Submitted:

04 April 2025

Posted:

04 April 2025

You are already at the latest version

Abstract

This study examines the impact of ESG (Environmental, Social, and Governance) management activities on organizational trust and commitment among employees in large manufacturing enterprises. Additionally, it investigates the moderating effect of job position on the relationship between ESG management activities and organizational performance. The key findings from the empirical analysis are as follows: First, all three ESG factors—environmental (E), social (S), and governance (G)—had a positive effect on organizational trust. Second, the environmental and governance factors had a positive effect on organizational commitment. However, the social factor exhibited a negative effect on organizational commitment. Third, the environmental factor showed a negative effect on organizational performance. In contrast, the social and governance factors had a positive effect on organizational performance. Fourth, organizational trust was found to enhance organizational commitment significantly, confirming that employees who trust their organization are more likely to be committed to it. Fifth, a strong sense of trust in the organization was shown to contribute positively to organizational performance and competitiveness. Sixth, organizational commitment positively impacted organizational performance, reinforcing the idea that highly committed employees contribute to better outcomes. Seventh, the study confirmed that job position moderated the relationship between ESG management activities and organizational performance, indicating that employees at different hierarchical levels perceive ESG management's impact differently. This study expands the research scope of ESG management beyond marketing, HR, and service industries to focus on employees in large manufacturing enterprises. This provides new insights into how ESG initiatives influence internal organizational dynamics. From a practical standpoint, the findings highlight the necessity of strategic initiatives to ensure employees fully understand and engage with ESG-related policies. To successfully implement ESG management, organizations must develop effective communication and integration strategies that foster employees' recognition of ESG initiatives.

Keywords:

ESG management activity

; organizational trust

; organizational commitment

; organizational performance

; moderating effect

1. Introduction

As ESG (Environmental, Social, and Governance) management becomes essential to corporate strategy, governments worldwide are actively implementing policies to support its adoption. In the European Union (EU), the Net Zero Industry Act was recently enacted to help European industries achieve carbon neutrality by 2050 while enhancing global competitiveness. Meanwhile, in the United States, the Securities and Exchange Commission (SEC) introduced a mandatory climate-related disclosure rule in March 2024, requiring publicly traded companies to report climate risks and greenhouse gas emissions. The regulation will be gradually enforced starting in 2026, depending on company size. Similarly, other countries—including the United Kingdom, Australia, Japan, Singapore, and China—are expected to introduce mandatory ESG disclosure requirements [1].

South Korea is also moving toward institutionalizing ESG disclosure based on corporate scale while integrating ESG principles into business practices and corporate culture [2]. Despite these regulatory advancements, South Korean firms have faced criticism for treating ESG management primarily as a risk-mitigation tool rather than embracing it as a fundamental policy transformation. However, as ESG principles become more deeply embedded, businesses are experiencing growing pressure from stakeholders and society to improve their ESG performance and proactively tackle sustainability challenges [3].

To successfully implement ESG initiatives, developing a clear understanding of how ESG activities influence business performance is essential. Numerous studies have highlighted a positive correlation between ESG engagement and corporate performance [4,5]. However, in South Korea, research on ESG management has mainly been qualitative, relying on literature reviews rather than empirical analysis [6,7,8]. ESG management signifies a fundamental shift in corporate values and business perspectives, shaping strategic decisions, corporate culture, and operational principles [9].

As values-based management is crucial for sustainable business practices, ESG management should also be deeply embedded in corporate strategies and core values [10]. While awareness of this necessity is increasing, empirical research remains insufficient [11]. In South Korea, existing studies have primarily focused on the relationship between ESG management and financial performance [12]. In contrast, research on non-financial performance has mainly been confined to marketing, human resources, and service industries [13,14]. However, South Korea is widely recognized as a manufacturing-driven economy, with the sector contributing 28% of the country’s GDP—a significantly higher share than Japan’s 20.5%. Given South Korea’s export-oriented industrial structure and dependence on a few major conglomerates, the future of the manufacturing sector is critical to the nation’s economic stability. Therefore, it is essential for manufacturing firms and their employees to develop a comprehensive understanding of ESG management and actively participate in its implementation to drive meaningful and sustainable outcomes.

This study aims to bridge the gap in ESG research by focusing on manufacturing conglomerates, rather than the marketing, HR, and service industries, which have traditionally dominated ESG-related studies. Specifically, it examines the impact of ESG management activities on organizational trust, commitment, and performance from the perspective of internal stakeholders—corporate employees. Additionally, it explores the moderating effect of job positions on these relationships. By analyzing these key dynamics, this study seeks to uncover the psychological mechanisms through which ESG management influences organizational trust and commitment within manufacturing enterprises. The findings will offer practical implications for corporate governance, providing strategic insights to help manufacturing executives and ESG management teams develop more effective ESG strategies. Furthermore, this study aims to foster a more positive perception of ESG management among employees in the manufacturing sector, ultimately enhancing ESG adoption and effectiveness within the industry.

2. Theoretical Background

2.1. ESG Management

ESG management is derived from the initials of Environmental (E), Social (S), and Governance (G) and refers to a management strategy that is formulated and implemented based on these three core pillars. ESG represents the evolution, normalization, and institutionalization of Corporate Sustainability Management (CSM) and Corporate Social Responsibility (CSR) [15]. It embodies fundamental values directly linked to a company’s long-term survival and growth [10].

Unlike traditional CSR and Creating Shared Value (CSV), ESG management takes a more strategic approach to addressing environmental, social, and governance challenges [16]. Today, many companies recognize the significance of long-term sustainability, which entails positively impacting the environment and society [17]. Additionally, sustainability has emerged as a critical factor in securing competitive advantage, leading to the rapid adoption of ESG practices in corporate management [18].

As societal expectations for corporate responsibility continue to rise, ESG has become a key priority in business management. One of the crucial lessons learned from the COVID-19 pandemic is that companies cannot thrive—or even survive—without aligning with societal progress. Consequently, businesses have been actively engaging in initiatives such as CSR and CSV to foster stronger ties between corporations and society.

At the same time, pressing issues like climate change and environmental pollution have become global concerns that transcend individual nations and corporations. With environmental regulations becoming increasingly stringent and public awareness of sustainability growing, companies now recognize that an eco-friendly corporate image is directly tied to business performance. As a result, many organizations are prioritizing environmental responsibility and actively participating in sustainability initiatives.

Furthermore, employees within companies must also develop a strong awareness of environmental issues and actively engage in sustainability efforts. As ESG continues to shape the future of business, fostering a corporate culture that values environmental and social responsibility will be essential for long-term success.

2.2. Organizational Trust

Trust is generally defined as the expectation that another party’s future actions will be favorable or, at the very least, not harmful [19]. It is also a mutual belief that individuals will act ethically in their interactions with others [20]. According to Chung & Lee (2014) [21], organizational trust refers to employees' expectation that the intentions and actions of their organization will align with common sense and general expectations. Similarly, Tan & Tan (2000) define organizational trust as employees' overall assessment of the organization’s reliability, emphasizing their confidence that the organization will act in ways that benefit them or, at the very least, do not cause harm [22].

Trust plays a crucial psychological and social role in interactions, facilitating cooperation and serving as a fundamental element of social capital and exchange relationships [19]. Establishing trust is essential for fostering employees' voluntary and active cooperation within an organization. Furthermore, organizational trust is a key factor in maintaining a competitive advantage, as it enhances confidence in others' words and actions while promoting goodwill. Organizational trust is typically categorized into institutional, supervisor, and coworker trust [23].

2.3. Organizational Commitment

The concept of organizational commitment was first introduced by March & Simon (1958) [24], who defined it as "the motivation to go beyond assigned tasks and actively engage in additional responsibilities." Becker (1960) [25], emphasizing the behavioral aspect of commitment, described it as "a consistent pattern of attachment to an organization, driven by the rewards gained from staying and the costs associated with leaving."

Prior research suggests that employees with higher organizational commitment tend to perform better than those with lower commitment [26]. Angel & Perry (1981) highlighted its role as a key determinant of organizational performance, defining commitment as an employee’s attachment to their organization [27]. Similarly, Allen & Meyer (1990) described it as an attitude that reflects employees' acceptance of organizational goals and values and their loyalty to the organization [28]. Further expanding this idea, Meyer & Herscovitch (2001) defined organizational commitment as a psychological state that drives employees to engage in organizational behaviors [29].

Empirical research by Li, Zhu, & Park (2018) examined Leader-Member Exchange (LMX), sales performance, job satisfaction, organizational commitment, and turnover intention among 228 sales employees [30]. Their findings revealed that job satisfaction and organizational commitment had a significant positive correlation with sales performance, while turnover intention negatively correlated with both variables. Additionally, domestic research suggests that high organizational commitment among employees positively influences customer service orientation, highlighting its importance in business success [31].

2.4. Organizational Performance

Organizational performance refers to the outcomes an organization achieves through its operations and strategies. It is influenced by multiple factors, including organizational goals, strategy, culture, leadership, and structure, making it a multifaceted and context-dependent concept [32]. When studying public sector organizations, organizational performance measurement varies depending on the research objectives and can be defined through different performance indicators. Quinn & McGrath (1985) identified organizational culture as a key factor influencing performance and introduced the Competing Values Model as an analytical framework [33].

Previous studies have classified organizational performance into financial and non-financial performance indicators. Financial performance includes revenue growth and market share, while non-financial performance encompasses customer and employee satisfaction, market responsiveness, and quality improvements [34].

Furthermore, research has demonstrated that ESG (Environmental, Social, and Governance) management performance positively affects financial performance, with its impact increasing over time [35]. Additionally, ESG performance is associated with positive business social outcomes [36].

Empirical studies on ESG management have also confirmed its positive impact on business performance. For instance, Lu et al. (2023) analyzed the ESG activities of 79 publicly listed apparel manufacturing companies and 80 service-related firms, revealing that ESG initiatives significantly positively impact corporate performance [37]. Similarly, Barrymore & Sampson (2021) conducted a large-scale analysis of 13,313 U.S. firms from 2008 to 2018, examining the relationship between ESG practices and productivity. Their study found that ESG initiatives had a statistically significant positive effect on average labor productivity, further reinforcing the importance of ESG management in modern corporate strategy.

3. Research Model and Hypothesis

3.1. Research Model

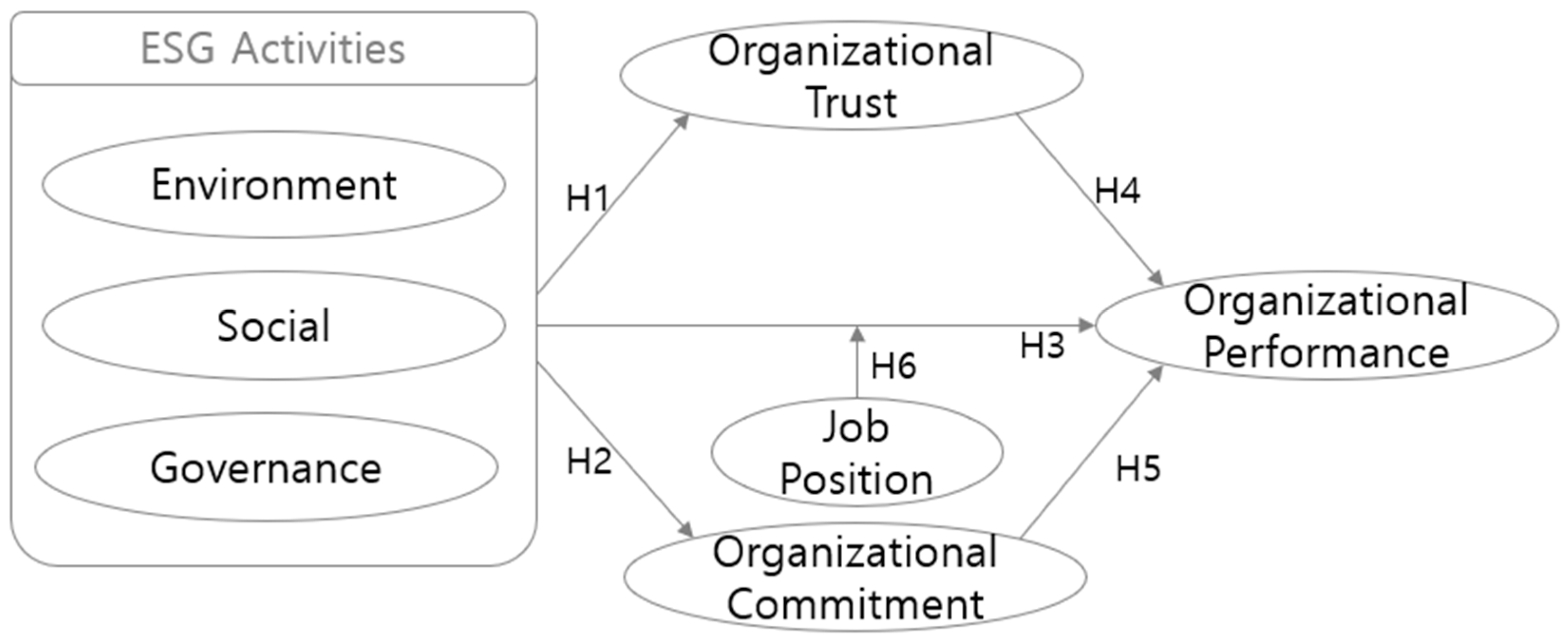

This study examines the impact of ESG management activities in large manufacturing enterprises on organizational trust, commitment, and performance based on prior research and theoretical background. Additionally, it seeks to verify the moderating effect of hierarchical position in the relationship between ESG management activities and organizational performance. The research model designed to achieve these objectives is illustrated in <Figure 1>.

3.2. Hypothesis

3.2.1. ESG Management Activities and Organizational Trust

According to organizational identity theory, strengthening corporate social responsibility (CSR) initiatives fosters a positive perception of the organization among its employees [39]. CSR activities enhance employees' perception of their organization, increasing their level of support and trust, a concept that extends to ESG management practices.

Research analyzing the relationship between corporate environmental responsibility and performance has shown that environmental management strategies significantly influence goodwill-based trust. In contrast, environmental risk management strategies impact professional and goodwill-based trust [40]. Furthermore, a study on small and medium-sized enterprises (SMEs) found that ESG activities positively affect intrapreneurship and trust, enhancing organizational effectiveness [41].

Building upon these prior studies, this research hypothesizes that ESG management activities in large manufacturing enterprises positively influence organizational trust:

Hypothesis 1.

ESG management activities in large manufacturing enterprises will significantly impact employees’ organizational trust.

Hypothesis 1-1.

Environmental (E) activities will significantly impact employees’ organizational trust.

Hypothesis 1-2.

Social (S) activities will significantly impact employees’ organizational trust.

Hypothesis 1-3.

Governance (G) activities will significantly impact employees’ organizational trust.

3.2.2. ESG Management Activities and Organizational Commitment

Previous studies examining the relationship between ESG management activities and organizational commitment indicate that environmental, social, and governance initiatives significantly influence employees' commitment within various industries, including food service companies [42]. Choi and Kim (2017) found that organizational commitment is shaped by individual characteristics, job environment, and corporate culture, improving management performance while reducing turnover and absenteeism [43]. Similarly, Ha and Lee (2017) noted that higher organizational commitment enhances customer service orientation [31]. Koller et al. (2019) suggested that ESG awareness strengthens employees’ motivation and organizational commitment by promoting sustainable goal-setting, ultimately boosting productivity [44]. Additionally, Kim and Lee (2020) [45] reported that integrating corporate social responsibility (CSR) into business operations enhances employees' organizational commitment.

Based on these findings, it is reasonable to assume a positive relationship between ESG management activities and organizational commitment, leading to the following hypothesis:

Hypothesis 2.

ESG management activities in large manufacturing enterprises will significantly impact employees’ organizational commitment.

Hypothesis 2-1.

Environmental (E) activities will significantly impact employees’ organizational commitment.

Hypothesis 2-2.

Social (S) activities will significantly impact employees’ organizational commitment.

Hypothesis 2-3.

Governance (G) activities will significantly impact employees’ organizational commitment.

3.2.3. ESG Management Activities and Organizational Performance

Prior research on ESG management activities and organizational performance suggests that when employees fully understand and support a company’s ESG strategies and vision, ESG management activities lead to better organizational performance [46]. Park and Han (2021) analyzed the impact of ESG management on consumer responses and corporate image formation, finding that ESG initiatives contribute to creating a warm and competent corporate image, positively influencing business performance [47]. Eliwa et al. (2021) also argue that ESG management activities yield positive business outcomes [36].

Synthesizing these findings, a positive relationship between ESG management activities and organizational performance can be inferred. Thus, this study proposes the following hypothesis:

Hypothesis 3.

ESG management activities in large manufacturing enterprises will significantly impact organizational performance.

Hypothesis 3-1.

Environmental (E) activities will significantly impact organizational performance.

Hypothesis 3-2.

Social (S) activities will significantly impact organizational performance.

Hypothesis 3-3.

Governance (G) activities will significantly impact organizational performance.

3.2.4. Organizational Trust and Organizational Performance

Research has consistently highlighted the significance of organizational trust in various contexts. Among corporate sustainability efforts, organizational trust directly influences the achievement of business goals [48]. Additionally, a study by Chae and Choi (2021) examining the impact of organizational trust on security performance in court security personnel found a significant positive relationship between trust and performance [49]. Similarly, Bong and Lee (2017) investigated hotel chefs and found that employees with high levels of trust in their organizations demonstrated higher job performance [50].

Furthermore, research on ESG management activities in the food service industry suggested that ESG initiatives positively impact job satisfaction and organizational commitment, ultimately improving performance [42]. While prior studies show variations in results, they collectively suggest that organizational trust significantly influences organizational performance.

Thus, this study presents the following hypothesis:

Hypothesis 4.

Organizational trust will significantly impact organizational performance.

3.2.5. Organizational Commitment and Organizational Performance

Previous studies have examined the relationship between organizational commitment and performance. Wagner and Rush (2000) found that trust in supervisors positively impacts organizational commitment, with subordinates' trust in their leaders significantly influencing workplace behavior and, ultimately, organizational performance [51]. Fu and Deshpande (2014) demonstrated that organizational commitment significantly impacts performance among employees in large insurance corporations [52]. Seo (2016) argued that higher organizational commitment reduces turnover rates and enhances performance by fostering proactive work attitudes [53]. Kwon (2017) also found that organizational commitment positively influences service innovation performance, emphasizing the need for strategies to enhance employee commitment [54].

Based on these findings, the following hypothesis is proposed:

Hypothesis 5.

Organizational commitment will significantly impact organizational performance.

3.2.6. Moderating Effect of Job Position Difference

A moderating effect occurs when a third variable influences the relationship between an independent variable and a dependent variable. In a corporate setting, an employee’s job position reflects their role and level of responsibility within the organization. Higher- position employees typically have greater decision-making authority and access to company resources, which can enhance their ability to drive innovation within the organization.

According to Lee & Eom (2013) [55], employees in higher positions tend to possess greater interpersonal and individual competencies. Their study suggests that managers and executives have stronger business capabilities compared to entry-level employees. Additionally, the scope of tasks, responsibilities, and authority varies across different job positions [56]. As a result, the nature of work experiences differs depending on one’s position, which in turn may impact work performance [57,58].

Building on these previous studies, this research aims to examine whether job position moderates the relationship between ESG management activities (independent variable) and organizational performance (dependent variable) in large manufacturing firms. Accordingly, the following hypotheses are proposed:

Hypothesis 6.

Job position will moderate the relationship between ESG management activities and organizational performance in large manufacturing firms.

H6-1.

Job position will moderate the relationship between environmental (E) activities and organizational performance in large manufacturing firms.

H6-2.

Job position will moderate the relationship between social (S) activities and organizational performance in large manufacturing firms.

H6-3.

Job position will moderate the relationship between governance (G) activities and organizational performance in large manufacturing firms.

3.3. Operational Definition of Variables

3.3.1. ESG Management Activities

ESG (Environmental, Social, and Governance) management activities go beyond corporate social responsibility (CSR) and shared value creation (CSV) to serve as a strategic approach for addressing environmental, social, and governance-related challenges [16]. In this study, ESG management activities are defined as the process of establishing and implementing management strategies based on the three key ESG pillars: environmental (E), social (S), and governance (G) [15].

To develop the survey questionnaire, previous studies by Park et al. (2021) [16], Piao et al. (2022) [59], and Daugaard (2020) [60] were referenced. The questionnaire consists of three sub-dimensions of ESG activities—environmental (E), social (S), and governance (G). A total of 12 items were adapted and refined for the study, including statements such as "Our company strives to develop eco-friendly products and services." Responses were measured using a five-point Likert scale.

3.3.2. Organizational Trust

Previous studies have defined organizational trust as employees' willingness to rely on and follow their organization, even in uncertain situations [61]. Based on these prior findings, this study defines organizational trust as "employees’ expectation that the organization's intentions and actions will align with common sense and general expectations" [2].

The survey items were adapted from studies by Jun(2023)[62] and Jung et al. (2022) [11], which employed job satisfaction scales. The questionnaire consists of five items: "Our company’s products and services are trustworthy." Responses were measured using a five-point Likert scale.

3.3.3. Organizational Commitment

High levels of organizational commitment offer numerous advantages to organizations [63]. Organizations provide employees with financial and psychological support and opportunities for professional development. In turn, employees foster close bonds with their organization, leading to greater engagement and commitment, ultimately contributing to improved performance.

Organizational commitment refers to employees’ belief in organizational goals and values, their desire to remain with the organization, and their loyalty toward it [64,65]. This study defines organizational commitment as "the strong willingness to remain a part of the organization, the motivation to work diligently for its aspirations, and the readiness to embrace its values and goals" [66].

The survey items were adapted from studies by Kang (2022)[67] and Kang(2023) [68], which utilized job satisfaction scales. The questionnaire consists of four items: "I feel a sense of belonging and ownership in my current organization." Responses were measured using a five-point Likert scale.

3.3.4. Organizational Performance

In the past, corporate performance was assessed separately regarding financial, customer, and organizational performance. However, recent studies increasingly integrate financial and non-financial performance into a comprehensive measure of organizational performance [69].

This study defines organizational performance as "the tangible outcomes of corporate management activities, focusing on non-financial results". Six key indicators of non-financial performance were selected based on respondents’ perceptions: product/service awareness, brand recognition, corporate reputation, product/service reliability, potential customer acquisition, and product/service repurchase rates.

The survey items were adapted from Kaplan & Norton (1992) [70] and Kim (2023) [71]. The questionnaire includes six items: "Our company’s brand recognition (image) is improving." Responses were measured using a five-point Likert scale.

3.4. Data Collection and Research Methods

The sample data for this study was collected through a survey targeting employees from three large manufacturing corporations—Company L, Company H, and another Company H—that have actively implemented ESG initiatives. The survey was conducted from October 10 to October 20, 2024. A total of 600 questionnaires (200 per company) were distributed, and 587 responses were collected. However, after excluding 26 responses due to uniform answers or insincere responses unsuitable for analysis, a final sample of 561 valid responses was used for empirical analysis. For data analysis, SPSS 29.0 was used for frequency and factor analyses, while AMOS 29.0 was employed to test the research model and hypotheses.

4. Empirical Analysis Results

4.1. Sample Characteristics

An analysis of the gender distribution among the 561 survey respondents reveals that males account for a majority, with 359 individuals (64.0%), while females make up 202 (36.0%). In terms of age groups, 90 respondents (16.0%) are in their 20s, 82 (14.6%) in their 30s, 164 (29.2%) in their 40s, 176 (31.4%) in their 50s, and 49 (8.7%) are aged 50 and above. Regarding educational background, 118 respondents (21.0%) have a high school diploma, 380 (67.7%) hold a bachelor’s degree, and 63 (11.2%) have completed graduate-level education or higher. This indicates a high level of educational attainment, reflecting the prevalence of highly educated individuals in large corporations. In terms of job positions, 133 respondents (23.7%) are entry-level employees, 168 (29.9%) hold assistant manager positions, 112 (20.0%) are managers, 72 (12.8%) are senior managers, and 76 (13.59%) hold director-level positions or higher.

When asked about their departments, 154 respondents (27.5%) work in sales and marketing, 148 (26.4%) in production and operations, 84 (15.0%) in other fields, 50 (8.9%) in research and development, 40 (7.11%) in planning and management, 61 (10.9%) in finance and accounting, and 24 (4.3%) in human resources. Regarding work experience, 109 respondents (19.4%) have less than five years of experience, 158 (28.2%) have between five and ten years, 79 (14.1%) have between ten and fifteen years, and 215 (38.3%) have over fifteen years of experience. These findings suggest a preference for employment in large manufacturing corporations, where working conditions tend to be more favorable than in small and medium-sized enterprises. The summarized results are presented in <Table 1>.

4.2. Reliability and Validity Testing

In this study, confirmatory factor analysis (CFA) was conducted to test the reliability and validity of the variables used. The reliability of measurement items was assessed using Cronbach’s alpha (α), calculated using SPSS 29.0, with a threshold of 0.6 or higher, indicating high internal consistency and reliability among the items. As shown in <Table 2>, the reliability analysis of the measurement tool revealed that all constructs—Environmental (E), Social (S), Governance (G), Organizational Trust, Organizational Commitment, and Organizational Performance—achieved Cronbach’s alpha values above 0.8, demonstrating a satisfactory level of reliability.

The goodness-of-fit indices for the measurement model were as follows: χ² = 340.596 (df = 89, p < .001), χ²/df = 3.827, GFI = 0.931 (≥ 0.8), IFI = 0.962 (≥ 0.9), TLI = 0.949 (≥ 0.9), CFI = 0.962 (≥ 0.9), and RMR = 0.036 (≤ 0.05). These values indicate that the model meets the required fit criteria. Convergent validity was assessed based on standardized factor loadings of 0.5 or higher, composite reliability (C.R.) of at least 0.7, and an average variance extracted (AVE) of 0.5 or higher, as recommended by Fornell and Larcker (1981) [72]. As presented in <Table 2>, all measurement items in this study met these thresholds, confirming convergent validity.

Discriminant validity was evaluated by comparing the square root of the AVE for each construct with the correlation coefficients between constructs [72]. As shown in <Table 3>, the square root of each construct’s AVE exceeded the correlation coefficients between constructs, confirming that discriminant validity was achieved.

4.3. Hypothesis Testing

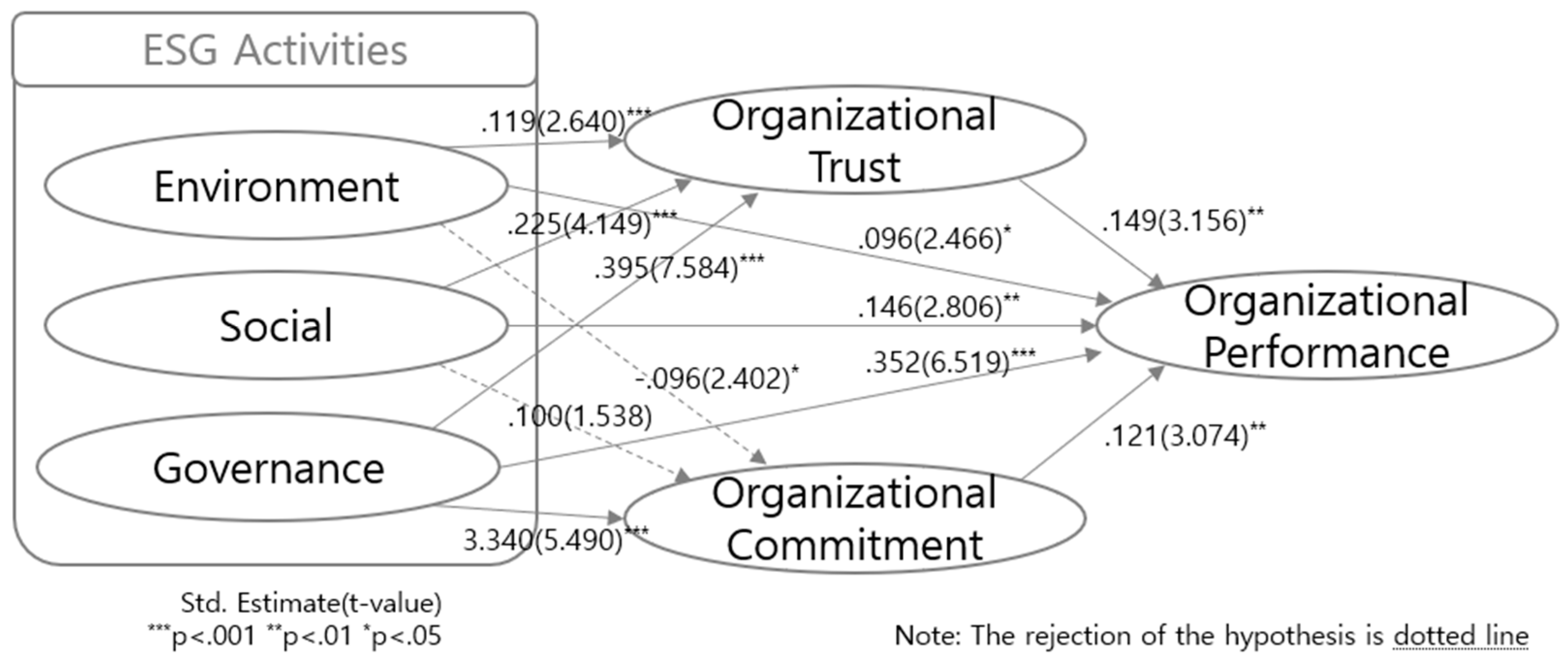

His study employed structural equation modeling (SEM) path analysis to examine the impact of ESG management activities on organizational trust, commitment, and performance. Additionally, it investigated the effect of organizational trust on organizational commitment and analyzed the moderating effect of employees' job positions. The measurement model’s reliability and validity were confirmed, providing a solid foundation for testing the structural model. The results of the structural model fit analysis indicated χ² = 280.700 (df = 90, p < .001), χ²/df = 3.119, meeting the recommended significance level (p > 0.05). Moreover, the fit indices—NFI = 0.961, RFI = 0.948, IFI = 0.973, TLI = 0.964, CFI = 0.973, and RMSEA = 0.062—suggest that the model demonstrates an overall good fit. The results of hypothesis testing using structural equation modeling are summarized in <Table 4> and <Figure 2>.

First, Hypothesis 1 examined the impact of ESG activities in large manufacturing corporations on organizational trust. The analysis revealed that the environmental (E) factor (standardized coefficient = 0.119, t = 2.840, p < 0.05), social (S) factor (standardized coefficient = 0.225, t = 4.149, p < 0.001), and governance (G) factor (standardized coefficient = 0.395, t = 7.584, p < 0.001) all had statistically significant positive effects on organizational trust. Consequently, Hypotheses 1-1, 1-2, and 1-3 were all supported.

These findings indicate that while the impact of corporate ESG activities on organizational trust can be mixed, employees’ perceptions of ESG initiatives in large manufacturing firms generally contribute positively to building organizational trust. This aligns with previous studies [40,73]. Additionally, the results suggest that the hierarchical culture and collectivist organizational dynamics still prevalent in large manufacturing corporations may influence employees' trust formation, reflecting the enduring top-down management style in Korean corporate culture.

Figure 4.

Results of hypothesis testing.

| Hypotheses: path | Std. Estimate |

S.E. | t-value | p-value | Results | |||

|---|---|---|---|---|---|---|---|---|

| H1-1: | Environment | → | Organizational trust |

.119 | 0.040 | 2.640** | 0.005 | Accepted |

| H1-2: | Social | → | .225 | 0.057 | 4.149*** | *** | Accepted | |

| H1-3: | Governance | → | .395 | 0.066 | 7.584*** | *** | Accepted | |

| H2-1: | Environment | → | Organizational Commitment |

-0.096 | 0.041 | -2.402* | 0.016 | Accepted |

| H2-2: | Social | → | 0.100 | 0.056 | 1.538 | 0.124 | Rejected | |

| H2-3: | Governance | → | 0.340 | 0.066 | 5.490*** | *** | Accepted | |

| H3-1: | Environment | → | Organizational Performance |

0.096 | 0.037 | 2.466* | 0.014 | Accepted |

| H3-2: | Social | → | 0.146 | 0.053 | 2.806** | 0.005 | Accepted | |

| H3-3: | Governance | → | 0.352 | 0.066 | 6.519*** | *** | Accepted | |

| H4: | Organizational trust | → | Organizational Performance |

0.149 | 0.053 | 3.156** | 0.002 | Accepted |

| H5: | Organizational Commitment | → | 0.121 | 0.045 | 3.074*** | 0.002 | Accepted | |

Note: χ²=280.700, df=90, p=0.000, NFI=0.961, RFI=0.948, IFI=0.973, TLI=0.964, CFI=0.973, RMSEA=0.062, ***p<0.001, **p<0.01, *p<0.05.

Hypothesis 2 examined the impact of corporate ESG management activities on organizational commitment. The analysis revealed that the environmental (E) factor (standardized coefficient = –0.096, t = –2.402, p < 0.05) had a statistically significant negative effect, while the social (S) factor (standardized coefficient = 0.100, t = 1.538, p = 0.124) was not statistically significant.

According to previous studies, corporate managers pursuing ESG or CSR initiatives often face increased non-productive expenditures, which can negatively affect corporate performance and value [74,75]. Additionally, it has been suggested that corporate environmental (E) activities can have a negative impact on firm value (Tobin’s Q), as they may lead to short-term cost increases and reduced profitability, ultimately affecting firm value negatively [76]. From this perspective, the adoption of ESG initiatives may impose additional financial burdens on companies, potentially leading to internal resistance. This aligns with previous findings that suggest such resistance can negatively impact organizational commitment [13,15,77]). Consequently, Hypotheses 2-1 and 2-2 were rejected.

However, the governance (G) factor (standardized coefficient = 0.327, t = 4.567, p < 0.001) demonstrated a statistically significant positive effect. This result supports the notion that governance (G) activities positively influence customer trust [78]. Effective governance enhances transparency in decision-making and implementation, increases internal autonomy and efficiency, and fosters higher organizational commitment among employees [79]. Furthermore, a transparent and well-structured governance system has been found to enhance investor confidence, leading to better capital market evaluations [71]. Therefore, Hypothesis 2-3 was supported.

Hypothesis 3 investigated the impact of ESG management activities in large manufacturing corporations on organizational performance. The analysis results indicated that the environmental (E) factor (standardized coefficient = 0.096, t = 2.466, p = 0.014), social (S) factor (standardized coefficient = 0.146, t = 2.806, p < 0.01), and governance (G) factor (standardized coefficient = 0.352, t = 6.519, p < 0.001) all had statistically significant positive effects.

According to previous studies, all three ESG components—environmental (E), social (S), and governance (G)—positively influence business performance [80,81,82]. Additionally, research by Mohammad, W.M.W. and Wasiuzzaman (2021) [83] and Nisar et al. (2021) [84] confirms that ESG initiatives positively affect corporate financial performance and have a significant impact on overall business success. The findings of this study reaffirm these previous research conclusions. As a result, Hypotheses 3-1, 3-2, and 3-3 were all supported.

Hypothesis 4 examined the impact of organizational trust on organizational performance. The analysis results indicated a standardized coefficient of 0.149 (t = 3.156, p < 0.01), demonstrating a statistically significant positive effect. These findings confirm that trust within an organization serves as a key driver of both corporate competitiveness and organizational performance. Furthermore, organizational trust acts as a positive factor in the relationship between business strategy and performance outcomes. Consequently, Hypothesis 4 was supported.

Hypothesis 5 assessed the relationship between organizational commitment and organizational performance. The analysis showed a standardized coefficient of 0.121 (t = 3.74, p < 0.01), confirming statistical significance and leading to the acceptance of Hypothesis 5. This result aligns with previous studies, which suggest that when employees' commitment to their colleagues, supervisors, and the organization itself is supported by a strong organizational system, it enhances overall job performance [85]. Additionally, it reaffirms prior research indicating that organizational commitment plays a crucial role in performance outcomes by fostering the internalization of organizational goals, values, and mission [86].

To examine the moderating effect of job position on the relationship between ESG management activities and organizational performance in large manufacturing corporations, this study conducted a multi-group analysis. Multi-group analysis allows for a comparison of path coefficients across different groups to determine whether the relationships in the model vary significantly between them. The chi-square difference test using AMOS revealed that, among employees in non-managerial positions (below manager level), the environmental (E) factor (t = 72.071, p < 0.05) and governance (G) factor (t = 7.985, p < 0.001) had a statistically significant positive impact on organizational performance. This indicates that job position moderates the effect of ESG activities on performance.

Similarly, the analysis of managerial-level employees (manager and above) showed that the social (S) factor (t = 3.291, p < 0.001) had a statistically significant impact on organizational performance, suggesting that job position plays a moderating role in this relationship.

The chi-square difference test using AMOS was conducted to examine the moderating effect of job position on the relationship between ESG activities and organizational performance. The comparison between the unconstrained model and the constrained model showed a chi-square difference of ⊿χ²(1) = 8.284, with χ² = 8.284, p = 0.040 (unconstrained model: χ² = 545.912, constrained model: χ² = 554.196; 554.196 - 545.912 = 8.284). Since this value exceeds the critical threshold of 7.81, the results indicate that job position significantly moderates the relationship between ESG activities and organizational performance. Consequently, Hypothesis 6 was supported.

Table 5.

Moderating effect testing.

| Hypotheses: path | Lower Job Position Group(n=301) | High Job Position Group(n=260) |

|||||||

|---|---|---|---|---|---|---|---|---|---|

| Estimate | t-value | p-value | Estimate | t-value | p-value | ||||

| H6-1: | Environment | → | Organizational Performance |

0.105 | 2.071* | 0.038 | 0.067 | 1.650 | 0.099 |

| H6-2: | Social | → | 0.094 | 1.366 | 0.172 | 0.265 | 3.291*** | 0.000 | |

| H6-3: | Governance | → | 0.555 | 7.985*** | 0.000 | 0.176 | 1.530 | 0.126 | |

***p<0.001, **p<0.01, *p<0.05.

Table 6.

Comparison of model.

| Model | DF | CMIN | P | NFI | IFI | RFI | TLI |

|---|---|---|---|---|---|---|---|

| Delta-1 | Delta-2 | rho-1 | rho2 | ||||

| Constrained Model | 3 | 8.284 | .040* | .001 | .001 | .000 | .000 |

*p<0.05.

5. Conclusion and Discussion

This study examines the impact of ESG (Environmental, Social, and Governance) management activities in large manufacturing corporations on organizational trust, organizational commitment, and organizational performance. Additionally, it seeks to verify the moderating effect of job position on the relationship between ESG management activities and organizational performance. While numerous previous studies have focused on external stakeholders' reactions to corporate ESG activities and their influence on employees' attitudes and behaviors, this study is significant in analyzing the perceptions of employees within large manufacturing corporations—internal stakeholders—regarding ESG management.

The key findings of this study are summarized as follows: First, hypothesis 1 analyzed the impact of ESG activities on organizational trust. The results revealed that all three ESG factors had a statistically significant positive impact on organizational trust: Environmental (E) factor (standardized coefficient = 0.119, t = 2.840, p < 0.05), Social (S) factor (standardized coefficient = 0.225, t = 4.149, p < 0.001), and Governance (G) factor (standardized coefficient = 0.395, t = 7.584, p < 0.001). Thus, hypotheses 1-1, 1-2, and 1-3 were all supported. While prior research has presented mixed findings on the impact of ESG activities on organizational trust, this study confirms that a higher awareness of ESG activities among employees in large manufacturing firms positively influences the formation of organizational trust [40,73]. However, this outcome may also reflect the influence of hierarchical corporate culture still prevalent in large manufacturing firms in South Korea, emphasizing top-down directives. Therefore, it is necessary to foster a corporate culture that supports mutual growth between the company and its employees.

Second, hypothesis 2 examined the impact of ESG management activities on organizational commitment. The Environmental (E) factor (standardized coefficient = –0.096, t = –2.402, p < 0.05) showed a statistically significant negative impact, while the Social (S) factor (standardized coefficient = 0.100, t = 1.538, p = 0.124) was not statistically significant. Consequently, hypotheses 2-1 and 2-2 were rejected. These findings align with previous research, which suggests that implementing ESG management in corporations may introduce additional cost burdens, leading to internal resistance and negatively affecting organizational commitment [13,71,77]). From this perspective, corporate executives and ESG management teams should focus on developing ESG strategies that emphasize economic value creation through Environmental (E) and Social (S) activities [79[]. Additionally, regular education programs on the implementation and necessity of ESG initiatives should be conducted to encourage voluntary participation and enhance job satisfaction, thereby increasing organizational commitment. On the other hand, the Governance (G) factor (standardized coefficient = 0.327, t = 4.567, p < 0.001) demonstrated a significant positive effect, supporting hypothesis 2-3. This suggests that governance activities enhance customer trust[78] and improve corporate decision-making transparency, autonomy, and efficiency, positively impacting employees' commitment [71]. Thus, companies should further strengthen their governance practices to build employee trust.

Third, hypothesis 3 investigated the impact of ESG management activities on organizational performance. The analysis revealed that all three ESG factors had statistically significant positive effects on organizational performance: Environmental (E) factor (standardized coefficient = 0.096, t = 2.466, p = 0.014), Social (S) factor (standardized coefficient = 0.146, t = 2.806, p < 0.01), and Governance (G) factor (standardized coefficient = 0.352, t = 6.519, p < 0.001). Thus, hypotheses 3-1, 3-2, and 3-3 were supported. These findings are consistent with prior studies that highlight the positive impact of ESG activities on corporate performance [80,81,82]. As a result, large manufacturing firms should actively promote ESG initiatives to establish a responsible corporate image regarding environmental, social, and governance aspects, thereby earning trust from internal stakeholders, including employees.

Fourth, hypothesis 4 examined the impact of organizational trust on organizational performance. The results (standardized coefficient = 0.149, t = 3.156, p < 0.01) confirmed that organizational trust positively influences corporate competitiveness and performance, reinforcing that trust within an organization is a key factor in linking business strategy and performance.

Fifth, hypothesis 5 explored the relationship between organizational commitment and organizational performance. The analysis (standardized coefficient = 0.121, t = 3.74, p < 0.01) demonstrated a statistically significant positive effect, supporting hypothesis 5. These results reaffirm prior findings that employee commitment—whether toward supervisors, colleagues, or the organization—affects organizational support systems and, consequently, business performance [85]. Furthermore, organizational commitment was shown to play a crucial role in achieving corporate goals, values, and missions, significantly influencing organizational outcomes [86].

Finally, hypothesis 6 investigated the moderating effect of job position on the relationship between ESG management activities and organizational performance using a chi-square difference test in AMOS. The results showed that the difference between the unconstrained and constrained models was ⊿χ²(1) = 7.928, p = 0.048 (unconstrained model χ² = 931.326, constrained model χ² = 939.254; 939.254 – 931.326 = 7.928), exceeding the critical value of 7.81. This indicates a significant moderating effect of job position, supporting hypothesis 6.

5.1. Theoretical and Practical Implications

This study categorizes the ESG (Environmental, Social, and Governance) management activities of large manufacturing enterprises into three distinct components—environmental (E) activities, social (S) activities, and governance (G) activities—and analyzes their impact on internal stakeholders, specifically organizational members. Based on the findings, the implications of this study are as follows:

First, while previous empirical studies on ESG management activities have primarily focused on marketing, human resources (HR), and the service industry [13,14]), this study expands the research domain by applying ESG management research to large manufacturing enterprises. This contributes to the academic field by broadening the scope of ESG-related research.

Second, while many studies have examined the effects of ESG activities on external stakeholders such as consumers and shareholders, this study focuses on internal stakeholders—organizational members—and analyzes the impact of ESG management activities on them. This perspective is particularly significant in the field of organizational behavior.

Third, through an empirical analysis of ESG management activities from the perspective of internal stakeholders, this study confirms that these activities positively influence organizational members. This finding underscores the importance of ESG engagement as a key factor in shaping employees’ perceptions and behaviors within the organization.

Fourth, this study reveals that ESG management activities positively influence employees' trust and commitment to the organization. By demonstrating this relationship, the research highlights that ESG initiatives benefit external corporate reputation and play a crucial role in strengthening internal organizational cohesion.

From a practical perspective, the study offers the following managerial implications:

First, the findings provide valuable insights for large manufacturing enterprises in shaping their future ESG management strategies. The empirical results suggest that the benefits of enhanced organizational trust, driven by ESG initiatives, may outweigh the associated costs. As such, companies should strive to design ESG programs that foster employee trust, maximizing organizational performance.

Second, as corporate interest in ESG management grows, ESG activities are increasingly recognized as essential business strategies. For large manufacturing enterprises facing challenges in recruiting specialized talent, it is particularly important to implement strategies that enhance employee engagement in ESG initiatives. Encouraging participation in ESG-related programs can help foster a sense of purpose and belonging among employees, ultimately leading to higher retention and satisfaction.

Third, the study finds that organizational commitment among employees significantly influences overall organizational performance. Therefore, companies must ensure that their workforce is well-informed about ESG management activities and that employees feel a sense of pride in their organization. This underscores the need for a comprehensive, company-wide communication strategy that promotes awareness and engagement in ESG initiatives.

In conclusion, this study provides theoretical and practical insights into the role of ESG management activities in shaping employee perceptions and organizational outcomes. By acknowledging the internal impact of ESG initiatives, companies can create a more sustainable and committed workforce while simultaneously achieving broader corporate objectives.

5.2. Limitations and Future Research Directions

While this study aims to provide theoretical and practical insights through empirical analysis, it has certain limitations. The limitations of this study are as follows. First, the study uses survey data to examine ESG management activities in large manufacturing enterprises, focusing on employees from specific manufacturing firms. As a result, the generalizability of the findings to the entire manufacturing industry may be limited. Second, although various survey items were used to measure ESG management sub-factors, organizational trust, organizational commitment, and organizational performance, responses may have been influenced by social desirability bias, as respondents were employees of the companies under study. Third, the lack of diversity in the sample selection presents another limitation.

For future research, several recommendations can be made. First, given that ESG management environments vary by industry and company, comparative studies should be conducted across different types of organizations. Second, since this study focused on employees of large manufacturing enterprises, future research should include comparative studies considering differences in company size. Third, it is necessary to incorporate standardized international or domestic criteria for measuring ESG management activities to overcome the limitations of survey-based measurement tools. Lastly, future studies should conduct analyses that account for the characteristics of a more diverse set of survey participants and consider differences between groups.

References

- KIF. Korea Institute of Finance; KIF: Seoul, Republic of Korean, 2024; Volume 33, pp. 3–9. [Google Scholar]

- Jung, Y.S.; Kim, M.K.; Song, J.S.; Lee, P.Y.; Choi, I.K. & Park, J.W. A Study on the Impact of Corporate ESG Activities on Brand Image, Corporate Trust, and Corporate Performance. Korean Journal of Business Administration 2024, 37, 1451–1482. [Google Scholar]

- Dakhli. Does Financial Performance Moderate the Relationship Between Board Attributes and Corporate Social Responsibility in French Firms? Journal of Global Responsibility 2021, 12, 373–399. [Google Scholar]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organization Studies 2003, 24, 403–441. [Google Scholar]

- Galbreath, J.; Charles, D.; Oczkowski, E. The Drivers of Climate Change Innovations, Evidence from the Australian Wine Industry. Journal of Business Ethics 2016, 135, 217–231. [Google Scholar]

- Oh, S.J. ESG Management and the Role of Outside Directors in Korean Listed Companies. Yonsei Law Journal 2021, 37, 401–433. [Google Scholar] [CrossRef]

- Seo, K.R. The Role of Finance to Promote ESG Management of SMEs. Global Financial Review 2021, 2, 171–204. [Google Scholar] [CrossRef]

- Min, J.H.; Kim, B.S.; Ha, S.Y. The Relationship between Firms` Environmental, Social, Governance Factors and Their Financial Performance: An Empirical Rationale for Creating Shared Value. Korean Management Science Review 2015, 32, 113–131. [Google Scholar] [CrossRef]

- Shin, H.C.; Yoo, S.W. A Comparative Study on Employee Communication between Two Companies with Different Cultural Background: Shared values, Clarity in Work and Communication Campaign. Journal of Public Relations 2004, 8, 125–161. [Google Scholar]

- KPMG Samjong Accounting Corp, What Should Companies Prepare for the Rise of ESG? , Samjong Insight 2021, 74.

- Jung, J.H.; Park, H.S. A Study on the Effect of Corporate ESG Activities on Business Performance: Focusing on the Moderating Effect of Corporate Values Perception. Industry Promotion Research 2022, 7, 15–29. [Google Scholar]

- Bae, C.H.; Kim, T.D.; Shin, S.C. The Trend of Studies Using Non-financial Measures in the Field of Accounting and ESG Issue. Korea Accounting Journal 2021, 30, 235–276. [Google Scholar] [CrossRef]

- Lee, G.H.; Seo, J.I.; Nam, Y.S. The Relationship between ESG Management Legitimacy and Corporate Giving: the Moderating Role of Family Executives. Journal of the Korea Industrial Systems Research 2022, 27, 63–77. [Google Scholar]

- Papalexandris. N. Sustainable Development and the Critical Role of HRM. Studia Universitatis Babes-Bolyai Oeconomica 2022, 67, 27–36.

- Kim, K.M.; Ju, S.W. A Study on the Effects of Entrepreneurship Environment on Entrepreneurial Will of the MZ Generation and the Moderating Effect of ESG Awareness. Asia-Pacific Journal of Convergent Research Interchange 2023, 9, 157–168. [Google Scholar] [CrossRef]

- Park, M.S.; Seo, J.H. An Analysis of The Real Estate Value Influenced by The Characteristics of ESG Management. Journal of the Korea Real Estate Management Review 2021, 24, 245–271. [Google Scholar] [CrossRef]

- Ameer, R.; Othman, R. Sustainability Practices and Corporate Financial Performance: A Study Based on the Top Global Corporations. Journal of Business Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Porter, M.E.; Vander, L.C. Green and Competitive: Ending the Stalemate; Harvard Business School Publishing: Boston, MA, USA, 1995. [Google Scholar]

- Mayer, R.C.; Davis, J.H.; Schoorman, D.F. An Integrative Model of Organizational Trust. Academy of Management Review 1995, 20, 709–734. [Google Scholar] [CrossRef]

- Hosmer, L.T. Trust: The Connecting Link between Organizational Theory and Philosophical Ethics. Academy of Management Review 1995, 20, 379–403. [Google Scholar] [CrossRef]

- Chung, Y.M.; Lee, M.H. The Impact of Social Responsibility CSR Has on Organizational Trust and Organizational Commitment in Travel Agencies. Journal of Tourism Management Research 2014, 58, 253–275. [Google Scholar]

- Tan, H.H.; Tan, C.S.F. Toward the Differentiation of Trust in Supervisor and Trust in Organization. Genetic, Social & General Psychology Monographs 2000, 126, 241. [Google Scholar]

- Cook, J.; Wall, T. New Work Attitude Measures of Trust, Organizational Commitment and Personal Need Non-Fulfillment. Journal of Occupational Psychology 1980, 53, 39–52. [Google Scholar] [CrossRef]

- March, J.G.; Simon, H.A. Organization; Wiley: New York, NY, USA, 1958. [Google Scholar]

- Becker, H.S. Notes on the Concept of Commitment. American Journal of Sociology 1960, 66, 32–42. [Google Scholar] [CrossRef]

- Bateman, T.S.; Organ, D.W. Job Satisfaction and The Good Soldier: The Relationship Between Affect And Employee “Citizenship”. Academy of Management Journal 1983, 26, 587–595. [Google Scholar] [CrossRef]

- Angle, H.L.; Perry, J.L. An Empirical Assessment of Organizational Commitment and Organizational Effectiveness. Administrative Science Quarterly 1981, 27, 1–14. [Google Scholar] [CrossRef]

- Allen, N.J.; Meyer, J.P. The Measurement and Antecedents of Affective, Continuance, and Normative Commitment to the Organization. Journal of Occupational Psychology 1990, 63, 1–18. [Google Scholar] [CrossRef]

- Meyer, J.P.; Herscovitch, L. Commitment in the workplace: Toward a general model. Human Resource Management Review 2001, 11, 299–326. [Google Scholar] [CrossRef]

- Li, L.; Zhu, Y.; Park, C.W. Leader-Member Exchange, Sales Performance, Job Satisfaction, and Organizational Commitment Affect Turnover Intention. Social Behavior and Personality 2018, 46, 1909–1922. [Google Scholar] [CrossRef]

- Ha, A.N.; Lee, H.S. The Effects of Organizational Culture within Airline`s Crew Team on Organizational Commitment the Team and Customer Orientation. Tourism Research, 2017, 42, 193–220. [Google Scholar]

- Collins, C.J.; Smith, K.G. Knowledge Exchange, and Combination: The Role of Human Resource Practices in The Performance of High-Technology Firms. Academy of Management Journal 2006, 49, 544–560. [Google Scholar] [CrossRef]

- Quinn, R.E.; McGrath, M.R. The Transformation of Organizational Cultures: A Competing Values Perspective. In Organizational Culture; Frost, P.J., Moore, L.F., Louis, M.R., Lundberg, C.C., Martin, J., Eds.; Sage Publications, Inc.: New York, NY, USA, 1985. [Google Scholar]

- Won, H.S.; Hong, J.H.; Cha, J.H. An Effect on Business Performance of S&M Business CEOs' Enterpreneurship. The Journal of Business Education 2015, 29, 309–340. [Google Scholar]

- Friede, G.; Busch, T.; Bassen, A. ESG and Financial Performance: Aggregated Evidence from more than 2000 Empirical Studies. Journal of Sustainable Finance & Investment 2015, 5, 210–233. [Google Scholar]

- Eliwa, Y.; Ahmed, A.; Ahmed, S. ESG Practices and The Cost of Debt: Evidence from EU Countries. Critical Perspectives on Accounting 2021, 79, 102097. [Google Scholar] [CrossRef]

- Lu, B.; Ding, J.; Lee, E.S. The Impact of ESG Investments on Corporate Value and Performance-A Comparative Study of Clothing Manufacturing and Service Industries in China. Journal of Industrial Innovation 2023, 39, 50–66. [Google Scholar]

- Barrymore, N.; Sampson, R.C. ESG Performance and Labor Productivity: Exploring Whether And When ESG Affects Firm Performance. Academy of Management Proceedings 2021, 1, 13997. [Google Scholar] [CrossRef]

- Turker, D. Measuring Corporate Social Responsibility: A Scale Development Study. Journal of Business Ethics 2009, 85, 411–427. [Google Scholar] [CrossRef]

- Qiang, H.; Park, J.C. The Effect of Corporate Environmental Responsibility Activities on Corporate Performance: Focusing on the Mediating Effect of Trust Types. Journal of Product Research 2022, 40, 7–14. [Google Scholar]

- Chang, S.I. The Effect of ESG Management Activities of Organizational Members of SMEs on Organizational Effectiveness through Organizational Trust and Corporate Entrepreneurship: Focusing on the Electrical and Electronic Industries in Chungnam and Sejong. Innovation Enterprise Research, 2023, 8, 329–358. [Google Scholar] [CrossRef]

- Kim, Y.H.; Kim, Y.O. The Effect of ESG Management Activities of Food Service Companies on Job Satisfaction and Organizational Commitment. Journal of Industrial Innovation 2023, 39, 132–142. [Google Scholar]

- Choi, Y.R.; Kim, H.D. The Effect of Service Orientation Effort on Job Satisfaction, Organizational Commitment, and Turnover Intention in Logistics Firms. Journal of Korea Port Economic Association 2017, 33, 33–52. [Google Scholar] [CrossRef]

- Koller, T.; Nuttall, R.; Henisz, W. Five Ways that ESG Creates Value. The McKinsey Quarterly 2019, 1–12. [Google Scholar]

- Kim, S.S.; Lee, Y.M. The Influence of Employees' Perceived Corporate Social Responsibility Motives on their Organizational Commitment. Korea Business Review 2020, 24, 117–140. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, Social and Governance Performance and Financial Risk: Moderating Role of ESG Controversies and Board Gender Diversity. Resources Policy 2021, 72, 102144. [Google Scholar] [CrossRef]

- Park, Y.N.; Han, S.L. The Effect of ESG Activities on Corporate Image, Perceived Price Fairness, and Consumer Responses. Korean Management Review 2021, 50, 643–664. [Google Scholar] [CrossRef]

- Gouthier, M.H.; Rhein, M. Organizational Pride and Its Positive Effects on Employee Behavior. Journal of Service Management 2011, 22, 633–649. [Google Scholar] [CrossRef]

- Chae, J.S.; Choi, Y.J. A Study on the Organizational Citizenship Behavior of Court Security Officials. Korean Journal of Industry Security 2020, 10, 175–207. [Google Scholar] [CrossRef]

- Bong, J.H.; Lee, S.H. The Effects Of Trust on Customer Orientation and Job Performance in Foodservice Industry: Focused On Contingent Workers. Korean Journal of Hospitality and Tourism 2017, 26, 131–142. [Google Scholar]

- Wagner, S.L.; Rush, M.C. Altruistic Organizational Citizenship Behavior: Context, Disposition, and Age. The Journal of Social Psychology 2000, 140, 379–391. [Google Scholar] [CrossRef]

- Fu, W.; Deshpande, S.P. The Impact of Caring Climate, Job Satisfaction, and Organizational Commitment on Job Performance of Employees In A China’S Insurance Company. Journal of Business Ethics 2014, 124, 339–349. [Google Scholar] [CrossRef]

- Seo, J.S. A Study on the Impact of Organizational Commitment on Workers’ Turnover Intention and Organizational Performance: Based on Analysis of Welfare Organizations in Busan, Korea. Asia-Pacific Journal of Business Venturing and Entrepreneurship 2016, 11, 215–225. [Google Scholar] [CrossRef]

- Kwon, M.Y. The Effects of Fun Management on the Organizational Commitment and Service Innovation Performance in Food Service Industry. Regional Industry Review 2017, 40, 149–168. [Google Scholar]

- Lee, S.A.; Eom, W.Y. Perceptual Difference in the Competences and Performance of Roles of HRD Practitioner at Small and Medium Business by Position, Work experience and Educational level. Journal of Corporate Education and Talent Research 2013, 15, 51–77. [Google Scholar]

- Kim, J.H.; Kim, S.Y.; Oh, S.Y.; Park, S.M. A Study on the Relationship between Transformational Leadership in Public Sector and Active Administration of Public Officials: Focused on Behavioral Mediating Effects, Moderating Effects of Recruitment System and Grade. Korean Society and Public Administration 2020, 31, 163–197. [Google Scholar] [CrossRef]

- Cohen, D.A.; Ridgeway, C.L. Decision Making Groups and Teams: An Information Perspective. Business & Economics 2006, 22, 1–29. [Google Scholar]

- Kim, I.K.; Kang, S.K. A Study on the Factors Affecting Organizational Innovation Behavior of SMEs: Focused on the Moderate Effect of Work Experience and Rank. Asia-Pacific Journal of Business Venturing and Entrepreneurship 2019, 14, 75–89. [Google Scholar]

- Piao, X.; Xie, J.; Managi, S. Environmental, Social, And Corporate Governance Activities with Employee Psychological Well-Being Improvement. BMC Public Health 2022, 22, 1–12. [Google Scholar] [CrossRef] [PubMed]

- Daugaard, D. Emerging New Themes in Environmental, Social and Governance Investing: A Systematic Literature Review. Accounting & Finance 2020, 60, 1501–1530. [Google Scholar]

- Ji, S.G. The Effects of Corporate Social Responsibility on Organizational Trust and Commitment to Customer Service in Service Corporate. Korea Journal of Business Administration 2006, 19, 1867–1893. [Google Scholar]

- Jun, S.H. An Empirical Study on the Effects of SMEs Competition, ESG Management Activities and Organizational Justice on Job Satisfaction: Focusing on Mediating Effects of Self-efficacy. Journal of Venture Innovation 2023, 6, 41–62. [Google Scholar]

- Mostafa, A.M.S.; Bottomley, P.; Gould-Williams, J.; Abouarghoub, W.; Lythreatis, S. High-Commitment Human Resource Practices and Employee Outcomes: The Contingent Role of Organisational Identification. Human Resource Management Journal 2019, 29, 620–636. [Google Scholar] [CrossRef]

- Mowday, R.T.; Porter, L.W.; Steers, R.M. Employee-organizational linkages: The psychology of commitment, absenteeism, and turnover; Academic Press: New York, NY, USA, 1982. [Google Scholar]

- Hackett, R.D.; Lapierre, L.M.; Hausdorf, P.A. Understanding The Links between Work Commitment Constructs. Journal of Vocational Behavior 2001, 58, 392–413. [Google Scholar] [CrossRef]

- Kang, N.Y. The Dual Mediating Effect of Lmx And SNS Information Sharing in The Relationship between E-Leadership and Organizational Commitment; Graduate School Dankook University: Yongin-si, Republic of Korean, 2023. [Google Scholar]

- Kang, I.T. A Study on the Effect of ESG Management on Financial Performance in Hotel Companies: Focused on Mediating Effects of Authentic Leadership and Affective Organizational Commitment; Graduate School Kyonggi University: Seoul, Republic of Korean, 2022. [Google Scholar]

- Kang, N.Y. The Dual Mediating Effect of LMX and SNS Information Sharing in the Relationship between E-leadership and Organizational Commitment; Graduate School Dankook University: Yongin-si, Republic of Korean, 2023. [Google Scholar]

- Park, J.Y. A Study on The Mediating Effect of Intrapreneurship Between CEO Entrepreneurship and Performance of Manufacturing Enterprise; Graduate School Soongsil University: Seoul, Republic of Korean, 2018. [Google Scholar]

- Kaplan, R.; Norton, D. The Balanced Scorecard—Measures That Drive Performance. Harvard Business Review 1992, 79. [Google Scholar]

- Kim, Y.H. Effect of Digital Transformation and ESG Management on Corporate Performance; Dankook University,: Yongin-si, Republic of Korean, 2023. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Park, S.M.; Jeong, H.I. A Study on ESG Management Strategy Case and Promotion Policy– Focusing on the Construction Industry. Logos Management Review 2023, 21, 169–190. [Google Scholar]

- Wright, P.; Ferris, S.P. Agency Conflict and Corporate Strategy: The effect of Divestment on Corporate value. Strategic Management Journal 1997, 18, 77–83. [Google Scholar] [CrossRef]

- Yu, J.M.; Yang, D.H. Does Firm's ESG Performance Mitigate the Negative Impact of Agency Costs on Firm Value? Korea International Accounting Review 2022, 104, 135–167. [Google Scholar]

- Eum, S.B.; Kim, H.D.; Kim, D.S. The Relations between Korean KOSDAQ-listed Firm's ESG Activities, Corporate Performance, and Firm Value. Korean Management Consulting Review 2023, 23, 219–232. [Google Scholar]

- Kim, S.H. Legal Issues on the Operation System of Electronic Administrative in Germany. Distribution Law Review 2021, 8, 203–236. [Google Scholar]

- Huh, J.H.; Hong, J.W. The Impact of ESG Management on Customer's Trust and Satisfaction: Focusing on the Moderating Effect of ESG Concern. Journal of Business Research 2023, 38, 125–138. [Google Scholar]

- Noh, J.H. The Impact of ESG Management on Job Satisfaction in Transportation Logistics Companies: The Mediating Effects of Organizational Commitment and Self-Efficacy. Korea Trade Review 2024, 49, 89–109. [Google Scholar] [CrossRef]

- Werther, W.B.; Chandler, D. Strategic Corporate Social Responsibility: Stakeholders in a Global Environment, 2nd ed; SAGE: Los Angeles, CA, USA, 2011. [Google Scholar]

- Ahn, J.S.; Chung, S.H.; Lee, S.R.; Park, J.W. The Effect of ESG Activities on the Business Performance. Journal of the Korean Society for Aviation and Aeronautics 2022, 30, 92–108. [Google Scholar] [CrossRef]

- Kang, H.; Lim, S.H. A Study on the Impact of ESG (Environmental, Social, and Governance) Management Activities of Small and Medium-sized Enterprises on the Organization's Non-financial Performance. Industry Promotion Research 2024, 9, 23–28. [Google Scholar]

- Mohammad, W.M.W.; Wasiuzzaman, S. Environmental, Social and Governance(ESG) Disclosure, Competitive Advantage and Performance of Firms in Malaysia. Cleaner Environmental Systems 2021, 2, 100015. [Google Scholar] [CrossRef]

- Nisar, Q.A.; Haider, S.; Ali, F.; Jamshed, S.; Ryu, K.; Gill, S.S. Green Human Resource Management Practices and Environ-Mental Performance in Malaysian Green Hotels; The Role of Green Intellectual Capital and Pro-Environmental Behavior. Journal of Cleaner Production 2021, 311, 127504. [Google Scholar] [CrossRef]

- Lee, S.H.; Olshfski, D. Employee Commitment And Firefighters: It`s My Job. Public Administration Review 2002, 62, 108–114. [Google Scholar]

- Lee, S.H.; Cho, J.Y. The Study On Receptiveness To Performance Appraisal System Based On BSC Among Public Employees At The Local Level Governments. Korean Society And Public Administration 2010, 20, 269–291. [Google Scholar]

Figure 1.

Research model.

Table 1.

Demographic characteristics.

| Categories | n(%) | Categories | n(%) | ||

|---|---|---|---|---|---|

| Gender | Male | 359(64.0) | Department | Planning Team | 40(7.1) |

| Female | 202(36.0) | Sales(Marketing) Team | 154(27.5) | ||

| Age | Twenties | 90(16.0) | Production Control Team | 148(26.4) | |

| Thirties | 82(14.6) | R&D Team | 50(8.9) | ||

| Forties | 164(29.2) | HR Team | 24(4.3) | ||

| Fifties | 176(31.4) | Finance&Accounting Dept | 61(10.9) | ||

| Above Fifties | 49(8.7) | Others | 84(15.0) | ||

| Academic background | High school graduate | 118(21.0) | Years of service |

less than 5 years | 109(19.4) |

| College graduate | 380(67.7) | 5 years or more∼ less than 10 years |

158(28.2) | ||

| Above Graduate school | 63(11.2) | ||||

| Job Position | Associate | 133(23.7) | 10 years or more∼ less than 15 years |

79(14.1) | |

| (Rank) | Assistant | 168(29.9) | |||

| Manager | 112(20.0) | 15 years or more | 215(38.3) | ||

| Senior Manager | 72(12.8) | Authenticity | Y | 381(67.9) | |

| Above General Manager | 76(13.5) | N | 180(32.1) | ||

| Total | 561(100) |

Table 2.

Reliability and validity for the measurement model.

| Construct | Estimate | t-value | Cronbach‘s ɑ | C.R. | AVE | ||

|---|---|---|---|---|---|---|---|

| Std. Estimate |

S.E. | ||||||

| Environment | a4 | .766 | 0.875 | 0.977 | 0.731 | ||

| a2 | 1.027 | .075 | 16.952*** | ||||

| Social | a8 | .931 | 0.904 | 0.975 | 0.712 | ||

| a7 | .903 | .040 | 27.299*** | ||||

| Governance | a12 | .742 | 0.920 | 0.977 | 0.731 | ||

| a10 | .947 | .051 | 23.355*** | ||||

| a9 | .932 | .050 | 23.094*** | ||||

| Organizational trust | b4 | .802 | 0.917 | 0.977 | 0.727 | ||

| b2 | .906 | .048 | 24.505*** | ||||

| b1 | .893 | .049 | 24.187*** | ||||

| Organizational Commitment |

b8 | .553 | 0.824 | 0.976 | 0.720 | ||

| b7 | .815 | .120 | 12.199*** | ||||

| b6 | .838 | .125 | 12.158*** | ||||

| Organizational Performance |

c6 | .813 | 0.958 | 0.982 | 0.741 | ||

| c4 | .922 | .040 | 26.825*** | ||||

| c3 | .932 | .041 | 27.106*** | ||||

Note: X²=340.596, χ²/df=3.827, p=0.000, GFI=0.931, RMR=0.036, IFI=0.962, TLI=0.949, CFI=0.962, RMSEA=0.071 ***p<.001.

Table 3.

Discriminant validity

| Construct | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| (1) Environment | (.855) | |||||

| (2) Social | .662** | (.844) | ||||

| (3) Governance | .517** | .630** | (.855) | |||

| (4) Organizational trust | .475** | .525** | .539** | (.853) | ||

| (5) Organizational Commitment | .157** | .262** | .383** | .249** | (.849) | |

| (6) Organizational Performance | .458** | .541** | .611** | .502** | .319** | (.861) |

The diagonal bold is the AVE square root value, ** p<0.01.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.