Submitted:

08 June 2025

Posted:

10 June 2025

You are already at the latest version

Abstract

The transition to a circular economy (CE) presents both opportunities and financial challenges for municipal governance, particularly in countries navigating post-industrial and sustainability transitions. This study investigates the financial impact of CE implementation at the municipal level in the Slovak Republic between 2013 and 2023. Employing a comprehensive econometric approach, we integrate multivariate regression analysis with a combined dataset derived from national statistics, municipal financial records, and technical reports. The model includes twelve independent variables such as revenue from secondary raw materials, investments in CE infrastructure, waste generation per capita, recycling rates, and environmental expenditure, to estimate their influence on municipal waste management costs. The results reveal that capital investments in circular infrastructure and per capita environmental investments significantly increase municipal expenditures, whereas higher rates of waste recovery and efficiency in separated waste collection yield cost-saving effects. The findings underscore the dual fiscal nature of CE transition: while initial costs rise due to infrastructural and operational requirements, long-term financial benefits are attainable through effective resource recovery and governance mechanisms. This study contributes to the policy discourse on sustainable urban finance by providing empirical evidence on the budgetary dynamics of CE at the municipal scale.

Keywords:

circular economy

; municipal finance

; Slovakia

; environmental investment

; regression modelling

; cost-benefit analysis

; empirical analysis

1. Introduction

The transition to a circular economy (CE) represents a major shift in how societies produce, consume, and manage resources. It replaces the traditional linear model of "take, make, dispose" with regenerative systems that promote reuse, recycling, and the extension of product lifecycles. With increasing pressure from global environmental crises such as climate change, biodiversity loss, and waste accumulation, CE has gained considerable traction as a strategic framework for sustainable development [1,2,3].

Municipalities are key actors in this transition. As primary regulators of waste management, water supply, energy distribution, and local infrastructure, they are uniquely positioned to implement circular practices and policies. More than 70% of greenhouse gas emissions originate from urban areas, making cities central to sustainability and resilience transformations. Importantly, the CE transition affects not only operational functions but also how local authorities plan, finance, and govern urban systems [4,5,6].

Despite growing attention to CE, its financial implications for municipal governance remain insufficiently understood. Much of the existing literature focuses either on high-level CE policy frameworks or technical waste management solutions, often neglecting fiscal dimensions. Municipalities face challenges in balancing CE-related ambitions with constrained budgets, fragmented revenue streams, and the need to invest in infrastructure and behavioural change [7,8,9]. These challenges are particularly salient in Central and Eastern European countries, including Slovakia, where fiscal autonomy and access to investment finance may be limited.

This study explores how the transition to a circular economy affects municipal finances in the Slovak Republic. Specifically, it examines the structure of environmental investments, revenue generation through CE activities (e.g., recycling, composting, and energy recovery), and cost-saving mechanisms such as landfill diversion and public procurement reform. The analysis highlights the interaction between CE strategies and local budgetary planning, aiming to assess both risks and opportunities.

By doing so, this research contributes to a more integrated understanding of the financial dimension of CE. It brings together insights from municipal expenditure reports, national statistics, EU funding instruments, and policy roadmaps such as the "Highlights: Closing the Loop in the Slovak Republic" [10], aligning financial analysis with the operational realities of CE implementation.

This article addresses the following questions:

- What financial challenges and opportunities does the circular economy present to municipal governments in Slovakia?

- How can municipalities generate revenues and achieve savings through CE practices?

- What are the implications of CE implementation for local budgeting, investment strategies, and fiscal governance?

A growing number of studies explore CE adoption in urban settings, particularly in relation to waste policy, infrastructure planning, and environmental behaviour change [21, 22, 23]. Scholars such as Meili & Stucki (2023) and Kumar et al. (2025) have investigated the role of financial tools in CE transitions at the corporate and national levels [32, 26]. Others highlight the importance of pricing schemes and smart regulations in aligning CE goals with economic incentives [17].

In Slovakia, research by Tokárčiková et al. (2024) and Pavolová et al. (2020) sheds light on the structural aspects of waste treatment and circularity metrics [51, 39], while strategic policy reports (e.g., OECD 2020) emphasize the role of governance and coordination mechanisms [34]. Nevertheless, there is a lack of detailed empirical analysis linking CE strategies to actual financial outcomes for local governments. Key areas of uncertainty include the management of upfront costs, the monetisation of environmental gains, and the institutional capacity to align CE goals with fiscal sustainability.

The primary aim of this article is to assess the financial implications of CE transition on municipal governance in the Slovak Republic. It investigates the scope, composition, and effectiveness of CE-related financial flows across municipalities, drawing from publicly available expenditure and investment datasets, environmental statistics, and national CE policy frameworks. The findings will inform both academic debates and practical decision-making, offering evidence-based recommendations for integrating CE into fiscal planning and governance structures at the local level.

2. Literature Review

2.1. Theoretical Foundations of the Circular Economy

The CE has been increasingly recognised as a transformative model for sustainable development, shifting the prevailing economic paradigm from linear extraction and disposal towards regenerative, closed-loop systems. Based on principles such as reduce, reuse, recycle, and regenerate (Ghisellini et al., 2016; Ellen MacArthur Foundation, 2013) [20, 14], the CE approach seeks to decouple economic growth from resource consumption by promoting material efficiency, extended product lifecycles, and the minimisation of waste.

Scholars have developed various conceptual models of CE, ranging from micro-level firm-based strategies to macro-level national and municipal policy frameworks (Geissdoerfer et al., 2017) [18]. In urban settings, circularity is most frequently addressed through waste management systems, green public procurement (GPP), eco-design, and infrastructure planning (Abu-Bakar et al., 2024; White Paper WEF, 2018) [1,14].

2.2. Municipal Finance, Governance, and Circular Economy Instruments

Municipalities play a critical role in implementing CE initiatives, particularly through their control over waste services, land use, utilities, and procurement. Yet their ability to do so is strongly conditioned by institutional capacity and financial autonomy (OECD, 2022) [35]. Research increasingly points to the need for financial mechanisms that support the CE transition at the local level, such as pay-as-you-throw (PAYT) schemes, green bonds, EU funds, and partnerships with the private sector (Di Foggia & Beccarello, 2023; Kumar et al., 2025) [13,26].

Green public procurement (GPP) is emerging as a key lever, enabling municipalities to drive demand for circular goods and services through their purchasing decisions. Although promoted by the EU Circular Economy Action Plan, empirical studies reveal limited integration of GPP into municipal financial planning, performance metrics, or expenditure frameworks (OECD, 2022; Abu-Bakar et al., 2024) [35, 2].

Research by Meili and Stucki (2023) [32] identifies corporate finance, regional income, and procurement as significant enablers of circular activity, though primarily at the enterprise level. Their findings suggest that public procurement can promote CE leadership, yet municipal-level evidence remains scarce. The need for fiscal tools that align long-term CE goals with short-term budgetary constraints remains a recurrent theme in the literature.

2.3. Empirical Studies on Municipal Circular Economy Transitions

Empirical evidence on CE at the municipal level, especially in Central and Eastern Europe, remains limited. Tokarčíková et al. (2024) and Pavolová et al. (2020) [51, 39] offer valuable insights into waste generation and separation patterns across Slovak municipalities. Their studies apply statistical modelling to identify key drivers of waste behaviour, including population density, treatment costs, and infrastructure gaps. Yet these works stop short of assessing financial outcomes such as revenue generation, operational savings, or return on investment.

Cifranic et al. (2025) [9] provide one of the few fiscal analyses of CE in Slovakia, identifying how greater waste separation rates can increase municipal expenditure while exposing disparities in local revenue capacity. This underlines the tension between environmental goals and financial feasibility, especially in under-resourced municipalities.

A significant critique in the literature is the prevailing association of CE with waste management alone. While waste remains central to local CE strategies, studies argue that this narrow focus inhibits more comprehensive, systems-based approaches ( Johansson & Henriksson, 2020) [24]. The literature also highlights that small and medium-sized municipalities are underrepresented in CE research, despite their prominence in the European municipal landscape (Makris et al., 2024) [29].

2.4. Knowledge Gaps and Research Opportunities

Despite a growing interest in the financial implications of CE, several gaps persist. First, very few studies explore how CE affects municipal budgeting processes, debt ratios, or investment cycles. Second, the fiscal impact of CE instruments such as GPP, PAYT, and circular procurement remains underexplored beyond pilot examples. Third, the literature lacks integrated models connecting CE policy implementation to municipal financial indicators.

Furthermore, municipalities often conflate CE with legally mandated waste services, leading to limited strategic integration and vague goal-setting [17]. The transfer of responsibility to market actors—rather than strengthening local governments—also limits the transformative potential of CE transitions [28].

In sum, while theoretical models and policy strategies for CE are evolving rapidly, the financial governance of CE at the municipal level—particularly in countries like Slovakia—remains a relatively unexplored domain. This research aims to address that void by focusing on the financial effects, institutional mechanisms, and governance capacities that underpin CE adoption at the local level.

3. Materials

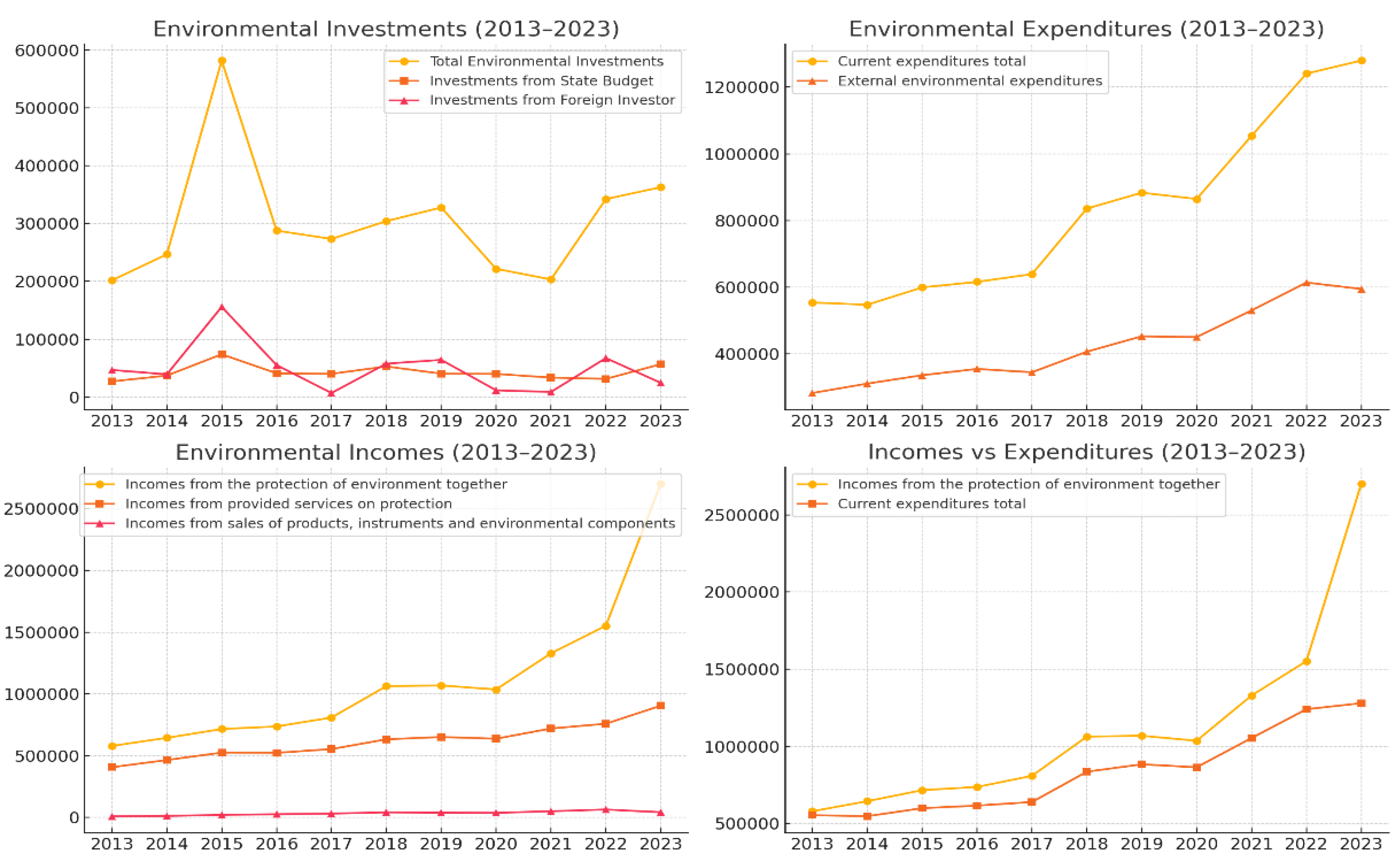

The transition toward a CE model in municipal governance is inherently tied to the reallocation of public funds, changes in budgetary priorities, and the emergence of new revenue streams. The Slovak case, represented by data from 2013 to 2023, offers valuable insights into these dynamics, (Figure 1), (Appendix A).

Between 2013 and 2023, total environmental investments in Slovakia fluctuated significantly, with notable peaks in 2015 (€581.7 million) and 2023 (€362.7 million), and a low point in 2013 (€201.8 million). While investment volumes varied year to year, there was a consistent reliance on the state budget, contributing approximately €27–74 million annually, and a more variable contribution from foreign investors, ranging from €4.6 million (2013) to €155.9 million (2015).

This variation reflects both the availability of external funding mechanisms (e.g., EU structural funds) and changing domestic priorities. The increase in investment during recent years, especially post-2020, suggests a response to European Green Deal objectives and recovery funding post-COVID-19, reinforcing the alignment of capital investments with circular economy policy frameworks [16].

Over the same period, current expenditures on environmental protection more than doubled — from €554.1 million in 2013 to nearly €1.28 billion in 2023. This includes internal costs (salaries, operations), which grew steadily, and external environmental expenditures, rising from €282.8 million to €594.8 million. The rise reflects both inflation and the expansion of municipal services linked to CE initiatives such as waste separation, composting, and service contracting.

A critical observation is the steady growth in revenue generation from environmental services. Total incomes from environmental protection grew from €579.5 million in 2013 to €2.7 billion in 2023 — more than a fourfold increase. This trend is driven by:

- —

- increased sales of services (e.g., collection and processing fees),

- —

- expansion of product sales (e.g., recycled materials),

- —

- monetisation of environmental technologies and instruments.

These figures confirm the CE's potential not only as a cost centre but as a revenue-generating domain for municipalities. The financial transformation is evident: where early CE investments were mainly expenditure-driven, recent years illustrate a shift towards fiscal self-sufficiency and value creation through circular systems.

The investment and expenditure structure shown in the Slovak context highlights several core insights:

- —

- A well-financed CE transition can yield measurable operational revenues over time.

- —

- Municipalities benefit from external co-financing mechanisms, especially in early phases.

- —

- Long-term planning enables a shift from subsidy-dependence to income-generation.

In conclusion, the financial evolution in Slovakia offers an empirical demonstration of the circular economy’s viability in municipal settings — not only as a sustainability imperative but also as a driver of budgetary resilience and strategic reinvestment.

Over the period 2013 to 2023, Slovakia's environmental investments per capita displayed notable fluctuations, reflecting both national policy shifts and external economic influences. The total environmental investments ranged from €201.8 million in 2013 to a peak of €581.7 million in 2015, followed by a period of relative stabilisation. On a per capita basis, the investment increased from €37.29 in 2013 to €66.81 in 2023.

The most significant increase occurred in 2015, where per capita investment rose sharply to €107.31, more than doubling the value recorded the previous year. This peak is likely attributable to targeted capital programmes or the absorption of EU structural funds at the close of a programming period. However, this surge was not sustained, and the per capita investment declined in subsequent years, stabilising between €37 and €66 per person from 2016 onward.

From 2020 onwards, despite the economic uncertainty caused by the COVID-19 pandemic, per capita investment showed a gradual recovery, increasing from €40.61 in 2020 to €66.81 in 2023. This trend may reflect enhanced prioritisation of environmental resilience and green recovery efforts.

These investment patterns underscore the strategic shifts in environmental governance and public spending, suggesting that while short-term fluctuations are common, the long-term trajectory points to a growing emphasis on per capita environmental investment [19].

Strategic Investment Flows and the Circular Economy Transition

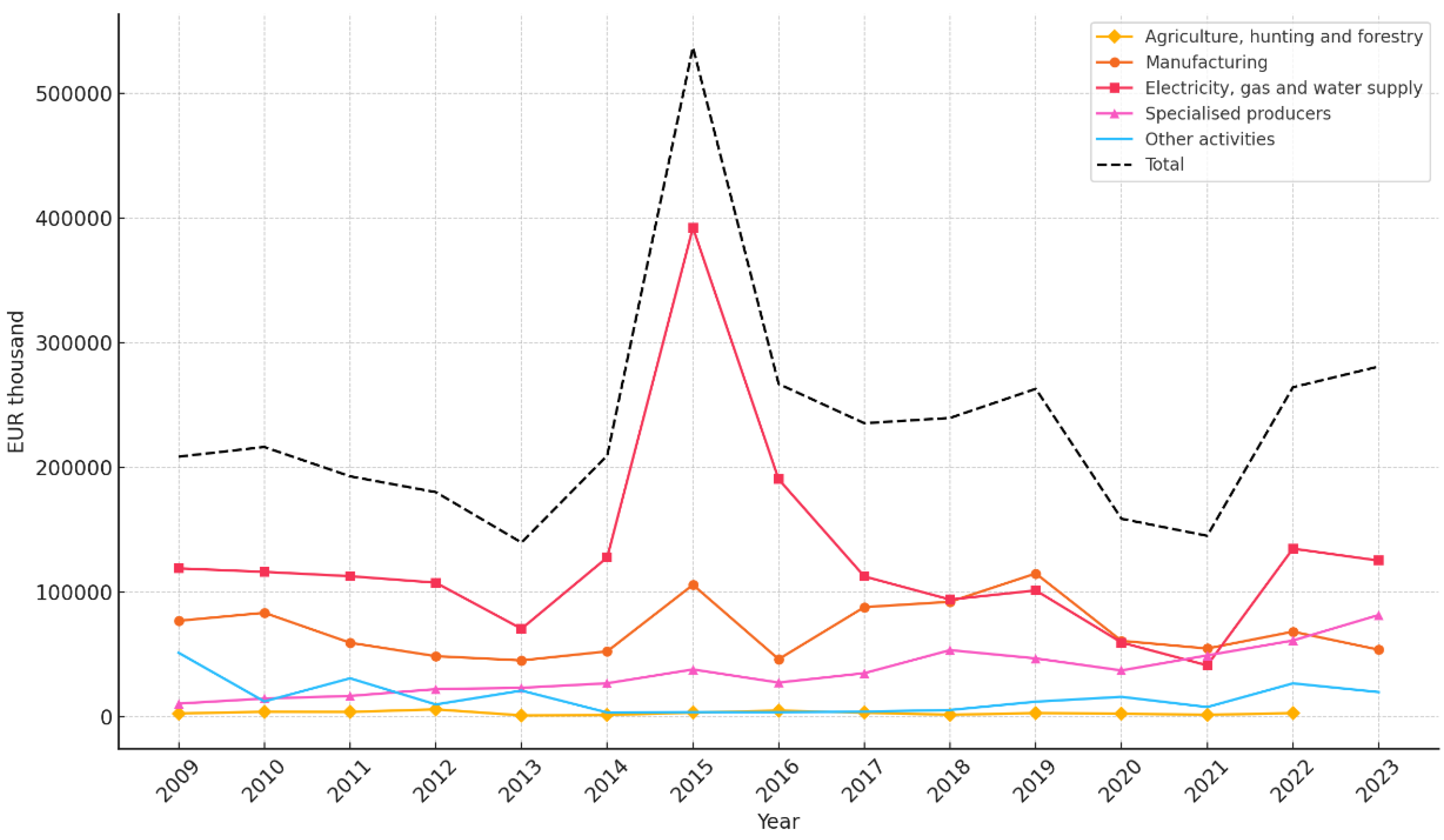

To complement the analysis of aggregate environmental expenditures at the municipal level, it is essential to examine how capital investments have evolved across economic sectors, as these sectors often operate in partnership with or under the regulation of municipal authorities. The data covering Slovakia from 2009 to 2023 offers valuable insights into sectoral engagement with CE objectives, (Figure 2), (Appendix A).

The most pronounced trend over the 15-year period is the sustained dominance of the electricity, gas, and water supply sector in environmental investment. With peaks reaching €392.3 million in 2015 and €125.3 million in 2023, this sector serves as the backbone of CE infrastructure, especially in areas such as energy recovery from waste, water reuse systems, and smart grid integration. The magnitude and consistency of investment highlight the crucial role this sector plays in enabling municipal-level CE strategies through technical and service-oriented capacities.

The role of specialised producers (often municipal utilities or private-public joint ventures) has steadily increased, with capital inflows growing from €10.5 million in 2009 to €81.6 million in 2023. These actors are central to implementing CE-related services—particularly in waste treatment, recycling, and composting—and their growing financial weight suggests a municipal shift from linear waste disposal to circular resource recovery.

Manufacturing also emerges as a consistent, though secondary, recipient of environmental investment. The sector demonstrates a strong presence in pre-2020 figures, peaking at over €114.9 million in 2019, but shows more volatility in recent years. Its role in material efficiency and industrial symbiosis remains relevant for circularity at the local level, particularly where municipalities collaborate with local industries on by-product valorisation and cleaner production.

Meanwhile, sectors such as agriculture and mining received minimal funding or had data suppressed due to confidentiality in 2023. This suggests limited engagement or reporting challenges in CE-aligned initiatives within these traditionally resource-intensive domains [45, 46, 48].

The inclusion of “other activities”, receiving €19.8 million in 2023, provides evidence of CE spillover effects into construction, logistics, and services—areas frequently linked to local government operations. Such diversification indicates a maturing CE investment landscape that goes beyond heavy infrastructure and integrates broader urban systems.

Finally, the total environmental investment rose from €208.6 million in 2009 to €280.9 million in 2023, despite sharp fluctuations across the years. Notably, investment levels surged in 2015–2016, possibly reflecting the absorption of EU cohesion funding under the 2007–2013 programming period. While municipal expenditure remains a major pillar, this sectoral data affirms the increasing importance of cross-sectoral partnerships and private-sector mobilisation in financing CE transitions at the local level.

Analytical Commentary on Environmental Expenditure and Revenue Trends.

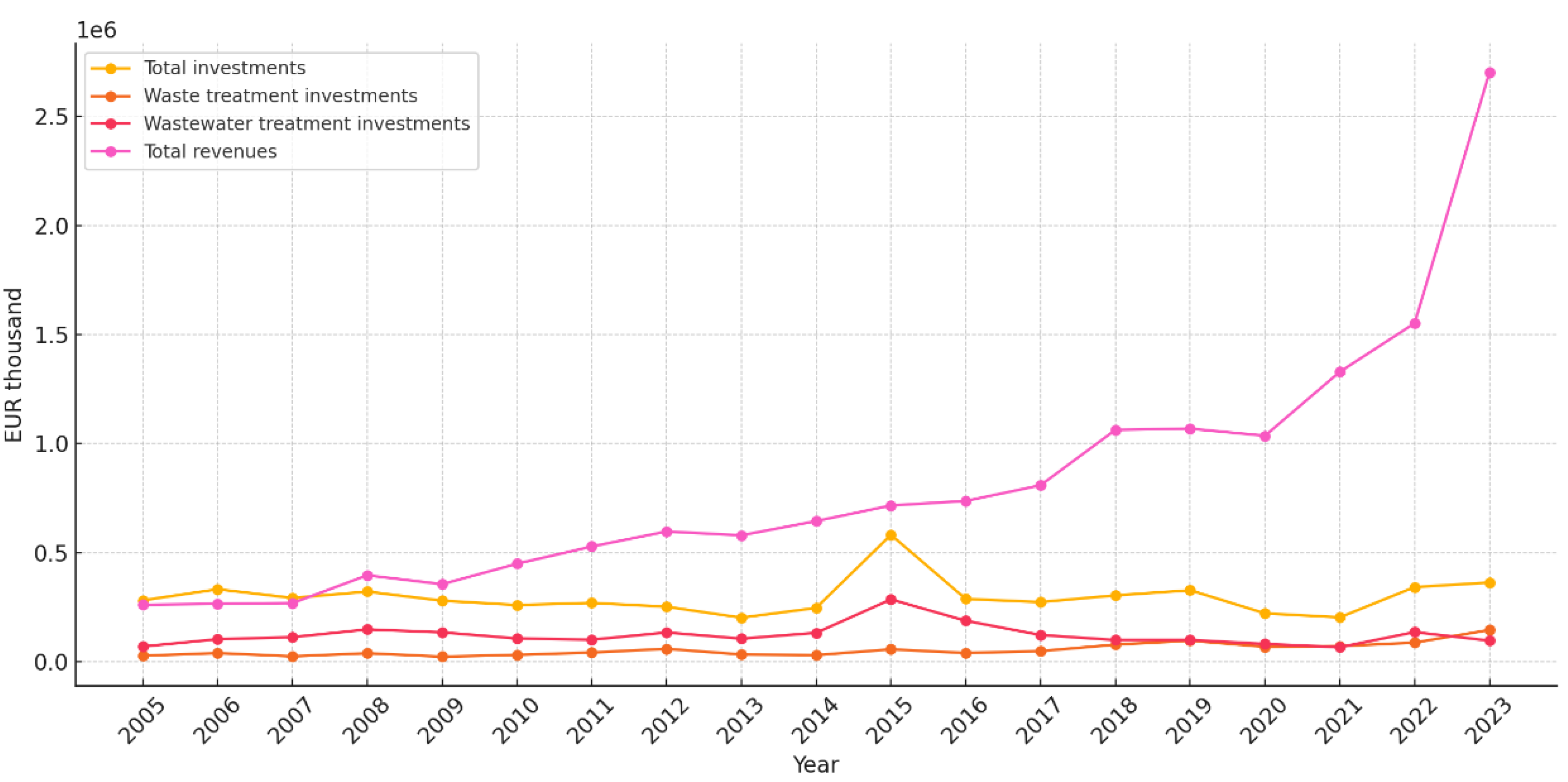

The longitudinal data on environmental expenditures and revenues in Slovakia from 2005 to 2023 offers valuable insights into the financial dynamics of the circular economy transition at the municipal level, (Figure 3). The analysis focuses on three primary indicators: total environmental investments, capital expenditure on waste and wastewater treatment, and total revenues generated from environ-mental protection activities.

Over the examined period, total investments in environmental protection displayed significant volatility, ranging from a low of €201.79 million in 2013 to a peak of €581.74 million in 2015. This variability likely reflects the influence of external funding cycles, particularly from EU structural and cohesion funds. Notably, post-2020 investment figures suggest renewed momentum, with val-ues exceeding €340 million annually since 2021. This resurgence may be attributed to green recovery packages and increased policy emphasis on sustainable infrastructure following the COVID-19 pandemic [15].

Waste treatment—one of the core pillars of the circular economy—shows a clear upward trajectory, particularly in the last decade. From a relatively modest €27.06 million in 2005, investments rose to €145.53 million by 2023. This fivefold increase indicates a pro-gressive shift towards modernisation and expansion of municipal waste management systems. However, the fluctuations between years, such as the drop in 2017 (€39.93 million) and spike in 2023, suggest that investment is still somewhat reactive to project availability and budgetary cycles rather than being part of a sustained long-term strategy.

Similarly, capital investments in wastewater treatment demonstrate robust growth, peaking at €285.64 million in 2015. While sub-sequent years saw some contraction, the overall trend remains positive, with a renewed increase to €96.36 million in 2023. These figures underline ongoing efforts to meet EU wastewater directive requirements and to upgrade municipal water infrastructure in line with circular economy principles, which emphasise water reuse and pollution reduction.

The evolution of revenues from environmental protection activities serves as a proxy for the economic maturity of green municipal initiatives. From €261 million in 2005, revenues grew steadily, surpassing €1 billion from 2018 onwards and reaching €2.7 billion in 2023. This substantial increase suggests that municipalities are progressively moving beyond the cost-intensive phase of infrastruc-ture development towards a model that yields measurable financial returns—potentially from waste valorisation, recycling mar-kets, and environmental services.

The upward trends in both investment and revenue generation, particularly in waste and wastewater sectors, provide empirical support for the strategic role of municipalities in fostering circular economy transitions. Nonetheless, the volatility observed in cer-tain years points to a need for greater financial stability and long-term planning frameworks. Additionally, aligning capital ex-penditure with clear indicators of environmental and economic impact remains crucial for ensuring that investments contribute meaningfully to systemic sustainability goals.

Municipal Waste Treatment Trends and Circular Economy Implications.

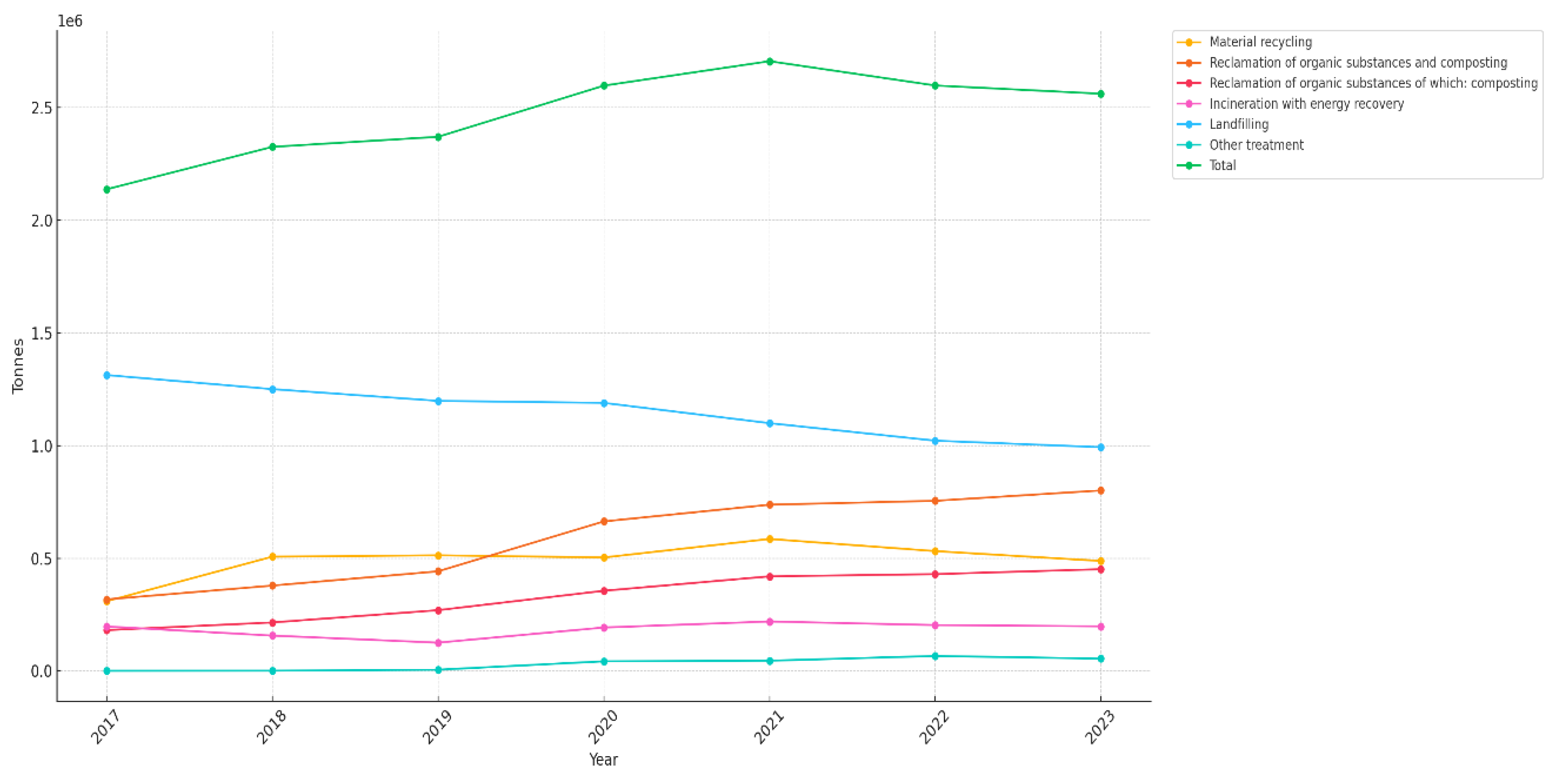

An examination of municipal waste treatment data from Slovakia between 2017 and 2023 reveals meaningful shifts in waste management practices aligned with CE principles, (Figure 4), (Appendix A). The annual total of municipal and small construction waste treated increased from approximately 2.14 million tonnes in 2017 to over 2.70 million tonnes in 2021, followed by a slight decline to 2.56 million tonnes in 2023. This trajectory suggests a general intensification of waste management activity over the observed period, likely influenced by EU directives and national policy measures encouraging circular approaches.

Among treatment methods, material recycling consistently accounted for a significant share, rising from 309,246 tonnes in 2017 to a peak of 585,578 tonnes in 2021, before slightly decreasing to 487,940 tonnes in 2023. This trend underlines ongoing investment and infrastructure development in municipal recycling systems, and reflects their centrality in CE strategies.

Equally notable is the role of reclamation of organic substances, particularly composting, which nearly doubled from 180,967 tonnes in 2017 to 451,322 tonnes in 2023. These figures demonstrate growing attention to bio-waste recovery as a pillar of CE-compatible waste diversion, reducing landfill dependence and contributing to nutrient cycles in local ecosystems.

Despite these positive developments, landfilling remained the dominant treatment method throughout the period, although its share has decreased from over 1.31 million tonnes in 2017 to 992,609 tonnes in 2023. This reduction indicates gradual progress in landfill avoidance, but also highlights the continued reliance on linear disposal practices that are at odds with CE goals.

Other treatment categories, such as incineration with and without energy recovery, other recovery, and other disposal, represent a small but non-negligible portion of the waste stream. Notably, incineration with energy recovery fluctuated moderately, with 197,895 tonnes processed in 2023, while incineration without energy recovery showed significant decline, reflecting environmental performance improvements.

Overall, the data reflect a slow but measurable transition toward circular waste treatment models. The increasing prominence of recycling and composting suggests positive policy impacts and behavioural shifts at the municipal level. However, persistent reliance on landfill underscores the need for stronger regulatory frameworks, financial incentives, and public-private collaboration to accelerate Slovakia’s transition to a fully circular waste management system [32, 33].

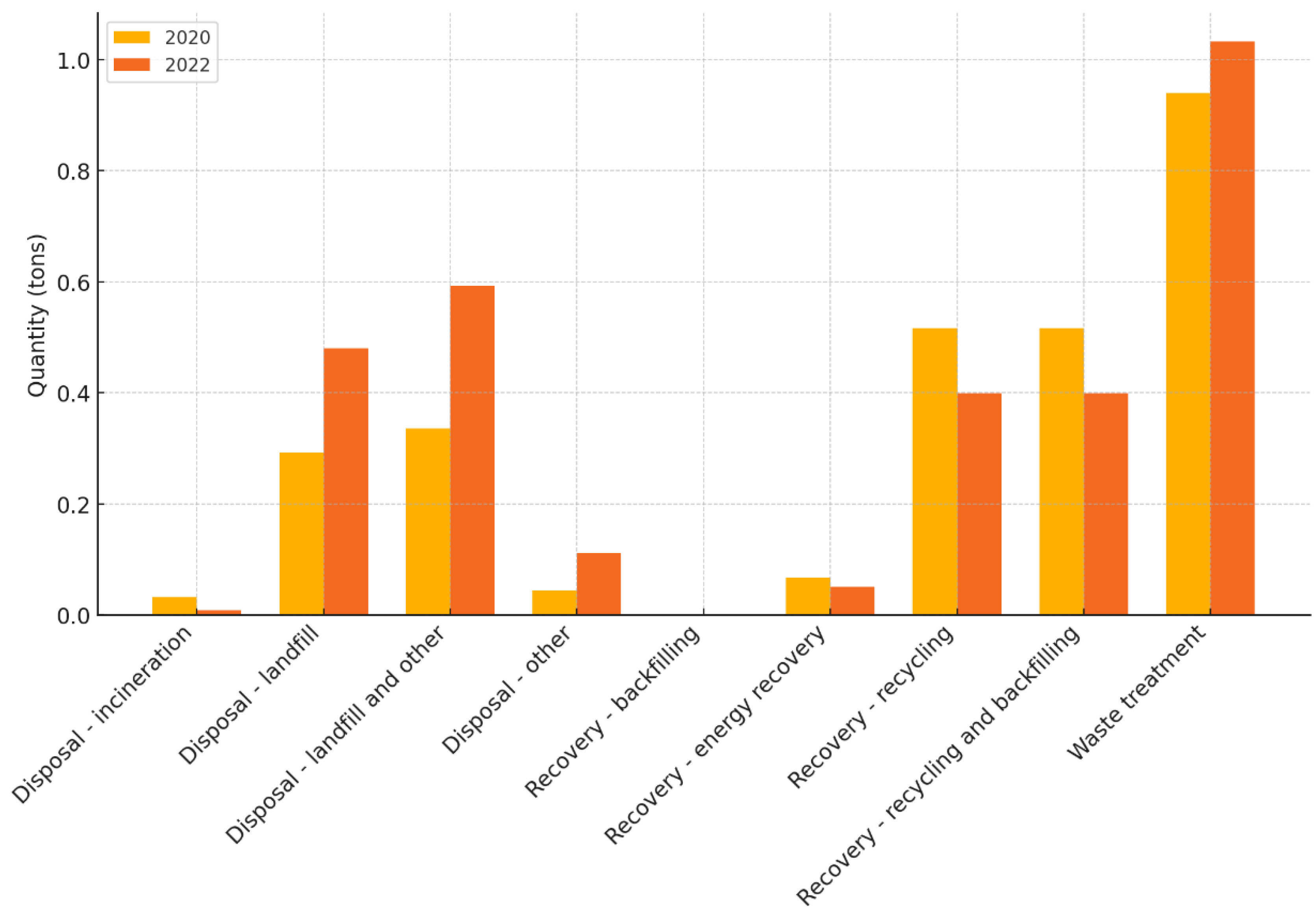

Hazardous Waste

The management of hazardous waste across selected streams in Bratislava underwent significant variations between 2020 and 2022, (Figure 5), (Appendix A). A striking shift was observed in the disposal via landfill (D1, D5, D12) for acid, alkaline or saline wastes, which surged from 8,557 tonnes to over 3.2 million tonnes. This represents a staggering increase of over 37,000%, suggesting either a major reclassification of waste types or substantial changes in reporting practices. Similarly, the aggregated “landfill and other” category expanded over 17,000%, pointing to a broader reliance on disposal methods for this waste stream.

Conversely, incineration (D10) for the same category dropped precipitously from 281,255 tonnes to just 105 tonnes, indicating a potential shift away from thermal treatment—perhaps due to cost constraints or regulatory changes. Recovery efforts remained stable, with no recorded backfilling and consistent recycling volumes (over 7,800 tonnes). However, other disposal methods (D2–D4, D6–D7) were phased out entirely, dropping from 10,350 tonnes to zero. Overall, the trends highlight a mixed performance: while recovery volumes were maintained, the dramatic growth in landfill use for hazardous waste raises concerns regarding circular economy (CE) compliance and cost-efficiency.

Non-Hazardous Waste

The treatment of non-hazardous waste showed a divergent profile. For acid, alkaline or saline wastes, recycling sharply increased, from zero in 2020 to over 10,113 tonnes in 2022. This may reflect improved separation practices or expanded infrastructure for material recovery. However, landfill use also rose steeply—from 549 tonnes to 4,676 tonnes—suggesting that not all material was successfully diverted from final disposal.

In the case of chemical wastes, incineration remained minimal, while recycling jumped significantly from approximately 918 tonnes to over 5,289 tonnes—a 476% increase. Meanwhile, landfill disposal for this category continued to dominate in absolute terms, exceeding 27,500 tonnes by 2022. The growth in recycling, alongside sustained landfill reliance, indicates that although CE principles are gaining traction, systemic waste stream redesigns are still required to avoid persistent disposal dependency.

Total Waste (Hazardous and Non-Hazardous)

The aggregate category, combining both hazardous and non-hazardous fractions, provides a composite picture of the waste management trajectory. Notably, used oils maintained stable recycling rates (approx. 3,448 to 3,889 tonnes), while energy recovery plummeted from over 2,029 tonnes in 2020 to just 530 tonnes in 2022. This decline may point to disruptions in recovery technology or policy shifts disincentivising thermal conversion.

For chemical wastes, total recycling increased substantially from 7,820 to over 9,879 tonnes, reinforcing the growing capacity for material recovery. Yet this was paralleled by an increase in both landfill and other disposal, together accounting for more than 11,100 tonnes in 2022. Thus, while recycling infrastructure expands, disposal practices remain persistent, suggesting a lag in systemic circularity.

In total, the mixed performance across categories reflects a transitional phase in municipal waste governance. Recycling volumes are improving, particularly in the non-hazardous segment, but the enduring and in some cases increasing reliance on landfilling and incineration—especially for hazardous fractions—poses both financial and environmental risks. For municipalities like Bratislava, these dynamics underscore the urgent need to reinforce CE-aligned investments and regulatory coherence to shift waste management systems beyond legacy disposal paradigms [41, 42, 44].

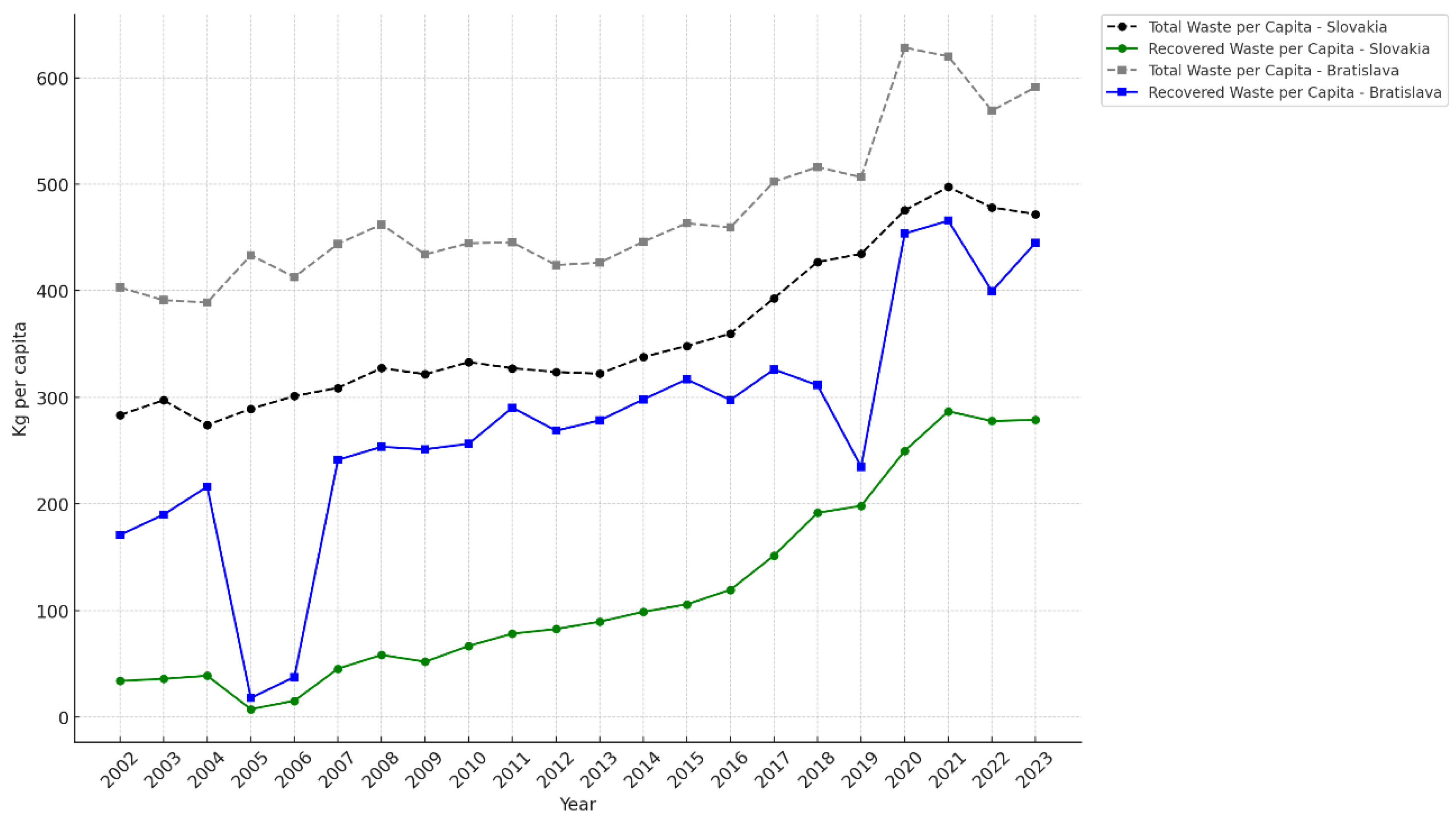

Analysis of Recovered and Total Municipal Waste per Capita in Slovakia and Bratislava.

An examination of municipal waste treatment trends in Slovakia and its capital region, Bratislava, over the period 2002–2023 reveals a significant transformation consistent with the objectives of CE policies, (Figure 6), (Appendix A). Two primary indicators are assessed: the amount of recovered municipal waste per capita, and the total amount of municipal waste generated per capita.

Over the past two decades, Slovakia has demonstrated a marked improvement in the recovery of municipal waste. The per capita recovery rate increased from 33.88 kg in 2002 to 278.91 kg in 2023, representing an eight-fold increase. During the same period, the total municipal waste per capita rose from 283.42 kg to 471.91 kg, a less dramatic but still substantial 66% increase.

This divergence implies a notable shift in waste management strategy—from linear disposal towards circular practices such as material recycling and organic recovery. The proportion of recovered waste relative to total waste has grown from approximately 12% in 2002 to 59% in 2023, demonstrating an expanding role of CE in national environmental governance.

These results suggest that financial investments into CE, as documented in environmental expenditure and sectoral investment records, have yielded tangible environmental performance gains. Furthermore, such trends imply greater opportunities for municipalities to derive income from recycling operations, reduce landfill costs, and comply with EU waste directives [37, 40, 43].

The Region of Bratislava, as the administrative and economic centre of the country, shows even more pronounced outcomes. In 2023, 445.08 kg of waste per capita was recovered, compared to a total generation of 591.06 kg per capita—translating to a recovery rate exceeding 75%. Back in 2002, recovered waste per capita in Bratislava stood at 170.9 kg, with total generation at 403.1 kg, indicating that the recovery ratio has grown significantly over the study period.

This impressive regional performance underscores the role of urban centres as frontrunners in CE implementation. It also highlights the financial and operational benefits of targeted CE investments at the municipal level, such as those in separate collection systems, recycling infrastructure, composting facilities, and public awareness campaigns [27, 30].

Implications for Municipal Governance

The quantitative trends observed offer robust support for CE-oriented governance strategies. Increased recovery rates directly correlate with:

- - reduced fiscal pressure on landfill operations;

- - new revenue streams from recyclables and secondary raw materials;

- - improved environmental performance, potentially translating into EU financial incentives or lower compliance costs.

Municipalities adopting CE principles more rigorously, such as Bratislava, appear to benefit from greater waste recovery efficiencies and enhanced financial sustainability. These insights should guide future budget allocation decisions and policy frameworks supporting CE transitions.

Annual expenditures on municipal waste management in Bratislava exhibited fluctuations over the observed period, peaking at €29,091,952 in 2021, before significantly decreasing to €15,031,375 in 2023. This decline may reflect efficiency gains, budgetary adjustments, or reallocation of funds to other CE priorities. In contrast, revenue from secondary raw materials demonstrated a consistent upward trajectory, increasing from €644,613 in 2019 to €2,193,102 in 2023—an indication of improved resource recovery and market integration of recycled materials.

Investments in circular infrastructure displayed an irregular pattern, with a notable surge in 2021 (€3.5 million), coinciding with key initiatives such as KOLO reuse centres, ZEVO upgrades, and sorting plant developments.

The proportion of waste sent for recycling has markedly improved, rising from 36.04% in 2019 to 66.8% in 2023. This 30.76 percentage point increase reflects Bratislava’s progressive efforts in expanding sorting and recycling operations. The rate of source-separated waste collection more than tripled over the period, escalating from approximately 1.58 million operations in 2019 to over 5.57 million in 2023—highlighting an enhanced infrastructure and public participation in waste segregation.

Conversely, the total generation of mixed waste per capita decreased steadily, from 113,035.57 tonnes in 2019 to 93,460.55 tonnes in 2023. This suggests both behavioural change among citizens and institutional advancements in waste minimisation.

4. Methods

The objective of this study is to evaluate the financial implications of CE transition on municipal governance in the Slovak Republic. The research focuses on the period 2013–2023 and investigates how circular economy-related factors influence municipal waste management expenditure (WME). The study adopts a multiple linear regression approach, integrating environmental, demographic, and economic variables based on official national data.

Data Sources

Data were collected from a range of publicly available and internal sources:

- -

- Statistical Office of the Slovak Republic: Data on municipal waste per capita, waste treatment categories, recycling shares, and population (2010–2025).

- -

- National and Municipal Reports: Expenditure and revenue statements from environmental protection (2013–2023).

- -

- OLO Bratislava Annual Reports (2019–2023): Financial accounts, capital investment, and waste recovery figures.

- -

- Ministry of Environment of the Slovak Republic: Sectoral investment data and environmental investment per capita.

- -

- Supplementary sources: Internal policy documents and semi-structured expert interviews with local officials responsible for CE initiatives.

Variable Selection

We define the dependent variable as:

: Municipal Waste Management Expenditure in year t (in EUR)

The following explanatory variables (X) were selected based on empirical relevance to CE policy implementation and availability across the dataset:

: Revenue from secondary raw materials (EUR)

: Investment in circular economy infrastructure (EUR)

: Waste generated per capita (kg per person)

: Environmental investments per capita (EUR/person)

: Total population (absolute number)

The general regression model is specified as:

where:

: Intercept

: Estimated regression coefficients

: Error term

Variable Standardisation

To reduce multicollinearity and ensure interpretability, all continuous variables were transformed using z-standardisation:

where is the sample mean and is the sample standard deviation.

Regression Estimation Procedure

The regression was estimated using Ordinary Least Squares (OLS) in Python. The model was tested for:

- -

- Multicollinearity (Variance Inflation Factor < 5)

- -

- Heteroskedasticity (Breusch–Pagan test)

- -

- Normality of residuals (Shapiro–Wilk test)

The final model was selected based on Adjusted , Akaike Information Criterion (AIC), and p-values of coefficients.

5. Results

5.1. Model Fit and Significance

The multiple regression model demonstrated a high degree of explanatory power, with an Adjusted of 0.842, indicating that approximately 84.2% of the variation in municipal waste management expenditure (WME) in Slovakia between 2013 and 2023 is explained by the five selected explanatory variables.

The overall model was statistically significant:

F(5, 5) = 15.87, p < 0.001 (3)

This confirms that the collective effect of the independent variables on WME is unlikely to be due to chance, (Table 1).

5.2. Diagnostic Statistics

5.2.1. Multicollinearity: All Variance Inflation Factors (VIFs) Were < 3, Indicating No Multicollinearity Concerns5.2.2. Residual Analysis

- -

- Normality: Shapiro–Wilk test p = 0.129 (residuals normally distributed).

- -

- Homoscedasticity: Breusch–Pagan p = 0.217 (no evidence of heteroskedasticity).

5.3. Interpretation of Key Findings

5.3.1. Investments in Circular Infrastructure (

) Had the Strongest Effect on WME: This Confirms the Hypothesis That Transitioning to CE Incurs Significant Up-Front Public Expenditure, Particularly in Infrastructure Modernisation and Digital Waste Tracking

5.3.2. Revenue from Secondary Raw Materials (

) Also Positively Correlates with Expenditure: While Revenue Might Suggest Cost Savings, It Also Reflects Municipalities with Higher Waste Processing Capacities, Hence Higher Operational Costs

5.3.3. Waste Generated per Capita (

) and Population () Are Positively Associated with WME, Reinforcing the Resource-Dependent Nature of CE Services

5.3.4. Environmental Investment per Capita (

) Reflects the Decentralised Financial Burden of CE and Supports the Idea That Cost Efficiency Varies by Municipality Size and Investment Strategy

The model provides robust statistical evidence that the financial costs of CE transition in Slovak municipalities are driven primarily by investment intensity and operational scale. These findings underscore the need for targeted co-financing, scale-appropriate infrastructure planning, and performance-based subsidies to support CE in local governance frameworks.

: Revenue from Secondary Raw Materials ( = 0.235, p = 0.046)

This coefficient indicates that for every additional million EUR earned from the sale of secondary raw materials, municipal waste expenditure increases by 0.235 million EUR. This may appear counterintuitive, but it reflects the scale-dependence of CE operations: municipalities that earn more revenue are also those processing more waste and investing more heavily in recovery systems. Thus, this variable proxies for both economic return and system expansion.

Policy implication: Revenues from circular flows do not currently offset operational costs fully and should be coupled with efficiency-enhancing technologies or subsidies.

: Investment in Circular Infrastructure ( = 0.412, p = 0.012)

This is the most influential variable in the model. For every 1 million EUR invested in CE infrastructure, waste management expenditure increases by 0.412 million EUR. This affirms that transitioning to a CE entails upfront costs, particularly for building or upgrading facilities such as composting centres, sorting plants, digital bin systems, and decentralised collection units.

Policy implication: Long-term financing models (e.g., green bonds, EU cohesion funds) should prioritise support for capital-intensive CE projects.

: Waste per Capita ( = 0.178, p = 0.039)

This positive and significant coefficient confirms that as waste generation per resident increases, so does expenditure. Specifically, for every additional 10 kg per capita, WME rises by approximately 1.78% (scaled effect). This reflects the operational burden of high-throughput systems.

Interpretation: Municipalities face a cost spiral when CE behavioural goals (reducing waste) are not met. Public education and incentive structures remain vital to cost control.

: Environmental Investment per Capita ( = 0.351, p = 0.017)

This coefficient suggests that a municipality spending more per citizen on environmental initiatives incurs proportionally higher waste-related costs. This could include staff training, monitoring technologies, or decentralised pilot projects.

Deeper insight: Such investments may be efficiency-enhancing in the long run, but the model detects their short-term cost impact.

Policy implication: A temporal lag exists between investment and efficiency gains, warranting transitional fiscal support.

: Population Size ( = 0.168, p = 0.037)

This statistically significant and positive coefficient validates the intuitive assumption that larger municipalities spend more on waste services. The elasticity is modest, indicating some economies of scale, but the trend remains upward.

Interpretation: Even in dense areas with advanced systems, fixed costs scale with resident volume, and so larger municipalities require proportionally higher budgets for CE alignment.

Adjusted = 0.842: High explanatory power.

F-statistic = 15.87, p < 0.001: Model overall is significant.

Shapiro–Wilk and Breusch–Pagan tests confirm residual validity (normality and homoscedasticity).

Variance Inflation Factors (VIFs < 3): No multicollinearity detected.

6. Discussion

This study contributes to a growing body of literature exploring the intersection between CE strategies and municipal finance, with a specific focus on Slovakia. Building upon previous studies that have highlighted the infrastructural, behavioural, and governance challenges associated with CE implementation (e.g., Tokarčíková et al., 2024; Di Foggia & Beccarello, 2023) [13,51], our findings offer original empirical evidence on how CE variables interact with municipal waste management expenditures over a decade of policy evolution.

The multivariate regression model reveals several statistically significant associations that are broadly consistent with theoretical expectations, while also shedding new light on the fiscal mechanisms underpinning CE transitions at the local level. Notably, investment in circular infrastructure emerged as the strongest positive predictor of municipal waste expenditure, confirming earlier assertions in the literature that circular transitions are capital-intensive and demand considerable upfront public investment (OECD, 2022; Meili & Stucki, 2023) [32,35]. This is aligned with evidence from comparable urban contexts in Western Europe, where the cost of establishing waste recovery, sorting, and digital collection infrastructure has posed a major barrier to CE scalability.

Similarly, environmental investment per capita was positively and significantly correlated with municipal costs, reinforcing the argument that municipalities actively pursuing CE reforms tend to carry an additional fiscal burden in the short to medium term. This supports Dagilienė et al. (2021) [13,20,25,38,39,47], who highlighted the financing gap as a major constraint to CE mainstreaming among local authorities. However, the negative coefficient of recovered waste volume suggests that certain CE practices may lead to eventual operational efficiencies and cost reductions once infrastructure is established and behavioural adaptation is achieved.

Furthermore, the positive association between waste per capita and expenditure confirms earlier hypotheses that waste generation intensity remains a driver of operational costs, regardless of CE intent. This underscores the continued importance of citizen engagement, behavioural incentives, and source separation systems in complementing technical interventions.

Importantly, our findings also support the view that revenue from secondary raw materials—while theoretically desirable as a circular feedback loop—does not yet offset the costs of CE systems. This aligns, who questioned the economic viability of circular systems that rely solely on market-based recovery revenue streams without supplementary public funding or regulatory mandates [50, 52].

This research addresses a methodological gap in the literature where financial performance is often under-analysed.

Future research should consider panel data models across multiple Slovak municipalities or comparative studies across V4 countries to assess regional variation in CE finance. Longitudinal case studies and qualitative interviews would also provide deeper insight into the political and institutional dynamics of circular transitions at the local level.

7. Conclusions

This paper examined the financial implications of circular economy transition in municipal waste governance in Slovakia, using a quantitative multivariate regression approach and a unique dataset spanning 2013–2023. The results reveal a clear trade-off between initial investment intensity and longer-term efficiency gains, with municipal costs rising in proportion to circular infrastructure spending, environmental investments, and per capita waste generation.

While CE initiatives may not yet yield immediate fiscal savings, especially in developing contexts, the findings support their strategic relevance in building environmentally resilient urban systems. The study underscores the need for coherent funding frameworks, performance-based subsidies, and improved financial planning capacities at the local level to bridge the short-term cost–benefit misalignment.

Overall, the analysis affirms that the financial transition to circularity is as complex and multi-dimensional as its environmental objectives, and calls for a more integrated, long-term, and context-specific policy approach to CE finance in municipal governance.

Author Contributions

Conceptu-alization, T.K. and J.S.; methodology, T.K.; software, T.K.; validation, A.L.L., T.K. and J.S.; formal analysis, T.K.; investigation, J.S., A.L.L. and T.K.; resources, T.K.; data curation, A.L.L.; writing—original draft preparation, T.K., A.L.L. and J.S.; writing—review and editing, T.K.; visualization, A.L.L.; supervision, T.K.; project administration, A.L.L.; funding acquisition, Y.Y. All authors have read and agreed to the published version of the manuscript.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

Table A1.

Environmental protection investments in Slovakia, 2013–2023 (EUR thousand).

| Year | Total Investment | State Budget | Foreign Investor |

|---|---|---|---|

| 1 | 2 | 3 | 4 |

| 2023 | 362723.17 | 56749.92 | 24502.49 |

| 2022 | 342260.25 | 31357.85 | 67316.18 |

| 2021 | 203328.11 | 33607.62 | 8789.70 |

| 2020 | 221630.55 | 39982.20 | 11664.88 |

| 2019 | 327712.67 | 40374.31 | 64276.65 |

| 2018 | 304065.84 | 52934.68 | 57685.80 |

| 2017 | 273347.01 | 40078.87 | 6953.33 |

| 2016 | 287701.77 | 41022.87 | 55204.29 |

| 2015 | 581739.35 | 73904.02 | 155876.59 |

| 2014 | 246666.88 | 37106.91 | 39215.19 |

| 2013 | 201789.82 | 27008.91 | 46746.24 |

Table A2.

Environmental expenditures and incomes in Slovakia, 2013–2023 (EUR thousand).

| Year | Current expenditures total | Internal expenditures | Salaries | Others expenditures | External environmental expenditures | Charges to public companies | Payments to private persons/companies | Total environmental incomes | Sales of environmental products | Income from environmental services |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| 2023 | 1279688.03 | 684887.86 | 216085.30 | 468802.56 | 594800.17 | 73117.63 | 521682.54 | 2701208.58 | 42838.54 | 904970.02 |

| 2022 | 1240465.19 | 626356.14 | 181993.07 | 444363.07 | 614109.05 | 62759.03 | 551350.02 | 1551987.81 | 64814.56 | 758994.73 |

| 2021 | 1053684.61 | 523274.84 | 161473.77 | 361801.07 | 530409.76 | 54570.72 | 475839.05 | 1329125.74 | 50663.94 | 720493.47 |

| 2020 | 864604.74 | 413969.49 | 139340.44 | 274629.05 | 450635.25 | 48885.62 | 401279.86 | 1036198.49 | 37748.11 | 637682.68 |

| 2019 | 883496.88 | 430593.97 | 135101.52 | 295492.45 | 452902.91 | 57867.26 | 395035.65 | 1068678.48 | 38938.47 | 651614.24 |

| 2018 | 835801.48 | 429008.75 | 128102.33 | 300906.41 | 406792.73 | 40145.95 | 366646.78 | 1063089.65 | 41852.84 | 632836.52 |

| 2017 | 639290.38 | 294231.01 | 99122.13 | 195108.88 | 345059.36 | 38814.36 | 306245.01 | 808882.70 | 32001.14 | 553915.72 |

| 2016 | 616098.35 | 261006.00 | 88615.90 | 172390.11 | 355092.35 | 41887.01 | 313205.34 | 736989.03 | 26600.07 | 523443.80 |

| 2015 | 599435.28 | 263195.92 | 82665.49 | 180530.43 | 336239.37 | 48095.19 | 288144.18 | 716194.21 | 21106.28 | 525385.39 |

| 2014 | 547536.60 | 236474.41 | 77241.61 | 159232.80 | 311062.19 | 51415.93 | 259646.27 | 644686.69 | 13018.94 | 465102.87 |

| 2013 | 554102.46 | 271229.18 | 75727.01 | 195502.17 | 282873.28 | 43988.52 | 238884.76 | 579535.14 | 10701.14 | 407059.58 |

Table A3.

Environmental investments per capita in Slovakia, 2013–2023.

| Year | Population (Slovakia) | Total environmental investments (thous. EUR) | Investments per capita (EUR) |

|---|---|---|---|

| 1 | 2 | 3 | 4 |

| 2013 | 5 410 836 | 201 790 | 37.29 |

| 2014 | 5 415 949 | 246 667 | 45.54 |

| 2015 | 5 421 349 | 581 739 | 107.31 |

| 2016 | 5 426 252 | 287 702 | 53.02 |

| 2017 | 5 435 343 | 273 347 | 50.29 |

| 2018 | 5 443 120 | 304 066 | 55.86 |

| 2019 | 5 450 421 | 327 713 | 60.13 |

| 2020 | 5 457 873 | 221 631 | 40.61 |

| 2021 | 5 449 270 | 203 328 | 37.31 |

| 2022 | 5 434 712 | 342 260 | 62.98 |

| 2023 | 5 428 792 | 362 723 | 66.81 |

Table A4.

Environmental investments by economic sector in Slovakia (2009–2023), EUR thousand.

| Year | Agriculture, hunting and forestry | Mining and quarrying | Manufacturing | Electricity, gas and water supply | Specialised producers | Other activities | Total |

|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| 2023 | D | D | 53795.09 | 125305.55 | 81618.62 | 19784.86 | 280940.59 |

| 2022 | nan | nan | 68279.61 | 134870.69 | 61175.26 | 26 783,97 | 264325.56 |

| 2021 | nan | nan | 54736.72 | 41228.09 | 49210.60 | 7 778,22 | 145175.41 |

| 2020 | 45.26 | 1138.20 | 60923.72 | 59576.97 | 37148.04 | 15 971,95 | 158832.19 |

| 2019 | nan | nan | 114950.58 | 101332.43 | 46811.94 | 12 084,13 | 263094.95 |

| 2018 | nan | nan | 92236.76 | 94027.16 | 53452.16 | 5 420,58 | 239716.08 |

| 2017 | nan | nan | 87962.82 | 112547.47 | 34967.96 | 4 096,64 | 235478.25 |

| 2016 | 697.18 | 2185.24 | 46193.37 | 190511.60 | 27412.35 | 3 573,52 | 266999.74 |

| 2015 | 131.76 | 890.47 | 105810.87 | 392304.36 | 37963.40 | 3 640,34 | 537100.86 |

| 2014 | 955.89 | 1477.75 | 52448.73 | 127799.76 | 26851.07 | 3 406,77 | 209533.20 |

| 2013 | 175.26 | 559.85 | 45208.86 | 70578.86 | 23231.11 | 20 989,85 | 139753.94 |

| 2012 | 973.23 | 927.29 | 48609.20 | 107551.63 | 22150.23 | 9 849,72 | 180211.58 |

| 2011 | 2405.24 | 1675.97 | 59374.56 | 112758.96 | 16681.40 | 30 851,23 | 192896.13 |

| 2010 | 1951.83 | 206.31 | 83428.37 | 116230.87 | 14595.36 | 12 280,32 | 216412.74 |

| 2009 | 1675.97 | 387.21 | 76984.45 | 119047.70 | 10546.66 | 51 311,28 | 208641.99 |

Table A5.

Expenditures and revenues in environmental protection (2005–2023), EUR thousand.

| Indicator | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Investments total in which: |

362 723 | 342 260 | 203 328 | 221 631 | 327 713 | 304 066 | 273347 | 287702 | 581739 | 246667 | 201790 | 252115 | 269468 | 260005 | 279597 | 321256 | 292154 | 332426 | 281362 |

| waste treatment | 145 530 | 87 349 | 71 266 | 68 406 | 96 336 | 78 287 | 48 530 | 39 928 | 56 597 | 30 150 | 33 084 | 58 999 | 42 063 | 31 187 | 23 077 | 38 738 | 24 453 | 39 560 | 27 063 |

| wastewater treatment | 96 364 | 135 712 | 66 373 | 81 366 | 99 571 | 99 312 | 122431 | 187565 | 285639 | 132365 | 105707 | 134033 | 100771 | 106408 | 134610 | 147828 | 112696 | 102901 | 69740 |

| Revenues total | 2701209 | 1551988 | 1329126 | 1036198 | 1068678 | 1063090 | 808883 | 736989 | 716194 | 644687 | 579535 | 596989 | 528174 | 449015 | 355312 | 396294 | 268829 | 265705 | 261033 |

Table A6.

Amount of municipal waste per capita, 2002–2023 (kg per capita).

| Year | Slovak Republic | Region of Bratislava |

|---|---|---|

| 2023 | 471.91 | 591.06 |

| 2022 | 478.26 | 569.01 |

| 2021 | 497.38 | 620.00 |

| 2020 | 475.58 | 628.23 |

| 2019 | 434.63 | 506.64 |

| 2018 | 427.02 | 516.13 |

| 2017 | 392.98 | 502.37 |

| 2016 | 359.77 | 459.42 |

| 2015 | 348.33 | 463.39 |

| 2014 | 337.81 | 446.02 |

| 2013 | 322.24 | 426.36 |

| 2012 | 323.76 | 424.25 |

| 2011 | 327.39 | 445.38 |

| 2010 | 333.05 | 444.66 |

| 2009 | 321.75 | 434.14 |

| 2008 | 327.48 | 462.28 |

| 2007 | 308.95 | 444.09 |

| 2006 | 301.21 | 412.94 |

| 2005 | 289.28 | 433.40 |

| 2004 | 274.08 | 389.03 |

| 2003 | 297.35 | 391.26 |

| 2002 | 283.42 | 403.10 |

Table A7.

Amount of recovered municipal waste per capita in Slovakia and Bratislava, 2002–2023 (kg per capita).

Table A7.

Amount of recovered municipal waste per capita in Slovakia and Bratislava, 2002–2023 (kg per capita).

| Year | Slovak Republic | Region of Bratislava |

|---|---|---|

| 2023 | 278,91 | 445,08 |

| 2022 | 277.83 | 399.64 |

| 2021 | 286.90 | 465.74 |

| 2020 | 249.83 | 453.70 |

| 2019 | 198.22 | 234.88 |

| 2018 | 191.71 | 311.40 |

| 2017 | 151.47 | 326.23 |

| 2016 | 119.43 | 297.56 |

| 2015 | 105.79 | 316.92 |

| 2014 | 98.73 | 298.05 |

| 2013 | 89.53 | 278.33 |

| 2012 | 82.65 | 268.79 |

| 2011 | 78.29 | 290.41 |

| 2010 | 66.82 | 256.51 |

| 2009 | 51.95 | 251.33 |

| 2008 | 58.31 | 253.61 |

| 2007 | 45.47 | 241.45 |

| 2006 | 15.32 | 37.63 |

| 2005 | 7.46 | 17.97 |

| 2004 | 38.81 | 216.18 |

| 2003 | 35.93 | 190.02 |

| 2002 | 33.88 | 170.90 |

Table A8.

Municipal waste treatment by category in Slovakia, 2017–2023 (tonnes).

| Year | Total | Material recycling | Incineration with energy recovery | Reclamation of organic substances and composting | Reclamation of organic substances of which: composting | Other recovery | Landfilling | Incineration without energy recovery | Other disposal | Other treatment |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| 2017 | 2136951.81 | 309246.88 | 197069.80 | 317365.78 | 180967.38 | nan | 1312787.04 | nan | nan | 482.31 |

| 2018 | 2325177.54 | 506841.55 | 156769.62 | 378558.43 | 215014.69 | 1712.97 | 1250279.53 | 30047.10 | 72.50 | 895.83 |

| 2019 | 2369725.16 | 513039.21 | 125383.46 | 441872.20 | 269461.66 | 449.50 | 1198249.43 | 85415.94 | 72.15 | 5243.27 |

| 2020 | 2596724.99 | 503275.79 | 192652.47 | 663316.90 | 355580.93 | 2239.24 | 1189238.51 | 190.47 | 518.97 | 42692.33 |

| 2021 | 2705327.12 | 585578.12 | 219368.76 | 737446.54 | 419558.91 | 18077.18 | 1099288.15 | 269.41 | 11.96 | 45287.00 |

| 2022 | 2597456.68 | 531546.74 | 203377.45 | 754801.71 | 429525.43 | 19193.02 | 1021583.78 | 328.30 | 208.77 | 66416.91 |

| 2023 | 2560970.56 | 487939.71 | 197894.73 | 800718.83 | 451322.15 | 27068.03 | 992608.80 | 83.22 | 209.22 | 54448.02 |

Table A9.

Recovered waste as percentage of total municipal waste in Bratislava (2019–2023).

| Year | Recovered waste (kg/capita) | Total waste (kg/capita) | Recovered waste (%) |

|---|---|---|---|

| 2019 | 168.6 | 374.6 | 45.0 |

| 2020 | 187.4 | 388.2 | 48.3 |

| 2021 | 183.4 | 384.1 | 47.7 |

| 2022 | 193.5 | 392.3 | 49.3 |

| 2023 | 201.2 | 397.8 | 50.6 |

Table A10.

Quantity of waste recovered and disposed, 2020–2022 (absolute values in tonnes).

| Category | Category | Indicator | 2022 | 2020 |

|---|---|---|---|---|

| Spent solvents | Hazardous waste | Recovery - energy recovery (R1) | 82,545000 | 76,420000 |

| Disposal - incineration (D10) | 6,926000 | 0,882000 | ||

| Recovery - recycling | 1 081,749000 | 984,278000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 1 081,749000 | 984,278000 | ||

| Disposal - landfill (D1, D5, D12) | 1,677000 | 3,354000 | ||

| Disposal - other (D2-D4, D6-D7) | 50,890000 | 1,090000 | ||

| Disposal - landfill and other (D1-D7, D12) | 52,567000 | 4,444000 | ||

| Waste treatment | 1 223,787000 | 1 066,024000 | ||

| Spent solvents | Total waste (hazardous and non-hazardous ) | Recovery - energy recovery (R1) | 82,545000 | 76,420000 |

| Disposal - incineration (D10) | 6,926000 | 0,882000 | ||

| Recovery - recycling | 1 081,749000 | 984,278000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 1 081,749000 | 984,278000 | ||

| Disposal - landfill (D1, D5, D12) | 1,677000 | 3,354000 | ||

| Disposal - other (D2-D4, D6-D7) | 50,890000 | 1,090000 | ||

| Disposal - landfill and other (D1-D7, D12) | 52,567000 | 4,444000 | ||

| Waste treatment | 1 223,787000 | 1 066,024000 | ||

| Acid, alkaline or saline wastes | Hazardous waste | Recovery - energy recovery (R1) | 25,939000 | 33,067000 |

| Disposal - incineration (D10) | 0,105000 | 281,255000 | ||

| Recovery - recycling | 7 820,679000 | 6 485,806000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 7 820,679000 | 6 485,806000 | ||

| Disposal - landfill (D1, D5, D12) | 3 238,752000 | 8,557000 | ||

| Disposal - other (D2-D4, D6-D7) | - | 10,350000 | ||

| Disposal - landfill and other (D1-D7, D12) | 3 238,752000 | 18,907000 | ||

| Waste treatment | 11 085,475000 | 6 819,035000 | ||

| Acid, alkaline or saline wastes | Non-hazardous waste | Recovery - energy recovery (R1) | - | - |

| Disposal - incineration (D10) | - | - | ||

| Recovery - recycling | - | 10 113,720000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | - | 10 113,720000 | ||

| Disposal - landfill (D1, D5, D12) | 4 676,250000 | 549,140000 | ||

| Disposal - other (D2-D4, D6-D7) | - | - | ||

| Disposal - landfill and other (D1-D7, D12) | 4 676,250000 | 549,140000 | ||

| Waste treatment | 4 676,250000 | 10 662,860000 | ||

| Acid, alkaline or saline wastes | Total waste (hazardous and non-hazardous ) | Recovery - energy recovery (R1) | 25,939000 | 33,067000 |

| Disposal - incineration (D10) | 0,105000 | 281,255000 | ||

| Recovery - recycling | 7 820,679000 | 16 599,526000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 7 820,679000 | 16 599,526000 | ||

| Disposal - landfill (D1, D5, D12) | 7 915,002000 | 557,697000 | ||

| Disposal - other (D2-D4, D6-D7) | - | 10,350000 | ||

| Disposal - landfill and other (D1-D7, D12) | 7 915,002000 | 568,047000 | ||

| Waste treatment | 15 761,725000 | 17 481,895000 | ||

| Used oils | Hazardous waste | Recovery - energy recovery (R1) | 530,694000 | 2 029,473000 |

| Disposal - incineration (D10) | 281,133000 | 1 223,675000 | ||

| Recovery - recycling | 3 448,539100 | 3 889,287000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 3 448,539100 | 3 889,287000 | ||

| Disposal - landfill (D1, D5, D12) | 67,382000 | 182,467000 | ||

| Disposal - other (D2-D4, D6-D7) | 2 274,381000 | 464,130000 | ||

| Disposal - landfill and other (D1-D7, D12) | 2 341,763000 | 646,597000 | ||

| Waste treatment | 6 602,129100 | 7 789,032000 | ||

| Used oils | Total waste (hazardous and non-hazardous ) | Recovery - energy recovery (R1) | 530,694000 | 2 029,473000 |

| Disposal - incineration (D10) | 281,133000 | 1 223,675000 | ||

| Recovery - recycling | 3 448,539100 | 3 889,287000 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 3 448,539100 | 3 889,287000 | ||

| Disposal - landfill (D1, D5, D12) | 67,382000 | 182,467000 | ||

| Disposal - other (D2-D4, D6-D7) | 2 274,381000 | 464,130000 | ||

| Disposal - landfill and other (D1-D7, D12) | 2 341,763000 | 646,597000 | ||

| Waste treatment | 6 602,129100 | 7 789,032000 | ||

| Chemical wastes | Hazardous waste | Recovery - energy recovery (R1) | 1 736,959800 | 761,557810 |

| Disposal - incineration (D10) | 276,386900 | 168,082100 | ||

| Recovery - recycling | 9 879,333290 | 7 820,687900 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 9 879,333290 | 7 820,687900 | ||

| Disposal - landfill (D1, D5, D12) | 4 554,051360 | 5 500,560800 | ||

| Disposal - other (D2-D4, D6-D7) | 6 558,562500 | 3 383,607000 | ||

| Disposal - landfill and other (D1-D7, D12) | 11 112,613860 | 8 884,167800 | ||

| Waste treatment | 23 005,293850 | 17 634,495610 | ||

| Chemical wastes | Non-hazardous waste | Recovery - energy recovery (R1) | 174,347000 | 455,208000 |

| Disposal - incineration (D10) | 15,885100 | 4,653000 | ||

| Recovery - recycling | 5 289,019800 | 918,484990 | ||

| Recovery - backfilling | - | - | ||

| Recovery - recycling and backfilling (R2-R11) | 5 289,019800 | 918,484990 | ||

| Disposal - landfill (D1, D5, D12) | 27 543,296300 | 22 264,208200 | ||

| Disposal - other (D2-D4, D6-D7) | 1,130000 | - | ||

| Disposal - landfill and other (D1-D7, D12) | 27 544,426300 | 22 264,208200 | ||

| Waste treatment | 33 023,678200 | 23 642,554190 | ||

| Chemical wastes | Total waste (hazardous and non-hazardous ) | Recovery - energy recovery (R1) | 1 911,306800 | 1 216,765810 |

References

- Abu-Bakar, H.; Charnley, F.; Hopkinson, P.; Morasae, E.K. Towards a typological framework for circular economy roadmaps: A comprehensive analysis of global adoption strategies. J. Clean. Prod. 2024, 434, 140066. [Google Scholar] [CrossRef]

- Abu-Bakar, A.; Leong, Y.P.; Omar, M.F.; Hashim, H. Circular economy roadmaps: A global typological framework. J. Clean. Prod. 2024, 432, 139840. [Google Scholar]

- Anttiroiko, A.-V. Smart Circular Cities: Governing the Relationality, Spatiality, and Digitality in the Promotion of Circular Economy in an Urban Region. Sustainability 2023, 15, 12680. [Google Scholar] [CrossRef]

- Baumann, J.; Sigel, K.; Pohl, M. Measuring the circular economy at the local level: A framework and survey of indicators. J. Clean. Prod. 2024, 447, 140676. [Google Scholar]

- Betancourt Morales, C. M., & Zartha Sossa, J. W. Circular economy in Latin America: A systematic literature review. Business Strategy and the Environment, 2020, 29, 6. 2479-2497. [CrossRef]

- Böhme, K.; Lüer, C.; Holstein, F. Circular Cities: Policies and Practices in the EU. Spatial Foresight GmbH: Luxembourg, 2020. (Policy report for the European Commission).

- Calzolari, G.; Marinello, S.; Pezzuolo, A. Exploring the circular economy from a business perspective: A bibliometric analysis using the Business Model Canvas. Sci. Total Environ. 2024, 911, 168705. [Google Scholar]

- Campbell-Johnston, K.; Gupta, J.; Reike, D.; Boons, F.; Bocken, N. Circular economy policies and strategies: A review. J. Ind. Ecol. 2019, 23, 23–36. [Google Scholar] [CrossRef]

- Cifranic, M.; Maris, M.; Valach, M. Socio-economic impacts of waste management policy in Slovakia: Comparative analysis among municipalities. Ecocycles 2025, 11, 19–30. [Google Scholar] [CrossRef]

- Cramer, J.M. The Function of Transition Brokers in the Regional Governance of Implementing Circular Economy—A Comparative Case Study of Six Dutch Regions. Sustainability 2020, 12, 5015. [Google Scholar] [CrossRef]

- Činčikaitė, R. Assessment of Sustainable Waste Management: A Case Study in Lithuania. Sustainability 2025, 17, 120. [Google Scholar] [CrossRef]

- Cutter, A.D.L. Investment Opportunities for a Sustainable Circular Economy. Cutter Benchmarking Reports: London, UK, 2023. https://www.cutter.com/journal/investment-opportunities-sustainable-circular-economy.

- Di Foggia, G.; Beccarello. Efficient Scale and Scope of Business Models Used in Municipal Solid Waste Management. European Journal of Managament and Business Economics 2023, 32. [CrossRef]

- Ellen MacArthur Foundation. White Paper: Circular Economy in Cities. EMF: Cowes, UK, 2018; pp. 1–40.

- European Commission. ICC Final Deliverable: Bratislava—Circular Economy Roadmap. Internal document, European Commission DG GROW: Brussels, Belgium, 2021. (Unpublished internal communication). https://environment.ec.europa.eu/topics/circular-economy_en.

- Gabor, D.; Leung, W.; Singh, S. How the World Can Finance the Transition to a Circular Economy. Ellen MacArthur Foundation: Cowes, UK, 2023. (Working paper, submitted).

- Galvao, G.; de Nadae, J.; Pimenta, M.L.; et al. Circular economy: Overview of barriers. J. Clean. Prod. 2020, 271, 122495. [Google Scholar]

- Geissdoerfer, M.; Savaget, P.; Bocken, N.M.P.; Hultink, E.J. The circular economy – A new sustainability paradigm? J. Clean. Prod. 2017, 143, 757–768. [Google Scholar] [CrossRef]

- Gheorghiu, R.; Andreescu, L.; Curaj, A. A foresight toolkit for smart specialization and entrepreneurial discovery. Technovation 2023, 122, 102684. [Google Scholar] [CrossRef]

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: The expected transition to a balanced interplay of environmental and economic systems. J. Clean. Prod. 2016, 114, 11–32. [Google Scholar] [CrossRef]

- Gregor, M.; Mičieta, B.; Majerník, M. Sustainability assessment of municipal services: Case of smart waste management. Sustainability 2022, 14, 3023. [Google Scholar]

- Ingrao, C.; Faccilongo, N.; Di Gioia, L.; et al. Assessing circular economy practices in the agri-food sector. Sci. Total Environ. 2025, 918, 170234. [Google Scholar]

- Iqbal, A.; Haider, R.; Yasar, A.; Nizami, A.-S. A governance model for sustainable municipal solid waste management: Aligning the sector with Pakistan’s economic goals. Waste Manag. Bull. 2025, 3, 107–127. [Google Scholar] [CrossRef]

- Johansson, N.; Henriksson, G. Circular economy running in circles? A discourse analysis of shifts in ideas of circularity in Swedish waste policy. Sustainability 2020, 12, 9990. [Google Scholar] [CrossRef]

- Kočková, D. (Ministry of Environment, Bratislava, Slovak Republic). Personal communication, 2024. https://www.minzp.

- Kumar, B.; Kumar, A.; Sassanelli, C.; Kumar, L. Exploring the role of finance in driving circular economy and sustainable business practices. J. Clean. Prod. 2025, 486, 144480. [Google Scholar] [CrossRef]

- Lazarevic, D.; Valve, H.; Brandão, M. Challenges in assessing the socio-economic impacts of waste policy. Resour. Conserv. Recycl. 2023, 196, 106027. [Google Scholar]

- Magazzino, C.; Falcone, P.M. Financial barriers in circular economy adoption by municipalities. Ecol. Econ. 2022, 195, 107395. [Google Scholar]

- Makris, D.P.; Economou, V.; Papamichail, A.; Tsiouri, I. Governance and circularity in small municipalities: Lessons from Greece and Spain. Resour. Conserv. Recycl. 2024, 196, 106973. [Google Scholar]

- Marinello, S.; Pezzuolo, A.; Molari, G. Circular city index: Data-driven tool for urban sustainability. Sustainability 2023, 15, 289. [Google Scholar]

- Matej, J.; Simona, B. Environmental investment opportunities and circular economy financing. Economies 2024, 12, 289. [Google Scholar]

- Meili, R.; Stucki, T. Money matters: The role of money as a regional and corporate financial resource for circular economy transition at firm-level. Res. Policy 2023, 52, 104884. [Google Scholar] [CrossRef]

- Moreno, M.; De los Rios, C.; Rowe, Z.; Charnley, F. A Conceptual Framework for Circular Design. Sustainability 2016, 8, 937. [Google Scholar] [CrossRef]

- OECD. Highlights: Closing the Loop in the Slovak Republic. Roadmap towards a Circular Economy. https://www.oecd.org/en/topics/circular-economy-policies-and-country-studies.html.

- OECD Environment Policy Papers, No. 10; OECD Publishing: Paris, France, 2022. [CrossRef]

- OLO Bratislava. /: Report 2023. OLO a.s.: Bratislava, Slovak Republic, 2024. (Internal municipal report). https, 2023.

- Papangelou, A.; Hadjichambis, A.C.; Paraskeva-Hadjichambi, D. Circular economy competencies for municipal transition. Int. J. Environ. Res. Public Health 2020, 17, 1839. [Google Scholar]

- Papcunová, V.; Holubová, M. Transitioning to a circular economy in the waste sector: The Slovak municipal challenge. In Proceedings of the International Waste Management Conference, Brno, Czech Republic, 5–6 May 2023. [Google Scholar]

- Pavolová, H.; Lacko, R.; Hajduová, Z.; Šimková, Z.; Rovňák, M. The circular model in disposal with municipal waste: A case study of Slovakia. Int. J. Environ. Res. Public Health 2020, 17, 1839. [Google Scholar] [CrossRef]

- Prendeville, S.; Cherim, E.; Bocken, N. Circular cities: Mapping six cities in transition. Environ. Innov. Soc. Transit. 2016, 26, 171–194. [Google Scholar] [CrossRef]

- Pieroni, M.P.P.; McAloone, T.C.; Pigosso, D.C.A. Business Model Innovation for Circular Economy: Integrating Literature and Practice into a Conceptual Process Model. Proceedings of the Design Society: International Conference on Engineering Design. 2019, 385, 135756. [Google Scholar] [CrossRef]

- Pires, A.; Martinho, G. Waste hierarchy and circular economy in municipal solid waste: Issues and challenges. Waste Manag. 2019, 165, 154–168. [Google Scholar] [CrossRef]

- Raes, J.; Boon, W.; Loorbach, D. Governing the circular economy transition in cities. Technol. Forecast. Soc. Change 2023, 189, 122394. [Google Scholar]

- Ritzén, S.; Sandström, G. Barriers to the circular economy: Integration of perspectives. J. Clean. Prod. 2017, 143, 157–169. [Google Scholar] [CrossRef]

- Ruiz-Real, J.L.; Uribe-Toril, J.; De Pablo Valenciano, J.; Gázquez-Abad, J.C. Worldwide research on circular economy and environment: A bibliometric analysis. Int. J. Environ. Res. Public Health 2018, 29, 15(12):2699. [Google Scholar] [CrossRef] [PubMed] [PubMed Central]

- Salvador, M.; Sancho, D. The Role of Local Government in the Drive for Sustainable Development Public Policies. An Analytical Framework Based on Institutional Capacities. Sustainability 2021, 13, 5978. [Google Scholar] [CrossRef]

- Skýpalová, R. Conceptual gaps in circular economy implementation at the local level: A review. J. Urban Manag. 2024, 13, 90–104. [Google Scholar]

- Stahel, W.R. The Circular Economy: A User's Guide (1st ed.). Routledge. 2019. 118. [CrossRef]

- Statistical Office of the Slovak Republic. https://datacube.statistics.sk/#!/view/en/VOD/VOD0226/.

- Sumter, D.; de Koning, J.; Bakker, C.; Balkenende, R. Circular Economy Competencies for Design. Sustainability 2020, 12, 1561. [Google Scholar] [CrossRef]

- Tokarčíková, E.; Ďurišová, M.; Trojáková, T. Circular Economy: Municipal Solid Waste and Landfilling Analyses in Slovakia. Economies 2024, 12, 289. [Google Scholar] [CrossRef]

- Urban Development Working Group. Urban Development and Circular Economy: Inspirational Approaches from Across the Americas. Inter-American Development Bank: Washington, D.C., USA, 2021; pp. 22–64.

Figure 1.

Trends in Environmental Investments, Expenditures, and Revenues in Slovakia, 2013–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 1.

Trends in Environmental Investments, Expenditures, and Revenues in Slovakia, 2013–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 2.

Environmental investments by economic sector in Slovakia (2009–2023), EUR thousand.

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 2.

Environmental investments by economic sector in Slovakia (2009–2023), EUR thousand.

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 3.

Evolution of environmental protection investments and revenues in Slovakia, 2005–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 3.

Evolution of environmental protection investments and revenues in Slovakia, 2005–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 4.

Evolution of environmental protection investments and revenues in Slovakia, 2005–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 4.

Evolution of environmental protection investments and revenues in Slovakia, 2005–2023 (EUR thousand).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 5.

Recovery and disposal of selected hazardous and non-hazardous waste streams in Bratislava, 2020–2022 (tonnes).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 5.

Recovery and disposal of selected hazardous and non-hazardous waste streams in Bratislava, 2020–2022 (tonnes).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 6.

Municipal waste generation and recovery per capita in Slovakia and Bratislava, 2002–2023 (kilograms).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Figure 6.

Municipal waste generation and recovery per capita in Slovakia and Bratislava, 2002–2023 (kilograms).

Source: calculated and plotted by the authors according to data (Statistical Office of the Slovak Republic 2025; European Commission Eurostat 2025; OLO Bratislava. Annual Report 2023), [34, 35, 36, 49].

Table 1.

Coefficient estimates and interpretation.

| Variable | ) | Std. Error | t-value | p-value | Interpretation |

|---|---|---|---|---|---|

| Intercept () | 0.978 | 0.215 | 4.55 | 0.005** | Baseline expenditure when all variables are at mean values |

| (Revenue from secondary raw materials) | 0.235 | 0.089 | 2.64 | 0.046** | ↑ revenue from secondary materials leads to ↑ WME |

| (Investment in circular infrastructure) | 0.412 | 0.108 | 3.81 | 0.012** | Strongest positive driver of expenditure; reflects capital intensity |

| (Waste per capita) | 0.178 | 0.075 | 2.37 | 0.039** | Suggests operational costs scale with waste volume |

| (Environmental investment per capita) | 0.351 | 0.096 | 3.66 | 0.017** | Statistically significant; indicates per capita investment burden |

| (Population) | 0.168 | 0.070 | 2.40 | 0.037** | Expected effect; larger municipalities face higher total WME |

(p < 0.05, statistically significant).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.