Submitted:

25 February 2026

Posted:

27 February 2026

You are already at the latest version

Abstract

This study assesses how a country’s digitalization impacts sustainability indicators as measured by unmonitored environmental, social and governance (ESG) risks, which serve as a proxy for the development of financial technology (FinTech). The study employs a cross-country approach using data for up to 163 countries, going beyond the firm-level focus of previous studies. The DiGiX Digitalization Index and the ICT Development Index are used to measure digitalization, while pillar-level indicators and Sustainalytics ESG country risk scores are used to assess ESG indicators. With evidence of nonlinear, threshold-type effects at higher levels of digitalization, the regression results suggest a strong negative correlation between digital maturity and ESG risk. Different country typologies are further identified using unsupervised cluster analysis, which reveals a continuous digital and ESG gradient in environmental, social and governance aspects. The analysis proves digitalization serves as a systemic enabler of ESG risk management by strengthening data availability, governance capacity and policy enforcement. These findings provide policy-related guidance for coordinating digitalization strategies in line with the Sustainable Development Goals.

Keywords:

digitalization

; FinTech

; sustainable development

; cross-countries analysis

; ESG risks

; cluster analysis

1. Introduction

A review of the newest literature indicates that digitalization serves as both a proxy and a primary driver of FinTech development, fundamentally altering financial intermediation, payment systems, credit allocation, and asset management. Digital technologies reduce transaction costs, facilitate the emergence of new business models, and accelerate data processing and risk assessment, thereby transforming the production, distribution, and consumption of financial services [1,2,3]. At the same time, research highlights the close integration of digitalization with sustainability agendas. Fintech supports greener and more inclusive growth by mobilizing capital inflows for low-carbon projects, raising the traceability of environmental impacts, and broadening access to financial services for broader groups of populations [4,5,6,7].

Digital tools facilitate the collection of granular environmental, social, and governance (ESG) data, enable automated disclosure, support real-time monitoring of environmental performance, and strengthen internal control systems [8,9]. These capabilities advance corporate governance reforms and promote more responsible investment practices. In addition, digitalization encourages green and technological innovation, enhances resource efficiency, and enables the development of sustainable business models, particularly in sectors with high innovation capacity and in economies with advanced digital infrastructure [10,11]. All the same, the literature also identifies new ESG-related risks associated with rapid fintech adoption and widespread digitalization. Several studies suggest that digital transformation may yield non-linear effects, with performance improvements plateauing or reversing as digitalization becomes excessive, potentially leading to diminishing returns or increased risk and reduced return on assets [12,13,14].

The majority of empirical evidence focuses on the firm or company level. Existing studies investigate the impact of digitalization and fintech adoption on individual firms’ environmental performance, innovation output, ESG scores, internal control quality, and market valuation. These studies frequently conclude that digital capabilities enhance transparency, mitigate agency problems, and facilitate greener investment decisions, particularly in firms with robust governance structures or government ownership. Conversely, weak governance tends to diminish these benefits. Sectoral analyses further indicate that the positive ESG effects of digitalization are more pronounced in knowledge-intensive and service sectors compared to heavy industry, and are contingent upon firms’ absorptive capacity and organizational resilience. In contrast, the governmental or country-level dimension is considerably less developed in the existing literature.

The objective of the current research is to enhance understanding of how a country’s degree of digitalization, serving as a proxy for fintech development, influences its sustainability performance in terms of ESG risk profile. By shifting the focus from the company level to the governmental level, this study aims to deeper the understanding of the topic on the level of individual country, providing a possibility of different regions comparison and evidence-based policy recommendations.

By expanding the analysis of the connections between digitalization and sustainability from the business level to the national level, this study contributes to the body of knowledge on digital innovation and green development. It considers digitalization as a system-level capability integrated into national innovation and governance institutions rather than as a stand-alone technological force. The study provides evidence that complementarities between digital infrastructure, institutional quality, and governance capability lead to sustainability improvements by experimentally showing a strong and non-linear relationship between digital maturity and unmanaged ESG risk across countries from different regions.

This article is structured as follows: Section 2 provides a systematic literature review on digitalization, financial technology, sustainable development and ESG, identifying research gaps at the country level. This is followed by a description of the data sources, variables and empirical methodology, including the regression framework and cluster analysis. The empirical results, detailing both regression and clustering findings on overall ESG risk and its dimensions, are followed by a discussion within a theory-driven framework, highlighting the implications for innovation, institutional governance and green development. Finally, the main conclusions are summarized, policy implications are outlined and directions for future research are identified.

2. Systematic Literature Review on Digitalization Role in Economic Development

As a new financial model incorporating digital technologies, FinTech can catalyze the green, low-carbon, and circular development More effectively than traditional finance. FinTech companies promote the efficiency of carbon emissions through green finance and green technological innovation [15]. Strong and effective development of digital financial solutions stimulates the decarbonization of the economy and the transformation of conventional economic activities into more sustainable practices [16,17]. Thus, FinTech stimulates the development of the financial system, promotes technological innovation, and enhances environmental management [18].

Authors employed updated PRISMA 2020 systematic literature review method by Page et al. (2021) [19] to identify relevant publications on the selected topic. Selected publications were further used for content analysis to investigate main relations identified between digitalization of financial sector and its impact on sustainable economic development.

Authors used two databases – SCOPUS and Web of Science as the most prominent source of publications in the field of research. Initial search of literature sources was done on 20 December, 2025. Search details for the selected databases are shown in Table 1.

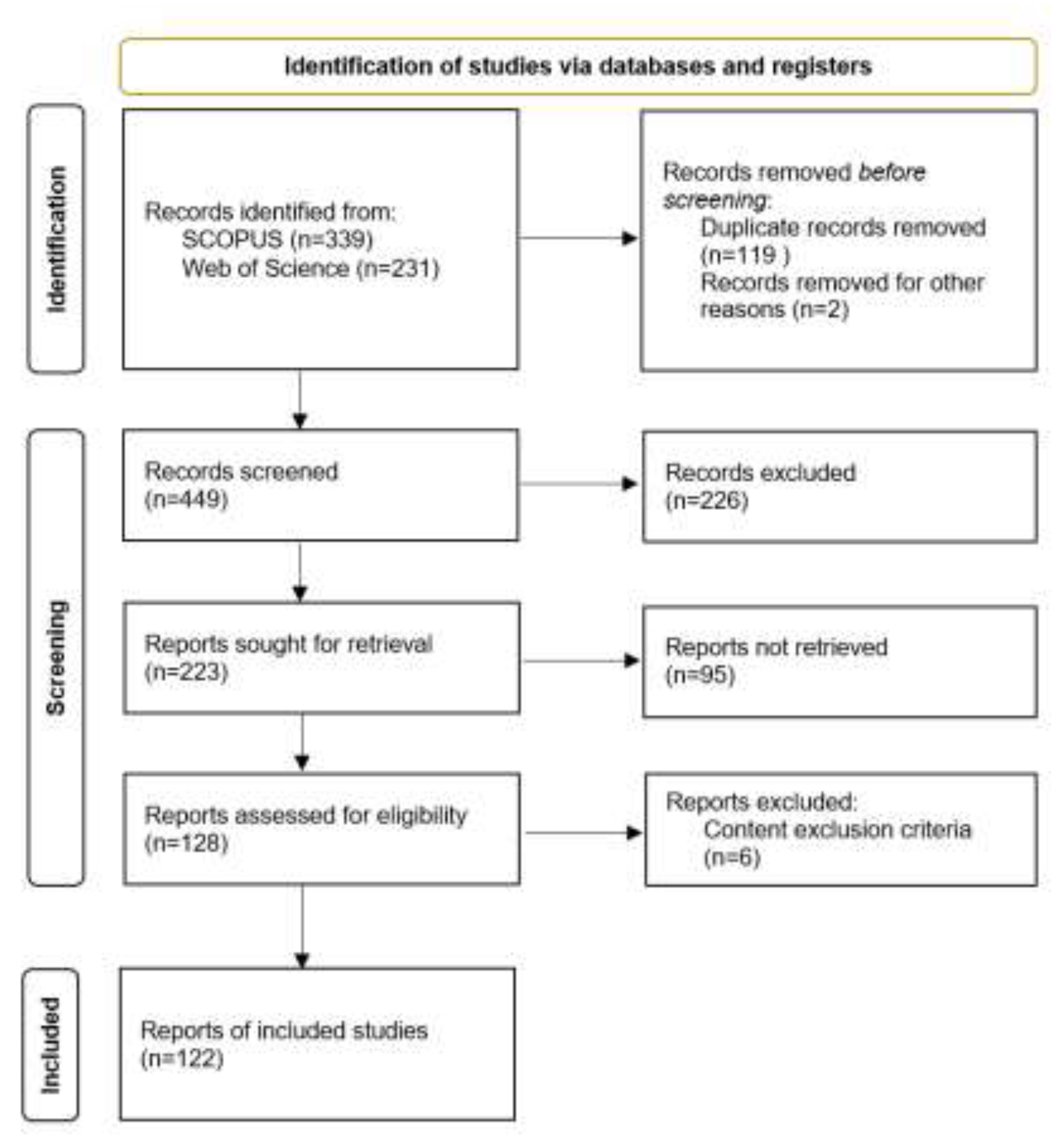

As Figure 1 indicates the authors used a set of 122 publications for detailed literature review to assess how digitalization of finances impacts sustainable development.

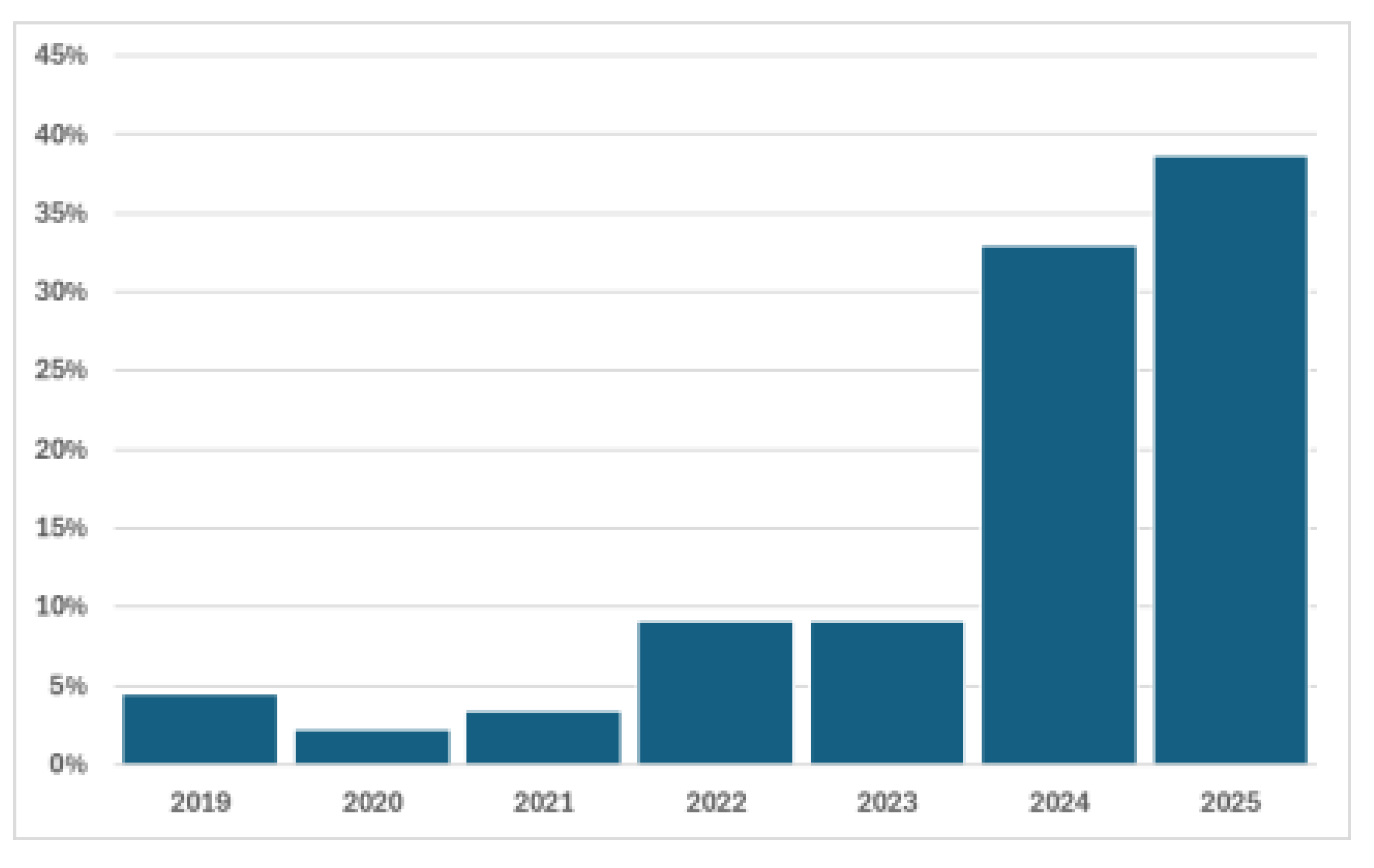

Following PRISMA methodology authors excluded publications with no clear objectives or aim of the research as well as publications that were not clearly related to sustainable development. In the screening part the authors were unable to obtain full texts of 95 publications with reason of being behind so called ‘pay-wall’. In the last step of screening authors excluded 6 publications based on two main reasons – publication was focused on Islamic finance or publication was not related to the research topic in general. After conducting the full selection process, the authors obtained 122 publications, which served as the basis for further content analysis. Figure 2 shows the relative distribution of the selected 122 publications by year. The reports that include content analysis and keyword network mapping are very recent, with more than 70% published in 2024 and 2025, suggesting that the selected research topic is new and little studied in academia.

During the content analysis of the selected publications, the authors’ main goal was to identify the most important areas of the studies. After analyzing the publications on the relationship between financial digitalization and sustainable development, the authors divided them into five categories, according to the areas of research. Categories of the publications on the topic are shown in Table 2.

Ecological factors as the key aspect of sustainable development is main topic for many publications. In this category there are publications related to blockchain technology and different aspects of it. Shu et al., 2022 [20] researches systems that can impact carbon emission levels while Basdekidou and Papapanagos, 2024 [21] research general blockchain adoption and its inclusion into ESG and DEI performance. Extensive bibliometric analysis [22] focusing on technology impact on more efficient (renewable) energy usage by adopting artificial intelligence solutions and restoration of degraded areas is also provide [23]. CO2 reduction is another topic of research for several authors from different aspects – how digital finance can reduce carbon emissions [24], fintech development role in promoting carbon neutrality [25] and general intersection of digital development and its relation to environmental sustainability [26]. Supporting sustainable customer choices is also one of the findings for further FinTech research identified by Hasan et al. 2024. [27].

Social inclusion is extensively researched in various articles – achieving SDG goals are often referenced as drivers for the researches, also FinTech development [28] mentioned as potential driver for achieving these goals. Gender equality promotion by financial inclusion in South Asia region is researched by Dhar et al., 2025 [29], additional aspect of rural empowerment is researched by Hoeyi et al., 2025 [30] and potential transformation of economic activity towards more sustainable approaches by adopting financial technologies is researched by Hasan et al., 2024 [31]. FinTech development [32] and financial inclusion [33] is mentioned as emerging field of research when it comes to income inequality and poverty reduction. It is identified that in general digital financial inclusion does have relations to more innovative, sustainable economic growth [34].

Economic development and digitalization – relations between financial technology and natural resource conversion rate and capital availability is described by Xie and Huang, 2024 [35]. Stable economic development is key for economic growth, reduction of inequality as one of impact factors is researched by Kumar et al., 2025 [36]. Framework of 8 domains including financial empowerment and social inclusion as well as technology adoption is developed and described by Munarso et al., 2025 [37] that give insights into potential rural economic transformation. At the same time FinTech business models and companies developing such solutions proved to be very adaptive to increase in scale very rapidly [38]. ESG aspect – specifically ESG risks are researched and described by evaluating and comparing ESG risk impact on S&P500 and Nasdaq100 companies and their valuations indicating relations between the size of the company and ESG risk scores [39].

Regulatory aspect is considered in different ways in line with technological development of financial solutions – need for more detailed regulations and consumer protection is described by Rambaud and Gazquez, 2022 [40], while governance mechanisms in the era of Artificial Intelligence is studied by Pashang and Weber, 2023 [41]. Role of regulatory institutions and its openness to new technologies is described by Campanella et al., 2025 [42], indicating positive impact of ‘sand-boxes’ for new product adoptions. General need for digitalization policies [43] and performance tracking [44] methodologies now can be interpret as an integral part for increased potential of sustainable development.

New technology development and innovative [45] approaches in traditional financial industry are also being widely studied [46]. Digital literacy of employees as important impact factor to companies to adopt new solutions Cetindamar et al., 2024 [47], while Dery et al., 2017 [48] research indicates that general employee experience in digital environment leads to digital innovations in general and even create new entrepreneurial ecosystems [49]. Open banking is mentioned in several publications – as one of the drivers to developing new banking platforms [50], as well as consumer perception towards adoption of open banking solutions is measured by Chan et al., 2022 [51].

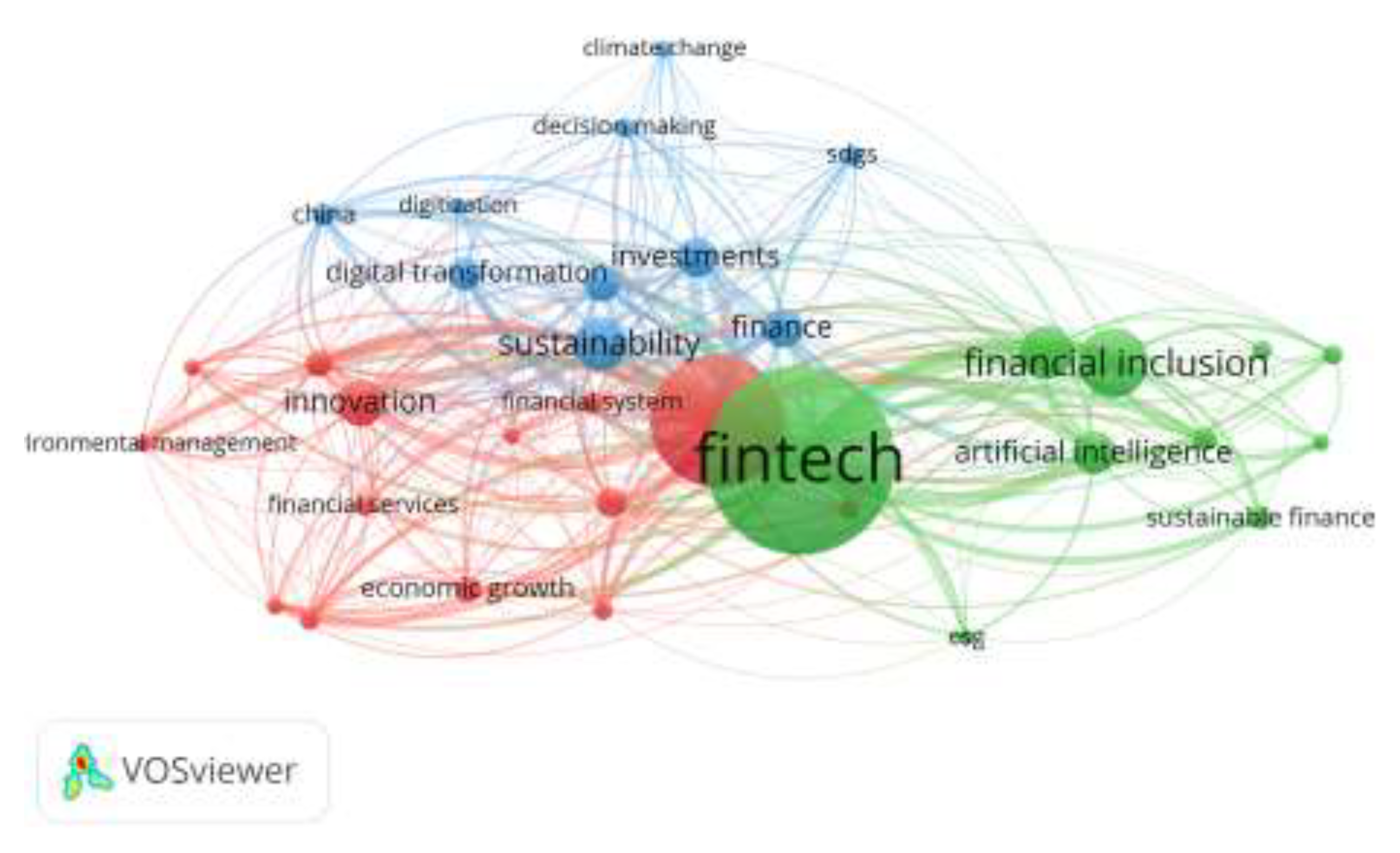

In addition to systematic review authors also created publication keyword and country of origin network maps by using automated tool VOSviewer. The keyword map, as shown in Figure 3, indicates three clusters of publications. Authors conclude automatic keyword analysis and mapping gives more general view on publications in comparison to manual content analysis. Automatic clustering indicates clusters of financial sector innovations and economic aspects (red cluster), digital development and technological aspect of financial sector (green cluster) and sustainability relations with financial technology developments (blue cluster).

Digital tools significantly improve the extent and quality of ESG disclosure The use of digital technologies helps to optimize all aspects of a company’s business processes, process large amounts of information in a more timely and efficient manner, thereby improving corporate governance efficiency [52]. Digital tools significantly improve the volume and quality of ESG disclosure, provide more detailed ESG data, automated information disclosure, real-time environmental monitoring, and better internal control systems, thus supporting corporate governance reforms and more responsible investments. Digitalization enhances ESG transparency in two strategic directions: green innovation and internal control quality. The positive effects of digitalization are more pronounced in manufacturing, high-tech companies, firms with greater analytical capabilities, and those in policy-supported industries. Companies in less-regulated industries use digital tools for compliance, e.g. AI is being used to generate standardized sustainability reports [53].

ESG disclosure is critical for investment decisions in sustainable investing, but its quality remains questionable due to human interference in the disclosure process. Therefore, IoT and blockchain technologies can help with ESG data collection. It can also guarantee security, transparency, and traceability in data collection and ESG report disclosure [54]. However, environmental performance metrics created with a machine learning approach have predictive validity, which aligns with solving proxy controversies [55]. Regulators should consider establishing international alliances to develop uniform ESG standards and regulatory tools [56].

Due to the growing generation of data and digitalization of assets, FinTechs are facing several challenges, including big data management, personal data protection, cybersecurity, and the privacy of customers’ financial data [57]. Digital transformation has driven the development of secure data storage solutions and trusted frameworks for sharing customers’ data within the FinTech ecosystem. A significant increase in the quantity of data processed by FinTechs has been observed recently; however, no corresponding changes have been noted in the level of transparency. The FinTechs are safeguarding themselves by using technical and legal terminology in their privacy statements, rather than the user comprehension required by the GDPR [58]. Current regional and national legal efforts are insufficient to address the challenges posed by the cross-border nature of the development and application of AI [59]. The rapid spread of FinTech and pervasive digitalization are creating new ESG-related risks: cyber risk, data privacy breaches, algorithmic bias and exclusion, greenwashing through unclear ESG valuation, and the risk that excessive digital investments undermine profitability and long-term sustainability.

It is important to determine how a country’s degree of digitalization, used as an indicator of the development of FinTech and AI, affects its sustainability and ESG risk profile. Moving from the company to the government level, an attempt is made to identify the mechanisms by which digitalization promotes or hinders sustainable development at the national level. Blockchain technology and financial literacy help shape a more inclusive and sustainable digital financial services [60]. Using blockchain technology in data management can improve its transparency and security. These aspects are critical for ensuring ESG compliance. Overall, ICT solutions can improve compliance and reporting efficiency, while the aforementioned technologies support financial institutions in achieving their sustainability and innovation goals, ensuring more efficient operations and corporate governance.

FinTech also stimulates investments in green technologies and projects, thus making access to financial resources easier. The data-driven capabilities of FinTech enhance transparency in financial decision-making [61]. FinTech can reduce information asymmetry and reduce transaction costs in the energy conservation and carbon reduction sectors [62]. Fintech has already shown potential for positive impact on the environment, although its further development requires constant alignment with green practices for maximum effectiveness [63]. Currently, the main FinTech challenges include technological scalability, regulatory compliance, and data privacy. FinTech innovations must be balanced with potential risks [64]. FinTech has democratized and eased companies and individuals access to financial services, particularly those who were traditionally excluded from the financial sector [65]. This development has facilitated a higher rate of participation in the financial sector, strengthening wealth accumulation and financial inclusivity [60].

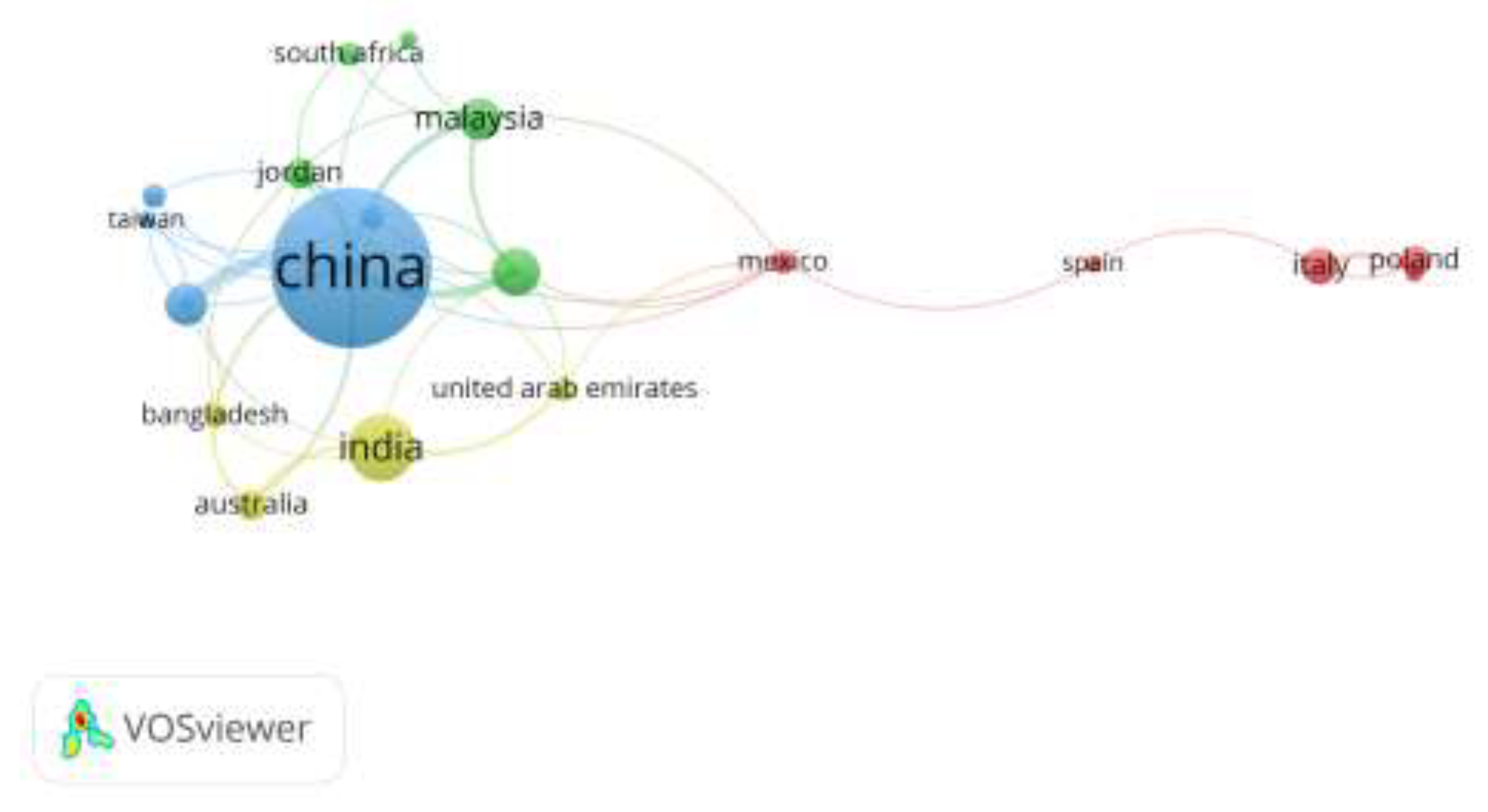

Network map based on authors countries of origin is also created. Figure 4 shows two powerful countries that occupy the leading positions in terms of the number of publications related to this topic, namely China and India. At the same time map clear indicates a lack of publications coming from European countries and their distant relations to other countries and its authors – a separate string of authors can be identified from Poland, Italy and Spain with minority of publication count from the selected dataset of publications.

Table 4 shows list of countries with number of publications and total citations of those publications. In the table included countries with five or more publications.

Figure 3 and Table 4 together highlight a strong geographical imbalance in the academic literature. The map of the publication network by country (Figure 3) shows that research activity is strongly concentrated in Asia-Pacific countries, especially China and India. This is also confirmed by Table 4, where China and India are the leaders in terms of the number of publications. In contrast, European countries in the network appear more fragmented with fewer publications overall, although Italy has the highest average citation rate. The findings indicate a clear research gap and highlight the need for more Europe-focused and comparative cross-country research on digitalization, financial technologies (FinTech) and sustainable development.

3. Methodology of the Research and Research Sample

To identify distinct groups of countries with similar configurations of fintech-related digitalization and ESG risks, this study applies cluster analysis at the country level. The analysis is used to uncover typologies of country performance that reflect diverse combinations of digital development and sustainability profiles as determined by the ESG Country Risk Rating.

To capture the nature of digitalization at the country level, the following indices are employed:

DiGiX – Digitalization Index (2024) [66]: The DiGiX index measures the overall level of digitalization by combining indicators related to digital infrastructure, connectivity, use of digital services, and digital skills. It provides a composite score for each country, with higher values indicating more advanced digital development.

ICT Development Index (IDI, 2025) [67]: the IDI is an internationally used composite measure of information and communication technology development, typically combining indicators of access (e.g. fixed and mobile networks), use (e.g. internet usage) and skills (e.g. basic education indicators). Higher scores reflect more advanced development.

ESG-related risks at the country level are measured using Sustainalytics’ ESG Country Risk Ratings [68] and the associated E (Enviromental), S (Social) and G (Governance) pillar indicators. Sustainalytics’ country ratings are designed to capture the extent to which a sovereign is exposed to, and manages, material environmental, social and governance risks. The overall rating summarizes a country’s unmanaged ESG risk on a continuous scale, with higher values indicating higher residual ESG risk. The score reflects both exposure to ESG issues (e.g. climate vulnerability, social conditions, institutional set-up) and the quality of policies and institutions that mitigate these risks. Where available, the authors additionally make use of selected sub-indicators from the Sustainalytics framework for descriptive profiling of clusters.

Before continuing with cluster analysis the authors are determining the linkage between digitalization and country ESG risk. In order to build the theoretical framework for the upcoming analysis let consider ESGi as Sustainalytics ESG Country Risk Rating for country i - interpreted as unmanaged ESG risk such that higher values indicate higher residual exposure after accounting for national risk management capacity. Let DiGiXi and IDIi denote two complementary proxies for country-level digital maturity: DiGiX capturing a broad multidimensional digitalization construct and IDI capturing access, use, and skills of technological solutions. The authors expect that digital capacity of the country reduces country`s unmanaged ESG risk through improved immeasurability and timeliness of ESG-relevant information, enhanced policy execution, supervision, and integrity of public administration, and better inclusiveness in digital finance and service delivery. So that higher level of digitalization is related to lower unmanaged ESG risk.

Digital transformation can reveal non-linear effects, the authors apply the standard way to test curvature via a quadratic extension:

To reduce sensitivity to heteroskedasticity that is typical in cross-country data, inference is based on heteroskedasticity-robust standard errors. A region-fixed effects robustness check is added.

The following hypotheses are formulated:

H1:

Countries exhibiting higher digitalization maturity are associated with lower levels of unmanaged ESG risk.

H2:

Each digitalization proxy retains explanatory power for ESG risk when controlling for the other, indicating that each proxy captures partially distinct aspects of digital maturity.

The dataset contains of 163 countries with non-missing ESG risk. Because DiGiX and IDI are not complete for all countries, the regressions use the maximum available sample for each specification (N = 86). Descriptive statistics is summarized in Table 5.

The correlation (presented in Table 6) indicates a strong digital–ESG gradient: higher digitalization is associated with lower ESG risk. At the same time, DiGiX and IDI are highly correlated, which anticipates collinearity effects in joint regressions.

The second part of the research aims to assess whether a country’s level of digitalization, as measured by the DiGiX index, is systematically associated with lower unmanaged ESG risk level. Moreover, it is necessary to determine whether the relationship between digitalization and ESG risk is consistent across ESG pillars, or if certain countries demonstrate pillar-specific deviations relative to their overall risk–digitalization alignment.

H3:

Countries with more advanced levels of digitalization are expected to exhibit significantly lower unmanaged risk, as indicated by the overall Country-Risk Score.

H4:

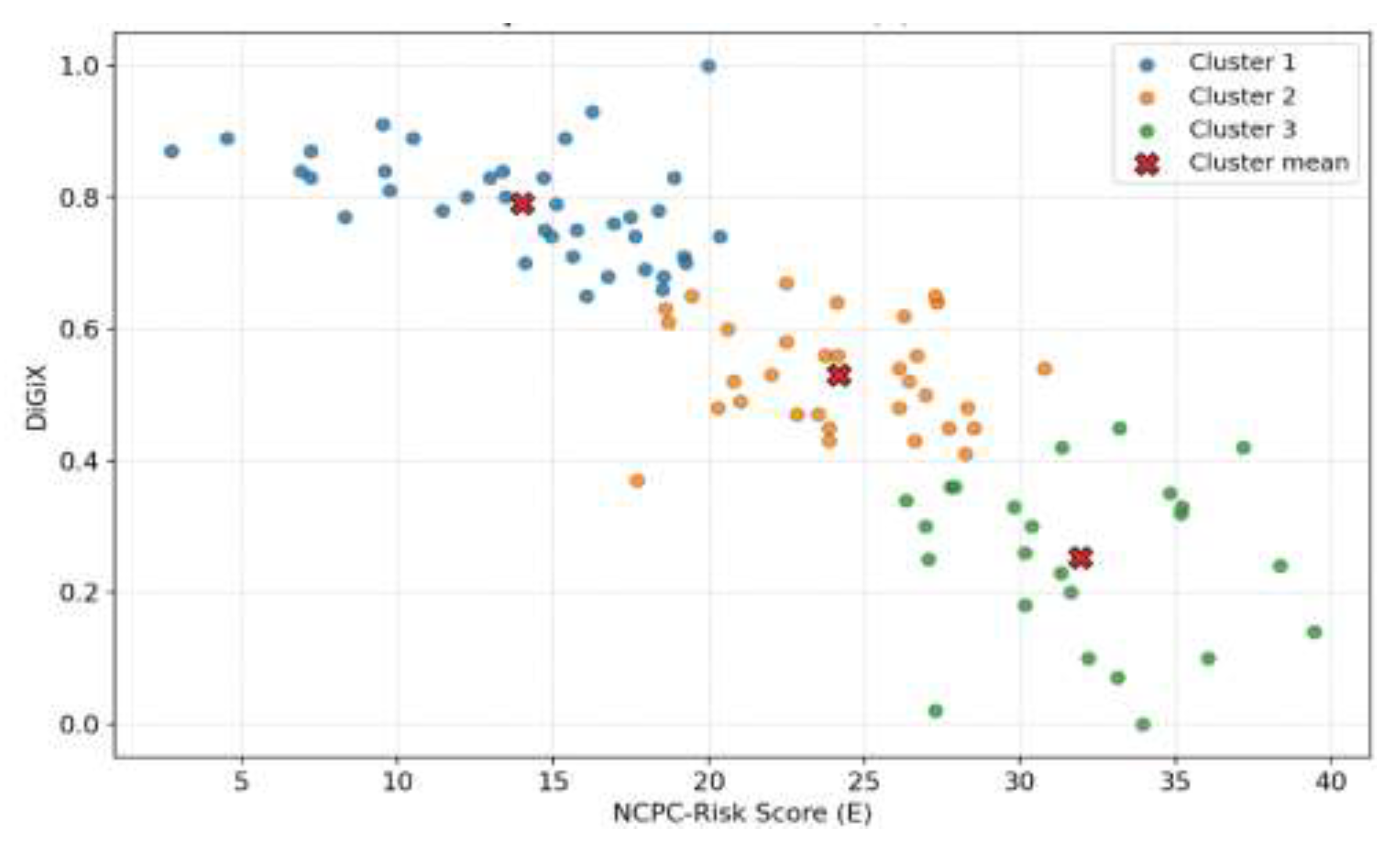

Countries with higher DiGiX level are expected to exhibit significantly lower unmanaged environmental risk, as measured by the NCPC-Risk Score (Environmental factors).

H5:

Countries with higher DiGiX score are expected to exhibit significantly lower unmanaged social risk, as indicated by the HC-Risk Score (Social factors).

H6:

Countries with more advanced levels of digitalization are expected to exhibit significantly lower unmanaged governance risk, as measured by the IC-Risk Score (Governance factors).

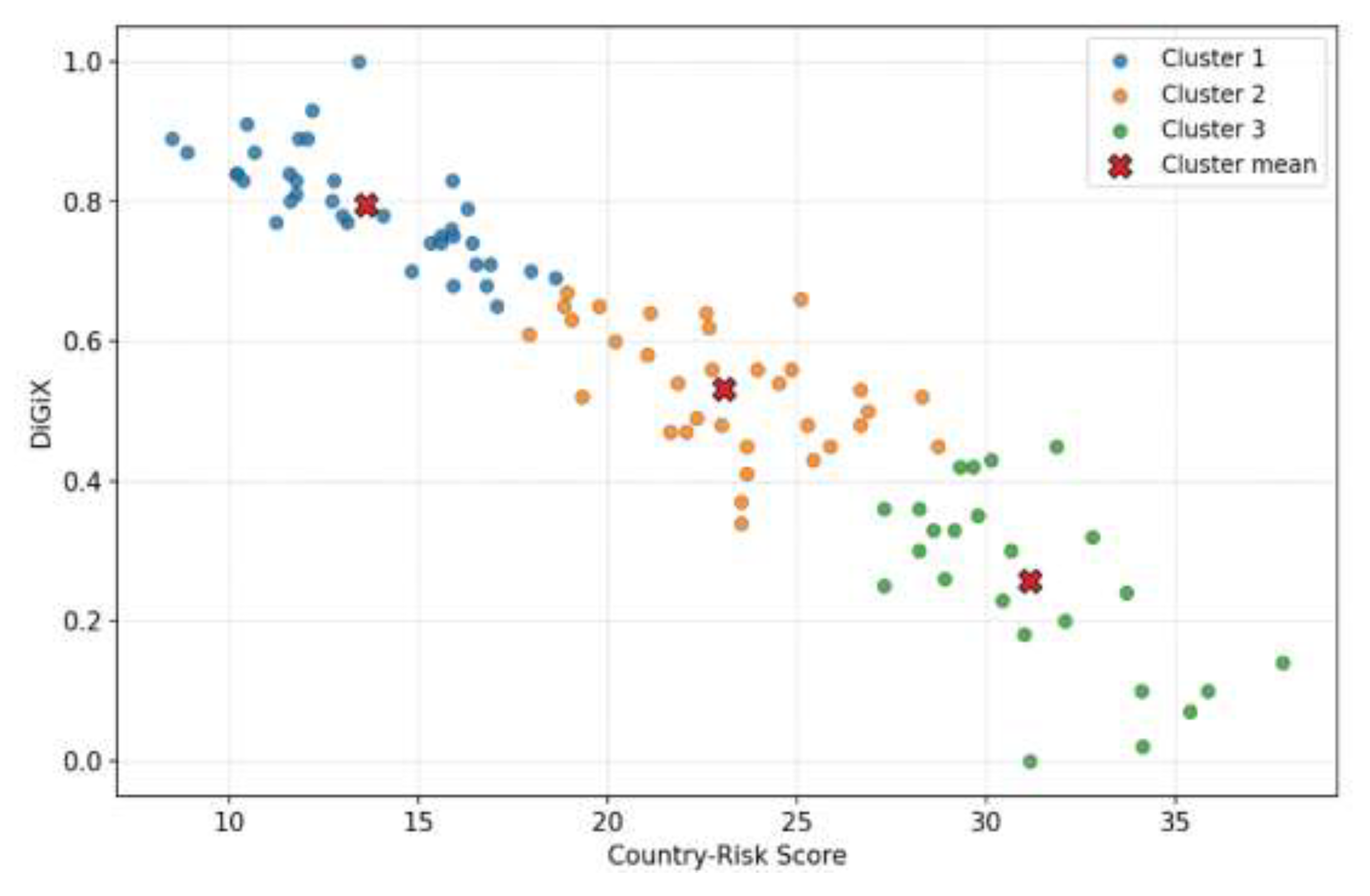

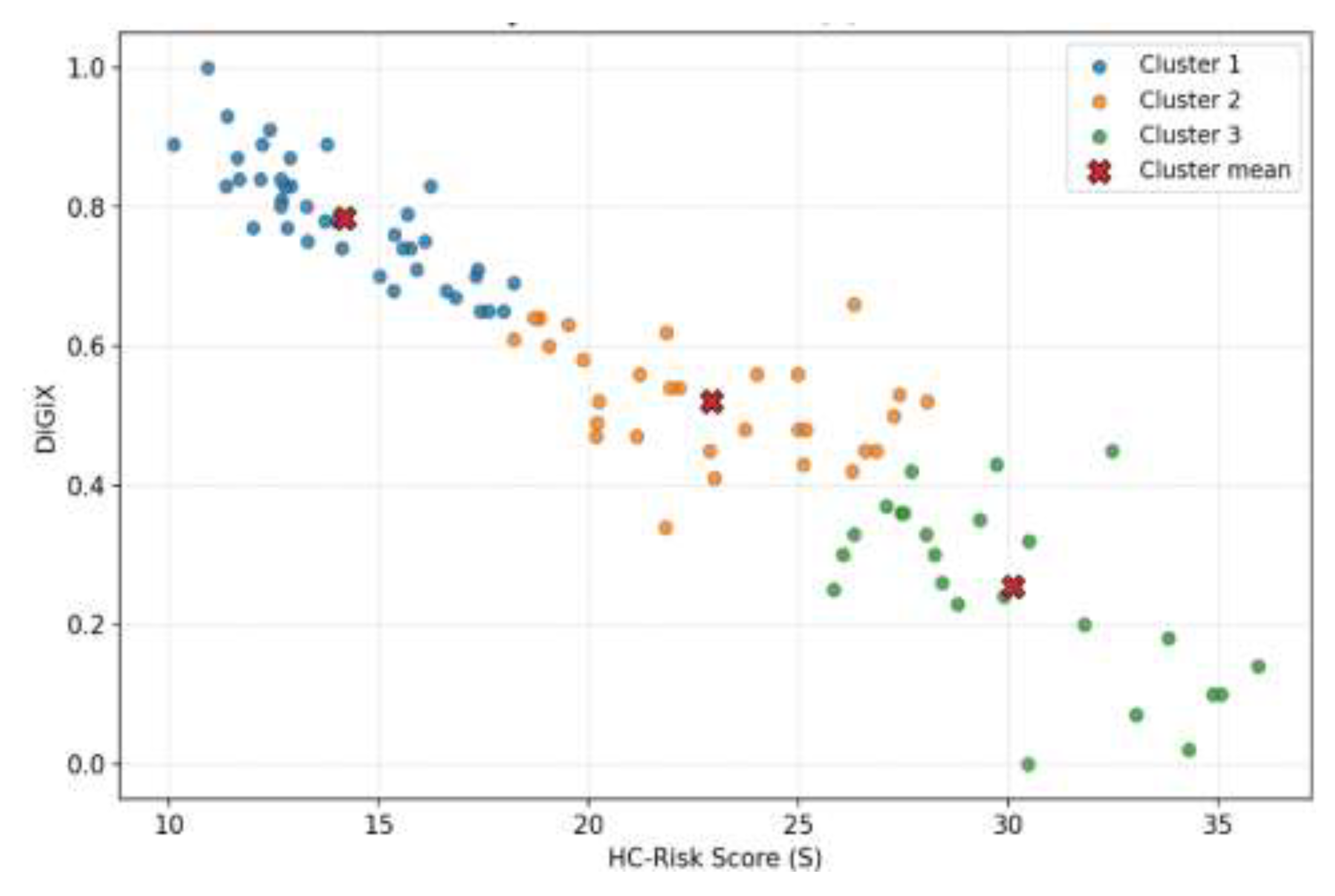

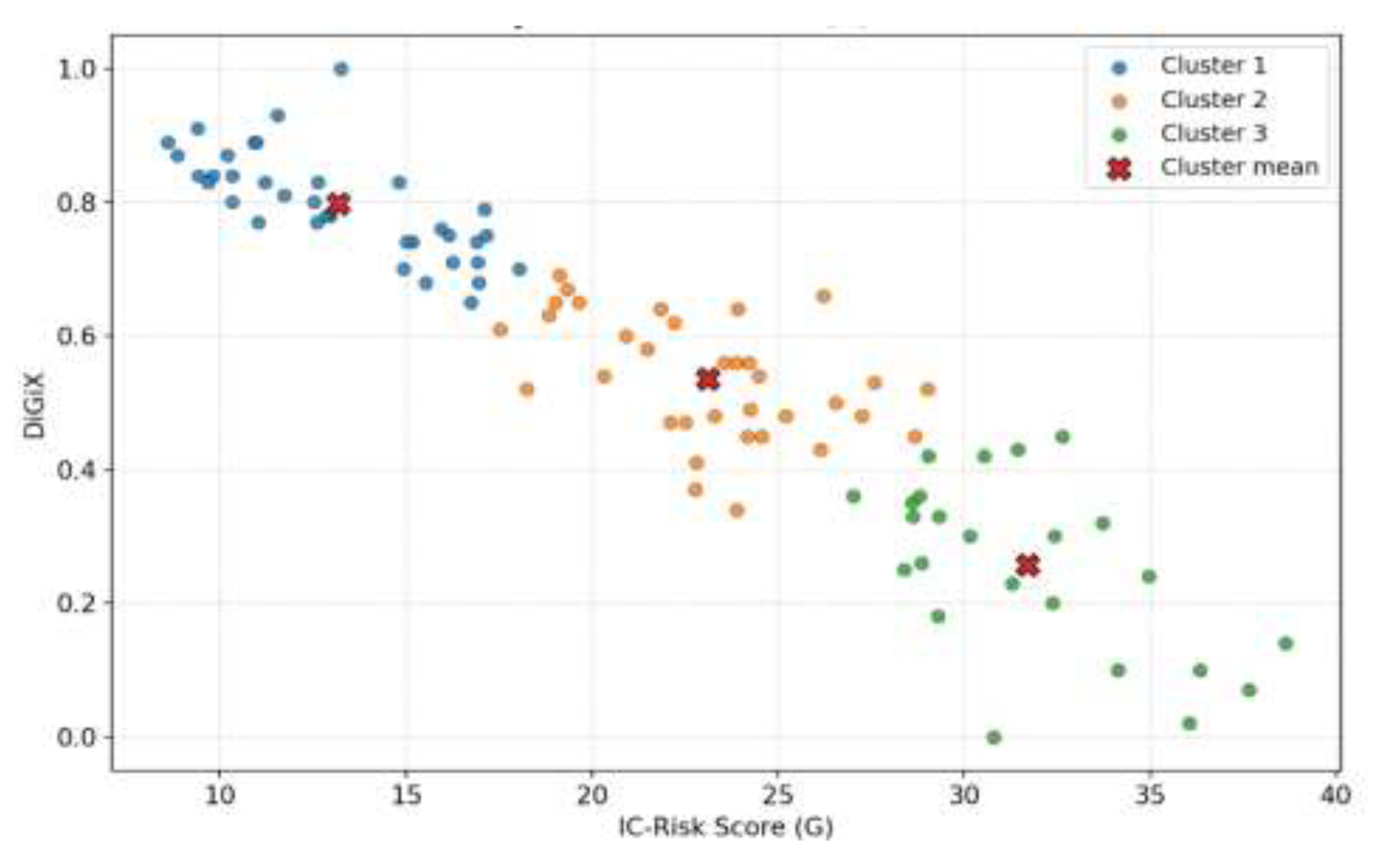

The authors use an unsupervised, comparative clustering approach to examine how country-level digitalization relates to unmanaged ESG risk. Four separate two-variable clustering exercises are run, each combining the DiGiX index with one risk measure: the overall Country-Risk Score, the Social pillar proxy (HC-Risk), the Environmental proxy (NCPC-Risk), and the Governance proxy (IC-Risk). Before clustering, both variables in each pairing are standardized using z-scores to ensure they are on the same scale and to avoid distortions from differences in variance. The authors apply k-means (with k = 3), chosen to produce intuitive low-, medium-, and high-risk groups while keeping clusters large enough for meaningful interpretation. To validate the results, the authors use one-way ANOVA to test whether the clusters differ significantly on both DiGiX and the corresponding risk score. As a robustness check, the authors also run Welch’s ANOVA for DiGiX in each analysis.

4. Results

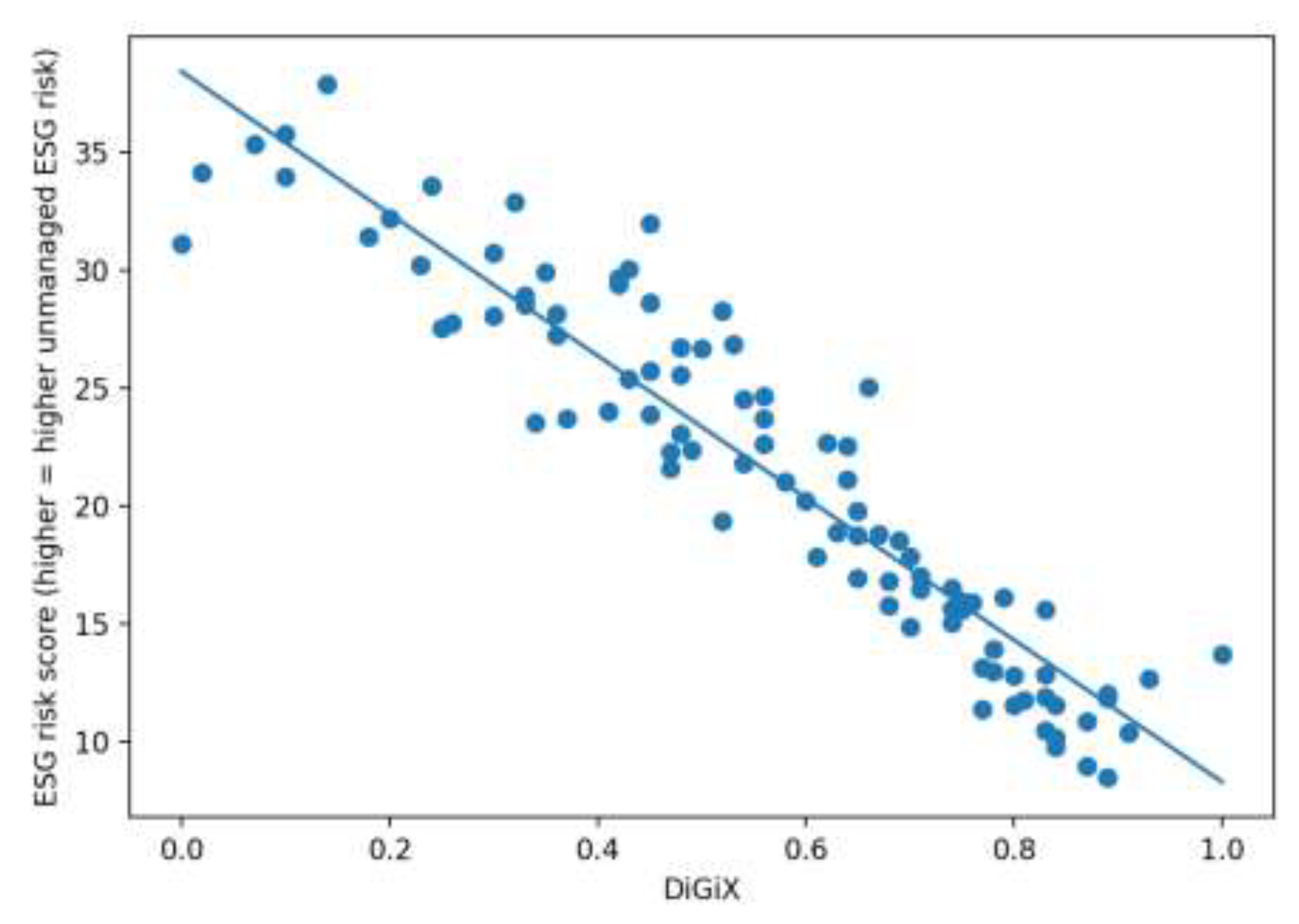

The results of the regression analysis are presented in Table 7. As shown, model (A) estimates the unconditional link between ESG risk and DiGiX. The results suggest that countries with higher levels of multidimensional digitalization tend to have significantly lower unmanaged ESG risk. The model fits the cross-country data well (R² = 0.88), which aligns with the pattern in Figure 5, where observations closely follow a downward-sloping trend.

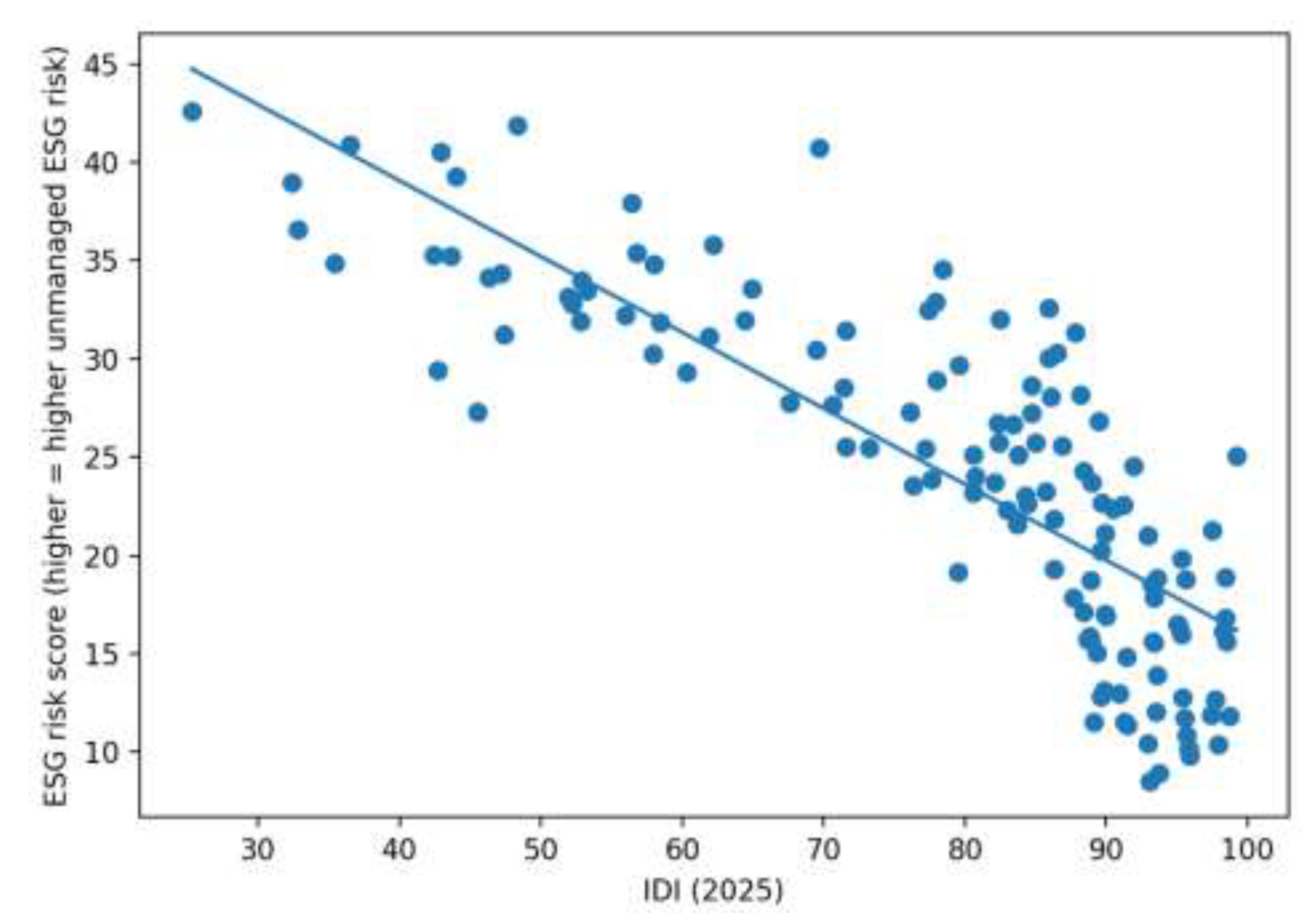

Model (B) repeats the baseline analysis using the IDI. The relationship remains negative and highly significant: a 0.1 increase in IDI is associated with roughly a 3.86 point decrease in ESG risk. Although the model fit (R² = 0.672) is lower than in Model (A), it is still strong and meaningful. Figure 6 also shows a clear downward trend, albeit with more dispersion than the DiGiX plot. This pattern supports the idea that DiGiX being a broader, multidimensional index captures institutional and ecosystem features more closely linked to unmanaged ESG risk, whereas the IDI reflects a narrower view of digital development.

Models (A2) and (B2) test whether the link between digitalization and ESG risk is strictly linear. For DiGiX, the negative and marginally significant quadratic term suggests that the decline in ESG risk becomes steeper as digitalization increases. This pattern is consistent with threshold type dynamics: once digitalization reaches a certain level, complementary capabilities (such as regulatory capacity, data integration, monitoring tools, and digital public services) scale more effectively, generating larger improvements in unmanaged ESG risk. For the IDI, the quadratic specification is also statistically supported, with a negative squared term. The coefficient pattern points to an inverted relationship, meaning that for most countries in the sample, the marginal effect of IDI on ESG risk is negative and becomes more pronounced at higher IDI levels.

Model (C) estimates the joint relationship using the complete case sample (N=86), matching the sample used in the clustering analysis. The DiGiX coefficient remains strongly negative and sizable. The IDI coefficient turns small and positive but remains statistically significant. This sign shift is best understood as a partial regression artifact arising from the high correlation between the two digitalization measures. When two highly overlapping indicators enter the model together, each coefficient reflects only the variable’s unique component after controlling for the other, which may not correspond to a meaningful theoretical construct on its own. Overall, the findings indicate that the digital-ESG relationship is robust and is primarily captured by DiGiX in this dataset, while IDI adds little explanatory value once DiGiX is included.

Table 8 presents the one way ANOVA results assessing whether mean values differ across the three clusters (k = 3), formed using k means on standardized variables (z scores). For each analysis, the ANOVA reports the F statistic, p value, and η² as an effect size indicator showing how much variance is explained by cluster membership. Levene’s test is also reported as a diagnostic for variance equality across clusters. Because Levene’s test indicates unequal variances for DiGiX in all cases, Welch’s ANOVA—robust to heteroskedasticity—was additionally performed. Welch’s ANOVA confirms that differences in DiGiX across clusters remain highly significant (Welch p values ≈ 10⁻²⁴).

Across all four ESG risk dimensions, the results reveal a clear and statistically significant pattern: countries in the lowest risk cluster consistently show the highest DiGiX values, while those in the highest risk cluster show the lowest. Cluster centroids remain stable across all analyses: approximately 0.79, 0.53, and 0.25, demonstrating a monotonic decline in digitalization capacity as unmanaged ESG risk increases. This pattern holds for each ESG pillar (environmental, social, and governance). The corresponding visual evidence is shown in the plots following Figure 7. Regionally, Europe displays a highly concentrated structure. The majority of European countries (26 out of 36) fall into Cluster 1, representing low unmanaged risk and high digitalization. This aligns with Europe’s generally strong performance on DiGiX, especially in advanced Western and Nordic economies. A smaller set of European countries (9 out of 36) are in Cluster 2, reflecting mid-range DiGiX and higher unmanaged risk. Only one European country, Ukraine, falls into Cluster 3, reflecting substantially higher unmanaged risk and comparatively low digitalization. The Asia Pacific region shows far greater diversity. The largest group (11 out of 28 countries) belongs to Cluster 2, a mid-risk, mid digitalization segment. This includes several large or rapidly developing economies. A notable advanced economy subgroup appears in Cluster 1. Cluster 3 is characterized by higher unmanaged risk and lower levels of digitalization and contains 9 out of 28 countries. Overall, the Asia Pacific distribution shows that digitalization differentiates countries more strongly along institutional and development lines than in Europe, where the digitalization landscape is more homogeneous.

Figure 8, Figure 9 and Figure 10 show the clustering results based on DiGiX and unmanaged ESG risk for each pillar (environmental, social, and governance).

Environmental risk: Most European countries fall into Cluster 1 (26 out of 36), placing them in the low-risk, high-digitalization category for unmanaged environmental risk. The remaining European countries fall into Cluster 2 (10 out of 36). Importantly, no European country appears in Cluster 3 for the environmental dimension. This indicates that environmental unmanaged risk in Europe ranges only from low to moderate, without reaching the highest-risk category. In the Asia-Pacific region, the distribution is more balanced. Cluster 2 is the largest group (10 out of 28), followed closely by Cluster 1 (9 out of 28) and Cluster 3 (9 out of 28). This balanced spread shows that several Asia-Pacific countries experience higher unmanaged environmental risks relative to their digitalization levels. The almost even distribution across clusters highlights how environmental risk varies substantially across the region—reflecting differences in regulatory capacity, exposure to environmental hazards, and the extent to which digital tools are integrated into monitoring and management systems.

Social risk: European countries show an even stronger concentration in the low-risk, high-digitalization segment when considering the social dimension. Cluster 1 includes 28 of the 36 European countries, covering most Western, Northern, and several Central European states. Cluster 2 comprises 7 out of 36 countries representing mid-range digitalization levels and higher unmanaged social risk. Cluster 3 again contains only Ukraine, which consistently appears as a higher-risk outlier once social unmanaged risk is considered alongside digitalization. In the Asia-Pacific region, Cluster 2 is also the largest group, including 11 out of 28 countries. This segment comprises middle-income and Gulf economies. Cluster 1, with 9 out of 28 countries, includes digitally advanced cases and specifically for the social context Malaysia. Cluster 3 contains 8 out of 28 countries with higher unmanaged social risk. The distribution highlights substantial variation in social unmanaged risk across the Asia-Pacific region, even among countries with comparable levels of digitalization.

Governance risk: The most European countries fall into Cluster 1, with 25 out of 36 represented. This pattern reflects Europe’s comparatively strong institutional capacity and higher levels of digitalization, both of which support more effective governance and risk management. A smaller group (10 out of 36 European countries) appears in Cluster 2. Cluster 3 again includes only Ukraine, consistent with its higher unmanaged governance risk when considered alongside digitalization. In the Asia-Pacific region, Cluster 2 is the dominant grouping for governance, containing 11 out of 28 countries. This includes countries with mid-range digitalization and higher unmanaged governance risks. Cluster 1 includes 8 out of 28 countries and consists mainly of digitally advanced and institutionally stronger economies. Cluster 3 comprises 9 out of 28 countries with higher-risk governance environments. Overall, the governance-pillar results mirror the broader regional dynamics observed in the environmental and social dimensions. In the Asia-Pacific region, differences in digitalization levels and institutional maturity lead to marked variation in cluster assignments, rather than a single dominant regional pattern.

The ANOVA results confirm that the cluster solutions are statistically meaningful: p-values are effectively zero, and effect sizes are substantial across all models. These findings support the interpretation that digitalization acts as a structural enabler of ESG risk management. Higher digital capacity improves data availability and quality, accelerates reporting and traceability, strengthens compliance mechanisms, and enables more scalable monitoring and control systems. As a result, ESG risks are less likely to remain unmanaged in digitally advanced environments, as institutions can detect issues earlier, document performance more reliably, and enforce governance processes more consistently. While the analysis does not establish causality, the relationship is strong, stable, and consistent across all four risk constructs examined. Comparing the results from the four analyses yields several overarching conclusions. First, the consolidated clustering results show a high degree of structural consistency across ESG pillars. 83 out of 94 countries remain in the same cluster across all four specifications. This stability suggests that countries’ relative positions are robust whether ESG risk is assessed as a composite or decomposed into its individual components. In other words, for most jurisdictions, the relationship between digitalization and unmanaged ESG risk does not depend on the specific pillar: countries with higher DiGiX consistently fall into low-risk clusters, and those with lower DiGiX consistently fall into high-risk clusters. A smaller subset (11 out of 94 countries) shows a one-pillar shift, meaning that their cluster assignment changes in exactly one pillar-based analysis while remaining consistent in the other three. These shifts highlight cases where a country’s ESG risk profile is uneven across dimensions relative to its overall position. For example, Croatia is generally aligned with the low-risk, high-digitalization group but shifts in the governance-specific clustering, suggesting that governance risk diverges from its environmental, social, and overall patterns. Several countries (e.g., Indonesia, Paraguay, Saudi Arabia, Azerbaijan, Ukraine, and Vietnam) shift in the environmental clustering, indicating that environmental risks deviate from their broader ESG profiles. Others (e.g., Botswana, Hungary, Malaysia, Poland, and Vietnam) shift in the social dimension, suggesting that human-capital or social-risk characteristics occasionally diverge from the general ESG-digitalization relationship.

In summary, the findings indicate that digitalization is closely linked to overall ESG risk management capacity rather than to a single ESG pillar. The high stability of cluster membership across the environmental, social, and governance dimensions demonstrates that higher levels of digitalization correspond to a broad-based reduction in unmanaged ESG risk. The limited number of one-pillar shifts implies that, while digitalization generally supports improvements across the board, some countries exhibit pillar-specific vulnerabilities (most often in the environmental or social dimensions) - that require targeted institutional and policy interventions beyond digital advancement alone.

5. Discussion

By analyzing the connection between unmanaged ESG risk and digital maturity at the national level, this study contributes to the theoretical understanding of how digitalization affects sustainability. The results underscore the significance of national digital systems as structural enablers of sustainability and contribute to macro-level perspectives on digital innovation and sustainable development by moving beyond company-level assessments.

The strong negative association between digitalization and ESG risk confirms that digital technologies act not only as productivity-enhancing tools, but also as important components of national innovation and governance systems. According to the reviewed literature, digitalization improves sustainability outcomes when included in complementary institutional, regulatory, and governance frameworks [1,43,69].

The stronger explanatory power of the DiGiX Index indicates that while ICT access and connectivity are necessary, they are not sufficient to mitigate ESG risk. Broader digital powers, including infrastructure, skills, institutional readiness, and the digital integration of the public sector, lead to higher sustainability. The finding aligns with other research that stresses the importance of governance and regulatory capacity in reducing the negative effects on the long-term of use FinTech and AI [41,42].

The nonlinear relationship between digitalization and ESG risk provides empirical support for technological change. The reduction in ESG risk is amplified at higher levels of digital maturity, suggesting the existence of digitalization thresholds above which sustainability is achievable. This finding is consistent with research that emphasizes capability building, organizational readiness and digital literacy to reap the benefits of digitalization [47,48].

Cross-country analysis reveals how digitalization impacts ESG risk mitigation, with European countries mostly concentrated in a relatively homogeneous cluster of low-risk, high-digitalization levels. This suggests that in Europe, digitalization has long been used in mature governance systems, regulatory enforcement and the public sector, and the use of digital tools reduces environmental, social and governance risks. In contrast, there is significantly more heterogeneity in the Asia-Pacific region, where digitally advanced economies such as (Japan, Australia and Singapore) have tended to follow the European model, with a large group of emerging economies concentrated in medium- or high-risk clusters. It helps to clarify that digitalization, especially FinTech, can have limited or even negative impacts in places where there isn’t enough government or regulatory control [12,13].

In Asia-Pacific region, digitalization is more uneven and often decoupled from governance maturity.

6. Conclusion

From a theoretical perspective, this study reveals how digitalization influences ESG risk management at the national level as a system-level capability. Digital maturity represents the co-evolution of infrastructure, institutions, governance, and innovation capacity rather than functioning as a stand-alone technology force.

The research highlights digitalization ought to be seen as a fundamental component of sustainable development plans from a policy perspective. A nation’s capacity to manage ESG risks and enhance policy execution can be enhanced by investments in digital infrastructure, data governance, and digital public services.

Cross-country evidence suggests that digitalization is not a stand-alone solution, but rather a systemic capability, as ESG risk management is influenced by strong national institutional and governance structures. In Europe, high levels of digital maturity are embedded in strong institutional structures, while the results from Asia-Pacific highlight that without improvements in governance, regulation and policy implementation, the sustainability benefits of digitalization remain uneven. Thus, digitalization can significantly reduce ESG risks, but only if it is based on strong institutions and well-designed policy frameworks.

However, rapid adoption of FinTech and AI might lead to new ESG-related risks, such as cybersecurity vulnerabilities, data privacy concerns, algorithmic bias, and greenwashing, in the absence of robust protections. Therefore, in order to ensure that innovations are in line with ethical standards, regulatory capability, and sustainability, policymakers should develop coordinated digital and sustainability regulations.

Limitations of the study include the use of aggregated country-level indices, which may mask important heterogeneity across countries; the analysis also has cross-sectional design, which limits the interpretation of causal relationships despite the strong associations found; further research using panel data could better capture dynamic effects and causal pathways; and ESG risk assessments, while comprehensive, are still subject to measurement and methodological assumptions.

Future research could expand this framework by using longitudinal data to explore causal dynamics, examining the relationship between digitalization and governance quality, or by disaggregating digitalization into specific policy instruments such as e-government systems, regulatory technologies, or digital financial infrastructures, and assessing ESG risks. Such methods would significantly improve understanding of how national digital innovation systems, including the financial sector, could be designed to promote long-term sustainable development.

Author Contributions

Conceptualization: I.M., J.K., A.N., Methodology: J.K., I.M., A.N., Investigation: I.M., J.K., Validation: A.F., J.K., I.M., Visualization: J.K., A.V., A.F., Writing – original draft: I.M., J.K., A.F, A.V., A.S., Writing – review & editing: I.M., J.K., Data curation: J.K., Formal analysis: J.K., I.M., A.V., A.F., Supervision: I.M., A.N. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Project No.5.2.1.1.i.0/2/24/I/CFLA/007 “Internal and external consolidation of the University of Latvia” (RRF project), Project No. LU-BAPA-2024/1–0031, UL and BASBF consolidation grant project.

Institutional Review Board Statement

Not applicable.

Data Availability Statement

Dataset available on request from the authors.

Acknowledgments

The authors have reviewed and edited the output and take full responsibility for the content of this publication.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Vial, G. Understanding digital transformation: A review and a research agenda. Managing Digital Transformation 2021, 13–66. [Google Scholar] [CrossRef]

- Königstorfer, F.; Thalmann, S. Applications of artificial intelligence in commercial banks: A research agenda for behavioral finance. J. Behav. Exp. Financ. 2020, 27, 100352. [Google Scholar] [CrossRef]

- Mhlanga, D. Industry 4.0 in finance: The impact of artificial intelligence (AI) on digital financial inclusion. Int. J. Financ. Stud. 2020, 8(3), 45. [Google Scholar] [CrossRef]

- Huang, Y. Fintech as a catalyst for sustainable development: A bibliographic review of drivers, technologies, econometrics and regional insights. J. Account. Lit. 2025. [Google Scholar] [CrossRef]

- Omeragic, N.; Zaimovic, A.; Zaimovic, T. FinTech and climate action, and affordable and clean energy. Procedia Comput. Sci. 2024, 236, 273–280. [Google Scholar] [CrossRef]

- Anwar, H.; Waheed, R.; Aziz, G. Importance of FinTech and green finance to achieve the carbon neutrality targets: A study of the Australian perspective. Environ. Res. Commun. 2024, 6(11), 115007. [Google Scholar] [CrossRef]

- Mavlutova, I.; Spilbergs, A.; Romanova, I.; Kuzmina, J.; Fomins, A.; Verdenhofs, A.; Natrins, A. The role of green digital investments in promoting sustainable development goals and green energy consumption. J. Open Innov. Technol. Mark. Complex. 2025, 11(2), 100518. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Castka, P. ESG and Industry 5.0: The role of technologies in enhancing ESG disclosure. Technol. Forecast. Soc. Change 2023, 195, 122806. [Google Scholar] [CrossRef]

- Lešinskis, K.; Mavļutova, I.; Hermanis, J. The emergence and significance of artificial intelligence in digital tools for entrepreneurship education. WSEAS Trans. Environ. Dev. 2025, 21, 1160–1167. [Google Scholar] [CrossRef]

- Xu, Q.; Li, X.; Dong, Y.; Guo, F. Digitization and green innovation: How does digitization affect enterprises’ green technology innovation? J. Environ. Plan. Manag. 2025, 68(6), 1282–1311. [Google Scholar] [CrossRef]

- Qiao, P.; Liu, S.; Fung, H.G.; Wang, C. Corporate green innovation in a digital economy. Int. Rev. Econ. Financ. 2024, 92, 870–883. [Google Scholar] [CrossRef]

- Al-Shari, H.A.; Lokhande, M.A. The relationship between the risks of adopting FinTech in banks and their impact on performance. Cogent Bus. Manag. 2023, 10(1), 2174242. [Google Scholar] [CrossRef]

- Kur Ahmad, A.; Schulz, M. Digital dilemmas: Unveiling the potential dark side of digital technologies on firm outcomes. In Acad. Manag. Proc.; Academy of Management: Valhalla, NY, USA, 2025; Volume 2025, 1, p. 11635. [Google Scholar] [CrossRef]

- Asiedu, E. Risk factors affecting customer adoption of FinTech in the financial services sector. In Navigating the Fintech Frontier: Transformative Innovations and Risk Factors in Financial Services; Bentham Science Publishers, 2025; pp. 21–27. [Google Scholar] [CrossRef]

- Zhang, Y.; Chen, M.; Zhong, S.; Liu, M. FinTech’s role in carbon emission efficiency: Dynamic spatial analysis. Sci. Rep. 2024, 14(1), 23941. [Google Scholar] [CrossRef] [PubMed]

- Zaman, Q.U.; Zaman, S.; Zhao, Y.; Rasool, S.F.; Qamar, R. Policy strategies for sustainable urban development in the 21st century: Fresh empirical evidence in a global framework. Sustain. Dev. 2025, 34, 1–16. [Google Scholar] [CrossRef]

- Mavlutova, I.; Spilbergs, A.; Romanova, I.; Kuzmina, J.; Fomins, A.; Verdenhofs, A.; Natrins, A. The role of green digital investments in promoting sustainable development goals and green energy consumption. J. Open Innov. Technol. Mark. Complex. 2025, 11(2), 100518. [Google Scholar] [CrossRef]

- Arefjevs, I.; Spilbergs, A.; Natrins, A.; Verdenhofs, A.; Mavlutova, I.; Volkova, T. Financial sector evolution and competencies development in the context of information and communication technologies. Research for Rural Development 2020, Proceedings of the 26th Annual International Scientific Conference Volume 35, 260–267. [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372. [Google Scholar] [CrossRef]

- Shu, Z.; Liu, W.; Fu, B.; Li, Z.; He, M. Blockchain-enhanced trading systems for the construction industry to control carbon emissions. Clean Technol. Environ. Policy 2022, 24(6), 1851–1870. [Google Scholar] [CrossRef]

- Basdekidou, V.; Papapanagos, H. The impact of FinTech/Blockchain adoption on corporate ESG and DEI performance. WSEAS Trans. Bus. Econ. 2024, 21, 2145–2157. [Google Scholar] [CrossRef]

- Nashruddin, S.N.A.M.; Nashruddin, S.N.A.B.M.; Salleh, F.H.M. A bibliometric analysis of AI-integrated electrochemical energy systems: A review of sustainability and FinTech innovations. Int. J. Hydrogen Energy 2025, 196, 152573. [Google Scholar] [CrossRef]

- Zhang, Y.; Chen, J.; Han, Y.; Qian, M.; Guo, X.; Chen, R.; et al. The contribution of FinTech to sustainable development in the digital age: Ant Forest and land restoration in China. Land Use Policy 2021, 103, 105306. [Google Scholar] [CrossRef]

- Dong, X.; Lv, S.; Wu, S. The green promise of digital finance: Exploring its effects and mechanisms on carbon reduction. China Econ. Rev. 2025, 90, 102374. [Google Scholar] [CrossRef]

- Yalcin, H.; Demirhan, D.; Aracioglu, B.; Daim, T.U.; Xing, Z.; Meissner, D. FinTech and the green transition: Exploring pathways to ignite innovation for carbon neutrality in global supply chains. Technol. Soc. 2025, 52, 103094. [Google Scholar] [CrossRef]

- Gálvez-Sánchez, F.J.; Lara-Rubio, J.; Verdú-Jóver, A.J.; Meseguer-Sánchez, V. Research advances on financial inclusion: A bibliometric analysis. Sustain. 2021, 13(6), 3156. [Google Scholar] [CrossRef]

- Hasan, M.; Hoque, A.; Abedin, M.Z.; Gasbarro, D. FinTech and sustainable development: A systematic thematic analysis using human- and machine-generated processing. Int. Rev. Financ. Anal. 2024, 95, 103473. [Google Scholar] [CrossRef]

- Mhlanga, D. The role of financial inclusion and FinTech in addressing climate-related challenges in the Industry 4.0: Lessons for sustainable development goals. Front. Clim. 2022, 4, 949178. [Google Scholar] [CrossRef]

- Dhar, B.K.; Roshid, M.M.; Dissanayake, S.; Chawla, U.; Faheem, M. Leveraging FinTech and GreenTech for long-term sustainability in South Asia: Strategic pathways toward Agenda 2050. Green Technol. Sustain. 2025, 100263. [Google Scholar] [CrossRef]

- Hoeyi, P.K.; Farisani, T.R.; Tshabalala, J.S. Assessing the implementation and impact of inclusivity and accessibility in the Free State South African banking sector. J. Risk Financ. Manag. 2025, 18(9), 474. [Google Scholar] [CrossRef]

- Hasan, M.M.; Hasan, M.E.; Ghosh, T. Transforming developing economies by shifting paradigms beyond natural resources: The FinTech and social dynamics for sustainable mineral policy. Resour. Policy 2024, 94, 105086. [Google Scholar] [CrossRef]

- Afjal, M. Bridging the financial divide: A bibliometric analysis on the role of digital financial services within FinTech in enhancing financial inclusion and economic development. Humanit. Soc. Sci. Commun. 2023, 10(1), 1–27. [Google Scholar] [CrossRef]

- Hossain, M.E.; Haron, R.; Mahadi, N.F.B.; Nor, R.M.; Rana, S.; Martoza, M.G. FinTech innovation and financial inclusion in Malaysia: A systematic review. 2024 3rd International Conference on Creative Communication and Innovative Technology (ICCIT); IEEE; pp. 1–6. [CrossRef]

- Uribe, M.Y.S.; Bustamante, A.T.; García, J.A.S.; Lara, A.B.H. Digital financial inclusion as a catalyst for innovation, economic growth, and sustainability: A bibliometric analysis (2014–2024). Iberoam. J. Sci. Meas. Commun. 2025, 5(4), 1–12. [Google Scholar] [CrossRef]

- Xie, C.; Huang, L. How to drive sustainable economic development: The role of FinTech, natural resources, and social vulnerability. Resour. Policy 2024, 94, 105104. [Google Scholar] [CrossRef]

- Kumar, M.; Al Muraqab, N.; Bshivanna, P.; Moonesar, I.A.; Braendle, U.C.; Rao, A. Strategies of financial inclusion for enriching sustainable development goals in BRICS economies. Foresight STI Gov. 2025, 19(1), 50–63. [Google Scholar] [CrossRef]

- Munarso, S.J.; Purwanta, W.; Elmatsani, H.M.; Hendriadi, A.; Arianto, A.; Sjafrina, N.; Santoso, A.D. Strategic sustainability assessment of rural agribusiness infrastructure systems in humid tropical regions. Glob. J. Environ. Sci. Manag. 2025, 11(4), 1–14. [Google Scholar] [CrossRef]

- Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An explanation through business model scalability and market valuation. Sustain. 2020, 12(24), 10316. [Google Scholar] [CrossRef]

- Cohen, G. The impact of ESG risks on corporate value. Rev. Quant. Financ. Acc. 2023, 60(4), 1451–1468. [Google Scholar] [CrossRef]

- Rambaud, S.C.; Gázquez, A.E. A RegTech approach to FinTech sustainability: The case of Spain. Eur. J. Risk Regul. 2022, 13(2), 333–349. [Google Scholar] [CrossRef]

- Pashang, S.; Weber, O. AI for sustainable finance: Governance mechanisms for institutional and societal approaches. In The Ethics of Artificial Intelligence for the Sustainable Development Goals; Springer International Publishing: Cham, 2023; pp. 203–229. [Google Scholar] [CrossRef]

- Campanella, F.; Ferri, L.; Serino, L.; Zampella, A. Driving sustainability: How FinTech transforms SDG performance in SMEs. J. Glob. Responsib. 2025. [Google Scholar] [CrossRef]

- Shlapak, A.; Zhavoronok, A.; Vdovenko, N.; Bilousov, O.; Horban, D.; Krylov, D. The impact of digital technologies and artificial intelligence on the management of socioeconomic processes in the context of sustainable development. J. Innov. Sustain. RISUS 2025, 16(2), 180–193. [Google Scholar] [CrossRef]

- Kalmane-Pivkina, E.; Gaile-Sarkane, E. Advancing digital sustainability KPIs in FinTech: Innovation, ethics, and integration in the European payments sector. In Proceedings of the 29th World Multi-Conference on Systemics, Cybernetics and Informatics (WMSCI 2025), 2025; pp. 186–195. [Google Scholar] [CrossRef]

- Zhao, Y. The FinTech revolution: Innovations reshaping the financial industry. Highlights Bus. Econ. Manag. 2023, 15, 123–128. [Google Scholar] [CrossRef]

- Anifa, M.; Ramakrishnan, S.; Joghee, S.; Kabiraj, S.; Bishnoi, M.M. FinTech innovations in the financial service industry. J. Risk Financ. Manag. 2022, 15(7), 287. [Google Scholar] [CrossRef]

- Cetindamar, D.; Abedin, B.; Gerdsri, N.; Shirahada, K. Editorial overview of digital literacy of employees and organizational transformation and innovation. IEEE Trans. Eng. Manag. 2024, 71, 7832–7836. [Google Scholar] [CrossRef]

- Dery, K.; Sebastian, I.M.; van der Meulen, N. The digital workplace is key to digital innovation. MIS Q. Exec. 2017, 16(2). [Google Scholar]

- Molla, A.; Biru, A. The evolution of the FinTech entrepreneurial ecosystem in Africa: An exploratory study and model for future development. Technol. Forecast. Soc. Change 2023, 186, 122123. [Google Scholar] [CrossRef]

- Łasak, P.; Wyciślak, S. The dichotomy of inclusiveness and vulnerability as a consequence of banking platform development. Res. Int. Bus. Financ. 2024, 72, 102536. [Google Scholar] [CrossRef]

- Chan, R.; Troshani, I.; Rao Hill, S.; Hoffmann, A. Towards an understanding of consumers’ FinTech adoption: The case of Open Banking. Int. J. Bank Mark. 2022, 40(4), 886–917. [Google Scholar] [CrossRef]

- Han, W.; Ozdemir, O.; Erkmen, E. ESG performance and bankruptcy risk in the hospitality and tourism industry: Moderating role of the Covid-19 pandemic and corporate governance attributes. Tour. Econ. 2025. [Google Scholar] [CrossRef]

- Sun, Y.; Huang, T.K.; Lu, Y. Is ESG transparency the fruit of corporate digitalization: Strategic pathways to enhanced ESG disclosure? Bus. Strat. Environ. 2025. [Google Scholar] [CrossRef]

- Chen, W.; Wu, W.; Ouyang, Z.; Fu, Y.; Li, M.; Huang, G.Q. Event-based data authenticity analytics for IoT and blockchain-enabled ESG disclosure. Comput. Ind. Eng. 2024, 190, 109992. [Google Scholar] [CrossRef]

- Biju, A.V.N.; Kodiyatt, S.J.; Krishna, P.P.N.; Sreelekshmi, G. ESG sentiments and divergent ESG scores: Suggesting a framework for ESG rating. SN Bus. Econ. 2023, 3(12). [Google Scholar] [CrossRef]

- Chien, F.; Mehmood, K.; Wang, Y.; Zhang, Y.; Piccardi, P. Smart ESG framework for corporate responsibility mechanism in decentralized finance. Corp. Soc. Responsib. Environ. Manag. 2025, 32(6), 7467–7489. [Google Scholar] [CrossRef]

- Sharma, A.; Chandrakar, P.; Kumari, S.; Chen, C. FINSEC: A consortium blockchain-enabled privacy-preserving and scalable framework for customer data protection in FinTech. Peer-to-Peer Netw. Appl. 2025, 18(3). [Google Scholar] [CrossRef]

- Dorfleitner, G.; Hornuf, L.; Kreppmeier, J. Promise not fulfilled: FinTech, data privacy, and the GDPR. Electron. Mark. 2023, 33(1). [Google Scholar] [CrossRef]

- Lendvai, G.F.; Gosztonyi, G. Algorithmic bias as a core legal dilemma in the age of artificial intelligence: Conceptual basis and the current state of regulation. Laws 2025, 14(3), 41. [Google Scholar] [CrossRef]

- Carè, R.; Boitan, I.A.; Stoian, A.M.; Fatima, R. Exploring the landscape of financial inclusion through the lens of financial technologies: A review. Fin. Res. Lett. 2024, 72, 106500. [Google Scholar] [CrossRef]

- Zeng, T.; Jiang, Y. Fintech and low-carbon urban development. Fin. Res. Lett. 2025, 79, 107229. [Google Scholar] [CrossRef]

- Yu, B.; Zhao, F. Revealing the impact of fintech on energy saving and carbon reduction innovation. Front. Environ. Sci. 2025, 13. [Google Scholar] [CrossRef]

- Bai, Y.; Eweade, B.S.; Aghazadeh, S.; Bamidele, R.O.; Xu, Y. Pathways to environmental sustainability: Do fintech, natural resources, and environmental patents matter in E-7 nations? Renew. Energy 2025, 247, 122987. [Google Scholar] [CrossRef]

- Dadabada, P.K. Analyzing the impact of ESG integration and FinTech innovations on green finance: A comparative case studies approach. J. Knowl. Econ. 2024, 16(2), 7959–7978. [Google Scholar] [CrossRef]

- Sun, X.; Wu, G. Leveraging FinTech for positive ESG outcomes through regional innovation: Insights from a knowledge capital perspective. Front. Public Health 2025, 13, 1641241. [Google Scholar] [CrossRef]

- BBVA Research. DiGiX 2024 update: A multidimensional index of digitization. 2024. Available online: https://www.bbvaresearch.com/wp-content/uploads/2024/08/DiGiX_2024_Update_A_Multidimensional_Index_of_Digitization_edi.pdf (accessed on 24 November 2025).

- International Telecommunication Union. ICT Multidimensional Development Index (MDD) 2025. 2025. Available online: https://www.itu.int/dms_pub/itu-d/opb/ind/D-IND-ICT_MDD-2025-1-PDF-E.pdf (accessed on 29 November 2025).

- Sustainalytics Global access. 2024. Available online: https://www.sustainalytics.com/global-access (accessed on 27 November 2025).

- Asif, M.; Searcy, C.; Castka, P. ESG and Industry 5.0: The role of technologies in enhancing ESG disclosure. Technol. Forecast. Soc. Change 2023, 195, 122806. [Google Scholar] [CrossRef]

Figure 1.

PRISMA flowchart.

Figure 2.

Publication distribution by years 2019-2025.

Figure 3.

Keyword network map.

Figure 4.

Network map of publications by countries.

Figure 5.

ESG risk vs. DiGiX.

Figure 6.

ESG risk vs. IDI.

Figure 7.

DiGiX vs country`s ESG risk score.

Figure 8.

DiGiX vs country`s environmental risk score.

Figure 9.

DiGiX vs country`s social risk score.

Figure 10.

DiGiX vs country`s governance risk score.

Table 1.

Search details.

| Database | Search string | Result |

|---|---|---|

| Scopus | TITLE-ABS-KEY ( digital* AND fintech AND “sustainable development” ) | 339 |

| Web of Science | (((TS = digital*) AND (TS = fintech)) AND (TS = “sustainable development”)) | 231 |

Source: created by authors.

Table 2.

Search details.

| Category | Sub-category and descriptions |

|---|---|

| 1. Digitalization impact on ecological sustainability | a. Blockchain based researches on the impact of new tools on ecology, how it can be made more efficient with ever evolving digital solutions b. Digital tool usage in optimizing renewable energy generation and utilization, efficient resource usage c. CO2 emission reduction as target by utilizing digital technologies |

| 2. Digitalization as a base for social inclusion | a. Empowerment of different social groups by providing access to financial tools that previously were not available b. Regional based research on fintech impact to underbanked social groups c. Financial literacy improvements by using easy access digital tools |

| 3. Digitalization impact on economic performance | a. Impact on ESG by using financial technology and artificial intelligence solutions b. Emerging economy region developments based on digitalization and financial inclusion improvements c. Individual entity changes in operations, efficiencies and provided services by utilizing new technologies |

| 4. Regulatory and governance evolution | a. Financial technology (FinTech) regulations in different regions and services b. Regulatory technology (RegTech) development alongside financial technology increase c. Institutional governance changes in evolving technological environment |

| 5. Innovation based researches | a. New entrepreneurship opportunities based on financial and general technological development b. Open Banking impact on financial services and market players c. Human Resources aspects of rapid digitalization and changes needed for adjusting competences |

Source: created by authors.

Table 4.

Countries with most publications.

| Country | Number of publications | Total citations | Average citation per publication |

|---|---|---|---|

| China | 26 | 372 | 14.3 |

| India | 11 | 170 | 15.5 |

| Saudi Arabia | 8 | 86 | 10.8 |

| United States | 7 | 44 | 6.3 |

| Malaysia | 7 | 56 | 8 |

| Italy | 6 | 173 | 28.8 |

| Jordan | 5 | 60 | 12 |

| Australia | 5 | 93 | 18.6 |

| Poland | 5 | 10 | 2 |

Source: created by authors.

Table 5.

Descriptive statistics.

| Variable | N | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|---|

| ESG risk score | 86 | 20.973 | 7.603 | 8.490 | 20.625 | 37.900 |

| DiGiX | 86 | 0.573 | 0.235 | 0.000 | 0.625 | 0.930 |

| IDI | 86 | 85.844 | 11.922 | 46.300 | 89.550 | 99.200 |

Source: created by authors.

Table 6.

Correlation.

| ESG | DiGiX | IDI | |

|---|---|---|---|

| ESG | 1.000 | -0.944 | -0.797 |

| DiGiX | -0.944 | 1.000 | 0.887 |

| IDI | -0.797 | 0.887 | 1.000 |

Source: created by authors.

Table 7.

Regression analysis results.

| (A) ESG~DiGiX | (A2) ESG~DiGiX+DiGiX² | (B) ESG~IDI | (B2) ESG~IDI+IDI² | (C) ESG~DiGiX+IDI (CC) | |

|---|---|---|---|---|---|

| DiGiX | -30.159*** (1.401) | -16.494** (6.866) | -36.125*** (2.654) | ||

| DiGiX² | -13.263* (6.828) | ||||

| IDI | -0.386*** (0.022) | 0.451** (0.205) | 0.123** (0.048) | ||

| IDI² | -0.006*** (0.001) | ||||

| Constant | 38.441*** (0.898) | 35.679*** (1.547) | 54.507*** (1.713) | 28.287*** (6.870) | 31.140*** (2.971) |

| N | 94 | 94 | 131 | 131 | 86 |

| R² | 0.880 | 0.891 | 0.672 | 0.722 | 0.900 |

Source: created by authors, Dependent variable is the ESG risk score. Standard errors are in parentheses. Significance: *** p<0.01, ** p<0.05, *** p<0.10.

Table 8.

Cluster analysis results.

| Variable tested | F | p-value | ηІ | Levene p-value | |

|---|---|---|---|---|---|

| Analysis 1: Country-Risk Score vs DiGiX | Country ESG Risk Score | 298.36 | 1.082e-40 | 0.868 | 9.470e-01 |

| DiGiX | 221.48 | 1.083e-35 | 0.830 | 1.320e-02 | |

| Analysis 2: HC-Risk Score (Social) vs DiGiX | HC-Risk Score (Social) | 265.63 | 1.025e-38 | 0.854 | 1.034e-01 |

| DiGiX | 229.43 | 2.853e-36 | 0.835 | 1.777e-02 | |

| Analysis 3: NCPC-Risk Score (Environmental) vs DiGiX | NCPC-Risk Score (Environmental) | 156.07 | 3.872e-30 | 0.774 | 3.973e-01 |

| DiGiX | 237.22 | 7.988e-37 | 0.839 | 2.191e-02 | |

| Analysis 4: IC-Risk Score (Governance) vs DiGiX | IC-Risk Score (Governance) | 277.72 | 1.809e-39 | 0.859 | 9.050e-01 |

| DiGiX | 217.55 | 2.128e-35 | 0.827 | 1.376e-02 |

Source: created by authors.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.