6. Step 6. Hourly loads by load area

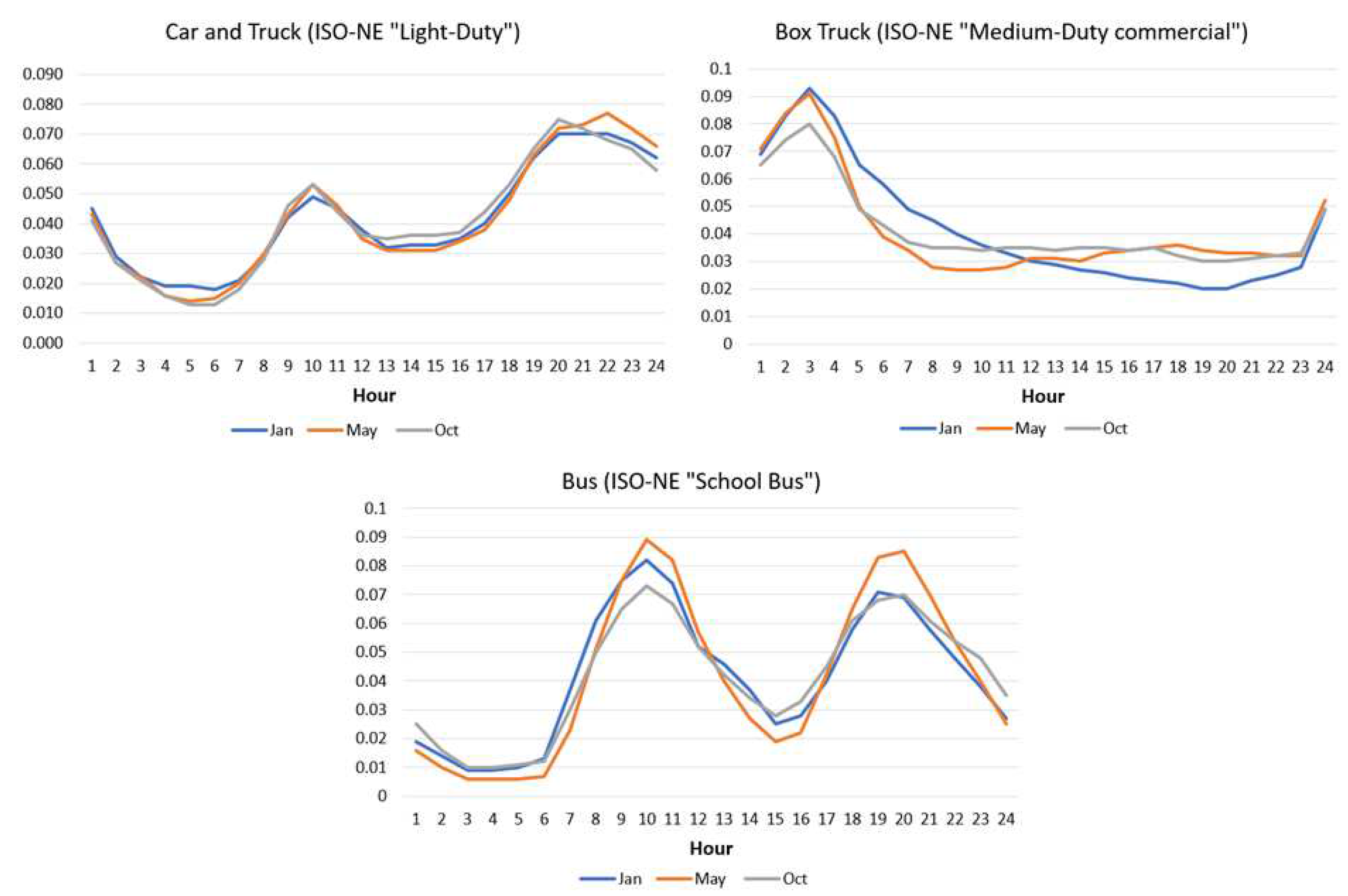

The final step is to apply load shapes to each daily load to determine hourly loads to be served by the Railbelt Grid. Load shapes reported and adopted by the New England Independent System Operator (ISO-NE) were used [39] .These load shapes were developed by ISO-NE planners from actual charging data collected for hundreds of vehicles by Chargepoint. These shapes are for the ISO-NE demand forecast, so they reflect reasonably expected diversity among vehicles. They are not load shapes for a particular vehicle, but for the class as a whole.

The hourly load shapes were derived from published data plots for January, May, and October and for the ISO-NE vehicle types “light-duty”, “medium-duty commercial,” and “school bus.” The load shapes are shown in Figure A5.

Figure A5.

Assumed load shapes that distribute daily energy requirements to hourly loads. The area under each curve equals 1.00.

Figure A5.

Assumed load shapes that distribute daily energy requirements to hourly loads. The area under each curve equals 1.00.

The load shapes were applied as follows:

- January load shape applies to Alaska months Nov-Mar (winter).

- May load shape applies to Alaska months Jun-Aug (summer).

- October load shape applies to Alaska months Apr, May, Sep, Oct (spring, fall).

The load shapes from New England data are only patterns to allocate the Alaska daily load data among the 24 hours in the day. There is no downward bias to the Alaska load projections due to using load shape data from a warmer climate.

yes

References

- Mai, T.T.; Jadun, P.; Logan, J.S.; McMillan, C.A.; Muratori, M.; Steinberg, D.C.; Vimmerstedt, L.J.; Haley, B.; Jones, R.; Nelson, B. Electrification Futures Study: Scenarios of Electric Technology Adoption and Power Consumption for the United States; Technical Report NREL/TP–6A20-71500, 1459351. 2018. [Google Scholar] [CrossRef]

- Waite, M.; Modi, V. Electricity Load Implications of Space Heating Decarbonization Pathways. Joule 2020, 4, 376–394. [Google Scholar] [CrossRef]

- Pike, C.; Whitney, E. Heat pump technology: An Alaska case study. J. Renew. Sustain. Energy 2017, 9, 061706. [Google Scholar] [CrossRef]

- Mathur, S.; Colt, S.; Wilber, M. Kake Heat Pump Rate Analysis for Inside Passage Electric Cooperative, Alaska. 2021. Available online: https://www.uaf.edu/acep/files/projects/Kake_HeatPumpRate_Analysis.pdf.

- Alaska Energy Authority. State of Alaska Electric Vehicle Infrastructure Implementation Plan. 2022. Available online: https://www.akenergyauthority.org/Portals/0/Electric%20Vehicles/2022.07.29%20State%20of%20Alaska%20NEVI%20Plan%20.

- Wilber, M.; Whitney, E.; Leach, T.; Haupert, C. Cold Weather Issues for Electric Vehicles (EVs) in Alaska. 2021. Available online: https://www.uaf.edu/acep/files/projects/Cold-Weather-Issues-for-EVs-in-Alaska.pdf.

- Rojo, V. ISO New England Draft 2023 Transportation Electrification Adoption Forecast. 2022. Available online: https://www.iso-ne.com/static-assets/documents/2022/12/transfx2023_adopt.pdf.

- Wilber, M.; Whitney, E.; Pike, C.; Johnston, J. Catching the Midnight Sun: Performance and Cost of Solar Photovoltaic Technology in Alaska. In Proceedings of the 2019 IEEE 46th Photovoltaic Specialists Conference (PVSC); 2019; pp. 1656–1662. [Google Scholar] [CrossRef]

- Howell, D.; Sandberg, E. Alaska Population Projections, 2021 to 2050; Technical Report; Alaska Department of Labor and Workforce Development: Juneau, AK, USA, 2022. [Google Scholar]

- United States Census Bureau. S2504 | Physical Housing Characteristics for Occupied Housing Units. 2022. Available online: https://data.census.gov/table?q=s2504+alaska+healy&tid=ACSST5Y2018.S2504.

- State of Alaska - Division of Motor Vehicles. VEHICLES REGISTERED IN 2022 BY GOVERNMENTAL BOUNDARY, 2023.

- Chugach Electric Association, Inc.. EVs in Alaska. 2022. Available online: https://www.chugachelectric.com/energy-solutions/electric-vehicles.

- Bloomberg New Energy Finance. Electric Vehicle Outlook 2022. Available online: https://about.bnef.com/electric-vehicle-outlook/.

- Larson, E.; Greig, C.; Jenkins, J.; Mayfield, E.; Pascale, A.; Zhang, C.; Drossman, J.; Williams, R.; Pacala, S.; Socolow, R.; et al. Net-Zero America: Potential Pathways, Infrastructure, and Impacts. 2021. Available online: https://netzeroamerica.princeton.edu/img/Princeton%20NZA%20FINAL%20REPORT%20SUMMARY%20.

- Wilber, M.; Whitney, E.; Haupert, C. A Global Daily Solar Photovoltaic Load Coverage Factor Map for Passenger Electric Vehicles. In Proceedings of the 2022 IEEE PES/IAS PowerAfrica; pp. 1–4. [CrossRef]

- Department of Energy, Solar Energy Technologies Office. Solar Investment Tax Credit: What Changed? | Department of Energy. 2023. Available online: https://www.energy.gov/eere/solar/articles/solar-investment-tax-credit-what-changed.

- Pike, C. 2021 Alaska Railbelt Net Metering Update; Technical Report; Alaska Center for Energy and Power: Fairbanks, AK, USA, 2021. [Google Scholar]

- U.S. Energy Information Administration. Total Energy Supply, Disposition, and Price Summary. 2023. Available online: https://www.eia.gov/outlooks/aeo/data/browser/#/?id=1-AEO2023®ion=0-0&cases=ref2023&start=2021&end=2050&f=A&linechart=~~~ref2023-d020623a.58-1-AEO2023~~~~~~~~~~&map=&ctype=linechart&sourcekey=0.

- National Renewable Energy Laboratory. Annual Technology Baseline: Residential PV. Available online: https://public.tableau.com/views/2022CostComponents/CostComponents?:embed=y&:toolbar=no&Technology=ResPV&:embed=y&:showVizHome=n&:bootstrapWhenNotified=y&:apiID=handler2.

- ISO New England. 2022 CELT Report, 2022-2031 Forecast Report of Capacity, Energy, Loads, and Transmission. Available online: https://www.iso-ne.com/system-planning/system-plans-studies/celt/?document-type=CELT%20Reports.

- Hawaiian Electric. Quarterly Installed Solar Data. Available online: http://www.hawaiianelectric.com/clean-energy-hawaii/our-clean-energy-portfolio/quarterly-installed-solar-data.

- ISO New England. Monthly Peak Load and Energy Data. 2023. Available online: https://www.iso-ne.com/isoexpress/web/reports/load-and-demand/-/tree/net-ener-peak-load.

- Hawai‘i Electric Light Company, Inc. 2021 Adequacy of Supply Report Summary. 2021. Available online: https://puc.hawaii.gov/wp-content/uploads/2021/02/GEN-RPT.HELCO_.ADEQUACY-OF-SUPPLY-2021.pdf.

- Hawaiian Electric Company, Inc.. 2021 Adequacy of Supply Report Summary. 2021. Available online: https://puc.hawaii.gov/wp-content/uploads/2021/02/GEN-RPT.HECO_.ADEQUACY-OF-SUPPLY-2021.pdf.

- Maui Electric Company, Limited. 2021 Adequacy of Supply Report Summary. 2021. Available online: https://puc.hawaii.gov/wp-content/uploads/2021/02/GEN-RPT.MECO_.ADEQUACY-OF-SUPPLY-2021.pdf.

- Henspeter, M. 2022 Heat Pump Feasibility Study Analysis and Pilot Program Recommendation. 2022. Available online: https://www.chugachelectric.com/sites/default/files/meetings/document_packets/10%2019%2022% 20Operations%20Committee%20Meeting%20Packet%20-%20POST_0.pdf.

- Energy Information Administration. Table WF01. Average Consumer Prices and Expenditures for Heating Fuels During the Winter. 2023. Available online: https://www.eia.gov/outlooks/steo/pdf/wf01.pdf.

- Highlights for space heating fuel in, U.S. homes by state, 2020. 2023. Available online: https://www.eia.gov/consumption/residential/data/2020/state/pdf/State.

- Register, F. Air Plan Partial Approval and Partial Disapproval; AK, Fairbanks North Star Borough; 2006 24-Hour PM2.5. 2023. Available online: https://www.federalregister.gov/documents/2023/01/10/2022-28666/air-plan-partial-approval-and-partial-disapproval-ak-fairbanks-north-star-borough-2006-24-hour-pm25.

- DeMarban, A. Hilcorp warns Alaska utilities about uncertain Cook Inlet natural gas supplies. 2022. Available online: https://www.adn.com/business-economy/energy/2022/05/17/hilcorp-warns-alaska-utilities-about-uncertain-cook-inlet-natural-gas-supplies/.

- Denholm, P.; Schwarz, M.; DeGeorge, E.; Stout, S.; Wiltse, N. Renewable Porftolio Standard Assessment for Alaska’s Railbelt. Technical report, National Renewable Energy Lab. (NREL), Golden, CO (United States).

- National Renewable Energy Laboratory. System Advisor Model. Available online: https://sam.nrel.gov/.

- PVWatts Calculator. Available online: https://pvwatts.nrel.gov/.

- Mitchell, Alan. Alaska Mini-Split Heat Pump Calculator. 2022. Available online: https://heatpump.cf/.

- Cicilio, P.; Francisco, A.; Wilber, M.; Colt, S. Railbelt 2050 Load, Electrification, and Behind- the-Meter Solar Hourly Load Demand for Aggressive and Moderate Electrification Forecasts. 2023. [CrossRef]

- The Car Connection. 2022 Ford F-150 Lightning Review, Ratings, Specs, Prices, and Photos. Available online: https://www.thecarconnection.com/overview/ford_f-150-lightning_2022.

- Geotab. Temperature Tool for EV Range. 2023. Available online: https://www.geotab.com/fleet-management-solutions/ev-temperature-tool/.

- U.S. Deparment of Energy, E.E.R.E. U.S. Deparment of Energy, E.E.R.E. Electric Vehicle Infrastructure Projection Tool (EVI-Pro) Lite. Available online: https://afdc.energy.gov/evi-pro-lite.

- ISO New England. 2022 Final Transportation Electrification Forecast. 2022. Available online: https://www.iso-ne.com/static-assets/documents/2022/04/final_2022_transp_elec_forecast.pdf.

Figure 1.

Alaska Railbelt transmission, load regions, and electric utility territories.

Figure 2.

Alaska population forecast [9].

Figure 2.

Alaska population forecast [9].

Figure 3.

Alaska Energy Authority electric vehicle forecast for the Railbelt, and historical numbers electric vehicles on the Railbelt.

Figure 3.

Alaska Energy Authority electric vehicle forecast for the Railbelt, and historical numbers electric vehicles on the Railbelt.

Figure 4.

Railbelt electric vehicle adoption forecasts extended through 2050, with aggressive and moderate forecast amounts in 2050.

Figure 4.

Railbelt electric vehicle adoption forecasts extended through 2050, with aggressive and moderate forecast amounts in 2050.

Figure 5.

Railbelt electric vehicle adoption forecasts by percent of vehicles with comparisons to other regional, national, and global EV adoption forecasts.

Figure 5.

Railbelt electric vehicle adoption forecasts by percent of vehicles with comparisons to other regional, national, and global EV adoption forecasts.

Figure 6.

Historical behind-the-meter Railbelt solar installations [17].

Figure 6.

Historical behind-the-meter Railbelt solar installations [17].

Figure 9.

Railbelt forecasted behind-the-meter solar installations from 2023 through 2050 for the moderate and aggressive adoption scenarios.

Figure 9.

Railbelt forecasted behind-the-meter solar installations from 2023 through 2050 for the moderate and aggressive adoption scenarios.

Figure 10.

CEA heat pump adoption forecasts extrapolated to 2050 and expanded to represent all of the Railbelt.

Figure 10.

CEA heat pump adoption forecasts extrapolated to 2050 and expanded to represent all of the Railbelt.

Figure 11.

Normalized heat pump forecasts for ISO-NE and from CEA extrapolated to the Railbelt.

Figure 12.

The hourly EV load for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 12.

The hourly EV load for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 13.

The hourly EV load for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 13.

The hourly EV load for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 14.

The hourly BTM Solar generation for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 14.

The hourly BTM Solar generation for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 15.

The hourly BTM solar generation for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 15.

The hourly BTM solar generation for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 16.

The hourly load demand from heat pumps for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 16.

The hourly load demand from heat pumps for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 17.

The hourly load demand from heat pumps for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 17.

The hourly load demand from heat pumps for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 18.

The total hourly load demand for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 18.

The total hourly load demand for the moderate forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 19.

The total hourly load demand for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Figure 19.

The total hourly load demand for the aggressive forecast for the year 2050, January 1st 2050, and June 1st 2050.

Table 1.

Building Counts for the Railbelt. *estimate based on census.

| Area | Electric Utility | Load Region | Residential | Commercial | Total |

|---|---|---|---|---|---|

| Fairbanks North Star Borough | GVEA | Northern | 29,100 | 14,992 | 44,092 |

| Healy* | GVEA | Northern | 377 | 25 | 402 |

| Cantwell* | GVEA | Northern | 93 | 6 | 99 |

| Denali Park* | GVEA | Northern | 44 | 23 | 67 |

| Anderson | GVEA | Northern | 50 | 3 | 53 |

| City of Nenana* | GVEA | Northern | 159 | 10 | 169 |

| City of Delta Junction* | GVEA | Northern | 320 | 21 | 341 |

| Matanuska-Susitna Borough | MEA | Central | 51,145 | 3,375 | 54,520 |

| Municipality of Anchorage | CEA | Central | 87,618 | 10,964 | 98,582 |

| Kenai Peninsula Borough | HEA | Southern | 43,937 | 4,550 | 48,487 |

Table 2.

Vehicle Counts for the Railbelt.

| Area | Electric Utility | Load Region | Car | Truck | Box Truck | Bus | Total |

|---|---|---|---|---|---|---|---|

| Fairbanks North Star Borough | GVEA | Northern | 54,009 | 27,107 | 7,393 | 385 | 88,894 |

| City of Nenana | GVEA | Northern | 343 | 231 | 43 | 2 | 619 |

| City of Delta Junction | GVEA | Northern | 2,632 | 1,728 | 332 | 29 | 4,721 |

| Matanuska-Susitna Borough | MEA | Central | 47,483 | 24,556 | 4,048 | 513 | 76,600 |

| Municipality of Anchorage | CEA | Central | 186,739 | 64,251 | 16,620 | 871 | 268,481 |

| Kenai Peninsula Borough | HEA | Southern | 33,432 | 21,998 | 3,895 | 223 | 59,548 |

Table 3.

Load Characteristics for 2021 and the aggressive and moderate 2050 load forecasts

| Characteristic | 2021 | 2050 Moderate | 2050 Aggressive |

|---|---|---|---|

| Total Annual Energy [TWh] | 4.72 | 8.48 | 10.2 |

| Heat Pump Energy [TWh] | - | 0.1 | 2 |

| Electric Vehicle Energy [TWh] | - | 3.1 | 4 |

| Residential Solar Energy [TWh] | - | 0.2 | 1 |

| Peak Load Demand [MW] | 765.3 | 1,626 | 2,403 |

| Low Load Demand [MW] | 381.1 | 580 | 144 |

| Maximum Hourly Change [MW] | 55.5 | 202 | 270 |

| Number of Installed Heat Pumps | - | 11,178 | 262,832 |

| Number of Electric Vehicles | - | 353,381 | 448,977 |

| BTM Solar Installed Capacity [MW] | 11 | 267 | 1,314 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.