Submitted:

22 January 2026

Posted:

23 January 2026

You are already at the latest version

Abstract

This paper examines the connection between Environmental, Social, and Governance (ESG) factors and the risk of geopolitics, as defined by the Geopolitical Risk (GPR) index. The concept of geopolitical risk is conventionally defined as the direct result of political incidents, war, and international tensions. The current study argues that the concept should be understood in a more structural and sustainable manner, relating to the underlying forces driving geopolitical risk. The main research question is whether and how the three pillars of the ESG factors contribute to the explanation and understanding of cross-country and over-time variations in geopolitical risk. In an effort to avoid the information losses associated with the aggregate nature of the ESG index, the three factors are considered separately and the three pillars are analyzed individually. The empirical context is a balanced cross-country panel data set including 42 countries over the 2000-2023 time period. The data for the three factors is obtained from the World Bank dataset in an effort to standardize and compare the data in a cross-country and cross-time manner. The GPR index is used to measure the level of geopolitical risk and is defined by Dario Caldara and Matteo Iacoviello. The GPR index captures the level of geopolitical tensions based on the analysis of media signals. The combination of the three sources allows for the direct connection and correlation between the three factors and the internationally recognized GPR index. The paper uses an integrated methodological approach that combines the results from three different approaches. The first method uses panel data analysis in an effort to identify the average marginal effects while controlling for unobserved heterogeneity. The second method uses the technique of clustering in an effort to identify structural patterns and divide the countries into groups based on their unique characteristics and risk profiles. The third method uses machine learning regressions and nonparametric analysis in an effort to capture the complex relationships and interactions in the data. The three-step method is used for each pillar in an effort to ensure consistency and comparability. The results suggest that the three factors contribute to the GPR index in a unique manner. The environment and energy structure contribute to the GPR index as a risk multiplier, the social factor is related to the exposure to instability, and the governance factor is a central stabilizing factor. The paper makes a unique contribution to the literature by defining the concept of the three factors and their relationship to the GPR index in a unique and sustainable manner.

Keywords:

ESG

; geopolitical risk

; sustainability

; environmental and social factors

; governance quality

1. Introduction

Geopolitical risk is a characteristic of the modern global order and plays a significant role in international politics and economics and in making global investments and development paths. Events of political instability and conflict, international tensions and institutional failures are increasingly impacting global and national economics and finance in a significant way, as is reflected in an emerging literature that treats geopolitical risk as a quantifiable and dynamic phenomenon and not a mere subjective concept (Caldara and Iacoviello, 2022). These types of risk are often manifested in terms of policy uncertainty and confidence shocks and are often accompanied by spillovers in international markets (Caldara et al., 2020). Simultaneously, the concept of Environmental, Social, and Governance (ESG) has also emerged as a holistic framework for country and corporate level sustainability and risk analyses in a world facing climate change and global systemic instability in finance (Bolton et al., 2020; Pedersen et al., 2021). While both concepts of geopolitical risk and ESG are rising in equal measures in global literature and policy discourse, they are largely progressing in parallel channels of research and policy discourse. This paper takes up this gap in literature and research by asking a primary research question: How far can the country-level Environment, Social, and Governance aspects of ESG help in explaining international and temporal variations in country-level geopolitical risk? The need to undertake this research arises from an increasingly acknowledged understanding that geopolitical instabilities are increasingly becoming a result of structural factors such as climate-related pressures, resource constraints, demographic factors, inequality, and a lack of effective governance structures and processes. Environmental degradation and climate change can contribute to increased resource competitions, increased instances of extreme weather events, and increased tensions between different international entities, with far-reaching macroeconomic and political repercussions (Kahn et al., 2021). There is a considerable body of literature that identifies a link between climatic shocks and conflict and political instabilities, and this highlights how environmental factors can become a threat multiplier in a fragile situation (Burke et al., 2015; Ide et al., 2021). Social factors, including inequality, migration pressures, and political polarization, can contribute to instabilities and instigations in a situation, and a lack of effective governance structures reduces a country’s ability and capacity to withstand both internal and external shocks and instabilities. Political economy theories highlight how changes in power and governance structures affect instabilities in a situation (Acemoglu et al., 2011). Governance factors, including rule of law, protection from corruption, and effectiveness in governance structures, are factors that affect political stability and are not new in understanding political stability and macroeconomic factors (Kaufmann et al., 2007). Even though these mechanisms are often analyzed from a qualitative point of view when it comes to strategic assessments, there is a lack of comprehensive evidence on how ESG variables are related to geopolitical risk. The reason behind this is that most studies are focused on treating geopolitical risk as an exogenous factor influencing economic outcomes, or they are focused on individual variables related to corporate governance without integrating them into an ESG framework (Caldara & Iacoviello, 2022). Even when it comes to outcomes on a corporate level, it’s often focused on finance or legal aspects rather than macro-political stability (Wang & Overby, 2022). The originality of this article is that it clearly recasts the concept of geopolitical risk in terms of an outcome that is embedded in sustainability conditions. Instead of focusing on the concept of geopolitical risk in terms of its relationship to conflict events in the international realm, this article recasts ESG factors in terms of structural drivers that determine the vulnerability/resilience of countries to geopolitical risk. This recasting of the concept of geopolitical risk makes it possible to examine this concept in terms of its relationship to the cumulative outcome of environmental factors, societal factors, and governance factors. This article thus seeks to combine two bodies of knowledge that have hitherto been quite unrelated to each other. These two bodies of knowledge that this article seeks to combine relate to the growing body of knowledge that has been focused primarily upon ESG factors in terms of sustainability (Pedersen et al., 2021). The methodological design of the study also makes an innovative contribution. While previous research on this topic has generally used only one empirical methodology, this article uses a multi-method design combining panel econometrics, clustering analysis, and machine learning regression techniques, which captures nonlinear relationships in macro-political risk research in an effective manner. Another innovative aspect of this article is the decomposition of ESG into its three-pillar structure in a systematic manner. While most of the previous research on this topic uses aggregated ESG scores, this article breaks down E, S, and G into separate categories and examines their individual impact on geopolitical risk, which makes it possible to compare the relative weights of climate-related variables, social issues, and institutional factors. In conclusion, the article makes an important contribution to existing literature by presenting a new conceptual and empirical connection between ESG and geopolitical risk. The article presents an integrated approach, breaks down ESG into basic elements, and shifts the focus of geopolitical risk as a result of basic sustainability factors. In doing so, it fills an important gap existing in existing literature while presenting important insights with clear policy implications for risk, sustainability, and geopolitics.

2. Literature Review

Common to these is the understanding that GPR is not only a shock, or exogenous event, but also a structural driver of sustainability, finance, and business behavior. Studies such as Benammar et al. (2026) and Doğan & Zeren (2025) illustrate the role of GPR in increasing ESG-related uncertainty, suggesting that the outcomes of sustainability are extremely sensitive to strategic and political tensions. This is reflected in the panel and machine-learning findings in the attached analysis, suggesting that GPR is the product of underlying conditions rather than a shock. A number of articles, including Boccaletti et al. (2026), Sovbetov (2025), and Sha et al. (2025), use significant geopolitical events, such as the Russia-Ukrainian war or the tensions between China and the USA, to illustrate that ESG performance is asymmetrically affected. This is reflected in the clustering findings in the analysis, in which countries with lower ESG performance are grouped with regimes of higher GPR. Some articles, such as Huo & Shi (2025) and Newaz & Aslam (2025), examine ESG rating disparities and ESG-related instruments, illustrating that GPR leads to greater disparities, volatilities, and portfolio rebalancing. This is reflected in the machine-learning findings, in which non-linear ESG-GPR correlations are identified that may not be observable in traditional models. Articles that examine specific channels, such as climate promises and green bonds (Das et al., 2026), clean energy markets (Akadiri & Özkan, 2026), or innovation and supply chains (Li et al., 2026), illustrate that ESG dimensions have multiple mechanisms. The attached analysis reflects the multidimensionality of the literature in that the E, S, and G dimensions of ESG are examined in separate analysis, illustrating that each ESG pillar drives GPR in distinct, yet related, ways. The literature on ESG-related connectivity and spillovers, such as Abdelkader & Si Mohammed, 2025; Ha, 2025; and Shen et al. 2025, provides robust support for the methodology used in the analysis, namely the use of panel analysis, clustering, and machine-learning. Taken as a whole, the literature provides support for the major finding of the analysis: ESG dimensions are structural, rather than peripheral, determinants of GPR. According to Kuai and Wang (2025), Al Amosh and Khatib (2025), and Cheng et al. (2025), the stronger the geopolitical risk, the weaker the ESG performance, although this effect is nonlinear and conditional on governance, attention, and policies. These findings correspond closely with the panel data estimates in this research, which also reveal governance factors as the strongest stabilizers of geopolitical risk and institutional deficiencies as risk multipliers. Likewise, the estimates in the research correspond with the findings in Xie et al. (2025) and Al-Yafei and Bennasr (2025), which demonstrate the structural economic and institutional mechanisms through which geopolitical risk is an outcome, and not an exogenous constraint on economic performance. On the financial market side, the role of spillovers, higher-order moments, and portfolio diversification in geopolitical risk is emphasized in the works of Karkowska and Urjasz (2025), Cui and Maghyereh (2025), Bajra et al. (2025), and Fabozzi (2025). These works correspond with the machine learning estimates in this research, which also found nonlinear responses and regime-dependent effects of ESG on geopolitical risk. Moreover, the clustering results in this research correspond with these works, which also found that stronger ESG performance in markets and countries is associated with reduced volatility transmission and resilience in geopolitical risk. Some works in this stream of research have extended the focus on sustainability beyond financial and capital markets. Thus, geopolitical risk is shown in the works of Kuzina and Steiner (2025) to suppress progress on the achievement of the SDGs in the supranational framework, while new methods for measuring sustainability in uncertain environments have been proposed in the works of Ma et al. (2025) and Ongan et al. (2025). These works correspond with this research in its methodology, which also decomposed ESG performance into Environmental, Social, and Governance dimensions, rather than using overall indices. Finally, works in this stream of research have emphasized the role of artificial intelligence and machine learning in risk research, such as in the works of Lin et al. (2025), which correspond with this research in its use of machine learning regression techniques, and which also highlight the role of flexible and adaptable methods in research on ESG and geopolitical risk interactions. Taken together, this stream of research reinforces the finding in this research that ESG dimensions have an active role in shaping geopolitical risk, through governance, expectations, and resilience, rather than being passive constraints on economic performance. Some works in this stream of research have emphasized the role of methodological innovation and artificial intelligence in research on risk and sustainability. As Gupta and Yan (2025), Pham (2025), Alam et al. (2025), and Lin et al. (2025) illustrate, large language models, AI analytical tools, and reinforcement learning techniques improve the detection and quantification of new risks. These techniques heavily validate the regression component of the attached analysis, a component using machine learning to identify non-linear correlations between ESG and GPR, beyond the capacities of traditional econometric models. The emphasis on information uncertainty and structural vulnerabilities also corresponds with the study’s definition of geopolitical risk as a result of endogenous processes, defined by expectations and vulnerabilities. There also exist analyses on the topic of resilience and various sectors and assets. Papathanasiou et al. (2025), Fabozzi (2025), and Loukil et al. (2025) examine how diversification, centrality, and cross-asset volatility transmissions function within conditions of extreme uncertainty, further supporting the clustering findings on high-resilience and high-fragility regimes. There also exist analyses on specific sectors, such as those on port sectors by Nagararan et al. (2025), supply chain sectors by Bai et al. (2025), and AI and sustainability sectors by Yu et al. (2025), further supporting the breakdown of ESG into Environmental, Social, and Governance categories, and how these categories expose varying levels of systemic risk. There also exist analyses on the topic of institutions and regulations. Zambelli (2025), Lin (2025), and Matviienko et al. (2025) place a strong emphasis on the need for legal systems, financial regulation, and climate-related banking regulation to reduce risks. These findings also support the panel data findings of the study, in which strong governance was repeatedly shown to be a stabilizing influence on geopolitical risk. Finally, analyses on ethical finance, Islamic risk management, and SDG development further support the study’s findings on sustainability and geopolitical risk, suggesting a deep and abiding link between sustainability and resilience. Taken together, these papers support the study’s major conclusion: ESG factors, when approached using a combination of econometric, clustering, and machine learning techniques, represent a structural, rather than a peripheral, driver of geopolitical risk (Table 1).

3. Methodology: An Integrated ESG-Based Multi-Method Framework for Geopolitical Risk Analysis

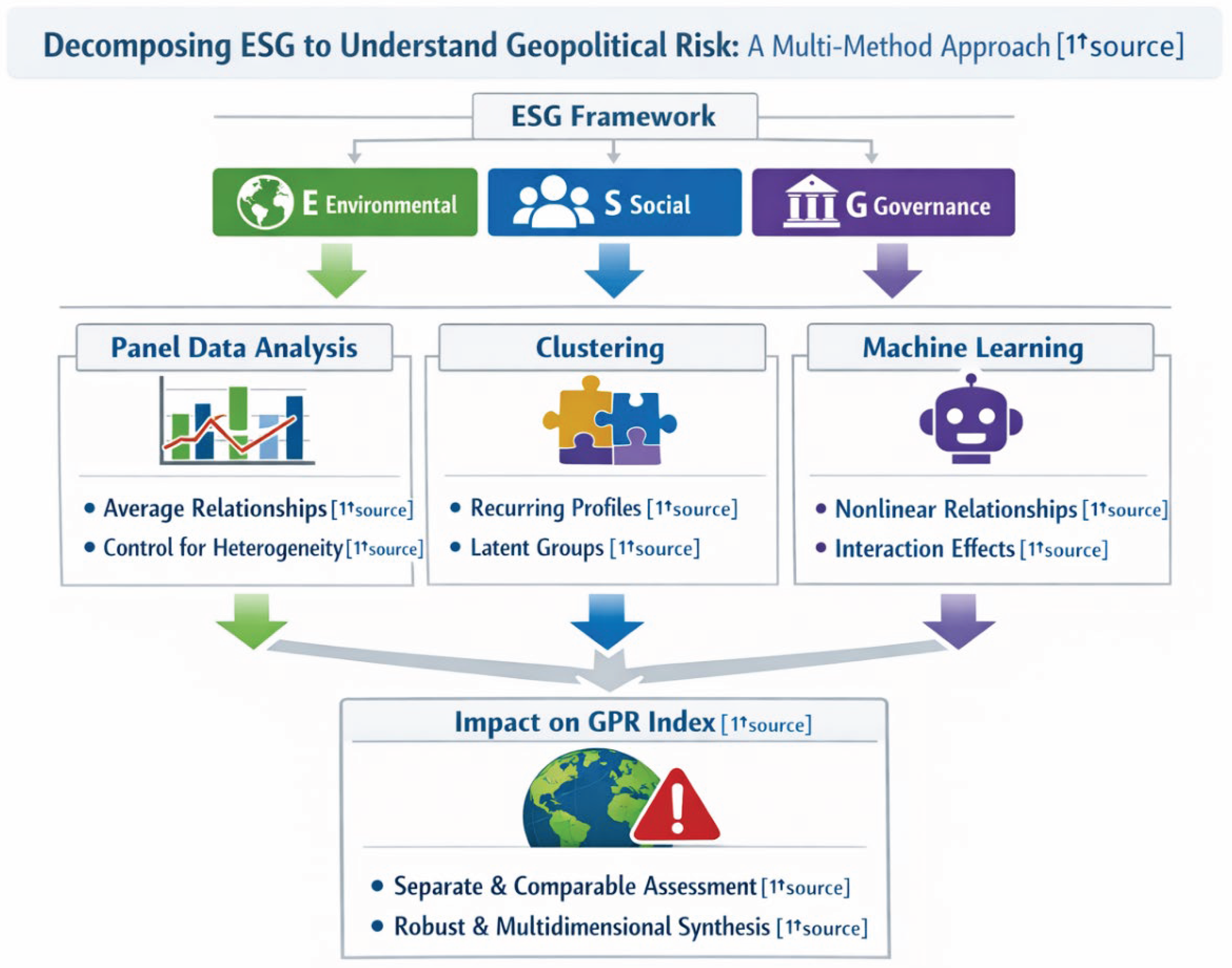

The research follows a methodological approach that clearly breaks down the ESG concept by its three pillars of Environmental (E), Social (S), and Governance (G). This helps to examine the individual effects of each of these ESG aspects in creating geopolitical risk, which is measured by the Geopolitical Risk (GPR) index introduced by Caldara and Iacoviello in 2022. Instead of focusing on ESG as an aggregate measure, this analysis distinguishes among the three factors to enable an individual investigation of each. This is because it has been argued that environmental factors, societal factors, and governance factors affect the creation of geopolitical risk in different channels, to say nothing of their relative strength in this regard, especially in the context of structural changes like climate change (Bolton et al., 2020; Kahn et al., 2021). For each ESG factor, these three steps of the methodology are systematically followed. To begin with, the panel econometric models are estimated to identify the relationships over time as well as across different countries by considering unobserved heterogeneity. This makes it possible to identify the statistically significant relationships that are interpretable from an economic theory point of view. This is similar to the empirical literature that suggests geopolitical risk as a measurable phenomenon that changes over time (Caldara & Iacoviello, 2022). Second, the application of clustering methods helps to uncover the heterogeneity of the underlying structure and the presence of hidden group memberships of countries according to their characteristics related to ESG. Clustering allows the exploration of the interconnections of ESG variables such as environmental vulnerability, social vulnerability, and governance capacity and the levels of geopolitical risks. This approach fits the perception of systemic risks being driven not only by isolated shocks but also through the interconnections of several dimensions of sustainability (Bolton et al., 2020). Thirdly, machine learning regression techniques are utilized to account for nonlinear relationships and patterns that could not be accounted for in econometric models. Such techniques are particularly useful in analyzing heterogeneous and nonlinear responses to environmental and climate-related variables in macroeconomic and political outcomes (Kahn et al., 2021). The approach combines panel data analysis, machine learning regression, and clustering techniques separately applied to each pillar of ESG factors in a manner that compares results while making use of their complementary advantages. In summary, this integrated framework for methodologies provides a holistic and strong evaluation of individual and combined influences of Environmental, Social, and Governance variables in relation to geopolitical risk and going beyond reduced forms to a more sustainability-focused perspective of geopolitical instability. See Figure 1.

4. Environmental ESG Drivers of Geopolitical Risk: Evidence from Panel Models, Clustering, and Machine Learning

This section explores the link between the E dimension of ESG, which stands for Environment, and geopolitical risk, as measured by the Geopolitical Risk Index (GPR). The hypothesis is that, besides being ecological outcomes, environmental conditions represent the structural risk drivers of instability, which can shape climate risk, pollution, resource depletion, as well as energy structure, thereby impacting the magnitude of occurrence of geopolitical risk, as captured by GPR. To test the link between the two, an empirical model is built, which uses the set of E dimension variables as the basis for an explanation of the values of GPR, using a panel of 42 countries between 2000 and 2023. The following subsections fulfill the above aim through three approaches: panel data, which estimates average effects of E dimension variables on GPR; clustering, which identifies groups of countries characterized by similar E dimension patterns, which are associated with varying levels of GPR; finally, machine learning regression, which explores non-linear patterns of interaction between E dimension variables, which would not be captured through traditional regression models.

4.1. Panel Data Evidence on the Environmental (E) Dimension of ESG and Geopolitical Risk

To analyze the relationship between the E-Environment component of the ESG model and the GPR dimension, i.e. geopolitical risk, we estimated the following equation:

Where and .

Specifically, the variables analyzed are described in the following Table 2.

For the analysis, the dependent variable is Geopolitical Risk (GPR) and is captured using the Caldara and Iacoviello (2022) index, which measures the level of geopolitical risk for a country by counting the number of news stories that are conflict-, politically tension-, and institutional instability-related. This approach has made it possible for GPR to be treated as a time-varying and measurable macro-political phenomenon that has significant economic effects (Caldara & Iacoviello, 2022; Caldara et al., 2020). The research will investigate how well the chosen factors are able to explain the differences in GPR levels for a panel data sample of 32 countries for 16-19 years, which will result in a sample size of 600 data points. This is consistent with the growing literature that focuses on the role of climate change, the degradation of the environment, and the structure of the energy system as the source of economic and political instability (Bolton et al., 2020; Kahn et al., 2021). Four different econometric models were estimated: Pooled OLS, Fixed Effects Model, Random Effects Model via GLS, and Weighted Least Squares. This allows for easy robustness checks under different assumptions regarding the nature of heterogeneity and country-specific structural differences. The Hausman test helped select between fixed and random effects models. It produced a p-value of 0.0086 and rejected the null hypothesis of consistency of the GLS estimator. This supported the fixed effects model. The fixed effects model had a very high R-squared of 0.92 under the LSDV model. This suggests that GPR is driven mostly by country-specific variables. However, the R-squared of 0.14 under the fixed effects model suggests a low explanatory power of the variables. The coefficients are comparable under the different models. This suggests that the results are robust. Natural Resource Depletion: The coefficient on Natural Resource Depletion is negative and significant in all models, suggesting that as natural resource depletion increases, geopolitical risk decreases. While this result might seem counterintuitive at first, it could be because resource-exploiting countries tend to adopt rent-based economies, which in turn might suppress political instabilities in the short run, as per political economy theories on resource rent and stability. The electricity from coal has a positive significant coefficient, meaning that higher dependence on coal to produce electricity is associated with higher GPR, which suggests vulnerability to systemic fragility. This implies that countries dependent on fossil fuels are vulnerable to global shocks, global decarbonization, or conflicts related to energy resources (Bolton et al., 2020). Methane emissions appear as one of the most significant factors, and they have a positive and highly significant coefficient in all models. An increase in methane emission could also indicate an unsustainable development trend, which could lead to social unrest, health issues, and climate change, all of which could contribute to an increase in geopolitical risk. This could also be linked to the fact that environmental stress and emission have been found to contribute to economic and political instability (Kahn et al., 2021; Miah et al., 2021). Safe Drinking Water also has a positive and significant coefficient. Care should be exercised in interpreting this result, since availability of safe water is usually a proxy for development, though in some cases it may be related to rapid urbanization and population concentration, which in institutionally weak environments may produce a different type of inequality and conflict dynamics (Böhmelt et al., 2014). Results for Renewable Energy Consumption are mixed, as it is positive in the Random Effects, Fixed Effects, and Random & Fixed Effects models, but negative in the Pooled OLS and Weighted Least Squares models. This volatility could be an indicator of endogeneity, as there might be correlation between Renewable Energy Consumption and country-specific effects. In the more accurate models, the positive sign may be an indicator of the fact that the transition process, especially during the initial stages, is associated with transition costs, which increase political uncertainties, as discussed by Bolton et al. (2020). Tree Cover Loss has a positive and significant coefficient, which means that deforestation is positively related to geopolitical risk. This is supported by literature that connects the degradation of the environment, rural livelihoods, and land use conflicts, especially in environments with low adaptive capacity (Burke et al., 2018). The fixed effects model has a strong explanatory ability, but there are a number of econometric issues that need to be noted. The White test for heteroskedasticity and the Wald test both reject the null hypothesis of homoskedasticity of the residuals, suggesting the presence of heteroskedasticity of residuals across countries. The Pesaran CD tests show the presence of cross-section dependence, suggesting the presence of cross-country spillovers in the sense that the shock in one country can spill over into other countries, which can be true in the sense of global geopolitical risks associated with the global energy markets (Pesaran & Tosetti, 2011). The Wooldridge test suggests the presence of first-order autocorrelation, while the tests for In sum, the findings of the analysis demonstrate that the role of environmental and energy-related dynamics is a crucial determinant of GPR. While the use of coal, methane emissions, and the destruction of forests are related to GPR, the relationship between GPR and the use of natural resources is much more complex and may be mediated by institutional and economic mechanisms. The relationship between the energy transition and GPR is not one-dimensional and may be contingent on various country-specific factors and adjustment costs. The findings of the analysis provide evidence that the role of environmental policy is not limited to its relationship with the environment, as the increasing relevance of environmental disasters to financial and geopolitical risk is well established in the literature, including the role of climate change in shaping global economic policy, including the prevention of global conflicts, as established in Caldara et al. (2020) and Pankratz et al. (2023). In addition, despite the econometric challenges of heteroscedasticity, cross-sectional dependence, and the possibility of endogeneity, the analysis provides clear evidence that the role of environmental sustainability is a structural determinant of GPR and should be mainstreamed in the strategies of policymakers seeking to contribute to long-term GPR. See Table 3.

4.2. Environmental Risk Regimes and Geopolitical Risk: A Clustering-Based Assessment

The choice of the most appropriate clustering algorithm must be based on a balanced evaluation of several performance indicators, since each metric captures a different aspect of clustering quality (Arbelaitz et al., 2013). In this comparison, all indicators have been normalized so that higher values always correspond to better performance, allowing a coherent cross-algorithm assessment. Among these indicators, particular attention is devoted to the HH index, which measures concentration and balance in cluster sizes and is especially relevant when interpretability and representativeness of clusters are important. Hierarchical clustering clearly stands out in terms of internal cohesion and separation. It achieves the maximum normalized score for minimum separation, Pearson’s γ, Dunn index, and entropy, and also performs very well on the Calinski–Harabasz index. These results indicate that hierarchical clustering produces well-separated and compact clusters with high structural quality (Arbelaitz et al., 2013). However, its HH index is equal to zero, signaling a very high concentration of observations in a small number of clusters. This severe imbalance reduces the practical usefulness of the solution, especially when the objective is to obtain clusters of comparable size or to avoid dominance by a few large groups. K-Means also shows excellent performance on some classical validity indices, particularly Pearson’s γ and the Calinski–Harabasz index, where it reaches the maximum normalized value. Nevertheless, its HH index is extremely low, indicating strong concentration and limited balance in cluster sizes. This makes K-Means less suitable in contexts where cluster size homogeneity is a priority. Density-based methods display the opposite profile. While they perform weakly on separation and compactness metrics, they achieve the maximum score on the HH index. This indicates a very balanced distribution of observations across clusters, which is a desirable property when the goal is to avoid overrepresentation and ensure interpretability; moreover, density-based clustering frameworks are explicitly designed to capture heterogeneous structures and distinguish clusters from noise (Campello et al., 2015). However, the poor performance on most quality indices suggests limited overall clustering structure. Random Forest–based clustering emerges as the most balanced solution. It does not dominate in any single metric, but it consistently performs well across all indicators and shows a high HH index, second only to the density-based approach. This implies a good compromise between cluster quality and size balance. More broadly, machine learning approaches are often preferred in applied settings when the underlying relationships are complex and potentially nonlinear, as they can enhance robustness and discriminative power across high-dimensional feature spaces (Martínez Torres et al., 2019). Considering all indicators jointly, and giving particular weight to the HH index, Random Forest appears to be the most appropriate algorithm, as it provides a robust trade-off between structural quality and balanced cluster composition. See Table 4.

This analysis endeavors to assess the role of variables included in the Environment dimension of ESG ratings on the explanation of geopolitical risk, as captured by the Geopolitical Risk (GPR) index. In grouping countries into clusters using a broad set of data on the environment, energy, climate, and natural resources, the analysis allows for the determination of persistent patterns of the environment, which correspond with levels of geopolitical risk. In this context, the Geopolitical Risk is understood not as an exclusively political phenomenon but as a phenomenon influenced by pressures of the environment, energy patterns, as well as climate exposure, consistent with the view that climate shocks have the role of systemic risk multipliers (Bolton et al., 2020; Kahn et al., 2021). Those with higher GPR values (such as clusters 1, 3, 5, 6, and 7) are likely to reflect a set of undesirable environmental factors. These are likely to be associated with high emissions of CO₂, methane, and the use of fossil fuel or coal-based power. In some cases, these are also likely to be associated with high Cooling Degree Days, Heat Index values, or energy intensity, reflecting a high degree of climate stress. This is consistent with the idea that environmental degradation and climate stress are associated with geopolitical instability in that these factors increase costs, tensions, and reliance on foreign energy sources (Bolton et al., 2020; Kahn et al., 2021). Further information on emissions dynamics is that energy shocks and emissions-intensive structures of production can be associated with economic and political stress (Şahin & Chen, 2023). Resource depletion indicators are also important for the differentiation of clusters. Losses of adjusted savings because of natural resource depletion or forest depletion are regularly found to be higher for clusters that have a higher GPR, implying that mismanagement of natural resources can impact negatively upon resilience as well as geopolitical risk. Similarly, Tree Cover Loss as well as a decrease in the area covered by forests is regularly found to be higher for clusters that have a higher geopolitical risk, as land degradation or deforestation can lead to increased conflict over natural resources as well as livelihoods (Burke et al., 2018). On the other hand, the probability of having less favorable environments would be associated with the lower or negative GPR value countries (e.g., countries 2 and 8). These countries would generally display a positive performance in terms of access to clean fuels and electricity, lower emissions intensity, and a higher share of renewable energy consumption/output. They would also display a lower level of pollution, such as PM2.5, along with a strong performance in the indicators related to the use of water, namely access to a safely managed drinking water source and sanitation facility. From the ESG point of view, these factors would denote a strong performance in terms of environmental sustainability, which would be associated with a low probability of having a geopolitical risk (Bolton et al., 2020). Also, the indicators of climate variability and water stress add more evidence for the above analysis. The regions that have higher levels of water stress, freshwater abstraction, and SPEI are more likely to be linked with higher levels of GPR. Water scarcity and climate conditions are structural risk multipliers that increase the level of resource competition and the chances of conflict both domestically and internationally. The existence of such regions in the higher levels of GPR adds evidence for the significance of environmental conditions as drivers for geopolitical events, as discussed in the literature on the relationship between conflict and cooperation and water (Böhmelt et al., 2014). The energy structure is seen as a significant channel in particular. The reliance on fossil fuels, electricity generated by coal, and energy imports is more prominent in clusters that are highly dependent on GPR, while those that are more reliant on renewable energy are associated with a low level of geopolitical risk. This is in line with the ESG framework where the Environment pillar focuses heavily on energy transition and its importance in terms of mitigation and adaptation to climate change but also in terms of minimizing reliance on global shocks and geopolitics (Bolton et al., 2020; Şahin and Chen, 2023). On the whole, the outcome of the cluster analysis indicates that the Environmental factor in the ESG is strongly related to GPR. Nations under strong environmental pressure, having inefficient energy resources, and being climate change vulnerable are more GPR-prone. The opposite is true for nations enhancing their environment, resource sustainably managed, and advancing in the clean energy transition. The result confirms the strategic importance of environmental sustainability for GPR and the relevance of including environment factors in the GPR model as explanatory variables (Kahn et al., 2021). Table 5.

This analysis uses the Environmental, Social, and Governance (ESG) approach, focusing specifically on the role of the Environmental (E) aspect in relation to geopolitical risk as defined by the Geopolitical Risk (GPR) index. The importance of the individual environmental variables in the explanation of the GPR index can be understood from the mean decrease in the Gini importance, which highlights the role of the environmental variables in the explanation of the GPR index rather than focusing on the direct relationships of the variables. The most important variables in the explanation of the GPR index are related to climate and temperature variables: Heating Degree Days (HDD), Land Surface Temperature (LST), Cooling Degree Days (CDD), and Energy Use per capita (ENU) rank among the highest variables. The results of the analysis imply the importance of the vulnerability of the environment to climate and temperature factors in the explanation of the GPR index, suggesting the vulnerability of the regions to climate and temperature factors, which are also characterized by increased requirements for energy in terms of heating and cooling, indicating increased structural pressures in terms of the infrastructure, financial, and energy sectors of the regions, which can be reflected in increased geopolitical risk vulnerability. The results of the analysis, from the ESG aspect, imply the importance of climate vulnerability in the explanation of political risk, which suggests a direct link to political risk factors, indicating the importance of climate vulnerability in the explanation of political risk factors, which support the idea of the role of weather and climate factors in the explanation of economic and social risk factors (Dong & Tremblay, 2021; Carleton & Hsiang, 2016). Energy-related factors also appear prominently. Energy imports (ENI), energy intensity (EINT), electricity from coal (ECOA), fossil fuel consumption (FOS), and renewable energy consumption (REN) appear prominently. This helps to reinforce the idea that energy systems and their efficiencies represent basic channels of transmission of environmental performance to geopolitical risk. High levels of energy imports and fossil fuel use increase risk vulnerability to global risk sources, while inefficient use of energy adds to environmental pressures. The prominence of renewable energy factors suggests that the issue of the energy transition has become increasingly important in terms of both environmental impacts and geopolitics, in accordance with the strategic-political economy approaches to climate/green transformation (Saidin & O'Neill, 2022). Depletion and land-use indicators: natural resource depletion (NRD), tree cover loss (TCL), forest area (FOR), and agricultural land (AGL) are also highly ranked. This is evidence that unsustainable use of natural capital can weaken resilience and heighten geopolitical risk through increased competition for land, food, and ecological services. The weight for agriculture, forestry, and fishing value added (AFF) supports the importance of resource-based economic systems to resilience to environmental and geopolitical shocks, as seen by evidence of relationships between environmental pressure, biocapacity, and economic resilience (Nathaniel, 2021). The water-related indicators are an integral part of this framework and include annual water withdrawal (WAT), water stress (WSTR), safely managed drinking water (SMDW), sanitation (SMSS), and water quality (WQG). The importance of water scarcity and mismanagement as a risk multiplier and potential cause of social unrest, international conflict, and instabilities in a region underlines its relevance in GPR and supports the hypothesis that water security and sustainability are inextricably intertwined and carry direct geopolitical significance in regions prone to climate change and instabilities in governance. Indicators of pollution and emissions such as CO2, CH4, N2O, and PM2.5 air pollution also carry significant weight in this context. These variables address not only climate change externalities but also damages to the local environment that may impact health, efficiency, and stability in social and economic terms. This significance further underscores that not only climate change, but overall degradation in the environment, is a component of geopolitical risk in a variety of ways. On the whole, the results for the feature importances offer strong empirical support for the relevance of the Environmental pillar of ESG as a whole for the explanation of geopolitical risk. GPR is clearly associated with climate change, the structure of the energy system, resource depletion, water scarcity, and overall pollution. The fact that some variables have a less strong explanatory power does not mean that they are irrelevant, but that they could be drivers of GPR along paths and processes that are difficult to distinguish from the paths and processes for other types of risk, at least in the short term, while they could be distinguished over the medium and longer term. What the study clearly shows, however, is that the consideration of environmental factors and sustainability issues is a must for the understanding of geopolitical risk as a whole. The Environmental pillar of ESG clearly represents a key element for the explanation of GPR, and confirms the idea that climate change, resource management, and the energy transition, and more generally the environmental issues, represent the foundation for the building of geopolitical resilience and stability. Table 6.

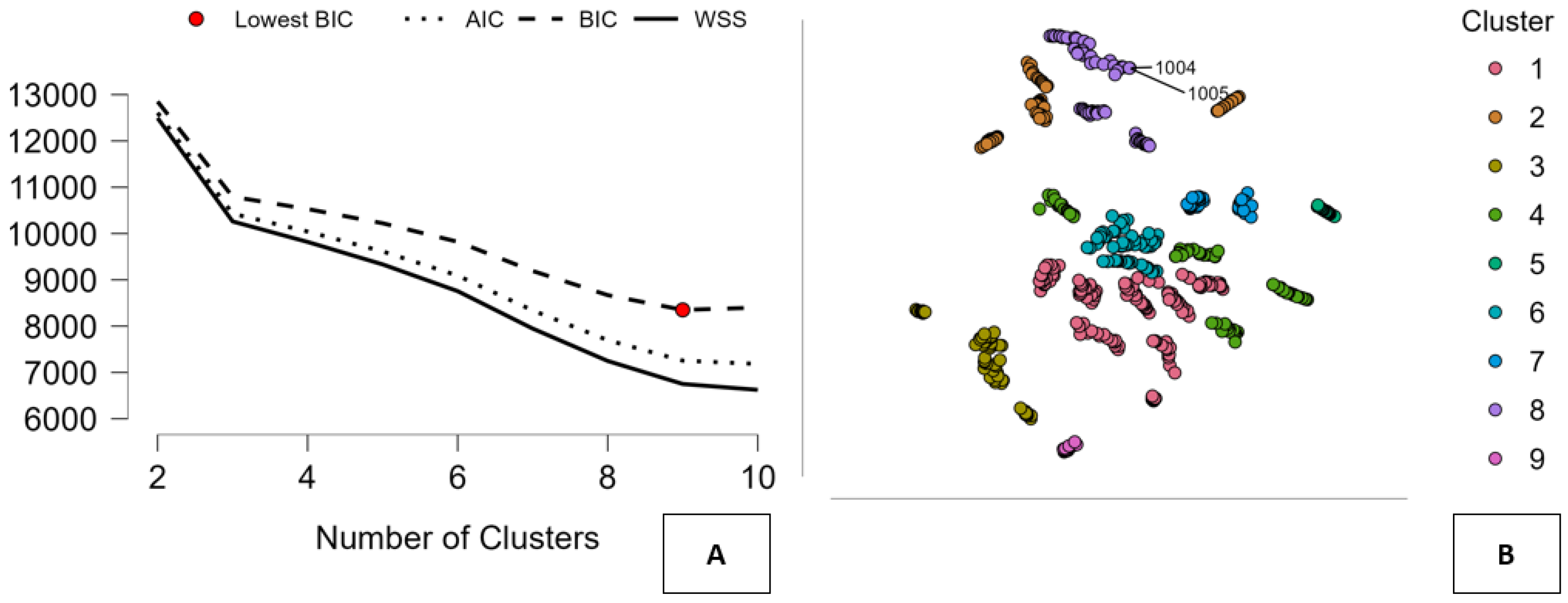

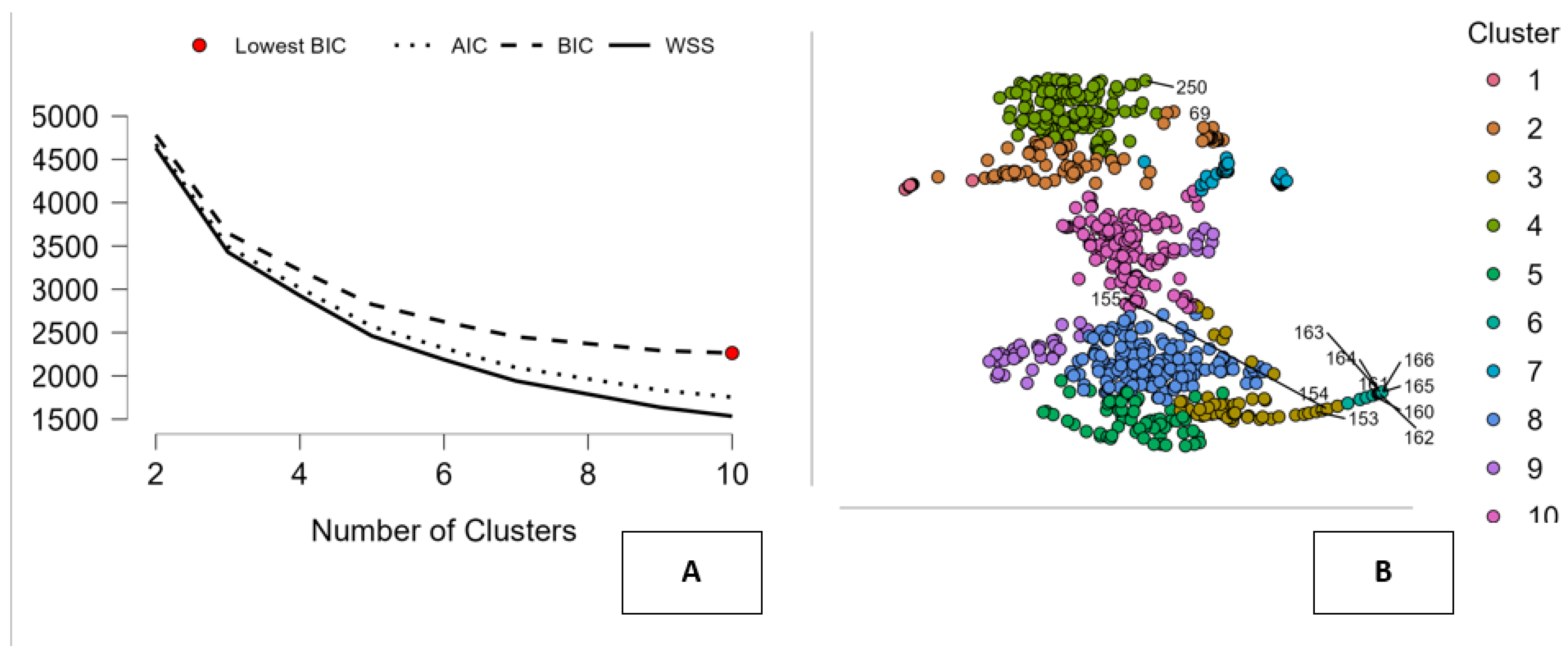

The following is a representation of the results of the Random Forest-based clustering technique on the Environment (E) dimension of ESG, which helps understand the impact of ESG on geopolitical risk (GPR). In panel A, the model selection step is depicted, which helps derive the appropriate number of clusters for the model. The graph of the Within-Cluster Sum of Squares (WSS) measure, together with the information criteria AIC and BIC, decreases as the number of clusters is incremented, thereby implying an improvement in the model's fit. However, the graph of the BIC reaches a trough at approximately nine clusters, marked with a red circle. This result helps derive an appropriate balance between model fit, as captured by the model's explanatory power, and model simplicity, thereby implying that nine clusters are appropriate for adequately characterizing the underlying structure of the data without falling prey to model complexity. The strategy of using multiple internal criteria for validating clusters is consistent with the literature on clustering, which suggests an appropriate balance between compactness, separation, and simplicity of clusters for adequately characterizing underlying patterns of multidimensional data (Arbelaitz et al., 2013). Panel B above shows a two-dimensional representation of this clustering outcome. Each data point in this graph represents an observation described by a variety of environmental factors, and these factors are grouped based on their cluster identities signified by different colors. This shows that the countries have been effectively grouped or partitioned based on their environmental characteristics through the use of the Random Forest method, and this is a clear indication that this method is capable of handling a variety of nonlinear relationships in a dataset (Martínez Torres et al., 2019). These groups or regimes represent different factors such as climate vulnerability, energy systems, resource use, and environmental distress that fall within the Environmental pillar of ESG analysis. In general, the use of sophisticated machine learning algorithms for representation learning and pattern extraction helps to provide a more complex description of environmental regimes compared to traditional linear approaches (Ismail Fawaz et al., 2019). The identification of different environmental profiles related to different degrees of GPR helps to interpret the concept of geopolitical risk as an effect driven by environmental sustainability, climate-related stress, and energy dependence. This further emphasizes the importance of the Environmental dimension in the ESG framework analysis of geopolitical risk. See Figure 2.

4.3. Machine Learning Prediction of Geopolitical Risk from Environmental ESG Indicators: Model Comparison and Key Drivers

On the basis of the normalized results (where a scale from 0 to 1 has been used, with higher results indicating better performance), it can be concluded that the best-performing model is indeed the KNN model. The objective evidence clearly reveals that for all the tested parameters, such as MSE, scaled MSE, RMSE, MAE/MAD, MAPE, and R², the best possible result of 1.00 has been achieved by the KNN model. It is clear that the model has been able to achieve the minimum possible error along with the maximum possible goodness of fit. Moreover, it can also be concluded that there is no trade-off between accuracy and goodness of fit because the minimum error is achieved at the highest value of R². The second-best algorithm here turns out to be the Random Forest algorithm. The performance of the algorithm is consistent in all aspects, particularly in terms of MSE, RMSE, and R², where it comes very close to the best results obtained by the KNN algorithm. It doesn’t obtain the highest score in all aspects, indicating a slightly lower accuracy than the KNN algorithm, though its robustness is very high. Linear Regression and Regularized Linear Models give intermediate results. They display good interpretability but moderate levels of error, which is clearly inferior to the performance of KNN and Random Forest Algorithms, but which could be useful if interpretability is of primary importance. Boosting, Decision Tree, and SVM have relatively weaker performances. Specifically, the Decision Tree has close to zero scores for some metrics, which shows that the model lacks the ability to generalize, while the SVM model has relatively low scores for most metrics, especially with regards to overall fit. In conclusion, KNN is the best method in the context of predictive accuracy, and Random Forest is a good alternative if robustness and generalization are the main priorities. Table 7.

The outcome of the KNN model provides a straightforward interpretation of the role of environmental factors in the explanation of geopolitical risk in the ESG model. The importance of the variables, considering the capability of the KNN model to identify nonlinear patterns, focuses on the actual role of environmental stressors in the explanation of geopolitical risk (GPR) rather than the importance based on a linear model. The most important variable in the model is the annual freshwater withdrawal (WAT) because it has the highest dropout loss in the model. The importance of the WAT variable positions the role of water availability as a pivotal environmental factor in the explanation of geopolitical risk. High freshwater withdrawal often indicates a stress situation in the availability of water resources, competition among sectors, and cross-boundary conflicts, especially in regions characterized by limited access to water resources, consistent with the theoretical explanation of the role of water scarcity in conflict patterns (Böhmelt et al., 2014). Very closely related to the importance of WSTR are the indicators of water infrastructure, including the safely managed sanitation (SMSS) and the safely managed drinking water (SMDW) variables, which also appear among the most important variables in the model. Emission-related variables also feature largely in terms of their importance. The emissions of nitrous oxide (N₂O), the usage of fossil fuels (FOS), CO2 emissions, methane emissions (CH₄), and pollution by particulate matter (PM2.5) are variables that feature large importance values and are thus closely linked to changes in GPR and feature a strong structural relationship with polluting production structures and energy types that are particularly susceptible to international climate policy pressure and costs of adaptation in terms of social tensions linked to environmental damage (Kahn et al., 2021; Şahin & Chen, 2023). Land use and environmental degradation also appear as prominent drivers. Tree cover loss (TCL), agricultural land (AGL), forest area (FOR), and agriculture, forestry, and fishing value added (AFF) score highly, indicating the impact of unsustainable use of the land and dependence on resource-intensive industries on geopolitical risk. Such drivers have been found to be associated with food security issues, subsistence in rural areas, and resource use disputes, as described in research on agricultural ecology and environmental degradation (Chowdhury et al., 2022). Another important dimension is energy structure and strength. Renewable energy use (REN), energy intensity (EINT), electricity generated from coal (ECOA), energy use per capita (ENU), as well as energy imports (ENI) all have been found to be of considerable importance, thus confirming that the way energy is generated as well as consumed is an important underlying factor of geopolitical risk. The importance of renewables, on the other hand, suggests that energy transition is an important factor of geopolitics, especially during structural changes in energy systems (Şahin & Chen, 2023). The role of Climate Variability Indices such as SPEI, Heat Index 35 (HI35), HDD, CDD, and Land Surface Temperature (LST) cannot be underestimated in this regard, further proving that vulnerability to extreme climatic conditions has the effect of acting as a risk multiplier in terms of geopolitical instabilities (Kahn et al., 2021). In conclusion, the KNN outcomes strongly verify the conclusion that geopolitical risk is ingrained in the environment. Water stress, emissions, land degradation, energy structure, and climate-related risks are found to be crucial components of the Environmental factor of ESG. These results emphasize that environmental sustainability is a concern that goes beyond ecology to become a core element of geopolitical risk. See Table 8.

From the table above, it can be seen that the local explanation for the GPR predictions based on the KNN model is provided, focusing clearly on the Environmental (E) factor of the ESG approach. For each of the five cases, a predicted GPR value is compared to a baseline value, with the individual contributions of the environmental variables explaining how the difference from the baseline is achieved. Positive contributions show factors increasing the level of geopolitical risk above the baseline, while negative contributions show factors that mitigate against it. For all five cases, the predicted GPR is always below the baseline value of 0.224, indicating that the environmental profiles for these five cases work to decrease geopolitical risk. This fits the definition of geopolitical risk as a measurable, dynamic process affected by structural factors rather than short-term political considerations (Caldara & Iacoviello, 2022). However, the decrease in GPR is due to the combined effect of different dimensions in the environment and not a single one. Energy structure and use stand out as a significant dimension in this respect. Variables like electricity from coal (ECOA), fossil fuel use (FOS), and energy use per capita (ENU) often display a negative contribution in many scenarios, especially in scenarios 1, 2, and 5, signifying that a lower dependence on carbon-rich energy and a moderate use level is correlated with a decrease in geopolitical risk. This result is consistent with the ESG view that cleaner and better energy systems result in a lower vulnerability to external shocks and geopolitical tensions (Bolton et al., 2020). Renewable energy use (REN) often shows a positive contribution in many scenarios, especially in scenario 1, signifying that a cleaner energy transition has a stabilizing effect in the geopolitical system and is consistent with evidence on climate transition and risk reduction and building resilience (Pankratz et al., 2023). Another important pathway involves water-related variables. Annual water withdrawal (WAT) and water stress (WSTR) often include negative weights, indicating that lower water pressure is a factor that decreases GPR. However, a high level of water withdrawal, as seen in case 5, positively affects GPR and confirms the idea that water scarcity and competition are important environmental risk-multipliers. This finding is supported by the literature that shows the impact of water availability and water-related variables on political instability and conflict (Böhmelt et al., 2014). Emissions and pollution indicators also demonstrate systemic effects. Methane emissions (CH₄) are always lowering the GPR, while nitrous oxide (N₂O) emissions have a positive impact. The impact of CO₂ emissions on GPR remains small and positive, indicating that higher emissions lead to higher geopolitical risks. The impact of particulate matter (PM2.5) on GPR remains inconclusive, with higher positive effects observed on some occasions, emphasizing the importance of environmental degradation to political stability. This confirms that climate change and environmental externalities impose systemic macroeconomic and political costs that may lead to higher geopolitical vulnerability (Kahn et al., 2021). Land use and ecosystem variables further influence the predictions. Agricultural land (AGL), forest area (FOR), and tree cover loss (TCL) are always negative factors, suggesting that better management of land and less degradation of ecosystems are factors that lead to a reduction in geopolitical risk. At the same time, variables associated with climate-related stress, such as Cooling Degree Days (CDD), Heating Degree Days (HDD), land surface temperature (LST), and Heat Index (HI35), are small but consistent factors, thus validating that climate-related extremes are a background driver of geopolitical risk (Kahn et al., 2021). In sum, these case-level findings further emphasize the overarching theme from the ESG analysis: the GPR is significantly impacted by the environment. Water security, energy mix, emissions, land use, and climate together drive whether a nation’s environment is an exacerbator or reducer of GPR. The clear pattern from these five cases that the predicted GPR is below the baseline in each one makes clear the benefit for geopolitical stability from enhancements in the Environmental component of the ESG and further supports the notion that environmental sustainability is a structural part of the GPR and the broader risk and resilience landscape (Bolton et al., 2020; Pankratz et al., 2023). See Table 9.

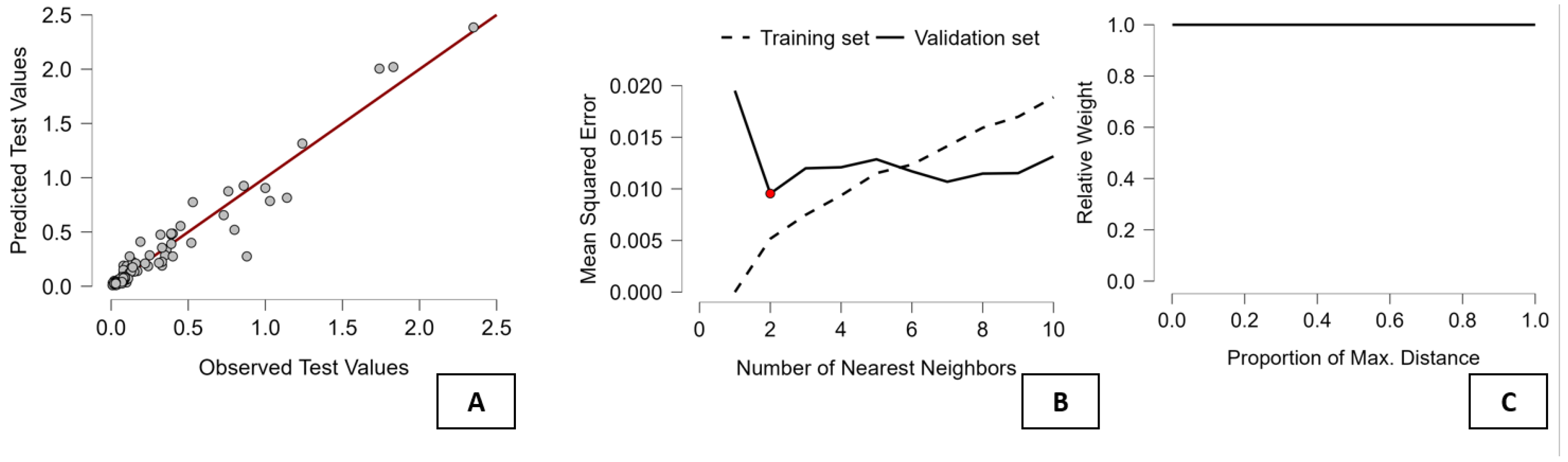

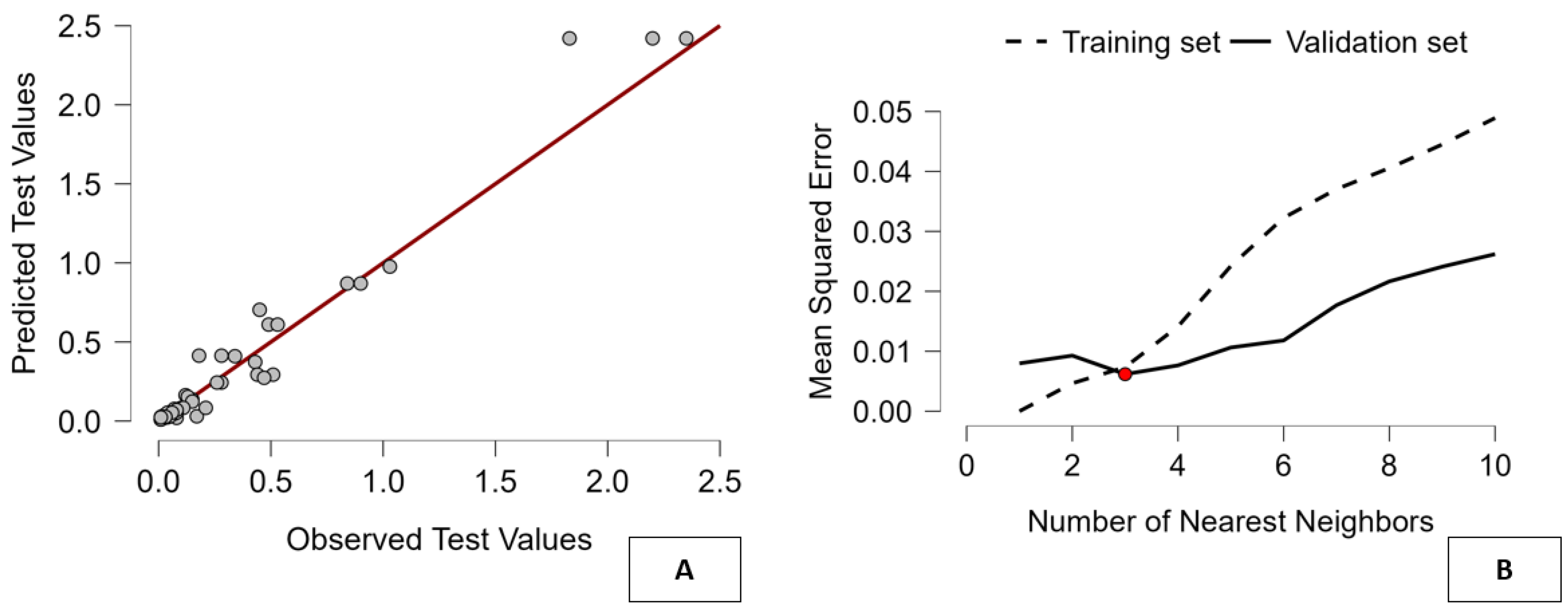

The figure provides a diagnostic summary of the K-Nearest Neighbors algorithm used for the estimation of geopolitical risk (GPR) based on environmental factors in the ESG model. The three graphs in the figure combine to illustrate the model's accuracy, the process of parameter determination, and the weighting system used in the model. Panel A of the figure illustrates the relationship between the actual values of GPR and the model's predictions for the values of GPR in the testing data set. The scatter diagram in the panel illustrates a very strong positive linear relationship, where most of the data points are closely aligned along the reference line representing a 45-degree angle, thus indicating the model's ability to accurately reproduce the actual values of GPR in the data set. The deviations from the reference line are small but slightly larger for the data points representing the highest GPR, thus indicating a slight worsening of the model's prediction accuracy in extreme GPR conditions, which aligns with the expected limitations of the model in extreme conditions based on the established principles of instance-based learning algorithms in model predictions (Kuhn & Johnson, 2019). Panel B focuses on model tuning, plotting the mean squared error against the number of nearest neighbors. The dashed line indicates the training error, which monotonically increases with the number of neighbors, as expected with the accompanying growth in bias. The solid line indicates the validation error, which decreases to a minimum around two nearest neighbors before growing again. The red dot indicates the optimal value of k that achieves a balance between bias and variance. This captures the traditional bias/variance tradeoff observed in non-parametric machine learning models, indicating that a small neighborhood size is all that is needed to identify local data structures (Kuhn & Johnson, 2019). This trend has been observed in applied studies on complex relationships using KNN in machine learning (García Rodríguez et al., 2021). Panel C shows the relative weights of neighbors by distance. The flat line represents uniform weights, which means that each of the selected neighbors has an equal say in the prediction. This selection aligns with the local averaging concept of the KNN algorithm to counterbalance the possibility of focusing too much on one observation. From an interpretability perspective, uniform weights make it easier to interpret local predictions. It follows best practices in interpretable machine learning for distance-based algorithms (Molnar, 2020). Together, the above figures show how the KNN model is a calibration, a stability, and a strong link between the Environmental aspect of ESG and geopolitical risks. Using its high predictability, clear parameters, and weighting, the model is a perfect solution to identify the non-linear and specific environmental factors influencing geopolitical risks. See Figure 3.

5. Social Foundations of Geopolitical Risk: An ESG-Based Multi-Method Assessment

In this section, we evaluate the impact of the Social (S) element of the ESG framework on geopolitical risk, as measured by the Geopolitical Risk (GPR) index. The primary research hypothesis is that geopolitical risk is a phenomenon that not only stems from political conditions in the present but also from deeper social structures such as demographically contingent risks, vulnerabilities to labor market risk, and dynamics of inclusion, which cumulatively may increase a nation's susceptibility to geopolitical risk. In order to capture the intricacies of such a relationship between these social structures and geopolitical risk, we use a combination of three different methods. First, we use a panel data econometric model to estimate a conditional relationship between GPR and a set of social variables such as net migration (MIG), unemployment (UNEM), and population aged 65 years or older (POP65), which are controlled for in a model that also accounts for unobservable country-specific heterogeneity. This allows for a meaningful point estimate to be derived that can be used to evaluate whether a relationship between these social factors and the variability of geopolitical risk exists. Second, we use a clustering analysis that groups countries on a set of additional social factors such as health, inequality, education, participation, and demographics. These allow for a mean difference analysis of country-specific groups on GPR to identify which groups of countries on these additional sets of social factors are associated with varying levels of geopolitical risk. Finally, we use machine learning models of regression analysis that focus on non-parametric models to identify any non-linear relationships between these sets of social factors that may exist in relation to geopolitical risk that are currently unidentified in standard econometric models of analysis.

5.1. Estimating the Social Pillar’s Effect on Geopolitical Risk: A Panel Econometric Approach

To estimate the impact of the S-Social component on geopolitical risk, we estimated the following equation:

Where i=42 and t=[2000;2023].

The description of the variables used is given in the Table 10 below.

The research is deliberately positioned within the ESG framework—Environmental, Social, and Governance issues—which is currently a prominent method for evaluating country and economic system sustainability and risk profiles (Iwanicz-Drozdowska et al., 2025). The current research focuses on the Social aspect of ESG and investigates its relationship to demographic and labor-market factors in explaining GPR (geo-political risk). The dependent variable is GPR (Geo-Political Risk), which is an indicator calculated by the number of news articles related to conflicts and political instability. The relationship of GPR to migration rates, unemployment levels, and aging populations is used to explain geo-political risk as a social-structural phenomenon (Kharlamova et al., 2025). The data set provides a panel of 42 countries over a period of 22-24 years, yielding a total of 1,006 observations. Four econometric models were applied: Fixed Effects, Random Effects GLS, Pooled OLS, and Weighted Least Squares (WLS). The Hausman test overwhelmingly rejects the null hypothesis of consistency for the GLS estimators (p = 7.8e-05), suggesting the fixed effects model as the best fit. The result matches the ESG view, which suggests that social factors are primarily explained by country-specific institutional differences rather than random variables. The LSDV R-squared measure of 0.81 for the fixed effects model suggests the explanation of a large part of the variation in GPR by structural factors of countries, whereas the within R-squared measure of 0.02 suggests the importance of the remaining social factors in the short run. The joint significance tests of the variables are highly significant in all four models, thus affirming the importance of migration, unemployment, and demographic factors in the explanation of GPR (Onomakpo, 2025). From the point of view of the ESG Social factor, the variable MIG (net migration) is a very important one. The migration process is a reflection of demographic pressure, labor market opportunities, and the ability for social integration (Zatonatskiy et al., 2024). The sign and significance of the coefficient for the variable MIG are positive in all models, and this indicates that the higher the net migration, the higher the level of geopolitical risk. This result can be explained in a number of ways: a large number of migrants can create tensions in society, competition for public services, and political polarization in countries that do not have effective policies for integrating migrants (Petrović & Vesković, 2025). At the same time, migration can be a result of regional conflicts, and thus a relationship exists in both directions between GPR and MIG (Rostetska et al., 2023). The high significance level for this variable indicates the importance of effective migration management for the ESG Social factor. Unemployment (UNEM) has a negative and significant coefficient in all specifications, which suggests that an increase in the level of unemployment is related to lower GPR. While this could be considered paradoxical, it could be argued that GPR reflects international political tensions rather than domestic instabilities (Adebanjo & Sibeate, 2022). Economies that have low levels of unemployment could be more active in the global economy, leading to greater levels of activity in geopolitical tensions. Alternatively, it could be that economic stagnation, which could be related to high levels of unemployment, results in less media coverage, leading to lower GPR. From an ESG perspective, this implies that the relationship between labor market conditions and GPR is complex. Population aged 65 years or older (POP65) has a positive and significant coefficient in both FE and RE models. Aging populations are often associated with a higher level of geopolitical risk, which may be explained in a number of social ways: pressure on welfare, pension, and healthcare systems; generational conflicts; unresponsiveness to economic change; and opposition to migration and globalization, which may cause political instability (Vollset et al., 2020). The significance of POP65 further reinforces that demographic sustainability is a key aspect of the Social dimension of ESG. The diagnostic tests identify econometric problems with important ESG considerations. The results from the White and Wald tests fail to support homoskedasticity, suggesting that differences in geopolitical risk are not constant from one country to another because of differing social structures. The results from the CD tests in Pesaran are highly significant (p-values close to zero) and support cross-sectional linkages in social factors such as migration crises and labor market shocks, thus confirming that the ESG Social pillar follows a transnational approach (Oliver-Smith, 2022). The results from Wooldridge tests reveal the presence of first-order autocorrelation, suggesting that geopolitical risk follows a persistent pattern in time and supports the idea that social tensions are cumulative and not easily overturned. From a substantive perspective, the findings indicate a number of implications from an ESG perspective. Firstly, geopolitical risks cannot be viewed independently of demographic and labor market dynamics, where the forces of migration and an aging population appear as the underlying causes of instability (Ongan et al., 2025). Secondly, the Social aspect is intertwined with political stories and media perception, where the GPR index is built upon. Thirdly, the management of social inclusion and demographic transition appears as a major tool for the mitigation of geopolitical risks. In summing up, the S (Social) component in ESG has a defining influence on geopolitical risk. Migration processes, labor markets, and a country’s aging population are not only social parameters in a country but also factors in global stability. Nations that do not address issues in integration, labor markets, and a balance between different age groups may end up with political instability expressed in a high level of GPR. Thus, ESG analysis has a correct perspective on this issue and shows that a country’s social sustainability has a defining influence on geopolitical security (Kharlamova et al., 2025; Iwanicz-Drozdowska et al., 2025). Improvement in the S component in ESG analysis may contribute to a reduction in geopolitical risks in a globalized world. See Table 11.

5.2. Clustering Social Structures and Geopolitical Risk: A Comparative Algorithmic Assessment

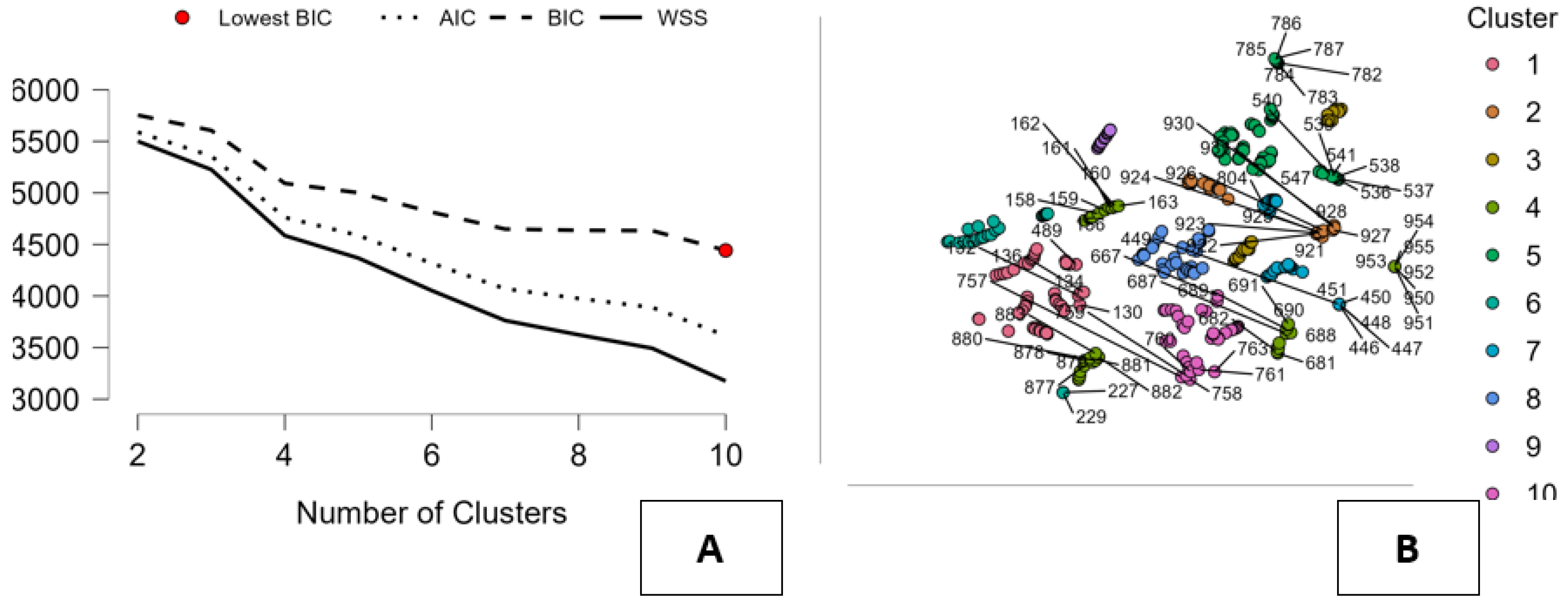

However, the choice of the best clustering algorithm must be based on a fair consideration of all the normalized measures, focusing on both the quality and the balance of the resulting clusters. Since each of the metrics is normalized such that the best result is denoted by a higher value, it is easy to compare the results across the algorithms. The hierarchical algorithm shows a marked superiority concerning the internal quality of the resulting clusters, achieving the highest value for minimum separation, Pearson's γ, Dunn's index, and entropy, which are combined indicators of highly compact and well-separated and internally consistent clusters (Hindupur et al., 2025). This level of superiority comes with a significant disadvantage: the value for the HH index for the hierarchical algorithm is zero, which is a clear indicator that the data points are highly concentrated around a few clusters. This level of unbalance makes the result less interpretable and less useful, especially for situations that call for a relatively balanced partitioning of the data points. On the contrary, the density-based algorithm shows the highest level of balance as far as the size of the resulting clusters is concerned, achieving the highest value for the HH index (Hindupur et al., 2025). This level of balance comes with a level of structural superiority that is remarkably low for all the metrics, which are combined indicators of the level of separation and internal cohesion of the resulting clusters (Hindupur et al., 2025). This indicates that while the algorithm produces a relatively balanced number of data points, the resulting data points are evenly distributed without any clear level of separation and internal cohesion. k-Means performs well on the Calinski-Harabasz index, as well as on Pearson's γ, but has a rather low HH index, indicating a preference for the concentration of observations into larger clusters. Model-based and Fuzzy C-Means methods result in medium values, neither of which is outstanding regarding structural quality, on the one hand, nor balance, on the other hand. Random Forest-based clustering is clearly the most balanced approach. Although it is not outstanding on any of the individual criteria, it is always close to the best values on all of them. In particular, it combines good separation and compactness (Dunn index, Pearson's γ, Minimum separation) with an extremely high HH index, which is an important indicator of a balanced distribution of observations into clusters (Sondag et al., 2025). This is particularly important if the aim is to identify heterogeneous structure without allowing a single cluster, or a small set of clusters, to dominate the others. Taking into consideration both quality of clustering, on the one hand, and concentration, on the other, Random Forest is clearly the best-performing algorithm, which provides the best balance of all the considered approaches (Sondag et al., 2025; Hindupur et al., 2025). See Table 12.

Results of the Random Forest clustering procedure paint a complex picture of the relationship between the Social (S) dimension of ESG ratings and geopolitical risk (GPR). By grouping countries on the basis of a broad set of social, demographic, health, inequality, and institutional variables, the results highlight specific social patterns, as well as illustrate how particular patterns of social characteristics are associated with varying levels of geopolitical risk. The results are given as standard scores, focusing attention on differences between clusters. Clusters with low or highly negative GPR, such as clusters 1 and 6, have relatively strong social fundamentals. These clusters have stronger performance in Economic and Social Rights (ESR), greater access to public services like education and healthcare, lower rates of undernourishment (UND), lower child mortality rates (U5MR), and higher female labor force participation (FLFP). However, life expectancy at birth (LEX) can be lower because of the composition of the population; nonetheless, these clusters tend to denote a society with greater cohesion and inclusiveness. From an ESG perspective, this data implies that a society that is more inclusive, less unequal, and has stronger social welfare systems acts as a factor that can offset the risks associated with geopolitics (Larson et al., 2025; Koumpagioti et al., 2025). On the contrary, the clusters that correspond to high GPR values, such as clusters 2, 3, 5, 7, 9, and 10, often indicate the presence of social vulnerabilities. These factors include high fertility (FER), undernourishment or prevalence of overweight individuals, high unemployment (UNEM), and poor education and healthcare infrastructure. Some of these clusters have been shown to have high income inequality, which is represented by high Gini coefficients and low income shares of the poorest 20 percent (INC20). These factors can often increase tensions in society, reduce trust in institutions, and increase political instabilities, which is represented by high geopolitical risk (Rao et al., 2023). Demographic dynamics are a crucial factor. Clusters that have a fast-growing population, a higher birth rate, or a large migration stream (MIG) are likely to have a higher GPR. Similarly, the density of the population (PDEN) or the dynamics of older ages (POP65) distinguish clusters, which suggests that demographic pressure as well as demographic imbalance can work as a risk multiplier (Gebreegziabher et al., 2024). Indicators linked to health care, such as the availability of hospital beds per 1,000 or child mortality rates or life expectancy rates, emphasize the need for social resilience to cushion the impact of geopolitical instability (Larson et al., 2025). Socio variables related to governance issues, Women’s Political Representation (WIP), Labor Force Participation (LFP), and Female to Male Labor Participation (FLFP), also explain variations in GPR across clusters. The more socially inclusive and economically participative clusters are associated with lower levels of GPR and thus strengthen the relationship between social inclusion and political stability (Koumpagioti et al., 2025). In sum, the Random Forest clustering approach confirms that geopolitical risk is firmly embedded within social structures. Inequality, exclusion, poor health and education infrastructure, and demographically stressed countries are all vulnerability-enhancing factors, while robust social structures and development on an inclusive basis are vulnerability-reducing (Rao et al., 2023; Gebreegziabher et al., 2024). The key takeaway from these results is that S, the pillar on Environmental, Social, and Governance criteria, remains an important factor influencing GPR, and hence, social equity-enhancing, health, education, and inclusion-focused policies are not only socially valuable goals, but they are absolutely necessary to ensure long-term geopolitical stability (Larson et al., 2025; Koumpagioti et al., 2025). See Table 13.

The results of the Random Forest clustering analysis provide a systematic explanation of the role of the Social (S) factor in the ESG model in terms of geopolitical risk (GPR). The importance of variables in terms of the average Gini reduction highlights the social factors most relevant to the identification of groups in terms of GPR. Rather than reflecting a linear relationship, the results point to the social factors with the strongest influence on the geopolitical risk posture of countries. The most influential variables are closely related to the outcome of healthcare, population structure, and inequality. The most important feature is the under-5 mortality rate (U5MR), which reflects the fundamental importance of healthcare conditions and the survival of children as a measure of social vulnerability. High child mortality rates are a measure of poor healthcare systems, poverty, and a lack of access to essential services, which can lead to social instability and increased geopolitical risk (Rangachari & Thapa, 2025; Crawshaw & Gray, 2025). Similarly, the role of population ageing (POP65) in the model suggests the importance of demographic imbalances, either due to ageing or dependency pressures, as a structural determinant of geopolitical risk (Lakioti et al., 2025). The role of income distribution and social inequality also stands out. The strong importance of the Gini index (GINI) and the share of the income of the lowest 20 percent of the population (INC20) suggests a positive relationship between inequality and geopolitical risk. Increased inequality can lead to social unrest, a breakdown of institutions, and a lack of political legitimacy, all of which are reflected in the increased levels of geopolitical risk (Lompo & Diendere, 2025). On the other hand, the importance of economic and social rights (ESR) performance and the role of increased life expectancy (LEX) suggest a stabilizing factor in terms of the role of social development in reducing geopolitical risk. The importance of human capital participation variables further strengthens the results. The importance of variables such as the use of the internet (INT), the participation of females in the workforce (FLFP), total labor participation (LFP), education expenditure (GEDU), school enrollment (PRIM, GPI), and the representation of women in the country's parliament (WIP) suggests the importance of social inclusion, knowledge access, and institutional participation in terms of the role of societies with a strong sense of inclusion in terms of managing social instability and geopolitical risk (Lakioti et al., 2025). Labor market dynamics and demographic factors are also important. Unemployment (UNEM), fertility rate (FER), migration (MIG), and population density (PDEN) are important for cluster differentiation. High unemployment rates and a rapidly changing demographic can heighten conflict over distribution as well as political instabilities, while mismanaged migration can heighten social and political tensions at a national as well as global level (Vesco et al., 2025). Overall, the results from the Random Forest clustering algorithm strongly support that geopolitical risk is integral to social structure. Rather than being ancillary issues, health outcomes, inequality, demographic trends, education, and engagement are fundamental to GPR. Under the ESG rubric, the Social factor is a fundamental foundation for geopolitical risk mitigation as well as a complement to the Environmental and Governance factors. Socially progressive policies that promote equality, improve health outcomes and educational attainment, as well as improve social inclusion are therefore important for a host of reasons that are simultaneously socially well-founded as well as fundamental to reducing geopolitical risk over the long term (Lakioti et al., 2025; Lompo & Diendere, 2025). See Table 14.