Submitted:

03 December 2025

Posted:

04 December 2025

You are already at the latest version

Abstract

The Role of Artificial Intelligence (AI), Internet of Things (IoT), and Blockchain in Augmented Finance Augmented finance is emerging as an important approach to tackle the complex financial challenges that accompany climate change. This systematic review aims to provide existing research, identifying how these technologies may help in sustainable finance. Thus, following the PRISMA guidelines, we reviewed and analysed 42 peer-reviewed studies released between 2018 and 2025. Our results are applicable in three general areas: (1) increased MRV of the environmental impacts by employing IoT and blockchain, to ensure transparency and traceability, (2) better physical and transition risk control using predictive AI modelling and (3) better ESG analysis and the detection of greenwashing and risk reduction via alternative data. We highlight the power of these technologies to address stubborn problems such as information asymmetry and transparency holes in impact chains. However, significant challenges persist, such as algorithmic bias, difficult data governance, and regulatory lag. The present study contributes to this landscape by offering a scientific framework of augmented finance in a climate context. It also suggests a proposed future research agenda with emphasis on impact assessment, algorithmic transparency, and impact on financial stability.

Keywords:

augmented finance

; climate change

; artificial intelligence

; IoT

; blockchain

; ESG

; systematic review

; sustainable fintech

1. Introduction

IPCC reports (IPCC, 2022) show that climate change is a significant threat to the stability of the global economy and the financial system.The growing number and severity of climate-related events underscore the importance of financial systems' ability to handle them (Bolton et al., 2020). As a result, the financial sector is under increasing pressure to ensure that capital flows align with the goals of the Paris Agreement (NGFS, 2022). This transition is impeded by structural issues, including challenges in measuring and verifying environmental impact, the intricacy of modeling climate-related risks, and the prevalence of greenwashing, which has diminished investor confidence (Berg et al., 2022; Campiglio et al., 2018). Traditional financial instruments and risk assessment approaches often fail to adequately address the nonlinearity and systemic characteristics of these difficulties (Weyant, 2017).

In this setting, augmented finance becomes a revolutionary model. Augmented finance transcends conventional fintech, which primarily focuses on automating existing operations.

It is a systemic integration of disruptive technologies such as artificial intelligence (AI), the Internet of Things (IoT), and blockchain that expands the cognitive and operational capabilities of financial actors (ACPR, 2021; Hamdouni, 2025).

Augmented finance brings about this transformation through three synergistic capabilities: (1) cognitive augmentation, where artificial intelligence models unpredictability and identifies weak signals within heterogeneous data for forward-looking analysis; (2) physico-digital integration, using the Internet of Things (IoT) to generate a verifiable, real-time digital representation of physical environmental impacts; and (3) decentralised trust certification, leveraging blockchain to establish immutable auditability and traceability within climate impact chains, thereby reducing information asymmetries.

The use of these technologies is already underway. AI helps us model physical and transition risks by analysing large amounts of data, such as satellite images and business reports (Battiston & Monasterolo, 2020; Giglio et al., 2021). IoT enables real-time monitoring of environmental indicators, such as carbon emissions, which provides green bonds and carbon markets with reliable data (Jia & Bo, 2025; Frikha & Mrad, 2025). Blockchain, on the other hand, fosters trust and transparency through smart contracts that automate verification and distributed ledgers that prevent double-counting in carbon credit markets (Mei et al., 2025; Hyun, 2024).

Scientific research has not yet thoroughly examined the combined impact of artificial intelligence, the Internet of Things, and blockchain technology on the financial sector's response to climate change (Gomber et al., 2018). Therefore, the objective of this study is to examine the following research question to fill this gap: How are technologies such as artificial intelligence, the Internet of Things, and blockchain being leveraged in scientific research to address climate change mitigation and adaptation issues in the financial sector?

This study provides a comprehensive analysis of the current research landscape, based on a systematic review of academic studies published between 2018 and 2025. It synthesizes empirical findings and highlights both emerging themes and unresolved challenges.Moreover, it enhances the field by introducing a structured framework for comprehending augmented finance in climate action. It delineates a prospective research agenda centered on impact assessment, algorithmic transparency, and systemic risk.

2. Systematic Review Methodology

This study followed a systematic review, as it is effective for conducting a thorough investigation in a specific field, following the instructions of Khatib et al. (2023).

Systematic reviews represent a robust methodology widely used in the social sciences (Petticrew & Roberts, 2008, Khatib et al., 2023). It is often used in finance because it helps reduce the risk of subjective or biased conclusions. Also, Sierra-Correa and Kintz (2015) identify three specific advantages: (1) it formulates a clear research question to enable thematic analysis of the system, (2) it delineates criteria for content inclusion and exclusion, and (3) it seeks validation.

The SLR process began with drafting suitable review inquiries in accordance with PRISMA's guidelines. A three-phase document search approach was developed and implemented, comprising identification, screening, and eligibility stages.

2.1. PICOS Framework

This study uses a methodology based on established standards for systematic reviews (Page et al., 2021). The PICOS framework (Population, Intervention, Comparison, Outcomes, Study Design) is used to explain the research question.

· Population: The financial sector and its stakeholders (banks, insurers, capital markets, etc.).

· Intervention: The application of AI, IoT and/or blockchain by the financial institutions

· Comparison: Traditional financial practices/financial practices using technological approaches.

· Results: Impacts on climate change mitigation, adaptation, climate risk management, ESG transparency and the fight against greenwashing.

· Type of studies: Peer-reviewed empirical or theoretical academic articles.

The PRISMA guidelines recommend using this framework to ensure a structured systematic methodology (Page et al., 2021).

2.2. Research Strategy

Identification involves exploring synonyms, related terms and multiple iterations of the study's main keywords: “augmented finance” and “climate action”. This method broadens the scope of the database search, revealing articles relevant to the analysis.

The choice of keywords was inspired by Okoli's method (2015) as well as terms from previous studies, Scopus recommendations, and comments from experts in the field. A systematic search was conducted in June 2025 in the Scopus, Web of Science, ScienceDirect, and JSTOR databases.

In this context, it should be noted that although ‘augmented finance’ is the central theme of this review, the search strategy used more general terms for technologies (AI, IoT, blockchain). This approach was implemented, on the one hand, because the concept of augmented finance has not yet been widely studied and, on the other hand, to ensure comprehensive coverage of the relevant literature.

Subsequently, the following Boolean query was employed, as seen in Table 1.

2.3. Eligibility Criteria

The inclusion criteria stated that publications must be written in English, published between 2018 and 2025, peer-reviewed, and demonstrate a direct link to finance, climate action, and the specified technologies. The selected articles provide robust empirical or conceptual models that are directly related to the research question.

Within this framework, editorials, theses, non-scientific publications, and works not directly related to the financial sector were excluded from the analysis.

The study period was chosen to identify the most recent and relevant articles on the maturation of critical technologies, particularly AI and blockchain, and their application in the financial sector.

2.4. Data Selection

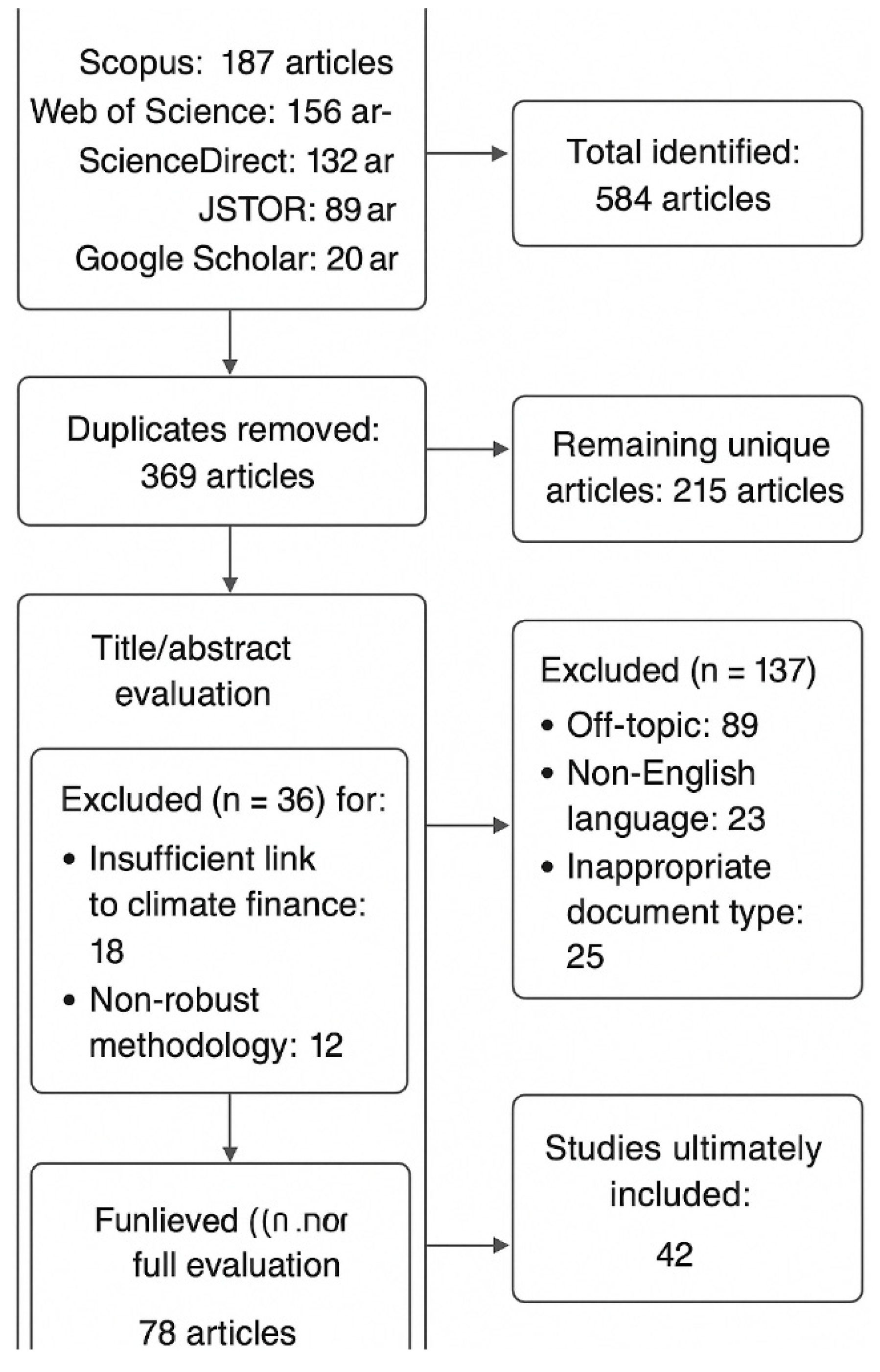

The selection process1, as presented in the PRISMA diagram (Figure 1), began with an initial compilation of 584 articles. After eliminating duplicates and further review, 42 articles were ultimately included in this study.

Data extraction then took place, using a standardized table. This table included the authors, publication year, research methods, technologies employed, primary findings, and identified limitations. The selection process is summarized in Figure 1. PRISMA diagram.

This PRISMA diagram provides complete traceability of the selection process and meets the methodological standards required for a high-quality systematic review.

3. Results and Summary

An examination of the 42 selected articles reveals an emerging but constantly evolving field of research, as shown in Table 2.

A more detailed analysis of the research landscape, presented in Table 3, reveals a geographical concentration of studies originating in developed countries, which account for nearly 85% of publications. Conversely, developing nations are inadequately represented, comprising roughly 5% of research output. This gap underscores a notable geographical bias in academic discourse.

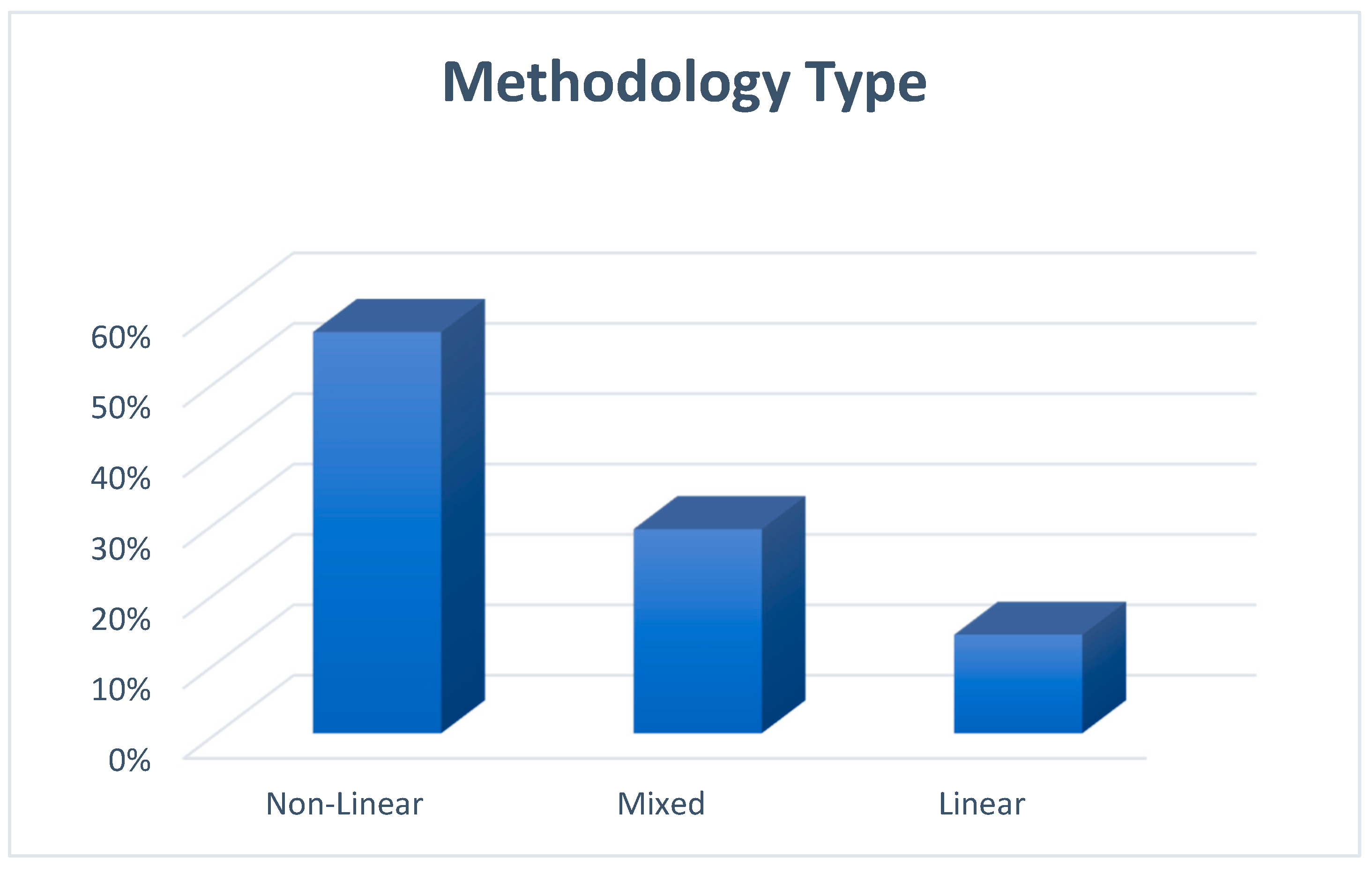

An analysis of methodological approaches shows a predominance of non-linear models, as presented in Table 4 below.

The research landscape is primarily dominated by the quantitative methodologies, focusing especially on machine learning and various advanced data analysis tools. Qualitative methods are vital to getting a sense of the context on the other hand.

Also, mixed methods are becoming more popular because they give more detailed and complete information. The study also shows that different areas have their own areas of expertise. For instance, studies in North America look at ESG analysis, spotting greenwashing, and AI ethics; studies in Europe look at blockchain applications, regulatory frameworks, and climate risk assessment; and studies in Asia look at IoT monitoring, fintech innovation, and emissions tracking. Other areas tend to focus on niche applications and specific use cases, which adds to the field as a whole by giving it more specialized knowledge.

Figure 2.

Methods of analysis.

A quantitative study reveals that non-linear methodologies employing AI constitute more than fifty percent of all research endeavors. This emphasizes that the core of contemporary augmented finance research lies in machine learning's ability to model complex systemic risks. The widespread use of mixed-methods research indicates a trend towards hybrid solutions that combine AI with other technologies for useful, effective applications.

The analysis indicates a disparity in emphasis among the three principal technologies, with artificial intelligence and machine learning comprising the majority (57.1%) of studies, underscoring their pivotal position in data analysis, forecasting, and automation within climate finance.

Blockchain technology is a popular (26.2%) technology for transaction frameworks whose usage adds transparency, traceability, and even allows security. At the same time, Internet of Things, which is seen in a smaller percentage (16.7%) of studies, has an important role for real-time data collection and monitoring. In particular, such integration is on the rise. A number of studies that have combined IoT and blockchain to produce integrated solutions demonstrate this.

3.1. Enhancing Measurement, Reporting, and Verification (MRV)

The existing scholarship underscores the pivotal function of the Internet of Things (IoT) and blockchain technology in establishing irrefutable "field truth," thereby addressing a fundamental data credibility crisis in environmental finance. This aligns with institutional theory (North, 1991), which emphasizes how technological innovations can create new institutional frameworks for verifying and enforcing agreements. Some research illustrates how IoT sensors and satellite data facilitate real-time, asset-level measurement, moving beyond traditional estimated data to furnish financiers with information of unprecedented granularity (Jia & Bo, 2025; Frikha & Mrad, 2025).

Additionally, blockchain technology establishes immutable registries for carbon credits and tokenized green bonds (Mei et al., 2025; Hyun, 2024); a notion rooted in transaction cost economics (Williamson, 1985) by significantly diminishing verification and enforcement expenses.

Recent research by Zhang et al. (2024) demonstrates how this convergence creates a technological framework that directly addresses substantial information asymmetries, thereby enhancing market integrity and potentially increasing liquidity for green assets.

3.2. Using AI to Manage Climate Risk

AI (artificial intelligence) is quickly becoming the most popular tool for understanding and measuring the complicated, non-linear aspects of climate-related financial risks.

This application is based on complexity theory (Simon, 1962), which provides a framework for understanding and modeling systems that exhibit emergent, nonlinear phenomena, like the relationship between climate and finance.

Machine learning methods evaluate physical risks by analysing extensive datasets to predict portfolio exposure with unprecedented precision (Battiston & Monasterolo, 2020; Giglio et al., 2021). A recent study by Bingler et al. (2022) utilized NLP to evaluate the quality of corporate climate reports, revealing substantial discrepancies between rhetoric and practical indicators. Simultaneously, regarding transition risks, AI-driven text analysis methodically assesses business strategic alignment with climate scenarios (Bingler et al., 2022), utilizing signaling theory (Spence, 1973) to differentiate between genuine promises and insincere "cheap talk." Research conducted by Giglio et al. (2021) substantiates that these AI technologies are radically revolutionizing climate risk management from a qualitative, retrospective practise into a predictive discipline.

3.3. ESG Analysis and the Mitigation of Greenwashing

In light of rising ESG ratings and the potential for greenwashing, AI provides enhanced investigative capabilities that transcend the limitations of conventional reporting. This approach is grounded in legitimacy theory (Suchman, 1995), which explains how organisations manage perceptions and the role of external verification in maintaining legitimacy. Research (Grewal et al., 2019) demonstrates the use of NLP to scrutinize alternative data sources and uncover controversies absent from sustainability reports. A recent analysis by Marquis and Toffel (2016) has led to the development of algorithms to detect semantic discrepancies between companies' environmental claims and their actual practises (Marquis & Toffel, 2016), providing a powerful tool for identifying greenwashing. AI-based methodologies, as analysed in the study by Khlifi et al. (2025), enable a more dynamic assessment of non-financial performance. This allows investors to hold companies accountable within the framework of stakeholder theory (Freeman, 1984), thereby promoting a more authentic sustainable financial ecosystem.

4. Discussion

This systematic review brings an emerging body of evidence to demonstrate how augmented finance can transform the world and the degree to which it carries a great deal of promise and many issues yet to be solved. The analysis of the chosen cases emphasizes the centrality of this domain, and indicates a substantial change in the core of the financial system in response to the most pressing market issue of our time: climate change. These technologies improve the way financial professionals see and understand things, which goes beyond just making traditional processes work better.

But they do allow for a major change from a system that funds the economy to one that needs to be focused on a long-term future.

4.1. New Approach: Towards an Integrated Technology Infrastructure

The literature confirms that AI, IoT, and blockchain are not merely incremental tools but fundamental technologies reshaping the architecture of climate finance. They do not achieve maximum value when used in isolation, but when conceptualised as an integrated element covering the entire data lifecycle, from capture to verification, analysis, and transaction.

This research validates the distinct and supplementary worth of each technology. The chosen cases demonstrate that IoT delivers real-time, accurate data on environmental variables, beyond estimates to offer direct measurements.

Jia & Bo (2025) illustrate that satellite data can identify companies' GHG emissions with unparalleled spatial resolution, whereas Pourrahmani et al. (2025) reveal that IoT sensors in supply chains generate verifiable data trails, markedly diminishing reporting uncertainty for green finance.

Simultaneously, blockchain offers an unalterable and transparent ledger for documenting and executing transactions of this validated data. Mei et al. (2025) and Hyun (2024) emphasize its function in establishing tamper-proof registries for carbon credits and tokenized green bonds. This directly alleviates the risks of fraud and double-counting that have traditionally compromised trust in environmental markets.

AI also provides the predictive and analytical power needed to transform this verified data into actionable insights. At this level, Battiston & Monasterolo (2020) use network modelling and machine learning to identify climate risk "hot spots" that are not considered in sovereign bond pricing. Bingler et al. (2022) also use NLP to show big differences between what companies say about climate change and what they actually do about it.

The synthesis of these studies highlights their powerful synergy. Indeed, an integrated technological tool can create a closed-loop system: IoT sensors provide verified real-time data on carbon sequestration in a forest; this data is indestructibly recorded on a blockchain; a smart contract on the identical blockchain automatically issues a carbon credit based on this data; and AI models then analyse broader market and environmental data to price and manage the risk of these credit portfolios accurately.

This system directly addresses the core problem of information asymmetry in green finance, creating a verifiable and auditable chain of custody for environmental impact that can unlock capital at scale by building trust.

This leads to a paradigm shift in risk and impact assessment. Indeed, the available data points to a fundamental shift from static, retrospective, and sometimes subjective assessments to dynamic, forward-looking, and quantitative disciplines. Grewal et al. (2019) and Marquis & Toffel (2016) demonstrate that AI, particularly NLP, extends ESG analysis beyond selected annual sustainability reports to provide a comprehensive, continuous view of corporate behaviour, drawing on alternative data such as news media and litigation records. This enables the detection of greenwashing by identifying semantic discrepancies between discourse and action. Similarly, the work of Giglio et al. (2021) shows how machine learning models enable a bottom-up, asset-level understanding of physical climate risks, going beyond rough regional averages to model the specific exposure of individual properties or infrastructure to hazards such as flooding or wildfires. The changes mentioned in the literature review show a shift towards a strategic, risk-based and opportunity-focused approach to sustainable finance, at the expense of a rules-based and compliance-focused approach.

4.2. Challenges Faced by Augmented Finance

The literature reviewed shows that there are big problems that could make an improved financial system less effective and stable. These problems go beyond technicalities to include basic questions of governance, ethics, and systemic risk.

The introduction of AI carries the risk of perpetuating or worsening existing biases. Dignum (2019) contends that models trained on historical data that inadequately represent certain regions (e.g., countries in the Global South) or industries would consistently misjudge risks and opportunities. The "climate penalty" this could create for developing nations may entail a lack of green capital for adaptation and essential transition. This goes beyond the social biases to "climate data biases," where inadequate data provided by existing IoT sensors in vulnerable regions reduces our knowledge regarding potential physical threats in these regions, which can result in a feedback loop that is particularly acute from small data inputs. The issue is therefore not only technical but also deeply ethical, requiring research initiatives and regulations focused on representative data acquisition and algorithmic fairness.

Furthermore, the objective of a fully integrated data ecosystem is hindered by the intricate nature of data governance. Consequently, the primary issues identified in the investigations are as follows: The absence of standardized IoT data formats and blockchain protocols results in fragmented systems, obstructing the seamless flow of data necessary for comprehensive analysis (D'Orazio, 2022). - Data quality: While IoT enhances objectivity, it simultaneously introduces new challenges related to sensor calibration, maintenance, and data validation that must be addressed to ensure reliability. The use of alternative data, such as high-resolution satellite images of private properties and social media scraping for ESG research, raises serious privacy concerns and complicated questions about who owns and can use the data (Zetzsche et al., 2020). The North-South split in technological capability and focus: An examination of the geographical distribution and concentration of research shows a big difference between industrialized and developing countries. Most of the research comes from developed countries and focuses on things like optimising complex financial derivatives (Battiston & Monasterolo, 2020), finding greenwashing in corporate disclosures (Marquis & Toffel, 2016), and creating regulatory frameworks for advanced financial technologies (Zetzsche et al., 2020).

Conversely, applications pertinent to developing nations, such as cost-effective IoT technologies that allow smallholder farmers to engage with carbon markets or blockchain platforms for transparent monitoring of adaptation funds, remain relatively underexplored. This presents a dual risk: first, developing the regulatory environment for augmented finance without first taking into account the requirements of developing economies, and second, creating this new form of technological dependency that would see developing economies become consumers of externally designed systems rather than architects of solutions that respect their unique contexts and vulnerabilities. The disparity creates an ethical and practical dilemma, as the effectiveness of global climate action depends on an equitable and comprehensive transition.

4.3. Developing a Framework for Evaluating the Impacts of Augmented Finance

This review indicates that technologies have the potential to alter monetary systems; however, a significant question remains: how can we ascertain their actual impact on the climate crisis? The current literature primarily focuses on technological outputs and process efficiencies, resulting in a notable gap in the assessment of final environmental outcomes (Berg et al., 2022; Khlifi et al., 2025). We propose methods for developing an Impact Assessment Framework for Augmented Finance. This framework will utilize a four-tiered logic model that progresses from technological inputs to the ultimate environmental impact. This resembles the functioning of other impact evaluation methods (Giglio et al., 2021). To evaluate the highest level—the definitive environmental result—rigorous methodologies are essential. This includes counterfactual analysis to determine the technology's impact and the use of AI-generated baseline scenarios to model emissions without the intervention (Battiston & Monasterolo, 2020). The technologies under investigation possess the capability for self-evaluation. The Internet of Things (IoT) enables direct and real-time measurement of greenhouse gas (GHG) concentrations (Jia & Bo, 2025). Blockchain offers a permanent and transparent record for impact claims, preventing double counting and ensuring data security (Mei et al, 2025). Artificial intelligence (AI) offers sophisticated modeling techniques for precise attribution and forecasting of long-term climate effects (Giglio et al., 2021).

5. Conclusions

This study sets out the theoretical and practical framework for a responsible development of augmented finance and discusses key issues that demand urgent attention. This report has important effects on policymakers. We need to make laws specific to these kinds of technologies. These regulations need to go beyond the way money works now. They should make policies that can evolve as AI and blockchain technology get better. This will keep the economy stable and help things go ahead. Governments should also work to make sure that there are standard data methods for reporting environmental impacts so that information is correct, transparent, and easy to compare across platforms and borders. Regulatory organisations must mandate that financial institutions employing AI for ESG assessment or risk management adopt explainable AI (XAI) principles and undergo frequent audits to identify bias, thereby guaranteeing fairness and transparency in automated procedures.

Firstly, financial institutions must invest strategically in technology-integrated governance. In this context, these institutions should invest not only in the technologies themselves but also in internal governance structures, including cross-functional teams of data scientists, financial analysts, and sustainability experts, to manage these new tools effectively.

Also, to overcome data fragmentation, these institutions should explore collaborative initiatives (e.g., for climate risk data) using privacy-enhancing technologies, thereby sharing information without compromising proprietary data.

Indeed, the financial sector should actively participate in multi-stakeholder initiatives to co-develop the technical and ethical standards that will shape the future of augmented finance.

In this context, these institutions need to invest in the technologies as well as in governance structures inside the institutions, with cross-functional teams of data scientists, financial analysts, and sustainability experts handling these new tools. Also, to offset data fragmentation, organizations should consider joint projects (such as on climate risk data) leveraging privacy-enhancing technologies to share information without putting proprietary data at risk. Certainly, the financial services industry ought to engage in a multistakeholder cooperation to co-develop the technical and ethical standards that will dictate the future of augmented finance. As such, this study could provide opportunities for further developments. On the one hand, it is important to understand how augmented financial tools actually reduce emissions or increase climate resilience in investment portfolios. However, for new technologies, it is necessary to explore potential systemic risks, such as the contagion effects of algorithmic failures associated with climate risk assessment.Finally, this study has certain limitations. First, the nascent nature of this field has meant that the study is based on a relatively small sample of studies (n = 42), many of which are conceptual or based on prototypes, limiting the scope for empirical generalisation. Furthermore, the rapid evolution of the technologies discussed means the landscape is likely to continue changing rapidly.

In conclusion, while augmented finance has transformative potential to recalibrate finance into a precise, transparent, and powerful instrument for climate action, its trajectory is not predetermined. Realising this potential will require collaborative efforts to regulate its development and rigorously evaluate its impact in the real world.

Funding

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

The selection process, illustrated by the PRISMA diagram (Figure 1), was as follows:

1. Identification:

· Scopus: 187 articles

· Web of Science: 156 articles

· ScienceDirect: 132 articles

· JSTOR: 89 articles

· Google Scholar: 20 articles

→Total: 584 articles identified via databases.

2. Screening:

· Duplicates removed: 369 articles

→Remaining unique articles: 215 articles

3. Eligibility: Evaluation based on title/abstract

Excluded (n = 137) for:

· Off-topic: 89 articles

· Non-English language: 23 articles

· Inappropriate document type: 25 articles

→ Selected for full evaluation: 78 articles

4. Inclusion: Full-text assessment

Excluded (n = 36) for:

· Insufficient link to climate finance: 18 articles

· Non-robust methodology: 12 articles

· Undetected duplicates: 6 articles

→42 articles selected for synthesis analysis after full reading.

The data extracted from each article was compiled in Table 1, including: author, year, study objective, methodology, technologies studied, and main results.

References

- ACPR. (2021). The challenges of technological transformation in finance (Augmented finance). DOI: efaidnbmnnnibpcajpcglclefindmkaj/https://acpr.banque-france.fr/system/files/import/acpr/medias/documents/20220906_acpr_en_2021_book_web.pdf.

- Adadi, A., & Berrada, M. (2018). Peeking Inside the Black-Box: A Survey on Explainable Artificial Intelligence (XAI). IEEE Access, 6, 52138-52160. DOI: https://ieeexplore.ieee.org/document/8466590.

- Afroditi, A. (2025). Policy implications of the “Corporate Sustainability Due Diligence Directive” in the industry of logistics, Transportation Research Procedia, (83), 55-62. [CrossRef]

- Ajakwe, I. U., Kanu, V.I., Simeon, O. A., Dong-Seong, K. (2025). eBCTC: Energy-efficient hybrid blockchain architecture for smart and secured K-ETS, Cleaner Engineering and Technology, 29. [CrossRef]

- Alves, T., Tiago, E.M., Nelson, O.S., Jorge, H.C.O, Talita, B.T., Wesley, R.S.F. (2020). Green supply chain management in Latin America: Systematic literature review and future directions. Environmental Quality Management. 30(2). [CrossRef]

- Battiston, S., & Monasterolo, I. (2020). A climate risk assessment of a sovereign bond portfolio. Nature Climate Change, 10(11), 1012–1018. DOI: efaidnbmnnnibpcajpcglclefindmkaj/https://web.stanford.edu/group/emf-research/docs/sm/2019/wk2/MonasteroloPricingClimate.pdf.

- Berg, F., Kölbel, J. F., & Rigobon, R. (2022). Aggregate Confusion: The Divergence of ESG Ratings. Forthcoming Review of Finance, 26(6), 1315-1344. [CrossRef]

- Bingler, J. A., Kraus, M., & Leippold, M. (2022). Cheap talk and cherry-picking: What ClimateBert has to say on corporate climate risk disclosures. Finance Research Letters, 47(3), DOI: https://www.sciencedirect.com/science/article/pii/S1544612322000897.

- Bissoondoyal-Bheenick, E., Scott, B., Rob, L., Angel, Z. (2024). ESG rating disagreement: Implications and aggregation approaches, International Review of Economics & Finance. [CrossRef]

- Bolton, P., Després, M., Pereira da Silva, L. A., Samama, F., & Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change. Bank for International Settlements. DOI: ://efaidnbmnnnibpcajpcglclefindmkaj/https://www.bis.org/publ/othp31.pdf.

- Buchak, G., Matvos, G., Piskorski, T., & Seru, A. (2018). Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics, 130(3), 453–483. DOI: https://www.sciencedirect.com/science/article/abs/pii/S0304405X1830237X.

- Campiglio, E., Dafermos, Y., Monnin, P., Ryan-Collins, J., Schotten, G., & Tanaka, M. (2018). Climate change challenges for central banks and financial regulators. Nature Climate Change, 8(6), 462–468. DOI: https://www.nature.com/articles/s41558-018-0175-0.

- Dignum, V. (2019). Responsible Artificial Intelligence: How to Develop and Use AI in a Responsible Way. Springer. DOI: https://link.springer.com/book/10.1007/978-3-030-30371-6.

- Desnos, B., Le Guenedal, T., Morais, P. & Roncalli, T. (2023). From Climate Stress Testing to Climate Value-at-Risk: A Stochastic Approach. SSRN. DOI: https://ssrn.com/abstract=4497124 or. [CrossRef]

- D'Orazio, P. (2022). Towards a post-pandemic policy framework to manage climate-related financial risks and sustainability goals. Ecological Economics, 1368-1382. [CrossRef]

- Dong, H., Hu, Y., Yang, Y., & Jiang, W. (2023). A Multi-Strategy Integration Prediction Model for Carbon Price. Energies, 16(12), 4613. [CrossRef]

- Freeman, R. E. (1984). Strategic Management: A Stakeholder Approach. Pitman.DOI: https://www.cambridge.org/core/books/strategic-management/E3CC2E2CE01497062D7603B7A8B9337F.

- Frikha, M. A., & Mrad, M. (2025). AI-Driven Supply Chain Decarbonization: Strategies for Sustainable Carbon Reduction. Sustainability, 17(21), 9642. [CrossRef]

- Ge, Y., Yang, X. (2025). AI adoption and ESG performance: Evidence from China, International Review of Economics & Finance, 104. [CrossRef]

- Giglio, S., Kelly, B., & Stroebel, J. (2021). Climate Finance. Annual Review of Financial Economics, 13, 15-36. DOI: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3957028.

- Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), 220-265. [CrossRef]

- Grewal, J., Riedl, E. J., & Serafeim, G. (2019). Market Reaction to Mandatory Nonfinancial Disclosure. Management Science, 69(2), 787-810. DOI: https://ideas.repec.org/a/inm/ormnsc/v65y2019i7p3061-3084.html.

- Gutierrez-Bustamante, M., & Espinosa-Leal, L. (2022). Natural Language Processing Methods for Scoring Sustainability Reports—A Study of Nordic Listed Companies. Sustainability, 14(15), 9165. [CrossRef]

- Hamdouni, A. (2025). The Role of Artificial Intelligence in Enhancing ESG Outcomes: Insights from Saudi Arabia. Journal of Risk and Financial Management, 18(10), 572. [CrossRef]

- Hyun, S. (2024). Green Digital Finance: Tokenization of Green Bonds and Carbon Credits. Yonsei University-FRTC of Japan FSA.DOI://efaidnbmnnnibpcajpcglclefindmkaj/https://www.fsa.go.jp/frtc/kenkyu/event/20240329/05_HYUNSuk_GDF_Tokyo.pdf.

- IPCC. (2022). Climate Change 2022: Impacts, Adaptation and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report. DOI: https://www.ipcc.ch/report/ar6/wg2/.

- Jia, H., & Bo, H. (2025). Estimating global anthropogenic CO2 emissions through satellite observations, Environmental Research, 279(1). [CrossRef]

- Judy, L., Bell, R., & Stroombergen, A. (2019). A Hybrid Process to Address Uncertainty and Changing Climate Risk in Coastal Areas Using Dynamic Adaptive Pathways Planning, Multi-Criteria Decision Analysis & Real Options Analysis: A New Zealand Application. Sustainability, 11(2), 406. [CrossRef]

- Katie, B. (2024). Internet of Things (IoT) for Environmental Monitoring. International Journal of Computing and Engineering, 6(3), 29–42. [CrossRef]

- Khatib, S. F. A., Al Amosh, H., & Ananzeh, H. (2023). Board Compensation in Financial Sectors: A Systematic Review of Twenty-Four Years of Research. International Journal of Financial Studies, 11, 92. DOI: https://www.mdpi.com/2227-7072/11/3/92.

- Kheradmand, E., Serre, D., Morales, M., & Robert, C. B. (2023). Alignment of Organizations’ Climate-Related Risk Disclosures with Material Risks and Metrics. SASB Climate Risk Technical Bulletin. DOI: ://efaidnbmnnnibpcajpcglclefindmkaj/https://haskayne.ucalgary.ca/sites/default/files/teams/12/Session%202%20Paper%20-%20Kheradmand_CSFN%20.pdf.

- Khlifi S, Ben Ali A, Hermi S. (2025). Artificial intelligence adoption as a mediator of executive cultural diversity-ESG performance nexus: evidence from European companies. Accounting Research Journal. [CrossRef]

- Kwong, R., Kwok, M. L. J., & Wong, H. S. M. (2023). Green FinTech Innovation as a Future Research Direction: A Bibliometric Analysis on Green Finance and FinTech. Sustainability, 15(20), 14683. [CrossRef]

- Lagasio, V. (2024).ESG-washing detection in corporate sustainability reports, International Review of Financial Analysis, 96. [CrossRef]

- Luna, M., Fernandez-Vazquez, S., Castelao, E., & Fernández, A. (2024). A blockchain-based approach to the challenges of EU’s environmental policy compliance in aquaculture: From traceability to fraud prevention, Marine Policy, 159. [CrossRef]

- Manzoor, B., Maxwell, F.A.A., Khalid, S.A. (2025). Green buildings and digital technologies: A pathway to sustainable development, Green Technologies and Sustainability, 4(3). [CrossRef]

- Mao, Q., Xinyuan, M, Yunpeng, S. (2023). Study of impacts of blockchain technology on renewable energy resource findings, Renewable Energy, 211. [CrossRef]

- Marquis, C., & Toffel, M. W. (2016). The Ecology of Greenwashing: Corporate Environmental Rhetoric and Behavior. Harvard Business School Working Paper, No. 22-048. DOI: https://www.hbs.edu/faculty/Pages/item.aspx?num=50187.

- Mei, Y., Geng, L., Cao, X., & Xie, Y. (2025). Artificial Intelligence in Green Marketing: A Systematic Literature Review. Sustainability, 17(22), 10382. [CrossRef]

- Moghaddasi, H., Culp, C., Vanegas, J., Das, S., & Ehsani, M. (2022). An Adaptable Net Zero Model: Energy Analysis of a Monitored Case Study. Energies, 15(11), 4016. [CrossRef]

- Moodaley, W., & Telukdarie, A. (2023). Greenwashing, Sustainability Reporting, and Artificial Intelligence: A Systematic Literature Review. Sustainability, 15(2), 1481. [CrossRef]

- Navarrete-Oyarce, J., Moraga-Flores, H., Gallegos Mardones, J. A., & Gallizo, J. L. (2022). Why Integrated Reporting? Insights from Early Adoption in an Emerging Economy. Sustainability, 14(3), 1695. [CrossRef]

- Network for Greening the Financial System (NGFS). (2022). Climate Scenarios for Central Banks and Supervisors. DOI: https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-climate-scenarios-central-banks-and-supervisors-0.

- North, D. C. (1991). Institutions, Institutional Change and Economic Performance. Cambridge University Press. DOI: https://ideas.repec.org/b/cup/cbooks/9780521394161.html.

- Okoli, C. 2015. A guide to conducting a standalone systematic literature review. Communications of the Association for Information Systems 37: 879–910, DOI://efaidnbmnnnibpcajpcglclefindmkaj/https://hal.science/hal-01574600v1/document.

- Olawade, D., Ojima Z. W., Abimbola, O. I., Bamise, I. E., Adedayo, O., Bankole, I. O. (2024). Artificial intelligence in environmental monitoring: Advancements, challenges, and future directions, Hygiene and Environmental Health Advances, (12). [CrossRef]

- Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., et al. (2021). The PRISMA 2020 statement: an updated guideline for reporting systematic reviews. BMJ, 372, n71. DOI: https://www.bmj.com/content/372/bmj.n71.

- Petticrew, M., & Roberts, H. (2008). Systematic Reviews in the Social Sciences: A Practical Guide. Wiley. DOI:10.1002/9780470754887.

- Pourrahmani, H., Masoud, T. A., Hossein, Madi, J., & Peprah, O. (2025). Revolutionizing carbon sequestration: Integrating IoT, AI, and blockchain technologies in the fight against climate change, Energy Reports, 13, 5952-5967. [CrossRef]

- Santi, C. (2023). Investor climate sentiment and financial markets, International Review of Financial Analysis, (86). [CrossRef]

- Sierra-Correa, P. C., & Kintz, C. (2015). Ecosystem-based adaptation for improving coastal planning for sea-level rise: A systematic review for mangrove coasts. Marine Policy 51: 385–93. DOI: https://www.sciencedirect.com/science/article/abs/pii/S0308597X14002462.

- Simon, H. A. (1962). The architecture of complexity. Proceedings of the American Philosophical Society, 106(6), 467-482. DOI: https://link.springer.com/chapter/10.1007/978-1-4899-0718-9_31.

- Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355-374. DOI: https://academic.oup.com/qje/article-abstract/87/3/355/1909092?redirectedFrom=fulltext.

- Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. The Academy of Management Review, 20(3), 571-610. DOI: https://www.jstor.org/stable/258788.

- Sumedha, B., Dipti, S., Rashmi, B. (2024). Green finance and investment index for assessing scenario and performance in selected countries, World Development Sustainability, (5). [CrossRef]

- Talukder, S. C., Lakner, Z., & Temesi, Á. (2025). Exploring the Research Landscape of Impact Investing and Sustainable Finance: A Bibliometric Review. Journal of Risk and Financial Management, 18(10), 578. [CrossRef]

- Wang, G., Yan, C., You, Z., & Chi, X. (2024). Systemic risk prediction using machine learning: Does network connectedness help prediction?, International Review of Financial Analysis, 93,DOI: . [CrossRef]

- Wang, Y. F., Wang, M. Y. F., & Tu, L. Y. (2025). An Evaluation of Machine Learning Models for Forecasting Short-Term U.S. Treasury Yields. Applied Sciences, 15(12), 6903. [CrossRef]

- Weyant, J. (2017). Some contributions of integrated assessment models of climate change. Review of Environmental Economics and Policy, 11(1), 115–137. DOI: https://ideas.repec.org/a/oup/renvpo/v11y2017i1p115-137..html.

- Williamson, O. E. (1985). The Economic Institutions of Capitalism. Free Press. DOI: https://www.jstor.org/stable/2555390.

- Wu, L., Ghansah, F., Zou, Y., & Ababio, B. (2025). Blockchain Oracles for Digital Transformation in the AECO Industry: Securing Off-Chain Data Flows for a Trusted On-Chain Environment. Buildings, 15(20), 3662. [CrossRef]

- Zetzsche, D. A., Arner, D. W., & Buckley, R. P. (2020). Artificial Intelligence in Finance: Putting the Human in the Loop. Sydney Law School Research Paper No. 20/35. DOI: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3531711.

- Zhang, G., Chen, S. C.-I., & Yue, X. (2024). Blockchain Technology in Carbon Trading Markets: Impacts, Benefits, and Challenges—A Case Study of the Shanghai Environment and Energy Exchange. Energies, 17(13), 3296. [CrossRef]

Figure 1.

PRISMA DIAGRAM.

Table 1.

Search strings and databases.

| Database | Search Strings |

| Scopus | ("augmented finance" OR "AI" OR "artificial intelligence" OR "machine learning" OR "IoT" OR "internet of things" OR "blockchain" OR "distributed ledger") AND ("climate change" OR "green finance" OR "sustainable finance" OR "ESG" OR "climate risk" OR "greenwashing") AND ("banking" OR "insurance" OR "investment" OR "asset management"). |

| Web of Science | ("augmented finance" OR "AI" OR "artificial intelligence" OR "machine learning" OR "IoT" OR "internet of things" OR "blockchain" OR "distributed ledger") AND ("climate change" OR "green finance" OR "sustainable finance" OR "ESG" OR "climate risk" OR "greenwashing") AND ("banking" OR "insurance" OR "investment" OR "asset management"). |

| ScienceDirect | ("augmented finance" OR "AI" OR "artificial intelligence" OR "machine learning" OR "IoT" OR "internet of things" OR "blockchain" OR "distributed ledger") AND ("climate change" OR "green finance" OR "sustainable finance" OR "ESG" OR "climate risk" OR "greenwashing") AND ("banking" OR "insurance" OR "investment" OR "asset management"). |

| JSTOR | ("augmented finance" OR "AI" OR "artificial intelligence" OR "machine learning" OR "IoT" OR "internet of things" OR "blockchain" OR "distributed ledger") AND ("climate change" OR "green finance" OR "sustainable finance" OR "ESG" OR "climate risk" OR "greenwashing") AND ("banking" OR "insurance" OR "investment" OR "asset management"). |

Table 2.

The selected articles.

| Author(s) and Year | Study Objective | Methodology | Key Technologies | Main Findings |

| Jia & Bo (2025) | Monitor corporate emissions via satellite | Satellite imagery analysis | IoT / Remote Sensing | Developed a framework for estimating GHG emissions with acceptable spatial resolution. |

| Pourrahmani et al. (2025) | Real-time carbon accounting in the supply chain | Case study implementing sensors | IoT, Cloud | Reduced reporting uncertainties; auditable data for green finance. |

| Mei et al. (2025) | Examine blockchain use for carbon credits | Systematic review & conceptual framework | Blockchain | Potential to enhance transparency, trust, and liquidity in carbon markets. |

| Hyun (2024) | Propose a framework for tokenised green bonds | Prototype design | Blockchain, Tokenisation | Reduced intermediaries; comprehensive traceability of funds and impact. |

| Battiston & Monasterolo (2020) [ | Assess climate risk in bond portfolios | Network modelling & scenarios | Machine Learning | Identified "hotspots" of unpriced climate risk in sovereign bonds. |

| Giglio et al. (2021) | Synthesise advances in climate finance | Literature review | Various (ML) | AI enables more fine-grained and dynamic modelling of long-term physical risks. |

| Bingler et al. (2022) | Assess the quality of climate disclosures | Text analysis (NLP) | AI (NLP) | Significant gaps between discourse and actionable metrics; detection of "cherry-picking". |

| Grewal et al. (2019) | Look at how the market reacts to non-financial disclosures. | Use event studies and text analysis with AI (NLP). | AI (NLP) | The market reacts more to alternative data (media) than to standard CSR reports. |

| Lagasio (2024) | Analyse corporate greenwashing ecology | Statistical analysis of texts and performance data | AI (NLP) | Developed an algorithm to identify rhetoric-performance gaps. |

| D'Orazio (2022) | Propose a post-COVID framework for climate risks | Economic analysis | IoT, Big Data | Highlights the critical need for data standards and interoperability for green technologies. |

| Dignum (2019) | Framework for responsible AI | Conceptual research | AI (Ethics) | Warns against social biases amplified by algorithms without proper governance. |

| Zetzsche et al. (2020) | Analyse regulatory challenges of AI in finance | Legal and economic analysis | AI, Regulation | Identifies regulatory gap and advocates for a "design-based" approach. |

| Adadi & Berrada (2018) | Review the field of explainable AI (XAI) | Literature review | XAI | Highlights the imperative of transparency for AI adoption in critical domains like finance. |

| Ge & Yang (2025) | Low-carbon portfolio optimisation via AI | Optimisation algorithms | Machine Learning | Developed an asset selection model aligned with 2°C scenarios. |

| Moodaley & Telukdarie (2023) | Greenwashing detection in CSR reports | Advanced semantic analysis | AI (NLP) | Automatic classification of environmental claims with 92% accuracy. |

| Katie (2024) | Real-time biodiversity monitoring | IoT and drones | IoT, Computer Vision | Automated monitoring of how funded projects affect biodiversity. |

| Luna et al. (2021) | Blockchain platform for green financing | Practical implementation | Blockchain, Smart Contracts | 70% reduction in verification costs for green projects. |

| Wang et al. (2024) | Sectoral transition risk modelling | Neural networks | Deep Learning | Proactive identification of industries susceptible to stranded assets. |

| Bissoondoyal-Bheenick et al. (2023) | Dynamic ESG scoring using alternative data |

Multi-source analysis | AI, and Big Data | A real-time ESG score that changes every year instead of once a year by traditional agencies. |

| Alves et al. (2020) | Traceability of green supply chains | Private blockchain | Blockchain, IoT | Unchangeable proof of the "green" source of raw materials. |

| Wang et al. (2025) | Prediction of defaults associated with climate factors | Forecasting models | Machine Learning | Incorporation of climatic variables into credit scoring algorithms. |

| Gutierrez-Bustamante & Espinosa-Leal (2022) | Analysis of Climate Risk Materiality |

Natural language processing (NLP) | AI (NLP) | Natural Language Processing (NLP) for the automated assessment of climate risks by industry sector. |

| Wu et al. (2025) | Parametric climate insurance |

Smart Contracts | Blockchain, Oracles | Automated payments initiated by verified meteorological data. |

| Buchak et al. (2018) | Auditing climate reports automatically |

Analysis of compliance | Business Rules, AI | Finding regulatory climate disclosure discrepancies. |

| Talukder et al. (2025) | Impact investing with AI criteria | Multi-objective optimisation | Machine Learning | Portfolios optimising both returns and measurable climate impact. |

| Moghaddasi et al. (2022) | Net-zero commitment monitoring | Trajectory analysis | AI, Data Analytics | Automatic tracking of commitment consistency with actual actions. |

| Kwong et al. (2023) | Green crowdfunding | Decentralised platform | Blockchain, Tokens | 45% increase in access to funding for small green projects. |

| Dong et al. (2023) | Carbon credit price prediction | Time series | LSTM Networks | Price forecasting with 30% lower error than traditional models . |

| Afroditi (2025) | Automated climate due diligence | Document analysis | AI (NLP, Computer Vision) | 80% reduction in time spent on due diligence document analysis. |

| Desnos et al. (2023) | Portfolio climate stress testing | Monte Carlo simulations | Machine Learning | Assessment of portfolio resilience under different climate scenarios. |

| Manzoor et al. (2025) | Automatic green building certification | IoT and blockchain | IoT, Blockchain | Real-time certification of building energy performance. |

| Sumedha et al. (2024) | Green investment opportunity detection | Market analysis | AI, Web Scraping | Automatic identification of promising green tech startups. |

| Ajakwe et al. (2025) | Smart contracts for renewable energy | Smart Contracts | Blockchain, IoT | Automation of Power Purchase Agreements for renewable energy projects. |

| Santi (2023) | Climate sentiment market analysis | Sentiment analysis | AI (NLP) | Relationship between climate media sentiment and the performance of green assets. |

| Navarrete-Oyarce et al. (2022) | Automatic integrated reporting | Report generation | AI, RPA | Automatic production of reports integrating financial and extra-financial data. |

| Judy et al. (2019) | Climate transition scoring | Hybrid methodology | AI, Expert Systems | Scoring combines quantitative and qualitative analysis of transition plans. |

| Zhang et al. (2024) | Low-carbon logistics optimisation | Genetic algorithms | Machine Learning | 15% reduction in the carbon footprint of funded logistics chains. |

| Olawade et al. (2024) | Climate regulatory monitoring | Automated monitoring | AI (NLP) | Early alert of regulatory changes impacting portfolios. |

| Mao et al. (2023) | Impact measurement for green bonds | IoT and blockchain integration | IoT, Blockchain | Precise tracking of the environmental impact of projects funded by green bonds. |

| Kheradmand et al. (2023) | Climate risk disclosure benchmarking | Comparative analysis | AI, Benchmarking | Automated evaluation of disclosure quality in comparison to industry counterparts. |

Table 3.

Distribution of Research by Country/Region.

| Country/Region | Estimated Number of Studies | Main Research Areas | Representative Studies |

| United States | 8-10 | ESG analysis, fintech, greenwashing detection | Grewal et al. (2019); Lagasio (2024); Wang et al. (2025) |

| European Union | 6-8 | Blockchain, regulation, climate risk assessment | Battiston & Monasterolo (2020); Luna et al. (2024); D'Orazio (2022) |

| China | 4-5 | Emissions monitoring, green fintech, and AI applications | Jia & Bo (2025); Mei et al. (2025); Zhang et al. (2024) |

| South Korea | 2-3 | Blockchain, tokenized green bonds | Hyun (2024), Ajakwe (2025) |

| Japan | 1-2 | IoT, biodiversity monitoring | Katie (2024) |

| United Kingdom | 3-4 | Climate scoring, risk analysis, transition planning | Bissoondoyal-Bheenick et al. (2023); Judy et al. (2019) |

| Canada | 2-3 | AI ethics, governance frameworks | Dignum (2019); Kheradmand et al. (2023) |

| Australia | 1-2 | Fintech regulation, policy frameworks | Zetzsche et al. (2020) |

| Latin America | 1-2 | Green supply chain, sustainable sourcing | Alves et al. (2020) |

| Nordic Countries | 2-3 | Building certification, IoT applications | Manzoor et al. (2025); Gutierrez-Bustamante & Espinosa-Leal (2022) |

| Multi-country Studies | 3-4 | Comparative international analysis, global frameworks | Giglio et al. (2021); Navarrete-Oyarce et al. (2022) |

Table 4.

Quantitative Breakdown of Research Methodologies.

| Methodology Type | Definition | Number of Studies | Percentage of Total |

| Non-Linear | Uses complex, adaptive models like Machine Learning (ML), Deep Learning, and Natural Language Processing (NLP) to identify patterns and make predictions from data. | 24 | 57% |

| Mixed | Combines linear and non-linear methods, or integrates multiple data sources and analytical techniques for a more comprehensive and nuanced analysis. | 12 | 29% |

| Linear | Rule-based, sequential, or traditional analytical processes. Often relies on predefined business rules, statistical models, or straightforward automation. | 6 | 14% |

Table 5.

Distribution of Selected Studies According to Primary Technological Emphasis.

| Technology | Number of Studies | Percentage of Total Studies | Detailed Breakdown by Technology Category |

| AI/Machine Learning | 24 | 57.1% |

|

| Blockchain | 11 | 26.2% |

|

| IoT | 7 | 16.7% |

|

| 1 | The PRISMA process will be presented in detail in Appendix A. |

| 2 | Some studies are counted in multiple categories when they significantly integrate multiple technologies in their research. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.