Submitted:

10 October 2025

Posted:

29 October 2025

You are already at the latest version

Abstract

This paper investigates the crucial role of internal control (IC) in business management and explores how advanced artificial intelligence (AI) technologies, such as Artificial General Intelligence (AGI), Artificial Super Intelligence (ASI), and systems related to Universal Basic Income (UBI), can enhance IC mechanisms. IC is vital for ensuring operational efficiency, risk management, compliance, and governance effectiveness inenterprises. The COSO framework provides a structured approach to achieving theseobjectives through its five components. AI technologies, particularly machine learning,natural language processing, and robotic process automation, offer significant potential toautomate routine tasks, provide enhanced decision support, and enable real-timemonitoring and alerts in IC systems. Practical case studies demonstrate AI’s impact onimproving inventory management, fraud detection, and employee performance evaluation.However, challenges such as data quality, skill shortages, and ethical issues must beaddressed. The integration of AI with other technologies like blockchain and IoT, alongwith the development of global standards, will shape the future of IC. This paper calls forfurther research and implementation of AI in IC to drive operational excellence andsustainable growth.

Keywords:

internal control

; business management

; artificial general intelligence (AGI)

; artificial super intelligence (ASI)

; universal basic income (UBI)

; advanced AI

; efficiency

I. Introduction

In today's rapidly evolving business landscape, enterprises and organizations are confronted with an unprecedented array of challenges and opportunities. The complexity of global markets, regulatory environments, and technological advancements has necessitated a reevaluation of traditional management practices. Among these practices, internal control (IC) stands out as a critical component for ensuring the stability, efficiency, and growth of businesses. As humanity stands on the cusp of an interstellar age, propelled by advancements in quantum computing, artificial intelligence (AI), and space exploration, the disciplines of accounting and financial management face unprecedented transformations. This transition highlights the critical role of internal control (IC) in adapting to new economic, social, and technological paradigms [1].This paper aims to delve into the pivotal role of internal control within the management framework of enterprises and organizations, elucidating its significance for sustainable development and operational excellence. Furthermore, the paper will explore the burgeoning field of artificial intelligence (AI), particularly in the context of Artificial General Intelligence (AGI), Artificial Super Intelligence (ASI), and the implications of Universal Basic Income (UBI) on business operations. The integration of AI into internal control systems promises to revolutionize the way businesses manage risks, optimize processes, and enhance governance. This paper will provide a comprehensive analysis of this integration, supported by theoretical frameworks and practical case studies, to demonstrate how AI can be harnessed to fortify internal control mechanisms and drive organizational success.

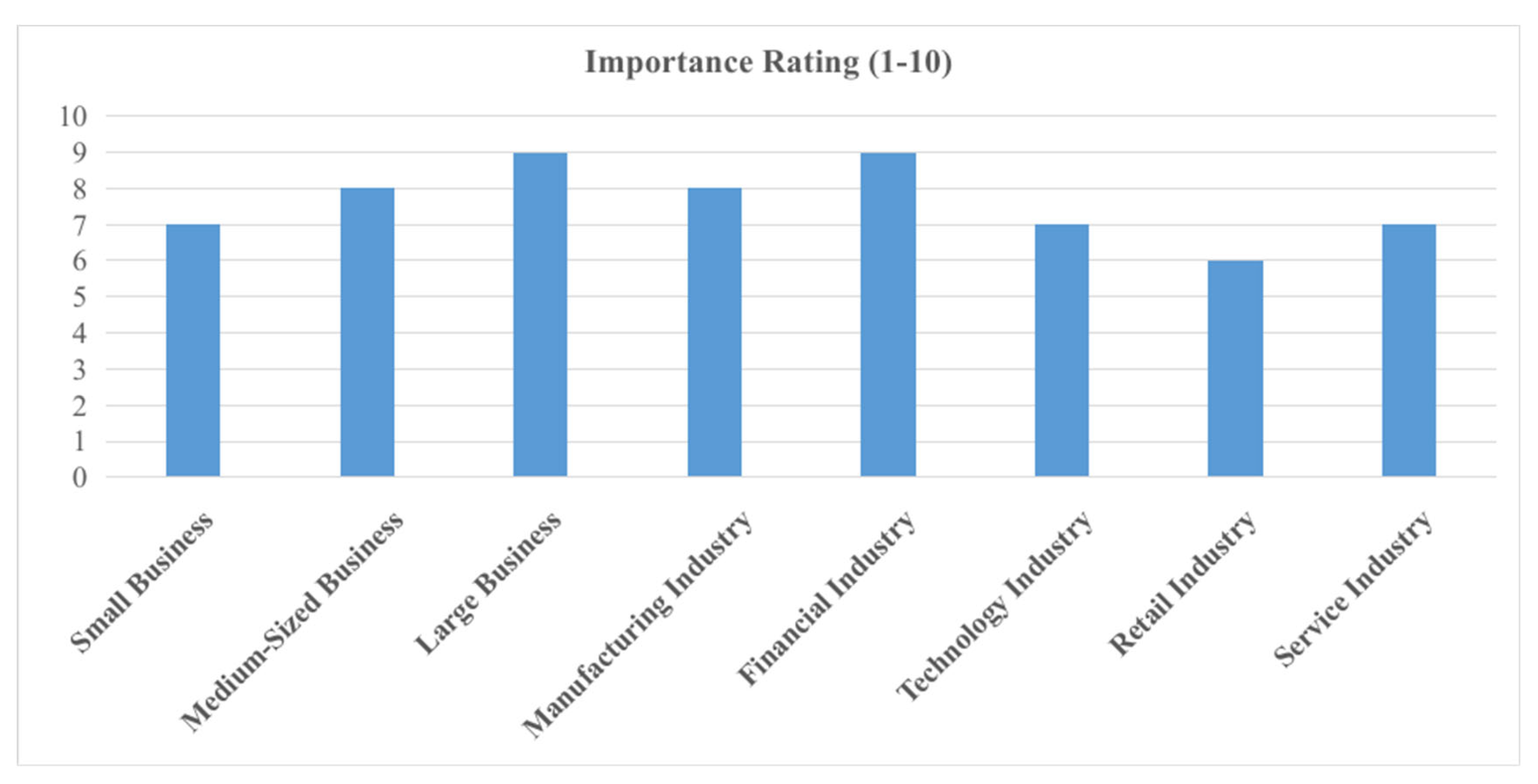

Figure 1.

A bar chart depicting the importance rating (1-10) of internal control across different business sizes and industries.

Figure 1.

A bar chart depicting the importance rating (1-10) of internal control across different business sizes and industries.

II. The Importance of Internal Control in Business Management

1. Definition and Objectives

Internal control is a system of policies, procedures, and practices designed to provide reasonable assurance that an organization's objectives are achieved. It encompasses a wide range of activities, from the most basic operational tasks to complex financial and compliance processes. The primary objectives of internal control are to ensure the effectiveness and efficiency of operations, the reliability of financial reporting, and compliance with applicable laws and regulations. The COSO (Committee of Sponsoring Organizations of the Treadway Commission) framework is widely recognized as the authoritative guide for internal control systems, providing a structured approach to achieving these objectives through five interrelated components: control environment, risk assessment, control activities, information and communication, and monitoring activities.

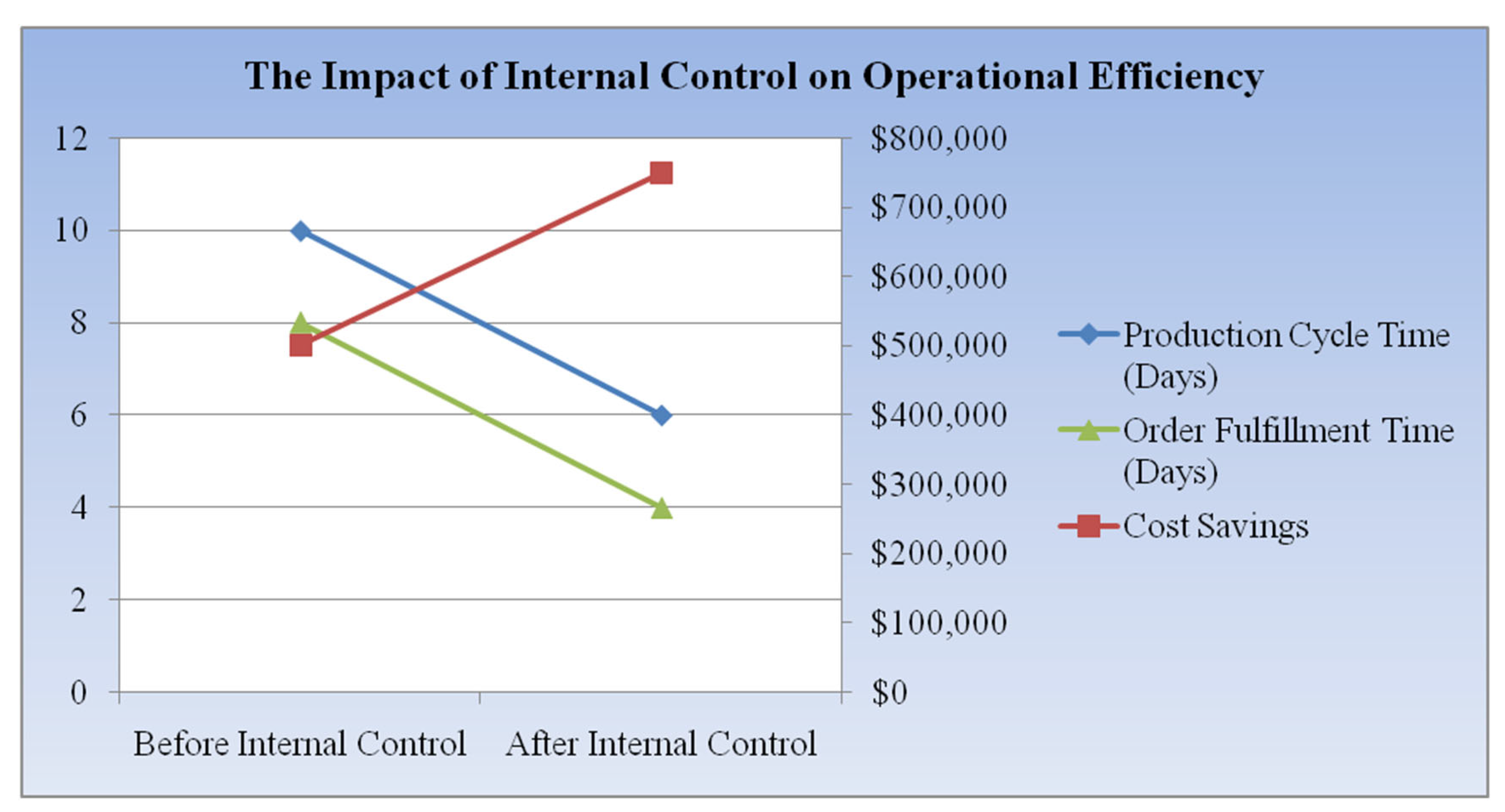

2. Operational Efficiency

One of the key benefits of a robust internal control system is the enhancement of operational efficiency. By establishing clear procedures and responsibilities, internal control ensures that tasks are performed consistently and effectively [1]. For example, in a manufacturing environment, internal controls can dictate the quality checks at various stages of production, ensuring that only products meeting the specified standards are released to the market. This not only improves customer satisfaction but also reduces the costs associated with rework and waste. Moreover, internal control systems can streamline processes by eliminating redundant steps and identifying bottlenecks, thereby accelerating the flow of goods and services through the organization. Shi et al. (2025) proposed a modified RIME algorithm to enhance numerical optimization by learning covariance and enhancing diversity, which similarly aims to optimize processes by identifying and eliminating inefficiencies [2]>.

Figure 2.

line graph showing the improvement in operational efficiency (e.g., production cycle time, cost savings) before and after implementing internal control.

Figure 2.

line graph showing the improvement in operational efficiency (e.g., production cycle time, cost savings) before and after implementing internal control.

3. Risk Management

Risk is an inherent part of any business endeavor, and internal control plays a crucial role in identifying, assessing, and mitigating these risks. Through systematic risk assessment procedures, organizations can anticipate potential threats and develop strategies to address them.For instance, in the financial sector, internal controls are vital for detecting and preventing fraud, ensuring the integrity of financial transactions, and managing credit risks. Yu et al. (2025) demonstrated the effectiveness of a CNN-Transformer framework in detecting financial fraud in listed companies, highlighting the importance of advanced algorithms in identifying fraudulent activities [3].By maintaining a strong internal control environment, businesses can minimize the likelihood of adverse events and their impact on the organization's financial health and reputation.

4. Compliance and Governance

Compliance with laws and regulations is non-negotiable for businesses operating in any jurisdiction. Internal control systems are instrumental in ensuring that organizations adhere to these requirements. They provide a framework for monitoring and reporting on compliance activities, enabling businesses to demonstrate their commitment to ethical and legal standards. Sound corporate governance hinges on transparency, and accounting is the primary mechanism for achieving it. Audited financial statements provide an objective snapshot of a company's operations to shareholders, creditors, and other stakeholders, holding management accountable for their stewardship [23]. In the context of corporate governance, internal control supports the board of directors and senior management in fulfilling their fiduciary duties. It helps to establish a culture of transparency and accountability, where decisions are made in the best interests of the organization and its stakeholders [6].

III. The Evolution of AI and Its Impact on Business

1. AI Technologies

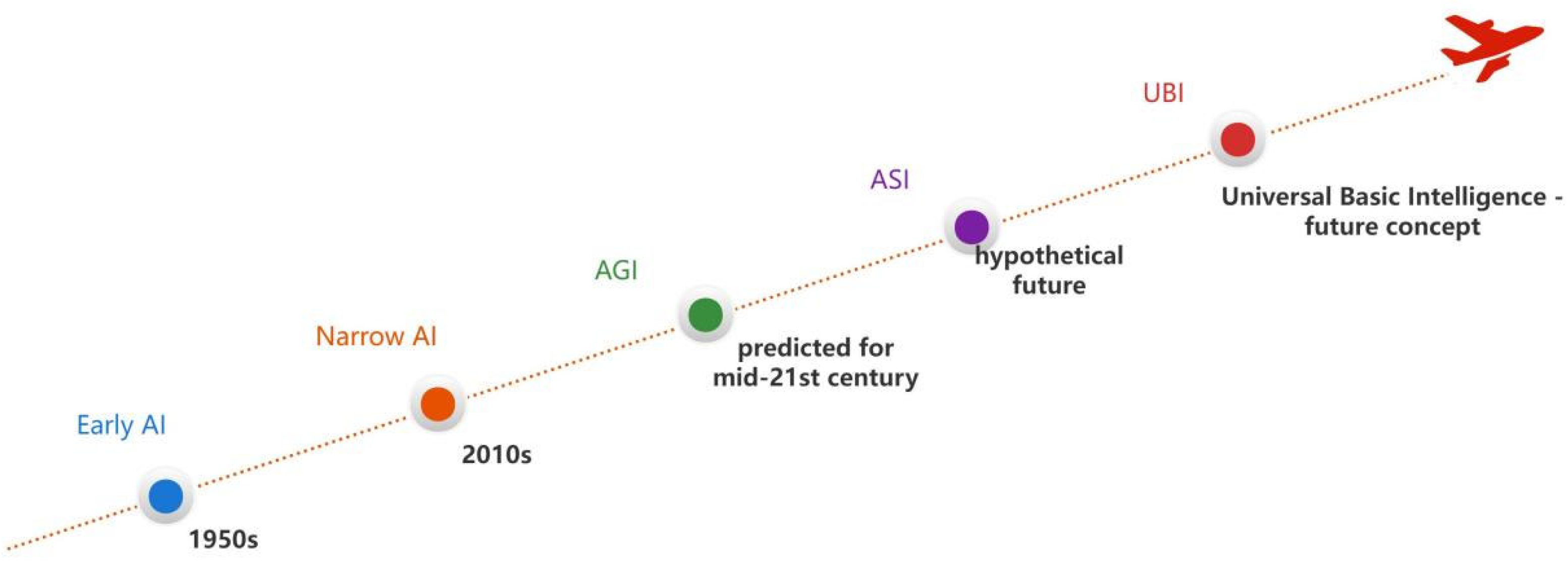

The field of artificial intelligence has witnessed remarkable advancements in recent years, with AGI, ASI, and UBI emerging as key concepts that will shape the future of business. AGI refers to a machine's ability to understand, learn, and apply knowledge across a broad range of tasks at a human level. ASI, on the other hand, represents a further evolution, where machines surpass human intelligence in virtually all domains. UBI, while not a form of AI, is a social policy concept that has implications for the workforce and business operations, as it may influence labor markets and consumer behavior. These technologies have the potential to transform business processes, from automating routine tasks to providing sophisticated decision support [4].

Figure 3.

A timeline showing the evolution of AI technologies (e.g., AGI, ASI, UBI) and future predictions on the historical development and future trends of AI technologies.

Figure 3.

A timeline showing the evolution of AI technologies (e.g., AGI, ASI, UBI) and future predictions on the historical development and future trends of AI technologies.

2. AI in Business

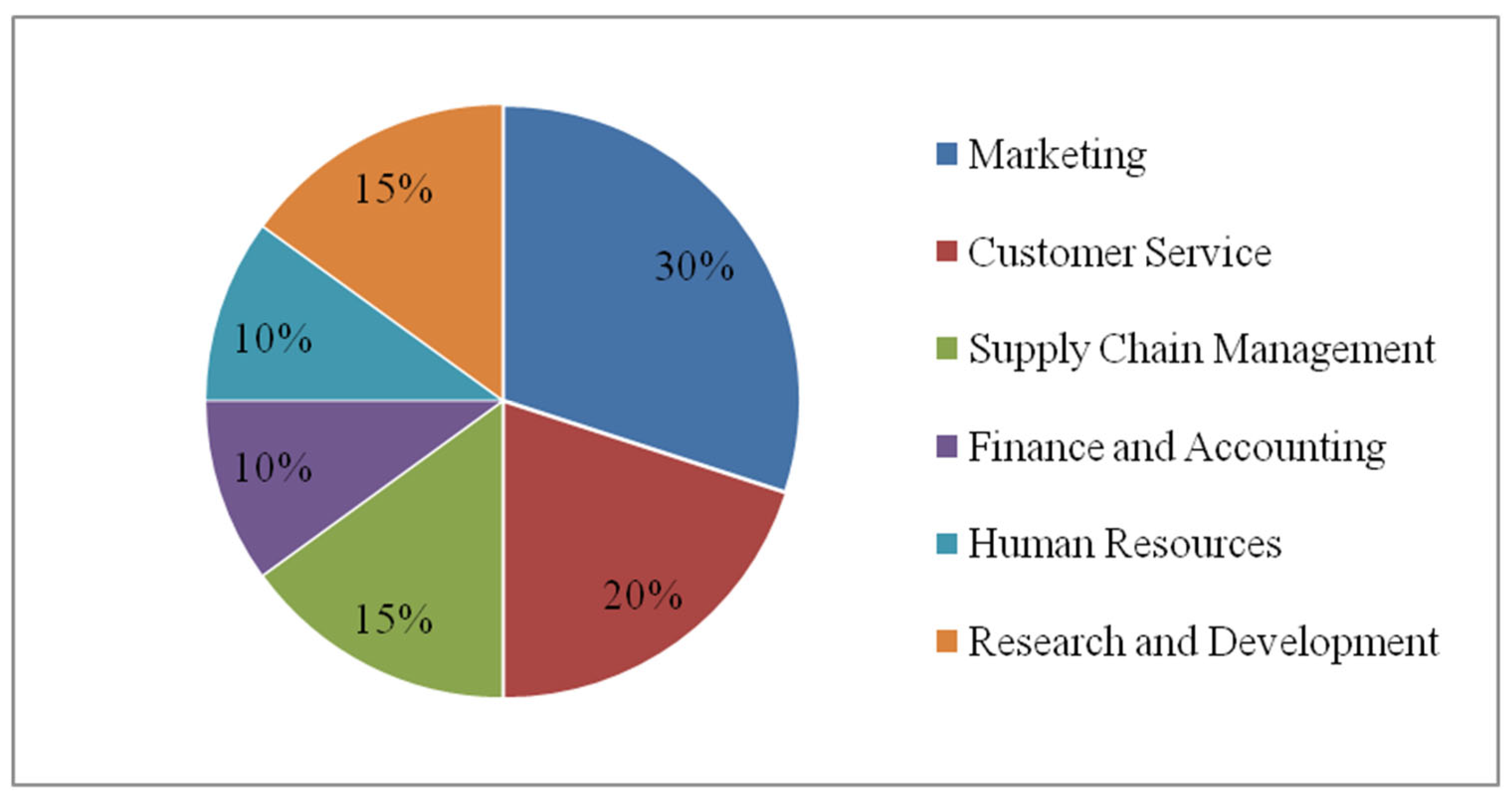

Currently, AI is being employed in various business functions to enhance productivity and decision-making. In marketing, AI algorithms analyze consumer data to predict buying patterns and personalize marketing campaigns. In customer service, chatbots powered by AI provide instant responses to customer inquiries, improving customer satisfaction. In supply chain management, AI optimizes logistics and inventory levels, reducing costs and improving delivery times. As AI technologies continue to mature, their application in business is expected to expand, offering new opportunities for innovation and competitive advantage [5].

Figure 4.

A pie chart illustrating the distribution of AI applications across various business functions.

Figure 4.

A pie chart illustrating the distribution of AI applications across various business functions.

VI. AI in Internal Control: Theoretical Frameworks

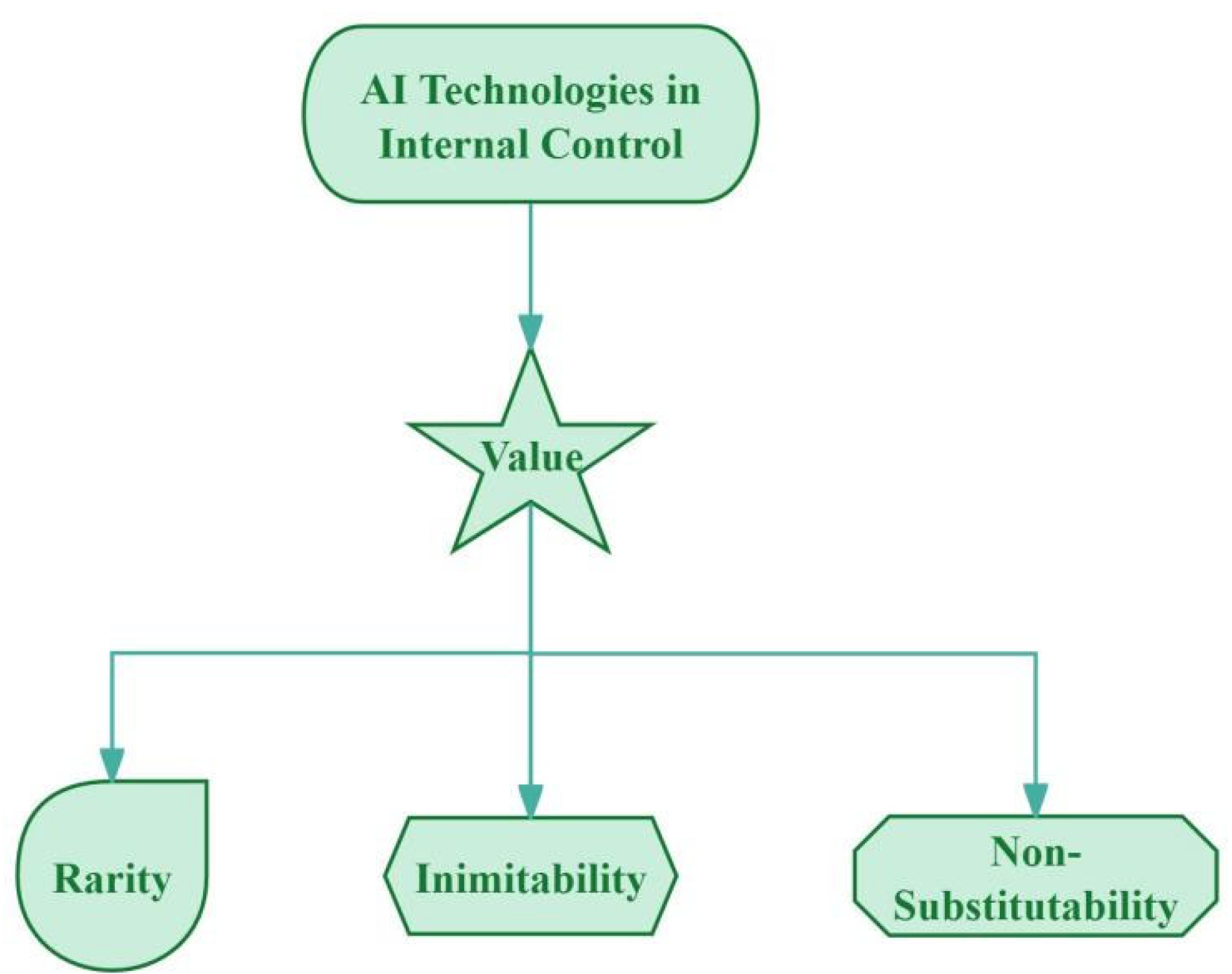

1. Resource-Based View (RBV)

The Resource-Based View (RBV) posits that organizations can gain a competitive advantage by leveraging their unique resources and capabilities. In the context of internal control, AI can be considered a strategic resource that, when effectively deployed, can enhance the organization's ability to manage risks, improve operational efficiency, and ensure compliance. By investing in AI technologies, businesses can develop capabilities that are valuable, rare, inimitable, and non-substitutable (VRIN), thereby creating a sustainable competitive edge. For example, an organization that uses AI for advanced fraud detection may be able to prevent significant financial losses, which not only protects its financial health but also enhances its reputation in the market [11].

Figure 5.

The following flowchart depicts how businesses can enhance the value, rarity, inimitability, and non-substitutability (VRIN) of their resources through AI technologies.

Figure 5.

The following flowchart depicts how businesses can enhance the value, rarity, inimitability, and non-substitutability (VRIN) of their resources through AI technologies.

In multi-departmental or geographically dispersed organizations, distributed control systems are essential. Liu and Zhu (2022) propose a distributed inverse constrained reinforcement learning framework that enables decentralized agents to learn optimal control policies while respecting shared constraints. This approach aligns with the resource-based view, as it allows each unit to develop localized AI capabilities that are coordinated globally, thereby enhancing the organization’s overall control resilience and adaptability without centralizing all decision-making authority [12].

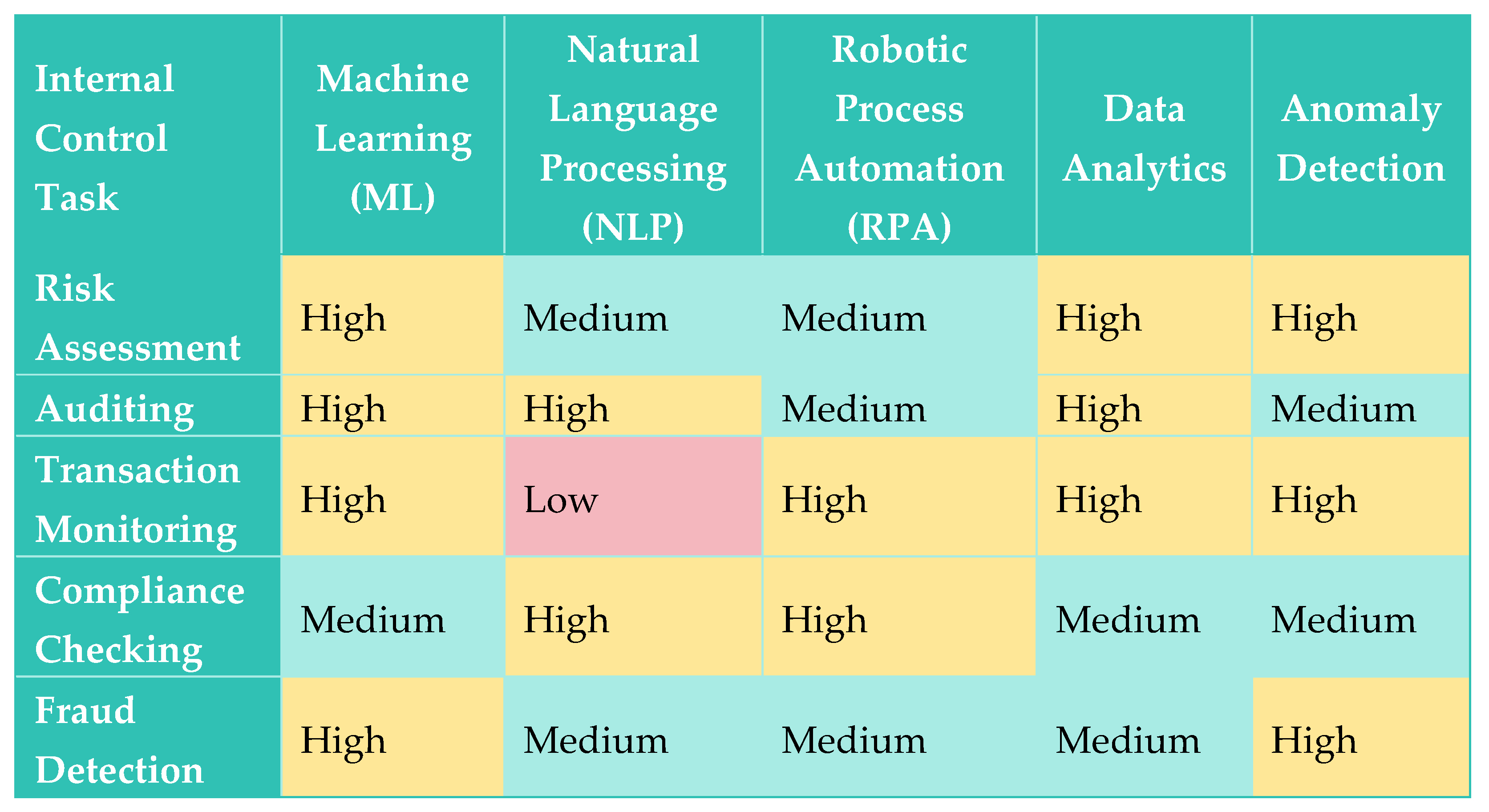

2. Task-Technology Fit (TTF)

The Task-Technology Fit (TTF) theory suggests that the effectiveness of a technology implementation depends on the alignment between the technology's capabilities and the requirements of the task. In internal control, this means that AI systems should be designed and configured to match the specific control activities and processes within the organization. For instance, if the task is to monitor financial transactions for fraud, the AI system should be capable of analyzing large volumes of data, identifying patterns, and flagging suspicious activities. By ensuring a good fit between AI technology and internal control tasks, organizations can maximize the benefits of AI while minimizing the risks of technology misalignment [13].

Figure 6.

A matrix illustrating the fit between various internal control tasks and AI technologies.

3. COSO Framework

The COSO framework provides a comprehensive and flexible structure for implementing internal control systems. It can be adapted to incorporate AI technologies, ensuring that the benefits of AI are realized within a well-defined control environment. The five components of the COSO framework can be enhanced by AI in the following ways: [14,15]

Control Environment: AI can support the development of a strong control culture by providing data-driven insights into employee behavior and performance.

Risk Assessment: AI algorithms can analyze vast amounts of data to identify emerging risks more quickly and accurately than traditional methods.

Control Activities: AI can automate and enhance control activities, such as reconciliations, approvals, and monitoring, reducing the risk of human error.

Information and Communication: AI can facilitate the timely and accurate flow of information within the organization, improving communication and decision-making.

Monitoring Activities: AI can continuously monitor internal control systems, providing real-time feedback and alerts on the effectiveness of controls.

Furthermore, the integration of AI into the COSO framework can be theoretically grounded in meta inverse constrained reinforcement learning (MICRL), as proposed by Liu and Zhu (2024). Their work introduces a principled approach to learning optimal policies under constraints, which is particularly relevant for internal control systems that must balance automation with regulatory and ethical boundaries. MICRL ensures convergence to feasible control policies while maintaining generalization across dynamic business environments, thereby enhancing the robustness of AI-enabled control mechanisms [16].

V. Practical Applications of AI in Internal Control

1. Automation of Routine Tasks

One of the most immediate and tangible benefits of AI in internal control is the automation of routine and repetitive tasks. These tasks, which often consume a significant amount of time and effort from employees, can be performed more efficiently and accurately by AI systems. For example, data entry tasks can be automated using optical character recognition (OCR) and machine learning algorithms, reducing the risk of transcription errors. Approval processes, such as purchase orders and expense reports, can be streamlined through AI-powered workflow systems that automatically route documents to the appropriate approvers based on predefined rules. Financial reconciliations, a critical control activity, can be enhanced by AI algorithms that compare data from different sources and identify discrepancies in real-time, ensuring the accuracy and integrity of financial statements [7].OuYang et al. (2025) developed the Beaver behavior optimizer for parameter identification in engineering problems, which similarly aims to optimize and automate routine tasks in internal control [8].

Figure 7.

A flowchart showing how AI systems automate routine tasks such as data entry, approval processes, and financial reconciliations.

Figure 7.

A flowchart showing how AI systems automate routine tasks such as data entry, approval processes, and financial reconciliations.

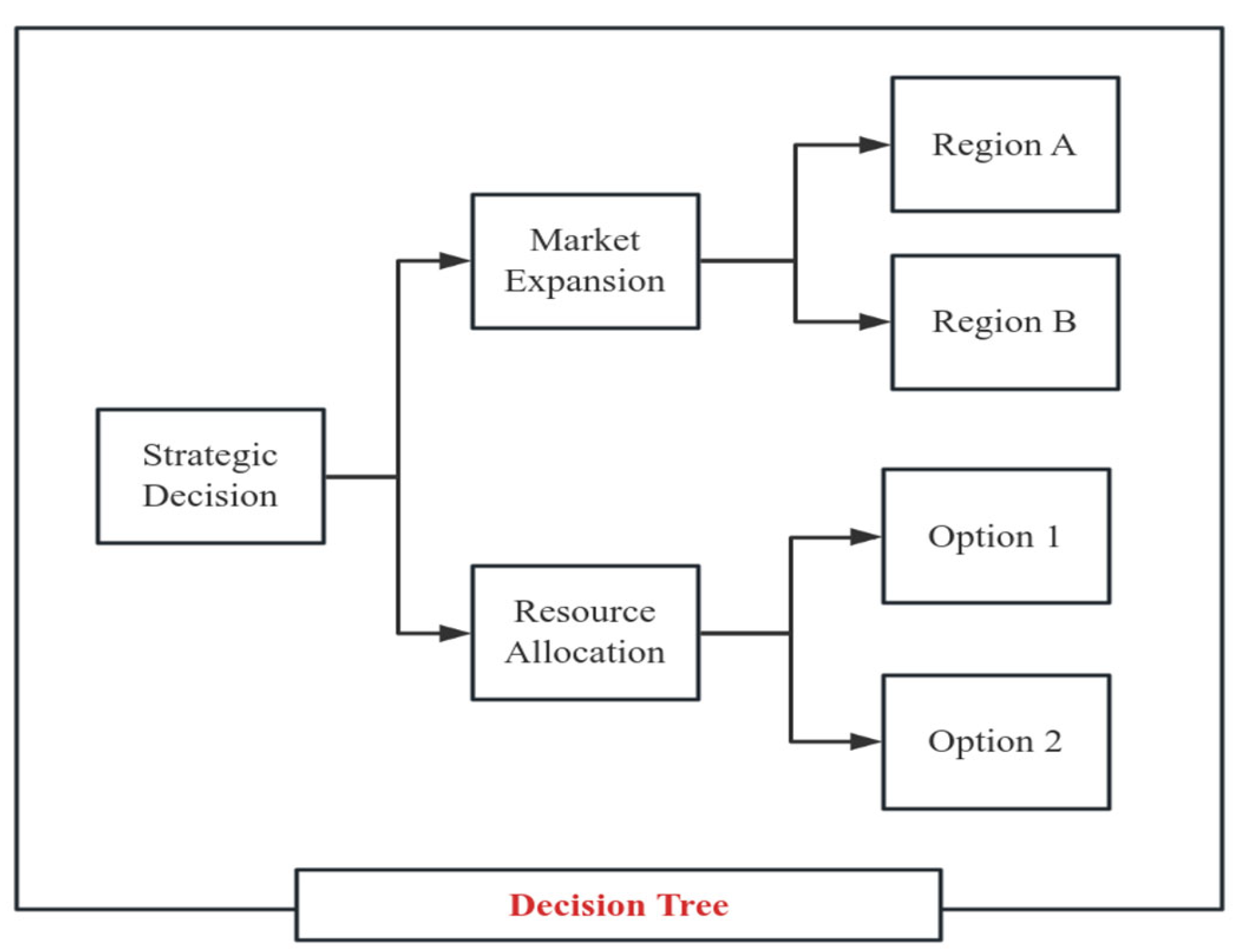

2. Enhanced Decision Support

AI has the potential to transform decision-making within organizations by providing managers with timely and actionable insights. Through advanced analytics and predictive modeling, AI systems can process large volumes of structured and unstructured data to identify trends, patterns, and correlations that may not be apparent to human analysts. AI-driven Activity-Based Costing (ABC) systems have been instrumental in enhancing cost management practices by providing real-time cost insights and predictive analytics. These systems automate data processing, identify cost drivers, and optimize resource allocation, supported by advanced algorithmic approaches. For example, a logistics firm adopted an AI-powered ABC system to address regional cost variances in delivery operations, reducing cost variances by 25% through the use of clustering algorithms and reinforcement learning for dynamic cost adjustments [24]. In risk management, AI can simulate various risk scenarios and quantify their potential impact on the organization, enabling managers to develop more effective risk mitigation strategies. Zhang et al. (2025) analyzed credit risk for SMEs using graph neural networks in supply chains, demonstrating the potential of AI in risk assessment and management [9].

Figure 8.

A decision tree diagram showing how AI systems support strategic planning, market expansion, and resource allocation through data analysis and predictive models.

Figure 8.

A decision tree diagram showing how AI systems support strategic planning, market expansion, and resource allocation through data analysis and predictive models.

In contexts where non-verbal cues or employee behavioral analytics are relevant—such as in compliance training or fraud interviews—AI systems can benefit from advanced multimodal perception models. Zhang et al. (2024) present the CF-DAN framework, which employs a cross-fusion dual-attention mechanism to enhance facial-expression recognition accuracy. Although originally designed for emotion recognition, the architecture’s ability to fuse heterogeneous data streams and focus on salient features can be adapted for AI-driven internal audits, especially in detecting anomalies in human-computer interactions or assessing stress patterns during compliance reviews [17].

3. Real-Time Monitoring and Alerts

A critical aspect of internal control is the ability to monitor activities and detect anomalies in real-time. AI systems, with their capacity for continuous learning and pattern recognition, are well-suited for this task. By analyzing data streams from various sources, such as financial transactions, operational logs, and employee activities, AI algorithms can identify deviations from established norms and trigger alerts for further investigation [10,18].Li et al. (2024) developed a bimodal convolutional neural network for deception detection from linguistic and physiological data streams, illustrating the potential of AI in real-time monitoring and anomaly detection [19].

VI. Case Studies

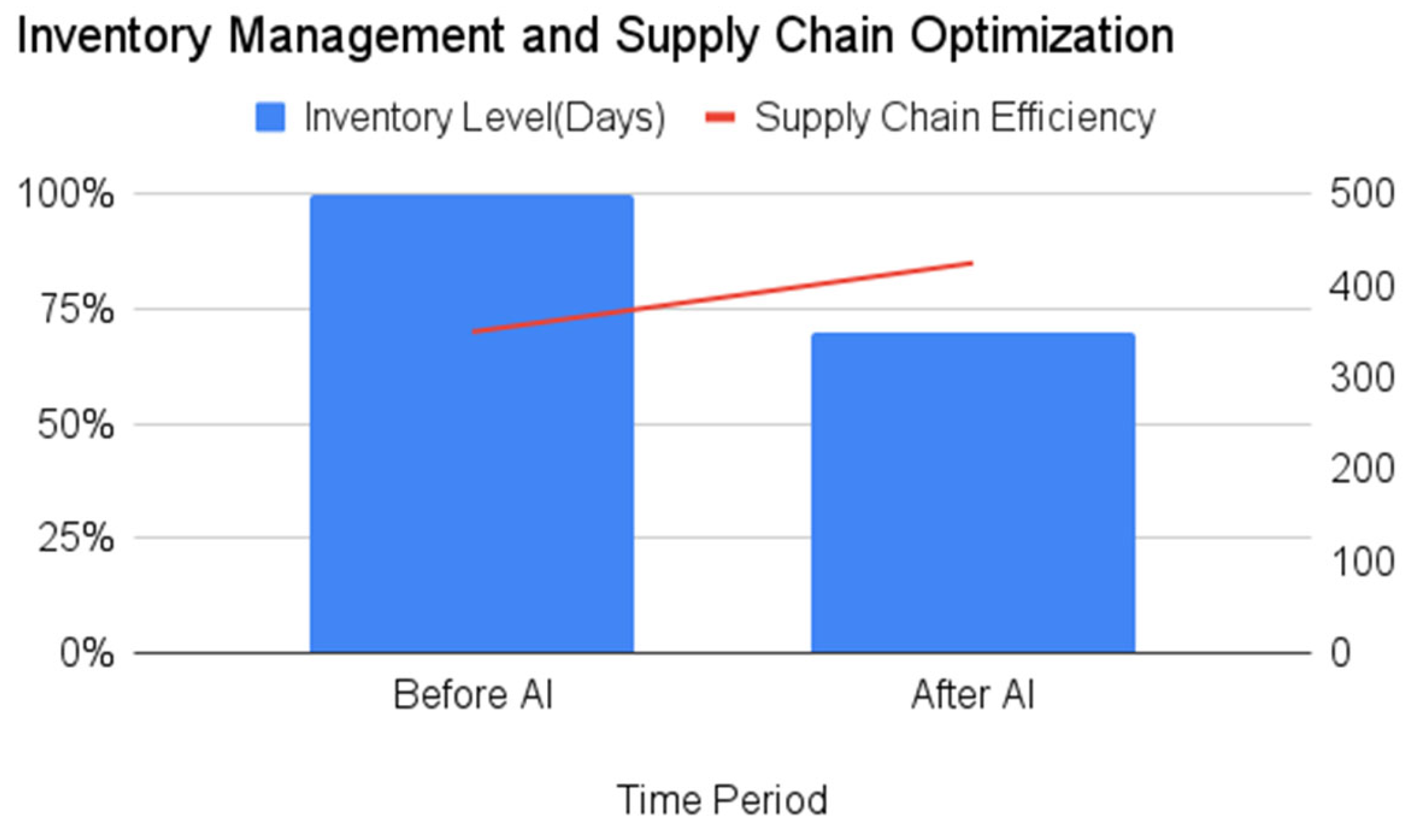

1. Case Study 1: Manufacturing Company - Inventory Management and Supply Chain Optimization

A leading manufacturing company implemented AI-driven internal control systems to optimize inventory management and supply chain operations. By integrating machine learning algorithms, the company was able to predict demand patterns more accurately, reducing inventory levels by 20% while maintaining high service levels. The AI system also monitored supplier performance in real-time, identifying potential delays and quality issues, allowing the company to take proactive measures to mitigate risks. This not only improved operational efficiency but also enhanced the company's reputation among customers. Zhao et al. (2025) developed probabilistic contingent planning based on hierarchical task networks for high-quality plans, which similarly aims to optimize supply chain and inventory management through advanced algorithms [20].

Figure 9.

A bar chart showing inventory levels and supply chain efficiency before and after implementing an AI-driven internal control system.

Figure 9.

A bar chart showing inventory levels and supply chain efficiency before and after implementing an AI-driven internal control system.

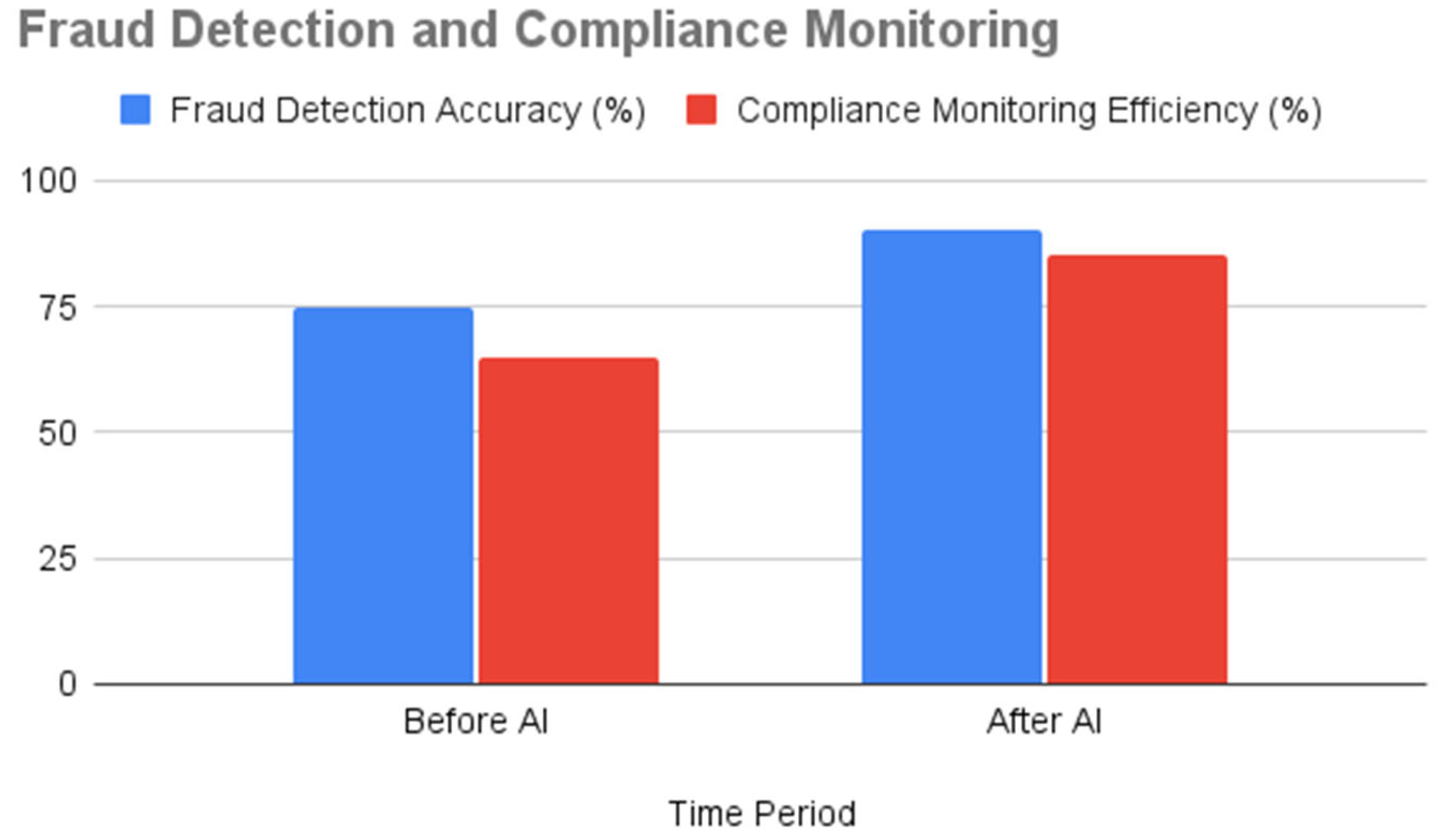

2. Case Study 2: Financial Institution - Fraud Detection and Compliance Monitoring

A major financial institution leveraged AI technologies to enhance its fraud detection and compliance monitoring capabilities. Using advanced analytics and machine learning, the institution was able to identify fraudulent transactions in real-time, reducing financial losses by 30%. The AI system also automated the process of regulatory compliance, ensuring that the institution met all legal requirements without manual intervention. This not only saved significant resources but also improved the institution's compliance posture and reduced the risk of regulatory penalties.

Figure 10.

A line graph depicting the improvement in fraud detection accuracy and compliance monitoring efficiency before and after implementing AI technologies.

Figure 10.

A line graph depicting the improvement in fraud detection accuracy and compliance monitoring efficiency before and after implementing AI technologies.

3. Case Study 3: Technology Firm - Employee Performance Evaluation and Resource Allocation

A technology firm employed AI to optimize employee performance evaluation and resource allocation. By analyzing employee data, including performance metrics, project outcomes, and feedback, the AI system provided personalized performance evaluations and recommendations for resource allocation. This led to a 25% improvement in employee productivity and a more efficient use of resources, supporting the firm's growth and innovation efforts.

Figure 10.

The following radar chart illustrates improvements in employee performance and resource allocation efficiency before and after implementing an AI system.

Figure 10.

The following radar chart illustrates improvements in employee performance and resource allocation efficiency before and after implementing an AI system.

VII. Challenges and Limitations

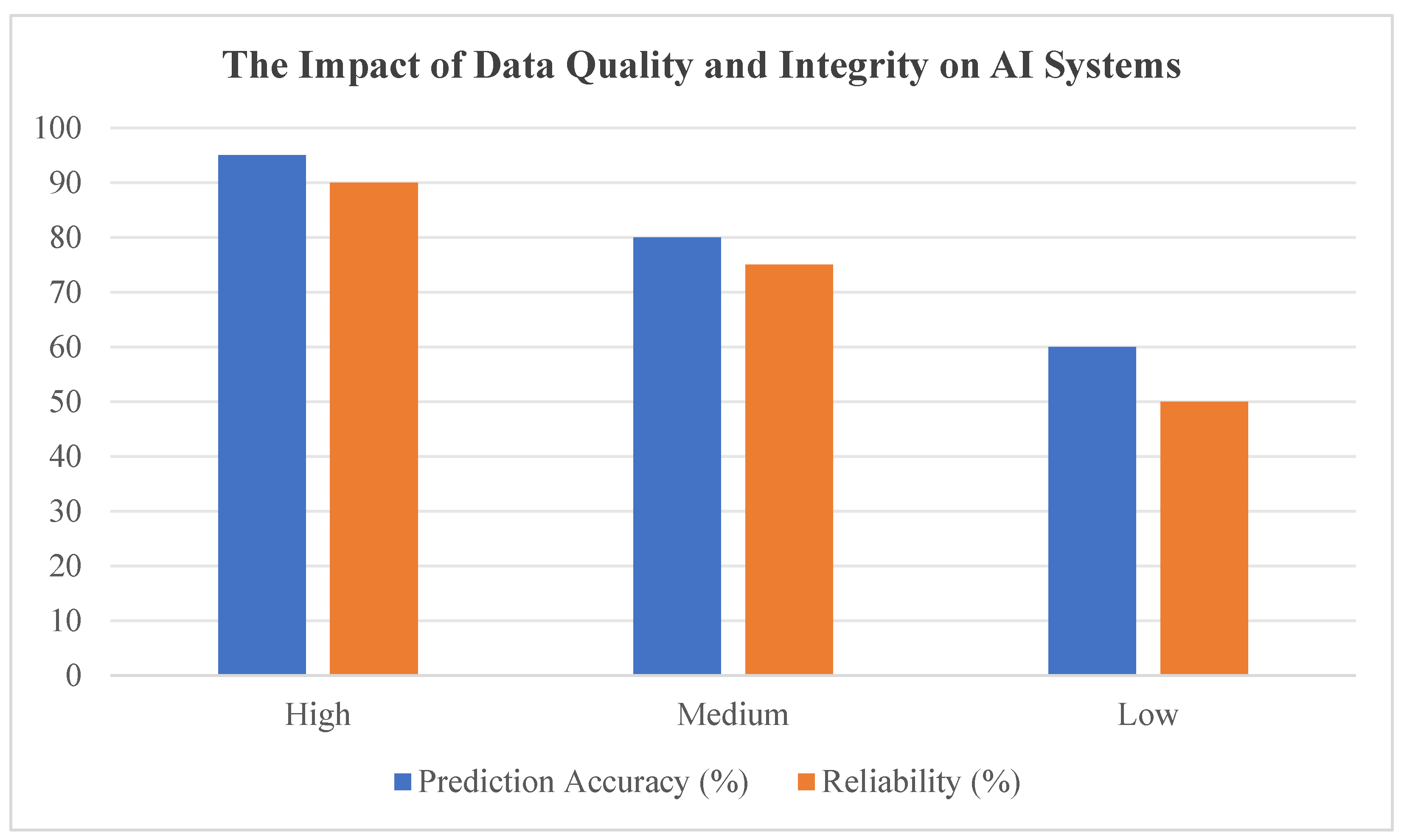

1. Data Quality and Integrity

The effectiveness of AI in internal control systems is highly dependent on the quality and integrity of the data used. Poor data quality can lead to inaccurate predictions and false alarms, undermining the reliability of the system. Organizations must invest in data governance and quality control measures to ensure that the data feeding into AI systems is accurate and reliable [21]. Wan et al. (2021) emphasized the role of regional governance environment in ownership structure and R&D, which similarly highlights the importance of governance in ensuring data quality [22].

Figure 11.

A bar chart showing the prediction accuracy and reliability of AI systems at different levels of data quality.

Figure 11.

A bar chart showing the prediction accuracy and reliability of AI systems at different levels of data quality.

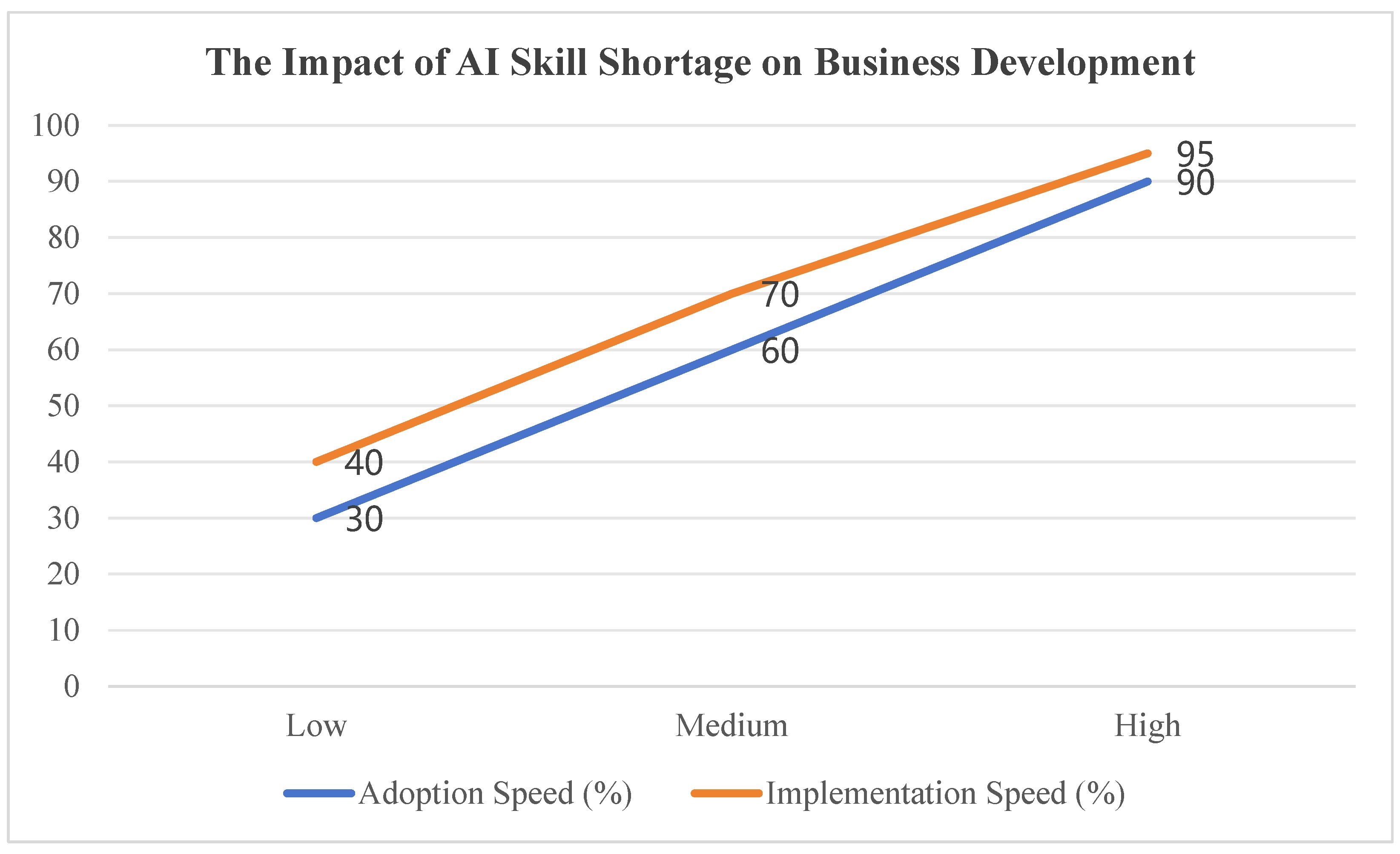

2. Skill Shortage

Implementing and managing AI systems requires specialized skills that are currently in short supply. Organizations may face challenges in finding and retaining talent with the necessary expertise in AI, data science, and internal control. This skill shortage can slow down the adoption and implementation of AI technologies, hindering the potential benefits.

Figure 11.

A line graph showing the adoption and implementation speed of AI technologies at different skill levels.

Figure 11.

A line graph showing the adoption and implementation speed of AI technologies at different skill levels.

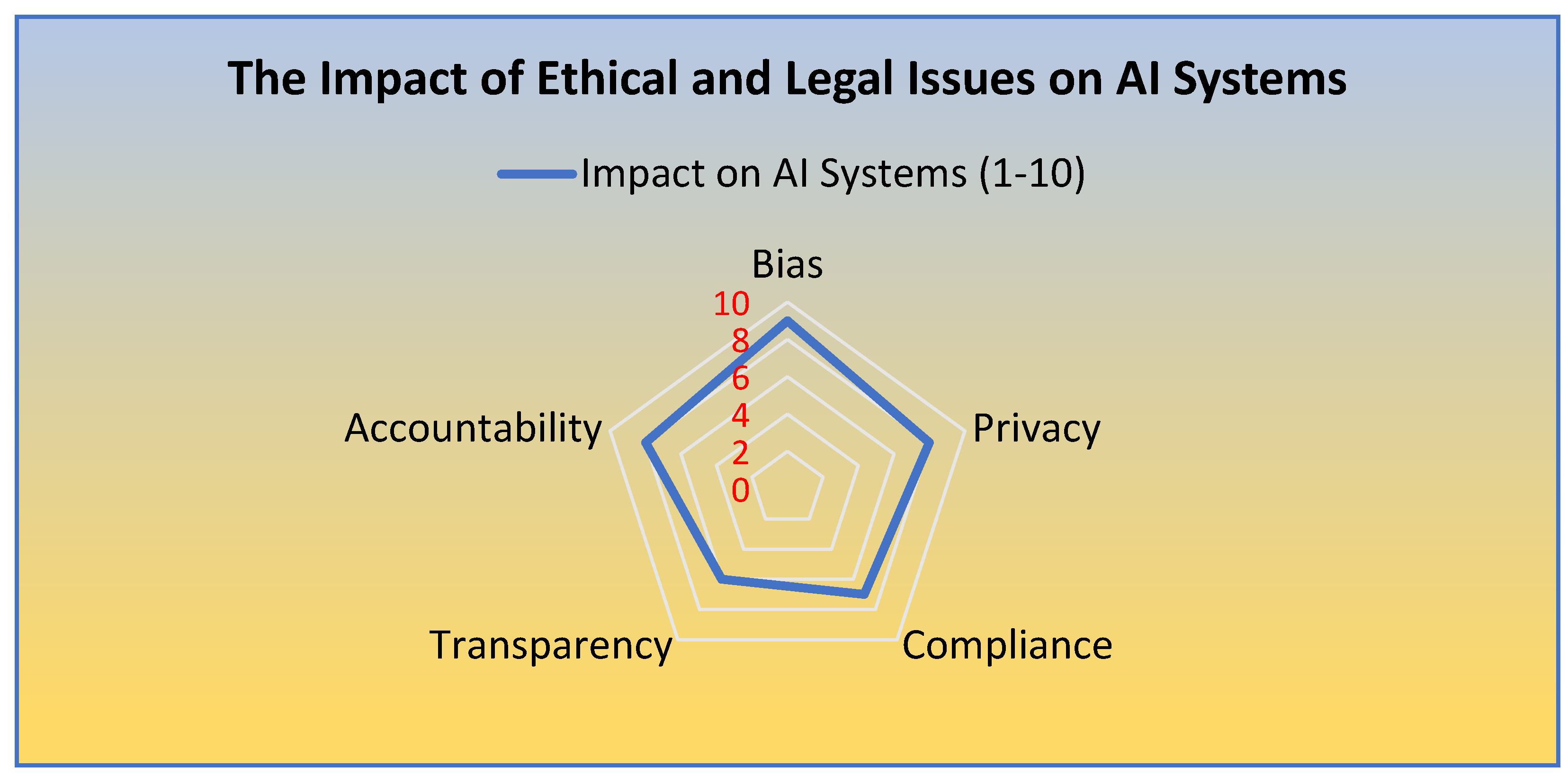

3. Ethical and Legal Issues

The use of AI in internal control raises several ethical and legal concerns. For example, the potential for bias in AI algorithms can lead to unfair treatment of employees or customers. Additionally, the use of AI for surveillance and monitoring may raise privacy concerns. Organizations must navigate these ethical and legal issues carefully, ensuring that their use of AI aligns with ethical standards and legal requirements.

The integration of AI in tax administration is a critical component of internal control, as it streamlines processes from data collection to fraud detection and compliance checks. As China considers tax reforms to align with global economic trends and advance social civilization, the adoption of AI in tax systems can significantly enhance compliance and efficiency. For example, AI can automate the collection and analysis of vast tax-related data, identify patterns and anomalies, detect fraudulent activities, and perform automated compliance checks. This not only improves the efficiency of tax management but also strengthens the tax system's ability to detect and prevent fraud, thereby reinforcing the internal control mechanisms within tax administration [25].

Figure 12.

A radar chart displaying the impact of various ethical and legal issues (e.g., bias, privacy, compliance) on AI systems.

Figure 12.

A radar chart displaying the impact of various ethical and legal issues (e.g., bias, privacy, compliance) on AI systems.

VIII. Future Directions

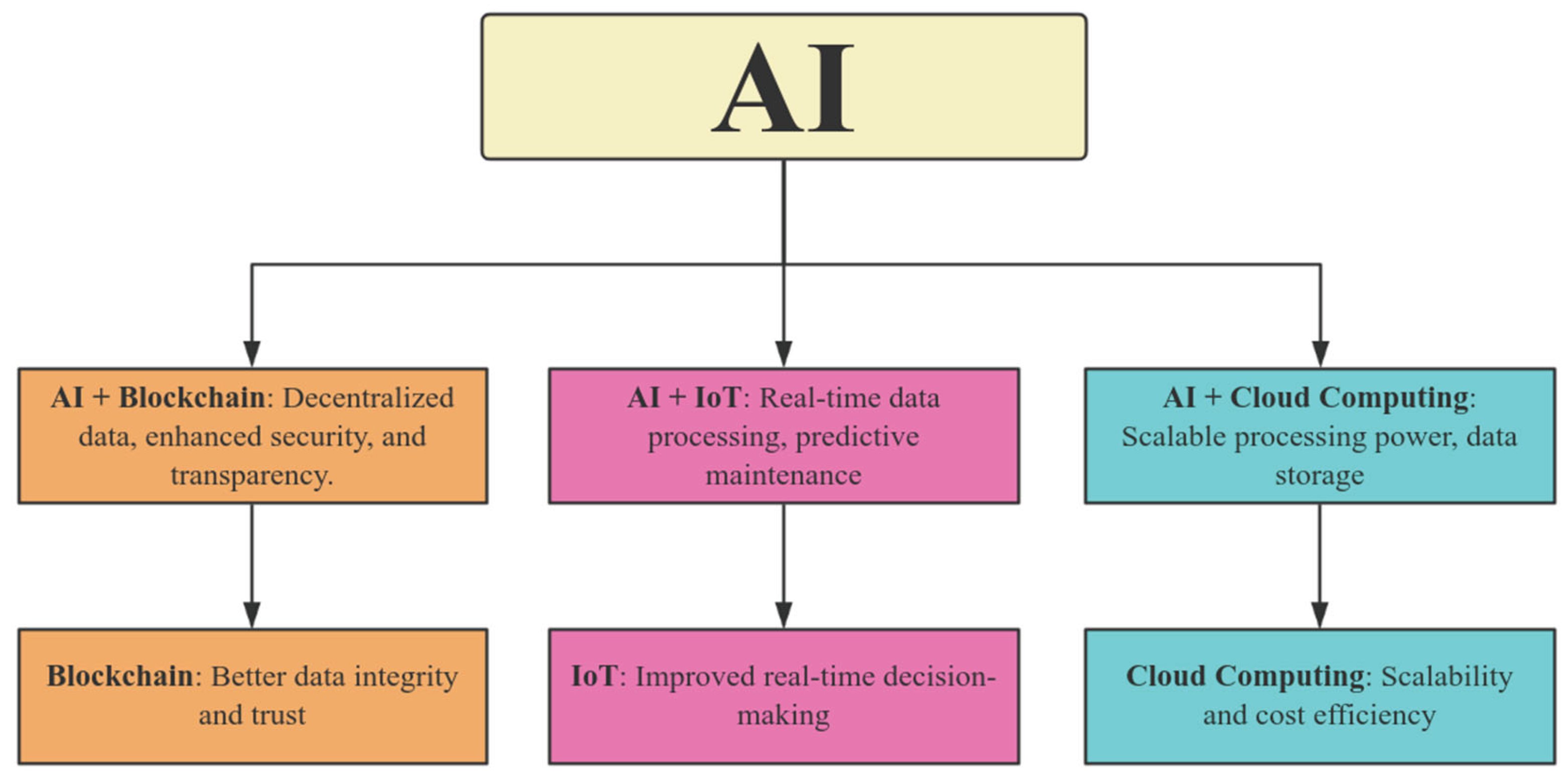

1. Integration with Other Technologies

The future of AI in internal control lies in its integration with other emerging technologies such as blockchain and the Internet of Things (IoT). Blockchain can provide a secure and transparent ledger for transactions, enhancing the integrity of data used by AI systems. IoT devices can provide real-time data on physical assets and processes, enabling more granular and timely control. This integration will create a more robust and comprehensive internal control environment.

Figure 13.

The following flowchart illustrates the integration paths and effects of AI with blockchain, IoT, and other technologies.

Figure 13.

The following flowchart illustrates the integration paths and effects of AI with blockchain, IoT, and other technologies.

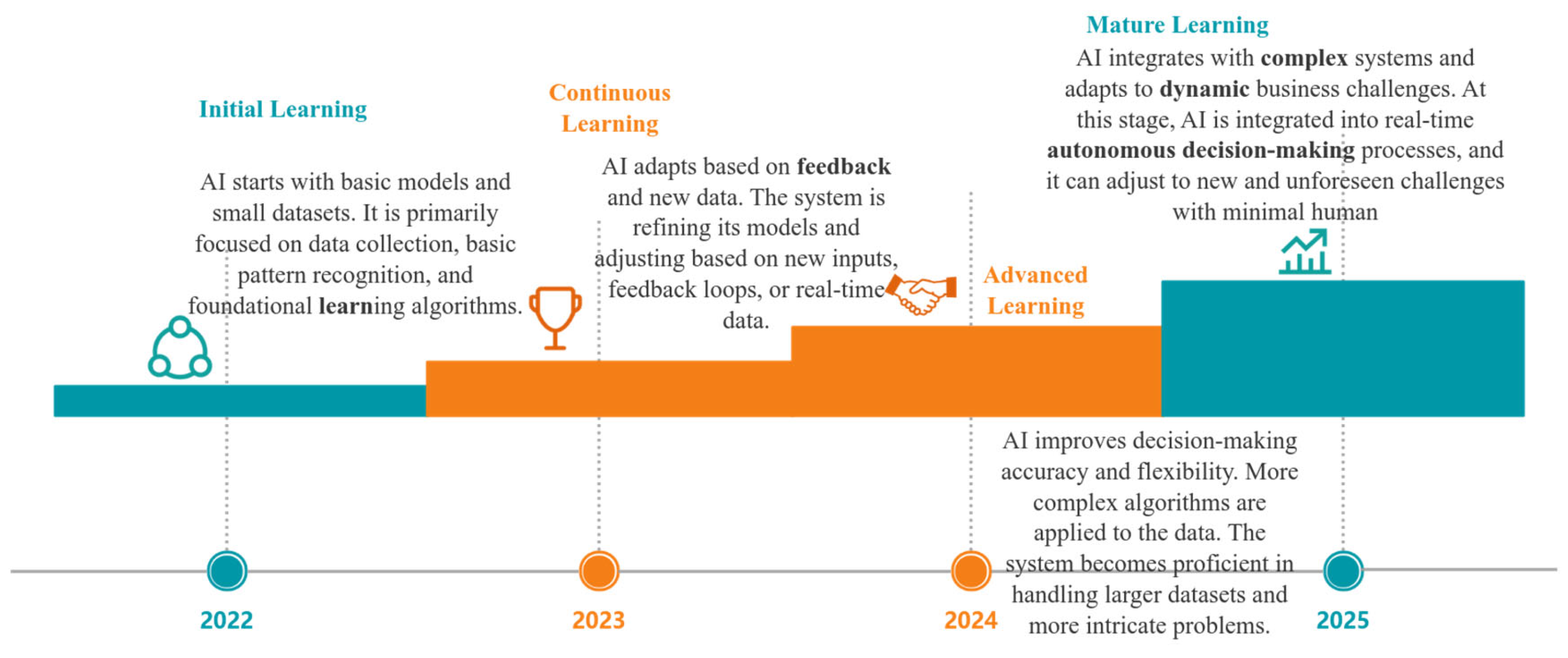

2. Continuous Learning and Adaptation

AI systems must be designed to learn and adapt continuously to changing business environments. This requires the development of self-learning algorithms that can update their models based on new data and feedback. Continuous learning will ensure that AI systems remain effective and relevant, adapting to new risks and challenges as they emerge.

Figure 14.

A timeline showing how AI systems continuously learn and adapt to new business environments and challenges.

Figure 14.

A timeline showing how AI systems continuously learn and adapt to new business environments and challenges.

3. Global Standards and Regulations

As AI becomes more prevalent in internal control, the need for global standards and regulations will increase. These standards will help ensure that AI systems are used responsibly and ethically, protecting the interests of all stakeholders. Organizations should actively participate in the development of these standards and ensure that their AI systems comply with them.

IX. Conclusion

1. Summary

This paper has explored the critical role of internal control in business management and the potential of AI technologies, particularly AGI, ASI, and UBI, in enhancing internal control systems. Through theoretical frameworks and practical case studies, the paper has demonstrated how AI can be integrated into internal control to improve efficiency, execution, and governance effectiveness. The paper has also discussed the challenges and limitations of implementing AI in internal control, emphasizing the need for data quality, skill development, and ethical considerations.

2. Implications

The implications of this research are significant for both businesses and policymakers. Businesses should invest in AI technologies to enhance their internal control systems, ensuring that they remain competitive and compliant in a rapidly changing business environment. Policymakers should develop and enforce standards and regulations to guide the responsible use of AI in internal control, protecting the interests of all stakeholders.

3. Call to Action

This paper calls for further research and practical implementation of AI in internal control systems. Organizations should explore the potential of AI technologies and develop strategies to integrate them into their existing internal control frameworks. By doing so, they can leverage the power of AI to drive operational excellence and sustainable growth.

References

- Chen, B. The Role of Accounting and Financial Management in Humanity's Transition to the Interstellar Era. Economics and Management Innovation 2025, 2, 61–68. [Google Scholar] [CrossRef]

- Shi, S. , Zhang, L., Yin, Y., Yang, X., & Lee, H. A modified RIME algorithm with covariance learning and diversity enhancement for numerical optimization. Cluster Computing 2025, 28, 658. [Google Scholar]

- Yu, Q. , Yin, Y., Zhou, S., Mu, H., & Hu, Z. (2025, March). Detecting Financial Fraud in Listed Companies via a CNN-Transformer Framework. In 2025 8th International Conference on Advanced Algorithms and Control Engineering (ICAACE) (pp. 1047–1051). IEEE.

- Zhongyin Law Firm. Lawyer's Perspective on Corporate Internal Control and Compliance Innovation - Taking the Application of Artificial Intelligence and Other Technologies as the Entry Point. 2024-03-06.

- NetEase, Application and Practice of Artificial Intelligence in Compliance Management - Financial Supervision. Internal Control Compliance Digitalization. 2024-12-24.

- On the Innovation and Development of Complex Adaptive Systems and Enterprise Management Research. Journal of Modern Business Administration. 2022-09-20.

- Modern Green Logistics Management and Its Optimization Path Research. Journal of Modern Business Administration". 2022-09-20.

- OuYang, K. , Wei, D., Sha, X., Yu, J., Zhao, Y., Qiu, M.,... & Chen, H. (2025). Beaver behavior optimizer: A novel metaheuristic algorithm for solar PV parameter identification and engineering problems. Journal of Advanced Research.

- Zhang, Z. , Shen, Q., Hu, Z., Liu, Q., & Shen, H. Credit risk analysis for SMEs using graph neural networks in supply chain. arXiv 2025, arXiv:2507.07854. [Google Scholar]

- On the Innovation and Development of Complex Adaptive Systems and Enterprise Management Research. Journal of Modern Business Administration. 2022.

- Aleksandra Przegalinska & Tamilla Triantoro. Collaborative AI in the workplace: Enhancing organizational performance through resource-based and task-technology fit perspectives. International Journal of Information Management 2025, 81, 102853.

- Liu, S. , & Zhu, M. Distributed inverse constrained reinforcement learning for multi-agent systems. Advances in Neural Information Processing Systems 2022, 35, 33444–33456. [Google Scholar]

- The Relationship between AI Adoption Intensity and Internal Control System and Accounting Information Quality. 2023-11-04. MDPI.

- INTERNAL CONTROL AND THE TRANSFORMATION OF ENTITIES KEY ACTIONS SUMMARY. 2022-04-01. ACCA Global.

- Internal Control System in Enterprise Management: Analysis and Interaction Matrices. European Research Studies Journal. 2018.

- Liu, S. , & Zhu, M. (2024, May). Meta inverse constrained reinforcement learning: Convergence guarantee and generalization analysis. International Conference on Learning Representations.

- Zhang, F. , Chen, G., Wang, H., & Zhang, C. CF-DAN: Facial-expression recognition based on cross-fusion dual-attention network. Computational Visual Media 2024, 10, 593–608. [Google Scholar]

- Artificial intelligence and the future of the internal audit function. Nature. 2024-03-11.

- Li, P. , Abouelenien, M., Mihalcea, R., Ding, Z., Yang, Q., & Zhou, Y. (2024, May). Deception detection from linguistic and physiological data streams using bimodal convolutional neural networks. In 2024 5th International Conference on Information Science, Parallel and Distributed Systems (ISPDS) (pp. 263–267). IEEE.

- Zhao, Peng, Xiaoyu Liu, Xuqi Su, Di Wu, Zi Li, Kai Kang, Keqin Li, and Armando Zhu. "Probabilistic Contingent Planning Based on Hierarchical Task Network for High-Quality Plans." Algorithms 18, no. 4 (2025): 214.

- Evaluating the impact of internal control systems on organizational effectiveness. LBS Journal of Management & Research. 2024-12-29.

- Wan, W. , Zhou, F., Liu, L., Fang, L., & Chen, X. Ownership structure and R&D: The role of regional governance environment. International Review of Economics & Finance 2021, 72, 45–58. [Google Scholar]

- Chen, B. The Pivotal Role of Accounting in Civilizational Progress and the Age of Advanced AI: A Unified Perspective. Economics and Management Innovation 2025, 2, 49–54. [Google Scholar] [CrossRef]

- Chen, B. Leveraging Advanced AI in Activity-Based Costing (ABC) for Enhanced Cost Management. Journal of Computer, Signal, and System Research 2025, 2, 53–62. [Google Scholar] [CrossRef]

- Chen, B. (2024). The Imperative Need for Tax Reform in China and Its Impact on Advancing Social Civilization. Available at SSRN 5129165.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.