Submitted:

29 January 2026

Posted:

29 January 2026

You are already at the latest version

Abstract

This study investigates how positive and negative framing affect sustainable investment behaviour, emphasising the mediating role of investor confidence and the moderating role of intention. An experimental design with 301 participants was employed, comparing control, positive, and negative framing conditions. Participants allocated both simulated and real monetary endowments to a green investment (recycling) project, and the PROCESS macro for SPSS was used to test mediation and moderation models. The results show that positive framing directly increases allocation to sustainable investment, while negative framing operates indirectly by enhancing investor confidence, which in turn drives greater investment. Moderation analysis further demonstrates that negative framing strengthens the link between intention and real monetary commitment, even though the direct effect of framing on actual financial behaviour remains weak. This paper contributes to behavioural finance by clarifying the differential mechanisms of positive and negative framing in investment decisions and highlighting confidence as a key psychological pathway in sustainable finance behaviour. It also differentiates short-term and long-term behaviour to capture the complexity of sustainable investment.

Keywords:

sustainable investment

; framing effect

; green investment intention

; experimental

; behavioural finance

Introduction

The term Sustainable Responsible Investment (SRI) has emerged as a prominent trend in recent investment studies. The terminology refers to the integration of environmental, social, and ethical (ESG) considerations into investment decisions (Mehta et al., 2020). The objective of investing has evolved beyond merely maximising the investor’s utility or capital gain to include supporting sustainability and intergenerational responsibility. Despite sustainable investments potentially generating lower returns, Gen-Z investors place a substantial value on environmental issues and prefer investments that align with ESG principles (Negash et al., 2025). According to the recent bibliometric literature review, investors’ preference for sustainability is multidimensional, presenting a gap that can be tested from the perspective of behavioural finance, particularly by applying behavioural finance theory in practical experimental settings (Paulsy and M, 2025).

The primary challenge in making green investments is the high uncertainty and low returns associated with them. Experimental evidence suggests that investors who invest in green projects expect high returns as compensation (Siemroth and Hornuf, 2023). Committing a fund to invest in green investments will require a confident attitude, a set of belief values and financial literacy that makes them persistent (Negash et al., 2025; Raut, 2020; Sivaramakrishnan et al., 2017). However, under certain circumstances, the framing effect can be a helpful tool for influencing human decisions, especially investment decisions (Kiky et al., 2024; Rossolini et al., 2021). Applying the negative message framing can effectively promote sustainable investment in green bonds (Rossolini et al., 2021). Understanding how behavioural cues, particularly negative framing, can be a critical avenue for investigation.

Despite the growing interest in sustainable and responsible investment (SRI), empirical research that tests sustainable investment decisions under an experimental method remains limited. Most prior studies have focused on institutional investors or analysed ESG preferences through surveys and secondary data, lacking controlled settings to observe actual decision behaviour. Furthermore, although the theory of planned behaviour and financial literacy have been shown to influence green investment intentions, the interaction between behavioural cues, such as message framing, and individual investor characteristics has received insufficient attention (Raut, 2020; Yanuarti Loebiantoro et al., 2024). While recent studies suggest that negative message framing can be more persuasive in encouraging sustainable investment, few have tested this phenomenon in a realistic, experimental setting involving individual investors. This creates a critical research gap in understanding how framing effects can influence investors’ willingness to commit funds to green financial instruments.

This paper aims to answer the two questions. First, can the way sustainability messages are framed (positive and negative) influence investors’ behaviour in funding green projects? The second question is whether the framing effect can be a moderating factor that strengthens investors’ intention to commit real money to a green recycling project. While previous studies have explored investor preferences toward green projects using surveys or interviews, few have adopted experimental designs to capture real investors’ commitments to funding green projects. By isolating the framing effect within a controlled simulation, we seek to provide empirical evidence on how behavioural nudges can support sustainable investment behaviour in practice.

Literature Review

Sustainable Investment and Funding for Green Projects

The concept of ethical investing can be traced back to 1993, when the idea of ethical investment was introduced (Anand and Cowton, 1993). From an ethical perspective, the investment is not solely about performance, but also about maintaining a long-term fiduciary relationship with stakeholders (Richardson, 2011). As the Sustainable Development Goals (SDGs) agenda emerged from the United Nations, sustainable investment became a leading trend. One of the current trends is carbon trading, where incentives have been designed to encourage firms to actively reduce their emissions (Casady and Monk, 2025). The optimism about earning from green stock was also high during 2008 and 2016 (Liu et al., 2025). This gives rise to sustainable investment as an essential research area in financial studies, especially to understand the actual behaviour of investing in green projects.

Investing in a green project can be a challenging endeavour because the odds of success are very low. It required a massive fund to explore green technology, where there is no guarantee of success for the project. The study of crowdfunding platforms suggests that investors still expect a high return as compensation for investing in a green project (Siemroth and Hornuf, 2023). Aruga (2025) found that only retail investors with high altruistic characteristics were interested in a 1.1% annual return on Japan Green bonds. These findings highlight a gap in understanding how behavioural finance tools can be applied in navigating green stock price volatility. Hence, investors are willing to add their funds to green projects when the price is down.

However, behavioural finance is not a standalone variable that can directly influence actual sustainable investment behaviour. Without strong confidence in the project’s future success, the desire to allocate funding would be weak. Previous research has indicated that high optimism without informational efficiency can pose a significant challenge to making long-term green investments (Liu et al., 2025; Lobão, 2025). Therefore, we set up an experiment to investigate the role of behavioural finance in actual investment behaviour. We believed that a negative message could be more effective in convincing investors of the green project’s success rate (Rossolini et al., 2021). The framing effect may be utilised to enhance investors’ confidence with a negative message, ultimately leading to the consistent funding of green projects. We suspect that investors’ confidence will mediate the framing effect before it has an impact on the actual sustainable behaviour, which in this case, is additional funding for the green project.

Based on the theory of planned behaviour applied to investment behaviour, intention is an antecedent factor of sustainable investment behaviour (Zhang and Huang, 2024). The theory proposed that several Internal factors shaped investment intention (Garg et al., 2022; Raut, 2020). In this paper, we explore the concept of investors’ intention to understand how the framing effect can be used as a behavioural nudge in an experimental setting. We suspect that the framing effect serves as the moderating variable in the relationship between intention and sustainable investment behaviour.

Sustainable investment behaviour in this paper is defined as the act of adding funds during the simulation and making actual investments for recycling projects. The participants will be asked to play a simulation of green stock investment and navigate the price volatility. We expect that the framing effect will increase investor confidence and cause them to make additional funding in the simulation at the decision points. We are also integrating the concept of intention from the theory of planned behaviour with the framing effect. In this case, the framing effect will moderate the relationship between investors’ intention and sustainable investment behaviour. We are not investigating the internal factors, such as attitude, social norms, and perceived behaviour control, from the original TPB model due to the complexity of applying it to the experimental setting. At the end of the experiment, we also asked participants whether they were willing to invest some of their money in a real recycling green project. This research is conducted in collaboration with the Tzu Chi Foundation to finance their recycling activities.

Framing Effect and Behavioural Nudges

Beyond the foundational work of Tversky and Kahneman (1981), research has demonstrated that framing effects occur across various domains, including risky-choice, attribute, and goal framing. Kühberger et al. (1999) showed that probability cues and evaluative descriptions systematically shift risk preferences even when objective outcomes stay constant. A meta-analysis by Piñon and Gambara (2005) further affirms the robustness of framing effects across contexts, indicating that both positive and negative cues can distort subjective judgments. In strategic environments, Dufwenberg et al. (2011) emphasise that framing alters beliefs and psychological play, illustrating how subtle wording can influence expectations and subsequent decisions. These insights reinforce the theoretical basis for investigating how message valence may influence investor confidence in sustainability settings.

The application of the framing effect is widespread and can be found in various academic studies. In the context of investment behaviour, several papers have found that framed information can lead to different results in decisions (van der Heijden et al., 2012; Kiky et al., 2024). However, the way framing effects work on sustainable behaviour can be very complex. Gain or loss-framed information has a three-way interaction on sustainable behaviour intention (Choi et al., 2023). Compared with Kim and Chon (2022), the narrative framing is more effective than gain-loss framing in CSR communication for advocating an environmental campaign.

Understanding how framed messages in terms of prevention or promotion focus can influence Gen Z’s sustainable behaviour remains a novel exploration (Negash et al., 2025). Through narrative framing as a communication medium, the public tends to build a strong, positive association between the company and the environmental domain (Kim and Chon, 2022). According to Kim and Chon (2022), the narration approach is more effective than a gain or loss-framed message in influencing supportive behaviour for pro-environmental advocacy. Other research has found that a loss-framed risk message enables participants to be more aware of environmental issues and take a more proactive approach (Choi et al., 2023). However, a different result was reported by Stadlthanner et al. (2022), who found that gain framing induces positive consumer sustainable behaviour.

The theoretical foundation for understanding how the framing effect influences sustainable behaviours can be traced back to communication and marketing literature. It can be beneficial in encouraging consumers to adopt sustainability behaviours (Wilkie et al., 2024). How the message is presented can influence actual purchasing behaviour for sustainable products (Jäger and Weber, 2020). The results indicated that the way the message is framed can evoke intention, but it leaves a gap to be expanded into actual behaviour (Kim and Chon, 2022; Wilkie et al., 2024). Choice behaviour is highly responsive to the evaluative aspect of the message, even when the objective probability remains the same (Kühberger et al., 1999; Piñon and Gambara, 2005). As proposed by Dufwenberg et al. (2011), framing manipulations influence not only through information but also via shifts in beliefs and psychological expectations. Integrating the framing effect into the experimental setting might provide a nuanced understanding of the sustainable investment research theme, which is now a dedicated research theme (Paulsy and M, 2025).

We believe that sustainable investment behaviour is a complex problem. According to the previous findings, a higher return is required as compensation for the inherent risk associated with green projects (Liu et al., 2025; Siemroth and Hornuf, 2023). Investors’ confidence in the future success of the green project is a critical factor that drives them to invest their funds. Therefore, the framing effect, as a behavioural nudge, will need confidence as a mediator before it can influence actual decisions.

Research papers on investing behaviour have highlighted the importance of intention as an antecedent variable preceding behaviour (Raut, 2020; Sivaramakrishnan et al., 2017; Yanuarti Loebiantoro et al., 2024). While previous research focuses on internal factors such as attitude, social norms, and perceived behavioural control’s influence on behaviour intention, this paper adopts an experimental approach as complementary research to understand how actual decisions are made, especially for long-term commitments. We agree with the previous finding that the intention to invest in a green project might be an antecedent variable in this experiment. In the case of behavioural nudge, the framing effect might not directly increase sustainable behaviour (Florence et al., 2022). Other sources highlighted the role of the framing effect as a moderating variable, which served as a communication strategy to ensure the success of sustainability funding (Rossolini et al., 2021).

This study contributes to the behavioural finance literature in three ways. First, it extends research on the framing effect by providing experimental evidence on how positive and negative framing influences sustainable investment decisions, moving beyond the predominantly survey-based approaches. Second, it introduces investor confidence as a mediating mechanism, clarifying how framing translates into actual financial behaviour through shifts in subjective certainty. Third, it incorporates investment intention as a moderated pathway, demonstrating how framing conditions influence the translation of intention into a real monetary commitment.

Hypothesis Development

Building on the behavioural finance literature, this study posits that framing effects influence sustainable investment decisions by altering investors’ subjective confidence in the success rate of green projects. Previous framing studies indicate that message valence influences subjective probability judgments (Kühberger et al., 1999), even when the numerical likelihood remains unchanged. Meta-analytic evidence also demonstrates that attribute and goal-framing systematically alter evaluative assessments (Piñon and Gambara, 2005), which may appear as differences in confidence. Dufwenberg et al. (2011) additionally argue that framing shapes psychological play, affecting expectations and perceived likelihoods of outcomes. Therefore, it is reasonable to expect that positive and negative sustainability messages will influence investors’ confidence in the project’s success. In the context of green investment, such framing is likely to affect the certainty with which investors evaluate their decisions. Thus, we expect that framing has an indirect effect on investment behaviour through investor confidence.

Furthermore, intention to invest represents a critical precursor to actual allocation of resources. However, behavioural biases may condition the extent to which intention translates into behaviour. Specifically, we argue that framing moderates this pathway by either amplifying or attenuating the investor’s intention to fund green projects. There are four hypotheses that we would like to test in this paper. The first three hypotheses will be tested based on the simulation input. In comparison, the last hypothesis will focus on the actual funding requested from the participant at the end of the simulation. The hypotheses are stated as:

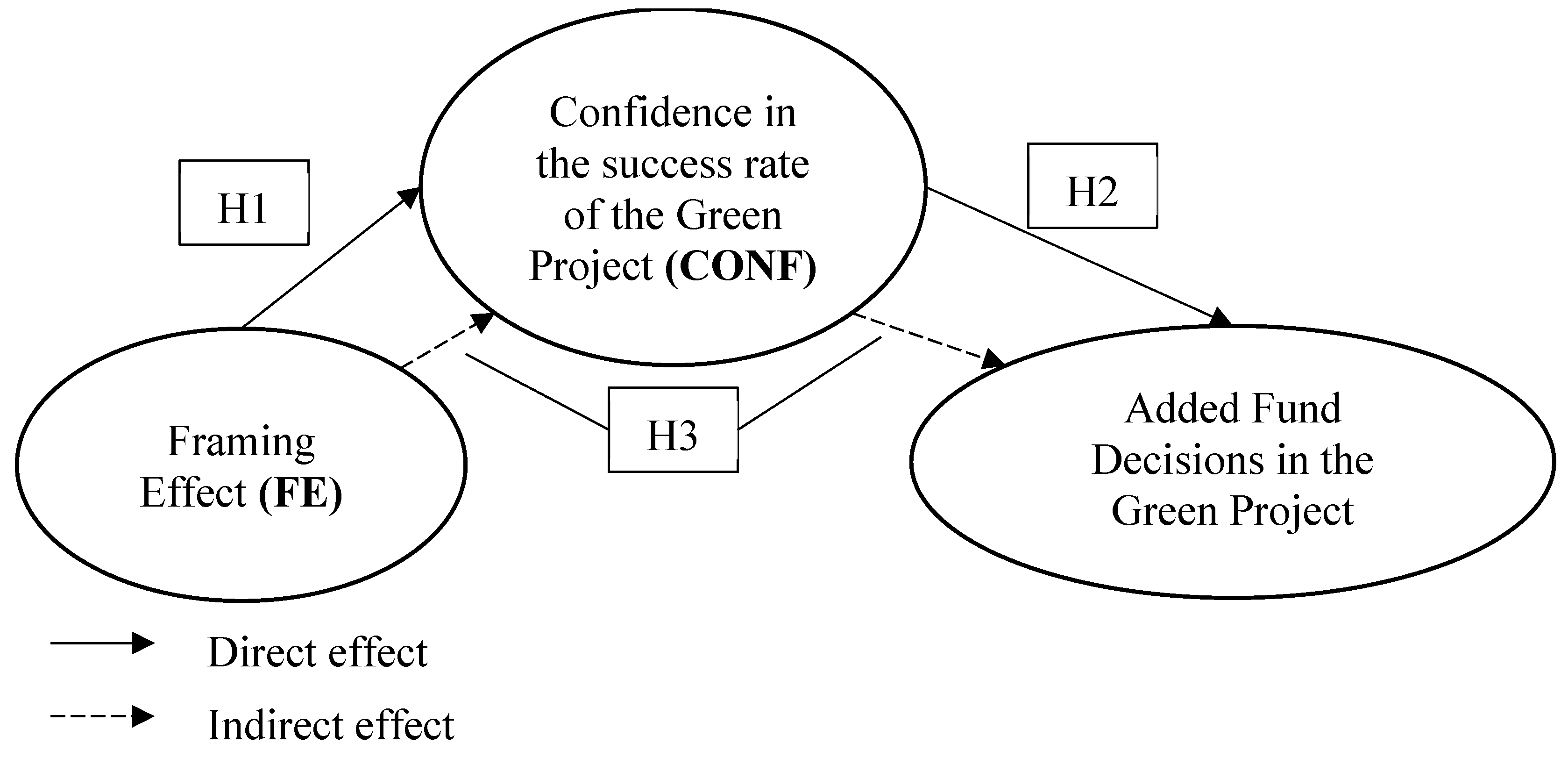

H1.

Framing effect influences investor confidence in the success of a green project.

H2.

Investor confidence positively predicts the proportion of funds allocated to green projects.

H3.

Investor confidence mediates the relationship between framing effect and green investment behaviour.

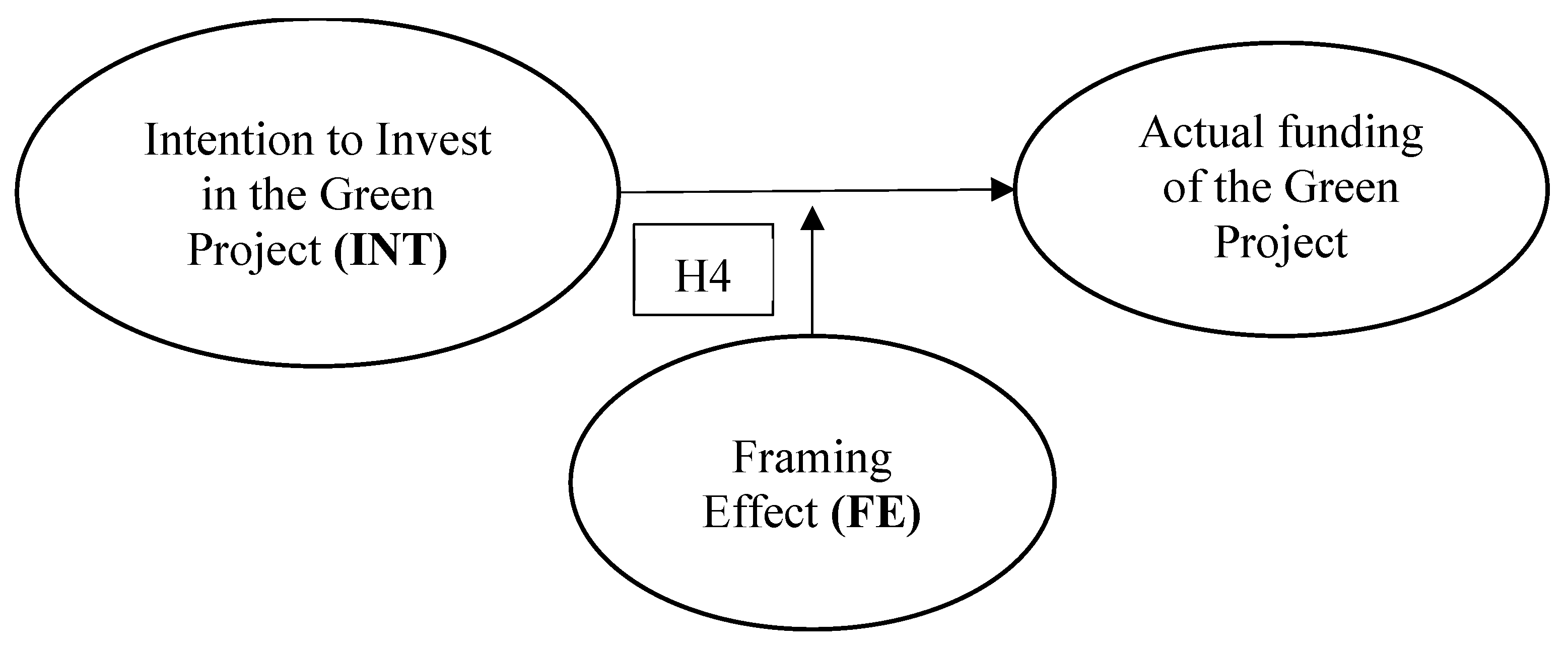

H4.

The framing effect moderates the relationship between investment intention and actual funding of green projects.

Figure 1.

The research framework 1 for the first three hypotheses. Source(s): Authors’ work.

Figure 2.

The research framework 2 for the fourth hypothesis. Source(s): Authors’ work.

Research Methods

This paper used an experimental method to investigate how the mechanism of the framing effect, as a behavioural nudge, influences sustainable investment behaviour. This lab experiment uses a self-developed website to simulate stock volatility and record participants’ decisions. The narrative for this stock was that the firm was working on a recycling project and needed funding to ensure the project’s success. We decided that the price trend is up, considering the complexity of the downtrend movement in investment decision-making (Kiky, 2025). Participants received an incentive based on their final asset value at the end of the experiment. This project is funded by the Indonesian Ministry of Higher Education (DIKTI) as a research grant to investigate green investment behaviour.

This design choice was motivated by two considerations. First, prior experimental evidence indicates that positive expected returns are necessary to sustain engagement and prevent premature exit in green investment simulations (Siemroth and Hornuf, 2023). Second, an upward-trending market allows us to isolate framing-induced behavioural responses from mechanical loss aversion and panic-selling effects, thereby increasing internal validity when identifying framing mechanisms. While our experimental design prioritises internal validity, it necessarily constrains external generalizability. In particular, the use of a laboratory simulation, student participants, and relatively small monetary incentives may not fully capture the complexity, emotional burden, and long-term risk exposure inherent in real-world sustainable investment decisions.

Participants were randomly assigned to one of three message conditions regarding the sustainability project: a neutral message (without an explicit probability cue), a positive message emphasising a “50% chance the project will succeed”, or a negative message emphasising a “50% chance the project will fail”. We regard the neutral condition as a baseline informational setting, similar to situations in which investors receive qualitative descriptions of a green project without quantitative success probabilities. The positive and negative conditions, however, present identical objective probabilities but differ in the framing valence of the 50% likelihood.

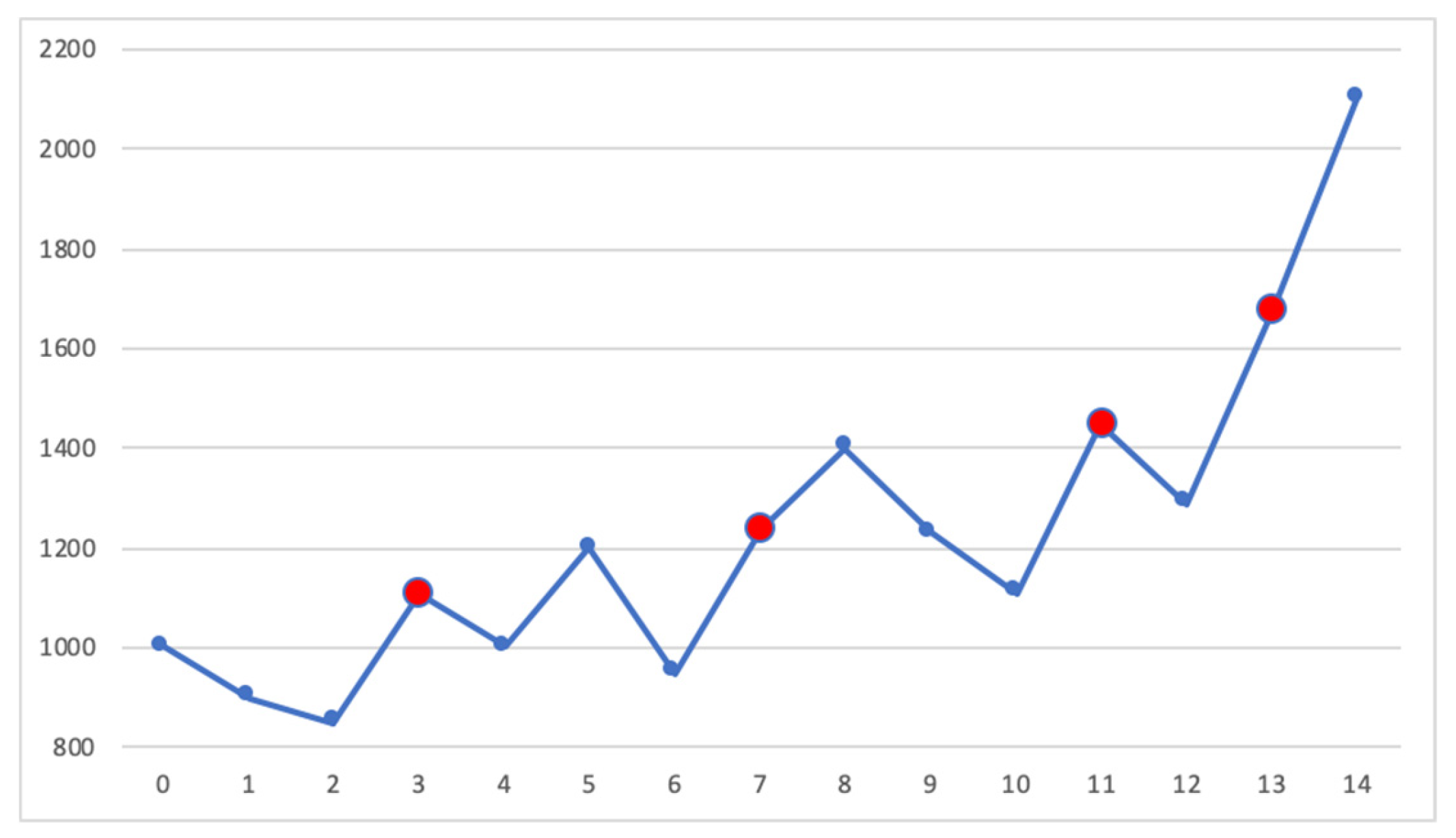

The experiment was designed to understand the relationship between the framing effect, investors’ confidence, intention, and sustainable investment behaviour. The first design principle was to integrate the findings from Siemroth and Hornuf (2023) and Liu et al. (2025), which stated that high returns remain relevant in sustainable investments. Therefore, the simulation price will have an uptrend movement with several volatilities in each session. There are fourteen sessions of price volatility, and participants only need to make four decisions at specific decision points. The decision points are established when the price rises by approximately 30% from the previous level, at sessions 3, 7, 11, and 13. This sudden price increase can prompt the sale of assets too early, a phenomenon known as the disposition effect (Jiao, 2017). This will prevent participants from experiencing exhaustion or saturation during the experiment, which improves upon the previous design of Kiky et al. (2024) that required participants to make decisions in all sessions.

Field studies in human-computer interaction show that people typically stay on a given digital screen for less than a minute before switching tasks (Mark et al., 2016). Therefore, the experimental design introduces a second delay to provide participants time to process the price movement before making impulsive decisions. Our eight-second delay between sessions is therefore not intended to measure maximum sustained attention, but rather to create a short, controlled pause that falls well within this attention window.

The details of the simulation price and four decision points are shown in Figure 3. For more information on the experimental setup, documentation, and handout, see: https://drive.google.com/file/d/197sveIZVlDkshYPYNNp1LQbwrP5IrCnr/view?usp=sharing. The details of the operationalisation of the research variables are described in Table 1.

The research model will be analysed using the PROCESS macro SPSS by Hayes (2022) to capture the mediating and moderating effects of behavioural finance. PROCESS is particularly suitable for this study because it allows the simultaneous estimation of direct, indirect, and interaction effects within a single analytical framework, while also accommodating categorical predictors through dummy coding (e.g., contrasts between control, positive, and negative framing conditions). Importantly, indirect effects were evaluated using non-parametric bootstrapping with 5,000 resamples, which generates bias-corrected confidence intervals and provides more reliable inference given the non-normal distribution of product terms in mediation analysis. This approach ensures a transparent, efficient, and statistically robust evaluation of how framing effects influence green investment behaviour both through confidence (mediation) and as a moderator of the intention–behaviour relationship.

The estimated models are:

where CONF denotes investor confidence, PROP denotes sustainable investment behaviour measured as the proportion of added funds, X1 represents the contrast between positive framing and the neutral condition, and X2 represents the contrast between negative and positive framing.

where G_INV denotes the proportion of real funds invested, INT represents green investment intention, and W1 and W2 capture the framing contrasts.

Result and Analysis

Descriptive Result

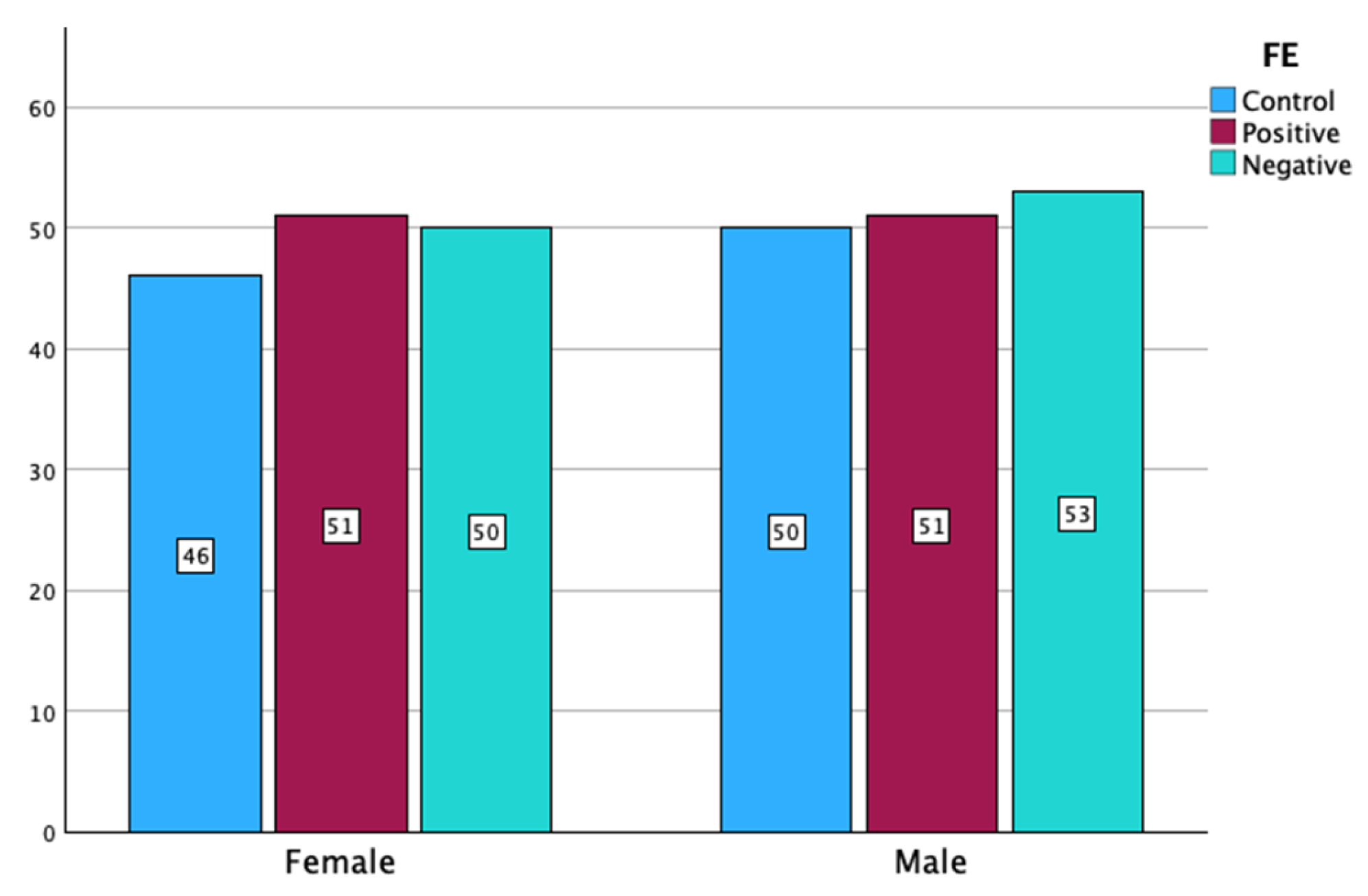

The experiment was conducted from June to September 2025. The participants of this experiment were the university students who had completed or were taking an investment-related course during their studies. Most of the participants are business school students. The experiment was conducted in the classroom according to the schedule set by the research team. We collected 301 participants. The participants in this experiment are Generation Z, born between 1997 and 2012. The sample is dominated by university students aged 19 to 21 (around 73% of the sample). The surveyor randomised the participants to ensure the experiment’s robustness. The samples were distributed fairly among the three groups in the experiment, comprising 147 females and 154 males. The distribution of samples is described in Figure 4. The experimental data can be accessed via this link: https://docs.google.com/spreadsheets/d/17WJuOlqrYOlCOWuLtlWdo5mweUUX2YJm/edit?usp=drive_link&ouid=111823552638738417863&rtpof=true&sd=true.

Table 2 reports pairwise comparisons of sustainable investment behaviour across framing conditions. Sustainable investment behaviour is measured by proportional outcomes, which capture the share of available resources allocated to the green project. In the simulation phase (PROP), the dependent variable represents the average proportion of funds added relative to the participant’s available endowment across four decision points, with a minimum of 0 (no additional funds allocated) and a maximum of 1 (all available funds allocated). For the real investment decision (G_INV), the dependent variable is the ratio of real funds donated to the recycling project to the participant’s final asset value, again bounded between 0 and 1.

Using proportional measures ensures comparability across participants with different endowment levels and decision histories, while preserving the economic meaning of the choice as an intensity of commitment rather than a binary decision. Ordinary least squares (OLS) estimation is employed for both descriptive comparisons and regression analysis, as the variables are continuous, bounded by design rather than censored, and exhibit sufficient variation within the interior of the [0,1] interval. This approach is common in experimental and behavioural finance research and allows for straightforward interpretation of marginal effects. To mitigate concerns about heteroskedasticity arising from bounded outcomes, all inferential analyses use heteroskedasticity-consistent standard errors.

Participants exposed to negative framing allocated a significantly higher proportion of funds to the green project than those in the neutral condition (t = 2.68, p = 0.008). By contrast, positive framing did not significantly differ from the neutral condition, and the difference between negative and positive framing did not reach conventional significance levels. These findings suggest that negative framing is more effective than a neutral message in promoting short-term sustainable investment behaviour, while its advantage over positive framing is more modest. Notably, although the direct difference between negative and positive framing is not statistically significant in the bivariate comparison, the mediation analysis shows that negative framing exerts a significant indirect effect on sustainable investment behaviour through investor confidence. This pattern is consistent with the interpretation that negative framing operates through psychological mechanisms rather than through a strong direct behavioural shift.

Before proceeding to the research model, we checked the effect size using ANOVA. The ANOVA results indicated that the framing condition explained a small but meaningful portion of the variance in PROP (η2 = 0.023) and CONF (η2 = 0.022), consistent with prior behavioural finance research where psychological manipulations typically account for modest effects. By contrast, the variance in G_INV explained by framing was negligible (η2 = 0.007), suggesting that while framing can shift participants’ reported allocation behaviour, its impact on real monetary commitment is weaker. Details are shown in Table 3.

Hypothesis Testing of Research Framework 1 (Mediation Analysis)

The regression results show that the direct and indirect effects of framing on sustainable investment behaviour (PROP) were modest and mixed. H1 proposed that framing would shape investor confidence in the success rate of green projects. This hypothesis is supported, as negative framing significantly increased confidence compared to positive framing (b = 0.0515, p < 0.05) [Table 4], while positive framing did not differ from the control group. These results indicate that negative framing is more effective in elevating psychological certainty than positive or neutral messages.

H2 posited that investor confidence in the success rate of green projects directly increases the proportion of funds invested. This hypothesis is confirmed as CONF significantly increases the invested fund (b = 0.8651, p < 0.01) [Table 4]. In the case of the direct effect of framing, we also found that positive framing can directly influence the proportion of invested funds in the simulation. Compared to the control group, participants exposed to positive framing allocated a significantly larger share of their endowment to the green project (b = 0.41, p < 0.01), indicating that the positive message was effective in stimulating investment, even when confidence was not taken into account. However, the contrast between negative and positive framing was not significant (b = -0.12, p = 0.45), indicating that the direct superiority of negative framing could not be established when considered in relation to the positive condition.

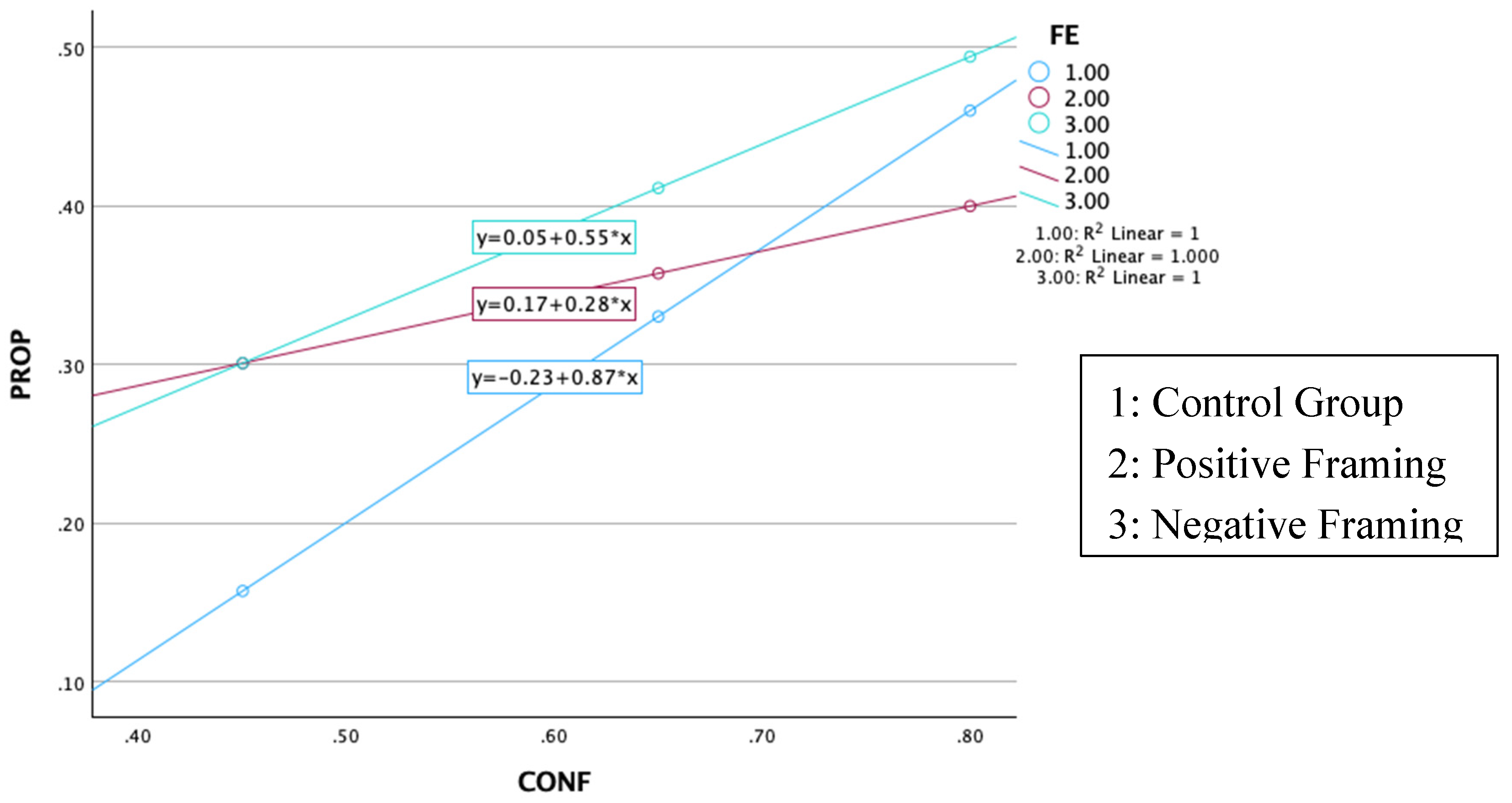

In contrast, the mediation analysis highlights the critical role of investor confidence in transmitting the effect of negative framing to the proportion of funds added. H3 posited that investor confidence mediates the effect of framing on sustainable investment. This hypothesis is supported, as evidenced by PROCESS analysis, which reveals a significant indirect effect of negative versus positive framing on PROP through confidence (b = 0.027, 95% CI [0.001, 0.064]) [Table 5]. This finding aligns with the PROCESS visualisation [Figure 5], which shows that confidence exerted a more substantial influence on investment under negative framing compared to positive or control conditions.

These findings suggest that framing manipulations, while influential, have mixed effects on sustainable fund allocation. The positive message has a direct influence on the proportion of allocated funds in green projects, albeit to a lesser extent than negative framing, with confidence serving as a mediator. Interestingly, negative framing indeed created a sense of urgency, making participants believe that the success of the green project was crucial. However, it will need the mediating factors before it can manifest into real behaviour. It will be discussed further in the discussion section.

Hypothesis Testing of Research Framework 2 (Moderation Analysis)

After the simulation, we tried to capture the real funds invested in the green project (recycling project). We used green investment intention from the TPB model as an antecedent variable before running the moderation analysis of the framing effect. The second framework tried to understand long-term commitment and comprehend how the framing effect can have a lasting impact on long-term decisions. The total of real funds invested in the Tzu Chi recycle project was IDR 7,719,395, and these funds were deducted from the participants’ incentives. TPB predicted that intention would have a positive influence on green investment (Raut, 2020; Zhang and Huang, 2024). However, our results indicate that the effect of INT on G_INV was not statistically significant (b = 0.014, p = 0.063) [Table 6]. The difference is in the measurement of actual behaviour in sustainable investment, where our findings complement the results from previous studies. With the experimental approach, we gained a better understanding of the sacrifices made by measuring the actual money that participants gave up, which was not covered by the survey (Zhang and Huang, 2024).

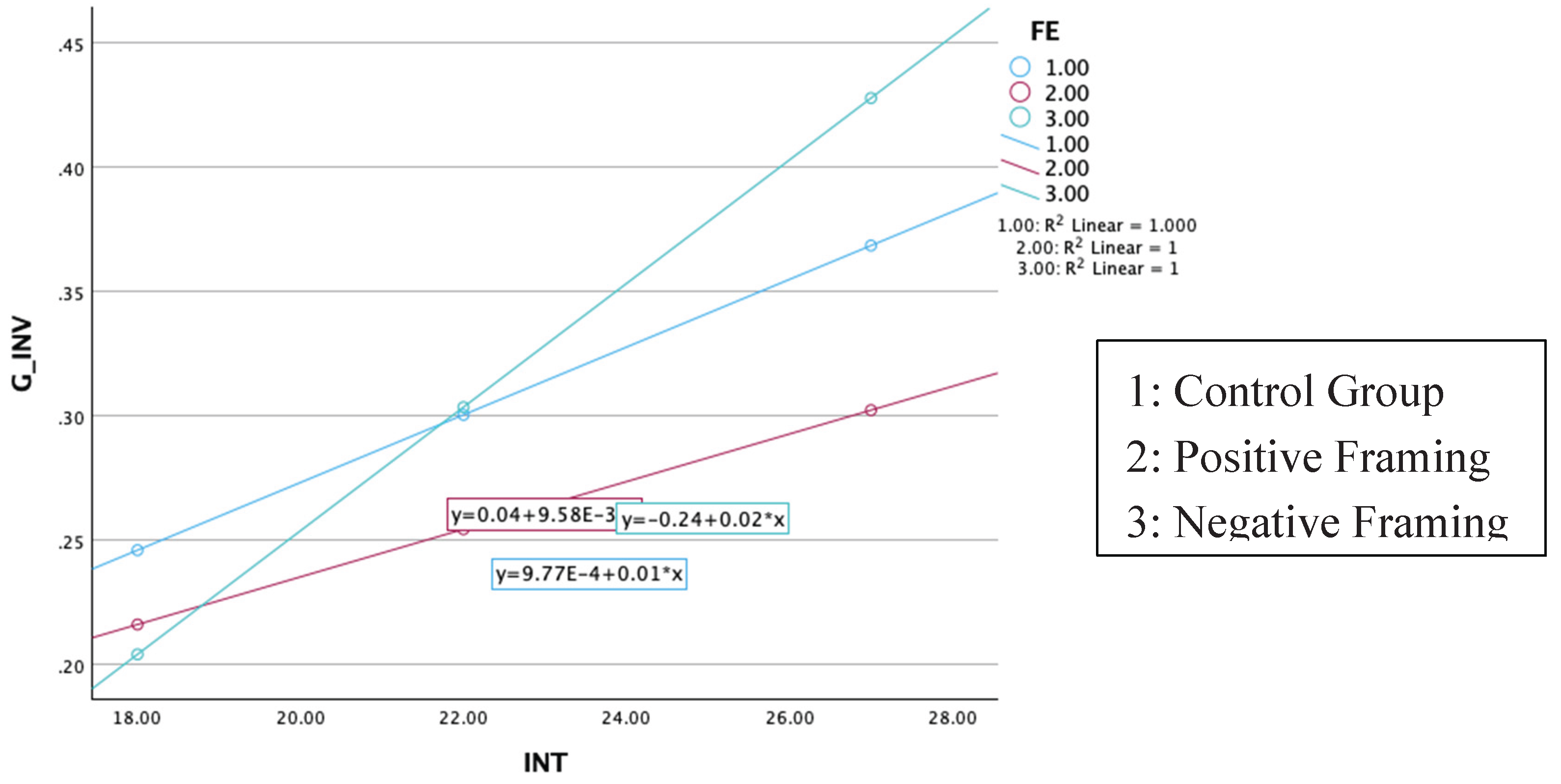

The final hypothesis (H4) focused on the moderating effect of framing on this relationship. We believe that the framing effect can have an amplifying effect on the investor’s intention, leading them to invest more funds. Negative framing (vs. positive) showed a significant moderating impact (b = 0.015, p < 0.05) [Table 6]. The interaction plot (Figure 6) illustrates that under negative framing, the slope between intention and investment is steeper, indicating that participants with higher intentions are more likely to translate those intentions into actual green investments when exposed to negative framing. The real invested fund was greater for participants who received a negative framing and had an inherent intention. The results suggest that negative framing was indeed effective in encouraging participants to invest more in the green project, provided they already had an internal motivation to do so. Let’s compare the direct effects of negative and positive framing. The result will be fewer funds invested than that of the participants who received the positive message (b = -0.287, p < 0.05) [Table 6]. Conditional analysis should be a crucial path to consider for understanding the mechanism of negative framing in sustainable investment decisions.

Overall, based on the R-squared values of these models, the framing effect is relatively better at explaining short-term decisions in Framework 1 than in Framework 2. The mediating model has an R-squared value of 0.123 [Table 4], while the real fund invested model (Framework 2) has an R-squared value of only 0.097 [Table 6]. The effect is relatively small for long-term decisions, as indicated by the ANOVA effect size in Table 3.

Discussion

Differential Impact of Positive and Negative Framing

Positive framing will have a direct effect on short-term decisions, while negative framing will require a mediating factor before it can influence behaviour. This finding aligns with a previous study by Daugaard et al. (2024), which found that an optimistic orientation does increase responsible investment. Our experimental setting enables participants to benefit from the simulation (gain), and the framing effect evokes incidental emotions in the process. The incidental emotions (such as fear and excitement) will affect the investment preference (Cantarella et al., 2023). In the case of positive framing and uptrend simulation, the effect does not need any mediating factor such as confidence.

The effectiveness of negative framing is more complex than that of positive framing. Due to the experiment design, after receiving a negative message, the participants were required to input their confidence in the success rate of the green project. It can influence a greater proportion of invested funds only for those who have a stronger belief in the project’s success. The result is also similar to the finding that negative framing requires a particular mediator before it can influence compliance behaviour (Menon et al., 2025). Compared to several studies on negative framing, it was indeed more evocative of attention (Zunckel et al., 2023). Our findings also supported Rossolini et al. (2021), who found that negative framing was more effective for climate preservation projects, which, in our case, is the green recycling project. Our findings extend the understanding of how negative framing works. It required conditional factors, and its impact was indeed more powerful than positive framing.

Confidence in the Green Project’s Success Rate as a Mediating Factor

Instead of directly shaping behaviour, framing influences subjective probability judgments, which then manifest as differences in reported confidence. Although the actual probability of project success or failure remains fixed at 50% across conditions, previous research shows that individuals systematically distort probability assessments depending on how outcomes are framed (Kühberger et al., 1999; Piñon and Gambara, 2005). In this way, confidence in the project’s success reflects a subjective belief shaped by probability weighting rather than a straightforward interpretation of objective information.

Negative framing emphasises the potential adverse consequences of project failure, thereby heightening cognitive salience and shifting attention to the importance of avoiding undesirable outcomes. This evaluative emphasis leads participants to overweight the implications of failure relative to its stated likelihood, thereby adjusting their subjective assessment of the project’s prospects. As shown by Dufwenberg et al. (2011), framing influences expectations and psychological beliefs even when the strategic environment remains unchanged. Consequently, differences in confidence across framing conditions should be understood as the result of framing-induced belief distortion, not as irrational departures from the provided probability information. Our results support the finding that negative framing can be more effective in communicating and driving the behaviour (Cantarella et al., 2023; Rossolini et al., 2021), but in our case, it needs confidence as a mediator.

We leave further exploration of the mediating factor for future research. Our findings are a result of the strict experimental design, which allowed participants to experience the framing effect first, then input their confidence. The result might be different if other researchers use a different experimental design, such as subjects input their confidence before the framing effect. Future research can explore how message effectiveness serves as a mediating factor between negative framing and sustainable investment behaviour, as Menon et al. (2025) have found in the context of public compliance behaviour.

Weak Effects on Actual Monetary Commitment (Long-Term Decisions)

The final hypothesis was set to capture the long-term commitment of participants in funding a sustainable project. Siemroth and Hornuf (2023) laid the foundation for our experimental design, in which we set the price trend in a simulation to an uptrend, compensating for the high returns of sustainable investments. The effect was relatively weak on the amount of money that participants gave up to fund the recycling project, as confirmed by our R2. It leaves a big room to explore, where long-term decisions are not easily driven by behavioural finance. Our best explanation for this finding is that the framing effect evokes incidental emotions on investment decisions (Cantarella et al., 2023), which relate to short-term decisions but not long-term ones. The behaviour is instantaneous, as a reaction to a particular stimulus (the framing effect), as suggested by the prospect theory and psychological literature (Kahneman and Tversky, 1979; Tversky and Kahneman, 1974, 1981).

Future Research into Altruistic Motivation

Based on current findings, investing in green projects remains a promising avenue. Our experiment examines the framing effect on sustainable investment decisions. We suggest that this research can be expanded to another ESG focus, such as health-related, social-related, or disaster relief (Baeckström et al., 2022). While our paper only covers the environmental area, there is plenty of room to explore the other three areas. Investing in socially related themes remains underexplored, and current research still leaves a gap to be examined (Siemroth and Hornuf, 2023). The other areas, health and disaster relief, are more complex to investigate than the other two, but offer great novelty to understanding altruistic motives in human decisions.

As we stated in the introduction section, investing in a sustainable cause was different from classical investment. A normal investment will focus on maximising utility and wealth, as the classical theories discuss. In contrast, a sustainable investment (in the long run) tends to be driven by a philanthropic motivation rather than an egoistic motive. The further extension of our experiment can include the altruistic motive as the driver in green investment, where several recent papers have indicated that this motive can influence the behaviour (Gutsche et al., 2023; Hervé and Marsat, 2024). The anxiety in the relationship between financial advisors and clients, caused by investment performance, remains a persistent issue that needs to be addressed (Courtenay et al., 2025). We believed that understanding the altruistic variable might help resolve the trust and anxiety issues that stem from egoistic and self-serving motives. Perhaps the psychological contract between a financial advisor and wealthy investors could begin with an altruistic motive, where the greater good is more impactful than merely accumulating additional wealth.

Conclusions

This study examined how framing influences sustainable investment behaviour, focusing on both direct and indirect pathways. Using a sample of 301 participants, the results demonstrate that positive and negative frames operate through different mechanisms. Positive framing directly increased participants’ allocation to green investments, while negative framing worked indirectly by boosting investor confidence, which in turn mediated higher allocations. Furthermore, the moderation analysis revealed that negative framing strengthened the link between investment intention and actual financial commitment, even though the overall effect size of framing on real monetary investment was modest. These findings provide empirical evidence that framing effects in finance are more nuanced than simple gain–loss contrasts and can activate different psychological processes.

From a broader perspective, these results contribute to the behavioural finance literature by demonstrating how cognitive and motivational mechanisms jointly influence sustainable investment decisions. Confidence plays a vital role in transmitting framing effects, while intention interacts with framing to shape more actual funding commitments. For practitioners and policymakers, the findings indicate that message design should be aligned with strategic goals: positive framing might be more effective for immediate engagement, whereas negative framing can be used to reinforce conviction and help motivated investors turn intentions into action. By elucidating the psychological pathways through which framing operates, this study emphasises the importance of combining behavioural nudges with structural incentives to encourage meaningful participation in sustainable finance.

Theoretical Contribution

Our findings indicate that negative framing can be a useful nudging tool to encourage sustainable investment behaviour, especially in a mini simulation. The negative message can alter risk perception, and, through the confidence it engenders, eventually lead to the decision to add funds to the green project. This result contributes to the application of behavioural finance research to sustainable investment behaviour, especially in the face of price volatility. However, the effect does not directly affect behaviour; it will need a mediator, an intervening variable, in the complex process of sustainable investment decisions. Future research could explore other mediators beyond confidence in project success, as we suspect some may help explain the process of sustainable investment decisions beyond our findings.

Managerial Implications

For investment services and financial advisors, the findings underscore the importance of tailoring communication strategies to client psychology. Positive framing can be employed to encourage immediate engagement with sustainable products, making it an effective tool in client acquisition or when introducing new green investment offerings. Conversely, negative framing is particularly valuable in deepening commitment among clients who already display strong pro-sustainability intentions, as it enhances confidence and strengthens the link between intention and behaviour. Advisors should therefore segment their clients not only by financial profile but also by motivational orientation, using positive messages to nudge hesitant investors and negative, loss-focused narratives to reinforce conviction among those with established sustainability goals. By aligning framing strategies with client psychology, financial advisors can more effectively guide investors toward consistent and meaningful participation in sustainable finance.

Limitations and Future Research Improvement

While this study offers new insights into how framing influences sustainable investment behaviour, several limitations should be acknowledged. First, a significant limitation of our design is that the neutral condition lacks an explicit probability statement. In contrast, both positive and negative messages specify a 50% chance of success or failure. As a result, the neutral and framed conditions are not directly comparable in terms of the information they convey. To address this, our main conclusions about framing effects are drawn from the contrast between the positive and negative conditions, which keep the objective probability constant and only vary the message’s evaluative valence. The neutral condition serves as a descriptive baseline and for exploratory analyses. Future research could include a neutral message that clearly states a 50% probability without valence, allowing for a clearer separation between information and framing effects.

Second, the experiment relied on a controlled setting with relatively short-term decision horizons, which may not fully capture the complexity of real-world investment contexts. Third, although confidence and intention were examined as key mechanisms, other psychological or social factors, such as risk perception, trust, and moral preferences, were not explicitly modelled. Finally, the measure of actual green investment was based on limited endowment stakes, which may underestimate the challenges investors face when committing substantial personal wealth; in this area, a qualitative study might be more powerful.

Future research could address these limitations in several ways. Field studies with real financial stakes over longer horizons would provide stronger external validity and clarify whether framing effects persist in market environments. Importantly, future work should also integrate altruistic motives as a core explanatory variable. Altruism is a strong driver of sustainable and prosocial investment, and its interaction with framing and confidence may help explain why some investors remain committed even when financial returns are uncertain. Examining how altruistic preferences interact with cognitive mechanisms, such as confidence, and motivational factors, like intention, could offer a richer understanding of sustainable finance behaviour. Additionally, cross-cultural comparisons and the use of longitudinal data would help assess the stability of these effects across contexts and over time.

References

- Anand, P.; Cowton, C.J. “The ethical investor: Exploring dimensions of investment behaviour”. Journal of Economic Psychology 1993, Vol. 14(No. 2), 377–385. [Google Scholar] [CrossRef]

- Aruga, K. “Are retail investors willing to buy green bonds? A case for Japan”. Journal of Sustainable Finance & Investment 2025, Vol. 15(No. 2), 388–402. [Google Scholar] [CrossRef]

- Baeckström, Y.; Hauff, J.J.C.; Elliot, V. “Wealthy individuals: Not to be overlooked when thinking ESG investment strategy”. Journal of Financial Transformation 2022, Vol. 56, 110–116. [Google Scholar]

- Cantarella, S.; Hillenbrand, C.; Brooks, C. “Do you follow your head or your heart? The simultaneous impact of framing effects and incidental emotions on investment decisions”. Journal of Behavioral and Experimental Economics 2023, Vol. 107, 102124. [Google Scholar] [CrossRef]

- Casady, C.B.; Monk, A. “The logic of net zero investment portfolios: positioning long-term investors for financial outperformance”. Journal of Sustainable Finance & Investment 2025, 1–27. [Google Scholar] [CrossRef]

- Choi, S.I.; Zhang, J.; Jin, Y. “The effects of threat type and gain–loss framing on publics’ responses to strategic environmental risk communication”. In Corporate Communications; Emerald Publishing, 2023; Vol. 28, No. 3, pp. 363–380. [Google Scholar] [CrossRef]

- Courtenay, P.; Taffler, R.; Baeckström, Y. “What do wealthy clients really want from their financial advisors?”. Review of Behavioral Finance 2025, Vol. 17(No. 4), 625–641. [Google Scholar] [CrossRef]

- Daugaard, D.; Kent, D.; Servátka, M.; Zhang, L. “Optimistic framing increases responsible investment of investment professionals”. Scientific Reports 2024, Vol. 14(No. 1), 583. [Google Scholar] [CrossRef] [PubMed]

- Dufwenberg, M.; Gächter, S.; Hennig-Schmidt, H. “The framing of games and the psychology of play”. Games and Economic Behavior 2011, Vol. 73(No. 2), 459–478. [Google Scholar] [CrossRef]

- Florence, E.S.; Fleischman, D.; Mulcahy, R.; Wynder, M. “Message framing effects on sustainable consumer behaviour: a systematic review and future research directions for social marketing”. In Journal of Social Marketing; Emerald Publishing, 12 October 2022. [Google Scholar] [CrossRef]

- Garg, A.; Goel, P.; Sharma, A.; Rana, N.P. “As you sow, so shall you reap: Assessing drivers of socially responsible investment attitude and intention”. In Technological Forecasting and Social Change; Elsevier Inc., 2022; Vol. 184. [Google Scholar] [CrossRef]

- Gutsche, G.; Wetzel, H.; Ziegler, A. “Determinants of individual sustainable investment behavior—A framed field experiment”. Journal of Economic Behavior & Organization 2023, Vol. 209, 491–508. [Google Scholar] [CrossRef]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, Third Edition.; Little, T.D., Ed.; Guilford Press: New York, 2022. [Google Scholar]

- van der Heijden, E.; Klein, T.J.; Müller, W.; Potters, J. “Framing effects and impatience: Evidence from a large scale experiment”. Journal of Economic Behavior & Organization 2012, Vol. 84(No. 2), 701–711. [Google Scholar] [CrossRef]

- Hervé, F.; Marsat, S. “Acting for good, being good or feeling good? Exploring factors influencing individual investors’ willingness to invest in green funds”. Finance Research Letters 2024, Vol. 67, 105736. [Google Scholar] [CrossRef]

- Jäger, A.K.; Weber, A. “Increasing sustainable consumption: message framing and in-store technology”. In International Journal of Retail and Distribution Management; Emerald Group Holdings Ltd., 2020; Vol. 48, No. 8, pp. 803–824. [Google Scholar] [CrossRef]

- Jiao, P. “Belief in Mean Reversion and the Disposition Effect: An Experimental Test”. Journal of Behavioral Finance, Institute of Behavioral Finance 2017, Vol. 18(No. 1), 29–44. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. “Prospect Theory: An Analysis of Decision under Risk”. Econometrica 1979, Vol. 47(No. 2), 263–292. [Google Scholar] [CrossRef]

- Kiky, A. “Ellsberg Paradox and Disposition Effect”. Journal of Resilient Economies (ISSN: 2653-1917) 2025, Vol. 5(No. 1). [Google Scholar] [CrossRef]

- Kiky, A.; Atahau, A.D.R.; Mahastanti, L.A.; Supatmi, S. “Framing effect and disposition effect: investment decisions tools to understand bounded rationality”. Review of Behavioral Finance 2024, No. 5, 883–903. [Google Scholar] [CrossRef]

- Kim, Y.; Chon, M.G. “Exploring effects of message framing on supportive behaviors toward environmental corporate social responsibility”. In Corporate Communications; Emerald Group Holdings Ltd., 2022. [Google Scholar] [CrossRef]

- Kühberger, A.; Schulte-Mecklenbeck, M.; Perner, J. “The Effects of Framing, Reflection, Probability, and Payoff on Risk Preference in Choice Tasks”. Organizational Behavior and Human Decision Processes 1999, Vol. 78(No. 3), 204–231. [Google Scholar] [CrossRef]

- Liu, Y.; Wang, M.; Yang, X. “Earnings optimism in green stocks”. Journal of Sustainable Finance & Investment 2025, Vol. 15(No. 2), 319–341. [Google Scholar] [CrossRef]

- Lobão, J. “Are green asset prices efficient? Evidence from a seasonal anomalies approach”. Journal of Sustainable Finance & Investment 2025, Vol. 15(No. 2), 342–364. [Google Scholar] [CrossRef]

- Mark, G.; Iqbal, S.T.; Czerwinski, M.; Johns, P.; Sano, A. “Neurotics Can’t Focus”. In Proceedings of the 2016 CHI Conference on Human Factors in Computing Systems; ACM: New York, NY, USA, 2016; pp. 1739–1744. [Google Scholar] [CrossRef]

- Mehta, P.; Singh, M.; Mittal, M. “It is not an investment if it is destroying the planet: A literature review of socially responsible investments and proposed conceptual framework”. In Management of Environmental Quality: An International Journal; Emerald Group Holdings Ltd., 13 March 2020. [Google Scholar] [CrossRef]

- Menon, P.; Roy, R.; Ramachandran, G.; Roy, R. “Enhancing effectiveness of public service advertisements: the role of mortality salience and negative message framing”. Marketing Intelligence & Planning 2025. [Google Scholar] [CrossRef]

- Negash, Y.T.; Rizaldy, H.; Rehman, S.U. “Gen Z’s willingness to pay for carbon offset in the fast fashion industry: regulatory focus and sustainability adapted value belief norms perspectives”. In Management of Environmental Quality; Emerald Publishing, 2025; Vol. 36, No. 5, pp. 1190–1207. [Google Scholar] [CrossRef]

- Paulsy, L.; M.L., M. “Why do investors prefer sustainability? A bibliometric review and research agenda”. In Vilakshan—XIMB Journal of Management; Emerald, 2025; Vol. 22, No. 1, pp. 133–157. [Google Scholar] [CrossRef]

- Piñon, A.; Gambara, H. “A meta-analytic review of framing effect: risky, attribute and goal framing”. Psicothema 2005, Vol. 17, 325–331. [Google Scholar]

- Raut, R.K. “Past behaviour, financial literacy and investment decision-making process of individual investors”. In International Journal of Emerging Markets; Emerald Group Holdings Ltd., 2020; Vol. 15, No. 6, pp. 1243–1263. [Google Scholar] [CrossRef]

- Richardson, B.J. “From fiduciary duties to fiduciary relationships for socially responsible investing: responding to the will of beneficiaries”. In Journal of Sustainable Finance & Investment; Taylor & Francis, 2011; Vol. 1, No. 1, pp. 5–19. [Google Scholar] [CrossRef]

- Rossolini, M.; Pedrazzoli, A.; Ronconi, A. “Greening crowdfunding campaigns: an investigation of message framing and effective communication strategies for funding success”. In International Journal of Bank Marketing; Emerald Group Holdings Ltd., 2021; Vol. 39, No. 7, pp. 1395–1419. [Google Scholar] [CrossRef]

- Siemroth, C.; Hornuf, L. “Why Do Retail Investors Pick Green Investments? A Lab-in-the-Field Experiment with Crowdfunders”. Journal of Economic Behavior & Organization 2023, Vol. 209, 74–90. [Google Scholar] [CrossRef]

- Sivaramakrishnan, S.; Srivastava, M.; Rastogi, A. “Attitudinal factors, financial literacy, and stock market participation”. In International Journal of Bank Marketing; Emerald Group Publishing Ltd., 2017; Vol. 35, No. 5, pp. 818–841. [Google Scholar] [CrossRef]

- Stadlthanner, K.A.; Andreu, L.; Font, X.; Ribeiro, M.A.; Currás-Pérez, R. “How environmental gain messages affect cause involvement, attitude and behavioural intentions: the moderating effects of CSR scepticism and biospheric values”. In Corporate Communications; Emerald Publishing, 2022; Vol. 27, No. 4, pp. 781–799. [Google Scholar] [CrossRef]

- Tversky, A.; Kahneman, D. “Judgment under uncertainty: Heuristics and biases”. Science 1974, Vol. 185(No. 4157), 1124–1131. [Google Scholar] [CrossRef]

- Tversky, A.; Kahneman, D. “The Framing of Decisions and the Psychology of Choice”. Science 1981, Vol. 211(No. 4481), 453–458. [Google Scholar] [CrossRef]

- Wilkie, D.C.H.; Rao Hill, S.; Silva, R.A.; Mirzaei, A. “Survival of the greenest: how evolutionary motives affect sustainability campaign message persuasiveness”. In European Journal of Marketing; Emerald Publishing, 2024; Vol. 58, No. 12, pp. 2705–2731. [Google Scholar] [CrossRef]

- Yanuarti Loebiantoro, I.; Hooi Cheng, E.; Annuar, N. “Smart investing: Unveiling key drivers of strategic investment for investors in the Indonesia Stock Exchange”. Investment Management and Financial Innovations 2024, Vol. 21(No. 4), 156–169. [Google Scholar] [CrossRef]

- Zhang, X.; Huang, C.-H. “Investor characteristics, intention toward socially responsible investment (SRI), and SRI behavior in Chinese stock market: The moderating role of risk propensity”. Heliyon 2024, Vol. 10(No. 14), e34230. [Google Scholar] [CrossRef] [PubMed]

- Zunckel, C.; Pillay, P.; Drummond, M.H.; Rosenstein, D. “Advertising to reduce meat consumption: positive framing versus negative framing effects on attention”. Journal of Social Marketing 2023, Vol. 13(No. 4), 609–630. [Google Scholar] [CrossRef]

Figure 3.

The price pattern in the experiment. Source(s): Authors’ work.

Figure 4.

Sample distribution between group A, B, and C. Source(s): Authors’ work.

Figure 5.

Visualisation of the mediation analysis on PROP. Source(s): SPSS PROCESS MACRO output by Andrew F HAYES.

Figure 5.

Visualisation of the mediation analysis on PROP. Source(s): SPSS PROCESS MACRO output by Andrew F HAYES.

Figure 6.

Visualisation of moderation analysis on G_INV. Source(s): SPSS PROCESS MACRO output by Andrew F Hayes.

Figure 6.

Visualisation of moderation analysis on G_INV. Source(s): SPSS PROCESS MACRO output by Andrew F Hayes.

Table 1.

Research variables operationalisation.

| Variables | Definition | Measurement |

| Sustainable Investment Behavior (SIB) | The decision to add funds for a sustainable green project. | For the first three hypotheses: The proportion of the transacted value compared with the available funds or assets. The positive sign will be applied for an added fund transaction, while the negative sign will be used for a selling transaction. Added fund to SRIX decisions = + transaction value / available funds to transact Selling SRIX decisions = - transaction value / available assets to transact PROP = average transaction proportion of four decisions points For the fourth hypothesis: The proportion of real funds invested in the Tzu Chi Foundation relative to the final asset value. Fund invested ratio (G_INV) = fund invested / final asset value |

| Investors’ Confidence (CONF) | The level of confidence that the green project will be successful in the future. |

Confidence percentage (%) in the success rate of the SRIX green project. CONF = average confidence rate of four decisions points |

| Investors’ Green Investment Intention (INT) | The investors’ intention to invest in a green recycling project (Raut, 2020). | Six questions about investors’ intention to fund the green project were measured using five Likert scales, which cover:

|

| Framing Effect (FE) | The difference in the framed message received by participants in the experimental setting. Positive framing: a sustainability message that emphasises positive impacts on future environmental outcomes, contingent on project success. Negative framing: a sustainability message that emphasises the negative (loss) on future environmental impacts, conditional on project failure due to insufficient funds. |

Neutral group A “You are entering the decision points, please decide whether you will add some funds or sell SRIX” Positive framing group B “If you were to add funding to SRIX, there is a 50% chance that this project will succeed and contribute to creating a better environment for your children and grandchildren” Negative framing group C “If you were selling SRIX, there is a 50% chance that this project will fail and destroy the ecosystem that might threaten the survival of your children and grandchildren” This study employs a sequential (multicategory) coding approach for the framing effect to account for the three experimental conditions (control, positive framing, and negative framing). By using this specification in PROCESS, the model generates separate contrasts (X1 and X2) that enable direct comparison between control and positive frames, as well as between positive and negative frames. This approach allows for a more nuanced understanding of how different framing types influence confidence and investment behaviour beyond a simple binary treatment. |

Source(s): Authors’ work.

Table 2.

T-Test for each group of observations.

| Group Comparison | Mean | S Dev | N | Mean Difference | t-test | p-value |

| Sustainable Investment Behaviours (PROP) | ||||||

| Neutral | 0.291 | 0.368 | 96 | |||

| Positive | 0.347 | 0.360 | 102 | |||

| Negative | 0.420 | 0.311 | 103 | |||

| Positive vs Neutral | 0.057 | 1.093 | 0.276 | |||

| Negative vs Neutral | 0.129 | 2.678 | 0.008** | |||

| Negative vs Positive | 0.072 | 1.544 | 0.124 | |||

| Sustainable Investment Behaviours (G_INV) | ||||||

| Neutral | 0.293 | 0.296 | 96 | |||

| Positive | 0.259 | 0.198 | 102 | |||

| Negative | 0.309 | 0.277 | 103 | |||

| Positive vs Neutral | -0.034 | -0.950 | 0.344 | |||

| Negative vs Neutral | 0.016 | 0.390 | 0.696 | |||

| Negative vs Positive | 0.050 | 1.492 | 0.137 | |||

* p < 0.05, ** p < 0.001. Source(s): Authors’ work.

Table 3.

ANOVA effect size result between the control, positive, and negative groups.

| Variables | η2 | F (p) |

| CONF | 0.022 | 3.344 (0.037)* |

| PROP | 0.023 | 3.473 (0.032)* |

| G_INV | 0.007 | 0.993 (0.372) |

* p < 0.05, ** p < 0.001. Source(s): Authors’ work.

Table 4.

OLS regression results for investor confidence and sustainable investment behaviour.

| Variables | CONF | PROP |

| X1 = Positive vs Neutral | 0.0096 | 0.4054 |

| (0.000)** | (0.0071)* | |

| X2 = Negative vs Positive | 0.0515 | -0.1210 |

| (0.0408)* | (0.4481) | |

| CONF | 0.8651 | |

| (0.000)** | ||

| Constant | 0.6041 | -0.2320 |

| (0.000)** | (0.0102)* | |

| Observation (N) | 301 | 301 |

| R2 | 0.0219 | 0.1229 |

Notes: Columns report ordinary least squares (OLS) estimates with heteroskedasticity-consistent (HC4) standard errors. The dependent variable in column (1) is investor confidence (CONF), and in column (2) is sustainable investment behaviour (PROP), measured as the average proportion of added funds during the simulation. Framing is coded using sequential contrasts, where X1 compares positive framing with the neutral condition, and X2 compares negative framing with positive framing; the neutral condition serves as the base category. * p < 0.05, ** p < 0.001. Source(s): Authors’ work.

Table 5.

OLS-based mediation analysis of framing effect on sustainable investment behaviour.

| Indirect effect | Effect | BootSE | LLCI | ULCI |

| X1 = Positive vs Neutral -> CONF -> PROP | 0.0027 | 0.0089 | -0.0157 | 0.0223 |

| X2 = Negative vs Positive -> CONF -> PROP | 0.0284* | 0.0162 | 0.0011 | 0.0644 |

Notes: Indirect effects are estimated using OLS-based mediation analysis implemented via the PROCESS macro for SPSS (Model 4) with 5,000 bootstrap resamples. CONF denotes investor confidence, and PROP denotes sustainable investment behaviour measured as the average proportion of added funds. Framing is coded using sequential contrasts, with the neutral condition as the base category. CI that does not include zero indicates significant mediation. Source(s): Authors’ work.

Table 6.

OLS regression results for investor intention and sustainable investment behaviour.

| Variables | G_INV |

| INT | 0.014 |

| (0.063) | |

| W1 = Positive vs Control | 0.043 |

| (0.814) | |

| W2 = Negative vs Positive | -0.287 |

| (0.023)* | |

| INT x W1 | -0.004 |

| (0.627) | |

| INT x W2 | 0.015 |

| (0.010)* | |

| Constant | 0.001 |

| 0.995 | |

| Observation (N) | 301 |

| R2 | 0.097 |

Notes: Columns report ordinary least squares (OLS) estimates with heteroskedasticity-consistent (HC4) standard errors. The dependent variable in column (1) is real invested fund (G_INV), measured as the proportion invested fund compared with available incentives. Framing is coded using sequential contrasts, where W1 compares positive framing with the neutral condition, and W2 compares negative framing with positive framing; the neutral condition serves as the base category. * p < 0.05, ** p < 0.001. Source(s): Authors’ work.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.