Submitted:

14 November 2025

Posted:

17 November 2025

You are already at the latest version

Abstract

Dynamic adjustment of capital structure is crucial for corporate financial stability and long-term resource allocation, and it is also an important foundation for sustainable economic development. In the context of global climate change, carbon finance is playing a key role in incentivizing emissions reductions and promoting the transition to a low-carbon economy. While the existing literature has explored the macroeconomic effects of carbon finance, its impact at the firm or micro—level, particularly on capital structure decisions, remains largely unexamined. This study aims to investigate the effect of carbon finance on the speed of dynamic capital structure adjustment and the degree of deviation of enterprises. Data were collected from China's A-share-listed companies between 2014 and 2024 to construct the provincial carbon finance development index, and a partial adjustment model was applied to measure the speed of capital structure adjustment. The findings indicate that carbon finance has a significantly positive effect on the speed of adjusting the capital structure and that carbon finance is consistent in keeping firms in line with their target leverage ratio, according to a number of robustness tests. Notably, cross-sectional analyses show that this effect is more pronounced among firms with higher green innovation outputs and greater indebtedness. Further research indicates that the underlying mechanism driving this relationship lies in alleviating financing constraints and reducing financing costs. By bridging the gap between market-oriented environmental regulations and corporate financial policies, our study provides policymakers with evidence to improve carbon finance mechanisms and gives managers a basis for using green finance tools to create sustainable value.

Keywords:

Carbon Finance

; Dynamic Capital Structure Adjustment

; green innovation

; financing constraints

1. Introduction

To effectively tackle global warming and climate change, many countries have implemented a series of command-control carbon reduction policies. For example, in 1997, the Kyoto Protocol proposed treating carbon emission rights as a tradable commodity in the market, thereby establishing a carbon emission trading system [1]. In 2005, the European Union took the lead in piloting its Emissions Trading System, followed by countries such as New Zealand and the United States. To give full play to the market’s role in carbon governance, the World Bank’s Carbon Finance Sector introduced the concept of carbon finance in 2006. Carbon finance is a trading and investment activity based on “carbon emission rights” and their derivatives. Carbon finance is the market-based environmental regulation and focuses on developing financial mechanisms to support greenhouse gas emission reduction targets and promote a low-carbon economy [2,3]. The growth of carbon finance is closely linked to the carbon finance market, primarily involving the secondary market for trading carbon emission rights. This market encompasses government entities, emission-control enterprises, green companies, financial institutions, and individual stakeholders. Emission-control firms can buy or sell carbon quotas, while green firms provide certified voluntary emission reductions. By facilitating the trading of carbon commodities, the carbon financial market effectively channels green investments and directs capital towards innovative firms, enhancing their incentives for sustainable practices.

Since then, China has established eight carbon emissions trading markets; thus, the development of carbon finance has accelerated rapidly. Policy support within the carbon finance systems, such as tax incentives and a financing chain, fosters a virtuous cycle and strengthens green energy in the macroeconomy by establishing a green supply chain, encouraging collaborative emission reduction among enterprises in the supply chain, promoting an overall green upgrade of the industrial chain, and providing the macroeconomy with sustainable green power. With the development of carbon finance, related research is emerging and is aimed at constructing a robust carbon finance market system [4,5,6] and analyzing its macroeconomic effects [7,8]. In fact, carbon finance drives the green transformation among microenterprises. However, little research examines the significant impact of carbon finance on microenterprises.

Realizing the influence of carbon finance on microenterprises is important to properly comprehend its true role in the economic system since carbon finance operates at a systematic level and depends finally upon how microenterprises alter the financial structure of their enterprises. This knowledge will enable policymakers to plan more carefully considered support measures, thereby assisting the sustainable growth of microenterprises, which is to emphasize fundamentally the great positive contribution that, with the aid of carbon finance, microenterprises will make to macroeconomic growth.

This research is concerned with the effects of carbon finance on the dynamic capital structure adjustments, while they are capital structure decisions and they are firm level and do much to dictate the future of economic development. It is inventively capital structure adjustments that are dynamic in nature which is one of the important methods for firms to respond to carbon finance. They induce much better efficient long-term allocation of resources to invigorate the market.

Using data from Chinese A-share listed companies covering the period from 2014 to 2024, we study the effect of carbon finance on the dynamic adjustment of capital structure. We find that the useful policies on carbon finance materially contribute to optimize the capital structures of enterprises. More particularly, carbon finance greatly increases the speed of dynamic capital structure adjustments, while the deviation from target capital structures is again much improved, it in turn materially promoting the enterprise financing efficiency and contributing to the economic sustainable growth in the future.

Furthermore, we examine whether carbon finance can help rectify the inefficiencies in the traditional credit allocation system. We expect that green innovation firms are more likely to optimize their capital structures and accelerate their low-carbon transformation when incentivized by policies. We also expect that the effect of carbon finance on the speed of dynamic structure adjustments is faster in firms with higher liability. Indeed, we find that the relationship between carbon finance and dynamic capital structure adjustment speed is more pronounced in firms with higher green innovation and liability. Additionally, we find that carbon finance affects dynamic capital structure adjustment by alleviating financing constraints and enhancing monitoring.

Our study contributes to the literature in two ways. First, this paper adds to the literature about the relationship between macroeconomic policies and the dynamic adjustment of capital structures. Existing literature mainly focuses on how macroeconomic [9,10], law [11], and economic policy uncertainty [12] affect corporate capital structure adjustments. This paper enriches prior literature by examining the impact of carbon finance on the dynamic adjustment of capital structure.

Secondly, this paper expands prior literature by examining how market-based environmental regulation affects firms’ behavior. Existing research mainly focuses on the effects of command-control carbon emissions on firms’ financial decision-making [13,14,15,16,17,18]. However, whether and how market-based environmental regulation affects firms’ behavior is unclear. This paper fills the gap by exploring the key role of carbon finance policy in optimizing corporate capital structure.

2. Literature Review

2.1. Determinants of Dynamic Capital Structure Adjustment

The study of optimal capital structure has evolved from a static to a dynamic framework, laying a solid theoretical foundation for this study. Early classical theories, such as the capital structure irrelevance theory (MM theory) proposed by Modigliani and Miller (1958) [19] in the late 1950s and the subsequent introduction of the ‘taxed MM theory’, opened the way for modern capital structure research. Since then, preferential financing theory, agency theory, and static trade-off theory have been developed, which together reveal how internal factors such as taxes, bankruptcy costs, information asymmetry, and agency conflicts determine the static optimal capital structure.

However, the above static theories have difficulty in explaining why, in reality, firms' capital structures consistently deviate from the theoretical optimum. These theories also do not explain why firms do not immediately adjust to the target level. To fill this theoretical gap, Fischer et al. (1989) [20] proposed the dynamic trade-off theory of capital structure. This theory states that firms are not always in the optimal state. Each firm has an optimal target capital structure. When a firm's capital structure deviates from this target, it will adjust its debt-to-equity ratios to bring them to, or close to, the target level [9,20,21,22]. Obviously, the more a firm's capital structure converges to the target, the more it favours enhancement of the firm's value [23]. However, many factors affect how firms actually adjust their capital structures. These factors influence both the speed of adjustment [8] and the extent to which actual structures deviate from targets [24]. For example, firms incur adjustment costs due to market frictions such as agency costs and information asymmetry. Firms will only adjust their capital structure when the expected benefit exceeds the adjustment cost. The speed of adjustment depends on the balance between these benefits and costs [25,26,27].

The focus of this study is primarily on external environmental factors affecting enterprises. Existing studies have shown that the macroeconomic environment [9,10,28], the legal environment [11], economic policy uncertainty [12] and other factors have a significant impact on the adjustment of the capital structure of enterprises. For example, the macroeconomic environment affects the speed and scale of the adjustment of the capital structure of enterprises. Enterprises generally speed up the adjustment faster and on a larger scale in the boom period, and slowly adjust in the recession period [9,10,28]. The institutional environment also plays an important role. Öztekin and Flannery (2012) [11] found that the better the legal system, the smaller the adjustment cost and the faster the adjustment speed. Economic policy uncertainty makes it difficult for enterprises to predict future policies and government assistance, which may make enterprises adopt a more prudent capital structure strategy to avoid potential shock [12]. Other factors, such as the marketization process and fiscal and monetary policy, are also found to have an impact on the capital structure decision-making of enterprises [29,30]. Firstly, the external environment can influence the investment opportunity of the enterprises, change the external business risk and capital demand of the enterprises, and thus influence the income of adjusting the capital structure [28]. On the other hand, the change of external environment may influence the availability and cost of the financing, and thus the cost of the adjustment of the capital structure [26]. These changes may, on affect the feasibility and convenience of adjusting the capital structure of the enterprises [31].

The results above show that dynamic capital structure adjustment is still a popular issue in the financial management of enterprises, which focuses on the influencing factors. As a new industry, carbon finance may have a significant impact on the external financial environment of enterprises. The study of how this changing environment leads to the change of capital structure provides a new research angle.

2.2. Research on the Impact of Carbon Finance on Enterprises

Global climate change is the most critical challenge for human society, and the transformation towards a low-carbon economy has become a strategic consensus of countries in this transition. It is the financial system that is engaged as an instrument of transformation. An effective financial system mobilizes and leverages social capital invested in energy-saving and emissions-reducing projects and in green low-carbon technologies. This provides vital financial support and innovative impetus for achieving global carbon neutrality. The concept of carbon finance originated in environmental finance at the end of the 20th century and has since become an emerging field as the low-carbon economy has developed [32]. Scholars generally agree that carbon finance is a vital part of the global climate governance system and that its influence on the financial sector cannot be ignored [33].

As an investment and financing activity focused on reducing carbon emissions, carbon finance centers on pricing carbon-emission rights through financial innovation. It guides the flow of funds to low-carbon technologies and applications and is attracting increasing attention from all quarters. Theoretically, academics have identified carbon finance as a key innovation in financial systems for addressing climate change. They have urged governments to formulate supporting policies to accelerate their adoption. In line with this, China has been developing the market since 2011 by launching carbon trading pilots in Beijing, Tianjin, Shanghai, Chongqing, Hubei, and Guangdong. These pilots began trading in 2013. After several years of smooth operation, they have accumulated valuable practical experience, laying a solid foundation for establishing a national carbon market. In this way, carbon finance actually connects the carbon market with the financial system, providing an international quality market mechanism for the price of carbon emissions rights. It also attracts social funds to the low-carbon sector by means of various financial instruments. In July 2017, the national carbon emissions rights trading market officially opened. Since then, it has developed rapidly and become the largest carbon market in the world, covering greenhouse gas emissions. This is a new stage of development in China's carbon finance, and it has great potential and far-reaching influence.

Carbon finance is attracting more and more scholars to study it profoundly. From a macro perspective, research abroad and at home on the effect of carbon finance has been carried out mainly about increasing carbon market capacity; also, the effects of reducing carbon emissions and stimulating macro-economic development have been investigated. Geng et al. (2022) [34] state that carbon finance can promote green and inclusive economic growth by reconstructing the financial system. Fullerton and West (2002) [35] found that carbon finance is a very rapidly growing subject which has already led to considerable reductions of greenhouse gases through ‘carbon trading and services’. Many studies have been made of the efficiency of carbon trading. Amongst others, the correctness of the following conclusions can be drawn from the studies carried out. Using a multi-actor general equilibrium model, Tang et al. (2015) [36] found that trading in carbon emissions substantially reduced GHG emissions. Zhou and Li (2019) [2] have seen that carbon finance helps reach low-price emissions reductions. Klemetsen et al. (2020) [37] and Colmer et al. (2025) [38] both found that schemes leading to trading in carbon emissions caused a substantial reduction in the emissions of the regulated factories, and enabled a direct effect on the level of emissions. Further from this, Gao (2023) [39] used county based satellite data from China to show that carbon finance helps promote low-carbon economic growth to a further extent, and pointed to the importance of financial mechanisms. Ren and Fu (2019) [40] have shown that measures like those referred to can also improve regional total factor productivity, leading thereby to greater economic effect. From the viewpoint of green economic efficiency Liao et al. (2020) [41] have shown that carbon emissions trading causes green economic growth by stimulating innovation. These conclusions have been confirmed Jiang et al. (2023) [7], who have seen that carbon finance is of great help to the attainment of qualitative high economic growth.

In addition to looking at the macro-level effects of carbon finance on emissions control and economic results, researchers have also studied the micro-level effects on the corporation with regard to profitability, corporate value, technology and R&D expenditures. Thus Chan et al (2013) [42] studied the relationship between carbon emission rights versus corporate value, and found that carbon rights policies had a significantly positive influence on the value of major polluter enterprises. Oestreich and Tsiakas (2015) [43] found that carbon trading raised cash flows for low-emission firms but increased risk on stock markets for high emissions firms. However, some contrary opinions exist. Koch and Bassen (2013) [44] used a discounted cash flow (DCF) model, which demonstrated that most power companies had carbon risk premiums and capital costs post-entry into carbon trading schemes, which had an adverse effect on equity value. Shen and Huang (2019) [15] using event study methodology also found that participation in corporate carbon trading activities enhanced firm value over the short term but that this was insignificant over the long term. On the impact of carbon finance on corporate technological innovation, the studies referred to in the literature tend overall to lend support to the view that there are indeed incentive effects. Calel and Dechezleprêtre (2016) [45] report that enterprises taking part in carbon emissions trading showed appreciably higher levels of technological innovation. On the other hand, Chen et al (2017) [46] found that the effects of carbon emissions trading were heterogeneous in their influence on the corporate innovation capacity, in that while there was a positive effect on the technic technological innovation workings, vis-a-vis regulated enterprises, there was an adverse effect among non-regulated enterprises. Extending this work, Lin et al (2018) [47] examined the effects of the Chinese carbon trading market on the corporate technological innovation, this from the viewpoint of carbon pricing, finding that this drew both a promotional effect and a dislocation effect, the higher the carbon price, the more did the promotional effect of the carbon trading system exert a positive dynamism on technological innovation. In terms of methodology, Cui et al (2018) [48] used a triple difference approach to examine the effects of carbon emission rights and concluded that pilot carbon trading schemes tended to enhance low-carbon technological innovation among enterprises. Particularly it was revealed that this effect of stimulating innovation was even greater the more the pilot carbon trading activity went on. Similarly, Zhu et al. (2019) [49] confirmed that pilot enterprises exhibited significantly higher levels of low-carbon innovation following the implementation of carbon trading pilot schemes. Further examining market conditions, Hu et al. (2020) [50] demonstrated that the catalytic role of carbon emission rights in corporate technological innovation is more pronounced in markets with greater liquidity and reduced product competition. Regarding R&D expenditure, numerous scholars have also conducted research. For example, Liu and Zhang (2017) [51] demonstrated that carbon emission rights effectively stimulate R&D expenditure among pilot enterprises, particularly among large-scale firms. Further confirmation that carbon emissions trading pilot schemes primarily motivate corporate innovation through product R&D and cost channels was provided by Guo and Xiao (2020) [52], effectively boosting R&D investment among micro-enterprises.

However, there remains a notable gap in research regarding the influence of carbon finance on corporate financing decisions as a financial tool in addressing firms’ decision-making. Our research is most closely connected to Campiglio (2016) [53], who gives the best general understanding of the function of green finance in low-carbon financing through real analysis of carbon finance. In this paper, Campiglio (2016) [53] notes the opportunity to discuss concrete obstacles related to corporate behaviors of transition to low-carbon, a possible problem of high risk and low return in the innovation link. Campiglio (2016) [53] proposes the establishment of new-specific financial institutions or of confirmed additional capital market policies distinct from the normal structures of interest rates to meet financial supply purposes. This research emphasizes the fact that if carbon finance makes advancement possible, it can reduce financial constraints a lot in the progress of time of transition to low-carbon. We have widened this literature again to think over the profit within the variable constitutional financial structure of the carbon finance.

3. Theoretical Analysis and Research Assumptions

3.1. Carbon Finance and Capital Structure Adjustment

The primary aim of carbon finance is to facilitate and encourage the development of a low carbon economy through various finance. This is done through a squeeze of mechanism based on markets. The duality of carbon finance as a device for government surveillance and as a market-based approach is effective in the change of the capital structure, through the easing of the constraint on finance and the improvement of regulatory surveillance.

From the vantage of alleviating financing constraints, carbon finance positively relates to the availability of funding to firms and accelerates the changes necessary in their capital structures. At the stage of financing alternatives, carbon finance embodies a new set of financial services which deṇgērate from conventional credit techniques. For example, green bonds diminish cost of fonanctions through reliance on third-party certification and effectual administration of investel funds, while carbon credits favor the adoption of dynamic pricing systems in which the rate of loan funds is contingent upon performance in emission reductions. Carbon credit pledge financing, too, inverts the rights of future revenue of carbon afeelits into existing collateral, thus unlocking illiquid form of environmental assets and effectually making use of them by the varying capital structures.

Moreover, it tackles the engineering problems raised by green projects through innovative financial mechanisms corresponding to the capital mismatch originated by high initial investments and a long cycle of return. The use of carbon futures and insurance, plus the new allocation framework of risk, reduces the financial institutions' fears concerning long-term climate problems. An advanced example of carbon finance innovation is re-engineering of market liquidity. The securitisation of carbon assets condenses 20 to 30 years' worth of emission-reduction benefits into tradable securities by means of a maturity conversion method, thereby bringing short-term capital for participation in long-term investments. According to World Bank empirical evidence, such innovations have reduced the overall financing costs of low-carbon projects to 3.2% to 4.5%. To summarise, the innovative financial tools provided by carbon finance renders enterprises diverse financing mechanisms and greatly improves the access to financing. These instruments/financial tools enable enterprises to adjust their leverage levels more flexibly by reducing financing costs and improving access to funds, thereby accelerating the convergence of capital structure toward target levels.

The governance aspect of carbon finance enhances the credit efficiency of financial institutions from the perspective of alleviating financing constraints. The funds which flow through carbon finance arise from banks, institutional investors, and even state treasuries. The funding basis and credit orientation permits more elastic financing of enterprises. As carbon finance is extended, the capital supply mechanism is also changing. The channels of financing have also shifted from being primarily governmental and by the banks to being more marketized. The potential introducing of central bank digital currencies into carbon accounting functions may also change the dynamics of fund supply, broadening the possibilities of financing to enterprises while also streamlining the process of obtaining credit. Thus as carbon finance continues, the transaction costs to the enterprises for obtaining external funds for credit will decrease. The new efficient and varied method will minimize the transaction costs normally incurred by the enterprises in changing their capital structure and expedite the adjustments.

Furthermore, carbon finance can improve supervision of debt and accelerate the process of restructuring capital. Debt in this case serves to control firms’ free cash flow, limit excessive spending by management and correct self-serving managers [54], so that induces managers to work with greater diligence. Carbon finance is subjected to a multi-layered system of strict state supervision, which system of achieving climate goals, prevention of greenwashing and preservation of market reliability. In particular, loans to various credit institutions are subject to state protection through legal enforcement measures and financial penalties. In this case, the government uses blockchain technologies to control transactions, diminishes the amount of credit attributed to moral hazard in the credit market and accelerates the process of corporate capital structure.

In conclusion, if a company’s capital structure is too low in terms of its target capital structure, it has to increase liabilities. The progress of carbon financing makes more financing available to the company. It also lowers the cost of funds raised on credit. This permit management to secure credit funds at reduced costs from a greater number of sources, so raising the liability level and diminishing the distance from the target capital structure. On the other hand, if the capital structure is above the target, too great liabilities may be incurred resulting in increased financial risk and bankruptcy costs, necessitating a reduction in liabilities. It follows that the overindebtedness resulting therefrom, increases the financial risk to the company and the bankruptcy costs, so inducing management to lower the level of indebtedness. Furthermore, the impact of carbon finance may increase the financial risk and bankruptcy costs resulting from over-indebtedness, which has the effect of inducing management to reduce liabilities. Hence the following hypothesis is advanced by this study:

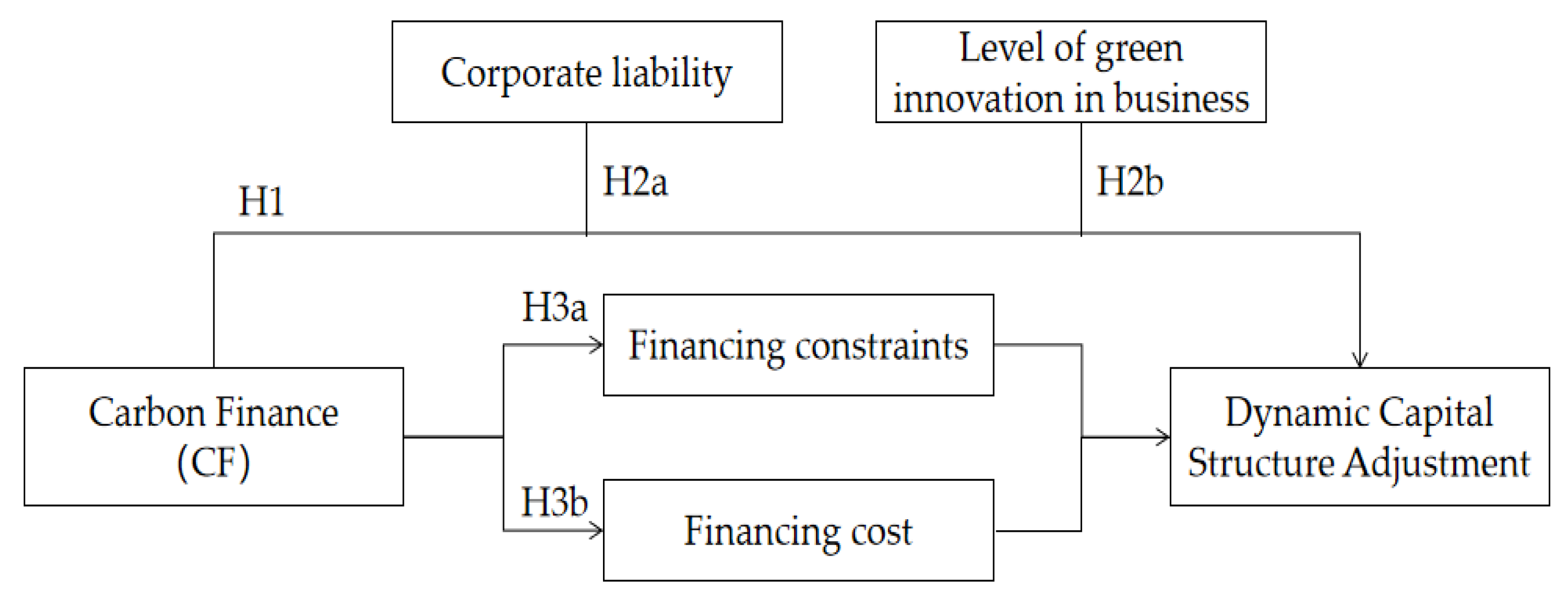

H1: Carbon finance has accelerated the pace of dynamic capital structure adjustments within enterprises.

3.2. Carbon Finance and the Allocation of Credit Resources

Research has shown that the distribution of lending resources in traditional financial systems is often inefficient and therefore leads to credit discrimination [55]. This can slow the distribution of credit resources to the real economy, creating excessive capital in corporations that invest their capital surpluses in financial investment, while those organizations that really require credit for constant financing are unable to secure it [56]. The result is a slower capital utilization of the concerned enterprises and a lower degree of value of the company.

Studies suggest that the level of debt is an important factor in the adjustment made by firms in their capital structure. The speed at which they move towards the target capital structure differs significantly between over-indebted and under-indebted firms. It is therefore essential to take this asymmetrical position into account in empirical studies of capital structure. In practice, however, it is exactly the motivation, weight and speed of adjustment to capital structure that differs widely between firms according to their levels of indebtedness. For example, over-indebted firms are likely to be more risk averse and more inclined to realign themselves with their normal objective gearing. On the other hand, under-indebted firms may be less likely to approach recapitalization because they have a lower level of financial risk [57].

Similarly, the development of carbon finance can be helpful to compensate for these inefficiencies in the traditional credit allocation system [58]. Carbon finance exists mainly for the purpose of supporting those green and innovative firms that have decided to change their practices in a sustainable direction and it provides a definite advantage in available access to the required credit resources in question. With enhanced policy signals and increased market liquidity, carbon finance expands its financial support for green and innovative firms, enabling them to secure more self-financing from financial institutions and overcome barriers to technological innovation. As a result, green innovative enterprises gain greater flexibility in their recapitalization efforts and can more swiftly adjust their capital structures.

In summary, we expect that the relationship between carbon finance and dynamic capital structure adjustment speed varies with liability and green innovation.

H2a: The relationship between carbon finance and the pace of dynamic capital structure adjustment is more pronounced among enterprises with relatively high debt ratios.

H2b: The relationship between carbon finance and the pace of corporate dynamic capital structure adjustment is more pronounced among enterprises with green innovation capabilities.

3.3. The Mediating Mechanism of Carbon Finance in Influencing Dynamic Capital Structure Adjustment

According to dynamic capital structure theory, firms have an optimal capital structure. However, due to adjustment costs, their actual capital structure continuously deviates from the target level [31]. These adjustment costs primarily manifest as frictions in external financing, centered on financing constraints (i.e., the ease of obtaining funds) and financing costs (i.e., the price of acquiring capital) [11]. Carbon finance is a market mechanism that internalizes environmental risks and rewards. This, in addition to reducing adjustment frictions through two parallel, interconnected pathways can be effective in accelerating the convergence to target capital structure for firms.

To begin with, there are mechanisms for relieving financing constraints. These constraints are caused by problems of information asymmetry and agency in capital markets. Such problems exclude enterprises from receiving, when they want it, sufficient outside finance on reasonable terms [60]. Carbon finance, with its specific information-governance, resource-allocation qualities, can, in a systematic manner, relieve such financing constraints. The systems in carbon finance such as carbon emissions trading systems and such procedures as the green credit approval process require firms to disclose standardized verifiable information about their carbon emissions and environmental impacts. This is a type of certification process. It transmits favorable signals to capital markets about a firms’ governance standards, technological advance, and long-run sustainable development competencies [61]. This diminishes information asymmetries between firms and the market [62]. This diminishment reduces adverse selection and credit rationing problems, which have their origins in problems of information asymmetry. Within the sustainable finance ambit, financiers are increasingly incorporating environmental performance into the core decision-making processes used in credit assessments. Strong carbon credentials are viewed as key indicators of less policy and transition risk for enterprises [63]. Hence, the evolution of carbon finance encourages banks to favorably allocate the credit resources to low-carbon enterprises. This enhances their access to debt finance. In addition, with the reduction in financing constraints, there are fewer impediments for enterprises which want to secure outside funding in the course of capital structure adjustments. When financing constraints are acute, firms, which have been used to formulating viable capital structure adjustments, often refrain or forgo implementing changes in structural arrangements because they cannot secure timely finance [11]. On the contrary, a loosening up of financing constraints improves the flexibility of firms and allows, more readily, swifter access when required to capital markets when they have deviations in their capital structure. The necessary finance is then able to be gotten for adjustments [9]. Hence, carbon finance enhances the feasibility of more rapid adjustments in capital structure, by modifying the accessibility of financing..

Secondly, there is a reduction in financing costs mechanism. Financing costs are direct price friction in capital structure adjustments. Carbon finance affects both the quantity (supply) and price (cost) of capital. Financial institutions incur substantial costs in collecting, processing and supervising information in its lending operations. The monitoring, reporting and verification (MRV) systems instituted by carbon finance provide reliable, third party certified information about corporate environmental performance. This greatly reduces the investigation costs and ongoing supervising costs to financial institutions [64]. Lower supervising costs induce financial institutions to be more willing and effective in taking advantage of the governance function of debt to reduce management's moral hazard [54]. As agency costs are reduced the resulting credit risk premium declines in parallel. Climate risks have also become a important factor in asset pricing. Empirical studies show that capital markets price the climate risks. Investors require higher expected returns on carbon intensive assets to compensate for the loss potential in the future [65]. Conversely, corporations with higher carbon performance demonstrate a greater reliability in the future cash flows and asset security. Therefore, the equity and debt capital markets require lower environmental risk premiums. By identifying and rewarding such corporations, carbon finance can lower their overall capital costs directly [63]. Lower financing costs also directly increase the marginal benefits of capital structure adjustments. According to the trade-off theory, firms constantly weight the benefits of adjusting to target levels against costs to be incurred. A major element of these adjustment costs are high financing costs and this inhibits the firms' motivation to adjust [31]. Where the financing costs decline to the result of carbon finance, the actual cost of equity financing or debt refinancing declines. Then the adjustment in either direction , up by increase in debt or down by decrease in debt becomes economically more viable, greatly increasing firms' incentives to proactively and quickly restructure their capital.

In summary, carbon finance influences the pace of capital structure adjustment through two mechanisms: alleviating financing constraints and reducing financing costs.

H3a: Carbon finance can accelerate firms' dynamic capital structure adjustments by alleviating financing constraints.

H3b: Carbon finance can also accelerate these adjustments by reducing financing costs.

3.4. Theoretical Framework

The theoretical framework for this study is depicted in Figure 1, which shows the causal relationships of the variables used in this study. The above research hypotheses provide the basis for the framework, which seeks to develop a clearly articulated, mechanistically consistent analytical framework. First, it is expressly concerned with the direct effects of carbon finance on firms' dynamic capital structure adjustments (H1). Second, it is concerned with the fact that this relationship will be different in different companies with different levels of indebtedness (H2a) and different levels of green vanvbn innovation (H2b). Finally, it will put forward the mechanisms of carbon finance which we have suggested operate synchronously, namely the alleviating of financing constraints (H3a) and the lowering of financing costs (H3b), in other words accelerating the dynamic capital structure adjustment process.

This theoretical framework offers detailed guidance to statistical testing later. By uniting direct effects, cross-sectional investigation and underlying mechanisms it clarifies the complex interaction between carbon finance and financial behaviour in corporations. It also gives a more systematic basis for investigation for what there is behind the improvement of capital structure. The following sections will use statistical models to test rigorously the theoretical concepts.

4. Research Design

4.1. Data Source and Sample

This research subject is focused on the state-owned listed companies in China for the period between 2014-2024 that guarantee the reliability and validity of the research results. The relevant data on enterprises comes from CSMAR database. The sample is narrowed according to the following rules: (1) financial companies are excluded; (2) companies tagged as ST, PT and *ST are omitted, (3) samples with missing variables or aberrant data are disregarded. All the continuous variables are winsorized in percentiles 1 and 99 to reduce the effect of outliers. The data for the development of the carbon finance are accounted for in the China Statistical Yearbook, China Energy Statistical Yearbook, Financial Statistical Yearbook. Some of this information integrated with the data on the firms’ data made a data basis with 15128 annual-being 2739 firms data.

4.2. Variable and Model Design

4.2.1. Independent Variables

This research utilizes the Carbon Finance Development Index (CFDI) as a means to gauge the level of development in carbon finance throughout the various provinces in China. The carbon finance system has multiple facets that demand evaluation from the economic, financial, environmental and energy angles. The evaluation confronted with certain conditions: the indices employed should be comparable, scientific, practical, operational, systematic and hierarchical. All of this is to be based upon the actuality of the situation and should fully appreciate the uniqueness and special features of carbon finance. The indicator system is constructed around five key aspects, as shown in Table 1. Subsequently, the entropy method is employed to evaluate the level of carbon finance development across 30 Chinese provinces, considering each indicator’s degree. To mitigate the impact of scale differences, extreme-value deviation standardization is applied to the raw data to convert them to a dimensionless format. The entropy value for each indicator is then calculated to determine the level of carbon finance development in each province.

4.2.2. Dependent Variable

Based on studies such as those by Byoun (2008) [65] and Flannery and Rangan (2006) [31], the partial adjustment model estimates the speed at which firms adjust their capital structures. We construct the following model:

Where Levi,t represents the actual debt ratio of firm i in year t. Lev_pi,t-1 denotes the adjusted debt ratio of firm i in the previous year t-1. Di,t is the book value of the firm's interest-bearing liabilities at the end of year t. Ai,t indicates the book value of the total assets of firm i at the close of year t. NIi,t refers to the net profit of firm i in year t. The term εi,t is a disturbance term. This study focuses on the coefficient γ in Equation (1), which value typically lying between 0 and 1. Levi,t is the reduction in the gap between the actual and target debt ratios of firm i in year t, at a rate of γ. A larger γ value indicates a faster adjustment rate to the firm’s capital structure. The literature has proved that a firm’s target capital structure is determined by factors such as the firm’s characteristics and continuous changes in response to changes in the firm’s internal and external environment [31]. Therefore, a firm’s target capital structure is measured by model (2).

where β signifies the regression coefficient associated with a set of characteristic variables related to capital structure, and Controlsi,t-1 represents a characteristic variable influencing the target capital structure. This Equation includes control variables such as firm size (Size), firm age (Age), and capital expenditure (Capex), while controlling for industry and year fixed effects. Equation (2) is incorporated into Equation (1) to estimate the target capital structure, resulting in Equation (3):

The firm’s target capital structure (Lev*i,t) is obtained by regressing Equation (3) and obtaining the estimated value of β, which is then brought into Equation (2). Substituting Lev*i,t into Equation (1) examines the impact of carbon finance on the speed of capital structure adjustment. The model adds the cross-multiplier term of the index of the level of development of carbon finance and the degree of deviation of the capital structure to Equation (1):

where , ; CFi,t-1 is the index of the level of carbon finance development. To alleviate the endogeneity problem, this study lags the independent variables by one period. The focus is on the γ1 coefficient, which measures the impact of carbon finance on the speed of corporate recapitalization. If γ1 is significantly greater than zero, it indicates that carbon finance accelerates the recapitalization process. Equation (4) controls for industry and year fixed effects and clusters standard errors at the firm level.

Based on this, the study goes on to analyze the impact of carbon finance on the degree of capital structure deviation. If carbon finance improves the speed at which firms adjust their capital structures, then, in practical terms, it will significantly reduce the deviation of firms’ capital structures from their target structures. Therefore, this study sets the AbsDevi,t variable, representing the degree of capital structure deviation from the target, as the explanatory variable in Equation (2). At the same time, the index representing the level of carbon finance development (CFi,t-1) is added to the right-hand side of the equation, resulting in the following model:

where AbsDevi,t is the absolute value of the difference between the actual and target debt ratios for the period, with the same control variables as in Equation (4), and still controlling for industry and year fixed effects.

4.2.3. Control Variables

(1) Firm age (Age): measured by the natural logarithm of the difference between the year of observation and the year of establishment. This variable reflects the firm’s historical experience, market maturity, and stability. (2) Firm size (Size): measured by the natural logarithm of total assets. This variable indicates the enterprise’s resource endowment, market position, and the effects of economies of scale and risk mitigation. (3) Total return on assets (ROA): measured by the ratio of total profit and interest expense to average total assets. This important measure of corporate profitability is useful in evaluating capital allocation decisions and investment policies. (4) Capital expenditures (Capex): measured as the ratio of capital expenditures to total assets. This provides an estimate of company growth in the nature of asset expansion, asset replacement and long-term strategic investments. (5) Selling general and administrative expenses (SG&A): Measured by the ratio of SG&A expenses to total assets. This indicates management efficiency, structure of operating expenses and use of company resources. (6) Total asset turnover (AssetsCh): measured by the ratio of net operating income to average total assets. This provides an estimate of operating efficiency and asset use, both of which are important in capital investment decisions. (7) Stock performance (return) : measured by the annual return of the individual stock, including the reinvestment of dividends. This variable reflects market recognition of the company and investor expectations and current market sentiment and valuations. (8) Institutional Investor Ownership (IO) : measured by the percent of shares owned by institutional investors. This indicates the intensity of institutional supervision of corporate governance and the extent of specialization of shareholders, with the overall indication of the company’s outside environment of corporate governance. (9) Reported volatility of stock (Sigma): Measured with the standard deviation of weekly annual stock returns. This indicates the risk of the firm in the market and uncertainty, as well as the company’s risk in the opinion of the investor.

This study introduces from an existing literature base control variables for each province of the country in order for the model to possess greater explanatory power and trend line strength of regression results. (1) Economic development level (GDP growth): Measured as the provincial gross of per capita GDP growth, is a representation of general economic dynamism of each province and cyclical oscillation thereof. (2) Financial development level (Loans): Measured as the percentage of the loans of financial institutions to GDP which is a measure of availability of financing of regional financial resources which plays a key role in the sources of financing and costs to companies relating to financing. (3) Industry structure (Industry): Measured as the ratio of the value added of the tertiary industry to that of the secondary. This Indicator shows the advanced characteristics of the economic structure of each of the provinces which again effects management performance competitive position and level of competitive advantage. By incorporating these provincial-level control variables, the study can more comprehensively assess the impact of provincial-level indicators on firms’ dynamic capital structure adjustments while controlling for the potential confounding effects of provincial characteristics.

4.2.4. Robustness Variables

In October 2011, China issued the Notice on Carbon Emission Right Trading Pilot Work, selecting six provinces, namely Beijing, Tianjin, Shanghai, Hubei, Chongqing, and Guangdong, to pilot carbon emission right trading. In May 2013, the State Council officially approved the Opinions on the Priorities of Deepening the Reform of the Economic System in 2013 and forwarded them to the NDRC. The document highlighted that China should fully utilize market-based mechanisms, focus on the practical implementation of carbon emission rights trading, and aim to liberalize the nationwide carbon emission rights trading system as soon as possible. Since 2013, China’s carbon emissions trading market has been launched in pilot cities one after another, so this study considers 2013 as the pilot year. To examine the impact of the carbon emissions trading pilot policy on the dynamic adjustment of corporate capital structure, the following model has been developed:

where, , Where Treat is a dummy variable for the experimental group, indicating whether a province is part of the pilot region (with a value of 1 indicating selection and zero indicating non-selection), and Post is a time dummy variable indicating the state of the pilot region before and after the policy was implemented (with a value of 1 for 2013 and 0 otherwise). The control variables are the same as in Equation (4). Industry and year fixed effects are still being controlled for. To examine how green finance influences the dynamic adjustment of capital structure, the following model has been developed:

Among them, GFi,t-1 is the level of green financial development, as measured by the entropy method. Controls are applied using the same model (4). It still controls for industry and year fixed effects.

4.2.5. Cross-Sectional Variables

To conduct cross-sectional tests, the following model was set up for this study:

where Misi,t represents Debt and GI. Debt is the difference between the firm’s capital structure at the beginning of year t. (Levi,t) and its target capital structure (Lev*i,t) are used to measure the level of corporate liabilities following Byoun (2008) [65]. When Levi,t - Lev*i,t > 0, the real debt level of the company at the beginning of the year is higher than the target debt ratio for the year, and the company is over-indebted; Debt takes the value of 1. Conversely, when Levi,t - Lev*i,t is less than zero, the company is under-indebted, and Scale takes the value of 0.

The green innovation level of the company (GI) is measured by the ratio of the number of green utility models independently filed by enterprises to the total number of patent applications in the same year. If this ratio is smaller than the median for that year, GI takes the value of 1; otherwise, it takes the value of 0. We are still controlling for industry and year fixed effects. If there is indeed a mismatch of credit resources, the coefficient ρ₂ in Equation (10) should be significantly negative. Conversely, if carbon finance can alleviate this mismatch, the coefficient ρ₃ in Equation (10) should be significantly positive.

4.2.6. Mediating Variables

To further validate this study’s theoretical logic and analyze how carbon finance influences the dynamic adjustment of corporate capital structure, the following mediation-effect model is set up, based on the mediation test by Glaveli and Geogas [67].

In equations (11) to (13), Med is the mediating variable. Specifically, Med includes two indicators: financing constraint (KZ) and financing cost (Cost). This study uses the KZ index to measure firms’ financing constraints and the cost of debt financing to measure financing costs. The latter is the ratio of total interest, fees, and other financial expenses to total liabilities at the end of the period. ϕ₀, φ₀ and θ₀ are constant terms and ϕ₁, ϕn, φ₁, φ₂, φ₃, θ₁, θ₂ and θn are regression coefficients. The control variables are the same as in model (4). Industry and year fixed effects are still controlled for. Suppose carbon finance eases financing constraints and reduces financing costs for enterprises, thereby improving the speed of enterprise capital structure adjustment and reducing target capital structure deviation. In that case, this study expects the ϕ₁ coefficient in Equation (11) to be significantly negative and the φ₃ coefficient in Equation (12) to be significantly negative. It also expects the θ₂ coefficient in Equation (13) to be significantly positive.

5. Empirical Analysis

5.1. Baseline Regression

Table 4 presents the results of the baseline regression analysis investigating the impact of the level of carbon finance on the dynamic adjustment of the capital structure. Columns (1) and (2) analyses the effects of carbon finance on the speed of capital structure adjustment. Column (1) controls for industry and year fixed effects, but no other control variables are included. The regression results show a significant positive relationship, indicating that carbon finance can effectively increase the speed of corporate capital structure adjustment. Column (2) introduces firm- and province-level control variables; the findings remain significant. Columns (3) and (4) analyze the effect of carbon finance on the degree of deviation from the target capital structure. Column (3) controls for industry and year fixed effects, but does not include other control variables. The regression results show a significant negative relationship, indicating that carbon finance reduces the deviation of firms’ capital structures from their target structures. The results remain significant when firm- and province-level control variables are included in Column (4). Therefore, we can confirm the hypothesis that carbon finance significantly increases the speed at which corporate capital structures adapt and reduces the degree to which they deviate from the target capital structure.

5.2. Robustness Tests

5.2.1. Endogeneity Test

Building on the main results, this study uses instrumental variables to mitigate the endogeneity problem caused by reverse causation. To further overcome the endogeneity problem, we use a difference-in-differences model (DID). This involved comparing two sets of data before and after the implementation of the carbon emissions trading pilot policy in the provinces where the firms in the experimental and control groups are located. This eliminates the intrinsic differences between individuals and the bias caused by the time trend unrelated to the experimental group, enabling us to obtain the net effect. The regression results are presented in Table 5. The interaction term of DID and TLev in Column (1) is significantly positive at the 1% level. The effect of DID on the dynamic adjustment of capital structure in Column (2) is significantly negative. This indicates that, even after overcoming the endogeneity problem using difference-in-differences, carbon finance increases the speed of dynamic adjustment of firms’ capital structures and reduces target capital structure deviation.

Furthermore, to mitigate the endogeneity problem due to reverse causality, we select the mean value of provincial cities’ carbon finance development level in the same year as an instrumental variable. The results of the two-stage regression are presented in Table 6, with columns (1) and (2) representing carbon finance and the speed of capital structure adjustment, and columns (3) and (4) representing carbon finance and the deviation from the target capital structure. The first-stage regression results in columns (1) and (3) show that the coefficients of Mean_CF*TLev and Mean_CF are significantly positive at the 1% level. They also pass the non-identifiability test and the weak instrumental variable test, indicating that the instrumental variables are appropriately selected. In the second-stage regression results in columns (2) and (4), the CF*TLev and CF coefficients are consistent with the benchmark regression results. These regression results suggest that using the instrumental variable method to address the endogeneity issue leads to a significant increase in the level of carbon finance development, which drives the speed of corporate capital structure adjustment and reduces the deviation from the target capital structure.

5.2.2. Other Robustness Tests

In addition, this study conducts further robustness tests. In this section, the independent variable, carbon finance, is replaced by the green finance development index in columns (1) and (2) of Table 7. The coefficient for the interaction term GF*TLev in column 1 is significantly positive, indicating that green finance accelerates firms’ capital structure adjustments. The coefficient of the interaction term GF*TLev in column 2 is significantly negative, indicating that green finance substantially reduces the degree of deviation from the target capital structure. The robustness of the above findings is further verified.

In Column (3), the estimation results are based on the partial adjustment model. This section uses the partial adjustment model to test the impact of carbon finance on the speed of firms’ capital structure adjustment, constructing the following model:

At this point, the speed at which firms adjust their capital structure is such that, if the coefficient λ is significantly negative, it indicates that carbon finance increases this speeditit, whereas a significantly positive coefficient indicates the opposite: it decreases this speed. Controls are the same as Equation (4). It still controls for industry and year fixed effects. The regression results are shown in column (3) of Table 7. The results show that the coefficient of the cross-multiplier term of CF*Lev_p is significantly negative, which is highly consistent with the main regression findings.

Given the higher level of carbon financial development in municipalities, the results of this study may be sample-specific. Therefore, the test was re-run with the municipalities removed, and the regression results are shown in Columns (4) to (5) in Table 7. These results show that, even after removing municipalities directly under the central government, the effect of the level of carbon financial development on the deviation of firms’ capital structure adjustment speed from the target capital structure remains consistent with the principal regression. This further verifies the robustness of the conclusions.

5.3. Cross-Sectional Test

In traditional finance, allocating credit resources poses a problem that manifests as certain forms of credit discrimination. This hinders support for green technology innovation, preventing enterprises that need credit support from obtaining funds. It also reduces the speed at which enterprises adjust their capital structure and decreases their value. The development of carbon finance can help alleviate traditional finance’s inefficiencies in allocating credit resources. This part of the empirical regression analysis is based on model (10), and the results are shown in Table 8. In Column (1), the coefficient of Debt*TLev is significantly negative at the 1% level, indicating that highly indebted firms have a slower rate of capital restructuring. In Comparison, the coefficient of Debt*CF*TLev is significantly positive at the 1% level. .This suggests that the correlation between carbon finance and the pace of dynamic capital structure adjustment is more pronounced among enterprises with higher debt ratios, thereby confirming H2a. In Column (2), the coefficient of GI*TLev is significantly negative, indicating that firms with a low level of green innovation have a slower rate of capital structure adjustment. Meanwhile, the coefficient of GI*CF*TLev is significantly positive at the 1% level, indicating that the effect of carbon finance on the rate of capital structure adjustment is stronger in firms with low levels of green innovation, thereby confirming H2b. Overall, these results suggest that a mismatch in credit resources in traditional finance decreases the speed of enterprise capital structure adjustment. However, carbon finance can alleviate this mismatch, thereby increasing the speed of capital structure adjustment in over-indebted enterprises and in enterprises with low levels of green innovation.

5.4. Mechanism Test

This study argues that carbon finance eases financing constraints and improves financing availability for enterprises. Moreover, it improves the supervisory ability of financial institutions and reduces financing costs for enterprises. This, in turn, reduces the Cost of adjusting the capital structure and the deviation from the target capital structure. To further verify the theoretical logic of this study and analyze how carbon finance affects the dynamic adjustment of corporate capital structures, this section conducts an empirical analysis based on models (12) and (13). The regression results are shown in Table 9.

The mechanisms for analyzing financing constraints are presented in columns (1) to (3) of Table 9. In column 1, the coefficient of CF is significantly negative at the 1% level, indicating that carbon finance significantly reduces financing constraints for enterprises. In column 2, the coefficient of KZ*TLev is significantly negative, indicating that the higher the level of financing constraints for enterprises, the slower their capital structure adjustment. In Column (3), the coefficient of KZ is significantly positive at the 1% level, indicating that the greater the financing constraints on enterprises, the greater the deviation from their target capital structure. These results demonstrate that carbon finance accelerates the adjustment of corporate capital structures and reduces the deviation from target structures by alleviating corporate financing constraints, thereby confirming H3a.

The mechanisms for analyzing financing costs are presented in Columns (4) to (6) of Table 9. In Column (4), the CF coefficient is significantly negative at the 1% level, indicating that carbon finance reduces firms’ financing costs. In Column (5), the Cost*Lev coefficient is significantly negative, indicating that firms’ financing costs reduce the speed of their capital structure adjustment. In Column (6), the coefficient of Cost is significantly positive at the 1% level, indicating that the greater the Cost of corporate finance, the greater the deviation from the target capital structure. These results demonstrate that carbon finance accelerates the adjustment of firms’ capital structures and reduces deviation from the target capital structure by lowering financing costs, thereby confirming H3b.

6. Conclusion and Policy Recommendations

6.1. Conclusions

In the context of global climate governance and the shift towards a low-carbon economy, Carbon finance is a trading and investment activity based on “carbon emission rights” and their derivatives. It has emerged as a key, market-driven tool.

Carbon finance is the market-based environmental regulation that promotes green and inclusive economic development by reshaping the financial system. The growth of carbon finance is closely linked to the carbon finance market, primarily involving the secondary market for trading carbon emission rights. This policy would lead to a comprehensive green upgrade of the industrial chain, infusing sustainable green energy into the macroeconomy. However, the significant impact of carbon finance on microenterprises, particularly on their financial decision-making processes, has not been adequately explored. This study addresses this important gap in the literature by constructing a provincial carbon finance development index, and employing a dynamic partial adjustment model to systematically examine the relationship between carbon finance on the adjustments of capital structure regarding the speed of adjustment and the deviation from target of the A-share listed companies of China for the period 2014–2024. The empirical results show that carbon finance has a significant incentivizing effect on the optimization of their financial structure. These conclusions stand the most stringent tests of robustness, when employed using the difference-in-differences (DID) model, instrumental variables (IV) method and substitution variable methods thus confirming their reliability. The analysis brings out the following important results:

- (1)

- The main conclusion of the study is that the impact of carbon finance speed up the adjustment of companies’ capital structure to reach target leverage ratios, while diminishing the extent of deviation from such goal. This suggested that carbon finance improves the efficiency of corporate financing, thereby enabling companies to maintain better their capital structure in accordance with long-term objectives of value maximisation.

- (2)

- Cross-sectional test: The impact of carbon finance is not the same for all firms but exists in two classes of firms which exhibit the phenomenon: firms with a higher degree of green innovation and firms with a higher ratio of debt to equity (overleveraged firms). This heterogeneity reveals a further important mechanism: carbon finance is helping to correct the inefficiencies lying within the traditional method of allocating credit. It is directing credit towards the vital sectors of the low-carbon transition, notably green innovation firms, and imposing more restrictions on, and benefiting fully overleveraged firms that are in urgent need of restructuring of their capital.

- (3)

- Test of mechanism: Financing constraints and financing cost mechanism. Our empirical research shows that carbon finance will affect capital structure through two channels: First, the reduction of financing constraints and the acceleration of corporate capital structure adjustment can be obtained through the optimization of financing channels and the added convenience of financing; Second, the financing cost caused by friction is reduced and the endogenous motivation of enterprises to actively and rapidly adjust capital can be improved.

6.2. Policy Recommendations

Based on these findings, we have formulated the following specific policy recommendations.

Carbon finance should be treated by governments and regulatory authorities as a core market instrument for high-quality sustainable economic growth. Support for carbon markets, at both institutional and guidance levels, should be strengthened and expanded more firmly so as to widen policy coverage. At the macro-institutional level, more intensive energy sectors should be added over time in order to enhance the coverage of policy. This step reflects international experience that growing markets can result in better cost-effectiveness in reduction of emissions [68]. Governments should promote innovation and pilot projects in financial derivatives, such as carbon futures, options and asset securitisation. These measures will deepen markets and provide better instruments for risk management and price discovery. Research shows that derivatives are essential in finetuning carbon pricing instruments [69]. At the same time, it is essential to enhance the legal and regulatory framework supportive of carbon market transactions. This should enhance both data integrity and transparent transactions, as well as impartial enforcement. Sustaining market confidence rests on drawing confidence from solid regulation, which research points out is one of the primary bulwarks against manipulation and fraud [70]. At the micro level, studies suggest that policy forms should take appropriate, differentiated incentives and constrain policies [71]. The heterogenity effects identified by these studies scientifically justify the adoption of these 'tailor-made' approaches. Governments should set up schemes of bespoke support [72]. For instance, a 'Green Innovation Enterprise Carbon Finance Entry List' — a list that confers competitive advantages on select enterprises using financial tools to reduce carbon diplacement — could also offer enterprises that join priority of review, preferential charging or interest support. This would enhance the role of carbon finance (to finance schemes to support emission reductions) towards a low-carbon economy structure. At the same time, availability in carbon market compliance for excessively indebted enterprises (which have been designated as slow in transition) should be attached more closely to enforcement of environmental controls and rating of credit. This creates a mechanism of 'reverse pressure', where regulations linking non-compliance with negative consequences induce better capital structural movement and transition. This interconnected signalling regulatory approach has been proven to influence corporate behaviour [73].

Financial institutions should actively integrate carbon finance into their basic activities and viewing it through the twin lenses of national strategy and market opportunity. Firstly, institutions should align their products with national strategic goals by creating and promoting a series of finance products closely aligned to carbon management and environmental performance. This is part of their social responsibility and is the critical way to open up emerging sectors. Some products that might be relevant are ‘carbon commitment loans’ against rights to future carbon receipts, ‘sustainability-linked loans’ (where prices vary according to emissions reduction performance), and special products such as ‘blue bonds’ and ‘transition finance bonds’ that meet green project needs. Empirical research has now shown that such product innovations can significantly reduce the financing costs of green projects [74,75]. The goal is to provide for green transition enterprises at varying stages and of varying kinds, refinancing channels that are cheaper and more flexible than traditional kinds of credit. Secondly, financial institutions should systematically integrate carbon performance, carbon assets, advantage of environmental involvements, and debt levels into their credit rating and risk pricing models. This provides a more accurate base for the identification and support of enterprises that are high quality and genuinely committed to green development, and alleviates their financial constraints and effectively reduces the chances of misjudgment about high-carbon, high-risk assets. As a result, the allocation of financial resources can be precisely directed to sectors in which the maximum transformational dynamism and potential is present. Modern risk theory supports the incorporation of environmental aspects into credit models to achieve a holistic assessment of the long-term risks involved [76], and thus facilitate the sustainable transformation of the real economy.

Enterprises themselves also must fundamentally improve the enterprise managers' understanding of carbon finance, redefining carbon finance from a passive cost to something positive, a reduction of operational and compliance costs in the enterprises. Instead of a policy burden or a compliance cost, the basis of carbon finance becomes a clear strategic tool that can be used by enterprises to create a strategic advantage in a low-carbon world. Development of the carbon markets and good carbon asset management becomes a way to create trading profits and reduce compliance costs directly and in addition sends a message to the larger markets that the enterprise is focused on sustainable development strategies and good governance produces. This signaling will improve corporate valuation and attract long-term investors. [77]. Proactive green innovation and technological research and development should also be pursued by enterprises. This creates output that meets the regulatory requirements of the environment and is in synchronization with the objectives of carbon finance support. Thus, low cost of capital can be derived and financing costs will also be reduced directly. At the same time, voluntary behaviour in the area of modern technological research and production should be improved, in particular in the area of social and environmental governance information, especially carbon information, since this is the area where the largest reductions in external investor or financial institution information symmetry will occur. In addition to improving the effectiveness of the oversight mechanisms, flexibility in the management of the enterprise's capital structures will be improved. A well established literature has shown clearly the positive effect of good ESG disclosure on reduced capital costs [78] and establishes a sound basis for the enterprises in the new low carbon capital landscape of the enterprises' long-term sustainable growth.

It is essential for better understanding of the actual role of carbon finance for microenterprises in the economic system, thus enabling policy-makers to promote help measures for the microenterprises with even more targeted impact. It is these help measures which can enhance the sustainable development capacity of microenterprises and show the role of carbon finance in macroeconomic growth. Since the change in the dynamic adaptation of the capital structure is an act of free choice of firms, it is of great benefit in the overall advantage of improvement of efficiency for the allocation of social resources conducive to improvement of risk resistance of the economic system. This adjustment is a necessary measure for the firms to overcome the effects of carbon finance. For this reason we are convinced that cooperation between governmental authorities, finance einstitutes and firms can lead to improvement of the carbon finance system which induces a greater number of enterprises to participate in their green innovation. This will lead to a qualitatively better economic growth.

Author Contributions

Conceptualization, X.T. and Y.Z.; methodology, X.W.; software, X.T. and X.W.; validation, X.W.; formal analysis, Y.Z.; investigation, X.W.; resources, X.W.; data curation, X.T. and Y.Z.; writing— original draft preparation, Y.Z. and S.M.L.; writing—review and editing, Y.Z.; visualization, Y.Z. and X.W.; supervision, X.T. and Y.Z.; project administration. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The original contributions presented in this study are included in the article. Further inquiries can be directed to the corresponding author.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Su, L.; Yu, W.; Zhou, Z. Global Trends of Carbon Finance: A Bibliometric Analysis. Sustainability 2023, 15, 6784. [CrossRef]

- Zhou, K.; Li, Y. Carbon finance and carbon market in China: Progress and challenges. J. Clean. Prod. 2019, 214, 536–549. [CrossRef]

- Wang, E.; Nie, J.; Zhan, H. The Impact of Carbon Emissions Trading on the Profitability and Debt Burden of Listed Companies. Sustainability 2022, 14, 13429. [CrossRef]

- Callon, M. Civilizing markets: Carbon trading between in vitro and in vivo experiments. Accounting, Organ. Soc. 2009, 34, 535–548. [CrossRef]

- Felli, R. On Climate Rent. Hist. Mater. 2014, 22, 251–280. [CrossRef]

- Bridge, G.; Bulkeley, H.; Langley, P.; van Veelen, B. Pluralizing and problematizing carbon finance. Prog. Hum. Geogr. 2019, 44, 724–742. [CrossRef]

- Jiang, L.; Niu, H.; Ru, Y.; Tong, A.; Wang, Y. Can carbon finance promote high quality economic development: evidence from China. Heliyon 2023, 9, e22698. [CrossRef]

- Carraro, C.; Favero, A.; Massetti, E. Investments and public finance in a green, low carbon, economy. Energy Econ. 2012, 34, S15–S28. [CrossRef]

- Drobetz, W.; Wanzenried, G. What determines the speed of adjustment to the target capital structure?. Appl. Financial Econ. 2006, 16, 941–958. [CrossRef]

- Cook, D.O.; Tang, T. Macroeconomic conditions and capital structure adjustment speed. J. Corp. Finance 2010, 16, 73–87. [CrossRef]

- Öztekin, Ö.; Flannery, M.J. Institutional determinants of capital structure adjustment speeds. J. Financial Econ. 2012, 103, 88–112. [CrossRef]

- Bajaj, Y.; Kashiramka, S.; Singh, S. Economic policy uncertainty and leverage dynamics: Evidence from an emerging economy. Int. Rev. Financial Anal. 2021, 77. [CrossRef]

- Li, G.M.; Zhang, W.J. Research on industrial carbon emissions and emission reduction mechanisms under carbon trading in China. China Popul. Resour. Environ. 2017, 27, 141–148.

- Huang, X.L.; Zhang, X.C.; Liu, Y. Has China’s carbon trading policy delivered an environmental dividend? Econ. Rev. 2018, 6, 86–99.

- Shen, H.T.; Huang, N. Will the Carbon Emission Trading Scheme Improve Firm Value? Financ. Trade Econ. 2019, 40, 144−161.

- Liu, H.Y.; Wang, Y. The Economic Dividend Effect of a Tradable Policy Mix of Energy Usage Rights and Carbon Emission Rights. China Popul. Resour. Environ. 2019, 29, 1–10.

- Zhang, H.J.; Deng, M.S.; Zhang, P. Analysis of the impact of China’s emissions trading scheme on reducing carbon emissions. Energy Procedia 2019, 158, 3596–3601.

- Li, Z.; Wang, J. Spatial emission reduction effects of China’s carbon emissions trading in China: quasi-natural experiments and policy spillovers. Chin. J. Popul. Resour. Environ. 2021, 19, 246–255. [CrossRef]

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. Am. Econ. Rev. 1958, 48, 261-297.

- Fischer, E.O.; Heinkel, R., Zechner, J. Dynamic capital structure choice: Theory and tests. J. Financ. 1989, 44, 19-40.

- Titman, S.; Wessels, R. The determinants of capital structure choice. J. Financ. 1988, 43, 1-19.

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: evidence from the field. J. Financial Econ. 2001, 60, 187–243. [CrossRef]

- Lööf, H. Dynamic optimal capital structure and technical change. Struct. Chang. Econ. Dyn. 2004, 15, 449-468.

- Titman, S.; Tsyplakov, S. A Dynamic Model of Optimal Capital Structure. Rev. Finance 2007, 11, 401–451. [CrossRef]

- Goldstein, R.; Ju, N.; Leland, H. An EBIT-Based Model of Dynamic Capital Structure. J. Bus. 2001, 74, 483–512. [CrossRef]

- Leary, M.T.; Roberts, M.R. Do firms rebalance their capital structures?. J. Financ. 2005, 60, 2575-2619.

- Harford, J.; Klasa, S.; Walcott, N. Do firms have leverage targets? Evidence from acquisitions. J. Financial Econ. 2009, 93, 1–14. [CrossRef]

- A Korajczyk, R.; Levy, A. Capital structure choice: macroeconomic conditions and financial constraints. J. Financ. Econ. 2003, 68, 75–109. [CrossRef]

- Jiang, F.X.; Huang, J.C. The process of marketization and the dynamic adjustment of the capital structure. Manag. World 2011, 27, 124-134+167.

- Luo, M.; Nie, W.Z. Fiscal policy, monetary policy and the dynamic adjustment of corporate capital structure: in view of empirical research on listed companies in China. Econ. Sci. 2012, 18−32.

- Flannery, M.J.; Rangan, K.P. Partial adjustment toward target capital structures. J. Financial Econ. 2006, 79, 469–506. [CrossRef]

- Cowan, E. Topical issues in environmental finance: plenary paper. EEPSEA 1998.

- Cavanagh, C.J.; Vedeld, P.O.; Petursson, J.G.; Chemarum, A.K. Agency, inequality, and additionality: contested assemblages of agricultural carbon finance in western Kenya. J. Peasant. Stud. 2020, 48, 1207–1227. [CrossRef]

- Geng, L.; Hu, J.; Shen, W. The impact of carbon finance on energy consumption structure: evidence from China. Environ. Sci. Pollut. Res. 2022, 30, 30107–30121. [CrossRef]

- Fullerton, D.; West, S.E. Can Taxes on Cars and on Gasoline Mimic an Unavailable Tax on Emissions?. J. Environ. Econ. Manag. 2002, 43, 135–157. [CrossRef]

- Tang, L.; Wu, J.; Yu, L.; Bao, Q. Carbon emissions trading scheme exploration in China: A multi-agent-based model. Energy Policy 2015, 81, 152–169. [CrossRef]

- Klemetsen, M.; Rosendahl, K.E.; Jakobsen, A.L. The impacts of the EU ETS on Norwegian plants' environmental and economic performance. Clim. Chang. Econ. 2020, 11, 2050006. [CrossRef]

- Colmer, J.; Martin, R.; Muûls, M.; Wagner, U.J. Does Pricing Carbon Mitigate Climate Change? Firm-Level Evidence from the European Union Emissions Trading System. Rev. Econ. Stud. 2024, 92, 1625–1660. [CrossRef]

- Gao, M. The impacts of carbon trading policy on China's low-carbon economy based on county-level perspectives. Energy Policy 2023, 175. [CrossRef]