Submitted:

05 July 2025

Posted:

07 July 2025

You are already at the latest version

Abstract

Purpose: This study aims to empirically examine the determinants of non-performing loans (NPLs) in selected private commercial banks in Ethiopia, focusing on both bank-specific and macroeconomic factors. Design/Methodology/Approach: The research adopts an explanatory design with a quantitative approach, analyzing panel data from twelve private commercial banks over a period of ten years (2012–2021). The data was processed using E-Views 10 software, employing descriptive statistics, correlation matrices, and multiple linear regression with both fixed and random effects models. Findings: The results indicate that exchange rates have a positive and statistically significant impact on NPLs. In contrast, income diversification, capital adequacy, loan growth rate, and loan-to-asset ratio show negative and significant effects on NPLs. Research Limitations/Implications: The study is limited to private commercial banks, thereby excluding public banks and non-bank financial institutions. Additionally, the reliance on secondary data may overlook qualitative factors that influence NPLs. Future research could broaden the sample size and incorporate primary data for deeper insights. Originality/Value: This study contributes to the literature by providing context-specific insights into the determinants of NPLs in Ethiopia's banking sector, addressing gaps in existing research. Its findings offer actionable recommendations for policymakers and bank managers to mitigate NPL risks, ultimately enhancing financial stability in emerging economies.

Keywords:

Non-performing loans

; bank-specific factors

; macroeconomic factors

; private commercial banks

; Ethiopia

1. Introduction

Bank loans are agreements between creditors and debtors, that is, between banks that lend money and other legal individuals that borrow it, with the promise of a future return of the principal plus interest. (Ramadhani, 2020).

An increase in non-performing loans (NPLs) in bank lending is a key warning sign of a currency crisis. Governments and banks have a lot of control over NPLs now that the global financial crisis is over because they are linked to banking system failures and crises. (Ghosh, 2015).

In Ethiopia, commercial banks have significantly expanded their loan accessibility during the previous two decades (Mesay, 2017a).However, data indicates that Ethiopian commercial banks experienced substantial financial fragility, as seen by an excessive amount of NPLs (Mehari, 2012). Recently, ECB NPLs have shown significant improvement, falling to an average of 5% (National Bank of Ethiopia, 2011). However, ECB NPLs remain high when compared to developing-country banks such as Namibia, Mozambique, and Uganda. (Zelalem, 2013).As a result, the focus of this study is on the primary causes of non-performing loans in the context of Ethiopian commercial banks.

- Specific Objectives

In line with the above general objective of the study, the following specific objectives are developing:

- To examine the impact of bank-specific variables on the NPLs of private commercial banks in Ethiopia;

- To examine the impact of macroeconomic variables on the NPLs of private commercial banks in Ethiopia;

- To examine the extent of the relationship that exists between bank-specific variables, macroeconomic variables, and the non-performing loans of private commercial banks in Ethiopia.

- 1.

- Literature Review

Researchers have identified various elements that affect the NPLs, including income diversification, capital adequacy, loan growth, loan-to-asset ratio, lending rate, and exchange rate. However, the relationship between NPLs and these factors is not clear. Some researchers concluded that these factors have positive relationships, while others reject their results.

1.1. Bank Specific Factors

- 1)

- Income diversification: Portfolio theory suggests that diversifying portfolios can minimize firm-specific risk by compensating losses in certain products with gains in others (Berhanu, 2019). However, scholars argue that revenue diversification doesn’t guarantee low NPLs due to excessive operational components (Zelalem, 2013).

H1:

Income diversification index has significant and negative relationship with NPLs of private commercial banks in Ethiopia.

- 2)

- Capital Adequacy: refers to the amount of capital needed by banks to withstand risks such as credit, market, and operational risks in order to absorb potential losses and protect the bank’s debtors. A bank’s capital adequacy is a measure of its overall financial strength. The higher the capital adequacy ratio, the greater the amount of protection provided to depositors, and it is crucial for maintaining the banking system’s soundness since it acts as a buffer against panic, bank runs, and other dangers. (Abdelbary, 2019).

H2:

There is a significant negative relationship between capital adequacy and the NPLs of private commercial banks in Ethiopia.

- 3)

- Loan Growth: Banks should focus on lending within their trade area and avoid lending outside of it. Emphasizing loan growth can negatively impact credit quality. Loan officers should avoid lending to marginal borrowers, limited expertise, or geographic areas without market presence (Natnael, 2017). Good loan supervision can reduce credit risk and improve loan growth. Credit risk is crucial for bank performance, and loan growth is related to nonperformance loans. Kirui (2014) cited Addae-Korankye (2014).

HP3:

There is a significant positive relationship between loan growth of a bank and the NPLs of private commercial banks in Ethiopia.

- 4)

- Loan to Asset Ratio: It is the ratio between the total loan amount and the total assets. A higher loan-to-assets ratio represents a high credit level and an increasing chance of credit risk. Therefore, a positive coefficient of loan-to-asset ratio is expected, which has also been shown by .(Klein & Shingjergji, 2013). However, (Ekanayake & Azeez, 2013) found a significant positive association between non-performing loans and the loans-to-assets ratio.

H4:

The loan-to asset ratio has a significant and negative relationship with the NPL of private commercial banks in Ethiopia.

1.2. Macroeconomic Factors

- 5)

- Lending Rates: Is a significant economic determinant of NPL. There is empirical evidence of a positive relationship between lending rates and NPLs. Banks anticipate normal loan portfolio performance in a healthy economy, as only a small percentage of loans default, and interest rates positively correlate with NPLs and bad loans(Sitina, 2018). A higher interest rate leads to even more adverse selection in this general situation; that is, a higher interest rate increases the possibility that the lender is lending to a risky credit risk, ultimately increasing NPLs (Rediet, 2020), (Sitina, 2018) and (Yonas, 2017).

H5:

There is a significant positive relationship between Lending rate and NPLs of private commercial banks in Ethiopia.

- 6)

- Exchange Rate: A change in the exchange rate, like inflation, can affect borrowers’ debt service capacity through several routes, and its impact on NPLs can be positive or negative (Atanasijević & Božović, 2016). Currency depreciation can boost export-orientated enterprises’ competitiveness by reducing domestic currency value and increasing their debt-servicing capabilities. However, it can negatively impact import-orientated firms, as their production costs are covered in less valuable domestic currency and revenue is collected in more valuable foreign currency (Khemraj & Pasha, 2009).

H6:

There is a significant negative relationship between the exchange rate and the NPLs of private commercial banks in Ethiopia.

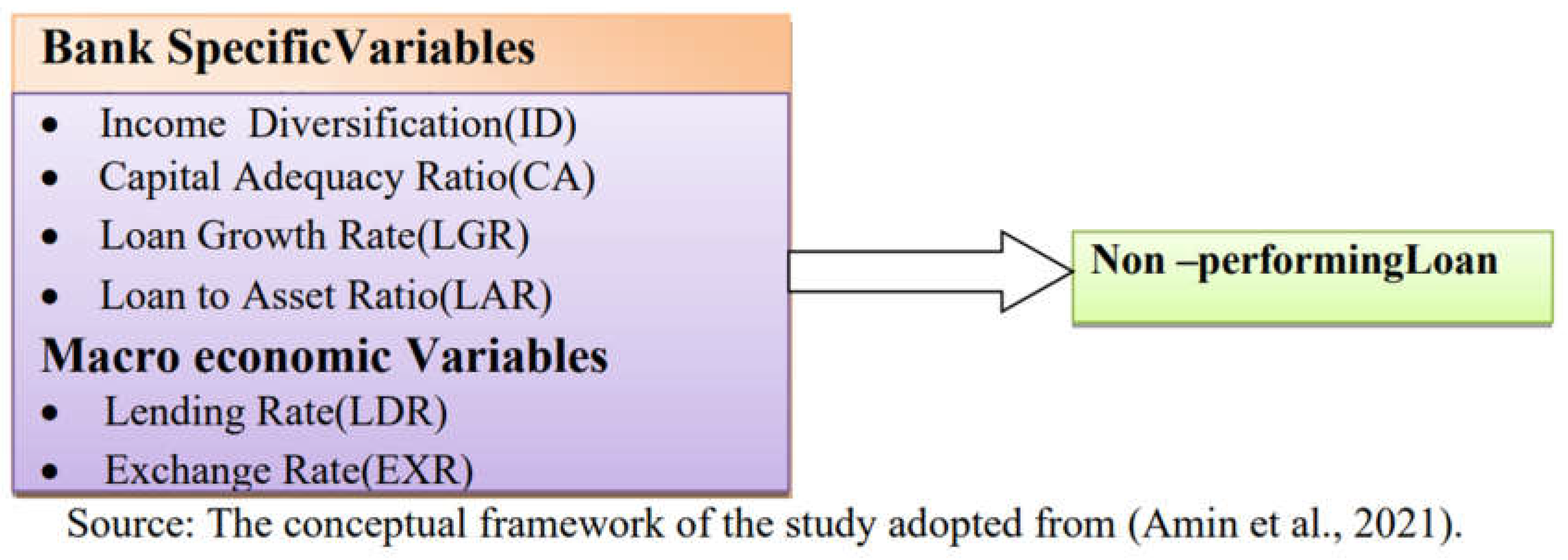

1.3. Conceptual Frame Work

Figure 1.

Conceptual framework.

2. Methodology

2.1. Research Design

The researcher utilized quantitative research methods to construct an empirical model and hypothesize its linear relationship between determinants and dependent variable.

2.2. Sources and types of data

The study utilized secondary data from audited financial statements from 2012 to 2021, focusing on the National Bank of Ethiopia’s financial statements. The researcher utilized panel data, combining cross-sectional and time series data, for reliable model parameter estimates, as per D. Gujarat (2004).

2.3. Population and Sample Size

The target population of the study includes all private commercial banks in Ethiopia, registered with the NBE. Twelve private commercial banks (Awash International Bank, Dashen Bank, Bank of Abyssinia, Wegegan Bank, Hibret Bank, Nib International Bank, Cooperative Bank of Oromia, Lion International Bank, Oromia International Bank, Zemen Bank, Buna International Bank and Berhan International Bank) were selected using purposive sampling method.

2.4. Model Specifications

The researcher used a panel data model to investigate the relationship between non-performing loans and income diversification, capital adequacy ratio, loan growth rate, loan-to-asset ratio, lending rate, and exchange rate, utilizing data from various empirical studies and utilizing fixed effects and random effect models.

The regression model for this investigation is estimated as follows:

Whereas the cross-section denotes the time-series dimension1, 2, 3, 4, 5, 6, and 6 represent the estimated coefficient for specific bank i at time t.0= the interceptNPL=non-performing-loan, ID = income diversification, CA = capital adequacy, LGR = loan growth rate, LAR = loan-to ratio, LDR = lending rate, EXR is the level of the exchange rate, and ε is the error term.

2.5. Data Analysis Methods

The study collects data from multiple sources and analyzes it using statistical techniques. Using descriptive statistics and regression, the study calculates patterns and determines the importance of explanatory variables in influencing commercial banks in Ethiopia.

3. Empirical Results and Discussions

Diagnostic test

The researcher used E-Views 10 software for statistical analysis and conducted diagnostic tests to verify OLS assumptions. The panel data model was run using random and fixed effect models, and multicollinearity, heteroscedasticity, normality, and autocorrelation tests were conducted to ensure the model met the classical linear regression model assumptions.

Table 1.

Descriptive Statistics.

| NPL | ID | CAR | LGR | LAR | LDR | EXR | |

| Mean | 0.034010 | 0.034336 | 0.139614 | 4.07420 | 0.57661 | 5.9180 | 0.343208 |

| Median | 0.033355 | 0.035341 | 0.137580 | 4.07580 | 0.58100 | 5.3900 | 0.345367 |

| Maximum | 0.057200 | 0.053251 | 0.199800 | 4.74250 | 0.92300 | 8.0000 | 0.529487 |

| Minimum | 0.010700 | 0.015646 | 0.097371 | 3.25720 | 0.26900 | 4.0000 | 0.175511 |

| Std. Dev. | 0.010954 | 0.009205 | 0.022697 | 0.355367 | 0.147598 | 1.421462 | 0.081027 |

| Observations | 120 | 120 | 120 | 120 | 120 | 120 | 120 |

Source: E-views-10 software output (2023).

As it can be seen from above table 1, for the total sample, the mean of NPLs was 3.4% with a minimum of 1.07 % and a maximum of 5.72%. This indicates that, from the total loans that EPCBs disbursed, an average of 3.34% were being default or uncollected over the sample period. The lowest NPLs ratio that ECBs experienced over the sample period was 1.07%. On the other extreme, the highest NPLs ratio of EPCBs was 5.72% which was in excess of the average 5% NPLs set by national bank of Ethiopia. The disparity between the minimum and the maximum of NPLs indicate the margin that NPLs ratio of EPCBs ranged over the sample period. The standard deviation (0.010954) of NPLs also shows the existence of low variation among EPCBs in terms of their loan recovering capacity as compared to other.

As can be seen from the above table for the total sample, the mean of income diversification, as measured by the ratio of non-interest income to total assets, was 3.43%, with a minimum of 1.57 % and a maximum of 5.33%. This indicates that there are banks that earn income other than interest income with a maximum and minimum value. The disparity between the minimum 1.57 % and the maximum 5.33 % of income diversification indicates the margin over which the income diversification ratio of Ethiopian private commercial banks(EPCBs) ranged over the sample period. The standard deviation (0.009205) of income diversification also shows the existence of low variation among EPCBs in terms of their income generation other than interest as compared to others.

The capital adequacy ratio shows the proportion of the owner’s equity to total assets. The mean value for the capital adequacy ratio was 13.96%, whereas the maximum level was 19.98% and the minimum one was 9.74%, with a standard deviation of 2.27%. The average amount of capital adequacy is greater than the minimum capital requirement of 8% of the NBE, showing that EPCBs have the ability to bear losses resulting from loan default.

LG of Ethiopian private commercial banks have a minimum of 17.55% growth rate, which shows it has no change on consecutive years, and the maximum of 52.94% with the third highest standard deviation of 8.103%, which implies that average annual loan growth has great variation in EPCBs. Among bank-specific variables employed in this study, LGR had a higher standard deviation, which was 8.103%, with a minimum of 17.55% (logarithm result) and a maximum of 52.94%.

As it can be seen from the above table, for the total sample, the mean loan asset ratio, measured by the total loan to asset ratio, was 57.66%, with a minimum of 26.9% and a maximum of 92.3%. This indicates that there are banks that have incurred collateral value so as to achieve improved credit risk management through adequate loan screening, monitoring, and control of borrowers with maximum and minimum value. Hence, it can be concluded that an increase in the loan-to-asset ratio of Ethiopian commercial banks can enhance the loan quality of banks and ultimately reduce the probability of NPLs. The standard deviation (0.147598) of the loan-to-asset ratio also shows the existence of low variation among EPCBs in terms of their outsourced resources other than payment as compared to others.

As can be seen from the above table, the exchange rate has a mean value of 34.32 birr, a minimum value of 17.55 birr, and a maximum value of 52.94 birr. This result tells us that the depreciation of the Ethiopian birr against the USD dollar was very high during the period 2012–2021.

As the above table 1 showed, for the total sample, the mean lending rate, as measured by the average lending rate, was 5.918000, with a minimum of 4 and a maximum of 8. This indicates that the bank’s maximum lending rate was 8 and the minimum was 4. This disparity between the minimum 4 and the maximum 8 of the lending rate indicates the margin over which the lending rate of EPCBs ranged over the sample period. The standard deviation (1.421462) of the lending rate also showed the existence of high variation over the sampled period. Thus, it can be concluded that the macroeconomic variables were relatively stable over the sample periods as compared to bank-specific variables, with the exception of some instability in the interest rate.

Table 2.

Result of Haussmann Tests.

| Correlated Random Effects - Hausman Test | ||||

| Equation: Untitled | ||||

| Test cross-section random effects | ||||

| Test Summary | Chi-Sq. Statistic | Chi-Sq. d.f. | Prob. | |

| Cross-section random | 0.000000 | 6 | 1.0000 | |

| The cross-sectional test variance is invalid. Hausman statistic set to zero. | ||||

Source: E-views-10 software output (2023)

The Haussmann test results indicate that a random effect model is more suitable for this study, as the P-value of 1.0000 is over 0.05, indicating its validity.

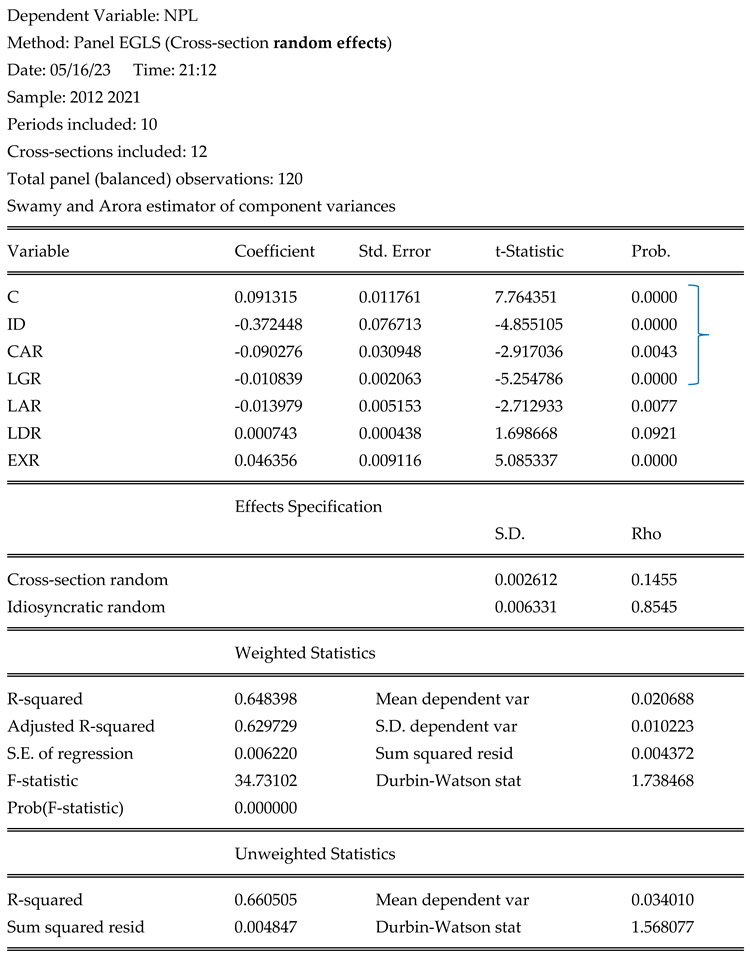

Table 3.

Regression Result.

Source: E-views-10 software output (2023)

Income diversification: As the above table 3 showed, the mean value of income diversification, which was measured by the ratio of non-interest income to total assets, is -0.372448, and its p-value is also 0.0000. This shows that when income diversification decrease by one NPL ratio increase by 0.37, keeping others constant. Based on the result, the study hypothesis is not rejected, and the result is also consistent with the findings of the previous study conducted by(Berhanu, 2019).

Capital Adequacy Ratio: As indicated in Table 3 above, the coefficient of capital adequacy (measured by equity to total asset) and the coefficient of beta are -0.090276 with a p-value of 0.0043. This concludes that there is a negative and statistically significant relationship between capital adequacy and NPLs reported by the sampled private commercial banks in Ethiopia. This means that if capital adequacy ratio decrease by 1%, the non-performing loans of private commercial banks will increases by 0.0903, keeping others constant. This finding was consistent with previous studies, for instance. (Gadise, 2014) and (Yosef, 2018) found that capital adequacy has a negative and statistically significant relationship with the NPLs of private commercial banks.

Loan growth: As indicated above in the regression result, a variable used to capture a bank’s loan growth rate had a coefficient estimate of -0.010839 and was statistically significant at the 1% significance level (P-value = 0.0000). This means that if loan growth rate decrease by 1%, the non-performing loans of private commercial banks will increases by 0.0108, keeping others constant. This finding was consistent with previous studies, for instance. (Sitina, 2018), and (Frehiwot 2020), found that loan growth rate has a negative and statistically significant relationship with the NPLs of private commercial banks.

Loan to Asset Ratio: Table 3 showed that the coefficient of loan to asset ratio is -0.014. The coefficient indicates that there is significant and negative relationship between loan to asset ratio and Ethiopian private commercial bank NPL even at 1% significant level. This means that when capital loan to asset ratio decrease by 1%, the non-performing loans of private commercial banks will e increases by 0.014, keeping others constant. This result was consistent with earlier research. However, the beta coefficient is different from the early study results, for example. (Klein & Shingjergji,2013) and (Ekanayake & Azeez, 2013) found that loan growth rate has a positive and statistically significant relationship with the NPLs of private commercial banks.

Lending Rate: as indicated in table 3 lending rate has insignificant relationship with nonperforming loans of private commercial banks in Ethiopia.

Exchange rate: as indicate in the table 3, there is a positive association between the birr-to-dollar exchange rate and nonperforming loans. This indicates that exchange rate increased by 1%, the non-performing loans ratio of private commercial banks increases by 0.04, keeping others constant. According to (Khemraj & Pasha, 2009), the literature on the relationship of the exchange rate produces mixed results. The currency rate and non-performing loans have a favorable association. An increase in exchange rates can have a negative impact on the loan payment capacity of export-oriented firms (Fofack & Fofack, 2005), but it can also have a positive impact on the loan payment capacity of borrowers who borrow in foreign currency. The relationship between nominal exchange rate and non-performing loans is indeterminate.

4. Conclusions

This research aimed to analyze the determinants of Non-Performing Assets (NPLs) in Ethiopian Private Commercial Banks (EPCBs) using a quantitative approach. Data from twelve banks was analyzed using descriptive statistics and multiple linear regression analysis from 2012 to 2021, comparing internal and external determinants.

Bank-specific variables like income diversification, capital adequacy, loan growth rate, and loan-to-asset ratio strongly negatively impact NPLs in Ethiopian private commercial banks, indicating a correlation between these factors. The regression results show a positive and significant linear relationship between macroeconomic variable exchange rate and non-performing loans of Ethiopian private commercial banks.

References

- Abdelbary, A. (2019). Changing The Game; New Framework Of Capital Adequacy Ratio.

- Akmel, D. (2019). Determinants of non-performing loan: The case of Ethiopian commercial banks.

- Amin, M. I., Ahsan, A., Al muktadir, M., Azad, M., & Rezanur, R. H. B. (2021). Macroeconomic and Firm-specific Factors Influencing Non-Performing Loans in Bangladesh: A Panel Data Regression Approach. The Journal of Asian Finance, Economics and Business, 8(12), 95–105.

- Atanasijević, J., & Božović, M. (2016). Exchange rate as a determinant of corporate loan defaults in a Euroized economy: Evidence from micro-level data. Eastern European Economics, 54(3), 228–250. [CrossRef]

- Ayele, F. (2017). Assesments Of Non-Performing Loans: A Study On Selected Commercial Banks In Ethiopia.

- Babu, B. S. (2018). Capping Of Commercial Bank Interest Rates and Its Impact on Number of Loan Advances Generated By Microfinance Institutions.

- Barr, R., Siems, T. (1994). “Predicting Bank Failure using DEA to quantify management quality” Federal Reserve Bank of Dallas, Financial industry Studies. 94.

- Belay, T. (2020).Determinants Of Non-Performingloans In Ethiopian Commercial BankS.

- Berhanu, B. B. (2019). Determinants of non- performing loan in commercial bank’s in Ethiopia. MSc Thesis, Addis Ababa University.

- Blanco, R., & Gimeno, R. (2012). Determinants of default ratios in the segment of loans toto households in spain.

- Bolt, W., Tieman, A. F. (2004). Banking Competition, Risk and Regulation. International Monetary Fund Working Paper WP/04/11.

- Boudriga, A., Taktak, N. B., &Jellouli, S. (2009). Banking supervision and nonperforming loans: A cross-country analysis. Journal of Financial Economic Policy.

- Braun, B., & Koddenbrock, K. (2022). The three phases of financial power: Leverage, infrastructure, and enforcement.

- Breuer, J. B. (2006). Problem bank loans, conflicts of interest, and institutions.Journal of Financial Stability, 2, 266–285.

- Brooks, C. (2008a). Introductory Econometrics for Finance,. Ntroductory Econometrics for Finance, 2nd Edn, Cambridge University Press, New York.

- Brooks, C. (2008b). Introductory Econometrics for Finance, 2nd edn, Cambridge University Press, New York. Book.

- Brooks, C. (2008c). Introductory Econometrics for Finance Second Edition, New York, University of Reading.

- Calice, P., Chando, V., & Sekioua, S. (2012). Bank Financing to Small and Medium Enterprises in East Africa: Findings of a Survey in Kenya, Tanzania, Uganda and Zambia. African Development Bank Group Working Paper, March, 1–41.

- Ciukaj, R., & Kil, K. (2020). Determinants of the non-performing loan ratio in the European Union banking sectors with a high level of impaired loans. Economics and Business Review, 6(1), 22–45. [CrossRef]

- De la Torre, A., Pería, M. S. M., & Schmukler, S. L. (2010). Bank involvement with SMEs: Beyond relationship lending. Journal of Banking & Finance, 34(9), 2280–2293. [CrossRef]

- Delil, A. (2019). School of Graduate Studies Determinants of Non-Performing Loan: The Case of Ethiopian Commercial Banks Determinants of Non-Performing Loan: The Case of Ethiopian Commercial Banks.

- Demirguc-Kunt and Enrica Detragiache. (1998). “The Determinants of Banking Crises in Developing and Developed Countries”,. IMF Staff Paper, 45(1), 81–109. [CrossRef]

- El-Maude, J. G., Abdul-Rahman, A., & Ibrahim, M. (2017). Determinants of non-performing loans in Nigeria’s deposit money banks. Archives of Business Research, 5(1), 74–88. [CrossRef]

- Fernández de Lis, S., Martínez Pagés, J., & Saurina Salas, J. (2000).Credit growth, problem loans and credit risk provisioning in Spain. Banco de España. Servicio de Estudios.

- Fisher, I. (1933). The Debt Deflation Theory of Great Depressions.Econometrical, 1, 337–357. [CrossRef]

- Fofack, H., & Fofack, H. L. (2005). Nonperforming loans in Sub-Saharan Africa: Causal analysis and macroeconomic implications (Vol. 3769). World Bank Publications.

- GADISE, G. (2014). Determinants of nonperforming loans: Empirical study in case of Commercial banks in Ethiopia. MSc thesis, Jimma University.

- Garr, D. K. (2013). Determinants of credit risk in the banking industry of Ghana.Developing Country Studies, 3(11), 64–77.

- Gezu, G. (2014). Determinants of nonperforming loans: Empirical study in case of commercial banks in Ethiopia.

- Ghorbani&Jakobsson. (2019). Determinants of Non-Performing Loans.Econometrica, 77, 1229–1279.

- Ghosh, A. (2015). Banking-industry specific and regional economic determinants of non-performing loans: Evidence from US states. Journal of Financial Stability, 20, 93–104. [CrossRef]

- Gujarat, D. (2004).Basic Econometric, 4th edn. USA: McGraw–Hil.

- Gujarat, N. (2004). Basic Econometric, 4th edition, USA: McGraw–Hill. Boston. Books.

- Gulati, R. (2022). Global and local banking crises and risk-adjusted efficiency of Indian banks: Are the impacts really perspective-dependent? The Quarterly Review of Economics and Finance, 84, 23–39.

- Habtamu, N. (2012). Determinants of Bank Profitability: An Empirical Study on Ethiopian Private Commercial Banks: Published Thesis (MSC), Addis Ababa University.

- Hafer, R. (2005). „The Federal Reserve System‟, Greenwood Publishing Group.

- Hox, J. J., & Boeije, H. R. (2005). Data collection, primary versus secondary.

- IMF. (2010). Determinations of NPL in Developing countries.Of Engineering Economics, 23(5), 496–504.

- Jeong, S., Jung, H. (2013). Bank Wholesale Funding and Credit Procyclicality: Evidence from Korea. Pano-economicus,. 60(5), 615–631. [CrossRef]

- Jovovic, J. (2014). Determinants of Non-Performing Loans: Econometric Evidence Based on 25 Countries. Master Thesis, City University London.

- Khemraj, T., & Pasha, S. (2009). The determinants of non-performing loans: An econometric case study of Guyana.

- Kindleberger, C. P. (2015). A financial history of Western Europe. Routledge.

- Kithinji, A. M. (2010). Credit risk management and profitability of commercial banks in Kenya.

- Kolapo, T. F., Ayeni, R. K., &Oke, M. O. (2012). Credit Risk And Commercial Banks’performance In Nigeria.Australian Journal of Business and Management Research,2(2), 3.

- Kirui, Simion. (2014). The effect of non-performing loans on profitability of commercial.

- banks in Kenya. (Master’s Degree Thesis), University of Nairobi, Kenya.

- Kwambai,.D.K .&Wandera, M. (2013). Effects of credit information sharing on nonperforming loanscommercial bank kenya. 9(13), 168–193.

- Louzis, P. D., Vouldis, A. T., Metaxas, V. L. (2012). Macroeconomic and Bank-Specific Determinants of Non-Performing Loans in Greece: A Comparative Study of Mortgage, Business and Consumer Loan Portfolios. Journal of Banking and Finance, 36(4), 1012–1027. [CrossRef]

- Machiraju, H. (2001). Modern Commercial Banking, India: VIKAS Publishing House Pvt. Ltd. Co.

- Makri et al. (2014). Determinants of Nonperforming Loans: The Case of Eurozone. Panoeconom, 2, 193–206.

- Marshal, I., & Onyekachi, O. (2014). Credit risk and performance of selected deposit money banks in Nigeria: An empirical investigation. European Journal of Humanities and Social Sciences Vol, 31(1).

- Mazreku, I., Morina, F., Misiri, V., Spiteri, J. V., & Grima, S. (2018). Determinants of the level of non-performing loans in commercial banks of transition countries. [CrossRef]

- Mehari, M. (2012). Credit risk management in Ethiopia banking industry‟, MBA thesis, Addis Ababa University.

- Mesay, T. (2017a). Determinant of non performing loan. THESIS.

- Mesay, T. (2017b). Determinant of non-performing loan in Ethiopian private commercial banks: With emphasis on manufacturing sector. MSc thesis, Addis Ababa University.

- Mesele, B. (2016). Determinants of nonperforming loans of ethiopian commercial banks.

- Meseret, H. (2018). Determinants of nonperforming loan: Evidence from private commercial banks in Ethiopia.MSc thesis, St. Mary’s university.

- Mileris, R. (2012a). Macroeconomic Determinants of Loan Portfolio Credit Risk in Banks.IzerineEkonomika-Engineering. Economics, 23(5), 496–504. [CrossRef]

- Mileris, R. (2012b). Macroeconomic Determinants of Loan Portfolio Credit Risk in Banks.IzerineEkonomika-Engineering Economics,. 23(5), 496–504. [CrossRef]

- Monicah W AnjruMuriithi. (2013). The Causes of Non-Performing Loans in Commercial Bank in Kenya.

- Moradi, Z. S., Mirzaeenejad, M., & Geraeenejad, G. (2016). Effect of bank-based or market-based financial systems on income distribution in selected countries. Procedia Economics and Finance, 36, 510–521. [CrossRef]

- Muriithi, J. G., Waweru, K. M., & Muturi, W. M. (2016). Effect of credit risk on financial performance of commercial banks Kenya. [CrossRef]

- Natnael, Tefera. (2017). Factors Affecting Non-Performing Loans In Banking Industry In.

- Ethiopia: A Case of Dashen Bank, MA Thesis, St. Mary’s University, School of Graduate Studies, Addis Abba, Ethiopia.

- NBE. (2008). Asset classification and Provisioning for development financial institution Directive. 43.

- NBE. (2012). Asset classification and Provisioning for development financial institution Directive , Addis Ababa Ethiopia. SBB, 52.

- Ogar, A., Nkamare, S., & Effiong, C. (2014). Commercial bank credit and its contributions on manufacturing sector in Nigeria. Research Journal of Finance and Accounting, 5(22), 188–196.

- Onyango, W. A., & Olando, C. O. (2020). Analysis on influence of bank specific factors on non-performing loans among commercial Banks in Kenya. Advances in Economics and Business, 8(3), 105–121. [CrossRef]

- Rajaraman, I., &Vasishtha, G. (2002). Non-performing loans of PSU banks: Some panel results. Economic a, 429–435.

- Ramadhani, R. (2020). Legal Consequences of Transfer of Home Ownership Loans without Creditors’ Permission. International Journal Reglement & Society (IJRS), 1(2), 31–37. [CrossRef]

- Rawlin Rajveer , M. Shwetha M., S. and P. B. L. (2012). Modeling the NPA of Midsized Indian Nationalized Bank as Function of Advances. European Journal of Business and Management, 4(5).

- Rediet, G. . (2020). Determinants of Non-performing loan: A case of Development bank of Ethiopia.

- Rhodes, C. J. (2014). Mycoremediation (bioremediation with fungi)–growing mushrooms to clean the earth. Chemical Speciation & Bioavailability, 26(3), 196–198. [CrossRef]

- Ruozi, R., Ferrari, P., Ruozi, R., & Ferrari, P. (2013). Liquidity risk management in banks: Economic and regulatory issues. Springer.

- Saba, I. (2018a). Determinants of Non-Performing Loans. Case of US Banking Sector, 44(3), 81–121.

- Saba, I. (2018b). Determinants of Non-Performing Loans: Case of US Banking Sector. 44(3), 81–121.

- Saba, I., Kouser, R., & Azeem, M. (2012). Determinants of non performing loans: Case of US banking sector. The Romanian Economic Journal, 44(6), 125–136.

- Sitina, A. (2018).Determinants of Non-performing Loans in Ethiopian Commercial Banks By: MSc thesis, Addis Ababa University College.

- Soedarmono, W., Machrouh, F., & Tarazi, A. (2011). Bank market power, economic growth and financial stability: Evidence from Asian banks. Journal of Asian Economics, 22(6), 460–470. [CrossRef]

- Spaseska, T., Hristoski, I., Odzaklieska, D., & Risteska, F. (2022). Macroeconomic Determinants of Non-Performing Loans in the Republic of North Macedonia. 190–204.

- Spuchľáková, E., Valašková, K., & Adamko, P. (2015). The credit risk and its measurement, hedging and monitoring. Procedia Economics and Finance, 24, 675–681.

- Tamang, B. (2022).Impact of Credit Performance on the Profitability of Commercial Banks in Nepal.

- Tseganesh. (2012). Determinants of Banks Liquidity and Their Impact on Financial Performance: Published thesis (MSc), University Addis Ababa, Ethiopia.

- Uppal, R. K. (2009). sector advances: Trends, issues and strategies. Journal of Accounting and Taxation, 1(5), 79–89.

- Yonas, A. B. (2017). Assessment of the determinants of non-performing loans: The case of commercial banks in Ethiopia. MSc thesis, Addis Ababa University.

- Yosef, F. (2018). “ Determinants of Non-Performing Loans: Evidence from Commercial Banks in Ethiopia.MSc thesis, Addis Ababa university. 1–88.

- Zelalem, T. . (2013). No TitleDeterminants of Non-performing Loans: Empirical Study on Ethiopian Commercial Banks. 66(1997), 37–39.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.