Submitted:

23 February 2026

Posted:

25 February 2026

You are already at the latest version

Abstract

This study examines the determinants of non-performing financing (NPF) in Islamic banks operating in the Gulf Cooperation Council (GCC) over the period 2014-2024. Motivated by the growing importance of asset quality for financial stability in Islamic banking systems, the analysis integrates macroeconomic conditions and global economic policy uncertainty within a structured panel econometric framework. The empirical strategy combines fixed-effects and random-effects estimators with panel quantile regression to capture both average and regime-dependent effects across the conditional NPF distribution. The Hausman test supports the fixed-effects specification, confirming the presence of correlated unobserved heterogeneity. Mean-based results indicate that bank size is the most robust determinant of NPF, while profitability and capital adequacy do not exhibit statistically significant average effects. Quantile regression reveals substantial heterogeneity: the effect of size strengthens markedly in higher NPF regimes, while liquidity becomes a significant stabilizing factor in the upper quantile. Economic growth reduces NPF in lower quantiles but loses explanatory power in high-distress states. Inflation and global policy uncertainty show limited statistical relevance. The findings suggest that financing distress in GCC Islamic banks is primarily driven by structural characteristics and liquidity conditions rather than profitability or capital strength alone. By adopting a distribution-sensitive approach, the study contributes nuanced evidence to the Islamic banking and financial stability literature and offers implications for risk-based supervisory frameworks.

Keywords:

non-performing financing

; islamic banking

; GCC countries

; fixed effects

; quantile regression

; financial stability

; economic policy uncertainty

1. Introduction

Non-performing financing (NPF) is a core indicator of credit risk in Islamic banking because it directly reflects deterioration in the quality of Shariah-compliant financing portfolios and the likelihood of loss recognition. When NPF rises, Islamic banks typically face higher impairment and provisioning pressures, weaker profitability, and tighter capital cushions, which can reduce new financing and intensify adverse feedback to the real economy through constrained intermediation. In bank centered systems, this channel is particularly important because financing conditions transmit quickly to investment and consumption.

The Gulf Cooperation Council (GCC) provides an informative setting for examining NPF dynamics in Islamic banks. GCC Islamic banks are systemically important and operate alongside conventional banks in a dual-banking structure, while the region’s financial conditions are influenced by oil-linked macro cycles and recurrent shifts in global risk sentiment. Comparative evidence indicates that Islamic banks in the GCC differ from conventional peers in liquidity, capitalization, and credit-risk profiles, implying that the drivers of NPF may not mirror those of conventional NPLs and may vary across institutions and jurisdictions (Khediri et al., 2015). At the same time, GCC studies report meaningful heterogeneity in Islamic banks’ efficiency and performance, suggesting that managerial capability and operating environments can translate into different risk outcomes including the accumulation of problem financing (El Moussawi & Obeid, 2011; Hadriche, 2015; Hidayat et al., 2021). More directly, work linking efficiency and survival to non-performing loans in GCC banking underscores that asset quality is intertwined with banks’ resilience and internal performance conditions (ALandejani & Abdulaziz, 2014).

The determinants of NPF are usually discussed through two complementary sets of drivers. The first centers on bank-specific fundamentals capital adequacy, profitability, liquidity, size, and operational efficiency which shape screening quality, monitoring intensity, and loss-absorption capacity. In Islamic banking, portfolio structure is also critical because financing modes can affect risk exposure and performance. Evidence for GCC Islamic banks shows that financing modes are connected to risk, efficiency, and profitability in ways that can plausibly translate into NPF outcomes (Belkhaoui et al., 2020). The second set of drivers emphasizes macroeconomic and systemic conditions, where growth, inflation, credit cycles, and crisis episodes influence borrower cash flows and repayment capacity, thereby affecting the evolution of problem financing. GCC evidence supports the relevance of macroeconomic conditions and crisis periods for problem-loan behavior (Abdelbaki, 2019; Farooq et al., 2019), and more recent research highlights that global factors can jointly matter with domestic conditions in explaining problem assets in GCC economies (Kumar et al., 2023).

However, two gaps remain salient for NPF-focused evidence in GCC Islamic banking. First, many studies rely on mean-based panel estimators that identify average effects but may obscure regime dependence in credit risk. NPF dynamics can be nonlinear: the determinants of problem financing may differ between low-NPF and high-NPF states, as provisioning constraints tighten, portfolio rebalancing becomes more aggressive, and supervisory pressures intensify when asset quality deteriorates. Distribution-sensitive approaches—especially quantile methods—are well suited to uncovering such heterogeneity, and quantile-based evidence in Islamic finance and banking-performance research demonstrates that key relationships can vary meaningfully across conditional regimes (Naifar, 2016; Jawadi et al., 2017; Chowdhury et al., 2017). Second, uncertainty has become increasingly relevant for credit risk, yet external uncertainty channels are still not systematically embedded in many empirical models of Islamic-bank problem assets. Recent regional evidence indicates that U.S. and global economic policy uncertainty can significantly shape problem assets in Islamic and conventional banks, strengthening the case for incorporating uncertainty alongside bank fundamentals and domestic macroeconomic controls when modeling NPF behavior (Aledeimat & Bein, 2025).

Against this backdrop, this paper Assessing the Non-Performing Finance Determinant: Empirical Evidence from the GCC Islamic Bank re-examines the drivers of NPF in GCC Islamic banks using an empirical strategy designed to capture heterogeneity across risk regimes and to account for external risk conditions. Building on GCC evidence on problem-asset determinants (Abdelbaki, 2019; Farooq et al., 2019; Kumar et al., 2023) and on distributional approaches applied in Islamic finance (Naifar, 2016; Jawadi et al., 2017; Chowdhury et al., 2017), we adopt a framework in which the effects of capitalization, profitability, liquidity, size, and financing structure are allowed to vary across the conditional NPF distribution. The central premise is that the marginal impact of bank fundamentals on NPF should be stronger in high-NPF regimes, where balance-sheet constraints and risk controls bind more tightly, while macro-financial conditions and uncertainty shocks may exert broader influence through borrower solvency and confidence channels.

This study contributes in three ways. First, it provides updated GCC Islamic-bank evidence on NPF determinants while integrating external uncertainty as a relevant risk channel, consistent with recent regional findings (Aledeimat & Bein, 2025). Second, it moves beyond mean effects by applying quantile-based inference to test whether core bank-level drivers capital adequacy, profitability, liquidity, size, and financing-mode structure exert asymmetric impacts across low-NPF and high-NPF regimes (Belkhaoui et al., 2020; Naifar, 2016; Jawadi et al., 2017). Third, it translates these regime-specific results into more targeted implications for supervisory monitoring and bank risk management by identifying where in the NPF distribution particular determinants matter most, supporting risk-based early-warning insights rather than reliance on average relationships.

The remainder of the paper is organized as follows. Section 2 reviews the literature and develops hypotheses. Section 3 describes the data and empirical strategy. Section 4 presents the main results and robustness checks. Section 5 concludes with implications for GCC Islamic-bank risk management and prudential policy.

2. Literature Review

2.1. Islamic Banking in the GCC

Islamic banking has become a structurally significant component of the Gulf Cooperation Council (GCC) financial system, evolving from a niche segment into a mainstream intermediary that competes directly with conventional banks across retail, corporate, and investment activities. The GCC environment is distinctive because Islamic banks operate within a dual-banking structure, under relatively strong regulatory oversight, and across economies that are closely tied to hydrocarbon cycles and global financial conditions. This combination has made the region a prominent empirical setting for understanding how Sharia-compliant banking models perform, how they manage risk, and how they respond to macroeconomic and institutional drivers (El Moussawi & Obeid, 2011; Khediri et al., 2015).

A consistent theme in the GCC literature is that Islamic banks display measurable heterogeneity in efficiency and performance, reflecting differences in managerial practices, scale, market structure, and country-level governance environments. Early evidence using non-parametric efficiency techniques shows meaningful variation in productive efficiency among GCC Islamic banks, indicating that operational capability and resource allocation are central to competitiveness and resilience (El Moussawi & Obeid, 2011). Subsequent comparative research further suggests that Islamic banks cannot be treated as a simple mirror of conventional banks. Using classification techniques, Khediri et al. (2015) demonstrate systematic distinctions between Islamic and conventional institutions in the GCC, reinforcing the view that business models, balance-sheet structures, and risk profiles differ in ways that can influence performance and stability. Complementary comparative analysis also reports that the determinants of bank performance vary across Islamic and conventional banks in the GCC, implying that profitability and resilience are shaped by bank-type-specific mechanisms and may respond differently to internal and external drivers (Hadriche, 2015).

Beyond performance comparisons, GCC research emphasizes that Islamic banking outcomes are shaped by a joint set of bank-specific and institutional factors. Governance-related evidence indicates that embedding conventional governance mechanisms into the GCC Islamic banking framework helps explain variation in financial performance, supporting the argument that oversight quality and institutional design matter for Islamic banks’ outcomes (Al-Malkawi & Pillai, 2018). Similarly, studies on efficiency and pricing dynamics highlight that bank performance is linked to broader governance and institutional contexts, suggesting that country-level structures can strengthen or weaken market discipline and resource allocation within banking systems (Kamarudin et al., 2018). These findings collectively position GCC Islamic banking performance as an outcome of both internal capabilities and the broader regulatory and governance ecosystem rather than a purely contract-based phenomenon.

Methodologically, the GCC Islamic banking literature increasingly recognizes that average relationships may conceal important regime-specific patterns. While conventional panel approaches remain common, researchers have expanded the toolkit to address dynamics and heterogeneity. For example, dynamic panel methods are used to account for persistence in bank performance measures and potential endogeneity, offering more credible inference on drivers of Islamic bank outcomes in the GCC context (Chowdhury & Rasid, 2016; Chowdhury et al., 2017). At the same time, quantile-based evidence illustrates that relationships between risk factors and outcomes can differ across the distribution, which is particularly relevant in environments characterized by cyclical volatility and cross-bank heterogeneity (Jawadi et al., 2017; Naifar, 2016). This shift is important for GCC Islamic banking because it aligns empirical strategies with the reality that banks may behave differently under stress than in normal times, and that risk and performance drivers may become more pronounced in adverse regimes.

Overall, the GCC Islamic banking literature converges on three implications. First, Islamic banks in the GCC exhibit meaningful cross-bank and cross-country differences in efficiency and performance, which supports analyses that are sensitive to heterogeneity (El Moussawi & Obeid, 2011; Khediri et al., 2015). Second, institutional quality—particularly governance mechanisms—matters for performance and likely for resilience, consistent with the argument that Islamic banking outcomes depend not only on Sharia-compliant contracting but also on oversight and incentives (Al-Malkawi & Pillai, 2018; Kamarudin et al., 2018). Third, modern empirical approaches that account for dynamics and distributional heterogeneity are increasingly appropriate for GCC Islamic banking research, especially when the objective is to understand performance and risk under varying macro-financial regimes (Chowdhury et al., 2017; Jawadi et al., 2017). These insights provide a strong foundation for studies that examine GCC Islamic banks through the combined lenses of efficiency, governance, macroeconomic exposure, and regime-dependent behavior.

Empirical studies on Islamic banking in the Gulf region underscore the intricate relationshipamong financing mechanisms, asset quality, efficiency, and financial stability. Belkhawi,

Alsaghir, and Van Heemen (2020) show that the way Islamic financing works is very important for figuring out how risky and successful banks are in the GCC countries. Their findings demonstrate that profit-and-loss sharing contracts and asset-backed financing structures impact both efficiency and profitability, indicating that portfolio composition may indirectly affect financing challenges through risk exposure and operational outcomes. Additional evidence from the Saudi banking sector indicates that declining asset quality adversely affects bank performance. Al-Shabami et al. (2020) report a significant inverse correlation between non-performing loans and profitability, indicating that increased credit risk diminishes profitability and undermines financial resilience. Recent studies, particularly those examining Islamic banks in the GCC, affirm that non-performing funding is intricately associated with institutional stability. Salsabella and Jaya (2024) found that banks are less stable when they can't get enough money, but that better operational efficiency can help with this problem. These studies indicate that funding limits in Islamic banks are not merely a singular balance sheet issue, but rather integral to a comprehensive framework that includes funding structure, operational efficiency, profitability, and systemic stability. This shows how important it is to look at both the bank's internal traits and how it handles risk when trying to figure out why funding is not available.

2.2. Determinants of Non-Performing Financing

Non-performing financing (NPF) is the principal indicator used in Islamic banking to capture deterioration in financing portfolios and the associated impairment of cash flows and collateral values. Conceptually, NPF reflects both borrower-side distress and bank-side underwriting/monitoring quality, which is why it is often treated as a governance and risk-management outcome rather than a purely macroeconomic phenomenon. Evidence from Islamic banking research emphasizes that problem financing is shaped by internal balance-sheet conditions and managerial quality, consistent with the “bad management” channel in which weaker operational discipline and monitoring increase impaired financing over time (ALandejani & Abdulaziz, 2014; Muhammad et al., 2020; Widarjono & Rudatin, 2021). A systematic synthesis also concludes that determinants of problem assets in Islamic banks commonly cluster around bank fundamentals (profitability, capital, liquidity, size) and macro conditions (growth and inflation), with effects varying by sample and institutional setting (Almuraikhi, 2022).

2.2.2. Profitability (Return on Assets, ROA)

Profitability typically proxied by return on assets (ROA)is widely theorized to reduce NPF because stronger earnings capacity supports screening, monitoring, and provisioning, thereby limiting the persistence of distressed financing. Empirically, Islamic banking performance research repeatedly places profitability among the most relevant internal correlates of risk and stability (Chowdhury & Rasid, 2016; Chowdhury et al., 2017). In addition, studies that connect risk, efficiency, and performance in GCC banking show that profitability and risk management are intertwined, implying that ROA can capture both operating strength and the outcomes of risk choices (Hidayat et al., 2021). Nevertheless, the relationship is not mechanically negative in all contexts: if profitability is achieved through aggressive financing expansion or concentration in higher-risk portfolios, ROA may coincide with higher future impairment, which motivates approaches that allow heterogeneous effects across bank risk regimes (Chowdhury et al., 2017; Jawadi et al., 2017).

2.2.3. Capital adequacy (CAR)

Capital adequacy (CAR) is the principal prudential buffer expected to mitigate financing impairment by strengthening loss-absorption capacity and reinforcing market discipline. The standard view predicts a negative association between CAR and NPF because well-capitalized banks can absorb shocks without destabilizing lending/financing operations. However, capital can also correlate with risk appetite: better-capitalized banks may extend riskier financing if capital buffers loosen constraints or if governance incentives encourage expansion. Evidence on GCC banking frameworks that integrate governance into performance assessment supports the idea that capital interacts with institutional mechanisms and risk behavior (Al-Malkawi & Pillai, 2018). More recent work linking capital and problem assets to provisioning behavior in GCC banks further underscores that capital conditions are closely connected to how banks recognize and manage impairment (Elfergani et al., 2024). Hence, CAR is typically retained as a core determinant of NPF with an empirically testable sign rather than assumed monotonic protection.

2.2.4. Bank Size

Bank size (often measured as the logarithm of total assets) is theorized to influence NPF through two competing channels. The diversification and capacity channel suggests that larger banks benefit from better risk systems, data, and sectoral diversification, lowering NPF. Conversely, the complexity channel argues that larger banks can face agency problems, weaker monitoring at scale, and incentives toward risk-taking, potentially increasing impairment. GCC evidence documenting systematic differences between Islamic and conventional banks implies that size may proxy for business model, market power, and governance quality rather than scale alone (Khediri et al., 2015; Hadriche, 2015). Empirical work using distribution-sensitive methods in Islamic banking performance further supports that size effects may differ across environments and regimes (Jawadi et al., 2017).

2.2.5. Liquidity Ratio

Liquidity captures a bank’s ability to meet short-term obligations and fund financing without forced asset sales, and it is therefore central to resilience in stress periods. Higher liquidity can reduce NPF by enabling restructuring and preventing funding shocks from turning temporary repayment problems into persistent impairment. Yet, abundant liquidity can also enable rapid financing growth and relaxed screening, which may increase future NPF. Evidence in GCC banking comparing Islamic and conventional institutions shows that risk, efficiency, and performance differ systematically across bank types, indicating that liquidity management is an important channel shaping outcomes (Hidayat et al., 2021). Work focusing on financing modes in GCC Islamic banks also indicates that portfolio structure and risk are closely tied to profitability and operational performance, suggesting that liquidity interacts with contract composition and risk exposure (Belkhaoui et al., 2020).

2.2.6. Economic Growth

Macroeconomic activity influences NPF mainly through borrower cash flows: stronger growth improves household income and firm revenues, reducing delinquency and impairment; downturns weaken repayment capacity and raise NPF. GCC-focused evidence consistently identifies growth-related variables as significant drivers of impaired assets, especially when credit cycles and crisis episodes are considered (Abdelbaki, 2019; Farooq et al., 2019). Recent work further emphasizes that macro and global conditions jointly shape impaired asset dynamics in GCC economies, reinforcing the need to include growth controls even in bank-level models (Kumar et al., 2023). These results support the standard hypothesis that economic growth is negatively associated with NPF, while acknowledging that the strength of the association can vary with sectoral composition and policy regime.

2.2.7. Inflation

Inflation affects repayment capacity through real income erosion, cost pressures, and policy transmission mechanisms. The dominant expectation is that higher inflation increases NPF by worsening household purchasing power and corporate margins, particularly when nominal financing burdens do not adjust smoothly. However, inflation effects can be context dependent: if inflation reduces the real value of nominal debt obligations or coincides with accommodative financial conditions, the net effect may differ across countries and periods. GCC evidence on macro determinants of impaired assets supports inflation as a meaningful explanatory variable, but also indicates that crisis conditions and institutional features can shape its impact (Abdelbaki, 2019). Accordingly, inflation is generally modeled as a core macro determinant with empirically identified sign and magnitude.

2.2.8. Global Economic Policy Uncertainty (GEPU)

Global economic policy uncertainty (GEPU) is increasingly treated as a structural driver of financing impairment because uncertainty depresses investment, delays consumption, worsens borrower cash flows, and tightens external financing conditions. Islamic finance research using quantile methods demonstrates that global risk factors and macro conditions can produce heterogeneous responses across regimes, implying that uncertainty effects may be stronger in high-distress states than in normal periods (Naifar, 2016). Related quantile-based evidence in banking performance similarly highlights regime dependence and cross-environment heterogeneity (Jawadi et al., 2017). More recent evidence focusing on Islamic and conventional banks in the broader MENA region finds that policy uncertainty is linked to impaired asset dynamics, supporting the inclusion of GEPU-type measures in models of Islamic bank portfolio quality (Aledeimat & Bein, 2025). Taken together, this strand suggests that GEPU should be expected to increase NPF, potentially with larger effects in the upper quentile of the NPF distribution

2.3. Research Gap

Despite extensive evidence on GCC banking efficiency and performance (El Moussawi & Obeid, 2011; Hadriche, 2015) and a growing macro literature on impaired assets in GCC economies (Farooq et al., 2019; Abdelbaki, 2019), there remains limited GCC-Islamic-bank evidence that models non-performing financing (NPF) explicitly while jointly incorporating bank fundamentals (ROA, CAR, size, liquidity), domestic macro conditions (growth and inflation), and global economic policy uncertainty (GEPU), with allowance for heterogeneous effects across risk regimes. This matters because Islamic banks’ financing distress can respond asymmetrically under stress and uncertainty, as suggested by regime-sensitive and quantile-oriented evidence in Islamic finance and banking (Naifar, 2016; Jawadi et al., 2017) and by recent findings that policy uncertainty is linked to impaired assets in Islamic and conventional banks (Aledeimat & Bein, 2025).

2.4. Hypotheses Development

H1 (Profitability and NPF). Higher profitability improves screening and monitoring capacity and strengthens internal buffers, which should reduce financing distress in Islamic banks; therefore, return on assets is expected to be negatively associated with NPF (Chowdhury & Rasid, 2016; Chowdhury et al., 2017; Muhammad et al., 2020).

H2 (Capital adequacy and NPF). Stronger capital buffers enhance loss-absorption capacity and support balance-sheet resilience, implying that better-capitalized Islamic banks should exhibit lower NPF (Al-Malkawi & Pillai, 2018; Elfergani et al., 2024).

H3 (Macroeconomic conditions and NPF). Improved macroeconomic activity strengthens borrower cash flows and repayment capacity, suggesting that economic growth reduces NPF; conversely, adverse macro conditions increase financing impairment (Abdelbaki, 2019; Farooq et al., 2019).

3. Data and Methodology

This study adopts a structured panel econometric framework combining Fixed Effects (FE), Random Effects (RE), and Panel Quantile Regression to examine the determinants of non-performing financing (NPF) in GCC Islamic banks. The methodological design is grounded in established panel data theory and distribution-sensitive estimation techniques to ensure robust and policy-relevant inference.

3.1. Panel Data Model Specification

Because the dataset contains repeated observations for multiple Islamic banks over time, panel estimation is appropriate for controlling unobserved heterogeneity and improving efficiency (Baltagi, 2008; Wooldridge, 2010). Panel models reduce omitted variable bias arising from unobserved institutional characteristics such as governance quality, ownership structure, and internal risk culture.

The baseline specification is expressed as:

where:

- denotes bank,

- denotes time,

- captures unobserved bank-specific effects,

- is the idiosyncratic disturbance term.

3.2. Fixed Effects (FE) &Random Effects (RE) Model

The Fixed Effects estimator controls for time-invariant unobserved heterogeneity that may correlate with explanatory variables (Baltagi, 2008; Wooldridge, 2010). In Islamic banking, factors such as Shariah governance, institutional reputation, and risk management culture may influence both profitability and asset quality.

The FE specification is:

The FE model relies on within-bank variation for identification. It is particularly appropriate when omitted variables are correlated with regressors.

The choice between FE and RE is formally evaluated using the Hausman specification test (Hausman, 1978), which tests whether individual effects are correlated with explanatory variables.The Random Effects estimator assumes that bank-specific effects are randomly distributed and uncorrelated with regressors (Baltagi, 2008). Under this assumption, RE is more efficient than FE because it exploits both within- and between-bank variation.

The RE specification is:

where represents random bank-specific effects.

If the Hausman test rejects the null hypothesis, FE is preferred due to inconsistency of RE (Hausman, 1978).

3.4. Panel Quantile Regression

While FE and RE provide average effects, they impose slope homogeneity across the conditional distribution of NPF. However, credit risk is often nonlinear and regime-dependent. To capture distributional heterogeneity, this study employs panel quantile regression based on the seminal framework of Koenker and Bassett (1978) and extended to panel settings (Koenker, 2004).

The quantile specification is:

for quantiles .

Quantile regression minimizes weighted absolute deviations rather than squared residuals, making it robust to outliers and non-normal error distributions (Koenker & Bassett, 1978). This is particularly relevant given the skewness and kurtosis observed in the descriptive statistics.

Quantile estimation allows:

- Identification of asymmetric effects across low- and high-NPF regimes.

- Tail-risk analysis in upper quantiles.

- Robust inference under heteroskedasticity.

Recent banking studies have employed quantile methods to uncover heterogeneous risk determinants (Chowdhury et al., 2017; Jawadi et al., 2017; Radulescu et al., 2022; Bortoluzzo et al., 2024), reinforcing the methodological suitability of this approachA basic quantile analysis was developed by Koenker and Bassett (1978) By considering quantile regression as a complementary approach to panel data, one important advantage is its ability to accommodate heterogeneous effects . The utility of quantile regression analysis is the existence of varying effects at different points in the conditional distribution of dependent variables for the variables of interest (Bitler, Gelbach, and Hoynes 2006; Powell 2020). Hence, one significant challenge is transforming the quantile regression function from a nonlinear form to a smooth linear one. Kato, Galvao, and Montes-Rojas (2012) in their study identified the asymptotic conditions for panel quantile regression models to be applied with individual effects. Thus, they show that a linear quantile regression is possible and that it is possible to have individual and quantile specific intercepts that are consistent and asymptotically normal. Accordingly, the methodology used in this study combines a panel approach with a quantile regression approach. The end target is to analyse the the determinants of non-performing financing (NPF) in Islamic banks , by applying a quantile regression with panel data. First, by summarizing a part of the analysis made related to panel quantile regression, let us consider the random unit period t, that defines the outcome vector Y =(Y1, …,YT)′ presented as a Tx1 outcome vector and regression vector X = (X1,…,XT)′as a T x P regressor matrix. The conditional quantile function is:

QYt|X (τ|X) = FYt|X−1 (y|X) (1)

Let QYt|X(τ|X) = (QY1|X(τ|X);…; QYT|X(τ|X))′ be the T x 1 vector of period-specific conditional quantile functions. As introduced by (Chamberlain 1992) and further analysed by (Graham and Powell 2012) and (Arellano and Bonhomme 2017), the conditional quantile function, having a semiparametric form, is defined as

QYt|X(τ|X) = Xβ(τ;X) + wδ(τ) (2)

F For all X ∈ XN T = Xtϵ{1,…,T}and all τϵ (0,1). The semiparametric form is due to the coefficients vector of X named β(τ;X) which are nonparametric functions of X. The linear form of panel quantile regression as defined by (Arellano and Bonhomme 2017; Canay 2011) is

Yit = Xit ′β(Uit) + αi + Vit (3)

The focus of our empirical analysis is the heterogeneous and non-constant effect in stage two of the quantile, which results from analysing the individual effects. We assume a differential impact on microfinance performance (financial performance and outreach). To structure the quantile function for panel quantile regression with non-additive fixed effects, we take the same approach as Chernozhukov et al. (2013), but without a fixed term. The quantile function for panel data in this case is specified by:

QYit|X (τ|X) = Xit ′ β (τ,X) (4)

The panel quantile function specified as equation (4) has τ quantiles with τϵ (0,1) where β̂(τ) is the coefficient on Xit in the τ linear quantile regression of Y on X. For each estimation relying on a specific τ quantile, the associated estimand β̂(τ) equals the τtℎ unconditional quantile effect (UQE) of a unit change in Xit . The UQE is the quantile analog of an average partial effect (APE) that represents the marginal effect of a unit change in Xit as being heterogeneous across units and dependent on X. The estimation equation takes the linear form

Yit = Xit ′β(Uit ∗); witℎ Uit ∗ ~ U(0,1) and Uit ∗ = f(αi ; Uit) (5)

The specification of the impact of the determinants of non-performing financing (NPF) in Islamic banks follows the approach. Therefore, the model is specified in detail as follows:

Yit = aitα +bitβ +xitγ +zitφ + eit (6)

Where Yit is the non-performing financing (NPF) in Islamic banks i at year t; ait is a vector of NPF determents that includes the indicators of financial performance is the dependent variable . This ait coefficient is important, because as the microfinance has shown the two are mutually linked. bit is the vector of microfinance controls; xit is the vector of microfinance structure, zit is the macro variables; and eit the terms of errors. The empirical design of this study is structured to address a central question: how do internal bank fundamentals and external macro-financial conditions shape non-performing financing (NPF) in GCC Islamic banks, and do these effects vary across different risk regimes? By specifying NPF as the dependent variable within a panel framework, the model evaluates how profitability, capitalization, liquidity, bank size, economic growth, inflation, and global economic policy uncertainty jointly influence financing distress.

The initial stage relies on panel least squares estimation using both fixed and random effects. The fixed-effects specification controls for time-invariant institutional characteristics such as governance structure and risk culture that may correlate with explanatory variables (Baltagi, 2008; Wooldridge, 2010). The Hausman (1978) test formally guides the choice between estimators and supports the use of fixed effects when unobserved heterogeneity is correlated with regressors. This approach ensures that the estimated relationships reflect within-bank variation rather than cross-sectional differences.

However, mean-based estimators impose slope homogeneity and may conceal nonlinear credit-risk dynamics. Credit impairment in Islamic banks can intensify disproportionately during adverse conditions, particularly in oil-dependent GCC economies (Farooq et al., 2019; Kumar et al., 2023). To account for this possibility, the analysis employs panel quantile regression following the framework introduced and extended to panel data settings (Koenker, 2004; Canay, 2011). This method allows coefficient estimates to vary across the conditional distribution of NPF.

By estimating the model across multiple quantiles, the study evaluates whether bank fundamentals exert stronger stabilizing effects in high-NPF regimes than in low-risk states. Quantile estimation is also robust to non-normal error distributions and heteroskedasticity, which are common in banking data (Koenker & Bassett, 1978). Recent Islamic banking research demonstrates that performance and risk relationships often differ across distributional regimes, supporting the relevance of this approach (Chowdhury et al., 2017; Jawadi et al., 2017).

Overall, the combined fixed-effects and quantile framework provides both consistent average inference and distribution-sensitive evidence. This dual strategy allows the study to capture heterogeneous risk dynamics and generate policy-relevant insights for supervisory monitoring in GCC Islamic banking systems.

3.1. Data and Sample

This study examines the determinants of non-performing financing (NPF) in Islamic banks operating in the Gulf Cooperation Council (GCC) countries. The sample covers Islamic banks from Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates over the period 2014-2024, subject to data availability. These countries represent the core of the global Islamic banking industry and share broadly similar regulatory and institutional environments, making them well suited for comparative analysis.

Table 1 represents Bank-specific data are obtained from the Islamic Financial Services Board (IFSB), which provides indicators for Islamic banks consistent with Shariah compliant financial reporting standards. Macroeconomic variables are sourced from the World Bank’s World Development Indicators, ensuring cross-country comparability. Global economic policy uncertainty is measured using the Global Economic Policy Uncertainty (GEPU) Index, which captures uncertainty related to global economic and policy developments.

The final panel is balanced and consists of 60 observations, allowing for consistent estimation across countries and time. All variables are checked for consistency and outliers prior to estimation.

3.2. Results and Analysis

3.2.1. Descriptive Statistics

Descriptive Statistics summarize the central tendency, dispersion, and shape of a dataset's distribution, presented in the table below.

Table 1 documents the construction of the study variables and their data provenance, indicating a coherent design that combines bank-level prudential indicators with macroeconomic conditions and an external uncertainty proxy. The dependent variable, non-performing financing (NPF), is measured as gross non-performing financing and is sourced from the Islamic Financial Services Board (IFSB), which provides standardized prudential indicators for Islamic banking systems, including asset-quality measures (IFSB, 2019). Profitability is captured by return on assets (ROA), measured as net profit/total assets, also consistent with IFSB prudential reporting conventions for earnings indicators (IFSB, 2019). Capital strength is proxied by capital adequacy ratio (CAR) computed as total regulatory capital/risk-weighted assets, aligning with the prudential capital framework embedded in IFSB indicators (IFSB, 2019). Bank structure is controlled via SIZE, defined as the natural logarithm of total assets, while liquidity conditions are represented by LIQU as liquid assets/total assets, both widely used in bank-level panel models to capture scale effects and funding resilience.

The macroeconomic environment is incorporated using the World Bank’s World Development Indicators (WDI). Economic growth is proxied by GDP per capita (constant 2015 US$), a real-term measure designed to capture income dynamics net of price changes and comparable across countries (World Bank). Inflation (INF) is measured as the annual percentage change in the consumer price index, which reflects changes in the cost of a representative consumption basket and is a standard macro control in credit-risk/asset-quality research (World Bank, n.d.-b). Finally, global conditions are proxied by GEPU, the Global Economic Policy Uncertainty index. GEPU is a widely used headline-based uncertainty measure and is available through the Economic Policy Uncertainty project’s global data series (Economic Policy Uncertainty, n.d.). Conceptually, including GEPU strengthens identification of external risk conditions that may affect financing quality beyond domestic macro variables.

Table 2 provides descriptive statistics that clarify the dataset’s central tendency, variability, and distributional shape. The mean NPF is 2056.17 with a median of 1372.23, while the maximum reaches 7423.39 and the minimum is 0.17. This pattern indicates a right-skewed distribution (skewness = 1.29) with moderate quentile thickness (kurtosis = 3.62). The relatively large standard deviation (2021.55) compared with the mean implies substantial dispersion in financing distress across observations, consistent with cross-country and/or cross-bank heterogeneity in Islamic banking asset quality. The Jarque Bera statistic strongly rejects normality for NPF (p < 0.001), suggesting that empirical modelling should be robust to non-normality and outliers (e.g., through log transformations where appropriate, robust standard errors, or distribution-sensitive estimators).

For the bank fundamentals, ROA averages 0.0116 (≈1.16%) with a median of 0.0117, but the minimum is −0.0453 and the maximum is 0.0257, implying that some observations record losses and that profitability varies considerably across the sample. ROA is highly non-normal (kurtosis = 14.25; Jarque–Bera p < 0.001), which is typical in bank panels where earnings are episodically affected by provisioning and macro shocks. CAR has a mean of 0.1939 and median of 0.1813, indicating generally healthy capitalization, but the maximum (0.7059) and extreme skewness/kurtosis (skewness 5.80, kurtosis 39.40) reveal the presence of very high capital observations that could represent specific jurisdictions, regulatory regimes, or periods of capital rebuilding. Like NPF and ROA, CAR fails the normality test (p < 0.001), reinforcing the case for robust inference.

SIZE (reported as a large numeric scale in your table) has a mean of 114,382.7 and a maximum of 392,339.3, indicating major differences in scale. The positive skewness (0.96) and non-normality (p < 0.001) suggest that a logarithmic transformation as stated in Table 1 helps stabilize variance and mitigate leverage from very large banks. LIQU averages 0.2100 (median 0.1864), ranging from 0.0669 to 0.4463. Unlike the other bank variables, LIQU displays no strong departure from normality at conventional levels (Jarque–Bera p ≈ 0.185), implying a comparatively smoother distribution and less extreme tail behavior.

Macroeconomic variables show meaningful variability as well. GDP per capita (constant 2015 US$) exhibits large dispersion (std. dev. ≈ 2.55E+11 in your reporting scale), with right-skewness (1.17) and non-normality (p < 0.001). This reinforces that real income conditions differ across observations and likely provide an important macro channel for financing quality (World Bank, n.d.-a). INF has a mean of 1.73% and includes negative values (minimum −2.54), consistent with periods of disinflation/deflation; its normality is not rejected (p ≈ 0.146), indicating a relatively moderate distribution in this sample (World Bank, n.d.-b). GEPU averages 204.01 (range 96.64 to 368.22) with mild skewness (0.35) and no strong evidence against normality (p ≈ 0.372), suggesting that global uncertainty varies substantially but without extreme outliers in the sample period (Economic Policy Uncertainty, n.d.)

Table 3 indicates that non-performing financing (NPF) is moderately and positively correlated with bank size (0.4837), implying that larger Islamic banks in the sample tend to exhibit higher impaired financing in the unconditional data, while NPF also co-moves positively with GDP (0.3414) and global economic policy uncertainty (GEPU) (0.3430), suggesting sensitivity of financing distress to macro conditions and external uncertainty. The NPF-ROA correlation is positive but modest (0.3106), which may reflect pro-cyclical balance-sheet expansion or omitted factors that require multivariate control. Capital adequacy (CAR) is weakly negatively associated with NPF (−0.1704), consistent with the buffering role of capital in mitigating financing distress. Notably, ROA and CAR are strongly negatively correlated (−0.7282), signalling a potential multicollinearity issue that should be assessed in regression diagnostics. Finally, SIZE is strongly correlated with GDP (0.7857) and moderately with GEPU (0.4321), indicating that scale effects are intertwined with macro and global conditions, which underscores the importance of controlling for these factors in the empirical model.

The panel unit-root evidence reported in Table 4 indicates that the variables in the NPF model are non-stationary in levels but become stationary after first differencing, implying that the series are predominantly integrated of order one, I(1) rather than I(0). At the level form, across the three deterministic specifications (with constant; with constant and trend; and without constant and trend), the reported probabilities for NPF, SIZE, ROA, CAR, LIQU, GDP, INF, and GEPU are generally above conventional significance thresholds, so the null hypothesis of a unit root cannot be rejected for most variables. In contrast, the first-difference results provide evidence of stationarity for several series under the “with constant” specification most notably d(NPF) (p = 0.0504), d(GDP) (p = 0.0323), and d(GEPU) (p = 0.0413) and stronger evidence under the “without constant and trend” specification, where d(NPF) (p = 0.0138), d(ROA) (p = 0.0256), d(LIQU) (p = 0.0050), d(GDP) (p = 0.0094), d(INF) (p = 0.0057), and d(GEPU) (p = 0.0035) reject the unit-root null at standard levels. The pattern therefore supports a mixed integration structure dominated by I(1) behavior, while SIZE and CAR show weaker first-difference evidence (often failing to reject the unit root), suggesting that their stochastic properties may be more sensitive to the deterministic specification or sample structure. Overall, the unit-root outcomes justify proceeding with empirical strategies designed for non-stationary panels particularly frameworks that allow variables to be I(0) or I(1) and then assess whether a long-run equilibrium relationship exists among NPF and its determinants through panel cointegration techniques and appropriately specified long-run estimators. This interpretation is aligned with standard panel econometric practice where unit-root diagnostics are used as a prerequisite for testing long-run relationships and for choosing estimators that remain valid under non-stationarity in levels.

The macroeconomic and global variables provide limited explanatory power in the fixed-effects specification reported in Table 5. Under fixed effects, GDP per capita is negative and statistically insignificant (p = 0.130), indicating that within-bank changes in income conditions are not associated with statistically detectable changes in the financial stability indicator over the sample period. Inflation and global economic policy uncertainty are also insignificant in the fixed-effects model (INF: p = 0.189; GEPU: p = 0.665), suggesting that contemporaneous macroeconomic fluctuations and global uncertainty do not explain within-bank variation in financial stability once unobserved bank-specific heterogeneity is controlled for. In contrast, the random-effects results closely resemble pooled OLS and likewise show GDP, inflation, and GEPU to be statistically insignificant (GDP: p = 0.308; INF: p = 0.894; GEPU: p = 0.209), reinforcing the interpretation that the macro-global block is not a primary driver in these linear mean-based panel estimates. Across specifications, bank size is the most robust predictor, remaining positive and statistically significant in pooled OLS, fixed effects, and random effects (p = 0.003, 0.007, and 0.002, respectively), implying that larger banks are associated with higher financial stability. The liquidity ratio is negative and significant in pooled OLS and random effects (p = 0.005 and 0.003) but becomes insignificant under fixed effects (p = 0.881), indicating that the pooled and random-effects liquidity association is likely driven by time-invariant cross-sectional differences that the fixed-effects model absorbs rather than by within-bank liquidity changes. Overall, Table 5 implies that financial stability in this dataset is more closely linked to bank structure, particularly scale, than to profitability, capitalization, or macro-global conditions, and it also highlights that inference for liquidity is sensitive to how unobserved heterogeneity is treated.

Table 6 illustrate the null is rejected , implying that the fixed-effects estimator is preferred because the random-effects estimates are inconsistent when unobserved bank-specific effects are correlated with the regressors. The warning that (Vb−VB) is not positive definite and that the rank of the differenced variance matrix is smaller than the number of coefficients indicates numerical limitations; however, the very small p-value still supports using FE as the baseline specification.

Table 7 shows the simultaneous quantitative regression estimates across the conditional distribution of the dependent variable. This allows for differentiation of the factors influencing the outcome between low and high-outcome systems, rather than imposing a single average effect. The results indicate that bank size is the most robust and consistent predictor: bank size is positive and statistically significant at almost all quantities, with its effect increasing markedly towards the upper end, rising from 0.0099 at quantity 0.10 (p < 0.001) to 0.0457 at quantity 0.90 (p = 0.003). This suggests that size becomes increasingly significant as the value of the dependent variable increases. Liquidity shows a clear edge-dependent pattern: it is slightly negative at the lower end (quantity 0.10, p = 0.063) and becomes strongly negative and highly statistically significant at the higher quantities (quantities 0.70–0.90, p = 0.002). This means that higher liquidity ratios are associated with significantly lower values for the dependent variable in countries with strong regulatory systems, consistent with the role of liquidity as a stabilizing factor during economic downturns. Macroeconomic growth (GDP) is negative and statistically significant only at the lower end of the distribution (Q0.10–Q0.20, p = 0.009 and 0.027), but loses significance at the middle and higher end. This suggests that income conditions largely explain changes in low- to middle-income countries, rather than at the extreme end. On the other hand, profitability (return on assets) and capital adequacy are not statistically significant at any point, and their coefficients become smaller and then negative at the upper end. This means that their marginal effects are not accurately assessed when considering differences between the distributions. Similarly, inflation and global policy uncertainty are not statistically significant at any end, meaning that in this sample, current price changes and global policy uncertainty do not have strong effects on the dependent variable across the entire distribution. Finally, the rise in the pseudo-R-squared value from 0.3668 at Q0.10 to 0.5175 at Q0.90 indicates that the model does a better job of explaining higher quantities, which is consistent with the idea that SIZE and LIQU mostly explain quantile behavior.

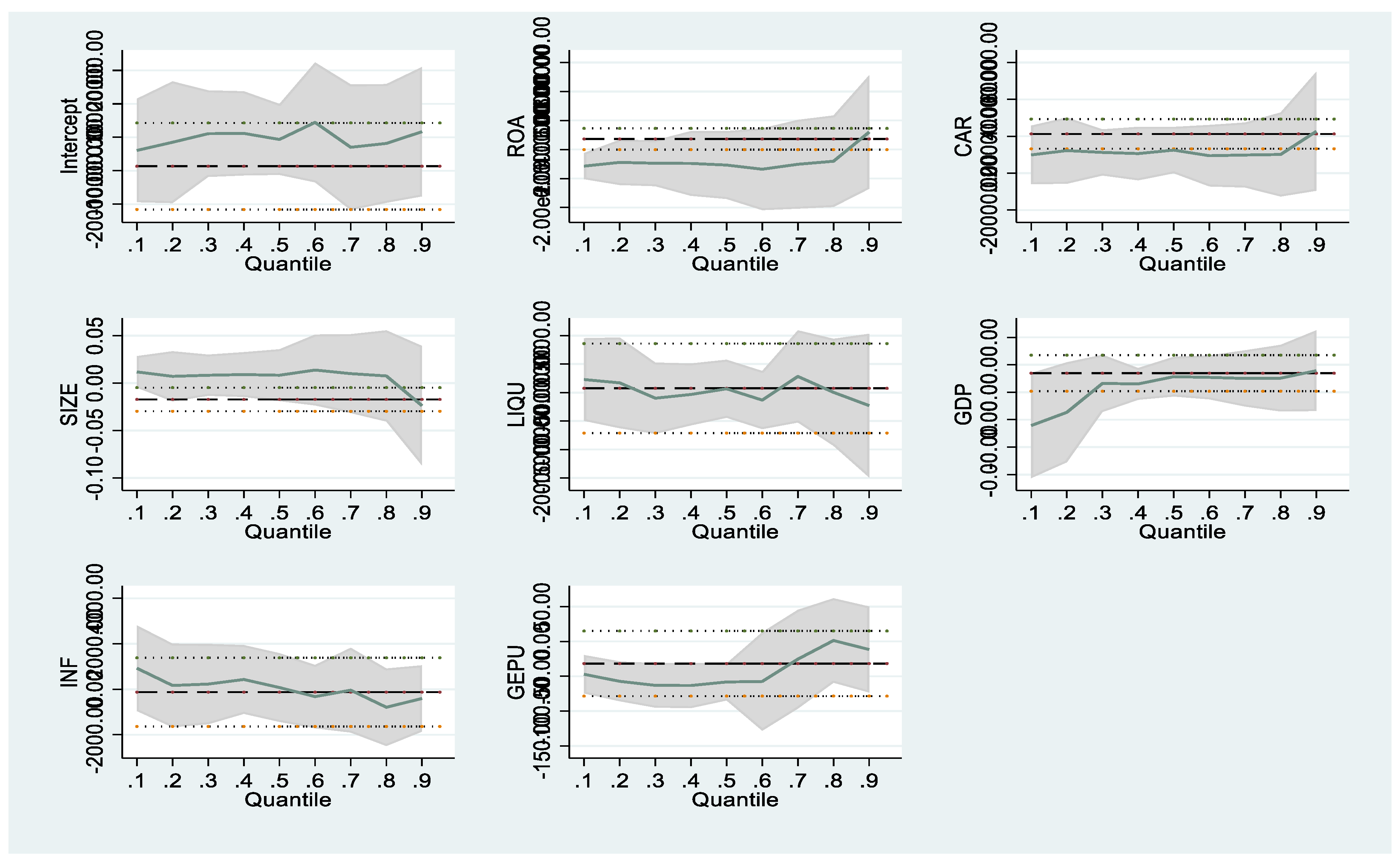

The figure 1 plots quantile-specific coefficient estimates with confidence bands, showing clear heterogeneity across the conditional distribution. Bank size exhibits a consistently positive effect that strengthens toward the upper quantiles, indicating that scale matters more in high-regime outcomes. Liquidity becomes increasingly negative and more precisely estimated in the upper quentile, suggesting a stronger stabilising role when the dependent variable is high. GDP is more influential in the lower quantiles and then flattens around the middle and upper quantiles, implying limited marginal impact outside low-regime states. ROA, CAR, inflation, and GEPU display comparatively flat profiles with wide bands at the extremes, indicating weak and generally statistically imprecise effects across most quantiles.

Figure 1.

Results of Quantile Regression.

4. Conclusion

This research investigates the factors influencing non-performing loans (NPLs) in Islamic banks in the GCC countries, using cross-sectional data analysis and distribution-sensitive quantitative regression analysis. The results show that funding challenges in GCC Islamic banks are primarily attributable to structural features and liquidity conditions, rather than solely to profitability or capital adequacy, highlighting the importance of bank-specific metrics in assessing asset quality.

The research indicates that the two main factors are bank size and liquidity. Larger institutions tend to have higher NPLs, particularly at the highest distribution levels. This suggests that the costs of complexity, rapid growth, or governance issues may outweigh the benefits of diversification. Liquidity is a key stabilizing factor in systems with high NPL ratios, demonstrating its role as a buffer during crises. These findings reinforce the view that funding challenges in Islamic banks reflect the robustness of the institutional framework and balance sheet, rather than temporary profitability indicators.

Hypothesis (H1) assumes that profitability reduces NPLs; However, the average results do not support this assumption, as they show no systematic statistical significance across the various quantitative segments. Theoretically, a higher return on assets should improve control and provisioning capabilities, but real-world data suggest that profitability does not necessarily guarantee the avoidance of loan losses. This conclusion aligns with research indicating that profitability may signal a shift towards riskier investment portfolios rather than enhanced auditing (Chowdhury et al., 2017; Jawadi et al., 2017). It also aligns with studies showing that the relationship between earnings performance and credit risk in Islamic banks is weak or conditional (Mohammad et al., 2020).

The second hypothesis (H2), which posits an inverse relationship between capital adequacy and non-disposable funding, lacks strong evidence. In most models, capital adequacy does not exhibit a statistically significant stabilizing effect. This implies that regulatory protection alone may not prevent the accumulation of non-performing loans. This study corroborates other research indicating that capital ratios may be associated with higher risk levels when banks implement growth strategies or operate under implicit guarantees (Al-Malkawi & Pillai, 2018; Al-Farghani et al., 2024). Therefore, while capitalization is important, it is insufficient to maintain portfolio quality.

On the other hand, economic development reduces net non-performing cash flows in the lower tiers. This means that improved macroeconomic conditions make it easier for borrowers to repay their loans under normal circumstances. The third hypothesis has been somewhat confirmed; however, this effect diminishes or disappears in severe financial crisis scenarios, suggesting that macroeconomic expansion cannot fully compensate for structural deficiencies once funding challenges have intensified. Banking studies in the GCC (Abdulbaqi, 2019; Farouk et al., 2019) have shown that macroeconomic factors can have a similarly varying impact on non-performing assets.

Overall, the results indicate significant variability in the distribution of net non-performing cash flows, supporting the notion that average-based models may mask important system-dependent dynamics. Consequently, the evidence underscores the effectiveness of quantitative methodologies in assessing financial stability within Islamic banking institutions.

5. Recommendations

These findings have significant implications for regulators, bank executives, and policymakers in the GCC economies.

First, regulators should place greater emphasis on structural risk indicators, particularly bank size and liquidity management, rather than solely focusing on capital ratios or profitability metrics. Strengthening oversight of large Islamic banks is crucial given their pivotal role in the financial system, which could exacerbate funding crises.

Second, Islamic banks should enhance their liquidity plans by incorporating stress tests, reserve funding schemes, and diversifying their funding sources. Liquidity is critical for stabilizing high-risk economic conditions, and proactive liquidity management can prevent funding crises from escalating.

Third, macroprudential policy should consider how different economic conditions affect individuals in varying ways. Under normal circumstances, economic growth improves asset quality, but it cannot fully address the difficulties that arise when funding problems worsen. Therefore, countercyclical policies and techniques that provide early warnings are essential.

Fourth, governance and risk management should be improved, particularly in rapidly growing institutions. Better screening and monitoring methods, along with broader investment, can help reduce the rise in non-performing loans. Finally, authorities may want to consider adding uncertainty indicators to regulatory frameworks, as global shocks can affect the quality of financing even when domestic conditions are stable.

Limitations and Future Research Prospects

Several limitations should be acknowledged. First, the analysis relies on annual data, which may not reflect short-term changes or changes in the quality of financing caused by crises. Second, the sample is limited to Islamic banks in the GCC countries, meaning the findings cannot be generalized to other regions or financial systems. Third, the study uses composite indicators of asset quality and macroeconomic conditions, which may mask sector-specific shortcomings. Fourth, while quantitative regression analysis indicates variations across risk systems, it does not explicitly account for dynamic feedback effects or the possibility of an inverse causal relationship between bank performance and financing failures.

There are several avenues for future studies to build upon. Researchers could investigate short-term changes and the mechanisms of crisis behavior using higher-frequency data. Including Islamic banks from other regions in the analysis would make the findings more relevant to researchers outside the scope of this study, providing a better understanding of how they compare. Dynamic panel models or nonlinear methodologies could enhance the investigation of feedback mechanisms between profitability, capital, and loan defaults. Comprehensive information about the types or sectors of financing also helps identify those causing the greatest financing problems. Finally, adding broader indicators of opacity, governance quality, and digital transformation helps us better understand the root causes of risk in Islamic banking institutions.

Funding

The author extends sincere appreciation to the Deanship of Research and Graduate Studies at the University of Tabuk for funding this work through Research No. 0130-2024-S.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data from this study can be requested from the corresponding author.

Conflicts of Interest

The author declares no conflict of interest.

References

- Hausman, J. A. Specification tests in econometrics. Econometrica 1978, 46(6), 1251–1271. [Google Scholar] [CrossRef]

- Koenker, R.; Bassett, G. Regression quantiles. Econometrica 1978, 46(1), 33–50. [Google Scholar] [CrossRef]

- Chamberlain, G. Efficiency bounds for semiparametric regression. Econometrica: Journal of the Econometric Society 1992, 567–596. [Google Scholar] [CrossRef]

- Bitler, M. P.; Gelbach, J. B.; Hoynes, H. W. What mean impacts miss: Distributional effects of welfare reform experiments. American Economic Review 2006, 96(4), 988–1012. [Google Scholar] [CrossRef]

- Baltagi, B. H. Econometric analysis of panel data; John wiley & sons: Chichester, 2008; Vol. 4, pp. 135–145. Available online: https://onlinelibrary.wiley.com/doi/book/10.1002/9780470518861.

- Wooldridge, J. M. Econometric analysis of cross section and panel data; MIT press, 2010; Available online: https://mitpress.mit.edu/9780262232586/econometric-analysis-of-cross-section-and-panel-data/.

- Canay, I. A. A simple approach to quantile regression for panel data. The econometrics journal 2011, 14(3), 368–386. [Google Scholar] [CrossRef]

- El Moussawi, C.; Obeid, H. Evaluating the productive efficiency of Islamic banking in GCC: A non-parametric approach. International Management Review 2011, 7(1), 10. [Google Scholar]

- Canay, I. A. A simple approach to quantile regression for panel data. The econometrics journal 2011, 14(3), 368–386. [Google Scholar] [CrossRef]

- Graham, B. S.; Powell, J. L. Identification and estimation of average partial effects in “irregular” correlated random coefficient panel data models. Econometrica 2012, 80(5), 2105–2152. [Google Scholar] [CrossRef]

- Chernozhukov, V.; Fernández-Val, I.; Melly, B. Inference on counterfactual distributions. Econometrica 2013, 81(6), 2205–2268. [Google Scholar] [CrossRef]

- ALANDEJANI, M.; ABDULAZIZ, Y. Efficiency, survival, and non-performing loans in islamic and conventional banking in the GCC. Doctoral dissertation, Durham University, 2014. [Google Scholar]

- Khediri, K. B.; Charfeddine, L.; Youssef, S. B. Islamic versus conventional banks in the GCC countries: A comparative study using classification techniques. Research in International Business and Finance 2015, 33, 75–98. [Google Scholar] [CrossRef]

- Hadriche, M. Banks performance determinants: Comparative analysis between conventional and Islamic banks from GCC countries. International Journal of Economics and Finance 2015, 7(9), 169–177. [Google Scholar] [CrossRef]

- Graham, B. S.; Hahn, J.; Poirier, A.; Powell, J. L. (2015). Quantile regression with panel data (No. w21034). National Bureau of Economic Research.

- Naifar, N. Do global risk factors and macroeconomic conditions affect global Islamic index dynamics? A quantile regression approach. The Quarterly Review of Economics and Finance 2016, 61, 29–39. [Google Scholar] [CrossRef]

- Chowdhury, M. A. F.; Rasid, M. E. S. M. Determinants of performance of Islamic banks in GCC countries: Dynamic GMM approach. In Advances in Islamic finance, marketing, and management: An Asian perspective; Emerald Group Publishing Limited, 2016; pp. 49–80. [Google Scholar]

- Chowdhury, M. A. F.; Haque, M. M.; Masih, M. Re-examining the determinants of Islamic bank performance: new evidence from dynamic GMM, quantile regression, and wavelet coherence approaches. Emerging Markets Finance and Trade 2017, 53(7), 1519–1534. [Google Scholar] [CrossRef]

- Arellano, M.; Bonhomme, S. Quantile selection models with an application to understanding changes in wage inequality. Econometrica 2017, 85(1), 1–28. [Google Scholar] [CrossRef]

- Jawadi, F.; Jawadi, N.; Cheffou, A. I.; Ameur, H. B.; Louhichi, W. Modelling the effect of the geographical environment on Islamic banking performance: A panel quantile regression analysis. Economic Modelling 2017, 67, 300–306. [Google Scholar] [CrossRef]

- Al-Malkawi, H. A. N.; Pillai, R. Analyzing financial performance by integrating conventional governance mechanisms into the GCC Islamic banking framework. Managerial Finance 2018, 44(5), 604–623. [Google Scholar] [CrossRef]

- Kamarudin, F.; Sufian, F.; Nassir, A. M.; Anwar, N. A. M.; Ramli, N. A.; Tan, K. M.; Hussain, H. I. Price efficiency on Islamic banks vs. conventional banks in Bahrain, UAE, Kuwait, Oman, Qatar and Saudi Arabia: impact of country governance. International Journal of Monetary Economics and Finance 2018, 11(4), 363–383. [Google Scholar] [CrossRef]

- Islamic Financial Services Board (IFSB). Islamic financial services industry stability report 2019. IFSB. 2019. Available online: https://www.ifsb.org.

- Farooq, M. O.; Abou Elseoud, M. S.; Turen, S.; Abdulla, M. Causes of non-performing loans: The experience of gulf cooperation council countries. Entrepreneurship and Sustainability Issues 2019, 6(4), 1955–1974. [Google Scholar] [CrossRef]

- Abdelbaki, H. H. Macroeconomic determinants of non-performing loans in GCC economies: does the global financial crisis matter? International Journal of Economics and Business Research 2019, 17(4), 433–447. [Google Scholar] [CrossRef]

- Belkhaoui, S.; Alsagr, N.; Van Hemmen, S. F. Financing modes, risk, efficiency and profitability in Islamic banks: Modeling for the GCC countries. Cogent Economics & Finance 2020, 8(1), 1750258. [Google Scholar] [CrossRef]

- Muhammad, R.; Suluki, A.; Nugraheni, P. Internal factors and non-performing financing in Indonesian Islamic rural banks. Cogent Business & Management 2020, 7(1), 1823583. [Google Scholar] [CrossRef]

- Belkhaoui, S.; Alsagr, N.; van Hemmen, S. F. Financing modes, risk, efficiency and profitability in Islamic banks: Modeling for the GCC countries. Cogent Economics & Finance 2020, 8(1). [Google Scholar] [CrossRef]

- Powell, D. Quantile treatment effects in the presence of covariates. Review of Economics and Statistics 2020, 102(5), 994–1005. [Google Scholar] [CrossRef]

- Alshebmi, A. S.; Adam, M. H. M.; Mustafa, A. M.; Abdelmaksoud, M. T. D. O. E. Assessing the non-performing loans and their effect on banks profitability: Empirical evidence from the Saudi Arabia banking sector. International Journal of Innovation, Creativity and Change 2020, 11(8), 69–93. [Google Scholar]

- Hidayat, S. E.; Sakti, M. R. P.; Al-Balushi, R. A. A. Risk, efficiency and financial performance in the GCC banking industry: Islamic versus conventional banks. Journal of Islamic Accounting and Business Research 2021, 12(4), 564–592. [Google Scholar] [CrossRef]

- Widarjono, A.; Rudatin, A. Financing diversification and Indonesian Islamic bank's non-performing financing. Jurnal Ekonomi & Keuangan Islam 2021, 45–58. [Google Scholar] [CrossRef]

- Radulescu, M.; Balsalobre-Lorente, D.; Joof, F.; Samour, A.; Tuersoy, T. Exploring the impacts of banking development, and renewable energy on ecological footprint in OECD: new evidence from method of moments quantile regression. Energies 2022, 15(24), 9290. [Google Scholar] [CrossRef]

- Almuraikhi, M. A. Determinants of Non-Performing Loans Between Islamic And Conventional Banks: A Systematic Literature Review. Economics and Business Quarterly Reviews 2022, 5(4). [Google Scholar] [CrossRef]

- Kumar, M.; Al-Romaihi, M. A.; Aktan, B. Do the macro and global economic factors drive the nonperforming loans in GCC economies? Journal of Financial Economic Policy 2023, 15(3), 190–207. [Google Scholar] [CrossRef]

- Bortoluzzo, A. B.; Ciganda, R. R.; Bortoluzzo, M. M. Determinant factors of banking profitability: an application of quantile regression for panel data. Future Business Journal 2024, 10(1), 56. [Google Scholar] [CrossRef]

- Salsabilla, L. Z.; Jaya, T. J. The impact of non-performing financing and operational efficiency on the stability of Islamic banks in Persian Gulf countries. Journal of Islamic Economics Lariba 2024, 10(2). [Google Scholar] [CrossRef]

- Elfergani, H. F.; Abdelhamid Alzwi, A. S.; Zagoub, A. The Impact of Capital Adequacy and Non-Performing Loans on Loan Loss Provisions for Gulf Cooperation Council (GCC) Banks: Econometric Study Using Panel Data. In Handbook of Banking and Finance in the MENA Region; 2024; pp. 245–286. [Google Scholar]

- Aledeimat, S. R. M.; Bein, M. A. Assessing US and Global Economic Policy Uncertainty Effects on Non-Performing Loans in MENA's Islamic and Conventional Banks. International Journal of Finance & Economics, 2025. [Google Scholar]

Table 1.

Variable and data sources.

| Symbol | Variable | Measurement | Source |

| NPF | Non-performing financing | Gross non-performing financing | Islamic Financial Services Board |

| ROA | Return on Assets | Net profit / Total assets | Islamic Financial Services Board |

| CAR | Capital Adequacy Ratio | Total regulatory capital / Risk-weighted assets | Islamic Financial Services Board |

| SIZE | Bank size | Natural logarithm of total assets | Islamic Financial Services Board |

| LIQU | Liquidity ratio | Liquid assets / Total assets | Islamic Financial Services Board |

| GDP | Economic growth | GDP per capita (constant 2015 US$) | https://databank.worldbank.org/ |

| INF | Inflation | Annual percentage change in Consumer Price Index (CPI) | https://databank.worldbank.org/ |

| GEPU | Global Economic Policy Uncertainty | Global Economic Policy Uncertainty Index | Economic Policy Uncertainty Index |

Note: own construction.

Table 2.

Descriptive Statistics.

| NPF | SIZE | ROA | CAR | LIQU | GDP | INF | GEPU | |

| Mean | 2056.168 | 114382.7 | 0.011615 | 0.193889 | 0.209988 | 2.60E+11 | 1.729421 | 204.0093 |

| Median | 1372.230 | 112103.9 | 0.011700 | 0.181313 | 0.186437 | 1.38E+11 | 2.017117 | 203.8314 |

| Maximum | 7423.390 | 392339.3 | 0.025675 | 0.705850 | 0.446300 | 8.64E+11 | 5.291226 | 368.2154 |

| Minimum | 0.170000 | 969.3800 | -0.045300 | 0.137750 | 0.066900 | 3.17E+10 | -2.540315 | 96.63517 |

| Std. Dev. | 2021.551 | 82539.54 | 0.010866 | 0.072914 | 0.087604 | 2.55E+11 | 1.746017 | 67.11474 |

| Skewness | 1.292902 | 0.960638 | -2.691484 | 5.802940 | 0.453043 | 1.165888 | -0.590600 | 0.354667 |

| Kurtosis | 3.623044 | 4.587614 | 14.25059 | 39.40048 | 2.361362 | 2.987676 | 3.071436 | 2.535479 |

| Jarque-Bera | 19.45506 | 17.08250 | 427.7687 | 4014.151 | 3.379338 | 14.95267 | 3.850919 | 1.977071 |

| Probability | 0.000060 | 0.000195 | 0.000000 | 0.000000 | 0.184581 | 0.000566 | 0.145809 | 0.372121 |

| Sum | 135707.1 | 7549258. | 0.766575 | 12.79665 | 13.85923 | 1.71E+13 | 114.1418 | 13464.61 |

| Sum Sq. Dev. | 2.66E+08 | 4.43E+11 | 0.007675 | 0.345570 | 0.498836 | 4.22E+24 | 198.1575 | 292785.2 |

| Observations | 66 | 66 | 66 | 66 | 66 | 66 | 66 | 66 |

Source: Author calculation.

Table 3.

Correlation Matrix.

| NPF | SIZE | ROA | CAR | LIQU | GDP | INF | GEPU | |

| NPF | 1 | |||||||

| SIZE | 0.4837 | 1 | ||||||

| ROA | 0.3106 | 0.5877 | 1 | |||||

| CAR | -0.1704 | -0.1484 | -0.7282 | 1 | ||||

| LIQU | -0.1748 | 0.2695 | 0.0711 | 0.3169 | 1 | |||

| GDP | 0.3414 | 0.7857 | 0.5671 | -0.0316 | 0.2251 | 1 | ||

| INF | 0.1608 | 0.2259 | 0.1953 | -0.0907 | 0.0651 | 0.0374 | 1 | |

| GEPU | 0.3430 | 0.4321 | 0.2981 | -0.1182 | 0.0553 | 0.4495 | 0.1749 | 1 |

Source: Author calculation.

Table 4.

Panel unit root test results (ADF).

| At Level | |||||||||

| NPF | SIZE | ROA | CAR | LIQU | GDP | INF | GEPU | ||

| With Constant | t-Statistic | 0.9714 | 0.2723 | 0.0004 | 0.4188 | 0.0001 | 0.4592 | 0.1511 | 0.9432 |

| Prob. | 0.9104 | 0.9708 | 0.3898 | 1.0000 | 0.4883 | 0.1744 | 0.4430 | 0.4167 | |

| n0 | n0 | n0 | n0 | n0 | n0 | n0 | n0 | ||

| With Constant & Trend | t-Statistic | 0.5021 | 0.9976 | 0.0584 | 0.0001 | 0.0001 | 0.1357 | 0.2512 | 0.4374 |

| Prob. | 0.5112 | 0.3658 | 0.9444 | 0.9983 | 0.6139 | 0.2049 | 0.6611 | 0.3724 | |

| n0 | n0 | n0 | n0 | n0 | n0 | n0 | n0 | ||

| Without Constant & Trend | t-Statistic | 0.9758 | 0.2785 | 0.1048 | 0.7485 | 0.3096 | 0.9599 | 0.2120 | 0.9704 |

| Prob. | 0.8834 | 0.9983 | 0.3768 | 0.8735 | 0.3196 | 0.9351 | 0.1875 | 0.7687 | |

| n0 | n0 | n0 | n0 | n0 | n0 | n0 | n0 | ||

| At First Difference | |||||||||

| d(NPF) | d(SIZE) | d(ROA) | d(CAR) | d(LIQU) | d(GDP) | d(INF) | d(GEPU) | ||

| With Constant | t-Statistic | 0.1941 | 0.7485 | 0.2219 | 0.0426 | 0.0000 | 0.0739 | 0.0380 | 0.1058 |

| Prob. | 0.0504 | 0.1254 | 0.2258 | 0.9487 | 0.0616 | 0.0323 | 0.0764 | 0.0413 | |

| * | n0 | n0 | n0 | * | ** | * | ** | ||

| With Constant & Trend | t-Statistic | 0.5104 | 0.5712 | 0.5952 | 0.1747 | 0.0134 | 0.2370 | 0.1121 | 0.3175 |

| Prob. | 0.1281 | 0.9689 | 0.1101 | 0.8197 | 0.2001 | 0.1288 | 0.1282 | 0.1583 | |

| n0 | n0 | n0 | n0 | n0 | n0 | n0 | n0 | ||

| Without Constant & Trend | t-Statistic | 0.1248 | 0.3128 | 0.0158 | 0.0001 | 0.0003 | 0.0378 | 0.0026 | 0.0430 |

| Prob. | 0.0138 | 0.4804 | 0.0256 | 0.9049 | 0.0050 | 0.0094 | 0.0057 | 0.0035 | |

| ** | n0 | ** | n0 | *** | *** | *** | *** | ||

| Note: Standard errors are in parentheses.***p <0.001,**p<0.05, and*p<0.1. | |||||||||

Table 5.

Panel least squares estimation using cross-sectional random and fixed effects for financial stability.

Table 5.

Panel least squares estimation using cross-sectional random and fixed effects for financial stability.

| Variable | Pooled OLS (No FE/RE) | Fixed Effects (FE) | Random Effects (RE) | ||||||

| Coef. | t-Stat | Prob. | Coef. | t-Stat | Prob. | Coef. | z-Stat | Prob. | |

| C | 753.049 | 0.37 | 0.716 | 2441.683 | 1.36 | 0.181 | 753.049 | 0.37 | 0.714 |

| ROA | 52165.06 | 0.91 | 0.367 | 1056.364 | 0.04 | 0.970 | 52165.06 | 0.91 | 0.363 |

| CAR | 2276.596 | 0.25 | 0.807 | 2208.195 | 0.53 | 0.598 | 2276.596 | 0.25 | 0.806 |

| SIZE | 0.0150 | 3.10 | 0.003 | 0.0165 | 2.82 | 0.007 | 0.0150 | 3.10 | 0.002 |

| LIQU | −9526.066 | −2.93 | 0.005 | 423.449 | 0.15 | 0.881 | −9526.066 | −2.93 | 0.003 |

| GDP | −1.97e-09 | −1.02 | 0.312 | −1.21e-08 | −1.54 | 0.130 | −1.97e-09 | −1.02 | 0.308 |

| INF | −18.304 | −0.13 | 0.894 | 82.101 | 1.33 | 0.189 | −18.304 | −0.13 | 0.894 |

| GEPU | 4.815 | 1.26 | 0.215 | 1.246 | 0.44 | 0.665 | 4.815 | 1.26 | 0.209 |

Source: Author calculation.

Table 6.

Hausman test (FE vs RE) for Model 1.

| Test summary (Model 1) | Chi-Sq. Statistic (Model 1) | Chi-Sq. d.f. (Model 1) | Prob. (Model 1) |

| Cross-section random | 48.00 | 4 | 0.0000 |

Significance codes: * p < 0.10.

Table 7.

Simultaneous Quantile Regression Results.

| Variable | Q0.10 | Q0.20 | Q0.30 | Q0.40 | Q0.50 | Q0.60 | Q0.70 | Q0.80 | Q0.90 |

| ROA | 39650.1 (0.124) | 30218.0 (0.275) | 25086.9 (0.468) | 28140.6 (0.447) | 28043.1 (0.695) | 22557.4 (0.767) | −3485.3 (0.972) | −11327.4 (0.936) | −18467.8 (0.876) |

| CAR | 3325.8 (0.553) | 2284.5 (0.666) | 2426.7 (0.679) | 2669.9 (0.701) | 2945.1 (0.890) | 3521.3 (0.845) | 1246.4 (0.948) | −97.9 (0.996) | −1439.1 (0.940) |

| SIZE | 0.0099 (0.000) | 0.0097 (0.000) | 0.0107 (0.018) | 0.0107 (0.077) | 0.0132 (0.322) | 0.0288 (0.070) | 0.0437 (0.016) | 0.0436 (0.033) | 0.0457 (0.003) |

| LIQU | −2218.9 (0.063) | −1245.0 (0.271) | −1401.5 (0.518) | −1008.1 (0.703) | −2130.6 (0.629) | −9309.9 (0.068) | −12622.6 (0.002) | −11326.3 (0.002) | −12470.4 (0.001) |

| GDP | −1.85e-09 (0.009) | −1.65e-09 (0.027) | −1.61e-09 (0.090) | −1.75e-09 (0.467) | −1.91e-09 (0.616) | −4.30e-09 (0.300) | −4.32e-09 (0.178) | −1.61e-09 (0.675) | 1.80e-09 (0.660) |

| INF | −57.12 (0.475) | −20.70 (0.790) | 16.99 (0.794) | 4.97 (0.961) | 51.29 (0.668) | 57.75 (0.691) | −21.70 (0.887) | −35.81 (0.795) | −57.95 (0.757) |

| GEPU | −2.76 (0.134) | −2.00 (0.263) | −2.78 (0.252) | −2.58 (0.471) | −1.07 (0.810) | 3.58 (0.426) | 0.70 (0.897) | −2.07 (0.758) | −4.69 (0.260) |

| Constant | 209.77 (0.870) | 159.60 (0.906) | 342.03 (0.803) | 245.29 (0.884) | 51.72 (0.991) | 92.59 (0.983) | 1273.11 (0.754) | 1680.63 (0.697) | 2352.60 (0.581) |

| Pseudo R² | 0.3668 | 0.3722 | 0.3238 | 0.2720 | 0.2335 | 0.2598 | 0.3475 | 0.4564 | 0.5175 |

Source: Author calculation.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.