Submitted:

16 December 2025

Posted:

18 December 2025

You are already at the latest version

Abstract

This study presents the problem of corruption in the context of the forestry industry in Chile, focusing its analysis on two companies in the sector. In this regard, there have been some cases of corruption that have affected their reputation, causing damage to their governance. The objective focuses on analyzing the anti-corruption mechanisms and policies implemented by these companies, as disclosed in their sustainability re-ports, considering the law on crime prevention, risk management, and existing control mechanisms. The results reveal significant differences in levels of transparency and implementation: CMPC shows more comprehensive disclosure in its discourse, struc-ture, and mechanisms, while Arauco reveals a more formalized structure and organi-zation, with a focus on control and compliance. However, the conclusions indicate the need to strengthen regulatory frameworks to move toward effective transparency, considering that they reveal a gap between what is applied and what is said.

Keywords:

corruption

; forest governance

; anti-corruption policies

; sustainability

; transparency

1. Introduction

As the sustainability of social and economic development has become a problem of global importance, the participation of capital markets in the management of the social environment has become a crucial strategy (Zeng and Jiang, 2023). Sustainability is a fundamental pillar for organizations, which must promote social equity, environmental care, and economic value creation, articulating corporate governance structures and processes that ensure compliance, ethics, transparency, and effective oversight of ESG performance (Fiandrino et al., 2021).

This requires governance policies and practices that enable performance measurement beyond traditional financial indicators, incorporating metrics and materiality criteria that prioritize the most significant issues for the company and its stakeholders (Lungu et al., 2024).

In this regard, governance operates as the mechanism that integrates and guides environmental and social goals within corporate strategy, ensuring informed and responsible decisions regarding present and future impacts. It must ensure transparency and reliability, which are necessary conditions for legitimacy and sustainability.

The Organization for Economic Cooperation and Development (2024), through the formulation of its principles, aims to “help policymakers and regulators assess and improve the legal, regulatory, and institutional framework of corporate governance to promote market confidence and integrity, economic efficiency, and financial stability” (p. 5).

As Mohammad and Wasiuzzaman (2021) point out, when companies disclose more information about their environmental, social, and governance practices, this is consistently associated with better business performance and greater competitive advantage. This implies that transparency not only improves stakeholder and investor confidence, but also strengthens internal governance mechanisms by encouraging more sustainable and responsible practices.

To achieve this, organizations must maintain ethical and responsible conduct, with high standards of transparency and accountability to the environment and their employees. Taking into account the statements by Farah et al. (2025), ESG information improves transparency and accountability, as it requires companies to submit detailed reports on their governance practices, including anti-corruption measures, ethical practices, and regulatory compliance.

However, there is one phenomenon that has not been eradicated: corporate corruption. According to Previtali and Cerchiello (2023), corruption, by its nature, is secretive, complex, hidden, and sensitive, and is frowned upon by companies. It is not only an ethical transgression, but also represents an element that negatively affects the trust of companies and individuals, with an impact on markets that prevents efficient functioning, affecting both their reputation and credibility.

Therefore, the implementation of strategies aimed at reducing the risk of corruption is a priority. One of the actions that contributes to its mitigation is the disclosure of information related to its management, with transparency contributing to the strengthening of corporate credibility and reputation among various stakeholders. In this regard, Gerged et al. (2024) offer solid empirical support for the positive relationship between companies’ anti-corruption disclosures and their sustainability performance. This suggests that transparency in anti-corruption initiatives is associated with better sustainability outcomes for companies.

The Organization for Economic Cooperation and Development (OECD, 2020) highlights in its Public Integrity report that corruption is one of the most devastating problems of our time, leading to waste of public resources, increased social and economic inequality with the dissatisfaction that this entails, and undermining trust in institutions.

At the same time, companies’ operating costs are increasing significantly as they face greater administrative barriers and mechanisms that discourage investment and organizational sustainability. As measures to counteract this harmful effect of corruption, Khaled et al. (2021) emphasize the existence of ESG practices and disclosures that constitute new accountability measures reflecting a voluntary commitment to non-financial objectives and sustainable development, also generating value for investors, other stakeholders, and society as a whole. One of the contributions emphasized in the academic discussion is the impact that companies and their particular characteristics have on their sustainability performance, within the context of emerging markets, both in terms of goals and objectives. Although they do not specifically mention Latin America, they point out that the emerging economies in the region have their own characteristics which, among other risks, include entrenched corruption, creating a weak institutional environment. This means that corporate disclosure and transparency strategies that seek to maintain or restore corporate confidence take on an important role.

One of the main organizations dedicated to the study and monitoring of corruption at the global level, Transparency International, through the results of its corruption indices calculated annually, points out that by 2024 corruption will constitute a growing global threat to sustainable development. Its president, François Valérian, stated in this regard:

Corruption is a growing global threat that not only undermines development, but is also a decisive factor in the decline of democracy, instability, and human rights violations. Combating corruption must be an absolute and constant priority for the international community and all countries. This is essential to roll back authoritarianism and ensure a peaceful, free, and sustainable world. The dangerous trends revealed in this year’s Corruption Perceptions Index highlight the need to respond with concrete measures now to tackle global corruption. (Transparency International, 2024)

The results of the Corruption Perceptions Index (CPI) for 2024 revealed that more than two-thirds of the 180 countries assessed scored below 50, indicating high levels of corruption. Measured from least to most corrupt, Denmark led with 90 points, while South Sudan, Somalia, and Venezuela ranked last. It is also evident that corruption seriously hinders climate action, diverting funds with a direct negative effect on corporate action. It also points to the identification of undue influence by fossil fuel industries in countries with high and low levels of corruption, delaying key environmental measures that are necessary. The lack of control favors environmental damage, which already generates up to $238 billion annually. (Transparency International, 2024)

In the case of Chile, based on data presented by Transparency International (2024), it ranks 32nd out of a total of 180 countries in this index (CPI), falling 5 points in the last 2 years. This position in the ranking reflects that in the last two years, the country has significantly worsened its results, falling from a score of 67 in 2022 to 63, reflecting a significantly deteriorated condition due to the increase in cases of corruption fraud in the territory.

However, at the global level, the forestry industry is no stranger to the problem of corruption. As Prakasa et al. (2022) point out, this has not only caused financial damage to the state, but also environmental degradation, leading to human rights violations in communities, such as that suffered by the Laman Kinipan indigenous people in Indonesia, where there are strong networks of influence and power, , thus addressing a more complex social problem due to the existence of governance with entrenched and deep-rooted corruption.

Similarly, the study by Ismariana et al. (2024) revealed that corruption in social forestry in Indonesia is systemically entrenched at all levels, such as NGO, foresters, and bureaucrats, which inevitably becomes normalized, thus undermining sustainability goals and tarnishing public management in the country.

As another form of illegal corruption, in Romania, corruption is associated with illegal logging, which is exacerbated by the presence of the informal economy and money laundering activities, with complex environmental and social consequences (Cozma et al., 2023).

However, despite Chile historical reputation as an institutionally sound economy, there have been a number of corporate corruption scandals in the last decade, one of which was the 2015 toilet paper collusion case involving CMPC, raising questions about the integrity of large companies and their relationship with public policy.

Araya (2016) mentions that during the investigation by the National Economic Prosecutor’s Office, a series of acts by executives were detected to intentionally conceal the cartel, so as not to reveal the management of these agreements in digital format or through institutional emails, which was achieved through printed documents and personal email accounts. In addition, they used cell phones to coordinate with competitors. The Prosecutor’s Office classified this case of collusion as one of the most serious economic crimes due to its duration and the large size of the market that was harmed.

The research conducted by Álvarez (2017) analyzes the main problems caused by the Chilean forestry industry controlled by the companies Arauco and CMPC in response to growing Chinese demand over the last seven years. The significant conclusion of this research indicates that, given this demand and the highly intensive structure of the production model implemented by Forestal Arauco and Celulosa CMPC, the main forestry companies in Chile, tensions have increased, such as the gradual precariousness of employment, environmental deterioration, and the intensification of the Mapuche conflict due to indiscriminate forestry activity spread across the regions of Biobío, La Araucanía, Los Ríos, and Los Lagos. Undurraga and Fergnani (2024) point out that improved relations between forestry companies and local communities are needed.

Corporate transparency is an essential objective in order to report to stakeholders on management and performance actions and results, with a commitment to corporate social responsibility. Valdebenito (2018) emphasizes that the purpose of making management and its impact visible goes beyond the financial sphere; companies have incorporated principles that promote disclosure practices focused on environmental, social, and governance (ESG) aspects. In this context, communicating actions and policies aimed at preventing corruption and reducing its impact takes on particular importance.

One of the two companies in the study is part of the Dow Jones Sustainability Index in Chile. This metric is a weighted index that measures performance in compliance with ESG (environmental, social, and governance) criteria and is considered among the 23 highest-rated companies in 2024 that are part of this index for this period. (Dow Jones Sustainability Chile, 2024).

These companies, which are corporations, trade their shares on international markets through the Santiago Stock Exchange. They are regulated based on the pronouncements, rules, and regulations issued by the CMF (Financial Market Commission), the institution that has the power to supervise their operations in Chile.

With regard to the regulatory framework in Chile, there have been significant changes over the last decade which, among other objectives, require the disclosure of sustainability information to ensure transparency regarding the impacts generated. In this regard, in 2015, General Regulation No. 385 was issued by the former Superintendency of Securities and Insurance, which required registered companies to disclose information on corporate governance in four areas: Board of Directors; shareholder relations, general public; risk management; external evaluation.

As of November 2021, the Financial Market Commission issued General Regulation No. 461, representing a significant advance in mandatory regulatory matters by requiring companies to include environmental, social, and governance aspects in their annual reports (Financial Market Commission, 2021, p. 5). One of these points refers to how corruption, money laundering, and terrorist financing are prevented.

However, as Valdebenito (2018) mentions in relation to the fight against corruption, this regulation lacks specific guidelines and focuses mainly on preventive actions. This means that many companies determine autonomously and arbitrarily both the content and the focus of the information they disclose on these topics, as there is no detailed regulatory framework to guide the disclosure of such practices in a complete and transparent manner. Therefore, the observations of Zeng and Jiang (2023) are noteworthy, as companies may conceal or disclose false information to obtain a good ESG rating, which allows them to enjoy a good social reputation and access various resources, a practice known as “greenwashing.”

Therefore, the issue addressed in this study is to analyze the extent to which CMPC and Arauco disclose corruption risk management in a transparent, specific, and verifiable manner through their internal control systems and clear, specific anti-corruption policies in accordance with regulatory frameworks. This is based on the information disclosed in their sustainability reports for the period considered in the study.

Therefore, the purpose of this research is to analyze the anti-corruption procedures and policies reported in their sustainability reports for the year 2023 by publicly traded companies in the forestry sector in Chile, considering current regulations, such as Law 20.393 and NCG 461, issued by the Financial Market Commission. Understanding the interaction between corruption and how governance can mitigate it is essential for developing effective strategies to combat it in the forestry sector.

The second part of this study presents a review of the literature focusing on anti-corruption mechanisms and policies. The third section outlines the methodology applied, including the data used and the methodological design for analyzing integrated reports and sustainability reports. The fourth part presents the results and discussion based on the established analytical dimensions and the literature. Finally, the fifth part summarizes the main conclusions of the study.

2. Literature Review

Governance is one of the pillars of sustainability, referring to the rules, principles, processes, and practices that underpin management with structures and mechanisms that ensure transparency, accountability, responsibility, ethics, and long-term sustainability.

Gutiérrez-Ponce et al. (2022) point out that the academic literature indicates that good corporate governance has a positive impact on organizations’ performance. With regard to , Cardoni et al. (2022) study the relevance of the value of corporate governance policies and incorporate anti-corruption as a characteristic of sustainable governance. According to Elamer & Boulhaga (2024), well-defined corporate governance frameworks and internal ESG strategies mitigate adverse impacts and can transform controversies with stakeholders into opportunities for growth and reputation enhancement. Lagasio & Cucari (2019) contribute to the debate on corporate governance mechanisms that lead to greater ESG disclosure and highlight the need for a new approach to these issues.

Armstrong (2020) considers that internal governance mechanisms are the structures and processes designed to ensure the independence and accountability of the board through reporting and transparent disclosure, risk management, and the prevention of corruption and bribery.

Table 1 shows some research that has explored the governance perspective in the context of sustainable development. It highlights that good practices such as the separation of CEO functions, the existence of ESG committees, and gender diversity on the board are positively associated with better environmental performance and greater disclosure of sustainability information. It is observed that sound corporate governance improves the quality of information, which positively influences dividend policies for shareholders and returns for investors, and is more common in publicly traded organizations, while financial difficulties are associated with lower quality ESG disclosure.

The problem of corruption in organizations has been addressed from different theoretical perspectives and regulatory frameworks, considering that its establishment undermines economic efficiency, the legitimacy of institutions, and investment, as well as causing often irreparable damage to stakeholders due to loss of credibility and mistrust.

Although the Organization for Economic Cooperation and Development (OECD, 2008) does not provide an explicit and unique definition of corruption in its glossary of international standards in criminal law, it classifies a series of crimes that correspond to corrupt actions or behaviors as “the abuse of a position in the public or private sector for personal gain.”

Argandoña and Morel (2009) point out that corruption has become a major problem with social, political, legal, economic, and ethical implications, affecting both public and private entities alike. It represents one of the main obstacles and difficulties for the growth and sustainable development of organizations.

In relation to the studies carried out by Transparency International, of the 180 countries considered in the evaluation, in the case of Chile, Table 2 shows a significant worsening in the last two years, compared to the trend that had been maintained until 2022, due to some acts of corruption in the country that have diminished citizens’ trust in institutions, such as the Audio case and the Convenios case.

Considering the negative impact that corruption has on stakeholders, which in turn undermines the relationship between senior management and investors, this study is based on the articulation of two main theories: agency theory and stakeholder theory.

Agency theory, as pointed out by Jensen and Meckling (1976), is based on a contract between a principal and an agent to perform a service on their behalf in the organization, with the delegation of authority that this implies. The agent has access to privileged information to the detriment of the principal, with an asymmetry of information between the parties that allows the agent to satisfy personal interests to the detriment of the principal’s interests.

In the case of companies in the forestry sector in Chile, there have been practices that are questionable from an ethical and legal point of view, such as collusion in the tissue paper market and practices in the forestry sector, Mapuche conflicts, and environmental impact. This theory explains behaviors in which there is moral hazard, in which company executives or managers made decisions that maximized private benefits such as profits or strategic positioning with immediate results, compromising the sustainability of companies with reputational, financial, and legal risks and costs. The lack of corporate governance with effective control and transparency mechanisms created the possibility for such a high level of corruption to occur, with negative results, compromising their institutionality and reputation.

As Fernández and Bajo (2012) , point outbased on Freeman’s (1984) contribution, stakeholder theory presents a business vision that goes beyond traditional approaches focused on shareholders or owners; the company interacts with a wide variety of actors who can influence its performance or be affected by it. The principle of this theory is based on corporate management aimed at creating value for groups such as local communities, customers, employees, suppliers, and other social agents. This new vision proposes a more complex stance in which corporate social responsibility plays a key role.

In the case of the Chilean forestry industry, stakeholders include indigenous communities, local governments, environmental NGOs, customers, suppliers, and workers. Governance policies on transparency and ethics must respond to the demands of these actors. The findings of the study by Pham & Yang (2025), based on agency, legitimacy, and signaling theories, are considered relevant to three main ideas: strong anti-corruption practices are positively linked to ESG transparency; companies with strong ethical orientations exhibit higher levels of ESG disclosure; and business ethics strengthens the positive association between corruption management and ESG transparency.

Taking into account the suggestion by Pollman (2021), who points out that companies should consider not only the interests of shareholders but also those of other stakeholders.

In this regard, it is necessary to assess whether the information disclosed in sustainability reports truly addresses the concerns of different strategic audiences, or whether it is a unilateral communication strategy without mechanisms for dialogue or participation.

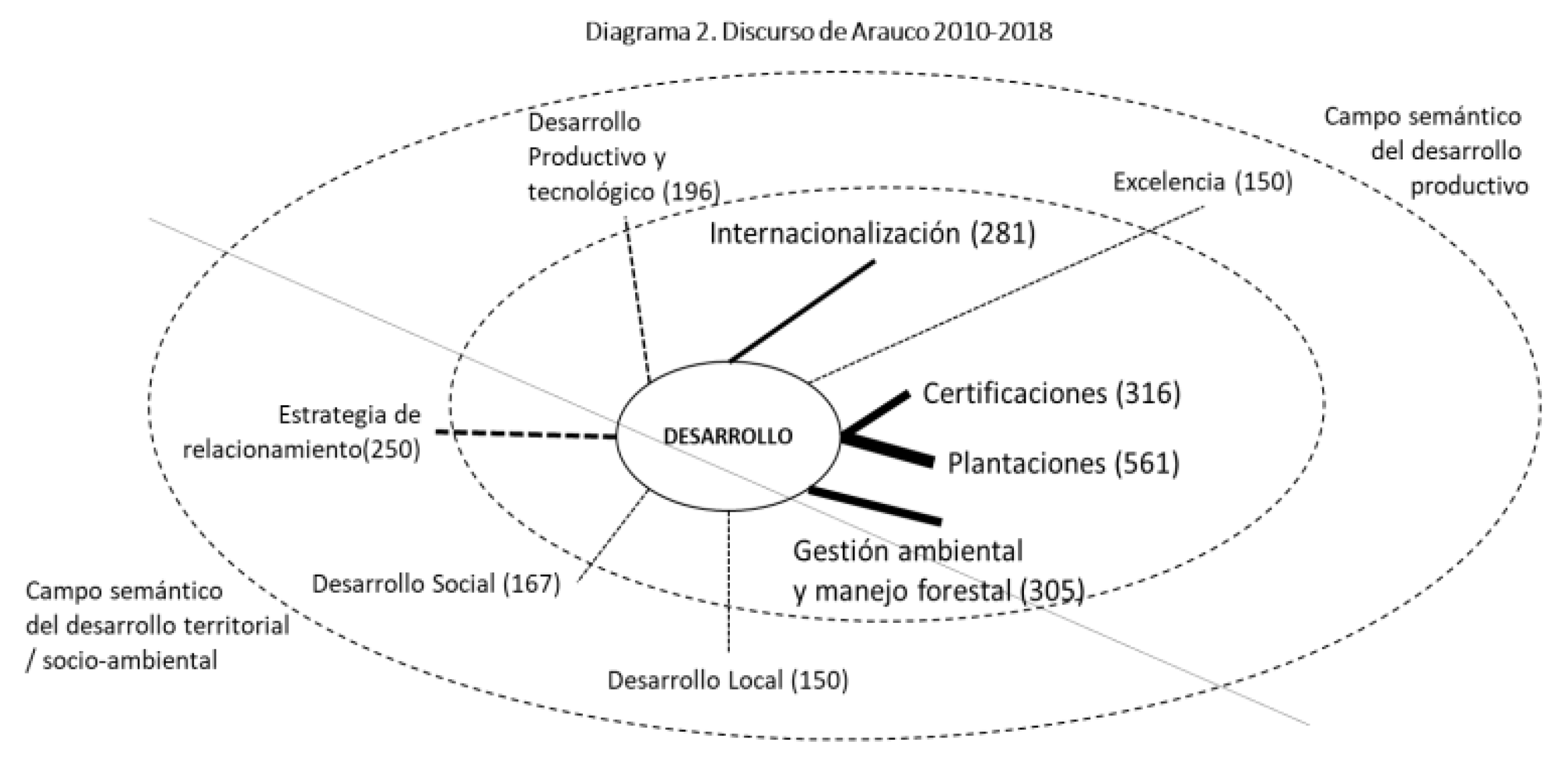

In a study conducted by Cuevas and Grosser (2022), the authors develop this structure and diagram of relationships and objectives based on Celulosa Arauco’s sustainability reports, presented as:

Figure 1.

Arauco Discourse Diagram 2010 - 2018. Note. Taken from research by Cuevas y Grosser (2022). The “sustainability” and “socialization” of forestry development: a critical content analysis of the discourse of the Arauco holding company, p. 20.

Figure 1.

Arauco Discourse Diagram 2010 - 2018. Note. Taken from research by Cuevas y Grosser (2022). The “sustainability” and “socialization” of forestry development: a critical content analysis of the discourse of the Arauco holding company, p. 20.

Arauco has made significant and ongoing efforts to build and maintain a favorable image in the environment for general acceptance by stakeholders. This discourse has not yet managed to become widely accepted. Evidence shows that conflicts between the forestry company and local communities persist due to a lack of interest in communities, a shared vision of development, and joint work. There have been no profound transformations, with these remaining only part of the discourse.

3. Materials and Methods

This research is part of a qualitative methodological strategy with a descriptive, cross-sectional approach. The objective is to identify and interpret the content that has been disclosed by CMPC and Arauco regarding their anti-corruption policies and practices in their respective sustainability reports for the year 2023.

For the content analysis, the forestry sector was defined as including publicly traded companies such as CMPC and Arauco that are regulated by the CMF. It is important to note that CMPC is also part of the Dow Jones Sustainability Index n Chile, which means it is rated as such for its good sustainability practices.

The document review defined the analysis of the official sustainability reports or annual reports of both companies for the year 2023:

- ▪ CMPC: “CMPC 2023 Annual Investment report” (CMPC S.A., 2024)

- ▪ Arauco: “Arauco 2023 Integrated Report” (Celulosa Arauco y Constitución S.A., 2023)

These documents were selected because they are the main accountability instruments published by the companies and are available to present sustainability information.

For the content analysis, the categories and subcategories were preliminarily defined based on the mandatory regulatory bodies issued by the CMF corresponding to Law 20,393 and NCG No. 461, which define the information requirements and requirements according to their structure.

This definition made it possible to construct a matrix with coding according to regulatory criteria, dimensions, themes, and transparency indicators. To this end, each regulation in the study was analyzed and categorized in relation to the disclosure of information on anti-corruption policies, practices, and mechanisms.

To establish the categories and subcategories for analyzing sustainability reports, the above analyses and classifications were considered in order to generate a document review with the following parameters:

4. Results

The main findings obtained from the content analysis of the 2023 sustainability reports of the forestry companies CMPC and Arauco have been organized into three thematic areas, which are outlined below:

4.1. Crime Prevention

In the comparative analysis of the crime prevention model between CMPC and Arauco, in accordance with Law No. 20,393, Table 2 reveals differences in the implementation and maturity of crime prevention systems.

In relation to the subcategory “Prevention Officer,” Arauco presents a more detailed structure, aligned with the principles of corporate responsibility and hierarchical supervision. CMPC indicates the unit in charge of the model, without presenting a more detailed organizational structure.

Regarding “Internal Procedures,” Arauco provides specific information on the formal reporting mechanism accessible to all stakeholders, such as employees, suppliers, and shareholders, which strengthens transparency and internal control. CMPC has a formal prevention policy based on the law, focused on monitoring, detection, and response, with certification from internal and external audits.

In the area of “Control Activities,” Arauco has a system that defines environmental obligations, sets compliance deadlines, and establishes responsible units. CMPC highlights internal mechanisms such as control activities, a code of ethics, an integrity policy, and model procedures.

In the subcategory of “Administrative sanctions,” Arauco clearly reports the results of its internal control procedures, indicating the resolution of cases with the application of sanctions. CMPC reports details of complaints received per year and their nature, classifying them according to their status. It reports 240 admissible complaints in 2023, of which 29 were related to fraud and corruption.

In summary, both companies reflect a commitment to integrity and transparency. CMPC declares a focus on certification and systemic control, while Arauco reveals complaint management and hierarchical responsibility in established processes and procedures.

4.2. Risk Management

In the analysis of Risk Management between CMPC and Arauco, different levels of maturity and disclosure of management information can be observed in Table 3.

For “Detection Procedures,” CMPC implements a management program that identifies strategic and emerging risks, although without detailing specific tools. Arauco has a structured policy and a risk matrix based on international standards, demonstrating greater technical formalization.

In the “Established Policies” subcategory, CMPC integrates its policies across various departments, addressing broad risks such as climate change. Arauco details key compliance-oriented policies, although it does not explicitly state how they are operationally linked to risk management.

Regarding the subcategory “Responsible unit,” CMPC has a broad organizational architecture with multiple committees and specialized management teams. Arauco mentions a semi-annual review team, without detailing its internal structure, suggesting less extensive governance.

For the subcategory “Information security risks,” both companies recognize cybersecurity as a key risk. Arauco aligns its framework with ISO standards and a corporate risk matrix, while CMPC uses contingency plans and an internal committee, without reference to international certifications.

Both recognize cybersecurity as a key risk; Arauco aligns its framework with ISO standards and the corporate risk matrix; CMPC integrates ISO 31000 and COSO ERM into its program.

Table 5.

Risk Management.

| Category: Risk Management | ||

|---|---|---|

| Analysis Subcategory |

CMPC | Arauco |

| Detection Procedures |

The Risk Management Program implemented aims to identify and manage the main established risks that threaten the business strategy and objectives. It includes ongoing monitoring of risks classified as emerging, physical, and transitional. It mentions that it has an Environmental Management policy. | There is a Corporate Framework and a Risk Management Policy, which are also reflected in the Corporate Risk Matrix that generates the greatest impact. The application of model statements is established based on international standards in this phase. |

| Established Policies |

Responsibility lies with different management teams whose function is to coordinate and control the implementation of policies for the prevention and mitigation of risks identified as material, including emerging risks such as climate change, transition risks, and physical risks. | Policies and mechanisms exist, such as the Code of Ethics, Crime Prevention Policy and Model, and Information Security Policy. |

| Responsible Unit |

Risk Management continuously monitors and reviews the quality and efficiency of the design and implementation of the components in order to achieve continuous improvement of the process and a risk culture within the organization. It mentions different departments that control the execution of policies: Risk Management, Finance Management, Compliance Management, Sustainability Management, Environment Management, Occupational Health and Safety Management, and the Internal Audit Unit. Committees are defined, such as the Ethics and Compliance Audit Committee, the Sustainability Committee, and the Risk Committee. | The team in charge of monitoring and managing risks classified as operational and non-operational evaluates their effectiveness every six months, reviewing policies, procedures, codes, and controls. |

| Information Security Risks |

The increase in cyberattacks represents a potential risk. CMPC and its suppliers have contingency plans in place and have adopted measures to prevent or mitigate the impact of events such as interruptions, failures, or breaches due to causes such as natural disasters, power outages, security breaches, computer viruses, or cybersecurity attacks. | A cybersecurity regulatory framework based on international ISO standards has been defined, as well as control mechanisms, technologies, and security policies that have been implemented. |

Note. Own elaboration.

4.3. Sustainability Governance

In the analysis of Sustainability Governance between CMPC and Arauco in Table 4, different levels of maturity and information disclosure on governance issues can be observed.

In the subcategory “Risk oversight by the board,” CMPC has a robust oversight structure, led by a Board Risk Committee. Arauco delegates this function to senior management, with periodic reports to the Board. CMPC’s governance is more direct and structured.

In the subcategory “Internal controls,” CMPC implements controls integrated with broad international standards, covering legal, environmental, and sustainability aspects. Arauco applies the SOX model focused on financial information.

In the “Performance Evaluation” subcategory, CMPC uses ESG audits and global standards to evaluate suppliers, prioritizing prevention and sustainability. Arauco focuses on complaint management and compliance.

With regard to the subcategory “Internal audit unit,” CMPC prioritizes a permanent and comprehensive oversight structure focused on compliance and governance, while Arauco focuses on reviewing more critical audits, specifically those classified as high risk.

In summary, CMPC presents a governance structure that is more aligned with international standards, comprehensively addressing sustainability, risks, and controls. On the other hand, Arauco maintains a focus more centered on compliance, auditing, and reporting at the management level, supervising regulatory and financial aspects. While CMPC shows greater maturity in sustainability, Arauco emphasizes internal control and compliance.

Table 6.

Sustainability Governance.

| Category: Sustainability Governance | ||

|---|---|---|

| Analysis Subcategory | CMPC | Arauco |

| Risk supervision by the board of directors | Overseen by the Risk Committee, made up of three members of the Board of Directors: Corporate Counsel, CEO, and Risk Manager. This structure is based on a clear assignment of roles and responsibilities, which allows for effective accountability. | The Risk Management Committee, led by members of senior management. The CEO is responsible for reporting on these matters to the Board of Directors. |

| Internal controls |

Supplier evaluation includes risk control, legal, environmental, and labor compliance, and a technical evaluation. This program is based on the ISO 31000 standard for the , as well as other international standards: COSO ERM and existing best practices. It is integrated with specific requirements from other standards in necessary areas, such as occupational health, safety, compliance, and sustainability. | Based on the SOX Law-based Corporate Internal Control Model, whose objective is to identify and mitigate risks associated with the reliability of the information presented in the financial statements. |

| Performance evaluation |

An ESG audit was implemented for strategic suppliers, which allows for the construction of a more resilient supply chain. For this review, the company applies international standards and methodologies such as CDP and DJSI, among others. Significant criteria are measured by applying assessments from independent organizations, based on international standards and the principles of the United Nations Global Compact. |

The Ethics and Compliance Committee oversaw compliance programs and regulatory updates. It also evaluated and resolved complaints made within the organization. |

| Internal Audit Unit |

Indicates the Internal Audit Department, with direct advice to the General Manager. Mentions the Audit, Ethics, and Compliance Committee, which directs the Internal Audit Department to ensure compliance and regulation. | The Audit Committee reviews cases audited by the Internal Audit Department that are categorized as high risk. |

Note. Own elaboration.

5. Discussion

Governance is one of the pillars of sustainability, referring to the rules, principles, processes, and practices that underpin management with structures and mechanisms that ensure transparency, accountability, responsibility, ethics, and long-term sustainability . Gutiérrez-Ponce et al. (2022) point out that academic literature indicates that good corporate governance has a positive impact on company performance. In this regard, Cardoni et al. (2022) study the relevance of the value of corporate governance policies and incorporate anti-corruption as a characteristic of sustainable governance. This conceptual framework allows us to understand how the differences between CMPC and Arauco in terms of crime prevention reflect different levels of maturity in governance.

In the crime prevention model, both companies demonstrate a commitment to corporate integrity and transparency in the management of legal and ethical risks. CMPC focuses on certifications and systematic controls, while Arauco emphasizes traceability and the accessibility of reporting channels for different stakeholders. This coincides with Armstrong (2020), who points out that internal governance mechanisms are the structures and processes designed to ensure the independence and accountability of the board through reporting and transparent disclosure, risk management, and the prevention of corruption and bribery. As Elamer & Boulhaga (2024) point out, well-defined corporate governance frameworks and internal ESG strategies mitigate adverse impacts and can transform controversies with stakeholders into opportunities for growth and reputation enhancement.

With regard to risk management, the results show that CMPC has a broad organizational structure with specialized committees and management teams, with a cross-cutting approach, unlike Arauco, which has a risk matrix based on international standards (ISO, COSO), with greater technical formalization in its application. This difference is linked to the findings of Lagasio & Cucari (2019), who contribute to the debate on corporate governance mechanisms that lead to greater ESG disclosure and highlight the need for a new approach to these issues.

In terms of sustainability governance, CMPC relies on a risk committee of the Board of Directors, with clearly defined roles, which is in line with agency theory (Jensen & Meckling, 1976), reducing information asymmetries and supervision costs, as well as clearly assigning roles and responsibilities. Arauco, on the other hand, delegates to senior management and bases its controls on the SOX Act, which limits the direct participation of the Board of Directors and generates a more operational than strategic control.

The difference observed between CMPC and Arauco can be interpreted as an example of the tension between discourse and evidence. While CMPC emphasizes broad structures, Arauco shows greater detail in sanctions and the results of complaints. This gap is consistent with the findings of Zeng & Jiang (2023), who warn that incomplete or biased disclosure can become “greenwashing,” generating a positive reputation without necessarily reflecting a real change in management. In contrast to the above, Mohammad and Wasiuzzaman (2021) point out that greater disclosure of corporate governance in environmental, social, and governance management is associated with better performance and transparency, not only improving stakeholder and investor confidence but also strengthening internal governance mechanisms by encouraging more sustainable and responsible practices.

In summary, the discussion shows that forestry companies in Chile are at an intermediate stage: although they are making progress in formalizing anti-corruption and sustainability frameworks, there are still gaps in independent verification and concrete metrics. This reinforces the idea that effective transparency must be based on data, evidence, and external audits to reduce agency costs and strengthen stakeholder confidence in a context where corruption risks are significant.

6. Conclusions

The comparative analysis between CMPC and Arauco reveals significant differences in the disclosure and management of these companies’ anti-corruption policies according to their 2023 sustainability reports. Arauco shows greater formalization in the implementation of a crime prevention model, with a policy focused on control and compliance. However, CMPC presents a more global approach, with guidelines based on a risk management structure, with little specific information on effective controls and measures. In both cases, compliance could be interpreted as more symbolic than real, considering the lack of greater detail and exposure.

Both companies disclose information showing progress with different levels of integration and exposure of regulatory frameworks such as Law No. 20,393, highlighting aspects that characterize them: CMPC in governance and Arauco in established internal control mechanisms. However, there are still gaps in the articulation between disclosed policies and concrete actions, which limits transparency and hinders the external verification of ethical commitment. It should be noted that the content analysis was carried out exclusively with sustainability reports for a single period.

Based on agency and stakeholder theories, when there are visible monitoring mechanisms responsible for prevention, controls, and internal auditing with functional independence, agency costs are reduced with less information asymmetry and reputational risk. However, when disclosure is based on discourse, with a lack of metrics and more information on investigations, sanctions, and measures, agency costs increase.

Likewise, effective transparency with data, goals, and results strengthens trust and allows organizations to legitimize themselves, with greater credibility in the eyes of investors, regulators, workers, communities, and society.

Therefore, disclosure must be carried out with evidence, independence, and external verification, which will reduce agency costs and contribute to validation by stakeholders.

Among the limitations of the study is its temporal focus on a single fiscal year, in this case 2023, which prevents the evolution of anti-corruption policies from being determined. Likewise, the exclusive reliance on institutional reports limits critical insight, especially given that this information is not reviewed by external auditors.

Future research could include a 10-year longitudinal analysis for robustness and temporal consistency to gain a deeper understanding of the link between disclosure, governance, and transparency in similar contexts.

Similarly, the methodological design could be expanded by obtaining complementary sources through semi-structured interviews with experts for triangulation.

Statement from the Research Ethics Committee

Not applicable.

Author Contributions

Conceptualization: Enrique Valenzuela and Evelyn Villarroel; methodology: Enrique Valenzuela and Evelyn Villarroel; validation: Enrique Valenzuela, Evelyn Villarroel, Lisette Sánchez and Paula Caballero; formal analysis: Enrique Valenzuela, Evelyn Villarroel, Lisette Sánchez and Paula Caballero; research: Enrique Valenzuela and Evelyn Villarroel; data curation: Enrique Valenzuela and Evelyn Villarroel; writing: Enrique Valenzuela, Evelyn Villarroel, Lisette Sánchez and Paula Caballero. All authors have read and approved the published version of the manuscript.

Institutional Review Board Statement

In this section, you should add the Institutional Review Board Statement and approval number, if relevant to your study. You might choose to exclude this statement if the study did not require ethical approval. Please note that the Editorial Office might ask you for further information. Please add “The study was conducted in accordance with the Declaration of Helsinki, and approved by the Institutional Review Board (or Ethics Committee) of NAME OF INSTITUTE (protocol code XXX and date of approval).” for studies involving humans. OR “The animal study protocol was approved by the Institutional Review Board (or Ethics Committee) of NAME OF INSTITUTE (protocol code XXX and date of approval).” for studies involving animals. OR “Ethical review and approval were waived for this study due to REASON (please provide a detailed justification).” OR “Not applicable” for studies not involving humans or animals.

Informed Consent Statement

Any research article describing a study involving humans should contain this statement. Please add “Informed consent was obtained from all subjects involved in the study.” OR “Patient consent was waived due to REASON (please provide a detailed justification).” OR “Not applicable.” for studies not involving humans. You might also choose to exclude this statement if the study did not involve humans. Written informed consent for publication must be obtained from participating patients who can be identified (including by the patients themselves). Please state “Written informed consent has been obtained from the patient(s) to publish this paper” if applicable.

Data availability statement

The raw data supporting the conclusions of this article will be available upon request from the authors.

Conflicts of Interest

The authors declare that they have no conflict of interest.

References

- Álvarez, H. Implications and effects of China’s growing importance in the Chilean forestry industry. The cases of ARAUCO and CMPC. Revista Latino-Americana de História 2017, Vol. 6. [Google Scholar]

- Araya, C. The toilet paper collusion: lexical fields in the comments of a Chilean newspaper; Journal of Linguistics, Philosophy, and Literature: Logos, 2016; Volume 26, 2, pp. 137–147. [Google Scholar] [CrossRef]

- Argandoña, A.; Morel Berendson, R. The fight against corruption: a business perspective (Notebook No. 4). In “la Caixa” Chair in Corporate Social Responsibility and Corporate Governance, University of Navarra; 2009. [Google Scholar] [CrossRef]

- Armstrong, A. Ethics and ESG. The Australasian Accounting Business and Finance Journal 2020, 14(3), 6–17. [Google Scholar] [CrossRef]

- Cardoni, A.; Kiseleva, E.; Arduini, S.; Terzani, S. From sustainable value to shareholder value: The impact of sustainable governance and anti-corruption programs on market valuation. In Business Strategy and The Environment; 2022. [Google Scholar] [CrossRef]

- Celulosa, Arauco; Constitución, S.A. 2023 INTEGRATED REPORT. 2023. Available online: https://www.arauco.com.

- Financial Market Commission (CMF). General Rule No. 461: Modifies the structure and content of the Annual Report of securities issuers and modifies and repeals the rules indicated. In Financial Market Commission; 2021. [Google Scholar]

- Cozma, A.-C.; Achim, M. V.; Safta, I. Economic and financial crime in the forest industry: internationally and in Romania. Brazilian Journal of Business 2023, 5(2), 1060–1083. [Google Scholar] [CrossRef]

- Cuevas, H.; Grosser, G. The “sustainability” and “socialization” of forestry development: a critical content analysis of the discourse of the Arauco holding company. 2022. Available online: https://orcid.org/0000-0002-4295-5652.

- Dow Jones Sustainability Chile. DOW JONES SUSTAINABILITY INDEX 2024. 2024. [Google Scholar]

- Elamer, A. A.; Boulhaga, M. ESG controversies and corporate performance: The moderating effect of governance mechanisms and ESG practices. In Corporate Social Responsibility and Environmental Management; 2024. [Google Scholar] [CrossRef]

- Empresas CMPC, S.A. Integrated Report 2023. 2024. Available online: https://www.cmpc.com/.

- Zainal, Farah Fatirah; Awis, Mahadir Ladisma; Fuzi, Sharifah Faatihah Syed Mohd. The Role of Corporate Governance in Enhancing Environmental, Social, and Governance (ESG) Disclosure. In Proceedings of the 2nd International Conference on Administrative Science (ICAS 2024); Atlantis Press 633 – 644, 2025; p. SN - 2352-5398. [Google Scholar] [CrossRef]

- Fernández, J.; Bajo, A. Stakeholder Theory, a key element of CSR, business success, and sustainability. ADRESEARCH ESIC INTERNATIONAL JOURNAL OF COMMUNICATION RESEARCH 2012, 6(6), 130–143. [Google Scholar] [CrossRef]

- Fiandrino, S.; Tonelli, A.; Devalle, A. Sustainability materiality research: A systematic literature review of methods, theories and academic themes. Qualitative Research in Accounting & Management 2022, 19(5), 665–695. [Google Scholar] [CrossRef]

- Gerged, A. M.; Salem, R. I. A.; Ghazwani, M. Corporate Anti-Corruption Disclosure and Corporate Sustainability Performance in the United Kingdom: Does Sustainability Governance Matter? Business Strategy and The Environment 2024. [Google Scholar] [CrossRef]

- Gonçalves, T.; Gaio, C.; Ferro, A. Corporate Social Responsibility and Earnings Management: Moderating Impact of Economic Cycles and Financial Performance. Sustainability 2021, 13(17), 9969. [Google Scholar] [CrossRef]

- Gutiérrez-Ponce, H.; Chamizo-González, J.; Arimany-Serrat, N. Disclosure of Environmental, Social, and Corporate Governance Information by Spanish Companies: A Compliance Analysis. Sustainability 2022, 14(6), 3254. [Google Scholar] [CrossRef]

- Ismariana, E.; Kusuma, A. F.; Permadi, D. B.; Kartodihardjo, H.; Santoso, W. B.; Maryudi, A. Corruption in Social Forestry in Indonesia. Forest and Society 2024, 8(2), 443–463. [Google Scholar] [CrossRef]

- Jensen, M.; Meckling, W. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. In Journal of Financial Economics (Issue 4); Harvard University Press, 1976; Available online: http://hupress.harvard.edu/catalog/JENTHF.html.

- Khaled, R.; Ali, H.; Mohamed, E. The Sustainable Development Goals and corporate sustainability performance: Mapping, extent and determinants. Journal of Cleaner Production 2021, 311. [Google Scholar] [CrossRef]

- Lagasio, V.; Cucari, N. Corporate governance and environmental social governance disclosure: A meta-analytical review. Corporate Social Responsibility, and Environmental Management 2019, 26(4), 701–711. [Google Scholar] [CrossRef]

- LAW NO. 20.393: ESTABLISHES THE CRIMINAL LIABILITY OF LEGAL ENTITIES FOR THE CRIMES INDICATED. (2009, December 2). Published in the Official Gazette.

- Lu, J.; Wang, J. Corporate governance, law, culture, environmental performance and CSR disclosure: A global perspective. Journal of International Financial Markets, Institutions and Money 2021, 70, 101264. [Google Scholar] [CrossRef]

- Lungu, C.; Caraiani, C.; Bojan, A. M. Double Materiality Approach and Sustainable Business Model Paradigm: A Three-Fold Analysis. European Conference on Management Leadership and Governance 2024, 20(1), 316–324. [Google Scholar] [CrossRef]

- Mohammad, W. M. W.; Wasiuzzaman, S. Environmental, Social and Governance (ESG) disclosure, competitive advantage and performance of firms in Malaysia. Cleaner Environmental Systems 2021, 100015. [Google Scholar] [CrossRef]

- OECD. OECD Glossaries Corruption: a Glossary of International Standards in Criminal Law. In Organisation for Economic Co-operation and Development; 2008. [Google Scholar]

- OECD. OECD Handbook on Public Integrity; 2020. [Google Scholar] [CrossRef]

- OECD. OECD and G20 Principles of Corporate Governance 2023; OECD Publishing: Paris, 2024. [Google Scholar] [CrossRef]

- Oh, H.; Park, S. Corporate Sustainable Management, Dividend Policy and Chaebol. Sustainability 2021, 13, 7495. [Google Scholar] [CrossRef]

- Pham, T.; Yang, Y. Does Ethics Matter? The Moderating Role of Business Ethics in Corruption Management and ESG Disclosure in Asia. In Business Ethics, the Environment and Responsibility; 2025. [Google Scholar] [CrossRef]

- Pollman, E. Corporate Social Responsibility, ESG, and Compliance. In Social Science Research Network; 2021. [Google Scholar] [CrossRef]

- Prakasa, S. U. W.; Hariri, A.; Arifin, S.; Asis, A. Forestry Sector Corruption and Oligarchy: A Case Study of the Laman Kinipan Indigenous People, Central Kalimantan. Unnes Law Journal 2022, 8(1), 87–104. [Google Scholar] [CrossRef]

- Pietro, Previtali; Paola, Cerchiello. Corporate governance and anti-corruption disclosure; Emerald Publishing Limited, 2023; Vol. 23, No. 6, pp. 1217–1232. ISSN 1472-0701. [Google Scholar] [CrossRef]

- Transparency International. Corruption perceptions index 2024. 2024. Available online: www.transparency.org.

- Undurraga, T.; Fergnani, M. Unpacking Forest Stewardship Council certification in Chile: The scope and limitations of neoliberal market-driven governance for achieving sustainable development. In Environmental Policy and Governance; 2024. [Google Scholar] [CrossRef]

- Valdebenito, A. Corporate Transparency in Chile: Voluntary Disclosure of Corruption in Major Chilean Companies. 2018. [Google Scholar] [CrossRef]

- Zeng, L.; Jiang, X. ESG and Corporate Performance: Evidence from Agriculture and Forestry Listed Companies. Sustainability 2023, 15, 6723. [Google Scholar] [CrossRef]

Table 1.

Governance Dimension.

| Authors | Title | Year | Relevant Aspects |

|---|---|---|---|

| Wan Mohammad Wan Masliza, Shaista Wasiuzzaman (Mohammad & Wasiuzzaman, 2021) |

Environmental, Social and Governance (ESG) disclosure, competitive advantage and performance of firms in Malaysia |

2021 | The effect of ESG (eviromental, social, and governance) disclosures on the performance of publicly traded organizations in Malasia is disclosed. ESG disclosure is shown to improve and positively impact company performance. |

| Hyunmin Oh, Sambock Park (Oh & Park, 2021) |

Corporate Sustainable Management, Dividend Policy and Chaebol | 2021 | This research references agency and signaling theory and how sustainable corporate management influences dividend policy in Korean companies. A positive relationship between corporate management and dividends is determined. |

| Tiago Gonçalves, Cristina Gaio y André Ferro (Gonçalves et al., 2021) |

Corporate Social Responsibility and Earnings Management: Moderating Impact of Economic Cycles and Financial Performance | 2021 | In earnings management and corporate social responsibility, the findings show a negative relationship between the two. This confirms that managers of companies with greater social responsibility behave more ethically, which results in higher-quality financial information. |

| Jing Lua, Jun Wang | Corporate governance, law, culture, environmental performance and CSR disclosure: A global perspective | 2021 | The research highlights good corporate governance practices, such as the separation of CEO functions, the existence of ESG committees, and gender diversity on boards, and their positive association with better environmental performance and greater disclosure of CSR information. One of the findings indicates that listed companies have better environmental performance and, therefore, disclose more information. |

Note. Prepared by the author based on articles included in the table.

Table 2.

Chile – Corruption Perceptions Index, Transparency International.

| Year | Corruption Ranking | Corruption Index |

|---|---|---|

| 2024 | 32 | 63 |

| 2023 | 29 | 66 |

| 2023 | 27 | 67 |

| 2021 | 27 | 67 |

| 2020 | 25 | 67 |

| 2019 | 26 | 67 |

| 2018 | 27 | 67 |

| 2017 | 26 | 67 |

Note. Data obtained from Chile corruption perception index, compiled by Chile Transparente. https://www.chiletransparente.cl/indice-de-percepcion-de-corrupcion/.

Table 3.

Categories and subcategories for reviewing CMPC and Arauco sustainability reports.

| Category | Subcategory for analysis | Regulatory source or standar |

|---|---|---|

| Crime prevention model | a. Prevention manager b. Internal procedures c. Control Activities d. Administrative sanction |

Law 20.393 |

| Governance | a. Supervision by the Board of Directors b. Internal Control c. Performance evaluation d. Internal Audit Unit |

NCG N.º 461 |

| Risk management | a. Detección procedures b. Established policies c. Responsible unit d. Information security risks |

NCG N.º 461 |

Note. Table prepared based on analysis of NCG N.º 461 (CMF, 2021) and Law N.º 20.393. (Law 20.393, 2009).

Table 4.

Crime Prevention Model.

| Category: Crime Prevention Model | ||

|---|---|---|

| Analysis Subcategory | CMPC | Arauco |

| Prevention Officer |

The model presented shows that the Corporate Prosecutor’s Office and Compliance Management are responsible for the crime prevention model. | It mentions the assignment to the Legal and Compliance Manager, with the Board of Directors having the power to appoint and remove the Crime Prevention Officer. |

| Internal Procedures |

Based on the law, it outlines a crime prevention policy focused on monitoring, prevention, detection, and response, with certification from Internal Audit and an external company. | This procedure defines the mechanism for investigating complaints filed by suppliers, employees, customers, shareholders, or other related parties. |

| Control Activities |

It mentions various actions in the control environment such as a code of ethics, reporting channel, and crime prevention procedure for monitoring. |

The company’s environmental obligations are explicitly defined, including both the unit responsible for monitoring compliance and the timeframe established for monitoring and enforcement. |

| Administrative Sanctions |

It details crimes such as smuggling of goods, customs fraud, and false customs declarations. It details the nature of the complaints. Of those admissible, 240 were resolved, of which 29 corresponded to fraud and corruption. |

Of the investigations carried out and resolved, 24 resulted in the termination of employment. Of all the complaints investigated and resolved in 2023, 15 were related to fraud or theft. |

Note. Own elaboration.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.