Submitted:

28 April 2026

Posted:

29 April 2026

You are already at the latest version

Abstract

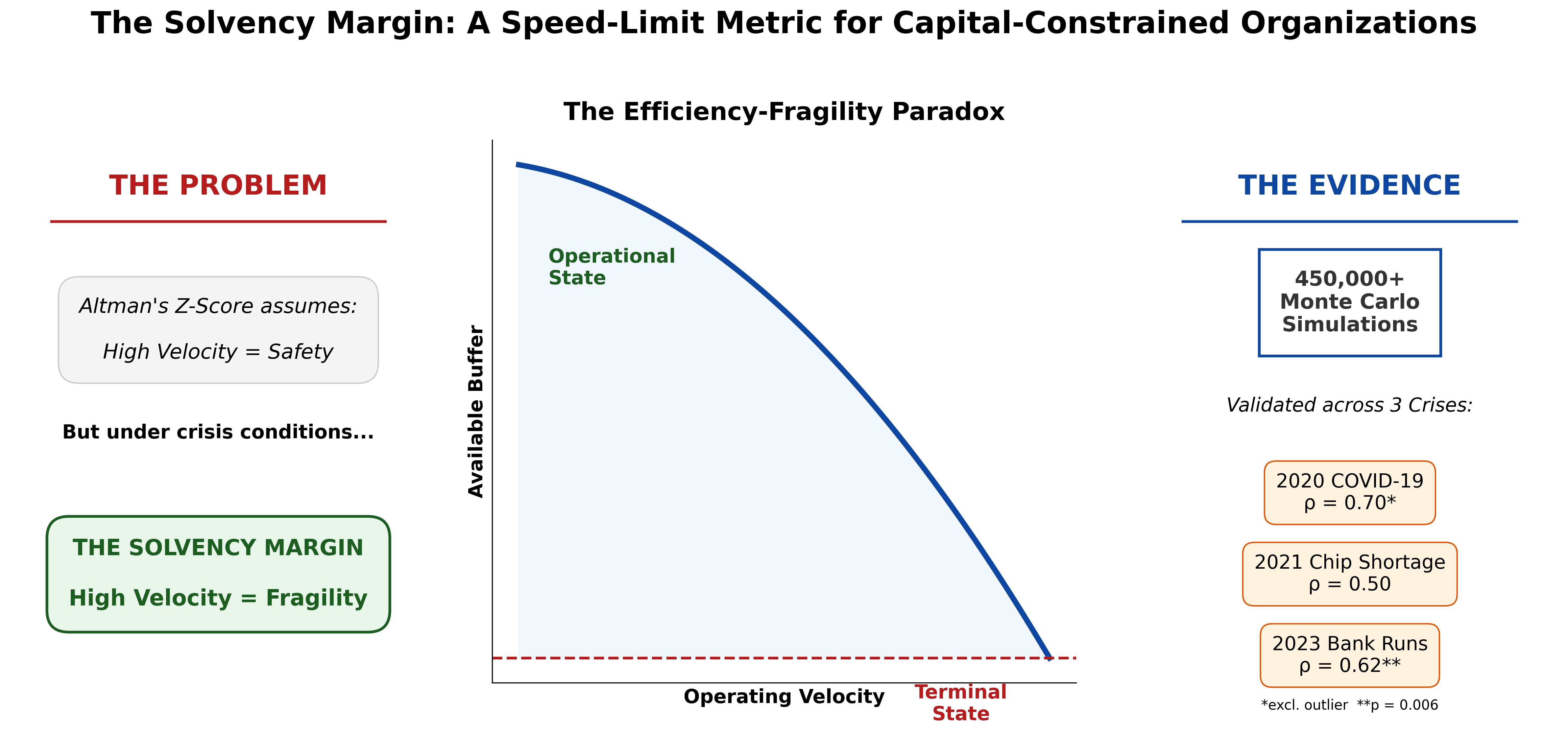

The most widely used bankruptcy predictor, Altman’s Z-Score, assigns a positive coefficient to asset turnover: faster firms are rated safer. Under crisis conditions, that assumption reverses. We introduce the Solvency Margin (SM), a diagnostic calculable from standard financial statements that measures, in dollars, how far an organization is from the threshold where operations become impossible. Unlike static liquidity ratios, the SM yields a concrete speed limit: the maximum operating velocity at which an organization can survive a defined shock. We validate the SM against pre-crisis financial data across three crises in two domains. In the automotive sector, SM computed from FY2019 filings showed directional predictive power among ten major automakers in both the 2021 semiconductor shortage (ρ = 0.50, p = 0.14) and the 2020 COVID-19 pandemic (ρ = 0.53, p = 0.12; ρ = 0.70, p = 0.036 excluding one governance-driven outlier). In the 2023 U.S. banking crisis, SM augmented with a Deposit Stability Factor predicted crisis outcomes among eighteen regional banks (Spearman ρ = 0.62, p = 0.006), correctly ranking three of four failed institutions in the bottom three positions. Monte Carlo simulation (450,000+ runs) confirms threshold behavior across a wide range of conditions. We present a five-step calculation method and a three-lever decision framework for practitioners.

Keywords:

Solvency Margin

; operational risk

; stress testing

; Supply Chain Resilience

; financial stability

; Monte Carlo Simulation

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.