Submitted:

03 June 2025

Posted:

03 June 2025

You are already at the latest version

Abstract

Aim: The article explores the contributing factors to the decline of auditors globally and aims to provide the consequences and possible recommendations. Auditors play a critical role in ensuring transparency, trust and credibility of financial statements. However, the profession is experiencing a decline across the globe. The decrease in the number of registered auditors has become a pressing issue, raising concerns about the future of the assurance industry’s ability to maintain the number of registered auditors and continue providing assurance services to public and private entities or companies.

Methodology: A scoping review methodology was adopted to analyse existing literature on the global decline of auditors. This approach utilises research evidence to identify trends, challenges, and opportunities within the audit profession. Relevant studies were sourced from databases such as ScienceDirect, Google Scholar, ResearchGate, and grey literature.

Main findings: The study identifies a combination of factors driving the decline of auditors globally. Economic pressures, such as cost reduction initiatives and outsourcing, have impacted demand for traditional auditing services. Complex regulatory requirements have increased barriers to entry, while technological advancements, such as artificial intelligence, are disrupting traditional auditing roles. Additionally, the profession suffers from negative perceptions regarding workload, remuneration, and work-life balance, discouraging new entrants.

Practical implications: The findings emphasise the urgent need for the auditing profession to adapt to evolving challenges. Stakeholders, including regulatory bodies and professional organisations, must address issues such as technological integration, career development pathways, and regulatory simplification. Enhanced public awareness campaigns and training initiatives are critical to attracting and retaining professional talent.

Contribution: This study contributes to the limited body of knowledge on the global decline of auditors by creating a broad spectrum of evidence. It highlights actionable strategies to address the profession's challenges and provides a foundation for future research on sustaining the relevance of auditors in a dynamic global economy.

Keywords:

decline of accountants

; decline of auditors

; emigration

; technology advancements

; regulatory challenges

1. Introduction

Audited financial statements that auditors sign off on are essential for investors, regulators, and other stakeholders, enabling them to make informed business decisions (Olojede et al., 2020) . However, in recent years, we have seen a yearly decline in the number of auditors globally (Caseware, 2024). The decline raises concerns about the assurance industry's ability to have sufficient auditors to provide assurance services to diverse industries. Various factors contribute to the decline of auditors globally, including increased pressure from regulatory bodies, a decrease in the profession's attractiveness to younger generations, technological advancements, and concerns about work-life balance (Harber, 2018, Knechel et al., 2021, Caseware, 2024). The consequences of the decline of auditors may potentially affect audit quality, lack of trust from the public, long-term sustainability of the profession in meeting increased demands by audit clients and insufficient auditors to provide assurance services to society (Harber, 2018).

This study is based on a global context for the decline of auditors, and there are many jurisdictions that govern the audit profession in various countries; however, the study determines the similarities of the contributing factors for the decline of auditors, and these factors are generic worldwide.

On a global level, the shortages have been documented, more than 300,000 accountants in the United States left their jobs in the past two years, resulting in a 17% decrease (Ellis, 2022). Furthermore, in the Times of India, Surray Sood, a practice leader in India, stated that there is a staff shortage as the young generation is less tolerant to the work demands of the profession and, in turn place pressure on existing staff to perform audits that motivates the latter to leave the profession (Sood, 2022).

In addition, Dawkins (2023), stated that undergraduate enrollment in United States colleges and universities has declined due to COVID-19 in 2020. Dawkins further states that there was a 9.4% decline from 2020 to 2022 and a total drop of 2.6 million students in the past decade. Dawkins anticipates that in 2025, there will be an increase followed by a decline due to lower birth rates. Dawkins stated that the American Institute of Certified Public Accountants (AICPA) Trends Report confirmed steady declines in bachelor's, master's and PhD enrollments and that Certified Public Accountant (CPA) examination participation has declined due to the 150 hours requirements and many do not see the credentials as valuable (Dawkins, 2023). These trends show that entry into the profession is on the decline because not many high school leavers are interested in studying for an accounting degree to be able to enter an audit profession.

According to Blood and Yong (2024), the decline persists beyond the USA, and it affects other countries such as Australia, Singapore, Malaysia, New Zealand, and many others that are struggling to attract people to the accounting profession. It further states that non-accountants will eventually be employed to provide services to the public if the shortage is not addressed. According to the 2018 Global SMP Survey by 6,000 respondents, the challenges of the shortage in the accounting profession are due to the lack of candidates, opportunities in other fields and concerns about work-life balance. The Association of Chartered Certified Accountants (ACCA) Global Talent Trend 2023 Report surveyed 8,405 respondents and highlighted various factors contributing to the decline, including dissatisfaction with remuneration, reversing of remote work or lack thereof, burnout was a significant concern due to long work hours and technological advancements (Blood and Yong, 2024).

According to Yiu and Zhong (2023), Clement Chan Kam-wing, chairman of the Hong Kong Association of Registered Public Interest Entity Auditors, warns of a severe talent shortage in Hong Kong's accounting industry. This may hinder firms' ability to perform complex audits and affect Hong Kong's status as a fundraising hub for listed companies. He stated that the government should consider recruiting talent from overseas to address this issue. A survey of 313 Hong Kong-based accounting firms revealed that one in three lacks 20% of the required manpower, with over half actively seeking new hires, potentially leading to South African CAs being recruited by other countries (Yiu and Zhong, 2023).

Notably, the State of Accounting Firms Trends Report for 2023, revealed that over 90% of accountants and 95% of auditors find recruiting skilled talent difficult. The study was conducted globally among 4,100 accountants and 2,300 auditors (Caseware, 2023). CaseWare conducted the 2023 State of Accounting Firms Survey from September to the end of November 2022 (Caseware, 2023). It was offered in three languages, English, Spanish and French, and garnered 4,143 validated survey completions (Caseware, 2023). The report stated that 40.57% of the survey suggested finding and hiring the right talent for accounting and auditing firms is extremely challenging, and 52.23% said it is somewhat challenging (Caseware, 2023).

According to Caseware (2024), adopting new technologies is one of the top three challenges faced in the past year, with 15.4% of respondents ranking it as one of the top three, and 33.1% of respondents stated that the technology adoption plan would increase significantly. The survey was based on various countries worldwide, of which 7.6% of respondents were in South Africa, 3.3% in the Netherlands, 2.9% in Latin America, 3% in Germany, 7.4% in the United Kingdom and 74% in North America. The use of data analytics could reduce the demand for traditional audit roles. The Fourth Industrial Revolution (4IR) will require new skills from the auditor, potentially leading to a decline in the profession due to the 4IR reducing the demand for traditional audit roles. Literature proves that the issue of registered auditors is a global concern, from developed to the developing countries experiencing the same irrespective of the jurisdiction.

Lastly, in South Africa, there has been a decline in overall registered auditors from the period 2019 to 2023 by 11.72%, according to The Independent Regulatory Board for Auditors (2023). The decline is due to numerous factors, from retired auditors to the younger generation not being attracted to the profession, education, and strict regulatory requirements (Harber, 2018).

The prominent research question underpinning this study is: what are the factors that contribute to the decline of auditors globally, its consequences and possible recommendation? To answer this research question, a scoping review is conducted to understand the causes and consequences of this decline and provide possible recommendations, which is crucial to ensuring the sustainability and effectiveness of the assurance industry globally. A structured scoping review allows for a comprehensive synthesis of available academic and industry research, highlighting both well-documented trends and underexplored dimensions (Peters et al., 2020a). The approach also ensures transparency in method and breadth in perspective, capturing both global patterns and South African realities. The findings aim to contribute to existing literature by framing actionable recommendations for regulators and practitioners working to stabilise and revitalise the audit profession.

To underpin this study, behavioural theory is used article as the article will consider the psychological factors that influence auditors' behavior that leads to the reduction of registration and lack of interest in the auditing profession by prospective auditors This theory better explains the underlying attitude that shape a particular human behavior (Garvey et al., 2021). According to Ajzen (1991), there are three different considerations that influence an individual's behaviour: behavioural, normative, and control beliefs. Ajzen (1991) states that behavioural belief is about the outcomes, whether good or bad, and this shapes an individual's attitude towards a behaviour. The behavioural theory underpins this. The theory is popularly used in accounting research see for instance (Merkl-Davies and Brennan, 2017, Minutiello and Tettamanzi, 2024, De Graaf, 2019).

Behavioural theory provides valuable insight into understanding individual and organisational responses to pressures within the auditing profession. It recognises that auditors, like all professionals, are influenced by bounded rationality, cognitive biases, risk aversion, and motivational factors when making decisions. In the context of the auditor shortage, behavioural theory helps explain phenomena such as early career exits, disengagement, and ethical erosion. In accounting research Knechel et al. (2015) applied behavioural theory to examine how individual auditor behaviour affects audit quality under different incentive structures and regulatory environments. Their findings highlight that auditor decisions are not purely technical but are shaped by behavioural responses to external pressures, reinforcing the importance of considering psychological and organisational behaviour dimensions when addressing the sustainability challenges facing the profession.

Note: In this article, the terms “auditors” and “accountants” are used interchangeably where applicable, recognising that many auditors are professionally qualified accountants performing assurance functions in line with global terminology practices.

The next sections of the article deal with the methodology, analyses, findings, gaps and conclusions.

2. Methodology

This study employed a scoping review methodology to investigate the contributing factors to the global decline of auditors, consequences and possible recommendations. The methodology followed the framework proposed by Arksey and O'malley (2005), which has since been enhanced by subsequent contributions from Levac et al. (2010), Peters et al. (2020b) and Anderson et al. (2008). Scoping reviews work well for broad, complex, or less-studied topics, like the changing challenges in the auditing profession. This approach helps gather existing research from various sources. It identifies trends, knowledge gaps, and areas where more research is needed (Arksey and O'malley, 2005, Peters et al., 2020b, Levac et al., 2010).

Scoping reviews differ from systematic reviews because are not limited to a narrow research question or confined to highly specific empirical studies. Instead, they are used to map the range and nature of existing evidence, providing an overview of key concepts and findings within a field (Peters et al., 2020a). This makes scoping review ideal for emerging or complex topics, such as the global auditor shortage, where studies may span academic disciplines, jurisdictions, and methodological approaches. Several prior studies within the fields of accounting and auditing have used scoping reviews to analyse educational trends, digitalisation impacts, and shifts in accounting standards, reinforcing its appropriateness for this research (e.g., (Matshona et al., 2024, Hasan and Miah, 2024, Han et al., 2023, Filip et al., 2017, Sithole et al., 2024)).

This study adhered to the five-stage scoping review process outlined by Arksey and O'malley (2005) and expanded upon by more recent frameworks as mentioned above. The five steps include: (1) identifying the research question, (2) identifying relevant studies, (3) selecting studies using pre-defined inclusion and exclusion criteria, (4) charting the data, and (5) collating, summarising, and reporting the results. Each step is detailed below incorporating how it fits into the study The next section covers these five steps that were taken in conducting this study.

Step 1: Identify the research question.

The research question guiding this review is:

“What are the factors that contribute to the decline of auditors globally, its consequences and possible recommendations?”

This broad but focused question allowed for the inclusion of behavioral theoretical studies from various regions, professions (e.g., chartered accountants, certified public accountants and auditors), and publication types. It also accommodated discussion of contributing factors, consequences and possible recommendations.

Step 2: Identifying relevant studies

To ensure comprehensive coverage, searches were conducted across multiple scholarly databases: ScienceDirect, Scopus, Google Scholar, EBSCOhost, and ProQuest. These databases were selected for their extensive peer-reviewed coverage in business, finance, and social sciences. In line with scoping review standards, grey literature, including industry reports from organisations such as IFAC, ACCA, and IRBA, these reports are useful as it is regulatory compliance reports that govern auditors who require professional regulatory guidance from these regulators.

The search strategy used Boolean operators and combinations of keywords, including:

“decline of auditors”, “auditor shortage”, “audit profession crisis”, “auditor recruitment and retention”, “emigration of auditors”, “regulatory impact on audit profession”, “technology and audit profession”, “audit quality and staffing”

These terms were chosen based on initial exploratory searches and existing literature themes. A keyword matrix was developed to standardise search queries across platforms and minimise omission of relevant sources.

Step 3: Study selection using inclusion and exclusion criteria

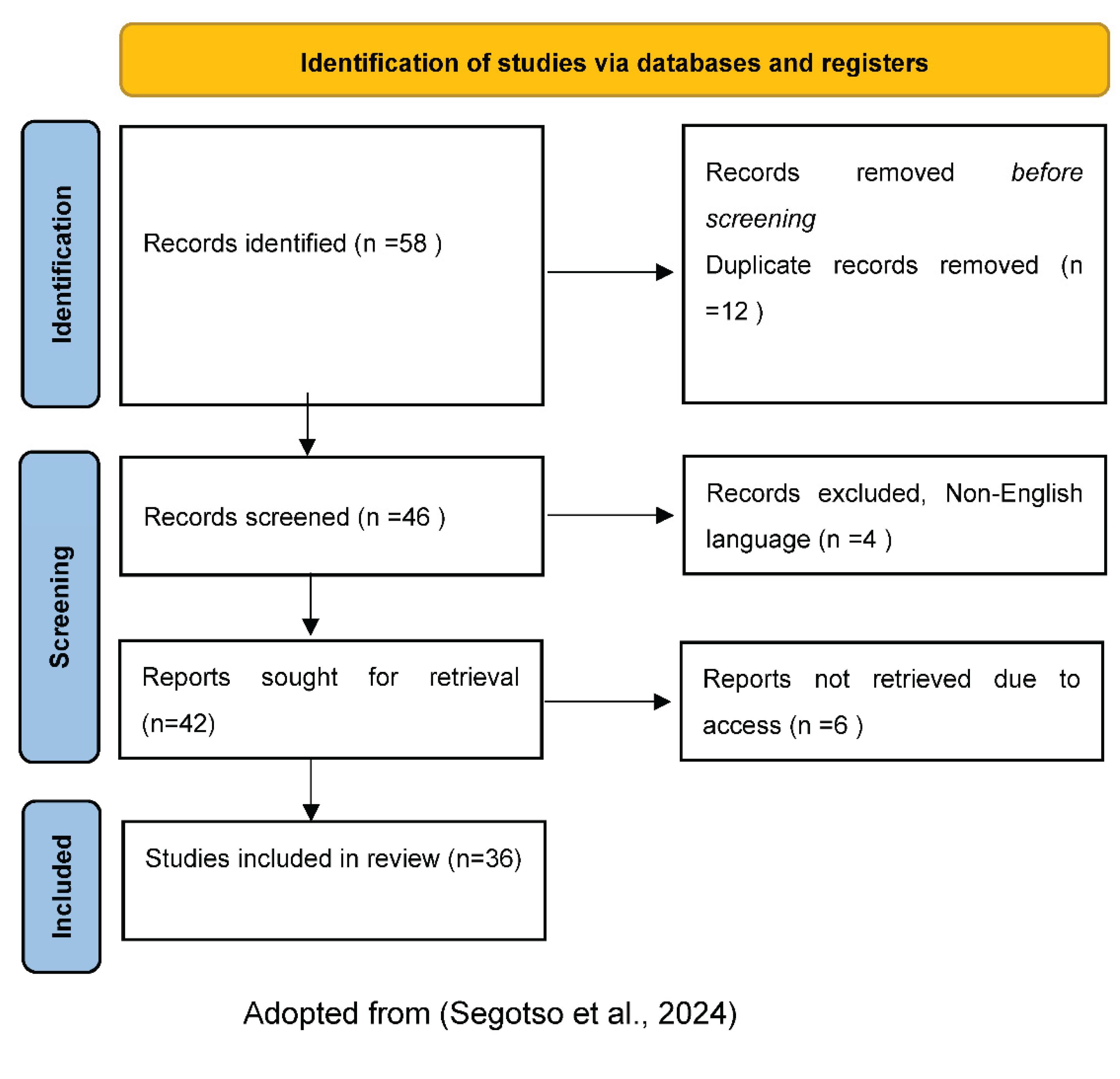

A total of 58 records were initially retrieved. After removing 12 duplicates, 36 unique records were screened for eligibility. The inclusion criteria required that studies: Be published between 2008 and 2024, studies conducted in English, studies that address at least one factor related to the global or national-level decline of auditors. Peer-reviewed journal articles, doctoral theses, conference proceedings, or authoritative industry reports (grey literature).

The exclusion criteria resulted in elimination studies that, lacked empirical or theoretical relevance (e.g., opinion pieces or editorial blogs), studies that did not explicitly discuss auditors, accounting professionals, or the audit profession, unrelated to staffing trends or profession sustainability and inaccessible or outside the defined time frame.

Following full-text screening, 4 non-English articles were excluded, and 6 additional articles could not be accessed due to paywall restrictions. The final number of studies included in the review was 36.

Step 4: Charting the data using a narrative approach to synthesize and interpret qualitative data

For the included studies, key information was extracted and compiled in a structured matrix (Table 1). Each entry documented:

- Author(s) and year

- Title

- Source type

- Source name

- Summary of results and possible recommendations

This process allowed for cross-study comparison, theme identification, and synthesis of commonalities across jurisdictions. The charting process also supported the identification of under-researched themes, such as gendered attrition in auditing, technological displacement of junior roles, and regulatory fatigue.

Step 5: Collating, summarising, and reporting results

Thematic analysis was used to organise the data into four broad categories:

- Contributing factors

- Consequences

- Possible recommendations

Each category was supported by multiple studies across diverse geographies, lending credence to the claim that the decline in auditor numbers is a global, multifactorial phenomenon. A synthesis narrative was developed to reflect the diversity of perspectives and to ensure that regional variations were captured alongside global trends.

The review also sought to identify research gaps, such as limited literature addressing the effectiveness of audit education reform, succession planning in firms facing talent exits, and ethical training impacts on professional retention. These gaps were later discussed in detail in the article’s findings and recommendations.

This study did not involve human participants, original fieldwork, or personal data collection. All data were derived from publicly available literature and industry reports. Accordingly, ethical clearance was not required. Nevertheless, the study adhered to principles of academic integrity and proper citation of all reviewed materials, in addition, ethical clearance was provided by the University of KwaZulu-Natal.

3. Analysis and Results

This section presents a descriptive summary of the 36 studies identified through the scoping review process, encompassing both peer-reviewed academic literature and authoritative grey sources. The objective of this descriptive analysis is to provide a transparent overview of the scope, focus, and quality of the literature informing the subsequent thematic discussion. Each entry summarises key details, including publication type, country or region of focus, main findings, and relevance to the decline of auditors. To promote transparency, Figure 1 was included to illustrate the article selection process. This visual summary outlines the identification, screening, and eligibility phases, enabling reproducibility and facilitating peer review.

This descriptive analysis forms the empirical foundation for the findings presented in the next section. It enables a structured synthesis of key themes, including economic pressures, regulatory burden, technological disruption, and workforce shifts, while also highlighting regional gaps, methodological trends, and areas requiring deeper scholarly engagement. A brief interpretive synthesis follows the table to consolidate patterns and draw links to the broader implications for audit sustainability and profession-wide reform.

Descriptive Analysis of the Identified and Reviewed Literature

The descriptive analysis of the 36 reviewed studies reveals several consistent patterns that inform the thematic synthesis presented in the next section. While the geographic spread of studies covers both developed and emerging economies, a disproportionate number originate from North America, the UK, and South Africa, indicating a need for broader inclusion of perspectives from Asia, Latin America, and sub-Saharan Africa. Across the literature, a recurring theme is the growing misalignment between the expectations placed on auditors and the structural conditions within which they operate, marked by rising regulatory demands, economic constraints, and shifting generational values.

4. Findings and Gaps

This section presents the integrated findings and gaps of the scoping review, reframed under three categories aligned with the study’s objective: contributing factors, consequences, and possible recommendations. Each theme draws on Institutional Theory to explain how systemic pressures influence auditor behaviour, professional attractiveness, and the sustainability of the field. This study adopts Institutional Theory as its theoretical lens to examine the systemic decline of auditors. Institutional Theory provides a framework for understanding how external pressures, such as regulation, professional norms, and industry expectations, can influence the behaviour of organisations and individuals within a professional setting. According to Scott (2013), institutions exert three primary types of influence: coercive pressures (stemming from formal regulations and laws), normative pressures (originating from professional values and cultural expectations), and mimetic pressures (arising from the tendency to imitate successful peers in response to uncertainty). These mechanisms help explain why audit firms may adopt certain practices, such as embracing technology or complying with burdensome regulations, not purely for efficiency but to maintain legitimacy, meet stakeholder expectations, or align with industry standards.

To deepen the understanding of the patterns emerging from the reviewed literature, the findings are presented thematically in response to the three guiding research questions: the contributing factors to the decline of auditors, the consequences of this trend, and possible recommendations. In interpreting these findings, behavioural theory is used as a complementary lens to examine the cognitive, motivational, and organisational dynamics influencing auditor behaviour (Ajzen, 1991). This perspective helps to illuminate how factors such as workload stress, regulatory fatigue, declining professional identity, and ethical disengagement contribute to the broader decline of the audit profession, often in ways that transcend purely structural or economic explanations.

We conducted a thematic content analysis using our own themes based on Table 1 and thereafter applied ChatGPT-4o to determine if our themes aligns with the key areas explored in previous research on the decline of auditors. To carry out the thematic content analysis, we imported all 36 eligible articles into ChatGPT-4o We then ran a word frequency analysis on all 36 articles using the tools available in ChatGPT-4o. Following this, we performed a concept analysis to identify the most commonly occurring concepts. We manually mapped the frequently appearing keywords to their relevant concepts to determine the most prevalent themes in the research. The themes we came up with aligned with ChatGPT-4o and this is a reliable artificial intelligence tool to use according to Bennis and Mouwafaq (2025).

The themes that were identified in the following categories were further discussed in detail:

- Contributing factors category has the following 6 themes identified:

- Talent pipeline and perception

- The impact of regulation and compliance costs on the audit profession

- Talent shortages and recruitment challenges in the industry including burnout

- The impact of technological advancements

- Financial pressure and profitability

- Audit resignations and risk factors

- 2.

- Consequences of the decline of the auditor’s category have the following 3 themes identified:

- Audit quality

- Market concentration

- Reduced public trust

- 3.

- Possible recommendations to address the decline in the auditors category have the following 3 themes identified:

- Technological training and tools

- Balance regulation with practicality

- Strengthen talent attraction and retention

The gaps of the study is addressed at the end of each theme where necessary.

4.1. Contributing Factors

4.1.1. Talent Pipeline and Perception

There is a global and local (example, in United States, United Kingdom, Australia, South Africa), decline in accounting graduates and auditors’ entrance due to perceived lack of high workload, low work-life balance and poor compensation compared to other field like finance and technology (Knechel et al., 2021, Blood and Yong, 2024, Tyson, 2023, Miles Education, 2024, Ahn et al., 2024, Persellin et al., 2019). The audit profession faces significant challenges resulting from a lack of public understanding of its roles and responsibilities (Harber, 2018). Based on the study according to Harber (2018) survey, 79% of auditors express concern that the public often misunderstands the true nature of their work, mistakenly believing that auditors are responsible for correcting and detecting all instances of fraud (Harber, 2018). This misconception places pressure on auditors, contributing to growing discouragement within the profession and leading to a decline in the number of auditors (Porter et al., 2012). Beyond public misunderstanding, the profession has personal risks and complex responsibilities (Eldaly, 2012). Auditors are tasked with navigating complex regulatory frameworks while ensuring compliance (Eldaly, 2012). These challenges are combined with the fact that compensation in the auditing field is often less than in corporate roles, which can discourage potential entrants into the profession (Ellis, 2022).

Furthermore, according to Harber (2018), the survey findings revealed that 62% of the survey respondents perceive the audit profession as overregulated (Harber, 2018). This perception of excessive regulation adds to the stress associated with the job and diminishes its attractiveness to younger generations who seek dynamic and flexible career paths (Cpa Ireland, 2023). As a result, the audit profession is increasingly viewed as a less desirable career option for emerging professionals, leading to concerns about the sustainability and future strength of the field.

In addition, persistent societal misunderstanding of auditors’ roles (example., fraud detection, guarantee providers) results in reputational damage and legal exposure (Porter et al., 2012, Malsch and Gendron, 2011, Church et al., 2008).

Moreover, according to Oben (2021), the audit profession’s reputation has been further jeopardised by a series of frequent and severe accounting and auditing malpractices, which have attracted significant public and regulatory scrutiny. High-profile scandals involving large corporations and audit firms have exposed failures in ethical conduct, independence, and professional scepticism, raising concerns about the effectiveness of existing oversight mechanisms and contributing to a broader crisis of trust in the auditing profession (Oben, 2021). Such incidents erode public trust and stress the urgent need for enhanced corporate governance practices, such as stronger audit committee oversight, improved board independence, transparent reporting structures, and stricter enforcement of ethical and accountability standards (Oben, 2021). To restore confidence in the auditing profession, it is essential that firms prioritise quality, invest in training and development, and uphold stringent ethical standards. This will help improve the profession's image and ensure that auditors can deliver informed and reliable opinions on the financial statementsin an increasingly complex business environment.

There is a disconnect between public expectations and auditors' actual responsibilities (Harber, 2018). Future research could explore how to bridge this gap through improved communication, public awareness campaigns, and changes in audit reporting.

4.1.2. The Impact of Regulation and Compliance Costs on the Audit Profession

Increased regulation (example. SOX, IRBA fines, Australian ASA enforcement) adds significant pressure, especially on smaller firms, resulting in exits from the profession. Compliance often increases documentation without necessarily improving audit quality (Harber, 2018, Ghosh and Tang, 2015, South African Accounting Academy, 2024, Fülöp and Pintea, 2014, Hecimovic et al., 2009). One of the top challenges facing audit firms today is the continuous introduction of new laws and regulations by regulatory bodies (Caseware, 2024). Many industry professionals, such as auditors and accountants, express concern that this escalating regulatory scrutiny may drive audit managers and partners to transition away from traditional assurance roles into non-assurance positions (Harber, 2018). This trend is troubling, as it could lead to a significant loss of experienced professionals in the assurance space, potentially weakening the overall integrity and credibility of the audit profession.

Moreover, a growing concern is that an excessive emphasis on compliance checklists is reducing the critical importance of professional judgement in auditing (Harber, 2018). When auditors are compelled to prioritise adherence to regulatory requirements over their expert assessments, the quality of audits may suffer. This compliance-driven mentality may dampen the professional skepticism that is essential for thorough and effective auditing.

As a result, the combination of stringent regulations also contributes to a less inviting atmosphere for new entrants into the field. Aspiring auditors may be discouraged by the perception that the profession is overly focused on ticking boxes rather than fostering critical thinking and analytical skills.

Many auditors believe excessive regulations reduce professional judgement and make the profession less attractive (Harber, 2018). Future studies could investigate the balance between regulation and professional discretion in auditing. In addition, another gap is whether regulatory reforms, such as an increase in IRBA fines (South African Accounting Academy, 2024), if it actually improves audit quality or contributes to talent shortages.

4.1.3. Talent Shortages and Recruitment Challenges in the Industry Including Burnout

One of the top challenges facing firms today is the significant shortage of skilled talent, which complicates the processes of hiring and retaining qualified staff (Caseware, 2024). Many organisations, such as audit and accounting firms, describe their recruitment efforts as ranging from somewhat challenging to extremely difficult (Caseware, 2024). This persistent issue is worsened by a declining interest in the profession among younger individuals, who may be discouraged by factors such as the demanding nature of the work, limited career advancement opportunities, or the perception of the industry.

To combat these challenges, firms are employing various strategies.Offshoring in the audit profession refers to employing audit staff in other countries to perform audit tasks remotely, often to reduce costs and access skilled labour(Caseware, 2024, Gold City Offshoring, 2023). At the same time, staff training initiatives aim to upskill existing employees and strengthen their competencies in response to evolving industry demands (Gold City Offshoring, 2023). Additionally, according to Caseware (2024), firms are responding to talent shortages by upskilling existing staff, investing in automation, and expanding service areas such as client advisory services, which signals a move toward a more agile and specialised workforce. . The audit firm’s reliance on third-party services and outsourcing has increased significantly as it faces pressure from talent shortages and rising workloads (Caseware, 2024). By outsourcing specific audit tasks, firms can address temporary gaps in expertise or capacity without overburdening their existing team members(Caseware, 2024). However, these solutions often come with their own set of challenges, such as ensuring quality control and maintaining the integrity of the audit firms.

The Public Company Accounting Oversight Board (PCAOB) has raised concerns regarding the ongoing shortage of qualified staff, noting that it directly affects audit quality (Vien, 2024). A decline in competent auditors can lead to increased audit deficiencies, weakening the reliability of financial reporting and ultimately eroding stakeholder trust (Vien, 2024). In addition, excessive hours, particularly during peak seasons (60–80 hours per week), impair judgement, decrease job satisfaction, and discourage retention (Knechel et al., 2021, Persellin et al., 2019). Addressing these recruitment and retention hurdles is crucial for maintaining robust audit practices and ensuring the long-term health of the profession.

Audit careers have a decreasing appeal, especially compared to corporate finance and tech-related fields (Blood and Yong, 2024). Future studies could examine why young professionals avoid auditing, whether due to concerns about work-life balance, salary expectations, or career growth limitations. How can the industry rebrand auditing as an attractive career choice?

Many countries, including the US, UK, Ireland, and Australia, face accounting talent shortages (Blood and Yong, 2024). Research could explore whether outsourcing or offshoring (e.g., South African talent solutions) effectively addresses the skills gap without lowering audit quality. Another research area is the impact of remote work and shared service centres on junior auditors’ development and professional skepticism. What strategies do audit firms use to attract and retain younger generations?

Studies suggest that burnout, long hours, and work-life balance issues are the primary reasons auditors leave the profession (Blood and Yong, 2024, Ellis, 2022). Research could explore how firms can redesign audit work structures to retain talent while maintaining professional standards. Can hybrid work models reduce stress without compromising audit quality? How do auditors' stress, long hours, and burnout impact their mental health and overall well-being?

4.1.4. The Impact of Technological Advancements

The impact of technological advancements on the auditing industry is becoming increasingly significant. According to Caseware (2024), the report stated that 15.4% of firms have identified technology advancement as a key challenge they face (Caseware, 2024). The rise of Artificial Intelligence (AI) and automation is fundamentally transforming traditional auditing processes. This shift necessitates that auditors acquire new skills, urgently requiring comprehensive training programs focused on various AI tools and platforms (Burke and Polimeni, 2023).

Moreover, many firms are strategically leveraging technology to mitigate the effects of staffing shortages (Caseware, 2024). By automating routine tasks and processes, these firms can significantly reduce manual workloads, thereby enhancing overall efficiency and productivity. This reliance on technology helps address immediate resource constraints and allows auditors to focus on more complex and high-value aspects of their work. As the profession continues to evolve, embracing these technological changes will be crucial for firms aiming to maintain a competitive edge in the fast-paced business environment.

The adoption of new technologies is a significant challenge for audit firms (Caseware, 2024). Future research could explore how AI and automation impact traditional auditing roles. How can firms integrate technological advancements while ensuring ethical and high-quality audits? How will AI impact the decline of auditors?

4.1.5. Financial Pressure and Profitability

The auditing profession faces significant challenges due to financial pressure and declining profitability across audit firms (Gold City Offshoring, 2023, Mattar, 2024). As margins contract, many audit firms are experiencing reduced revenues, which directly translates to lower salaries for auditors. This decline in compensation not only diminishes job appeal but also raises the risks associated with audit practices. Consequently, the overall attractiveness of the profession suffers, potentially leading to a talent shortage.

Larger firms that generate higher revenue are better positioned to sustain their operations in this competitive landscape (Mattar, 2024). These firms tend to retain skilled professionals, which helps maintain their audit quality and commitment to rigorous standards. In contrast, smaller firms and non-Big Four auditors face a riskier situation, particularly those struggling with client retention. As losing clients can significantly impact their financial stability, these auditors may be more inclined to exit the profession, contributing to a decline in overall audit quality.

Research indicates that auditors with higher revenue are less likely to leave the profession, yet decreasing profit margins in audit firms reduce salaries and incentives (Knechel et al., 2021). Future research could investigate whether higher audit fees improve retention and audit quality or whether they push clients toward opinion shopping (Mattar, 2024).

4.1.6. Audit Resignations and Risk Factors

Auditors often resign for several key reasons, primarily related to litigation risks and audit and business risks (Ghosh and Tang, 2015). Firms within the Big Four are increasingly focused on the potential for litigation, which can create significant liability concerns and impact their reputation (Ghosh and Tang, 2015). This heightened awareness of litigation risks often leads to a decline in the number of auditors willing to take on potentially critical or high-profile audits, as the possibility of legal repercussions is large (Ghosh and Tang, 2015). Additionally, the complexities involved in specific audit engagements and uncertainties in the business environment contribute to these resignations (Ghosh and Tang, 2015). These include dealing with rapidly changing regulations, technically challenging financial reporting areas, inconsistent or limited client data, and unpredictable economic conditions. As a result, firms are compelled to navigate these challenges carefully, balancing clients' demands with the auditing profession's inherent risks.

4.2. Consequences of the Decline of Auditors

4.2.1. Audit Quality

Talent shortages, lowered hiring standards, regulatory pressure, and overwork have led to increased audit deficiencies, especially in high-risk engagements (Vien, 2024, Ahn et al., 2024, Tarek et al., 2017, Eldaly, 2012). High audit quality enhances the credibility and reliability of financial reports and is closely linked to the transparency of financial reporting (Darmawan, 2023). According to Darmawan (2023), audit quality plays a vital role in strengthening stakeholder trust through transparent disclosures. One of the key factors influencing audit quality is the size of the audit firm, which often determines access to resources, expertise, and robust internal processes (Darmawan, 2023). Consequently, a decline in the number of auditors may negatively affect audit quality by limiting the profession’s capacity to meet growing reporting demands and uphold high assurance standards.

Findings suggest that the audit firm size have an impact on audit quality and financial reporting transparency (Darmawan, 2023). Future studies could explore how does the decline of auditors impact the audit quality of the audit firms. Is there an interconnected relationship between audit quality and the decline of auditors? Does the audit quality due to the decline of auditors have any impact on the audit firm, such as negative findings by regulatory bodies and fines relating to non-compliance?

4.2.2. Market Concentration

Audit markets are increasingly dominated by the Big Four, reducing competition and audit firm diversity and especially in statutory audit work (Cpa Ireland, 2023, Ck Search Global, 2024, Financial Reporting Council, 2024). Smaller firms struggle to absorb compliance costs, leading to consolidation or exit from the profession, especially in jurisdictions like Ireland, South Africa, and Australia (Cpa Ireland, 2023, Brownlee, 2023).

4.2.3. Reduced Public Trust

Audit scandals and inadequate responses have contributed to diminishing public confidence in auditors and audit reports (Oben, 2021, Mdhluli et al., 2023). In addition, A shift toward commercialism over professional values, especially due to consulting dominance and weakened ethical education, has undermined auditor integrity (Edu and Esang, 2008) and familiarity threats, pressure from clients, and rotational fatigue affect auditor independence and objectivity (Daugherty et al., 2012, Ball et al., 2015, Carey and Simnett, 2006).

4.3. Possible Recommendations to Address the Decline in Auditors

4.3.1. Technological Training and Tools

Equip auditors with the skills and standards to handle IT-driven environments, automation, and cybersecurity audits (Tarek et al., 2017, Caseware, 2024).

4.3.2. Balance Regulation with Practicality

Regulators should avoid overburdening firms with documentation, heavy processes and instead support principle-based frameworks with proportional oversight and coordinate cross-border oversight to match the global reach of audit firms, ensuring consistent accountability and reducing regulatory arbitrage (Malsch and Gendron, 2011, Fülöp and Pintea, 2014, Hecimovic et al., 2009).

4.3.3. Strengthen Talent Attraction and Retention

Increase salaries, support flexible work, reduce workloads, and provide mentorship and clear career paths, especially for young and diverse talent (Tyson, 2023, Ahn et al., 2024, Persellin et al., 2019). In addition in Spain, it is found that women view auditing more favourably and are more likely to enter the profession, that has implications for diversity, inclusion, and addressing gender-related attrition in auditing (Amondarain et al., 2023). Reform licensing (example, 150-hour CPA rule to be reduced), create flexible pathways (example, non-degree or STEM entrants), and make the profession more accessible and appealing (Miles Education, 2024, Fülöp and Pintea, 2014, Ahn et al., 2024).

Furthermore the gap in the study suggest that there is a global decline in the number of students pursuing CPA/CA qualifications (Burke and Polimeni, 2023, Gold City Offshoring, 2023). Research could explore alternative pathways to become a CPA.CA, such as reducing the 150-hour requirement in the US. What incentives can be introduced to encourage more students to pursue professional accounting qualifications?

The data suggests an increasing proportion of female accounting students remain understated at senior levels (Ck Search Global, 2024), yet in Spain females are more likely to enter into the audit profession (Amondarain et al., 2023). Future research could investigate barriers to female progression in auditing and how firms can support diversity in leadership roles.

5. Conclusions

The aim of this study was to analyse the contributing factors to the decline of auditors globally, its consequences and possible recommendation. . The main research question to address the aim of the study was: what are the key factors contributing to the global decline of auditors, its consequences and possible recommendations? The findings confirmed that the audit profession and the public’s perception, impact of regulations, talent shortages and recruitment challenges, impact of technological advancements, financial pressure and profitability, audit resignations and risk factors and audit quality are the main reasons for the decline of the registered auditors worldwide. The audit profession faces a significant challenge in achieving the right balance between stringent regulations and the application of professional judgement to enhance overall audit quality. To address this challenge, it is essential to develop comprehensive educational programs and career promotion strategies that actively encourage more individuals to pursue auditing careers. This could involve partnerships with universities, internships, and mentorship opportunities that highlight the profession's importance and impact. Additionally, as technological advancements continue to reshape the auditing landscape, it is crucial for the profession to embrace these changes while also focusing on the retention of skilled auditors. This includes investing in training programs that equip auditors with the necessary skills to effectively use new technologies, ensuring they can enhance their audit efficiency and accuracy. By fostering an environment that values regulatory compliance and professional expertise, the audit profession can significantly improve its quality and appeal to prospective professionals. In addition, the study produced findings from a global perspective that includes South Africa. The study has notable limitations, including the choice to use a scoping review as the method. While this method was needed, other types of reviews could also be considered. Further studies may narrow the contributing factors specifically based on the gaps identified in this study. This study adds to the limited research on auditors' decline. It suggests actionable strategies for addressing these challenges, laying a foundation for future research on the audit profession's sustainability.

References

- Ahn, J., R. Hoitash, U. Hoitash, and E. Krause. 2024. Labor supply drought: the case of accountant talent shortage and audit outcomes. Available at SSRN 4792026.

- Ajzen, I. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50, 2: 179–211. [Google Scholar] [CrossRef]

- Amondarain, J., M. E. Aldazabal, and M. Espinosa-Pike. 2023. Gender differences in the auditing stereotype and their influence on the intention to enter the profession. Journal of Behavioral and Experimental Finance 37: 100784. [Google Scholar] [CrossRef]

- Anderson, S., P. Allen, S. Peckham, and N. Goodwin. 2008. Asking the right questions: Scoping studies in the commissioning of research on the organisation and delivery of health services. Health Research Policy and Systems 7. [Google Scholar] [CrossRef]

- Arksey, H., and L. O'malley. 2005. Scoping studies: towards a methodological framework. International journal of social research methodology 8: 19–32. [Google Scholar] [CrossRef]

- Ball, F., J. Tyler, and P. Wells. 2015. Is audit quality impacted by auditor relationships? Journal of Contemporary Accounting & Economics 11: 166–181. [Google Scholar]

- Beasley, M. S., J. V. Carcello, D. R. Hermanson, and T. L. Neal. 2009. The audit committee oversight process. Contemporary Accounting Research 26: 65–122. [Google Scholar] [CrossRef]

- Bennis, I., and S. Mouwafaq. 2025. Advancing AI-driven thematic analysis in qualitative research: a comparative study of nine generative models on Cutaneous Leishmaniasis data. BMC Medical Informatics and Decision Making 25: 1–14. [Google Scholar] [CrossRef]

- Blood, B., and J. Yong. 2024. Addressing the Decline in the Accounting Talent Pipeline. International Federation of Accountants (IFAC).

- Brás, J. C., R. F. Pereira, M. Fonseca, R. Ribeiro, and I. Bianchi. 2024. Advances in auditing and business continuity: A study in financial companies. Journal of Open Innovation: Technology, Market, and Complexity 10: 100304. [Google Scholar] [CrossRef]

- Brownlee, M. 2023. Company auditor numbers in steady decline, ASIC data reveals [Online]. Available online: https://www.accountingtimes.com.au/profession/company-auditor-numbers-in-steady-decline-asic-data-reveals#:~:text=SMSF%20auditor%20numbers%20also%20in,to%20the%20report%20by%20ASIC (accessed on 20 December 2023).

- Burke, J. A., and R. S. Polimeni. 2023. The Accounting Profession Is in Crisis [Online]. Available online: https://www.cpajournal.com/2023/12/01/the-accounting-profession-is-in-crisis/ (accessed on 11 February 2025).

- Carey, P., and R. Simnett. 2006. Audit partner tenure and audit quality. The accounting review 81: 653–676. [Google Scholar] [CrossRef]

- Caseware. 2023. CaseWare state of accounting firms trends report.

- Caseware. 2024. CaseWare state of accounting firms trends report.

- Church, B. K., S. M. Davis, and S. A. Mccracken. 2008. The auditor's reporting model: A literature overview and research synthesis. Accounting Horizons 22: 69–90. [Google Scholar] [CrossRef]

- Ck Search Global. 2024. Decline in audit firm numbers continues. Available online: https://cksearchglobal.com/decline-in-audit-firm-numbers-continues/ (accessed on 11 February 2025).

- Cpa, and Ireland. 2023. Decline in the Number of Auditors to Hit SMEs With Higher Costs [Online]. Available online: https://www.cpaireland.ie/Latest-News/News/News-2023/Decline-in-the-Number-of-Auditors-to-Hit-SMEs-With (accessed on 20 December 2023).

- Darmawan, A. 2023. Audit Quality and Its Impact on Financial Reporting Transparency. Golden Ratio of Auditing Research 3.

- Daugherty, B. E., D. Dickins, R. C. Hatfield, and J. L. Higgs. 2012. An examination of partner perceptions of partner rotation: Direct and indirect consequences to audit quality. Auditing: A Journal of Practice & Theory 31: 97–114. [Google Scholar]

- Dawkins, M. C. 2023. Declining Enrollments—A Call to Action! Issues in Accounting Education 38, (1): 9–18. [Google Scholar] [CrossRef]

- De Graaf, F. J. 2019. Ethics and behavioural theory: how do professionals assess their mental models? Journal of Business Ethics 157: 933–947. [Google Scholar] [CrossRef]

- Edu, B. E., and A. E. Esang. 2008. The Decline in Accounting Professionalism-Causes and Effects. SSRN.

- Eldaly, M. K. 2012. Effects of the new regulations of the audit profession on the audit firms’ strategies.

- Ellis, L. 2022. Why So Many Accountants Are Quitting. In Wall Street Journal. [Google Scholar]

- Filip, A., A. Hammami, Z. Huang, A. Jeny, M. Magnan, and R. Moldovan. 2017. Literature review on the effect of implementation of IFRS 13 fair value measurement. International Accounting Standard Board’s public January 2018 meeting and referenced as Agenda Paper C. [Google Scholar]

- Financial Reporting Council 2024. 2024. Key Facts and Trends in the Accountancy Profession. The Financial Reporting Council Limited. [Google Scholar]

- Fülöp, M. T., and M.-O. Pintea. 2014. Effects of the new regulation and corporate governance of the audit profession. SEA-Practical Application of Science 4: 545–554. [Google Scholar]

- Garvey, A. M., L. Parte, B. Mcnally, and J. A. Gonzalo-Angulo. 2021. True and fair override: Accounting expert opinions, explanations from behavioural theories, and discussions for sustainability accounting. Sustainability 13: 1928. [Google Scholar] [CrossRef]

- Ghosh, A., and C. Y. Tang. 2015. Auditor Resignation and Risk Factors. Accounting Horizons.

- Girardin, M., E. Courtney, and Z. Kaplan. 2024. Accountant vs. Auditor: What’s the Difference and Which Role Is Right for You? [Online]. Available online: https://www.theforage.com/blog/careers/accountant-vs-auditor-whats-the-difference? (accessed on 15 February 2025).

- Offshoring, Gold City. 2023. Navigating the Skills Deficit in the Audit and Accounting Sector: Gold City Offshoring's Solution. Available online: https://goldcityoffshoring.com/wp-content/uploads/2023/12/1-Navigating-the-Skills-Deficit-in-the-Audit-and-Accounting-Sector-Gold-City-Offshorings-Solution.pdf.

- Han, H., R. K. Shiwakoti, R. Jarvis, C. Mordi, and D. Botchie. 2023. Accounting and auditing with blockchain technology and artificial Intelligence: A literature review. International Journal of Accounting Information Systems 48: 100598. [Google Scholar] [CrossRef]

- Harber, M. 2018. Exploring the nature and consequences of a possible decline in the appeal of the South African audit profession. Southern African Journal of Accountability and Auditing Research 20: 13–28. [Google Scholar]

- Hasan, R., and M. Miah. 2024. Two Decades of Board Co-Option Research: A Scoping Review. Accounting, Finance & Governance Review 32. [Google Scholar]

- Hecimovic, A., N. Martinov-Bennie, and P. Roebuck. 2009. The force of law: Australian auditing standards and their impact on the auditing profession. Australian accounting review 19: 1–10. [Google Scholar] [CrossRef]

- International Federation of Accountants. 2013. Roles and Importance of Professional Accountants in Business [Online]. Available online: https://www.ifac.org/news-events/2013-10/roles-and-importance-professional-accountants-business (accessed on 31 January 2025).

- Knechel, R. W., A. Vanstraelen, and M. Zerni. 2015. Does the identity of engagement partners matter? An analysis of audit partner reporting decisions. Contemporary Accounting Research 32: 1443–1478. [Google Scholar] [CrossRef]

- Knechel, W. R., J. Mao, B. Qi, and Z. Zhuang. 2021. Is There a Brain Drain in Auditing? The Determinants and Consequences of Auditors Leaving Public Accounting. Contemporary Accounting Research 38, (4): 2461–2495. [Google Scholar] [CrossRef]

- Levac, D., H. Colquhoun, and K. K. O'brien. 2010. Scoping studies: advancing the methodology. Implementation science 5: 1–9. [Google Scholar] [CrossRef]

- Malsch, B., and Y. Gendron. 2011. Reining in auditors: On the dynamics of power surrounding an “innovation” in the regulatory space. Accounting, Organizations and Society 36: 456–476. [Google Scholar] [CrossRef]

- Matshona, Z., S. Mabutho, and M. Phesa. 2024. Tax Knowledge and Tax Behaviour of Individual Taxpayers in South Africa: A Scoping Review. International Journal of Economics and Financial Issues 14: 304–307. [Google Scholar] [CrossRef]

- Mattar, D., R. El Khoury, and M. Chaanine. 2024. Factors Affecting Auditor Change Decisions: The Case of United Kingdom. Sage, 1–18. [Google Scholar] [CrossRef]

- Mdhluli, S., M. Mkhize, and M. Phesa. 2023. Accounting and Finance Professionals’ Perception on The Current State of The Accountancy Profession in South Africa. International Journal of Environmental, Sustainability, and Social Science 4: 1790–1821. [Google Scholar] [CrossRef]

- Merkl-Davies, D. M., and N. M. Brennan. 2017. A theoretical framework of external accounting communication: Research perspectives, traditions, and theories. Accounting, Auditing & Accountability Journal 30: 433–469. [Google Scholar]

- Miles, and Education. 2024. The Accountant Shortage Is Real: Here’s What You Need to Know [Online]. Available online: https://www.mileseducation.com/accounting/blogs/the-accountant-shortage-is-real-heres-what-you-need-to-know (accessed on 11 February 2025).

- Minutiello, V., and P. Tettamanzi. 2024. A systematic literature network analysis of the development of behavioural accounting research. International Journal of Behavioural Accounting and Finance 7: 113–134. [Google Scholar] [CrossRef]

- Murray, L. 2024. Understanding Large Accounting Firm Perceptions on the Decline of Accounting Graduates and Implications of Supply Shortages. Bachelor of Science Senior Honors Thesis, University of New Hampshire. [Google Scholar]

- Oben, J. A. 2021. CREDIBILITY CRISES FACING THE ACCOUNTING PROFESSION IN SOUTH AFRICA.

- Olojede, P., O. Erin, O. Asiriuwa, and M. Usman. 2020. Audit expectation gap: an empirical analysis. Future Business Journal 6: 1–12. [Google Scholar] [CrossRef]

- Persellin, J. S., J. J. Schmidt, S. D. Vandervelde, and M. S. Wilkins. 2019. Auditor perceptions of audit workloads, audit quality, and job satisfaction. Accounting horizons 33: 95–117. [Google Scholar] [CrossRef]

- Peters, M. D., C. Godfrey, P. Mcinerney, Z. Munn, A. C. Tricco, and H. Khalil. 2020a. Scoping reviews. JBI manual for evidence synthesis 10: 10.46658. [Google Scholar]

- Peters, M. D., C. Marnie, A. C. Tricco, D. Pollock, Z. Munn, L. Alexander, P. Mcinerney, C. M. Godfrey, and H. Khalil. 2020b. Updated methodological guidance for the conduct of scoping reviews. JBI evidence synthesis 18: 2119–2126. [Google Scholar] [CrossRef] [PubMed]

- Porter, B., C. Ó. Hógartaigh, and R. Baskerville. 2012. Audit expectation-performance gap revisited: Evidence from New Zealand and the United Kingdom. Part 2: Changes in the gap in New Zealand 1989–2008 and in the United Kingdom 1999–2008. International Journal of Auditing 16: 215–247. [Google Scholar] [CrossRef]

- Scott, W. R. 2013. Institutions and organizations: Ideas, interests, and identities. Sage publications. [Google Scholar]

- Segotso, T., J. D. Mvunabandi, and M. Phesa. 2024. A Systematic Literature Review of the Challenges of Adopting and Implementing IFRS for SMEs in South Africa. International Journal of Economics and Financial Issues 14: 131–147. [Google Scholar] [CrossRef]

- Sithole, N., M. Phesa, and M. Sibanda. 2024. Nexus of Tax Law and Non-Profit Organizations: Incentives and challenges in compliance with tax laws by Public Benefit Organizations in South Africa: a scoping review. International Journal of Business Ecosystem & Strategy (2687-2293) 6: 225–242. [Google Scholar]

- Sood, S. 2022. The Times of India: Auditing, a serious job: Top challenges faced by auditors while auditing [Online]. Available online: https://timesofindia.indiatimes.com/blogs/voices/auditing-a-serious-job-top-challenges-faced-by-auditors-while-auditing/ (accessed on 30 September 2023).

- South African Accounting Academy. 2024. IRBA: Maximum Fines for Auditors–Notice of withdrawal and reissue [Online]. Available online: https://accountingacademy.co.za/news/read/irba-maximum-fines-for-auditors-notice-of-withdrawal-and-reissue (accessed on 12 February 2025).

- Tarek, M., E. K. Mohamed, M. M. Hussain, and M. A. Basuony. 2017. The implication of information technology on the audit profession in developing country: Extent of use and perceived importance. International Journal of Accounting & Information Management 25: 237–255. [Google Scholar]

- The Independent Regulatory Board for Auditors 2023. Annual Report.

- Tyson, J. 2023. Auditors say accountant shortage ramps up work pressure: CAQ [Online]. CFO Dive. Available online: https://www.cfodive.com/news/auditors-say-accountant-shortage-increases-work-pressure-caq/701796/ (accessed on 11 February 2025).

- Vien, C. 2024. Is the accounting shortage behind the drop in audit quality? [Online]. CFO Brew. Available online: https://www.cfobrew.com/stories/2024/12/09/is-the-accounting-shortage-behind-the-drop-in-audit-quality (accessed on 11 February 2025).

- Yiu, E., and J. Zhong. 2023. Shortage of audit professionals will ‘affect Hong Kong’s position as a fundraising centre’, industry body says, asks government to recruit overseas auditors [Online]. Available online: https://www.scmp.com/business/article/3228197/shortage-audit-professionals-will-affect-hong-kongs-position-fundraising-centre-industry-body-says?campaign=3228197&module=perpetual_scroll_0&pgtype=article (accessed on 30 September 2023).

Figure 1.

PRISMA article selection included in the review.

Table 1.

Summary of the reviewed studies.

| No | Authors | Title of the Study | Source Type | Source Name | Summary of the Result and/Possible Recommendations |

|---|---|---|---|---|---|

| 1 | Harber (2018) | Exploring the nature and consequences of a possible decline in the appeal of the South African audit profession | Peer-reviewed journal | Southern African Journal of Accountability and Auditing Research | This South African study explored the decreasing appeal of the audit profession, citing overregulation, increasing liability, and career unattractiveness as core issues. A significant proportion of audit partners expressed concern over regulatory burdens such as MAFR and diminishing margins. The study also revealed that younger professionals increasingly prefer alternative career paths with better work-life balance and remuneration, raising concerns about the future talent pipeline and audit quality. |

| 2 | Caseware (2024) | State of Accounting Firms Trends Report 2024. | Grey literature – industry report | State of Accounting Firms Trends Report 2024. | Based on a global survey, this report highlights talent shortages, difficulty in tech adoption, and regulatory challenges as top concerns for audit and accounting firms. It identifies staff recruitment and retention as the most pressing issue, with over 90% of auditors reporting difficulties. The findings underscore a systemic strain on firms to innovate while coping with limited resources, impacting not just operational efficiency but also staff engagement and long-term audit sustainability. |

| 3 | Knechel et al. (2021) | Is There a Brain Drain in Auditing? The Determinants and Consequences of Auditors Leaving Public Accounting. | Peer-reviewed journal | Contemporary Accounting Research, | The study found that auditors who generate higher revenue are less likely to leave the profession, and these auditors tend to maintain high audit quality. Auditors who work at companies outside the Big Four and lose clients are likelier to leave the profession and have low audit quality. In turn, the clients will leave for another audit firm or want to pay less in audit fees. |

| 4 | Oben (2021) | Credibility Crises Facing The Accounting Profession In South Africa | Dissertation | Researchgate | Accounting malpractices have become frequent and severe, and trust in the profession is declining, impacting the broader economic environment. The study highlights the need for stricter regulations and strong corporate governance to restore public confidence. |

| 5 | Mdhluli et al. (2023) | Accounting and Finance Professionals’ Perception on The Current State of The Accountancy Profession in South Africa. | Peer-reviewed journal | International Journal of Environmental, Sustainability, and Social Science | The findings highlight key insights regarding ethics among South African accounting and finance professionals, including ethical knowledge, pressure to compromise ethics, the responsibility of professional members, the knowledge-ethics-pressure relationship, and the influence of accounting bodies. |

| 6 | Ghosh and Tang (2015) | Auditor Resignation and Risk Factors | Peer-reviewed journal | Accounting Horizons | The study investigates how litigation, audit, and business risks influence auditor resignation decisions. It finds that auditors often resign in anticipation of negative outcomes such as internal control failures or financial distress. These resignations are especially prevalent among Big Four firms and signal potential issues to stakeholders. The study emphasises the importance of understanding resignation patterns as indicators of engagement risk and declining audit quality. |

| 7 | Mattar (2024) | Factors Affecting Auditor Change Decisions: The Case of the United Kingdom | Peer-reviewed journal | Sage Journals | This UK-based study explores factors influencing auditor change decisions. It identifies firm size, leverage, profitability, and governance features such as board diversity and independence as significant variables. The findings suggest that opinion shopping may still influence auditor switching, despite regulatory efforts. This challenges assumptions about auditor independence and indicates the need for stronger governance practices to reinforce audit objectivity. |

| 8 | Cpa Ireland (2023) | Decline in the Number of Auditors to Hit SMEs With Higher Costs | Grey literature – institutional report | CPA Ireland news | This report highlights a 31% reduction in licensed audit firms in Ireland between 2014 and 2023, disproportionately affecting SMEs. The causes include talent shortages, regulatory compliance burdens, and rising operational costs. As a result, SMEs face increasing audit fees and diminished choice. The report advocates for regulatory reform and support mechanisms to sustain audit access and market diversity. |

| 9 | Blood and Yong (2024) | Addressing the Decline in the Accounting Talent Pipeline | Grey literature – professional body | International Federation of Accountants | This global IFAC report addresses the worsening shortage of accounting professionals. It attributes the trend to generational changes, unattractive work conditions, and declining enrolments. The report calls for coordinated action among regulators, educators, and firms to modernise certification pathways and improve career appeal to sustain the talent pipeline. |

| 10 | Burke and Polimeni (2023) | The Accounting Profession Is in Crisis | Grey literature – practitioner journal | The CPA Journal | Burke outlines the structural decline in the US accounting profession, citing falling CPA exam registrations, an ageing workforce, and poor adaptation to technological change. The article argues that public accounting no longer meets career expectations for younger professionals and urges reform to restore professional relevance. |

| 11 | Brownlee (2023) | Company auditor numbers in steady decline, ASIC data reveals | Grey literature – newsfeed | Accounting Times | This article documents the decline in registered company auditors in Australia, falling over 30% in the past decade. Demographic shifts, firm consolidation, and an ageing workforce are cited. The article also highlights concerns about maintaining audit independence and staff development under constrained conditions |

| 12 | Vien (2024) | Is the accounting shortage behind the drop in audit quality? | Grey literature – industry report | CFO Brew | A PCAOB study links declining audit quality to talent shortages across major firms. Interviews with audit leaders reveal that staff turnover, remote work, and outsourcing weaken training and engagement. These factors lead to higher error rates and insufficient documentation. |

| 13 | Ck Search Global (2024), (Financial Reporting Council, 2024) | Decline in audit firm numbers continues and Key Facts and Trends in theAccountancy Profession | Grey literature – professional site and industry report | CK Search Global and Financial Reporting Council (FRC) | The Financial Reporting Council's (FRC) Key Facts and Trends report tracks a continuing decline in UK and Irish audit firms. Although audit fee income continues to rise, the report notes a decrease in new accounting students and underrepresentation of women in senior roles, raising sustainability concerns. . |

| 14 | Gold City Offshoring (2023) | Navigating the Skills Deficit in the Audit and Accounting Sector: Gold City Offshoring's Solution | Grey literature – corporate white paper | Gold City Offshoring | This white paper outlines how offshoring from South Africa is helping address talent shortages in the UK and US. It discusses benefits and risks, including the need for quality control and cross-jurisdictional alignment, highlighting offshoring as both a strategic and logistical challenge. |

| 15 | Tyson (2023) | Auditors say accountant shortage ramps up work pressure: CAQ. CFO Dive | Grey literature – media article | CFO dive | A survey of 748 US audit partners reveals that staff shortages are increasing workloads and turnover. Firms are offering higher pay and more flexibility to retain staff. The article ties well-being to audit performance, calling for long-term workforce reforms. |

| 16 | Miles Education (2024) | The Accountant Shortage Is Real: Here’s What You Need to Know | Grey literature – education blog | Miles Education | This article highlights how the 150-hour CPA requirement in the US has become a barrier to entry. It suggests alternative licensure paths and proposes curriculum updates and employer partnerships to reinvigorate student interest in accounting. |

| 17 | Edu and Esang (2008) | The Decline in Accounting Professionalism - Causes and Effects | Peer-reviewed journal | SSRN Electronic Journal | This study links declining professionalism in accounting to ethics erosion, corporate scandals, and regulatory gaps. It calls for stricter enforcement and ethics education reform to strengthen integrity and accountability in the profession. |

| 18 | Murray (2024) | Understanding Large Accounting Firm Perceptions on the Decline of Accounting Graduates and Implications of Supply Shortages | Dissertation | Honors Theses and Capstones. University of New Hampshire | Interviews with audit firms reveal that students find accounting unappealing due to perceived lack of creativity and rigid career structures. The thesis advocates for career rebranding and stronger academic-practice collaboration to reverse the trend. |

| 19 | Ellis (2022) | Why So Many Accountants Are Quitting | Grey literature – newsfeed | The Wall Street Journal | The article highlights a 17% drop in US accounting staff from 2020–2022, attributed to burnout and low pay. Many opt for careers in finance or tech instead. Firms are increasing salaries and flexibility to retain talent. |

| 20 | South African Accounting Academy (2024) | IRBA: Maximum Fines for Auditors – Notice of withdrawal and reissue | Grey literature – professional body | South African Accounting Academy | This article reports on IRBA's new fine structure in South Africa. It discusses implications for auditor morale and risk appetite and raises questions about the balance between enforcement and profession-wide support. |

| 21 | Darmawan (2023) | Audit Quality and Its Impact on Financial Reporting Transparency | Peer-reviewed journal | Golden Ratio of Auditing Research | This study from Indonesia links audit firm size, tenure, and specialisation to higher financial reporting transparency. It warns that reduced audit capacity could undermine credibility and regulatory compliance in emerging markets. |

| 22 | Beasley et al. (2009) | Audit Committee Oversight Process | Peer-reviewed journal | Contemporary Accounting Research | Explores audit committee practices in the U.S. post-SOX. Finds that engagement varies based on member expertise, and effective committees support improved oversight of audit quality. |

| 23 | Malsch and Gendron (2011) | Reining in auditors: On the dynamics of power surrounding an‘‘innovation’’ in the regulatory space | Peer-reviewed journal | Accounting, Organizations and Society | Investigates Canadian audit regulation and reveals symbolic compliance by firms despite oversight. It applies institutional theory to explain regulatory capture and limited reform, which is relevant to understanding systemic legitimacy decline in auditing. |

| 24 | Porter et al. (2012) | Audit expectation-performance gap revisited: evidence from New Zealand and the United Kingdom. Part 1: the gap in New Zealand and the United Kingdom in 2008 | Peer-reviewed journal | International Journal of Auditing | This study tracks the evolution of the audit expectation-performance gap over two decades in New Zealand and the UK. It finds that while monitoring helped narrow the performance gap in the UK, a lack of public engagement in NZ allowed the gap to widen. It recommends stakeholder education and regulatory alignment to address society’s unrealistic expectations of auditors. |

| 25 | Church et al. (2008) | The auditor's reporting model: A literature overview and research synthesis | Peer-reviewed journal | Accounting Horizons | This article synthesises literature related to the auditor’s reporting model and its communicative limitations. The authors argue that the standard pass/fail format provides little informational value to users and contributes to the expectations gap. It calls for enhanced auditor disclosures and more nuanced reports to bridge user misunderstandings. |

| 26 | Daugherty et al. (2012) | An Examination of Partner Perceptions ofPartner Rotation: Direct and IndirectConsequences to Audit Quality | Peer-reviewed journal | Auditing: A Journal of Practice & Theory | This study surveys 170 audit partners across various U.S. firms to assess the unintended consequences of mandatory partner rotation. Findings suggest that partner rotation, while improving independence in appearance, leads to loss of client-specific knowledge and negatively impacts audit quality. |

| 27 | Ball et al. (2015) | Is audit quality impacted by auditor relationships? | Peer-reviewed journal | Journal of Contemporary Accounting & Economics | Examining Australian firms, the study finds that longer person-to-person relationships between audit partners and client executives reduce audit quality, while longer firm-to-client tenure enhances it. This dual effect informs debates around partner vs. firm rotation. |

| 28 | Carey and Simnett (2006) | Audit Partner Tenure and Audit Quality | Peer-reviewed journal | The Accounting Review | This Australian study explores whether extended audit partner tenure negatively impacts audit quality. It finds that long tenure is associated with fewer going-concern opinions for distressed companies and more cases of just meeting earnings benchmarks, suggesting compromised scepticism over time. |

| 29 | Amondarain et al. (2023) | Gender differences in the auditing stereotype and their influence on the intention to enter the profession | Peer-reviewed journal | Journal of Behavioral and Experimental Finance | Examines how gendered perceptions affect interest in audit careers among Spanish students. Found that women view auditing more favourably and are more likely to enter the profession. This has implications for diversity, inclusion, and addressing gender-related attrition in auditing. |

| 30 | Brás et al. (2024) | Advances in auditing and business continuity: A study in financial companies | Peer-reviewed journal | Journal of Open Innovation: Technology, Market, and Complexity | Explores how intelligent automation enhances audit processes and resilience in Portuguese banks. Highlights how tech adoption boosts auditor efficiency but may displace routine roles, adding pressure on traditional training pathways and firm models. |

| 31 | Ahn et al. (2024) | Labor supply drought: the case of accountant talent shortage and audit outcomes | Peer-reviewed journal | Northeastern U. D’Amore-McKim School of Business Research Paper | This study uses workforce data from Revelio Labs to examine how the decline in accounting graduates affects audit firm recruitment patterns and audit quality. It finds that although hiring volume has not dropped, firms have widened their recruitment net (hiring more from non-target schools) and reduced selectivity. These shifts are empirically associated with increased financial statement misstatements but not slower audit delivery. The effects are more pronounced in offices handling complex clients or new engagements. |

| 32 | Persellin et al. (2019) | Auditor perceptions of audit workloads, audit quality, and job satisfaction | Peer-reviewed journal | Accounting Horizons | Based on a survey of 776 current and former auditors, the study finds that excessive workloads, especially during the busy season, significantly impair audit quality and job satisfaction. Audit staff regularly work above the threshold where they perceive audit quality begins to decline. Key issues include impaired judgment, reduced scepticism, and shortcuts in documentation. Staff shortages and tight deadlines are cited as the root causes. |

| 33 | Eldaly (2012) | Effects of the new regulations of the audit profession on the audit firms' strategies | Dissertation | University of Bedfordshire | Identifies strategic responses of Big Four firms to regulatory changes, including methodological reviews, conservative client acceptance, and audit quality control. Suggests that audit regulations increase operational costs, centralisation, and stress among auditors. |

| 34 | Fülöp and Pintea (2014) | Effects of the new regulation and corporate governance of the audit profession | Peer-reviewed journal | SEA – Practical Application of Science | This study explores the evolving role of regulation and corporate governance in shaping audit quality and public trust in the profession, particularly in post-crisis Europe. It highlights how the International Auditing and Assurance Standards Board (IAASB), the European Union (EU), and the Financial Accounting Standards Board (FASB) reforms aim to address audit report transparency, auditor independence, and going concern disclosure. The authors argue that enhanced governance structures, such as stronger audit committees and revised reporting standards, are crucial to restoring audit credibility and professional sustainability. |

| 35 | Hecimovic et al. (2009) | The force of law: Australian auditing standards and their impact on the auditing profession | Peer-reviewed journal | Australian Accounting Review | This qualitative study examines the impact of the legally enforceable Australian Auditing Standards (ASAs) on audit quality, firm behaviour, and public confidence. It finds that while regulation aimed to enhance audit credibility post-corporate collapses, most stakeholders (especially audit firms) viewed the changes as burdensome and ineffective in raising audit quality. Increased documentation, regulatory compliance costs, and talent loss were recurring concerns. The study highlights the growing expectations gap and the need for more balanced regulation. |