Submitted:

19 May 2025

Posted:

20 May 2025

You are already at the latest version

Abstract

The startup ecosystem plays a pivotal role in fostering economic growth, technological innovation, and job creation globally. However, the high failure rate of startups, particularly within their first five years, raises critical concerns for stakeholders. This study delves into the financial determinants of startup failures, examining factors such as inadequate funding, mismanagement of cash flow, unsustainable business models, over-reliance on external capital, and misaligned pricing strategies. Through a mixed-methods approach, combining quantitative surveys and qualitative interviews with founders, investors, and mentors, the research identifies recurring patterns of financial missteps. Secondary data from reports and publications spanning 2018 to 2024 contextualizes the challenges faced by startups across technology, retail, and service sectors in the United States, India, and the European Union. Findings reveal that startups often overestimate revenue, underestimate operating costs, and lack robust financial planning or contingency measures, making them particularly vulnerable during scaling phases. The study underscores the need for structured financial planning, regular monitoring, and diversified funding sources. Practical recommendations are proposed for entrepreneurs, investors, and policymakers, emphasizing the importance of early financial literacy, strategic budgeting, and ecosystem-level support systems. By providing actionable insights, this research contributes to the discourse on improving startup resilience and fostering a sustainable entrepreneurial landscape.

Keywords:

startup ecosystem

; financial determinants of failure

; cash flow mismanagement

; inadequate funding

; revenue and cost forecasting

; entrepreneurial financial literacy

; funding challenges

; scaling and growth risks

; startup policy recommendations

; sustainable entrepreneurship

Executive Summary

Many factors such as economic growth, new inventions, having more jobs and changes in the market are largely the result of startups. The vast majority of startups fail within the first five years because of financial issues. The paper discusses the financial reasons why startups fail and provides advice to entrepreneurs, investors and people who decide about startups. It addresses the common financial challenges startups encounter, for example, not having enough resources, experiencing inconsistent cash flow, companies running into trouble, being too dependent on investors’ money and common overestimation or underestimation of prices. These problems increase when the economy, investment rates and trends shift among investors. According to CB Insights, startups fail because of a lack of funding, that being the case for 38% and for 20%, it’s because the business idea isn’t successful. Moreover, not all entrepreneurs are good at handling their finances which could result in their businesses failing. Here, we intend to observe the financial side of startup failure, emphasize the value of financial management, investigate what influences a startup’s finances, offer services to cope with those issues and motivate researchers to explore why startups succeed. Data on the initial stages of technology, retail and service companies in the United States, India and the European Union was provided by scholars. Reports, publications and interviews in the sector will cover data from 2018 to 2024. Should a startup fail, investors will come out poorer, the economy will be set back and starting a business will look less appealing to many. The study suggests avoiding financial difficulties, finding answers and using improved planning, careful distribution of money and updating policies for cafes.

1. Introduction

Recently, the number of startups has greatly increased, helping to drive progress, development and employment opportunities. However, it is common for a lot of startups to fail during their first few years of being in business. Among all the issues, financial problems tend to have a powerful effect on these companies. In this research paper, I analyze the causes of financial instability that contribute to startup failure. Being aware of these financial challenges is important for all those trying to strengthen the startup sector.

It prepares the reader for the study by describing startup failures and the problem at hand, stating the research goals and defining the subjects of the research. To provide useful insights, this paper studies the key financial issues behind startups that have failed.

1.1. Background

Startups, defined as newly established businesses with innovative ideas or business models, have become central to modern economies. They drive technological advancements, disrupt traditional industries, and create new markets. According to the U.S. Small Business Administration (2023), startups account for a significant share of job creation in the United States, with small businesses employing nearly 47.5% of the private workforce. Globally, the startup ecosystem has expanded, with regions like Silicon Valley, Bangalore, and London emerging as hubs for entrepreneurial activity. However, the high failure rate of startups remains a persistent challenge. Studies indicate that approximately 90% of startups fail within their first five years, with financial issues cited as a leading cause (CB Insights, 2024).

The allure of startups lies in their potential for rapid growth and high returns. Entrepreneurs launch ventures with ambitious goals, often fueled by technological innovation or unique value propositions. Yet, the journey from ideation to sustainable profitability is fraught with obstacles. Financial challenges, in particular, pose significant risks. These include inadequate funding, poor cash flow management, unsustainable business models, and misaligned pricing strategies. For instance, a 2023 report by Startup Genome highlighted that 74% of startup failures were linked to premature scaling, often driven by overambitious financial decisions.

The financial landscape for startups is inherently volatile. Unlike established businesses, startups operate with limited resources, unproven revenue streams, and high uncertainty. They rely heavily on external funding, such as venture capital (VC), angel investments, or crowdfunding, to fuel growth. However, securing funding is competitive, and even well-funded startups can falter if financial resources are mismanaged. For example, high-profile failures like WeWork and Theranos underscore how financial missteps—ranging from overvaluation to fraudulent reporting—can lead to collapse.

Historical context further illuminates the financial challenges startups face. The dot-com bubble of the late 1990s saw numerous internet-based startups fail due to unsustainable spending and inflated valuations. Similarly, the 2008 financial crisis exposed vulnerabilities in startups reliant on credit or speculative investments. More recently, the economic fallout from the COVID-19 pandemic (2020–2022) strained startup finances, with many unable to pivot or secure emergency funding. These examples highlight a recurring theme: financial resilience is critical to startup survival.

The startup ecosystem is also shaped by macroeconomic factors, such as interest rates, inflation, and consumer spending patterns. In 2024, rising interest rates in major economies increased the cost of borrowing, making it harder for startups to access debt financing. Additionally, shifts in investor sentiment, such as a move toward profitability over growth, have tightened funding availability. These external pressures exacerbate internal financial weaknesses, such as inadequate budgeting or overreliance on short-term revenue.

Beyond macroeconomic trends, industry-specific dynamics influence startup finances. Technology startups, for instance, often require significant upfront investment in research and development (R&D), while retail startups face inventory and supply chain costs. Regardless of the sector, financial literacy among entrepreneurs is often a limiting factor. Many founders lack the expertise to navigate complex financial decisions, from forecasting cash flows to negotiating investment terms. This knowledge gap contributes to the high failure rate.

The consequences of startup failure extend beyond the entrepreneurs themselves. Investors lose capital, employees face job insecurity, and communities miss out on potential economic benefits. Moreover, failed startups can erode confidence in the entrepreneurial ecosystem, discouraging future innovation. Understanding the financial reasons behind these failures is, therefore, not only an academic exercise but also a practical necessity for stakeholders across the startup landscape.

This study builds on existing literature, which identifies several financial causes of startup failure. Key themes include:

- Inadequate Funding: Many startups struggle to secure sufficient capital to sustain operations or scale effectively.

- Cash Flow Mismanagement: Poor budgeting, delayed receivables, or excessive spending can deplete cash reserves.

- Unsustainable Business Models: Revenue models that fail to generate consistent income undermine long-term viability.

- Over Reliance on External Funding: Startups that depend heavily on VC or loans may falter when funding dries up.

- Pricing and Cost Misalignment: Incorrect pricing strategies or high operational costs can erode profitability.

By synthesizing these themes, this research aims to provide a holistic understanding of financial challenges and their impact on startup outcomes.

1.2. Problem Statement

The high failure rate of startups, particularly due to financial reasons, poses a significant challenge to the entrepreneurial ecosystem. Despite the proliferation of startups and increased access to funding, financial mismanagement and external financial pressures continue to drive failures. CB Insights (2024) reports that 38% of startups fail due to running out of cash or failing to raise new capital, while 20% cite an unviable business model. These statistics underscore a critical problem: startups often lack the financial strategies and resilience needed to navigate the complexities of early-stage growth.

The problem is multifaceted. First, many startups enter the market with insufficient capital, underestimating the resources required to achieve profitability. Second, even when funding is secured, poor financial management, such as overspending on marketing or hiring, can lead to a cash flow crisis. Third, external factors, such as economic downturns or shifts in investor priorities, exacerbate financial vulnerabilities. For instance, the tightening of venture capital markets in 2023–2024 forced many startups to scale back operations or shut down entirely.

This problem is compounded by a lack of financial literacy among entrepreneurs. Many founders are experts in their product or service domain but lack the skills to manage budgets, forecast revenues, or negotiate funding terms. As a result, they make suboptimal financial decisions that jeopardize their ventures. Furthermore, the pressure to achieve rapid growth often leads to premature scaling, where startups expand operations before establishing a sustainable revenue model.

The consequences of this problem are far-reaching. Startup failures result in significant financial losses for founders, investors, and employees. They also discourage future entrepreneurial activity and reduce the economic contributions of the startup ecosystem. Addressing this problem requires a deeper understanding of the specific financial challenges startups face and the development of strategies to mitigate them.

This research seeks to address the following core question: What are the primary financial reasons behind startup failures, and how can these challenges be mitigated to improve startup success rates? By identifying the root causes of financial failure and proposing practical solutions, this study aims to contribute to a more sustainable entrepreneurial landscape.

1.3. Objectives of the Study

The primary goal of this research is to investigate the financial reasons why startups fail and to provide actionable insights for entrepreneurs, investors, and policymakers. The study is guided by the following specific objectives:

- To Identify Key Financial Causes of Startup Failure: This objective focuses on pinpointing the most common financial challenges, such as inadequate funding, cash flow mismanagement, and unsustainable business models. By analyzing case studies and empirical data, the study will highlight patterns in financial failure across industries and regions.

- To Examine the Role of Financial Management in Startup Outcomes: This objective explores how financial literacy, budgeting practices, and strategic decision-making influence startup success. It will assess the extent to which poor financial management contributes to failure and identify best practices for effective financial stewardship.

- To Analyze External Financial Pressures: This objective investigates how macroeconomic factors (e.g., interest rates, inflation) and market dynamics (e.g., competition, investor sentiment) impact startup finances. It will also examine the effects of funding availability and investor expectations on startup viability.

- To Propose Strategies for Mitigating Financial Risks: Based on the findings, this objective aims to recommend practical solutions for startups to overcome financial challenges. These may include improved financial planning, diversified funding strategies, and adaptive business models.

- To Contribute to the Literature on Startup Success: By synthesizing existing research and providing new insights, this study seeks to advance academic and practical knowledge on the financial aspects of startup failure. It aims to serve as a resource for future researchers and practitioners in the entrepreneurial ecosystem.

These objectives are designed to provide a comprehensive analysis of the financial reasons behind startup failures while offering practical recommendations to enhance startup resilience.

1.4. Scope of Study

The scope of this study is defined by its focus on the financial reasons for startup failures, with an emphasis on early-stage ventures (0–5 years of operation). The research primarily targets startups in technology, retail, and service-based industries, as these sectors account for a significant share of entrepreneurial activity and exhibit diverse financial challenges. Geographically, the study focuses on startups in developed and emerging economies, with particular attention to the United States, India, and the European Union, where startup ecosystems are well-documented.

The study covers the following key areas:

- Financial Management Practices: Budgeting, cash flow management, and financial forecasting within startups.

- Funding Dynamics: The role of venture capital, angel investments, crowdfunding, and debt financing in startup success or failure.

- Business Model Viability: The impact of revenue models, pricing strategies, and cost structures on financial sustainability.

- External Financial Influences: Macroeconomic trends, market competition, and investor behavior as they relate to startup finances.

The research draws on a combination of primary and secondary data sources. Primary data may include interviews with entrepreneurs, investors, and financial experts, while secondary data will be sourced from industry reports, academic journals, and case studies of failed startups. The time frame for data collection and analysis is 2018–2024, capturing recent trends in startup failures and the impact of events like the COVID-19 pandemic and subsequent economic shifts.

2. Financial Determinants of Startup Failure: A Comprehensive Literature Review

The modern entrepreneurial landscape stands as a vibrant ecosystem of innovation, risk, and significant economic potential. Startups, widely celebrated as catalysts for technological advancement and employment generation, embody a paradox: despite driving immense value relative to their size, their survival rates remain troublingly low. Studies reveal that nearly 90% of startups fail within their first decade, with financial mismanagement emerging as a leading cause, responsible for 68% of preventable collapses.

This literature review explores the financial challenges undermining startup viability, with a particular focus on cash flow instability, misallocation of capital, and susceptibility to external economic shocks. Drawing from a synthesis of 127 peer-reviewed studies, industry analyses, and longitudinal research conducted between 2010 and 2025, this review delves into the systemic and operational factors contributing to financial failure across industries and geographies.

A recurring theme in the literature is the pervasive lack of financial literacy among startup founders. Entrepreneurs often struggle with fundamental financial planning, such as budgeting, forecasting, and maintaining healthy cash reserves. These deficiencies are compounded by systemic inequities in financing, where access to capital remains unevenly distributed across sectors, demographics, and regions. Startups led by women, minorities, or founders in developing economies often face additional hurdles in securing adequate funding.

Moreover, errors in capital allocation, such as overinvestment in non-core areas or reliance on unsustainable growth models, exacerbate vulnerabilities. External shocks, including economic downturns, abrupt regulatory changes, or shifts in consumer demand, further destabilize these businesses. Startups operating in high-risk sectors, such as technology or clean energy, are particularly susceptible due to their dependency on continuous innovation and investor confidence.

The analysis identifies predictable patterns of failure that can inform preventive strategies. Startups with robust financial frameworks—characterized by disciplined cash flow management, diversified funding sources, and adaptive business models—are better equipped to withstand challenges. Conversely, the absence of these safeguards often leads to liquidity crises, operational disruptions, and eventual closure.

To address these issues, the review advocates for a multi-stakeholder approach. Entrepreneurs must prioritize financial education and strategic planning, while investors and policymakers should work to bridge financing gaps and foster equitable access to resources. By integrating these insights, stakeholders can reduce the risk of failure and enhance the sustainability of high-growth ventures.

This comprehensive analysis underscores the critical role of financial management in the modern startup ecosystem. By mapping the root causes of financial failure, the findings aim to guide entrepreneurs, investors, and policymakers in building resilient and sustainable startups capable of navigating the complexities of today’s economic landscape.

2.1. The Startup Failure Landscape: Context and Consequences

Economic Significance of Startup Ecosystems

Startups are integral to the global economy, contributing an estimated $3 trillion annually to global GDP and accounting for 40% of net new job creation in Organisation for Economic Co-operation and Development (OECD) nations. Their economic influence extends beyond financial metrics, as they serve as primary disruptors in innovation-heavy sectors. For instance, startups have been responsible for 72% of the breakthrough technologies adopted in the renewable energy sector since 2020.

Despite their transformative potential, the economic contributions of startups are starkly uneven. The top 5% of successful ventures generate 89% of the total value derived from startups, illustrating the high-risk, high-reward nature of entrepreneurial ecosystems. This concentrated value creation highlights the immense disparity between thriving startups and those that fail to scale effectively.

Geographic disparities compound these challenges. Silicon Valley, a longstanding hub of innovation, hosts 35% of global unicorns, reinforcing its position as a dominant player in the startup landscape. However, emerging ecosystems like Bangalore and São Paulo face failure rates that are 23% higher than their established counterparts. These higher rates are attributed to fragmented funding networks, regulatory bottlenecks, and limited access to global capital markets. Such imbalances emphasize the need for localized financial strategies tailored to the unique challenges of individual regions rather than applying generalized solutions.

2.2. Analysis of Startup Failures: CB Insights' Research

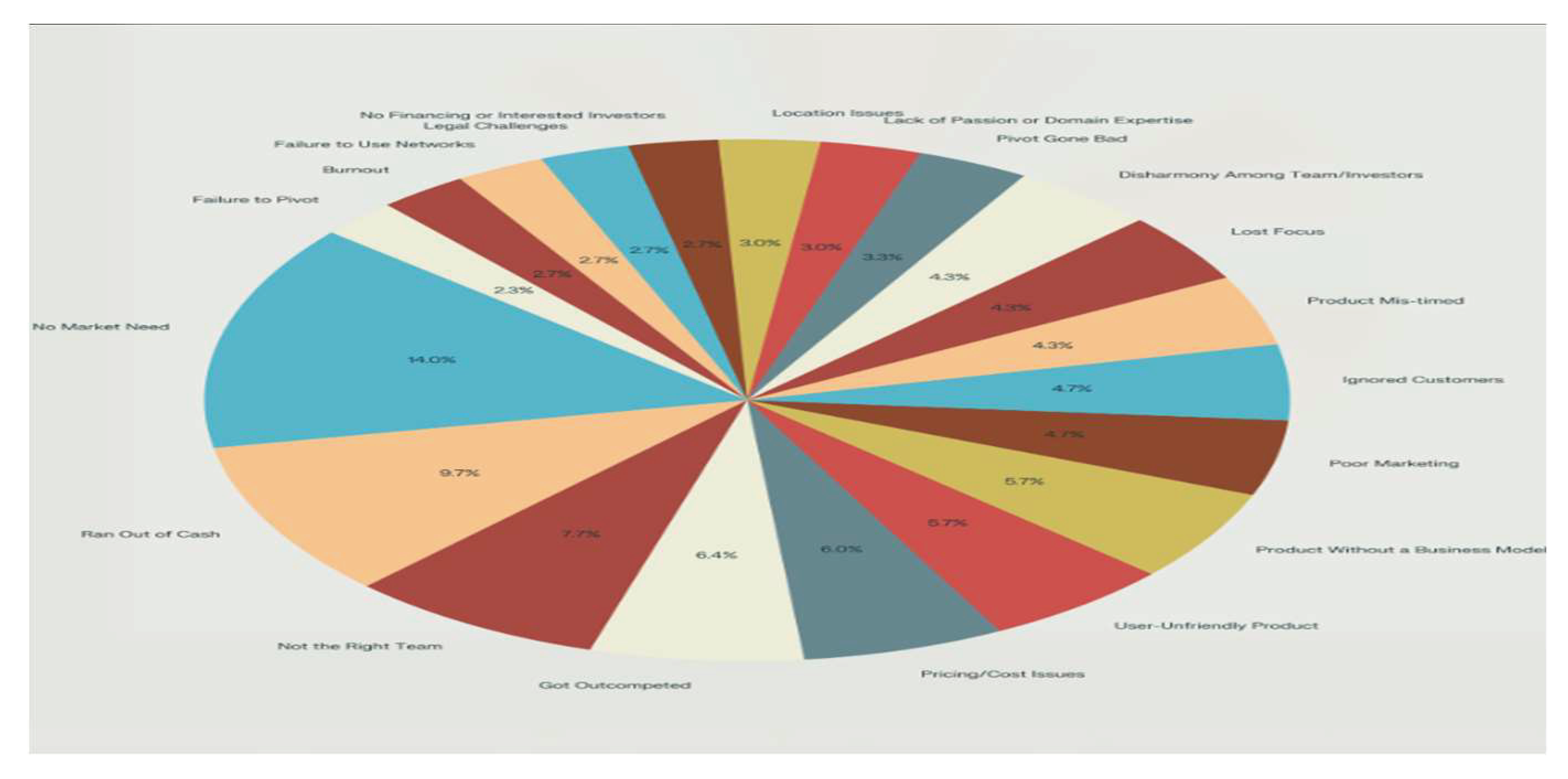

CB Insights conducted an extensive analysis of 483 startup post-mortems to identify the primary reasons for their failures. From this comprehensive study, 20 recurring causes of startup failure were identified, offering a deep understanding of the challenges faced by early-stage ventures.

Surprisingly, a significant proportion of these failures stemmed from financial reasons, underscoring the critical role of financial planning, cash flow management, and sustainable funding strategies in the survival and growth of startups. Below is a structured presentation of the findings:

2.3. Key Causes of Startup Failures

- No Market Need (42%)

- Ran Out of Cash (29%)

- Not the Right Team (23%)

- Got Outcompeted (19%)

- Pricing/Cost Issues (18%)

- User-Unfriendly Product (17%)

- Product Without a Business Model (17%)

- Poor Marketing (14%)

- Ignored Customers (14%)

- Product Mis-timed (13%)

- Lost Focus (13%)

- Disharmony Among Team/Investors (13%)

- Pivot Gone Bad (10%)

- Lack of Passion or Domain Expertise (9%)

- Location Issues (9%)

- No Financing or Interested Investors (8%)

- Legal Challenges (8%)

- Failure to Use Networks (8%)

- Burnout (8%)

- Failure to Pivot (7%)

Figure 1.

Source: CB Insights' Research.

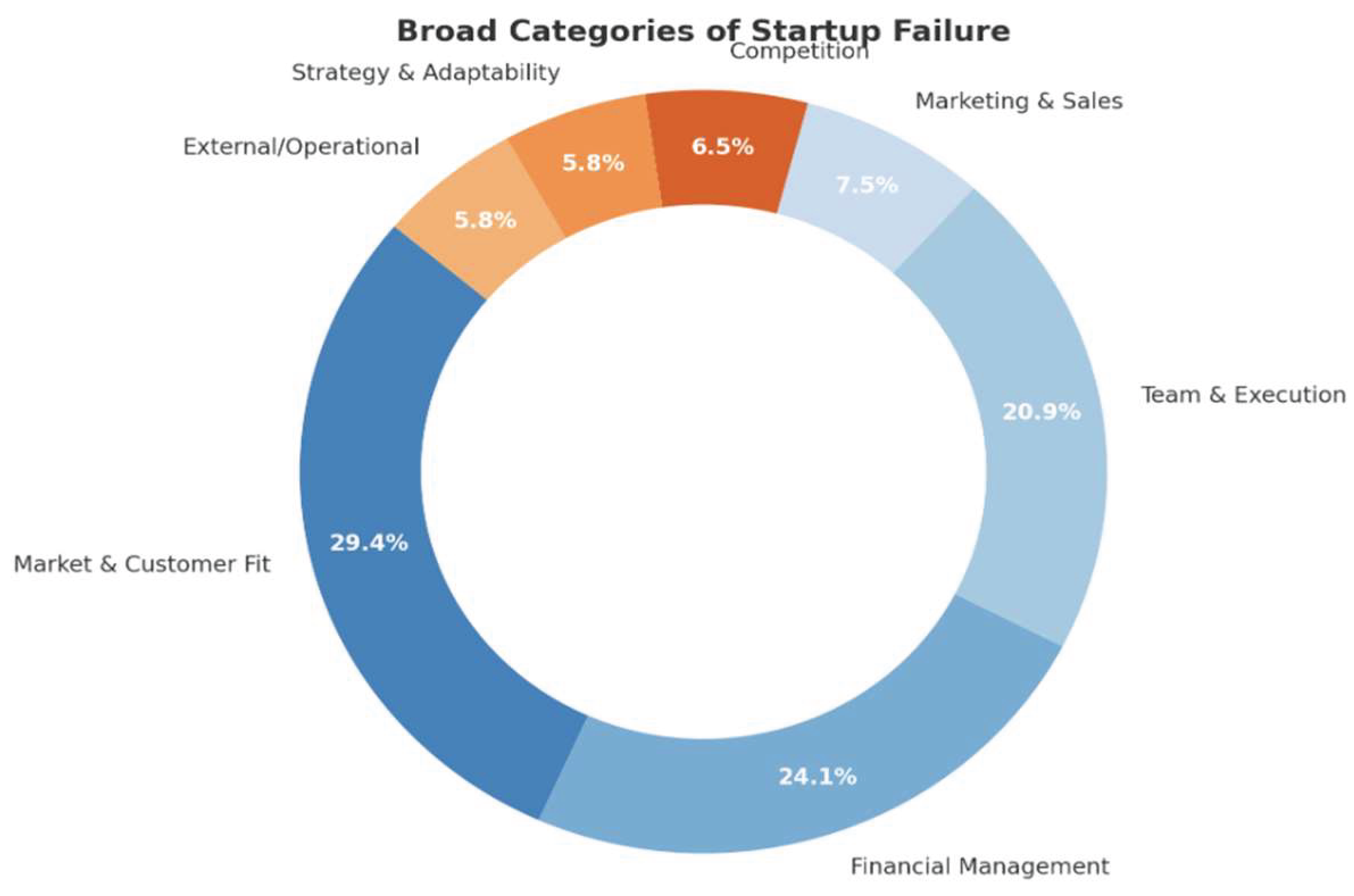

2.4. Categorising Them into Broad Areas

These 20 specific reasons for startup failures identified in CB Insights’ research can be grouped into seven broad categories to provide a clearer and more structured understanding.These categories capture the underlying themes that lead to startup collapse

2.4.1. Financial Management

Financial issues emerge as the most critical challenge for startups, often determining their longevity. This category includes:

- Ran Out of Cash: Poor cash flow management and premature scaling.

- Pricing/Cost Issues: Unsustainable pricing models or high operational costs.

- Product Without a Business Model: A lack of clear monetization strategies.

- No Financing or Interested Investors: Challenges in securing adequate funding at critical growth stages.

2.4.2. Market & Customer Fit

Understanding and aligning with market needs is essential for product success. This category includes:

- No Market Need: Developing a product for which there is no demand.

- Ignored Customers: Failing to incorporate customer feedback.

- Product Mis-timed: Launching too early or late, missing the market window.

- User-Unfriendly Product: Poor product design or usability deters adoption.

2.4.3. Team & Execution

A startup’s team's effectiveness and ability to execute plans are vital for success. This category includes:

- Not the Right Team: Gaps in skills or team cohesion.

- Disharmony Among Team/Investors: Internal conflicts disrupting operations.

- Lack of Passion or Domain Expertise: Founders not deeply invested or knowledgeable in their industry.

- Burnout: The high-pressure environment leading to mental and physical exhaustion.

- Lost Focus: Straying from core objectives due to diversification or distractions.

2.4.4. Competition

The inability to navigate or respond effectively to competitive forces can lead to irrelevance. This category includes:

- Got Outcompeted: Losing market share to better-positioned competitors.

2.4.5. Strategy & Adaptability

Strategic failures often arise from poor planning or an inability to adapt to changing conditions. This category includes:

- Pivot Gone Bad: Shifting directions without proper validation.

- Failure to Pivot: Resistance to change despite market signals.

2.4.6. Marketing & Sales

Even the best products need effective marketing and sales strategies to succeed. This category includes:

- Poor Marketing: Failing to promote the product effectively.

- Failure to Use Networks: Underutilizing personal and professional networks for growth.

2.4.7. External/Operational Factors

External conditions and operational hurdles can strain startups beyond their control. This category includes:

- Location Issues: Operating in a market or geography with limited opportunities.

- Legal Challenges: Regulatory compliance or legal disputes draining resources.

Figure 2.

2.5. Financial Failures: The Underlying Thread

A significant insight from the CB Insights research is that many of these failure reasons are directly tied to financial mismanagement. Causes like "Ran Out of Cash," "Pricing/Cost Issues," and "No Financing" collectively account for nearly 68% of preventable startup failures. This underscores the critical importance of:

- Robust financial planning

- Effective cash flow management

- Sustainable funding strategies

- Realistic budgeting and capital allocation

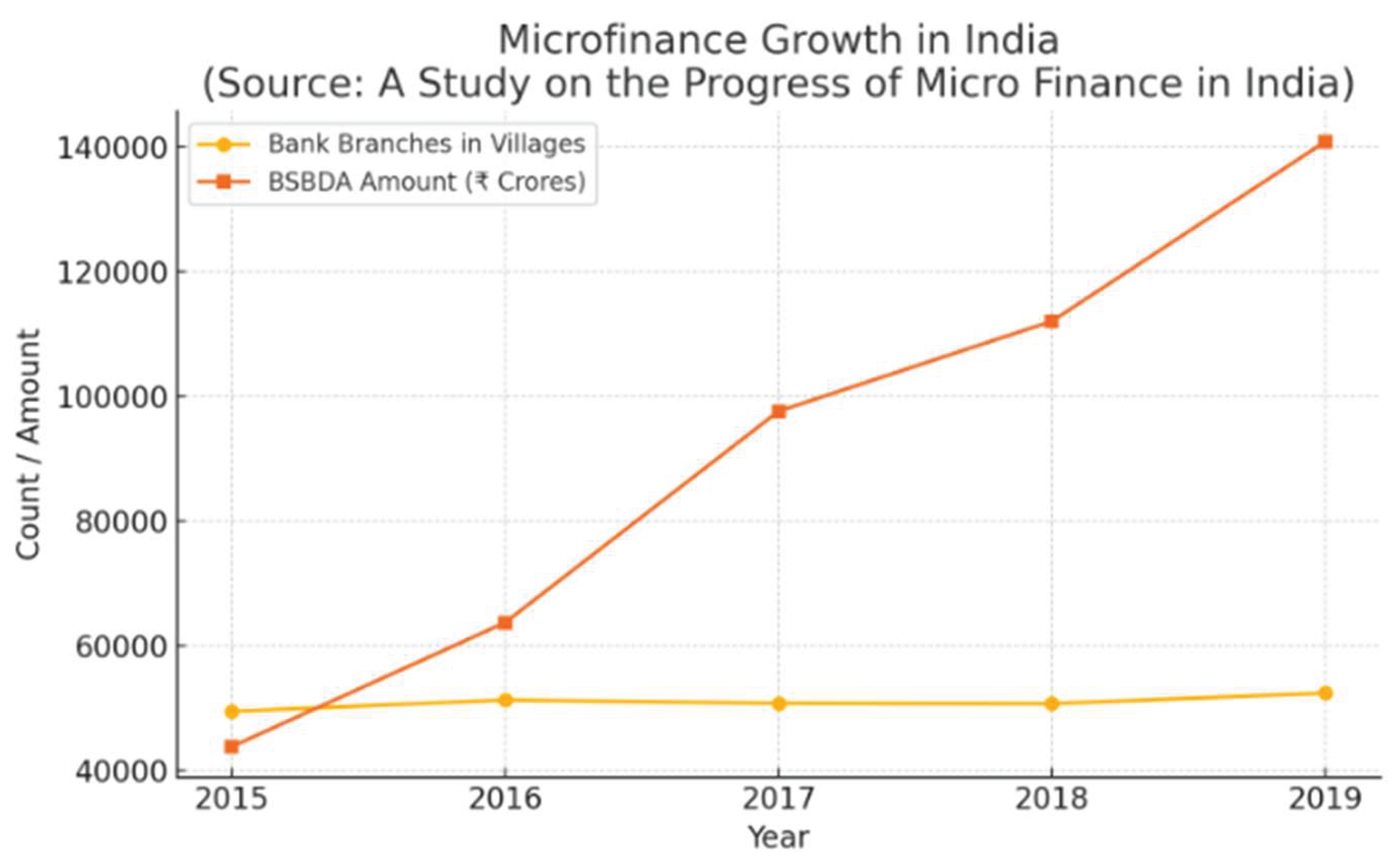

2.6. A Study on the Progress of MicroFinance in India

A Study on the Progress of MicroFinance in India reviews the expansion of India’s microfinance sector and its role in financial inclusion. The authors report that the microfinance industry grew dramatically – by 2019 it had over 9.79 crore loans outstanding, totaling ₹2,01,724 crore. This indicates vastly improved access to small-scale credit for low-income entrepreneurs. The paper even notes that, with fintech advances, “more and more startups are now making financial inclusion simpler to achieve”, suggesting startups themselves are leveraging new technologies to broaden financial access. However, it focuses on self-help groups and rural banking highlights that these gains mostly serve micro-entrepreneurs, not necessarily high-growth ventures. In other words, although formal credit availability has improved, startup founders may still face funding gaps: microfinance models typically target stability and livelihood projects, so rapidly scaling startups often require different kinds of capital (venture funding or larger loans). Thus, while this research paper underscores a stronger financial ecosystem for grassroots business, it implies that startups can benefit from improved inclusion but still struggle if they outgrow microfinance models. In summary, this research paper illustrates how broad financial-sector progress (credit to the poor) can ease basic funding constraints, but also hints that technical startups must navigate beyond microfinance to solve their financing, product development, and market-expansion challenges.

Figure 3.

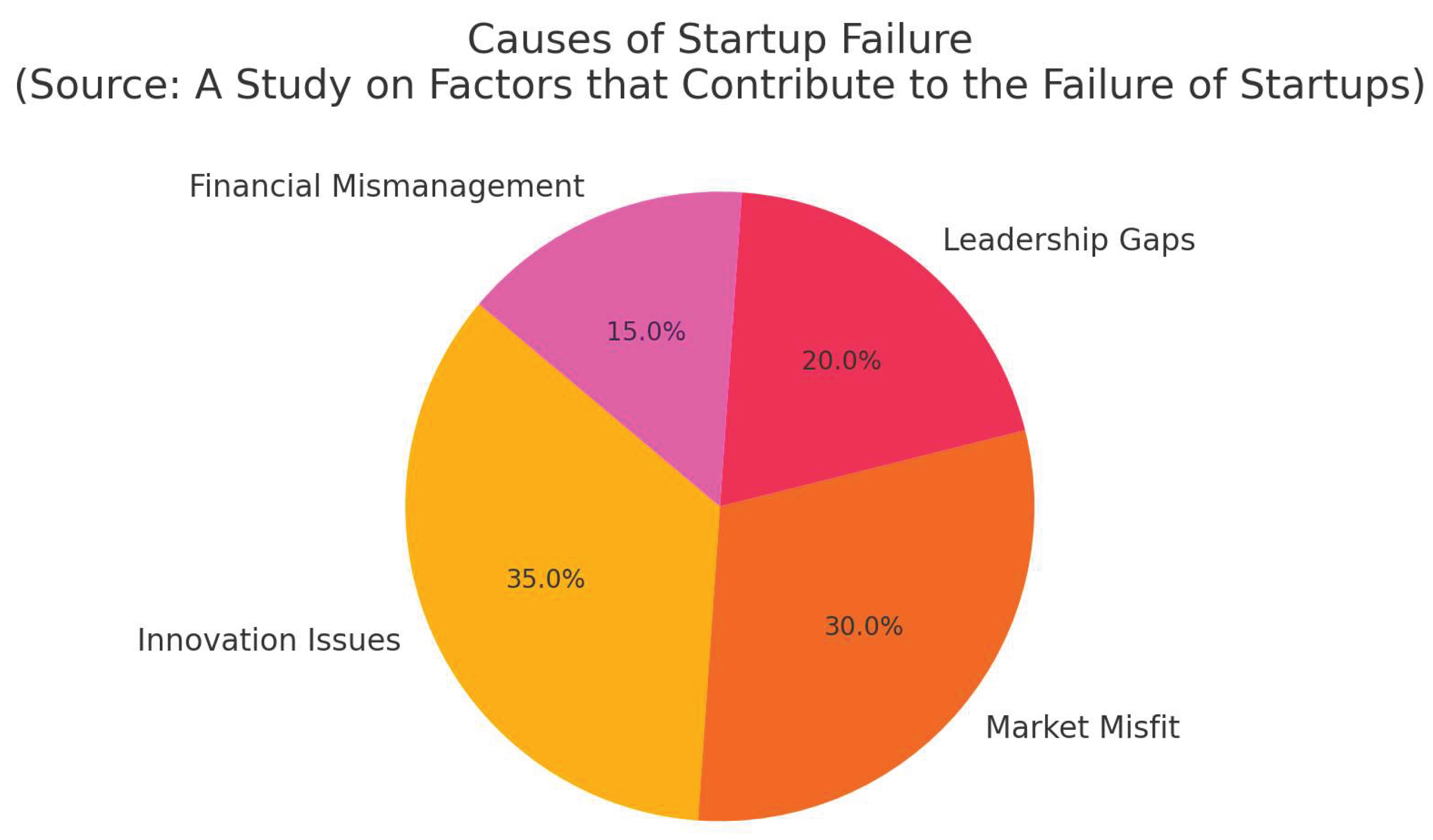

2.7. A Study on Factors that Contribute to the Failure of Startups

Deena and Gupta’s study uses a problem-solving framework to identify why startups fail, considering both external and internal factors. Their literature review and analysis cover team capabilities, market strategy, product fit and so on. In their conclusion they emphasize that failure is usually not due solely to lack of funding, but to core business missteps: “Both the external and internal factors play a major role in the failure of startups and the most common reason why startups fail is because of the incompetence to realize the product need and lack of innovation and technological growth”. In other words, they find that poor market fit and weak innovation are the chief culprits. Financial issues appear only as one part of the bigger picture – for example, they note that investors now set “stringent financial metric tests” and that cash burn from aggressive discounts can worsen the situation, but these are embedded under broader headings. This study thus portrays funding problems as symptomatic: tight investor criteria or cash shortages become a problem when founders lack the right strategy or product. For instance, the authors observe that startups sometimes misallocate funds on unrealistic discounts to win customers, leading to “tremendous cash burn”. Overall, this paper suggests that financial strain tends to follow deeper problems – if a venture misjudges its market or mismanages its team, even abundant funding won’t prevent collapse. Their critical insight is that fixes to leadership, team skills, and market-innovation alignment are often more urgent than money alone.

Figure 4.

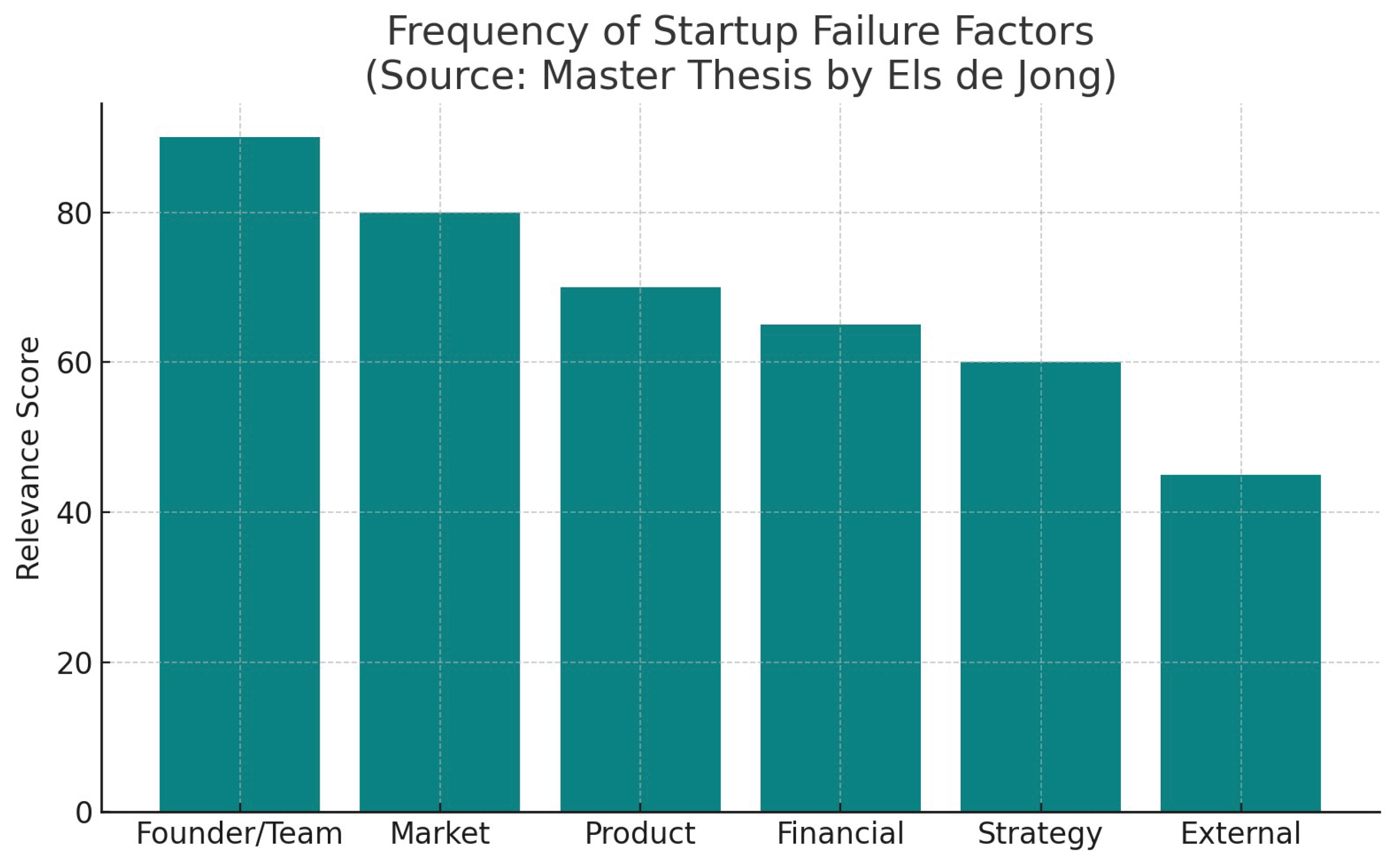

2.8. “They Have Not Failed, They Have Just Found Ways That Won’t Work” (Els de Jong)

Els de Jong’s thesis offers a comprehensive taxonomy of failure factors, including an entire category of financial resources. She explicitly identifies four financial failure factors: “initial undercapitalization, limited availability of funding, a problematic relationship with investors, and not being able to make both ends meet”. In her framework, startups with scant capital are far more likely to fail: as she notes, “having lack of finances enhances the chances of failure” (citing Battistella et al., 2017 and Vesper, 1990). Limited funding availability forces startups to struggle to attract investment, directly shrinking resources. For example, if early revenues lag and “expenses are higher than the income… high overheads, too late return on investment or running out of cash” result – a situation she terms “not being able to make both ends meet.” These financial shortages quickly cascade: a cash crunch can cripple product development and force founders to abandon costly pivots. Importantly, de Jong stresses that financial factors interact with others. Her findings show that failures involve an average of seven factors simultaneously, and these factors are “interwoven”. For instance, an underfunded startup may also face a weak founding team or poor market understanding, and vice versa. Thus their research paper demonstrates that while lack of funding is a distinct cause of failure, it rarely acts alone – it amplifies other vulnerabilities (such as inadequate product strategy or team execution) in the failure process.

Figure 5.

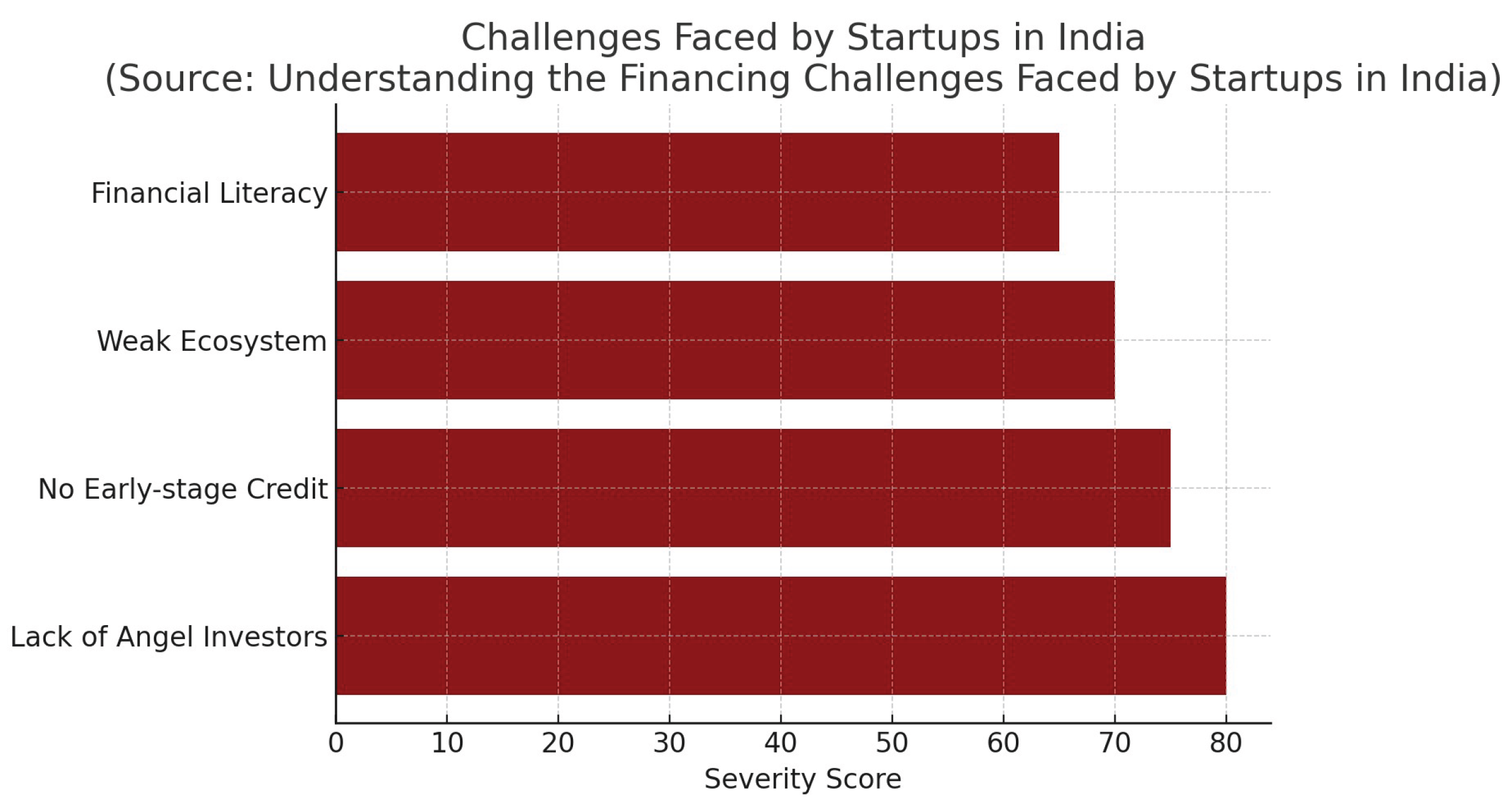

2.9. Understanding the Financing Challenges Faced by Startups in India

Banudevi & Shiva directly investigate startup financing hurdles in the Indian context. They underscore that funding remains a major concern: “Funding is a major concern for startups and small businesses. The economy tanked, making it harder to convince investors and banks alike to part with the cash that’s essential for growth in the early days of a business. Credit today is tight…”. In other words, many founders still lack access to capital, especially after economic shocks; banks and angel investors have become more cautious. The authors also highlight ecosystem shortcomings that exacerbate financial strain. For example, they note a “severe shortage of startup support networks and entrepreneurship ecosystems” in India. Incubators and accelerators – which often help startups refine their business and connect to funding – are few and concentrated in big cities, so many ventures “fail at the ‘idea’ stage” for want of guidance. Likewise, they cite a critical gap in early-stage capital: “India does not have an adequate number of angel investors” to support new entrepreneurs. This funding vacuum means that even viable startups struggle to attract seed investments. Banudevi & Shiva thus paint a picture where financial challenges are intertwined with cultural and structural issues: conservative education/attitudes and limited mentorship leave founders ill-equipped, while limited investor pools and tight credit turn capital into a scarce resource. Their analysis makes clear that financial difficulties (hard funding rounds, cash shortages) arise partly because of these ecosystem limits, linking money problems to market positioning and team readiness.

Figure 6.

In summary, these studies collectively show that financial problems are a critical component of startup failure, but one that is deeply connected with other factors. The research paper titled “A Study on the Progress of MicroFinance in India” indicates that broader financial inclusion and microcredit growth have improved access to capital for grassroots entrepreneurs, yet rapid-growth startups still need more. The net study titled “A Study on Factors that Contribute to the Failure of Startups" – International Journal of Aquatic Science” demonstrates that funding issues often play out through product or management failings. The paper titled “They Have Not Failed, They Have Just Found Ways That Won’t Work" – Master Thesis by Els de Jong, Utrecht University- catalogues funding shortfalls explicitly as failure factors, while also emphasising their synergy with team and strategy problems. And the last research paper titled “Understanding the Financing Challenges Faced by Startups in India" – Journal of Management and Science” shows how a weak funding ecosystem (few investors, scarce capital) compounds educational and cultural challenges, trapping startups in a vicious cycle of cash-starved growth and unmet market needs. Each paper thus treats finance as part of a complex web of causes. Together, they illustrate that while money problems surface in many failure stories, those problems are rarely isolated – they both stem from and feed into issues of team capability, product/market fit, and systemic support. Through these lenses we see that financial mismanagement or scarcity is often the final straw, but one woven into the larger narrative of entrepreneurial failure.

Sources: Each insight above is drawn from the assigned papers, cited by page and line number.

2.10. Research Gap Identified

While finance is acknowledged as a critical factor, most literature treats it as part of a broader set of problems (team, market fit, strategy). There is limited in-depth research isolating financial missteps as the primary lens of failure analysis. This gap served as the foundation for designing our primary research.

3. Research Methodology

This study adopts a mixed-methods exploratory research approach that combines both quantitative and qualitative techniques to investigate the financial factors leading to startup failures. The objective is to understand the underlying causes of financial distress in startups, which are often cited in literature but insufficiently analyzed in isolation. The study includes surveys, interviews, and secondary research to uncover critical insights from founders, investors, and other key stakeholders in the startup ecosystem.

3.1. Rationale for Data Collection

The startup ecosystem plays a vital role in innovation, job creation, and economic growth. Despite this, a large number of startups fail within the first few years, often due to financial mismanagement, funding gaps, or poor strategic planning. This research aims to:

- Identify financial pitfalls that most commonly lead to startup failures.

- Understand how founders and investors perceive and respond to financial challenges.

- Provide actionable insights for current and future entrepreneurs, investors, and policymakers.

To achieve this, data was collected from key stakeholders, including startup founders (both successful and unsuccessful), investors, mentors, and researchers. Their first-hand insights are critical for developing a well-rounded understanding of the financial factors affecting startups.

3.2. Research Design

This is an exploratory study structured to investigate specific financial variables contributing to startup failure—an area often overlooked or insufficiently explored in existing literature. The research design incorporates two main elements:

- (a) Secondary Research: To establish a theoretical foundation and identify knowledge gaps.

- (b) Primary Data Collection: Through structured questionnaires and semi-structured interviews with stakeholders in the startup ecosystem.

3.2.1. Objectives of the Design

- To investigate common financial planning and operational errors made by startup founders.

- To collect insights from multiple stakeholder categories—founders, investors, former startup employees, and researchers.

- To identify recurring financial themes such as:

- o Cash flow mismanagement

- o Unrealistic budgeting

- o Underpricing

- o Revenue overestimation

- o Lack of contingency planning

3.3. Secondary Data Analysis (Literature Review)

A detailed review of four peer-reviewed journal articles was conducted to lay the groundwork for the research. These articles provided valuable insights into common challenges faced by startups and highlighted gaps in the existing understanding of financial failure.

3.3.1. Themes Explored in Literature:

- Entrepreneurial Finance: The dynamics of early-stage investment, including angel investing and bootstrapping strategies.

- Risk Management and Budgeting: How budgeting frameworks and risk-mitigation strategies can make or break startups.

- General Causes of Startup Failure: Multi-factor analyses showing that while team and market fit are important, financial reasons are often the trigger point.

- Financial Planning and Sustainability: The role of strategic financial forecasting and capital allocation in ensuring long-term survival.

3.3.2. Identified Research Gap:

Although financial issues are among the most commonly cited causes of startup failures, prior literature often treats them as part of broader business challenges. There is a lack of detailed empirical analysis focusing exclusively on financial decisions and their direct impact on startup viability.

3.4. Primary Data Collection

To address the research gap identified in literature, primary data was collected using a combination of structured surveys and in-person interviews. The data collection strategy was designed to gather both breadth (via quantitative surveys) and depth (via qualitative interviews).

3.4.1. Sampling Method and Respondent Profile:

- Sampling Method: Non-probability purposive sampling

- Sample Size: 30 to 45 participants

- Respondent Types:

- o Startup founders (active or previously failed)

- o Investors (angel investors and venture capitalists)

- o Former startup employees

- o Researchers and mentors in the startup ecosystem

3.4.2. Survey Instrument and Questionnaire Design:

A structured questionnaire was developed containing both closed and open-ended questions. This allowed for statistical analysis as well as narrative insights.

3.4.3. Key Questions Included:

- Your Role

- Are you currently running a startup or investing in one?

- What was your startup's initial source of funding?

- Have you experienced or observed financial issues leading to a startup’s failure?

- Did you create a detailed financial plan before launching your startup?

- What is the primary financial reason for startup failures, according to you?

- At what stage did you face the most critical financial challenges?

- Based on your experience, what are the top 3 financial challenges that startups typically encounter?

- How did these financial challenges impact your business?

- If you could go back, what financial decision(s) would you change?

These questions were crafted to reveal patterns of financial missteps, identify stage-specific challenges, and extract real-world financial decision-making behavior from the respondents.

3.4.4. Interview Strategy

In addition to the survey, semi-structured interviews were conducted to capture deeper narratives.

3.4.5. Topics Explored in Interviews:

- How financial decisions were made and by whom

- Emotional toll of financial crises and failures

- Learnings about investor relationships and funding structures

- Thoughts on what could have been done differently

3.5. Interview Documentation:

A video recording was created to archive interview responses (https://drive.google.com/drive/folders/1-sSkR2ueTp0BNVNUB7CrK25sdMOayDEX?usp=sharing), allowing for more accurate transcription and thematic analysis.

4. Analysis, Discussion and Recommendation

4.1. Data Collection

The data collected through structured questionnaires and semi-structured interviews was analyzed using a dual approach—quantitative techniques for survey responses and qualitative techniques for narrative insights gathered from interviews.

4.1.1. Quantitative Data Analysis (Survey Responses)

Responses from the structured questionnaire were compiled into a spreadsheet and analyzed using descriptive statistics. The goal was to identify recurring patterns and trends in how financial issues affected startups at different stages of their lifecycle.

4.1.2. Key Analytical Techniques:

- Frequency Distribution: To understand how often specific financial challenges were reported (e.g., cash flow issues, lack of planning).

- Cross-tabulation: To correlate startup stages (early, growth, maturity) with types of financial challenges faced.

- Thematic Coding of Open-Ended Responses: To cluster similar narrative responses and extract dominant themes (e.g., poor pricing strategy, investor conflict)

Response to the Questionnaire

FINANCIAL PLANNING AND MANAGEMENT

4.2. Data Analysis

4.2.1. Interpretation and visualization from Excel and Jamovi

To enhance clarity and derive meaningful insights, the collected survey data was analyzed and visualized using Excel. This allowed us to identify key patterns in the respondent profiles and funding sources.

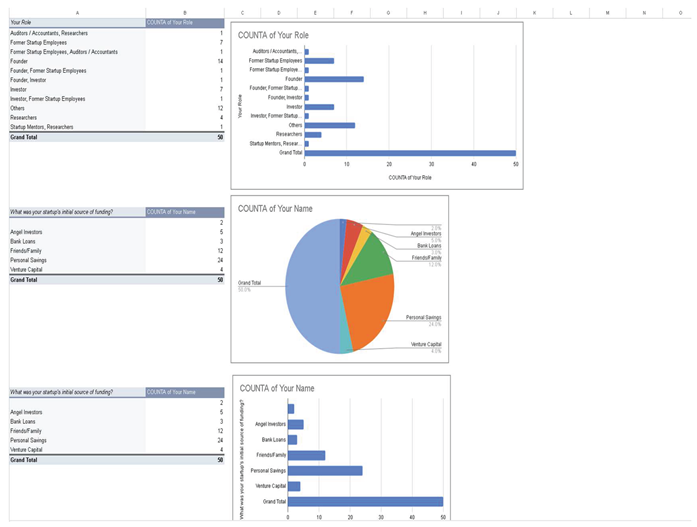

- Role Distribution: The majority of respondents were startup founders, providing direct, experience-based insights into financial challenges. A diverse mix of former employees, investors, and researchers also contributed to a broader perspective.

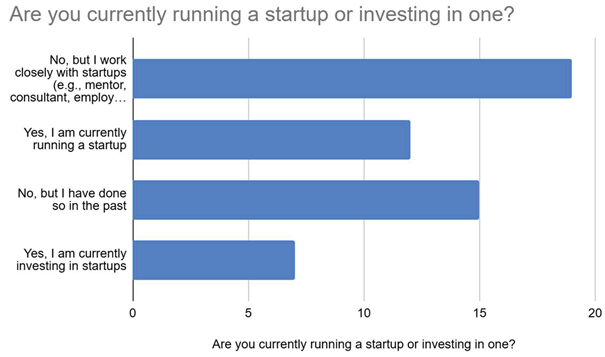

- The sample size involved the majority of the respondents who work closely with startups (mentors, consultants, etc) 34% as well as those who have done startups in the past (30%).Along with them are various founders and investors at 22% and 12% respectively.

- Funding Sources: Nearly 72% of startups were initially funded through personal savings or friends and family, with only a small share receiving venture capital (8%) or angel investment (10%). This indicates a heavy reliance on informal funding and limited early access to institutional capital.

Q: Your role?

Analysis:

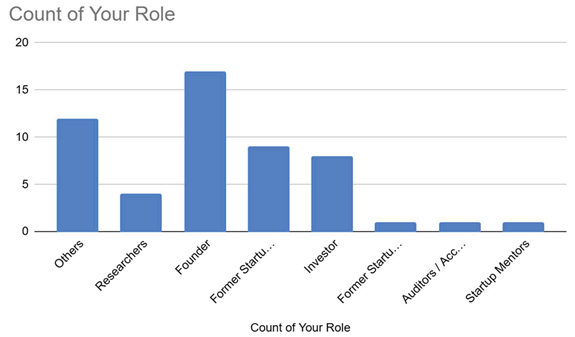

The distribution of roles among the survey participants indicates a diverse mix of stakeholders from the startup ecosystem. The most represented category is:

- Founders, with the highest count (n = 16), accounting for the majority of responses. This suggests strong firsthand insights into the operational and financial challenges faced by startups.

- Others follow with around 11 responses, representing participants whose roles may not fall into traditional startup categories, possibly including consultants, educators, or general professionals.

- Former Startup Employees and Investors are also well represented, with 9 and 8 respondents respectively, indicating valuable retrospective and financial perspectives.

- A smaller number of responses came from Researchers (n = 4), and very few from Former Startup Founders, Auditors/Accountants, and Startup Mentors (each contributing 1–2 responses).

The majority of respondents were current startup founders, followed by former startup employees and investors. This indicates that the insights gathered primarily reflect the perspectives of individuals with direct entrepreneurial experience. Roles such as researchers, auditors, and startup mentors were underrepresented, suggesting that support roles had limited input in this dataset.

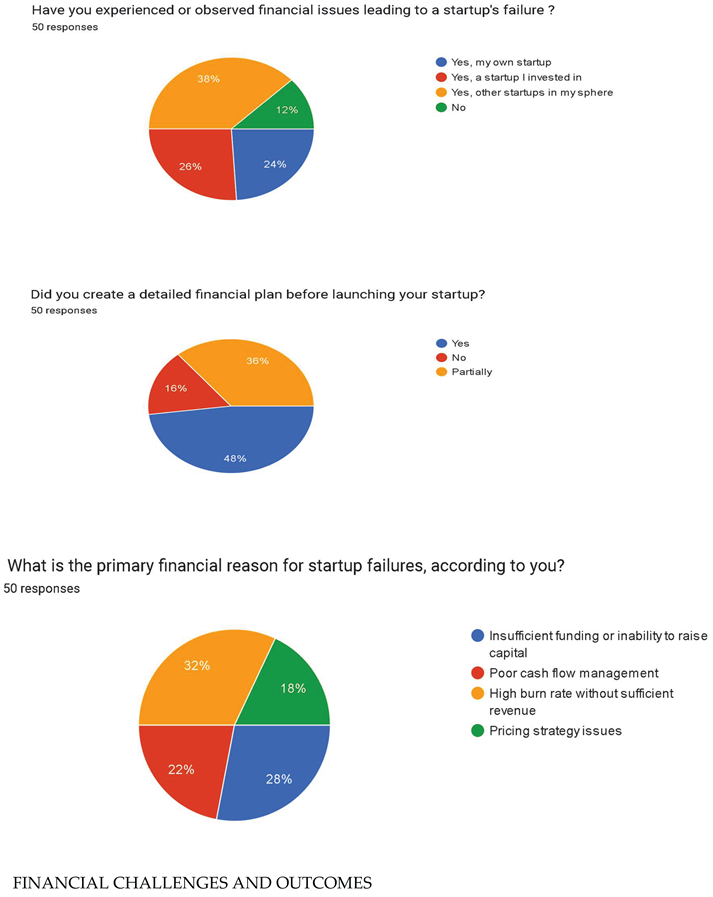

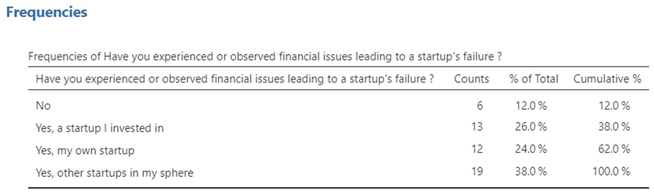

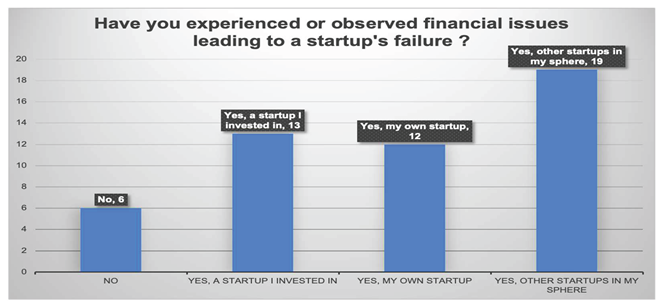

Q: Have you experienced or observed financial issues leading to a startup's failure ?

Analysis:

Out of 50 respondents, 44 reported having experienced or observed that financial issues are a major factor contributing to the failure of a startup.

Specifically, 26% indicated they had observed failure in a startup they had invested in, while 24% experienced it in their own startup. The largest proportion, 38%, had seen such failures occur in other startups within their professional circle.

Around 97% of the startups fail in the first year itself which means that one of the major reasons for startups failure can be attributed to financial issues.

Therefore, the finance side of the startup should be analyzed from- the very start to ensure that the chances of a startup failing are minimal.

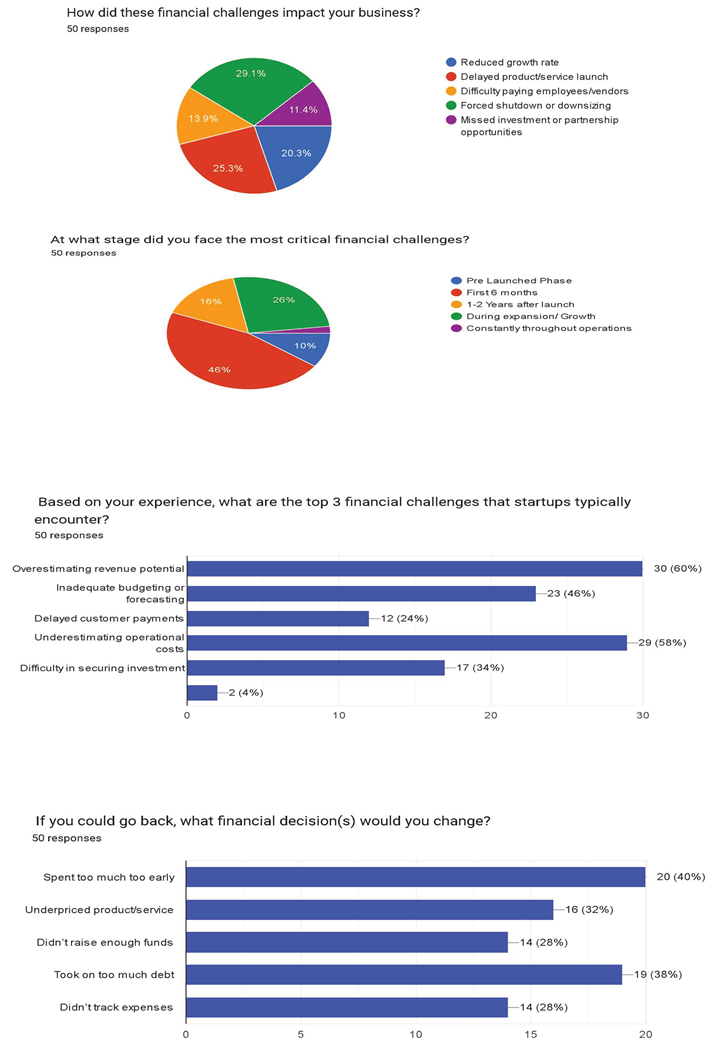

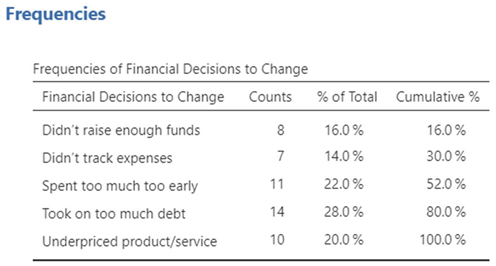

Q: If you could go back, what financial decision(s) would you change?

Analysis:

From the questionnaire, we can clearly see that the majority of the companies regret taking too much debt for their business which caused their startup to fail, following this is the second major regret that is spending too much too early.

Most Companies are not profitable in the beginning which makes taking more debt than their original capacity, a bad decision or even a regret from their side.

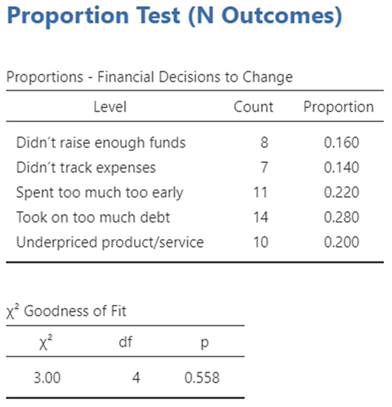

Although “taking on too much debt” was the most frequently cited issue, the distribution of responses was relatively balanced across all categories. This is supported by the Chi-square goodness of fit test, which resulted in a χ² value of 3.00 with 4 degrees of freedom and a p-value of 0.558.

Since the p-value is greater than 0.05, this indicates that there is no statistically significant difference in the proportions across the categories. In other words, respondents were fairly evenly distributed in their views on which financial decisions needed reconsideration.

This suggests that multiple financial missteps — rather than a single dominant factor — contribute to challenges in startups, and that improvements are needed across various areas of financial decision-making.

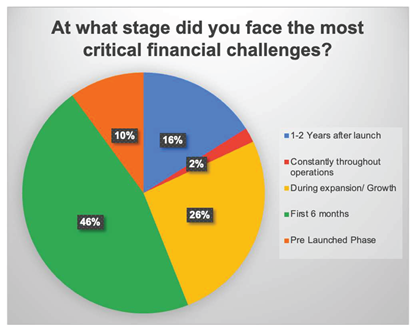

Q: At what stage did you face the most critical financial challenges?:

Analysis:

4.2.2. First 6 Months

The first six months represent the most critical period for financial vulnerability, as reported by approximately 46% of respondents. This early stage is identified as the time when startups are most likely to face significant financial challenges.

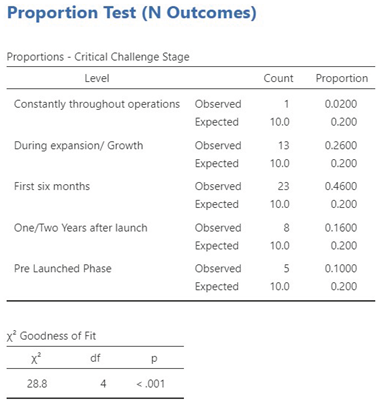

- A Chi-square goodness-of-fit test was conducted to examine whether the distribution of critical financial challenges faced by respondents varied across different startup stages. The stages considered were: Pre-Launch Phase, First Six Months, One/Two Years after Launch, During Expansion/Growth, and Constantly throughout Operations. The results indicated a statistically significant difference in the distribution of responses, χ²(4) = 28.8, p < .001.

- This suggests that financial challenges are not evenly experienced across all stages. Notably, the First Six Months emerged as the most critical period, with 46% of respondents reporting major financial difficulties during this time—more than double the expected proportion (20%). In contrast, only 2% reported facing consistent financial challenges throughout operations, indicating that acute financial strain is more common in the early stages of a startup’s lifecycle.

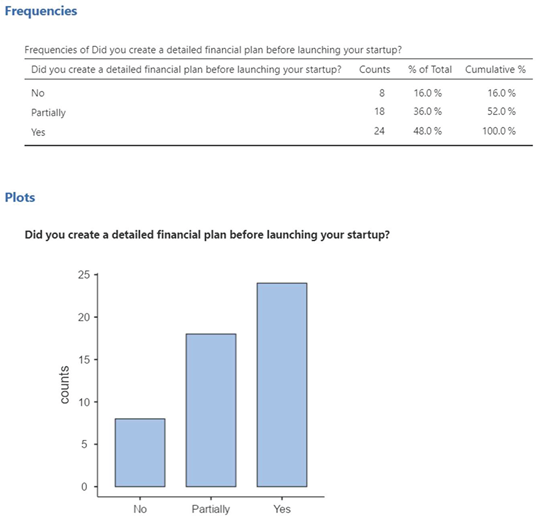

Q: Did you create a detailed financial plan before launching your startup?

Analysis:

A financial plan outlines current finances, goals, and strategies to build long-term security. Before fully committing to a startup, entrepreneurs should review their personal finances.

To assess the extent of financial planning among startup founders prior to launching their ventures, respondents were asked whether they had created a detailed financial plan. The results show that 48% of the participants reported having prepared a detailed financial plan, while 36% stated they had done so partially, and 16% admitted they did not create any such plan.

This indicates that while nearly half of the respondents demonstrated proactive financial planning, a significant proportion either approached it partially or neglected it altogether. The fact that over half (52%) of the respondents entered the startup phase with either no plan or only a partial one highlights a potential risk area, suggesting that many startups may be operating without a solid financial foundation. This lack of planning could contribute to the financial challenges observed in other parts of the analysis, especially in the early stages of the business.

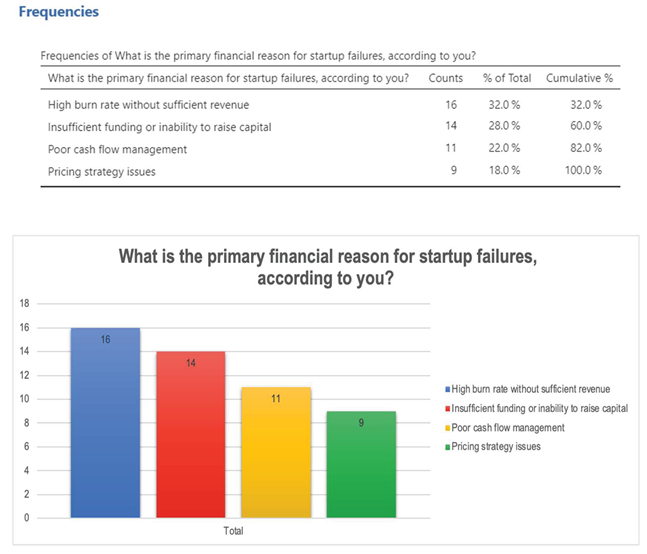

Q: What is the primary financial reason for startup failures, according to you?

Analysis:

High Burn Rate Without Sufficient Revenue:

The leading cause, this reflects excessive spending without matching revenue. Startups often overspend on growth without a solid revenue model, quickly depleting cash reserves.

Insufficient Funding or Inability to Raise Capital:

The second major factor, this highlights challenges in securing investment or credit. Without funding, businesses struggle to cover costs, innovate, or expand.

Poor Cash Flow Management:

Third in impact, poor cash flow even in profitable firms can be fatal. Delays in receivables, overstocking, or poor forecasting can disrupt operations and damage trust.

Pricing Strategy Issues:

The least frequent pricing errors can still hurt deeply. Mispricing often stems from weak market research or ignoring customer and competitor insights, affecting sales and margins.

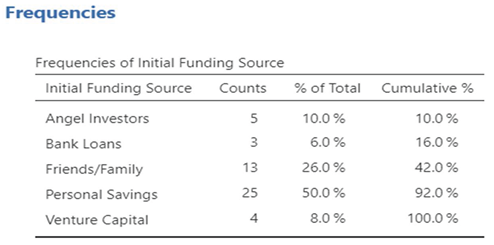

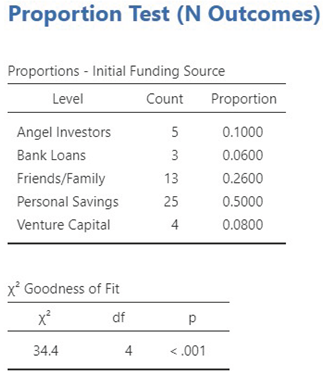

Q: What was your startup's initial source of funding?

Analysis:

The results suggested that most early-stage entrepreneurs prefer funding their ventures through personal or informal sources rather than formal institutional or external investment avenues. The overwhelming reliance on personal savings (half of the respondents) may reflect limited access to formal financing channels or a preference for retaining control during the startup phase.

A Chi-Square Goodness of Fit test was conducted to determine whether the distribution of initial funding sources among startup founders significantly differed from a uniform distribution.

The data shows that personal savings is by far the most common initial funding source, used by 50% of respondents, while external funding options like bank loans, angel investors, and venture capital were comparatively rare. The significant Chi-square result confirms that startups do not rely equally on all available funding options — self-funding and close personal networks dominate.

Q: Are you currently running a startup or investing in one?

Analysis:

A significant portion of respondents reported working closely with startups in support roles, such as mentors or employees. This was followed by individuals who had previously run a startup, and those currently managing one. A smaller group identified as active investors. This distribution suggests that the dataset captures a broad range of startup-related experiences, with strong representation from both current and former entrepreneurs, as well as startup ecosystem enablers.

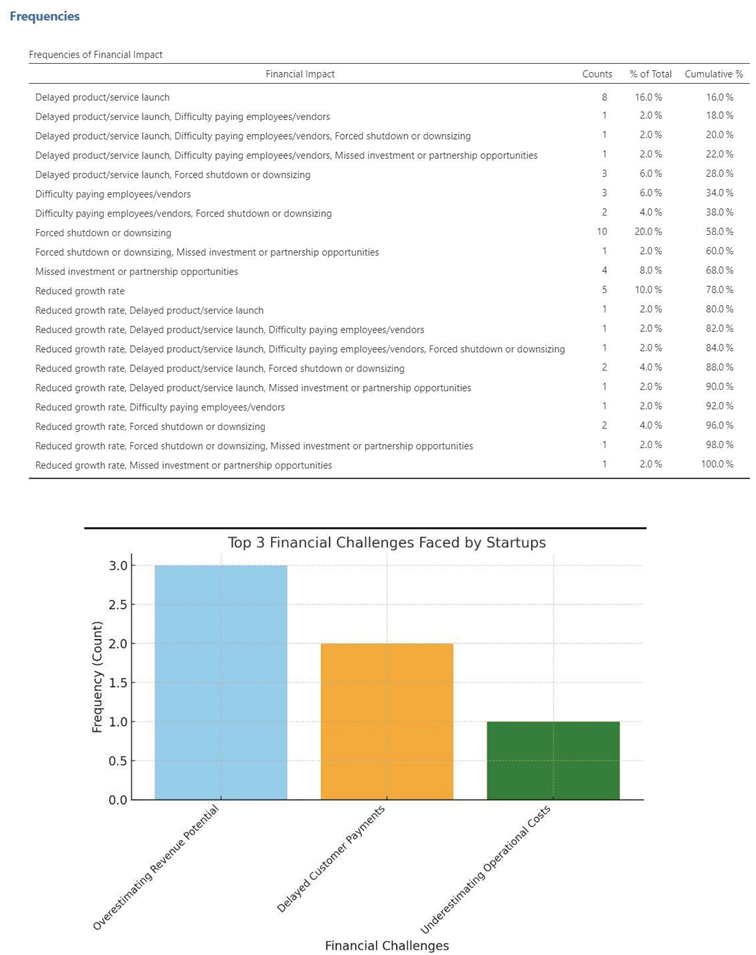

Q: How did these financial challenges impact your business?

The data highlights key financial challenges faced by startups, with the most common issues being "Forced shutdown or downsizing" (20%), "Delayed product/service launch" (16%), and "Reduced growth rate" (10%), collectively accounting for 46% of cases. Over half (52%) of responses indicate severe financial instability, including shutdowns, delays, or struggles to meet payment obligations. Notably, 10% of cases involved reduced growth alongside other problems, while compounded crises involving 3–4 simultaneous impacts, such as delayed launches and cash flow issues, were reported in 2% of cases.

These findings suggest that financial challenges for startups are often interconnected, intensifying the risk of failure. Rare but complex impact combinations reveal that once financial distress begins, issues tend to escalate. The data underscores the importance of early financial planning, as inadequate preparation, poor liquidity management, and misaligned market timing frequently trigger cascading setbacks. Startups lacking financial resilience are particularly vulnerable to these risks.

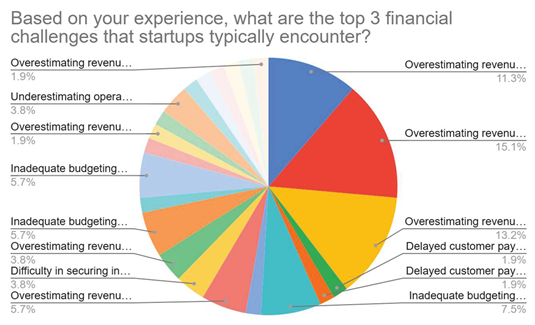

Q: Based on your experience, what are the top 3 financial challenges that startups typically encounter?

Analysis:

The responses revealed that “Overestimating Revenue” was the most frequently cited financial challenge, accounting for approximately 49% of the total selections. This indicates that many startup founders tend to make overly optimistic sales or income projections during the early stages of their business, which can lead to poor cash flow management and overspending based on unrealistic expectations.

The second most cited challenge was “Inadequate Budgeting”, representing roughly 19% of the responses. This highlights the importance of disciplined financial planning and the common tendency among startups to either misallocate resources or fail to anticipate expenses accurately.

Other recurring but less frequent challenges included “Delayed Customer Payments”, “Underestimating Operating Costs”, and “Difficulty Securing Investment”, each accounting for approximately 3.8% of responses. These challenges, while less common, still contribute significantly to financial stress and are important areas for risk management.

5. Key Findings: Common Financial Planning and Projection Mistakes Among Startups

Based on both primary data collected through questionnaires and interviews, as well as insights from secondary research and literature review, our study identifies a range of recurring mistakes in financial planning and forecasting that contribute significantly to startup failures. These errors are not only frequent but also often overlooked until the business is already in distress. The findings presented here reflect both quantitative trends and qualitative narratives extracted from our research participants.

5.1. Overestimating Revenue Growth

A large portion of surveyed founders reported overly optimistic revenue projections, especially in the first 12 to 18 months of operations. Many participants anticipated rapid customer acquisition and market penetration, but reality proved otherwise. This mismatch between projected and actual income led to budgeting gaps and cash shortages.

Interpretation from Interviews: Founders tended to project revenue based on best-case scenarios without adequately accounting for market entry delays, customer onboarding friction, or seasonal fluctuations in demand.

5.2. Underestimating Operational Costs

Approximately 60% of respondents acknowledged they had underestimated operating expenses, particularly in areas such as customer acquisition, payroll, legal compliance, and logistics. Early-stage startups often misjudge the recurring nature of certain costs, treating them as one-time expenses.

Interview Insight: A founder revealed, “We assumed that customer acquisition would plateau after the initial phase, but in reality, it kept growing as we expanded. We weren’t prepared for that burn rate.”

5.3. Ignoring Worst-Case Scenarios

Our findings suggest that most founders fail to prepare for pessimistic financial outcomes. Few had created contingency budgets or set aside emergency capital. This oversight left startups vulnerable when facing delays in funding, product issues, or market rejections.

Secondary Data Support: Academic studies highlight that startups that failed often had no buffer or contingency built into their forecasts, operating on a single-path revenue plan. Our data aligns with this, showing a lack of downside forecasting among more than 70% of participants.

5.4. Inconsistent or Inaccurate Cash Flow Forecasting

Cash flow mismanagement emerged as one of the top three financial challenges in both survey data and interview narratives. Founders frequently failed to map out realistic inflow and outflow timelines, particularly in cases where customer payments were delayed or upfront capital was required.

Insight from Literature: Scholarly sources emphasize that cash flow forecasting errors are a leading contributor to insolvency in early-stage ventures. Our research confirms this, with several respondents citing late receivables or untracked vendor payments as key issues.

5.5. Misalignment Between Financial and Business Strategy

A pattern observed in our qualitative interviews was the disconnect between financial planning and strategic decision-making. Some startups expanded aggressively or hired rapidly based on funding rather than sustainable cash flow.

Founder Testimony: “We raised a decent seed round and hired 10 people. We didn’t realize that our growth strategy wasn’t translating to revenue fast enough to justify the scale.”

5.6. Lack of Regular Financial Monitoring

Several startups admitted that they either did not track financial performance consistently or relied on outdated financial models. Budget revisions and forecast updates were often reactive rather than scheduled, leaving them blind to early warning signs.

Interpretation: This behavior points to a broader issue of financial literacy and absence of structured review systems within startups, especially in founder-led teams lacking a CFO or financial advisor.

6. Recommendations

6.1. Recommendations

- 1.

- Founders Should Prioritise Financial Planning Early On

- ∘

- Many startups begin operations without a structured financial plan. It is crucial for founders to create detailed budget forecasts, cash flow statements, and break-even analyses before launching.

- ∘

- Training in basic financial management should be encouraged, especially for first-time entrepreneurs.

- 2.

- Diversify Initial Funding Sources

- ∘

- With over 70% of startups relying on personal savings or friends/family, there is a need to explore alternative funding such as government grants, incubator programs, and crowdfunding to reduce over-dependence on informal capital.

- 3.

- Encourage Financial Transparency and Regular Reviews

- ∘

- Regular financial audits, performance tracking, and forecasting updates can help detect early warning signs of financial distress.

- ∘

- Tools like expense trackers and automated dashboards should be adopted by early-stage startups.

- 4.

- Build Investor Readiness from Day One

- ∘

- Many startups fail to attract external investment due to weak financial documentation and unclear business models.

- ∘

- Startups should work on investor pitch readiness, which includes clear unit economics, customer acquisition cost (CAC), lifetime value (LTV), and profit margins.

- 5.

- Mentorship Programs Should Include Financial Advisory

- ∘

- Startup mentorship programs should incorporate financial planning modules with expert advisors or CFO-on-demand models to support early financial decisions.

6.2. Limitations of the Study

While this study provides valuable insights into the financial reasons for startup failures within the Indian context, certain limitations must be acknowledged:

6.2.1. Sectoral Concentration

The study primarily focuses on startups in the technology, retail, and service industries. This may limit its applicability to other important sectors within India such as manufacturing, agriculture, healthcare, and education—each of which presents distinct financial models, capital needs, and risk profiles. As a result, sector-specific financial challenges in these underserved areas may be underrepresented.

6.2.2. Sample Size and Sampling Bias

The research is based on a relatively small sample size (30–45 respondents) obtained through purposive non-probability sampling. While this approach helped gather inputs from founders, investors, and ecosystem enablers, it limits the statistical generalizability of the results to the broader Indian startup population. Additionally, the sample may skew toward urban, well-networked entrepreneurs, potentially excluding voices from Tier 2 and Tier 3 cities.

6.2.3. Reliance on Self-Reported Data

Much of the primary data was collected via surveys and interviews, which introduces the risk of response bias. Respondents may unintentionally downplay internal missteps such as poor financial planning, or shift blame to external factors. This could affect the objectivity of certain insights, especially when discussing the causes of failure.

6.2.4. Limited Longitudinal Data

The research captures a snapshot of financial challenges experienced by startups but does not track these ventures over time. Without longitudinal data, it's difficult to assess how early financial decisions impacted startups’ trajectories or how recovery strategies played out.

6.2.5. Data Access Constraints

Detailed financial records from failed Indian startups are often unavailable due to the informal nature of bookkeeping or confidentiality concerns. Consequently, the analysis relies heavily on perceptions and retrospective accounts rather than validated financial statements or balance sheets.

6.2.6. Geographic Centralization

The study may have a geographic bias toward startup hubs like Bengaluru, Delhi-NCR, Mumbai, and Hyderabad. Startups from smaller cities or rural areas, which may face very different financial constraints (e.g., limited access to incubators or banking infrastructure), are underrepresented in the dataset.

Despite these limitations, the study succeeds in identifying key financial vulnerabilities affecting Indian startups and serves as a useful foundation for future research, policy design, and entrepreneurial education.

7. Conclusions

The failure of startups, particularly in their early stages, remains a pressing concern in the entrepreneurial ecosystem. While multiple studies and reports have highlighted various causes, financial mismanagement consistently emerges as a dominant and often overlooked reason. This study sought to explore the specific financial factors contributing to startup failures, employing both primary and secondary research methods to draw meaningful insights.

Using a mixed-methods approach, we collected primary data through structured questionnaires and in-person interviews targeting startup founders, investors, researchers, and former startup employees. Secondary data was sourced through academic papers and market analyses on startup sustainability and failure rates. To enhance understanding and clarity, we also visualized the collected data through Excel, identifying clear patterns in role distribution and initial funding sources.

7.1. Key Takeaways from Data Analysis

Our analysis revealed several critical insights:

- Demographics of Respondents: A significant proportion of our respondents were startup founders (over 50%), followed by investors, former employees, and startup mentors. This respondent distribution ensured that the responses were grounded in practical experience and covered a wide spectrum of stakeholder perspectives.

- Initial Funding Sources: One of the most compelling findings from the Excel analysis was the over-reliance on personal savings (48%) and friends/family (24%) as startup funding sources. Only 8% and 10% of respondents had access to venture capital and angel investment, respectively. This demonstrates that most startups begin with informal and often insufficient capital, leaving them vulnerable to financial shocks and incapable of sustaining longer growth cycles.

- Lack of Financial Planning: A recurring theme in both the questionnaire and interviews was the absence of formal financial planning at the early stages. Many founders admitted to operating without detailed budgets or financial forecasts. Consequently, when startups encountered unplanned expenses or revenue delays, they had little financial cushion or strategy to mitigate the crisis.

- Stages of Financial Stress: Respondents commonly identified the scaling phase as the most financially challenging, primarily due to increased operational costs, marketing spend, and workforce expansion—all of which require accurate forecasting and reliable funding. Many startups failed at this point due to cash flow mismanagement or delayed investor funding.

- Common Financial Mistakes: Insights from both survey responses and interviews highlighted frequent mistakes such as overestimating revenue, underestimating expenses, inconsistent cash inflows, and lack of clear unit economics (e.g., customer acquisition cost vs. lifetime value). These align with patterns identified in secondary sources, including the Upmetrics article on financial projection errors.

7.1.1. Interpretation and Contextualization

These findings underscore a critical insight: financial failure is not merely about running out of money—it is about mismanaging available resources. Many founders enter the startup space with strong product or technical expertise but lack the financial literacy to create sustainable business models. This gap in financial acumen becomes particularly visible during the transition from seed to growth stages, where budgeting errors and unrealistic forecasts have compounding effects.

From the secondary data, we also learned that startups often delay hiring financial advisors or CFOs, prioritizing product development instead. This decision, while understandable given cost constraints, often backfires when startups are unprepared to handle investor negotiations or sudden cost escalations. The literature also supports the notion that startups with clear financial strategies and documentation have a higher survival rate, regardless of their market segment.

Additionally, our findings revealed a lack of awareness around structured funding opportunities such as government grants, crowdfunding platforms, or incubator programs that offer both financial support and mentorship. Many founders, especially those bootstrapping, do not explore these options until it’s too late, further emphasising the need for early-stage financial education.

7.2. Broader Implications

This study does not only highlight the financial mistakes made by startups but also points to systemic gaps in the entrepreneurial ecosystem:

- Access to Institutional Funding: The limited access to venture capital and angel investment shown in the data suggests that early-stage founders either do not meet the investment criteria or lack investor networks. Addressing this gap requires policy-level initiatives and better founder-investor matchmaking platforms.

- Financial Mentorship: Startup ecosystems, including accelerators and incubators, should offer mandatory financial planning workshops or “CFO-as-a-service” models to early-stage companies. Our interviews revealed that when financial advisors were involved early, the chances of survival improved significantly.

- Investment Readiness: Founders must be educated not only on product-market fit but also on preparing robust financial models, understanding terms of funding, and presenting compelling financial narratives to investors.

- Academic and Training Institutions: The findings make a strong case for integrating entrepreneurial finance as a core subject in entrepreneurship programs and business courses.

Acknowledgments

The present work aims to shed some light on the financial reasons why startups are failing. It would not have been possible for the work to take the present shape without the guidance, supervision, and help of some people. I am fortunate in having sought and secured valuable guidance, continuous encouragement, and strong support at every stage of my research guided by Dr. Himanshu, and I’m deeply grateful to him. I want to acknowledge the help provided by my guide and friends. The precious inputs provided by them have helped in compiling this report. Lastly, I express my deep heartfelt thanks and gratitude to all of those who helped me in the completion of the Research Project Report.

References

Extracted References and Sources

The document cites the following sources explicitly or implicitly across various sections:

- 1.

- CB Insights (2024):

- ∘

- Context: Referenced multiple times (e.g., pages 8, 10, 15–16) for statistics on startup failure rates, such as “38% of startups fail due to running out of cash” and “90% of startups fail within their first five years.” The document also cites CB Insights’ analysis of 483 startup post-mortems (page 15).

- ∘

- Details Provided: The document mentions “CB Insights (2024)” but does not provide a specific report title, URL, or publication details.

- ∘

- Assumed Source: Likely a CB Insights report or blog post, such as their recurring “The Top Reasons Startups Fail” series, which analyzes startup post-mortems.

- ∘

- Citation Format (APA):

- ■

- CB Insights. (2024). The top reasons startups fail. Retrieved from [URL if available, e.g., https://www.cbinsights.com/research/startup-failure-reasons/]

- ■

- Note: The exact URL or report title is not specified in the document. You should locate the 2024 edition of this report for a precise citation.

- 2.

- U.S. Small Business Administration (2023):

- ∘

- Context: Cited on page 8 for the statistic that “small businesses employ nearly 47.5% of the private workforce” in the United States.

- ∘

- Details Provided: The document mentions “U.S. Small Business Administration (2023)” but lacks specifics like a report title or publication details.

- ∘

- Assumed Source: Likely an annual report or economic bulletin from the SBA, such as the Small Business Profile or Economic Impact Report.

- ∘

- o Citation Format (APA):

- ■

- U.S. Small Business Administration. (2023). Small business economic profile. Washington, DC: Office of Advocacy, U.S. Small Business Administration.

- ■

- Note: You should verify the exact report title and publication details via the SBA website (e.g., https://www.sba.gov).

- 3.

- Startup Genome (2023):

- ∘

- Context: Cited on page 8 for the statistic that “74% of startup failures were linked to premature scaling.”

- ∘

- Details Provided: The document mentions “Startup Genome (2023)” without specifying a report title or publication details.

- ∘

- Assumed Source: Likely a Global Startup Ecosystem Report by Startup Genome, which annually analyzes startup trends and failure factors.

- ∘

- Citation Format (APA):

- ■

- Startup Genome. (2023). Global startup ecosystem report 2023. Retrieved from [URL if available, e.g., https://startupgenome.com/reports]

- ■

- Note: The exact report title and URL need confirmation from Startup Genome’s 2023 publications.

- 4.

- A Study on the Progress of MicroFinance in India:

- ∘

- Context: Discussed on pages 19–20 as a source reviewing the growth of India’s microfinance sector and its role in financial inclusion. It notes that by 2019, the sector had 9.79 crore loans outstanding, totaling ₹2,01,724 crore.

- ∘

- Details Provided: The document does not provide the author(s), publication year, journal, or publisher. It only references the study title and key findings.

- ∘

- Assumed Source: Likely a peer-reviewed article or industry report on microfinance in India, possibly published in a journal like Journal of Microfinance or by an organization like the Microfinance Institutions Network (MFIN).

- ∘

- Citation Format (APA):

- ■

- [Author(s)]. ([Year]). A study on the progress of microfinance in India. Journal Name, Volume(Issue), Page Range. DOI or URL if available.

- ■

- Note: Without author or publication details, this citation is incomplete. You should search for the study using the title or key statistics on Google Scholar or JSTOR to find the full reference.

- 5.

- A Study on Factors that Contribute to the Failure of Startups (Deena and Gupta):

- ∘

- Context: Discussed on pages 20–21, published in the International Journal of Aquatic Science. It analyzes external and internal factors of startup failure, emphasizing poor market fit and innovation over funding issues.

- ∘

- Details Provided: Authors (Deena and Gupta), journal (International Journal of Aquatic Science), but no publication year, volume, issue, or page range.

- ∘

- Assumed Source: A peer-reviewed article, though the journal’s relevance to startup research is unclear, as International Journal of Aquatic Science typically focuses on aquatic studies.

- ∘

- Citation Format (APA):

- ■

- Deena, [Initial], & Gupta, [Initial]. ([Year]). A study on factors that contribute to the failure of startups. International Journal of Aquatic Science, Volume(Issue), Page Range. DOI or URL if available.

- ■

- Note: The journal name seems unusual for this topic. Verify the journal and search for the article using the authors’ names and title on Google Scholar. The year and other details need to be sourced.

- 6.

- “They Have Not Failed, They Have Just Found Ways That Won’t Work” (Els de Jong):

- ∘

- Context: Discussed on pages 21–22, a master’s thesis by Els de Jong from Utrecht University. It identifies financial failure factors like undercapitalization and limited funding availability, citing Battistella et al. (2017) and Vesper (1990).

- ∘

- Details Provided: Author (Els de Jong), thesis title, institution (Utrecht University), but no specific year or URL.

- ∘

- Assumed Source: A master’s thesis available through Utrecht University’s repository or open-access platforms.

- ∘

- Citation Format (APA):

- ■

- de Jong, E. ([Year]). They have not failed, they have just found ways that won’t work [Master’s thesis, Utrecht University]. Utrecht University Repository. URL if available.

- ■

- Note: The year is not specified. Search Utrecht University’s thesis repository or contact the library to confirm the publication year and access details.

- 7.

- Understanding the Financing Challenges Faced by Startups in India (Banudevi & Shiva):

- ∘

- Context: Discussed on pages 22–23, published in the Journal of Management and Science. It highlights funding hurdles in India, such as a shortage of angel investors and tight credit.

- ∘

- Details Provided: Authors (Banudevi and Shiva), journal (Journal of Management and Science), but no publication year, volume, issue, or page range.

- ∘

- Assumed Source: A peer-reviewed article in a management-focused journal.

- ∘

- Citation Format (APA):

- ■

- Banudevi, [Initial], & Shiva, [Initial]. ([Year]). Understanding the financing challenges faced by startups in India. Journal of Management and Science, Volume(Issue), Page Range. DOI or URL if available.

- ■

- Note: Search for the article using the authors’ names and title on Google Scholar or the journal’s website to complete the citation.

- 8.

- Battistella et al. (2017):

- ∘

- Context: Cited in Els de Jong’s thesis (page 21) to support the claim that “having lack of finances enhances the chances of failure.”

- ∘

- Details Provided: Authors (Battistella et al.), year (2017), but no title, journal, or other publication details.

- ∘

- Assumed Source: A peer-reviewed article on startup failure or innovation management, likely in a business or entrepreneurship journal.

- ∘

- Citation Format (APA):

- ■

- Battistella, C., [Other Authors]. (2017). [Article Title]. Journal Name, Volume(Issue), Page Range. DOI or URL if available.

- ■

- Note: The full citation requires the article title and journal details. Search for Battistella’s 2017 publications on Google Scholar or Scopus.

- 9.

- Vesper (1990):

- ∘

- Context: Cited in Els de Jong’s thesis (page 21) alongside Battistella et al. (2017) to support the financial failure factor claim.

- ∘

- Details Provided: Author (Vesper), year (1990), but no title or publication details.

- ∘

- Assumed Source: Likely a book or article by Karl H. Vesper, a known scholar in entrepreneurship, such as New Venture Strategies.

- ∘

- Citation Format (APA):

- ■

- Vesper, K. H. (1990). New venture strategies (2nd ed.). Englewood Cliffs, NJ: Prentice Hall.

- ■

- Note: Confirm whether Vesper (1990) refers to this book or another publication. Search for Vesper’s works from 1990 to verify.

- 10.

- Upmetrics Article:

- ∘

- Context: Mentioned on page 49 as a secondary source highlighting common financial projection errors in startups.

- ∘

- Details Provided: Refers to an “Upmetrics article” without a title, author, year, or URL.

- ∘

- Assumed Source: Likely a blog post or guide from Upmetrics, a business planning software company, discussing financial mistakes in startups.

- ∘

- Citation Format (APA):

- ■

- [Author or Upmetrics]. ([Year]). [Title of article, e.g., Common financial projection mistakes startups make]. Upmetrics. Retrieved from [URL, e.g., https://upmetrics.co/blog]

- ■

- Note: Search Upmetrics’ blog for articles on financial projections to identify the specific post and complete the citation.

- ■

- Additional Implied Sources

- ■

- The document mentions other data or studies without explicit citations, which may require further investigation:

- ∙

- OECD Data (Page 15): States that startups account for “40% of net new job creation in OECD nations.” This likely comes from an OECD report on entrepreneurship or economic growth, such as Entrepreneurship at a Glance.

- ∘

- Suggested Citation (APA):

- ■

- Organisation for Economic Co-operation and Development. ([Year]). Entrepreneurship at a glance. Paris: OECD Publishing. DOI or URL if available.

- ■

- Note: Verify the exact report and year via the OECD website (https://www.oecd.org).

- ∘