Submitted:

03 July 2023

Posted:

04 July 2023

You are already at the latest version

Abstract

Criticism has been directed towards the traditional methods of management accounting employed by organizations thus far, as they fail to adequately address the growing need for competitiveness and sustainable development in a globalized environment. This criticism stems from both economic factors, such as insufficient monitoring of material, energy, and escalating overhead costs, and environmental concerns, where inadequate attention is given to vital information regarding significant environmental aspects, impacts, risks, and damages arising from the organization's activities and processes. Additionally, these methods do not sufficiently support the implementation of a functional environmental management system (EMS). Drawing upon our research in EMS standardization following the international standards ISO 1400X, as well as our knowledge gained during the development of the Slovak Technical Standard (STN) for ISO 14051, this paper presents an innovative model of environmental management accounting. This model is based on the cost accounting of material and energy flows within organizations. It serves as an enhancement framework for organizations with an existing EMS built according to the EN ISO 14001 model, as well as for organizations lacking a formalized EMS based on this standard. Within this paper, we specify, decompose, and apply the new model, focusing on the cost accounting of material-energy flows in a hypothetical organization. We meticulously examine the ten key steps of the model's structure, particularly in terms of costing and the allocation of costs to material, energy, system, and waste management.

Keywords:

organization

; material-energy flows

; economics & environment

; cost accounting

; quantity node

; standardization

1. Introduction

Management accounting plays a critical role in organizations by applying financial management accounting principles to create, preserve, and enhance enterprise value for stakeholders [1]. It serves as an essential component of management, providing valuable information for business strategy, decision-making, resource allocation, performance improvement, and overall organizational sustainability [2].

Emerging trends in management accounting are driven by the need to adapt to dynamic business environments and meet global challenges. These trends focus on various aspects, including improving product quality, reducing corporate costs, increasing productivity, and integrating environmental considerations into production processes [3,4]. Organizations are increasingly recognizing the importance of environmental sustainability and the role of management accounting in addressing environmental issues [5–7].

In today's business landscape, the integration of environmental and energy management systems has become crucial for effective environmental management accounting (EMA) [8]. Environmental and energy management systems provide organizations with frameworks and tools to manage and account for environmental aspects and impacts [9,10]. They enable a proactive approach to environmental performance and facilitate the optimization of environmental costs [11,12]. Standardized cost accounting of material and energy flows in organizations represents a powerful tool for aligning economic and environmental objectives, fostering a green economy, and promoting efficiency, environmental performance, and sustainable production [7,13,14]. It enables organizations to identify, measure, and manage the environmental costs associated with their operations.

2. Literature Review

The growing awareness and concern surrounding environmental and energy issues, combined with the increasingly complex global business environment, have compelled companies to address environmental and energy management challenges. Researchers such as Lopéz-Gamero et al. [15], Galdeano Gomez et al. [16], and Henri et al. [17] emphasize the strategic importance of accounting for environmental and energy costs within enterprises.

Environmental Management Accounting (EMA) practices offer businesses a means to promote sustainable growth by facilitating cost reduction, cleaner production methods, competitive advantage [18,19], improved pricing strategies, and increased shareholder value. As highlighted by Burritt & Schaltegger [8], EMA serves as a crucial decision-making tool for managing environmental costs.

However, traditional approaches often overlook the full financial implications of waste, which is a significant yet hidden burden for businesses, as noted by Jasch [20]. By solely considering waste disposal costs and neglecting the underlying expenses related to raw materials, labour, and energy, the true cost of waste is not fully captured.

To align economic and environmental objectives, it is imperative to enhance efficiency in material and energy usage. The adoption of material flow accounting has proven effective in reducing environmental impacts and improving productivity, as exemplified by Hinz, Wagner & Enzler [21]; Kokubu-Kitada [22]; and Majernik [23].

Despite the increasing recognition of the importance of environmental and energy management in business, there is a literature gap regarding the specific application and effectiveness of material flow accounting as a tool for optimizing material and energy flows. While studies have highlighted the benefits of implementing environmental management accounting practices, there is a lack of comprehensive research on how material flow accounting can contribute to achieving economic and environmental objectives simultaneously.

The aim of our research is to bridge this literature gap by investigating the role of material flow accounting in enhancing the efficiency of material and energy utilization within businesses. Specifically, we seek to explore how the implementation of material flow accounting practices can lead to improved environmental performance and cost savings. By examining real-world examples and conducting a thorough analysis, we aim to provide insights into the potential benefits and challenges of adopting material flow accounting as a strategic tool for sustainable resource management. Ultimately, our research aims to contribute to the existing knowledge base on environmental management accounting and provide practical recommendations for businesses striving to achieve both economic and environmental sustainability.

3. Modelling the Processability of Cost Accounting for Material and Energy Flows

Cost accounting of material and energy flows in organizations serves as a proactive quantitative management tool, involving several hierarchically ordered implementation steps [24]. The level of detail and complexity of economic-environmental analysis depends on factors such as organization size, nature of activities and products, process structure, selection of quantification nodes, and the presence of an environmental management system (EMS) following ISO 14001 or a less formal or non-existent system.

Cost accounting of material and energy flows can be conducted within an organization with or without a standard EMS. The process becomes easier, faster, and more efficient when integrated into a certified system based on ISO 14001, and even more streamlined within an integrated management system (IMS) encompassing environmental and energy aspects following ISO 50001 [25]. Environmental-energy cost accounting of material flows yields valuable information at different stages of the continuous improvement cycle, benefiting both the environmental profile and economic performance of the organization [8].

This approach enables organizations to incorporate financial considerations and forecasts when setting long and short-term development goals. Understanding the potential environmental aspects, impacts, risks, and financial implications of processes enhances the quality of an organization's environmental profile assessment and provides valuable insights for management decision-making [8,14,22].

4. Modelling Material and Energy Flows and Costing

In the business environment, and particularly for enterprises, there is a growing need for accurate and visual models that depict the various quantity nodes where materials are stored, used, and transformed. Understanding the transfer of materials between different quantity nodes, such as production and recycling units, is crucial.

Costing, in essence, involves the allocation of system costs, energy costs, material costs, and waste management costs to individual material and energy flows within a company. Once all costs associated with a specific quantity node have been identified (through positive and negative product analysis), these costs are further assigned and distributed to the outputs of each quantity node within the production process of a specific product. This allocation is based on the proportion of material inputs and the corresponding material losses.

5. Inputs and Outputs of Business Processes

The overall balance of material and energy flows within an enterprise is founded on the recognition that whatever enters the enterprise must also exit the enterprise at some point. This includes all input materials, energy, information, as well as products and by-products. It is crucial to compare the procured inputs with the total production volume, sales statistics, and waste and emissions records. The objective is to enhance the company's efficiency in utilizing materials and energy, leading to improvements in economic, environmental, and energy aspects.

The cost accounting process is depicted in Figure 2. For instance, out of 100 kg of raw material input, 30 kg is allocated to material losses. Consequently, the total costs are distributed in this ratio, except for waste management costs, which are only allocated to material losses. This is because only the material losses require additional processes and financial resources for waste management.

The modelling and models serve as representations of the overall material flows within the chosen boundaries for cost analysis. The specification of material costs can generally be categorized into two situations:

- Simple manufacturing process: This involves tracing the flow of each material and energy from start to finish, from input to output. In this case, it is possible to track and identify the contribution of each material and energy input in the final products.

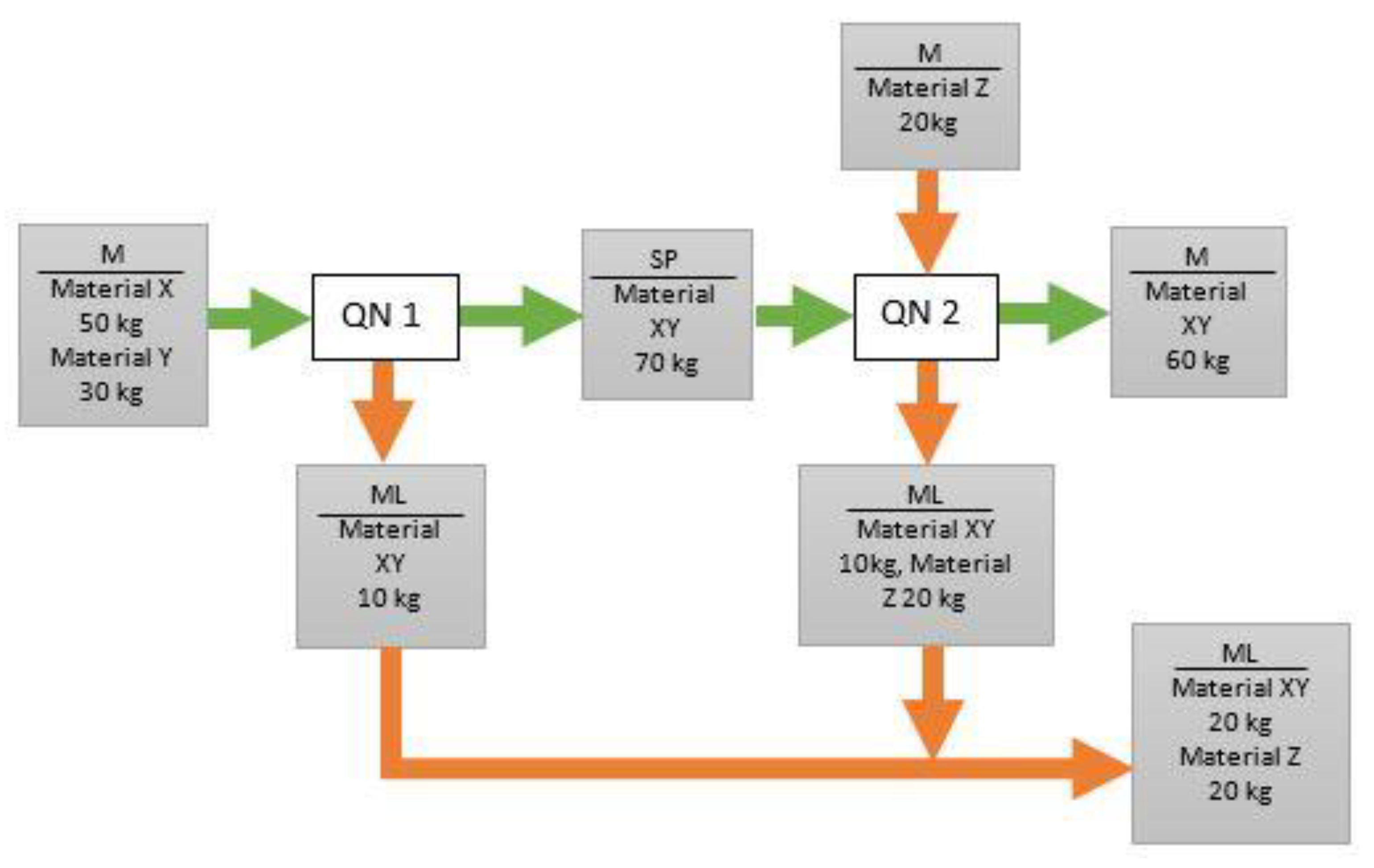

- Complex process: In more complex processes, the initial material and energy inputs are transformed into intermediate inputs, which cannot be individually recognized in the final products. In such cases, the intermediate products are considered as outputs. Please refer to Figure 3 for a visual representation.

In a simple production process, two quantity nodes are defined, each generating a product and a corresponding material loss. However, for more intricate processes, the consideration of intermediate products as outputs becomes necessary to accurately capture the material flows.

The precise composition of semi-finished product flows and material losses is often unknown in complex systems, making it challenging to calculate the exact unit material cost for these material-energy flows.

Table 2 presents the material costs associated with the model depicted in Figure 3. Please note that for the sake of simplicity, the table does not encompass all costs within the quantity nodes. The total unit material cost has been estimated by considering the cost of the initial material inputs at 77.5 EUR/kg.

Energy, system, and waste management costs, along with their allocation to products and material losses, are ideally determined directly from the available production cost data for each quantity node. If direct determination is not possible, these costs should be estimated using other available data, such as the organization's standardized energy management indicators.

There are four methods that can be employed:

- 1.

- Allocating energy, system, and waste management costs between quantity nodes:

- 2.

- More aggregated data for the entire process or technical installation can be utilized to quantify the costs of quantity nodes (QNs) in two sequential steps. First, these costs are calculated for the entire process within the cost accounting boundaries. Subsequently, they are allocated to individual quantity nodes based on an appropriate criterion, such as machine time, production volume, number of employees, hours worked, production area, etc. Table 3 provides an example of such a breakdown for a specified period.

- 3.

- Allocating energy, system, and waste management costs to products and material losses in each quantity node:

- 4.

- In this approach, all waste management costs are attributed to material losses. Table 4 illustrates such an allocation for a specific period using the percentage distribution of material in QN1 and QN2 as the criterion. For example, in QN1, 87.5% of the material is allocated to products (70 kg/80 kg), while 12.5% is allocated to material losses (10 kg/80 kg). Similarly, in QN2, 66.67 % is allocated to products (60 kg/90 kg), and 33.33% is allocated to material losses (30 kg/90 kg) [23].

- 5.

- Alternative to percentage distribution of material:

- 6.

- Instead of using a percentage distribution of material based on weight, an alternative approach can be employed. This alternative approach utilizes the weight distribution of all materials in each quantity node as the allocation criterion. If this is not feasible, the percentage distribution of the main material directly related to the process is used as the criterion.

- 7.

- An alternative approach to the allocation criteria for energy consumption:

- 8.

-

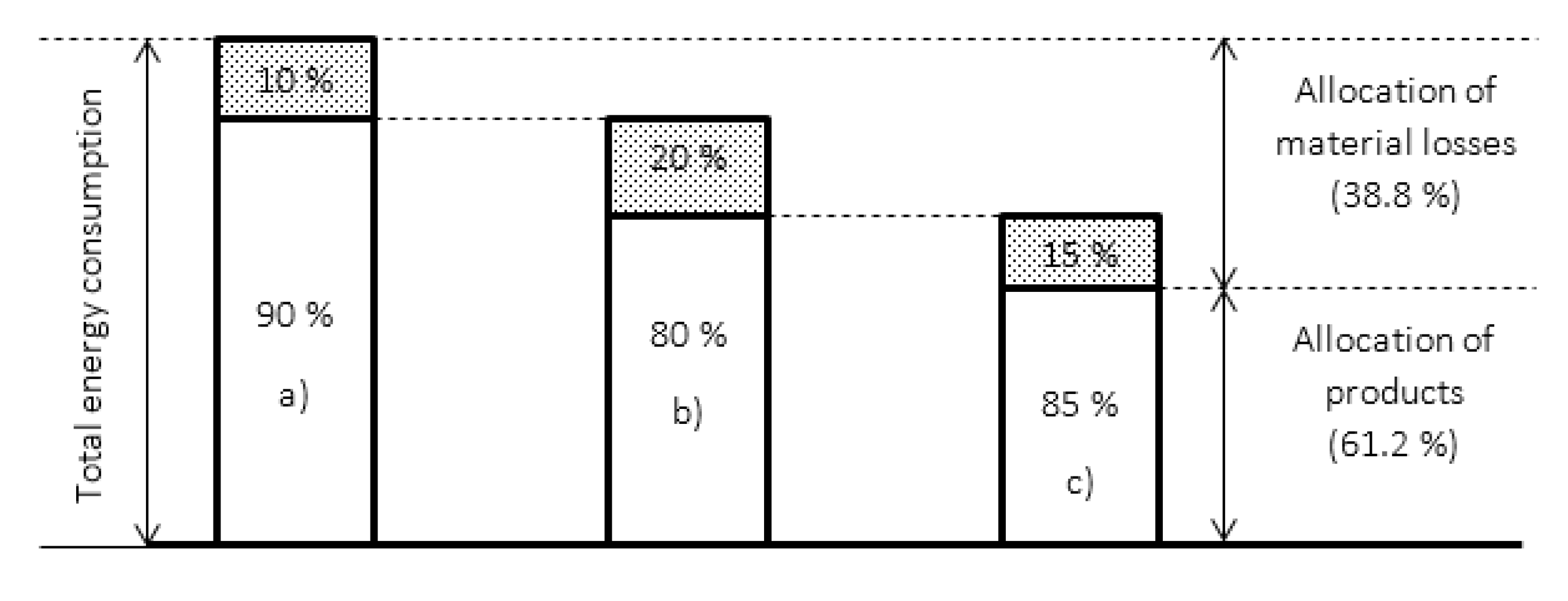

The common criterion for allocating energy consumption between products and material losses is the mass distribution of material inputs. However, if more detailed information on the energy efficiency of machines in the quantity nodes is available, a more accurate quantification of inefficiency and energy waste can be implemented (Figure 4). For example:

- (a)

- If 10% of a machine's operation represents idle running, this portion of energy is allocated to material losses rather than products.

- (b)

- A material inefficiency of 20% results in allocating 80% of the remaining energy consumption to products.

- (c)

- A 15% reduction inefficiency from the optimal state leads to allocating only 85% of the increased energy consumption to products.

When employing the alternative approach, the energy consumption in quantity nodes is divided as follows:

- Energy allocated to products: 90%, 80%, 85%, 61.2%

- Energy allocated to material losses: 100% - 61.2% = 38.8%

The higher percentage of energy allocated to material losses in the alternative approach indicates inefficiency and highlights opportunities for improvement.

Table 3.

Breakdown of energy, system and waste management costs (EUR).

| Cost Types | QN1 | QN2 | Total |

|---|---|---|---|

| Energy costs | 400 | 300 | 700 |

| System costs | 800 | 1200 | 2000 |

| Waste management costs | 300 | 400 | 700 |

Table 4.

Distribution of energy, system and waste management costs per products and material losses in QN1 and QN2 (EUR).

Table 4.

Distribution of energy, system and waste management costs per products and material losses in QN1 and QN2 (EUR).

| Cost Types | QN1 | QN2 |

|---|---|---|

| Energy costs | 400 | 300 |

| Products | 350 | 200 |

| Material losses | 50 | 100 |

| System costs | 800 | 1200 |

| Products | 700 | 800 |

| Material losses | 100 | 400 |

| Waste management costs | 300 | 400 |

| Products | 0 | 0 |

| Material losses | 300 | 400 |

Figure 4.

Quantification of energy losses.

6. Integrated Presentation and Analysis of Cost Data

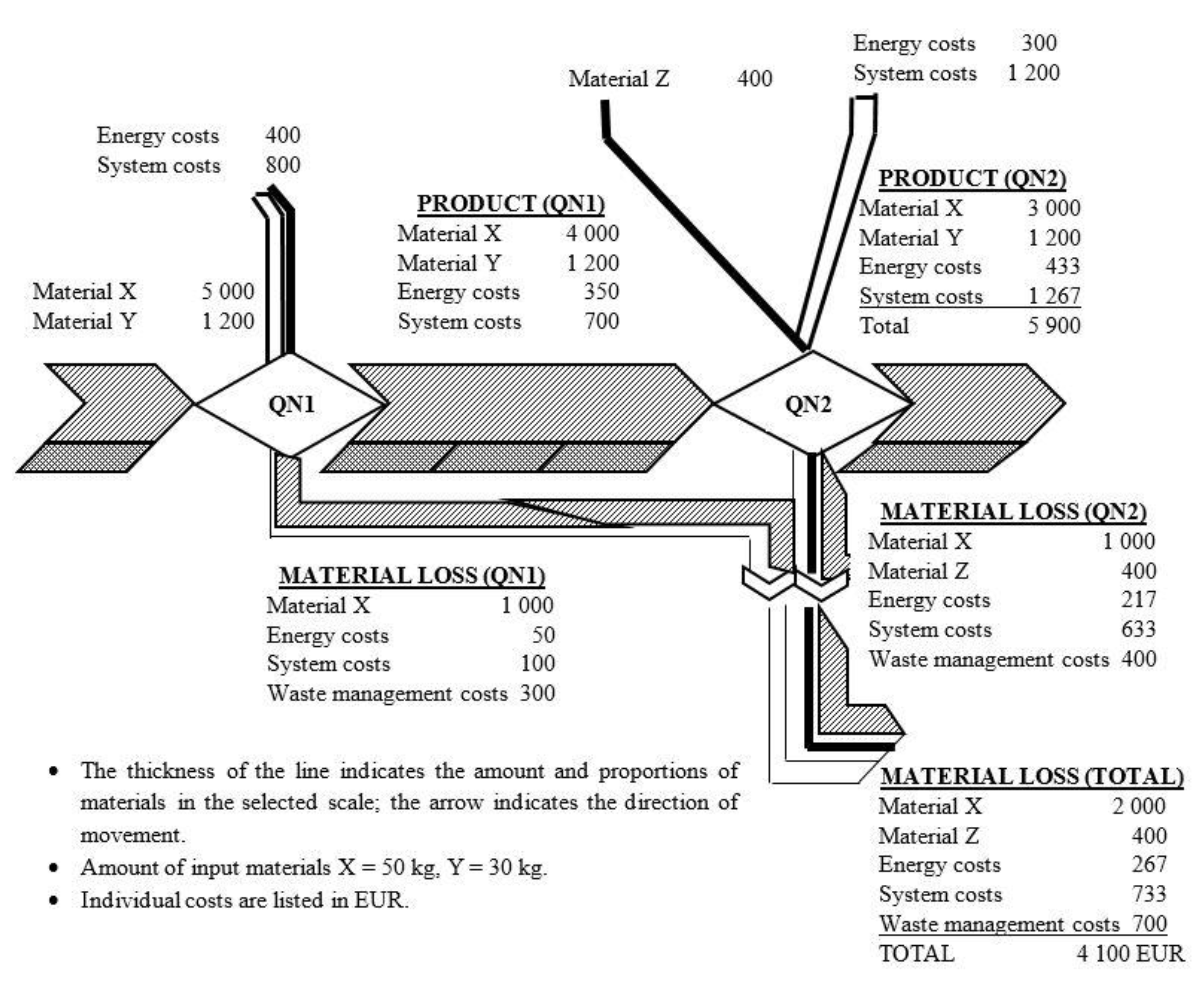

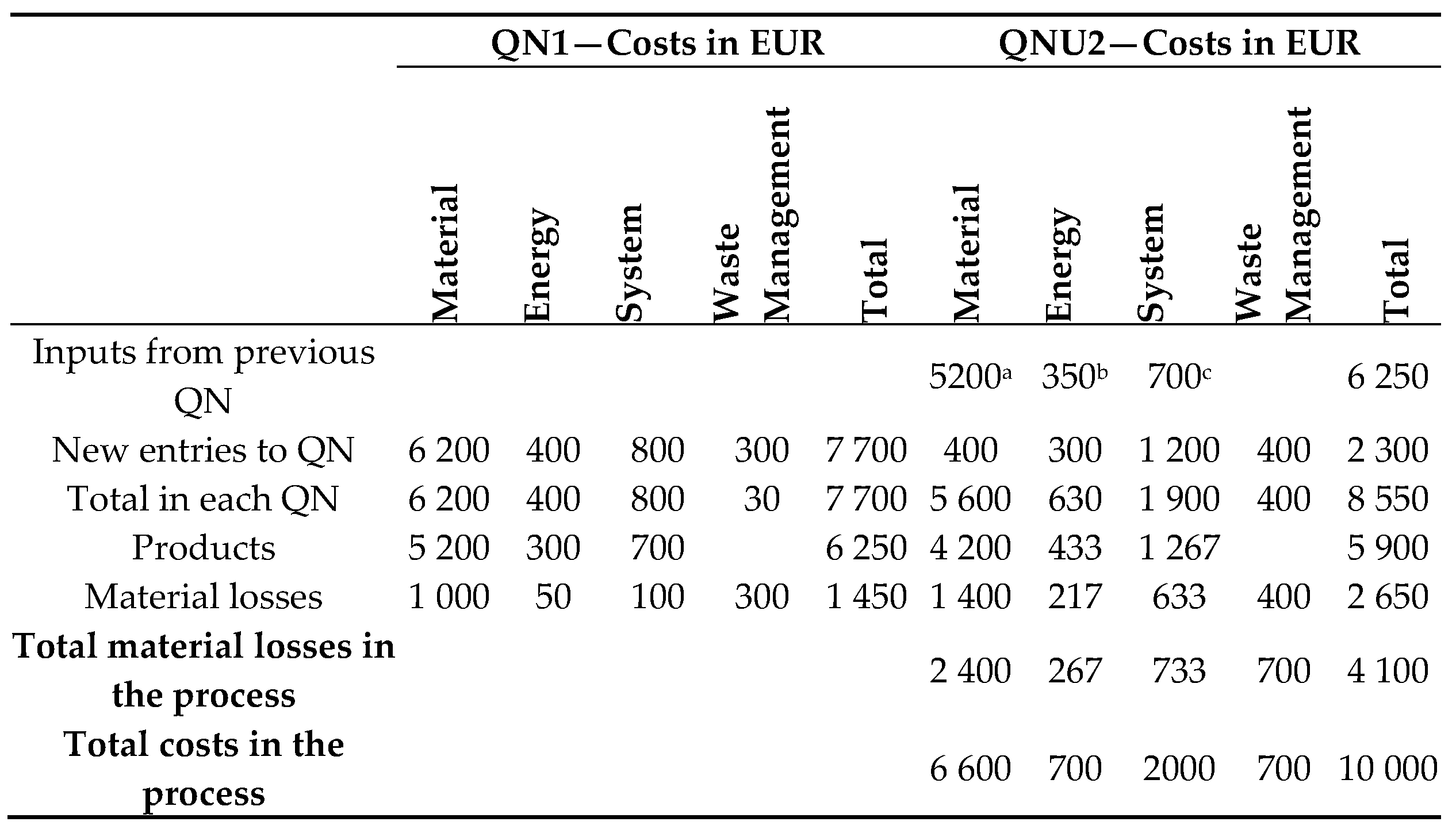

Material, energy, system, and waste management cost data can be summarized in various ways to facilitate further analysis and utilization. In our case study, we have presented a material flow cost matrix in Table 5, which incorporates the data for the two quantity nodes (QNs) examined in Figure 3. Additionally, Figure 5 visually represents this information through a clear and informative Sankey diagram.

Explanatory notes: a, b, c, d - values of costs transferred from QN1 to QN2, The data have been taken from Table 2, Table 3 and Table 4.

The energy costs in QN2 were determined to be 433 EUR for products and 217 EUR for material losses, based on the percentage material distribution in QN2 (66.67 % for products and 33.33 % for material losses). The total energy cost amounts to 650 EUR, which comprises the energy cost of products in QN1 (350 EUR) and the new input in QN2 (300 EUR).

Similarly, the system cost in QN2 was calculated as 1 270 EUR for products and 633 EUR for material losses, using the percentage material distribution in QN2 (66.67 % for products and 33.33 % for material losses). The overall system cost totals 1 900 EUR, consisting of the system cost for products in QN1 (700 EUR) and the new input in QN2 (1 200 EUR).

7. Implications and Benefits of Adopting Material-Energy Flows Accounting

By combining the principles of environmental management systems and rigorous accounting methodologies, companies can achieve significant improvements in both economic efficiency and environmental performance, including:

- Cost Reduction: The implementation of a functional environmental management system and the adoption of cost accounting practices for material-energy flows can yield significant cost reductions for companies. By meticulously tracking and analyzing material and energy costs, organizations can identify areas of inefficiency and waste, leading to the implementation of cost-saving measures, resource optimization, and reduction of material and energy losses. This proactive approach enables companies to achieve improved profitability by minimizing production costs.

- Environmental Performance: The establishment of an environmental management system and the integration of cost accounting practices focused on material-energy flows empower companies to assess and address their environmental impacts. Through quantification and analysis of these impacts, organizations can develop effective strategies to mitigate their carbon footprint, minimize waste generation, and enhance overall environmental performance. This comprehensive approach ensures that companies prioritize sustainability objectives and contribute to the preservation of the environment.

- Regulatory Compliance: Stringent environmental regulations and requirements are imposed by regulatory bodies on businesses across various industries. By implementing an environmental management system aligned with ISO standards and employing accurate cost accounting practices for material-energy flows, companies can ensure compliance with these regulations. The ability to precisely track and report environmental performance facilitates audits and regulatory inspections, enabling companies to demonstrate their adherence to regulatory guidelines effectively.

- Sustainable Supply Chain: Extending the material-energy flow cost accounting system to encompass the supply chain enables collaborative efforts between companies, suppliers, and customers to optimize resource utilization and improve environmental performance. This integrated approach fosters sustainable practices throughout the entire value chain, promoting the achievement of sustainability objectives and enhancing the reputation of all stakeholders involved.

- Decision-Making and Goal Setting: The availability of reliable and accurate data on material-energy flows empowers informed decision-making and goal setting within organizations. By leveraging this data, companies can identify areas for improvement, establish realistic targets for reducing material and energy consumption, and effectively track progress towards sustainability goals. This data-driven approach facilitates strategic decision-making that aligns economic and environmental objectives, enabling companies to make informed choices that balance financial viability with environmental responsibility.

8. Conclusions

The global consumption of materials and energy has been steadily increasing in recent years, despite the implementation of various regulatory measures at both global and regional levels. In the manufacturing industry, for instance, material and energy costs account for approximately 50% of a company's total expenses. Reducing their consumption can lead to tangible economic and environmental benefits, such as savings in material, energy, and waste management expenses.

The key solution to address the challenges faced by companies lies in implementing a functional environmental management system that is built and certified according to the international standards of the ISO 1400 family. Our research in this field highlights that cost accounting of material-energy flows, as a management tool, enables a comprehensive improvement of both the economic efficiency and environmental performance of the product system. This approach allows for the examination and enhancement of the transformation process from inputs to desired outputs.

By employing more precise cost accounting models for material-energy flows, the data becomes readily demonstrable, accessible, and useful in the continuous pursuit of optimization opportunities. It also aids in setting realistic economic and environmental development goals for the enterprise. A material-energy flow cost accounting system, adhering to ISO standards, can be implemented in various types of enterprises, economies, and industries, with the potential for extension to the entire supply-customer chain.

Author Contributions

Conceptualization, M.M. and J.C.; methodology, M.M.; validation, J.C., P.M., L.P.; formal analysis, J.C.; investigation, P.M., L.P.; resources, P.M.; data curation, J.C.; writing—original draft preparation, M.M.; writing—review and editing, J.C.; visualization, P.M..; supervision, M.M.; project administration, M.M.; funding acquisition, M.M. All authors have read and agreed to the published version of the manuscript.”.

Funding

This work was supported by KEGA 030EU-4/2022, KEGA 019TUKE-4/2022 and VEGA 1/0508/21.

Conflicts of Interest

The authors declare no conflict of interest. The founding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, and in the decision to publish the results.

References

- Atkinson, A. A.; Kaplan, R. S.; Matsumura, E. M.; Young, S. M. Management Accounting: Information for Decision-Making and Strategy Execution, 6th ed.; Pearson Education Limited, 2012; p. 550. [CrossRef]

- Schaltegger, S.; Burritt, R. Contemporary environmental accounting: issues, concepts and practice, 1st ed.; Routledge, 2017; pp. 441. [CrossRef]

- Chovancová, J.; Rovňák, M.; Shpintal, M.; Shevchenko, T.; Chovanec, F. Perception of Benefits and Barriers Associated with the Management Systems Integration - A Comparative Study of Slovak and Ukrainian Organizations. TEM J. 2022, 11, 772. [Google Scholar] [CrossRef]

- Varaniūtė, V.; Žičkutė, I.; Žandaravičiūtė, A. The Changing Role of Management Accounting in Product Development: Directions to Digitalization, Sustainability, and Circularity. Sustainability 2022, 14, 4740. [Google Scholar] [CrossRef]

- Chung, J.; Cho, C.H. Current Trends within Social and Environmental Accounting Research: A Literature Review. Account. Perspect. 2018, 17, 207–239. [Google Scholar] [CrossRef]

- Deegan, C. An overview of legitimacy theory as applied within the social and environmental accounting literature. In Sustainability accounting and accountability, 2nd ed.; Routledge, 2014; pp. 248-272.

- Schaltegger, S.; Freund, F.L.; Hansen, E.G. Business cases for sustainability: the role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119. [Google Scholar] [CrossRef]

- Burritt, R.L.; Schaltegger, S. Sustainability accounting and reporting: fad or trend? Accounting, Audit. Account. J. 2010, 23, 829–846. [Google Scholar] [CrossRef]

- Epstein, M. J.; Buhovac, A. R. Making sustainability work: Best practices in managing and measuring corporate social, environmental, and economic impacts, 2nd ed.; Berrett-koehler publishers, 2014; p. 304.

- ISO 14001:2015. Environmental management systems - Requirements with guidance for use. 2015.

- Bebbington, J.; Unerman, J.; O’Dwyer, B. Introduction to sustainability accounting and accountability. In Sustainability accounting and accountability, 2nd ed.; Routledge, 2014; pp. 3-14.

- Suadiye, G. Contemporary Developments on Sustainability Accounting and Reporting: An Overview Perspective. In Auditing Ecosystem and Strategic Accounting in the Digital Era: Global Approaches and New Opportunities, 1st ed.; Springer, Cham, 2021; pp. 59-86.

- Azapagic, A.; Stamford, L.; Youds, L.; Barteczko-Hibbert, C. Towards sustainable production and consumption: A novel DEcision-Support Framework IntegRating Economic, Environmental and Social Sustainability (DESIRES). Comput. Chem. Eng. 2016, 91, 93–103. [Google Scholar] [CrossRef]

- Chovancová, J.; Huttmanová, E. Possibilities of management systems implementation with focus on their mutual integration. Hradec Economic Days (13th International Scientific Conference on Hradec Economic Days). Hradec Králové, Czech republic, 2015.

- López-Gamero, M.D.; Molina-Azorín, J.F.; Claver-Cortés, E. The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. J. Environ. Manag. 2009, 90, 3110–3121. [Google Scholar] [CrossRef] [PubMed]

- Galdeano-Gómez, E. Does an Endogenous Relationship Exist between Environmental and Economic Performance? A Resource-Based View on the Horticultural Sector. Environ. Resour. Econ. 2008, 40, 73–89. [Google Scholar] [CrossRef]

- Henri, J.-F.; Journeault, M.; Rodrigue, M. The Domino Effect of Perceived Stakeholder Pressures on Eco-Controls. Account. Public Interes. 2021, 21, 105–136. [Google Scholar] [CrossRef]

- Burritt, R.L.; Saka, C. Environmental management accounting applications and eco-efficiency: case studies from Japan. J. Clean. Prod. 2006, 14, 1262–1275. [Google Scholar] [CrossRef]

- Dunk, A. Assessing the Effects of Product Quality and Environmental Management Accounting on the Competitive Advantage of Firms. Australas. Account. Bus. Finance J. 2007, 1, 28–38. [Google Scholar] [CrossRef]

- Jasch, C. The use of Environmental Management Accounting (EMA) for identifying environmental costs. J. Clean. Prod. 2003, 11, 667–676. [Google Scholar] [CrossRef]

- Hinz, K.; Wagner, B.; Enzler, S. Developments in material flow management: outlook and perspectives, 1st ed.; Physica-Verlag HD, 2006; pp. 201.

- Kokubu, K.; Kitada, H. Material flow cost accounting and existing management perspectives. J. Clean. Prod. 2015, 108, 1279–1288. [Google Scholar] [CrossRef]

- Majerník, M.; Andrejovský, P.; Daneshjo, N.; Sančiová, G. Environmental Business Economics, 1st ed.; Typopress s. r. o., 2017; pp. 250.

- ISO 14051: 2011. Material flow cost accounting - General framework. 2011.

- ISO 50001:2018. Energy management systems - Requirements with guidance for use. 2018.

- Kokubu, K.; Kitada, H.; Nishitani, K.; Shinohara, A. How material flow cost accounting contributes to the SDGs through improving management decision-making. J. Mater. Cycles Waste Manag. 2023, 1–11. [Google Scholar] [CrossRef]

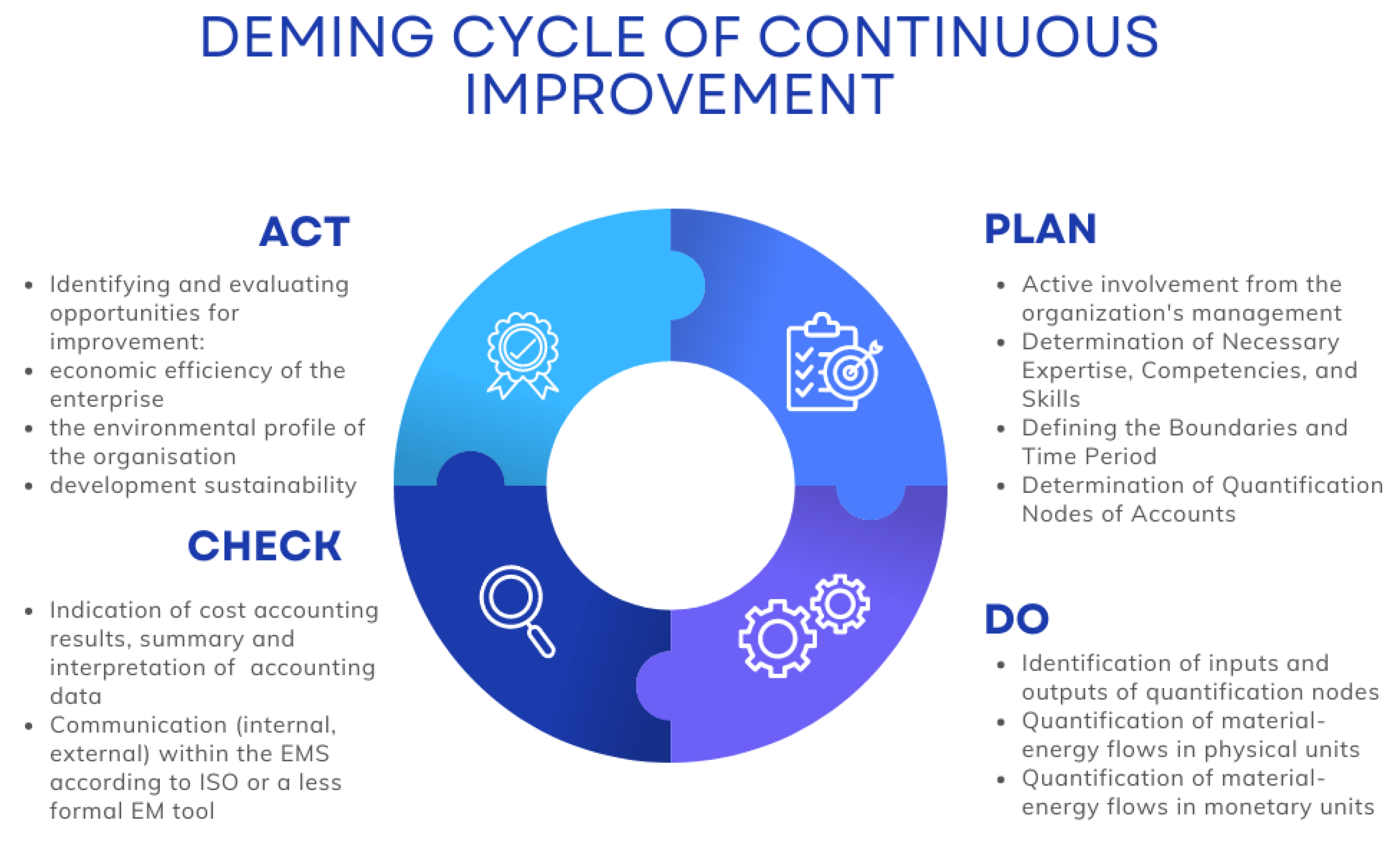

Figure 1.

Cost accounting model of an organisation's material and energy flows - standardising the processability in the P-D-C-A cycle.

Figure 1.

Cost accounting model of an organisation's material and energy flows - standardising the processability in the P-D-C-A cycle.

Figure 2.

Calculation of process costs in accounting for material and energy flows in an enterprise.

Figure 2.

Calculation of process costs in accounting for material and energy flows in an enterprise.

Figure 3.

Material-energy flow model including semi-finished products. Notes: M—material or energy, ML—material-energy loss, QN—quantity node, SP—semi-finished product,  finished product flow,

finished product flow,  material loss flow.

material loss flow.

finished product flow, material loss flow.

Figure 3.

Material-energy flow model including semi-finished products. Notes: M—material or energy, ML—material-energy loss, QN—quantity node, SP—semi-finished product, finished product flow, material loss flow.

finished product flow, material loss flow.

Figure 5.

Informative Sankey diagram.

Table 1.

Hierarchy of cost accounting steps for material and energy flows.

| Step | Description |

|---|---|

| 1 MANAGEMENT INVOLVEMENT |

The effective implementation of accounting practices requires strong support from top management within the organization. Management should actively participate in the process by providing leadership during implementation, assigning roles and responsibilities, allocating necessary resources, monitoring progress, reviewing results, and making decisions to improve the environmental-economic profile. |

| 2 DETERMINING THE REQUIRED EXPERTISE |

A comprehensive range of expertise is needed, particularly in areas such as operations design, production procurement, and technical knowledge related to material and energy flows within the organization. This includes understanding the implications of processes, quality management, corrective actions for environmental management, and knowledge of environmental aspects, impacts, and risks (EAI&R). Additionally, expertise in cost-benefit accounting for material and energy flows is essential. |

| 3 DEFINING BOUNDARIES AND TIME PERIOD FOR ACCOUNTING ANALYSES |

Organizations have the flexibility to determine the boundaries for accounting analyses, whether it involves a single process, multiple processes, an entire facility, or a supply chain. It is crucial to focus on processes with significant EAI&R potential. The time period for data collection should be sufficiently long to capture all relevant data and variations in processes, such as monthly, multiple months, six months, or a year. The time period can be aligned with the production of specific product items, for example. |

| 4 IDENTIFYING QUANTITY NODES (QNs) |

Various processes can be designated as quantity nodes (QNs) within the accounting framework. Examples of QNs include material receiving, semi-finished goods splitting, storage, intermediate storage, machining, welding, shipping, and others. The selection of quantity nodes is based on process information. Additional quantity nodes can be determined at locations with significant material losses, such as energy for transportation, oil leaks, pressurized air, or system costs. |

| 5 IDENTIFYING INPUTS AND OUTPUTS FOR EACH QN |

For each quantification node within the accounting boundaries, it is essential to identify inputs (materials and energy) and outputs (products, material losses, and energy losses). Energy and energy losses can either be included in the materials and material losses or estimated separately, depending on the organization's discretion. Identifying inputs and outputs for quantity nodes facilitates the linking of quantity nodes within the cost accounting boundaries, enabling interrelated evaluation of quantity nodes data throughout the system under study. |

| 6 QUANTIFYING MATERIAL FLOWS IN PHYSICAL UNITS |

For each quantity node, it is necessary to quantify inputs and outputs in physical units, such as weight, number of pieces, volume, length, etc. These measurements should be converted into a standardized unit (e.g., weight) to enable material balances for each quantity node. Material balance requires ensuring that the total quantity of outputs (products and material losses) equals the total quantity of inputs. All materials within the accounting boundaries should be quantified, while materials with minimal environmental or financial significance may be excluded. |

| 7 QUANTIFICATION OF MATERIAL FLOWS IN MONETARY UNITS |

MATERIAL COSTS For each quantity node, it is necessary to quantify the costs of inputs and outputs, including products and material losses. These costs can be determined based on various factors such as historical data, current costs, or costs for reproduction, depending on the organization's chosen cost accounting method. Additionally, material costs associated with changes in material inventory within each quantity node should also be quantified. ENERGY COSTS Energy costs need to be quantified for each quantity node in terms of energy consumption. If the energy costs of individual tasks are unknown or challenging to measure, the total energy costs of the selected processes should be allocated among the quantity nodes. Subsequently, the energy costs within each quantity node should be divided between products and material losses. SYSTEM COSTS System costs encompass all in-house material handling costs, excluding material, energy, and waste management costs. These costs include labour, depreciation, maintenance, transportation, and other relevant expenses. If the costs within each quantity node are unknown or difficult to measure, they should be allocated to the total system costs of the selected processes among the quantity nodes. Afterwards, the system costs of each quantity node should be apportioned between products and material losses. WASTE TREATMENT COSTS Waste treatment costs pertain to the expenses associated with managing material losses generated within each quantity node. It is essential to quantify these costs for each quantity node. |

| 8 SUMMARIZATION AND INTERPRETATION OF ACCOUNTING DATA |

The data acquired during the accounting analysis should be summarized in a format suitable for further interpretation, such as a material flow cost matrix or a material flow diagram. Summarized data allows organizations to identify quantity nodes with significant environmental and financial material losses. These quantity nodes can then undergo more detailed analysis and can be aggregated for the entire process under examination. |

| 9 COMMUNICATION OF ACCOUNTING RESULTS |

The outcomes of the accounting analysis should be effectively communicated to relevant stakeholders both within and outside the organization. This includes internal communication with management and external communication with stakeholders. The information derived from the accounting analysis can support decision-making processes aimed at improving both environmental and financial performance. Additionally, it can assist in developing effective communication tools to engage stakeholders. |

| 10 IDENTIFYING AND ASSESSING OPPORTUNITIES FOR IMPROVEMENT |

Identifying opportunities for improvement is a crucial aspect of cost accounting for material and energy flows in an organization. Actions aimed at achieving improvements may involve material substitution, modifications to production line processes or products, and the identification of research and innovation activities focused on enhancing material and energy efficiency. The cost accounting process not only facilitates improvements in accounting and information systems but also opens up avenues for overall organizational improvement. |

Table 2.

Material costs in the intermediate process (EUR).

| Composition of Products and Material Losses | Production Result (Weight-kg) | Unit Cost (EUR/kg) | Composition of Products and Material Losses |

|---|---|---|---|

| Products | 60 | 4650 | |

| Material XY | 60 | 77.5 | 4650 |

| Material Z | 0 | 20 | 0 |

| Material losses | 40 | 1950 | |

| Material XY | 20 | 77.5 | 1550 |

| Material Z | 20 | 20 | 400 |

| Total | 100 | 6600 |

Table 5.

Material-energy flow cost matrix (EUR): Period 20xx.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.