Submitted:

04 February 2026

Posted:

06 February 2026

You are already at the latest version

Abstract

This study presents a bibliometric analysis of behavioral finance and investment decision-making research published between 2015 and 2025. We used VOSviewer and bibliometrix in R to apply science mapping techniques and performance indicators to 3,110 Scopus-indexed articles from Q1 and Q2 journals. The findings indicate that behavioral biases, financial crises, fintech, cryptocurrencies, and sustainable finance are the main areas of research. Strong cooperation between Asia, Europe, and North America is demonstrated by international co-authorship networks. The results demonstrate how traditional behavioral theories have come together as well as how new topics like digital assets, ESG investing, and pandemic-driven financial behavior are becoming more prevalent. This mapping indicates understudied areas for further research and provides an organized summary of the field's development.

Keywords:

behavioral finance

; investment decision-making

; bibliometric analysis

; Scopus

1. Introduction

The traditional paradigms of rationality that form the idea of conventional finance theories are being challenged through behavioral finance, which has ended up as one of the most active fields of financial research. According to behavioral finance, the limitations of the mind, mental biases, and emotional factors, to put it simply, are the main causes of the investors’ behavior (Kahneman and Tversky, 1979; Barberis and Thaler, 2003). This is in disagreement with the efficient market hypothesis that claims that investors are rational and that markets fully reflect all the available information (Fama, 1970). Most of the subsequent theoretical framework ideas for the phenomena of asset pricing, portfolio allocation, and trading come from the first pieces of work like prospect theory (Kahneman and Tversky, 1979) and the paper on investor sentiment (De Long et al., 1990).

In overconfidence (Odean, 1998), herding (Bikhchandani and Sharma, 2001), mental accounting (Thaler, 1985), and the disposition effect (Shefrin and Statman, 1985) among which the biases have been found only those which influence the decision-making process of individual and institutional investors to a significant extent have been identified. Besides theoretical advancements, these findings have had an impact on practical debates about market efficiency, financial regulation, and portfolio management (Shiller, 2000; Statman, 2019).

Global crises and disruptive innovations have brought about a surge in interest in behavioral finance over the past ten years. While more recent shocks, just like the COVID-19 pandemic, sparked new waves of research into financial contagion, secure-haven assets, and investor psychology under uncertainty (Akhtaruzzaman et al., 2021; Conlon and McGee, 2020), the 2008 financial disaster brought to light the systemic implications of herding, risk misperception, and excessive optimism (Akerlof and Shiller, 2009; Lo, 2017). In parallel, the advent of fintech, artificial intelligence, and cryptocurrencies has expanded the scope of behavioral finance into domains such as digital trading platforms (Lo, 2017), algorithmic decision-making (Adam et al., 2020), and sustainable finance (Hartzmark and Sussman, 2019).

Because of this variety in the area of behavioral finance and investment decision-making research, we can use bibliometric methods such as co-citation, co-authors, and co-words to systematically portray how academics have developed the themes in this area over time; looking at these techniques will allow the researcher to discover where the major research areas are, the collaboration between various researchers, and any new thematic trends within this research domain (Aria & Cuccurullo, 2017; Donthu et al., 2021). Examples of bibliometric tools being used in conjunction with co-citation, co-authorship, and co-words include VOSviewer (van Eck & Waltman, 2010) and the Bibliometrix R package (Aria & Cuccurullo, 2017). These tools provide tremendous insight into what the academic foundations of the area are, popular research topics, and unexplored research areas, as seen in recent literature reviews that were undertaken for both management and finance research (Merigó & Yang, 2017; Gaviria-Marin et al., 2018).

Through the use of bibliometric mappings to explore the trajectory of behavioral finance and investment decision-making literature (the period of 2015-2025), this paper contributes to the literature. By examining and investigating the trajectory of behavioral finance over the period from 2015-2025, the study evaluates articles published, citation patterns, authors and institutions publishing the articles, and topic clusters identified within Q1 and Q2 journals contained in the Scopus database. By analyzing and assessing the performance (via bibliometric mapping) and network visualization techniques, the study offers an all-encompassing perspective of the dramatic shift in behavioral finance and investment decision-making literature as influenced by both crises, the impact of technology, and changes in socioeconomic environments.

The study is based on the overarching research question: “What are the relationships among the intellectual, social and conceptual foundations underlying behavioral finance and investment decision making, and how have they changed over the period 2015-2025?”

In order to tackle this, we develop the subsequent subquestions:

- How have citation impact and research volume in behavioral finance changed over time?

- What authors, institutions, and countries have the highest scholarly influence and productivity?

- What does the co-authorship network reveal about local and global institutional collaborations that lead to the field?

- What concepts and topics are most recognized in the literature?

- How did sustainability issues, technological advancements, and crises affect the way of research in recent times?

Besides providing a comprehensive mapping of the field, the study’s answers to these questions prepare the ground for a critical assessment of the field’s future directions.

2. Literature Review

Behavioral finance emerged as a signal of a dramatic change of the fork between the old and new theories of finance. It was a major blow to the assumptions of traditional finance that earlier theories, among them the efficient market hypothesis (EMH) (Fama, 1970), assumed that investors were rational and that asset prices reflected all available information, leaving a very small room for systematic mispricing. Nevertheless, an increasing number of anomalies, bubbles, and persistent inefficiencies have been observed to challenge these propositions. Prospect theory (Kahneman and Tversky, 1979) argues that people’s judgments deviate from those of expected utility theory because they are loss averse and at that same time, they consider reference points when evaluating outcomes. By showing the ways in which people use heuristics and are limited by their cognitive capacities thus leading to systematic biases, this theory eventually became the foundation of behavioral finance. An understanding of mental accounting, endowment effects, and bounded rationality (Thaler, 1985; Tversky and Kahneman, 1983) showed how social and psychological factors fundamentally influence financial behavior, offering a more comprehensive view of decision-making analysis than merely rational models.

Several behavioral biases that affect investment decisions have been found by subsequent empirical research. According to Odean (1998), investors often overestimate their knowledge and forecasting skills, which results in excessive trading and lower returns. Investors’ tendency to hold onto losing positions while selling winning stocks too soon was exposed by the disposition effect (Shefrin and Statman, 1985), which defies the rationale of portfolio optimization. Collective shifts in investor sentiment exacerbate volatility and fuel bubbles and crashes, as demonstrated by herding behavior (Bikhchandani and Sharma, 2001; Christie and Huang, 1995). The reasons why investors extrapolate trends or place an undue emphasis on salient but irrelevant information were further explained by other heuristics like representativeness and anchoring (Barberis and Thaler, 2003). Together, these contributions created an increasing body of evidence that investor psychology is a major factor in determining results and that markets are not totally efficient.

Mental accounting, endowment, and bounded rationality are all social and psychological factors that have a significant impact on financial decision-making and therefore create a more comprehensive view of financial analysis, rather than simply using rational decision-making models. To support this research, many behavioral biases which affect investments have now been documented through empirical studies since the original TRF (Thaler et al., 1985; Tversky and Kahneman, 1983) study.

According to Odean (1998), investors have a tendency to overrate their ability to predict future pricing trends and have therefore overtraded, resulting in lower returns. The disposition effect (Shefrin and Statman, 1985) shows that most investors are unable to sell stocks when they are at their highest value and keep them for the longer term, regardless of whether or not the stocks will perform well. The herding behavioral disruption describes how collective movement on the part of investors causes exaggerated volatility as well as creating bubbles and crashes in the marketplace, as noted in Bikhchandani and Sharma’s (2001) and Christie and Huang’s (1995) studies. Other heuristics like representativeness and anchoring have been identified, to explain the reason why investors use past trends as a reference for their future decisions, even though the past is not relevant to their current decision-making process (Barberis and Thaler, 2003). All of the above research provides overwhelming evidence that the psychology of investors plays a key role in determining market outcomes and therefore renders financial markets not entirely efficient.

Over the past two decades, behavioral finance has also been applied through the lenses of sustainability, technological innovation, and crisis. The global financial crisis of 2008 proved that systemic risk arises from cognitive errors and overconfidence (Akerlof and Shiller, 2009). The COVID-19 pandemic serves as an ideal scenario to analyze psychological impacts on investors in situations of extreme uncertainty. Research shows that the pandemic caused investors to become increasingly risk-averse, to experience contagion effects, and to pursue safe-haven investments (e.g., gold, cryptocurrencies) (Akhtaruzzaman et al., 2021; Conlon and McGee, 2020). Furthermore, with the rise of financial technology (fintech) and cryptocurrencies, there are now additional areas of inquiry available for behavioral researchers due to the volatility stemmed from the aforementioned crises. Studies have also been undertaken concerning algorithms used in algorithmic trading from Adaptive Market Perspectives, while numerous researchers have examined both the behavioral and speculative characteristics surrounding Bitcoin and other digital assets such as cryptocurrencies (Corbet et al., 2019). However, one of the most established areas of research is the intersection between social and psychological forces with sustainable investing or investment in assets designed to support environmental sustainability (Hartzmark and Susman, 2019). Therefore, it is clear that the field of behavioral finance has progressed beyond its initial focus on psychology and is now being used in multidisciplinary applications to study a broad range of contemporary global challenges.

Bibliometrics has been necessary for the organization of previously unreconciled sources into cohesive patterns, due to the fact that literature continues to grow exponentially. Using quantitative methods to create bibliometric maps (rather than narrative reviews), allows for the identification of intellectual patterns associated with authorships (their influence), networks of researchers working collaboratively, and emerging patterns within areas of study. R’s Bibliometrix Package (Aria and Cuccurullo, 2017) and VOSviewer (van Eck & Waltman, 2010) are some of the best tools available for creating science maps and visualizing networks, and they have both been utilized extensively in the fields of finance and management to create overviews (thematic evolution) of the intellectual foundations of disciplines. Both tools have also assisted in identifying early-stage research developments within those areas through recent bibliometric mapping studies (Gaviria-Marin et al., 2018; Khan et al., 2020; Merigó & Yang, 2017; Vo, 2021). The progress associated with utilizing those tools to develop bibliometric mapping techniques, though still somewhat limited in scope and primarily focused on specific geographic regions, represents a major shift in the literature of behavioral finance (Donthu et al., 2021).

Unfortunately, despite these advances and efforts to complete systematic and bibliometric reviews of behavioral finance, the current literature remains widely scattered and difficult to locate on a single topic. Without providing a comprehensive, worldwide view of the field’s development, many focus on specific biases, asset classes, or regional samples. Additionally, new fields like artificial intelligence, cryptocurrencies, pandemic-driven behavioral responses, and sustainability considerations are still underrepresented in earlier mappings. Therefore, a thorough bibliometric analysis that incorporates both these new frontiers and conventional behavioral biases is desperately needed. Addressing this gap, the present study analyzes 3,110 Scopus-indexed publications from 2015 to 2025, focusing on Q1 and Q2 journals, with the objective of mapping the intellectual, social, and conceptual structures of behavioral finance and tracing its development in response to crises, technological disruption, and socio-economic transformation.

3. Materials and Methods

We performed a performance analysis and bibliometric mapping of the research domain “behavioral finance and investment decision-making.” The workflow followed best practices for science mapping studies and included: (A) database selection and query design; (B) screening and eligibility; (C) journal-quality filtering (Q1/Q2); (D) performance indicators; and (E) network analyses (co-word, co-citation, bibliographic coupling, and co-authorship) using bibliometrix/Biblioshiny (Aria & Cuccurullo) and VOSviewer (van Eck & Waltman).

Data Source and Search Strategy

The following Advanced Search string (All fields scope), which was designed to simultaneously require (a) an investment/finance decision context and (b) behavioral/psychological constructs, was used to retrieve all records from Scopus:

ALL FIELDS ((“behavioral finance” OR “behavioural finance” OR “investor psychology” OR “investment psychology” OR “financial decision*” OR “investment decision*” OR “investment behavior” OR “investment behaviour” OR “portfolio choice” OR “trading behavior” OR “trading behaviour” OR “stock market” OR “retail investor*” OR “individual investor*”) AND (“cognitive bias*” OR “emotional bias*” OR overconfidence OR “loss aversion” OR herding OR “disposition effect” OR “mental accounting” OR “anchoring bias” OR “representativeness bias” OR “prospect theory” OR heuristic*))

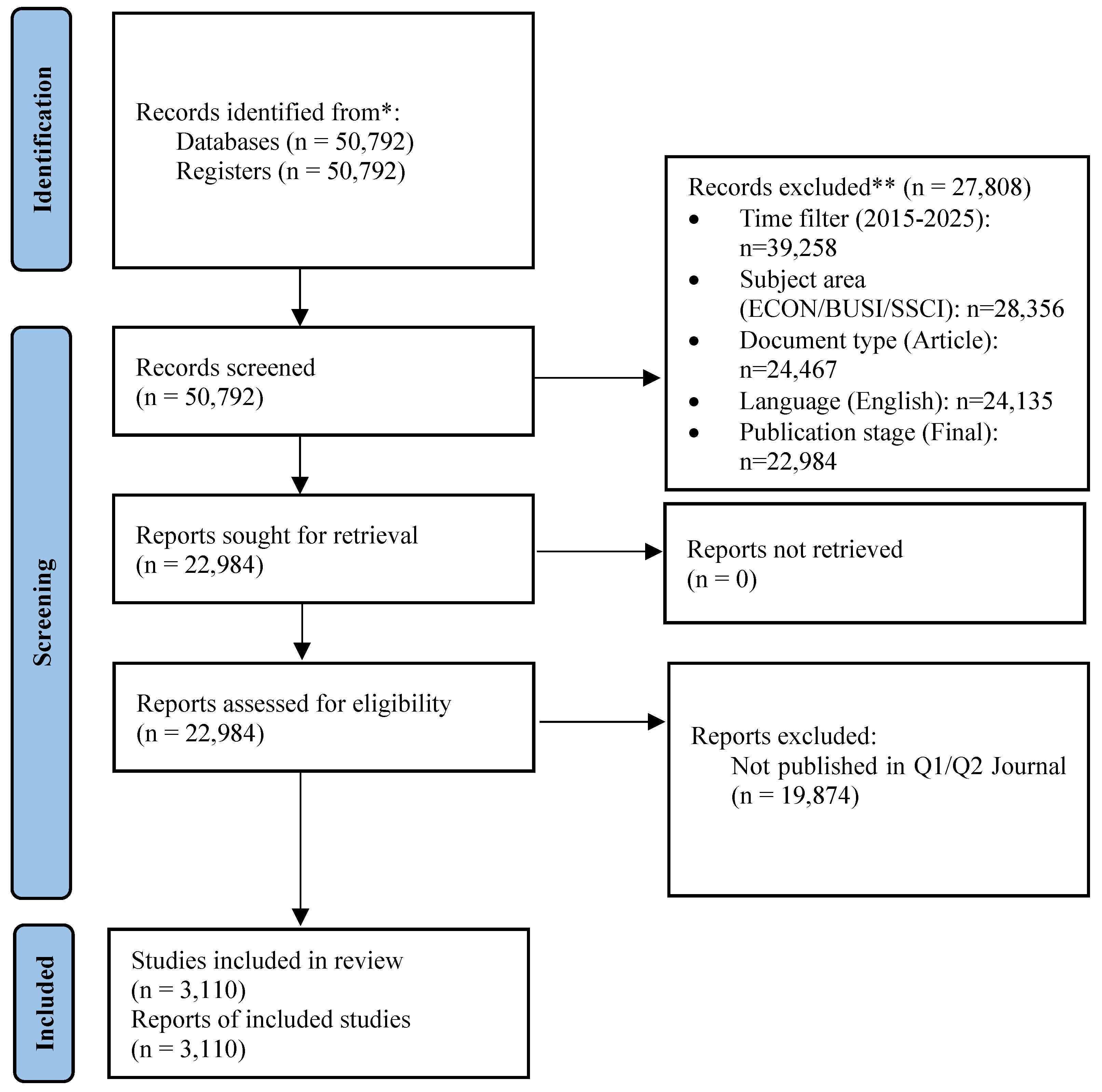

We later restricted to Scopus subject areas relevant to our field (Economics, Econometrics & Finance; Business, Management & Accounting; Social Sciences), limited the document type to articles, limited the language to English, and set the publication stage to Final in order to concentrate on the finance/management literature and prevent medical/clinical spillovers. The dataset snapshot used here covers 2015–2025. Screening counts at each stage are reported below.

Screening and Eligibility

- Initial retrieval with the domain query: N = 50,791 records.

- Time filter (2015–2025): N = 39,258.

- Subject-area restriction (ECON/BUSI/SSCI): N = 28,356.

- Document type (Article): N = 24,467.

- Language (English): N = 24,135.

- Publication stage (Final): N = 22,984.

- After Q1/Q2 journal filtering and harmonization (see below), the analytical corpus contained 3,110 records

Keeping a broad, recent window (2015–2025) supports both trend detection and contemporary thematic mapping; restricting to articles and English ensures peer-reviewed comparability and metadata completeness. A detailed visual representation of this process is provided in the Figure 1 below (PRISMA 2020):

Because Scopus does not natively filter by quartile, we matched each record’s Source title to SCImago Journal Rank (SJR) data and kept journals classified Q1 or Q2 in the relevant categories (Economics, Econometrics & Finance; Business, Management & Accounting). Operationally, we:

Exported Scopus results with Source title and full metadata (CSV).

Downloaded SJR journal lists (by subject category and year) and compiled a journal–quartile lookup.

Standardized journal names in both files (case-folding, trimming, punctuation normalization).

Merged Scopus ↔ SJR on Source title; retained rows with Quartile ∈ {Q1, Q2}.

Resolved residual mismatches manually (e.g., variant abbreviations) and deduplicated DOIs.

In addition, the Author Keywords and Index Keywords were cleaned and standardized. Specifically, all terms were converted to lowercase; “behavioural finance” was harmonized to “behavioral finance”; “decision-making” to “decision making”; “cryptocurrencies” was unified to “cryptocurrency” and “humans” to “human” and extra spaces were removed.

Performance Indicators (Biblioshiny)

We computed standard bibliometric indicators: annual production trend; top journals, authors, institutions, and countries; global and local citation counts; and reference statistics (e.g., total references in corpus). Where available in the dataset summary, we report growth dynamics and citation density (e.g., annual counts, average citations per publication by year).

Structural Indicators (VOSviewers)

We conducted bibliometric mapping through network visualizations, including co-occurrence analysis of authors and keywords, co-citation structures, and bibliographic coupling. In order to uncover the field’s intellectual, conceptual, and social structures as well as thematic concentrations, cluster density visualizations were utilized. Through these analyses, we were able to identify patterns of collaboration between authors and nations as well as core, emerging, and peripheral research areas.

4. Results

The bibliometric dataset was made up of 3,110 publications between 2015 and 2025 in 570 sources, ranging from top finance and management journals to related fields. The collection forms a pertinent corpus of investment decision-making and behavioral finance literature with an estimated 190,348 cited references. There were on average 61.21 citations for every publication, demonstrating both high scholarly impact and dissemination of the field into related research fields. The yearly growth rate was stated at −38.51%, evidencing both an increase in publications within certain peaks (e.g., finance research on COVID-19 within 2020–2021) and relative stabilization in recent years. The dataset covers a mean document age of 5.81 years, showing a balance between past and recent contributions. With respect to authorship, the discipline shows strong collaboration: a total of 7,883 distinctive authors contributed, with 250 publishing single-authored contributions. There were 259 single-authored papers (8.3%), though many were multi-authored, with a mean of 3.02 co-authors per article. The high rate of international co-authorship (76.17%) is a reflection of the world’s interest in research in behavioral finance and the widespread application of behavioral theories to discuss and explain diverse economic and cultural milieu. Table 1 is a descriptive overview of the dataset.

The dataset’s top referenced works reflect the theoretical underpinnings and innovative uses of behavioral finance. The top ten most referenced works, which together influence the conceptual, methodological, and applied growth of the discipline, are highlighted in Table 2.

Taken together, these highly cited works demonstrate how behavioral finance research has expanded beyond traditional biases to encompass fintech, ESG, crises, and digital platforms etc., while retaining its theoretical grounding in investor psychology and decision-making under uncertainty.

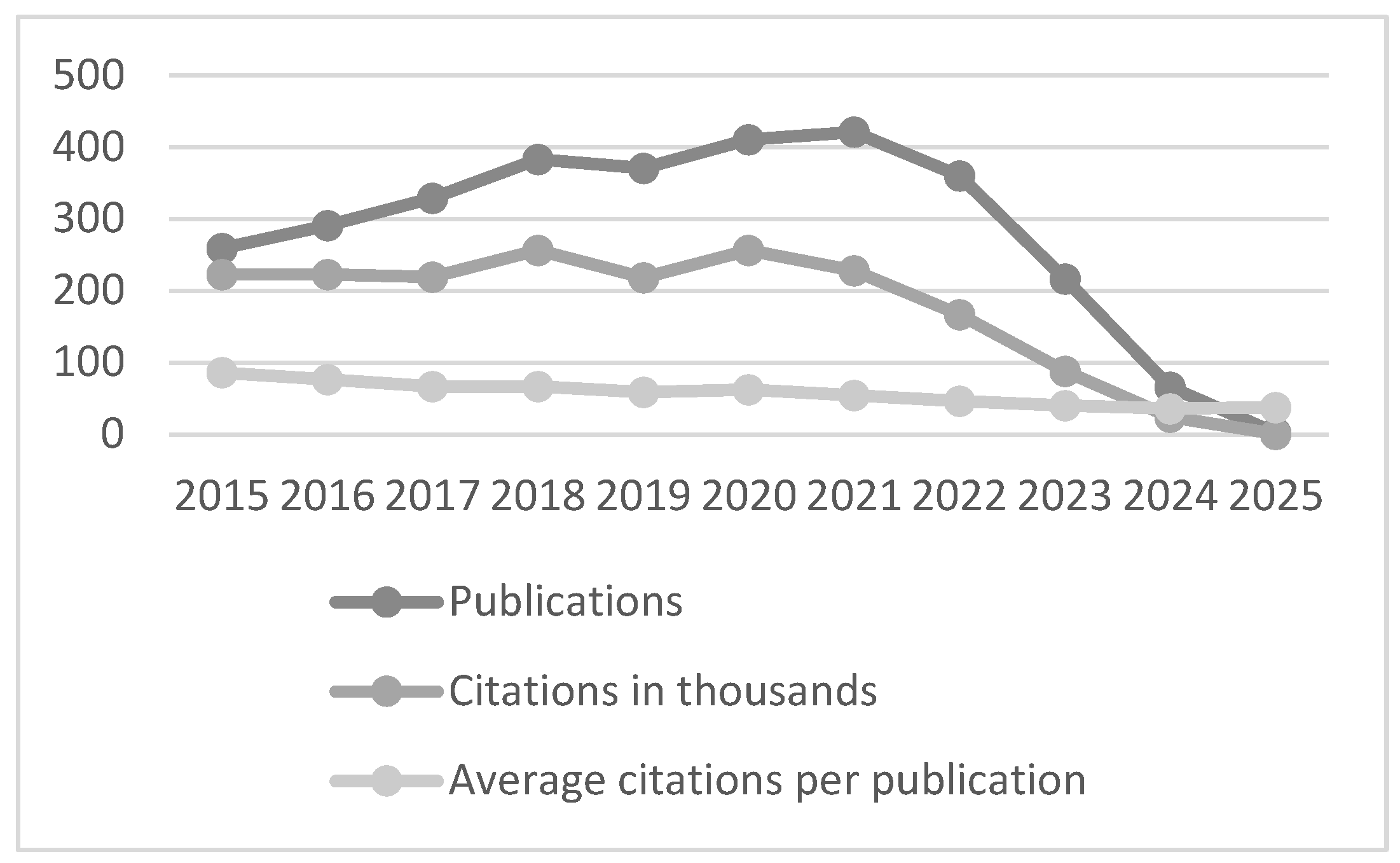

Publications Trend

Figure 2. presents the annual scientific production in behavioral finance and investment decision-making research between 2015 and 2025. A total of 3,110 articles were published over this period, with output peaking in 2021 (421 publications) before declining in subsequent years.

The trend illustrates two key directions. On the one hand, there were more publications in a regular increase from 2015 to 2021, reflecting the emergence of behavioral finance as a mainstream area of study. The peak in 2020–2021 superimposes over the COVID-19 pandemic when the surprise market shocks triggered research on financial contagion, investor sentiment, and crisis-induced decision-making.

Second, as much as there has been a sharp decline in production since 2022, the earlier publications continue to be strongly cited, and articles for 2015–2018 have the highest citation averages (85.9–67 per article). This indicates that early work in the dataset established much of the intellectual foundation of the discipline, and more recent works have not yet achieved such comparable citation figures since they are still recent.

Overall, the pattern in publications shows that studies in behavioral finance have been responsive to global events, with booms in periods of adversity, and it is presently moving into an age of thematic concentration and expertise, where focus may shift away from volume growth towards concentration and depth of research.

Most Relevant Sources

The analysis of source journals reveals the publication outlets that have most actively contributed to the field of behavioral finance and investment decision-making during the period 2015–2025. Table 3 summarizes the top 20 journals in terms of publication volume, along with their publishers and quartile classification.

As shown, most publications are concentrated in Finance Research Letters (108 papers, Q1), Management Science (96, Q1), the Journal of Finance (80, Q1), and the Review of Financial Studies (78, Q1). These top journals are a hub of the finance discipline, indicating the mainstream position of behavioral finance in financial economics.

At the same time, a number of interdisciplinary and field journals play a significant part in disseminating behavioral finance research. For example, Research in International Business and Finance (77, Q2) and the Journal of Behavioral and Experimental Finance (52, Q2) are oriented towards applied and experimental work, while journals such as Energy Economics and Journal of Cleaner Production represent the intersection of behavioral finance with sustainability and energy studies.

Interestingly, several general management and accounting journals (Strategic Management Journal, Journal of Business Ethics, Accounting Review, Small Business Economics) are also highly ranked, reflecting the diffusion of behavioral finance concepts beyond finance field journals to general organizational and decision-making domains.

Overall, the diffusion of sources confirms two primary dynamics:

- Behavioral finance research is based in elite finance journals, with strong academic legitimacy.

- The field has overflowed to adjacent areas, echoing the relevance to corporate governance, sustainability, risk management, and entrepreneurship.

Most Relevant Authors

The examination at the author level determines the leading contributors to scholarship in behavioral finance and investment decision-making. Table 4 provides the Top 10 authors ranked by citation frequency, together with their primary affiliations, nations, and publication frequencies.

The analysis finds Satish Kumar (Malaviya National Institute of Technology, India) to be the most productive researcher, with 15 papers and 1,228 citations. His steady productivity says a lot about India’s growing contribution in the body of work in behavioral finance. Next are Elie Bouri (Holy Spirit University of Kaslik, Lebanon) and Rangan Gupta (University of Pretoria, South Africa) with 14 papers each, contributing 910 and 869 citations, respectively. Their extensive co-authorship networks and contributions to applied finance themes have made them visible figures across regional and global outlets.

Alfredo De Massis is an example of a prolific researcher, with 11 publications and the most citations (1,263) of all the top authors, illustrating the profound impact of his research on both organization-related issues and the behavior of finance. Larisa Yarovaya is equally impressive, with 12 publications and 1,180 citations, and her research appears to have had significant visibility and impact in the fields of financial contagion, herding behavior and crisis management.

The next generation of academics is also represented in this analysis, with Imran Yousaf (Prince Sultan University, Saudi Arabia) and Chien-Chiang Lee (City University of Macau, China) each having nine publications, and Vo Xuan Vinh (University of Economics Ho Chi Minh City, Vietnam) has 11 publications. A few authors, such as Jing Jian Xiao (University of Rhode Island, USA) and Muhammad Abubakr Naeem (United Arab Emirates University) have also represented an increase in research rates from both the Middle East and North America.

Overall, the findings from the author-level analysis reveal the broad heterogeneity and level of collaboration between researchers in their respective research cultures worldwide. Although Europe, Africa, and Asia dominate the field of research quantitatively through high-productivity authors, citation leaders such as De Massis and Yarovaya show that influence is not merely a product of productivity but also thematic relevance and intellectual contribution.

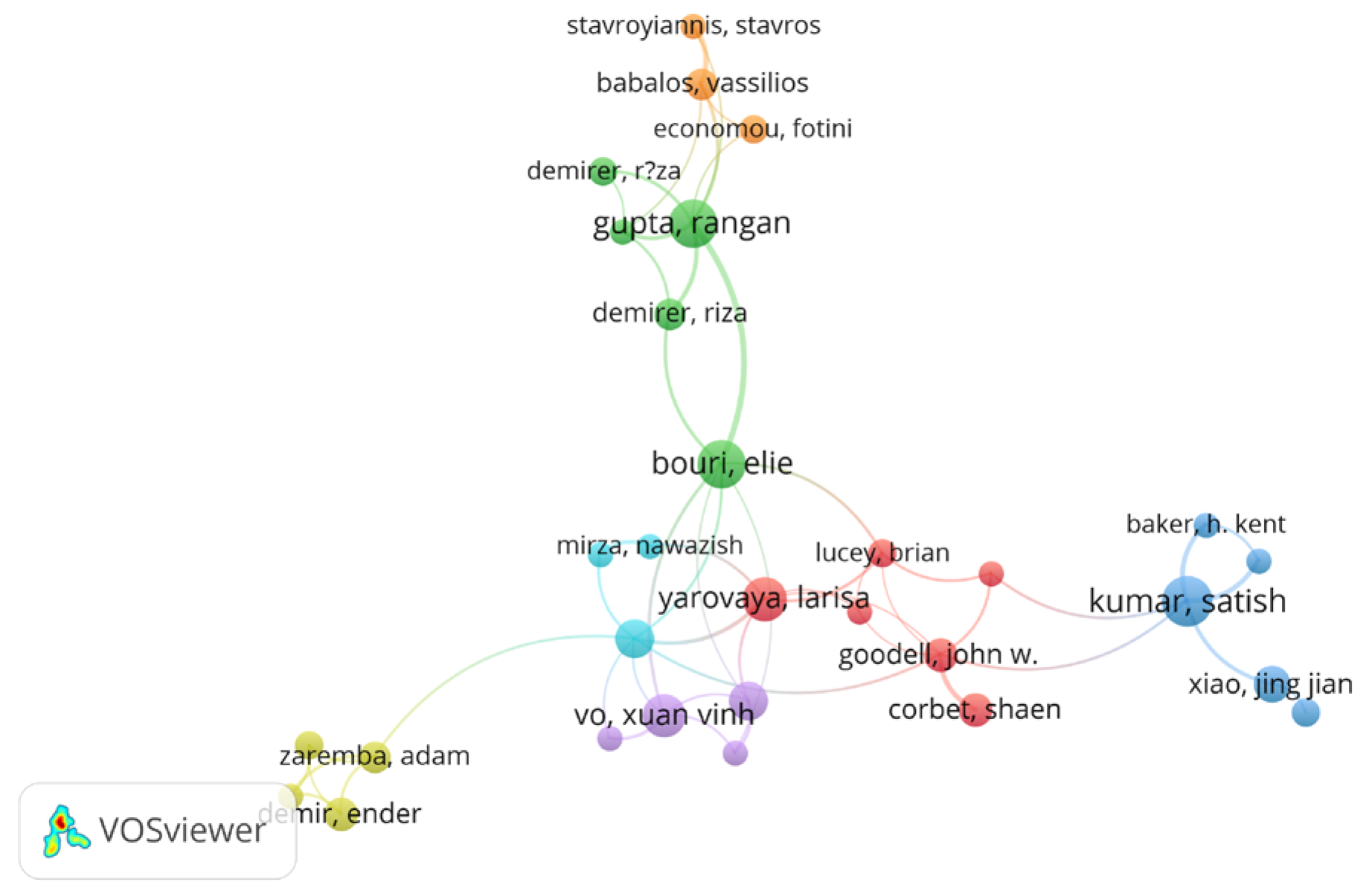

Co-Authorship Network

Using VOSviewer, we constructed a co-authorship network based on fractional counting, applying a minimum threshold of six publications per author. This approach yielded a set of highly productive and collaborative scholars whose interconnections form distinct clusters (Figure 3).

The co-authorship analysis identified seven distinct clusters of scholars meeting the threshold of six publications.

- Cluster 1, headed by Larisa Yarovaya, Brian Lucey, and John Goodell, reflects a highly international collaboration spanning the US, UK, and Ireland and focuses on financial contagion, crisis markets, and global volatility.

- Cluster 2, led by Elie Bouri, Rangan Gupta, and Riza Demirer, is heavily focused on applied finance and commodity markets, with partnerships connecting the US, Africa, and the Middle East

- Cluster 3 centers on Satish Kumar and includes Kent Baker, Jing Jian Xiao, and Andrzej Cwynar, emphasizing behavioral biases, financial literacy, and investor psychology.

- Cluster 4 brings together Ender Demir and Adam Zaremba, primarily working on emerging markets and cryptocurrency-related behavioral dynamics.

- Cluster 5 includes Xuan Vinh Vo, Muhammad Abubakr Naeem, Walid Mensi, and Syed Jawad Hussain Shahzad, with a thematic orientation toward herding behavior, Islamic finance, and crisis episodes.

- Cluster 6, led by Imran Yousaf and Nawazish Mirza, focuses on volatility spillovers and cross-market linkages.

- Lastly, Cluster 7, which was established by Vassilios Babalos, Fotini Economou, and Stavros Stavroyiannis, focuses on applications in the European market and sustainable finance.

When combined, the map demonstrates how behavioral finance is organized around a few highly cooperative clusters that each focus on certain thematic niches while preserving close ties across borders and academic fields.

Network Visualization

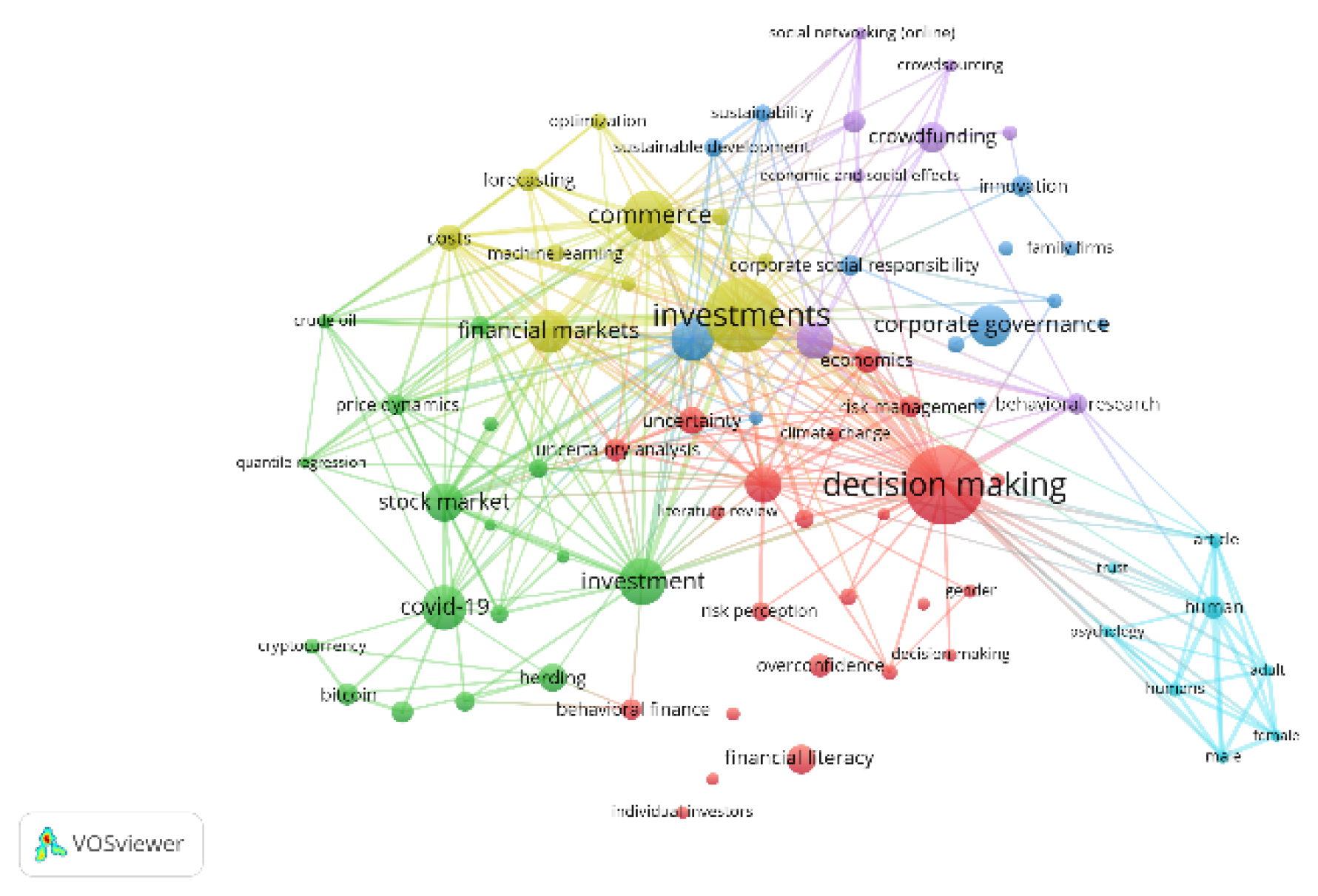

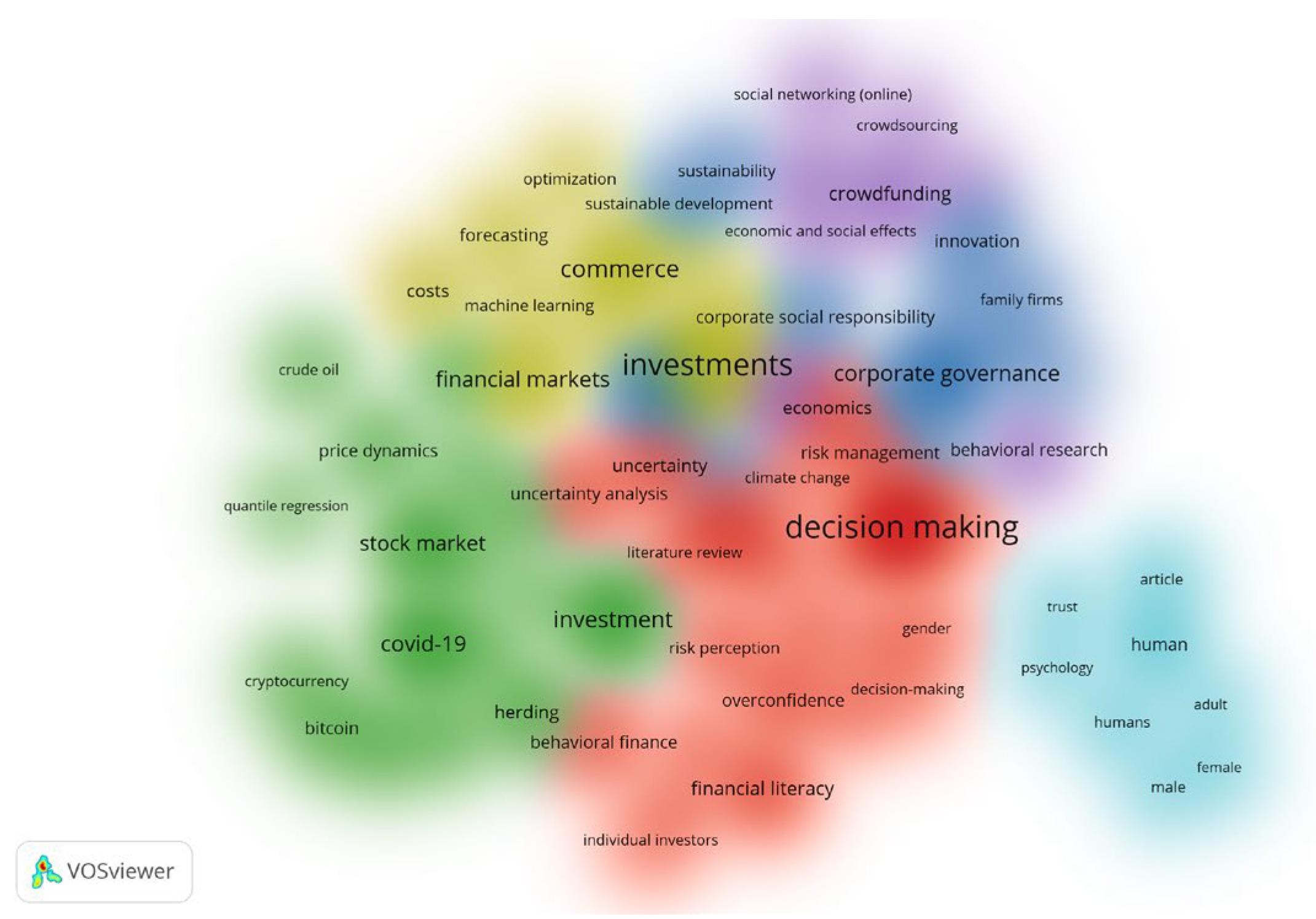

To highlight the most influential research themes, a co-occurrence analysis was conducted using VOSviewer with a minimum threshold of 24 keyword occurrences. Compared to the broader map (≥2 occurrences), this stricter filter isolates the core conceptual domains of the field while reducing noise (Figure 4).

- The first cluster (shown in red) has the greatest number of elements (21), they are related to Behavioral Biases associated with Decision Making and include the general areas of; Behavioral Finance, Decision Making, Prospect Theory, Decision Theory, Risk Assessment/ Perception/ Aversion, Over-Confidence, Heuristics, Financial Literacy, Economics, Uncertainty Analysis. This cluster forms the knowledge base from which all other themes grow; that is, it illustrates how cognitive and emotional biases affect both the way an investor behaves as well as the decisions they make.

- The second cluster in green) contains a total of 17 items and relates to the Financial Markets/ Crises. It includes the general areas of; Stock Market, Financial Crisis, Bitcoin and other Cryptocurrencies, COVID-19, Crude Oil, Investor Sentiment, Financial Markets (general), Financial Market (specific), Macroeconomics, Herding, Regression Analysis, Quantile Regression, and Price Dynamics. This cluster represents the use of Behavioral Finance in a stressful Economic context (i.e., such as crises like Covid-19) and the increased importance of Digital Assets like Cryptocurrencies.

- The third cluster (in blue) contains a total of 13 items and relates to Corporate Governance and Firm Performance. It includes the general areas of; Corporate Governance, Agency Theory, Corporate Social Responsibility, Family Firms, Manager’s behavior, Earnings Management, Sustainability, Innovation, and Firm Performance. This cluster illustrates the relationship between Behavioral Finance and Firm/ Corporate Outcomes; specifically, it illustrates how Decision Making is associated with Governance, Firm Performance, and Sustainability.

- The fourth cluster (in Yellow) contains 9 items and relates to Digital Finance and Social Commerce. It includes the general areas of; Commerce, Finance, Behavioral Research, Entrepreneurialism, Crowdfunding, Crowdsourcing, Social Media, Social Networking, Economic and Social Impacts of Digital Assets (i.e., via FinTech companies). This cluster represents the interaction between the field of Behavioral Finance and its use of technology, as well as the emergence of Social Dynamics as an influencing factor in shaping both Financial Behavior and Entrepreneurial Behavior.

- The fifth cluster (in Purple) has 8 items and relates to Technology and Forecasting. It includes the general areas of Artificial Intelligence, Machine Learning, Optimization, Forecasting, Sales, Costs, Supply Chain, and Investments. This illustrates the emerging collaboration between Behavioral Finance and Technology (including Analytics) and Predictive Modelling.

- Cluster 6 (aqua/light blue, 7 items): Demographics and psychology. Comprises human, male, female, adult, psychology, trust, and article. This cluster reflects the growing role of demographic and psychological factors in financial behavior, underscoring how identity and social context shape investment decision-making.

Density Visualization

To further explore the prominence of research themes, a density visualization was generated using VOSviewer (Figure 5). In this map, the color intensity represents the frequency of keyword co-occurrence: warmer areas (red and yellow) denote higher density of publications, whereas cooler areas (green and blue) indicate less frequent, yet still significant, themes.

The density visualization identifies the major research themes found in this body of literature. The areas of greatest density (indicated by red and yellow) show the terms used most often; areas of less density (designated by green and blue) show the keywords that although less frequently used, are still important in the research area. In the center of the densest areas are the terms “decision making” and “investments” indicating that both are key to the development of theory in this area. Surrounding the density centers are keywords associated with “risk assessment,” “uncertainty,” “behavioral finance,” “overconfidence,” “financial literacy,” and “herding” which reinforce the notion that behavioral bias and risk are of paramount importance.

There are other peripheral areas in the areas indicating themes in financial markets, stock markets, and crises such as COVID-19 and the financial crisis, as well as digital assets like bitcoin and cryptocurrency indicating how this area of study has been used in real-world shocks/events. Other densities emerge from the themes of corporate governance, sustainability, and artificial intelligence which are interdisciplinary areas that examine how organizations, ethics, and technology shapes financial decisions.

The cluster in the lower left corner consists of the keywords human, gender (Because this study relies exclusively on bibliographic metadata, sex- and gender-based analyses at the individual level could not be conducted, which may limit the generalizability of sociodemographic interpretations.), male, female, psychology and trust, which indicates an increasing emphasis on the sociodemographic and psychological aspects of investment behavior. This cluster reinforces the findings that in addition to financial processes, the personal attributes and social environment of an individual moderate the relationship between behavioral factors and investment decisions, and that the manifestation of behavioral factors varies and not unanimous.

5. Discussion

The bibliometric mapping of 3,110 articles published between 2015 and 2025 provides new insights into the intellectual, social, and conceptual structures of behavioral finance and investment decision-making research. The findings confirm that the field has matured into a globally connected and thematically diverse domain, while also revealing several important dynamics that warrant discussion.

First of all, publication trends indicate that behavioral finance research has been highly responsive to external shocks. Production growth during 2020–2021 occurs in conjunction with the COVID-19 crisis, consistent with previous evidence that crises trigger more interest in investor psychology and contagion mechanisms (Akhtaruzzaman et al., 2021; Conlon and McGee, 2020). Nevertheless, the decline in volume after 2022 signals that the field is moving towards a phase of thematic consolidation, from expansiveness to more specialized and sophisticated explorations. This is aligning with the general pattern observed in other fields related to finance where initial surges in publications are later followed by stabilization and optimization (Donthu et al., 2021).

Second, the authors and journals most frequently cited reveal the central role of global scattered researchers. Although Elie Bouri, Rangan Gupta, and Satish Kumar are productivity champions, citation leaders Larisa Yarovaya and Alfredo De Massis reveal that influence is as much determined by thematic consistency as by quantitative output. While its infiltration into journals like the Journal of Cleaner Production and the Journal of Business Ethics suggests growing interdisciplinarity, particularly in sustainability and ethics, the existence of Q1 journals like Finance Research Letters, Management Science, and Review of Financial Studies shows that behavioral finance has established itself in prestigious finance journals.

Third, co-authorship patterns also demonstrate the international level of collaboration that exists in the field. By looking at the co-authorship maps, it is apparent that there are several interconnected cross-regional clusters between Europe, Asia, and North America. The three primary clusters of Yarovaya, Bouri, and Kumar show how many unique theme niches, such as crisis market research, commodity finance, and investor psychology, are created through international collaboration. This is consistent with the previous findings that behavioral finance is considered one of the most internationalized areas of financial research (Merigó and Yang, 2017). The international co-authorship rate is an astonishing 76.17%, which suggests that the probable advancement of the discipline will occur within transnational teams, as opposed to isolated national schools.

Fourth, the conceptual mapping also identifies new avenues for research. Stable anchors can be seen in the recurring themes of overconfidence, herding, and loss aversion, which continue to be critical to the support of Kahneman and Tversky’s Prospect Theory (Kahneman and Tversky, 1979), as well as other theories on related behavioral biases. Additionally, the cryptocurrency, big data, and AI cluster continues to represent new areas of exploration, which further reinforces the calling for researchers to meld behavioral finance with new and emerging technology (Lo, 2017; Adam et al., 2020). Finally, the increasing recognition and importance of sustainability and ESG have been noted in the bibliometric density maps as being areas of growing concern, as demonstrated by the publications of Hartzmark and Sussman (2019).

The findings from research identified several gaps in knowledge. Although, there has been much research conducted to understand how sociodemographic characteristics (gender, education, cultural differences) impact these issues, further research needs to be completed in this arena, in terms of how social biases and market relationships can affect these issues. Additionally, while behavioral finance is a global discipline, there remain substantial gaps in the representation of certain regions, namely Africa and Latin America, indicating the potential for additional research in these areas. Furthermore, still, a lot of research is being completed using traditional surveys and econometric methods, while experimental design approaches and interdisciplinary methodologies (using psychology and data science) are significantly less prevalent.

The outcome of the research shows that behavioral finance has matured from being a niche area of interest to being an area of interest that encompasses the globe, has many disciplines of study, and has gained maturity in the academic arena as such. The growth and development of this area of study in the future will be determined, to some extent, by three fundamental aspects. They are: (a) continual integration of technology and data analysis; (b) continued emphasis on the role of sustainability and diversity within demographic considerations; and (c) the ability to convert theoretical findings into substantial implications for market participants, policy makers, and regulators.

6. Conclusion

This study performed an extended bibliometric mapping on investment choice and behavioral finance research through 3110 articles (that were published from 2015 to 2025) that were published in Scopus Q1 and Q2 journals. By combining performance metrics and using graphical representations, this study provides a thorough overview of the intellectual, social, and conceptual landscape of the behavioral finance field. It also clearly identifies several key trends including; increased output levels during crises such as the COVID-19 pandemic (due, in part, to increased media attention); several researchers gaining prominence at a global level, including Satish Kumar, Elie Bouri and Larisa Yarovaya; and the development of an increasing trend toward international collaborations with over 75% of authors utilizing authors from different countries in their publications.

Conceptual maps demonstrate the continued relevance of several central behavioral biases including overconfidence, herding, loss aversion and the disposition effect, while also demonstrating that new themes are developing including cryptocurrencies, sustainability, artificial intelligence and ESG finance. These results suggest that behavioral finance has moved beyond being just a tool to explain market anomalies, to increasingly being used to address interdisciplinary and frontier issues, broadening the field’s scope and appeal.

This study presents three overall contributions. To start with, it develops the body of knowledge in behavioral finance into a concise framework for the last 10 years of literature and provides an overview of the major developments in this area. Second, this research will identify gaps that exist within the current literature, including sociodemographic factors such as gender, location and lack of new measurement methods that will expand the scope of behavioral finance research. Lastly, it will provide a conceptual model for future research, specifically the effect of economic shocks (such as the post-pandemic era), technological advancements (e.g., fintech), and the increasing demand for sustainability on how finance will be practiced in the future.

One limitation of this bibliometric analysis is that the Scopus database and Q1/Q2 filters were used; therefore, other journals may have published notable works which were not included in our analysis of this literature. In addition, bibliometric indicators only provide insight regarding citation counts as a measure of the impact of the literature. As a result, bibliometric indicators cannot be used to quantify how this research affects the practical application of finance and the decisions made by policymakers.

Although this study will provide a baseline for researchers and practitioners who wish to advance and contribute to the knowledge base of behavioral finance, these efforts should best be supplemented by qualitative and empirical methods. By continuing to evolve the fields of finance, psychology, and technology with a focus on sustainability, behavioral finance will remain an evolving and influencing area of financial research.

Author Contributions

Conceptualization, [El Mehdi Douhabi, Issam El Azzaoui, Zineb Drissi]; Methodology, [El Mehdi Douhabi]; Data curation, [El Mehdi Douhabi]; Formal Analysis [El Mehdi Douhabi, Issam El Azzaoui, Zineb Drissi]; Writing – Original Draft, [El Mehdi Douhabi, Issam El Azzaoui]; Writing – Review & Editing, [Zineb Drissi], Supervision, [Zineb Drissi].

Funding

The main author benefits from the PhD Associate Scholarship provided by the National Centre for Scientific and Technical Research (N* = 38USMBA2024).

Data Availability Statement

The data supporting the findings of this study were derived from the Scopus database. Processed data and analytical procedures are available from the corresponding author upon request.

Acknowledgments

The corresponding author would like to express his sincere gratitude to the National Centre for Scientific and Technical Research (CNRST, Morocco) for its financial support, which had no influence on the research itself. This support simply enabled selected PhD candidates to fully dedicate their time to their studies, in line with CNRST’s mission to advance education and scientific research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Adam, M.; Wessel, M.; Benlian, A. AI-based chatbots in customer service and their effects on user compliance. Electron. Mark. 2020, 31, 427–445. [Google Scholar] [CrossRef]

- Akerlof, G.A.; Shiller, R.J. Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

- Akhtaruzzaman, M.; Boubaker, S.; Sensoy, A. Financial contagion during COVID–19 crisis. Financ. Res. Lett. 2021, 101604, 101604. [Google Scholar] [CrossRef] [PubMed]

- Aria, M.; Cuccurullo, C. bibliometrix: An R-tool for comprehensive science mapping analysis. J. Informetr. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Barberis, N.; Thaler, R. A survey of behavioral finance. In Handbook of The Economics of Finance; Elsevier: Amsterdam, The Netherlands, 2003; Volume 1, pp. 1053–1128. [Google Scholar] [CrossRef]

- Bikhchandani, S.; Sharma, S. Herd Behavior in Financial Markets. IMF Staff. Pap. 2001, 47, 279–310. [Google Scholar] [CrossRef]

- Christie, W.G.; Huang, R.D. Following the Pied Piper: Do Individual Returns Herd around the Market? Financial Anal. J. 1995, 51, 31–37. [Google Scholar] [CrossRef]

- Conlon, T.; McGee, R. Safe haven or risky hazard? Bitcoin during the Covid-19 bear market. Finance Res. Lett. 2020, 35, 101607–101607. [Google Scholar] [CrossRef] [PubMed]

- Corbet, S.; Lucey, B.M.; Yarovaya, L. “The Financial Market Effects of Cryptocurrency Energy Usage”. 2019. [Google Scholar] [CrossRef]

- De Long, J.B.; Shleifer, A.; Summers, L.H.; Waldmann, R.J. Noise Trader Risk in Financial Markets. J. Politi- Econ. 1990, 98, 703–738. [Google Scholar] [CrossRef]

- Donthu, N.; Kumar, S.; Mukherjee, D.; Pandey, N.; Lim, W.M. How to conduct a bibliometric analysis: An overview and guidelines. J. Bus. Res. 2021, 133, 285–296. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient Capital Markets: A Review of Theory and Empirical Work. J. Finance 1970, 25, 383. [Google Scholar] [CrossRef]

- Gaviria-Marin, M.; Merigo, J.M.; Popa, S. Twenty years of theJournal of Knowledge Management: a bibliometric analysis. J. Knowl. Manag. 2018, 22, 1655–1687. [Google Scholar] [CrossRef]

- Hartzmark, S.M.; Sussman, A.B. Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows. J. Finance 2019, 74, 2789–2837. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- Lo, A.W. Adaptive Markets: Financial Evolution at the Speed of Thought; Princeton University Press: Princeton, NJ, USA, 2017. [Google Scholar]

- Merigó, J.M.; Yang, J.-B. A bibliometric analysis of operations research and management science. Omega 2017, 73, 37–48. [Google Scholar] [CrossRef]

- Odean, T. Are Investors Reluctant to Realize Their Losses? J. Finance 1998, 53, 1775–1798. [Google Scholar] [CrossRef]

- Shefrin, H.; Statman, M. The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence. J. Finance 1985, 40, 777–790. [Google Scholar] [CrossRef]

- Shiller, R. Irrational Exuberance; Princeton University Press: Princeton, NJ, USA, 2000. [Google Scholar]

- Shiller, R. Irrational Exuberance, 2nd ed.; Princeton University Press: Princeton, NJ, USA, 2015. [Google Scholar]

- Statman, M. Behavioral Finance: The Second Generation; CFA Institute Research Foundation: Charlottesville, VA, USA, 2019. [Google Scholar]

- Thaler, R. Mental Accounting and Consumer Choice. Mark. Sci. 1985, 4, 199–214. [Google Scholar] [CrossRef]

- Tversky, A.; Kahneman, D. Extensional versus intuitive reasoning: The conjunction fallacy in probability judgment. Psychol. Rev. 1983, 90, 293–315. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [PubMed]

Figure 1.

Screening And Eligibility Protocol (Prisma 2020 Workflow).

Figure 2.

Annual Publications and Citation Impact.

Figure 3.

Co-Authorship Network.

Figure 4.

Network Visualization.

Figure 5.

Density Visualization.

Table 1.

Main Information About the Dataset.

| Description | Results |

| Main information about data | |

| Timespan | 2015:2025 |

| Sources (journals, books, etc.) | 570 |

| Document type | |

| Article | 3110 |

| Annual growth rate % | -38.51 |

| Document average age | 5.81 |

| Average citations per doc | 61.21 |

| References | 190348 |

| Document contents | |

| Keywords plus (id) | 900 |

| Authors keywords | 2626 |

| Authors | |

| Authors | 7883 |

| Authors of single-authored docs | 250 |

| Authors collaboration | |

| Single-authored docs | 259 |

| Co-authors per doc | 3.02 |

| International co-authorships % | 76.17 |

Table 2.

Summary Of Key Contributions in Behavioral Finance and Investment Decision Making.

| Study | Title | Key findings | Citations |

| Agrawal, A.; Catalini, C.; Goldfarb, A. | Crowdfunding: Geography, Social Networks, and the Timing of Investment Decisions | Examine crowdfunding platforms, showing that geography and social networks significantly shape investment decisions. | 725 |

| Adam, M.; Wessel, M.; Benlian, A. | AI-based Chatbots in Customer Service and Their Impact on Decision-Making | Finds that AI chatbots influence consumer trust and decision processes in financial and service contexts. | 700 |

| Huang, D.; Jiang, F.; Tu, J.; Zhou, G. | Investor Sentiment Aligned: A Powerful Predictor of Stock Returns | Proposes a sentiment index strongly predictive of asset prices, showing sentiment-driven market movements. | 697 |

| Akhtaruzzaman, M.; Boubaker, S.; Sensoy, A. | Financial Contagion during COVID-19 Crisis | Demonstrates how the COVID-19 pandemic triggered strong financial contagion across global markets. | 695 |

| Hartzmark, S.; Sussman, A. | Do Investors Value Sustainability? A Natural Experiment Examining ESG Factors | Provides evidence that sustainability salience increases investors’ valuation of ESG-friendly stocks. | 670 |

| Thakor, A. V. | Fintech and Banking: What Do We Know? | Reviews fintech literature, highlighting impacts on banking structure, regulation, and decision-making. | 662 |

| Choi, T.M.; Wallace, S.; Wang, Y. | Big Data Analytics in Operations Management | Shows that big data analytics enhances operational and financial decision efficiency. | 654 |

| Conlon, T.; McGee, R. | Safe Haven or Risky Hazard? Bitcoin during the COVID-19 Bear Market | Tests Bitcoin’s role during crises; finds mixed evidence on whether it functions as a safe haven. | 603 |

| Bernile, G.; Bhagwat, V.; Rau, P. R. | What Doesn’t Kill You Will Only Make You More Risk-Loving? Managerial Experience and Risk-Taking | Shows that managers exposed to crises take greater risks later, influencing corporate investment decisions. | 587 |

| Stambaugh, R.; Yu, J.; Yuan, Y. | Arbitrage Asymmetry and the Idiosyncratic Volatility Puzzle | Identifies limits to arbitrage and explains persistent volatility anomalies through asymmetric investor behavior. | 542 |

Table 3.

Most Relevant Journals.

| Source | Volume | Publisher | Index | Quartile |

| Finance Research Letters | 108 | Elsevier Ltd. | Scopus | Q1 |

| Management Science | 96 | INFORMS | Scopus | Q1 |

| Journal of Finance | 80 | Blackwell Publishing Ltd. | Scopus | Q1 |

| Review of Financial Studies | 78 | Oxford University Press | Scopus | Q1 |

| Research in International Business and Finance | 77 | Elsevier Ltd. | Scopus | Q2 |

| International Review of Economics and Finance | 59 | Elsevier Inc. | Scopus | Q2 |

| Journal of Business Ethics | 53 | Springer Netherlands | Scopus | Q1 |

| Journal of Behavioral and Experimental Finance | 52 | Elsevier B.V. | Scopus | Q2 |

| Strategic Management Journal | 50 | Wiley | Scopus | Q1 |

| Energy Economics | 48 | Elsevier B.V. | Scopus | Q1 |

| Journal of Cleaner Production | 45 | Elsevier Ltd. | Scopus | Q1 |

| Journal of International Financial Markets, Institutions and Money | 38 | Elsevier Ltd. | Scopus | Q2 |

| Resources Policy | 36 | Elsevier Ltd. | Scopus | Q2 |

| Journal of Management | 33 | SAGE Publications | Scopus | Q1 |

| Accounting Review | 33 | American Accounting Association | Scopus | Q1 |

| Accounting and Finance | 33 | Blackwell Publishing | Scopus | Q1 |

| Small Business Economics | 33 | Springer | Scopus | Q1 |

| Journal of Financial and Quantitative Analysis | 32 | Cambridge University Press | Scopus | Q1 |

| Journal of Behavioral Finance | 28 | Institute of Behavioral Finance | Scopus | Q2 |

| Review of Quantitative Finance and Accounting | 25 | Springer | Scopus | Q2 |

Table 4.

Most Influential Authors.

| Author | #ofArts | Affiliations | Country | Cited by |

| Kumar, Satish | 15 | Malaviya National Institute of Technology | India | 1228 |

| Bouri, Elie | 14 | Holy Spirit University of Kaslik, Jounieh, | Lebanon | 910 |

| Gupta, Rangan | 14 | University of Pretoria | South Africa | 869 |

| Yarovaya, Larisa | 12 | Namal University | United Kingdom | 1180 |

| Vo, Xuan Vinh | 11 | University of Economics Ho Chi Minh City | Vietnam | 774 |

| De Massis, Alfredo | 11 | University of Bozen-Bolzano | Italy | 1263 |

| Yousaf, Imran | 9 | Prince Sultan University | Saudi arabia | 930 |

| Lee, Chien-Chiang | 9 | City University of Macau | China | 549 |

| Naeem, Muhammad Abubakr | 9 | United Arab Emirates University | United Arab Emirates | 445 |

| Xiao, Jing Jian | 8 | University of Rhode Island | United States | 604 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.