Submitted:

12 March 2025

Posted:

13 March 2025

You are already at the latest version

Abstract

In this paper, we study the relationship between board characteristics and non-performing loans in the MENA region. To this end, we used a sample of 70 banks operating in 12 countries in the MENA region from 2010 to 2022. The System Generalized Method of Moments (SGMM) was employed as an empirical technique. To benefit from a comparative analysis, we divided the whole sample into two sub-samples. The first one covers six Gulf Cooperation Council countries (GCC) with 42 banks. The second one is also relative to six non-Gulf Cooperation Council countries (NGCC) with 28 banks. The empirical findings indicate that board independence, gender diversity, board compensation, and the board index decrease NPLs across all regions, including MENA, GCC, and NGCC, while board size and tenure increase NPLs. However, duality increases NPLs only in the MENA and GCC regions.

Keywords:

Board Characteristics

; Non-performing Loans

; MENA Region

; SGMM

1. Introduction

Board composition and non-performing loans play a significant role in sustainability, particularly in the environmental, social, and governance (ESG) framework. Strong governance, responsible lending, and ESG-driven financial strategies ensure long-term resilience, aligning financial stability with sustainability goals. Furthermore, the banking sector plays a crucial role in economic development due to its financial functions. Therefore, its main priority is ensuring the sustained progression of economic and financial development (Sallemi et al., 2023). Since the financial crisis, this sector has faced serious problems, including a significant accumulation of non-performing loans. These lastly pose serious risks to banks and can even lead to their failure (Jin et al., 2011; Lu and Whidbee, 2016). Non-performing loans have become an alarming problem because they undermine the quality of bank assets and jeopardize the viability of the sector. Thus, banks must pay close attention to their growth to maintain stability (Polat (2018), Park (2012)).

Researchers have given great attention to the determinants of non-performing loans, which can be classified into three main categories. The first category includes bank-specific variables like size, capital, liquidity risk, and performance (Chaibi and Ftiti, 2015; Hassan et al., 2018; Naili and Lahrichi, 2022). According to Saliba et al. (2023), bank-specific variables are significant predictors of non-performing loans in BRICS countries. The second category contains macroeconomic variables that serve to check the environment in which a bank operates, such as GDP growth, inflation, unemployment, and institutional quality. Kumar et al. (2018); Jabbouri et al. (2022); and Karismaulia et al. (2023). Following Manz (2019), the role of these factors is still poorly understood and requires further research. Moreover, Adusei and Bannerman (2022) highlighted that economic conditions are a significant determinant of the financial circumstances of bank clients, ultimately impacting banking activities and performance. Lastly, the third category focuses on industry-specific indicators, offering a comprehensive perspective on the structure of the banking sector, such as competition and market concentration (Karadima and Louri, 2021; Alnabulsi et al., 2022).

Several studies have examined the structure of banking governance and its potential role in reducing non-performing loans. An effective governance structure improves operational efficiency and helps mitigate fraud and information asymmetry (Massi, 2016). In this context, there is a growing emphasis on the bank governance structure, particularly regarding internal governance mechanisms that significantly impact banking risks (Golliard and Poder, 2007).

Banking governance differs from corporate governance due to its rising opacity, linked to information asymmetry, high levels of indebtedness, and strict regulation. These factors amplify the role of the board of directors in reducing risks (Salas and Saurina, 2003). The board serves as a crucial control mechanism, supervising executives and guiding the bank's strategy and implementation (Andres and Vallelado, 2008; Fernandes et al., 2017).

The discussion around its effectiveness is based on these main characteristics. John et al. (2016) mentioned that the effectiveness of a board depends on its structure, namely its independence, size, committees, and the duality between the CEO and the Chairman as well as its quality. Furthermore, Sumner and Webb (2005) concluded that the board structure influences credit policies. Jensen (1993) adds that board’s effectiveness is linked to its attributes, notably non-duality, board size, and the presence of potential shareholders. Recently, the literature has emphasized the relationship between credit risk and non-performing loans.

This research aims to investigate the impact of board characteristics on credit risk across a sample of 12 countries in the MENA region, divided into 6 GCC countries and 6 NGCC countries. The empirical model employed in this study includes data from 2010 to 2022 related to 70 banks and is estimated using the SGMM. The findings indicate that board size and tenure positively impact NPLs across all the regions analyzed. Regarding duality, it has a positive and significant impact only in the MENA and GCC regions. Conversely, board independence, gender diversity, board compensation, and the board index significantly and negatively affect NPLs across all regions, including MENA, GCC, and NGCC.

This study makes several significant contributions to the existing literature on bank governance in developing countries. First, it addresses a notable research gap by examining the effects of board characteristics such as gender diversity, board tenure, and administrators' compensation on non-performing loans (NPLs). This issue has become a priority across the MENA region. Second, while previous research has typically analyzed two or three board characteristics separately, this study takes a more holistic approach by constructing a board of directors’ index using the Principal Component Analysis (PCA) method. Third, the whole sample of MENA countries was divided into two sub-samples to benefit from a comparative analysis. Fourth, based on the findings of this paper, policymakers and bankers can adjust the structure and composition of the board of directors to reduce credit risk effectively.

The rest of this paper is organized as follows: Section 2 provides a review of the related literature and outlines the development of the hypotheses. Section 3 describes the sample, the empirical approach, and the model specification. Section 4 presents the analysis and discusses the empirical results. Finally, Section 5 concludes the paper with policy recommendations.

2. Literature Review and Hypotheses

2.1. Board Size and NPLs

Board size refers to the total number of bank board administrators (Muchemwa et al., 2016). Several studies confirm the inverse relationship between board size and NPLs (Switzer and Jun, 2013; Abid et al., 2021). According to this hypothesis, Lu and Boateng (2018) concluded that a larger board, with well-qualified directors, adopts prudent and less risky credit management strategies, and a more regulated decision-making process. Rose (2017) concluded that adding two or more internal directors minimizes credit risk exposure and creates a stronger system of governance. Jensen (1993) concluded that an optimal size of 7 to 8 members seems necessary to coordinate its members' viewpoints, promote speedy and appropriate decision-making, eliminate agency difficulties, and mitigate abusive behaviors. Other research has not demonstrated any significant effect of board size on NPLs. (Boussaada et al., 2020; Djebali and Zaghdoudi, 2019).

Several studies have found a positive relationship between board size and the level of NPLs (Hakimi et al., 2023; Tarchouna et al., 2021; Boussaada et al., 2018). According to Hakimi et al. (2022), board members face severe information asymmetries and intense pressure to handle loan applications, which leads to poor credit decisions. Doğan and Eksi (2020) found that small board sizes negatively impact bank performance and credit portfolio quality, which causes financial instability. Consequently, a larger board is beneficial for minimizing NPLs and maintaining banking stability. In contrast, Pathan (2009) identified smaller boards as crucial in promoting excessive risk-taking. While, it allows shareholders to apply more direct pressure on decisions, potentially encouraging directors to adopt riskier behaviors (Beltratti and Stulz, 2009; Pathan, 2009).

H1:

Board size increases NPLs.

2.2. Board Independence and NPLs

The inclusion of independent directors on a board has attracted considerable attention from researchers. Weisbach (1988) demonstrated that more independent directors can mitigate conflicts of interest. Furthermore, these directors enhance the board's independence, ensure more effective management oversight, improve overall board efficiency, and enable a more accurate assessment of the company's performance (Ploix, 2003).

Empirically, Abid et al. (2021) and Djebali and Zaghdoudi (2019) found that independent directors positively impact NPLs. However, independent directors tend to have less comprehensive knowledge of management policies and decision-making processes than internal directors. However, Tarchouna et al. (2021), using the GMM approach on a sample of 184 American commercial banks from 2000 to 2013, found that a higher proportion of independent directors on the board ensures effective oversight. This, in turn, contributes to improved loan quality, (Doğan and Eksi, 2020). In addition, Boussada et al. (2018) concluded that the presence of independent directors is essential for resolving agency conflict issues. Switzer and Jun (2013) attributed this association to the board's capacity to provide independent oversight, effectively assess management practices, and improve bank performance. Similarly, Pathan (2009) showed the negative relationship between the presence of independent directors and risk-taking, emphasizing their role in balancing the interests of shareholders and other stakeholders.

H2:

Board independence reduces NPLs.

2.3. Duality and NPLs

In corporate governance literature, there is no agreement on the impact of duality on NPLs. Hakimi et al. (2022) and Lu and Boateng (2018) discovered that duality increases NPL levels. Combining the responsibilities of the CEO and board chair might have a detrimental impact on the approval of credit decisions since it promotes entrenchment and prioritizes personal interests. Separating decision-making from supervisory responsibilities, on the other hand, helps in the decentralization of authority and provides more effective executive monitoring. Furthermore, Abid et al. (2021) revealed that duality positively impacts credit risk in public banks it contributes to reducing non-performing loans in private banks.

However, Djebali and Zaghdoudi (2019) discovered that combining the positions of chairman and CEO helps reduce credit risk. This duality improves decision-making control, protecting both individual and shareholder interests. Similarly, Pathan (2009) pointed out that when CEOs accomplish various functions, they could convince directors to pursue less risky strategies, as they are often motivated by a preference for risk aversion. Simpson and Gleason (1999) found that such duality minimizes the likelihood of bankruptcy. Daily and Dalton (1994) discovered a negative relationship between leadership duality and the probability of corporate failure. Furthermore, Switzer and Jun (2013) found no significant relationship between duality and credit risk.

H3:

Duality increases NPLs

2.4. Gender Diversity and NPLs

This study considers gender diversity as essential characteristic that can significantly affect NPLs. Board Gender diversity, marked by the participation of female directors, is commonly considered essential in the board, (Mohsni et al., 2021). They contribute significantly to improving the company's reputation and value while also increasing its performance (Lückerath-Rovers, 2013; Olaoye and Adewum, 2020)). Furthermore, Post et al. (2011) noted that the participation of women enhances the integration of diverse knowledge, perspectives, and viewpoints into decision-making processes. Kramer et al. (2006) demonstrated that having a single woman on the board can improve its efficacy.

Kinateder et al. (2021) proved that gender diversity is a key factor in reducing credit risk. Furthermore, they deployed the critical mass theory to prove that boards with three or more women are more likely to manage and minimize credit risks than boards composed of men. Setiawan and Khoirotunnisa (2020) indicated that a higher proportion of women leads to a more effective control system. Lu and Boateng (2018) noted that female directors are recognized for their risk aversion in implementing and controlling risk management strategies and making financial decisions. However, Berger et al. (2014) discovered that increasing the number of women on a bank's board of directors raises its risk portfolio because they tend to lack knowledge, even though they are generally more risk-averse than men.

H4:

Gender diversity reduces NPLs.

2.5. Board Tenure and NPLs

Another crucial characteristic of a board is tenure, which is a fundamental aspect of a management team, as it shapes engagement, experience, and decision-making processes (Golden and Zajac, 2001). However, Huang and Hilary (2018) contend that a director's tenure represents a trade-off between the accumulation of knowledge and board independence. According to Vafeas (2003), extended board tenure enhances both management commitment and competence while expanding the organization's knowledge base. Similarly, Golden and Zajac (2001) emphasize the importance of tenure in enhancing institutional knowledge.

Furthermore, Beasley (1996) emphasizes that directors with longer tenure are less vulnerable to managerial pressure, hence increasing their effectiveness in reducing opportunistic behavior within the management team. In contrast, Byrd et al. (2010) present the "CEO loyalty hypothesis," which contends that long-serving directors may build close relationships with executives, including the CEO, thereby jeopardizing their ability to prioritize shareholders' interests. To study the relationship between board tenure and banking credit risk on an international scale, Kinateder et al. (2021) used data from 141 listed banks over the period 2006-2017. They concluded that banks with a higher tenure face lower risks.

H5:

Board tenure increases NPLs.

2.6. Board Compensation and NPLs

Administrator compensation significantly affects company investment decisions, especially when moral hazard and managerial discretion are present (John et al., 2003). Furthermore, Brewer et al. (2004) found a relationship between increased banking risk and a higher proportion of CEO compensation based on equity capital growth. Chen et al. (2006) found that remuneration structures based on stock-options increased risk-taking in the banking sector. Similarly, Bebchuk and Spamann (2009) argued that incentive-based remuneration in the bank encouraged excessive risk-taking, which played a significant part in the current financial crisis. Faccio et al. (2016) established a positive relationship between CEO compensation and risk-taking measures, suggesting that higher financial incentives motivate riskier decision-making among banking executives.

Some empirical studies have examined the relationship between the compensation and the NPLs. Lu and Boateng (2018) and Rose (2017) found that higher CEO compensation is linked to an increase in NPLs, suggesting that it incentivizes executives to engage in excessive risk-taking to achieve potential income. These findings align with the results of Deyoung and Torna (2013), who analyzed quarterly data from U.S. banks during the 2008–2010 financial crisis. They concluded that high compensation for stakeholders, including CEOs, increases the likelihood of bank failures, as higher income motivates CEOs to make riskier decisions. Based on this empirical discussion, we propose the following hypothesis:

H6:

Board compensation increases NPLs.

3. Methodology

3.1. The Sample

This research used a sample of 70 banks from 12 MENA countries, observed over the period 2010-2022. Initially, we compiled a sample of 181 banks from the MENA region for the period 2000-2022. Due to the unavailability of certain data, we retained only the banks with at least 5 board characteristics over 10 years. Our final sample includes 70 banks, distributed as follows: 42 banks from the 6 GCC countries and 28 banks from non-GCC countries.

To begin this study, we collected data related to the banks and their revenue characteristics from the Eikon Refinitiv database and the annual reports of each bank. We also obtained macroeconomic variables and industry-specific variables from the World Bank database (World Bank Indicators - WDI, Global Financial Development - GFD). Table 1 presents the distribution of our sample by country.

3.2. Empirical Approach and Model Specification

As the panel data framework, the System Generalized Method of Moment (SGMM) is more effective as it resolves biases caused by missing data. Additionally, it addresses the endogeneity issue of explanatory variables, leading to more efficient and reliable results.

In this study, we measured the dependent variable using the non-performing loan (NPL) ratio, which is widely recognized in the literature as the indicator for assessing bank credit risk (). To assess the impact of board characteristics on NPLs, the key independent variables include board size, duality, board independence, gender diversity, compensation, and board Tenure.

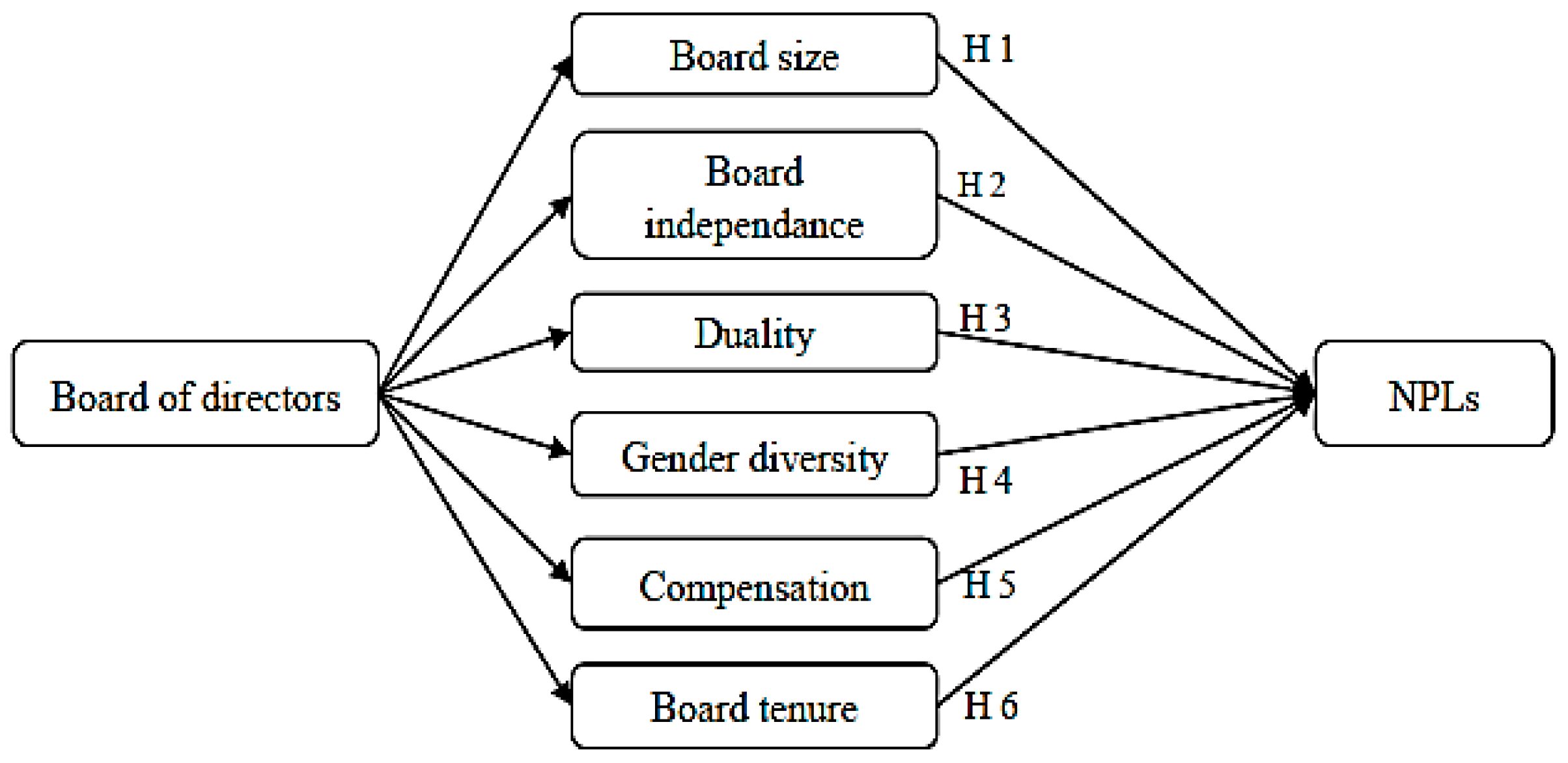

The empirical strategy is based on two models. In the first model, we estimate the impact of board characteristics on NPLs separately (Figure 1), according to the following equation (1):

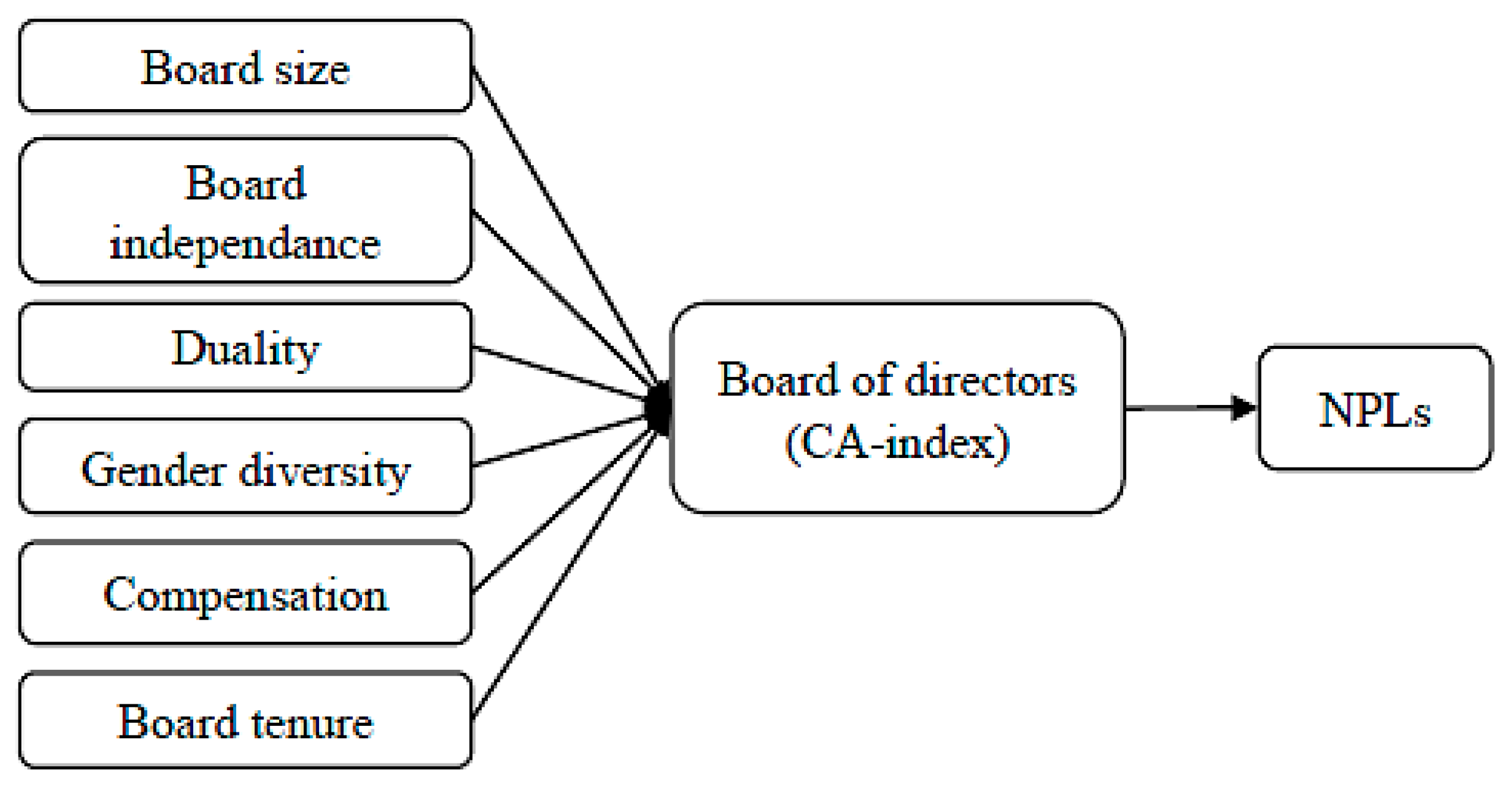

In the second model, we propose constructing a Board of Directors index (CA_index). To do this, we will use only the characteristics that significantly explain the level of NPLs in our sample. The index is constructed through two main steps. The first step is normalization using the Min-Max method (Hakimi et al 2021), which adjusts the data values within a fixed range, typically between 0 and 1. This step reduces the data's dimensionality while preserving the most relevant information. We chose normalization because it allows us to standardize highly variable data onto a uniform scale. VNk is the normalized value of each board characteristic (CA) during period t, and min (CA) and max (CA) represent the minimum and maximum values of each characteristic, respectively.

The second step is the ponderation of each normalized variable by equal coefficients (equal to 1/N) to ensure that the influence of each variable is uniform. This approach is simpler, more practical, and fairer, facilitating a consistent analysis of the variables' importance without bias and avoiding weighting biases. Once the CA_index is calculated, the resulting values will range from 0 to 1, where 0 represents the lowest level of board effectiveness and 1 represents the highest level. N is the number of board characteristics used in the construction of the CA_index.

The second model (Figure 2) to be tested is given in Equation (2).

4. Analysis and Results

In this section, we will first examine the descriptive statistics of our variables, followed by a Pearson correlation test between them. Next, we will discuss and evaluate the findings on the board characteristics and NPLs relationship in the MENA, GCC, and NGCC regions.

4.1. Summary Statistics and Correlation Matrix

Table 3 provides the descriptive statistics for our variables. The average NPLs ratio is 7.3%, with a maximum value of 261% recorded by a Turkish bank in 2012 and a minimum value of 4% observed by a Saudi bank in 2011.

Statistics indicate that the average board size in the MENA region is 10.52 members. The largest recorded board consisted of 19 members at a Turkish bank in 2010, while a Tunisian bank had a much smaller board with only 5 members that same year. In terms of board independence, 28.81% of board members are independent, with the highest proportion reaching 100%. The average percentage of women on boards is 6.62%, with a maximum of 40%. The minimum proportion for both independent members and women on the board is 0%. Board tenure varies from 1 to 6 years, with an average Board Tenure of 3.1 years. The mean ratio of board member compensation to total assets is 0.01%, with the highest value recorded at 0.18% and the lowest at 0%.

The average bank size is 23.737, with a maximum value of 26.512 and a minimum value of 20.942. The mean value of bank capital is 16.7%, ranging from a maximum of 42.9% to a minimum of 3.5%. The highest value for bank performance (ROA) was 6.3%, while the lowest was -3.8%. The mean value of the LTD ratio is 98.76%, with a maximum of 162% and a minimum of 1.4%. The average value for bank diversification (NII) is 38.44%, with a maximum of 96% and a minimum of 9.55%. The mean value of concentration is 82.197%, with a maximum value of 100% and a minimum value of 56.035%. As for the macroeconomic factors, the average values for GDP and inflation (INF) are 3.120% and 4.833%, respectively. The maximum values are 19.592% for GDP and 29.5% for inflation, while the minimum values are -2.4% and -3.749%.

Table 4 presents the descriptive statistics for the dichotomous variable "Duality." The majority of banks in the MENA region, 87.79%, opt to separate the roles of Chairman of the Board and CEO. In contrast, 12.21% of banks follow a policy of combining these roles, which contradicts the recommendations of best governance practices that advocate for the separation of these functions.

Table 5 displays the results of the correlation matrix between our variables. The Pearson correlation test shows that the coefficients are below 0.7 in absolute value (Kervin, 2010). Therefore, our model is free from multicollinearity.

4.2. Discussion of the Empirical Findings

The results showed that both the Sargan test and the autocorrelation test did not reject the null hypothesis, confirming the validity of the over-identification restrictions and the absence of correlation. The p-values for both the Sargan test and AR (2) exceeded 5%. The lagged dependent variable (NPLs (-1)) has a positive and significant effect at the 1% level on credit risk in the MENA regions, as well as in the GCC and NGCC countries. This suggests that the volume of NPLs from the previous year has a significant impact on those of the current year.

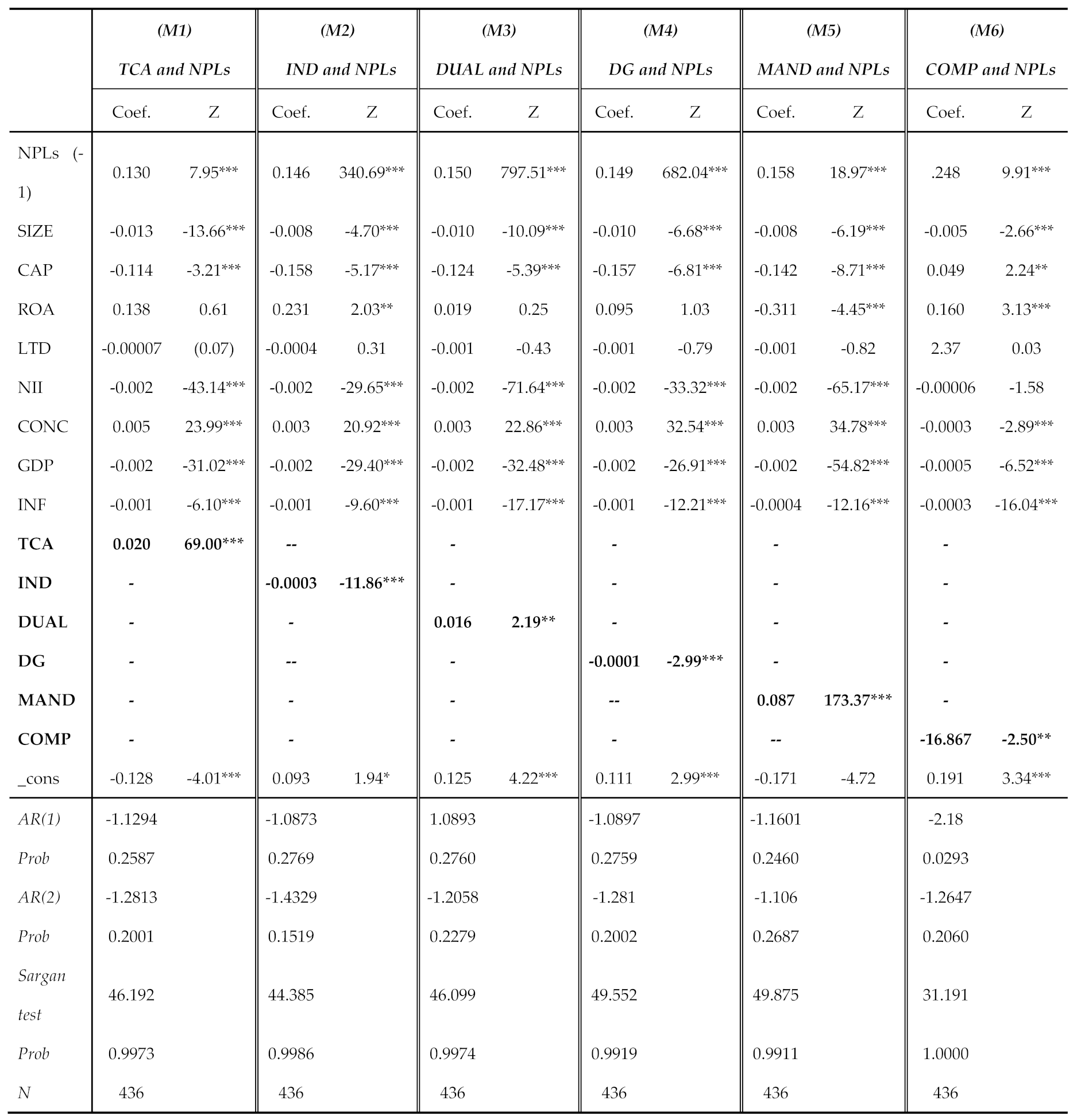

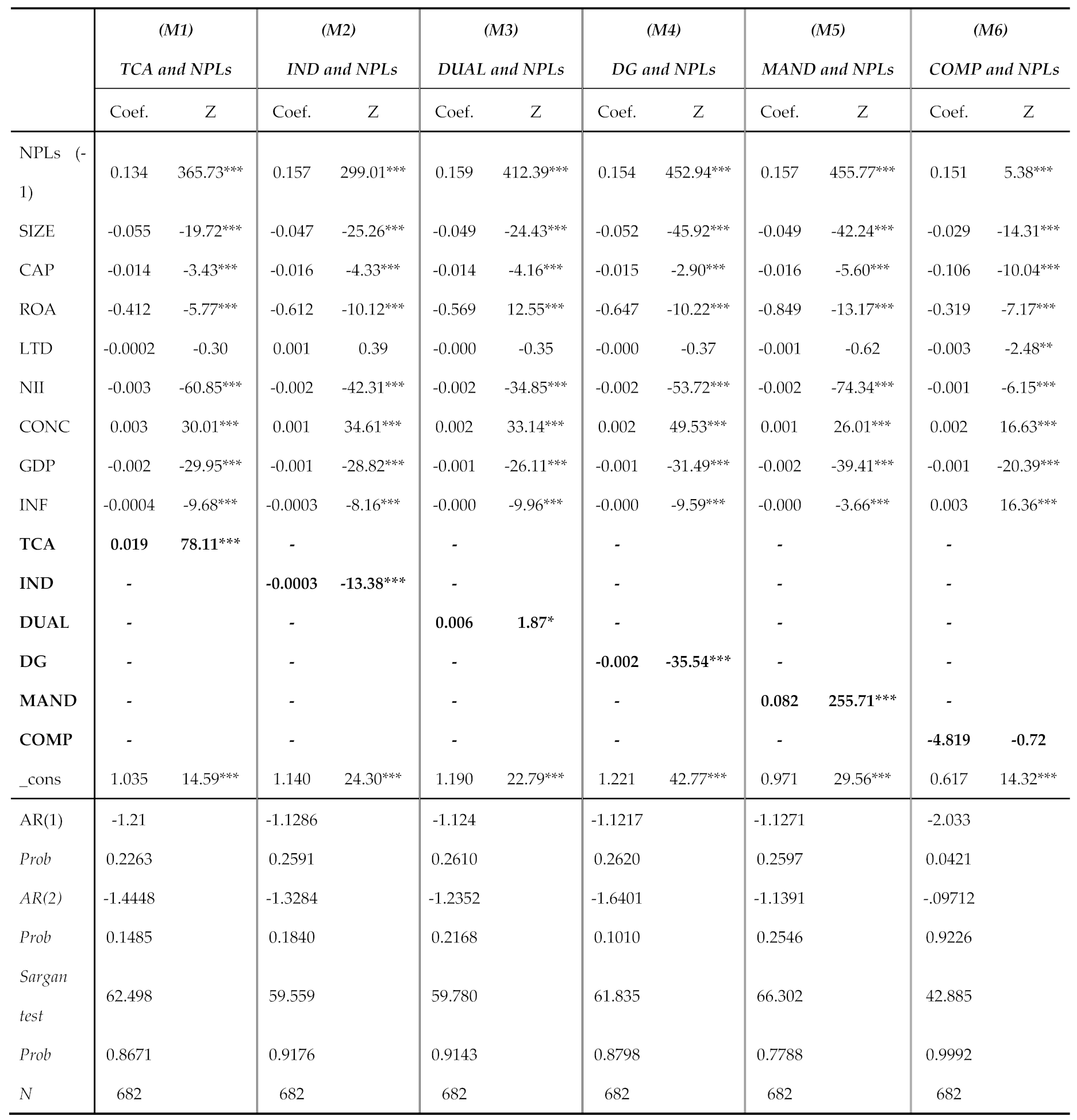

The board size has a positive and significant effect at the 1% level for the MENA region, GCC countries, and NGCC countries. These findings show that a 1% increase in board members increases the NPL rate by 1.9% in the MENA region, 2% in GCC banks, and 2.6% in NGCC banks. A larger board size can complicate negotiation and decision-making processes, making them less efficient and slower. Furthermore, a large number of directors might dilute individual responsibility, reducing the effectiveness of supervision and risk management. The diversity of opinions and interests on an extended board may also hinder consensus-building, leading to divergences that make it difficult to develop coherent strategies for managing credit risk. Furthermore, when there is severe information asymmetry and intense pressure on directors to approve inadequate credit requests, it might lead to poor credit judgments. Our results are consistent with those of Tarchouna et al. (2021) and Doğan and Eksi (2020). The positive sign observed for both regions confirms hypothesis H1.

Board independence has a negative coefficient with a statistically significant effect of 1% in the MENA region and GCC countries, while it is significant at 5% for NGCC banks. Thus, a 1% increase in the number of independent directors reduces the level of NPLs by 0.03% in these two regions and by 0.04% for NGCC countries. The presence of independent directors also promotes transparency in decision-making processes, since they are less likely to be influenced by internal conflicts of interest. More specifically, the recruitment of independent directors provides new financial skills and knowledge, allowing for a more rigorous and critical evaluation of credit requests. Their independence from internal and external pressures helps in the quick identification of risky loan portfolios and the recommendation of necessary adjustments to prevent potential losses. Moreover, their diversified expertise and independence ensure thorough oversight and control of decisions, contributing to valuable advice and effective strategic guidance. These results corroborate those of Switzer and Jun (2013) and Pathan (2009). Therefore, we accept hypothesis H2.

CEO duality has a positive and significant impact on NPLs. Specifically, a 1% increase in CEO duality leads to a 0.6% increase in NPLs in the MENA region. Likewise, a 1% increase in the DUAL variable results in a 1.6% increase in NPLs for banks in the GCC. However, no significant relationship is found between CEO duality and NPLs in NGCC banks. The concentration of power in the hands of a single person can reduce decision-making transparency, as it may lead to prioritizing personal interests over the financial institution's prudence. This can cause conflicts of interest, weakening the board’s ability to independently oversee the executive. Moreover, combining the CEO and chair positions may limit the diversity of viewpoints, undermine internal controls, and diminish independent monitoring. As a result, the decision-making process becomes less susceptible to critique and review, potentially concealing issues and heightening credit risk. These findings align with the studies of Abid et al. (2021) and Lu and Boateng (2018). Hence, we accept the hypothesis H3.

The results regarding gender diversity reveal a negative and significant impact at the 1% level for banks in the MENA, GCC, and NGCC regions. A 1% increase in the number of women on a board leads to a notable reduction in Non-Performing Loans (NPLs) by 0.2% for the MENA region, 0.01% for GCC countries, and 0.3% for NGCC banks. The presence of women on boards promotes more balanced decision-making, as women are often more detail-oriented and adopt a more cautious financial approach. Additionally, they bring valuable skills such as empathy, innovation, improved communication, and enhanced relationships with other board members. Female directors also contribute to the diversity of perspectives within credit teams, allowing for better understanding and a more balanced evaluation of credit applications. Furthermore, they tend to foster an inclusive organizational culture, leading to more thorough risk assessments and thereby reducing levels of NPLs. Our findings support those of Kinateder et al. (2021) and Lu and Boateng (2018). Based on these results, we accept the hypothesis H4.

The length of board tenure shows a positive and statistically significant association at 1%. As such, a 1% increase in the board tenure results in an 8.2% increase in the NPLs ratio for banks in the MENA region, 8.7% for GCC banks, and 6.4% for NGCC banks. Extending the board tenure allows board members to build closer and more lasting relationships with a bank's stakeholders, which may influence their decisions regarding loan management and control. As a result, administrators may become less rigorous in applying risk management procedures, thereby weakening loan control and increasing the likelihood of defaults. Moreover, a longer mandate can lead to more subjective and personal decisions, resulting in less stringent management of credit processes. These findings confirm the results of Kinateder et al. (2021) and support our hypothesis H5, which suggests that longer tenure increases NPL levels.

Table 7.

The Impact of Board Characteristics on NPLs in the GCC countries.

***, ** and * Level of significance at 1%, 5% and 10%.

Regarding director compensation, the results show a statistically significant negative relationship between the compensation variable (COMP) and NPLs at the 5% level for GCC countries and at the 10% level for NGCC banks. However, compensation has no significant impact on NPLs for banks in the MENA region. A higher performance-based compensation can incentivize board members to engage more actively in the prudent management of credit risk. Indeed, substantial compensation encourages board members to implement rigorous oversight policies and establish robust risk management processes. Moreover, higher compensation improves the financial position of directors and may also reduce conflicts of interest. As a result, it would be less likely for directors to take excessive risks or adopt strategies that might generate quick profits but jeopardize long-term financial stability. Our findings contradict those of Lu and Boateng (2018) and Rose (2017). Therefore, we reject hypothesis H6.

The size of the bank significantly reduces NPLs at the 1% level in the MENA region, GCC countries, and NGCC countries. Larger banks are generally more diversified, and equipped with advanced technologies, skilled human resources, and expertise in risk management, which enables them to better control credit risk. These results are consistent with those of Jenkins et al. (2021).

Moreover, capital has a negative and significant effect on NPLs in the MENA region, GCC countries, and NGCC countries. This result supports the findings of Naili and Lahrichi (2022), who observed that banks with excess capital tend to avoid NPLs in order to protect their capital reserves, which are usually mobilized in the event of significant risks.

Bank performance shows a negative and significant relationship with NPLs in the MENA region, GCC countries (M5), and NGCC countries (M3 and M5). This indicates that high-performing banks are less likely to grant risky loans. This result confirms the findings from the previous chapter and aligns with the studies by Jenkins et al. (2021) and Bashir et al. (2017).

Regarding the effect of banking diversification, the results reveal a negative and significant relationship at the 1% level across all three groups: MENA, GCC, and NGCC countries. This suggests that diversified banks focus more on maximizing non-interest income rather than taking on excessive risk. This finding is consistent with the work of Ghosh (2017).

Table 8.

The Impact of Board Characteristics on NPLs in the NGCC countries.

***, ** and * Level of significance at 1%, 5% and 10%.

The variable CONC shows a positive and significant impact at the 1% level on NPLs for banks in the MENA region, GCC, and NGCC countries. Banks with higher market concentration receive a greater number of credit applications, making them more flexible in managing these requests. On the other hand, concentration has a negative and significant effect at the 1% level (M6) on NPLs for GCC banks. This result is consistent with the findings of Hakimi and Khemiri (2024), who observed that a more concentrated banking sector is associated with lower levels of non-performing loans.

Regarding macroeconomic conditions, GDP growth and inflation rates have statistically significant negative effects at the 1% level on NPLs in the MENA region, GCC countries, and NGCC countries. A favorable macroeconomic environment, characterized by strong growth and low inflation, enhances borrowers' ability to repay their loans by improving their financial situation and increasing their solvency. These results align with the conclusions of Jabbouri et al. (2022), who found that improved economic conditions are associated with a decrease in credit risk.

The results showed that all the board characteristics chosen significantly influenced the volume of NPLs. As a result, we will construct a board index (CA_index) that incorporates key characteristics such as board size, duality, board independence, gender diversity, director compensation, and board tenure. This index will allow us to better understand the combined impact of these characteristics on credit risk. The results are presented in the table below. Moreover, the board of directors index (CA_index) has a negative and statistically significant impact on NPLs. In the MENA region, GCC countries, and NGCC countries, a 1% increase in the index coefficient reduces NPLs levels by 13.6%, 9.4%, and 13%, respectively. These results suggest that banks with effective board characteristics are more likely to reduce their NPL levels. Additionally, a robust board structure enables board members to enhance their skills and perspectives, thereby enriching decision-making and improving oversight of management processes. A higher quality of board members is better equipped to develop risk management strategies that are responsive to economic changes. Furthermore, such a board promotes transparency and responsibility within the organization, facilitating the timely detection and resolution of potential credit issues. Our findings contradict the conclusions of Srairi et al. (2021), who argued that Islamic banks with strong governance are associated with higher risk-taking.

Table 9.

The Impact of Board Characteristics index on NPLs.

| MENA | GCC | NGCC | ||||

| Coef. | Z | Coef. | Z | Coef. | Z | |

| NPLs (-1) | 0.156 | 313.48*** | 0.151 | 11.28*** | 0.104 | 2.28** |

| SIZE | -0.064 | -47.50*** | -0.028 | -15.77*** | -0.029 | -3.03*** |

| CAP | -0.017 | -8.75*** | -0.198 | -12.12*** | -0.017 | -1.76* |

| ROA | -0.787 | -12.53*** | -0.074 | -1.75* | -0.781 | -2.26** |

| LTD | -0.002 | 1.82 | -0.001 | -0.68 | -0.00001 | -0.01 |

| NII | -0.002 | -67.39*** | -0.001 | -27.27*** | -0.003 | -5.84*** |

| CONC | 0.002 | 43.96** | 0.003 | 32.00*** | 0.002 | 4.37*** |

| GDP | -0.001 | -39.08*** | -0.001 | -16.56*** | -0.003 | -4.49*** |

| INF | -0.000 | -5.09*** | -0.001 | -16.82*** | -0.000 | -2.07** |

| CA_index | -0.136 | -19.67*** | -0.094 | -8.20*** | -0.130 | -3.82*** |

| _cons | 1.476 | 40.63*** | 0.495 | 10.21*** | 0.709 | 3.21*** |

| AR(1) | -1.1312 | -1.1043 | -1.9127 | |||

| Prob | 0.2580 | 0.2694 | 0.0558 | |||

| AR(2) | -1.6633 | -1.3959 | -1.3593 | |||

| Prob | 0.0962 | 0.1627 | 0.1741 | |||

| Sargan test | 63.481 | 47.206 | 17.022 | |||

| Prob | 0.8467 | 0.9961 | 1.0000 | |||

| N | 682 | 436 | 292 | |||

***, ** and * indicate the 1%, 5% and 10% significance lelvels.

5. Conclusions

This research significantly contributes to the debate on bank credit risk, particularly the relationship between board characteristics and credit risk. We used data from 70 banks across 12 countries in the MENA region over the period 2010–2022 and applied the SGMM. Furthermore, we performed a comparative analysis between the sub-regions of MENA: GCC countries and NGCC countries.

The empirical results revealed that in the MENA region and GCC countries, a larger board size, CEO duality, and longer tenure significantly increase the volume of NPLs. Conversely, an increase in the number of independent directors, the proportion of female directors, and board compensation significantly reduce the level of NPLs. Regarding the NGCC countries, board size and tenure are positively associated with higher NPLs. In contrast, board independence, gender diversity, and compensation significantly lower the NPLs ratio. Additionally, the findings show that as board quality improves, the NPL ratio decreases across all three regions: MENA, GCC, and NGCC. These results allow us to conclude that an effective board of directors is a key factor in mitigating credit risk.

This study presents several implications, highlighting the necessity to prioritize the effectiveness of boards, as well as their essential role in the control and supervision of banking activities. Policymakers, regulators, and financial institutions should focus on fostering board independence and diversity, as these factors can significantly mitigate credit risk. Indeed, adopting sound governance practices helps reduce insolvency risk and address the issue of information asymmetry. Consequently, Effective governance strengthens the banking sector's stability, enhancing financial resilience.

While the results of this study are interesting, it has some limitations. First, we were unable to examine this relationship across all countries in the MENA region due to a lack of available data. Second, including additional board characteristics, such as board culture and specific features of the audit committee, could have enriched our study. As a future research, a comparative analysis based on the level of corruption or board size could provide valuable insights and open new perspectives for future research. Furthermore, it is crucial to examine whether a threshold effect exists in the relationship between board characteristics and non-performing loans (NPLs) in the MENA region.

Author Contributions

Conceptualization, S.S. and A.H.; Methodology, S.S. and A.H.; Software, H.S.; Validation, S.S. and A.H.; and H.S.; Formal Analysis, H.A.; Investigation, S.S.; Resources, H.S.; Data Curation, H.S.; Writing – Original Draft Preparation, S.S. A.H. and H.S.; Writing – Review & Editing, S.S. A.H. and H.S. Visualization, H.S.; Supervision, A.H.; Project Administration, A.H.; Funding Acquisition, H.S.

Funding

This work was supported and funded by the Deanship of Scientific Research at Imam Mohammad Ibn Saud Islamic University (IMSIU) (grant number IMSIU-DDRSP2504).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Derived data supporting the findings of this study are available from the corresponding author on request.

Conflicts of Interest

The authors have no conflicts of interest to declare that are relevant to the content of this article.

References

- Abid, A.; Gull, A.A.; Hussain, N.; Nguyen, D.K. Risk governance and bank risk-taking behavior: Evidence from Asian banks. J. Int. Financial Mark. Institutions Money 2021, 75, 101466. https://doi.org/10.1016/j.intfin.2021.101466.

- Adusei, M.; Sarpong-Danquah, B. Institutional quality and the capital structure of microfinance institutions: the moderating role of board gender diversity. J. Institutional Econ. 2021, 17, 641–661, https://doi.org/10.1017/s1744137421000023.

- Alnabulsi, K.; Kozarević, E.; Hakimi, A. Assessing the determinants of non-performing loans under financial crisis and health crisis: evidence from the MENA banks. Cogent Econ. Finance 2022, 10, 2124665. https://doi.org/10.1080/23322039.2022.2124665.

- Andres, P. & Vallelado. E. (2008) Corporate governance in banking: The role of the board of directors. Journal of Banking and Finance, vol. 32, pp. 2570–2580.

- Bashir, U.; Yu, Y.; Hussain, M.; Wang, X.; Ali, A. Do banking system transparency and competition affect nonperforming loans in the Chinese banking sector?. Appl. Econ. Lett. 2017, 24, 1519–1525, https://doi.org/10.1080/13504851.2017.1305082.

- Beasley, M.S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review, 71(4), 443–465.

- Bebchuk, L.A., & Spamann, H. (2009). Regulating Bankers’ Pay, Harvard Law and Economics Discussion Paper 641.

- Beltratti, A. & Stulz, R. M. (2009). Why Did Some Banks Perform Better during the Credit Crisis? A Cross- Country Study of the Impact of Governance and Regulation. Charles A Dice Center Working Paper No. 2009-12, http://dx.doi.org/10.2139/ssrn.1433502.

- Berger, A.N.; Kick, T.; Schaeck, K. Executive board composition and bank risk taking. J. Corp. Finance 2014, 28, 48–65, https://doi.org/10.1016/j.jcorpfin.2013.11.006.

- Boussaada, R, Hakimi, A., & Karmani, M. (2020). Is there a threshold effect in the liquidity risk–nonperforming loans relationship? A PSTR approach for MENA banks. International Journal of Finance & Economics, 1‑13. https://doi.org/DOI: 10.1002/ijfe.2248.

- Boussaada, R., & Labaronne, D. (2015). Ownership Concentration, Board Structure and Credit Risk: The Case of MENA Banks. Bankers, Markets & Investors.

- Boussaada, R., Ammari, A., & Ben arfa, N. (2018). Board characteristics and MENA banks’ credit risk : A fuzzy-set analysis. Economics Bulletin, 38, 2284-2303.

- Brewer, E., Hunter, W.C., & Jackson, W., E. (2004). Investment opportunity, product mix, and the relationship between bank CEO compensation and risk-taking. Working Paper n°36, Federal Reserve Bank of Atlanta.

- Byrd, J.; Cooperman, E.S.; Wolfe, G.A. Director tenure and the compensation of bank CEOs. Manag. Finance 2010, 36, 86–102, https://doi.org/10.1108/03074351011014523.

- Carter, C.B. & Lorsch, J. (2004). Back to the drawing Board: Designing corporate boards for a complex world. Harvard Business School Press.

- Chaibi, H.; Ftiti, Z. Credit risk determinants: Evidence from a cross-country study. Res. Int. Bus. Finance 2015, 33, 1–16, https://doi.org/10.1016/j.ribaf.2014.06.001.

- Chen, C.R.; Steiner, T.L.; Whyte, A.M. Does stock option-based executive compensation induce risk-taking? An analysis of the banking industry. J. Bank. Finance 2006, 30, 915–945, https://doi.org/10.1016/j.jbankfin.2005.06.004.

- Daily, C.M. & Dalton, D.R. (1994). Corporate governance and the bankrupt firm: An empirical assessment. Strategic Management Journal, Wiley Blackwell, vol. 15(8), pages 643-654, October.

- DeYoung, R.; Torna, G. Nontraditional banking activities and bank failures during the financial crisis. J. Financial Intermediation 2013, 22, 397–421, https://doi.org/10.1016/j.jfi.2013.01.001.

- Djebali, N.; Zaghdoudi, K. Corporate Governance in Banks and its Impact on Credit and Liquidity Risks: Case of Tunisian Banks. Asian J. Finance Account. 2019, 11, 148–168, https://doi.org/10.5296/ajfa.v11i2.13929.

- Doğan, B.; Ekşi, İ.H. The effect of board of directors characteristics on risk and bank performance: Evidence from Turkey. Econ. Bus. Rev. 2020, 6, 88–104, https://doi.org/10.18559/ebr.2020.3.5.

- Faccio, M., Marchica, M.T., & Mura, R. (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance, 39, 193-209.

- Fernandes, J.G.; Olsson, I.A.S.; de Castro, A.C.V. Do aversive-based training methods actually compromise dog welfare?: A literature review. Appl. Anim. Behav. Sci. 2017, 196, 1–12, https://doi.org/10.1016/j.applanim.2017.07.001.

- Ghosh, A. Sector-specific analysis of non-performing loans in the US banking system and their macroeconomic impact. J. Econ. Bus. 2017, 93, 29–45, https://doi.org/10.1016/j.jeconbus.2017.06.002.

- Golden, B.R.; Zajac, E.J. When will boards influence strategy? inclination × power = strategic change. Strat. Manag. J. 2001, 22, 1087–1111, https://doi.org/10.1002/smj.202.

- Golliard, J.T. & Poder, L. (2007). Optimal Capital Structure of capital in the banking sector.

- Hakimi, A., & Khemiri, M. A. (2024). Bank diversification and non-performing loans in the MENA region: The moderating role of financial inclusion. In Elsevier eBooks. https://doi.org/10.1016/b978-0-44-313776-1.00204-x.

- Hakimi, A.; Boussaada, R.; Karmani, M. Is the relationship between corruption, government stability and non-performing loans non-linear? A threshold analysis for the MENA region. Int. J. Finance Econ. 2020, 27, 4383–4398, https://doi.org/10.1002/ijfe.2377.

- Hakimi, A.; Boussaada, R.; Karmani, M. Financial inclusion and non-performing loans in MENA region: the moderating role of board characteristics. Appl. Econ. 2023, 56, 2900–2914, https://doi.org/10.1080/00036846.2023.2203456.

- Hassan, M.K.; Khan, A.; Paltrinieri, A. Liquidity risk, credit risk and stability in Islamic and conventional banks. Res. Int. Bus. Finance 2019, 48, 17–31, https://doi.org/10.1016/j.ribaf.2018.10.006.

- Huang, S.; Hilary, G. Zombie Board: Board Tenure and Firm Performance. J. Account. Res. 2018, 56, 1285–1329, https://doi.org/10.1111/1475-679x.12209.

- Jabbouri, I., Naili, M., Almustafa, H., & Jabbouri, R. (2022). Does ownership concentration affect banks’ credit risk? Evidence from MENA emerging markets. Bulletin of Economic Research, 1‑22. https://doi.org/DOI: 10.1111/boer.12345.

- Jenkins, H.; Alshareef, E.; Mohamad, A. The impact of corruption on commercial banks' credit risk: Evidence from a panel quantile regression. Int. J. Finance Econ. 2021, 28, 1364–1375, https://doi.org/10.1002/ijfe.2481.

- Jensen, C, M. (1993). The Modern Industrial Revolution, Exit, and the Failure of Internal Control Systems. In American Finance Association, The Journal of Finance: Vol. XLVIII (Issue 3, pp. 831–833).

- Jensen, C, M. (1993). The Modern Industrial Revolution, Exit, and the Failure of Internal Control Systems. In American Finance Association, The Journal of Finance: Vol. XLVIII (Issue 3, pp. 831–833).

- John, K., De Masi, S., & Paci, A. (2016). Corporate Governance in Banks. Corporate Governance: An International Review, (pp. 303–321), https://doi.org/10.1111/corg.12161.

- John, K., De Masi, S., & Paci, A. (2016). Corporate Governance in Banks. Corporate Governance: An International Review, (pp. 303–321), https://doi.org/10.1111/corg.12161.

- Karadima, M.; Louri, H. Non-performing loans in the euro area: Does bank market power matter? Int. Rev. Financial Anal. 2020, 72, 101593, https://doi.org/10.1016/j.irfa.2020.101593.

- Karismaulia, A., Ratnawati, K., & Wijayanti, R. (2023). The Effect of Macroeconomic and Bank-Specific Variables on Non-Performing Loans with Bank Size as A Moderating Variable. The International Journal of Social Sciences World, 5(1), 381-393.https://doi.org/10.5281/zenodo.8056076.

- Kervin, J.B. Kervin, J.B. (1992). Methods for business research. Harper Collins, New York.

- Kinateder, H.; Choudhury, T.; Zaman, R.; Scagnelli, S.D.; Sohel, N. Does boardroom gender diversity decrease credit risk in the financial sector? Worldwide evidence. J. Int. Financial Mark. Institutions Money 2021, 73, https://doi.org/10.1016/j.intfin.2021.101347.

- Kramer, V.W., Konrad, A.M., & Erkut, S. (2006). Critical mass on corporate boards: Why three or more women enhance governance. Wellesley Center for Women, Report No. WCW 11.

- Kumar, R. R., Stauvermann, J. P., Patel, A., & Prasad, S. S. (2018). Determinants of non-performing loans in small developing economies: A case of Fiji’s banking sector. Accounting Research Journal, 1‑28. https://doi.org/10.1108/ARJ-06-2015-0077.

- Lu, J.; Boateng, A. Board composition, monitoring and credit risk: evidence from the UK banking industry. Rev. Quant. Finance Account. 2017, 51, 1107–1128, https://doi.org/10.1007/s11156-017-0698-x.

- Lückerath-Rovers, M. Women on boards and firm performance. J. Manag. Gov. 2013, 17, 491–509, https://doi.org/10.1007/s10997-011-9186-1.

- Manz, F. Determinants of non-performing loans: What do we know? A systematic review and avenues for future research. Manag. Rev. Q. 2019, 69, 351–389, https://doi.org/10.1007/s11301-019-00156-7.

- Massi, M. L. G. (2016). Effectiveness Of Best Practices in Corporate Governance in Combating Corruption. Revista Científica Hermes, 15–15, 122–141. https://doi.org/10.21710/rch.v15i0.268.

- Mohsni, S.; Otchere, I.; Shahriar, S. Board gender diversity, firm performance and risk-taking in developing countries: The moderating effect of culture. J. Int. Financial Mark. Institutions Money 2021, 73, https://doi.org/10.1016/j.intfin.2021.101360.

- Muchemwa, M.R.; Padia, N.; Callaghan, C.W. Board composition, board size and financial performance of Johannesburg stock exchange companies. South Afr. J. Econ. Manag. Sci. 2016, 19, 497–513, https://doi.org/10.4102/sajems.v19i4.1342.

- Naili, M.; Lahrichi, Y. The determinants of banks' credit risk: Review of the literature and future research agenda. Int. J. Finance Econ. 2020, 27, 334–360, https://doi.org/10.1002/ijfe.2156.

- Olaoye, F.O.; Adewumi, A.A. Corporate Governance and the Earnings Quality of Nigerian Firms. Int. J. Financial Res. 2020, 11, 161, https://doi.org/10.5430/ijfr.v11n5p161.

- Park, J. Corruption, soundness of the banking sector, and economic growth: A cross-country study. J. Int. Money Finance 2012, 31, 907–929, https://doi.org/10.1016/j.jimonfin.2011.07.007.

- Pathan, S. Strong boards, CEO power and bank risk-taking. J. Bank. Finance 2009, 33, 1340–1350, https://doi.org/10.1016/j.jbankfin.2009.02.001.

- Ploix. H. (2003). Bâle II et le capital-investissement. Revue d'Économie Financière, vol. 73(4), pages 189-200.

- Polat, A. Macroeconomic Determinants of Non-Performing Loans: Case of Turkey and Saudi Arabia. J. Bus. Res. - Turk 2018, 10, 693–709, https://doi.org/10.20491/isarder.2018.495.

- Post, C., Rahman. N., &Rubow. E. (2011). Diversity in the Composition of Board of Directors and Environmental Corporate Social Responsibility (ECSR), Business & Society 49 (forthcoming).

- Rose, C. The relationship between corporate governance characteristics and credit risk exposure in banks: implications for financial regulation. Eur. J. Law Econ. 2016, 43, 167–194, https://doi.org/10.1007/s10657-016-9535-2.

- Salas, V. & Saurina, J. (2003). Deregulation, market power and risk behaviour in Spanish banks. European Economic Review, 47, 1061–1075.

- Saliba, C.; Farmanesh, P.; Athari, S.A. Does country risk impact the banking sectors’ non-performing loans? Evidence from BRICS emerging economies. Financial Innov. 2023, 9, 1–30, https://doi.org/10.1186/s40854-023-00494-2.

- Sallemi, M.; Ben Hamad, S.; Ellili, N.O.D. Impact of board of directors on insolvency risk: which role of the corruption control? Evidence from OECD banks. Rev. Manag. Sci. 2022, 17, 2831–2868, https://doi.org/10.1007/s11846-022-00605-w.

- Setiawan, R.; Khoirotunnisa, F. The Impact of Board Gender Diversity on Bank Credit Risk. Int. J. Bus. Rev. (The Jobs Rev. 2020, 3, 47–52, https://doi.org/10.17509/tjr.v3i2.28158.

- Srairi, S.; Bourkhis, K.; Houcine, A. Does bank governance affect risk and efficiency? Evidence from Islamic banks in GCC countries. Int. J. Islam. Middle East. Finance Manag. 2021, 15, 644–663, https://doi.org/10.1108/imefm-05-2020-0206.

- Sumner, S., & Webb, E., (2005). Does corporate governance determine bank loan portfolio choice ? Journal of Academy of Business and Economics, vol. 5, issue 2.

- Switzer, L.N.; Wang, J. Default Risk Estimation, Bank Credit Risk, and Corporate Governance. Financial Mark. Institutions Instruments 2013, 22, 91–112, https://doi.org/10.1111/fmii.12005.

- Tarchouna, A.; Jarraya, B.; Bouri, A. Do board characteristics and ownership structure matter for bank non-performing loans? Empirical evidence from US commercial banks. J. Manag. Gov. 2021, 26, 479–518, https://doi.org/10.1007/s10997-020-09558-2.

- Vafeas, N. Length of Board Tenure and Outside Director Independence. J. Bus. Finance Account. 2003, 30, 1043–1064. [Google Scholar] [CrossRef]

Figure 1.

The effect of board characteristics on NPLs.

Figure 2.

The effect of board index on NPLs.

Table 1.

Sample distribution and composition.

| The Middle East and North Africa (MENA) countries. | |||||

| GCC countries | NGCC countries | ||||

| Countries | N | % | Countries | N | % |

|

1. Saudi Arabia 2. Bahrain 3. United Arab Emirates 4. Kuwait 5. Qatar 6. Oman |

10 2 11 7 7 5 |

14.28% 2.86% 15.71% 10% 10% 7.14% |

7. Egypt 8. Jordan 9. Lebanon 10. Morocco 11. Tunisia 12. Turkey |

3 4 1 2 10 8 |

4.28% 5.71% 1.43% 2.86 14.28% 11.43% |

| Total | 42 | 60% | Total | 28 | 40% |

Table 2.

Definition and measurement of variables.

| Variables | Definitions | Measures |

|---|---|---|

| Dependent variable | ||

| NPLs | Non-performing loans | Non-performing loans to total loans ratio (%). |

| Board characteristics | ||

| TCA | Board size | Total number of directors within a Board of Directors |

| IND | Independent directors | Proportion of independent directors on a Board of Directors |

| DUAL | Duality | Binary variable takes 1 if the CEO is the Chairman of the Board, 0 otherwise. |

| BGD | Gender diversity | Women on the Board as a percentage of the total number of directors. |

| MAND | Board Tenure | The term length of a Board of Directors. |

| COMP | Compensation | Total compensation of directors in US dollars relative to total assets (%). |

| CA_INDEX | Board characteristics index | Composite index of board characteristics based on the PCA method, ranging from 0 to 1, with '1' indicating an effective board and '0' otherwise. |

| Control variables | ||

| SIZE | Bank size | The natural logarithm of the total assets of each bank |

| CAP | Capital | Equity to total assets (%). |

| LTD | Liquidity risk | Loan-to-deposit ratio, (%). |

| ROA | Bank performance | Return on assets (ROA), (%) |

| NII | Bank diversification | Non-interest income as a percentage of total assets. |

| CONC | Concentration | The share of the five biggest banks' assets to all banks' assets (%). |

| GDP | Economic growth | Annual GDP growth rate, (%) |

| INF | Inflation rate | Annual growth of CPI, (%) |

Table 3.

Descriptive statistics.

| Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|

| NPLs | 7.3 | 1.8 | 4.01 | 261 |

| TCA | 10.52 | 1.95 | 5.02 | 19 |

| IND | 28.81 | 23.48 | 13.1 | 100 |

| DG | 6.62 | 8.41 | 1.4 | 40 |

| MAND | 3.10 | 0.59 | 1 | 6 |

| COMP | 0.01 | 0.03 | 0 | 0.18 |

| SIZE | 23.74 | 1.22 | 20.94 | 26.51 |

| CAP | 16.7 | 4.6 | 3.5 | 42.9 |

| ROA | 1.4 | 0.8 | -3.8 | 6.3 |

| LTD | 98.76 | 5.84 | 1.4 | 162 |

| NII | 38.44 | 17.26 | 9.55 | 96 |

| CONC | 82.20 | 13.36 | 56.04 | 100 |

| GDP | 3.12 | 4.07 | -2.4 | 19.59 |

| INF | 4.83 | 10.96 | -3.75 | 29.5 |

Table 4.

Descriptive statistics for the dichotomous variable.

| DUAL | Frequency | Percentage |

|---|---|---|

| 0 | 599 | 87.79% |

| 1 | 83 | 12.21% |

| Total | 682 | 100% |

Table 5.

Correlation matrix.

| NPLs | TCA | IND | DUAL | DG | MAND | COMP | SIZE | CAP | ROA | LTD | NII | CONC | GDP | INF | |

| NPLs | 1.0000 | ||||||||||||||

| TCA | 0.2801* | 1.0000 | |||||||||||||

| (0.0000) | |||||||||||||||

| IND | -0.1264* | -0.0729 | 1.0000 | ||||||||||||

| (0.0023) | (0.0790) | ||||||||||||||

| DUAL | 0.0562 | 0.1680* | -0.0999* | 1.0000 | |||||||||||

| (0.1765) | (0.0000) | (0.0147) | |||||||||||||

| DG | 0.2524* | 0.2375* | -0.1397* | -0.0833* | 1.0000 | ||||||||||

| (0.0000) | (0.0000) | (0.0007) | (0.0428) | ||||||||||||

| MAND | -0.0235 | 0.0537 | -0.1279* | 0.3443* | -0.0853* | 1.0000 | |||||||||

| (0.5765) | (0.2014) | (0.0020) | (0.0000) | (0.0407) | |||||||||||

| COMP | 0.1480* | -0.0474 | -0.2020* | 0.1559* | 0.3829* | -0.0748 | 1.0000 | ||||||||

| (0.0111) | (0.4169) | (0.0005) | (0.0072) | (0.0000) | (0.2066) | ||||||||||

| SIZE | -0.1867* | -0.0606 | 0.0904* | 0.1377* | -0.3643* | 0.0912* | -0.5102 | 1.0000 | |||||||

| (0.0000) | (0.1662) | (0.0376) | (0.0015) | (0.0000) | (0.0380) | (0.0000) | |||||||||

| CAP | -0.1057* | -0.0414 | 0.1254* | 0.0712 | -0.1474* | 0.2518* | -0.3640* | 0.1943* | 1.0000 | ||||||

| (0.0023) | (0.3213) | (0.0024) | (0.0843) | (0.0004) | (0.0000) | (0.0000) | (0.0000 | ||||||||

| ROA | -0.1725* | -0.0358 | -0.0224 | -0.0530 | 0.0695 | -0.0307 | 0.1635* | 0.1648*) | 0.0823* | 1.0000 | |||||

| (0.0000) | (0.3876) | (0.5854) | (0.1956) | (0.0910) | (0.4591) | (0.0048) | (0.0000 | (0.0149) | |||||||

| LTD | -0.0520 | 0.0380 | -0.0515 | -0.0430 | 0.1046* | -0.0191 | -0.0184 | -0.0411 | 0.0197 | 0.0950* | 1.0000 | ||||

| (0.1298) | (0.3617) | (0.2136) | (0.2980) | (0.0116) | (0.6478) | (0.7524) | (0.2804) | (0.5680) | (0.0050) | ||||||

| NII | -0.0016 | 0.0723 | -0.0744 | 0.0164 | -0.1013* | 0.3225* | -0.1536* | 0.3106* | 0.1425* | -0.0791* | 0.0853* | 1.0000 | |||

| (0.9643) | (0.0814) | (0.0699) | (0.6902) | (0.0138) | (0.0000) | (0.0083) | (0.0000) | (0.0001) | (0.0256) | (0.0176) | |||||

| CONC | -0.2255* | -0.3393* | 0.2763* | -0.1467* | -0.4319* | 0.0805 | -0.5140* | 0.2194* | 0.2336* | -0.0099 | -0.1181* | -0.0298 | 1.0000 | ||

| (0.0000) | (0.0000) | (0.0000) | (0.0004) | (0.0000) | (0.0538) | (0.0000) | (0.0000) | (0.0000) | (0.7689) | (0.0006) | (0.4088) | ||||

| GDP | -0.0666 | 0.1410* | -0.0188 | 0.0578 | 0.0442 | 0.0737 | - 0.0813 | 0.0757* | 0.0386 | 0.3077* | 0.0578 | 0.1127* | -0.0360 | 1.0000 | |

| (0.0521) | (0.0006) | (0.6469) | (0.1586) | (0.2834) | (0.0758) | (0.1632) | (0.0462) | (0.2547) | (0.0000) | (0.0885) | (0.0014) | (0.2879) | |||

| INF | 0.0638 | 0.1093* | 0.0283 | 0.0279 | 0.1209* | -0.2337* | 0.3666* | 0.0022 | -0.0548 | 0.1216 | 0.0732* | -0.0661 | -0.2669* | 0.0281 | 1.0000 |

| (0.0625) | (0.0082) | (0.4898) | (0.4954) | (0.0032) | (0.0000) | (0.0000) | (0.9533) | (0.1054) | (0.0002) | (0.0309) | (0.0622) | (0.0000) | (0.3981) |

*indicates the level of significance at 5%.

Table 6.

The Impact of Board Characteristics on NPLs in the MENA Region.

***, ** and * Level of significance at 1%, 5% and 10%.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.