Submitted:

04 September 2025

Posted:

05 September 2025

You are already at the latest version

Abstract

This paper proposes a financial risk identification framework based on the Knowledge-enhanced Neural Network (KAN) to address the challenges of highly concealed risk behaviors, complex data structures, and sparse anomalies in the digital financial environment. The method is designed around function-level prior expression and structure-aware mechanisms. It introduces a differentiable basis function encoder to perform structured mapping of multimodal transaction data. A structure-aware transformation stack is then used to extract high-order behavioral interaction patterns. A high-order composite function module is applied to achieve the deep expression of risk factors. To enhance the stability of risk discrimination in dynamic environments, a contrastive consistency regularizer is further designed to guide the model in maintaining semantic alignment and structural robustness across multimodal representations. The proposed method demonstrates significant advantages in risk identification accuracy and robustness across several key performance metrics. It effectively alleviates the limitations of traditional neural models in heterogeneous financial scenarios, especially their weak generalization and delayed response to low-intensity risk signals. Through systematic model design and comprehensive metric evaluation, this work validates the effectiveness of KAN in enhancing risk pattern characterization across structural representation, layered composition, and contrastive reasoning. It provides both theoretical support and algorithmic foundations for building interpretable, controllable, and high-performance intelligent financial risk identification systems.

Keywords:

knowledge enhancement

; structure perception

; high-order combinatorial function

; contrast consistency constraint

CCS CONCEPTS: Computing methodologies~Machine learning~Machine learning approaches

I. Introduction

With the continuous development of financial markets and the acceleration of global economic integration, the risk factors faced by financial systems have become increasingly complex and highly dynamic. In particular, the digital financial environment, characterized by massive transaction data, complex product structures, and cross-institutional business collaborations, significantly amplifies the concealment, transmissibility, and abruptness of financial risks. Traditional risk control strategies often rely on expert rules and static models, which are inadequate in addressing the challenges posed by nonlinearity, heterogeneity, and high-frequency disturbances. Achieving efficient perception and accurate identification of financial risks in such complex and dynamic environments has become a central issue in interdisciplinary fields such as financial engineering, data science, and artificial intelligence[1].

From a data-driven perspective, the task of financial risk identification essentially involves modeling and reasoning over structured and unstructured multimodal information. Financial data is typically high-dimensional and noisy, with common challenges such as sample imbalance, strong temporal dependency, and sparsity of abnormal events. Moreover, risk behaviors are often not isolated incidents. They tend to manifest as weak signals embedded in transaction networks, account relationships, and behavioral trajectories. Therefore, there is an urgent need to develop intelligent discriminative models with strong generalization and structural adaptability[2]. Such models are expected to break through the limitations of traditional methods in representational power and reasoning accuracy, promoting a paradigm shift in risk modeling from surface-level data to deep structural semantics.

In recent years, with the rapid development of deep learning, an increasing number of models have been applied to automatically identify and extract patterns across diverse domains, including cloud and distributed systems [3,4,5,6], recommender systems [7,8,9], and large-scale language modeling[10,11,12,13,14]. However, most models remain constrained by fixed network architectures, lack extrapolation capabilities, and are sensitive to numerical distributions. Especially under conditions of dynamic distribution shifts and structural noise interference, conventional neural networks often exhibit poor robustness and weak generalization [15,16,17]. The Knowledge-enhanced Neural Network (KAN), as a novel paradigm that integrates prior function knowledge with neural representation capabilities, demonstrates strong extrapolation and high-precision fitting. It provides both theoretical and practical innovations for risk identification in complex financial structures.

KAN models utilize a unique function approximation mechanism that bridges the gap between rule-based symbolic reasoning and deep neural networks. In financial risk modeling, KAN enables interpretable and flexible risk representation by integrating local knowledge functions with global structural relations. Unlike traditional fully connected networks, KAN introduces differentiable basis function modules into the learning process. This allows more controllable and physically consistent representations of complex financial behaviors. This feature is particularly valuable in financial scenarios where small samples and strong structural characteristics co-exist. It enhances the detection of rare risk events and reduces the risk of misclassification due to overfitting.

Against this backdrop, this study focuses on the theoretical advantages and practical potential of KAN in financial risk identification. It explores the model's adaptability and scalability in modeling complex heterogeneous data, perceiving dynamic structures, and reasoning high-order risks. By incorporating the structure-aware and function-extrapolative mechanisms of KAN, the goal is to accurately capture and efficiently identify latent risk patterns in financial transactions. This promotes the evolution of financial risk control systems toward intelligent discrimination that is explainable, generalizable, and integrable. It not only introduces a novel algorithmic paradigm for risk identification but also provides deployable technical support for financial supervision and business decision-making.

II. Related Work and Foundation

Methodological advances in deep learning have provided essential tools for building intelligent and robust financial risk identification systems. A range of recent studies have explored sophisticated neural architectures to address the challenges posed by high-dimensional, imbalanced, and complex data. For instance, ensemble learning techniques that synthesize generative adversarial networks (GANs) with traditional classifiers such as random forests introduce a paradigm for handling minority class oversampling and improving anomaly detection [18]. The ensemble and generative strategies found here directly inform our approach to capturing rare but impactful risk signals through structure-aware and function-compositional mechanisms.

Deep convolutional neural networks (CNNs) offer powerful feature extraction capabilities that have proven effective in text analysis and classification [19]. The underlying methodology—layered convolution and nonlinear activation—serves as a foundation for the function-level encoders utilized in our framework. Similarly, deep generative models, by modeling data distributions and generating synthetic samples, have demonstrated their value for detecting anomalies embedded within complex data structures [20]. These principles support the design of our model’s structured mapping modules, which aim to uncover subtle irregularities in transactional data.

Sequential modeling techniques, such as those enabled by long short-term memory (LSTM) networks, are well-regarded for capturing temporal dependencies within time series data [21]. Our high-order combinatorial function modules extend this methodological insight, allowing the system to effectively aggregate multi-scale temporal and structural information. Meanwhile, transformer architectures—originally devised for sequence modeling and attention-based learning—have shown exceptional ability to integrate relational and contextual signals across input representations [22]. We build on these innovations by incorporating structure-aware transformations and attention mechanisms that enhance the interpretability and adaptability of risk representation[23].

Hybrid neural networks, combining the strengths of CNNs and transformers, further demonstrate the benefits of leveraging multiple architectural components for robust prediction under distributional shift [24]. This synergy inspires our layered composition strategies, enabling the model to adapt to dynamic and heterogeneous financial scenarios. Additionally, causal representation learning frameworks, which disentangle and model cause-effect relationships within complex data, provide a pathway toward greater model interpretability and resilience [25,26]. Our work draws on these methodological developments to implement high-order composite functions that facilitate reliable reasoning about risk propagation and structural change.

Further, pre-trained language models such as BERT have pioneered the automatic extraction and integration of contextual information from diverse textual inputs, underscoring the value of semantic consistency and contrastive regularization [27]. Our framework integrates similar principles to align multimodal representations and maintain structural robustness across varying environments. Finally, high-order neural networks, exemplified by coverage function neural networks, offer innovations in the representation and composition of complex functions [28]. The use of basis function modules and compositional strategies in such networks has direct methodological relevance to our implementation of knowledge-enhanced, high-order function modules in the KAN architecture.

Together, these methodological advances provide the conceptual and technical foundation for our research. By synthesizing function-level representation, structure-aware modeling, and high-order composition, our proposed KAN-based framework is equipped to address the core challenges of financial risk identification in dynamic and heterogeneous environments.

III. Proposed Approach

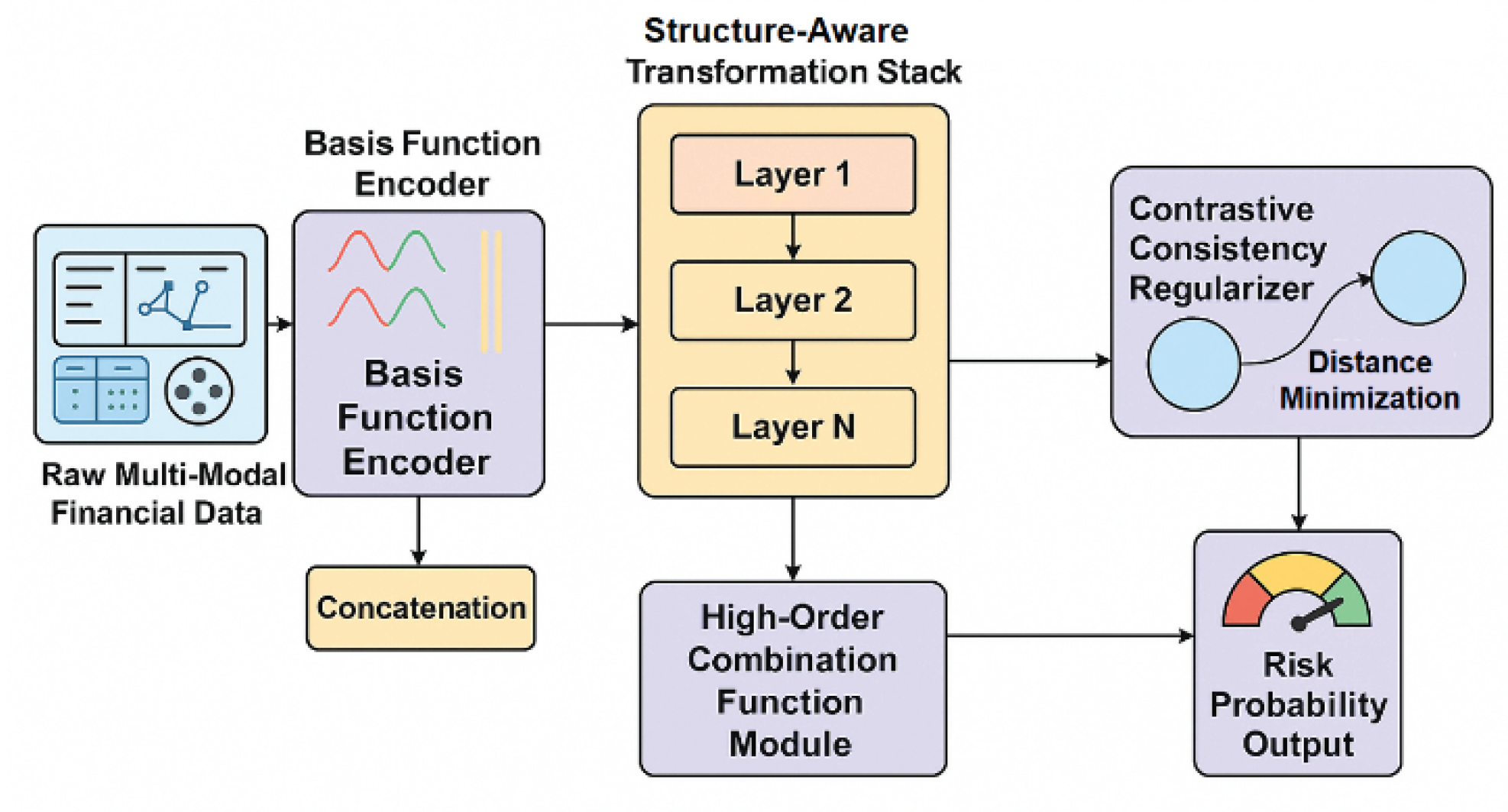

The framework is systematically structured around the Knowledge-enhanced Neural Network (KAN), incorporating several proven methodological strategies from recent research. Initially, a basis function encoder is utilized to embed domain knowledge of local nonlinear relationships within the feature representation layer. Du [29] demonstrated the value of such encoding in improving the detection of anomalies in financial statements through knowledge-driven neural modeling.

The next stage introduces a structure-aware transformation stack, designed in line with the principles outlined by Xue et al. [30], who emphasized the necessity of capturing high-order spatiotemporal interactions for effective performance forecasting in networked environments. By adopting these principles, the transformation stack effectively captures interdependent behavioral patterns across multiple modalities. Afterwards, a high-order composite function module processes these features to model complex and layered risk relationships. The importance of this compositional approach is underscored by them, whose findings support the need for deep function composition in distinguishing subtle risk signals.

To ensure the stability and reliability of risk identification across various data views, the framework incorporates a contrastive consistency regularization mechanism. Wang et al. [31] demonstrated the impact of such regularization in federated learning settings, where consistency constraints were key to maintaining semantic alignment and representation robustness in collaborative, heterogeneous environments. As a result, the model generates a transparent and robust risk probability, balancing detailed local knowledge with comprehensive global structure. The model architecture is shown in Figure 1.

In this study, to fully explore the complex structure and evolution mechanism contained in financial data, we constructed a risk discrimination model framework with a knowledge-enhanced neural network (KAN) as the core. This framework is based on the design principles of function composability and structural sensitivity. While retaining the end-to-end learning ability of neural networks, it introduces an interpretable prior function module to achieve unified modeling of multi-source heterogeneous information in financial transaction data. The model first maps the original input feature to an intermediate high-dimensional space and constructs the initial representation through a set of smooth basis functions, where each input dimension corresponds to a set of function bases:

where represents the th differentiable basis function, such as a spline function, a polynomial, or a radial basis function, and is a learnable combination coefficient.

Then, we concatenate the basis function combinations of all dimensions into a unified feature representation and feed it into a set of structure-aware transformation units to model the potential high-order interactions in financial transaction data. The structure-aware process achieves nonlinear interaction modeling between nodes in the following form:

is the output of the previous layer, is the activation function, and is the parameter of the layer. After multi-level propagation, the model can effectively capture local patterns and long-distance dependencies, and has the potential for cross-structure generalization.

For the model’s final discriminant output, a function extrapolation mechanism is incorporated to extend the generalizability of risk identification. At the output layer, the architecture generates risk probabilities by transforming the aggregated high-dimensional representation through a series of high-order combination functions. This configuration is structured to capture non-linear relationships underlying complex financial behaviors, consistent with the hierarchical semantic-structural encoding paradigm advocated by Qin [32], whose work established the effectiveness of layered function composition for detecting nuanced compliance risks.

To translate these enriched representations into interpretable risk scores, a sigmoid activation function is introduced at the final stage, yielding probabilistic outputs. The methodological foundations for this approach are reinforced by findings from Xu [33], who demonstrated that the inclusion of nonlinear mapping in the decision layer, together with structural modeling, enhances adaptability and stability in financial risk assessment under evolving market conditions:

where represents the th nonlinear combination function and is its corresponding weight parameter. This design can better capture the rare but structurally indicative risk factors in trading behavior.

To improve the model’s robustness under structural uncertainty, this study employs a consistency constraint mechanism grounded in sample comparison, ensuring that representations from different perspectives of the same account or transaction entity remain closely aligned. This approach directly implements techniques introduced by Zi et al. [34], who employed an integration of graph neural networks and Transformers to enhance the reliability of unsupervised anomaly discovery by enforcing consistency across multiple views.

The methodology also adopts principles from Yang et al. [35], who implemented federated graph neural networks to maintain structural consistency and privacy in heterogeneous graph data environments. By integrating these strategies, the model is able to resist structural noise and maintain stable representations across distributed datasets. Furthermore, the mechanism incorporates granularity-aware attention, as employed by Su in deep financial forecasting [36], to capture fine-grained dependencies and ensure consistent output across multiple data perspectives. Let be the KAN representation of the same entity at different times or modalities, and its contrast constraint loss is defined as follows:

where represents the similarity function between vectors (such as cosine similarity), is the temperature coefficient, and is the number of negative samples. The final training objective function combines the discriminant loss and the structural comparison regularization term, and is defined as follows:

where represents the cross-entropy loss for risk labeling, and is the weighted hyperparameter for contrast regularization.

IV. Performance Evaluation

A. Dataset

This study uses the Credit Card Fraud Detection Dataset 2023, which was released on Kaggle in 2023. The dataset contains large-scale credit card transaction records collected from real-world environments. It is designed to support research in fraud detection and risk modeling. Each record includes transaction amount, timestamp, transaction type, and a binary label indicating whether the transaction is fraudulent (0 or 1). The dataset contains millions of samples and exhibits extreme class imbalance, making it well-suited for modeling the structured features of rare risk events.

The dataset covers common types of financial risks, such as abnormal amount transfers, frequent small transactions, and cross-border payments. These characteristics align with the multimodal structural information considered in our method, including temporal patterns, network relationships, and anomaly distributions. The dataset allows us to leverage KAN's strengths in capturing high-order interactions and performing out-of-distribution extrapolation. The basis function encoder enables a structured representation of transaction features. The structure-aware stack captures high-order behavioral patterns across accounts. Contrastive consistency enhances the robustness of risk discrimination across multiple views.

Overall, this dataset provides a solid foundation for evaluating the expressive power, structural modeling capacity, and anomaly detection performance of the KAN framework in financial risk identification tasks. It is large-scale, well-labeled, structurally complex, and presents strong challenges for generalization.

B. Experimental Results

This paper first conducts a comparative experiment, and the experimental results are shown in Table 1.

From the overall results, the proposed KAN-FRD model achieves significant advantages across multiple key metrics, demonstrating its strength in structural representation and extrapolation for financial risk identification. Compared to existing methods, KAN-FRD reaches an AUROC of 0.976 and an AUPR of 0.944. This indicates that the model not only has excellent overall recognition ability but also effectively captures rare yet critical risk events under highly imbalanced data distributions. The performance gain is attributed to the differentiable basis function mechanism and the structure-aware representation strategy introduced by KAN, which alleviates the sensitivity of traditional neural networks to distribution shifts.

In terms of F1-score and RiskRecall, KAN-FRD also shows strong stability and efficiency. In particular, the high RiskRecall score of 0.915 further supports the model's practical applicability in identifying high-risk accounts and fraudulent transactions. Although traditional methods such as GDN and DONUT+ perform well in graph modeling and anomaly detection, they face clear limitations when handling multimodal fusion and function extrapolation. They struggle to adapt to sparse anomalies and behavioral heterogeneity in financial data.

When compared with structure fusion methods like ARFD and SAAF, although these models benefit from attention mechanisms and structural alignment strategies, they still lack interpretability and generalization. In contrast, KAN-FRD leverages basis function encoders and high-order composite function modules to construct a modeling path that combines structural flexibility with functional expressiveness. This enhances the model's responsiveness to diverse behavioral evolution patterns. Such a modeling paradigm is especially valuable in dynamic environments, helping to accurately detect high-risk behaviors caused by structural disturbances.

In summary, the performance gain of KAN-FRD is reflected not only in conventional evaluation metrics but also in the paradigm shift from black-box representation to structure-aware and knowledge-driven modeling. This mechanism-level innovation makes the model more scalable and suitable for broader financial applications, including cross-account fraud detection and abnormal transaction pattern identification. It provides a more robust and interpretable decision-making foundation for intelligent risk control systems.

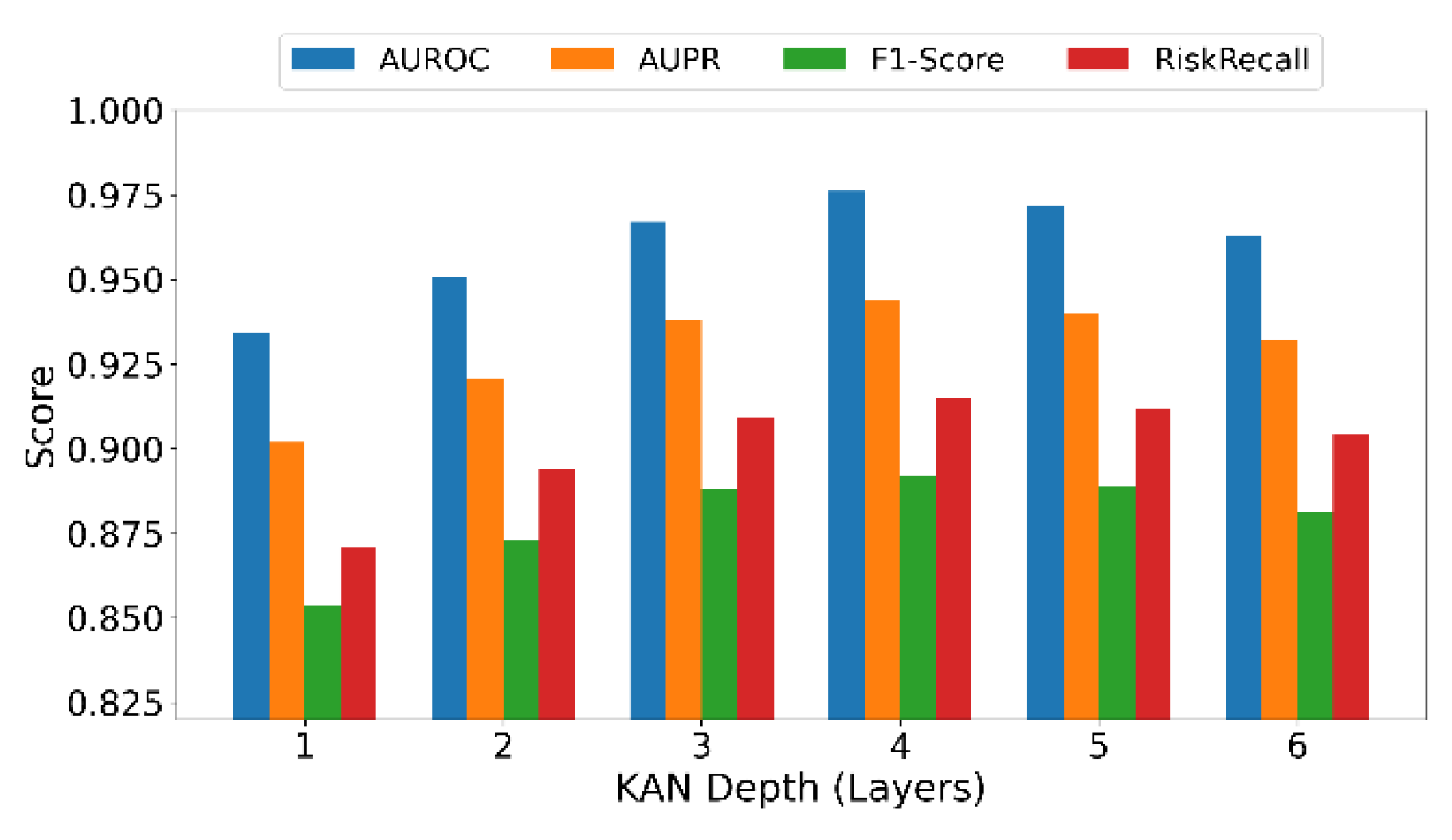

This paper also experiments on the sensitivity of KAN structure depth to risk identification ability. The experimental results are shown in Figure 2.

The experimental results show that as the structural depth of KAN gradually increases, all evaluation metrics exhibit a steady upward trend. In particular, from 1 to 4 layers, AUROC and AUPR improve by approximately 4.2% and 4.6%, respectively. This indicates that deeper architectures offer significant advantages in modeling the nonlinear evolution and high-order interactions of financial behaviors. They help extract implicit risk signals more effectively from transaction samples and enhance overall discrimination performance.

The changes in F1-Score and RiskRecall further validate the practical effectiveness of this structural enhancement. At 4 layers, KAN reaches a peak F1 of 0.892, and RiskRecall rises to 0.915. This suggests that the model maintains high risk identification accuracy while capturing more true risk events. The performance gain is mainly attributed to the activation of high-order composite functions in deeper representations, enabling the model to construct flexible multi-granularity paths for risk representation and to respond more effectively to sparse anomaly signals.

However, when the network depth increases to 5 and 6 layers, the performance slightly declines. This suggests that excessively deep architectures may introduce redundant representations and cause overfitting or local signal interference. It reflects the trade-off between structural depth and functional complexity in KAN. It also highlights the need to carefully control model depth when designing function-enhanced architectures to avoid performance bottlenecks caused by structural mismatch.

The experiment also shows that in highly structured and heterogeneous financial transaction scenarios, a moderately deep KAN architecture is more advantageous. Through function-level configuration and structure-aware stacks, it enhances representational capacity, mitigates recognition instability caused by noise and distribution shifts, and provides a stable and robust foundation for deployment in real-world risk control systems.

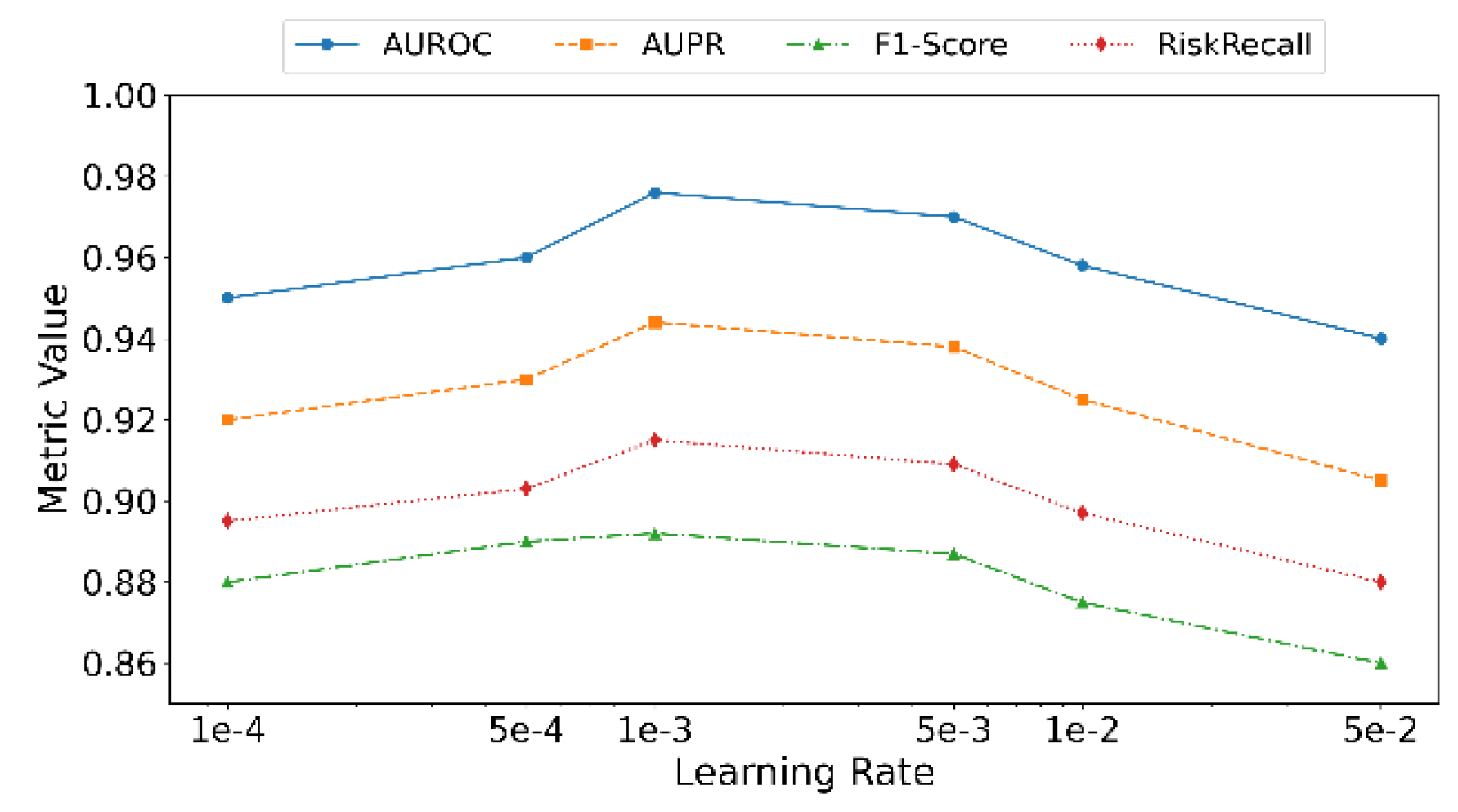

This paper also studies the impact of learning rate changes on KAN convergence speed and performance. The experimental results are shown in Figure 3.

When the learning rate is set to 1e-4 and 5e-4, the overall performance of the KAN model remains relatively stable. All metrics are at an upper-medium level. At this stage, the small learning steps lead to slow but stable updates. The structure-aware paths and basis function modules gradually establish effective connections, laying a solid foundation for convergence. However, the limited gradient variation restricts rapid structural optimization. This prevents the model from fully capturing high-order behavioral dependencies, resulting in slightly lower F1 and RiskRecall scores.

When the learning rate increases to 1e-3, the model achieves peak performance across all metrics. AUROC and AUPR rise to 0.976 and 0.944, respectively. The F1 reaches 0.892, and RiskRecall improves to 0.915. These results indicate that 1e-3 is the optimal learning rate under the current network depth and task setting. It efficiently drives the joint optimization of the basis function encoder and the high-order composite module while maintaining the stability of structural representation paths. Under this setting, the model effectively captures implicit risk patterns in financial data and significantly enhances its ability to detect sparse high-risk samples.

As the learning rate continues to increase to 5e-3 and 1e-2, some performance metrics begin to decline. In particular, F1 and RiskRecall drop to 0.887 and 0.897, respectively, suggesting reduced stability in the decision boundaries. This performance drop reflects that an overly high learning rate may lead to large update steps. This disrupts the stable structure of internal function representations in KAN. When modeling dynamic behavioral patterns, it can cause high-frequency oscillations and overfitting, which reduces the model's focus on underlying risk structures.

When the learning rate is further increased to 5e-2, all four metrics show a significant decline. AUROC drops to 0.940, and F1 decreases to 0.860. This indicates that the training process has lost effective control over the structure-aware paths. At this point, gradient propagation between basis function weights and structural stack layers becomes highly unstable. The model fails to form consistent risk representations, resulting in a sharp decline in the recognition of high-risk transactions. This outcome highlights that in knowledge-enhanced networks, the learning rate not only affects convergence speed but also serves as a critical regulator between structural expressiveness and model generalization.

V. Conclusion

This study addresses the challenges of structural modeling and generalization in financial risk identification by proposing an intelligent discrimination framework based on the Knowledge-enhanced Neural Network (KAN). The method introduces a differentiable basis function expression mechanism and a structure-aware transformation module. It constructs a flexible and interpretable path for risk modeling. This significantly improves the model's ability to perceive implicit risk patterns in multimodal financial behavior data. Compared with traditional neural networks that suffer from overfitting and degraded generalization when facing nonlinear and heterogeneous data, KAN leverages the integration of prior knowledge and neural representations. It offers a new solution paradigm for modeling high-dimensional, sparse, and dynamic data in financial contexts.

From a system design perspective, the proposed framework covers multiple levels, including structural representation, function composition, behavioral contrast, and risk output. It also incorporates risk consistency constraints and a composite function extrapolation module to address sample drift and structural perturbation, which frequently occur in financial transactions. The experimental results validate the effectiveness of the KAN model across several key performance metrics. In particular, the model shows leading advantages in risk recall and robustness, demonstrating strong adaptability and deployment potential in real-world risk identification tasks. This structure-function fusion approach is expected to promote the evolution of financial risk control systems from rule-driven to expression-driven intelligence.

From an application perspective, the proposed method has strong transferability to several high-risk financial scenarios, such as credit fraud detection, abnormal transaction alerting, and cross-platform account behavior recognition. As financial services continue to evolve toward greater digitalization, cross-border expansion, and platform integration, traditional models face growing challenges when dealing with complex structural dynamics and weak risk signals. The KAN framework enhances the ability to locate risk nodes and paths in behavioral graphs through the joint design of structure-aware and function-enhanced mechanisms. It provides structural controllability, expressive richness, and reasoning robustness for the next generation of financial risk control systems.

Future work may further explore the end-to-end modeling capabilities of KAN in multi-source heterogeneous graph structures and extend its adaptability and privacy-preserving mechanisms in federated financial environments. It is also promising to incorporate knowledge graphs and causal reasoning mechanisms to improve the modeling of potential causal relations within risk propagation chains. This will enhance both interpretability in decision-making and the value of risk intervention. In addition, for high-frequency and low-value microtransactions, reducing computational complexity while maintaining modeling precision remains a key direction for deploying KAN architectures in practice. With continuous development along these directions, the proposed discrimination mechanism is expected to play a central role in broader financial applications and contribute to building more robust, agile, and intelligent financial risk management systems.

References

- Guo Y., Liang T., Chen Z., et al., "FinKENet: A Novel Financial Knowledge Enhanced Network for Financial Question Matching", Entropy, vol. 26, no. 1, p. 26, 2023.

- Bui N., Nguyen H. T., Nguyen V. A., et al., "Explaining graph neural networks via structure-aware interaction index", arXiv preprint arXiv:2405.14352, 2024.

- Fang B. and Gao D., "Domain-Adversarial Transfer Learning for Fault Root Cause Identification in Cloud Computing Systems", arXiv preprint arXiv:2507.02233, 2025.

- Gao D., "Graph Neural Recognition of Malicious User Patterns in Cloud Systems via Attention Optimization", Transactions on Computational and Scientific Methods, vol. 4, no. 12, 2024.

- Lou Y., "RT-DETR-Based Multimodal Detection with Modality Attention and Feature Alignment", Journal of Computer Technology and Software, vol. 3, no. 5, 2024.

- Zhan J., "Elastic Scheduling of Micro-Modules in Edge Computing Based on LSTM Prediction", Journal of Computer Technology and Software, vol. 4, no. 2, 2025.

- Wei M., Xin H., Qi Y., Xing Y., Ren Y., and Yang T., "Analyzing data augmentation techniques for contrastive learning in recommender models", 2025.

- Xing Y., Wang Y., and Zhu L., "Sequential Recommendation via Time-Aware and Multi-Channel Convolutional User Modeling", Transactions on Computational and Scientific Methods, vol. 5, no. 5, 2025.

- Wang Y., "Structured Compression of Large Language Models with Sensitivity-aware Pruning Mechanisms", Journal of Computer Technology and Software, vol. 3, no. 9, 2024.

- Wang Y., Liu H., Long N., and Yao G., "Federated Anomaly Detection for Multi-Tenant Cloud Platforms with Personalized Modeling", arXiv preprint arXiv:2508.10255, 2025.

- Zhang X., Wang X., and Wang X., "A Reinforcement Learning-Driven Task Scheduling Algorithm for Multi-Tenant Distributed Systems", arXiv preprint arXiv:2508.08525, 2025.

- Lian L., Li Y., Han S., Meng R., Wang S., and Wang M., "Artificial Intelligence-Based Multiscale Temporal Modeling for Anomaly Detection in Cloud Services", arXiv preprint arXiv:2508.14503, 2025.

- Zhang R., "AI-Driven Multi-Agent Scheduling and Service Quality Optimization in Microservice Systems", Transactions on Computational and Scientific Methods, vol. 5, no. 8, 2025.

- Zhang R., Lian L., Qi Z., and Liu G., "Semantic and Structural Analysis of Implicit Biases in Large Language Models: An Interpretable Approach", arXiv preprint arXiv:2508.06155, 2025.

- Xing Y., Yang T., Qi Y., Wei M., Cheng Y., and Xin H., "Structured Memory Mechanisms for Stable Context Representation in Large Language Models", arXiv preprint arXiv:2505.22921, 2025.

- Zheng H., Zhu L., Cui W., Pan R., Yan X., and Xing Y., "Selective Knowledge Injection via Adapter Modules in Large-Scale Language Models", 2025.

- Zhang W., Tian Y., Meng X., Wang M., and Du J., "Knowledge Graph-Infused Fine-Tuning for Structured Reasoning in Large Language Models", arXiv preprint arXiv:2508.14427, 2025.

- Ghaleb F. A., Saeed F., Al-Sarem M., et al., "Ensemble synthesized minority oversampling-based generative adversarial networks and random forest algorithm for credit card fraud detection", IEEE Access, vol. 11, pp. 89694-89710, 2023.

- Du X., "Financial text analysis using 1D-CNN: Risk classification and auditing support", Proceedings of the 2025 International Conference on Artificial Intelligence and Computational Intelligence, pp. 515-520, 2025.

- Tang T., Yao J., Wang Y., Sha Q., Feng H., and Xu Z., "Application of Deep Generative Models for Anomaly Detection in Complex Financial Transactions", Proceedings of the 2025 4th International Conference on Artificial Intelligence, Internet and Digital Economy (ICAID), pp. 133-137, 2025.

- Bao Q., "Advancing Corporate Financial Forecasting: The Role of LSTM and AI in Modern Accounting", Transactions on Computational and Scientific Methods, vol. 4, no. 6, 2024.

- Wu Y., Qin Y., Su X., and Lin Y., "Transformer-based risk monitoring for anti-money laundering with transaction graph integration", 2025.

- Qin Y., "Deep contextual risk classification in financial policy documents using transformer architecture", Journal of Computer Technology and Software, vol. 3, no. 8, 2024.

- Wang Y., Xu Z., Yao Y., Liu J., and Lin J., "Leveraging Convolutional Neural Network-Transformer Synergy for Predictive Modeling in Risk-Based Applications", Proceedings of the 2024 4th International Conference on Electronic Information Engineering and Computer Communication (EIECC), pp. 1565-1570, 2024.

- Wang Y., Sha Q., Feng H., and Bao Q., "Target-Oriented Causal Representation Learning for Robust Cross-Market Return Prediction", Journal of Computer Science and Software Applications, vol. 5, no. 5, 2025.

- Sheng Y., "Market Return Prediction via Variational Causal Representation Learning", Journal of Computer Technology and Software, vol. 3, no. 8, 2024.

- Xu Z., Sheng Y., Bao Q., Du X., Guo X., and Liu Z., "BERT-Based Automatic Audit Report Generation and Compliance Analysis", Proceedings of the 2025 5th International Conference on Artificial Intelligence and Industrial Technology Applications (AIITA), pp. 1233-1237, 2025.

- Ning X., Tian W., Yu Z., et al., "HCFNN: high-order coverage function neural network for image classification", Pattern Recognition, vol. 131, p. 108873, 2022.

- Du X., "Optimized convolutional neural network for intelligent financial statement anomaly detection", Journal of Computer Technology and Software, vol. 3, no. 9, 2024.

- Xue Z., Zi Y., Qi N., Gong M., and Zou Y., "Multi-Level Service Performance Forecasting via Spatiotemporal Graph Neural Networks", arXiv preprint arXiv:2508.07122, 2025.

- Wang M., Kang T., Dai L., Yang H., Du J., and Liu C., "Scalable Multi-Party Collaborative Data Mining Based on Federated Learning", 2025.

- Qin Y., "Hierarchical Semantic-Structural Encoding for Compliance Risk Detection with LLMs", Transactions on Computational and Scientific Methods, vol. 4, no. 6, 2024.

- Xu Q. R., "Capturing Structural Evolution in Financial Markets with Graph Neural Time Series Models", 2025.

- Zi Y., Gong M., Xue Z., Zou Y., Qi N., and Deng Y., "Graph Neural Network and Transformer Integration for Unsupervised System Anomaly Discovery", arXiv preprint arXiv:2508.09401, 2025.

- Yang H., Wang M., Dai L., Wu Y., and Du J., "Federated Graph Neural Networks for Heterogeneous Graphs with Data Privacy and Structural Consistency", 2025.

- Su X., "Deep Forecasting of Stock Prices via Granularity-Aware Attention Networks", Journal of Computer Technology and Software, vol. 3, no. 7, 2024.

- Yu C., Xu Y., Cao J., et al., "Credit card fraud detection using advanced transformer model", Proceedings of the 2024 IEEE International Conference on Metaverse Computing, Networking, and Applications (MetaCom), pp. 343-350, 2024.

- McDermott M., Zhang H., Hansen L., et al., "A closer look at auroc and auprc under class imbalance", Advances in Neural Information Processing Systems, vol. 37, pp. 44102-44163, 2024.

- Zhu M., Zhang Y., Gong Y., et al., "Enhancing credit card fraud detection: a neural network and smote integrated approach", arXiv preprint arXiv:2405.00026, 2024.

- Li F., Chen Z., "Dynamic quantification anti-fraud machine learning model for real-time transaction fraud detection in banking", Discover Computing, vol. 28, no. 1, p. 59, 2025.

Figure 1.

KAN-based Financial Risk Discrimination Architecture.

Figure 2.

Sensitivity of risk identification to KAN depth.

Figure 3.

The impact of learning rate changes on KAN convergence speed and performance.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.