Submitted:

07 February 2026

Posted:

12 February 2026

You are already at the latest version

Abstract

Financial inclusion has remained a persistent challenge in Zambia, where structural barriers such as limited banking infrastructure, high service costs, and uneven financial literacy have historically restricted access to formal financial services for low-income and marginalised populations. Despite recent national initiatives and financial sector reforms, significant gaps remain between inclusion targets and actual usage of formal financial systems. This study therefore examines the core problem of whether financial technology—specifically FinTech credit, savings, and transaction services—has meaningfully expanded access, usage, and quality of financial participation among Zambian consumers. The primary aim of the research is to generate a nuanced and disaggregated assessment of how different FinTech service categories influence financial inclusion outcomes rather than treating FinTech as a homogenous technological phenomenon. To achieve this, the study employed a mixed-methods research design that integrates quantitative survey data from FinTech users in Lusaka District with qualitative interviews involving service providers, regulatory officials, and targeted user groups. The quantitative findings demonstrate that transactional FinTech services exert the strongest positive effect on inclusion by reducing barriers to payments and enabling everyday financial activity, while savings services show moderate contributions to financial resilience. Digital credit services expand liquidity access but also introduce risks associated with repayment pressure and pricing transparency. The study’s implications emphasise the need for consumer protection, strengthened regulatory frameworks, improved digital literacy, and service designs aligned with users’ socio-economic contexts to ensure that FinTech operates as a genuine driver of inclusive financial development.

Keywords:

FinTech

; digital credit

; mobile transactions

; digital savings

; financial technology

; financial inclusion

; mobile money

; digital wallets

; economic empowerment

; digital divide

; emerging economies

; financial services access

1. Introduction

Financial inclusion has become a central pillar of socio-economic development in many emerging economies, including Zambia. Broadly defined as the availability, accessibility, and usage of affordable financial services by all segments of society, financial inclusion promotes poverty reduction, economic stability, and inclusive growth. In Zambia, financial exclusion remains high, particularly among low-income earners, informal sector workers, rural populations, and women. Although policy reforms and the expansion of mobile money have improved access over the past decade, gaps between the financially included and excluded persist. Within this context, financial technology (Fintech) has emerged as a transformative force, offering innovative solutions to structural barriers such as distance, documentation requirements, high transaction costs, and limited banking infrastructure. Through mobile money, digital credit, savings platforms, and online payment systems, Fintech extends financial services to previously underserved populations who historically relied on informal financial mechanisms.

Despite these advances, evidence regarding the impact of Fintech on financial inclusion in Zambia remains limited and inconclusive. While global and regional studies highlight Fintech’s potential to improve access to payments, credit, and savings, there are concerns about predatory lending, digital fraud, and exclusionary design. In Zambia, much of the existing knowledge is derived from industry reports, regulatory statements, or descriptive analyses rather than empirical research grounded in user experiences. Consequently, there is limited understanding of how specific Fintech services—credit, savings, and transactional platforms—affect financial inclusion outcomes among everyday users, presenting a clear research gap.

Lusaka District, as Zambia’s economic hub and the region with the highest Fintech activity, offers a unique context for examining these dynamics. The city hosts a diverse ecosystem of mobile network operators, digital lenders, banks, and emerging Fintech startups. Understanding user engagement in this setting provides empirical insights for national financial inclusion strategies, regulatory interventions, and digital finance policies. Lusaka also serves as a reference point for potential scaling of Fintech solutions to regions with lower connectivity or digital literacy.

This study is academically significant because it addresses the knowledge deficit regarding Fintech’s role in inclusive finance in developing economies. While Fintech has been studied extensively in countries such as Kenya, India, and China, Zambia has received comparatively limited attention. By focusing on credit, savings, and transaction services, this research examines the mechanisms through which digital financial tools influence financial inclusion, highlighting both enabling and constraining factors. Practically, the findings offer insights for banks, mobile network operators, Fintech firms, and consumer protection agencies to design effective financial products, enhance digital access, and reduce vulnerabilities. For government institutions, such as the Bank of Zambia and Ministry of Finance, understanding these dynamics provides evidence for improving regulatory frameworks, expanding digital infrastructure, and fostering innovation.

The study is guided by three core research objectives: assessing the influence of Fintech credit services on financial inclusion in Lusaka District; examining the impact of Fintech savings services on financial inclusion; and evaluating the effect of Fintech transaction services on financial inclusion. These objectives enable the study to explore different dimensions of Fintech usage—from digital loans to mobile money payments—while considering user demographics, behavioural patterns, and perceptions, which are critical for understanding the translation of adoption into meaningful financial participation. The research also highlights potential risks, limitations, and inequalities that may accompany digital financial expansion.

The structure of the article reflects this approach. Following this introduction, the literature review presents theoretical perspectives and prior studies on Fintech and financial inclusion, identifying knowledge gaps. The conceptual framework outlines the theoretical lens and relationships guiding the study. The methodology section details the mixed-methods design, sampling strategies, and analytical procedures. The findings section presents results from user responses and interviews, highlighting the influence of credit, savings, and transactional Fintech services. The discussion interprets the findings in relation to existing scholarship and draws implications for policy and practice. Finally, the conclusion summarises contributions, provides recommendations, and suggests avenues for future research.

Through this structure, the article provides a focused and empirically grounded analysis of Fintech’s contribution to financial inclusion in Zambia, offering insights to inform national strategies for digital finance and inclusive socio-economic development.

2. Literature Review

Financial inclusion, defined by the World Bank (2017) as access to useful and affordable financial services for individuals and businesses, has been widely recognized as essential for reducing poverty and stimulating economic growth. Across global scholarship, financial technology (Fintech) emerges as a critical enabler of this agenda, offering innovative digital solutions that circumvent the limitations of traditional banking systems, especially in underserved regions (Arner, Barberis & Buckley, 2016). A large body of research from North America, Europe, Latin America, Asia, and Africa consistently highlights how mobile payments, digital credit, online banking, peer-to-peer platforms, and algorithm-driven lending mechanisms broaden financial participation for those excluded from conventional systems (Gomber et al., 2017). In North America, studies demonstrate that Fintech enhances access to financial services among low-income, rural, and minority communities. For instance, the U.S. Consumer Financial Protection Bureau (CFPB, 2018) documents how mobile banking applications and digital financial tools have expanded formal financial participation, although gaps in financial literacy continue to impede the full realization of these benefits. Similarly, research from the Bank of Canada (2019) shows that Fintech lenders have eased credit constraints for small and medium-sized enterprises (SMEs) through alternative credit assessments rooted in big data analytics. However, this body of literature repeatedly raises concerns about inadequate regulatory mechanisms, transparency risks, and the lack of long-term evidence regarding the sustainability of digital lending practices (Demirgüç-Kunt & Klapper, 2020; IMF, 2020).

In Europe, the rise of digital-only banks such as N26 and Revolut—supported by the European Union’s PSD2 framework—has accelerated financial inclusion by lowering costs and expanding access to banking services (Zavolokina et al., 2020). Nevertheless, much of this research focuses on urban populations, neglecting adoption challenges in rural areas and underexploring cybersecurity risks associated with open-banking data sharing. In Latin America, where financial exclusion has historically been high, Fintech platforms such as Nubank and Mercado Pago have broadened access to credit and payments by reducing bureaucratic barriers and offering low-cost services (Frost, 2020). Yet these studies often fail to interrogate structural challenges such as digital literacy limitations, unequal internet access, and macroeconomic instability, which can affect both adoption and long-term sustainability of Fintech innovations. Asian studies reveal similar patterns of transformative impact alongside critical limitations. India’s Unified Payments Interface (UPI), for example, has democratized digital transactions and reduced reliance on cash (Shankar, 2021), but researchers acknowledge that digital divides—particularly in rural areas—continue to restrict comprehensive inclusion (Chuen & Teo, 2015). In China, Ant Group’s Sesame Credit has broadened credit access for individuals with minimal credit history, yet studies highlight privacy concerns, data-driven discrimination, and insufficient regulatory oversight as significant risks that require deeper scholarly and policy attention (Kshetri, 2020).

Across Africa, Fintech has gained immense traction due to limited formal banking infrastructure and widespread reliance on informal economic systems. Mobile money platforms such as Kenya’s M-Pesa have demonstrated profound poverty-reducing effects, enabling secure transactions, savings, and transfers for low-income populations who lack access to formal banking (Jack & Suri, 2011; Suri & Jack, 2016). While the Kenyan model is celebrated globally, scholars note that its replication across the continent has been uneven due to regulatory constraints, limited network coverage, and insufficient research on long-term socio-economic outcomes (Aker & Mbiti, 2010). In Tanzania and Ghana, mobile money has supported micro-entrepreneurship and boosted account ownership (Demirgüç-Kunt et al., 2018; Muthiora, 2015), though existing studies rarely explore intra-country disparities, the long-term impacts on business performance, or the interaction between mobile money and broader development indicators such as health and education. African scholarship also highlights the role of Fintech in addressing gender disparities. Studies indicate that mobile banking has helped reduce the gender gap in financial access by enabling women to bypass socio-economic barriers that traditionally restrict engagement with formal banking systems (Suri & Cull, 2019). However, persistent socio-cultural restrictions, limited digital literacy, and affordability issues continue to constrain women’s meaningful participation. Research on digital microloans—offered by platforms such as Branch and Tala—underscores their contribution to credit expansion for underserved populations in countries like Uganda and Tanzania (Chen & Mazer, 2016), but recurrent concerns about over-indebtedness, exploitative interest rates, and inadequate consumer protection remain unresolved. Additional African literature discusses cryptocurrency’s potential to address inflationary instability in economies such as Zimbabwe and Nigeria (IMF, 2020), and the role of remittance platforms like WorldRemit in lowering transaction costs and increasing economic resilience (Beck & Munzele Maimbo, 2013). Yet, gaps persist regarding regulatory harmonization, user protection, and integration of remittances with broader financial services such as savings and insurance. Moreover, rural Africa continues to suffer from weak digital infrastructure, limiting the reach of Fintech innovations (World Bank, 2020).

Within Zambia, Fintech has similarly transformed the financial landscape, particularly through mobile money platforms such as MTN Mobile Money and Airtel Money. According to the Bank of Zambia’s Financial Inclusion Survey (2015), over half of the population now has access to mobile money, significantly improving access in remote areas with limited banking infrastructure. Studies by Kumwenda and Chileshe (2018) affirm these positive impacts but also emphasize low financial literacy as a barrier to maximizing mobile money’s benefits. Research also shows that Fintech has supported economic empowerment, especially among women and young people, by facilitating access to credit and savings tools that enable income-generating activities (Zulu, 2017). However, socio-cultural limitations and gendered economic barriers continue to constrain the full potential of these technologies. Studies on MSMEs highlight that while Fintech platforms such as Zoona and PayPal have improved payment systems and access to working capital, digital financial services in Zambia remain predominantly consumer-oriented rather than business-oriented, limiting MSMEs' ability to fully leverage digital finance for growth (Mwansa & Mwewa, 2019).

Furthermore, a lack of an enabling regulatory environment poses challenges for Fintech expansion, particularly regarding AML/KYC compliance, startup barriers, and uneven enforcement of digital finance regulations (Sikalinda & Mulenga, 2020). Research on digital credit services in Zambia—particularly platforms like Branch and Tala—shows that these services have broadened credit access for unbanked populations (Chanda & Banda, 2018), though concerns regarding multiple borrowing, over-indebtedness, and weak consumer protection frameworks are recurrent themes. Studies also highlight the growing importance of Fintech in facilitating remittances, where digital platforms have reduced costs and increased speed, though gaps remain regarding integration with savings, investment tools, and the broader financial ecosystem (Mwale & Mumba, 2019). Broader analyses of Zambia’s Fintech environment identify continuing barriers such as low digital literacy, high data costs, limited smartphone access, and inadequate rural digital infrastructure, which significantly restrict the reach and impact of Fintech services (Kasongo & Mutale, 2020).

Overall, the literature establishes that Fintech has dramatically expanded financial access globally, regionally, and within Zambia by offering innovative and accessible digital solutions that overcome traditional banking barriers. However, across all contexts, persistent gaps remain, including insufficient digital literacy, incomplete regulatory frameworks, uneven rural access, gender-based constraints, data privacy concerns, weak consumer protection, limited MSME-specific digital products, and a lack of longitudinal evidence on the sustainability and socio-economic impact of Fintech adoption. These gaps underscore the need for more targeted, context-specific, and empirically grounded research to fully understand how Fintech can sustainably enhance financial inclusion, particularly in developing economies such as Zambia.

3. Conceptual / Theoretical Framework

The conceptual framework for understanding the relationship between Fintech services and financial inclusion in Zambia is grounded in a synthesis of technology adoption, financial intermediation, and behavioural finance perspectives. At its core, the framework posits that Fintech services—specifically credit, savings, and transactional platforms—serve as independent variables that influence financial inclusion, which is conceptualized as access, usage, and quality of financial services among underserved populations. Technology adoption theories, particularly the Technology Acceptance Model (TAM), provide a foundation for understanding user engagement with Fintech platforms. According to TAM, perceived usefulness and perceived ease of use significantly determine an individual’s decision to adopt digital financial tools (Davis, 1989; Venkatesh & Davis, 2000). In the Zambian context, these constructs manifest through mobile money applications, digital credit services, and online savings accounts, where convenience, speed, and accessibility enhance uptake among low-income and informal sector users. Complementing TAM, Rogers’ Diffusion of Innovations Theory emphasizes the role of relative advantage, compatibility, trialability, and observability in the spread of new technologies (Rogers, 2003). This theory elucidates why certain Fintech innovations, such as M-Pesa-inspired mobile money services or app-based digital lending platforms, gain rapid acceptance: they provide clear benefits over traditional banking methods, integrate with existing financial practices, allow low-risk experimentation, and make benefits visible to peers.

Financial Intermediation Theory further underpins the conceptual framework by explaining how Fintech platforms reduce traditional barriers to accessing financial services. Digital financial services lower transaction costs, mitigate information asymmetries, and facilitate alternative credit assessment mechanisms, allowing individuals without formal collateral or credit history to engage with financial markets (Levine, 2005; Ozili, 2018). This mechanism is evident in Zambia’s digital credit offerings, where mobile-based algorithms assess repayment capacity using behavioural and transactional data rather than formal documentation, thereby broadening the financial reach of underserved communities. Behavioural Finance Theory adds another layer by highlighting how cognitive biases, trust, and socio-economic constraints shape financial decision-making (Karlan et al., 2016; Schaner, 2017). Users’ willingness to adopt Fintech services is influenced by perceptions of reliability, fear of fraud, and prior experiences with formal financial institutions, which interact with socio-economic status to determine patterns of savings, borrowing, and transactional behaviour.

The framework integrates these theoretical perspectives to conceptualize Fintech adoption as a mediating factor between technological innovation and financial inclusion outcomes. Credit services are expected to expand access to short-term loans, improve household liquidity, and support entrepreneurial activities, whereas digital savings tools enhance financial discipline, convenience, and the accumulation of emergency funds. Transactional services, particularly mobile money, are conceptualized as facilitating daily financial interactions, enabling remittances, and promoting financial resilience. Moderating factors such as digital literacy, trust in technology, socio-economic status, and regulatory environment are incorporated to account for variations in adoption and impact. Digital literacy affects users’ capacity to navigate Fintech interfaces effectively, while trust mediates the perceived security and reliability of these platforms (Kombian & Zulu, 2021). Socio-economic factors, including income level, employment status, and urban-rural location, influence both the ability to access and the incentives to use digital financial services. Regulatory and institutional frameworks further shape the operational environment for Fintech providers, affecting transparency, consumer protection, and overall service reliability (Gabor & Brooks, 2017; Bank of Zambia, 2022).

Empirical evidence supports the framework’s relevance. Studies from Kenya, Tanzania, and Uganda demonstrate that mobile money adoption significantly enhances financial inclusion by lowering transaction costs and providing alternative credit channels for previously unbanked populations (Aker & Mbiti, 2010; Suri & Jack, 2016; Ky & Venkatesh, 2021). In Zambia, research shows that mobile money platforms increase accessibility for informal sector workers, simplify small business payments, and provide short-term credit opportunities, although challenges related to trust, high-interest rates, and digital literacy persist (Chikumbi, 2020; Musawa & Mwaanga, 2021; Mwila & Mvunga, 2022). These findings validate the inclusion of behavioural, technological, and institutional variables within the framework, highlighting the complex interplay of factors that mediate the relationship between Fintech services and financial inclusion.

The conceptual framework thus provides a structured lens for examining how credit, savings, and transactional Fintech services influence financial inclusion outcomes in Zambia. By integrating technology adoption, financial intermediation, and behavioural finance perspectives, it captures the multi-dimensional nature of digital financial ecosystems and the socio-economic and institutional factors that shape user behaviour. This framework guides the operationalization of variables in empirical research, where Fintech services are treated as independent variables, financial inclusion as the dependent variable, and digital literacy, trust, socio-economic status, and regulatory environment as moderating variables. Such a framework ensures that analyses account for both the technological potential and the contextual realities affecting adoption, usage, and impact, offering a comprehensive approach for evaluating the effectiveness of Fintech interventions in promoting financial inclusion within Zambia.

4. Methodology

This study investigates the impact of Fintech services on financial inclusion in Zambia. To achieve a comprehensive understanding of this phenomenon, a mixed-methods research design was employed, integrating both quantitative and qualitative approaches. The combination of these methods allowed the researcher to quantify trends and usage patterns while exploring the experiences, perceptions, and challenges faced by Fintech users, service providers, and regulatory authorities. This integrated approach enhances the validity and depth of the study by triangulating numerical data with contextual insights (Creswell & Creswell, 2017; Johnson & Onwuegbuzie, 2004).

The research site was Lusaka District, Zambia’s capital and primary economic hub, selected due to its high concentration of Fintech users, service providers, and regulatory bodies. Lusaka’s rapid urbanization, mobile and internet penetration, and the presence of headquarters for major Fintech stakeholders, including commercial banks, Fintech companies, the Bank of Zambia (BoZ), and the Zambia Information and Communications Technology Authority (ZICTA), provided an ideal environment for this study. The urban setting also allowed the research to capture financial inclusion dynamics across diverse demographics and economic activities.

The study population consisted of three primary groups: adult Fintech users (aged 18 and above), financial service providers (Fintech companies and traditional banks offering digital financial services), and regulatory authorities (BoZ, ZICTA, and the Ministry of Finance). According to the Bank of Zambia (2020), approximately 4.5 million Zambians actively use mobile money services, with Lusaka accounting for about 40% of this user base. This equates to roughly 1.8 million users, with 1.3 million adults forming the target population. Financial service providers included 10 Fintech companies and 7 commercial banks in Lusaka offering digital financial services, while regulatory authorities were represented by officials involved in Fintech policy formulation, oversight, and regulation (ZICTA, 2019).

A multi-stage sampling approach was used to ensure representativeness and depth. Stratified random sampling was applied to select 400 Fintech users, ensuring proportional representation based on demographic factors and the type of Fintech service used (mobile money, digital loans, or mobile banking). Purposive sampling was employed to select 30 representatives from Fintech service providers and 12 officials from regulatory bodies, targeting individuals with expertise relevant to Fintech operations and financial inclusion strategies (Palinkas et al., 2015; Etikan, Musa, & Alkassim, 2016). This multi-stage strategy ensured both breadth across user experiences and depth in expert insights.

Data collection involved both quantitative and qualitative methods. Self-administered questionnaires were distributed to Fintech users to gather numerical data on usage patterns, demographic information, and financial inclusion indicators such as access to credit, savings, and transaction services. Closed-ended questions on a Likert scale (strongly disagree to strongly agree) were used to quantify perceptions of accessibility, affordability, reliability, and user satisfaction. Structured interviews were conducted with service providers and regulatory officials to obtain qualitative insights into operational challenges, policy environments, and strategies for promoting financial inclusion (Creswell, 2014; Kvale & Brinkmann, 2015).

Prior to full deployment, the instruments were pilot-tested with a small subset of participants to assess clarity, reliability, and validity, with adjustments made based on feedback (Bryman, 2016). Data collection occurred over three months, following a structured timeline: a preparation phase for instrument finalization and ethical approval, a data collection phase for administering questionnaires, and an interview phase for conducting structured interviews. A post-collection review was undertaken to ensure completeness and consistency of the dataset.

Quantitative data analysis was conducted using the Statistical Package for the Social Sciences (SPSS). Descriptive statistics (frequencies, means, and standard deviations) summarized respondents’ demographic characteristics and Fintech usage, while inferential analyses, including correlation and regression, examined relationships between Fintech usage and financial inclusion outcomes. Cross-tabulations and Chi-square tests assessed differences across demographic groups (Field, 2018; Pallant, 2020). Qualitative data from interviews were transcribed verbatim and subjected to thematic analysis. Coding was performed to identify recurring themes and patterns relating to opportunities, barriers, and user experiences with Fintech services. Themes were analyzed to interpret stakeholder perspectives on Fintech adoption and its role in enhancing financial inclusion, providing contextual understanding that complemented the quantitative findings (Braun & Clarke, 2006; Miles, Huberman, & Saldana, 2014). Integration of quantitative and qualitative results allowed a comprehensive understanding of both measurable trends and experiential insights.

Validity and reliability were ensured through expert reviews of instruments, alignment with established frameworks such as FinScope surveys, and pilot testing. Statistical reliability was verified using Cronbach’s alpha, targeting a value of 0.7 or above to indicate acceptable internal consistency (Bryman, 2016). Inter-rater reliability for qualitative coding was maintained by having multiple researchers independently review and code data. Ethical considerations were rigorously observed. Informed consent was obtained from all participants, emphasizing voluntary participation and the right to withdraw without repercussions (Resnik, 2020). Confidentiality and anonymity were ensured through data anonymization, secure storage, and restricted access. Non-maleficence was observed by designing sensitive questions to avoid psychological discomfort, and participants were provided with support resources if needed. The study received ethical clearance from the University of Zambia Research Ethics Committee, guaranteeing compliance with institutional and national research standards (Flick, 2018; Walliman, 2017).

This integrated methodology, combining stratified random and purposive sampling, quantitative and qualitative data collection, and rigorous analysis, provided a robust framework to assess the impact of Fintech services on financial inclusion in Lusaka, Zambia, ensuring both reliability and depth of insight.

5. Findings/Results

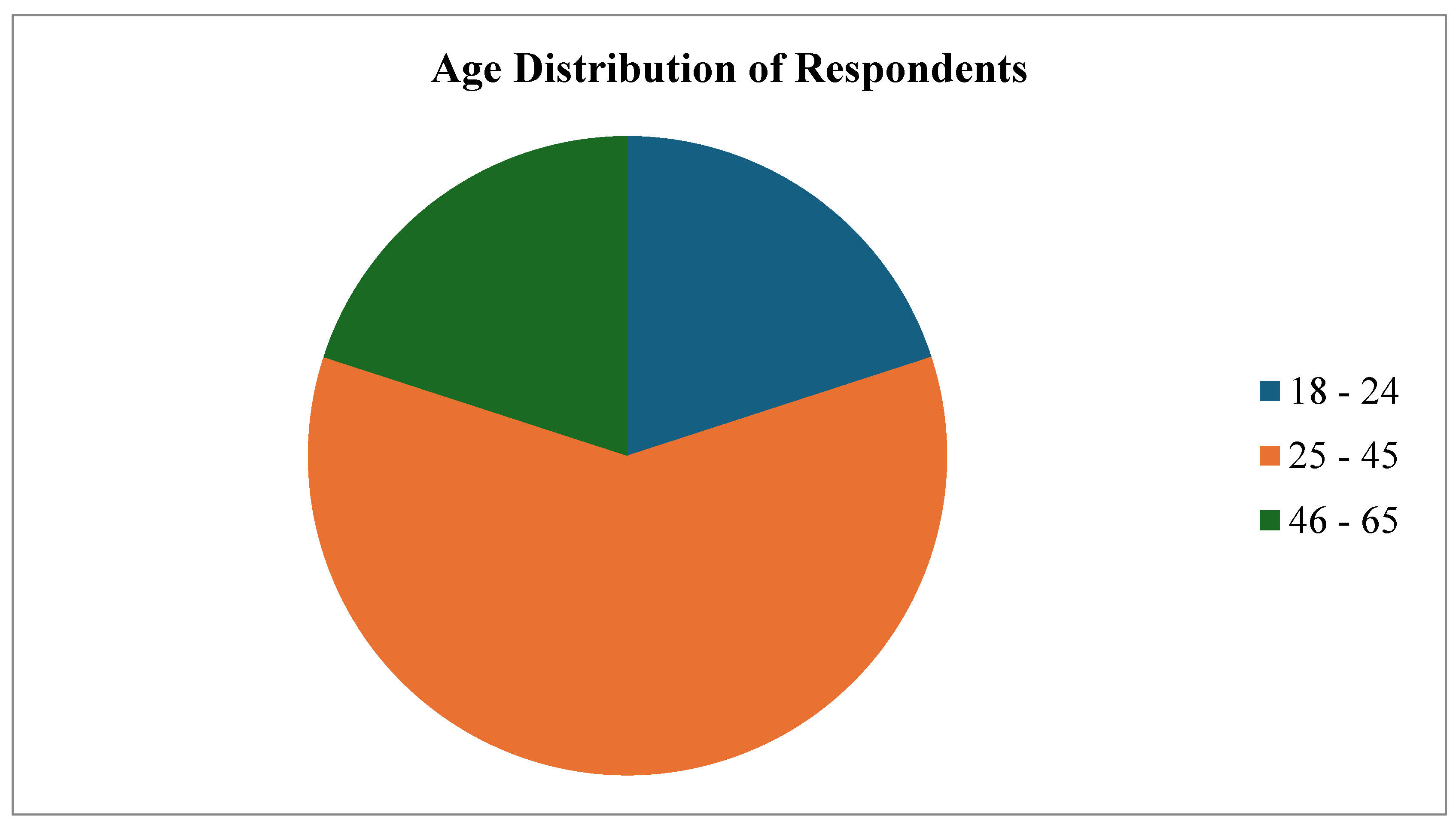

The findings of this study provide a comprehensive understanding of the impact of FinTech services on financial inclusion in Zambia, drawing upon the perspectives of 400 FinTech users, 30 service providers, and 12 regulatory officials. The respondents represented a diverse range of demographic characteristics, which are crucial in explaining the patterns of FinTech adoption and utilization across the country. Age was a significant factor, with 60% of respondents falling within the 25–45 age bracket, representing the most active group of technology adopters. The younger age group, 18–24 years, accounted for 20% of respondents and demonstrated a propensity to experiment with mobile-based financial services, leveraging their higher digital literacy and familiarity with smartphones. The remaining 20% of respondents, aged 46–65 years, engaged cautiously with FinTech platforms, reflecting the generational differences that influence both the frequency and confidence of usage. This distribution underscores the need for FinTech providers to design services that are accessible and user-friendly across age groups, particularly to enhance adoption among older populations who may face technological barriers.

Table 1.

Age Distribution of Respondents.

| Age Group | Percentage (%) | Description |

|---|---|---|

| 18–24 years | 20% | Younger, tech-savvy users; early adopters |

| 25–45 years | 60% | Most active group; majority of fintech users |

| 46–65 years | 20% | Cautious adopters; growing engagement |

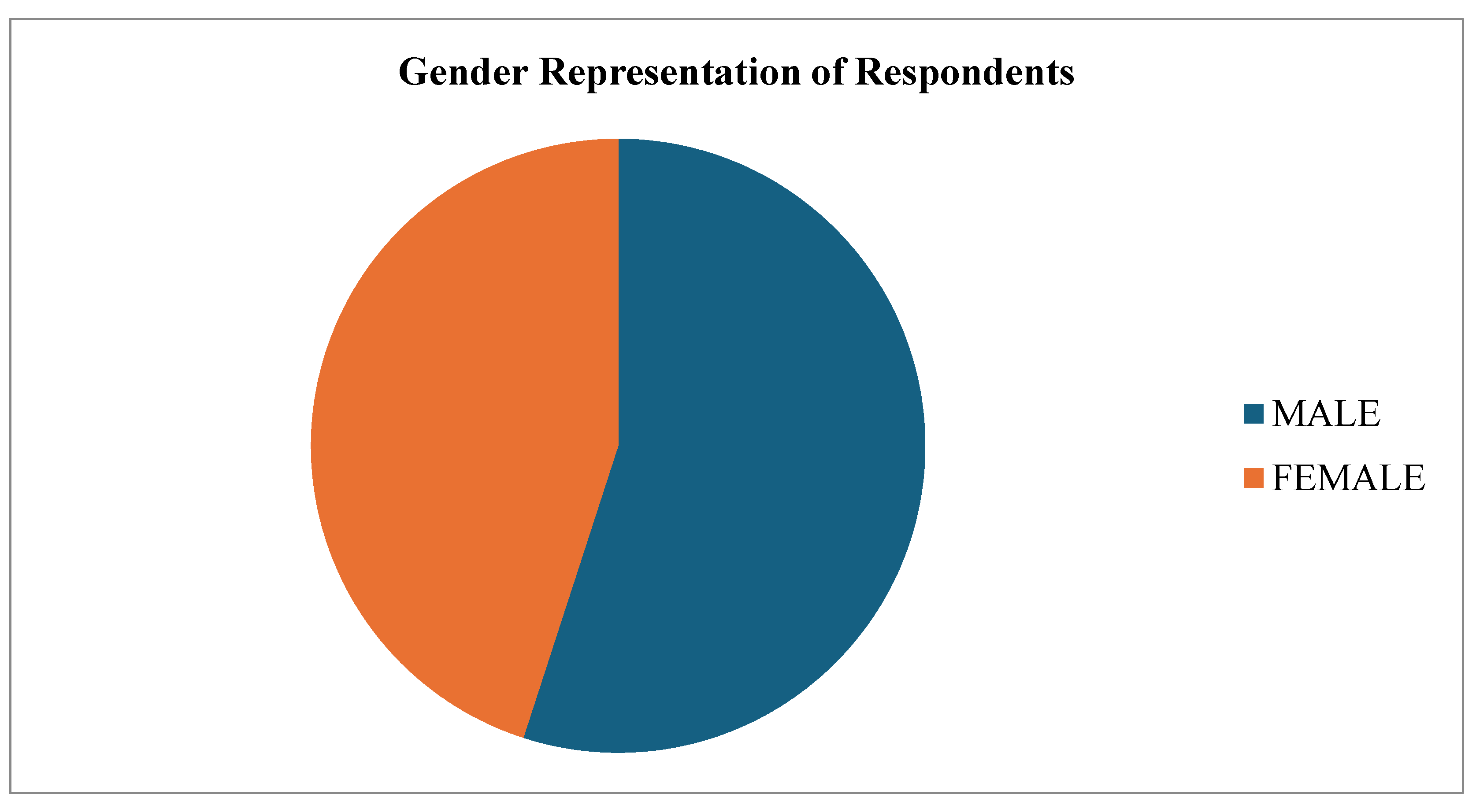

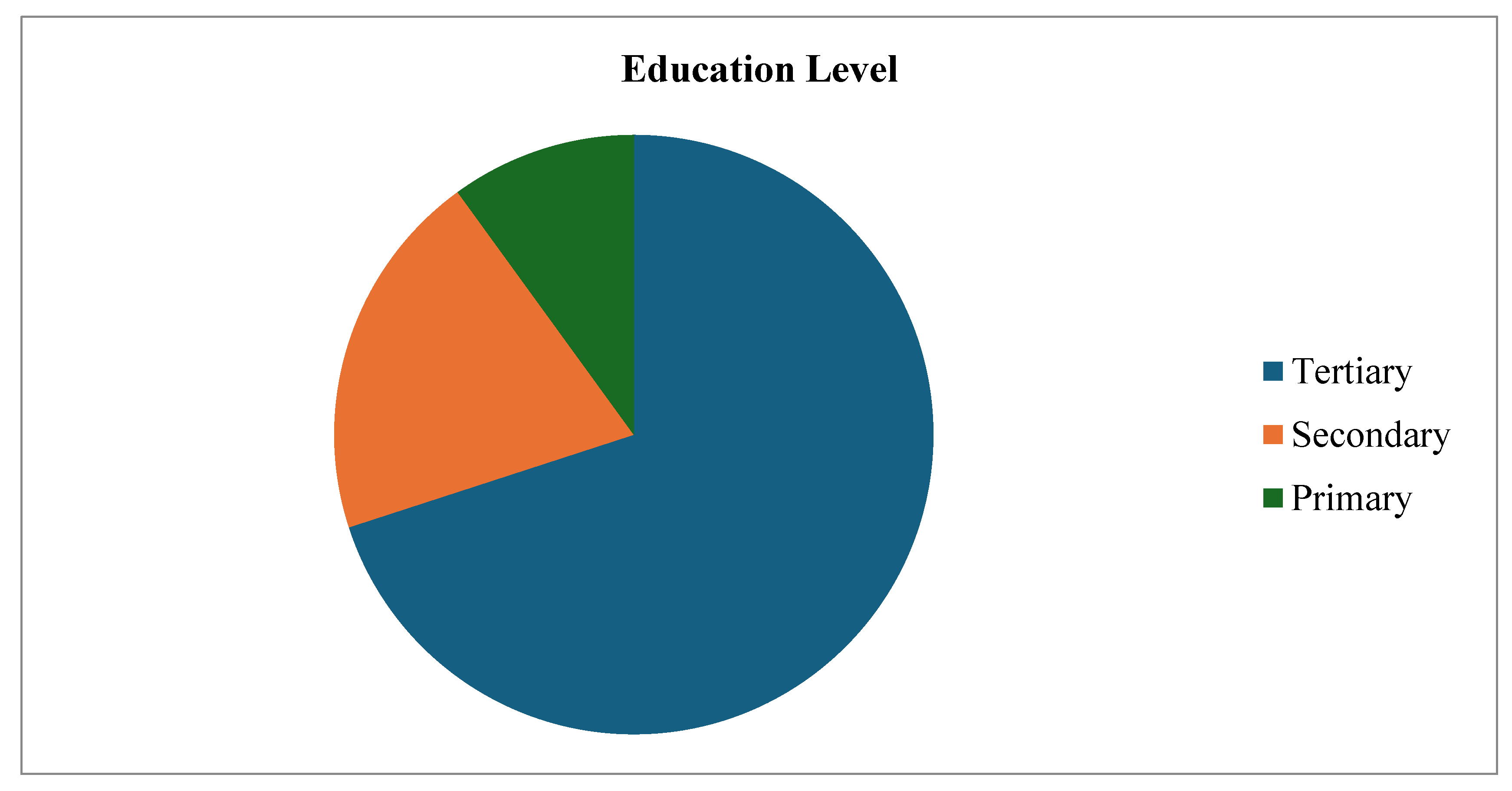

Gender distribution was relatively balanced, with males constituting 55% and females 45% of the sample. While men tended to adopt FinTech services slightly more, the near parity indicates that women in Zambia are increasingly accessing mobile money and digital financial services, gaining financial autonomy and greater control over household economic decisions. However, gendered disparities persist, particularly in rural areas where socio-cultural norms, limited access to mobile devices, and gaps in digital literacy hinder women’s engagement. These insights suggest that FinTech interventions need to adopt gender-sensitive approaches to ensure equitable access and inclusion. Education level emerged as another critical determinant of FinTech adoption. Approximately 70% of respondents had attained tertiary education, while 20% had completed secondary education and only 10% had primary or lower levels of education. Higher education was strongly correlated with greater digital literacy, awareness of financial products, and confidence in engaging with FinTech platforms, whereas lower educational attainment was associated with limited understanding, lower usage rates, and higher susceptibility to mistrust or misuse of services. This highlights the importance of targeted financial literacy initiatives to bridge knowledge gaps and foster inclusive adoption.

Table 2.

Gender Distribution.

| Gender | Percentage (%) | Observations |

|---|---|---|

| Male | 55% | Higher participation among men |

| Female | 45% | Increasing adoption by women |

Table 3.

Education Levels.

| Education Level | Percentage (%) | Notes |

|---|---|---|

| Tertiary | 70% | High correlation with fintech adoption |

| Secondary | | 20% | Moderate digital literacy |

| Primary or lower | 10% | Significant gap in adoption |

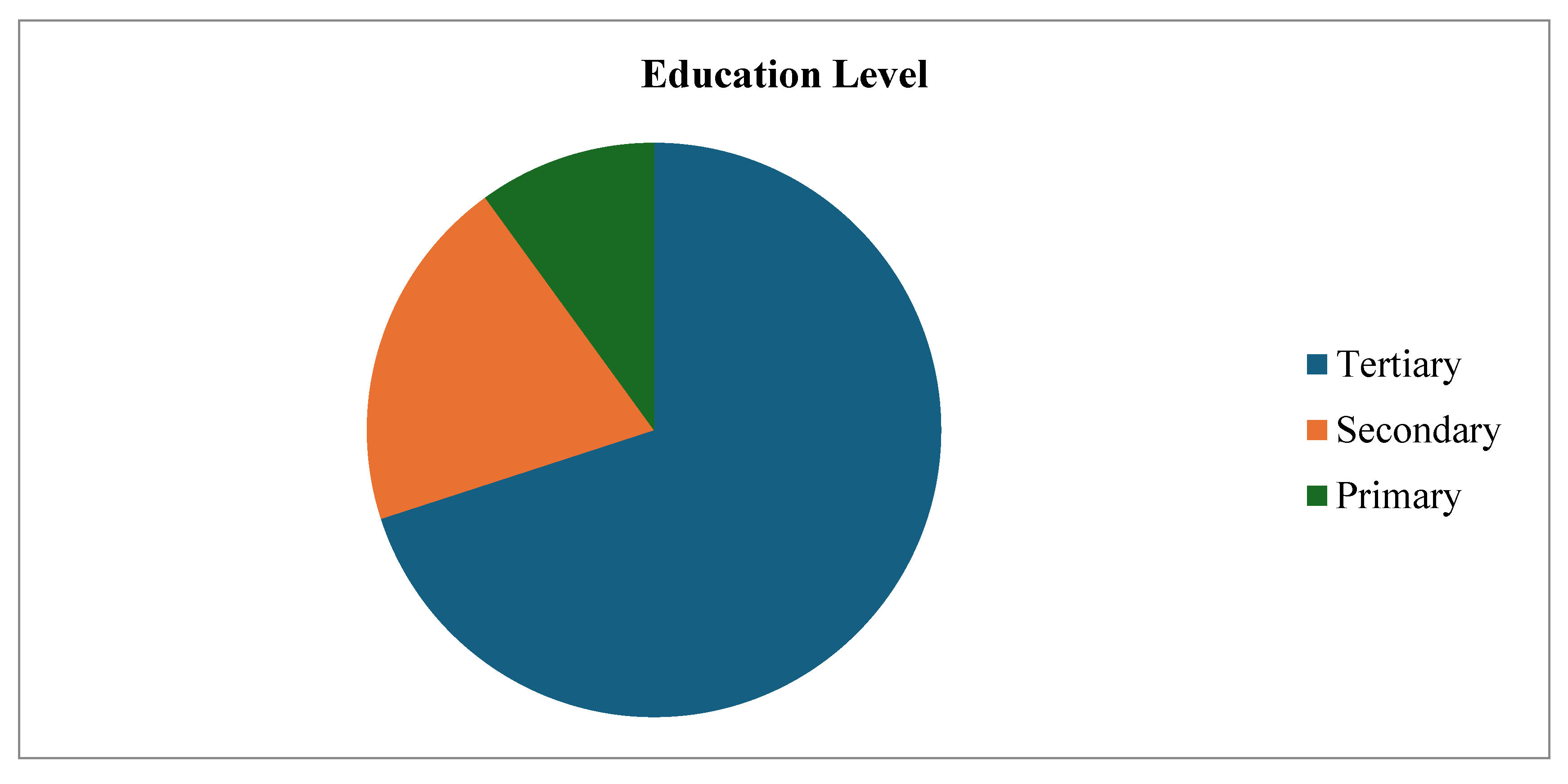

Employment status further shaped respondents’ engagement with FinTech services. Half of the respondents were formally employed, using FinTech primarily for salary management, savings, and investment purposes. The informal sector, comprising 30% of respondents, relied heavily on mobile money and digital lending platforms to support daily operations and microenterprise activities, reflecting the critical role of FinTech in reaching populations outside traditional banking systems. The remaining 20% of respondents, including students and unemployed individuals, highlighted the potential for FinTech to provide accessible financial solutions to economically vulnerable groups. These demographic patterns suggest that while FinTech adoption is growing, it remains unevenly distributed across economic sectors, necessitating inclusive service delivery strategies to reach all segments of society.

Table 4.

Education Levels.

| Education Level | Percentage (%) | Notes |

|---|---|---|

| Tertiary | 70% | High correlation with fintech adoption |

| Secondary | | 20% | Moderate digital literacy |

| Primary or lower | 10% | Significant gap in adoption |

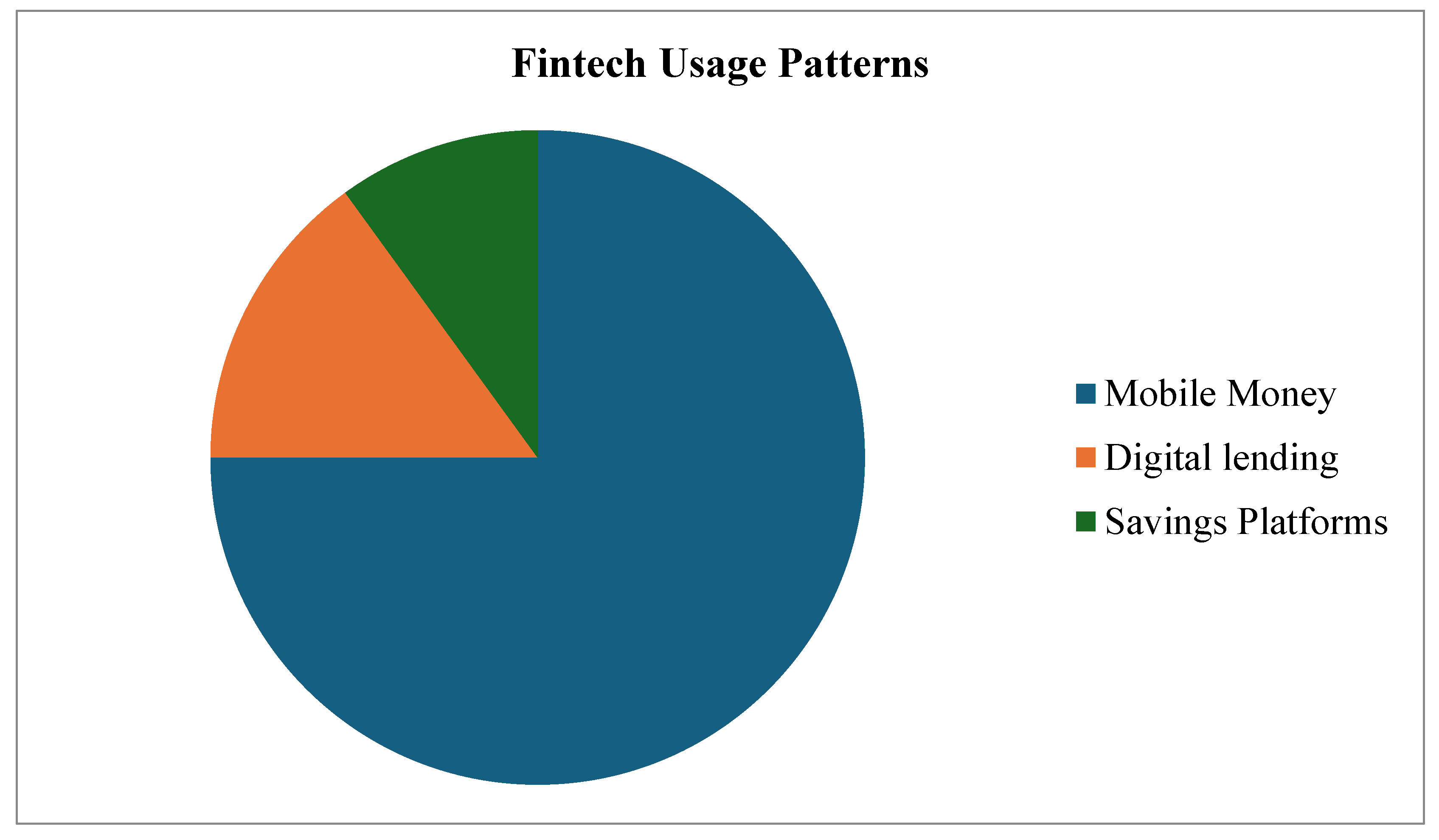

Analysis of FinTech usage patterns revealed that mobile money platforms dominated financial activity, with 75% of respondents actively utilizing services such as MTN Mobile Money and Airtel Money for transfers, bill payments, and savings. Digital lending platforms were accessed by 15% of users, primarily for microloans to support small businesses or personal emergencies, while 10% engaged with digital savings products. The duration of usage further indicated growing trust and reliance on FinTech services, with 40% of respondents reporting over three years of continuous engagement, 35% between one and three years, and 25% less than one year. This longevity suggests that FinTech has not only enhanced access to financial services but has also fostered habitual usage, although concerns about over-indebtedness and responsible borrowing remain relevant, particularly among frequent users of digital loans.

Table 5.

Fintech Usage Patterns.

| Fintech Service | Percentage (%) | Description |

|---|---|---|

| Mobile Money | 75% | Widely used for transactions and savings |

| Digital Lending | 15% | Popular for accessing microloans |

| Savings Platforms | 10% | Used for financial management tools |

Credit FinTech services were identified as critical in bridging gaps left by traditional banking, with 70% of respondents reporting access to short-term loans via platforms such as Branch and ZamCash. These services were particularly valued by informal sector workers who face collateral requirements and rigid lending criteria in conventional banks. Respondents emphasized the convenience of mobile applications, the speed of loan disbursement—often within 24 hours—and the ease of managing repayments digitally. Despite these advantages, approximately 20% of users raised concerns regarding limited loan sizes and unclear repayment terms, which sometimes led to multiple concurrent loans and over-indebtedness. These findings highlight the dual nature of digital lending: while it expands access to credit, it also necessitates strong user education, transparency, and regulatory oversight to mitigate financial risk.

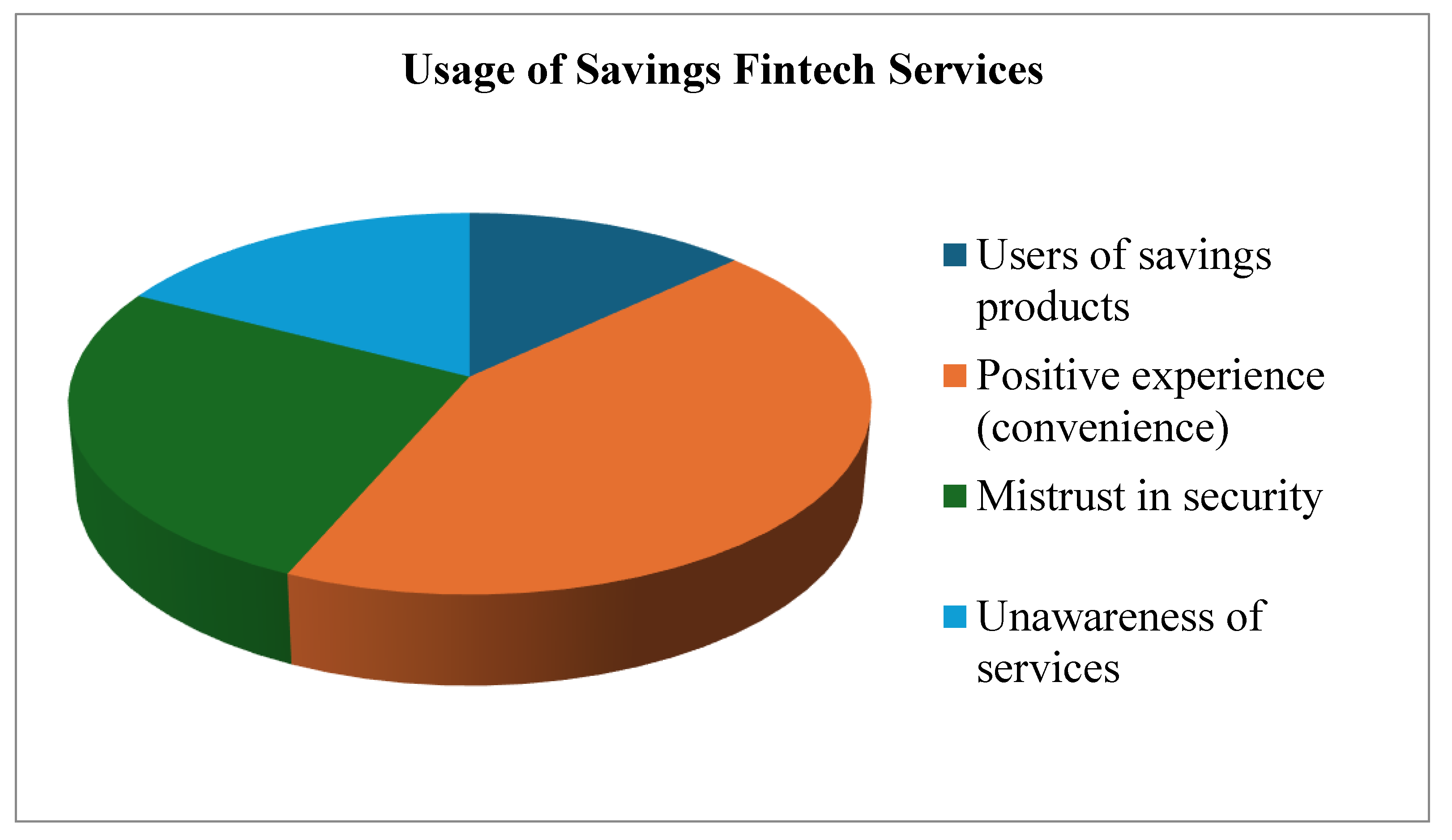

Savings services, in contrast, showed lower levels of adoption, with only 15% of respondents actively engaging. Among these users, 50% utilized digital savings platforms for short-term goals, such as emergency funds or school fees. However, mistrust regarding the security of funds affected 30% of respondents, while 20% were unaware of the existence of such services, reflecting significant gaps in awareness and confidence. These findings underscore the need for FinTech providers to implement robust cybersecurity measures and for policymakers to promote financial literacy campaigns that enhance trust, understanding, and engagement with digital savings products. Expanding the adoption of savings services is essential for building financial resilience and long-term inclusion.

Table 6.

Usage of Savings Fintech Services.

| Aspect | Percentage (%) | Observations |

|---|---|---|

| Users of savings products | 15% | Limited adoption due to low awareness and trust issues. |

| Positive experience (convenience) | 50% | Users found mobile-based accounts useful for short-term goals |

| Mistrust in security | 30% | Concerns about cybersecurity and fraud. |

| Unawareness of services | 20% | Highlighted need for awareness campaigns and education |

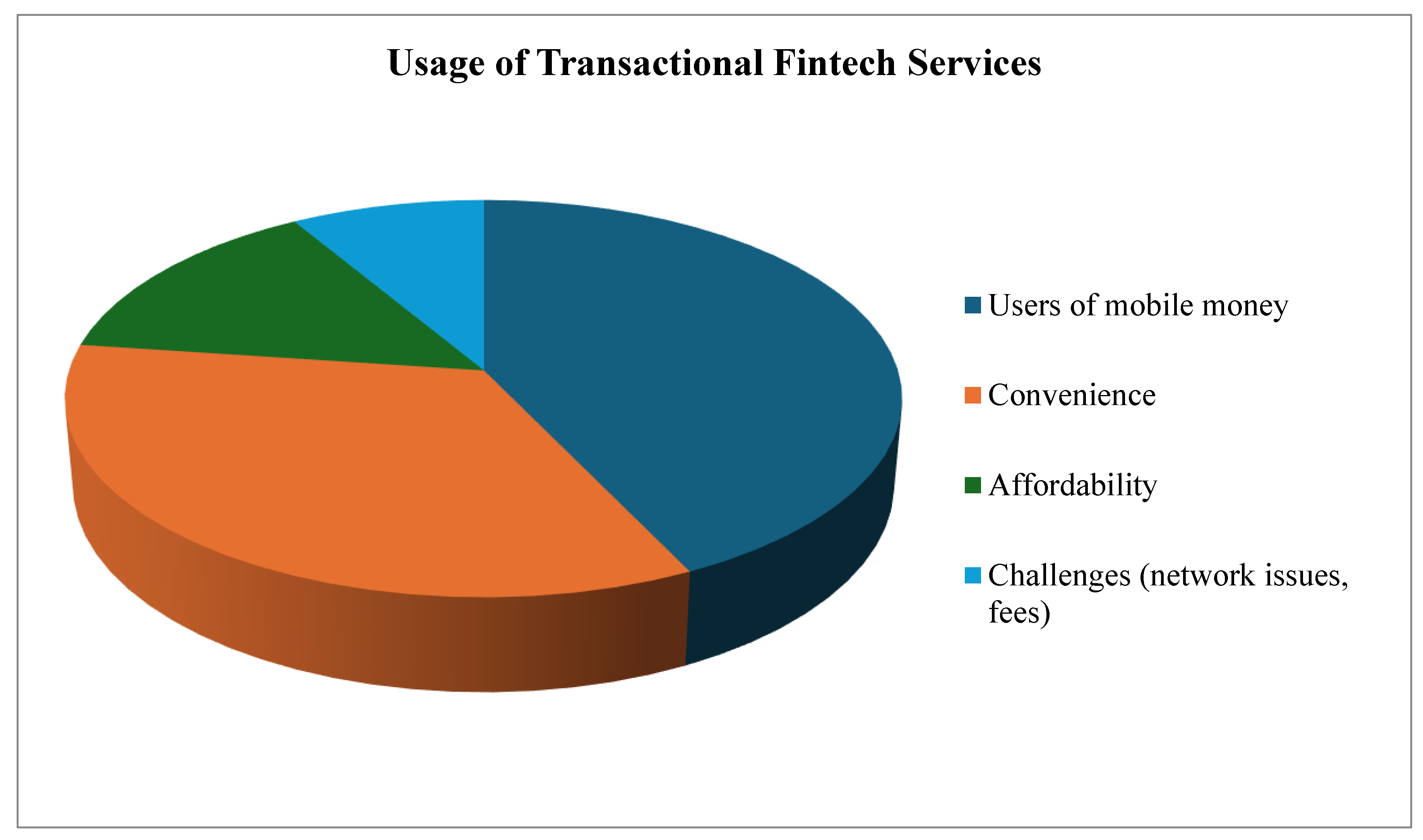

Transactional services, particularly mobile money, have had a transformative impact on financial inclusion, with 75% of respondents actively using these platforms for daily transactions. Convenience and accessibility were repeatedly cited, with 60% highlighting the ability to conduct transactions without visiting a bank branch, and 25% noting lower costs compared to traditional banking or informal money transfer methods. Nonetheless, 15% of users reported challenges such as network disruptions and high transaction fees, particularly for cash withdrawals, suggesting that infrastructure improvements and cost management are essential to sustaining growth and expanding reach, especially in rural and underserved areas.

Table 7.

Usage of Transactional Fintech Services.

| Aspect | Percentage (%) | Observations |

|---|---|---|

| Users of mobile money | 75% | Most widely used fintech service for transactions. |

| Convenience | 60% | Ability to transact anywhere, benefiting rural users. |

| Affordability | 25% | Lower costs than traditional banking. |

| Challenges (network issues, fees) | 15% | Frequent disruptions and high transaction fees. |

Overall, the findings reveal that FinTech services have significantly enhanced financial inclusion in Zambia, particularly for younger, educated, and urban populations. However, adoption remains uneven, with older, less-educated, and rural users less likely to engage due to limited literacy, awareness, and technological access. Persistent challenges such as mistrust, limited financial literacy, affordability, and network reliability highlight the need for multi-faceted interventions. Addressing these gaps through targeted education, robust cybersecurity, gender-sensitive approaches, and inclusive infrastructure can strengthen the impact of FinTech, ensuring that it reaches diverse demographic groups and contributes to sustainable economic empowerment across Zambia. These insights provide a holistic understanding of the current state of digital financial services and identify critical areas where policy, education, and service delivery can work synergistically to maximize the benefits of financial inclusion.

6. Discussion

The findings of this study demonstrate that FinTech services are a significant driver of financial inclusion in Zambia, particularly for populations historically excluded from formal banking systems. The study shows that mobile money platforms are the most widely adopted digital financial services, used by approximately 75% of respondents, largely due to their convenience, accessibility, and ability to facilitate financial transactions without the need for traditional bank infrastructure. These findings align with prior research indicating that mobile money has transformed financial behavior across sub-Saharan Africa, enabling individuals to access secure and affordable transactional services regardless of geographic location (Jack & Suri, 2014). The high adoption rates among younger and urban respondents suggest that digital literacy and access to mobile devices are crucial determinants of FinTech adoption, supporting existing evidence that age, education, and urbanization are positively correlated with financial inclusion (Demirgüç-Kunt et al., 2018).

Digital credit services emerged as another critical component of financial inclusion. The study found that 70% of respondents have accessed short-term loans through digital lending platforms, primarily to support small-scale businesses or meet urgent personal financial needs. This finding mirrors evidence from other African contexts where digital lending has bridged gaps for populations lacking collateral or formal credit histories, often using alternative data sources and mobile-based credit scoring (Mbiti & Weil, 2016). Despite the accessibility benefits, respondents reported challenges including limited loan sizes, unclear repayment terms, and multiple concurrent loans, highlighting the risk of over-indebtedness. Similar concerns have been raised in the literature, emphasizing the importance of regulatory oversight and consumer protection to ensure responsible lending and sustainable financial inclusion outcomes (Cull et al., 2018).

Savings-oriented FinTech services, although less widely adopted, are increasingly recognized for their potential to improve financial resilience. In this study, only 15% of respondents actively used digital savings products, largely due to limited awareness, mistrust of platform security, and low financial literacy. These barriers are consistent with broader African research, which indicates that while mobile-based savings can encourage better financial planning and mitigate vulnerability to financial shocks, adoption is heavily influenced by trust, familiarity with technology, and perceived reliability (FSD Africa, 2020). Furthermore, the study reveals that older and less-educated individuals are disproportionately underrepresented among users of digital savings services, suggesting that targeted educational initiatives and user-friendly interfaces are needed to expand uptake and reduce disparities in financial inclusion (Klapper et al., 2016).

Transactional services, particularly mobile money platforms, were found to have the most immediate and widespread impact on financial inclusion. Respondents highlighted convenience, affordability, and the ability to conduct financial transactions without physically visiting bank branches as key drivers of adoption. These findings are consistent with studies demonstrating that mobile money enables broader participation in the financial system by reducing transaction costs and improving access for both rural and low-income populations (Suri & Jack, 2016). However, challenges remain, including network disruptions, occasional high transaction fees, and limited agent coverage, which constrain seamless access to these services. Addressing these infrastructural and systemic barriers is critical for maximizing the benefits of mobile-based transactional services and ensuring equitable financial inclusion across all demographic groups (Mbiti & Weil, 2016).

Demographic characteristics play a significant role in shaping the adoption and utilization of FinTech services. The study highlights that younger, urban, and highly educated respondents are more likely to adopt digital financial services, whereas older, rural, and less-educated individuals face barriers that limit their engagement. This pattern reinforces existing research suggesting that digital and financial literacy, combined with access to technology, are key determinants of financial inclusion (Demirgüç-Kunt et al., 2018). Gender also emerged as an important factor. While the study achieved a relatively balanced representation of men and women, women continue to face socio-economic and cultural barriers that affect access to and use of digital financial services. Evidence from multiple African countries suggests that targeted interventions, such as digital literacy programs and inclusive product design, are necessary to reduce gender gaps and ensure that women fully benefit from FinTech adoption (GSMA, 2020).

Overall, the findings of this study underscore that FinTech services have substantial potential to enhance financial inclusion in Zambia, particularly through mobile money and digital credit platforms. Nevertheless, challenges persist, including uneven adoption across demographic groups, insufficient awareness and trust in savings products, infrastructural constraints, and the risk of over-indebtedness. To maximize the impact of FinTech on financial inclusion, stakeholders—including service providers, policymakers, and regulators—must address these barriers by promoting financial literacy, ensuring consumer protection, expanding digital infrastructure, and tailoring services to meet the diverse needs of all Zambian populations. If effectively managed, FinTech has the potential to transform Zambia’s financial landscape by reducing inequalities, increasing access to essential financial services, and fostering economic empowerment.

7. Conclusion

The findings of this study clearly demonstrate that FinTech services have significantly contributed to advancing financial inclusion in Zambia, albeit with varying degrees of impact across different demographic groups, service types, and regions. Mobile money platforms have emerged as the most widely adopted FinTech service, driven by their convenience, affordability, and ability to facilitate transactions for populations previously excluded from formal banking systems. Credit-oriented FinTech services have provided crucial access to short-term loans for small businesses and informal sector workers, addressing financing gaps that traditional banks have historically been unable or unwilling to fill. However, challenges such as limited loan sizes, unclear repayment terms, and risks of over-indebtedness highlight the necessity of regulatory oversight and user education to ensure that the benefits of digital credit are sustainable and inclusive.

Savings FinTech services, while offering potential for financial resilience and long-term planning, remain underutilized due to mistrust, low awareness, and limited digital literacy, particularly among older and less-educated users. Transactional FinTech services, particularly mobile money, have reshaped the financial landscape by enabling secure, timely, and cost-effective transactions, particularly for rural and low-income populations. Nonetheless, issues such as network disruptions and transaction fees indicate that infrastructural and operational challenges continue to limit the full potential of these services.

Demographic factors, including age, education, gender, and employment status, were found to strongly influence FinTech adoption and usage patterns. Younger, educated, and urban respondents were more likely to embrace digital financial services, while older, less-educated, and rural individuals demonstrated cautious engagement. Gender disparities, although narrower in urban contexts, persist in rural areas, reflecting socio-cultural and economic barriers that must be addressed to achieve equitable inclusion.

In summary, the study underscores the transformative potential of FinTech in promoting financial inclusion in Zambia, while simultaneously highlighting critical gaps that require attention. Achieving sustainable and equitable financial inclusion will necessitate coordinated efforts by FinTech providers, policymakers, regulators, and community stakeholders to improve awareness, enhance security, expand accessibility, and strengthen infrastructure. By addressing these gaps, FinTech can empower a broader cross-section of the population, fostering economic participation, resilience, and growth, and contributing meaningfully to Zambia’s financial and socio-economic development.

References

- Aker, J. C., & Mbiti, I. M. (2010). Mobile phones and economic development in Africa. Journal of Economic Perspectives, 24(3), 207–232. [CrossRef]

- Allen, F., Demirgüç-Kunt, A., & Peria, M. S. M. (2012). The foundations of financial inclusion: Understanding ownership and use of formal accounts. World Bank Policy Research Working Paper 6290. Washington, DC: World Bank.

- Allen, F., Demirgüç-Kunt, A., Klapper, L., & Martinez Peria, M. S. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of Financial Intermediation, 27, 1–30.

- Aron, J. (2018). Mobile money and the economy: A review of the evidence. The World Bank Research Observer, 33(2), 135–188.

- Bahia, K., Kinyanjui, M., & Smith, L. (2022). Digital credit in Africa: Access and consumer protection. Development Policy Review, 40(4), 567–586.

- Bank of Zambia. (2019). Annual report on financial sector performance and FinTech regulation. Lusaka: Bank of Zambia.

- Bank of Zambia. (2020). Financial Sector Development Plan. Bank of Zambia.

- Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77–101.

- CGAP. (2017). Consumer protection in digital financial services. Washington, DC: Consultative Group to Assist the Poor.

- CGAP. (2018). Digital credit: Consumer protection for inclusive financial services. Washington, DC: Consultative Group to Assist the Poor.

- Chen, G., & Mazer, R. (2016). Digital finance and financial inclusion: Impacts and policy implications. Journal of Development Studies, 52(5), 677–689.

- Cull, R., Ehrbeck, T., & Holle, N. (2018). Financial inclusion and development: Recent impact evidence. CGAP Working Paper. Washington, DC: Consultative Group to Assist the Poor.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340.

- Demirgüç-Kunt, A., Beck, T., & Honohan, P. (2008). Finance for all? Policies and pitfalls in expanding access. World Bank Policy Research Report. Washington, DC: World Bank.

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring financial inclusion and the fintech revolution. Washington, DC: World Bank.

- Diamond, D. W. (1984). Financial intermediation and delegated monitoring. The Review of Economic Studies, 51(3), 393–414.

- Frost, J. (2020). FinTech and financial inclusion in Latin America. Journal of Financial Innovation, 6(2), 123–147.

- FSD Africa. (2020). The state of digital financial services in Africa. Nairobi: Financial Sector Deepening Africa.

- GSMA. (2020). Women and mobile money: Bridging the gender gap. London: GSM Association.

- Jack, W., & Suri, T. (2014). Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. American Economic Review, 104(1), 183–223.

- Kaffenberger, M., & Totolo, E. (2018). The impact of digital credit on consumer well-being. CGAP Working Paper.

- Karlan, D., Ratan, A. L., & Zinman, J. (2016). Savings by and for the poor: A research review and agenda. Review of Income and Wealth, 62(1), 1–40.

- Klapper, L., & Singer, D. (2014). The opportunities of fintech for financial inclusion. World Bank Policy Research Working Paper 7071. Washington, DC: World Bank.

- Klapper, L., Lusardi, A., & Van Oudheusden, P. (2016). Financial literacy around the world. World Bank Policy Research Working Paper 8046. Washington, DC: World Bank.

- Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30, 607–610.

- Kshetri, N. (2020). FinTech, big data and the future of financial inclusion. Information Systems Journal, 30(4), 624–641.

- Mbiti, I., & Weil, D. N. (2016). Mobile banking: The impact of M-Pesa in Kenya. NBER Working Paper No. 17129. Cambridge, MA: National Bureau of Economic Research.

- Merriam, S., & Tisdell, E. (2016). Qualitative research: A guide to design and implementation (4th ed.). Jossey-Bass.

- Muijs, D. (2011). Doing quantitative research in education with SPSS. Sage.

- NFIS (National Financial Inclusion Strategy). (2017). Zambia National Financial Inclusion Strategy 2017–2022.

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329–340.

- Ozili, P. K. (2020). Financial inclusion in Africa: An overview. Journal of African Business, 21(1), 1–22.

- Ozili, P. K. (2021). FinTech, financial inclusion and digital banking: A review. Borsa Istanbul Review, 21(1), 1–15.

- Phiri, T., & Zulu, M. (2022). Fintech adoption in Zambia: Patterns and policy implications. Zambia Economic Journal, 9(1), 45–69.

- Rogers, E. M. (2003). Diffusion of innovations (5th ed.). Free Press.

- Sarma, M., & Pais, J. (2011). Financial inclusion and development. Journal of International Development, 23(5), 613–628.

- Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288–1292.

- Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288–1292.

- Tashakkori, A., & Teddlie, C. (2010). Sage handbook of mixed methods in social & behavioral research (2nd ed.). Sage.

- World Bank. (2014). Global financial development report 2014: Financial inclusion. Washington, DC: World Bank.

- World Bank. (2022). Global financial inclusion report. Washington, DC: World Bank.

- Zambia Statistics Agency (ZamStats). (2020). Household survey on access to financial services. Lusaka: ZamStats.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.