Submitted:

07 August 2025

Posted:

07 August 2025

You are already at the latest version

Abstract

This study investigates the role of Greek chartered accountants in implementing ESG criteria, crucial as businesses prioritize sustainability. Chartered accountants, responsible for accurate ESG reporting, face challenges due to inconsistent reporting standards, complicating cross-company comparisons. This research seeks to understand accountants’ knowledge of ESG implementation, perceptions of its effectiveness, and the challenges faced. A quantitave cross-sectional survey was conducted with 100 charted accountants, utilizing a structured questionnaire with SPSS software for data analysis. Independent t-tests and one-way ANOVA examined the influence of factors like experience and training on ESG related views. The results show moderate ESG adoption, with higher implementation in data security and lower indirect emissions. Accountants with ESG training are more supportive of comprehensive ESG practices, recognizing benefits such us enhanced client trust, competitive advantage, and risk mitigation. Findings underscore the need for standardized ESG frameworks and ongoing training to support effective ESG integration in Greek corporate governance.

Keywords:

chartered accountants

; ESG

; accounting

; auditing

1. Introduction

The global business environment is increasingly recognizing the importance of integrating Environmental, Social, and Governance (ESG) factors into corporate decision-making and reporting processes [1]. Chartered accountants, as key figures in corporate governance and financial reporting, play a crucial role in ensuring the accuracy, completeness, and transparency of ESG-related data [2,3]. However, they face numerous challenges in fulfilling this responsibility, highlighting the need for continuous professional development and awareness of emerging trends and best practices in ESG reporting.

One of the main challenges is the absence of a uniform set of ESG reporting standards. While several frameworks, such as the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), and the Task Force on Climate-related Financial Disclosures (TCFD), provide guidance, the lack of universally accepted standards creates difficulties in comparing and evaluating ESG reports across companies [1,4,5]. This inconsistency forces auditors to navigate multiple frameworks and determine which are most relevant based on industry-specific and regional considerations[6,7,8].

Moreover, assessing and verifying ESG data pose additional challenges the reliability and accuracy of ESG information are essential for credible corporate reporting [9,10,11]. Chartered accountants must be equipped with the skills and tools to identify and rectify inaccurate or misleading data, while also keeping up with evolving methods for assessing the environmental and social impacts of corporate activities [12].

Ethical concerns also play a significant role in ESG reporting [13,14,15]. Chartered accountants must remain mindful of the ethical implications of ESG assessments, particularly regarding transparency, employee treatment, and environmental responsibility. Their ability to assess and verify the credibility of ESG disclosures is vital to maintaining the trust of investors and the public [12,16].

Furthermore, the rapidly changing nature of ESG criteria, coupled with involving regulatory requirements, demands that auditors stay agile and responsive to new developments. Continuous training in ESG practices has become increasingly important, as ESG assessment is now a fundamental aspect of corporate transparency and reporting [1].

Given these challenges, chartered accountants are positioned to play a central role in integrating ESG factors into corporate reporting. By adopting best practices and remaining informed about current developments, they can contribute significantly to the successful implementation of ESG strategies and promote more sustainable and responsible business practices [17].

Despite the growing recognition of the importance of embedding ESG into business models and corporate cultures, accountants face multifaceted challenges. The lack of standardized reporting frameworks complicates their tasks, leading to potential ambiguities in assessing ESG factors for individual organizations. Addressing these challenges through thoughtful strategies can enable companies to integrate ESG principles effectively while navigating the complexities of corporate reporting.

In light of the above, this research aims to address the following research questions:

RQ1: What level of knowledge do chartered accountants possess about ESG criteria?

RQ2: To what extent are ESG criteria implemented in practice by chartered accountants?

RQ3: What are the perceptions of chartered accountants regarding the effectiveness of ESG criteria?

RQ4: What do chartered accountants perceive as the main challenges to ESG implementation?

The structure of this paper is as follows: Section 2 defines the concept of ESG and discusses the challenges faced by chartered accountants in its application. Section 3 outlines the methodology employed in this study. Section 4 presents the results, visualized using SPSS software. Section 5 discusses the findings and proposes directions for future research, while Section 6 offers concluding remarks.

2. Literature Review

Corporate reputation is widely regarded as one of the most critical intangible assets for businesses, influencing not only customer perceptions but also relationships with suppliers and other stakeholders. A company’s reputation is inherently linked to its transparency, social responsibility, and the quality of its products and services. Existing research emphasizes that maintaining a positive reputation requires continuous efforts aimed at building customer trust and satisfaction [18,19,20].

Strategic risk management plays a crucial role in protecting corporate reputation, as firms must navigate unpredictable threats that could undermine their image. Through systematic risk assessment, companies can adapt to changing conditions and mitigate potential reputational damage [21].

The integration of ESG principles has shown significant benefits for businesses [22,23]. Studies indicate that companies investing in sustainable practices not only enhance their competitiveness and productivity but also gain access to emerging markets and strengthen relationships with investors [24,25]. Sustainability is increasingly seen as a key driver of innovation, prompting firms to develop new products and services that meet the rising demand for environmentally and socially responsible options.

Adopting ESG principle can significantly improve a company’s reputation by demonstrating a commitment to ethical practices, social responsibility, and environmental stewardship [26,27]. This commitment fosters trust among stakeholders, including customers, investors, and employees, thereby strengthening the company's market position. For instance, integrating ESG considerations into human resource management can enhance entrepreneurial effectiveness by aligning organizational practices with broader societal values [28].

Additionally, adopting ESG principles can lead to improved economic efficiency through initiatives such as resource recycling and cost reduction. Companies implementing these strategies can achieve cost savings while building consumer and investor trust, thus creating a strong competitive advantage [29,30,31].

However, the relationship between environmental practices and economic performance is not always straightforward. While long-term benefits often accrue from environmental investments, short-term impacts can be more complex [32,33]. Nevertheless, addressing global challenges such as climate change and pollution has become essential for sustainable development. Key industries such as energy, manufacturing, and transportation are critical areas for emission reduction, facilitating the shift towards more sustainable business models [34] .

Incorporating ESG factors into risk management strategies enables companies to identify and mitigate potential risks related to environmental impact, social responsibility, and governance issues. This proactive approach not only safeguards the company's reputation but also contributes to financial performance by attracting investors who prioritize sustainable practices. A strategic roadmap for ESG in construction risk management illustrates how integrating ESG considerations can lead to long-term value creation and environmental protection [35,36].

The social dimension of sustainable development encompasses issues of social equity, justice, and community engagement. Collaboration among governments, businesses, and communities is essential for promoting social cohesion and addressing inequalities [37,38]. Sustainable business practices not only serve economic objectives but also contribute to improving the quality of life for individuals impacted by corporate activities.

The intersection of ESG principles and digital transformation presents new opportunities for companies to innovate and enhance their sustainability efforts. Digital technologies can facilitate the implementation of ESG strategies by providing tools for better data collection, analysis, and reporting, thereby improving transparency and accountability. A study on the impact of digital transformation in SMEs highlights how embracing digital technologies can support sustainable practices and operational efficiency [39,40].

The field of sustainability accounting has experienced significant growth, as more companies recognize the need to integrate ESG principles into their operations. This trend has increased demand for accounting professionals who are knowledgeable about sustainability reporting standards, such as the GRI, SASB, and TCFD [41,42]. Educational institutions are also adapting their curricula to equip future accountants with the necessary skills to meet these challenges.

However, the integration of ESG principles into accounting education faces challenges, particularly in the areas of practical training and the ethical considerations of transparent reporting. Accountants are increasingly encountering ethical dilemmas, especially in an international context where cultural norms and ethical standards vary widely [43]. It is essential to provide education that addresses the ethical dimensions of ESG accounting to prepare future professionals to apply these principles responsibly and promote sustainability within organizations [44,45].

In conclusion, incorporating ESG criteria into business strategy and accounting education is not merely a passing trend but a vital approach for promoting long-term sustainable growth and enhancing social and environmental value. This research aims to explore the perspectives of chartered accountants on the application of ESG criteria within the Greek business context [46].

3. Materials and Methods

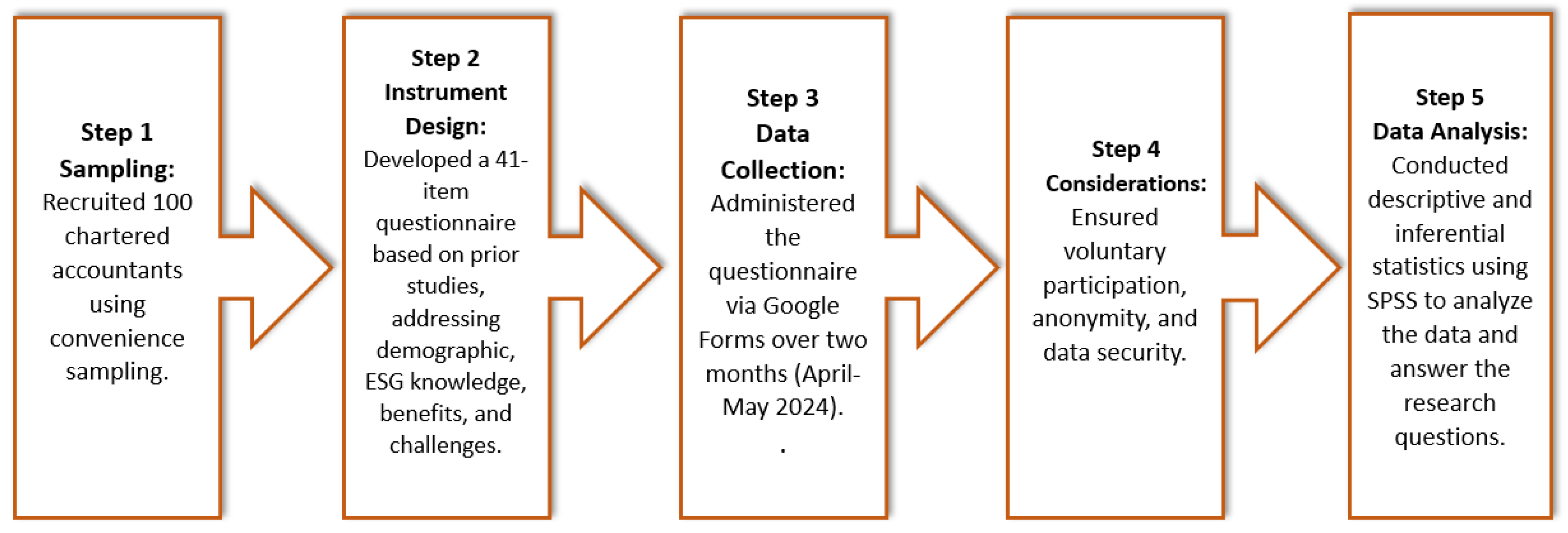

This study investigates the perspectives of chartered accountants in Greece regarding the application of ESG criteria. A quantitative, cross-sectional survey design was adopted to ensure a systematic and efficient approach to data collection from a substantial and representative sample. The research utilized a structured questionnaire as the primary data collection instrument, which was carefully designed to align with the study’s objectives and informed by relevant academic literature [47,48,49].

The questionnaire consisted of 41 items and was structured to comprehensively address the research objectives. It included questions that collected demographic information, alongside items that assessed participants’ knowledge of ESG principles, their application of these criteria, and their perceptions of the benefits and challenges associated with ESG implementation. A variety of question formats, including closed-ended, open-ended, and Likert-scale items, were incorporated to enable a nuanced exploration of the topic.

Participants were fully briefed on the purpose of the study and informed that the research was conducted as part of an academic investigation. Ethical considerations were rigorously observed throughout the process. Participation was entirely voluntary, and all responses were collected anonymously and treated with strict confidentiality. Participants were also informed that their data would be securely stored for one year and subsequently deleted, in accordance with data protection regulations. Constant information was provided to ensure transparency and address any inquires, reinforcing trust and accessibility through the study.

Data analysis was performed using SPSS software and consisted of two main stages. The first stage involved descriptive statistical analyses, including the calculation of frequencies, means, and standard deviations, to summarize participant responses. The second stage employed inferential statistical methods to examine relationships and differences within the data. Specifically, independent t-tests were conducted to assess the relationships between binary categorical variables and continuous dependent variables[50,51]. Additionally, one-way ANOVA was applied to investigate associations between multi-level categorical variables and continuous outcomes. These statistical techniques were selected for their robustness and ability to detect significant group differences and correlations, thereby ensuring the reliability of the findings. The methodological steps are summarized in the following table.

Table 1.

Summarized methodological steps.

4. Results

4.1. Implementation of Key ESG Factors

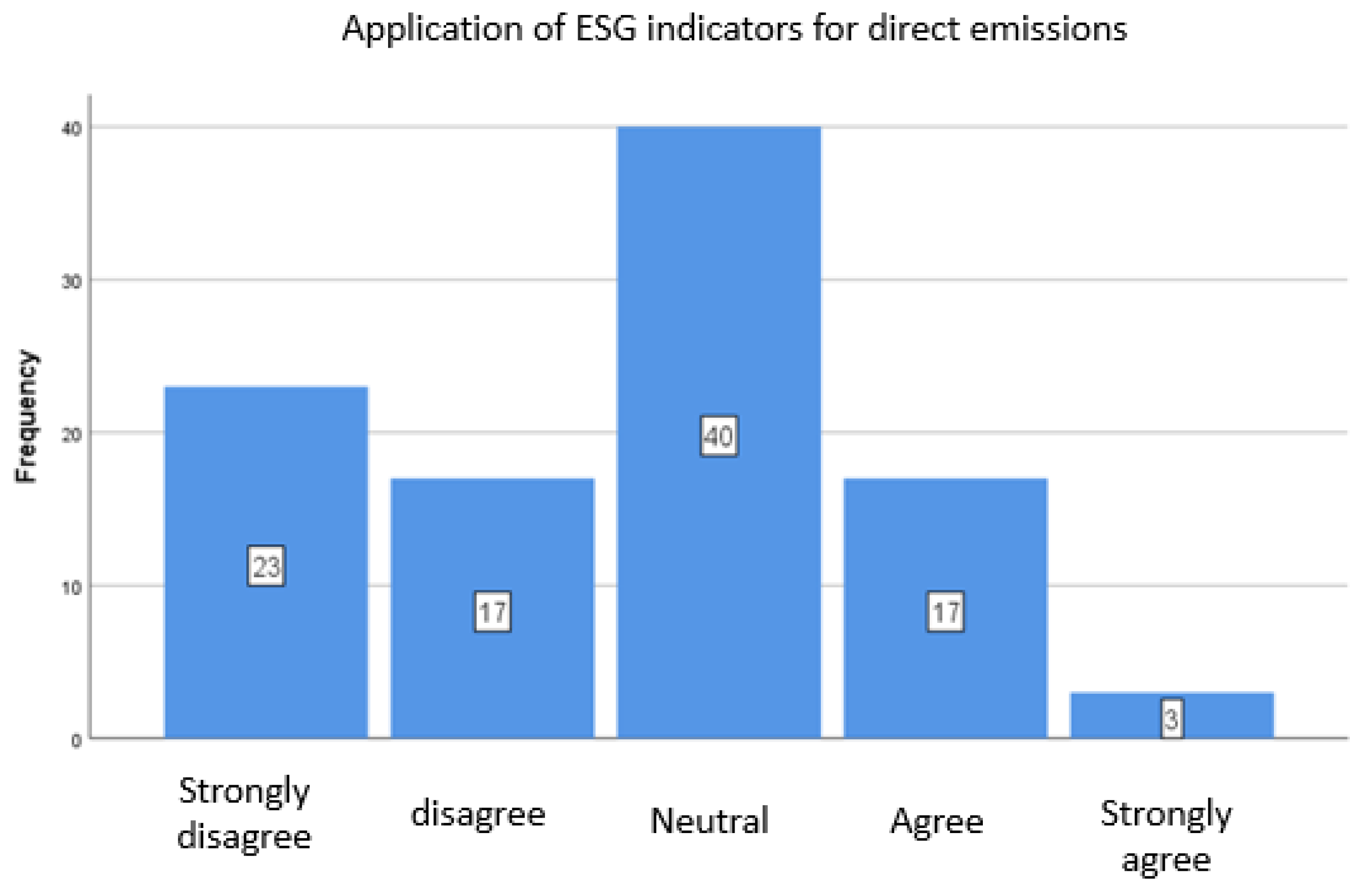

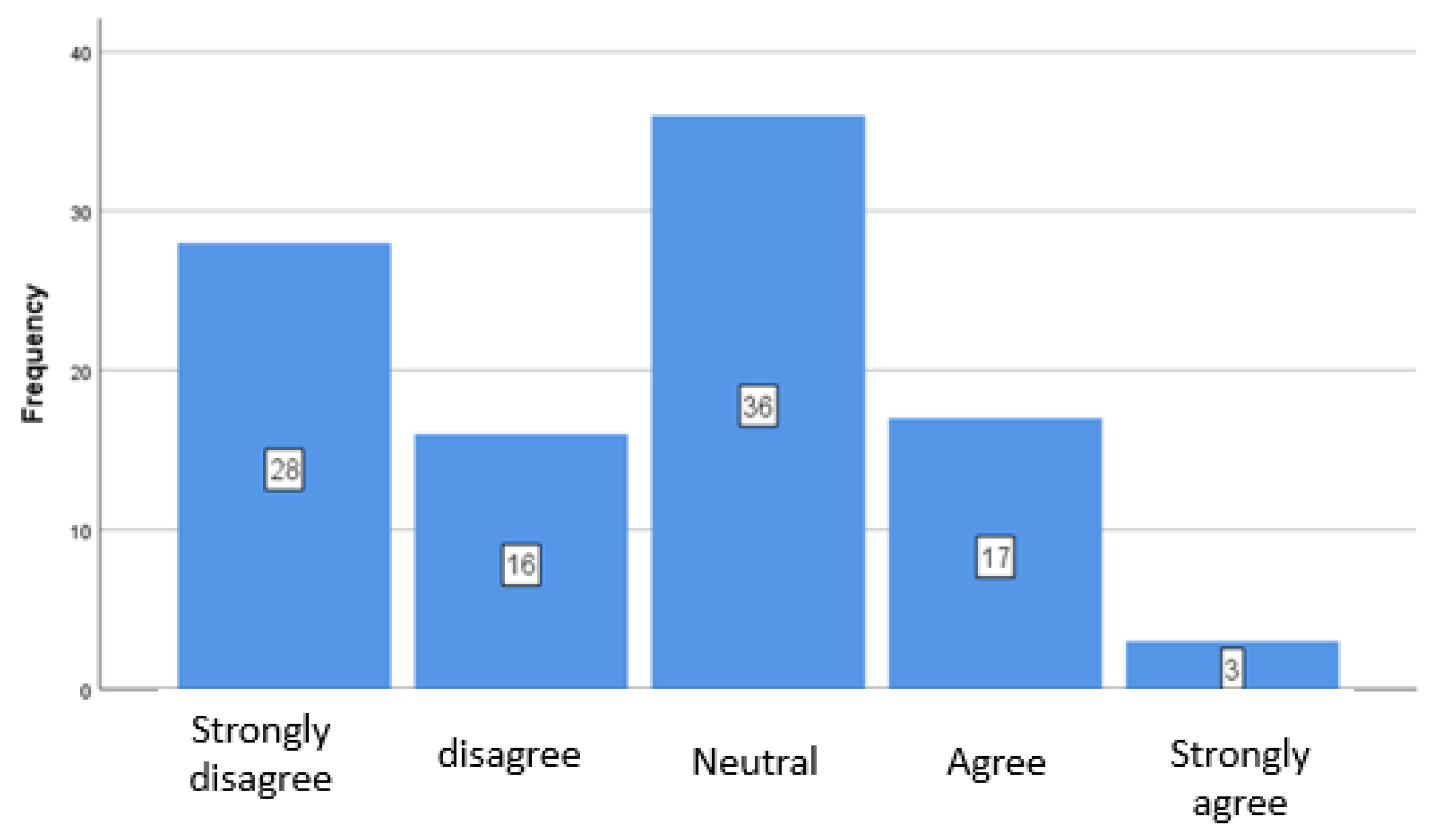

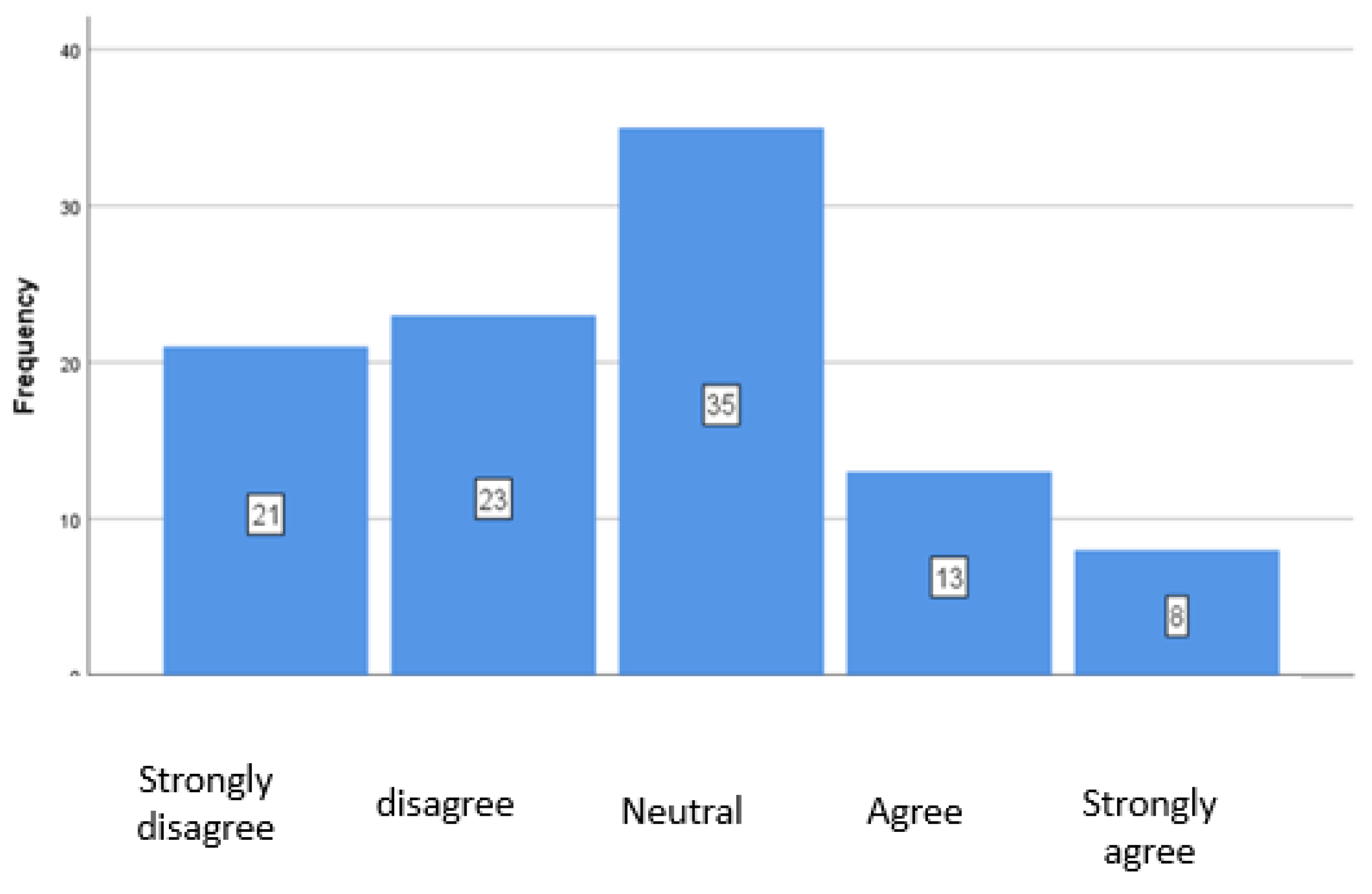

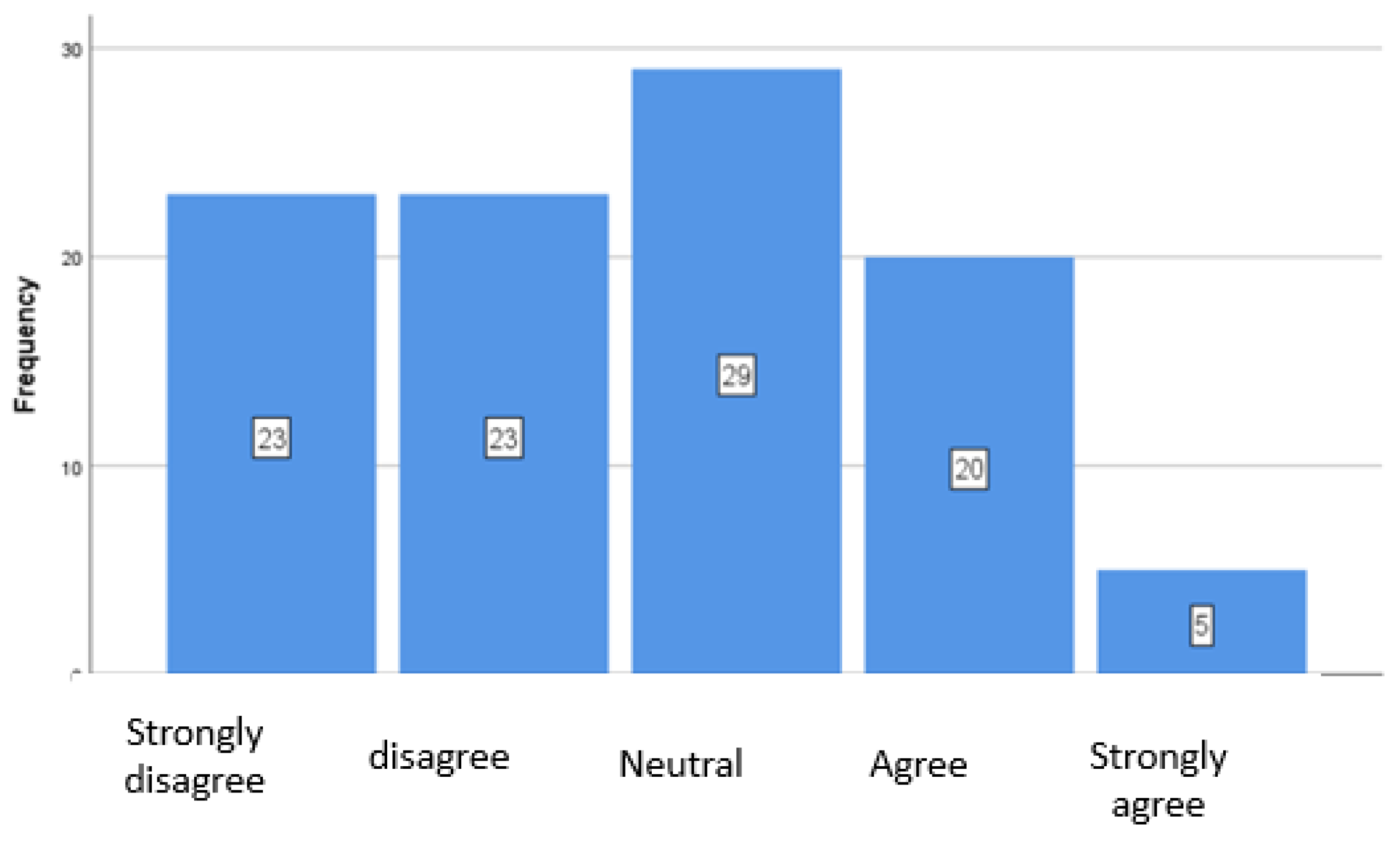

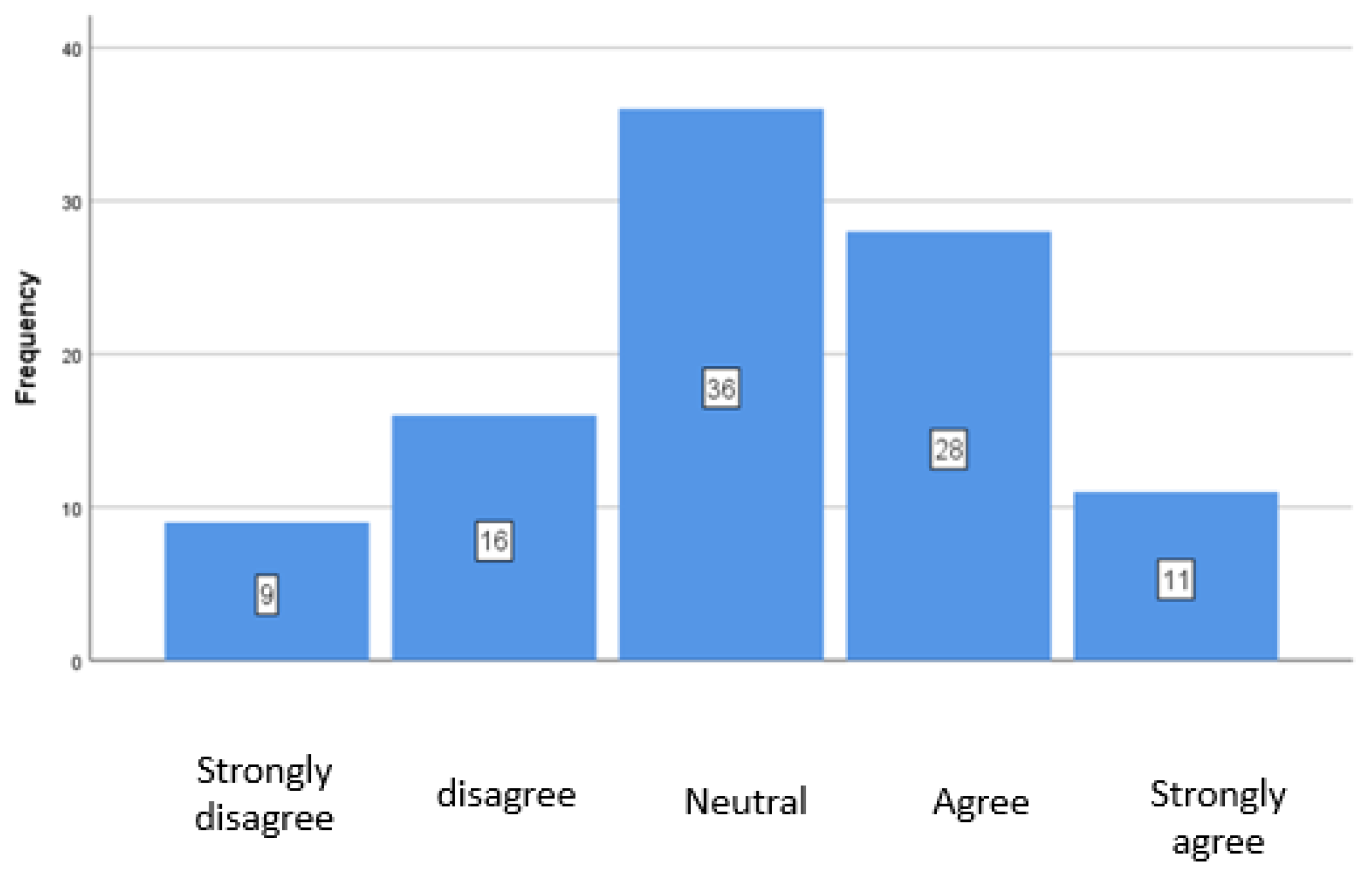

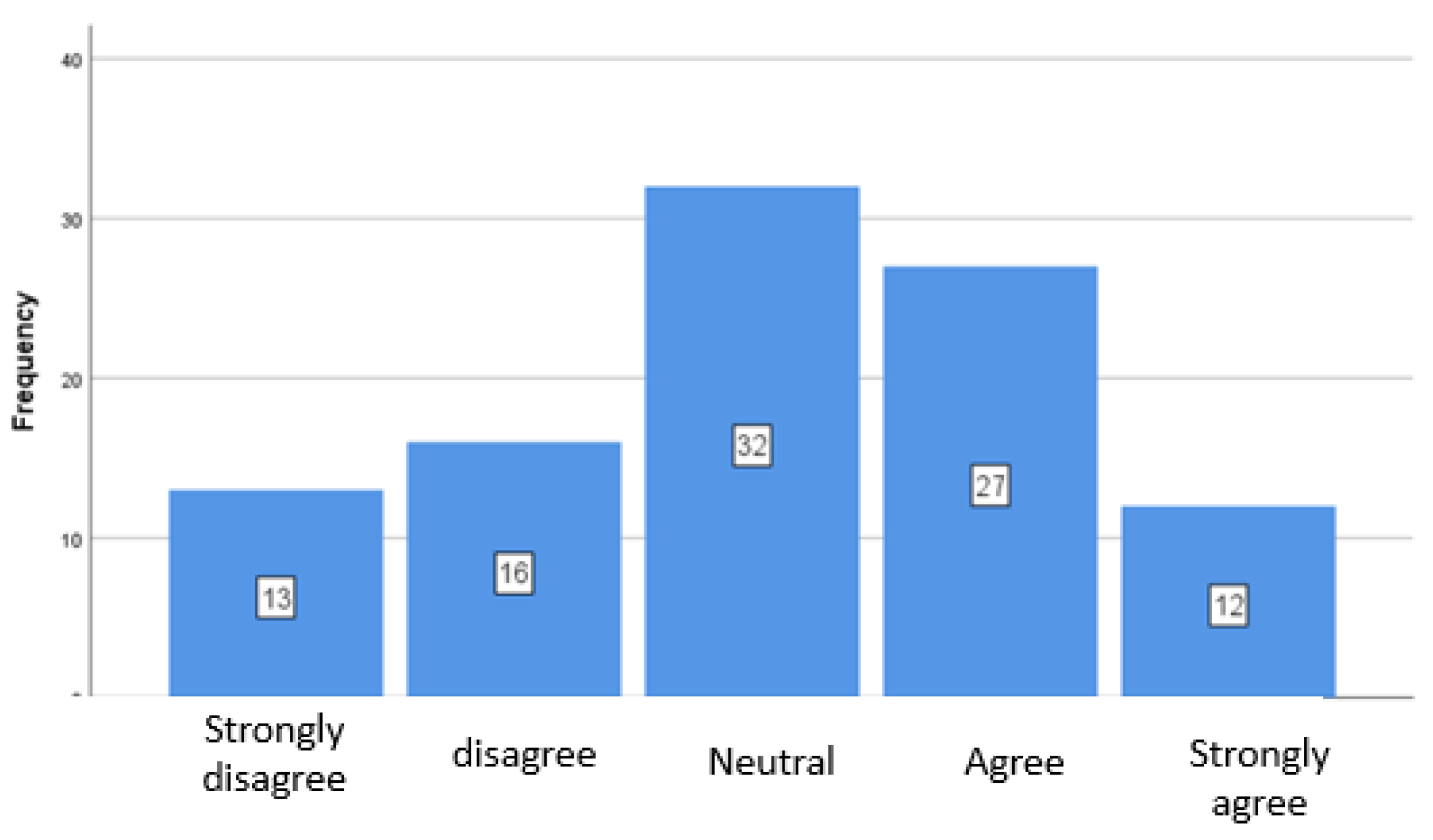

Regarding the implementation of key ESG indicators by companies where the chartered accountants were employed or which they audited, 40% of respondents (n = 40) reported a moderate application of ESG criteria concerning direct emissions (Figure 1), while 36% (n = 36) indicated a moderate application for indirect emissions. Interestingly, 28% (n = 28) noted that ESG criteria for indirect emissions were not applied at all (Figure 2). Similar trends were identified for energy consumption and production (Figure 3), while responses diverged on stakeholder engagement (Figure 4). A one-way ANOVA was performed to examine potential differences in opinions based on years of service, but no statistically significant correlations were found, as the significance values (sig) for all tests exceeded the threshold of 0.05.

4.2. Influence on ESG Training on Options

To determine if ESG training influenced options, independent t-tests were conducted. Statistically, significant differences emerged across several areas. Chartered accountants with ESG training demonstrated a higher level of understanding of ESG criteria (p = .000) and expressed stronger support for the application of ESG indicators in direct emissions (p = .000), indirect emissions (p = .000), energy consumption and production (p = .000), and stakeholder engagement (p = .000). Additionally, those with ESG training showed stronger endorsement for the application of ESG criteria related to female employees (p = .000), women in managerial positions (p = .000), staff mobility (p = .000), employee training (p = .000), human rights policies (p = .000), collective bargaining agreements (p = .000), supplier evaluation (p = .000), board composition (p = .000), and business ethics policies (p = .000).

Moreover, trained accountants expressed stronger beliefs in the effectiveness of ESG criteria for attracting new clients (p = .000), gaining competitive advantage (p = .000), increasing revenue (p = .000), enhancing firm credibility (p = .000), mitigating risk (p = .000), attracting new investors (p = .000), and improving productivity and adaptability to technological, customer, and regulatory changes (p = .000). Those with ESG training also highlighted more significant challenges to ESG implementation, including climate change (p = .000), human resource management (p = .000), corruption and bribery (p = .000), and the absence of standardized evaluation guidelines or regulatory oversight (p = .000) (Table 1_Appendix).

4.3. ESG Criteria in Specific Practices

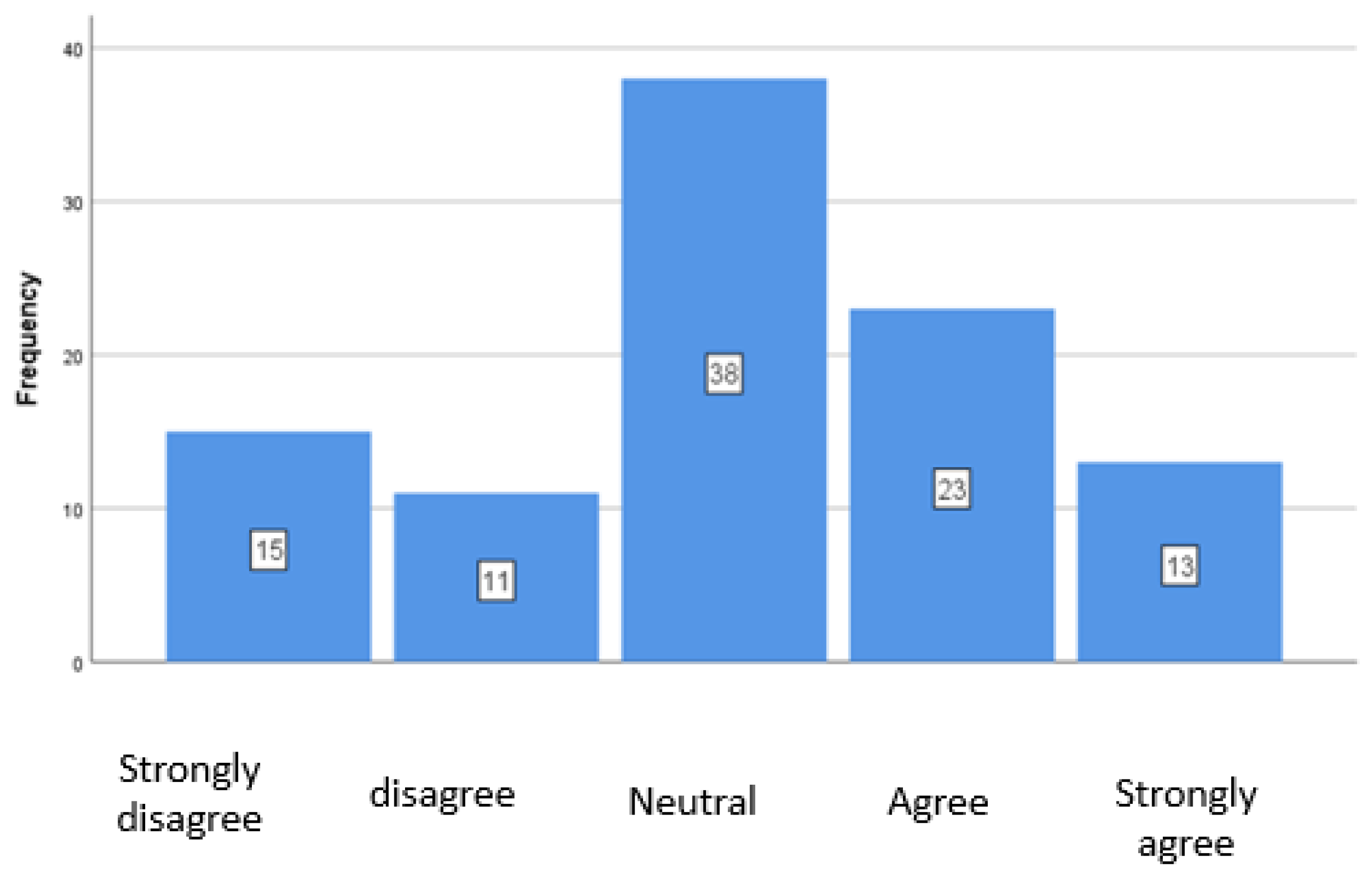

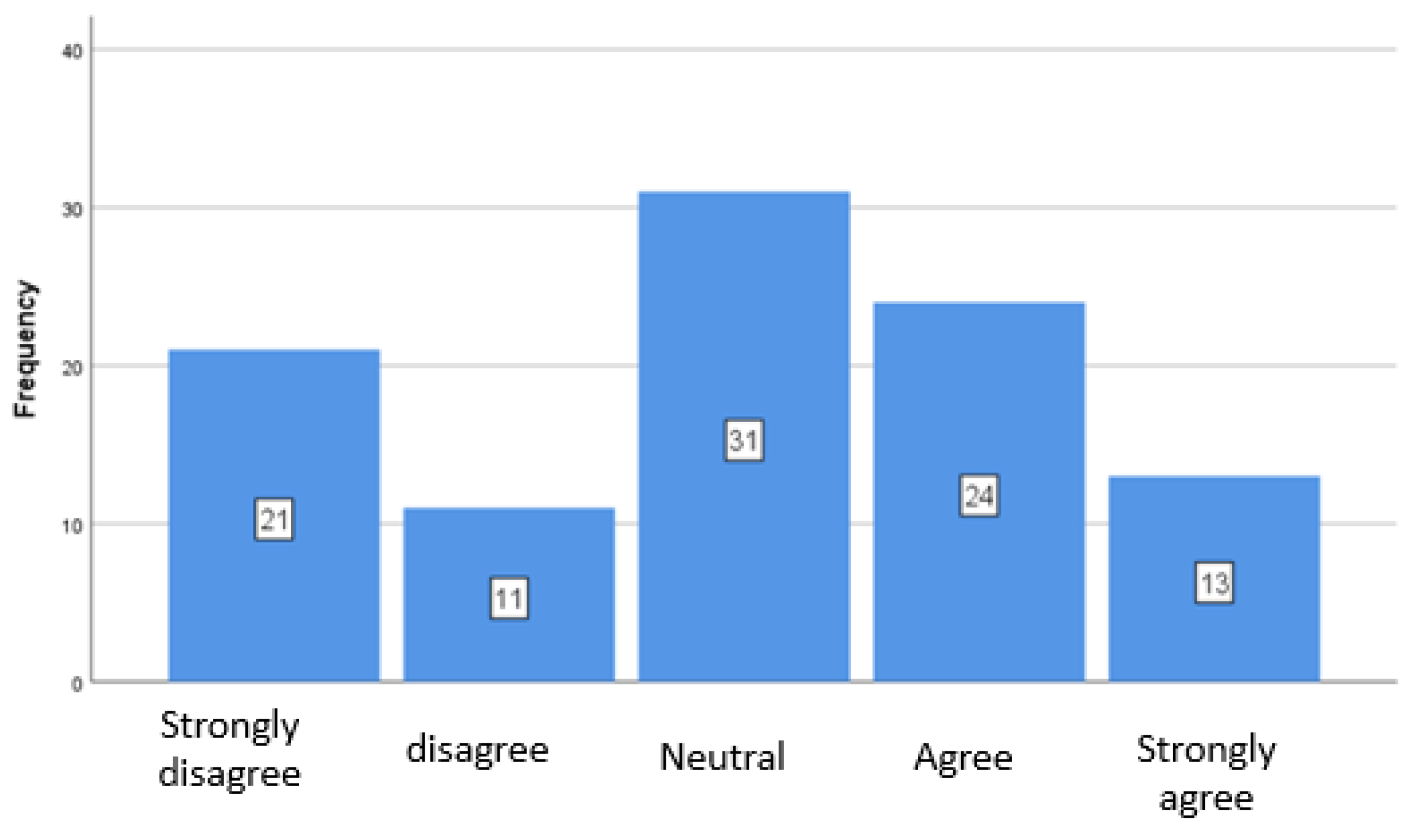

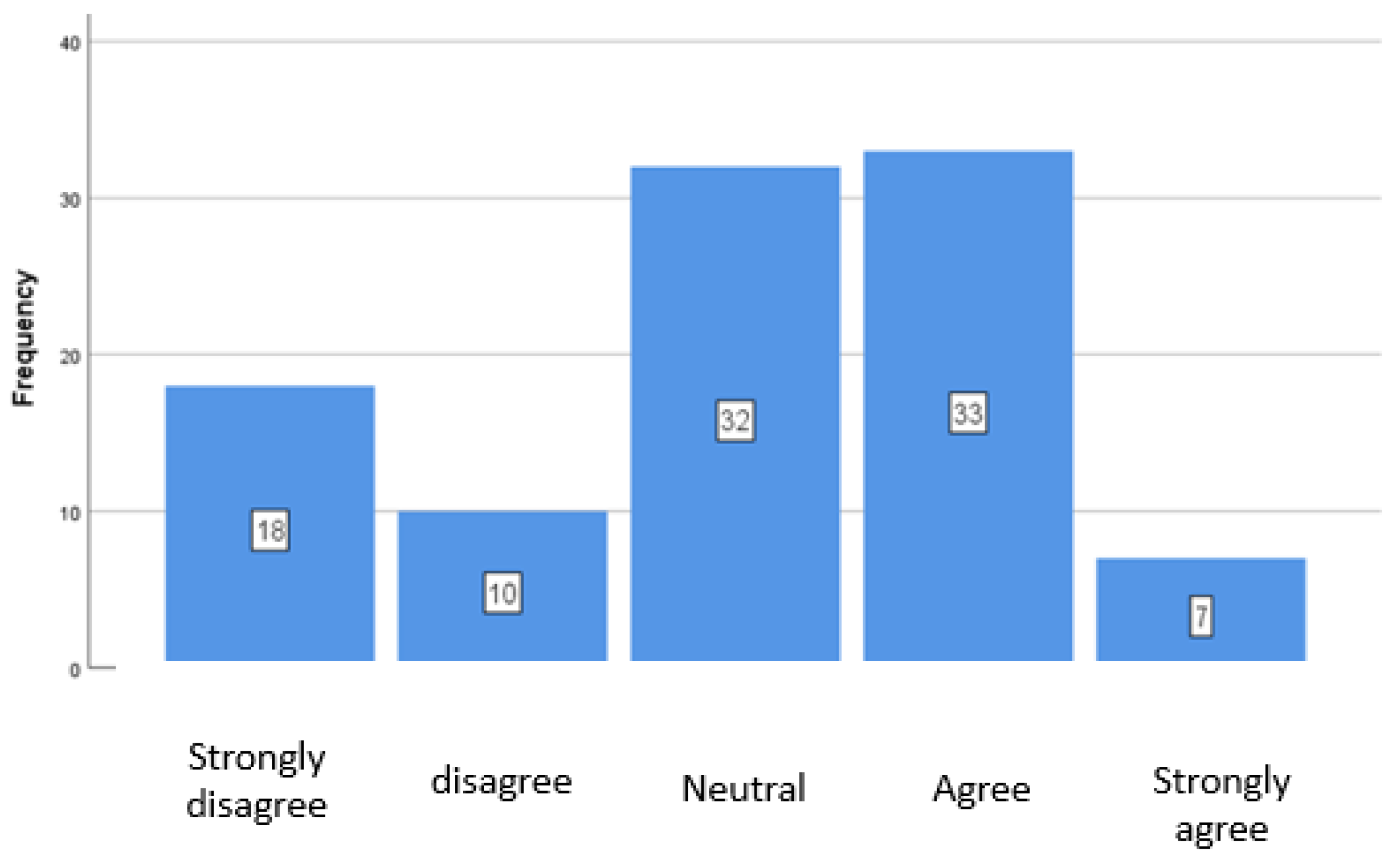

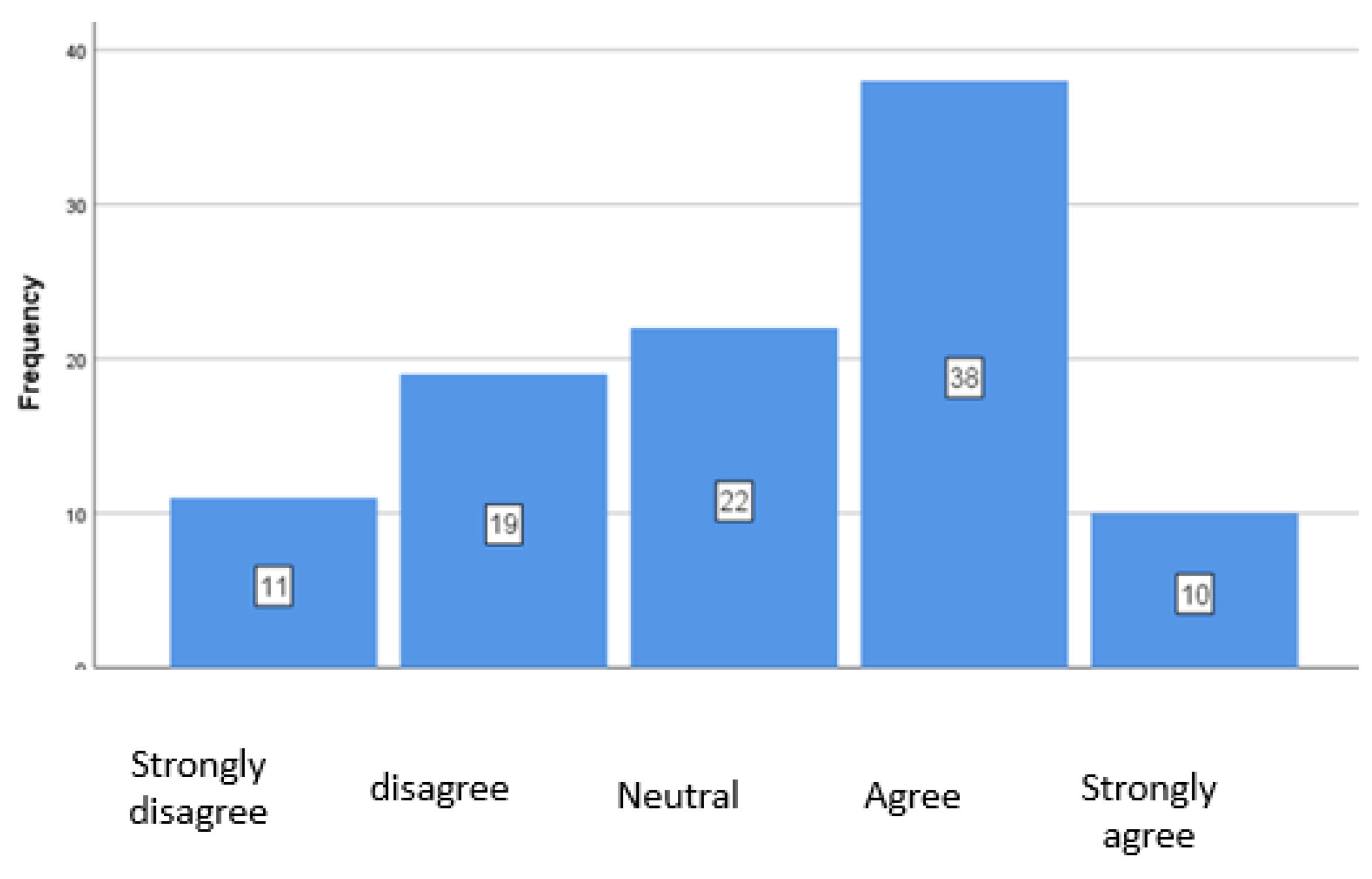

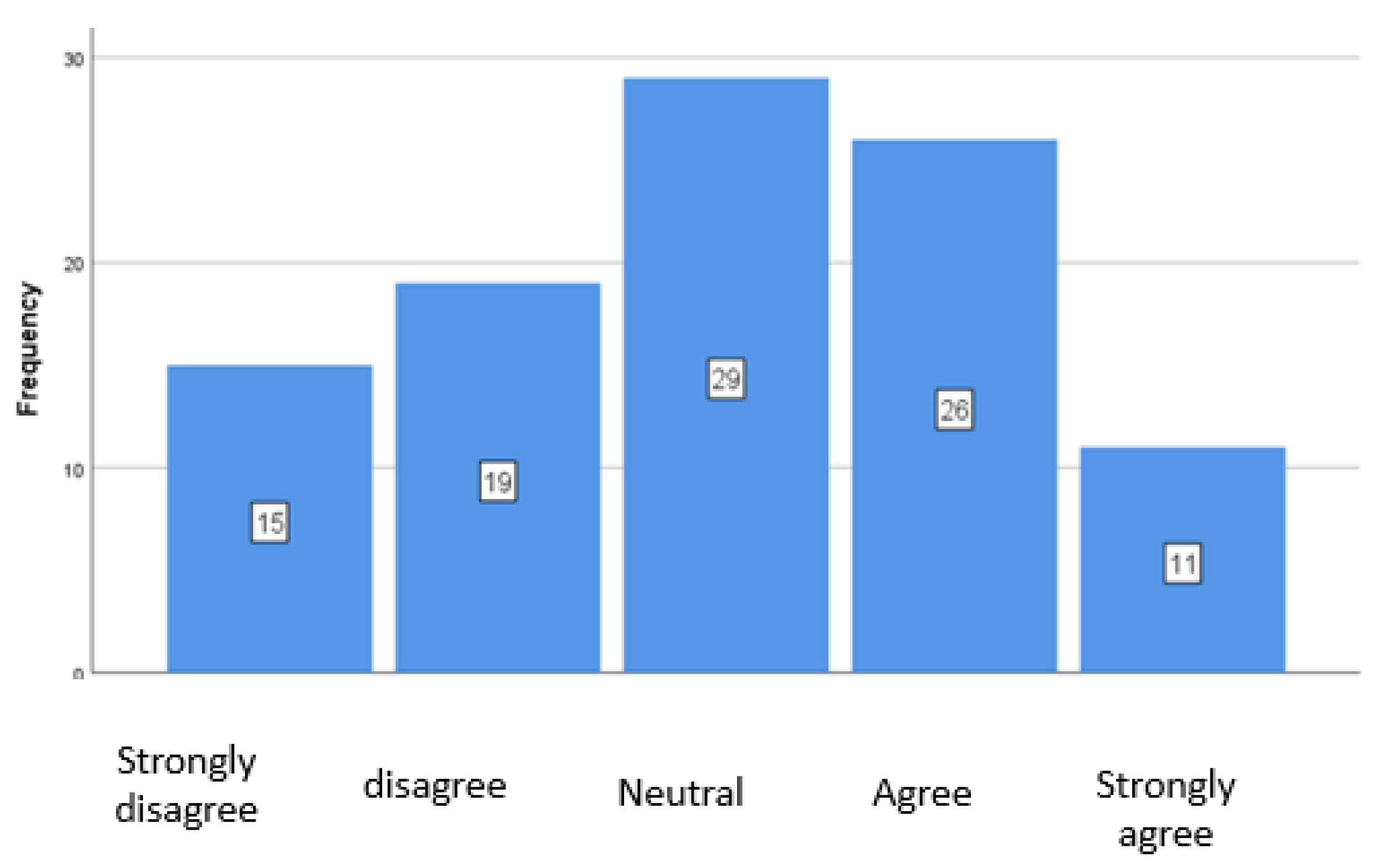

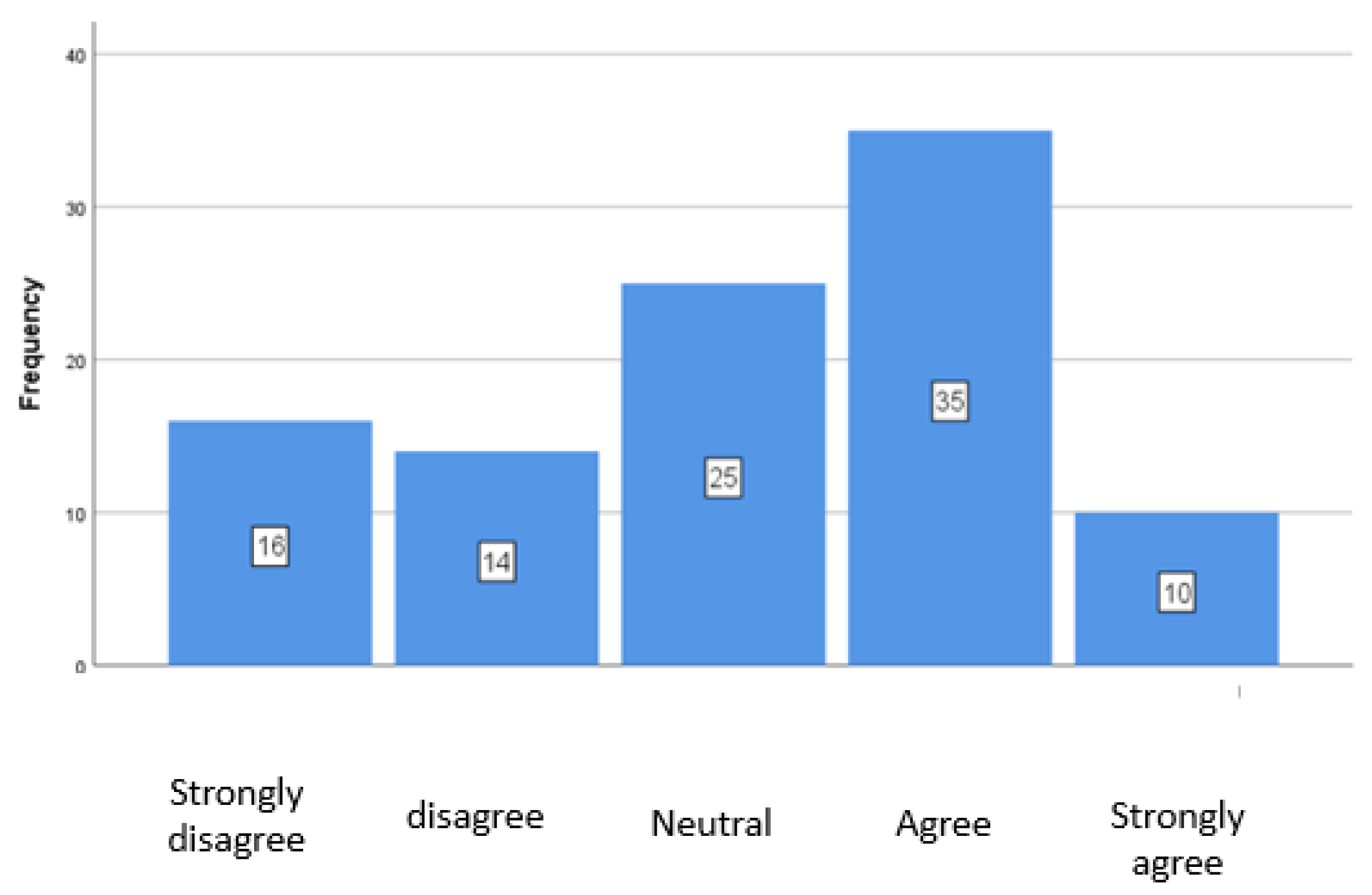

There were variations in the responses regarding specific ESG criteria. For example, 38% (n = 38) of respondents reported a moderate number of female employees in their organizations (Figure 5), while 31% (n = 31) indicated moderate representation of women in managerial positions (Figure 6). Interestingly, 33% (n = 33) noted that ESG criteria related to staff mobility were strongly enforced (Figure 13), and 36% (n = 36) reported moderate application of ESG criteria for employee training (Figure 7). However, there were conflicting views on collective labor agreements (Figure 8) and supplier evaluation (Figure 9), with 32% (n = 32) noting moderate application of ESG criteria for board composition (Figure 10).

In general, ESG criteria were moderately applied, with lower implementation rates for indirect emissions (M = 2.51, SD = 1.159) and higher implementation for data security policies (M = 3.30, SD = 1.168) (Table 2).

Conflict opinions were observed on the application of ESG criteria for collective labor agreements (Figure 10) and supplier evaluation (Figure 11). Additionally, 32% (n = 32) of respondents stated that ESG criteria for board composition were moderately applied (Figure 12). Similarly, the implementation of ESG criteria for sustainable development monitoring, substantive issues, sustainability policy, business ethics policy, and data security policy followed the same pattern.

In conclusion, while ESG indicators were generally implemented to a moderate degree, indirect emissions (M = 2.51, SD = 1.159) showed lower implementation, while data security policies (M = 3.30, SD = 1.168) were applied more extensively. (Table 2_Appendix).

4.4. Age Based Correlations

To examine the influence of the age on the opinions of chartered accountants regarding ESG (Environmental, Social, and Governance) implementation, a one-way ANOVA analysis was conducted. The results indicated several statistically significant correlations. Younger accountants exhibited greater support for ESG initiatives, particularly in areas such as gender diversity (female employees) (p = .039), employee mobility (p = .011), employee training programs (p = .043), business ethics policies (p = .017), and data security policies (p = .003). Moreover, younger accountants perceived ESG criteria as being more effective for attracting new clients (p = .001), gaining a competitive edge (p = .002), increasing revenue (p = .000), enhancing the organization's credibility (p = .000), reducing business risks (p = .019), and improving opportunities for growth and adaptability to change (p = .000). They also identified greater challenges associated with ESG implementation, such as climate change (p = .002), corruption and bribery (p = .000), and a lack of transparency in evaluation processes (p = .001) (refer to Table 6).

4.5. Educational Level – Based Correlations

A similar one – way ANOVA analysis was conducted to explore how opinions varied based on educational attainment[52,53]. The findings revealed that respondents with higher levels of education demonstrated better knowledge of ESG criteria (p = .000) and stronger support for the application of key ESG indicators across multiple domains. These domains included direct and indirect emissions, energy consumption, stakeholder participation, and sustainability policies, with most cases showing a p-value of .000. Furthermore, chartered accountants with higher education levels believed that ESG indicators were more effective in attracting new clients, enhancing competitive advantage, increasing firm credibility, reducing risks, and improving adaptability to evolving business conditions (p = .000). This group also viewed challenges, such as climate change, human resource management, and the absence of standardized evaluation oversight, as more significant (refer to Table 7).

4.6. Training on ESG Assessment

The impact of ESG assessment training on accountants’ opinions was also evaluated using independent t-tests. Several statistically significant correlations were found. Chartered accountants who had received training on the proper assessment of ESG indicators exhibited a deeper knowledge of ESG criteria (p = .000) and were more supportive of applying ESG indicators in various areas. These areas included direct and indirect emissions (p = .000), energy consumption and production (p = .000), stakeholder engagement (p = .000), female representation in the workforce and managerial roles (p = .000), employee mobility (p = .000), employee training (p = .000), human rights policies (p = .000), collective agreements (p = .000), supplier evaluation (p = .000), board composition (p = .000), sustainable development oversight (p = .000), substantive issues (p = .000), sustainability policies (p = .000), business ethics policies (p = .000), and data security policies (p = .000).

Additionally, chartered accountants with ESG training were more likely to perceive ESG criteria as effective in attracting new clients (p = .000), gaining a competitive advantage (p = .000), increasing revenue (p = .000), enhancing firm credibility (p = .000), reducing risks (p = .000), attracting new investors (p = .000), boosting productivity (p = .000), increasing growth opportunities (p = .000), and improving adaptability to technological, customer, and regulatory changes (p = .000). Furthermore, they were more likely to identify significant challenges in ESG implementation, including climate change (p = .000), human resource management (p = .000), corruption and bribery (p = .000), the lack of common evaluation guidelines (p = .000), the absence of evaluation oversight authorities (p = .000), a lack of transparency in evaluations (p = .000), and difficulties in regulatory compliance (p = .000) (refer to Table 9).

5. Discussion & Conclusions

The study examined the perspectives of chartered accountants of chartered accountants regarding the implementation of Environmental, Social, and Governance (ESG) criteria in Greece. The findings suggest that chartered accountants possess only a basic understanding of ESG, which is consistent with prior research, such as the study conducted by [54] This limited knowledge emphasizes the importance of enhancing education and professional training on ESG issues, a need similarly identified by [55]

With respect to ESG implementation, respondents reported a moderate degree of adoption, with the least progress made in the area of indirect emissions and the most progress observed in the implementation of data security policies. These results mirror global patterns, as identified by [45,56] , who highlighted that data governance is often more widely implemented due to regulatory pressures, whereas environmental metrics tend to lag behind.

Respondents, perceived ESG criteria as positively impacting key areas such as attracting new clients, gaining competitive advantage, and enhancing organizational credibility. Nonetheless, they also identified considerable challenges to ESG implementation, notably in addressing climate change and the lack of a formal oversight body for ESG assessments. Interestingly, issues related to corruption and bribery were viewed as moderate challenges, which stands in contrast to traditional governance concerns reported in the International Transparency (2019) report.

Additionally, the study found that younger accountants, as well as those with higher levels of education, were more likely to apply ESG criteria and acknowledge the challenges involved in their implementation. This aligns with the conclusions of Adams and [57], who emphasize the role of education in promoting a deeper understanding and effective application of ESG criteria, thereby contributing to a stronger commitment to sustainability.

Continuous professional development in ESG topics is therefore crucial. Integrating sustainability into the education of accountants can enhance their ability to apply ESG criteria effectively. In addition, the use of robust measurement tools for environmental indicators is recommended to support the improved implementation of ESG within professional practices.

Future research should consider cross-regional comparative studies to identify universal trends and explore contextual variations in ESG adoption. Understanding regional differences may guide the development of educational programs and regulatory frameworks tailored to the specific needs of diverse markets. Moreover, incorporating qualitative methods, such as interviews and focus groups, would offer deeper insights into the motivations and challenges behind ESG adoption. Investigating the direct link between ESG practices and financial performance in future research could also provide valuable insights into the business case for sustainability, which may encourage more widespread adoption of ESG measures.

Several limitations of the current study should be acknowledged. The results may not be fully generalizable due to the relatively small sample size, and the sample was predominantly male, limiting gender diversity. Additionally, the study relied on self-reported data, which may introduce response bias. Furthermore, the research focused on a limited set of ESG indicators, potentially overlooking other significant aspects of ESG that are relevant to the accounting profession. Important topics, such as biodiversity, water management, waste management, and specific social governance issues, were not comprehensively addressed in this study.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “Conceptualization, I.P. and E.A.; methodology, D.K.; software, E.A .; validation, I.P., S.G and E.A..; formal analysis, E.A.; investigation, D.K.; resources, R.M.; data curation, E.A and D.K.; writing—original draft preparation, I.P., R.M. and E.A.; writing—review and editing, I.P., E.A and S.G.; visualization, D.K.; supervision, I.P.; project administration, I.P.; funding acquisition, R.M. All authors have read and agreed to the published version of the manuscript.”

Appendix A

A.1.1. Application of Key ESG Indicators

| M | SD | |

| Application of key ESG indicators_Direct emissions | 2,60 | 1,110 |

| Application of key ESG indicators_Direct emissions | 2,51 | 1,159 |

| Application of ESG_Energy consumption and production key indicators | 2,64 | 1,185 |

| Implementation of ESG_Stakeholder participation key indicators | 2,61 | 1,188 |

| Application of ESG_Women workers key indicators | 3,08 | 1,212 |

| Implementation of ESG_Women employees in managerial positions | 2,97 | 1,314 |

| Implementation of ESG_Personnel mobility key indicators | 3,01 | 1,202 |

| Application of ESG_Employee training key indicators | 3,16 | 1,108 |

| Application of ESG_Human rights policy key indicators | 3,17 | 1,181 |

| Implementation of key ESG indicators_Collective labour agreements | 2,99 | 1,227 |

| Implementation of ESG key indicators_Supplier assessment | 3,09 | 1,240 |

| Implementation of ESG core indicators_Board composition | 3,09 | 1,198 |

| Implementation of ESG key indicators_Sustainable development monitoring | 2,89 | 1,214 |

| Implementation of ESG KPIs_Substantial issues | 2,78 | 1,219 |

| Implementation of ESG core indicators_Sustainability policy | 2,96 | 1,348 |

| Implementation of ESG core indicators_Business ethics policy | 3,00 | 1,385 |

| Implementation of ESG_Geographical security policy | 3,30 | 1,168 |

A.1.2. Correlations with Age

| Age | Μ | SD | p | ||

| How well do you know the ESG criteria? | Up to 30 years old | 3,27 | 0,467 | 0,156 | |

| 31-40 years old | 2,79 | 0,992 | |||

| 41-50 years old | 3 | 0,943 | |||

| 51-60 years old | 2,62 | 0,921 | |||

| Over 60 years old | 2,29 | 1,254 | |||

| Application of key ESG indicators Direct emissions | Up to 30 years old | 2,91 | 1,044 | 0,081 | |

| 31-40 years old | 2,64 | 1,084 | |||

| 41-50 years old | 2,79 | 1,228 | |||

| 51-60 years old | 2,24 | 0,944 | |||

| Over 60 years old | 2,29 | 1,254 | |||

| Application of key ESG Indirect emissions indicators | Up to 30 years old | 2,91 | 1,044 | 0,173 | |

| 31-40 years old | 2,58 | 1,146 | |||

| 41-50 years old | 2,79 | 1,228 | |||

| 51-60 years old | 2 | 1,095 | |||

| Over 60 years old | 2 | 0,816 | |||

| Application of ESG Energy consumption and production key indicators | Up to 30 years old | 3,18 | 1,401 | 0,245 | |

| 31-40 years old | 2,61 | 0,998 | |||

| 41-50 years old | 2,79 | 1,228 | |||

| 51-60 years old | 2,43 | 1,326 | |||

| Over 60 years old | 2 | 0,816 | |||

| Implementation of ESG_Stakeholder participation key indicators | Up to 30 years old | 3,09 | 1,136 | 0,26 | |

| 31-40 years old | 2,76 | 1,2 | |||

| 41-50 years old | 2,61 | 1,066 | |||

| 51-60 years old | 2,33 | 1,39 | |||

| Over 60 years old | 2 | 0,816 | |||

| Application of ESG_Women workers key indicators | Up to 30 years old | 3,55 | 1,44 | 0,039 | |

| 31-40 years old | 3,39 | 1,059 | |||

| 41-50 years old | 3,07 | 1,086 | |||

| 51-60 years old | 2,62 | 1,284 | |||

| Over 60 years old | 2,29 | 1,254 | |||

| Implementation of ESG_Women employees in managerial positions | Up to 30 years old | 3,27 | 1,191 | 0,139 | |

| 31-40 years old | 3,24 | 1,119 | |||

| 41-50 years old | 3,07 | 1,359 | |||

| 51-60 years old | 2,48 | 1,504 | |||

| Over 60 years old | 2,29 | 1,254 | |||

| Implementation of ESG_Personnel mobility key indicators | Up to 30 years old | 3,45 | 0,522 | 0,011 | |

| 31-40 years old | 3,33 | 1,137 | |||

| 41-50 years old | 2,86 | 1,177 | |||

| 51-60 years old | 2,9 | 1,446 | |||

| Over 60 years old | 1,71 | 0,488 | |||

| Application of ESG Employee training key indicators | Up to 30 years old | 3,73 | 1,104 | 0,043 | |

| 31-40 years old | 3,33 | 1,051 | |||

| 41-50 years old | 3,18 | 1,02 | |||

| 51-60 years old | 2,86 | 1,276 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| Application of ESG Human rights policy key indicators | Up to 30 years old | 3,45 | 0,82 | 0,08 | |

| 31-40 years old | 3,12 | 1,111 | |||

| 41-50 years old | 3,57 | 1,168 | |||

| 51-60 years old | 2,76 | 1,375 | |||

| Over 60 years old | 2,57 | 0,976 | |||

| Implementation of key ESG indicators Collective labour agreements | Up to 30 years old | 3,09 | 0,701 | 0,854 | |

| 31-40 years old | 3,12 | 1,364 | |||

| 41-50 years old | 2,96 | 1,232 | |||

| 51-60 years old | 2,9 | 1,338 | |||

| Over 60 years old | 2,57 | 0,976 | |||

| Implementation of ESG key indicators Supplier assessment | Up to 30 years old | 3,27 | 0,467 | 0,177 | |

| 31-40 years old | 3,21 | 1,364 | |||

| 41-50 years old | 3,36 | 1,162 | |||

| 51-60 years old | 2,67 | 1,461 | |||

| Over 60 years old | 2,43 | 0,535 | |||

| Implementation of ESG core indicators Board composition | Up to 30 years old | 3,64 | 0,505 | 0,48 | |

| 31-40 years old | 3,18 | 1,31 | |||

| 41-50 years old | 2,93 | 1,12 | |||

| 51-60 years old | 2,9 | 1,446 | |||

| Over 60 years old | 3 | 0,816 | |||

| Implementation of ESG key indicators Sustainable development monitoring | Up to 30 years old | 3,27 | 0,467 | 0,069 | |

| 31-40 years old | 2,94 | 1,368 | |||

| 41-50 years old | 3,21 | 1,101 | |||

| 51-60 years old | 2,38 | 1,359 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| Implementation of ESG KPIs_Substantial issues | Up to 30 years old | 3,55 | 0,934 | 0,208 | |

| 31-40 years old | 2,82 | 1,236 | |||

| 41-50 years old | 2,68 | 1,124 | |||

| 51-60 years old | 2,48 | 1,504 | |||

| Over 60 years old | 2,71 | 0,488 | |||

| Implementation of ESG core indicators Sustainability policy | Up to 30 years old | 3,73 | 0,905 | 0,162 | |

| 31-40 years old | 3,06 | 1,391 | |||

| 41-50 years old | 2,89 | 1,343 | |||

| 51-60 years old | 2,48 | 1,504 | |||

| Over 60 years old | 3 | 0,816 | |||

| Implementation of ESG core indicators Business ethics policy | Up to 30 years old | 3,91 | 0,831 | 0,017 | |

| 31-40 years old | 3,18 | 1,402 | |||

| 41-50 years old | 3 | 1,388 | |||

| 51-60 years old | 2,24 | 1,446 | |||

| Over 60 years old | 3 | 0,816 | |||

| Implementation of ESG_Geographical security policy | Up to 30 years old | 3,91 | 0,831 | 0,003 | |

| 31-40 years old | 3,36 | 1,27 | |||

| 41-50 years old | 3,61 | 0,685 | |||

| 51-60 years old | 2,48 | 1,289 | |||

| Over 60 years old | 3,29 | 1,254 | |||

| ESG effectiveness in attracting new customers | Up to 30 years old | 4,27 | 0,786 | 0,001 | |

| 31-40 years old | 3,12 | 0,927 | |||

| 41-50 years old | 3,14 | 0,97 | |||

| 51-60 years old | 2,62 | 1,284 | |||

| Over 60 years old | 2,57 | 0,976 | |||

| ESG effectiveness for competitive advantage | Up to 30 years old | 4,27 | 0,467 | 0,002 | |

| 31-40 years old | 3,45 | 1,201 | |||

| 41-50 years old | 3,46 | 0,922 | |||

| 51-60 years old | 2,86 | 1,108 | |||

| Over 60 years old | 2,57 | 0,976 | |||

| ESG effectiveness for revenue growth | Up to 30 years old | 4,09 | 0,701 | 0 | |

| 31-40 years old | 3,21 | 0,96 | |||

| 41-50 years old | 3,25 | 0,585 | |||

| 51-60 years old | 2,76 | 1,044 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG effectiveness for increasing business credibility | Up to 30 years old | 4,45 | 0,522 | 0 | |

| 31-40 years old | 3,82 | 0,392 | |||

| 41-50 years old | 3,75 | 0,799 | |||

| 51-60 years old | 3,14 | 1,558 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG effectiveness to reduce risk | Up to 30 years old | 3,73 | 0,905 | 0,019 | |

| 31-40 years old | 3,36 | 0,699 | |||

| 41-50 years old | 3,25 | 0,752 | |||

| 51-60 years old | 2,95 | 1,499 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG effectiveness for attracting new investors | Up to 30 years old | 4,27 | 0,467 | 0 | |

| 31-40 years old | 3,85 | 0,712 | |||

| 41-50 years old | 3,96 | 0,693 | |||

| 51-60 years old | 3,05 | 1,284 | |||

| Over 60 years old | 2,57 | 0,976 | |||

| ESG effectiveness to increase productivity | Up to 30 years old | 4,09 | 0,701 | 0 | |

| 31-40 years old | 3,36 | 0,895 | |||

| 41-50 years old | 3,25 | 0,752 | |||

| 51-60 years old | 2,86 | 1,108 | |||

| Over 60 years old | 2 | 0 | |||

| ESG effectiveness to increase opportunities for growth | Up to 30 years old | 4,27 | 0,786 | 0 | |

| 31-40 years old | 3,82 | 0,882 | |||

| 41-50 years old | 3,36 | 1,129 | |||

| 51-60 years old | 3,1 | 1,338 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG effectiveness to improve adaptability to technological, customer and regulatory changes | Up to 30 years old | 4,45 | 0,522 | 0 | |

| 31-40 years old | 4,12 | 0,485 | |||

| 41-50 years old | 3,75 | 0,799 | |||

| 51-60 years old | 3,05 | 1,284 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG implementation challenges Climate change | Up to 30 years old | 4,64 | 0,505 | 0,002 | |

| 31-40 years old | 4,27 | 0,977 | |||

| 41-50 years old | 3,89 | 0,737 | |||

| 51-60 years old | 3,57 | 1,207 | |||

| Over 60 years old | 3,29 | 0,488 | |||

| ESG Human Resources Management implementation challenges | Up to 30 years old | 4,45 | 0,522 | 0 | |

| 31-40 years old | 3,82 | 0,882 | |||

| 41-50 years old | 3,71 | 0,659 | |||

| 51-60 years old | 3,43 | 1,165 | |||

| Over 60 years old | 1,86 | 0,9 | |||

| ESG Corruption and bribery implementation challenges | Up to 30 years old | 4,09 | 0,701 | 0 | |

| 31-40 years old | 3,52 | 1,253 | |||

| 41-50 years old | 3,21 | 0,917 | |||

| 51-60 years old | 3,57 | 1,287 | |||

| Over 60 years old | 2,57 | 0,535 | |||

| ESG implementation challenges Lack of common guidelines for ESG assessment | Up to 30 years old | 4,45 | 0,522 | 0,047 | |

| 31-40 years old | 4,03 | 0,883 | |||

| 41-50 years old | 3,43 | 1,034 | |||

| 51-60 years old | 3,52 | 1,289 | |||

| Over 60 years old | 2,57 | 0,535 | |||

| ESG implementation challenges Lack of a supervisory authority for ESG evaluations | Up to 30 years old | 4,27 | 0,467 | 0 | |

| 31-40 years old | 4,09 | 0,98 | |||

| 41-50 years old | 3,71 | 0,937 | |||

| 51-60 years old | 3,67 | 1,278 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG implementation challenges Lack of transparency of ESG assessments | Up to 30 years old | 4,27 | 0,467 | 0,001 | |

| 31-40 years old | 4 | 1,031 | |||

| 41-50 years old | 3,71 | 0,81 | |||

| 51-60 years old | 3,71 | 1,309 | |||

| Over 60 years old | 2,29 | 0,488 | |||

| ESG implementation challenges Difficulty in complying with regulations | Up to 30 years old | 4,27 | 0,467 | 0 | |

| 31-40 years old | 4,06 | 0,788 | |||

| 41-50 years old | 3,93 | 0,858 | |||

| 51-60 years old | 3,67 | 1,278 | |||

| Over 60 years old | 2,29 | 0,488 |

A.1.3. Correlations with Educational Level

| Educational level | Μ | SD | p | ||

| How well do you know the ESG criteria? | Graduate of higher education institution | 2,3 | 0,65 | 0 | |

| Master's degree holder | 2,9 | 0,9 | |||

| Doctorate holder | 5 | 0 | |||

| Application of key ESG indicators Direct emissions | Graduate of higher education institution | 2,4 | 0,68 | 0 | |

| Master's degree holder | 2,6 | 1,11 | |||

| Doctorate holder | 5 | 0 | |||

| Application of key ESG Indirect emissions indicators | Graduate of higher education institution | 2,2 | 1,08 | 0 | |

| Master's degree holder | 2,5 | 1,09 | |||

| Doctorate holder | 5 | 0 | |||

| Application of ESG Energy consumption and production key indicators | Graduate of higher education institution | 2,4 | 1,07 | 0 | |

| Master's degree holder | 2,6 | 1,14 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG_Stakeholder participation key indicators | Graduate of higher education institution | 2,6 | 1,26 | 0 | |

| Master's degree holder | 2,5 | 1,1 | |||

| Doctorate holder | 5 | 0 | |||

| Application of ESG Women workers key indicators | Graduate of higher education institution | 2,6 | 1,01 | 0 | |

| Master's degree holder | 3,1 | 1,21 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG Women employees in managerial positions | Graduate of higher education institution | 2,5 | 1,17 | 0 | |

| Master's degree holder | 3 | 1,29 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG_Personnel mobility key indicators | Graduate of higher education institution | 2,7 | 1,1 | 0 | |

| Master's degree holder | 3 | 1,18 | |||

| Doctorate holder | 5 | 0 | |||

| Application of ESG Employee training key indicators | Graduate of higher education institution | 3 | 1,03 | 0 | |

| Master's degree holder | 3,1 | 1,09 | |||

| Doctorate holder | 5 | 0 | |||

| Application of ESG Human rights policy key indicators | Graduate of higher education institution | 2,7 | 1,06 | 0 | |

| Master's degree holder | 3,2 | 1,16 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of key ESG indicators Collective labour agreements | Graduate of higher education institution | 2,6 | 0,69 | 0 | |

| Master's degree holder | 3 | 1,27 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG key indicators Supplier assessment | Graduate of higher education institution | 2,6 | 1,17 | 0,02 | |

| Master's degree holder | 3,1 | 1,21 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG core indicators Board composition | Graduate of higher education institution | 3 | 0,88 | 0,02 | |

| Master's degree holder | 3 | 1,23 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG key indicators Sustainable development monitoring | Graduate of higher education institution | 2,7 | 1,16 | 0,05 | |

| Master's degree holder | 2,9 | 1,18 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG KPIs_Substantial issues | Graduate of higher education institution | 2,7 | 1,05 | 0 | |

| Master's degree holder | 2,7 | 1,21 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG core indicators Sustainability policy | Graduate of higher education institution | 2,7 | 1,05 | 0 | |

| Master's degree holder | 2,9 | 1,38 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG core indicators Business ethics policy | Graduate of higher education institution | 2,8 | 1,3 | 0 | |

| Master's degree holder | 3 | 1,38 | |||

| Doctorate holder | 5 | 0 | |||

| Implementation of ESG_Geographical security policy | Graduate of higher education institution | 3 | 1,11 | 0 | |

| Master's degree holder | 3,3 | 1,15 | |||

| Doctorate holder | 5 | 0 | |||

| ESG effectiveness in attracting new customers | Graduate of higher education institution | 2,6 | 1,26 | 0 | |

| Master's degree holder | 3,2 | 1,04 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness for competitive advantage | Graduate of higher education institution | 2,7 | 0,87 | 0 | |

| Master's degree holder | 3,5 | 1,13 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness for revenue growth | Graduate of higher education institution | 2,6 | 0,9 | 0 | |

| Master's degree holder | 3,3 | 0,9 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness for increasing business credibility | Graduate of higher education institution | 2,9 | 1,29 | 0 | |

| Master's degree holder | 3,8 | 0,88 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness to reduce risk | Graduate of higher education institution | 2,6 | 1,07 | 0 | |

| Master's degree holder | 3,3 | 0,92 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness for attracting new investors | Graduate of higher education institution | 3 | 1,03 | 0 | |

| Master's degree holder | 3,8 | 0,9 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness to increase productivity | Graduate of higher education institution | 2,8 | 0,96 | 0 | |

| Master's degree holder | 3,3 | 0,96 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness to increase opportunities for growth | Graduate of higher education institution | 3,1 | 1,18 | 0 | |

| Master's degree holder | 3,6 | 1,12 | |||

| Doctorate holder | 4 | 0 | |||

| ESG effectiveness to improve adaptability to technological, customer and regulatory changes | Graduate of higher education institution | 3,1 | 1,18 | 0 | |

| Master's degree holder | 3,9 | 0,9 | |||

| Doctorate holder | 4 | 0 | |||

| ESG implementation challenges Climate change | Graduate of higher education institution | 3,7 | 0,67 | 0 | |

| Master's degree holder | 4,1 | 1,04 | |||

| Doctorate holder | 4 | 0 | |||

| ESG Human Resources Management implementation challenges | Graduate of higher education institution | 3,2 | 1,17 | 0 | |

| Master's degree holder | 3,7 | 0,97 | |||

| Doctorate holder | 4 | 0 | |||

| ESG Corruption and bribery implementation challenges | Graduate of higher education institution | 3,1 | 0,81 | 0 | |

| Master's degree holder | 3,5 | 1,19 | |||

| Doctorate holder | 4 | 0 | |||

| ESG implementation challenges Lack of common guidelines for ESG assessment | Graduate of higher education institution | 3,5 | 0,91 | 0 | |

| Master's degree holder | 3,7 | 1,12 | |||

| Doctorate holder | 4 | 0 | |||

| ESG implementation challenges Lack of a supervisory authority for ESG evaluations | Graduate of higher education institution | 3,3 | 0,75 | 0 | |

| Master's degree holder | 3,9 | 1,12 | |||

| Doctorate holder | 4 | 0 | |||

| ESG implementation challenges Lack of transparency of ESG assessments | Graduate of higher education institution | 3,3 | 0,75 | 0 | |

| Master's degree holder | 3,9 | 1,11 | |||

| Doctorate holder | 4 | 0 | |||

| ESG implementation challenges Difficulty in complying with regulations | Graduate of higher education institution | 3,4 | 0,77 | 0 | |

| Master's degree holder | 3,9 | 1,04 | |||

| Doctorate holder | 4 | 0 |

A.1.4. Links to Training on ESG Criteria

| Have you received training on the proper assessment of ESG indicators? | Μ | SD | p | ||

| How well do you know the ESG criteria? | Yes | 3,61 | 0,838 | 0 | |

| No | 2,39 | 0,704 | |||

| Application of key ESG indicators Direct emissions | Yes | 3,58 | 0,732 | 0 | |

| No | 2,05 | 0,881 | |||

| Application of key ESG Indirect emissions indicators | Yes | 3,47 | 0,941 | 0 | |

| No | 1,97 | 0,89 | |||

| Application of ESG Energy consumption and production key indicators | Yes | 3,61 | 0,964 | 0 | |

| No | 2,09 | 0,921 | |||

| Implementation of ESG_Stakeholder participation key indicators | Yes | 3,44 | 0,877 | 0 | |

| No | 2,14 | 1,082 | |||

| Application of ESG Women workers key indicators | Yes | 3,89 | 0,919 | 0 | |

| No | 2,63 | 1,12 | |||

| Implementation of ESG Women employees in managerial positions | Yes | 3,83 | 0,845 | 0 | |

| No | 2,48 | 1,285 | |||

| Implementation of ESG_Personnel mobility key indicators | Yes | 3,64 | 0,867 | 0 | |

| No | 2,66 | 1,224 | |||

| Application of ESG Employee training key indicators | Yes | 3,92 | 0,906 | 0 | |

| No | 2,73 | 0,98 | |||

| Application of ESG Human rights policy key indicators | Yes | 3,94 | 0,893 | 0 | |

| No | 2,73 | 1,102 | |||

| Implementation of key ESG indicators Collective labour agreements | Yes | 3,61 | 1,103 | 0 | |

| No | 2,64 | 1,16 | |||

| Implementation of ESG key indicators Supplier assessment | Yes | 3,69 | 0,98 | 0 | |

| No | 2,75 | 1,247 | |||

| Implementation of ESG core indicators Board composition | Yes | 3,75 | 0,841 | 0 | |

| No | 2,72 | 1,215 | |||

| Implementation of ESG key indicators Sustainable development monitoring | Yes | 3,94 | 0,893 | 0 | |

| No | 2,3 | 0,937 | |||

| Implementation of ESG KPIs_Substantial issues | Yes | 3,67 | 0,986 | 0 | |

| No | 2,28 | 1,046 | |||

| Implementation of ESG core indicators Sustainability policy | Yes | 3,97 | 1,028 | 0 | |

| No | 2,39 | 1,163 | |||

| Implementation of ESG core indicators Business ethics policy | Yes | 4 | 1,069 | 0 | |

| No | 2,44 | 1,22 | |||

| Implementation of ESG_Geographical security policy | Yes | 3,97 | 1,108 | 0 | |

| No | 2,92 | 1,028 | |||

| ESG effectiveness in attracting new customers | Yes | 3,81 | 0,668 | 0 | |

| No | 2,72 | 1,105 | |||

| ESG effectiveness for competitive advantage | Yes | 4,03 | 0,845 | 0 | |

| No | 2,98 | 1,061 | |||

| ESG effectiveness for revenue growth | Yes | 3,61 | 0,728 | 0 | |

| No | 2,91 | 0,938 | |||

| ESG effectiveness for increasing business credibility | Yes | 4,08 | 0,732 | 0 | |

| No | 3,36 | 1,06 | |||

| ESG effectiveness to reduce risk | Yes | 3,75 | 0,806 | 0 | |

| No | 2,91 | 0,955 | |||

| ESG effectiveness for attracting new investors | Yes | 4,11 | 0,747 | 0 | |

| No | 3,42 | 1,005 | |||

| ESG effectiveness to increase productivity | Yes | 3,61 | 0,871 | 0 | |

| No | 2,98 | 0,951 | |||

| ESG effectiveness to increase opportunities for growth | Yes | 4,11 | 0,887 | 0 | |

| No | 3,13 | 1,106 | |||

| ESG effectiveness to improve adaptability to technological, customer and regulatory changes | Yes | 4,11 | 0,82 | 0 | |

| No | 3,47 | 1,007 | |||

| ESG implementation challenges Climate change | Yes | 4,14 | 0,351 | 0 | |

| No | 3,91 | 1,178 | |||

| ESG Human Resources Management implementation challenges | Yes | 4,17 | 0,775 | 0 | |

| No | 3,34 | 1,027 | |||

| ESG Corruption and bribery implementation challenges | Yes | 4,08 | 0,906 | 0 | |

| No | 3,08 | 1,074 | |||

| ESG implementation challenges Lack of common guidelines for ESG assessment | Yes | 4,14 | 0,639 | 0 | |

| No | 3,45 | 1,181 | |||

| ESG implementation challenges Lack of a supervisory authority for ESG evaluations | Yes | 4,06 | 0,791 | 0 | |

| No | 3,64 | 1,173 | |||

| ESG implementation challenges Lack of transparency of ESG assessments | Yes | 4,14 | 0,762 | 0 | |

| No | 3,56 | 1,139 | |||

| ESG implementation challenges Difficulty in complying with regulations | Yes | 4,17 | 0,697 | 0 | |

| No | 3,66 | 1,087 |

References

- Passas, I. “The Evolution of ESG: From CSR to ESG 2.0,” Encyclopedia 2024, Vol. 4, Pages 1711-1720, vol. 4, no. 4, pp. 1711–1720, Nov. 2024. [CrossRef]

- K. Ragazou, I. Passas, A. Garefalakis, and C. Zopounidis, “ESG in Construction Risk Management: A Strategic Roadmap for Controlling Risks and Maximizing Profits,” in https://services.igi-global.com/resolvedoi/resolve.aspx?doi=10.4018/978-1-6684-7786-1.ch003, IGI Global, 1AD, pp. 58–81. [CrossRef]

- Passas, I. “Accounting for integrity: ESG and financial disclosures: the challenge of internal fraud in management decision-making,” Hellenic Mediterranean University, Heraklon, 2023. [CrossRef]

- C. Hervieux, M. McKee, and C. Driscoll, “Room for improvement: Using GRI principles to explore potential for advancing PRME SIP reporting,” The International Journal of Management Education, vol. 15, no. 2, Part B, pp. 219–237, 2017. [CrossRef]

- GRI, “CONSOLIDATED SET OF GRI SUSTAINABILITY REPORTING STANDARDS 2020 2 Consolidated Set of GRI Sustainability Reporting Standards 2020,” 2020.

- B. Adiloglu and B. Vuran, “Identification of key performance indicators of auditor’s reports: Evidence from Borsa Istanbul (BIST),” Journal of Economics, Finance and Accounting, vol. 4, no. 3, pp. 256–261, 2017, [Online]. Available: https://dergipark.org.tr/en/download/article-file/370239.

- Sundgren, “Auditor choices and reporting practices: evidence from Finnish small firms,” The European Accounting Review, 7:3, 441-65., 1998.

- W. Steve. Albrecht, K. R. Howe, and M. B. Romney, “Deterring fraud : the internal auditor’s perspective,” p. 169, 1984.

- G. Serafeim and Y. Kontopoulos, “ESG Reporting Guide 2022,” 2022.

- M. D. Kimbrough, X. Wang, S. Wei, and J. Zhang, “Does Voluntary ESG Reporting Resolve Disagreement among ESG Rating Agencies?,” European Accounting Review, Jul. 2022. [CrossRef]

- N. Darnall, H. Ji, K. Iwata, and T. H. Arimura, “Do ESG reporting guidelines and verifications enhance firms’ information disclosure?,” Corp Soc Responsib Environ Manag, vol. 29, no. 5, pp. 1214–1230, Sep. 2022. [CrossRef]

- D. Jackson, G. Michelson, and R. Munir, “Developing accountants for the future: new technology, skills, and the role of stakeholders,” Accounting Education, vol. 32, no. 2, pp. 150–177, Mar. 2023. [CrossRef]

- T. Dathe, R. Dathe, I. Dathe, and M. Helmold, “Corporate Social Responsibility (CSR) and Ethical Management,” Management for Professionals, vol. Part F361, pp. 107–115, 2022. [CrossRef]

- T. Dathe, R. Dathe, I. Dathe, and M. Helmold, “Corporate social responsibility (CSR), sustainability and environmental social governance (ESG) : approaches to ethical management”.

- T. Dathe, R. Dathe, I. Dathe, and M. Helmold, “Corporate social responsibility (CSR), sustainability and environmental social governance (ESG) : approaches to ethical management”.

- F. Bhuiyan, K. Baird, and R. Munir, “The association between organisational culture, CSR practices and organisational performance in an emerging economy,” Meditari Accountancy Research, vol. 28, no. 6, pp. 977–1011, Nov. 2020. [CrossRef]

- N. Buhr, “The Professional Accountancy Bodies and the Provision of Education and Training in Relation to Environmental Issues,” The International Journal of Accounting, vol. 37, no. 3, pp. 367–369, 2002. [CrossRef]

- S. Jeffrey, S. Rosenberg, and B. McCabe, “Corporate social responsibility behaviors and corporate reputation,” Social Responsibility Journal, vol. 15, no. 3, pp. 395–408, May 2019. [CrossRef]

- P. Grover, A. K. Kar, and P. V. Ilavarasan, “Impact of corporate social responsibility on reputation—Insights from tweets on sustainable development goals by CEOs,” Int J Inf Manage, vol. 48, pp. 39–52, 2019. [CrossRef]

- G. Walsh, V. W. Mitchell, P. R. Jackson, and S. E. Beatty, “Examining the antecedents and consequences of corporate reputation: A customer perspective,” British Journal of Management, vol. 20, no. 2, pp. 187–203, Jun. 2009. [CrossRef]

- D. Klitou, Privacy-Invading Technologies and Privacy by Design, vol. 25. in Information Technology and Law Series, vol. 25. The Hague: T.M.C. Asser Press, 2014. [CrossRef]

- C. Zopounidis, A. Garefalakis, C. Lemonakis, and I. Passas, “Environmental, social and corporate governance framework for corporate disclosure: a multicriteria dimension analysis approach,” Management Decision, vol. 58, no. 11, pp. 2473–2496, 2020. [CrossRef]

- K. Ragazou, I. Passas, A. Garefalakis, and · Constantin Zopounidis, “Business intelligence model empowering SMEs to make better decisions and enhance their competitive advantage,” Discover Analytics 2022 1:1, vol. 1, no. 1, pp. 1–15, Feb. 2023. [CrossRef]

- N. Barrymore and R. C. Sampson, “ESG Performance and Labor Productivity: Exploring whether and when ESG affects firm performance,” 2021. [Online]. Available: https://www.morningstar.com/articles/959379/10-sustainable-investing-stories-of-2019.

- E. Escrig-Olmedo, M. ángeles Fernández-Izquierdo, I. Ferrero-Ferrero, J. M. Rivera-Lirio, and M. J. Muñoz-Torres, “Rating the raters: Evaluating how ESG rating agencies integrate sustainability principles,” Sustainability (Switzerland), vol. 11, no. 3, Feb. 2019. [CrossRef]

- K. Ragazou, C. Lemonakis, I. Passas, C. Zopounidis, and A. Garefalakis, “ESG-driven ecopreneur selection in European financial institutions: entropy and TOPSIS analysis,” Management Decision, vol. 63, no. 4, pp. 1316–1345, 2024. [CrossRef]

- W. Ping, M. Yue, Z. Qi, and S. Hao, “ESG-Driven Corporate Value Creation under the Paradigm of Ecological Civilization: Evidence from the Shareholder, Industrial Chain and Consumer Channels,” Soc Sci China, vol. 44, no. 1, pp. 129–157, 2023. [CrossRef]

- K. Ragazou, S. Nikolaos, A. Garefalakis, and C. Papademetriou, “Improving the Effectiveness of Entrepreneurs by Integrating Environmental, Social, and Governance Principles Into the Management of Human Resources,” in ESG and Total Quality Management in Human Resources, 2024, ch. 12, pp. 243–260. [CrossRef]

- L. H. Pedersen, S. Fitzgibbons, and L. Pomorski, “Responsible investing: The ESG-efficient frontier,” J financ econ, vol. 142, no. 2, pp. 572–597, Nov. 2021. [CrossRef]

- Y. Bofinger, K. J. Heyden, and B. Rock, “Corporate social responsibility and market efficiency: Evidence from ESG and misvaluation measures,” J Bank Financ, vol. 134, Jan. 2022. [CrossRef]

- I. Passas, K. Ragazou, E. Zafeiriou, A. Garefalakis, and C. Zopounidis, “ESG Controversies: A Quantitative and Qualitative Analysis for the Sociopolitical Determinants in EU Firms,” Sustainability 2022, Vol. 14, Page 12879, vol. 14, no. 19, p. 12879, Oct. 2022. [CrossRef]

- H. Ahmad, M. Yaqub, and S. H. Lee, “Environmental-, social-, and governance-related factors for business investment and sustainability: a scientometric review of global trends,” Feb. 01, 2024, Springer Science and Business Media B.V. [CrossRef]

- E. van Duuren, A. Plantinga, and B. Scholtens, “ESG Integration and the Investment Management Process: Fundamental Investing Reinvented,” Journal of Business Ethics, vol. 138, no. 3, pp. 525–533, Oct. 2016. [CrossRef]

- E. B. Barbier, “The Concept of Sustainable Economic Development,” Environ Conserv, vol. 14, no. 2, pp. 101–110, 1987. [CrossRef]

- K. Ragazou, I. Passas, A. Garefalakis, and C. Zopounidis, “ESG in Construction Risk Management,” in IGI Global, 2023, ch. 3, pp. 58–81. [CrossRef]

- T. T. Li, K. Wang, T. Sueyoshi, and D. D. Wang, “Esg: Research progress and future prospects,” Nov. 01, 2021, MDPI. [CrossRef]

- N. Lior, M. Radovanović, and S. Filipović, “Comparing sustainable development measurement based on different priorities: sustainable development goals, economics, and human well-being—Southeast Europe case,” Sustain Sci, vol. 13, no. 4, pp. 973–1000, Jul. 2018. [CrossRef]

- M. C. Tavares, G. Azevedo, R. P. Marques, and M. A. Bastos, “Challenges of education in the accounting profession in the Era 5.0: A systematic review,” 2023, Cogent OA. [CrossRef]

- Petropoulou, E. Angelaki, I. Rompogiannakis, I. Passas, A. Garefalakis, and G. Thanasas, “Digital Transformation in SMEs: Pre- and Post-COVID-19 Era: A Comparative Bibliometric Analysis,” Sustainability (Switzerland), vol. 16, no. 23, Dec. 2024. [CrossRef]

- E. B. Barbier, “The Concept of Sustainable Economic Development,” Environ Conserv, vol. 14, no. 2, pp. 101–110, 1987. [CrossRef]

- S. S. Chopra et al., “Navigating the Challenges of Environmental, Social, and Governance (ESG) Reporting: The Path to Broader Sustainable Development,” Jan. 01, 2024, Multidisciplinary Digital Publishing Institute (MDPI). [CrossRef]

- T. Nakajima et al., “ESG Investment in the Global Economy.” [Online]. Available: http://www.springer.com/series/15423.

- Armstrong, “Ethics and esg,” Australasian Accounting, Business and Finance Journal, vol. 14, no. 3, pp. 6–17, 2020. [CrossRef]

- de Souza Barbosa, M. C. B. C. da Silva, L. B. da Silva, S. N. Morioka, and V. F. de Souza, “Integration of Environmental, Social, and Governance (ESG) criteria: their impacts on corporate sustainability performance,” Dec. 01, 2023, Springer Nature. [CrossRef]

- M. Jain, G. D. Sharma, and M. Srivastava, “Can sustainable investment yield better financial returns: A comparative study of ESG indices and MSCI indices,” Mar. 01, 2019, MDPI AG. [CrossRef]

- E. Chatzopoulou, “449U Analysis of Esg Criteria and Sectoral Study of Sustainable Development in Greece (The Mast Project) Analysis of Esg Criteria and Sectoral Study of Sustainable Development in Greece (The Mast Project),” 449U London Journal of Research in Management & Business, vol. 24, 2024.

- Δ. Εργασία, “Σχολή Κοινωνικών Επιστημών Μεταπτυχιακό Πρόγραμμα Σπουδών στην Τραπεζική.”.

- W. Henisz, T. Koller, and R. Nuttall, “Five ways that ESG creates value Getting your environmental, social, and governance (ESG) proposition right links to higher value creation. Here’s why,” 2019.

- J. Öhman, “Exploring Managerial Attitudes to Environmental, Social, and Governance (ESG): A case study.”.

- M. Fiandini, A. B. D. Nandiyanto, D. F. Al Husaeni, D. N. Al Husaeni, and M. Mushiban, “How to Calculate Statistics for Significant Difference Test Using SPSS: Understanding Students Comprehension on the Concept of Steam Engines as Power Plant,” Indonesian Journal of Science and Technology, vol. 9, no. 1, pp. 45–108, 2024. [CrossRef]

- F. Y. Soumena, “The Effect Of Entrepreneurship Competence And Islamic Business Ethics On The Performance Of Micro And Small Enterprises (SMEs) Makassar,” Jurnal Ilmiah Ekonomi Islam, vol. 10, no. 1, p. 156, Mar. 2024. [CrossRef]

- H. S. Eti, “The Effects of Perceptions of Economic Sustainability and Barriers on Organic Farming Implementation,” Sustainability (Switzerland), vol. 17, no. 2, Jan. 2025. [CrossRef]

- Y. Le and X. Zhang, “How Green Entrepreneurial Orientation Influences Corporate Performance: The Missing Link of Green Knowledge Sharing,” Sustainability (Switzerland), vol. 16, no. 24, Dec. 2024. [CrossRef]

- T. Haque and M. M. Rahman, “Sustainability Reporting: Empirical Evidence from Listed Firms of Fuel and Power Sector of Bangladesh,” Dhaka University Journal of Business Studies, pp. 175–212, Jun. 2021. [CrossRef]

- J. Dumay, J. Guthrie, and F. Farneti, “GRI sustainability reporting guidelines for public and third sector organizations: A critical review,” Public Management Review, vol. 12, no. 4, pp. 531–548, 2010. [CrossRef]

- R. G. Eccles, I. Ioannou, and G. Serafeim, “The Impact of Corporate Sustainability on Organizational Processes and Performance.”.

- A. Adams and C. Larrinaga-González, “Engaging with organisations in pursuit of improved sustainability accounting and performance,” Jun. 12, 2007. [CrossRef]

Figure 1.

Application of ESG Indicators for Direct Emissions.

Figure 2.

Application of ESG Indicators for Indirect Emissions.

Figure 3.

Application of ESG Indicators for Energy Consumption and Production.

Figure 4.

Application of ESG Indicators for Stakeholder Engagement.

Figure 5.

Application of ESG Criteria for Female Employees.

Figure 6.

Application of ESG Criteria for Female Employees in Managerial Positions.

Figure 7.

Application of ESG Criteria for Staff Mobility.

Figure 8.

Application of ESG Criteria for Employee Training.

Figure 9.

Application of ESG Criteria for Human Rights Policy.

Figure 10.

Application of ESG Criteria for Collective Labor Agreements.

Figure 11.

Application of ESG Criteria for Supplier Evaluation.

Figure 12.

Application of ESG Criteria for Board Composition.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.