Submitted:

01 April 2026

Posted:

02 April 2026

You are already at the latest version

Abstract

Sustainability has become a crucial strategic priority for firms operating in re-source-intensive industries such as food processing, where long-term competitiveness depends on responsible governance, strategic orientation, resource management and or-ganizational resilience. While prior research has established a general link between sus-tainability and organizational performance, less is known about how specific internal sustainability governance and management components contribute to firm financial per-formance. Drawing on the Resource-Based View and institutional theory, this study ex-amines the direct effects of a sustainability-oriented vision, business policy, organization-al culture, and strategies on firm financial performance. The study is based on survey data collected from 247 food processing firms operating in Slovenia, an EU member state. Ex-ploratory factor analysis and multiple regression analysis were used to test the proposed relationships. The results show that sustainability strategies have the strongest direct, sta-tistically significant positive effect on firm financial performance, followed by sustainabil-ity-oriented organizational culture. In contrast, sustainability vision and business policy exhibit a statistically significant, but negative, direct association, suggesting that formal sustainability commitments alone may not yield financial benefits without effective cul-tural support and strategic integration. These findings indicate that firm financial perfor-mance is directly driven primarily by sustainability strategies that are via practices opera-tionally embedded and supported by organizational capabilities such as organizational culture, rather than by normative symbolic commitments alone. This opens up possibili-ties for further research, based on the probability that the sustainable development vision and business policy serve as a catalyst for defining sustainable development strategies and implementing sustainable development practices, and that the normative commit-ments, in particular, indirectly influence financial performance. The study contributes to the sustainability governance and management literature by distinguishing the norma-tive, cultural, and strategic dimensions of sustainability and demonstrating their distinct direct implications for financial performance. The findings also provide practical insights for owners/governors and managers by highlighting the importance of integrating sus-tainability into organizational culture and core strategic processes to achieve long-term financial value.

Keywords:

sustainability governance

; sustainability management

; vision

; business policy

; organizational culture

; strategies

; financial performance

; food processing industry

1. Introduction

The integration of sustainability into core organizational strategy has become a critical challenge for firms operating in resource-intensive and environmentally sensitive industries [1]. The growing attention to responsible production, efficient use of natural resources and ethical business behavior has encouraged firms around the world to reconsider how sustainability is integrated into their long-term sustainability-oriented vision [2], thus business policy, (strategic) management, and operations. Regulatory frameworks at the European and global levels, along with technological advancements and shifting consumer attitudes, continually shape the competitive environment in which firms must operate. For many companies, sustainability has shifted from being an optional initiative to becoming a central part of organizational identity and long-term competitiveness [3,4].

The food processing industry is one of the sectors where the importance of sustainability is especially pronounced. This industry plays a crucial role in food security and public health, yet at the same time, it also faces significant environmental and social challenges. It depends heavily on natural resources, is vulnerable to fluctuations in global supply chains and must meet increasingly strict quality and safety standards [5]. Firms in this sector must manage complex relationships with suppliers, comply with environmental regulations and respond to the growing expectations of consumers who are increasingly aware of social and ecological impacts. These pressures make the food processing industry a unique context for analyzing how sustainability-related practices shape organizational outcomes [6,7].

In recent years, a growing body of research has explored the relationship between sustainability and organizational performance. Scholars have examined how environmental initiatives, social responsibility, and stakeholder engagement influence competitiveness and long-term success [1,8]. However, much of this research has focused primarily on environmental or social outcomes, while the financial dimension of sustainability has received comparatively less attention. Sustainable financial performance is understood as the firm’s ability to create long-term economic value through responsible resource management, reduced exposure to environmental and social risks, improved operational efficiency, and strengthened relationships with key stakeholders. It combines traditional financial indicators with sustainability-oriented practices to enhance a firm’s resilience and stability over time [9,10]. Although sustainability is widely recognized as a potential driver of financial benefits, empirical evidence regarding the specific organizational mechanisms that lead to firm financial performance remains fragmented. Previous studies often examined sustainability at a broad conceptual level, without distinguishing among the particular strategic and cultural elements that enable firms to convert sustainability ambitions into measurable financial outcomes. There is a need for a more detailed examination of the internal drivers of sustainability-oriented financial success, particularly in industries characterized by strict regulation, high resource dependence, and increasing public scrutiny [11,12].

Among the various dimensions of sustainability governance and management, three organizational components are particularly critical for understanding how firms translate sustainability commitments into performance outcomes. The first is the sustainability-oriented vision and business policy [1,13]. A clear sustainability-oriented vision signals organizational commitment, communicates long-term priorities, and strengthens the legitimacy of sustainability initiatives among internal and external stakeholders. The second component is a sustainability-oriented organizational culture. Culture shapes how employees behave, how they understand sustainability, and their willingness to engage in practices that support long-term responsibility. A supportive culture encourages collaboration, learning, and continuous improvement and increases the organization’s ability to implement sustainability initiatives effectively [8,9,14]. The third component compose sustainability strategies, which provide a clear direction for integrating sustainability objectives into the development and core business orientations. Well-developed sustainability-related strategies can shape decision-making, support the identification of new opportunities, determine the appropriate competitive advantage, and guide investments into environmentally and socially responsible practices.

Although previous studies have examined individual aspects of sustainability governance and management, considerably less attention has been devoted to understanding their combined influence on firm financial performance. The existing literature often treats sustainability governance and management tools as a uniform construct and does not explicitly identify which governance, cultural and strategic factors contribute most strongly to financial outcomes. Moreover, empirical research in the food processing sector remains limited, even though firms in this industry face intense pressure to adopt sustainability practices that influence both their competitiveness and their long-term financial stability. Understanding how sustainability-oriented vision and business policy, a sustainability-oriented organizational culture, and sustainability strategies contribute to firm financial performance is therefore highly relevant for both scholars and practitioners [5,13,15,16].

The purpose of this study is to address this gap by examining the extent to which three core components of sustainability governance and management, namely sustainability-oriented vision and business policy, a sustainability-oriented organizational culture, and sustainability strategies, influence firm financial performance in the food processing industry. Although prior research recognizes the broader importance of sustainability for organizational outcomes, empirical studies rarely examine how these specific internal mechanisms contribute to financial value creation within a sustainability context. This study responds to this need by developing a research model that conceptualizes financial performance as a potential outcome of a firm’s strategic orientation toward sustainability, considering its formalized long-term sustainability commitments in vision and business policy, its cultural capacity and strategies to support sustainability-related behavior throughout the organization. The research model developed in this study offers a comprehensive perspective that enables a more precise examination of how sustainability is embedded within organizational systems. Rather than treating sustainability governance and management as a single undifferentiated construct, the model distinguishes between normative, cultural, and strategic dimensions, thereby enabling a more precise examination of how each mechanism contributes to firm financial performance. By empirically testing this model on data collected from firms in the food processing industry, the study provides new insights into the organizational processes through which sustainability practices may influence long-term financial performance. This analytical approach deepens theoretical understanding and clarifies how internal governance and management structures support the transformation of sustainability commitments into measurable financial value.

This study makes several important contributions to sustainability governance and management literature and to understanding the relationship between sustainability and financial performance. First, drawing on the Resource-Based View and institutional theory, the study conceptualizes sustainability governance and management as a multidimensional organizational system consisting of normative, cultural, and strategic components. By examining sustainability-oriented vision and business policy, sustainability culture, and sustainability strategies as distinct organizational dimensions, the study provides a more refined framework for analyzing how internal sustainability management mechanisms relate to firm financial performance. Second, the study addresses an important gap in the literature by focusing on internal organizational drivers of financial performance, rather than treating sustainability governance and management as a single undifferentiated construct. Third, by examining firms operating in the food processing industry, the study provides empirical insights into a resource-intensive and sustainability-sensitive sector that remains relatively underrepresented in empirical sustainability research. Overall, the study contributes to a deeper theoretical and empirical understanding of how sustainability governance and management are embedded within organizational systems and how they may influence long-term financial performance.

2. Literature Review

2.1. Sustainability-Oriented Vision and Business Policy in the Food Processing Industry

A sustainability vision and business policy reflect the organization’s long-term product, market, and stakeholder commitments, values, and guiding principles related to sustainability. Whereas the sustainability strategies determine how sustainability is integrated into operations, the vision and business policy articulate why sustainability matters and what future the organization aims to achieve [17,18]. The vision and business policy component serves as a symbolic and normative foundation for organizational behavior. It communicates to employees, stakeholders, and the broader public that the organization is committed to responsible and ethical conduct [19]. In the food processing industry, the importance of a clear sustainability vision and a well-structured sustainability business policy is particularly pronounced due to the sector’s strong exposure to environmental and societal expectations [9,13]. Firms in this industry operate within complex supply chains that involve sensitive materials, perishable products, and resource-intensive production processes, thereby increasing the need for transparent and forward-looking sustainability commitments. A well-articulated sustainability vision provides strategic clarity in navigating these complexities by setting long-term priorities that integrate environmental responsibility, food safety, and social considerations into the organization’s purpose [15,20] and other business policy components.

Firms operate within environments that are continuously shaped by regulations, norms, and broader societal expectations. These external influences create a framework within which firms define their responsibilities and long-term priorities. A clear sustainability vision supports this process by providing a coherent reference point that guides organizational behavior and communicates a long-term commitment to responsible and forward-looking development [16,18]. Such a vision helps firms interpret and respond to external expectations in a consistent manner and signals that sustainability is an integral part of the organization’s identity and purpose. A well-articulated sustainability vision also strengthens internal alignment [20]. It clarifies how sustainability relates to the organization’s broader mission and ensures that employees at different hierarchical levels understand the direction the firm intends to pursue. This shared understanding reduces decision-making uncertainty and promotes internal coherence, particularly when firms face complex environmental or social challenges [21]. A formalized sustainability business policy further reinforces these effects by translating the vision into concrete organizational guidelines. It defines internal responsibilities, establishes behavioral expectations, and provides structure for the implementation of sustainability-related initiatives. Through this formalization, sustainability becomes embedded in organizational culture and is approached systematically rather than informally or on an occasional basis. Over time, this creates a stable internal environment in which sustainability considerations are naturally integrated into planning, communication, and operational processes, thereby supporting consistent progress toward long term sustainability objectives [17,18,21]. This is particularly relevant in the food processing industry, where firms operate in a highly regulated environment and face increasing expectations regarding product quality, resource efficiency, and socially responsible practices, making a clear sustainability vision and business policy essential for maintaining long term organizational stability [22]. Modern consumers increasingly expect transparency regarding ingredient origins, production methods, and environmental impacts. Firms that communicate a clear sustainability vision and integrate these values into their business policy are better positioned to build trust, strengthen brand reputation, and differentiate themselves in a competitive marketplace. This alignment between long-term sustainability aims, strategies orientation and operational routines contributes to the development of a more stable organizational environment, which supports both reputational and financial performance [17,23]. Thus, the following hypothesis is proposed:

H1.

The development of a sustainability vision and business policy impacts firm financial performance in the food processing industry.

2.2. Sustainability-Oriented Organizational Culture in the Food Processing Industry

A sustainability-oriented organizational culture reflects the shared values, assumptions, and behavioral expectations that encourage employees to act in ways that support long-term environmental and social responsibility [24]. Such a culture influences how individuals interpret sustainability goals, how they prioritize competing demands, and how they approach decision-making in situations where sustainability considerations may not be explicitly defined by rules or procedures [25]. When sustainability becomes an integral part of the organization’s collective mindset, employees are more likely to recognize the relevance of responsible practices in their daily activities and to proactively engage in behaviors that contribute to long term organizational well-being [17,25].

In the food processing industry, a sustainability-oriented organizational culture is particularly important because many sustainability-related outcomes depend on the everyday decisions, reactions, and informal practices of employees working in production, processing, and quality control [25]. Unlike formal governance and strategies determinations, which provide direction at the organizational level and give the firm’s culture the appropriate framework, culture also shapes how individuals interpret sustainability expectations during fast-paced operational routines [8]. Food processing environments require constant vigilance, coordination, and judgment, since employees often respond to rapidly changing production conditions, unexpected variations in raw materials, or time-sensitive quality demands. Under these circumstances, shared values and behavioral norms strongly influence whether sustainability considerations are consistently upheld in practice [24,26].

The effectiveness of sustainability initiatives in food processing firms, therefore, depends not only on formal guidelines but also on whether employees internalize sustainability as part of their professional identity [7,9]. A culture that encourages responsibility, attention to detail, and collective problem solving helps prevent small operational deviations from escalating into larger quality, environmental, or safety issues [8]. This is especially relevant in settings where production processes are highly interconnected, meaning that the actions of one department can easily affect the performance of others. When sustainability is embedded in organizational culture, employees communicate more effectively, recognize potential risks earlier, and cooperate more readily across functional boundaries [5,24,26]. Such cultural characteristics foster a work environment in which continuous improvement is viewed as a shared responsibility. Employees become more willing to identify inefficiencies, propose changes, and adapt their practices to emerging sustainability requirements. Over time, this proactive orientation strengthens organizational resilience and supports the long-term ability of food processing firms to meet both internal performance goals and external sustainability expectations [13,15,22,27]. Moreover, the following hypothesis is proposed:

H2.

A sustainability-oriented organizational culture impacts firm financial performance in the food processing industry.

2.3. Sustainability Strategies in the Food Processing Industry

Sustainability strategies refer to a firm’s formalized long-term orientation toward integrating environmental, social, and governance principles into its core business model. It provides a structured framework that guides decisions, investments, and organizational priorities in ways that align economic objectives with sustainability-related goals [4,28]. Well-developed sustainability strategies enhance a firm’s ability to identify new opportunities, reduce operational risks, and create value for a broad set of stakeholders [3]. It enables firms to anticipate regulatory trends, adapt to market expectations, and build competitive advantage through responsible resource use, innovation, and transparency [4,9]. In the food processing industry, sustainability-oriented strategies often drive innovations in product development, packaging, and resource use, enabling firms to reduce costs, meet market expectations, and strengthen their long-term competitive position [20].

Sustainability-oriented firms operate on the premise that long-term success depends on the integration of economic, environmental, and social considerations into organizational planning and decision-making [29]. In such firms, sustainability functions as a guiding perspective that shapes priorities, influences resource allocation, and encourages the development of structures that support resilience, learning, and responsible use of resources [30]. This perspective broadens the understanding of value creation by recognizing that financial outcomes emerge not only from internal efficiency but also from the organization’s ability to maintain stable external relationships and to respond effectively to changing societal and market expectations [19,31]. A sustainability-oriented approach also strengthens the internal foundations of the firm. Firms that integrate sustainability into their strategic thinking gradually build specialized knowledge, routines, and competencies that enhance adaptability and long-term competitiveness [12]. These capabilities are often difficult for competitors to imitate because they develop over time and are embedded in organizational processes, values, and decision-making patterns [14]. At the same time, firms that consistently act in line with broader societal expectations tend to gain trust and credibility, which reinforces organizational stability and creates favorable conditions for achieving superior financial results [6]. In the food processing sector, where supply chains are vulnerable to environmental disruptions and regulatory pressures are continuously intensifying, well-developed sustainability-oriented strategies enhance organizational resilience and support more stable financial outcomes [6,22].

Research has shown that firms with a clearly articulated sustainability strategies tend to achieve better financial outcomes through enhanced resource efficiency, reduced compliance costs, better risk management, and improved brand reputation. Coherent strategies also increase organizational capacity to implement sustainability initiatives consistently across departments and business functions [3,32,33]. In addition to these effects, sustainability strategies strengthen long-term organizational orientation by encouraging firms to systematically evaluate how environmental and social factors influence their future competitiveness [4]. A well-formulated sustainability strategies also improve organizational alignment [28]. When sustainability objectives are integrated into core planning processes, employees across different functions share a clearer sense of direction, which supports coordination and reduces decision-making fragmentation [11]. This integration fosters a more unified organizational response to sustainability challenges and ensures that sustainability-related activities are not limited to isolated departments but become embedded across the entire firm [3,28]. Over time, this generates internal capabilities that enhance resilience and adaptability, especially in environments exposed to frequent economic, regulatory, or supply chain disruptions. By guiding organizational priorities and shaping long-term investment decisions, sustainability strategies provide the direction necessary for translating sustainability ambitions into measurable financial value [6,19]. It stimulates the development of internal strengths, supports external legitimacy, and creates a more coherent organizational environment in which sustainability-related goals can be systematically realized [17,23]. The relevance of a comprehensive sustainability strategies is especially evident in the food processing industry, which is characterized by resource-intensive production processes, complex supplier networks, and increasing societal expectations regarding transparency, safety, and environmental responsibility [5,22]. Based on these theoretical considerations, we propose the following hypothesis:

H3.

The development of a sustainability strategies impact firm financial performance in the food processing industry.

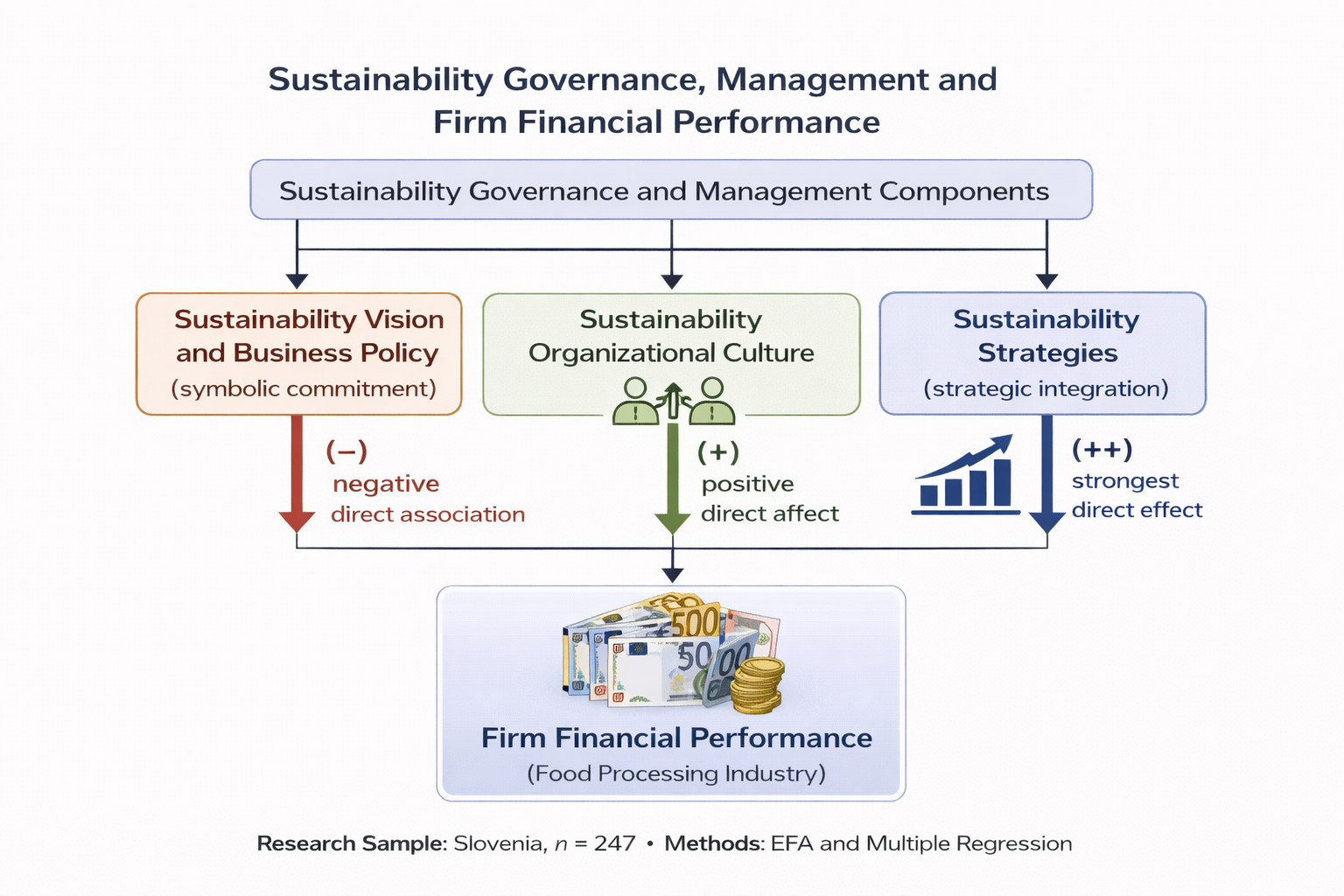

Based on the proposed hypotheses, this study presents a conceptual model linking the three dimensions of sustainability governance and management to firm financial performance. The model provides a structured overview of the assumed relationships and clarifies how sustainability-oriented vision and business policy, a sustainability-oriented organizational culture, and sustainability strategies are expected to influence firm financial outcomes in the food processing industry. The conceptual model that guides the empirical analysis is presented in Figure 1.

2.4. Theoretical Foundations of the Research Model

The relationships examined in this study can be theoretically explained through the lens of the Resource-Based View (RBV) of the firm and institutional theory. These complementary perspectives provide a coherent foundation for understanding how internal sustainability governance and management components influence firm financial performance.

The Resource-Based View posits that organizational performance differences arise from firm-specific resources and capabilities that are valuable, rare, inimitable, and non-substitutable [34]. Such resources enable firms to develop competitive advantages that translate into superior financial outcomes over time. In the context of sustainability management, strategic orientation toward sustainability and sustainability-oriented organizational culture present internal organizational capabilities that shape how firms respond to environmental and societal challenges. Sustainability strategies reflect the firm’s ability to integrate sustainability considerations into its core planning, therefore, resource acquisition and allocation, and operational decision-making processes. This strategic capability allows firms to improve resource efficiency, reduce operational risks, enhance stakeholder relationships, and identify new opportunities for innovation and value creation. Similarly, a sustainability-oriented organizational culture represents an embedded organizational capability that supports consistent implementation of sustainability-related practices. Cultural alignment facilitates coordination, strengthens employee engagement, and enhances organizational adaptability, thereby contributing to long-term financial stability and performance. From an RBV perspective, sustainability strategies and sustainability-oriented organizational culture function as strategic organizational capabilities that enable firms to convert sustainability-related commitments into tangible financial benefits.

At the same time, institutional theory provides important insight into the role of sustainability vision and business policy. Institutional theory suggests that firms adopt formal structures, policies, and declarations not only to improve efficiency but also to achieve legitimacy and conform to societal expectations, regulatory pressures, and stakeholder demands [35,36]. In this context, sustainability vision and business policy represent formal expressions of organizational commitment to sustainability that communicate legitimacy to external stakeholders and establish normative expectations within the organization. These symbolic and declarative elements play an important role in shaping organizational identity and stakeholder perceptions. However, institutional theory also highlights that formal sustainability commitments may not always translate directly into improved financial performance, particularly when they are not fully integrated into strategic and operational processes. This phenomenon, often referred to as decoupling, occurs when formal policies and declarations are not accompanied by corresponding changes in organizational practices. As a result, sustainability vision and business policy may serve primarily symbolic or legitimacy-enhancing functions rather than directly improving financial outcomes.

By integrating insights from the Resource-Based View and institutional theory, this study conceptualizes sustainability governance and management as a multidimensional organizational system consisting of symbolic normative, cultural, and strategic components. Sustainability-oriented organizational culture and sustainability strategies represent internal capabilities that directly enhance organizational effectiveness and financial performance, consistent with RBV. In contrast, sustainability vision and business policy represent formal and symbolic organizational commitments that provide normative direction and legitimacy but may influence financial performance indirectly or conditionally, as suggested by institutional theory. This theoretical framework provides a coherent foundation for examining how different dimensions of sustainability management contribute to firm financial performance in the food processing industry and supports the development of the proposed research hypotheses.

3. Methodology

3.1. Data and Sample

The study was conducted among companies operating in the food processing industry in Slovenia, an EU state, between December 2025 and January 2026. Data were collected using a structured online questionnaire that was sent to the owners or authorized governance or top management representatives of each firm. The final sample consisted of 247 firms operating in the food processing industry in Slovenia. Regarding firm size, micro firms present the majority of the sample (71.3%), followed by small firms (17.4%). Medium-sized firms account for 6.5%, while large firms present 4.9% of the participating firms. This distribution indicates that the sample is strongly dominated by smaller firms, which is consistent with the general structure of the food processing sector in Slovenia. In terms of ownership structure, most firms are privately owned (98.0%), while only 2.0% reported other forms of ownership, including mixed ownership structures combining private and public capital. Regarding the origin of majority ownership, the vast majority of firms are domestically owned (93.9%). Foreign ownership accounts for 3.6% of firms, while mixed ownership (combining domestic and foreign capital) accounts for 2.4%.

3.2. Measurement Instrument

A closed-type online questionnaire was employed as the research instrument. The owner of each company was asked to rate their agreement with the provided statements on a 7-point Likert-type scale ranging from 1, which corresponds to ‘strongly disagree’, to 7, which corresponds to ‘completely agree’. The research was conducted using an online survey, which ensures complete anonymity and the absence of any collection of personal data. Reliability of the constructs was tested using Cronbach’s alpha, with all constructs exceeding the recommended value of 0.8. The questionnaire design was initially informed by an industry-developed sustainability self-assessment tool [37] and subsequently re-specified and theoretically grounded in peer-reviewed academic literature. Measurement items for the construct Sustainability-oriented vision and business policy were developed, drawing on Zhang [17]. Measurement items for the construct Sustainability-oriented organizational culture were developed drawing on Ali et al. [25] and Dorda and Shtembari [24]. Measurement items for the construct Sustainability strategies were developed drawing on Lloret [29] and Coppola and Ianuario [6], while also reflecting the integration of sustainability into strategic management processes [38]. The construct Firm’s financial performance in the food processing industry was developed drawing on Arian et al. [3] and Alshehhi et al. [30].

3.3. Data Analysis

Data analysis was conducted in several stages to ensure a comprehensive examination of the proposed research model. In the first step, descriptive statistics were calculated to provide an overview of respondents’ agreement levels with each item related to the three sustainability management constructs and the firm’s financial performance in the food processing industry. In the second step, an exploratory factor analysis was conducted with the aim of reducing a larger number of observed variables into a smaller set of underlying factors and of confirming whether the items for each construct measure a single latent dimension. The suitability of the data for factor analysis was verified using the Kaiser–Meyer–Olkin (KMO) measure and Bartlett’s test of sphericity, both of which indicated that the correlations among items were adequate for factor extraction. Communalities and factor loadings were examined to ensure that items contributed meaningfully to their respective constructs. Item Q4e was excluded from subsequent analyses following the exploratory factor analysis due to low communality. Across all four constructs, the analysis yielded a clear one-factor solution, confirming that each scale represented a single underlying dimension. Following this, multiple regression analysis was conducted to examine the effects of the three independent variables, namely sustainability-oriented vision and business policy, sustainability-oriented organizational culture, and sustainability strategies, on the dependent variable, firm financial performance. The analysis enabled the assessment of how each predictor contributes to explaining variations in firm financial performance while simultaneously controlling for shared variance among the constructs. In addition to standardized regression coefficients and their significance levels, the multiple correlation coefficient, the adjusted coefficient of determination, and the overall F-test of model fit were examined to evaluate the explanatory power of the regression model.

Because all variables in this study were collected using a self-reported survey questionnaire from a single respondent per firm, the potential presence of common method bias was assessed. Harman’s single-factor test was conducted by including all measurement items in an exploratory factor analysis. The results showed that the first unrotated factor accounted for less than 50% of the total variance, indicating that no single factor dominated the variance structure. This suggests that common method bias is unlikely to be a serious concern in this study and does not significantly affect the validity of the results.

4. Results

The results of the empirical analysis are presented in this section. First, descriptive statistics are reported for each of the main constructs included in the research model, namely sustainability-oriented vision and business policy, sustainability-oriented organizational culture, sustainability strategies, and firm financial performance in the food processing industry. These statistics provide an overview of respondents’ evaluations of sustainability-related governance and management directions and practices, as well as financial outcomes within their firms. The descriptive statistics for the construct sustainability-oriented vision and business policy are presented in Table 1.

The descriptive statistics for the construct Sustainability-oriented vision and business policy indicate generally high levels of agreement among respondents, suggesting that firms in the food processing industry tend to perceive their sustainability-related vision and business policy commitments positively. Among the four statements, the highest mean value was recorded for “The firm’s vision clearly emphasizes its responsibility for environmental protection” (Mean = 5.71, Std. deviation = 1.286), indicating that environmental responsibility is the most strongly recognized element of sustainability-related vision. A similarly high level of agreement was observed for “The firm’s vision clearly emphasizes its responsibility toward society and future generations” (Mean = 5.62, Std. deviation = 1.356), showing that respondents also view intergenerational and societal responsibility as an integral part of their organizational vision. The statement “The firm’s mission clearly expresses its commitment to sustainable development” also received a relatively high mean score (Mean = 5.64, Std. deviation = 1.357), suggesting that sustainability is embedded not only in vision but also in the broader firm’s mission and long-term orientation. The lowest level of agreement was found for the statement “The firm has a designated manager or specialist responsible for implementing its sustainability business policy and objectives” (Mean = 4.48, Std. deviation = 2.034). This suggests that sustainability orientation is well-established at the level of the company’s vision and mission, while its’ operational implementation, particularly in terms of clearly defined responsibilities, is less consistent and represents an important opportunity for further development. The following Table 2 presents descriptive statistics for the construct Sustainability-oriented organizational culture.

The descriptive statistics for the construct Sustainability-oriented organizational culture show generally positive perceptions of how sustainability is embedded in firms’ development, decision-making, practices, and employee behavior. The highest mean value was observed for the statement “Sustainability is part of the firm’s development decisions and everyday work routines” (Mean = 5.11, Std. deviation = 1.371), indicating that sustainability is, to a considerable extent, integrated into development decision-making and day-to-day operations and processes within the firms surveyed. A similarly high level of agreement was recorded for the statement “The organizational culture encourages sustainability-oriented decision-making” (Mean = 5.02, Std. deviation = 1.328). This suggests that organizational norms and values embedded in the organizational culture generally support decisions that take environmental and social considerations into account. The lowest mean value within this construct was reported for “Employees at all levels actively participate in sustainability initiatives” (Mean = 4.71, Std. deviation = 1.494). Although still above the midpoint of the scale, this lower value implies that employee involvement in sustainability-related activities is less consistent across firms surveyed. The higher variance for this item further indicates notable differences among firms in terms of how widely sustainability engagement is distributed among employees. These findings indicate that although sustainability is already embedded in key firms’ processes, the extent of employee involvement varies across firms, suggesting opportunities to further encourage their engagement and foster a more consistently sustainability-oriented organizational culture. Table 3 presents the results of descriptive statistics for the construct Sustainability strategies.

The descriptive statistics for the construct Sustainability strategies indicate moderate to relatively high levels of agreement among respondents, suggesting that sustainability considerations are incorporated into strategic decision-making within the firms under study. Among the items, the highest mean score was recorded for the statement referring to the definition of social sustainability objectives (Mean = 5.08, Std. deviation = 1.863), indicating that social aspects such as employee well-being, safety, equality, and community impact are relatively well integrated into firms’ strategies. Similarly, managerial sustainability objectives (Mean = 4.94, Std. deviation = 1.829) and environmental sustainability objectives (Mean = 4.86, Std. deviation = 1.899) show comparatively high levels of agreement. Lower levels of agreement were observed for the existence of a formal sustainability committee or management team (Mean = 3.12, Std. deviation = 1.936), indicating that formal management structures dedicated specifically to sustainability are less consistently established across the firms examined. The item referring to the adaptation of the business model to enhance sustainability orientation (Mean = 4.23, Std. deviation = 2.083) and the incorporation of sustainability objectives into strategic business plans (Mean = 4.33, Std. deviation = 2.094) show moderate agreement, but also relatively higher variability among the firms observed. Overall, the results suggest that while sustainability principles are generally embedded within strategic frameworks, the level of formalization and institutionalization of sustainability structures varies across the firms. Table 4 presents descriptive statistics for the construct of the firm’s financial performance in the food processing industry.

The descriptive statistics for the construct Firm financial performance in the food processing industry indicate generally positive perceptions of financial stability and performance among the surveyed firms. The highest mean value was recorded for the statement “The firm maintains adequate liquidity and cash flow” (Mean = 5.55, Std. deviation = 1.277), suggesting that liquidity management represents one of the strongest financial aspects across the sample. Relatively high levels of agreement were also observed for indicators related to revenue growth and market position. The statement “The firm has recorded stable revenue growth over the past three years” achieved a mean score of 5.42 (Std. deviation = 1.471), while the statement “The firm’s market share in key markets has increased or remained stable over the past three years” received a mean value of 5.22 (Std. deviation = 1.514). These results indicate that many firms perceive their financial performance as stable and improve or at least maintain their competitive market position over time. Moderate to high agreement was found for operational efficiency and access to financial resources. The statements concerning efficient cost management (Mean = 5.02, Std. deviation = 1.502) and access to external sources of financing (Mean = 5.00, Std. deviation = 1.613) suggest that firms generally consider themselves capable of managing operational costs and securing external funding when needed, although some variability across the firms examined is evident. Slightly lower agreement was reported for profitability improvements and value creation per employee. The statement related to improved profitability over the past three years (Mean = 4.97, Std. deviation = 1.591) indicates moderately positive perceptions, while the statement “The firm generates high value added per employee compared to its competitors” received the lowest mean score within the construct (M = 4.64, Std. deviation = 1.663). This suggests that, despite overall financial stability, differences remain in firms’ ability to translate performance into higher productivity and value creation. In Table 5, exploratory factor analysis is conducted to examine the underlying factor structure of all constructs included in the study.

Table 5 presents the results of the exploratory factor analysis conducted to assess the underlying factor structure of all constructs included in the study and to evaluate the suitability of the measurement scales. Before factor extraction, the adequacy of the data was examined using the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy and Bartlett’s test of sphericity. For all constructs, the KMO values exceeded the recommended threshold of 0.60, indicating that the sample was adequate for factor analysis. Bartlett’s test of sphericity was statistically significant for all constructs (p < 0.001), demonstrating that the correlation matrices were not identity matrices and that factor analysis was appropriate. The examination of communalities showed that, across all constructs, item communalities exceeded the recommended minimum value of 0.40, indicating that the retained items shared a sufficient proportion of variance with their respective factors. An exception was observed for item Q4e (“The firm has good access to external sources of financing (e.g., loans, investments)”) within the construct Firm financial performance in the food processing industry. This item exhibited a communality below the acceptable threshold of 0.40 and was therefore removed from further analysis. After the exclusion of this item, all remaining indicators demonstrated adequate communalities and factor loadings. The results of the factor extraction revealed a clear one-factor solution for each construct. For the sustainability-oriented vision and business policy, a single factor explained 77.40% of the total variance, with all items showing strong factor loadings. Similarly, the sustainability strategies yielded a one-factor solution explaining 74.14% of the variance, while sustainability-oriented organizational culture demonstrated a particularly high explained variance of 83.72%, indicating a highly coherent construct. The construct firm financial performance in the food processing industry, after the removal of the item Q4e, also formed a single factor, explaining 70.48% of the total variance. In the next step, multiple regression analysis is employed to test the proposed hypotheses (Table 6).

The results of the multiple regression analysis indicate a moderate relationship between the set of independent variables and firm financial performance in the food processing industry. The multiple correlation coefficient equals R = 0.575, suggesting that sustainability-oriented vision and business policy, sustainability-oriented organizational culture, and sustainability strategies are collectively associated with firm financial performance. The adjusted coefficient of determination equals 0.322, indicating that approximately 32.2% of the variance in firm financial performance is explained by the sustainability governance and management components included in the model. The F-test value equals 39.767 and is statistically significant (p < 0.001), indicating that the regression model as a whole is statistically significant and of satisfactory quality. This result means that the set of independent variables jointly explains a significant portion of variance in firm financial performance, confirming the overall quality and adequacy of the regression model. An examination of the individual regression coefficients presented in Table 6 reveals statistically significant effects for all three hypothesized relationships.

Regarding hypothesis H1, sustainability-oriented vision and business policy exhibit a statistically significant but negative relationship with firm financial performance (β = −0.200, p = 0.039). This finding suggests that formal sustainability commitments alone may not directly translate into improved financial outcomes. From an institutional theory perspective, a sustainability-oriented vision and business policy represent symbolic and normative elements that enhance a firm’s legitimacy and signal its commitment to external stakeholders. However, such declarative commitments may not improve financial performance unless they are effectively translated into strategies and practices. This finding may support the distinction between symbolic and substantive sustainability, suggesting that sustainability initiatives create financial value primarily when they are strategically integrated and behaviorally embedded within the firm. In the absence of effective strategic implementation and cultural alignment, sustainability-oriented vision and business policy may remain symbolic rather than performance-enhancing firm elements. Regarding hypothesis H2, a sustainability-oriented organizational culture shows a positive, statistically significant relationship with firm financial performance (β = 0.191, t = 2.138, p = 0.034). This result supports H2 and suggests that organizational cultures encouraging sustainability-oriented decision-making and employee engagement contribute positively to financial outcomes. In line with hypothesis H3, sustainability strategies exhibit the strongest positive and statistically significant effect on firm financial performance (β = 0.576, t = 6.594, p < 0.001). This finding provides strong support for H3 and indicates that firms with more developed and operationally integrated sustainability strategies tend to achieve higher levels of firm financial performance. Overall, the regression results demonstrate that all proposed hypotheses are supported at the 5% significance level. However, contrary to expectations, sustainability-oriented vision and business policy exhibit a statistically significant negative effect on firm financial performance. At the same time, the direction and magnitude of the effects indicate that sustainability-oriented organizational culture and sustainability strategies have statistically significant positive effects and play a more direct role in enhancing firm financial performance, while the impact of sustainability vision and business policy appears to be more nuanced and potentially indirect.

5. Discussion

5.1. Discussion of Findings

The purpose of this study was to examine how key internal components of sustainability governance and management influence firm financial performance in the food processing industry. By distinguishing between sustainability-oriented vision and business policy, a sustainability-oriented organizational culture, and sustainability strategies, the study responds to calls in the literature for a more nuanced understanding of the organizational mechanisms through which sustainability contributes to long-term financial outcomes. The results provide important insights into the relative importance and nature of these components and highlight the need to move beyond symbolic commitments toward more deeply embedded sustainability directions and practices.

From a theoretical perspective, sustainability governance and management processes are increasingly viewed as a multidimensional organizational phenomenon that encompasses formal governance structures, strategic intent, and shared behavioral norms [2,22]. Prior research suggests that while sustainability-related declarations and commitments are important for signaling responsibility and legitimacy, financial benefits are more likely to emerge when sustainability is operationalized through concrete strategies and supported by organizational culture [8,24]. The findings of this study are largely consistent with this perspective and help clarify the distinct roles played by each sustainability governance and management component [3,8]. The descriptive statistics of this study provide additional insight into how sustainability is perceived and implemented within the food processing industry. In food processing firms in Slovenia, high levels of agreement with statements related to sustainability vision, mission, and strategic intentions suggest that sustainability is widely recognized at a formal and declarative level. In contrast, lower mean values for items related to dedicated sustainability formal governance structures, roles, and active employee participation indicate that the operationalization of sustainability remains uneven across firms. This pattern points to a gap between normative and strategic commitment and practical implementation, where sustainability is strongly embedded in organizational narratives but less consistently supported by formal structures and broad-based employee involvement. From a financial perspective, firms report greater confidence in stability-related outcomes, such as liquidity and revenue growth, than in productivity and value creation indicators, highlighting challenges in translating sustainability ambitions into efficiency gains. Taken together, these findings suggest that in the context of Slovenian food processing firms, moving beyond symbolic sustainability commitments toward deeper strategic integration and cultural embedding is essential for achieving financial performance.

The results regarding sustainability-oriented vision and business policy reveal a statistically significant but negative association with firm financial performance. Although hypothesis H1 is supported in statistical terms, the direction of the relationship suggests that sustainability-oriented vision and business policy alone may not directly translate into positive financial outcomes. This finding suggests that formal sustainability commitments can be difficult to translate into substantive outcomes, and symbolic commitments are often critiqued for their limited practical impact on stakeholders’ behavior and organizational effectiveness, especially when not integrated into operational strategies [16,18]. Such formal commitments are essential for articulating long-term intentions, strengthening firm identity, and responding to external expectations. However, when not accompanied by effective strategic integration and behavioral support, they may remain aspirational and detached from operational decision-making and behavior [15,20]. In the food processing industry, where firms face substantial regulatory requirements and reporting obligations, developing formal sustainability policies may also entail additional administrative and compliance-related costs that do not immediately yield financial returns [20,22]. This may help explain the observed negative coefficient and indicates that the financial implications of sustainability-oriented vision and business policy are likely indirect and contingent upon complementary organizational mechanisms.

In contrast, a sustainability-oriented organizational culture positively influences firm financial performance in the food processing industry in Slovenia (H2). This result underscores the importance of shared values, norms, and behaviors in translating sustainability strategies into effective action. In food processing firms, many sustainability outcomes depend on everyday employee decisions related to production, quality control, and resource management [7,13]. A culture that encourages sustainability-oriented decision making and active employee involvement strengthens coordination across organizational units and reduces the risk that sustainability remains confined to formal plans or managerial rhetoric [13,15]. The positive effect of organizational culture observed in this study among food processing companies in Slovenia is consistent with previous research highlighting the role of employee engagement and internal alignment in achieving both sustainability and financial objectives. In this context, a supportive organizational culture appears to facilitate the integration of sustainability principles into everyday practices, thereby enhancing firms’ ability to translate sustainability initiatives into measurable financial outcomes.

The findings also provide support for hypothesis H3, indicating that sustainability strategies are the most influential predictor of financial performance in food processing firms in Slovenia. This finding confirms that firms that integrate sustainability into their core strategic planning processes are better positioned to achieve stable and resilient financial outcomes [6,31]. A well-developed sustainability strategies enable firms to align sustainability goals with business objectives, optimize resource use, reduce long-term risks, and identify new opportunities for innovation and value creation [6]. In the food processing industry, where production processes are resource-intensive and supply chains are vulnerable to environmental and regulatory disruptions, strategic sustainability orientation appears to play a particularly critical role [9,22]. The results of this study, based on data from food processing firms operating in Slovenia, indicate that a sustainability strategy plays a key role in enhancing financial performance by supporting operational efficiency, strengthening competitiveness, and improving long-term adaptability.

5.2. Theoretical Implications

This study offers several important theoretical implications for sustainability governance and management research by advancing the understanding of how different internal dimensions of sustainability governance and management directly relate to firm financial performance. While prior research has widely recognized sustainability as a driver of organizational performance, sustainability governance and management have often been conceptualized as a relatively homogeneous construct, without clearly distinguishing between its normative symbolic, cultural and strategic management components. This study contributes to the literature by demonstrating that sustainability governance and management represent a multidimensional organizational system in which different components play distinct roles and have different implications for financial outcomes.

This study contributes to institutional theory by highlighting the distinct role of sustainability-oriented vision and business policy as symbolic and normative organizational elements. While sustainability-oriented vision and business policy are essential for communicating firm commitment and achieving legitimacy, the results indicate that these declarative elements do not necessarily translate directly into improved financial performance. The observed negative association suggests that formal sustainability commitments may primarily fulfil symbolic or legitimacy-enhancing functions when not supported by corresponding strategic integration and firm capabilities. This finding provides empirical support for the concept of decoupling, which suggests that formal policies and declarations may be adopted to satisfy institutional expectations without necessarily producing immediate performance benefits. By empirically distinguishing between normative symbolic sustainability commitments (represented by a firm’s vision and business policy) and operationally embedded strategic sustainability capabilities (represented by a firm’s organizational culture and the determination of its strategies), this study contributes to a more nuanced theoretical understanding of the mechanisms through which sustainability influences organizational outcomes.

This study also contributes to the Resource-Based View by providing empirical evidence that sustainability-oriented organizational culture and sustainability strategies function as strategic organizational capabilities that enhance firm financial performance. These findings support the argument that sustainability-related capabilities can serve as valuable and difficult-to-imitate organizational resources that strengthen long-term competitiveness and financial resilience. By showing that sustainability strategies exhibit the strongest positive effect on sustainable financial performance, the study reinforces the view that sustainability creates financial value when it is embedded in core organizational decision-making and influences resource allocation processes. Similarly, the positive effect of sustainability-oriented organizational culture highlights the importance of behavioral alignment and shared organizational values in enabling firms to effectively implement sustainability initiatives and translate them into measurable financial outcomes.

Further, this study advances the sustainability governance and management literature by explicitly distinguishing between the normative symbolic, cultural, and strategic dimensions of sustainability governance and management and demonstrating that these dimensions have distinct direct financial implications. This dissimilarity provides a more refined conceptualization of sustainability governance and management, and helps explain previously mixed findings regarding the sustainability–financial performance relationship. The results suggest that direct financial benefits are more likely to arise from sustainability practices that are strategically integrated into strategies and culturally embedded, rather than from normative symbolic declarations alone. This theoretical insight contributes to a deeper understanding of how sustainability creates firm value and clarifies the internal firm conditions under which sustainability initiatives are most likely to enhance direct financial performance.

Overall, this study extends existing sustainability governance and management research by providing a theoretically grounded and empirically supported framework that distinguishes between different firm mechanisms of sustainability integration. By integrating insights from the Resource-Based View and institutional theory, the study demonstrates that sustainable financial performance is primarily driven by strategic and behavioral sustainability capabilities via firm strategies and culture, while normative symbolic sustainability commitments via firm vision and business policy play a more indirect and context-dependent role. This refined conceptual perspective enhances theoretical understanding of the sustainability–performance relationship and provides a stronger foundation for future research examining internal firm drivers of sustainability-related outcomes.

5.3. Practical Implications

From a governance–managerial perspective, the findings provide several actionable implications for decision-makers in food processing firms. The results indicate that sustainability contributes to financial performance most effectively when it is strategically integrated into strategies and thus core organizational processes and supported by a sustainability-oriented organizational culture. Managers should therefore prioritize the development of a clearly defined sustainability strategies that are aligned with the firm’s vision and business policy, thus also overall business objectives, which allows the firm to provide adequate resources and their appropriate allocation, and direct the firm towards the correct operational decision-making, i.e., allocation of implementation tasks. Treating sustainability as a compliance-driven or normative symbolic activity should only be a starting point for properly embedding sustainability considerations into strategic management planning, investment decisions, and performance management systems.

The findings further highlight the importance of organizational culture in supporting sustainability implementation. Managers should actively promote sustainability-oriented values, encourage employee engagement in sustainability initiatives, and ensure that sustainability responsibilities are integrated across organizational functions. This may include establishing dedicated sustainability roles, incorporating sustainability into employee educational and training programs, and aligning incentives with sustainability objectives. Such measures can strengthen organizational capabilities and improve the effectiveness of sustainability strategies.

Importantly, the results suggest that sustainability-oriented vision and business policy, while predominant for signaling commitment and providing strategic directions, are not sufficient on their own to direct improvement in financial performance. Managers should therefore ensure that governance-related sustainability commitments are translated into concrete organizational strategies practices and supported by appropriate structures and operational processes. This requires moving beyond declarative commitments toward strategic and practical implementation, and with a strong organizational culture continuous integration of sustainability into everyday organizational activities.

From an industry and policy perspective, the findings highlight the importance of supporting firms in developing internal organizational capabilities for sustainability management. Policymakers and industry associations may contribute by providing guidance, training, and institutional support that enable firms to integrate sustainability into their strategic and, thus, operational organizational systems. Overall, the study provides practical guidance for firms seeking to directly enhance financial performance by demonstrating that financial benefits are most likely to emerge when sustainability is treated as a strategic capability rather than solely as a formal or symbolic commitment.

5.4. Limitations and Future Research

Despite the theoretical and empirical contributions of this study, several limitations should be acknowledged. The study relies on cross-sectional survey data collected at a single point in time, which limits the ability to draw causal conclusions and to capture the dynamic nature of sustainability governance, management and financial performance. Future research could employ longitudinal research designs to examine how sustainability vision and business policy, sustainability-oriented organizational culture, and sustainability strategies develop over time and how their effects on financial performance evolve.

Also, the study is based on self-reported data provided by firm owners or authorized representatives of mainly micro and small firms. Although such respondents are well positioned to evaluate firm development, practices and performance, perceptual measures may be subject to potential response bias. Future research could strengthen the validity of findings by combining survey-based measures with objective financial indicators, external sustainability ratings, or archival data.

Next, the empirical analysis focuses exclusively on food processing firms operating in Slovenia. While this industry and national context provide a relevant setting due to the resource-intensive nature of food processing and increasing sustainability pressures, the generalizability of the findings may be limited. Future studies could replicate the proposed research model in other industries and national contexts or conduct cross-country comparative studies to examine how institutional environments influence the relationship between sustainability governance, organizational culture, management and financial performance.

Finally, this study focuses on firm financial performance as the primary outcome variable. Future research could adopt a more comprehensive performance perspective by simultaneously examining financial, environmental, and social performance outcomes. Such an approach would provide deeper insight into the mechanisms through which sustainability governance and management contribute to overall organizational performance and would help clarify potential synergies or trade-offs among different dimensions of sustainability.

6. Conclusions

This study examined how key internal components of sustainability governance, organizational culture, and management directly influence firm financial performance in the food processing industry. By distinguishing between sustainability-oriented vision and business policy, sustainability-oriented organizational culture, and sustainability strategies, the study addressed an important gap in understanding the internal organizational mechanisms linking sustainability and firm financial performance. Using empirical evidence from food processing firms operating in Slovenia, the EU state, the study provides industry-specific insights into how sustainability governance and management are embedded within organizational systems. The findings demonstrate that sustainability governance and management processes are a multidimensional organizational phenomenon in which different components play distinct roles. Sustainability strategies emerge as the most important direct driver of firm financial performance, highlighting the importance of integrating sustainability into core strategic organizational planning and decision-making processes. Sustainability-oriented organizational culture also directly contributes positively to firm financial performance by supporting effective implementation of sustainability vision, business policy and strategies via practices, and reinforcing sustainability-related behaviors across the organization. In contrast, sustainability-oriented vision and business policy primarily represent formal and normative symbolic commitments that provide strategic direction but do not directly enhance financial performance unless supported by effective strategic integration and organizational alignment. These findings contribute to sustainability governance and management literature by demonstrating that financial benefits arise primarily from sustainability practices that are strategically integrated into a firm’s strategies and culturally embedded, rather than from normative symbolic commitments alone. This distinction provides a more refined understanding of the organizational mechanisms through which sustainability creates financial value. From a practical perspective, the study highlights the importance for managers of embedding sustainability into strategic processes and organizational culture to directly achieve long-term financial resilience and competitiveness. Overall, the study reinforces the view that sustainability represents not only an ethical or regulatory obligation but also a strategic organizational capability that can enhance long-term financial performance when effectively implemented.

Author Contributions

Conceptualization, D.K., T.Š. and M.R.; methodology, D.K., T.Š. and M.R; validation, D.K., T.Š. and M.R.; formal analysis, D.K., T.Š. and M.R.; investigation, D.K., T.Š. and M.R.; data curation, D.K., T.Š. and M.R.; writing—original draft preparation, D.K., T.Š. and M.R.; writing—review and editing, D.K., T.Š. and M.R.; visualization, D.K., T.Š. and M.R.; supervision, D.K., T.Š. and M.R. All authors have read and agreed to the published version of the manuscript.

Funding

The corresponding and leading authors report financial support from the Slovenian Research Agency (research core funding No. P5–0023 “Entrepreneurship for Innovative Society” and research core funding No. BI-BA/24-25-001 “Sustainable development goals for the sustainable development of the company”).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The original contributions presented in this study are included in the article. Further inquiries can be directed to the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Ansell, C.; Sørensen, E.; Torfing, J. Co-creation for sustainability: The UN SDGs and the power of local partnerships. Emerald Publishing, 2022.

- Abd-Elmabod, S.K.; Muñoz-Rojas, M.; Jordán, A.; Anaya-Romero, M.; Phillips, J.D.; Jones, L.; Zhang, Z.; Pereira, P.; Fleskens, L.; van der Ploeg, M.; et al. Climate change impacts on agricultural suitability and yield reduction in a Mediterranean region. Geoderma 2020, 374. [CrossRef]

- Arian, A.; Sands, J.; Tooley, S. Industry and Stakeholder Impacts on Corporate Social Responsibility (CSR) and Financial Performance: Consumer vs. Industrial Sectors. Sustainability 2023, 15, 12254. [CrossRef]

- Bai, C.; Sarkis, J. Green information technologies and systems for innovation. Technological Forecasting and Social Change 2020, 153, 119918.

- Carrillo-Labella, R.; Fort, F.; Parras-Rosa, M. Motives, Barriers, and Expected Benefits of ISO 14001 in the Agri-Food Sector. Sustainability 2020, 12, 1724. [CrossRef]

- Coppola, A.; Ianuario, S. Environmental and social sustainability in Producer Organizations’ strategies. Br. Food J. 2017, 119, 1732–1747. [CrossRef]

- Coteur, I.; Marchand, F.; Debruyne, L.; Lauwers, L. Structuring the myriad of sustainability assessments in agri-food systems: A case in Flanders. J. Clean. Prod. 2019, 209, 472–480. [CrossRef]

- Dreichuk, M.; Sytnyk, Y. CREATING A SUSTAINABLE CORPORATE CULTURE IN THE CONTEXT OF GREEN AND DIGITAL ECONOMY. Green, Blue Digit. Econ. J. 2024, 5, 16–21. [CrossRef]

- Cupertino, S.; Vitale, G.; Riccaboni, A. Sustainability and short-term profitability in the agri-food sector, a cross-sectional time-series investigation on global corporations. Br. Food J. 2021, 123, 317–336. [CrossRef]

- Ermenc, A.; Klemenčič, M.; Buhovac, A.R. Sustainability Reporting in Slovenia: Does Sustainability Reporting Impact Financial Performance? In Sustainability Reporting in Central and Eastern European Companies; Horváth, P.; Pütter, J.M.; Eds.; Springer: Cham, Switzerland, 2017; pp. 181–197.

- Bertini, M.; Pineda, J.; Petzke, A.; Izaret, J.-M. Can We Afford Sustainable Business? MIT Sloan Management Review 2021, 63, 25–33.

- Burawat, P. The relationships among transformational leadership, sustainable leadership, lean manufacturing and sustainability performance in Thai SMEs manufacturing industry. Int. J. Qual. Reliab. Manag. 2019, 36, 1014–1036. [CrossRef]

- Gangi, F.; D'Angelo, E.; Daniele, L.M.; Varrone, N. The impact of corporate governance on social and environmental engagement: what effect on firm performance in the food industry?. Br. Food J. 2020, 123, 610–626. [CrossRef]

- Calabrese, A.; Costa, R.; Gastaldi, M.; Ghiron, N.L.; Montalvan, R.A.V. Implications for Sustainable Development Goals: A framework to assess company disclosure in sustainability reporting. J. Clean. Prod. 2021, 319. [CrossRef]

- Fadeyev, V.; Balatskyi, A.; Shapoval, S.; Galka, A. Resource-Saving Innovative Solutions for the Agricultural Sector of the Economy. Bulletin of the Transilvania University of Braşov, Series II: Forestry, Wood Industry, Agricultural Food Engineering 2022, 14, 9–16.

- Hameed, I.; Hyder, Z.; Imran, M.; Shafiq, K. Greenwash and green purchase behavior: an environmentally sustainable perspective. Environ. Dev. Sustain. 2021, 23, 13113–13134. [CrossRef]

- Zhang, Y. A path to sustainable development of agri-industries : Analysis of agriculture 5.0 versus industry 5.0 using stakeholder theory with moderation of environmental policy. Sustain. Dev. 2024, 32, 4829–4843. [CrossRef]

- Mont, O.; Lehner, M.; Dalhammar, C. Sustainable consumption through policy intervention—A review of research themes. Front. Sustain. 2022, 3. [CrossRef]

- Abualfaraa, W.; Salonitis, K.; Al-Ashaab, A.; Ala’raj, M. Lean-Green Manufacturing Practices and Their Link with Sustainability: A Critical Review. Sustainability 2020, 12, 981. [CrossRef]

- Martens, M.L.; Carvalho, M.M.D. Sustainability assessment in project management: an exploratory study of the food sector. Production 2016, 26, 782–800.

- Mao, W.; Yang, Q.; Zhang, D.; Li, X. The influence of agricultural industrial policy on non-grain production of cultivated land: A case study of the “one village, one product” strategy implemented in Guanzhong Plain of China. Land Use Policy 2022, 108, 105579.

- Mastos, T.; Gotzamani, K. Sustainable Supply Chain Management in the Food Industry: A Conceptual Model from a Literature Review and a Case Study. Foods 2022, 11, 2295. [CrossRef]

- Wandosell, G.; Parra-Meroño, M.C.; Alcayde, A.; Baños, R. Green Packaging from Consumer and Business Perspectives. Sustainability 2021, 13, 1356. [CrossRef]

- Dorda, B.; Shtembari, E. A new perspective on organizational culture in emergency situations. International Journal of Business Research and Management 2020, 11, 16–26.

- Ali, H.; Yin, J.; Manzoor, F.; An, M. The impact of corporate social responsibility on firm reputation and organizational citizenship behavior: The mediation of organic organizational cultures. Front. Psychol. 2023, 13, 1100448. [CrossRef]

- Assoratgoon, W.; Kantabutra, S. Toward a sustainability organizational culture model. J. Clean. Prod. 2023, 400. [CrossRef]

- Vacchi, M.; Siligardi, C.; Demaria, F.; Cedillo-González, E.I.; González-Sánchez, R.; Settembre-Blundo, D. Technological Sustainability or Sustainable Technology? A Multidimensional Vision of Sustainability in Manufacturing. Sustainability 2021, 13, 9942. [CrossRef]

- Jung, J.; Kim, S.J.; Kim, K.H. Sustainable marketing activities of traditional fashion market and brand loyalty. J. Bus. Res. 2020, 120, 294–301. [CrossRef]

- Lloret, A. Modeling corporate sustainability strategy. J. Bus. Res. 2016, 69, 418–425. [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 2018, 10, 494. [CrossRef]

- Lopes, J.M.; Gomes, S.; Pacheco, R.; Monteiro, E.; Santos, C. Drivers of Sustainable Innovation Strategies for Increased Competition among Companies. Sustainability 2022, 14, 5471. [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest. 2015, 5, 210–233. [CrossRef]

- Kopecká, N. A literature review of financial performance measures and value relevance. In The Impact of Globalization on International Finance and Accounting: Proceedings of the 18th Annual Conference on Finance and Accounting (ACFA); Springer International Publishing: Cham, Switzerland, 2018; pp. 385–393.

- Barney, J.B. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120.

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [CrossRef]

- Scott, W.R. Institutions and Firms: Ideas, Interests, and Identities, 4th ed.; Sage Publications: Thousand Oaks, CA, USA, 2014.

- Guelph Food Technology Centre. (GFTC); Ontario Centre for Environmental Technology Advancement (OCETA). Raising the Bar for Sustainability Performance in Ontario’s Food & Beverage Processing Industry: Phase 1 Final Report – Appendices; Guelph Food Technology Centre: Guelph, ON, Canada, 2010.

- Duh, M.; Štrukelj, T. Incorporating Sustainability into Strategic Management for Maintaining Competitive Advantage: The Requisite Holism of Process, Institutional, and Instrumental Dimensions. In Strategic Management and International Business Policies for Maintaining Competitive Advantage; De Moraes, A.J., Ed.; IGI Global: Hershey, PA, USA, 2023; pp. 189–218.

Figure 1.

Conceptual model of sustainability governance and management components and firm financial performance in the food processing industry.

Figure 1.

Conceptual model of sustainability governance and management components and firm financial performance in the food processing industry.

Table 1.

Descriptive statistics for the construct Sustainability-oriented vision and business policy.

Table 1.