Submitted:

25 September 2025

Posted:

26 September 2025

You are already at the latest version

Abstract

Sustainable development, with its three pillars (environmental, social, and governance, ESG), is a must for humans. Climate change is occurring faster than expected. In 2015, 193 countries signed the United Nations Agenda 2030, and it must be realized in time, together with the 17 Sustainable Development Goals. In the PDCA (Plan, Do, Check, Act) cycle, the Check phase is very important – sustainability reporting (SR) is necessary. This article presents an overview of the existing SR standards (SRS) and their future development. Information review methodology shows that SRS are already well developed in large companies. The different standards are described, e.g. voluntary ISO (International Organization for Standardizations) standards, and Global Reporting Initiative (GRI) ones, mandatory European Sustainability Reporting Standards (ESRS), or the International Financial Reporting Standards (IFRS). National SRS are often aligned with the IFRS Sustainability Disclosure Standards. Besides the corporate SRS, public ones, covering governmental and non-governmental institutions, universities and associations are described. Public SRS should be adapted to the needs of public institutions. Finally, the SRS for individuals and communities are discussed to cover these important parts of humanity. The social and governance sustainability reports could be extended with the annual personal or community Carbon or Ecological Footprint reports.

Keywords:

sustainability reporting

; ESG reporting

; corporate sustainability

; public sustainability

; personal sustainability

; mandatory reporting

; voluntary reporting

; international standards

; national standards

1. Introduction

Human historical development is composed of the number of people living (population growth), their life expectancy (mortality), biodiversity and infectious diseases, unsustainable resource consumption (energy, materials, water, air), etc. The world population is not increasing at an exponential rate anymore (except in Africa and some countries in Asia) but it is still growing. World population growth rate peaked in 1962 and 1963 with an annual growth rate of 2.2%; however, since then, world population growth has halved [1]. Global life expectancy is increasing rapidly, too; it was less than 30 a (years) before 1800, and it has grown to 73 a in 2023 [1]. Also, global child mortality, which was around 50% before 1800, fell to 27% until 1950 and to 4,3% in 2022 (Norway, Japan, Estonia and Slovenia have the lowest mortality rates – 0.3%) [2].

1.1. Exponential Growth of Human Needs

The growth was positive for the human species, but not for other living creatures – loss of biodiversity is occurring. The world’s largest threats to biodiversity are agriculture and aquaculture (17.1% share), followed by biological resource use (15.2%), human intrusion and disturbance (11.8%), natural system modifications (11.1%), residential and commercial development (8.8%), invasive and other problematic species, genes and diseases (8.3%), pollution (7.8%), etc.

Global extraction of four main material groups – biomass, fossil fuels, metal ores and non-metallic minerals – reached 31.1 Gt/a (billion tons per year) in 1970 [3], or 8.42 t/a per person. By 2024, world extraction from the Earth increased to 107 Gt/a, or 13.11 t/a per person (55.7% more). The number of cars reached 1.5 G (billion) globally in 2025 (5.5 inhabitants per car) and is expected to grow to 2.0 G by 2040 (4.6 inhabitants per car) [4]. In the same period, the number of trucks will increase from 507 M (million) to 790 M, and the air travel distance in passenger distance (km) will increase from 12 T (trillion) to 20 T.

Because of the increased extraction of materials and production of goods, the global primary energy and food production (and consumption) increased from 5.6 PW h/a in 1800 (using traditional biomass, and only 1.7% of coal), to 12.1 PW h in 1900 (47.7% from coal), and 181.9 PW h in 2024 (24.9% from coal, 30.2% from oil, 22.1% from natural gas, 5.7% from hydropower, 6.1% from traditional biomass, 7.4% from other renewables, and 3.8% from nuclear) [5].

The most worrying results of the increased extraction of materials, production and consumption of energy and goods are the greenhouse gas (GHG) emissions. GHGs include carbon dioxide, methane and nitrous oxide from all sources, including land-use change; they are measured as a mass flow rate (qm, t/a, tons per year) in ‘carbon dioxide-equivalents’ (CO2e). Globally, we emit more than 50 Gt/a of GHGs. In 1850, 4.2 Gt/a were emitted, increasing to 8,7 Gt/a in 1900, 16.7 Gt/a in 1950, 40.7 Gt/a in 2000, and 53.8 Gt/a in 2023 [6], or 6,65 t/a per capita (2.05 t/a by electricity and heat production, 0.98 t/a transport, 0.74 t/a agriculture, 0.41 t/a industry, 0.41 t/a fugitive emissions, 0.38 t/a buildings, 0.21 t/a waste, etc.) [7].

1.2. Human Agreements

To slow down the dangerous development of climate change, 154 member states of the United Nations (UN) signed the United Nations Framework Convention on Climate Change (UNFCCC) in 1992 at the Earth Summit in Rio de Janeiro [8]. In 1997, 192 parties signed the Kyoto Protocol, which entered into force in 2005, committing themselves to reducing GHG emissions until 2020. The Paris Agreement was agreed by 196 parties at the 2015 UNFCCC conference and signed in 2016.

To realize the Paris agreement and keep the global temperature rise below 2.0 °C (the 1.5 °C goal is already missed), the additional GHG emissions could sum to 1050 Gt, i.e., 18 a (years) of current emissions at a 50% chance to succeed, or 12 a at an 85% chance (updated from [9]). The higher the limit achieved, the more damage can be expected. Categories of climate impacts include: 1) agriculture (changes in land and aquaculture productivity, livestock mortality and morbidity from heat and cold exposure), 2) coastal zones (loss of land and capital from sea level rise, and non-market impacts), 3) extreme events (mortality, land and capital damages from hurricanes, floods, heat waves, etc.), 4) health (mortality and morbidity from heat and cold exposure, infectious and other diseases), 5) energy demand (changes for cooling and heating), 6) tourism demand (changes in tourism flows and services), 7) water stress (changes in energy supply, availability of drinking water), 8) human security (civil conflicts and wars, human migration), and 9) tipping points (large scale disruptive events) [10]. The global annual average loss of GDP (Gross Domestic Product) in 2060 is estimated to be 2.0% globally (3.3% for the Middle East and Northern Africa, 3.7% for South and Southeast Asia, and 3.8% for Sub-Saharan Africa, respectively).

Environmental concerns are not the only dimension of sustainability that is problematic. The social dimension has been developed by the UN; first, the eight Millennium Development Goals (MDGs) for the year 2015, followed by the 17 Sustainable Development Goals, SDGs [11]. This 2030 Agenda is a plan of action for people, planet and prosperity. It also seeks to strengthen universal peace and partnership. The Paris Agreement followed in the same year [12]. In 2019, the EU (European Union) accepted the European Green Deal to transform the EU into a modern, resource-efficient, and competitive economy, ensuring: a) no net emissions of greenhouse gases by 2050, b) economic growth decoupled from resource use, and c) no person and no place left behind [13].

In 2013, fewer than 10% of the largest EU companies disclosed their non-financial information regularly. Therefore, the EU accepted a Non-Financial Reporting Directive (NFRD) for large companies with more than 500 employees [14]. Companies concerned were required to disclose in their management report and material information on: a) policies, b) outcomes and risks, including due diligence that they implemented, c) relevant non-financial key performance indicators concerning environmental aspects, d) social and employee-related matters, e) respect for human rights, f) anti-corruption and bribery issues, and g) diversity on the boards of directors.

In 2022, the NFRD was updated with the Corporate Sustainability Reporting Directive (CSRD) to modernize and strengthen the rules on social and environmental information that companies must report [15]. A broader set of companies was planned to report on sustainability in the EU, about 50 000 companies as compared with the 11 700 in the NFRD. Large companies (regardless of their capital market orientation) that met at least two of the following three requirements: 250 or more employees; 50 MEUR (million EUR) in net turnover; and/or 25 MEUR in assets were planned to report.

Current policies are not following the Paris agreement – they are leading towards around 2.5 °C of warming. Lack of government regulations does not support faster and more profound adaptation and mitigation. Besides, in January 2025, the United States of America (US) withdrew from the Paris Agreement under the UNFCCC. Fortunately, there are many states within the US that will continue to respect and fulfil the Paris Agreement.

The EU also reduced the requirements for the CSRD by lowering the number of participating companies below that of the NFRD, to corporations with more than 1000 employees. The EU reduced the content of the reports and the time limits to start reporting (Omnibus package) [16]. In July 2025, the Commission adopted targeted “quick fix” amendments to the first set of European Sustainability Reporting Standards (ESRS) [17]. This will reduce the burden and number of companies that had to start reporting for the financial year 2024 (commonly referred to as “wave one” companies) by 80%. The “quick fix” amendment, which applies from the financial year 2025, will allow them to omit that same information for financial years 2025 and 2026. For large companies with 250 or more employees and listed small and medium-sized enterprises (SMEs, waves 2 and 3), the start will be postponed by two years [18]. For companies no longer in the scope of the CSRD, the Commission plans to adopt a voluntary reporting standard for SMEs (VSME), developed by the European Financial Reporting Advisory Group (EFRAG).

The slowdown of CSR in the EU and the US withdrawal are endangering the UN Paris Agreement by 2050 and the realization of the SDGs by 2030. Voluntary reporting using available sustainability reporting standards (SRS), voluntary or mandatory, will become more important. It is encouraging that the voluntary ISO (International Organization for Standardization) and GRI (Global Reporting Initiative) standards are already widespread in the world.

2. Methods

Environmental, social, and governance (ESG) reporting discloses information covering an organization’s operations and risks in three areas: environmental stewardship, social responsibility, and corporate governance. As sustainability and ethical governance become increasingly critical for businesses, ESG reporting helps organizations showcase their commitment to addressing societal challenges, reducing environmental impact, and ensuring strong governance practices [19]. By consistently communicating ESG performance, companies can enhance their reputation.

Key performance indicators help businesses measure progress in the three ESG areas: 1) Environmental metrics (carbon emissions, water usage, waste management); 2) Social metrics (labor practices, diversity, equity, and inclusion, DEI, human rights); 3) Governance metrics (board diversity, executive compensation, shareholder rights, anti-corruption efforts). Best practices for successful ESG reporting require: 1) identify and manage key ESG risks; 2) improve data collection; 3) align ESG reporting with business strategy; 4) engage stakeholders; 5) include ESG initiatives and sustainability efforts; 6) report climate change efforts and environmental impact; 7) report on social responsibility and community impact; 8) incorporate governance practices.

Sustainability and ESG are widely used yet distinct concepts, but the differences are not always well understood. While both ESG and sustainability are concerned with the environmental and social impact of business, they have different goals and priorities [20]. ESG is a framework used to evaluate the performance of companies across specific areas such as carbon emissions, diversity and inclusion, and executive pay; it is used to identify and manage specific risks and opportunities associated with a company or investment. Conversely, sustainability provides a broader, holistic approach for long-term value creation that encompasses a range of responsible and ethical business practices across areas such as supply chain management, stakeholder engagement, and community development.

Current sustainability reporting is a set of four methods: CSRD, Corporate Sustainability Due Diligence Directive (CSDDD), EU Taxonomy Regulation, and Carbon Border Adjustment Mechanism (CBAM) [21]. In more detail:

- 1)

- The CSRD described above includes the development of ESRS; companies within the CSRD will have to report on double materiality — financial and impact materiality.

- 2)

- The aim of CSDDD is to foster sustainable and responsible corporate behavior in companies’ operations and across their global value chains; it limits the information large companies can request from SMEs and small mid-cap business partners to that laid out in the CSRD’s VSME.

- 3)

- The EU taxonomy helps direct investments to the economic activities most needed for the transition, in line with the European Green Deal objectives. The taxonomy is a classification system that defines criteria for economic activities that are aligned with a net-zero trajectory by 2050 and the broader environmental goals, other than climate.

- 4)

- CBAM is the EU’s tool to put a fair price on carbon emitted during the production of carbon-intensive goods that are entering the EU, and to encourage cleaner industrial production in non-EU countries.

3. Results

3.1. GRI Standards

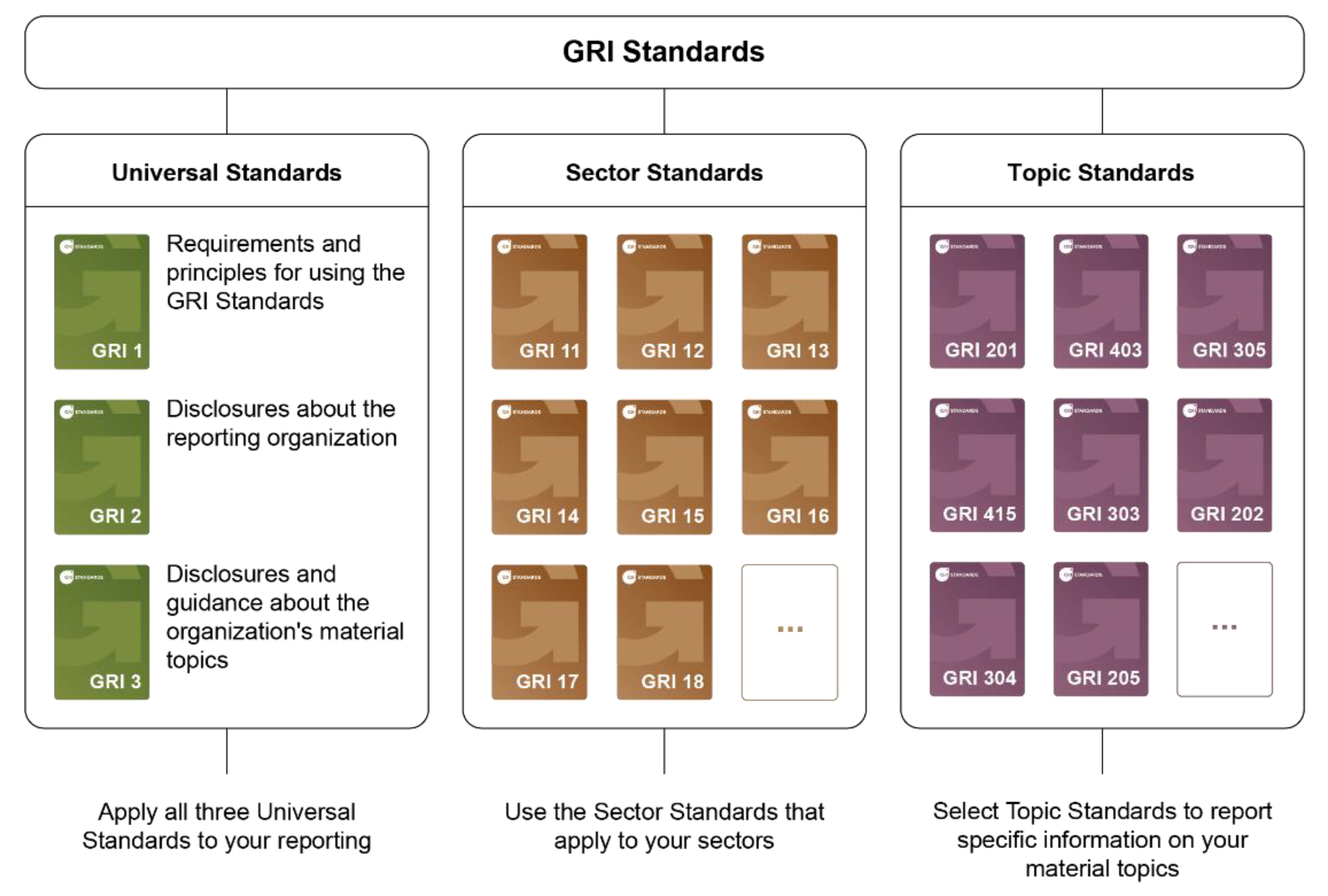

GRI (Global Reporting Initiative) standards are the world’s most widely used standards for sustainability reporting [22]. Original standards are in English, with authorized translations in ten other languages. They are regularly updated. The Global Sustainability Standards Board (GSSB) sets out a new work program every three years. The GSSB work program includes projects to review existing GRI Standards as well as to develop new ones. Standards can be used by small or large organizations to cover the interests of investors, policymakers, capital markets, and civil society. The standards are organized in three groups: 1) Universal Standards, 2) Sector Standards, and 3) Topic Standards (Figure 1) [23].

The three universal standards cover essential information about an organization or company; they report on human rights and environmental due diligence:

- GRI 1, Foundation 2021, explains the purpose of the GRI Standards, their critical concepts, and usage. It presents the requirements that an organization must fulfil to report according to the GRI Standards. It must respect the elementary principles of good-quality reporting, e.g., accuracy, balance, and verifiability.

- GRI 2, General Disclosures 2021, includes disclosures of the organization: structure and reporting practices, activities and workers, governance, strategy, policies, practices, and stakeholder engagement. The profile of the organization and its scale are presented, providing a context for understanding.

- GRI 3, Material Topics 2021, gives the steps that help the organization to determine the most relevant topics, their impacts, materials, and how the Sector Standards are used in this process. It also discloses the list of material topics, the process of determining them, and how it manages each topic.

The 40 sector standards report on sector-specific impacts on the economy, environment and society. The sectors belong to four groups [24]:

- Basic materials and needs (oil and gas, coal, agriculture and aquaculture with fishing, mining, food and beverages, textiles and apparel, banking, insurance, capital markets, utilities, renewable energy, forestry, metal processing).

- Industry (construction materials, aerospace and defense, automotive, construction, chemicals, machinery and equipment, pharmaceuticals, electronics).

- Transport, infrastructure and tourism (media and communication, software, real estate, transportation infrastructure, shipping, trucking, airlines, trading with distribution and logistics, packaging, hotels).

- Other services and light manufacturing (educational services, household durables, managed healthcare, medical equipment and services, retail, security services, restaurants, commercial services, non-profit organizations).

The 31 topic standards deal with 19 categories, covering: a) all themes (1 category), b) business integrity and prosperity (7 categories), c) environment (6 categories), and d) people (5 categories). They contain 19 topics (with exemplary sub-topics) [25]:

- 1)

- Supply chain sustainability and responsible sourcing: supplier engagement, selection, screening and auditing, sustainable materials, supply chain impacts, supply chain management.

- 1.

- Governance and leadership: corporate management, sustainability program leadership, board structure and independence, risk management and business continuity, executive compensation, accountability.

- 2.

- Customer satisfaction and engagement: customer satisfaction, engagement and provision of information to customers and consumers.

- 3.

- Economic performance: direct economic value generated and distributed; other disclosures related to economic performance.

- 4.

- Ethical business conduct: prevention of anti-competitive practices, anti-corruption/anti-bribery practices, human rights, data security and privacy, responsible marketing and product labelling, transparency, regulatory compliance, animal welfare, and clinical trials.

- 5.

- Innovation and R&D: research in unmet needs, developing new technologies, innovative solutions, and intellectual property.

- 6.

- Market presence and pricing: growth strategy in emerging/developed markets, pricing and affordability of products and solutions.

- 7.

- Product safety and quality: product responsibility, product safety design, quality management, customer health and safety.

- 1)

- Air quality and other emissions: ozone-depleting substances, NOX and SOX, other (non-GHG) emissions.

- 2)

- Chemicals and hazardous materials: management of toxic substances, hazardous materials, chemicals, and restricted substances.

- 3)

- Climate change and energy-related GHG emissions: climate change strategy, carbon footprint reductions (Scopes 1, 2 and 3), energy consumption and efficiency, renewable energy.

- 4)

- Sustainable products and solutions: Life Cycle Assessment, sustainable design, product take-back, resource efficiency, product energy efficiency.

- 5)

- Waste management: waste generation and recycling, electronic and hazardous waste, and packaging waste.

- 6)

- Water and effluents: water consumption, effluents and wastewater management, water scarcity.

- 1.

- Community and donations: volunteerism, philanthropy, local development, engagement and dialogue with local communities, non-governmental organizations, local governments, academia, etc.

- 2.

- Diversity and inclusion: employee diversity and inclusion, equal opportunity, non-discrimination, gender equality.

- 3.

- Labor practices: employment practices, labor management relations, freedom of association and collective bargaining, forced or compulsory labor, child labor.

- 4.

- Occupational health and safety (OHS): hazard minimization precautions, employee health, safety and well-being, emergency response plans, occupational accidents, biosafety and laboratory biosecurity, OHS management system.

- 5.

- Talent attraction, development and retention: training and development, recruitment, career management and promotion, compensation and benefits.

Each topic and its sub-topics are considered by several GRI standards, e.g., the first one on Supply Chain Sustainability and responsible sourcing deals with GRI 102 – General Disclosures, GRI 103 – Management Approach, GRI 204 – Procurement Practices, GRI 307 – Environmental Compliance, GRI 308 – Supplier Environmental Assessment, and GRI 414 – Supplier Social Assessment. GRIs 201–207 deal with economic topics, GRIs 301–307 with environmental ones, and GRIs 401–419 with social topics. More information can be found in [26].

3.2. ESRS Standards

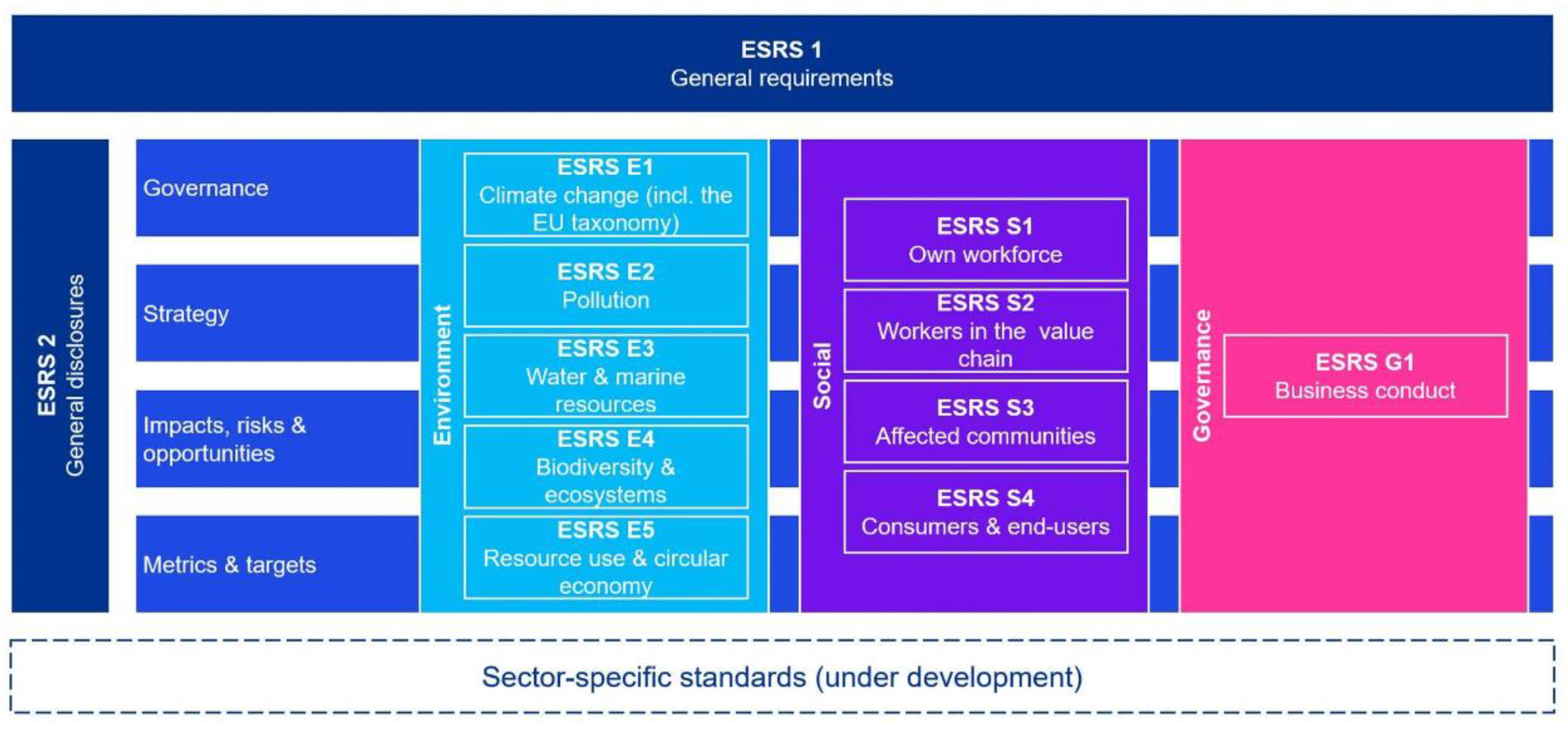

The ESRS are a substantial part of the CSRD – they define how companies in the EU must report on their sustainability performance [27,28]. The ESRS are intended to enable uniform, transparent and comparable sustainability reporting. They are divided into different categories to ensure comprehensive and transparent reporting. They consist of: 1) general requirements, 2) topic-specific standards for: a) environment (E), b) society (S) and c) governance (G), and 3) sector- and company-specific regulations (Figure 2).

Each ESRS shall cover the four central reporting areas: strategy, policies, actions and targets. Strategy includes relevance, risks and opportunities, double materiality, effect on long-term value creation, and inclusion of stakeholder expectations. Policies must adopt internal guidelines and codes of conduct to respect official sustainability guidelines, to adopt governance structures, to comply with regulatory requirements, and to commit to the selected international standards. Actions embrace operational measures to reduce environmental impact, programs for social sustainability (e.g., diversity, working conditions), management of supply chain and ESG risk, investments in sustainable technologies or processes. Targets demonstrate specific goals and key performance indicators (KPIs) of the company with clearly defined ESG targets, indicators and KPIs, methodology for reviewing progress (e.g., frequency of reporting), and a link to remuneration models or internal incentives.

The overarching standards ESRS 1 and ESRS 2 set out the basic principles and general disclosure requirements: ESRS 1 – General requirements (structure, concepts, preparation and presentation of information, reporting principles, double materiality, coherence with other standards), and ESRS 2 – General information (requirements for information on governance, strategy and governance, impacts, risks and opportunities (IROs), key figures and targets, reporting obligations, structure of the report). The thematic European Sustainability Reporting Standards cover the three sustainability dimensions: Environment (E), Social (S) and Governance (G):

Environmental ESRS are: E1 – Climate change (impact on climate change, Paris agreement, adaptation strategies, GHG emissions Scope 1–3, energy consumption and energy mix), E2 – Pollution (actual and potential impacts on air, water and soil pollution, substances of concern, strategies and finance to prevent and mitigate them), E3 – Water and marine resources (use and impacts on water and marine resources, their protection, mitigation of negative impacts, risks and opportunities), E4 – Biodiversity and Ecosystems (impacts on biodiversity and ecosystems, material risks and opportunities, measures to mitigate them, financial implications), and E5 – Circular economy (resource efficiency, waste minimization, use of renewable resources, prevention to deplete non-renewable resources, decoupling economic growth from the use of resources, their reuse and recycling).

Social ESRS are: S1 – Own workforce (positive and negative influences, financial risks and opportunities, working conditions, equal treatment and opportunities for all, child and forced labor, addressing these factors), S2 – Workforce in the value chain (impact on workers, labor-related rights, transparency, equal treatment and opportunities, approach to assessing and addressing impacts on working conditions), S3 – Affected communities (IROs on economic, social and cultural, civil and political rights of communities, people, and indigenous peoples in its value chain), and S4 – Consumers and end users (privacy, freedom of expression), (ii) personal safety (e.g., health and safety, personal security and child protection, non-discrimination, access to products and services and responsible marketing practices).

Governance ESRS is: G1: Business conduct (corporate ethics and culture, anti-corruption, protection of whistleblowers, supplier relationships, political influence and obligations, including lobbying).

EFRAG has published two other standards:

- ESRS LSME (ESRS for Listed Small- and Medium-sized Enterprises): The standard offers simplified and proportionally adjusted reporting for small and medium-sized listed companies, while the comprehensive ESRS standard requires detailed and in-depth disclosure of all relevant sustainability aspects in accordance with the CSRD.

- ESRS VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs): The Standard offers a voluntary and greatly reduced reporting scheme that is geared to the limited resources of very small companies. A helpful Word report template for the VSME standard is available, and it additionally compiles all report requirements in a clear VSME data point list.

ESRS requires companies to implement (double) materiality assessment, do inventory and gap analysis, optimize data management and internal processes, integrate information into the annual report, and prepare an external audit. To enable external auditing, the ESRS data must be published in machine-readable format (Extensible HyperText Markup Language, XHTML, or European Single Electronic Format, ESEF), suitable for digital evaluations.

Compared to voluntary reporting standards, the ESRS are mandatory for all companies subject to CSRD. They require the usage of double materiality between the company, society and environment. The reporting framework is legally binding within the EU; therefore, it avoids multiple reporting. ESRS are coordinated with the International Financial Reporting Standards (IFRS) Foundation and the International Sustainability Standards Board (ISSB), GRI standards, and the Task Force on Climate-related Financial Disclosures (TCFD).

3.3. ISO Standards

ISO was a front runner for ESG reporting, which has a direct impact on revenue and costs, market share, and a company’s reputation. The 2022 report from the Governance & Accountability Institute found that 96% of companies on the S&P 500 index had published an ESG report [30]. ISO standards support ESG goals by increasing credibility, measuring impact and its reduction, improving cost efficiency and stakeholder confidence (expectations of investors, customers, and employees) [31].

The most important ISO voluntary standards that support ESG in connection with environmental impact are: ISO 14001 – Environmental management systems, ISO 14064 – Greenhouse gas emissions quantification and reporting, ISO 14046 – Water footprint, ISO 46001 – Water efficiency management systems, ISO 50001 – Energy management, ISO 14008 and 14007 – Monetary valuation of environmental impacts and determining environmental costs and benefits [31]. The most used standards of the social component are ISO 26000 – Social responsibility with the seven core principles (Accountability, Transparency, Ethical behavior, Respect for stakeholder interests, Respect for the rule of law, Respect for international norms of behavior, Respect for human rights), ISO 45001 – Occupational health and safety, and ISO 20400 – Sustainable procurement. Regarding the governance items, ISO 37301 – Compliance management systems, ISO 27001 – Information security management, and ISO 37001 – Anti-bribery management systems are the most popular.

Some experts also include among the 10 most important ISO standards the new ISO 53001 (Management systems for UN SDGs) and ISO 30415 (Human resource management — Diversity and inclusion) [32].

3.4. Other International Sustainability Reporting Standards

Voluntary GRI standards for sustainability reporting have been the most used ones in 2024 [33]. An investigation of 5 800 companies (the largest 100 companies in 58 countries) showed that 71% of them used GRI standards (3% more than in 2022), while among the 250 largest multinationals (the G250), GRI was adopted at 77% of them. About 14 000 organizations around the world were GRI reporters [34].

The Omnibus package of the EU’s CSRD reduced the number of potential users of mandatory ESRS from the forecasted 50 0000 to about 10 000. EFRAG is planning to simplify the ESRS by reducing the reporting burden for companies [35]. The simplifications will streamline the double materiality assessment, reduce overlaps across standards, clarify language and structure, and remove all voluntary disclosures.

CDP (formerly the Carbon Disclosure Project) manages a global environmental disclosure system used by more than 23 000 companies. Companies disclose by completing any or all three CDP questionnaires on climate change, forests, and water security. CDP also includes an optional (4th) supply chain reporting module. CDP publishes the scores of reporting companies on its website [36].

The TCFD guides companies on disclosing climate-related financial risks to investors, lenders, insurers, and other stakeholders. TCFD is primarily a theme or pillar-based recommendations framework, one that is increasingly being used throughout the finance and banking sectors. It is used by more than 2 600 organizations, mainly in the US, UK and Singapore.

The IFRS Sustainability Disclosure Standards were created in 2022 by the International Sustainability Standards Board (ISSB) to serve as a global format for sustainability and climate reporting that meets the needs of Chief Financial Officers (CFOs) and investors. The first IFRS S1 and S2 standards were released in June 2023. Companies are advised to start following ISSB standards and making relevant disclosures in 2025. The ISSB has taken over the Sustainability Accounting Standards Board (SASB) and is in the process of integrating it into the preparation of new ISSB (IFRS) sustainability reporting standards.

3.5. National Sustainability Reporting Standards

Many countries have issued their national standards for sustainability reporting. Most of them are aligned with the IFRS Sustainability Disclosure Standards.

The Canadian Sustainability Disclosure Standards are a set of national ESG reporting standards aligned with the global IFRS S1 and S2 frameworks but tailored for the Canadian context by the Canadian Sustainability Standards Board (CSSB) [37]. PwC Indonesia has developed a guide for the National Sustainability Reporting Framework (NSRF), aligning sustainability reporting with IFRS Sustainability Disclosure Standards as issued by the ISSB [38].

In March 2024, the United States Securities Exchange Commission (SEC) laid out the final rules requiring issuers (domestic public companies or foreign private issuers) to disclose their climate-related risks and impact [39]. Companies must report climate-related disclosures, including sustainability governance, targets and goals, strategy and risk management, and materiality.

The Australian Accounting Standards Board (AASB) met to approve the final Australian Sustainability Reporting Standards (ASRSs) on 20 September 2024 [40]. The final version of the ASRSs is broadly aligned with the IFRS Sustainability Disclosure Standards.

In December 2024, China took a significant step forward in corporate sustainability reporting by publishing the first draft of its Corporate Sustainability Reporting Standards (CSRS); the Basic Standards were developed using the ISSB Standards – specifically IFRS S1 – as a base [41].

In March 2025, the Sustainability Standards Board of Japan (SSBJ) announced the release of its finalized sustainability disclosure standards, based on the standards developed by the IFRS Foundation’s ISSB, and anticipated to form the basis of mandatory reporting for listed Japanese companies on sustainability and climate-related information [42].

The UK government is now consulting on the exposure drafts of the UK versions of IFRS S1 and IFRS S2 – respectively called UK SRS S1 and UK SRS S2 [43].

3.5. Reporting Sustainability in the Public Sector

The International Public Sector Accounting Standards Board (IPSASB) is developing and publishing sustainability reporting standards for public sector entities: a) national, regional, state and local governments; b) government ministries, departments, programs, boards, commissions, agencies; c) public sector social security funds, trusts and statutory authorities; d) International governmental organizations [44]. The World Bank’s 2022 report, ‘Sovereign Climate and Nature Reporting,’ raised the critical issue of advancing sustainability reporting in the public sector. The IPSASB Board prioritized General Requirements for Disclosure of Sustainability-related Financial Information, Climate-related Disclosures, and Natural Resources – Non-Financial Disclosures. In 2023, IPSASB published a brief Climate-Related Disclosures project.

3.5.1. Sustainability Reporting in the Higher Education Sector

The first reports date back to 2007 with the Leuphana University of Lüneburg and the University of Michigan [45]. In 2015, the 2030 Agenda for Sustainable Development and its 17 Sustainable Development Goals (SDGs) accelerated the introduction of sustainability reporting at universities. The annual average of publications on university sustainability increased from 2 in the period 2011–2014 to 7 in 2015–2017, and to 11 in 2018–2024 [46].

The leading sustainability reporting tool for higher education belongs to GRI (39 studies), the only one based on standards, followed by STARS (Sustainability Tracking, Assessment & Rating System, 33 studies), Global Compact (20 studies), and GreenMetric (15 studies) [47]. Many other rankings of universities exist.

STARS is a self-reporting framework for colleges and universities to measure their sustainability performance; rated institutions are featured in AASHE’s annual Sustainable Campus Index (SCI), which highlights best practices and top performers by impact area and institution type; they are included in the STARS Benchmarking Tool, which allows AASHE members to compare institutions on the basis of their sustainability performance [48]. As of March 2023, STARS reports were submitted by over 595 institutions in 21 countries, covering mostly the 49 US States and the District of Columbia (83.5%), and eight Canadian provinces (11.5%). Their sustainability performance is evaluated in five categories: 1) Academics (curriculum, research), 2) Operations (air and climate, buildings, energy, food and dining, grounds, purchasing, transportation, waste, water); 3) Engagement (on campus, in public), 4) Planning and Administration (coordination and planning, diversity and affordability, investment and finance, wellbeing and work), and 5) Innovation and Leadership (Exemplary Practice, Innovation).

The Ten Principles of the UN Global Compact address fundamental responsibilities in the areas of human rights, labor, environment and anti-corruption; it is a voluntary initiative and institution’s responsibility [49]. The Ten Principles include:

- a)

- Human Rights: 1) Businesses should support and respect the protection of internationally proclaimed human rights; and 2) make sure that they are not complicit in human rights abuses.

- b)

- Labor: 3) Businesses should uphold the freedom of association and the effective recognition of the right to collective bargaining; 4) the elimination of all forms of forced and compulsory labor; 5) the effective abolition of child labor; and 6) the elimination of discrimination in respect of employment and occupation.

- c)

- Environment: 7) Businesses should support a precautionary approach to environmental challenges; 8) undertake initiatives to promote greater environmental responsibility; and 9) encourage the development and diffusion of environmentally friendly technologies.

- d)

- Anti-Corruption: 10) Businesses should work against corruption in all its forms, including extortion and bribery.

The UI GreenMetric World University Ranking is based on the annual sustainability performance of universities and has been conducted by Universitas Indonesia since 2010 [50]. Through 39 indicators in 6 criteria, it determines the rankings of 1 477 institutions across 95 countries by the environmental commitments and initiatives of universities. In 2018, they included the SDGs to become more socially and governance oriented.

4. Discussion

4.1. Corporate Sustainability Reporting Standards

Results from the literature and practice of corporate sustainability reporting standards indicate that the ISO and GRI ones are still the most widespread and vital ones. The GRI standards are voluntary and the most numerous, having 74 items – 3 general standards, 40 sector ones, and 31 topic ones. To keep the GRI Standards relevant and up to date, the Global Sustainability Standards Board (GSSB) sets out a new work program every three years. The GSSB work program includes projects to review existing GRI Standards as well as to develop new ones [24]. GRI is actively collaborating with other standard setters such as EFRAG, ISSB, and IFRS [51,52,53].

ESRS are mandatory and had the chance to overtake the GRI ones by prevalence with the CSRD, accepted in December 2022, with the ESRS being published in December 2023. In contrast to the GRI, which is focused on impact materiality but not on the financial materiality dimension, the ESRS are based on double materiality. But in February 2024, the EU decided to postpone the deadline for the sector-specific standards from mid-2024 to mid-2026. For companies with fewer than 1000 employees, voluntary use of ESRS is recommended. EFRAG developed a voluntary sustainability reporting standard even for non-listed micro, small, and medium enterprises (VSME) [54].

In the US, the new government made a strong pushback on the concept of ESG, and federal US laws will not follow the sustainability disclosure as planned before [55]. Yet, some US states, e.g., California, will continue introducing their own mandatory state regulations. The California Senate Bills, SB 253: The Climate Corporate Data Accountability Act (CCDAA), SB 261: The Climate-Related Financial Risk Act (CRFRA), and SB 219: Amendments to California’s Climate Disclosure Laws will require thousands of companies to disclose their carbon emissions [56]. Companies are preparing for their 2026 disclosures on 2025 operations. Decisions of the largest sub-national economy in the world will have a strong effect on large companies and other states in the US.

The latest data indicate a continued trend favoring voluntary over mandatory measures – voluntary frameworks, which now account for 58% of policies set around the world; however, to drive meaningful progress, a transition to robust mandatory policies is essential [57]. Companies worldwide are preparing for the advent of mandatory reporting on sustainability [33]. The global map of countries adopting sustainability due diligence laws and the ESG regulations development over time is available [58].

4.2. Public Sustainability Reporting Standards

While the private sector already has sustainability reporting rules through various standards, the public sector faces unique challenges in implementing comparable frameworks: its governance structure for sustainability reporting is particularly complex, with commitments derived from international treaties and national plans, and implemented through multiple governmental entities [59]. The introduction of new reporting standards like those used in the private sector is now being considered, including key lessons from past reforms. Key steps to assist public organizations in planning and preparing their reports and developing a strategy for further improvements in their reporting were published by the Chartered Institute of Public Finance and Accountancy, CIPFA [60].

Universities are expected to lead sustainability reporting in the public sector. Abello-Romero et al. concluded in their research that although higher education institutions (HEIs) have begun to adopt sustainability reporting, this practice remains at an early stage. Universities shall play a key role in global sustainability, but the quality, frequency, and scope of reporting must be improved [46]. There is a need to standardize reporting through a framework specifically adapted to HEIs, addressing social, cultural, and economic dimensions besides the environmental one. GRI guidelines and STARS Tool need to be customized to reflect the particularities of the higher education sector and promote effective institutionalization of reporting. The sustainability report shall be aligned with the report on SDGs.

Finally, there is the personal level of sustainability. Individuals have a dual role – to act on individual-level change while simultaneously influencing system-level change [61]. We live in an interconnected world, playing different roles: as individuals, we consume goods and services; as employees, we design and implement organizational policies; and as citizens, we elect governments. Our choice and extent of consumption determine our social and environmental impact. We are accountable for our actions and their impacts. The system-level change is needed, but it requires individuals to understand the need for change, along with a well-understood definition of the problem [62]. We shall work hard to understand the varied cultures, values and perceptions that can contribute to the transition to an environmentally sustainable global economy [63].

4.3. Personal and Community Sustainability Reporting

This discussion leads us to the question of what sustainable reporting should be for individuals or for communities (municipal, provincial, regional, state, country, Union). Social and governance components are well covered, but the environmental reporting is not. It could be done with the Carbon Footprint (CF) or, even better, the Ecological Footprint (EF) of an individual, city, country, or region [64]. CF evaluates the GHG emissions of a person, event, organization, or product in a given period, e.g., in t/a (tons per year); for an individual, it includes energy used (electricity, heat and cooling, transportation, etc.), production of goods and use of services, and agriculture (food and drinks). The global average FP per capita is 4 t/a, and it must drop below 2 t/a by 2050 to keep the temperature rise below 2 °C.

EF measures the rate of consumption of natural resources and waste production compared to how quickly nature can renew these resources and absorb the waste created [65]. It includes the CF (which amounts to about 60% of the EF), agricultural and forest land (food, wood), water (for irrigation, drinking and industry), biodiversity, waste management (to absorb CO2 and CH4 emissions, etc.), and urban infrastructure; it is measured in global hectares (ha), the globally available area of equivalent productivity. A state or nation’s biocapacity represents the productivity of its ecological assets (including cropland, grazing land, forest land, fishing grounds, and built-up land). As the world population increases, the biocapacity per capita decreases. In 2024, the biocapacity per person was 1.5 ha, and the EF per person was 2.6 ha, giving a deficit per person of 1.1 ha (the first deficit appeared in 1973).

Today, the CF and EF calculations using several available calculators are voluntary, but in future they shall be mandatory. Experience with calculations by students is good; they are surprised by the high personal deficit, and they try to reduce it from 4–6 ha to 3–4 ha, but they cannot reach the biocapacity area. To reach it requires profound changes in their lifestyle – no car, no flights, insulated buildings, renewable energy, no meat, zero packaging, etc. Laws on spending and control of measurement, calculations and reporting will be needed.

Another possibility for a personal environmental sustainability reporting standard is individual mass (weight); if someone is overweight or even obese, he or she needs to pay an additional health insurance premium. Energy-intensive activities could be taxed more heavily. Personal and community social sustainability reporting covers various protected characteristics, including age, disability, gender reassignment, race, religion or belief, sex and sexual orientation. Community reporting does not differ too much from the public one, but personal reporting is more difficult to control and report. Education and lifelong learning, social life and cooperation are very important for enabling it.

In terms of sustainability, wars pose the greatest problem. They cause a) a large, unnecessary environmental burden through the destruction of buildings and infrastructure, air, soil and water pollution; b) human rights violations through killing, wounding and destruction of property; and c) the economic devastation of warring parties. As a continuation of the UN Agenda 2030 with the 17 SDGs [11] and the Pact for the Future [66], the UN should adopt international agreements with standards for mutual problem-solving through diplomacy and stop further armaments for warfare.

5. Conclusions

Profound changes and dangers are threatening humanity. Climate change is speeding up, and human reactions to keep the temperature rising below 1.5 °C or at least 2 °C must be strengthened. The European Union followed this trend by accepting the Green Deal and the CSRD together with the mandatory ESRS. The two-year delay is understandable in the present geostrategic situation, but the planned corporate sustainability reporting must be carried out within the planned scope and by the agreed deadlines.

It would be urgent to extend mandatory reporting to the public sector from the municipal to the national and international (UN, EU, US, BRICS, etc.) level: from state bodies and local community administrations, agencies, funds, to institutions, public economic institutions, universities, research institutes, schools, healthcare, culture, police, military and other public law entities with more than 250 employees. Smaller entities shall cooperate within the value chains. Sustainability reporting standards shall be adopted to the needs and capabilities of public institutions.

Net zero will not be achieved without the participation of individual citizens of the world. Their habits and actions must be adapted to the available resources and biocapacity of the Earth. It is necessary to adopt appropriate legislation, personal standards, action plans and individual or family reports (like tax revenue reports) on the gradual CF/EF achievement of changes in the habits, behaviors and actions of individuals.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The author declares no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| AASB | Australian Accounting Standards Board |

| AASHE | Association for the Advancement of Sustainability in Higher Education |

| ASRS | Australian Sustainability Reporting Standard |

| CBAM | Carbon Border Adjustment Mechanism |

| CCDAA | Climate Corporate Data Accountability Act |

| CIPFA | Chartered Institute of Public Finance and Accountancy |

| CDP | Carbon Disclosure Project |

| CF | Carbon Footprint |

| CFO | Chief Financial Officers |

| CSDDD | Corporate Sustainability Due Diligence Directive |

| CSRD | Corporate Sustainability Reporting Directive |

| CSR | Corporate Social Responsibility |

| CSRS | Corporate Sustainability Reporting Standards |

| CSSB | Canadian Sustainability Standards Board |

| DEI | Diversity, Equity, and Inclusion |

| EF | Ecological Footprint |

| EFRAG | European Financial Reporting Advisory Group |

| ESG | Environmental, Social, and Governance |

| ESRS | European Sustainability Reporting Standards |

| EU | European Union |

| GHG | Greenhouse Gas |

| GRI | Global Reporting Initiative |

| GSSB | Global Sustainability Standards Board |

| HEI | Higher Education Institution |

| IFRS | International Financial Reporting Standards |

| IPSASB | International Public Sector Accounting Standards Board |

| ISSB | International Sustainability Standards Board |

| ISO | International Organization for Standardization |

| KPI | key performance indicator |

| NFRD | Non-Financial Reporting Directive |

| OHS | Occupational Health and Safety |

| SASB | Sustainability Accounting Standards Board |

| SDG | Sustainable Development Goal |

| SME | Small and Medium-sized Enterprise |

| TCFD | Task Force on Climate-related Financial Disclosures |

| UN | United Nations |

| US | United States (of America) |

| VSME | Voluntary Reporting Standard for SMEs |

References

- Roser, M.; Mortality in the past: every second child died, Our World in Data. November 2024. Available online: https://ourworldindata.org/child-mortality-in-the-past (accessed on 19 July 2025).

- Roser, M.; Ritchie, H.; How has world population growth changed over time? Our World in Data. 1 June 2023. Available online: https://ourworldindata.org/population-growth-over-time (accessed on 19 July 2025).

- Fleck, A.; A History of Resource Extraction and Acceleration, Statista. 31 July 2024. Available online: https://www.statista.com/chart/32750/global-extraction-of-the-four-main-material-groups/ (accessed on 27 July 2025).

- WEF, World Economic Forum. The number of cars worldwide is set to double by 2040. 22 April 2016. Available online: https://www.weforum.org/stories/2016/04/the-number-of-cars-worldwide-is-set-to-double-by-2040/ (accessed on 27 July 2025).

- Ritchie, H.; Rosado, P.; Roser, M.; Energy Production and Consumption. Our World in Data. January 2024. Available online: https://ourworldindata.org/energy-production-consumption#article-citation (accessed on 27 July 2025).

- Ritchie, H.; Rosado, P.; Roser, M.; Greenhouse gas emissions. Our World in Data. January 2024. Available online: https://ourworldindata.org/greenhouse-gas-emissions (accessed on 27 July 2025).

- Ritchie, H.; Rosado, P.; Roser, M.; Breakdown of carbon dioxide, methane and nitrous oxide emissions by sector. Our World in Data. January 2024. Available online: https://ourworldindata.org/emissions-by-sector (accessed on 27 July 2025).

- United Nations, Climate change, Process and meetings. Available online: https://unfccc.int/ (accessed on 7 September 2025).

- Ritchie, H.; How much CO2 can the world emit while keeping warming below 1.5 °C and 2 °C? Our World in Data. 29 September 2023. Available online: https://ourworldindata.org/how-much-co2-can-the-world-emit-while-keeping-warming-below-15c-and-2c (accessed on 27 July 2025).

- OECD (2015), The Economic Consequences of Climate Change, OECD Publishing, Paris. 3 November 2015. Available online: http://dx.doi.org/10.1787/9789264235410-en (accessed on 27 July 2025).

- United Nations. Transforming our world: the 2030 Agenda for Sustainable Development. 25 September 2015. Available online: https://sdgs.un.org/2030agenda (accessed on 28 July 2025).

- United Nations. The Paris Agreement. 12 December 2015. Available online: https://www.un.org/en/climatechange/paris-agreement (accessed on 28 July 2025).

- European Commission. The European Green Deal. Available online: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal_en (accessed on 28 July 2025).

- Directive 2014/95/EU of the European Parliament and of the Council amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. O.J. 2014 (L. 330) 1–9.

- Directive 2022/2464/EU of the European Parliament and of the Council amending Regulation 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting. O.J. 2022 (L 322) 15–80.

- European Commission, Simplification: Council gives final green light on the ‘Stop-the-clock’ mechanism to boost EU competitiveness and provide legal certainty to businesses. 14 April 2025. Available online: https://www.consilium.europa.eu/en/press/press-releases/2025/04/14/simplification-council-gives-final-green-light-on-the-stop-the-clock-mechanism-to-boost-eu-competitiveness-and-provide-legal-certainty-to-businesses/ (accessed on 29 July 2025).

- Commission adopts “quick fix” for companies already conducting corporate sustainability reporting. 11 July 2025. Available online: https://finance.ec.europa.eu/publications/commission-adopts-quick-fix-companies-already-conducting-corporate-sustainability-reporting_en (accessed on 29 July 2025).

- Reuter, A.S.; EU Omnibus proposal: Essential insights and how to navigate the upcoming changes. Sphera. Available online: https://www.sphera.com (accessed on 2 August 2025).

- IMD. Best practices in ESG reporting: enhancing corporate responsibility. August 2025. Available online: https://www.imd.org/blog/sustainability/esg-reporting/ (accessed on 2 August 2025).

- Institute of Directors. Sustainability and ESG – What’s the difference? 17 July 2024. Available online: https://www.iod.com/resources/sustainable-business/sustainability-and-esg-whats-the-difference/ (accessed on 3 August 2025).

- European Commission. Questions and answers on simplification omnibus I and II. 26 February 2025. Available online: https://ec.europa.eu/commission/presscorner/detail/en/qanda_25_615 (accessed on 3 August 2025).

- Global Reporting Initiative, GRI. Continuous improvement. Available online: https://www.globalreporting.org/standards/ (accessed on 8 August 2025).

- GRI Standards. A Short Introduction to the GRI Standards. Available online: http://www.globalreporting.org (accessed on 9 August 2025).

- Global Sustainability Standards Board (GSSB). GRI Sector Program – List of prioritized sectors, Revision 3. 19 October 2021. Available online: https://www.globalreporting.org/media/mqznr5mz/gri-sector-program-list-of-prioritized-sectors.pdf (accessed on 9 August 2025).

- Agilent. Final List of Topics, Example Sub-topics and GRI Standards to Consider. Available online: https://www.agilent.com/environment/Material%20Topics%20and%20Sub%20topic%202019.pdf (accessed on 9 August 2025).

- The GRI Standards: A guide for policy makers. Available online: https://www.globalreporting.org/media/nmmnwfsm/gri-policymakers-guide.pdf (accessed on 9 August 2025).

- Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards, C/2023/5303. OJ L 2023, 2772, 1–284.

- CSR Tools. ESRS – short and compact. Available online: https://csr-tools.com/en/esrs/ (accessed on 9 August 2025).

- KPMG. ESRS. Available online: https://kpmg.com/se/en/services/esg-sustainability/esrs.html (accessed on 9 August 2025).

- ISO (International Organization for Standardization). Building a sustainable path to ESG reporting. Available online: https://www.iso.org/climate-change/esg-reporting (accessed on 10 August 2025).

- Duvernay, G.; Plan A. All ISO standards for ESG and sustainability. 27 May 2025. Available online: https://plana.earth/academy/iso-esg (accessed on 10 August 2025).

- Poirmeur, P. Top 10 ISO sustainability standards. Available online: https://www.trustditto.com/en/resources/blog/top-10-iso-sustainability-standards#iso-14001-environmental-management-system (accessed on 15 August 2025).

- KPMG. The move to mandatory reporting: Survey of Sustainability Reporting 2024. Available online: https://kpmg.com/xx/en/our-insights/esg/the-move-to-mandatory-reporting.html#accordion-57530f0dfc-item-b09872126f (accessed on 15 August 2025).

- GRI. GRI and sustainability reporting in the EU. July 2024. Available online: https://chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.globalreporting.org/media/d4faazel/gri-and-the-esrs-qa-final.pdf (accessed on 15 August 2025).

- EFRAG. Amended ESRS Exposure Draft. July 2025. Available online: https://www.efrag.org/sites/default/files/media/document/2025-07/Amended_ESRS_Exposure_Draft_July_2025_ESRS_1.pdf (accessed on 15 August 2025).

- Brightest. The Top 7 Sustainability Reporting Standards in 2024. Available online: https://www.brightest.io/sustainability-reporting-standards#issb (accessed on 15 August 2025).

- EcoActive. Canadian Sustainability Disclosure Standards: Timeline, Scope and What’s Next. 4 August 2025. Available online: https://ecoactivetech.com/csds-1-2-esg-reporting-canada/ (accessed on 15 August 2025).

- PwC (PricewaterhouseCoopers) Indonesia, Spotlight on sustainability: National Sustainability Reporting Framework. October 2024. Available online: https://www.pwc.com/my/en/publications/2024/national-sustainability-reporting-framework.html (accessed on 15 August 2025).

- Keslio. Sustainability Reporting Requirements in the United States. 2 January 2025. Available online: https://www.keslio.com/kesliox/sustainability-reporting-requirements-in-the-united-states (accessed on 15 August 2025).

- PwC. Sustainability reporting standards and legislation finalized: mandatory sustainability reporting begins. Available online: https://www.pwc.com.au/assurance/sustainability-reporting-and-assurance/australian-sustainability-reporting-standards.html (accessed on 15 August 2025).

- China Briefing. China Unveils Its First Set of Basic Standards for Corporate Sustainability (ESG) Disclosure. Available online: https://www.china-briefing.com/news/china-unveils-basic-standards-for-corporate-sustainability-esg-disclosure/ (accessed on 15 August 2025).

- ESG Today. Japan Releases Inaugural IFRS-Aligned Sustainability Reporting Standards. Disclosure. 6 March 2025. Available online: https://www.esgtoday.com/japan-releases-inaugural-ifrs-aligned-sustainability-reporting-standards/ (accessed on 15 August 2025).

- UK government. Guidance – UK Sustainability Reporting Standards. 25 June 2025. Available online: https://www.gov.uk/guidance/uk-sustainability-reporting-standards (accessed on 15 August 2025).

- IPSASB. Advancing Public Sector Sustainability Reporting. Available online: https://www.ipsasb.org/focus-areas/sustainability-reporting (accessed on 15 August 2025).

- Leal Filho, W.; Coronado-Marín, A.; Salvia, A.L.; Silva, F.F.; Wolf, F.; LeVasseur, T.; Kirrane, M.J.; Doni, F.; Paço, A.; Blicharska, M.; et al. International Trends and Practices on Sustainability Reporting in Higher Education Institutions. Sustainability 2022, 14, 12238. [Google Scholar] [CrossRef]

- Abello-Romero, J.; Mancilla, C.; Restrepo, K.; Sáez, W.; Durán-Seguel, I.; Ganga-Contreras, F. Sustainability Reporting in the University Context—A Review and Analysis of the Literature. Sustainability 2024, 16, 10888. [Google Scholar] [CrossRef]

- Moggi, S. Sustainability reporting, universities and global reporting initiative applicability: a still open issue. Sustain. Account. Manag. Policy J. 2023, 14/4, 699–742. [Google Scholar] [CrossRef]

- Association for the Advancement of Sustainability in Higher Education (AASHE). STARS, The Sustainability Tracking, Assessment and Rating System. Available online: https://stars.aashe.org/about-stars/ (accessed on 17 August 2025).

- United Nations Global Compact. The power of principles. Available online: https://unglobalcompact.org/what-is-gc/mission/principles (accessed on 17 August 2025).

- University of Indonesia. UI GreenMetric World University Ranking. Available online: https://greenmetric.ui.ac.id/ (accessed on 17 August 2025).

- GRI and EFRAG. GRI-ESRS Interoperability Index. Version 1. 22 November 2024. Available online: https://www.globalreporting.org/media/qzmoeixv/esrs-gri-interoperability-index-november-2024.pdf (accessed on 17 August 2025).

- IFRS. GRI and IFRS Foundation collaboration to deliver full interoperability that enables seamless sustainability reporting. Available online: https://www.ifrs.org/news-and-events/news/2024/05/gri-and-ifrs-foundation-collaboration-to-deliver-full-interoperability/ (accessed on 17 August 2025).

- EFRAG and IFRS. ESRS–ISSB Standards Interoperability Guidance. Available online: https://www.efrag.org/sites/default/files/sites/webpublishing/SiteAssets/ESRS-ISSB%20Standards%20Interoperability%20Guidance.pdf (accessed on 17 August 2025).

- EFRAG. Voluntary reporting standard for SMEs (VSME). Available online: https://www.efrag.org/en/projects/voluntary-reporting-standard-for-smes-vsme/concluded (accessed on 23 August 2025).

- Buchanan, R.; Trump 2.0: potential impact on sustainability regulations and reporting. Jupiter, 29 January 2025. Available online: https://www.jupiteram.com/global/en/corporate/insights/trump-potential-impact-sustainability-regulations-reporting/ (accessed on 23 August 2025).

- Salesforce, Net Zero. California’s Climate Disclosure Laws: A Guide for Companies. Available online: https://www.salesforce.com/net-zero/california-climate-disclosure-laws/ (accessed on 23 August 2025).

- GRI. Sustainability disclosure still driven by voluntary policies. 18 November 2024. Available online: https://www.globalreporting.org/news/news-center/sustainability-disclosure-still-driven-by-voluntary-policies/ (accessed on 23 August 2025).

- Worldfavor guide. The sustainability reporting playbook. 2024; pp. 8,9.

- OECD. Advancing public sector sustainability reporting. OECD papers on budgeting, Vol. 2025/05. Available online: https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/06/advancing-public-sector-sustainability-reporting_6f80aa9d/ad5fb10f-en.pdf (accessed on 24 August 2025).

- Adams, C.A.; Public sector sustainability reporting: time to step it up. CIPFA. April 2023. Available online: https://www.cipfa.org/protecting-place-and-planet/sustainability-reporting (accessed on 24 August 2025).

- Mantzikopoulou, N.; The Power of Individual and Systemic Action in Driving Sustainability. AIMS International. 23 April 2025. Available online: https://www.aimsinternational.com/news/the-power-of-individual-and-systemic-action-in-driving-sustainability (accessed on 30 August 2025).

- Levermann, A.; Individuals can’t solve the climate crisis. Governments need to step up. The Guardian, 10 July 2019. Available online: https://www.theguardian.com/commentisfree/2019/jul/10/individuals-climate-crisis-government-planet-priority (accessed on 30 August 2025).

- Cohen, S.; Responsibility in the Transition to Environmental Sustainability. Columbia Climate School. 10 May 2021. Available online: https://news.climate.columbia.edu/2021/05/10/the-role-of-individual-responsibility-in-the-transition-to-environmental-sustainability/ (accessed on 30 August 2025).

- Global Footprint Network. How Ecological Footprint accounting helps us recognize that engaging in meaningful climate action is critical for our own success. 9 November 2017. Available online: https://www.footprintnetwork.org/2017/11/09/ecological-footprint-climate-change/ (accessed on 31 August 2025).

- CO2NEWS. Carbon Footprint vs. Ecological Footprint: What’s the Difference and Why Does It Matter? 9 November 2024. Available online: https://www.co2news.sk/en/2024/11/09/carbon-footprint-versus-ecological-footprint-what-is-the-difference-and-why-does-it-matter/ (accessed on 31 August 2025).

- UN. Pact for the Future: A Vision for Global Collaboration. 28 November 2024. Available online: https://unric.org/en/pact-for-the-future/ (accessed on 31 August 2025).

Figure 1.

The Structure of the GRI Standards.

Figure 2.

The 12 current ESRS standards and the common areas of reporting [29].

Figure 2.

The 12 current ESRS standards and the common areas of reporting [29].

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.