Submitted:

30 December 2025

Posted:

31 December 2025

You are already at the latest version

Abstract

The current study aims to identify the impact of strategic leadership through itsdimensions employee focus operational efficiency business development, andorganizational creativity based on the scale, onachieving distinguished performance. The study was applied at Misan OilCompany (MOC), where the questionnaire was distributed to a sample of 90senior management respondents, with 81 valid questionnaires analyzed. Thedescriptive-analytical method was employed to complete this study, and theresearch questions were addressed by testing several variance, correlation, andinfluence hypotheses using the statistical software (SPSS V.26). The studyreached several conclusions, the most important of which are: strategic leadershipand its dimensions significantly affect distinguished performance; there is astatistically significant correlation between strategic leadership (and itsdimensions) and distinguished performance; there is a statistically significantimpact of strategic leadership at both the overall level and the dimensional levelon distinguished performance; and there is variance in the effect of strategicleadership dimensions on distinguished performance in the studied oil company.

Keywords:

strategic leadership

; distinguished performance

Introduction

Strategic leadership is considered the core of the strategic management process and the primary driver of organizational success, development, and the achievement of goals. It is also regarded as one of the most important contemporary administrative concepts that grants organizations the strength ensuring survival, continuity, development, and adaptation to rapid changes and developments, owing to its ability to influence others and to entrench the principles of initiative, innovation, and creativity as effective means of enhancing performance effectiveness. This fundamentally contributes to the extent of organizational success in achieving strategic objectives efficiently and effectively. Therefore, the presence of strategic leadership plays a fundamental and significant role in the development of companies in general, and oil companies in particular, in achieving their objectives and granting them the ability to develop, grow, and adapt to their environment. This is achieved through its capacity for influence and its high degree of flexibility in confronting crises by focusing on employees, supporting them, and providing the requirements necessary for the performance of their work; enhancing process efficiency represented by the optimal investment of available resources and their development, support, and strengthening; developing and training employees to keep pace with new technological updates and advancements; and promoting organizational creativity within the framework of pursuing all that serves the operations of oil companies. This constitutes an effective means of increasing and improving the performance of employees and the company as a whole, as working under a creative, effective, and efficient strategic leadership—distinguished by the personal, creative, and cognitive attributes it possesses—enables organizations to confront crises and events they face and to improve their performance.

This study was conducted to reveal the positive role that strategic leadership can play in achieving distinguished performance in the company under study. The current study aimed to clarify the effect of strategic leadership, with its dimensions, on achieving distinguished performance in companies. Its importance is manifested in drawing the attention of strategic leaders to enhancing subordinate performance, which is reflected in the overall performance of the company. This was achieved through selecting a sample of senior administrative leaders at Maysan Oil Company, totaling (81) respondents. The researcher formulated several main hypotheses expressing the relationships of effect and correlation between strategic leadership, with its dimensions, and the achievement of distinguished performance, through the use of a number of appropriate statistical methods.

The current study reached a set of conclusions that provide explanations for some of the results that emerged from the study, based on data analysis and hypothesis testing. This contributes to guiding researchers and specialists toward new horizons and fields worthy of research, study, and development through a set of main recommendations related to the study, which aim to advance the situation toward a better reality by overcoming all obstacles and negatives, thereby leading to the achievement of distinguished performance and the accomplishment of the required objectives.Top of Form

Chapter One: Research Methodology

Research Problem

Both practitioners and researchers recognize the role of strategic leaders in light of rapid transformations, as organizations operate in a business environment characterized by rapid change and continuous disruption. Moreover, high global competition, technological and scientific revolutions, economic and financial crises, and other challenges threaten the survival and continuity of organizations, making their development imperative. Public organizations, in particular, are more obligated than others to employ new ideas in their operations because they aim to provide the best services to members of society, either directly through offering goods and services or indirectly due to their significant role in shaping the national economy. Success, entering new horizons, and achieving distinguished performance depend on the extent to which organizations focus on strategic leadership. This study seeks to explore this issue within Misan Oil Company under the Iraqi Ministry of Oil.

After reviewing the nature of the company’s operations through informal interviews conducted with several managers and employees, the researcher observed a significant need to enhance strategic leadership practices, as they are not at the level required to meet the company’s ambitions. Additionally, the low performance level of employees undermines operational efficiency and slows down work processes. Given the company’s responsibilities in implementing oil projects, this presents a research problem that requires investigation and inquiry.

Therefore, the research problem can be summarized through the following questions:

- What is the level of practicing strategic leadership through its dimensions (employee focus, operational efficiency, business development, and organizational creativity) in the studied oil company?

- Does the studied company have the capacity to achieve distinguished performance through strategic leadership?

- Is there an impact of strategic leadership dimensions (employee focus, operational efficiency, business development, and organizational creativity) on distinguished performance?

- What is the perspective of managers in the studied company regarding the impact of strategic leadership dimensions (employee focus, operational efficiency, business development, and organizational creativity) on achieving distinguished performance in their company?

Significance of the Study

The significance of the study in Misan Oil Company (MOC), the research population, is derived as follows:

- Strategic leadership plays an important role in achieving distinguished performance. This gives the current study considerable importance as it adopts the study of leadership from a strategic perspective, as well as its potential in achieving distinguished performance in the company under study.

- Its significance also stems from being one of the first studies to address the relationship between strategic leadership and distinguished performance in Misan Oil Company and, more broadly, in all oil companies in Iraq, according to the researcher’s knowledge.

- Providing a comprehensive conceptual framework for the main research topics, represented by strategic leadership with its sub-dimensions and distinguished performance.

Research Objectives

- To develop a comprehensive knowledge framework for the main study topics, represented by strategic leadership and distinguished performance and their sub-variables, by reviewing recent scientific research and studies and consolidating the knowledge contained therein.

- To identify the nature of the relationship and the effect between strategic leadership and distinguished performance in the company under study.

- To assess the level of perception of the sample members regarding strategic leadership and its sub-dimensions in the company under study.

- To assess the level of perception of the studied sample regarding distinguished performance in the company under study.

- To determine the extent of contribution of strategic leadership dimensions in achieving distinguished performance in the company under study.

- To examine the impact of strategic leadership and its dimensions on distinguished performance in the company under study.

- To provide recommendations and proposals that the company under study can utilize to enhance and strengthen the relationship between strategic leadership and distinguished performance.

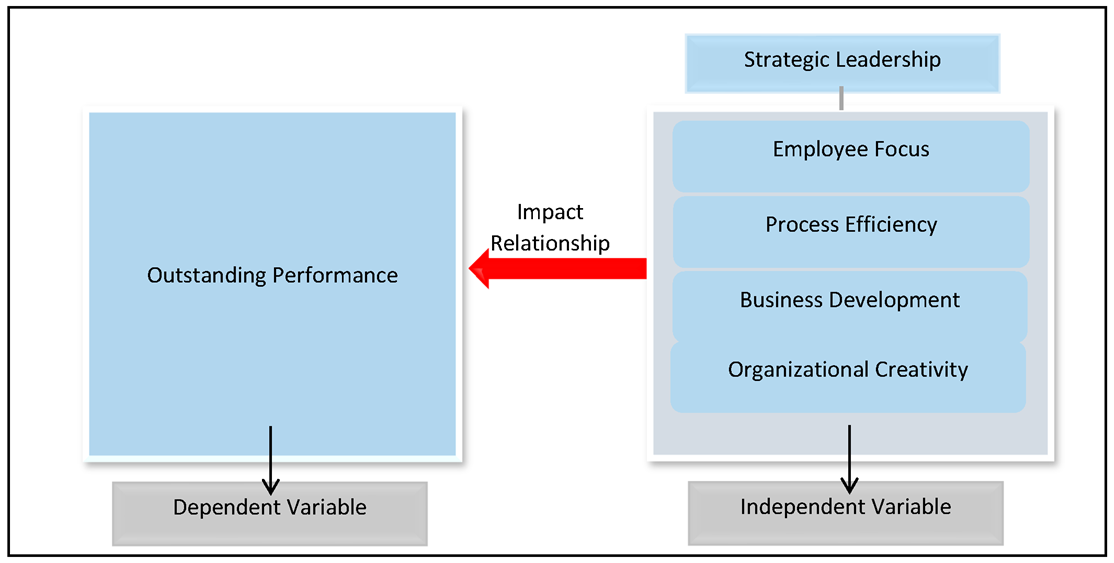

Study Framework

Research Model Diagram

Study Hypotheses

- Main Hypothesis 1: There is a statistically significant relationship at the significance level (0.05) in the attitudes of managers in the studied oil company regarding strategic leadership and distinguished performance, attributed to variables (gender, age, educational level, job level, years of experience).

- Main Hypothesis 2: There is a statistically significant correlation between strategic leadership in its dimensions and distinguished performance.

- Main Hypothesis 3: There is a statistically significant effect of strategic leadership in its dimensions on distinguished performance.

Study Boundaries

The spatial and temporal boundaries of the study are as follows:

- Spatial Boundaries: The study is conducted at Misan Oil Company, which is one of the oil companies operating in Misan Governorate, southern Iraq.

- Temporal Boundaries: The study covers the period from 2022 to 2023.

- Human Boundaries: The sample consists of senior administrative leaders in the company (heads of authorities and departments) in senior management.

- Scientific Boundaries: The study focuses on (strategic leadership and distinguished performance), extending its scientific boundaries to the field of strategic management.

Method of Data Collection and Study Tools

Sources of Information

- Desk Research: The study relied on Arabic and foreign sources including books, reputable scientific research, theses, and recent dissertations related to the study topic, in addition to online sources.

- Questionnaire: This tool is suitable for obtaining data and information related to the study population and sample.

Study Tools

- Statistical Software: The Statistical Package for Social Sciences (SPSS) was used to analyze the collected data for study purposes.

- Descriptive Statistics Methods: Methods such as percentages, frequencies, mean, and standard deviation were used to provide a comprehensive description of the responses of the sample individuals to the questionnaire items.

Chapter Two: Theoretical Framework of the Study

Concept, Importance, and Objectives of Strategic Leadership

Concept of Strategic Leadership

Most authors and researchers agree that the concept of strategic leadership is a modern concept in the field of management. Its roots can be traced back to military systems, but it quickly gained exceptional importance in today’s business world more than ever before. The main reason for this is the rapid environmental changes as well as the increasing complexity of organizations themselves. This concept first appeared in the works of Kotter (1982) and Mintzberg (1984), with reference to the emergence of executive leadership and the company CEO (Shati, 2017, p.25).

Mintzberg believes that strategic leadership involves controlling the direction, rate, and growth of organizations and achieving long-term goals. Accordingly, control strategies aim to identify external opportunities and risks, safeguard and formulate strengths, and recognize internal weaknesses of organizations (Mintzberg, 1990, p.18). This necessitated organizations to develop the necessary tools to deal with environmental changes in order to ensure continuity and survival (Aslan et al., 2011, p.628).

Therefore, leadership is the ability to continuously generate motivation to sustain the organization, focus on operational activities, and monitor changes affecting the organization internally and externally, since these changes determine the organization’s existence in the future. The performance of any organization depends on its leaders (Finkelstein & Hambrick, 2008). Business performance declines if strategic leadership suffers from deficiencies, such as an inability to persuade employees to follow its vision. Consequently, the main importance for any leader is to develop the capabilities of their followers to transform the workplace into an environment where they can achieve their full potential (Sharma, 2007, p.20).

Daft (2011, p.350) did not differ much in his definition of strategic leadership, describing it as the ability to anticipate and envision the future, maintain flexibility, think strategically, and initiate changes that create a competitive advantage for the organization. Similarly, Abd Al-Abbas (2020, p.8) defined it as the process of influencing employees through the skills and behaviors possessed by the leader to create strategic change in the organization and encourage employees toward creativity and innovation to achieve organizational goals.

The concept of strategic leadership also provides the values and capabilities required for medium and large business owners to enable them to succeed in managing operations and to anticipate the organization’s position in the business environment to achieve continuity, survival, and success (Rodgers, 2016, p.4).

Importance of Strategic Leadership

Strategic leadership is considered an important managerial tool, as its significance lies in helping organizations maintain their success by enhancing their adaptability and managing both internal and external environments. Its importance stems from strengthening managers’ ability to respond and be aware of internal and external influences. It also contributes to developing, improving, and nurturing future-oriented ideas, assists in accurately anticipating strategic outcomes, seeks to develop the organization’s long-term financial performance, identifies future opportunities, and anticipates problems that may affect operations (Tabidi, 2010, p.30).

The strategic qualities and skills of leaders include their ability to define the organization’s future vision and transform it into reality by formulating visions and objectives, developing comprehensive plans, communicating with employees, implementing necessary changes in organizational structure and culture, exploiting opportunities, confronting external threats, as well as enhancing strengths and addressing internal weaknesses (Al-Shahri, 2020, p.204).

Strategic leadership also contributes to building an effective organizational culture characterized by flexibility and the capacity for strategic change to achieve the organization’s desired goals through a positive and reciprocal relationship between strategic leadership and the execution of organizational tasks (Lee & Chen, 2007, p.1028). Additionally, strategic leadership greatly assists in achieving organizational success and excellence, as it can enhance performance in a changing and turbulent environment, making strategic leadership practices a source of competitive advantage that enables the organization to strengthen its strategic competitiveness (Al-Jubouri, 2019, p.49).

Roles and Functions of Strategic Leadership

In the pursuit of achieving strategic success and increasing organizational efficiency, effective strategic leadership is essential, capable of performing various strategic roles and tasks. The agreed-upon roles of strategic leadership by most researchers include the following:

1. Strategic Decision-Making

Preparing and making strategic decisions is of great importance to senior management because of its impact on organizational effectiveness and survival. Strategic decisions involve planning the organization’s future and defining its policies, which enable it to achieve long-term objectives (Karam, 2021, p.75). Strategic decisions are defined as decisions objectively measured to achieve organizational goals, distinguished by their quality in contributing to efficiency and effectiveness (Al-Wadaya, 2015, p.10).

2. Strategic Thinking

Strategic thinking is an important and fundamental entry point for distinguished leadership, serving as the engine and driver of strategic leadership. It represents a contemporary approach and pioneering strategic mindset that goes beyond problems, crises, and internal and external environmental variables to envision what the organization should be in the future (Al-Janabi, 2020, p.3). Strategic thinking is described as the process of formulating a realistic vision by developing team capabilities, problem-solving, and critical thinking, which helps in responding to change, planning for the future, and exploiting opportunities. Hence, strategic thinking is a high-level mental activity possessed only by highly competent strategic leaders within the organization (Al-Ammar, 2011, p.6).

3. Strategic Planning

Strategic planning is the primary function of strategic leadership and represents the thinking that precedes decision-making to execute specific tasks or projects. Planning includes designing plans, objectives, and all activities that lead to achieving desired goals and, generally, represents the roadmap for achieving organizational objectives (Mustafa, 2011, p.115). Strategic leadership, whether in the public or private sector, is primarily responsible for guiding, developing, and updating organizational performance. Leadership behavior and orientations serve as key indicators of efforts made to improve performance, develop the organization and its human resources, and effectively implement the organization’s strategy to achieve creativity and excellence in operations (Al-Shamili, 2017, p.17).

4. Setting Strategic Goals

The need for strategic leadership increases in modern organizations because it significantly contributes to defining future organizational goals and solving problems occurring in daily operations (Hilal, 2008, p.36). The role of the strategic leader is reflected in formulating organizational goals after identifying opportunities and threats (external environmental factors) and determining strengths and weaknesses (internal environmental factors), and shaping these goals based on these factors (Ajel, 2021, p.558).

5. Strategic Change Management

Strategic change management is closely linked to the organization’s vision and strategic objectives. The absence of strategic leadership in the change process is akin to an unattainable dream, as effective strategic leadership possesses the ability to construct strategies through mental planning of what the organization should become in the future (Atli & Qani, 2021, p.18).

Dimensions of Strategic Leadership

According to the model of Duursema (2013, p.86), strategic leadership consists of four main dimensions or measures through which it can be assessed. This model was adopted in the current study and will be explained in detail as follows:

- Employee Focus: Followers of strategic leadership adopt methods and plans that enhance employee performance and foster a high level of trust with all employees and partners.

- Operational Efficiency: Includes detailed plans regarding how tasks or work are completed.

- Business Development: Refers to procedures encompassing initiatives, plans, and concepts.

- Organizational Creativity: Refers to innovation through generating ideas, visions, and proposals for distinctive and innovative organizational services.

Concept of Distinguished Performance

The concept of performance in general, and superior, high, or distinguished performance in particular, is considered one of the modern and contemporary managerial concepts that receive wide attention from both business organizations and governmental organizations due to its direct link to the success of these organizations, as well as achieving their objectives in a volatile environment characterized by continuous change and intense competition (Ismail, 2020, p.396).

Distinguished performance therefore requires an approach that encompasses all elements and components of organizational building on superior or distinguished foundations, which enables organizations to possess high capabilities to face competitors and environmental changes on the one hand, and to achieve cohesion and harmony among internal elements, exploit core competencies, and provide benefits to stakeholders and employees on the other hand (Abdul-Samad, 2018, p.310).

Importance of Distinguished Performance

The topic of distinguished performance is of significant importance, as both business and governmental organizations strive to achieve it at various levels, whether organizational or individual. It reflects the results achieved through operations and activities and provides an opportunity for comparison with other competing organizations, previous results, and standards (Molina & Callahan, 2010, p.38).

It is also considered an important and vital tool for evaluating the organization’s position and a factor that enhances its ability to make decisions and achieve objectives. Distinguished performance serves as a comprehensive support for organizational goals, innovation and creativity, growth, and continuous improvement to cope with pressures arising in operations.

Essential Requirements for Achieving Distinguished Performance

Achieving distinguished performance requires designing work in scientifically and practically sound ways, through which the required performance, appropriate methods for implementation, and the expected results upon completion are clearly defined. This also involves providing the essential resources for performance (material, technical, and other resources required for proper and distinguished execution), ensuring suitable conditions for completing tasks in accordance with correct implementation requirements, and providing skilled and experienced personnel to perform tasks, continually develop, and train them.

Furthermore, monitoring employees’ work is necessary to supply them with updated and essential information, overcome obstacles they may encounter, track results, evaluate them, and compare them with the predetermined objectives and targets (Amin, 2021, p.18).

Chapter Three: Hypotheses Testing

3.1 Testing Variance Hypotheses:

Main Hypothesis (H1): There is a statistically significant relationship at the significance level (0.05) in the attitudes of managers in the studied oil company regarding strategic leadership and distinguished performance, attributable to the variables of (gender, age, educational level, job level, years of experience).

The following sub-hypotheses fall under this main hypothesis:

(H1.1): There are statistically significant differences at the significance level (0.05) in the attitudes of managers in the studied oil company attributable to the variable of gender.

To test the statistical significance of differences in the study sample for the gender variable, a one-way ANOVA was used. The statistical data indicate that there are no statistically significant differences, as the significance value of F for all dimensions and variables is greater than the significance level (0.05), meaning it is not statistically significant. Therefore, the first sub-hypothesis is rejected, and it is concluded that there are no statistically significant differences at the 0.05 level in the attitudes of managers in the studied oil company attributable to the gender variable.

Table. One-Way ANOVA Indicator According to Gender for the Study Variables.

| Variables | F-value | Significance Level (Sig.) |

| Focus on Employees | 0.058 | 0.810 |

| Operational Efficiency | 2.810 | 0.098 |

| Business Development | 0.001 | 0.973 |

| Organizational Creativity | 0.003 | 0.958 |

| Outstanding Performance | 3.174 | 0.079 |

Source: Prepared by the researcher based on the outputs of statistical analysis.

(H1.2): There are statistically significant differences at the significance level (0.05) in the attitudes of managers in the studied oil company attributable to the variable of age.

To test the statistical significance of differences in the study sample for the age variable, a one-way ANOVA was used. The statistical data indicate that there are statistically significant differences, as the F significance values for all dimensions and variables are less than the significance level (0.05), except for the variable “Business Development”, which was statistically insignificant. Therefore, the second sub-hypothesis is partially accepted. This means that statistically significant differences exist, except for the Business Development dimension, at the 0.05 significance level in the attitudes of managers in the studied oil company attributable to the variable of age.

Table. One-Way ANOVA Index According to Age for Study Variables.

| Variables | F-value | Significance Level (Sig.) |

| Focus on Employees | 3.474 | 0.020 |

| Operational Efficiency | 3.126 | 0.031 |

| Business Development | 1.056 | 0.373 |

| Organizational Creativity | 2.667 | 0.054 |

| Outstanding Performance | 5.235 | 0.002 |

Source: Prepared by the researcher based on the outputs of statistical analysis.

(H1.3): There are statistically significant differences at the significance level (0.05) in the attitudes of managers in the studied oil company attributable to the educational level variable.

To test the statistical significance of differences in the study sample for the educational level variable, a one-way ANOVA was used. The statistical data indicate that there are no statistically significant differences, as the F significance values for all dimensions and variables are greater than the significance level (0.05), i.e., not statistically significant. Therefore, the third sub-hypothesis is rejected, and it can be concluded that there are no statistically significant differences at the 0.05 significance level in the attitudes of managers in the studied oil company attributable to the educational level variable.

Table. One-Way ANOVA indicator according to educational level for the study variables.

| Variables | F-value | Significance Level (Sig.) |

| Focus on Employees | 0.780 | 0.462 |

| Operational Efficiency | 0.567 | 0.569 |

| Business Development | 0.231 | 0.794 |

| Organizational Creativity | 0.891 | 0.414 |

| Outstanding Performance | 0.636 | 0.532 |

Source: Prepared by the researcher based on the outputs of statistical analysis.

(H1.4): There are statistically significant differences at the significance level (0.05) in the attitudes of managers in the studied oil company attributable to the job level variable.

To test the statistical significance of differences in the study sample for the job level variable, a one-way ANOVA was used. The statistical data indicate that there are no statistically significant differences, as the F significance values for all dimensions and variables are greater than the significance level (0.05), i.e., not statistically significant. Therefore, the fourth sub-hypothesis is rejected, and it can be concluded that there are no statistically significant differences at the 0.05 significance level in the attitudes of managers in the studied oil company attributable to the job level variable.

Table. One-way ANOVA indicator according to job level for the study variables.

| Variables | F-value | Significance Level (Sig.) |

| Focus on Employees | 1.241 | 0.295 |

| Operational Efficiency | 0.582 | 0.561 |

| Business Development | 1.193 | 0.309 |

| Organizational Creativity | 0.126 | 0.882 |

| Outstanding Performance | 0.371 | 0.692 |

Source: Prepared by the researcher based on the outputs of statistical analysis.

(H1.5): There are statistically significant differences at the significance level (0.05) in the attitudes of managers in the studied oil company attributable to the years of experience variable.

To test the statistical significance of differences in the study sample for the years of experience variable, a one-way ANOVA was used. The statistical data indicate that there are statistically significant differences, as the F significance values for most dimensions and variables are less than the significance level (0.05), except for the variables (Focus on Employees, Business Development, and Organizational Creativity), for which the significance was not observed. Therefore, the fifth sub-hypothesis is partially accepted, meaning that there are statistically significant differences, except for the dimensions (Focus on Employees, Business Development, and Organizational Creativity), at the 0.05 significance level in the attitudes of managers in the studied oil company attributable to years of experience.

Table. One-way ANOVA indicator according to years of experience for the study variables.

| Variables | F-value | Significance Level (Sig.) |

| Focus on Employees | 3.393 | 0.075 |

| Operational Efficiency | 4.180 | 0.009 |

| Business Development | 1.218 | 0.309 |

| Organizational Creativity | 0.558 | 0.644 |

| Outstanding Performance | 3.428 | 0.021 |

Source: Prepared by the researcher based on the outputs of statistical analysis.

Testing the Correlation Hypothesis

(H2) Main Hypothesis 2:

There is a statistically significant correlation between strategic leadership and its dimensions and distinguished performance.

To determine the type of correlation between the study variables, the Pearson correlation coefficient was used. The following table presents the correlation matrix between the study variables and their dimensions:

Table. Correlation coefficients between the study variables.

| Strategic Leadership | Focus on Employees | Operational Efficiency | Business Development | Organizational Creativity |

| Outstanding Performance | 0.60** | 0.74** | 0.73** | 0.68** |

Source: Prepared by the researcher based on the outputs of statistical analysis.

From the data in the table, it can be observed that there is a correlational relationship between strategic leadership and distinguished performance. The highest correlation was for operational efficiency, which reached 74%, while the business development dimension reached 73%, and the lowest correlation was for the employee focus dimension at 60%. Therefore, Main Hypothesis 2 is accepted, indicating that there is a statistically significant correlation between strategic leadership and its dimensions and distinguished performance.

Testing the Effect Hypotheses

(H3) Main Hypothesis 3:

There is a statistically significant effect of strategic leadership and its dimensions on distinguished performance.

Derived from Main Hypothesis 3 are the following sub-hypotheses:

(H3.1) There is a statistically significant effect of the Employee Focus dimension on distinguished performance in the investigated oil company.

The linear regression equation was used to test this hypothesis and to determine the extent of the effect of the Employee Focus dimension on distinguished performance, as shown in the following table:

Table. Regression Equation for the Effect of Employee Focus on Distinguished Performance.

| Dimension | Β | T (sig.) |

F (sig.) |

R2 | R2 |

| Focuson Employees |

0.606 |

6.764 (0.000) |

45.75 (0.000) |

0.367 | 0.359 |

Source: Prepared by the researcher based on the outputs of the statistical analysis.

- The significance of the regression model is confirmed, where the F-value reached (45.75), which is significant at the 0.05 level.

- The significance of the regression coefficients for the Employee Focus dimension and the constant term is confirmed, where the T-value for the Employee Focus dimension reached (6.764) at a significance level of 0.05.

- The significance of the effect of the Employee Focus dimension on distinguished performance is confirmed at the 0.05 level, where the regression coefficient (β) reached (0.606), indicating a positive effect.

- The coefficient of determination (R²) reached (0.367), indicating that the Employee Focus dimension explains 36.7% of the variance in the level of distinguished performance.

These results confirm the validity of Sub-Hypothesis 1 of Hypothesis 3, indicating that there is a statistically significant effect of the Employee Focus dimension on distinguished performance in the investigated oil company.

(H3.2) There is a statistically significant effect of the Operational Efficiency dimension on distinguished performance in the investigated oil company.

The linear regression equation was used to test this hypothesis and determine the extent of the effect of the Operational Efficiency dimension on distinguished performance, as shown in the following table:

Table. Regression Equation for the Effect of Operational Efficiency on Distinguished Performance.

| Dimension | Β | T (sig.) |

F (sig.) |

R2 | R2 |

| Operational Efficiency | 0.74 |

10.05 (0.000) |

101.07 (0.000) |

0.561 | 0.556 |

Source: Prepared by the researcher based on the outputs of the statistical analysis.

- The significance of the regression model is confirmed, where the F-value reached (101.07), which is significant at the 0.05 level.

- The significance of the regression coefficients for the Operational Efficiency dimension and the constant term is confirmed, where the T-value for the Operational Efficiency dimension reached (10.05) at a significance level of 0.05.

- The significance of the effect of the Operational Efficiency dimension on distinguished performance is confirmed at the 0.05 level, where the regression coefficient (β) reached (0.74), confirming a positive effect.

- The coefficient of determination (R²) reached (0.561), indicating that the Operational Efficiency dimension explains 56.1% of the variance in the level of distinguished performance.

These results confirm the validity of Sub-Hypothesis 2 of Hypothesis 3, indicating that there is a statistically significant effect of the Operational Efficiency dimension on distinguished performance in the investigated oil company.

(H3.3) There is a statistically significant effect of the Business Development dimension on distinguished performance in the investigated oil company.

The linear regression equation was used to test this hypothesis and determine the extent of the effect of the Business Development dimension on distinguished performance, as shown in the following table:

Table. Regression Equation for the Effect of Business Development on Distinguished Performance.

| Dimension | β | T (sig.) |

F (sig.) |

R2 | R2 |

| Business Development | 0.73 |

9.55 (0.000) |

91.32 (0.000) |

0.536 | 0.530 |

Source: Prepared by the researcher based on the outputs of the statistical analysis.

- The significance of the regression model is confirmed, where the F-value reached (91.32), which is significant at the 0.05 level.

- The significance of the regression coefficients for the Business Development dimension and the constant term is confirmed, where the T-value for the Business Development dimension reached (9.55) at a significance level of 0.05.

- The significance of the effect of the Business Development dimension on distinguished performance is confirmed at the 0.05 level, where the regression coefficient (β) reached (0.73), confirming a positive effect.

- The coefficient of determination (R²) reached (0.536), indicating that the Business Development dimension explains 53.6% of the variance in the level of distinguished performance.

These results confirm the validity of Sub-Hypothesis 3 of Hypothesis 3, indicating that there is a statistically significant effect of the Business Development dimension on distinguished performance in the investigated oil company.

(H3.4) There is a statistically significant effect of the Organizational Creativity dimension on distinguished performance in the investigated oil company.

The linear regression equation was used to test this hypothesis and determine the extent of the effect of the Organizational Creativity dimension on distinguished performance, as shown in the following table:

Table. Regression Equation for the Effect of Organizational Creativity on Distinguished Performance.

Table. Regression Equation for the Effect of Organizational Creativity on Distinguished Performance.

| Dimension | Β | T (sig.) |

F (sig.) |

R2 | R2 |

| Organizational Creativity | 0.68 | 8.42 (0.000) |

70.96 (0.000) |

0.473 | 0.467 |

Source: Prepared by the researcher based on the outputs of the statistical analysis.

- The significance of the regression model is confirmed, where the F-value reached (70.96), which is significant at the 0.05 level.

- The significance of the regression coefficients for the Organizational Creativity dimension and the constant term is confirmed, where the T-value for the Organizational Creativity dimension reached (8.42) at a significance level of 0.05.

- The significance of the effect of the Organizational Creativity dimension on distinguished performance is confirmed at the 0.05 level, where the regression coefficient (β) reached (0.68), confirming a positive effect.

- The coefficient of determination (R²) reached (0.473), indicating that the Organizational Creativity dimension explains 47.3% of the variance in the level of distinguished performance.

These results confirm the validity of Sub-Hypothesis 4 of Hypothesis 3, indicating that there is a statistically significant effect of the Organizational Creativity dimension on distinguished performance in the investigated oil company.

(H3.5) There is a statistically significant effect of the Strategic Leadership variable as a whole on distinguished performance in the investigated oil company.

The linear regression equation was used to test this hypothesis and determine the extent of the effect of Strategic Leadership on distinguished performance, as shown in the following table:

Table.Table. Regression Equation for the Effect of Strategic Leadership on Distinguished Performance.

Table.Table. Regression Equation for the Effect of Strategic Leadership on Distinguished Performance.

| Dimension |

β |

T (sig.) |

F (sig.) |

R2 | R2 |

|

Strategic Leadership |

0.79 | 11.78 (0.000) |

138.9 (0.000) |

0.638 | 0.633 |

Source: Prepared by the researcher based on the outputs of the statistical analysis.

- The significance of the regression model is confirmed, where the F-value reached (138.9), which is significant at the 0.05 level.

- The significance of the regression coefficients for the Strategic Leadership dimension and the constant term is confirmed, where the T-value for Strategic Leadership reached (11.78) at a significance level of 0.05.

- The significance of the effect of Strategic Leadership on distinguished performance is confirmed at the 0.05 level, where the regression coefficient (β) reached (0.79), indicating a positive effect.

- The coefficient of determination (R²) reached (0.638), indicating that Strategic Leadership explains 63.8% of the variance in the level of distinguished performance.

These results confirm the validity of Sub-Hypothesis 5 of Hypothesis 3, indicating that there is a statistically significant effect of Strategic Leadership on distinguished performance in the investigated oil company.

Results of Hypotheses Testing

The results related to hypothesis testing were obtained using ANOVA (one-way), linear regression equations, and Pearson correlation coefficients, with the following details:

- The results indicated homogeneity in the responses of the sample individuals from the investigated oil company, as reflected by achieving good arithmetic means for the study variables (Strategic Leadership and Distinguished Performance). This serves as an indicator of the company’s awareness of the importance of Strategic Leadership and Distinguished Performance.

- The results showed no statistically significant differences at the 0.05 level in the managers’ attitudes toward Strategic Leadership and Distinguished Performance attributed to the variables of gender, age, and job level, except for educational level and years of experience, which were partially accepted. This suggests that managers’ attitudes in the investigated company regarding Strategic Leadership and Distinguished Performance are largely based on intellectual and scientific foundations rather than personal characteristics, except in some dimensions.

- The results revealed a statistically significant correlation between Strategic Leadership dimensions and Distinguished Performance. The highest correlation was observed for Operational Efficiency at 74%, followed by Business Development at 73%, and the lowest for Employee Focus at 60%. This indicates the company’s attention to achieving a good level of Strategic Leadership by implementing the four dimensions (Employee Focus, Operational Efficiency, Business Development, Organizational Creativity), which contributes to enhancing performance and achieving excellence.

- The study found a statistically significant positive effect of Strategic Leadership at both the overall level and at the level of dimensions (Employee Focus, Operational Efficiency, Business Development, Organizational Creativity) on Distinguished Performance in the investigated company. The variable Strategic Leadership as a whole had the strongest impact on Distinguished Performance.

- The results showed variance in the impact of the Strategic Leadership dimensions (Employee Focus, Operational Efficiency, Business Development, Organizational Creativity) on Distinguished Performance. Statistical analysis indicated that most managers in the investigated oil company confirmed the ability of Strategic Leadership, through its dimensions, to influence Distinguished Performance in the company

Recommendations and Suggestions

- The researcher recommends that the management of the investigated oil company deepen their focus on the concept of Strategic Leadership, given its critical importance in the development and achievement of the company’s strategic objectives. This can be achieved by organizing seminars and development courses for all managers, educating them on the importance of Strategic Leadership and the results achieved through its application, and by enhancing awareness of the dimensions of Strategic Leadership and how to adopt them to achieve a high level of Distinguished Performance.

- The researcher recommends focusing on employees by implementing a periodic methodology to evaluate their performance according to pre-established standards, listening carefully to their suggestions and ideas, identifying their training needs, and maintaining good and trust-based relationships to identify problems and obstacles they face in their work. Special attention should be given to employees to improve and develop performance levels, which will enhance morale.

- The researcher recommends enhancing operational efficiency in the management of company operations by formulating clear short- and long-term objectives, ensuring that tasks are completed according to set goals, clarifying methods for task execution, and continuously monitoring progress through regular reviews of schedules and deadlines. Coordination between departments and the company’s management should also be strengthened to achieve integration in executing oil projects.

- The researcher recommends continuously developing the company’s business by adopting modern approaches in extraction or production processes carried out by the company, encouraging employees to achieve excellence, and fostering a spirit of teamwork.

- The researcher recommends promoting proactive behavior and creativity among employees by creating an organizational climate that encourages innovation, motivates out-of-the-box thinking, and avoids routine procedures when implementing new ideas at work.

- The researcher recommends that the management gain employees’ trust and increase their sense of belonging, enabling them to demonstrate their best capabilities and creativity, which significantly impacts the achievement of high performance. This can be supported by continuous monitoring of employee performance and establishing an administrative unit dedicated to supporting innovation and creativity to keep pace with developments in administrative and technological aspects.

- The researcher recommends adopting the Distinguished Performance approach in the company to elevate its performance and achieve excellence in its operations and services, reducing reliance on foreign companies for task execution.

- The researcher recommends maintaining an effective organizational culture in the company that encourages cooperation, openness, and the exchange of information and feedback among employees to improve the company’s overall performance.

- The researcher recommends that the company management develop continuous development and updating plans to execute operations with quality, cost-effectiveness, and adherence to timelines.

- The researcher recommends that managers adopt unique strategies for addressing deviations in work, achieving targets, or executing oil projects within the company.

- The researcher recommends ensuring a diverse and competent workforce by adding new skilled personnel, selecting and hiring based on experience and competence, and providing necessary training to elevate the company toward achieving excellence in its field as an oil company.

References

- Amin, Hinar Ibrahim. (2021). The Role of Creative Thinking Skills in Achieving Distinguished Performance: An Exploratory Study of the Opinions of a Sample of Administrative Leaders in Several Colleges of Duhok University. Global Academic Journal of Economics and Administrative Sciences, 3(1), 12-36.

- Al-Ammar, Abdullah Ali. (2020). The Impact of Human Resource Development on Job Loyalty – An Applied Study in Asir Region. Iraqi Journal of University, 51(3), 421-442.

- Al-Jabouri, Haider Abdullah Abdul. (2016). Strategic Leadership Behaviors and Their Impact on Investing Weak Signals to Avoid Strategic Deviations: An Analytical Study in the Diwan of Al-Diwaniyah Governorate (Unpublished Master’s Thesis). College of Administration and Economics, University of Kufa, Iraq.

- Al-Shahri, Salhah bint Abdullah. (2020). Strategic Leadership among Academic Leaders at King Saud University and Ways to Enhance It. Arab Journal of Administration, College of Business Administration, King Saud University, 40(1), 201-204.

- Al-Shamili, Aisha Youssef. (2017). Modern Strategic Management: (Strategic Planning – Organizational Structure – Creative Leadership – Control and Governance). Cairo, Egypt: Dar Al-Fajr for Publishing and Distribution.

- Ajel, Balqees Naji. (2020). Strategic Leadership and Its Impact on IT Entrepreneurial Orientation: An Applied Study at the University of Information Technology, College of Administration and Economics, Iraqi University. Dananeer Journal, 22, 574-581.

- Aslan, Ş., Diken, A., & Şendoğdu, A.A. (2011). Investigation of the Effects of Strategic Leadership on Strategic Change and Innovativeness of SMEs in a Perceived Environmental Uncertainty. Procedia Social and Behavioral Sciences, 24, 627–642.

- Chadha, S., & Sharma, A. K. (2015). Capital Structure and Firm Performance: Empirical Evidence from India. Vision, 19(4), 295-302.

- Daft, Richard L. (2011). The Leadership Experience (5th ed.). Cincinnati, OH: Cengage Learning South-Western.

- Duursema, Hester. (2013). Strategic Leadership: Moving Beyond the Leader-Follower Dyad. Thesis to Obtain the Degree of Doctor, Erasmus University Rotterdam, P.143.

- Finkelstein, S., & Hambrick, D.C. (2008). Strategic Leadership: Top Executives and Their Effects on Organisations. St. Paul, MN: West Publishing Company.

- Hilal, Mohamed Abdelghani. (2008). Strategic Thinking and Planning Skills: How to Connect the Present with the Future. Performance and Development Center, Part Two, Cairo, Egypt.

- Karam, Mohsen Hashem. (2021). Internal Audit Practices to Reduce Risks of Computerized Systems and Their Impact on Strategic Decisions of Iraqi Public Companies (Unpublished Master’s Thesis). College of Administration and Economics, University of Karbala, Iraq.

- Lee, Yuan-Puen & Chen, Shin-Hao. (2007). A Study of the Correlations Model Between Strategic Leadership and Business Execution – An Empirical Research of Top Managers of Small and Medium Enterprises in Taiwan. Proceedings of the 13th Asia Pacific Management Conference, Melbourne, Australia, 1028.

- Mustafa, Ahmed El-Sayed. (2011). The Manager and the Challenges of Globalization: A New Management for a New World. Cairo, Egypt: Dar Al-Nahda Al-Arabiya.

- Ogechithe, Rodgers Nyamao. Effect of Strategic Leadership on the Performance of Small and Medium Enterprises in Kenya.

- Rodgers, N. (2016). Strategic Leadership for SMEs. [Details as per original publication].

- Tabidi, Mohamed Hanafi. (2010). The Impact of Strategic Management on Performance Efficiency and Effectiveness: A Study of the Sudanese Telecommunications Sector (Doctoral Dissertation). School of Administrative Sciences, University of Khartoum, Sudan.

- Al-Wadayah, Mohamed Samih Mohamed. (2015). The Relationship of Management Information Systems to the Quality of Administrative Decisions: A Case Study of the Ministry of Education and Higher Education, Gaza (Master’s Thesis). Al-Azhar University, Gaza.

- Abdul Abbas, Suad Ali. (2020). The Impact of Strategic Leadership on Achieving Distinguished Performance. Iraqi Journal of Administrative Sciences, 16(63), 1-22.

- Sharma, S. (2007). Strategic Leadership and Organizational Change. [Details as per original publication].

- Amri, T., & Qani, T. (2021). The Impact of Transformational Leadership on Change Management: A Case Study of Institutions in Wilaya El Oued (Master’s Thesis). Faculty of Economic and Commercial Sciences and Management, University of El Oued, Algeria.

- Abd Al-Samad, Samira. (2018). The Role of Developing Human Competencies in Achieving Distinguished Performance in Organizations: A Case Study of Ain Touta Cement Company. Journal of Business Economics and Trade, University of Hadj Lakhdar, Batna, Algeria, 6, 308-322.

- Al-Janabi, Kifah Abbas Muheimed. (2020). Introduction to Strategic Thinking Study. College of Administration and Economics, University of Tikrit, Iraq.

- Molina, C., & Callahan, J. (2010). Fostering Organizational Performance. Journal of Management Development, 29(1), 38.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.