Submitted:

22 February 2026

Posted:

25 February 2026

You are already at the latest version

Abstract

This study examines the relationship between board composition and integrated reporting quality (IRQ) and tests whether firm performance mediates this relationship. Using content analysis, IRQ is measured through a disclosure index based on the 2021 International Integrated Reporting Framework. The sample comprises 550 integrated annual reports from 110 companies listed on the Johannesburg Stock Exchange across multiple sectors for the period 2020–2024. Panel multiple regression analysis reveals that board size and gender diversity are positively and significantly associated with IRQ, suggesting that larger and more gender-diverse boards enhance monitoring effectiveness and stakeholder-oriented transparency. In contrast, board independence and audit committee size show no significant association with IRQ. The findings further indicate that firm performance does not mediate the relationship between board composition and IRQ, implying that reporting quality is driven more by governance structures than by financial outcomes. This study contributes post-2021 Framework evidence from a mandatory integrated reporting context, refines governance theory by highlighting the importance of board heterogeneity over formal independence, and positions IRQ as a governance outcome rather than a financial signalling mechanism. The results offer practical insights for regulators, investors, and policymakers seeking to enhance reporting quality.

Keywords:

audit committee size

; board composition

; board independence

; board size

; firm performance

; gender diversity

; Integrated reporting quality

1. Introduction

The increasing interest in integrated reporting (IR) and its disclosure among regulators, policymakers, shareholders, professionals, and scholars is driven by concerns over corporate information asymmetries, corporate scandals, and the limitations of traditional corporate reporting in meeting stakeholder information needs (Ghaleb, Qaderi, & Al-Qadasi, 2024). Stakeholders, particularly providers of financial capital, are now demanding high-quality, value relevant non-financial information alongside financial information (Farooq, Azantouti, & Zaman, 2024; García-Sánchez, Raimo, Amor-Esteban, & Vitolla, 2023). In response to these demands, the International Integrated Reporting Council (IIRC) introduced a voluntary, principles-based reporting framework known as 'integrated reporting' on December 9, 2013. This reporting framework integrates both financial and non-financial information to improve the quality of reporting (IIRC, 2021; Khatlisi & Mashamba, 2025; Qaderi, Ghaleb, Qasem, & Waked, 2024). IR aims to promote a more cohesive and efficient approach to corporate reporting, enhance accountability and stewardship, and encourage integrated thinking, decision-making, and actions that prioritise value creation across short-, medium-, and long-term horizons (IIRC, 2013; 2021).

Board composition plays a vital role in the effective performance of a Board of Directors (the "Board") (Pucheta-Martínez, Bel-Oms, & Gallego-Álvarez, 2023; Yusuf et al., 2024). The Board serves as a key internal control mechanism, appointed by shareholders to make decisions, supervise, and manage the company on their behalf (Anojan, 2024). To ensure good corporate governance practices, factors such as board size, power balance, independence, diversity, skills, and rotation should be considered when determining optimal Board composition. These elements are outlined in best-practice codes for corporate governance, such as King V, as well as in the relevant laws and regulations governing this area (Institute of Directors South Africa [IoDSA], 2025; Cooray et al., 2020).

While there are legal stipulations regarding minimum Board size, terms of office for members, and qualification criteria for directors, the Companies Act No. 71 of 2008 (Republic of South Africa, 2009) provides relatively limited guidance on Board composition for companies in South Africa. However, the King V code provide detail information on board composition, stating that “the governing body ensures that its composition is balanced with respect to the mix of competencies, diversity and independence that enables it to discharge its obligations objectively and effectively” (IoDSA, 2025, p.11). Therefore, companies should refer to best practices in corporate governance for guidance when evaluating their ideal Board composition (Amanamah, 2024; Pozzoli et al., 2022).

According to Principle 5 of the King V Report on Corporate Governance for South Africa, the Board of Directors should oversee the preparation of high-quality annual reports, including integrated reports, to enable stakeholders to make well-informed decisions about the company's performance and its ability to create value over time (IoDSA, 2025). The Board is responsible for ensuring that the information needs of stakeholders are met within the corporate governance framework. A balanced composition of the Board of Directors can mitigate agency problems, enhance corporate governance practices, maintain and boost company performance, improve transparency in reporting, reduce information asymmetry, gain legitimacy, and respond to pressure from institutional stakeholders (Al Amosh & Khatib, 2022; Qaderi, Ghaleb, Hashed, Chandren & Abdullah, 2022; Martens & Bui, 2023).

Recent studies have provided empirical evidence indicating the relationship between IR and good corporate governance practices (Anojan, 2024; Appiagyei, Hadrian, & Roni, 2023; Arinta & Ashari, 2022; Chouaibi et al., 2022; Cooray et al., 2020; Devarapalli & Mohapatra, 2024; Dumitru & Dragomir, 2023; Halid et al., 2021; Lawal & Yahaya, 2024; Qaderi et al., 2022; Yusuf et al., 2024). However, other studies in the literature, such as those of Ahmed (2023), Amanamah (2024), and Mawardani and Harymawan (2021), document no association between IR quality and corporate governance practices. There is also evidence suggesting that the relationship between corporate governance characteristics and IRQ can be strengthened by incorporating moderating factors such as firm performance (Alatawi, Mat Daud & Johari, 2025). A company's performance is intricately tied to its value, measured by profitability and the meeting of stakeholder expectations (Khunkaew, Wichianrak & Suttipun, 2023). Firm performance encompasses financial results, operational efficiency, and market growth (Islam, 2021), all critical elements that can influence the relationship between IRQ and board composition.

Several investigations into IRQ have been conducted in South Africa, where IR and compliance with the King V Report on Corporate Governance are mandatory for companies listed on the JSE. However, there remains a significant lack of empirical evidence regarding how board composition affects the quality of IR disclosures (Appiagyei, Hadrian, & Roni, 2023; Arinta & Ashari, 2022; Devarapalli & Mohapatra, 2024; Mawardani & Harymawan, 2021). Additionally, the moderating role of corporate characteristics, such as firm performance, has been overlooked in the existing literature (Alatawi et al., 2025; Islam, 2021; Khunkaew et al., 2023). Therefore, this research aims to contribute to the corporate governance and IR disclosure literature by empirically examining the relationship between board composition, including board size, board independence, board gender diversity, and audit committee size and IRQ in South Africa. This research is motivated by the increasing regulatory emphasis on corporate governance and IR, as well as rising stakeholder expectations for enhanced disclosure quality (Alatawi et al., 2025). Moreover, this study introduces the examination of firm performance as a mediating variable in the relationship between board composition and IRQ. By incorporating this often-overlooked mediating role of firm performance, our analysis provides novel insights and addresses a significant gap in the IR disclosure and corporate governance literature, particularly in the unique South African context.

Furthermore, previous research on IR disclosure practices in South Africa has employed various approaches to population selection. For example, some studies have focused on the top-listed companies by market capitalisation (Chikutuma, 2024; Khatlisi & Enwereji, 2025) or on best-practice companies recognised through external awards, such as the Nkonki Top Companies Awards and Ernst & Young (EY) Excellence Awards (Chirairo & Molele, 2024; Zúñiga et al., 2020). Mans-Kemp and van der Lugt (2020) argue that the largest and best-practice companies on the JSE represent approximately 95% of market capitalisation. These companies tend to be well-managed, transparent, and more likely to produce high-quality integrated reports aligned with the IIRF. In contrast, our research aims to evaluate the quality of IR across the entire population of JSE-listed companies, rather than focusing exclusively on specific groups, sectors, or industries.

The South African setting is significant because this was the first country to formally mandate IR as a fundamental aspect of corporate reporting (Mokabane & du Toit, 2022; Sabelfeld et al., 2024). More specifically, the JSE mandated that all companies with a primary listing on the exchange produce integrated reports for financial years ending on or after March 1, 2010, in accordance with the IIRF (Mokabane & du Toit, 2022; Sabelfeld et al., 2023). Additionally, it is important to note that most non-listed South African companies, including public, private, non-profit, and state-owned enterprises have also adopted IR as their main mode of corporate reporting.

The JSE is the focus of this study due to its status as the largest and most advanced stock exchange in Africa and one of the world’s top 20 by market capitalisation (JSE, 2024). Additionally, the JSE is internationally recognised as a leader in promoting the adoption and practice of IR (Khatlisi & Enwereji, 2025; Mokabane & du Toit, 2022; Sabelfeld et al., 2023).

This study explores the mediating role of firm performance in the relationship between board composition and IRQ, an area where these variables have previously been understudied or analysed in isolation. To address this research gap, the following questions are raised:

- What is the impact of board composition on the IRQ of companies listed on the JSE?

- Does firm performance play any mediating role in the relationship between board composition and IRQ in the context of companies listed on the JSE?

Employing multivariate OLS regression models, we analysed the panel data collected from 550 integrated annual reports of a randomly selected sample of 110 companies across various sectors listed on the JSE for a five-year period (2020 – 2024). The findings demonstrate substantial evidence that board size, board independence, and gender diversity are positively associated with IRQ, indicating that the board of directors plays a critical role in monitoring and addressing agency problems while protecting stakeholders' interests. Moreover, the results suggest that firm performance positively moderates the relationship between board composition and IRQ. This study emphasises the need for alignment between corporate governance practices, specifically board composition and IR practices to build stakeholder trust and foster long-term value creation.

This study makes several contributions to the fields of corporate governance and IR by providing empirical evidence on the importance of balanced board composition and its relationship with IRQ in an emerging market where IR is mandatory. Additionally, the research offers new insights into the mediating role of firm performance in the relationship between board composition and IRQ within JSE-listed companies. The implications of our findings extend widely, providing valuable insights to financial capital providers, corporate leaders, regulators, and policymakers striving to encourage companies to achieve a more balanced composition of governing bodies and independent members. Furthermore, regulators need to adopt a more proactive approach to regulations surrounding corporate governance frameworks and IR strategies to enhance the overall quality of IR, thereby fostering greater transparency and accountability across business sectors.

The rest of the study proceeds as follows: Section 2 presents the literature review, including the theoretical framework and research hypotheses. Section 3 details the research methodology employed, including data collection methods. Section 4 presents and discusses the empirical results, while Section 5 offers a robustness analysis. Finally, Section 6 concludes the study.

2. Literature Review and Hypothesis Development

2.1. Theoretical Framework

This study employs agency theory and stakeholder theory to investigate the relationship between board composition and IRQ, while further examining the mediating role of firm performance in this relationship.

2.1.1. Agency Theory

Agency theory, developed by Jensen and Meckling (1976), explains organisational behaviour by highlighting the relationship between the board (management), acting as the "agent," and shareholders, the "principals." According to Jensen and Meckling (1976), an agency relationship occurs when one or more individuals (the principals) hire a third party (the agent) to make decisions on their behalf. Conflicts of interest may arise when the agent's interests do not align with the principal's, complicating the relationship (Amanamah, 2024). Conflicts of interest between these groups can lead to agency costs, which may harm the firm's financial performance (Rao & Juma, 2024).

This study emphasises the importance of agency theory in high-quality IR, as agency financial capital providers trust the board of directors (the agent) to act in their best interests (Amanamah, 2024). Such trust and confidence are critical factors in agency theory. In this context, high-quality IR is expected to minimise conflicts of interest, as well as reduce information asymmetry and agency costs that occur in the relationships between the board of directors, shareholders, and other stakeholders (Khunkaew et al., 2023). This can help improve firm performance (Citation).

The Agency theory also suggests that effective corporate governance mechanisms should aim to minimise these agency costs (Al-Faryan, 2024; Thi Lan Anh & Thi Hai Yen, 2025; Said, 2025). Good corporate governance establishes rules and practices that the board can implement to ensure accountability, fairness, and transparency with stakeholders, as well as strengthen a company's reputation (Jensen & Meckling, 1976; Rao & Juma, 2024). This includes mechanisms like a well-defined board structure, the presence of independent directors, gender diversity on the board, and adequate controls by the audit committee (Amanamah, 2024). These factors contribute to better financial performance.

An effective board of directors can align its interests with those of financial capital providers, monitor managerial behaviour, produce quality annual reports, and ultimately reduce information asymmetry and agency costs (Almulhim, 2023; Bui & Krajcsák, 2024; Hong & Marnet, 2025; Lubis et al., 2025). The presence of independent and female directors can serve as a mechanism for addressing the conflicting interests between shareholders and managers, thereby aligning their goals (Ghaleb, Qaderi & Al-Qadasi, 2024). Failing to reconcile these interests can lead to information asymmetry and decreased transparency in the information disclosed to other stakeholders (Ghaleb et al., 2024; Jensen & Meckling, 1976). Empirical research using agency theory (e.g., Amanamah, 2024; Chouaibi et al., 2021; Cooray et al., 2020; Ghaleb et al., 2024; Qaderi et al., 2022; Vitolla et al., 2020) supports the agency perspective, indicating that an effective board of directors can enhance IRQ. Consequently, agency theory serves as a valuable framework for informing how companies navigate the dynamics between the board of directors (agents) and providers of financial capital (principals), along with other stakeholders, by maintaining a balanced composition of the board of directors (Al Amosh & Khatib, 2022; Qaderi et al., 2022; Martens & Bui, 2023).

2.1.2. Stakeholder Theory

The stakeholder theory of organisational management and business ethics was first introduced by Freeman in 1984 in his seminal work, “Strategic Management: A Stakeholder Approach” (Mahajan et al., 2023). This theory serves as a conceptual framework designed to address the ethical considerations and values inherent in organisational management (Bridoux & Stoelhorst, 2022). Freeman (1984) synthesised insights from various disciplines such as corporate planning, systems theory, and corporate social responsibility (CSR), while also incorporating established theories like transaction cost theory, agency theory, and the theory of the firm to develop his stakeholder approach (Kivits & Sawang, 2021).

Since its inception, stakeholder theory has positioned itself as a sophisticated and well-supported framework for understanding corporate disclosure. This foundation is based on its normative legitimacy, instrumental effectiveness, and descriptive accuracy (Bridoux & Stoelhorst, 2022; Kivits & Sawang, 2021; Mahajan et al., 2023; Valentinov & Roth, 2024).

In line with the perspectives of the stakeholder theory, an integrated report serves as an innovative tool through which companies demonstrate their responsiveness to the informational needs of key stakeholder constituents (Shirabe & Nakano, 2022). Providing comprehensive financial and non-financial information in integrated reports is believed to positively impact capital providers and other stakeholders by enabling more effective capital allocation and investment decisions (Biehl, Bleibtreu, & Stefani, 2024). An integrated report should shed light on the nature and quality of the firm’s relationships with its principal stakeholders, including how well the firm understands, considers, and addresses the legitimate needs and interests of all stakeholder groups (IIRC, 2021). High-quality disclosures in integrated reports can enhance transparency and accountability, fostering stakeholder trust and providing essential information to support improved decision-making processes (Nishitani et al., 2021).

From the perspective of stakeholder theory, board composition is an interconnected factor that influences both the scope and quality of corporate disclosure, as the board is responsible for representing and protecting the interests of various stakeholders (Colak & Sarioglu, 2025). An effective board can reduce managerial opportunism and provide a broader perspective on stakeholder interests, thereby potentially enhancing the quality of disclosures (Ghazalat, 2025).

Stakeholder theory emphasises the significance of board size, suggesting that larger boards are more likely to consider a wide range of stakeholder interests (Tajuddin et al., 2024). Larger boards protect diverse stakeholder interests by promoting comprehensive and extensive information disclosure. Furthermore, stakeholder theory provides a framework for understanding how board diversity can improve the board’s capacity to meet the diverse needs of different stakeholder groups. Research has argued that women in managerial positions tend to foster more participative communication among board members (Abdelkader et al., 2024; Babiker et al., 205). As a result, boards with greater gender diversity may be better equipped to address the information needs of various stakeholder groups. Therefore, increasing gender diversity on boards could enhance their ability to assess the interests of diverse stakeholders.

2.2. Hypothesis Development

2.2.1. Integrated Reporting Quality

An integrated report aims to provide a holistic view of corporate activities by combining separate disclosures related to sustainability reporting, corporate governance, management commentary, and traditional financial reporting into a single report (Darminto et al., 2024; Qaderi et al., 2024). The preparation of an integrated report should follow the guidelines outlined by the IIRF, except in cases where legal restrictions prevent the disclosure of material information or where such disclosure would create a significant competitive disadvantage (IIRC, 2021). The IIRC (2021) outlines seven guiding principles and eight content elements that shape the overall structure and substance of an integrated report, supported by two foundational elements.

On the other hand, the eight content elements are: organisational overview and external environment, governance, business model, risks and opportunities, strategy and resource allocation, performance, outlook, and basis of preparation and presentation (IIRC, 2021). These content elements are not mutually exclusive; they are interconnected and significantly influence one another. This means that if the reporting quality of one content element is poor, it will negatively impact the reporting quality of all the other elements (Muhi & Benaissa, 2023). High-quality disclosure of these content elements in an integrated report is expected to positively correlate with stakeholders' expectations and information needs, leading to improved corporate outcomes, including firm value and overall performance over time (Khunkaew et al., 2023; Maroun et al., 2023).

Recent empirical studies have shown that quality IR enhances audit quality (Ahmed, Abubakar, Abd-Mutalib, & Hassan, 2024), helps mitigate regulatory and reputational risks, improves corporate performance (Abdelmoneim & El-Deeb, 2024), increases earnings quality (Darminto et al., 2024), improves the accuracy of analysts’ forecasts, and lowers the cost of capital (Boujelben et al., 2024; Chircop et al., 2024). High-quality IR also supports more effective internal decision-making processes and boosts overall firm value (Boujelben et al., 2024; Darminto et al., 2024). Collectively, these advantages provide a strong argument for organisations to adopt IR practices (Qaderi et al., 2024). However, there remains a significant lack of evidence regarding how board composition, which includes factors such as board size, board independence, board gender diversity, and audit committee size, affects the IRQ of companies listed on the JSE. Additionally, the moderating role of firm performance in the relationship between corporate characteristics and IRQ has been overlooked in the existing literature. Therefore, this research aims to contribute to the corporate governance and IR disclosure literature by empirically exploring the relationship between board composition and IRQ.

2.2.2. Board Composition

The composition of a board of directors is a critical factor that affects its overall effectiveness and responsibilities (Garcia-Torea et al., 2016; Shabbir et al., 2024). As outlined in the King V Report, an appropriate Board composition requires a suitable blend of expertise, size, distribution of authority, independence, diversity, skills, and personal attributes (IoDSA, 2025). Additionally, the rotation of Board members is essential for an effective governance structure (IoDSA, 2025). In South Africa, company registration is regulated by the Companies Act 71 of 2008, which emphasises the critical role of an effective board in company management (Republic of South Africa, 2009). The board of directors acts as a central internal control mechanism, appointed by shareholders to make decisions, oversee, and govern companies on their behalf (Anojan, 2024). The board of directors is responsible for informing shareholders who are not actively involved in the company about the firm's performance and accomplishments, often through corporate reports (Amanamah, 2024).

According to Principle 5 of the King V guidelines, the board of directors should oversee the preparation of high-quality annual reports, including integrated reports, by companies to enable stakeholders to make well-informed assessments of the company's performance and its ability to generate value over the short-, medium-, and long-term (IoDSA, 2025). The responsibility of the company's board of directors within the framework of corporate governance is to ensure the fulfilment of stakeholders' information requirements. Anojan (2024) emphasises the importance of publicly traded companies focusing on board composition factors. These include increasing the representation of women on the board, promoting board independence, and holding regular audit committee meetings to support the implementation of IR practices.

According to stakeholder theory, the composition of a corporate board is a critical mechanism for effective corporate governance (Pozzoli et al., 2022). In line with the agency theory, an effective board of directors can help reduce agency problems, improve corporate governance practices, maintain and enhance company performance, increase transparency in reporting, reduce information asymmetry, gain legitimacy, and respond to pressures from institutions and stakeholders (Al Amosh & Khatib, 2022; Qaderi, Ghaleb, Hashed, Chandren & Abdullah, 2022; Martens & Bui, 2023). Board composition plays a critical role in enhancing the effectiveness of corporate governance mechanisms designed to mitigate agency conflicts.

The current research has examined the broad concept of corporate governance by analysing various practices and attributes, including board size, board independence, board gender diversity, and the audit committee. These elements are outlined in the best-practice codes for corporate governance, as well as in the relevant laws and regulations governing corporate governance (Cooray et al., 2020). The subsequent subsections will elaborate on these points in relation to the corresponding hypothesis.

2.2.3. Board Size and Integrated Reporting Quality

The term "board size" refers to the total number of directors influencing a board's operations and overall effectiveness (Qaderi et al., 2022). Board size is widely recognised as a crucial mechanism for corporate governance oversight and a key determinant of board effectiveness (Cooray et al., 2020). In line with agency theory, Cooray et al. (2020) argue that board size serves as a proxy for managerial capability and helps reduce information asymmetry between management and stakeholders.

Organisations with larger boards and subcommittees may experience an expansion of managerial authority and improved access to resources, enhancing legitimacy and strengthening the firm’s ability to implement strategic initiatives (Qaderi et al., 2022). Larger boards are often characterised by greater diversity and a broader range of expertise, which positively influence both the scope and quality of voluntary information disclosure, including the amount of forward-looking disclosures (Cooray et al., 2020; Denhere, 2024; Mawardani & Harymawan, 2021; Qaderi et al., 2022).

Conversely, Qaderi et al. (2022) suggest that smaller boards may offer advantages over larger ones by facilitating better communication and coordination during decision-making processes, thereby enhancing managerial oversight. A reduced board size can help mitigate agency conflicts between managers and shareholders, reduce information asymmetry, and subsequently improve the level of voluntary disclosure (Munisi, 2023).

In this field of study, prior empirical studies have investigated the relationship between board size and IRQ, yielding mixed findings. For example, Lawal and Yahaya (2024) analysed the effect of corporate governance on the quality of IR by examining data from 155 publicly listed companies in Nigeria over 10 years (2013-2022). Their results indicated that factors such as board gender diversity and board size significantly affect IRQ, whereas the effect of board independence on IRQ was negligible.

Munisi (2023) explored the impact of board structure on information disclosure in the annual reports of publicly listed firms across eleven sub-Saharan African countries. Using an unbalanced panel dataset comprising 531 firm-year observations from 2005 to 2009, the study focused on non-financial firms listed on African stock exchanges. The findings indicated a positive, statistically significant association between board size and information disclosure, whereas the presence of independent non-executive directors did not show a significant effect. Munisi (2023) concluded that larger boards enhance monitoring and advisory functions, given the diverse perspectives, skills, knowledge, experience, and competencies inherent in a larger group of directors.

Additional research conducted in various countries (Amanamah, 2024; Cooray et al., 2020; Devarapalli & Mohapatra, 2024; Mawardani & Harymawan, 2021; Mohammadi et al., 2021; Qaderi et al., 2022) generally supports the notion that larger boards are associated with increased corporate disclosure, including higher levels of Information Quality Reporting (IRQ). However, some studies have reported divergent findings. For instance, Amanamah (2024) found no significant impact of board size on the extent or quality of disclosure, while Halid et al. (2021) identified a significant negative relationship between board size and IRQ. These inconsistencies across different national contexts highlight the need for further research to clarify the relationship between board size and IRQ. Accordingly, the present study proposes the following hypothesis.

H1: Board size has a significant impact on IRQ.

2.2.4. Board Independence and Integrated Reporting Quality

Board independence is a fundamental aspect of corporate governance with significant implications for IRQ. The King V Report on Corporate Governance defines independence as “the exercise of objective, unfettered judgment, without any interest, position, association, or relationship that could unduly influence or bias decision-making, as perceived by a reasonable and informed third party” (IoDSA, 2025, p. 13). From the perspective of agency theory, independent directors can exert considerable influence in monitoring and evaluating management performance (Amanamah, 2024). The potential misalignment between independent directors and company management could lead to a decline in both the quality and quantity of voluntary disclosures (Fun et al., 2023).

In line with this perspective, King V emphasises the critical role of board independence in corporate governance by recommending that a substantial proportion of board members be non-executive, with the majority classified as independent (IoDSA, 2025). Furthermore, the chairperson of the board should be an independent non-executive director, and all members of the audit committee must also be independent non-executive directors (IoDSA, 2025). An independent board is essential for mitigating biased economic and non-economic decision-making. An independent board underscores the importance of including skilled and experienced non-executive directors who prioritise shareholders' interests and reduce the influence of executive directors in decision-making processes, thereby enhancing the quality of information provided to stakeholders (Anojan, 2024; Cooray et al., 2020).

Mawardani and Harymawan (2021) argue that a higher proportion of independent board members improves board effectiveness, reduces agency conflicts and information asymmetry, and promotes greater corporate information disclosure. When independent directors hold a majority on the board, they can empower the board to compel management to provide more comprehensive information (Anojan, 2024). Independent directors often focus on monitoring firm behaviour and are committed to improving corporate reputation, which can lead to higher-quality disclosures. Additionally, since independent directors are less influenced by competitive pressures compared to executive directors, they are more likely to address emerging information demands (García-Sánchez et al., 2023). Bamahros et al. (2022) emphasise that board independence, combined with relevant expertise and due diligence, can motivate management to uphold high standards of transparency, integrity, and disclosure practices. Cooray et al. (2020) further assert that boards with a greater number of independent directors are more likely to voluntarily disclose comprehensive forward-looking quantitative and strategic information.

Empirical investigations into the relationship between board independence and IRQ across various countries have yielded mixed results. For example, Sobhan and Mia (2024) examined IR practices in Bangladesh, India, and Sri Lanka and found a positive and significant association between board independence and IRQ. Other studies (Anojan, 2024; Ahmed, Hassan, & Magar, 2024; Chouaibi, Chouaibi, & Zouari, 2022; Qaderi et al., 2022) have also reported a positive correlation between board independence and IRQ.

On the other hand, some researchers have observed an unexpected negative relationship between board independence and IRQ (Ahmed, 2023; Cooray et al., 2020; Zampone et al., 2024). Moreover, Halid, Mahmud, Zakaria, and Rahman (2021) found no empirical support for a connection between director independence and IRQ. Notably, the impact of independent directors on IR disclosure within the South African context remains unclear. Given these conflicting findings and the limited research focused on South Africa, the present study aims to address this gap. Therefore, it was hypothesised that,

H2: Board independence has a significant impact on IRQ.

2.2.5. Board Gender Diversity and Integrated Reporting Quality

Gender diversity is a crucial component of corporate governance and significantly affects board decision-making processes, particularly regarding the quality of corporate reporting (Centinaio, 2024). The King V Report on Corporate Governance defines diversity as "the varied perspectives and approaches offered by members of different identity groups" (IoDSA, 2025, p. 12). This definition includes a range of factors, such as diversity in expertise, competencies, and backgrounds, along with demographic aspects like age, cultural background, ethnicity, and gender.

Cooray et al. (2020) argue that female board members play a vital role in enhancing corporate reputation by prioritising social issues. Similarly, Qaderi et al. (2022) assert that including women on corporate boards brings additional expertise, experience, and skills, which strengthens the board’s monitoring functions, reduces information asymmetry, and alleviates agency problems. Furthermore, Cooray et al. (2020) note that boards with a higher representation of women tend to produce higher-quality voluntary disclosures.

The presence of women on corporate boards is widely recognised as an indicator of effective governance and acts as a catalyst for increased transparency and accountability in non-financial reporting (Zampone et al., 2024). Therefore, promoting gender diversity within boards is essential for fostering balanced decision-making and improving governance practices (Denhere, 2024). However, Denhere (2024) observes that boards with higher female representation may still face challenges in enhancing the quality of IR disclosures.

An investigation conducted by Issa, Zaid, Hanaysha, and Gull (2021, p. 22), which examined the impact of board diversity on voluntary corporate social responsibility (CSR) disclosures among banks listed in the Arabian Gulf Council countries from 2011 to 2019. Their results indicated a significant negative association between gender diversity on boards and the extent of voluntary CSR disclosures. This suggests that firms with a higher proportion of female directors may be less inclined to disclose non-financial information, potentially diminishing the overall quality of corporate disclosures.

In contrast, research by Toerien, Breedt, and de Jager (2023) in South Africa investigated the relationship between board gender diversity and environmental, social, and governance (ESG) disclosures among companies listed on the JSE. Using panel regression analysis on an unbalanced dataset comprising 92 companies (equivalent to 725 company-years) listed on the JSE All Share Index between 2011 and 2021, the study identified a positive correlation between female board representation and the extent of ESG disclosures. However, Toerien et al. (2023) acknowledge a limitation in their study, noting that the sample was restricted to only 92 companies listed on the JSE FTSE All Share Index.

Zampone et al. (2024) conducted an empirical investigation into the relationship between board gender diversity and the disclosure of Sustainable Development Goals (SDGs) on a global scale over time. Their study analysed annual progress reports from 526 firms across 39 countries and ten industry sectors during the period from 2017 to 2020, aiming to assess the extent of SDG disclosure. The results indicated a positive association between board gender diversity and the level of SDG disclosure. Furthermore, the study revealed that this relationship is mediated not only directly by gender diversity but also through the presence of a sustainability committee. However, a notable limitation of Zampone et al.'s (2024) research is its exclusive focus on the largest multinational corporations, which does not account for sector-specific variations. It is critical to recognise that board gender diversity may influence corporate disclosure differently across various industry sectors. To address this limitation, the current study aims to examine board gender diversity across all ten industry sectors represented on the JSE.

In a recent study, Centinaio (2024) employed a Systematic Literature Network Analysis to synthesise existing research on the impact of board gender diversity on corporate disclosure practices. Most of the reviewed literature supports a positive correlation between board gender diversity and both the extent and quality of corporate disclosures. However, some studies report divergent findings, highlighting the need for further research to enhance understanding of how increased gender equality on boards may promote improved corporate communication and transparency.

Given the inconsistent findings in the existing literature, further empirical investigation is necessary to clarify the impact of board gender diversity on IRQ, particularly within the context of the South African market. Therefore, it was hypothesised that,

H3: Board gender diversity has a significant impact on IRQ.

2.2.6. Audit Committee Size and Integrated Reporting Quality

The audit committee serves as a representative body of corporate boards and plays an active role in evaluating organisational practices related to corporate reporting and internal controls, with the goal of improving the quality of financial reporting (Qaderi et al., 2024). Including independent non-executive members who possess the necessary financial literacy, skills, and experience on audit committees enhances effective oversight of both financial and non-financial reporting. This setup helps to reduce information asymmetry and agency conflicts between management and stakeholders (Mohammadi et al., 2021).

From the perspective of agency theory, audit committees are crucial in protecting stakeholder interests by functioning as internal governance mechanisms. They reduce information asymmetry by overseeing financial and non-financial disclosures, external audits, and internal control systems (Pozzoli et al., 2022). Mwangi et al. (2024) argue that audit committees with a higher proportion of independent directors who have financial expertise are better equipped to fulfil essential responsibilities. This includes influencing board decisions, ensuring the accuracy and reliability of information disclosed by the board, and overseeing both the disclosure process and the work of independent auditors. Additionally, Cooray et al. (2020) suggest that independent members of audit committees tend to seek higher assurance levels and better support both internal and external auditors in conducting more rigorous testing procedures.

The existing literature documents a significant positive impact of audit committee characteristics on various forms of corporate disclosure, such as corporate social responsibility (CSR) reporting (Mohammadi et al., 2021; Qaderi et al., 2020), risk disclosure (Almunawwaroh & Setiawan, 2023), forward-looking disclosure (Al Lawati et al., 2021), and sustainability reporting practices (Pozzoli et al., 2022). Moreover, prior studies have examined the influence of specific audit committee attributes—including size, independence, financial expertise, and meeting frequency—on information quality, yielding mixed and sometimes conflicting findings. Research by Mohammadi et al. (2021), Qaderi et al. (2024), and Raimo et al. (2020) across various countries indicates a positive association between audit committee size and the quality of corporate disclosures.

Arinta and Ashari (2022) conducted a study to investigate the impact of Islamic corporate governance mechanisms on the quality of IR in 12 Islamic banks. Their findings revealed that the presence of independent commissioners and certain characteristics of the audit committee, including the number of members, their educational qualifications, and the frequency of meetings, have a positive and significant effect on the improvement of IRQ.

Belhouchet and Chouaibi (2024) explored the relationship between audit committee attributes and the quality of IR by analysing data from 360 European firms listed on the STOXX Europe 600 index over the period from 2010 to 2021. Their findings suggest that both the independence of audit committee members and the frequency of their meetings are positively correlated with IRQ.

However, while some studies report no significant relationship between audit committee size and IRQ in the South African context (Ahmed, 2023; Erin & Adegboye, 2021), others have found a positive correlation (Erin & Adegboye, 2022; Wang et al., 2020). These inconsistent results across different national contexts highlight the need for further research to clarify the impact of audit committee size on IRQ. This study aims to fill this gap and contribute to the ongoing academic discussion on this topic. Therefore, it was hypothesised that,

H4: Audit committee size has a significant impact on IRQ.

2.2.7. Mediating Role of Firm Performance

The performance of a company, which encompasses financial, operational, and market growth, is closely tied to its value in terms of profitability and meeting the expectations of stakeholders (Islam, 2021; Khunkaew et al., 2023). Scholars have measured firm performance using financial and operational indicators such as revenue growth (Darminto et al., 2024), total sales, net profit, return on assets, and return on equity (Darminto et al., 2024), and market indicators such as share price and earnings per share (Pathiraja & Priyadarshanie, 2020).

According to Darminto et al. (2024), highly profitable companies are more likely to disclose forward-looking information in integrated reports, which can help them identify new opportunities for developing profitable business segments. Darminto et al. (2024) further observe that companies with greater profitability may not feel as compelled to engage in IR to attract investors or lenders, as they believe that strong financial performance alone is sufficient to earn stakeholders' trust and attract investments. Consequently, these companies may have less motivation to adopt IR practices that focus on non-financial aspects and long-term sustainability.

Darminto et al. (2024) observe that companies with limited growth potential are often encouraged by stakeholders such as investors and shareholders to concentrate on achieving financial goals and enhancing operational efficiency. From the perspective of agency theory, producing high-quality integrated reports serves as an effective way to communicate organisational performance to the investor community, capital markets, and other beneficial stakeholders (Senani et al., 2022). Additionally, these reports help mitigate the information asymmetry problem between the board and shareholders, as well as reduce agency costs, and ultimately enhance corporate value (Senani et al., 2022).

Various researchers have presented empirical findings relating to the association between corporate governance and firm performance (Atugeba & Acquah-Sam, 2024; Gezgin et al., 2024; Bui & Krajcsák, 2024; Miao et al., 2023; Osinupebi & Bodunde, 2025; Shakri et al., 2024). For instance, Atugeba and Acquah-Sam (2024) indicate that corporate governance practices negatively impact firm performance. Conversely, the findings by Osinupebi and Bodunde (2025) reveal a significant positive correlation between IR and financial performance, as measured by return on assets. Their research also demonstrates that corporate governance moderates this relationship, whereby a stronger governance framework enhances the association between IR and financial performance.

Another strand of literature has studied the relationship between firm performance and IRQ (Alatawi et al., 2025; Darminto et al., 2024; Oyong et al., 2022; Pathiraja & Priyadarshanie, 2020). For example, Islam (2021) conducted a study that examined the disclosure practices of IR and their relationship with a company's operational, financial, and market growth performance indicators, specifically return on assets, return on equity, and market-to-book value ratio. The study's empirical findings revealed a significant positive relationship between the IR disclosure index and all three-performance metrics. Furthermore, a content analysis of the integrated reports indicated an increasing trend in the disclosure of the index elements by the sampled companies. The study by Islam (2021) is limited by its focus solely on companies within non-financial sectors, overlooking other industry sectors. This constraint hinders the generalisability of the results to a wider context.

Bek-Gaik and Surowiec (2021) conducted a study to explore the relationship between various aspects of a company's current financial performance, such as total assets, equity capital, sales revenue, return on equity, return on assets, net profit, and earnings per share, and the quality of forward-looking disclosure in IR. Their analysis found that factors such as equity level and sales revenues were positively associated with the quality of forward-looking disclosures. However, there was no significant correlation observed between indicators like return on equity, return on assets, net profit, earnings per share, and the quality of forward-looking disclosures.

Studies by Cojocaru et al. (2024) and Mediaty and Pratiwi (2023) found that profitability does not significantly affect the quality of IR. This is because profitability mainly emphasises financial performance and corporate earnings, while IR aims to combine financial aspects with sustainability factors such as social, environmental, and governance issues. On the other hand, Darminto et al. (2024) found that revenue growth has a negative influence on IRQ. This implies that companies with low or stagnant growth rates may struggle to prioritise sustainability and social responsibility in IR.

Overall, prior research has yielded mixed results regarding the relationship between firm performance and corporate governance, as well as with IRQ. However, there remains a significant lack of empirical evidence regarding the mediating role of firm performance in the relationship between board composition and IRQ, which has been overlooked in the existing literature. Consistent with agency theory and supported by findings from existing literature, the following hypothesis was formulated:

H5: Firm performance moderates the relationship between board composition and IRQ.

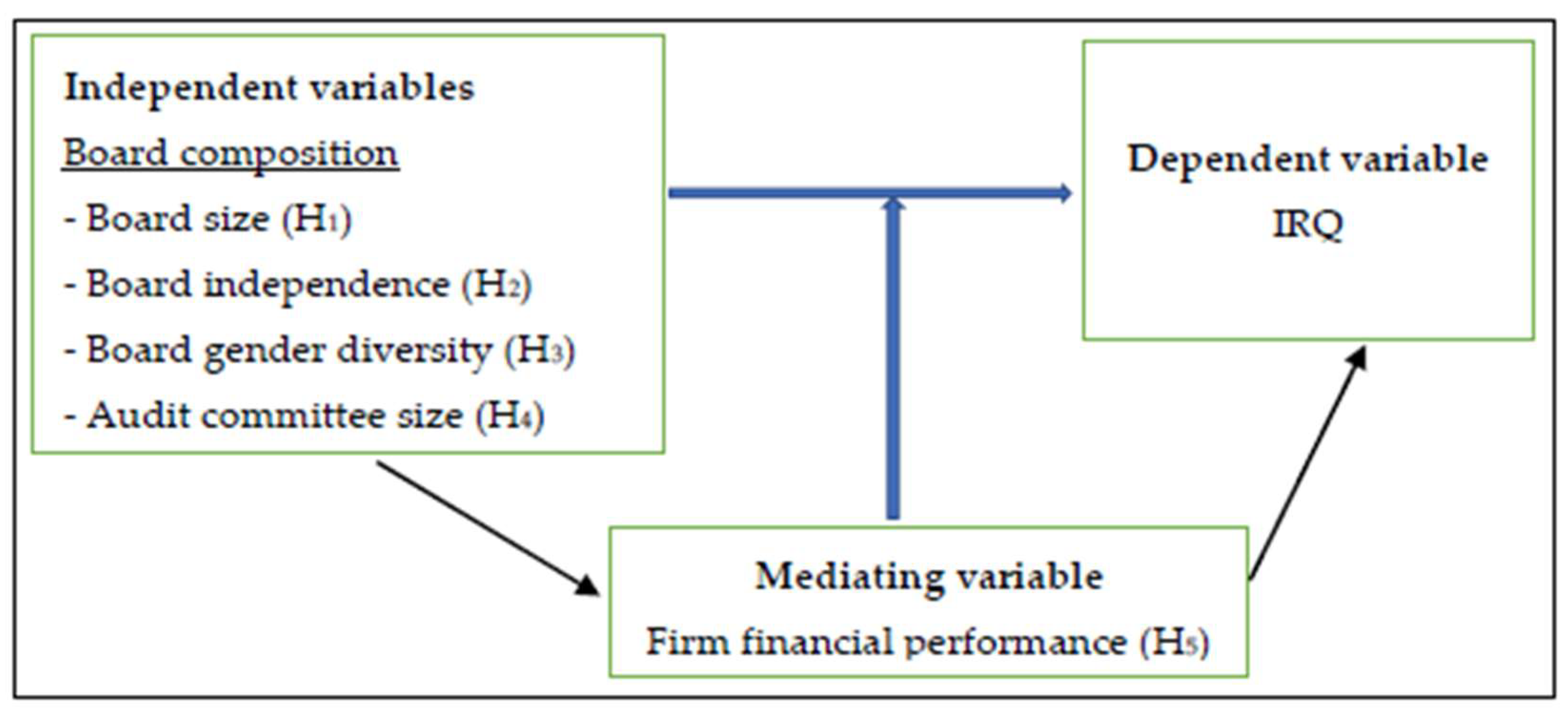

2.3. Conceptual Framework

This study aims to enrich the existing literature by identifying and testing some characteristics of board composition that can be considered as determinants of IRQ. Previous literature suggests that the quality of corporate disclosure and IR is affected by the characteristics of the board, specifically by its size (Amanamah, 2024; Devarapalli & Mohapatra, 2024; Lawal & Yahaya, 2024; Munisi, 2023; Qaderi et al., 2022), independence (Anojan, 2024; Ahmed et al., 2024; Chouaibi et al., 2022), gender diversity (Centinaio, 2024; Denhere, 2024; Toerien et al., 2023; Zampone et al., 2024), and audit committee size (Mwangi et al., 2024; Almunawwaroh & Setiawan, 2023; Belhouchet & Chouaibi, 2024). The conceptual framework depicted in Figure 1 provides a comprehensive overview of the key variables under investigation, and shows how firm financial performance may mediate the relationship between board composition and IR quality.

3. Materials and Methods

This study uses an inductive approach to examine the relationship between board composition and IRQ within JSE-listed companies from 2020 to 2024 and whether this relationship is mediated by firm performance.

3.1. Population and Sample Selection

The primary objective of this study is to investigate the relationship between board composition and IRQ among companies listed on the JSE, as well as to examine whether this relationship is mediated by firm performance. The study population consists of all 348 firms listed on the JSE across various sectors for the financial years ending between 2020 and 2024. To be included in the study, a company must have maintained a continuous listing on the JSE as of June 30 for each year from 2020 through 2024. This population is suitable for providing relevant data to address the research objectives, as all companies with a primary listing on the JSE are required to produce integrated reports (EY, 2023; Mokabane & du Toit, 2022). Out of the 348 listed firms, 308 hold primary listings, while 40 have secondary listings on the JSE. Although IR is compulsory for companies with primary listings, firms with primary listings on foreign stock exchanges and secondary listings on the JSE often voluntarily prepare integrated reports (Mokabane & du Toit, 2022).

In the initial phase of the study, the authors used a stratified sampling method to categorise all 348 companies listed on the JSE into their respective industry sectors, identifying 11 distinct industries (see Table 1). This stratification was crucial due to the diverse and unrelated nature of the business sectors in which these companies operate. Following this, a proportionate probability sampling approach was employed to select samples from each identified industry cluster. This technique ensures adequate representation of each subgroup (stratum) within the overall population (Aubry et al., 2023). The application of this sampling strategy recommended a minimum sample size of 110 companies, which corresponds to 31.7% of the total population (N = 348) of firms listed on the JSE as of June 30 for the years 2020 through 2024. This sample size was considered sufficient to guarantee representation across all industry sectors within the JSE, with each company within an industry having an equal probability of selection (Aubry et al., 2023). The composition of the sample is detailed in Table 1, which outlines the industry classification, the number of companies per industry, population percentages, the final sample size, and observations per industry.

As noted in Table 1, no companies were listed under the utility industry at the time of data collection, resulting in the exclusion of this sector from subsequent analyses. 9).

3.2. Measurement of Research Variables

3.2.1. Dependent Variable

The dependent variable in this research is IRQ, which is operationalised as a weighted disclosure score derived from the content elements of IR included in a disclosure index. Specifically, the proxy used is the aggregate IRQ scores for each of the five years under review (2020–2024).

There are two main approaches to employing disclosure indices (Abasi et al., 2022). The first involves using an externally developed disclosure index, while the second entails constructing a customised index tailored to the specific research context (Bondar et al., 2024; Chikutuma, 2024). This study adopts the latter approach by developing a self-constructed weighted disclosure index, also known as a polychotomous disclosure index. This index is contemporary and comprehensive, encompassing all eight content elements of the IIRF. It was developed using the IR disclosure requirements specified in the 2021 edition of the IIRF, published by the IIRC (IIRF, 2021).

The coding of the disclosure index employed two types of ordinal scoring systems, as detailed in Table 2: a 0–3 scale and a 0–4 scale, depending on the nature of the disclosed item as mandated by the IIRF. Using these ordinal scoring systems, the overall disclosure index has a maximum possible score of 219, as shown in Table 3.

The IRQ score is expressed as a percentage of the maximum possible score, as shown in Figure 2. This is calculated using the following formula:

Where:

| IRQit = | IRSit | X 100 | …………….Formular 1 |

| Maximum achieved score |

- IRDit indicates the extent and quality of IR for firm i in year t; and

- IRSit represents the IR disclosure score of firm i at time t.

3.2.2. Empirical Model

Since both the dependent, independent, and mediating variables for this study are continuous, the multivariate linear ordinary least squares (OLS) regression model was used. In this analysis, board composition is considered the independent variable. Four indicators serve as proxies for board composition: board size, board independence, board gender diversity, and audit committee size (model 1). These variables collectively facilitate an analysis of how board composition affects IRQ. Model 2 incorporates an additional mediating variable, firm performance, which interacts with key independent variables. The inclusion of the moderating effect provides further depth on how the relationship between board composition and IRQ may be contingent on the firm's financial performance.

Table 4 below presents the codes, conceptual definitions, and proxies for the dependent, independent and mediating variables. The model specification is as follows:

Empirical model : IRQ = β0 + β1BoC + εᵢ

Model 1: IRQ = β0 + β1BSIZE +β2BINDP + β3BGDIV + β4ACSIZE+ εᵢ

Model 2: IRQ = β0 + β1BSIZE + β2BINDP + β3BGDIV + β4ACSIZE + β2PERF + β1(BSIZE*PERF) + β2(BINDP*PERF) + β3(BGDIV*PERF) + β4(ACSIZE*PERF) + εᵢ

Where:

IRQ = Integrated report quality

β0 = constant (intercept) of proportionality in the regression model, representing the unaccounted variables affecting IRQ.

β1-4 = regression coefficients (slope) for respective variables.

εᵢ = error estimation reflecting the difference between predicted and observed values of IRQ.

BSIZE Board size

BINDP Board independence

BGDIV Board gender diversity

PERF Firm performance

3.2.3. Control Variables

In line with previous research, this study includes several control variables to improve the explanatory power of the regression models, addresses their influence and minimises potential bias from omitted variables. Following the approach of Bui and Krajcsak (2024), the study includes two control variables, firm size and firm age to represent firm-specific effects, with their definitions provided in Table 4 above. Specifically, firm size (FSIZE) is measured as the natural logarithm of the firm's total market capitalisation (in billion Rands) at the end of each financial year under review (2020-2024) in accordance with established studies (Khatlisi & Mashamba, 2025; Susianti & Oktorina, 2023), as larger and older firms typically disclose more IR information. Firm age (FAGE), defined as the natural logarithm of the total number of years listed on the JSE at the end of each financial year under review (Obeng et al., 2020), serves as an additional control variable and reflects the tendency for older firms to enhance their IR disclosures.

3.2.4. Diagnostics Tests

While ordinary least squares (OLS) regression is a widely used statistical method, it has certain limitations, such as sensitivity to outliers, multicollinearity, and a tendency to overfit data. To address these issues, several advanced statistical techniques have been developed. Before conducting regression analyses, diagnostic tests were performed to evaluate the data for multicollinearity, heteroscedasticity, and autocorrelation. This ensured the data's suitability in order to prevent misleading conclusions. To mitigate the impact of outliers, all continuous variables were winsorized at the 1st and 99th percentiles. A variance inflation factor (VIF) analysis was conducted to assess multicollinearity among the independent and mediating variables. The results indicated that none of the variables demonstrated problematic multicollinearity, with VIF values ranging from 1.105 to 3.110as shown in Table 6. According to the criteria established by Kyriazos and Poga (2023), multicollinearity is considered negligible when all VIF values are below the threshold of 10. Additionally, the Durbin-Watson test was used to examine autocorrelation in the error terms, revealing no evidence of autocorrelation, with a Durbin-Watson statistic of 1.7084 (refer to Table 7). Standard guidelines suggest that Durbin-Watson values between 1.5 and 2.5 are generally acceptable (Durbin & Watson, 1950), while values outside this range may warrant further investigation. Consequently, OLS regression was deemed an appropriate method, providing reliable estimates and unbiased standard errors.

4. Results

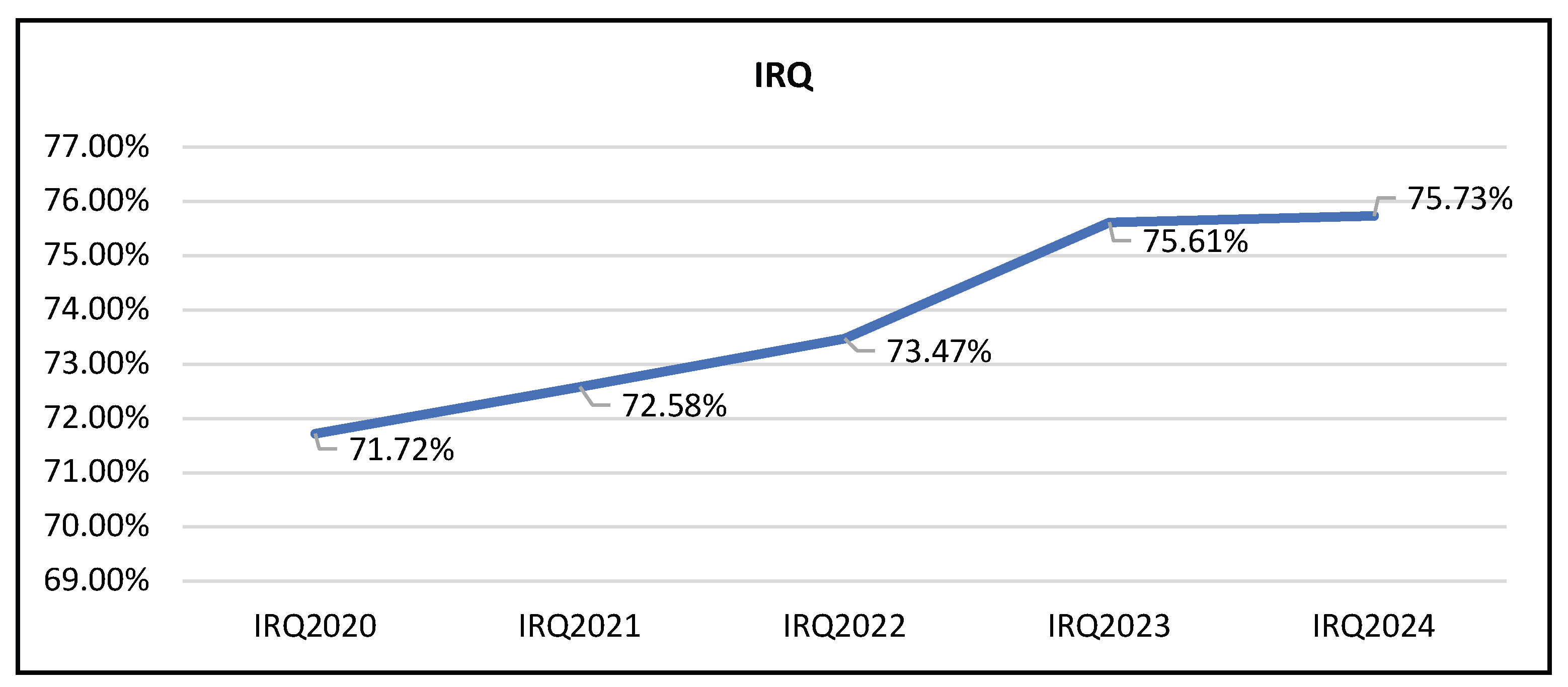

Statistical Package for Social Sciences (SPSS) was used for data analysis. This tool allowed the researchers to investigate the mediating effects and assess hypothesised correlations between the variables. Descriptive statistics, correlation analysis and multivariate OLS regression models were used to analyse the data. The dataset underwent a thorough cleaning process and was subsequently evaluated for accuracy, missing values, multicollinearity, and outliers. No missing data were identified. Table 5 presents the descriptive statistics for the analysed variables, including the Variance Inflation Factor (VIF) values. The analysis includes 550 firm-year observations from a sample of 110 companies listed on the JSE. Firstly, the results of the average IRQ over the five-year period under review are presented in Figure 2.

As shown in Figure 2, the average IRQ scores demonstrated a consistent upward trend over the five-year period: 71.72% in 2020, 72.58% in 2021, 73.47% in 2022, 75.61% in 2023, and 75.73% in 2024. This progression reflects a significant improvement in the quality of content disclosures within the integrated annual reports of companies listed on the JSE between 2020 and 2024. Moreover, these scores substantially exceed those reported by Chikutuma (2019), who documented mean annual IRQ scores of 52.45% in 2013, 58.48% in 2014, 64.72% in 2015, and 68.29% in 2016 among JSE-listed companies. The current study’s scores also surpass those reported by Islam (2021), who observed mean scores of 65.97% in 2016 and 65.83% in 2017, followed by a marked increase in 2018, exceeding the 70.00% threshold for a sample of 20 firms listed on the Dhaka Stock Exchange from 2015-2018.

The high IRQ score observed in this study may be due in part to the fact that several universities in South Africa are now offering comprehensive academic programs in IR. These programs have equipped report preparers with the necessary skills and competence to produce high-quality integrated reports (Oben, 2025). The upward trend in IRQ observed in our study could also be attributed to the accumulated experience of JSE-listed entities in preparing Integrated Annual Reports over time (Chikutuma, 2019). It is also possible that the introduction of the revised IIRF in 2021 contributed to this positive development. This upward trend suggests that companies are increasingly articulating their value creation capabilities in a manner that aligns with their unique business contexts (EY, 2024). The observed positive trend in overall mean IRQ scores over the five years supports the fundamental principles of stakeholder theory, which suggests that companies can enhance the quality of their integrated reports to address the informational needs of key stakeholder groups, as well as provide a holistic view of the companies' ability to generate long-term value for all stakeholders (IIRC, 2021; Karim et al., 2024; Kılıç et al., 2021; Mokabane & Du Toit, 2022; Sun et al., 2022, Wahl et al., 2020).

4.1. Descriptive Statistics and Univariate Analysis

Focusing on the dependent variable, IRQ, the minimum recorded score was 20.70%, while the maximum reached 95.90%, indicating a substantial range between these two extremes. This variation suggests that while some companies in the sample demonstrate near-complete compliance with the IIRF, others fall significantly behind. A plausible explanation for this discrepancy is that companies with a primary listing on the JSE are required to prepare integrated reports, while those with a secondary listing do so voluntarily. The mean IRQ score of 73.8230% indicates a central tendency around which the data are concentrated, suggesting that, on average, the quality of integrated reports among the sampled JSE-listed firms is relatively high compared to previous studies, such as those conducted by in South Africa (see Bondar et al., 2024; Boujelben et al., 2024; Eloff & Steenkamp. 2022; Mans–Kemp & van der Lugt, 2020; Marrone & Oliva, 2020; Mokabane & du Toit, 2022; Toerien et al., 2023), Islam (2021) in Bangladesh, Sun et al (2022) in China and Nada and Győri (2023) in Europe. The standard deviation of 16.71156 for IRQ also reflects considerable variability in compliance with the IIRF among the sampled companies.

The board size ranges from a minimum of 4 members to a maximum of 22, with an average board size of 10.8091 members and a standard deviation of 3.24050. These findings indicate that, on average, the sampled companies comply with Section 66 of the South African Companies Act 71 of 2008, which requires public companies to have at least three directors. Regarding board independence, the average number of independent directors is 6.7218, with values ranging from two to fifteen members and a standard deviation of 3.11248.

In terms of gender diversity, the boards include an average of 3.6709 female members, ranging from 1 to 8 members, with a standard deviation of 1.61923. This highlights a significant lack of gender diversity in the board compositions of certain companies listed on the JSE. The size of the audit committees varies from two to ten members, with an average of 3.9255 and a standard deviation of 0.94468. These findings indicate that, on average, the companies comply with the requirements of section 94 of the Companies Act 71 of 2008, which mandates that audit committees consist of at least three members.

Firm performance (PERF), operationalised as net profit after tax (net income) measured in millions of South African Rands at the end of each financial year under review, provides insights into the financial performance of the sampled companies. The mean PERF is reported as R5,748.6906 million, serving as an indicator of overall profitability. The standard deviation of PERF, calculated at R49,067.86274 million, reflects substantial variability in net profit after tax across the firms, indicating a wide dispersion in financial performance. The minimum and maximum PERF values are -R707,583.00 million and R517,643.10 million, respectively, facilitating the identification of firms with the lowest and highest net profits and enabling a comprehensive evaluation of the heterogeneity in their financial performance.

In terms of firm size, the market capitalisation ranges from a minimum of ranges from a minimum of R0.03 billion to a maximum of R2343.80 billion, with a mean value of R65.6308 billion. The standard deviation of R234.68469 billion reflects considerable heterogeneity in firm size within the sample. Regarding firm age (FAGE), the sample encompasses firms aged between 4 and 82 years, with an average age of 27.8250 years. This suggests that the firms included in the study are relatively mature, with a mean operational duration of approximately 28 years. The standard deviation of 21.10952 years denotes substantial variability in the length of time these firms have been listed on the JSE.

4.2. Hypothesis Testing

4.2.1. Correlation Analysis

Since the dependent variable (IRQ) was measured on an ordinal scale and the independent variables were continuous, we employed Pearson correlation analysis to evaluate the strength and direction of the linear relationships between these variables. The results of the Pearson correlation matrix for the variables studied are presented in Table 6. A statistical significance level of 1% (p < 0.01) is indicated by **, and significance at the 5% level (p < 0.05) is denoted by *.

All the independent variables, BSIZE (r = 0.216), BINDP (r = 0.191), BGDIV (r = 0.200), and ACSIZE (r = 0.101), show very weak positive correlations with the dependent variable IRQ. These results suggest that companies with large board size, independence and audit committee size are likely to produce high-quality integrated reports. A large board size and audit committee size, as well as the presence of independent members on the board, may have greater collective oversight and monitoring capabilities, as highlighted in the agency theory (El-Deeb & Mohamed, 2024). This observation is consistent with the findings of Songini et al. (2022), who reported a weak positive statistical relationship between IRQ and both BSIZE and BINDP, while revealing a negative association between BGDIV and IRQ.

The positive statistical relationship between IRQ with FSIZE (r = 0.194) and FAGE (r = 0.084) suggests that larger and older companies in this sample are more likely to comply with the IIRF by producing high-quality integrated reports. In contrast, the variable PERF did not show any statistically significant associations with IRQ. This suggests that the financial performance of JSE-listed firms may not directly impact the quality of the integrated reports produced by these companies. These findings align with those of Senani, Ajward, and Kumari (2024), who discovered that profitability (financial performance) does not have a systematic or significant relationship with IRQ. This underscores the complexity of compliance determinants, which are influenced by multiple factors rather than solely by any single governance or firm characteristic. Further regression analysis is warranted to isolate the predictive effects of these variables.

Table 6.

Pearson correlation coefficient for the association between variables.

| Variables | IRQ | BSIZE | BINDP | BGDIV | ACSIZE | PERF | FSIZE | FAGE | VIF |

| IRQ | 1.000 | ||||||||

| BSIZE | 0.216** | 1.000 | 3.110 | ||||||

| BINDP | 0.191** | 0.762** | 1.000 | 2.951 | |||||

| BGDIV | 0.200** | 0.649** | 0.622** | 1.000 | 1.920 | ||||

| ACSIZE | 0.101* | 0.573** | 0.601** | 0.520** | 1.000 | 1.773 | |||

| PERF | 0.019 | -0.005 | 0.018 | 0.026 | -.099* | 1.000 | 1.025 | ||

| FSIZE | 0.194** | 0.202** | 0.016 | 0.099* | 0.013 | 0.013 | 1.00 | 1.106 | |

| FAGE | 0.084* | 0.039 | 0.190** | 0.128** | 0.204** | -0.049 | -0.120** | 1.000 | 1.105 |

**. Correlation is significant at the 0.01 level (2-tailed). * Correlation is significant at the 0.05 level (2-tailed).

Table 7.

Ordinary least squares regression analysis.

| Model 1 | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | |||

| B | Std. Error | Beta | |||||

| IRQ | 65.574 | 3.170 | 20.685 | 0.000 | |||

| BSIZE | 0.713** | 0.344 | 0.143 | 2.070 | 0.039 | ||

| BINDP | 0.299 | 0.357 | 0.058 | 0.838 | 0.403 | ||

| BGDIV | 0.976* | 0.518 | 0.108 | 1.886 | 0.060 | ||

| ACSIZE | -1.237 | 0.924 | -0.073 | -1.339 | 0.181 | ||

| Model summary | ANOVA | ||||||

| R | 0.238a | ||||||

| R Square | 0.056 | Regression | Residual | Total | |||

| Adjusted R Square | 0.049 | Sum of Squares | 8032.251 | 134345.556 | 142377.807 | ||

| Std. Error of the Estimate | 15.70050 | df | 4 | 545 | 549 | ||

| Durbin Watson | 1.7084 | Mean Square | 2008.063 | 246.506 | |||

| F | 8.146 | ||||||

| Sig. | <.001b | ||||||

Note(s): ***, **, *denotes significance at 1%, 5%, and10% levels respectively.

4.2.2. Multivariate Ordinary Least Squares Regression Analysis

The study uses a linear regression model to examine the relationship between the dependent variable IRQ and the independent variables BSIZE, BINDP, BGDIV and ACSIZE. Model 1 examines the relationship between board composition and IRQ. In contrast, Model 2 evaluates the mediating effect of firm performance on the association between board composition and IRQ among firms listed on the JSE. The results are presented in Table 7 and Table 8, respectively.

Consistent with the Pearson correlation results reported in Table 6, board size (BSIZE) exhibits a positive and statistically significant relationship with IRQ (p=0.039), with a coefficient of 0.713 at the 5% significance level. This supports hypothesis H1, which posits a positive and statistically significant association between board size and IRQ among JSE-listed companies. These findings indicate that firms with larger boards tend to produce higher-quality integrated reports than those with smaller boards.

Board independence, with a coefficient of 0.299, does not show a statistically significant relationship with IRQ (p = 0.403). In contrast, board gender diversity has a positive and statistically significant association with IRQ, indicated by a coefficient of 0.976 and a significance level of 10% (p = 0.060). This finding is further supported by correlation analysis, which demonstrates a positive correlation between BGDIV and IRQ (r = 0.200) at the 1% significance level. These results suggest that firms with greater female representation on their boards tend to produce higher-quality integrated reports. Conversely, the size of the audit committee does not show a statistically significant relationship with IRQ (p = 0.181).

The regression analysis resulted in an R squared value of 0.056 and an adjusted R squared of 0.049, indicating that the independent variables explain a small portion (5.6%) of the variance in the dependent variable. This suggests that there are likely other factors, not included in this study, influencing IRQ. The F-statistic was F(4, n) = 8.146, with a significance level of p < 0.001, indicating that the independent variables significantly predict the dependent variable, which confirms the overall suitability of the regression model for the data. These results imply that the model is modestly effective in explaining the variability in IRQ compared to a null model that lacks predictors.

4.2.3. Robustness Analysis: Mediating Role of Firm Performance

To further validate our findings, additional analyses were conducted to explore the moderating effect of firm performance on the relationship between independent board composition (BSIZE, BINDP, BGDIV, and ACSIZE) and IRQ. The overall model was significant (p < 0.001) and explained 5.65% of the variance in IRQ. Given the significance of the regression tests, we employed the PROCESS Procedure for SPSS Version 5.0. These findings support the robustness of our results. Following the approach of Amanamah (2024), Bui and Krajcsák (2024), and Mshana, Mzenzi, and Suluo (2025), we excluded control variables and re-estimated the empirical regression model. Importantly, our analysis showed that the control variables did not influence the primary results, confirming the stability of all research variables, as presented in Table 7.

The results in Table 8 demonstrate that the effects of all variables remain consistent with those reported in Table 7, indicating a direct, positive, and significant association between the independent variable BIZE and IRQ (coefficient = 0.7142, p = 0.0388) without the mediation of performance (PERF). Additionally, these results support the conclusions of Chouaibi et al. (2022), whose empirical study identified a positive and significant relationship between the total number of board directors and IRQ. BINDP does not show a significant unique effect on IRQ in this model (p = 0.4111). Additionally, the results reveal that the direct effect of BGDIV is positive and statistically significant (p = 0.0620) at the 10% level, with a confidence interval of 0.9703. Furthermore, ACSIZE does not exhibit a significant unique effect on IRQ in this model (p = 0.4111). However, there was no evidence of mediation, suggesting that firm performance does not mediate the relationship between board composition and IRQ.

6. Discussion

This study examines the relationship between board composition and IRQ and whether this relationship is mediated by firm performance. The findings indicate a positive trend in the quality of content elements disclosures within the integrated annual reports of companies listed on the JSE from 2020 to 2024. This upward trend in IRQ can be attributed to the incorporation of key elements of integrated reporting, including governance, risk management, and strategic management, into the accounting curriculum in South Africa. This integration may have equipped preparers of integrated reports with the skills and knowledge necessary to produce high-quality reports (Oben, 2025).

The empirical evidence reveals that various board characteristics do not uniformly impact the quality of integrated reports issued by JSE-listed companies. The variable board size (BSIZE) and board gender diversity (BGDIV) are seen to have a substantial impact, serving as important factors influencing IRQ.

The observed positive and significant relationship between board size and IRQ suggests that board size serves as an effective governance mechanism for overseeing IR. This finding implies that board members may place greater emphasis on information relevant to IR. These results align with prior research (Amanamah, 2024; Cooray et al., 2020; Devarapalli & Mohapatra, 2024; Mawardani & Harymawan, 2021; Mohammadi et al., 2021; Qaderi et al., 2022), which similarly identified a significant positive relationship between board size and IRQ across various national contexts. This finding aligns with agency theory, which suggests that board size is an indicator of managerial competence and reflects effective monitoring practices. These practices help mitigate information asymmetry and agency conflicts between managers and stakeholders (Cooray et al., 2020). Ultimately, enhanced transparency contributes to reducing information asymmetry, lowering agency costs, and decreasing the cost of capital (Pozzoli et al., 2022). From the perspective of stakeholder theory, the positive and significant association between board size and IRQ may be attributed to stakeholders relying more heavily on publicly available information, which is enhanced by direct insights from the board.

The statistically significant positive association between board gender diversity and the quality of integrated reports among companies listed on the JSE indicates that firms with a higher proportion of female board members tend to produce integrated reports of better quality. These findings are consistent with prior research conducted in South Africa by Toerien et al. (2023), which also identified a positive relationship between female board representation and both the extent and quality of corporate disclosures. This evidence further supports stakeholder theory, which posits that including female directors enhances a company’s ability to be attentive to and responsive to the needs and expectations of its stakeholders (Denhere, 2024). From the perspective of agency theory, an increase in female representation on corporate boards may help reduce information asymmetry and improve societal legitimacy (Mazumder, 2024; Mazumder & Hossain, 2023).

Conversely, the board is independent, and the audit committee does not have a direct and statistically significant influence on IRQ. The absence of a significant direct impact of board independence and audit committee size on IRQ may stem from the limited involvement of independent directors and the audit committee in the firm’s reporting activities. Independent directors and audit committee members are typically less engaged in the day-to-day operations (Anojan, 2024; Fun et al., 2023; Qaderi et al., 2024). Supporting this perspective, it is believed that board independence and audit committee enhances accountability, which is likely to lead to an increase in corporate disclosure. In contrast, agency theory emphasises the important role of board composition, particularly the inclusion of independent non-executive directors, in achieving effective corporate governance (Akhter, 2019).

Furthermore, there was no evidence of mediation, suggesting that firm performance does not mediate the relationship between board composition and IRQ.

6.1. Practical and Policy Implications

This study provides several practical insights for the IIRC, stock exchanges, financial capital providers, and those preparing integrated reports, whether the reporting is mandatory or voluntary. Consistent with prior research (Denhere, 2024; Qaderi et al., 2023; Samy & Mohamed, 2024), high-quality integrated reports help to build investor confidence and significantly impact investment decision-making processes. Therefore, companies should implement appropriate measures to enhance the quality of their integrated reports, ensuring their usefulness for investors.