Submitted:

18 May 2025

Posted:

19 May 2025

You are already at the latest version

Abstract

This article systematically reviews the execution of strategic CSR programs and initiatives in the financial sector of emerging economies, exploring their impact within distinctive regulatory and socio-economic environments. The article has addressed gaps in the existing literature by evaluating CSR practices beyond the banking sector, including insurance and fintech, and their adherence to sustainability performance. A systematic literature review was conducted using peer-reviewed journals, case studies, and credible industry reports published in the past decade, yielding 121 relevant studies after rigorous screening from an initial pool of 11,200 sources. The review focused on strategic CSR in the financial sectors of World Bank-defined emerging economies. The findings revealed that CSR in the financial sectors of emerging economies is truly effective when strategically integrated with business operations and aligned with stakeholder expectations and globally proclaimed sustainability goals. Despite persistent barriers, CSR, when contextually adapted, enhances both financial and non-financial performance, including stakeholder trust, brand value, and long-term resistance of the respective company. However, its context-dependent impact highlights the need for robust frameworks, ethical leadership, and rigorous, localized research to completely realize its transformative potential.

Keywords:

Strategic CSR

; Emerging Economies

; Financial Sector

; Key Performance Indices

; Sustainable Practices

1. Introduction

Corporate social responsibility (CSR) within corporations has been widely debated in academic discourse for a long time, particularly as corporations are increasingly facing pressure to reform their operational practices [6,108,112]. Overall, CSR refers to an organization’s commitment to operating in a socially and environmentally responsible manner, taking into consideration the impact of CSR initiatives on stakeholders [96,119]. This approach requires companies to consider their impact on a broad range of stakeholders and society at large, beyond the sole objective of profit generation [1].

Scholars have long explored the relationship between CSR and organizational growth and profitability. However, findings on this relationship have varied significantly across countries. A 2022 KPMG survey noted a significant increase in global CSR reporting rates since the early 2000s, with a more substantial rise observed in developed nations compared to emerging economies [122]. The survey highlighted that the countries in Africa, the Middle East, Eastern Europe, and Latin America continue to lag compared to emerging economies such as India, Malaysia, South Africa, Mexico, and Taiwan in CSR reporting [6]. The COVID-19 pandemic further underscored existing global disparities, disproportionately affecting emerging and developing nations categorized as low-income economies [2,45]. In these regions, issues such as inadequate working conditions, poverty, and human rights violations remain critical challenges [1,3]. Additionally, organizations operating in such environments often face additional obstacles, including corruption, limited educational opportunities, social inequality, and power imbalances, all of which increase the risk of corporate misconduct. Yet rather than exploiting these institutional voids or market failures, some organizations have leveraged CSR as a tool to address these challenges [2,3].

Historically, corporations have engaged in CSR initiatives aiming at inclusive economic development by involving diverse stakeholders in decision-making processes and addressing poverty in surrounding communities [3]. Early empirical research on CSR was driven by the intention to demonstrate that socially responsible actions could be strategically justified by their positive performance outcomes [4]. Consequently, CSR has evolved from being perceived as a voluntary initiative to a strategic necessity, especially in emerging economies [4]. In certain cases, corporations in these regions have contributed to broader societal goals by implementing programs that provide marginalized groups with access to resources, enabling them to benefit from local assets and create new opportunities [2,3]. Nevertheless, empirical evidence suggests that the relationship between CSR and organizational performance is complex, context-dependent, and not always immediately apparent. This complexity is due to the intangible nature and long-term orientation of CSR outcomes [1,3,4]. Moreover, the majority of the prior literature has focused on industries such as engineering, construction, and real estate [1,2,5,7], creating a gap in the literature regarding the financial sector.

There is a growing call for financial institutions to align their financial flows with climate-resilient development goals, as outlined by the COP-UNFCCC framework [7]. This requires institutions to integrate sustainability into their corporate strategies. Unlike conventional finance, sustainable finance aims to allocate capital to sectors that are likely to generate positive economic, environmental, and social impacts [7,10]. Given the central role financial institutions play in national economic development, their commitment to sustainability has significant societal and environmental implications. For example, in today’s environmentally conscious society, banking customers can easily access information such as annual reports to evaluate their banks' sustainability performance [9]. Despite the growing emphasis on sustainability, existing literature tends to focus primarily on the banking sector, resulting in a limited understanding and raising concerns about data validity and generalizability.

To address this gap, this systematic review examines how strategic CSR initiatives are implemented across the broader financial sector in emerging markets, including banking, insurance, and fintech. The study evaluates the sustainability performance of these institutions and seeks to deepen the understanding of CSR practices within the unique regulatory, socio-economic, and market contexts of emerging economies, as these contexts shape CSR implementation in ways distinct from those in developed economies [8].

2. Methodology

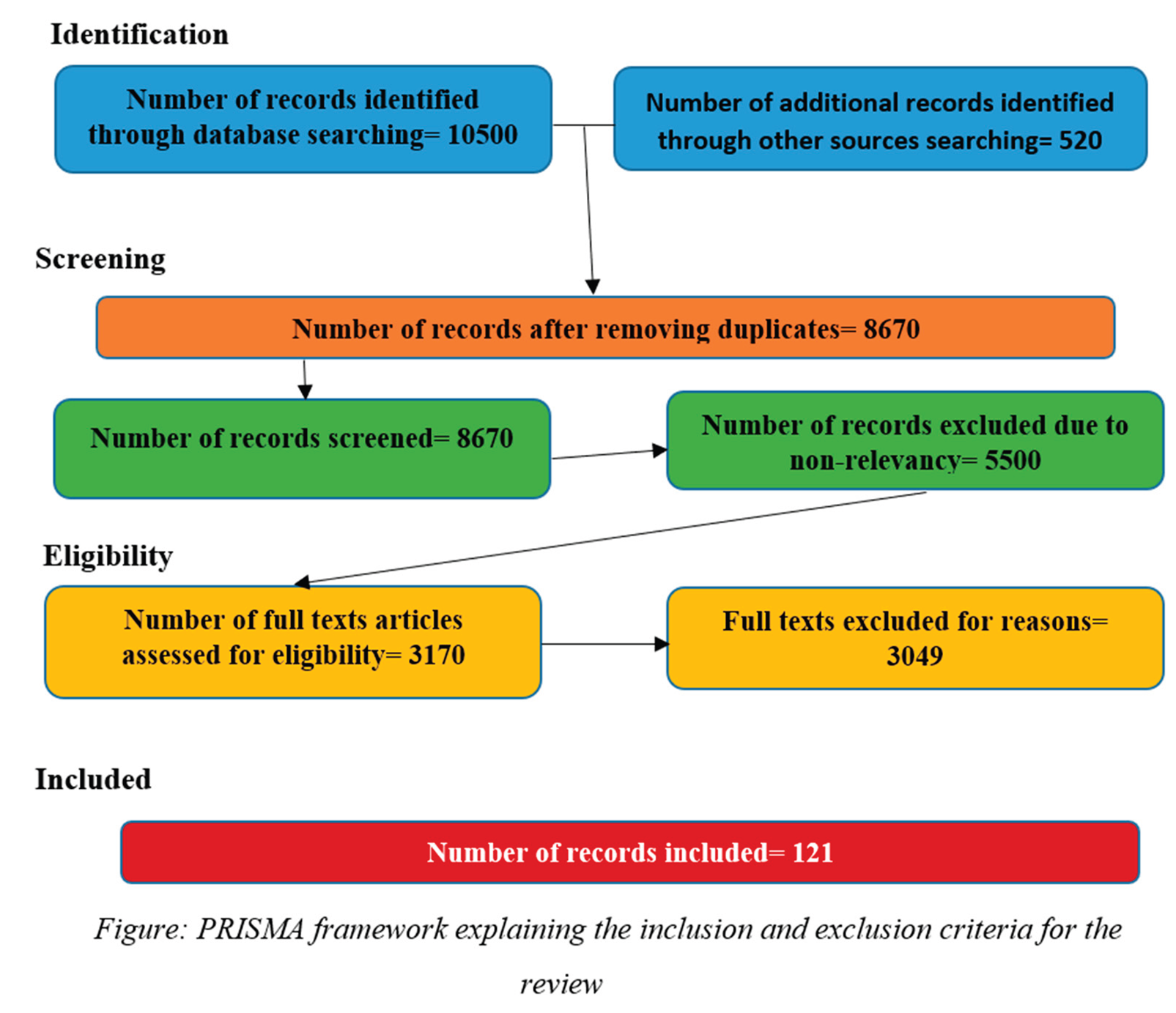

The methodology employed for this review follows a systematic approach grounded in a comprehensive synthesis of literature sourced from peer-reviewed journals, case studies, and industry or corporate reports published over the past decade (2015–2025). The review focused on high-quality, relevant, and credible sources to ensure rigor and relevance. The primary search terms guiding the literature identification and selection process included "Strategic CSR," "Emerging or Developing Countries," "Financial Sector," "Sustainability Practices," and "Key Performance Metrics." These terms were chosen to capture literature that addressed corporate social responsibility (CSR) from a strategic perspective within the context of emerging economies and the financial services sector.

The initial phase of the methodology began with a scoping search aimed at mapping the breadth and depth of existing literature. This phase enabled the identification of the quantity, scope, and nature of available studies, with an emphasis on scholarly rigor and relevance to the research focus. The scoping review also revealed that CSR literature is both expansive and multidimensional, necessitating a systematic approach to identify studies that specifically addressed strategic CSR initiatives in emerging or developing countries. Approximately 11,200 articles were initially retrieved from reputable academic databases such as ProQuest, ScienceDirect, Wiley Online Library, and Taylor & Francis. Supplementary sources, including ResearchGate, Academia.edu, and Google Scholar, were also consulted to ensure comprehensive coverage.

In the subsequent screening phase, duplicate entries were eliminated, reducing the pool to 8670 articles. Titles and abstracts were then carefully examined to determine alignment with the study’s inclusion criteria. Priority was given to studies that explored CSR as an integral component of long-term corporate strategy rather than as isolated philanthropic efforts. Only those articles focusing on CSR embedded within core business operations, particularly in the context of World Bank-defined emerging economies and within the financial sector, including banking, microfinance, investment, insurance, and asset management, were retained. As a result, 5,500 articles were excluded due to a lack of relevance or failure to meet the predetermined inclusion parameters.

During the evaluation phase, the remaining articles were rigorously assessed for quality and credibility. Full-text screening was conducted to evaluate the type of publication, research methodology, time frame, and language. Editorials, opinion pieces, blog posts, and book reviews were excluded because they do not meet scholarly standards for peer review. Only peer-reviewed journal articles, conference proceedings, book chapters, and official corporate or government publications were considered. Furthermore, only articles published in English between 2015 and 2025 were included, reflecting the contemporary relevance of strategic CSR following the adoption of the United Nations Sustainable Development Goals (SDGs) in 2015. Both qualitative and quantitative studies were included, encompassing systematic reviews, case studies, theoretical contributions, and empirical investigations. Conceptual papers lacking empirical or contextual grounding, as well as studies with incomplete reporting of results, were excluded. An additional 3,049 articles were removed during this phase, resulting in a final dataset of 121 articles that formed the foundation of this systematic literature review.

3. Conceptualizing Strategic CSR and Sustainability in Emerging Economies

The concept of corporate social responsibility (CSR) has been extensively recognized in the existing literature. Historically regarded as a voluntary concept, CSR encompasses activities aimed at generating benefits for the greater good [9,11]. In emerging economies, CSR initiatives have traditionally been philanthropic, rooted in cultural practices, and intended to compensate for inadequate social services. However, perceptions and interpretations of CSR have evolved [10,11,13]. Despite ongoing debates surrounding the components of CSR, the most widely accepted definition remains that proposed by Carroll in 1979 [12,14]. Carroll describes CSR as the moral responsibility of businesses to contribute towards societal well-being, encompassing ethical and philanthropic expectations alongside the pursuit of economic profits.

Numerous earlier studies have highlighted the voluntary disclosure of CSR achievements, yet there remains limited insight into the actual extent of CSR expenditures [10,15]. The philanthropic aspect of CSR, often known as ethical CSR, aims to prevent social harm, even if it does not yield immediate tangible benefits for the organization [12]. Over time, the legitimacy of CSR efforts not embedded within organizational strategy began to be questioned [17]. As a result, scholars turned their attention to the relationship between CSR and organizational performance [11], and eventually, to the integration of CSR initiatives into corporate strategy [10,11].

This shift was largely influenced by rising public expectations, especially following the adoption of the Sustainable Development Goals (SDGs), which have served as a major catalyst for embedding CSR into corporate strategies [12,14]. Organizations now face growing pressure from a wide range of stakeholders to deepen their CSR engagement [10,12,13]. This approach is sometimes labelled as altruistic CSR, where the primary objective is to benefit society, not necessarily the company. In contrast, strategic CSR refers to the alignment of a firm’s social responsibilities with its business objectives, creating mutual value for both the organization and its stakeholders [12]. Consequently, firms are increasingly adopting systematic, strategic approaches to integrate social and environmental outcomes with financial performance.

Research has shown that while family-owned businesses may continue to focus on philanthropy due to traditional values, multinational and progressive firms are adopting integrated frameworks that position CSR as a sustainable business strategy [78]. Strategic CSR has thus become a key component of corporate differentiation, aiding in reputation building and the establishment of enduring quality standards for various stakeholders [14]. Baron (2001) was the first to introduce the concept of "strategic CSR," describing it as a market-oriented strategy often driven by self-interest, whereby companies engage in socially beneficial activities that also support their business goals. Over the years, scholars have observed that organizations have made efforts to minimize the negative impacts of their operations, creating dual benefits for society and the environment. Nevertheless, the degree of commitment to CSR varies significantly across industries and regions [11,12,14,15]. While some firms approach CSR as a voluntary act, others genuinely prioritize societal well-being without sacrificing profitability.

Strategic CSR underscores the essential connection between business and society and its role in supporting a functional economy. As such, the strategic importance of CSR compels leaders and managers to embed CSR into their core strategic objectives, aligning them with organizational values [12]. This integration has contributed to the rise of sustainable innovations and growing emphasis on ethical business practices [11]. From a theoretical standpoint, stakeholder theory, legitimacy theory, and the resource-based view (RBV) offer foundational perspectives for shaping CSR strategies. Stakeholder theory posits that organizations must address the interests of various stakeholders to ensure alignment between corporate strategy and stakeholder expectations, thereby generating sustainable value [28,29]. Stakeholder engagement has evolved beyond superficial communication to more meaningful collaboration, prompting companies to implement socially responsible initiatives targeting critical issues such as climate change and human rights [29,30,33].

Legitimacy theory complements stakeholder theory by emphasizing the necessity for organizations to conform to societal values, norms, and expectations [31]. Companies seek to maintain legitimacy by demonstrating socially responsible behavior, especially in an era characterized by fast information flow and increased public scrutiny [29,32]. Recent studies show that firms strategically use CSR to enhance or recover legitimacy, particularly during crises or periods of reputational risk [34]. In this context, CSR is not only a moral obligation but also a pragmatic tool for sustaining societal approval and ensuring business continuity. Simultaneously, RBV offers valuable insights into how CSR can be harnessed to build a competitive advantage [35,38]. RBV suggests that sustainable competitive advantage arises from the possession and effective utilization of resources that are valuable, rare, inimitable, and non-substitutable (VRIN) [36,37]. CSR efforts that are deeply embedded in an organization’s culture and operational systems can develop into such strategic resources. For example, a strong commitment to sustainability can enhance brand equity, improve employee morale, attract loyal customers, drive innovation, and foster competitive differentiation [30]. Recent research confirms that CSR contributes to intangible assets such as corporate reputation and relational capital, both of which are essential for long-term performance and resilience [24,26,32]. Combining stakeholder theory, legitimacy theory, and RBV into CSR strategies enables organizations to proactively design CSR as a core value-creating function, rather than a reactive measure to external demands [31].

CSR originated in developed economies, initially in the United States emerging from the challenges of the Great Depression and post-World War II recovery. Due to globalization and reduced government interventions, expectations for CSR have increasingly extended to emerging economies [19,26]. However, notable differences remain between CSR practices in developed and emerging markets. In the latter, CSR is often shaped by country-level factors, including governance quality, political affiliations, legal frameworks, and levels of economic development [6,18]. Furthermore, the existence of institutional voids, underdeveloped or absent formal institutions is a defining characteristic of emerging economies [18,19]. These institutional deficiencies provide firms with context-specific justifications for adopting CSR practices under specific conditions [6,18,19,20]. For instance, during the COVID-19 pandemic, developed economies had access to strong institutional support, such as subsidies and unemployment benefits, which cushioned the economic blow. In contrast, emerging economies relied on under-resourced local institutions, which hindered business operations [21,26]. Local firms, including SMEs and family-run businesses, often received limited government support during the crisis, compounding financial challenges associated with CSR implementation [22,24]. As a result, CSR adoption in emerging markets has generally been weaker than in developed countries [21,24,31].

Nevertheless, in the context of an increasingly globalized economy, CSR is rapidly transforming from a philanthropic initiative into a strategic imperative, especially in emerging economies [19,20,22]. These regions present significant commercial opportunities, nearly 82% of the world’s population lives in emerging economies, and projections suggest that their collective GDP could surpass that of five major developed economies by 2035 [24]. Moreover, these markets are experiencing a surge in middle-class consumers with growing disposable incomes and expanding urban populations [25].

The growing emphasis on renewable energy reflects a global urgency to mitigate environmental degradation and promote sustainable economic growth. Businesses increasingly acknowledge that long-term success depends on achieving social equity and protecting the environment. Accordingly, corporate strategies and core values are transforming [27]. Despite the increasing significance of CSR, substantial gaps persist in its implementation across emerging economies, particularly in areas like deforestation, biodiversity conservation, and inclusive waste management strategies [24,25]. Notably, the literature evaluating the impact of CSR in the financial sector within these economies remains sparse and fragmented [23,24].

4. CSR Practices in the Financial Sector of Emerging Economies

Corporate Social Responsibility (CSR) has evolved into a crucial strategic necessity for organizations globally, including those operating within the financial sector [42]. In emerging economies, the financial sector is undergoing a significant transformation, wherein CSR has shifted from being a peripheral, philanthropic activity to becoming an essential element of business strategy and governance [79]. Financial institutions, particularly those in banking, insurance, fintech, and microfinance, play a pivotal role in driving economic growth and maintaining financial stability [43,47,51,72]. CSR initiatives in banks from emerging markets are undergirded by diverse theoretical frameworks that account for both the formal regulatory environment and the informal social, cultural, and religious norms that shape CSR decisions [79]. Institutional pressures include coercive forces such as statutory and regulatory requirements, along with normative and mimetic pressures that drive organizations to emulate leading CSR practices among peers and competitors [79]. These pressures are compounded in emerging markets by institutional voids and weak governance structures, prompting financial institutions to embrace CSR as a means of building trust and securing legitimacy in the eyes of stakeholders [76,79].

CSR initiatives undertaken by financial organizations often have wide-ranging impacts, contributing to poverty alleviation, environmental sustainability, financial literacy, and broader community development [39,46,72]. Consequently, CSR functions as an internal mechanism that aligns a bank’s operations with broader socio-economic, environmental, and ethical priorities, thereby reinforcing stakeholder confidence. Recent trends show a marked shift in CSR practices from traditional philanthropy to more integrated, strategic models that are closely aligned with the sustainability goals and core operations of financial institutions [37,44,45]. In emerging economies, CSR is shaped by a confluence of socio-political expectations, regulatory reforms, and prevailing cultural norms [40,48]. Moreover, stakeholders are increasingly demanding accountability and transparency, which has compelled financial institutions to demonstrate measurable and credible CSR outcomes [41,66].

Distinct CSR strategies within the financial sector, such as green banking, financial inclusion, and ethical investment, have gained traction as critical tools for achieving socio-economic and environmental sustainability [47,48,49,50]. Green banking promotes environmentally sustainable financial practices, including reduced resource consumption, sustainable lending policies, and financing of renewable energy projects [43,52,67,72]. These initiatives help financial institutions mitigate climate-related risks in their portfolios while also reinforcing environmental stewardship [53,55]. In parallel, financial inclusion strategies aim to serve historically marginalized groups, such as women, rural populations, and micro-entrepreneurs through mobile banking, agent banking, and microfinance services [72]. These practices not only improve institutional reputation but also contribute meaningfully to poverty reduction and economic empowerment, thereby advancing sustainable development goals [54,60,72]. In contexts where access to formal financial systems remains limited, such CSR efforts simultaneously expand market presence and deliver significant societal value [60,73].

Ethical investing has also emerged as a core aspect of CSR in the financial sector, particularly within emerging markets. These practices are often driven by growing scrutiny from international investors and ESG (Environmental, Social, and Governance) rating agencies [56]. Financial institutions are increasingly incorporating ESG criteria into credit assessments and investment decisions, signalling a paradigm shift from shareholder-centric to stakeholder-oriented governance models [57,60,65]. This evolution is further propelled by regulatory developments and international frameworks, such as the UN Principles for Responsible Banking, that encourage banks in developing nations to align operations with the Sustainable Development Goals (SDGs) [58,59]. Nonetheless, several challenges hinder effective implementation, including weak regulatory oversight, institutional capacity deficits, and the growing threat of greenwashing [62,63]. Overcoming these barriers requires financial institutions to embrace transparent reporting practices, engage stakeholders meaningfully, and adopt rigorous impact assessment tools. Ultimately, sector-specific CSR practices must transcend compliance to become embedded in the strategic core of financial institutions, thereby ensuring long-term legitimacy and value creation [61,64].

Recognizing this imperative, emerging economies are progressively institutionalizing CSR through robust regulatory frameworks and mandates such as ESG compliance and non-financial disclosures [68]. Regulatory reform has become a critical lever for shaping CSR practices within the financial sector, with mandatory reporting requirements and policy initiatives serving as primary drivers of CSR adoption [80]. These reforms are often catalysed by a mix of global investor influence, pursuit of the SDGs, and local governance challenges. Regulatory frameworks help elevate baseline CSR performance while fostering transparency and accountability through structured reporting systems [80]. Notably, countries like India, Brazil, and South Africa have introduced comprehensive CSR disclosure mandates, often linking them to corporate governance laws or stock exchange regulations. For instance, India’s Companies Act mandates that companies above a certain financial threshold allocate a portion of their profits to CSR and provide public disclosures, blending legal mandates with social accountability expectations [69]. Similarly, Brazil’s CVM Resolution 59 and South Africa’s King IV Report mandate integrated ESG disclosures [70]. These efforts aim to bridge governance gaps and mitigate systemic risks related to industrial growth and institutional fragility [73]. Yet, challenges such as inconsistent enforcement, limited regulatory capacity, and varying corporate maturity levels continue to undermine implementation efforts [70,71].

ESG compliance is increasingly recognized as a key determinant of corporate legitimacy and access to global capital. However, structural constraints such as fragmented regulatory systems, institutional capacity gaps, and weak enforcement mechanisms create hurdles to implementation in emerging markets [70,72,73]. Scholars also warn of the prevalence of greenwashing and symbolic CSR when firms perceive ESG mandates as externally imposed obligations rather than strategic imperatives [72,73]. Additionally, the lack of harmonized standards across jurisdictions complicates benchmarking and investor evaluations [75]. Nevertheless, emerging economies are gradually transitioning toward mandatory ESG reporting aligned with the SDGs. For instance, Nigeria’s Securities and Exchange Commission introduced ESG guidelines in 2021 to strengthen sustainability practices within capital markets [76]. These shifts indicate growing regulatory sophistication, although successful implementation depends on coherent policies, stakeholder education, and the integration of CSR into long-term corporate strategy [68,75,76]. Building ethical governance cultures and strengthening enforcement capacity remain vital for ensuring CSR delivers meaningful impact beyond reputational compliance. Despite increased regulatory pressure, the effectiveness of such mandates in delivering real sustainability outcomes remains contested. Scholars argue that while transparency has improved, actual CSR performance remains limited in the absence of robust enforcement and stakeholder engagement [77,79].

Several key drivers influence CSR adoption, including institutional pressure, stakeholder expectations, competitive differentiation, and reputational management [20,85,86]. Financial institutions increasingly view CSR as a strategic asset that can enhance brand equity, build customer trust, and unlock access to capital linked to sustainability performance [79,80]. Beyond regulatory interventions, technological innovation has further advanced transparency and CSR reporting, shaping organizational behaviour [20,88]. In emerging economies, CSR is now commonly integrated into risk management strategies, particularly in response to climate-related financial threats and the urgency of social inclusion [83,84]. Stakeholders, including investors, employees, and civil society, are demanding heightened corporate responsibility, urging financial institutions to go beyond compliance in demonstrating ethical conduct. CSR in these contexts also serves as a mechanism for aligning with the SDGs, achieving ESG benchmarks, and attracting international investment [82,83].

Nevertheless, several barriers inhibit the full institutionalization of CSR in emerging markets [18,22,62,63]. Chief among these are inconsistent regulatory enforcement and insufficient institutional capabilities, which result in symbolic or superficial CSR practices. Financial constraints and short-term performance pressures also deter firms from committing to long-term social or environmental investments. Many institutions face internal capacity issues, including limited CSR expertise and underdeveloped monitoring and evaluation systems. Cultural and institutional voids, such as low levels of stakeholder activism and weak public accountability, further hinder meaningful CSR engagement. Additionally, corruption and weak governance can distort CSR incentives, leading to insincere or greenwashed initiatives [72,73]. While CSR has transformative potential, realizing its benefits requires addressing structural, institutional, and capacity-related limitations. Low public trust in financial institutions and resistance to externally driven CSR frameworks only exacerbate implementation challenges [20]. The lack of enforcement coherence and overreliance on voluntary compliance further contribute to inconsistent outcomes across regions. As CSR discourse gains momentum, its practical application remains fragmented, underscoring the need for deeper institutional alignment and capacity-building efforts.

Regionally, CSR practices in the financial sector of emerging economies reflect unique socio-economic conditions, institutional pressures, and stakeholder demands. In Latin America, financial institutions have embraced CSR in response to socio-political instability and ecological threats [89]. For example, Brazilian banks have embedded ESG considerations into reporting systems under both domestic and international regulatory frameworks [83]. Similarly, financial institutions in Colombia and Mexico have pursued inclusive finance by supporting underserved populations through microfinance and digital banking [90,91]. These actions represent an evolving synergy between CSR and inclusive financial systems. However, institutionalization and accountability remain persistent challenges across the region.

In Sub-Saharan Africa, CSR initiatives by financial institutions are primarily shaped by development imperatives such as poverty alleviation, education, and healthcare access [6,69,70]. Banks in Nigeria, Kenya, and South Africa often adopt CSR both to meet societal needs and manage reputational risks within complex governance landscapes [76,78]. There is growing interest in sustainability reporting and stakeholder engagement, especially among institutions aiming to attract global investors. Meanwhile, in South Asia, regulatory frameworks, most notably India’s Companies Act 2013, have driven CSR integration in banking and financial services [62,69]. Indian banks have taken active roles in promoting rural development, gender equity, and environmental sustainability. Nonetheless, critics argue that CSR practices in the region tend to be compliance-oriented rather than impact-driven [92,93]. Across these regions, while CSR strategies are increasingly aligning with the SDGs and organizational priorities, disparities in implementation and transparency persist, reflecting broader structural and governance challenges.

Impact of CSR Strategies and Organizational Performance Outcomes: Context of Financial Sector of Emerging Economies

In emerging economies, characterized by institutional voids and dynamic regulatory environments, the integration of corporate social responsibility (CSR) into core business strategies within banks and financial institutions has garnered increasing scholarly interest. This attention is particularly directed toward understanding how CSR influences both financial and non-financial performance outcomes [8,68,119]. The multidimensional nature of organizational performance, encompassing profitability, sales growth, customer satisfaction, employee retention, innovation, and corporate reputation, necessitates the combination of traditional financial indicators with broader, more subjective metrics [3,4,11]. Scholars emphasize that comprehensive assessments of organizational performance should include both objective (financial) and subjective (non-financial) components. For example, integrating financial performance with indicators such as customer loyalty, product quality, employee relations, and innovation provides a more holistic view of CSR’s impact [94].

In emerging market contexts, CSR is frequently shown to bolster not only financial metrics but also enhance intangible assets such as stakeholder trust and corporate reputation [95]. Accordingly, CSR is conceptualized as a multifaceted construct encompassing economic (profit and competitiveness), legal (compliance), ethical (moral responsibilities), and philanthropic (community engagement) dimensions. In the financial services sector, additional strategic components, such as corporate governance practices and transparent disclosures, are also found to influence performance outcomes significantly [96,97,98]. Empirical studies comparing CSR practices across emerging economies reveal notable heterogeneity, influenced by macroeconomic conditions, cultural norms, and the developmental maturity of domestic financial markets [81]. For instance, research on Sub-Saharan Africa shows that South African banks typically outperform Mozambican counterparts in both the scope and quality of CSR disclosures, a pattern attributed to stronger regulatory frameworks and heightened stakeholder expectations [82]. Similarly, comparative studies across BRICS nations highlight disparities in CSR engagement and reporting practices. While India and China exhibit rigorous compliance with mandatory CSR reporting regulations, countries such as Brazil and Russia tend to adopt more voluntary, less standardized approaches [83]. Proximity to major financial centres also plays a role; banks located closer to these hubs often face greater scrutiny and are more inclined to engage in comprehensive CSR reporting [84].

Further evidence from Morocco underscores the positive relationship between CSR and both financial and non-financial outcomes, with ethical leadership acting as a moderating factor that enhances the relationship between CSR and outcomes like corporate image and customer satisfaction [47]. In Ecuador, CSR initiatives in the banking sector have been linked to increases in customer trust, loyalty, perceived quality, and satisfaction factors that, in turn, positively affect financial metrics such as return on assets (ROA) and return on equity (ROE) [103,107]. However, the relationship between CSR and performance is not universally positive. In India, for example, firms with limited financial slack may experience negative impacts from high CSR expenditures, underscoring the risks of overinvestment in CSR without sufficient financial buffers [104,116,119]. Other studies report no statistically significant relationship between CSR/ESG practices and ROE in emerging markets, highlighting the nuanced and context-dependent nature of these dynamics [105,119].

CSR strategies are increasingly recognized as instrumental in cultivating corporate reputation and stakeholder trust, which are some of the key assets in the financial services industry. Studies indicate that CSR initiatives contribute to sustainable competitive advantage by enhancing corporate reputation and deepening stakeholder relationships [108,116,118]. Evidence from Vietnam further supports this notion, revealing that various CSR dimensions (legal, economic, philanthropic, ethical, and environmental) positively affect employee commitment and organizational reputation, both of which are critical for competitive positioning [114,119]. Moreover, CSR disclosures influence investor behaviour; companies that effectively communicate ESG performance are perceived as lower-risk, more sustainable investments, thereby attracting greater capital inflows [117,120]. This not only improves financial outcomes but also reinforces market positioning [109,118].

The evaluation of CSR performance is increasingly formalized through tools such as ESG ratings, CSR indices, and sustainability reports. However, in many emerging markets, the adoption and standardization of such metrics remain underdeveloped [99,100,119]. While indices like the Dow Jones Sustainability Index (DJSI) and regional adaptations such as the Johannesburg Stock Exchange Socially Responsible Investment (JSE SRI) Index serve as proxies for CSR commitment, many financial institutions in developing regions either underreport or utilize non-standardized CSR reporting frameworks, complicating performance evaluation [22,63,119]. In countries such as India, the implementation of mandatory frameworks like SEBI’s Business Responsibility and Sustainability Reporting (BRSR) has increased the visibility and accountability of CSR in corporate disclosures [118,120]. Nonetheless, research suggests that such disclosures are often symbolic rather than substantive, particularly in politically unstable or corrupt environments [102]. Further, scholars caution that excessive CSR investment can divert resources from core operational areas, especially in economies where systems for assessing CSR’s financial impact are still maturing [121].

The temporal dimension of CSR investments is another important consideration. While CSR initiatives can yield long-term benefits, such as reputational gains and stakeholder loyalty, they may impose short-term financial constraints [119,120]. In BRICS nations, for instance, ESG activities have been found to enhance firm reputation over time, though they can concurrently increase short-term capital costs. Investors may initially view CSR disclosures as expense centres, potentially reducing immediate profitability [46,68,97]. Notably, research from China reveals that the impact of CSR on financial performance varies by strategic orientation. Organizations with a prospector strategy experience positive outcomes, whereas defender-type organizations often see a negative correlation, underscoring the critical role of aligning CSR initiatives with strategic and financial capabilities [116,118]. These findings collectively emphasize the need for financial institutions in emerging markets to calibrate their CSR strategies in alignment with their long-term vision and resource availability to balance short-term costs with enduring competitive advantage [122].

5. Discussion

The discourse around Corporate Social Responsibility (CSR) has undergone a notable transformation, increasingly shaped by multi-stakeholder expectations and global sustainability agendas such as the United Nations Sustainable Development Goals (SDGs)[12,14]. Scholars assert that the true value of CSR emerges only when it is deeply embedded in an organization's strategic direction and operational capabilities, enabling sustainable performance gains over time [107,111]. In emerging markets, the framing of CSR strategies is heavily influenced by the local institutional environment. Weak regulatory systems, gaps in enforcement mechanisms, and broader institutional voids create both challenges and opportunities for firms to tailor their CSR practices [6,18,19,20]. The COVID-19 pandemic further exposed these systemic weaknesses, revealing how limited state capacity often necessitates corporate intervention in addressing social vulnerabilities [21,26]. Despite these structural impediments, emerging economies offer compelling justifications for adopting strategic CSR approaches. With expanding urban populations, a burgeoning middle class, and increasing global integration, these regions provide fertile ground for business models that prioritize social impact. Industries such as renewable energy, waste reduction, and ecosystem conservation are particularly receptive to such efforts [25,27]. When CSR is strategically implemented, it not only addresses ethical responsibilities but also becomes a source of competitive advantage and organizational resilience [12,14,30].

In the financial sector specifically, CSR has evolved from a peripheral concern to a strategic priority. Financial institutions, including traditional banks, fintech startups, and microfinance entities, are leveraging CSR to meet sustainability mandates, address environmental and social risks, and cultivate long-term stakeholder relationships [37,44,72]. The financial-sector-specific CSR strategies, such as green banking, financial inclusion, and ethical investing, have gained notable traction [76,79]. These strategies enhance public trust and contribute to broader socio-economic progress. For instance, green banking helps institutions manage environmental risks while advancing global sustainability objectives. Similarly, financial inclusion efforts, via microloans, mobile banking, and other digital tools, have widened access to financial services for underserved communities [43,52,67]. Similarly, financial inclusion programs through microcredit, agent banking, etc, have empowered marginalized populations and expanded market reach, particularly in underserved regions [54,60,72].

Nonetheless, CSR in these markets faces persistent implementation challenges. Fragmented regulations, enforcement limitations, and capacity deficits often hinder meaningful progress [63,70]. Research indicates that in many emerging economies, CSR activities tend to be compliance-oriented rather than focused on creating a tangible impact [72,73]. There are concerns over symbolic participation and instances of greenwashing, where firms report CSR activities without delivering real social value. Mandatory reporting requirements, such as those introduced in India and Brazil, have improved CSR visibility but often fall short of achieving substantive results due to weak enforcement and superficial adoption [69,70,77].

Regional contrasts further illustrate the varied nature of CSR execution. In Latin America, financial institutions frequently adopt ESG models in response to political volatility and ecological threats [83,89]. In contrast, Sub-Saharan Africa prioritizes CSR in areas like poverty reduction and healthcare, while countries like India follow a regulation-led model that sometimes lacks meaningful outcomes [70,77,93]. These differences underscore the need to align CSR practices with local governance capacities, cultural expectations, and national development goals. Meanwhile, digital innovation is playing a growing role in enhancing CSR accountability. Tools for data transparency, impact tracking, and stakeholder communication are improving the responsiveness and legitimacy of CSR initiatives [20,88]. Yet, aligning CSR efforts with business strategy remains a complex endeavour. True transformation requires more than ticking regulatory boxes, it demands internal commitment, stakeholder-inclusive governance, and integration with long-term corporate goals [62,65].

Organizational success is no longer measured solely by financial indicators such as Return on Assets (ROA) or Return on Equity (ROE), but also by intangible factors including stakeholder trust, brand equity, and employee engagement [103,107]. CSR initiatives that align with ethical governance, transparency, and community engagement significantly contribute to positive performance indicators [77,98]. Notably, CSR outcomes differ significantly across countries, reflecting disparities in institutional maturity, cultural norms, and investor expectations. For example, South African banks are more rigorous in CSR reporting than their counterparts in Mozambique, largely due to stronger institutional pressures [82]. Similarly, Indian and Chinese banks demonstrate higher CSR compliance due to legal mandates, whereas CSR in Brazil and Russia remains largely voluntary [57,70,79]. These disparities underscore the influence of national policy and investor expectations in shaping CSR behaviour and outcomes. Ethical leadership emerges as a significant moderator in this equation, enhancing the effectiveness of CSR in building customer satisfaction and a positive corporate image, as evidenced in Moroccan banks [47].

However, the link between CSR and performance is not universally positive. In India, excessive CSR spending has, in some cases, reduced financial performance, particularly for firms with constrained resources. This suggests that CSR must be strategically proportioned to avoid overstretching financial capacities. Moreover, CSR’s impact on performance is influenced by time horizon and strategic orientation. Short-term costs may be significant, but long-term gains, such as enhanced reputation and stakeholder loyalty, can outweigh initial expenditures. Organizations that adopt proactive, innovation-driven strategies (e.g., prospector-type firms in China) tend to derive greater benefits from CSR than more conservative, risk-averse organizations [116,118]. These insights underscore the importance of embedding CSR within the broader strategic and market context of each organization. Summarizing, CSR is not a panacea, but when strategically aligned with an institution’s core competencies, stakeholder expectations, and operational realities serves as a valuable driver of both financial and non-financial success within the financial sectors of emerging markets.

6. Conclusions

The synthesis of evidence across emerging economies affirms that Corporate Social Responsibility (CSR) has transcended its philanthropic origins to become a critical lever of strategic value creation within the financial sector. When CSR is embedded within core business strategies and aligned with long-term sustainability imperatives, it facilitates mutual value generation for both firms and society. This is particularly pertinent in emerging markets, where demographic dynamism, developmental deficits, and institutional evolution demand a reimagining of CSR not merely as a moral duty but as a catalytic tool for inclusive economic transformation.

The financial sector in these economies is undergoing a paradigmatic shift in which CSR is no longer perceived as an ancillary concern but rather as an integral dimension of organizational legitimacy, resilience, and competitive strategy. This evolution is catalysed by mounting institutional pressures, escalating stakeholder expectations, and the proliferation of global sustainability frameworks. Sector-specific CSR manifestations, such as green banking, financial inclusion, and ESG-integrated investment strategies, signal meaningful progress. Yet, their efficacy remains heterogeneous due to persistent regulatory, structural, and cultural constraints. While governments and financial authorities in emerging economies have initiated regulatory mandates and reporting standards, their impact hinges on enforcement mechanisms, organizational capacity, and the depth of institutional commitment. Superficial compliance and reputational greenwashing continue to pose risks, underscoring the necessity of integrating CSR into governance structures, decision-making frameworks, and performance metrics.

Empirical findings underscore that CSR, when strategically orchestrated and contextually attuned, positively correlates with both financial and non-financial performance metrics. Quantitative analyses reveal improvements in profitability indicators such as ROA, ROE, and EPS, particularly in jurisdictions like Pakistan, where CSR integration has demonstrably enhanced firm value [106]. Simultaneously, CSR initiatives fortify intangible assets, including brand reputation, employee engagement, and customer loyalty, that constitute the bedrock of long-term financial sustainability [108]. These performance outcomes are moderated by internal variables such as resource capacity and strategic orientation, and external variables including stakeholder salience, institutional maturity, and macroeconomic volatility.

Importantly, CSR-driven strategies enhance stakeholder engagement and serve as credibility signals in environments fraught with information asymmetry and governance deficits. Effective CSR communication builds trust, mitigates reputational risk, and lowers capital costs which is an especially valuable function in volatile emerging markets [6,111,112]. Furthermore, CSR engagement reinforces ethical governance practices, augments transparency, and promotes accountability, thereby contributing to enhanced firm valuation and operational resilience [6,113].

An integrative approach to CSR, where ethical, legal, and philanthropic responsibilities are seamlessly aligned with business strategy, proves most effective. Financial institutions that embed CSR objectives into innovation, stakeholder communication, and performance management systems gain a durable strategic edge. The cultivation of “stakeholder influence capacity,” wherein internal and external stakeholders are mobilized around shared sustainability goals, further amplifies the value of CSR in volatile environments. In doing so, CSR becomes not merely a tool for compliance but a dynamic driver of innovation, efficiency, and risk mitigation.

However, the implementation of CSR is not without its challenges. The costs associated with CSR, particularly when driven by regulatory compulsion rather than intrinsic corporate values, can undercut short-term profitability [114]. Moreover, the temporal lag between CSR investments and performance payoffs necessitates strategic patience and long-term vision. This necessitates a shift from symbolic gestures to outcome-oriented models, supported by robust metrics that capture both qualitative and quantitative dimensions of impact.

Future research must bridge existing empirical and theoretical gaps through longitudinal, sector-specific, and contextually grounded studies. There remains a critical need to standardize CSR metrics, explore moderating variables such as ethical leadership and market maturity, and assess the temporal dynamics of CSR’s return on investment. In parallel, policymakers should institutionalize transparent, enforceable CSR frameworks that harmonize reporting practices and reward genuine sustainability performance.

In conclusion, the financial sectors of emerging economies stand at a critical juncture. By institutionalizing CSR as a cornerstone of strategic management, these economies can foster inclusive growth, ethical resilience, and long-term financial stability. CSR, when strategically aligned and operationalized with integrity, has the transformative potential to redefine not only firm-level competitiveness but also the developmental trajectories of entire financial ecosystems. The imperative now is to ensure that CSR is not an episodic add-on but a systemic, measurable, and mission-critical function within financial institutions committed to equitable and sustainable development.

7. Future Scope of Research

Future research on the nexus between corporate social responsibility (CSR) and organizational performance could address several critical and underexplored dimensions to enrich both theoretical development and practical application. Longitudinal studies are particularly essential to elucidate the temporal dynamics and causal relationships inherent in CSR-performance linkages. These studies could reveal whether CSR initiatives translate into enduring organizational value or produce only transient gains. Furthermore, disaggregating CSR into its constituent dimensions, economic, legal, ethical, philanthropic, and governance, also offers a promising analytical avenue. Such granularity will enable scholars to assess the differential impacts of each CSR component on financial and non-financial outcomes across various sub-sectors of the financial industry, thereby identifying the most potent levers for strategic value creation.

Additionally, the role of contextual moderators, such as firm size, ownership structure, industry maturity, and cultural and institutional factors, demands greater empirical scrutiny. Given the heterogeneity of emerging economies, these variables may significantly shape how CSR strategies are formulated, implemented, and ultimately perceived by stakeholders. Exploring these moderating influences is essential for developing a more contingent and context-sensitive understanding of CSR's efficacy. In parallel, the rapid evolution of digital technologies and the increasing integration of advanced analytics, AI-driven stakeholder engagement, and real-time CSR disclosures present a transformative opportunity. These innovations are not merely operational tools, but they redefine transparency, accountability, and stakeholder interaction in ways that can fundamentally alter the perceived legitimacy and strategic value of CSR. Investigating how digital platforms and integrated reporting frameworks influence stakeholder trust, reputational capital, and financial performance constitutes a timely and impactful research direction.

By addressing these gaps, future scholarship can advance a more nuanced, dynamic, and empirically grounded understanding of CSR as a strategic asset. This will not only inform more effective CSR design and implementation but also guide policymakers and practitioners in leveraging CSR to enhance both firm competitiveness and societal well-being in the complex, interconnected landscape of emerging markets.

References

- Abdullah, H. Corporate social responsibility and firm performance from developing markets: The role of audit committee expertise. Sustain. Futur. 2024, 8. [Google Scholar] [CrossRef]

- Cezarino, L.O.; Liboni, L.B.; Hunter, T.; Pacheco, L.M.; Martins, F.P. Corporate social responsibility in emerging markets: Opportunities and challenges for sustainability integration. J. Clean. Prod. 2022, 362. [Google Scholar] [CrossRef]

- Bhattacharyya, A.; Wright, S.; Rahman, L. Is better banking performance associated with financial inclusion and mandated CSR expenditure in a developing country? Account. Finance 2019, 61, 125–161. [Google Scholar] [CrossRef]

- Vishwanathan, P.; van Oosterhout, H. (.; Heugens, P.P.M.A.R.; Duran, P.; van Essen, M. Strategic CSR: A Concept Building Meta-Analysis. J. Manag. Stud. 2019, 57, 314–350. [Google Scholar] [CrossRef]

- Al-Mamun, A.; Seamer, M. Board of director attributes and CSR engagement in emerging economy firms: Evidence from across Asia. Emerg. Mark. Rev. 2021, 46. [Google Scholar] [CrossRef]

- Boubakri, Narjess, Sadok El Ghoul, Omrane Guedhami, and He Helen Wang. "Corporate social responsibility in emerging market economies: Determinants, consequences, and future research directions." Emerging Markets Review 46 (2021): 100758.

- Kashi, A.; Shah, M.E. Bibliometric Review on Sustainable Finance. Sustainability 2023, 15, 7119. [Google Scholar] [CrossRef]

- Sindhu, M.I.; Windijarto; Wong, W. -K.; Maswadi, L. Implications of corporate social responsibility on the financial and non-financial performance of the banking sector: A moderated and mediated mechanism. Heliyon 2024, 10, e30557. [Google Scholar] [CrossRef]

- Campbell, J.L. 2017 Decade Award Invited Article Reflections on the 2017 Decade Award: Corporate Social Responsibility and the Financial Crisis. Acad. Manag. Rev. 2018, 43, 546–556. [Google Scholar] [CrossRef]

- Afrin, Samina. "Traditional vs strategic corporate social responsibility: In pursuit of supporting sustainable development." Journal of Economics and Sustainable Development 4, no. 20 (2013): 1-6.

- Ślęzak, M. From Traditional to Strategic CSR: Systematic Literature Review. J. Corp. Responsib. Leadersh. 2020, 7, 39–53. [Google Scholar] [CrossRef]

- McCall, Andrei. "The Strategic Use of Corporate Social Responsibility (CSR) for Competitive Advantage and Stakeholder Engagement." (2024).

- Kalagond, Gouri. "Compliance to CSR Mandate: Heading Which Way?." Gouri Kalagond (2022).

- Abugre, J.B.; Anlesinya, A. Corporate social responsibility strategy and economic business value of multinational companies in emerging economies: The mediating role of corporate reputation. Bus. Strat. Dev. 2019, 3, 4–15. [Google Scholar] [CrossRef]

- Marques, Ana Cristina, and Padmini Srinivasan. "Corporate social responsibility involvement: Determinants and consequences in a mandatory setting." IIM Bangalore Research Paper 565 (2019).

- Baron, David P. "Private politics, corporate social responsibility, and integrated strategy." Journal of economics & management strategy 10, no. 1 (2001): 7-45.

- Ahen, F.; Zettinig, P. Critical perspectives on strategic CSR: what is sustainable value co-creation orientation? Crit. Perspect. Int. Bus. 2015, 11, 92–109. [Google Scholar] [CrossRef]

- Alizadeh, A. The Drivers and Barriers of Corporate Social Responsibility: A Comparison of the MENA Region and Western Countries. Sustainability 2022, 14, 909. [Google Scholar] [CrossRef]

- Doh, Jonathan P., Benjamin Littell, and Narda R. Quigley. "CSR and sustainability in emerging markets: Societal, institutional, and organizational influences." Organizational Dynamics 44, no. 2 (2015): 112-120.

- Gulema, T.F.; Roba, Y.T. Internal and external determinants of corporate social responsibility practices in multinational enterprise subsidiaries in developing countries: evidence from Ethiopia. Futur. Bus. J. 2021, 7, 1–19. [Google Scholar] [CrossRef]

- Lu, J.; Khan, S. Are sustainable firms more profitable during COVID-19? Recent global evidence of firms in developed and emerging economies. Asian Rev. Account. 2022, 31, 57–85. [Google Scholar] [CrossRef]

- Mahmood, A.; Naveed, R.T.; Ahmad, N.; Scholz, M.; Khalique, M.; Adnan, M. Unleashing the Barriers to CSR Implementation in the SME Sector of a Developing Economy: A Thematic Analysis Approach. Sustainability 2021, 13, 12710. [Google Scholar] [CrossRef]

- Zhang, K.; Hao, X. Corporate social responsibility as the pathway towards sustainability: a state-of-the-art review in Asia economics. Discov. Sustain. 2024, 5, 1–17. [Google Scholar] [CrossRef]

- Herndon, Dale, and Richard Baskerville. "Building Reputation in Emerging Markets through Corporate Social Responsibility." In Proceedings of the Eleventh International Conference on Engaged Management Scholarship-EMS. 2021.

- Cavusgil, S.T. Advancing knowledge on emerging markets: Past and future research in perspective. Int. Bus. Rev. 2021, 30. [Google Scholar] [CrossRef]

- Al Frijat, Yaser Saleh, and Ahmed A. Elamer. "Human capital efficiency, corporate sustainability, and performance: Evidence from emerging economies." Corporate Social Responsibility and Environmental Management 32, no. 2 (2025): 1457-1472.

- Nosratabadi, Saeed, Amir Mosavi, Shahaboddin Shamshirband, Edmundas Kazimieras Zavadskas, Andry Rakotonirainy, and Kwok Wing Chau. "Sustainable business models: A review." Sustainability 11, no. 6 (2019): 1663.

- Freudenreich, Brigitte, Florian Lüdeke-Freund, and Stefan Schaltegger. Sustainability-oriented Business Model Assessment: A Conceptual Foundation. Journal of Cleaner Production 2020, 267, 122051.

- Waheed, A.; Zhang, Q. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. J. Bus. Ethic- 2020, 175, 837–855. [Google Scholar] [CrossRef]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social Capital, Trust, and Firm Performance: The Value of Corporate Social Responsibility during the Financial Crisis. J. Finance 2017, 72, 1785–1824. [Google Scholar] [CrossRef]

- Velte, P. Meta-analyses on Corporate Social Responsibility (CSR): a literature review. Manag. Rev. Q. 2021, 72, 627–675. [Google Scholar] [CrossRef]

- Tiep Le, Thanh, Huan Quang Ngo, and Leonardo Aureliano-Silva. "Contribution of corporate social responsibility on SMEs' performance in an emerging market–the mediating roles of brand trust and brand loyalty." International Journal of Emerging Markets 18, no. 8 (2023): 1868-1891.

- Tauringana, V. Sustainability reporting challenges in developing countries: towards management perceptions research evidence-based practices. J. Account. Emerg. Econ. 2020, 11, 194–215. [Google Scholar] [CrossRef]

- Truong, T.H.D. Environmental, social and governance performance and firm value: does ownership concentration matter?. Manag. Decis. 2024, ahead-of-p. [CrossRef]

- Freeman, R.E.; Dmytriyev, S.D.; Phillips, R.A. Stakeholder Theory and the Resource-Based View of the Firm. J. Manag. 2021, 47, 1757–1770. [Google Scholar] [CrossRef]

- Barney, J.B. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Hoepner, A.G.; Li, Q. A stakeholder resource-based view of corporate social irresponsibility: Evidence from China. J. Bus. Res. 2022, 144, 830–843. [Google Scholar] [CrossRef]

- Chen, S.; Ji, Y. Do Corporate Social Responsibility Categories Distinctly Influence Innovation? A Resource-Based Theory Perspective. Sustainability 2022, 14, 3154. [Google Scholar] [CrossRef]

- Jahid, A.; Yaya, R.; Pratolo, S.; Pribadi, F. Institutional factors and CSR reporting in a developing country: Evidence from the neo-institutional perspective. Cogent Bus. Manag. 2023, 10. [Google Scholar] [CrossRef]

- Ebaid, I.E.-S. Corporate governance mechanisms and corporate social responsibility disclosure: evidence from an emerging market. J. Glob. Responsib. 2022, 13, 396–420. [Google Scholar] [CrossRef]

- Shabir, M.; Ping, J.; Işik, Ö.; Razzaq, K. Impact of corporate social responsibility on bank performance in emerging markets. Int. J. Emerg. Mark. 2024, ahead-of-p. [CrossRef]

- Pan, X.; Oh, K.-S.; Wang, M. Strategic Orientation, Digital Capabilities, and New Product Development in Emerging Market Firms: The Moderating Role of Corporate Social Responsibility. Sustainability 2021, 13, 12703. [Google Scholar] [CrossRef]

- Bedendo, M.; Nocera, G.; Siming, L. Greening the Financial Sector: Evidence from Bank Green Bonds. J. Bus. Ethic- 2022, 188, 259–279. [Google Scholar] [CrossRef]

- Hieu, V.M.; Hai, N.T. The role of environmental, social, and governance responsibilities and economic development on achieving the SDGs: evidence from BRICS countries. Econ. Res. Istraz. 2022, 36, 1338–1360. [Google Scholar] [CrossRef]

- Hasan, E.; Ahmed, A.; Akhi, R.A. The Exogenous Shock of COVID-19: An Evidence from Financial Sector of an Emerging Economy. Bus. Manag. Horizons 2021, 9, 27. [Google Scholar] [CrossRef]

- van Hierden, Y.T.; Dietrich, T.; Rundle-Thiele, S. A citizen-centred approach to CSR in banking. Int. J. Bank Mark. 2021, 39, 638–660. [Google Scholar] [CrossRef]

- Abdallah-Ou-Moussa, S.; Wynn, M.; Kharbouch, O.; Rouaine, Z. Digitalization and Corporate Social Responsibility: A Case Study of the Moroccan Auto Insurance Sector. Adm. Sci. 2024, 14, 282. [Google Scholar] [CrossRef]

- Katenova, M.; Qudrat-Ullah, H. Corporate social responsibility and firm performance: Case of Kazakhstan. Heliyon 2024, 10, e31580. [Google Scholar] [CrossRef]

- Kabir, M.A.; Chowdhury, S.S. Empirical analysis of the corporate social responsibility and financial performance causal nexus: Evidence from the banking sector of Bangladesh. Asia Pac. Manag. Rev. 2022, 28, 1–12. [Google Scholar] [CrossRef]

- Barone, M.; Bussoli, C.; Conte, D.; Fattobene, L.; Morrone, D. Perceptions of CSR initiatives as a strategic driver in strengthening relationships among banks and Italian consumers: an empirical approach in the Italian banking context. Int. J. Bank Mark. 2024, 43, 685–709. [Google Scholar] [CrossRef]

- Brammer, S.; Nardella, G.; Surdu, I. Defining and deterring corporate social irresponsibility: embracing the institutional complexity of international business. Multinatl. Bus. Rev. 2021, 29, 301–320. [Google Scholar] [CrossRef]

- Chikazhe, Lovemore, Farirayi Jecha, Brighton Nyagadza, Thomas Bhebhe, and Josphat Manyeruke. "Mediators of the effect of corporate social responsibility on product uptake: insights from the insurance sector in Harare, Zimbabwe." International Journal of Business and Emerging Markets 14, no. 4 (2022): 435-453.

- Ongena, S. Which banks for green growth? A review and a tentative research agenda. J. Sustain. Finance Account. 2024, 1. [Google Scholar] [CrossRef]

- Burki, M.A.K.; Burki, U.; Najam, U. Environmental degradation and poverty: A bibliometric review. Reg. Sustain. 2021, 2, 324–336. [Google Scholar] [CrossRef]

- Asare, Joseph. "The Role of Financial Institutions in Climate-Conscious Investments and Risk Preclusion in Africa Based on Five Core Sustainable Growth and Development Variables." Available at SSRN 5035726.

- Kholjigitov, Golib. "Sustainable Finance and Investments: Principles, Tools, and Effectiveness Assessment." Tools, and Effectiveness Assessment (August 15, 2023) (2023).

- Sadiq, M.; Nonthapot, S.; Mohamad, S.; Keong, O.C.; Ehsanullah, S.; Iqbal, N. Does green finance matter for sustainable entrepreneurship and environmental corporate social responsibility during COVID-19? China Finance Rev. Int. 2021, 12, 317–333. [Google Scholar] [CrossRef]

- Martin, Patrick, Zeinab Elbeltagy, Zenathan Adnin Hasannudin, and Masato Abe. "Factors affecting the environmental and social risk management of financial institutions in selected Asia-Pacific developing countries." (2021).

- Raisa, Khadija Khan. "Navigating Sustainable Finance in Bangladesh: The Role of Banks and Financial Institutions." (2024).

- Attah-Botchwey, Edward, Michael Gift Soku, and David Mensah Awadzıe. Sustainability reporting and the financial performance of banks in Africa. Journal of Business Economics and Finance 2022, 11, 43–57.

- Botchwey, E.A.; Soku, M.G.; Awadzie, D.M. SUSTAINABILITY REPORTING AND THE FINANCIAL PERFORMANCE OF BANKS IN AFRICA. Pressacademia 2022. [Google Scholar] [CrossRef]

- Dixit, S.K.; Priya, S.S. Barriers to corporate social responsibility: an Indian SME perspective. Int. J. Emerg. Mark. 2021, 18, 2438–2454. [Google Scholar] [CrossRef]

- Milhem, Marwan, Ali Ateeq, Ranyia Ali Ateeq, Dalili Izni Shafie, T. Santhanamery, and Ahmad Al Astal. "Bridging Worlds: Envisioning a Sustainable Future Through CSR in Developing Countries." In Business Sustainability with Artificial Intelligence (AI): Challenges and Opportunities: Volume 2, pp. 285-293. Cham: Springer Nature Switzerland, 2024.

- Wu, W.; Ji, Z.; Liu, J. Impact of green financing on CSR and environmental policies and procedures. Heliyon 2024, 10, e31101. [Google Scholar] [CrossRef] [PubMed]

- Qian, W.; Tilt, C.; Belal, A. Social and environmental accounting in developing countries: contextual challenges and insights. Accounting, Audit. Account. J. 2021, 34, 1021–1050. [Google Scholar] [CrossRef]

- Kuzey, C.; Uyar, A.; Nizaeva, M.; Karaman, A.S. CSR performance and firm performance in the tourism, healthcare, and financial sectors: Do metrics and CSR committees matter? J. Clean. Prod. 2021, 319. [Google Scholar] [CrossRef]

- Hariadi, Melia, and Kyle Bruce. "Contending Logics and CSR Practices in Mnes in Emerging Economies: Evidence from Indonesia." Available at SSRN 5169750.

- Baah, Charles, Yaw Agyabeng-Mensah, Ebenezer Afum, and Minenhle Siphesihle Mncwango. "Do green legitimacy and regulatory stakeholder demands stimulate corporate social and environmental responsibilities, environmental and financial performance? Evidence from an emerging economy." Management of Environmental Quality: An International Journal 32, no. 4 (2021): 787-803.

- Maqbool, Shafat, Nayan Mitra, and Asiya Chaudhury. "Corporate social responsibility reporting in the post-mandate period: an in-depth content analysis of indian top-listed companies." In Emerging Economic Models for Sustainable Businesses: A Practical Approach, pp. 9-24. Singapore: Springer Nature Singapore, 2022.

- Hieu, V.M.; Hai, N.T. The role of environmental, social, and governance responsibilities and economic development on achieving the SDGs: evidence from BRICS countries. Econ. Res. Istraz. 2022, 36, 1338–1360. [Google Scholar] [CrossRef]

- Arun, Thankom, Claudia Girardone, and Stefano Piserà. "ESG issues in emerging markets and the role of banks." In Handbook of banking and finance in emerging markets, pp. 321-344. Edward Elgar Publishing, 2022.

- Van Caenegem, Arnaud. "Regulating Sustainability Communications in the Financial Services Sector: The Sustainable Finance Disclosure Regulation." A. Van Caenegem and T. van de Werve," Regulating Sustainability Communications in the Financial Services Sector: The Sustainable Finance Disclosure Regulation" in V. Colaert (ed.), Sustainable Finance in Europe and Belgium (Anthemis, 2021) (2021).

- Sorour, M.K.; Shrives, P.J.; El-Sakhawy, A.A.; Soobaroyen, T. Exploring the evolving motives underlying corporate social responsibility (CSR) disclosures in developing countries: the case of “political CSR” reporting. Accounting, Audit. Account. J. 2020, 34, 1051–1079. [Google Scholar] [CrossRef]

- AlAjmi, J.; Buallay, A.; Saudagaran, S. Corporate social responsibility disclosure and banks' performance: the role of economic performance and institutional quality. Int. J. Soc. Econ. 2022, 50, 359–376. [Google Scholar] [CrossRef]

- Rojas Molina, Leidy Katerine, José Ángel Pérez López, and María Soledad Campos Lucena. "Meta-analysis: associated factors for the adoption and disclosure of CSR practices in the banking sector." Management Review Quarterly 73, no. 3 (2023): 1017-1044.

- Ozili, Peterson K. "Effect of climate change on financial institutions and the financial system." In Uncertainty and challenges in contemporary economic behaviour, pp. 139-144. Emerald Publishing Limited, 2020.

- Forliano, C.; Battisti, E.; de Bernardi, P.; Kliestik, T. Mapping the greenwashing research landscape: a theoretical and field analysis. Rev. Manag. Sci. 2025, 1–50. [Google Scholar] [CrossRef]

- Abdelhalim, K.; Eldin, A.G. Can CSR help achieve sustainable development? Applying a new assessment model to CSR cases from Egypt. Int. J. Sociol. Soc. Policy 2019, 39, 773–795. [Google Scholar] [CrossRef]

- Aracil, Elisa. "Corporate social responsibility of Islamic and conventional banks: The influence of institutions in emerging countries." International Journal of Emerging Markets 14, no. 4 (2019): 582-600.

- Arun, Thankom, Claudia Girardone, and Stefano Piserà. "ESG issues in emerging markets and the role of banks." In Handbook of banking and finance in emerging markets, pp. 321-344. Edward Elgar Publishing, 2022.

- Platonova, E.; Asutay, M.; Dixon, R.; Mohammad, S. The Impact of Corporate Social Responsibility Disclosure on Financial Performance: Evidence from the GCC Islamic Banking Sector. J. Bus. Ethics 2018, 151, 451–471. [Google Scholar] [CrossRef]

- Siueia, T.T.; Wang, J.; Deladem, T.G. Corporate Social Responsibility and financial performance: A comparative study in the Sub-Saharan Africa banking sector. J. Clean. Prod. 2019, 226, 658–668. [Google Scholar] [CrossRef]

- Szegedi, K.; Khan, Y.; Lentner, C. Corporate Social Responsibility and Financial Performance: Evidence from Pakistani Listed Banks. Sustainability 2020, 12, 4080. [Google Scholar] [CrossRef]

- Zamir, F.; Saeed, A. Location matters: Impact of geographical proximity to financial centers on corporate social responsibility (CSR) disclosure in emerging economies. Asia Pac. J. Manag. 2018, 37, 263–295. [Google Scholar] [CrossRef]

- Li, T.; Trinh, V.Q.; Elnahass, M. Drivers of Global Banking Stability in Times of Crisis: The Role of Corporate Social Responsibility. Br. J. Manag. 2022, 34, 595–622. [Google Scholar] [CrossRef]

- Alizadeh, A. The Drivers and Barriers of Corporate Social Responsibility: A Comparison of the MENA Region and Western Countries. Sustainability 2022, 14, 909. [Google Scholar] [CrossRef]

- The Manager’s Vision of CSR in an Emerging Economy: From Implementation to Market Impact.

- Slimi, Houmem. "Enhancing Sustainable Performance in Financial Institutions: The Impact of Customerfocus, Internal Processes, Learning &Amp; Growth, Moderated by Management Commitment." Internal Processes, Learning &Amp.

- Prior, F.; Argandoña, A. Credit accessibility and corporate social responsibility in financial institutions: the case of microfinance. Bus. Ethic- A Eur. Rev. 2009, 18, 349–363. [Google Scholar] [CrossRef]

- Logsdon, Jeanne M., Douglas E. Thomas, and Harry J. Van Buren. "Corporate social responsibility in large Mexican firms." In Corporate Citizenship in Latin America: New Challenges for Business, pp. 51-60. Routledge, 2022.

- Mesta-Cabrejos, V.F.; Huertas-Vilca, K.S.; Wong-Aitken, H.G.; Cordova-Buiza, F. Corporate social responsibility in the banking sector: a focus on Latin America and the Caribbean. Humanit. Soc. Sci. Commun. 2023, 10, 1–6. [Google Scholar] [CrossRef]

- Usman, Berto, Ridwan Nurazi, Intan Zoraya, and Nurna Aziza. "CSR Performance and Profitability of the Banking Industry in Southeast Asia Nations (ASEAN)." Capital Markets Review 31, no. 2 (2023): 55-68.

- Tran, M.; Beddewela, E.; Ntim, C.G. Governance and sustainability in Southeast Asia. Account. Res. J. 2021, 34, 516–545. [Google Scholar] [CrossRef]

- Al-Samman, E.; Al-Nashmi, M.M. Effect of corporate social responsibility on nonfinancial organizational performance: evidence from Yemeni for-profit public and private enterprises. Soc. Responsib. J. 2016, 12, 247–262. [Google Scholar] [CrossRef]

- Bhuiyan, F.; Baird, K.; Munir, R. The association between organisational culture, CSR practices and organisational performance in an emerging economy. Meditari Account. Res. 2020, 28, 977–1011. [Google Scholar] [CrossRef]

- Platonova, E.; Asutay, M.; Dixon, R.; Mohammad, S. The Impact of Corporate Social Responsibility Disclosure on Financial Performance: Evidence from the GCC Islamic Banking Sector. J. Bus. Ethics 2018, 151, 451–471. [Google Scholar] [CrossRef]

- Balon, V.; Kottala, S.Y.; Reddy, K. Mandatory corporate social responsibility and firm performance in emerging economies: An institution-based view. Sustain. Technol. Entrep. 2022, 1. [Google Scholar] [CrossRef]

- Shanyu, L. Corporate social responsibilities (CSR) and sustainable business performance: evidence from BRICS countries. Econ. Res. Istraz. 2022, 35, 6105–6120. [Google Scholar] [CrossRef]

- Singhania, M.; Saini, N. Institutional framework of ESG disclosures: comparative analysis of developed and developing countries. J. Sustain. Finance Invest. 2021, 13, 516–559. [Google Scholar] [CrossRef]

- Tarczynska-Luniewska, Malgorzata, Saule Maciukaite-Zviniene, Ninditya Nareswari, and Udisubakti Ciptomulyono. "Analysing the Complexity of ESG Integration in Emerging Economies: An Examination of Key Challenges." In Exploring ESG Challenges and Opportunities: Navigating Towards a Better Future, vol. 116, pp. 41-60. Emerald Publishing Limited, 2024.

- Mathebula, Andzani George. "An analysis of the relationship between corporate carbon disclosure and financial performance: a study of companies listed in the FTSE/JSE responsible investing index." PhD diss., 2023.

- Solomons, Ruth. "Assessing the business case for environmental, social and corporate governance practices in South Africa." PhD diss., Stellenbosch: Stellenbosch University, 2018.

- Taneja, Pawan, Ameeta Jain, Mahesh Joshi, and Monika Kansal. "Mandatory corporate social responsibility in India: reporting reality, issues and way forward." Meditari Accountancy Research 30, no. 3 (2022): 472-494.

- Retamal Ferrada, Lorena, Melita Vega, Jaime Alberto Orozco-Toro, and Caroline Ávila. "The sdgs in sustainability reports among companies in ecuador, colombia, and chile." Contratexto 40 (2023): 117-147.

- Prakash, N.; Hawaldar, A. Moderating role of firm characteristics on the relationship between corporate social responsibility and financial performance: evidence from India. J. Econ. Dev. 2024, 26, 346–361. [Google Scholar] [CrossRef]

- Singhal, N.; Paul, P.; Giri, S.; Taneja, S. Corporate Social Responsibility: Impact on Firm Performance for an Emerging Economy. J. Risk Financial Manag. 2024, 17, 171. [Google Scholar] [CrossRef]

- Maqbool, S.; Zameer, M.N. Corporate social responsibility and financial performance: An empirical analysis of Indian banks. Futur. Bus. J. 2018, 4, 84–93. [Google Scholar] [CrossRef]

- Tulcanaza-Prieto, A.B.; Shin, H.; Lee, Y.; Lee, C.W. Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment. Sustainability 2020, 12, 1621. [Google Scholar] [CrossRef]

- Salam, M.A.; Abu Jahed, M. CSR orientation for competitive advantage in business-to-business markets of emerging economies: the mediating role of trust and corporate reputation. J. Bus. Ind. Mark. 2023, 38, 2277–2293. [Google Scholar] [CrossRef]

- Roque, Ana Filipa Marques. "ESG in the Sustainability Report and the Impact on Investors' Choices: A Literature Review." (2024).

- Al-Samman, E.; Al-Nashmi, M.M. Effect of corporate social responsibility on nonfinancial organizational performance: evidence from Yemeni for-profit public and private enterprises. Soc. Responsib. J. 2016, 12, 247–262. [Google Scholar] [CrossRef]

- Saeed, M.M.; Mudliar, M.; Kumari, M. Corporate social responsibility and financial performance nexus: Empirical evidence from Ghana. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 2799–2815. [Google Scholar] [CrossRef]

- Guang-Wen, Z.; Siddik, A.B. Do Corporate Social Responsibility Practices and Green Finance Dimensions Determine Environmental Performance? An Empirical Study on Bangladeshi Banking Institutions. Front. Environ. Sci. 2022, 10. [Google Scholar] [CrossRef]

- Sekhon, A.K.; Kathuria, L.M. Analyzing the impact of corporate social responsibility on corporate financial performance: evidence from top Indian firms. Corp. Governance: Int. J. Bus. Soc. 2019, 20, 143–157. [Google Scholar] [CrossRef]

- Mai, Ngoc Khuong, Khoa Truong An Nguyen, Thanh Tung Do, and Long Nhat Phan. "Corporate Social Responsibility Strategy Practices, Employee Commitment, Reputation as Sources of Competitive Advantage." SAGE Open 13, no. 4 (2023): 21582440231216248.

- Deng, B.; Ji, L.; Liu, Z. The Effect of Strategic Corporate Social Responsibility on Financial Performance: Evidence from China. Emerg. Mark. Finance Trade 2021, 58, 1726–1739. [Google Scholar] [CrossRef]

- Hui, Z.; Li, H.; Elamer, A.A. Financing sustainability: How environmental disclosures shape bank lending decisions in emerging markets. Corp. Soc. Responsib. Environ. Manag. 2024, 31, 3940–3967. [Google Scholar] [CrossRef]

- Benlemlih, M.; Jaballah, J.; Peillex, J. Does it really pay to do better? Exploring the financial effects of changes in CSR ratings. Appl. Econ. 2018, 50, 5464–5482. [Google Scholar] [CrossRef]

- Tripathi, V.; Kaur, A. Does Socially Responsible Investing Pay in Developing Countries? A Comparative Study Across Select Developed and Developing Markets. FIIB Bus. Rev. 2021, 11, 189–205. [Google Scholar] [CrossRef]