Submitted:

10 January 2025

Posted:

10 January 2025

You are already at the latest version

Abstract

Online banking services was highlighted as a key factor enhancing customer satisfaction and sustainable development. However, the mediating role of customer experience in the relationship between online banking service clues and customer satisfaction has received minimal attention. This study belongs to Haeckel online banking theory. Haeckel’s model in online banking fosters a more dynamic, customer-centered experience by emphasizing real-time responsiveness and adaptability as a tool of sustainable development. To determine sample convenience sampling technique has been used. Total participants to the study are 400 individual and corporate online banking user customers in North Cyprus. For statistical analyses Structural Equation Modelling (SEM) has been used. (SEM). The results showed that functional service clues positively influenced satisfaction only among individual customers, while mechanic clues positively impacted satisfaction across both customer types as a result sustainable development. In contrast, humanic clues did not affect either group. Online service clues enhanced the overall customer experience, which in turn positively impacted customer satisfaction which is the corporate’s social responsibility. However, customer experience did not mediate the relationship between online banking service clues and satisfaction. Additionally, demographic characteristics moderated this relationship. These findings underscore the importance of online banking service cues in enhancing customer satisfaction and contribute valuable insights to the digital marketing literature on customer experience in the banking sector as a sustainable development.

Keywords:

Sustainable development

; Haeckel’s Model

; Online Banking

; Corporate Social Responsibilities

; Service Clues

; Functional Clues

; Humanic Clues

; Mechanic Clues

; Customer Experience

; Customer Satisfaction

1. Introduction

Advancements in technology have accelerated digitalization, driving innovation across various sectors which ensures sustainable development [1]. In banking, this shift has enabled the rise of online banking, allowing customers to access a wide range of banking services virtually [2,3]. With online banking, customers can effortlessly transfer funds within minutes across geographical boundaries, track their finances, invest, exchange currencies, pay bills, communicate with the bank, and complete numerous other essential transactions—all without the need for a physical bank visit [4,5]. Banking applications and websites have become the new platforms for conducting transactions over the internet, offering convenient access to a wide range of banking services [6]. However, internet-based transactions also increase the risk of exposing confidential information, which, if compromised, can be highly damaging—not only to the company’s reputation and growth but also in terms of financial loss and eroded customer trust. This shift has brought changes in service delivery, among other areas. This has become each corporate’s social responsibility to adapt their services accordingly. However, certain aspects, such as ensuring customer satisfaction, remain unchanged. In fact, given the potential challenges in using technology, it is more critical than ever for banks to continually strive to enhance customer satisfaction to retain and attract customers, as it is their responsibility. The demand for online services has grown due to the convenience they offer [2] and Banks that offer online services are likely to attract more clientele, making it a key factor that can provide a competitive edge over rivals [7]. A seamless online banking experience can significantly enhance customer satisfaction and provide a competitive advantage [8]. Companies must prioritize the security of customers' funds and information, ensure that their platforms operate smoothly, and provide real-time updates to create an optimal online experience. Consequently, customer experience is crucial in online banking services, enabling banks to attract and retain more customers.

Customer experience is an integral part of using any product or service [9]. It plays a vital role in enhancing customer satisfaction, which fosters repeat patronage [10]. In today's competitive landscape, customer satisfaction is essential for businesses to thrive [11]. Companies must innovate to keep pace with developments in this dynamic industry, retaining existing customers while attracting new ones. This focus on customer experience also strengthens their reputation and brand, positively influencing their growth. Consequently, online banking has enabled banks to expand, offer a diverse range of services, and effectively meet their customers' needs.

Cyprus has experienced increased demand for banking services due to the growth of sectors such as education, real estate, and various service industries to ensure sustainable development [12]. This trend has resulted in a heightened demand for online banking services. Although many people in the country are affiliated with one or two banks, a large majority still prefer conducting their banking transactions in person at branches [13]. Online banking services were introduced in Cyprus in 2004, and there are currently 22 banks operating, as reported by the TRNC Central Bank. Recent studies on online banking in Cyprus have primarily concentrated on profitability [14,15], the effectiveness of public banks compared to private banks [16], the use of online banking [17,18] and the adoption and risks associated with online banking [12,19,20].

However, studies by Alhassany and Faisal [12] and Serener [20] revealed that a substantial number of banking customers in Cyprus prefer traditional banking, visiting branches to access services. This preference is influenced by factors such as perceived risk and a reluctance to adopt new technologies. Therefore, it is crucial to conduct a thorough exploration of online banking and its impact on customer satisfaction. Furthermore, there has been no recent research examining the role of online banking service clues in enhancing both individual and corporate customer satisfaction, particularly considering the mediating role of customer experience and the moderating effects of customer demographics. In their review article, Chauhan et al. [21] explored the applicability of Haeckel’s model to customer experience in India. A similar study was previously conducted by Wasan [22], which focused on traditional banking. However, there has been no research in Cyprus examining customer experience in the context of Haeckel’s model and service clues in online banking. Consequently, the researcher seeks to fill this gap. The primary objective of this study is to investigate the role of online banking service clues in customer satisfaction within the context of Cyprus. In exploring this relationship, the researcher will also assess whether customer experience mediates this connection. Additionally, the study will examine how online banking service cues relate to customer satisfaction among different customer types, specifically individual and corporate customers.

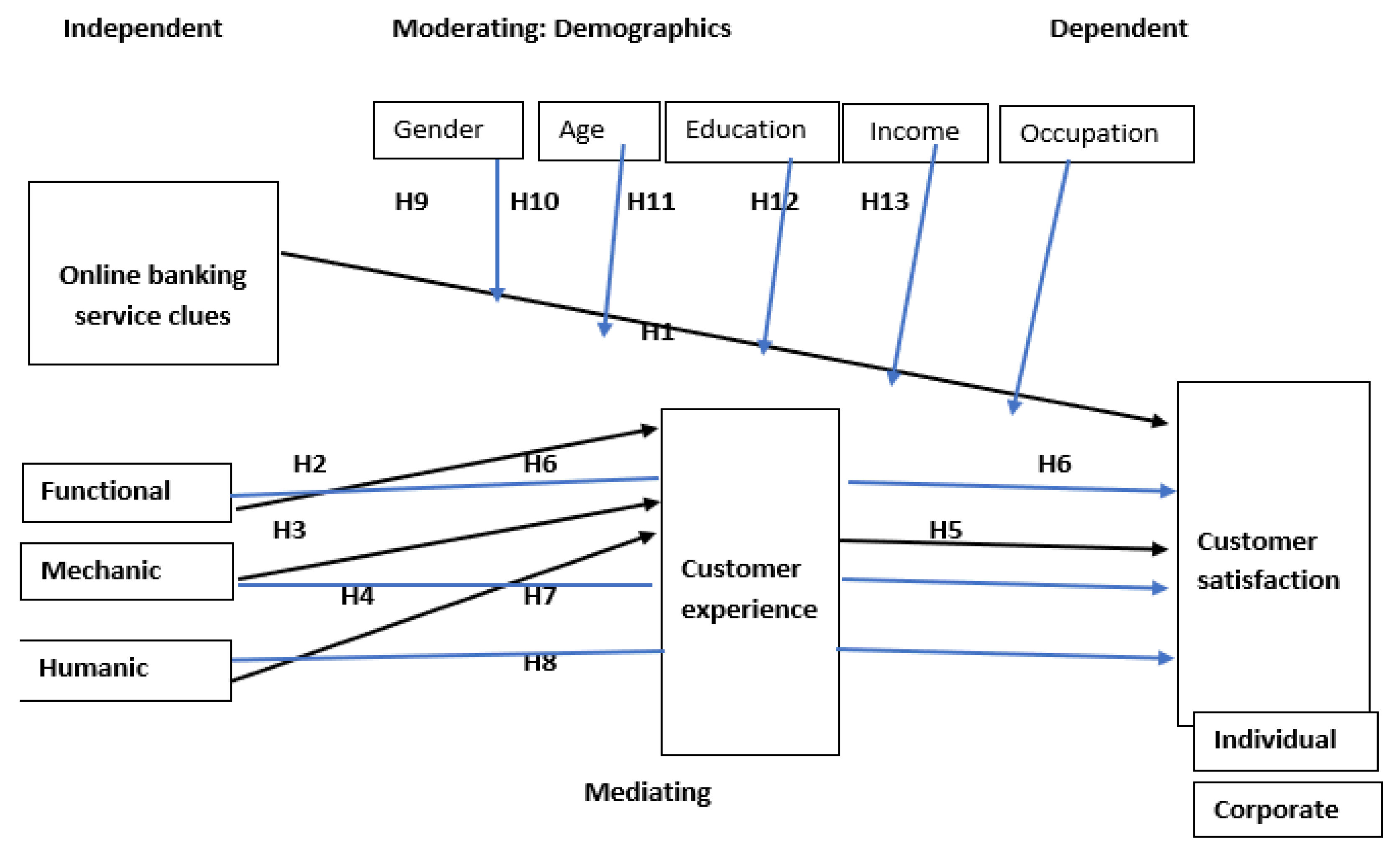

To explore the role of online banking service clues in customer satisfaction in Cyprus, the following research questions are proposed for the study: How do service clues impact customers’ satisfaction with online banking?, What is the relationship between service clues and customer experience in online banking?, How does customer experience relate to customer satisfaction?, Are there differences in customer satisfaction levels based on customer types and demographic characteristics?. In order to answer these question some hypotheses have been proposed.

- H1: Online Banking Service Clues have a direct positive relationship with Customer Satisfaction.

- H2: Online Banking Service Clues (Functional Clues) have a direct positive relationship with Customer Experience.

- H3: Online Banking Service Clues (Mechanic Clues) have a direct positive relationship with Customer Experience.

- H4: Online Banking Service Clues (Humanic Clues) have a direct positive relationship with Customer Experience.

- H5: Customer Experience has a direct positive relationship with Customer Satisfaction.

- H6: Customer Experience mediates the effects of Online Banking Service Clues (Functional Clues) on Customer Satisfaction.

- H7: Customer Experience mediates the effects of Online Banking Service Clues (Mechanic Clues) on Customer Satisfaction.

- H8: Customer Experience mediates the effects of Online Banking Service Clues (Humanic Clues) on Customer Satisfaction.

- H9: Gender has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H10: Age has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H11: Education level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H12: Occupation has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H13: Income level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

The results of this study are expected to significantly influence how banks enhance customer experience and satisfaction by customizing their services to meet customer needs while addressing any existing insecurities to ensure sustainable development. Additionally, this research aims to contribute to the limited literature on the mediating role of customer experience in the relationship between online banking service clues and customer satisfaction as corporate’s social responsibility. The findings will provide banks with valuable insights into online banking service clues and their impact on customer satisfaction. Furthermore, this study will establish a theoretical and conceptual foundation for future research in this area.

This paper is organized into several sections, beginning with the introduction in Section 1. Section 2 presents the literature review, where relevant theoretical and empirical studies are discussed, and hypotheses are formulated. Following this, Section 3 outlines the methodology, detailing how the research was conducted. In Section 4, data analysis is presented, describing and explaining the relationships between the variables under investigation and the results of the hypotheses. Section 5 discusses the research findings, comparing them with previous related studies and the theoretical framework applied. The managerial and theoretical implications of the findings are also highlighted. Finally, the study's limitations are acknowledged, and recommendations for future research are provided.

2. Literature Review

2.1. Customer Experience

Customer experience is extensively defined by Carbone and Haeckel [23], who describe it as the impressions customers form through their interactions with a company's services or products. This experience can vary from person to person and often arises from the gap between actual experiences and customer expectations. Customer expectations play a crucial role in determining customer satisfaction [7]. According to Hussadintorn and Koomsap [24], customer experience encompasses the entire journey, beginning before a customer purchases a service or product and continuing even after the service has been delivered. The authors emphasize that at various stages of this journey, customers rely on their past experiences to shape their future interactions with the brand and its services. Lemon and Verhoef [25] noted that early scholars conceptualized customer experience as encompassing physical, sensory, affective, and socio-identity dimensions. Subsequent research has expanded this framework to include spiritual, social, emotional, and behavioral aspects. Nevertheless, there is a general consensus among scholars that customer experience is inherently complex [26] and encompasses multiple dimensions [27]. As such, management must remain flexible and adapt to the ever-changing demands and market conditions [28].

2.2. Service Clues

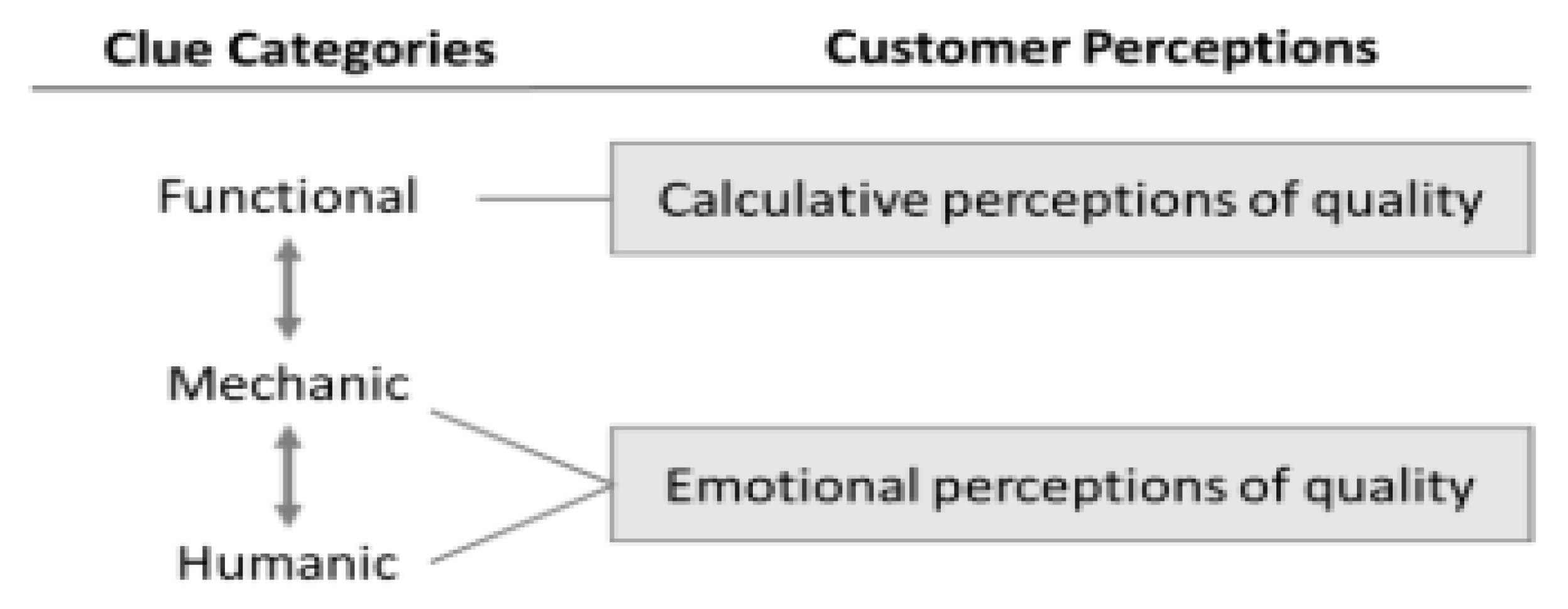

Haeckel et al. [9] emphasized that organizational management must cultivate an awareness and understanding of the signals it communicates to customers to effectively manage the customer experience. These signals allow organizations to proactively anticipate and respond to changes, ultimately enhancing customer satisfaction. The authors categorize these signals into functional and emotional clues (humanic and mechanic), as illustrated in Figure 1 below.

According to Hussadintorn and Koomsap [24], service clues are classified into three categories: functional, mechanic, and humanic. Functional clues pertain to rational thinking, mechanic clues relate to the service environment, and humanic clues focus on behavioral aspects. Both mechanic and humanic clues are grounded in the emotional dimension [29]. Customer experience in online banking should be centered on the customer and can be influenced by the usability and perceived value of the service as the corporate’s social responsibility [30]. It also influences customer recommendations to others and the retention of services [31]. Since customer experience is inherently personal, it can be subjective and challenging to assess [32]. Bleier et al [33] argues that in online customer experiences, the cognitive aspect—particularly through informativeness—is one of the most significant factors and the impressions formed can linger long after the interaction with the online interface has concluded. De Keyser et al. [34] emphasizes the importance of factors such as touchpoints, context, and qualities in shaping customer experience. These elements correspond to customer interactions, the overall environment, and the availability of resources, as well as the responses generated from those interactions. Since customer experience reflects a customer’s perception of a service, it can be leveraged to foster positive customer behavior [35]. A positive customer experience not only meets expectations but also enhances customer loyalty and satisfaction [27]. An ordinary customer experience, characterized by routine, simplicity, familiarity, and convenience, enhances the overall perception of service and reinforces positive outcomes [28,36].

2.3. Customer Satisfaction

By Ban and Jun [37] customer satisfaction is defined as a measure of performance that indicates the gap between customer expectations and the actual experience. Customer satisfaction is vital for organizational growth and for sustainable development. This view is supported by Almaiah et al. [4], who argued that customer satisfaction fosters loyalty, which in turn aids in customer retention and ultimately contributes to growth and profitability. Manyanga et al [8] emphasized that banks need to provide exceptional services to enhance customer satisfaction. Customer satisfaction is influenced by various factors, including trust, attitude, and perceived usefulness [38] among others. Models such as the Technology Acceptance Model, the Service Quality Model, and the Unified Theory of Acceptance and Use of Technology Model have thoroughly explored the factors influencing technology acceptance and the determinants of customer satisfaction. Groonros [39], a pioneer in service quality, noted that both the technical and functional aspects of a service can impact customer satisfaction, a viewpoint also supported by Nkwede et al. [40].

2.3.1. Customer Satisfaction in Online Banking

Several studies have sought to explain the role of online banking in customer satisfaction and the adoption of technology among individuals as a tool for sustainable development. Customer satisfaction with online banking services is influenced by various factors, including efficacy, usage, behavior, performance, environmental conditions, and adoption-related issues [41]. Online banking has gained prominence due to the rise of digitalization. Sathar et al. [42] noted that the convenience of online banking has significantly boosted its adoption, with trust playing a crucial role in customer satisfaction with the service. It has turned to a social responsibility of the corporates. Lin et al. [43] explained that trust is essential for fostering customer satisfaction when adopting new technologies like online banking, with higher trust levels leading to a greater willingness to access online services. Ma [44] added that the quality of information and trust in the expertise of the information source are also key determinants of customer satisfaction. This sentiment was echoed by Cele and Kwenda [45], who highlighted that while online banking has increased the risk of cyber threats, security and trust are critical factors in encouraging more individuals to use the service. Banu et al. [2] noted that self-efficacy influences customer satisfaction regarding online banking, indicating that individuals familiar with using computers are more likely to embrace online banking. The significance of self-efficacy was further emphasized by Shaikh et al. [46], whose study found that self-efficacy is a driving factor in the adoption of online banking among those who had not previously used it. Similarly, Park et al. [47] pointed out that online banking adoption varies by generation, with Generation Z showing a greater inclination to adopt these services due to their frequent use of the internet, while Generation X is more likely to embrace it if the process is user-friendly.

Raza et al. [48] highlighted the importance of service quality in online banking, noting that customers assess it to determine their satisfaction with the service and to make future decisions about its use. Zia [49] also identified a direct relationship between service quality and customer satisfaction. Additionally, Supriyanto et al. [50] explained that reliable service, effective problem-solving, and trustworthiness contribute to satisfaction with bank services and foster customer loyalty as a result sustainable development.

Lei et al. [51] explained that credibility and ease of use are critical factors impacting customer satisfaction. A credible and user-friendly service dispels doubts and minimizes complaints, leading to increased customer satisfaction and a higher likelihood of recommendations and repeat usage. Mazhar et al. [52] noted that, in the context of online services, how complaints are handled can significantly affect customer satisfaction. They highlighted that the time it takes to receive feedback compared to offline transactions can influence customer perception of satisfaction, with quicker responses enhancing overall satisfaction [53]. This perspective was echoed by Islam et al. [54], who found that responsiveness also impacts customer satisfaction in private banking.

2.4. Expectancy Disconfirmation Theory

Yüksel and Yüksel [55] emphasized that the expectancy disconfirmation theory highlights the discrepancies between expectations and reality. Satisfaction typically arises after using a service, and dissatisfaction is directly related to the differences between prior expectations and actual performance [56]. Zhang et al. [57] noted that this theory is one of the most widely accepted frameworks for understanding customer satisfaction with services. Satisfaction is achieved when performance surpasses expectations, a phenomenon referred to as positive disconfirmation. Positive disconfirmation contributes to customer satisfaction [52,58]. Moreover, high levels of previous performance lead to heightened expectations for future interactions.

Sreelakshmi and Prathap [59] found that the expectancy disconfirmation theory is applicable to online banking payments, with perceived usefulness having a significant impact on customer satisfaction. Understanding these dynamics is crucial, as negative disconfirmation can have serious repercussions for businesses, often resulting in customers switching to competitors [52].

2.5. Hypothesis Development and Research Framework

2.5.1. Online Service Clues and Customer Satisfaction

Gautam and Sah [60] supported this idea with their study, which revealed that website usability and features significantly influence customer satisfaction. Wasan [22] found that functional service clues related to credibility and convenience were most positively and significantly associated with customer satisfaction, while humanic clues followed. Mechanic clues, on the other hand, were found to primarily encourage customer behavior. Similarly, Ayinnadis et al. [61] highlighted the importance of functional clues in online banking, noting that a focus on these factors leads to increased customer satisfaction. Khan et al. [62] also discovered that improved online banking services contribute to customer satisfaction.

Anouze et al. [63] pointed out that emotional factors, such as a sense of security, affect the adoption of online banking services, emphasizing that a strong feeling of security correlates with higher customer satisfaction. Park and Han [64] found that service clues influence the decision to use and continue utilizing a service. Likewise, Quiber [65] stressed the importance of security and reliability, identifying them as significant factors impacting customer satisfaction. Thus, the hypothesis can be stated as follows:

H1: Online Banking Service Clues have a direct positive relationship with Customer Satisfaction.

2.5.2. Online Service Clues and Customer Experience

Numerous studies have highlighted the significance of service clues in enhancing customer experience. Berry et al. [66] asserted that service clues are instrumental in evaluating customer experience and influencing decision-making. Kesa [6] found that internet quality has a positive impact on customer satisfaction. Borishade [67] argued that functional clues affect customer experience by contributing to the creation of quality service, which, in turn, influences customer satisfaction. Meeting customer expectations concerning functional clues can enhance their satisfaction. Likewise, Liu et al. [68]emphasized that service clues play a crucial role in shaping customer experience. In their study on customer experience and online banking in India, Chauhan et al. [21] identified functional, mechanic, and humanic service clues as determinants of customer experience and sustainable development.

The hypotheses are therefore formulated as follows:

- H2: Online Banking Service Clues (Functional Clues) have a direct positive relationship with Customer Experience.

- H3: Online Banking Service Clues (Mechanic Clues) have a direct positive relationship with Customer Experience.

- H4: Online Banking Service Clues (Humanic Clues) have a direct positive relationship with Customer Experience.

2.5.3. Customer Experience and Customer Satisfaction

Researchers have identified a positive relationship between customer experience and customer satisfaction. Manyanga et al. [8] noted that customer experience contributes to customer satisfaction by reducing complaints and narrowing the gap between expectations and actual experiences. Chauhan et al. [21] found that customer experience significantly impacts customer satisfaction. Prentice and Nguyen [69] reported that enhanced customer experience leads to increased customer satisfaction, which subsequently drives customer loyalty. Similar findings were observed in the studies conducted by Zaid and Patwayati [70] and Ha [71], which showed that positive customer experiences lead to improved customer satisfaction and retention. Tjahjaningsih et al. [72] further emphasized that effective problem-solving and management of customer issues enhance customer satisfaction which ensures sustainable development.

The hypothesis is therefore formulated as follows:

- H5: Customer Experience has a direct positive relationship with Customer Satisfaction.

2.5.4. Mediating Effect of Customer Experience

Customer experience plays a crucial role in mediating the relationship between service clues and customer satisfaction across various sectors, including online banking. To connect service clues, customer experience, and customer satisfaction, the service clues model proposed by Haeckel [9] is utilized. Haeckel’s framework posits that customer experience in the service sector is influenced by service-related clues, which, in turn, affect customer satisfaction. A positive customer experience enhances every interaction with the business, leading to higher levels of satisfaction [73] [74]. Therefore, service clues contribute to customer satisfaction, with customer experience serving as a mediator. Wasan [22] explored the impact of service clues and found that customer experience significantly mediates the relationship between service clues and customer satisfaction within the context of traditional banking.

The hypotheses are thus formulated as follows:

- H6: Customer Experience mediates the effects of Online Banking Service Clues (Functional Clues) on Customer Satisfaction.

- H7: Customer Experience mediates the effects of Online Banking Service Clues (Mechanic Clues) on Customer Satisfaction.

- H8: Customer Experience mediates the effects of Online Banking Service Clues (Humanic Clues) on Customer Satisfaction.

2.5.5. Demographics, Service Clues and Customer Satisfaction

Kamboj and Singh [75] emphasized that demographic characteristics significantly influence customer satisfaction. Prior research by Bhatt and Bhatt [76] demonstrated that demographics affect the adoption of technology. Sambaombe and Phiri [77] suggested that age influences the relationship between online banking and customer satisfaction. Additionally, Islam et al. [54] found that occupation impacts customer satisfaction in private banking. Wang and Pang [78] also noted that demographics play a critical role in customer satisfaction, explaining that individuals with lower incomes may avoid more expensive options, while those with higher incomes and education levels may prioritize service quality and ambiance over cost.

The hypotheses are thus formulated as follows:

- H9: Gender has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H10: Age has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H11: Education level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H12: Occupation has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

- H13: Income level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

These relationships are illustrated in the conceptual framework for the study presented in Figure 2 below 3.

3. Methodology

3.1. Population and Sample

The population for this study consists of all individuals involved, totaling 390,745 people. However, due to practical limitations in reaching every individual, a target population must be established from which a sample can be drawn. In this case, the target population includes customers who engage in online banking with any of the 22 banks in Cyprus. A sample size of 400 customers was selected, considering a confidence level of 95% and a margin of error of ±5%. This approach aligns with the recommended sample size criteria established by Hair et al. [79].

The study participants were chosen using the convenience sampling method, which was selected for its straightforwardness in accessing potential participants [80]. This method allows for the efficient identification of individuals who meet the specific criteria for online banking usage, ensuring that the appropriate participants were included in the study [81]. The conceptual framework developed by the authors is illustrated in Figure 2 below.

3.2. Data Collection

The study utilized both primary and secondary data. Secondary data were gathered from various sources, including textbooks, journals, and articles, to provide a comprehensive theoretical and empirical foundation for evaluating the current study's findings.

Primary data were collected through a survey using self-administered questionnaires distributed to bank customers both in-person and online via email and social media. This data collection occurred in September and October 2023. The questionnaires were made available in both English and Turkish to accommodate both the foreign and local populations.

A pilot study was conducted with 30 participants to test the effectiveness of the research instrument, ensuring that the questions were clearly understood and free from ambiguity. Any necessary adjustments were made based on the feedback received before the final distribution. Ethical considerations were prioritized throughout the research process, with institutional, bank, and individual permissions obtained to conduct the study, which was conducted on a voluntary basis.

3.3. Questionnaire Construct

3.3.1. Demographic Characteristics

Data were collected from two categories of customers: individual and corporate clients. The demographic information sought included gender, age, education, income, and occupation. Table 1 below illustrates that out of the 400 respondents, 50% were individual customers while the remaining 50% were corporate customers.

In terms of gender, 62.5% of the respondents identified as female, while 37.5% identified as male. Age-wise, 61% of the customers were under the age of 40, with only 10.5% aged 51 and above. Regarding education, a mere 1.5% had completed secondary school as their highest level of education. A significant proportion of respondents (43.75%) held a Bachelor’s degree as their highest educational attainment, indicating that most respondents were highly educated.

When examining occupation, half of the respondents (50%) identified as business owners, while a small percentage (4.25%) were employed in the public sector. In terms of income, 48.25% of respondents reported earnings of less than 25,000 Turkish Lira, whereas the majority (51.75%) earned at least 25,000 Turkish Lira.

This demographic profile provides valuable insights into the characteristics of the participants involved in the study.

Table 1.

Demographic Profile.

| Variable | Description | Frequency | Percentage |

| Gender | Female | 250 | 62.50 |

| Male | 150 | 37.50 | |

| Total | 400 | 100 | |

| Age | 20 years and below | 2 | 0.50 |

| 21-30 years | 81 | 20.25 | |

| 31-40 years | 193 | 48.25 | |

| 41-50 years | 82 | 20.50 | |

| 51-60 years | 28 | 7.00 | |

| 61 years and above | 14 | 3.50 | |

| Total | 400 | 100 | |

| Type of customer | Individual bank customers | 200 | 50.00 |

| Corporate bank customers | 200 | 50.00 | |

| Total | 400 | 100 | |

| Academic qualification |

Primary school | 3 | 0.75 |

| Secondary school | 6 | 1.50 | |

| High school | 13.5 | ||

| Bachelor’s degree | 17554 | 43.75 | |

| Two-year associate degree | 27 | 6.75 | |

| Master’s degree and above | 135 | 33.75 | |

| Total | 400 | 100 | |

| Occupation | Private sector employee | 58 | 14.50 |

| Public sector employee | 17 | 4.25 | |

| Retired | 18 | 4.50 | |

| Self-employed | 47 | 11.75 | |

| Business owner | 200 | 50.00 | |

| Others | 60 | 15.00 | |

| Total | 400 | 100 | |

| Monthly income | 15 750TL and less | 52 | 13.00 |

| 15 750TL to 20 000TL | 85 | 21.25 | |

| 20 000TL to 25 000TL | 56 | 14.00 | |

| 25 000TL to 30 000TL | 80 | 20.00 | |

| 30 000TL to 35 000TL | 36 | 9.00 | |

| 35 000TL to 40 000TL | 24 | 6.00 | |

| 45 000TL and more | 67 | 16.75 | |

| Total | 400 | 100 |

3.3.2. Measurement

The independent, mediating, and dependent variables in this research were measured using scales that were adopted and adapted from prior studies. Online banking service clues were categorized into three distinct groups: functional, mechanic, and humanic.

- -Functional Clues: These were assessed based on criteria such as functional quality, trust, and convenience.

- -Mechanic Clues: Measurement for these clues focused on aspects of website design and usability.

- -Humanic Clues: This category was evaluated through customer complaint handling practices.

3.4. Data Analysis

Statistical analysis for the study was conducted using SmartPLS 4.0 software. Structural Equation Modeling (SEM) was employed to assess the relationships among the variables. PLS-SEM is particularly suitable for data analysis involving multiple indicators and complex models [93]. The researcher evaluated the goodness of fit for the model based on constructs proposed by previous scholars, as detailed in Table 3.

4. Results

4.1. Measurement Model Results

Prior to conducting the path analysis of the proposed research model using Structural Equation Modeling (SEM), measurement model analyses were performed to assess the suitability of the data through Confirmatory Factor Analysis (CFA). Factor loadings were analyzed to evaluate the relationships between the constructs and their respective indicators. The results indicated that all factor loading values met the threshold of at least 0.70, signifying that each indicator explains at least 70% of its corresponding construct. A value of 0.70 or higher is considered to reflect good and acceptable reliability [93,99].

Additionally, the Variance Inflation Factor (VIF) was employed to assess multicollinearity among the indicators, as high correlation could skew the results. The VIF values obtained were all below 5, which is considered ideal; values exceeding 5 indicate potential multicollinearity issues [100]. Hair et al. [93] recommend a VIF close to 3 as optimal, while Bhatti et al. [101] suggest that a VIF below 2 is free from bias (see Table 4).

To determine the reliability of the research instrument for measuring each variable, both Cronbach’s alpha and Composite Reliability were calculated. Relying solely on Cronbach’s alpha is insufficient; hence, Composite Reliability was also assessed [99]. The findings revealed that the research instrument demonstrated significant reliability, with Cronbach’s alpha values for both individual and corporate customer models all being at least 0.70 (see Table 5). A Cronbach’s alpha value should ideally fall between 0.70 and 0.95 to ensure acceptable internal consistency [99,102,103,104]. Furthermore, the composite reliability values, represented by Rho A and Rho C, were both at least 0.70, with values ranging from 0.70 to 0.90 considered satisfactory [105].

Table 4.

Factor Loadings and VIF Results.

| Constructs | Factor loadings |

Outer weight (p-values) |

Variance Inflation Factor | |||

| Individual Customer | Corporate Customer | Individual Customer | Corporate Customer | |||

| Trust (TR) | TR1 | 0.761 | 0.812 | 0.000 | 2.945 | - |

| TR2 | - | 0.798 | 0.000 | 2.820 | - | |

| TR3 | 0.733 | 0.800 | 0.000 | - | - | |

| Functional Quality (FQ) | FQ5 | - | 0.804 | 0.000 | - | 1.708 |

| Web design (WD) | WD3 | 0.735 | 0.786 | 0.000 | - | 1.761 |

| WD4 | - | 0.793 | 0.000 | 1.748 | - | |

| WD5 | - | 0.764 | 0.000 | - | 1.940 | |

| WD6 | - | 0.805 | 0.000 | - | - | |

| WD8 | 0.729 | 0.719 | 0.000 | - | 2.006 | |

| Customer Complaint Handling (CCH) | CCH1 | 0.856 | 0.833 | 0.000 | - | 1.775 |

| CCH2 | 0.864 | 0.817 | 0.000 | 1.912 | 1.831 | |

| CCH3 | 0.846 | 0.823 | 0.000 | 1.649 | - | |

| Customer Experience (CE) |

CE1 | 0.811 | - | 0.000 | 2.048 | 1.415 |

| CE2 | 0.781 | 0.733 | 0.000 | 1.897 | 1.415 | |

| CE3 | 0.826 | 0.716 | 0.000 | 1.420 | 1.584 | |

| CE4 | - | 0.745 | 0.000 | 1.405 | - | |

| CE5 | - | 0.779 | 0.000 | 1.524 | 1.369 | |

| Convenience (CNV) |

CNV1 | 0.791 | 0.818 | 0.000 | - | 1.725 |

| CNV2 | 0.792 | 0.810 | 0.000 | - | 1.387 | |

| CNV3 | 0.767 | 0.806 | 0.000 | 1.711 | 1.900 | |

| Website Usability (WU) |

WU2 | - | 0.769 | 0.000 | 1.906 | 2.120 |

| WU3 | 0.750 | 0.777 | 0.000 | 1.827 | 2.122 | |

| WU4 | 0.701 | 0.794 | 0.000 | 1.374 | 1.403 | |

| WU5 | 0.775 | 0.782 | 0.000 | 1.519 | 1.516 | |

| WU6 | 0.780 | 0.795 | 0.000 | 1.564 | - | |

| WU7 | 0.756 | 0.803 | 0.000 | - | 1.406 | |

Table 5.

Internal Consistency Reliability.

| Cronbach’s alpha | Rho_A | Rho_C | ||

| Individual customer model | Customer experience | 0.731 | 0.733 | 0.848 |

| Customer satisfaction | 0.740 | 0.747 | 0.851 | |

| Functional clues | 0.829 | 0.834 | 0.879 | |

| Humanic clues | 0.818 | 0.827 | 0.891 | |

| Mechanic clues | 0.868 | 0.874 | 0.898 | |

| Corporate customer model | Customer experience | 0.761 | 0.767 | 0.848 |

| Customer satisfaction | 0.728 | 0.730 | 0.846 | |

| Functional clues | 0.830 | 0.835 | 0.887 | |

| Humanic clues | 0.703 | 0.705 | 0.870 | |

| Mechanic clues | 0.871 | 0.874 | 0.901 |

Furthermore, the Heterotrait-Monotrait Ratio of correlations (HTMT) was analyzed to assess discriminant validity. This evaluation ensures that each variable demonstrates stronger correlations with its own indicators compared to those of other variables within the model. The results indicate that both the individual and corporate customer models exhibit robust relationships, with all HTMT values being below the threshold of 0.90. According to Hair et al. [105], an HTMT value not exceeding 0.90 is deemed satisfactory and indicative of discriminant validity between constructs [106,107].

Additionally, the convergent validity, as assessed by the Average Variance Extracted (AVE), was found to be at least 0.50 for both individual and corporate customer models. An AVE value of 0.50 or higher is recommended as a standard [99]. This threshold indicates that each construct accounts for at least half of the variance in the indicators, further supporting the validity of the measurement model (see Table 6).

4.2. Structural Model Results

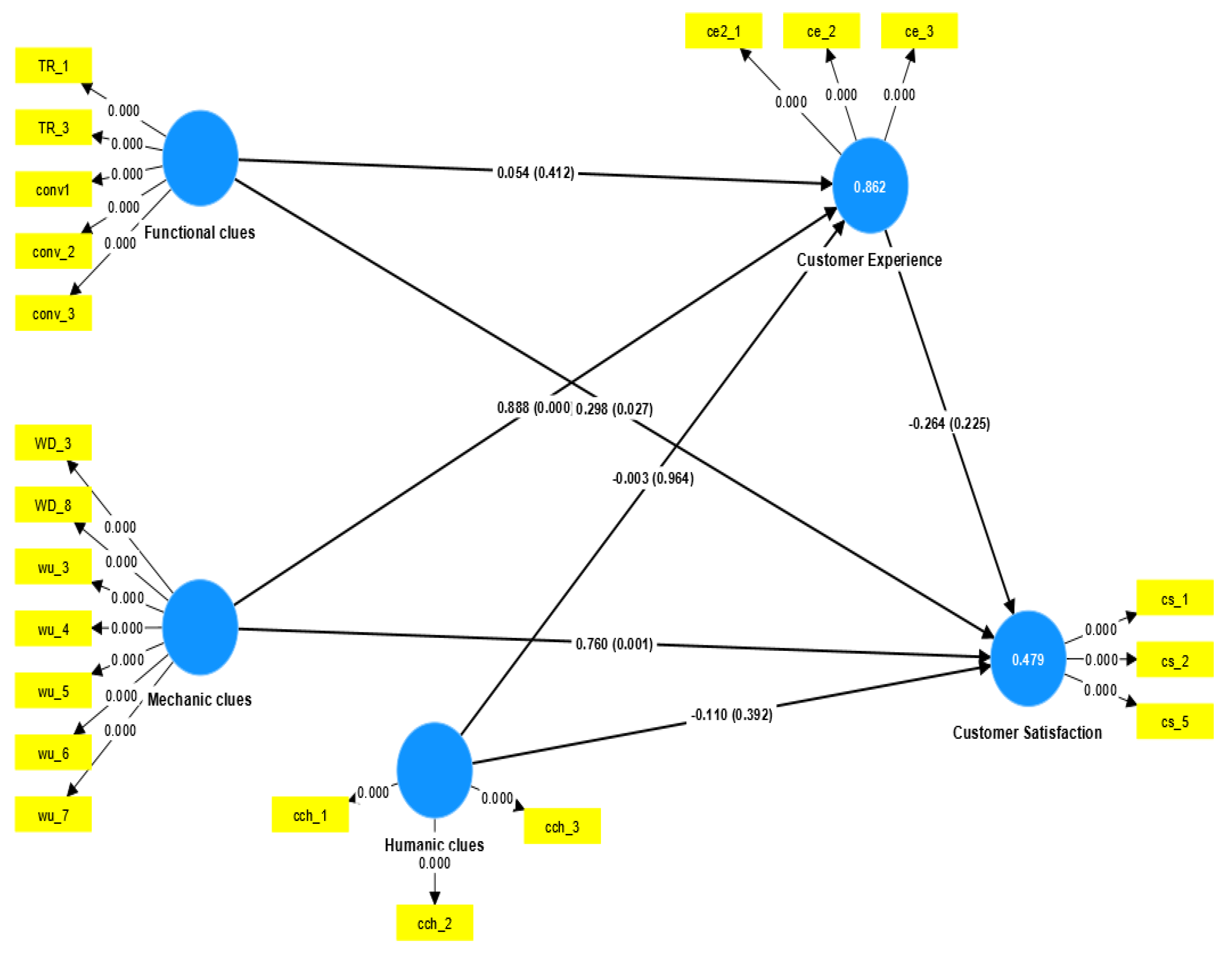

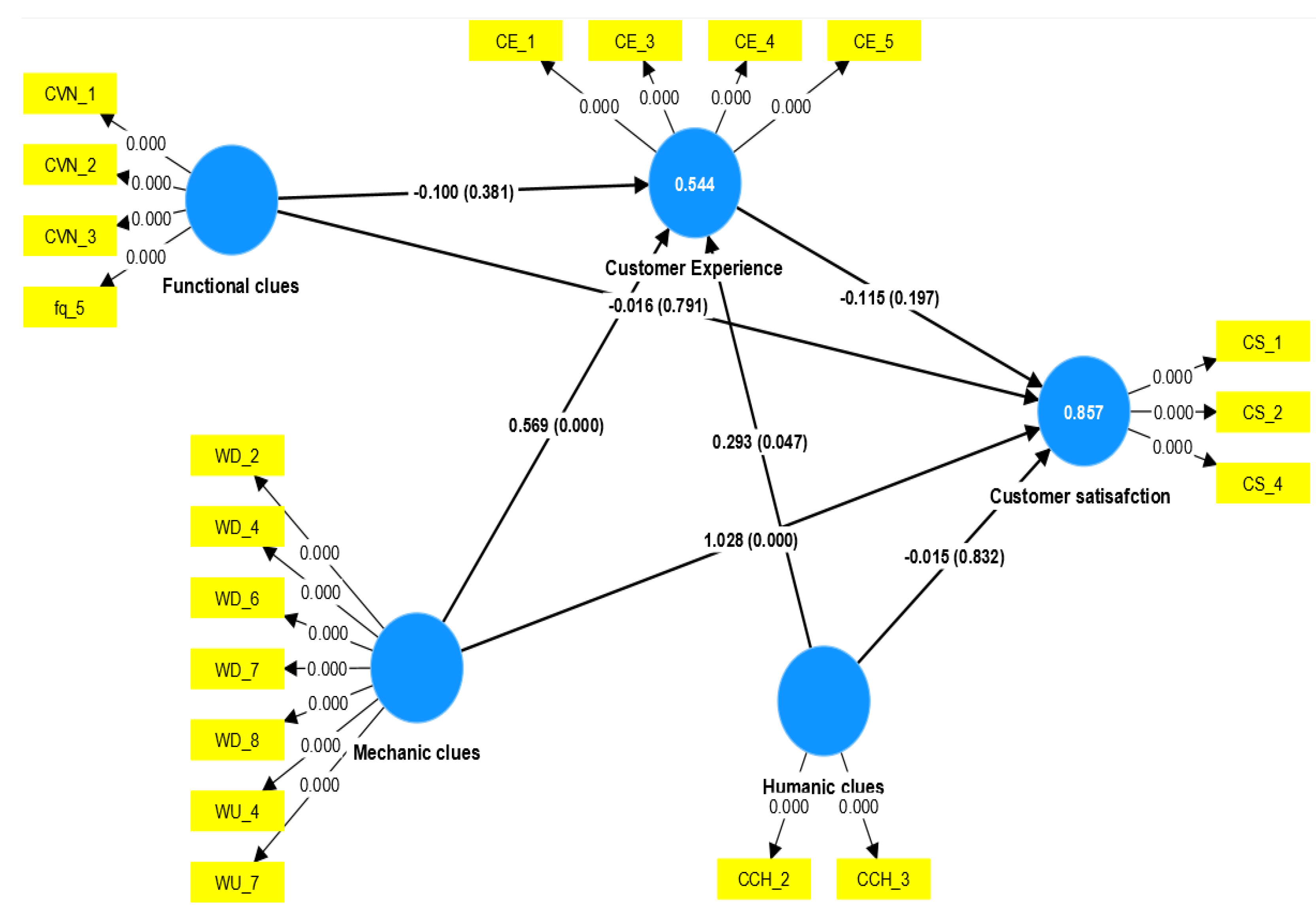

The analysis comparing individual and corporate bank customers, as shown in Table 7, reveals distinct impacts of functional and mechanic clues on customer satisfaction. Functional clues positively influence satisfaction among individual bank customers by 0.054, while they negatively affect corporate bank customers by 0.1. Therefore, hypothesis H1(a) is supported, while hypothesis H1(d) is not.

Further analysis confirms that hypothesis H1(b), which posits that mechanic clues have a direct positive relationship with individual online banking customers’ satisfaction, is accepted. Similarly, hypothesis H1(e), suggesting that mechanic clues positively impact corporate online banking customers’ satisfaction, is also accepted at the 5% significance level. Specifically, enhancements in mechanic clues lead to increases in satisfaction of 0.760 units for individual customers and 1.028 units for corporate customers.

However, hypotheses H1(c) and H1(f) are rejected, indicating that humanic clues do not have a direct positive relationship with satisfaction for either individual or corporate online banking customers. In fact, improvements in humanic clues resulted in insignificant negative changes in satisfaction, recorded at -0.110 for individual customers and -0.015 for corporate customers as it is the corporate’s social responsibility.

Table 7.

Path Analysis.

| Individual customer | Corporate customer | ||||||

| β | p-value | f-square | β | p-value | f-square | ||

| H1(a) | FC->CS | 0.054 | 0.412 | 1.254 | -0.100 | 0.381 | 1.203 |

| H1(b) | MC->CS | 0.760 | 0.001* | 1.814 | 1.028 | 0.000* | 1.728 |

| H1(c) | HC->CS | -0.110 | 0.392 | 1.215 | -0.015 | 0.832 | 1.016 |

| Combined model | |||||||

| Β | t-sta. | p-value | |||||

| H2 | FC->CE | 0.298 | 4.096 | 0.000* | |||

| H3 | MC->CE | 0.888 | 3.627 | 0.000* | |||

| H4 | HC->CE | 0.003 | 7.491 | 0.000* | |||

| H5 | CE->CS | 0.109 | 5.010 | 0.000* | |||

Additionally, the study found a positive and significant relationship between online banking clues and customer experience, evidenced by p-values of 0.000, which are below the 0.05 threshold. The coefficient values for functional clues, mechanic clues, and humanic clues were 0.298, 0.888, and 0.003, respectively, indicating that mechanic clues lead to the most substantial increase in customer experience.

Moreover, customer experience was shown to have a positive association with customer satisfaction, with enhancements in customer experience correlating to an increase in customer satisfaction by 0.109 units. The results indicate that all tested hypotheses were significant. Specifically, hypotheses H2 through H5 confirm the significant positive relationships among functional clues, mechanic clues, humanic clues, customer experience, and customer satisfaction, with coefficients of β = 0.298 (p < 0.005), β = 0.888 (p < 0.005), β = 0.003 (p < 0.005), and β = 0.109 (p < 0.005), respectively. Therefore H2, H3, H4 and H5 were all confirmed.

4.3. Test of the Mediating Effects

The study aimed to investigate the mediating effects of customer experience on the relationship between online banking service clues and customer satisfaction. To achieve this, an analysis of indirect effects was conducted.

Table 8 illustrates that customer experience does not serve as a mediator in the relationship between any of the three online banking service clues—functional clues, mechanic clues, and humanic clues—and customer satisfaction. The results show insignificant p-values of 0.821, 0.558, and 0.446 for humanic clues, mechanic clues, and functional clues, respectively, all of which exceed the recommended threshold of 0.05 for significance. Consequently, hypotheses H6, H7, and H8 were not supported.

4.4. Test of the Moderating Effects

The study aimed to assess whether demographic factors—gender, age, education, occupation, and income—moderate the relationship between online banking service cues and customer satisfaction. To analyze this, a multiple group analysis was conducted using both unconstrained and structural weight models. The results, displayed in Table 9, indicate a positive and significant moderating impact of these demographic characteristics on the relationship between online banking service cues and customer satisfaction, affecting both individual and corporate customers.

Table 9 further reveals that there is a significant difference between the unconstrained and structural weight models, as indicated by chi-square values. Specifically, the moderating effects of gender (χ2=12.819, р=0.000), age (χ2=17.514, р=0.000), education level (χ2=10.686, р=0.000), occupation (χ2=8.193, р=0.000), and income level (χ2=11.714, р=0.000) were statistically significant across different customer types. Consequently, these findings support hypotheses H9 through H13.

Table 9.

Moderating Effects of Demographic Variables.

| Variable | Description | Unconstrained | Structured weight | Model Comparison | |||

| Β | p | β | p | χ (p) | |||

| H9 | Gender | Male Female |

0.647 0.410 |

0.000 0.015 |

0.926 0.788 |

0.000 0.000 |

12.819 (0.000)* |

| H10 | Age | 20 years and below 21-30 years 31-40 years 41-50 years 51-60 years 61 years and above |

0.556 0.977 1.148 0.633 0.252 0.041 |

0.000 0.002 0.042 0.000 0.001 0.004 |

0.066 0.082 1.156 1.192 0.044 0.070 |

0.000 0.002 0.042 0.000 0.001 0.004 |

17.514 (0.000)* |

| H11 | Education | Primary school Secondary school High school Bachelor’s degree Two-year degree Master’s degree & above |

0.025 0.189 0.368 0.743 1.981 1.452 |

0.000 0.000 0.000 0.000 0.000 0.000 |

0.05 0.39 0.44 1.03 1.64 1.65 |

0.000 0.002 0.042 0.000 0.000 0.000 |

10.686 (0.000)* |

| H12 | Occupation | Private sector employee Public sector employee Retired Self-employed Business owner Others |

0.113 0.000 0.000 0.630 1.400 0.000 |

0.000 0.000 0.000 0.000 0.000 0.000 |

0.551 0.890 0.140 1.03 0.015 0.044 |

0.000 0.000 0.001 0.000 0.001 0.001 |

8.193 (0.000)* |

| H13 | Income | 15 750TL and less 15 750TL to 20 000TL 20 000TL to 25 000TL 25 000TL to 30 000TL 30 000TL to 35 000TL 35 000TL to 40 000TL 45 000TL and more |

0.172 0.272 0.593 0.622 0.548 0.716 0.945 |

0.000 0.000 0.000 0.000 0.000 0.000 0.000 |

0.263 0.287 0.196 1.032 1.150 1.770 1.100 |

0.028 0.016 0.039 0.000 0.000 0.000 0.000 |

11.714 (0.000)* |

4.5. Summary of Individual and Corporate Customer Satisfaction

5. Discussion

5.1. Findings of the Study

The study highlighted significant relationships between online banking service cues, customer experience, and customer satisfaction, adding valuable insights to existing research. A key finding was that service cues affect customer satisfaction differently for individual and corporate customers which ensures sustainable development. Also, customer satisfaction has become each corporate’s social responsibility in a sustainable developed coporation.

Overall, according to the above mentioned hypotheses’ results are:

- H1: Online Banking Service Clues have a direct positive relationship with Customer Satisfaction.

H1, which posits that mechanic clues have a direct positive relationship with individual online banking customers’ satisfaction, is accepted

- H2: Online Banking Service Clues (Functional Clues) have a direct positive relationship with Customer Experience.

Hypotheses H2 was confirmed confirm the significant positive relationships among functional clues

- H3: Online Banking Service Clues (Mechanic Clues) have a direct positive relationship with Customer Experience.

Hypotheses H3 was confirmed confirm the significant positive relationships among mechanic clues

- H4: Online Banking Service Clues (Humanic Clues) have a direct positive relationship with Customer Experience.

Hypotheses H4 was confirmed the significant positive relationships among humanic values

- H5: Customer Experience has a direct positive relationship with Customer Satisfaction.

H5 has been confirmed as which posits there is a direct positive relationship with Customer Satisfaction

- H6: Customer Experience mediates the effects of Online Banking Service Clues (Functional Clues) on Customer Satisfaction.

H6 was not supported

- H7: Customer Experience mediates the effects of Online Banking Service Clues (Mechanic Clues) on Customer Satisfaction.

H7 was not supported

- H8: Customer Experience mediates the effects of Online Banking Service Clues (Humanic Clues) on Customer Satisfaction.

H8 was not supported

- H9: Gender has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

H9 was supported

- H10: Age has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

H10 was supported

- H1: Education level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

H11 was supported

- H12: Occupation has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

H12 was supported

- H13: Income level has a significant moderating effect on the relationship between online banking service clues and customer satisfaction.

H13 was supported

Specifically, functional cues positively impacted individual customer satisfaction, supporting the results of Borishade et al. [108]. For corporate customers, however, this relationship was negative and insignificant, suggesting distinct expectations across customer types. This difference indicates that management should tailor improvements to better address the unique needs of each group.

Humanic cues, meanwhile, had a negative yet statistically insignificant effect on satisfaction for both individual and corporate customers. In online banking contexts, customers may view humanic cues as less important due to minimal direct interaction, placing greater value on other service elements. Conversely, mechanic cues showed a positive and significant impact on satisfaction for both groups, with the strongest effect seen in corporate customer satisfaction as its responsibility.

Regarding the relationship between online banking service cues and customer experience, all service cues demonstrated a direct and positive association with customer experience. These findings align with earlier studies by Liu et al. [68] and Chauhan et al. [21], suggesting that focusing on these service cues is essential for providing a comprehensive customer experience that can give banks a competitive edge. Enhancements in service cues translate to improvements in customer experience, with factors such as functional quality, website design, usability, and service impression all positively impacting the customer experience as a sustainable development. This supports Haeckel’s theory and highlights its relevance in modern online banking, indicating that management should emphasize these service cues to optimize customer satisfaction.

Mechanic cues exhibited the strongest positive relationship, where an increase in mechanic cues led to a 0.888 rise in customer experience. This insight is crucial for bank management, as it underscores the importance of website design and usability in shaping customer experience. It is vital for online banking platforms to be user-friendly, allowing customers to easily find information, navigate smoothly, and avoid slow loading times or website freezing. These findings further validate theoretical models like SERVQUAL, which emphasize perceived ease of use and design in technology applications. In contrast, humanic cues showed the weakest relationship with customer experience, a finding consistent with research by Hussadintorn and Koomsap [24]. Given the nature of online services, where direct human interaction is limited, humanic cues are less impactful compared to physical banking.

Customer experience was found to have a direct, positive impact on customer satisfaction, indicating that improvements in customer experience lead to increased customer satisfaction. These findings are consistent with those of numerous previous studies [60,109,110,111].

Demographic characteristics were shown to moderate the relationship between online banking service cues and customer satisfaction, with age having the strongest moderating effect. This may be due to varying levels of computer literacy, as younger individuals tend to be more technology-oriented than older adults [99]. Gender had the second most significant effect, aligning with findings by Teeroovengadum [113] and Lou and Xie [114], who noted gender differences in online information processing. Men exhibited a stronger moderating effect than women, possibly because they are generally more inclined to use online banking for convenience, whereas women tend to be more cautious due to perceived risks. This observation is supported by Pei et al. [115], who reported that men favor online services for their convenience, while women may be more hesitant. Management should consider these differences and implement strategies to appeal to more female clients, ensuring a customer experience that addresses their concerns.

Education was also identified as a moderating factor. The majority of study respondents held at least a bachelor’s degree, suggesting that individuals with higher education levels are generally more comfortable using online services. Additionally, income was found to moderate the relationship between service cues and satisfaction, a result consistent with Shandilya et al. [116]. High-income customers tend to have greater expectations and demand higher-quality service.

The study further revealed that occupation moderates the relationship between online banking service cues and customer satisfaction as a corporate’s social responsibility. Similar findings were observed in the research by Kubeyinje and Omigie [112] in Nigeria. In this study, business owners reported the highest satisfaction with online banking, followed by self-employed individuals. These groups, typically more accustomed to taking risks, are more likely to use and find satisfaction in online banking services compared to others.

5.2. Managerial Implications

This study offers several key implications for bank management in Cyprus and beyond. Bank leaders should focus on providing distinctive service cues to enhance the overall customer experience, ultimately driving customer satisfaction. Since online banking service cues showed a direct positive relationship with customer satisfaction, elements such as website design, usability, trust, and complaint handling should be prioritized and addressed efficiently to ensure sustainable development.

Additionally, the moderating effects of demographic characteristics on the relationship between online banking service cues and customer satisfaction highlight the need for tailored approaches. Management in sectors offering online services should recognize and address the unique service preferences associated with different demographic groups to maximize customer satisfaction. Specific service elements may be more relevant to certain demographic segments, and these should be considered when developing and refining online banking platforms.

It is also crucial to acknowledge the distinctions between customer types: functional cues had a stronger impact on individual customers than on corporate customers, while mechanic cues positively influenced satisfaction across both groups. Continual enhancement of mechanic cues should remain a priority to meet the needs of both individual and corporate clients.

5.3. Theoretical Implications

This study was conducted to address a gap in the literature on customer experience and online banking service cues. It identified positive relationships between customer experience and various online banking service cues, underscoring Haeckel’s model and contributing to its validation in the literature. Specifically, the study found a positive relationship between functional cues and customer satisfaction among individual customers, while other cues showed negative associations. Differences in humanic cues—such as tone of voice, communication style, customer service availability, and visual design—appeared to have minimal impact on customer experience in the online banking context, where direct human interaction is limited. These findings contribute new insights to the body of literature on online banking service cues, customer satisfaction, corporates’ social responsibility and sustainable development.

Related studies by Wasan [22] and Chauhan et al. [21] in India also explore similar themes; however, Wasan focused on traditional banking, and Chauhan et al. did not consider customer experience as a mediator. In contrast, this study found no mediating effect of customer experience on the relationship between online banking service cues and customer satisfaction, adding valuable insights to the limited research in this area and laying a foundation for further studies in varied contexts. This research may inform the theoretical framework around customer experience, particularly by exploring its potential mediating role. It provides a deeper understanding of how online banking service cues contribute to the overall customer experience and influence satisfaction. Additionally, the study highlights differences in the needs of individual versus corporate customers, an important consideration for marketing strategies and service delivery frameworks.

5.4. Limitations and Future Research Suggestions

This study utilized a convenience sampling technique, which may limit the generalizability of the results to the broader population. Future research should consider employing probability sampling methods to enhance representativeness. Additionally, this study focused solely on a quantitative approach; incorporating qualitative methods in future research could provide deeper insights and greater contextual understanding of the subjects being studied.

Given the growing popularity of mobile banking, future studies could specifically investigate service cues and customer satisfaction within the context of mobile banking applications. This would offer valuable insights into the unique challenges and opportunities present in this area. It is also important to consider additional variables, such as cultural differences, technological literacy, and external economic conditions, that may influence customer perceptions.

Furthermore, future research could explore additional service cues that were not included in the current study, allowing for a more comprehensive understanding of the online banking landscape.

5.5. Conclusion

The study examined the relationship between online banking service cues and customer satisfaction, specifically investigating the mediating effects of customer experience and the moderating effects of demographic characteristics on this relationship. Among the different types of service cues, mechanic cues were found to have the most positive impact on sustainable development. In today's competitive landscape, enhancing these cues is crucial for promoting customer satisfaction as a corporate’s social responsibility and gaining a competitive advantage for companies offering online services.

While customer experience did not mediate the relationship between online service cues and customer satisfaction, demographic characteristics were identified as significant moderators. This suggests that services should be tailored to address these demographic differences effectively. The study also noted limitations related to the sampling technique and provided recommendations for future research. Overall, it contributes valuable insights to the literature, particularly for small islands and the online banking sector, and is especially relevant given the global increase in the adoption of online services.

Author Contributions

Conceptualization: S.D. and A.G.K.; Methodology: S.D. and A.G.K.; Software: S.D.; Validation: S.D. and A.G.K.; Formal Analysis: S.D. and A.G.K.; Investigation: S.D.; Resources: S.D.; Data Curation: S.D.; Writing—Original Draft Preparation: S.D.; Writing—Review and Editing: S.D. and A.G.K.; Visualization: S.D.; Supervision: A.G.K.; Project Administration: S.D. and A.G.K. S.D. and A.G.K. All authors have read and approved the final version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki and was approved by the Institutional Review Board of Near East University, Cyprus. (NEU/SS/2023/1552, 20 March 2023).

Informed Consent Statement

Written informed consent has been obtained from the participants to publish this paper.

Data Availability Statement

The data presented in this study will be available on demand from the corresponding author.

Acknowledgments

The first author would like to express her thanks to the supervisor who has supported and contributed in her dissertation. The authors would like to thank anonymous reviewers for their valuable feedbacks to the article.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Zeebaree, M., Ismael, G. Y., Nakshabandi, O. A., Saleh, S. S., & Aqel, M. (2020). Impact of innovation technology in enhancing organizational management. Studies of Applied Economics, 38(4), 3970. [CrossRef]

- Banu, A. M., Mohamed, N. S., & Parayitam, S. (2019). Online banking and customer satisfaction: evidence from India. Asia-Pacific Journal of Management Research and Innovation, 15(1-2), 68-80. [CrossRef]

- Sleimi, M., & Musleh, M. (2020). E-Banking services quality and customer loyalty: The moderating effect of customer service satisfaction: Empirical evidence from the UAE banking sector. Management Science Letters, 10(15), 3663–3674. [CrossRef]

- Almaiah, M. A., Al-Rahmi, A. M., Alturise, F., Alrawad, M., Alkhalaf, S., Lutfi, A., ... & Awad, A. B. (2022). Factors influencing the adoption of internet banking: An integration of ISSM and UTAUT with price value and perceived risk. Frontiers in Psychology, 13, 919198. [CrossRef]

- Wiryawan, D., Suhartono, J., Hiererra, S. E., & Gui, A. (2022). Factors affecting digital banking customer satisfaction in Indonesia using D&M model. In 2022 10th International Conference on Cyber and IT Service Management (CITSM) (pp. 01-04). IEEE.

- Kesa, D. D. (2018). Cosumer Perception Toward Online Banking Services to Build Brand Loyalty: Evidence from Indonesia. KnE Social Sciences, 1183-1191. [CrossRef]

- Suchánek, P., & Králová, M. (2019). Customer satisfaction, loyalty, knowledge and competitiveness in the food industry. Economic Research-Ekonomska Istraživanja, 32(1), 1237–1255. [CrossRef]

- Manyanga, W., Makanyeza, C., & Muranda, Z. (2022). The effect of customer experience, customer satisfaction and word of mouth intention on customer loyalty: The moderating role of consumer demographics. Cogent Business & Management, 9(1), 2082015. [CrossRef]

- Haeckel, S. H., Carbone, L. P., & Berry, L. L. (2003). How to lead the customer experience. Marketing Management, 12(1), 18-18.

- Rita, P., Oliveira, T., & Farisa, A. (2019). The impact of e-service quality and customer satisfaction on customer behavior in online shopping. Heliyon, 5(10), e02690. [CrossRef]

- Ahmed, R. R., Romeika, G., Kauliene, R., Streimikis, J., & Dapkus, R. (2020). ES-QUAL model and customer satisfaction in online banking: evidence from multivariate analysis techniques. Oeconomia Copernicana, 11(1), 59–93. [CrossRef]

- Alhassany, H., & Faisal, F. (2018). Factors influencing the internet banking adoption decision in North Cyprus: an evidence from the partial least square approach of the structural equation modeling. Financial Innovation, 4, 1-21. [CrossRef]

- Ozatac, N., Saner, T., & Sen, Z. S. (2016). Customer satisfaction in the banking sector: the case of North Cyprus. Procedia Economics and Finance, 39, 870-878. [CrossRef]

- Altay, O., & Olkan, L. A. (2015). 2009-2013 Döneminde KKTC’deki Ticari Bankaların Performans Analizi. EUL Journal of Social Sciences, 6(2), 59-75.

- Kutlay, K. (2017, September). Kuzey Kıbrıs’ ta Banka Karlığını Etkileyen Faktörler: Ampirik bir Çalışma. In Proceedings of 2 nd International Conference on Scientific Cooperation for the Future in the Economics and Administrative Sciences (p. 231).

- Yeşilada, T., & Yalyalı, P. (2016). KKTC’de Bankacılık Sektöründe Şube ve Personel Sayısındaki Gelişmeler ile Veri Zarflama Analizi Yöntemi Kullanılarak Yapılan Etkinlik Analizi Çalışması, Lefke Avrupa Üniversitesi Sosyal Bilimler Dergisi, 7(1), 27-49.

- Şafakli, O. V. (2017). Perceptions of academicians towards the reasons of using internet banking: Case of Cyprus. International Journal of Academic Research in Accounting, Finance and Management Sciences, 7(1), 197-202.

- Serener, B. (2017). Internet bankıng adoptıon ın Cyprus: adopters versus non-adopters. Ponte International Journal of Science and Research, 73(1).

- Serener, B. (2018). Barriers to the use of internet banking among Nigerian and Zimbabwean students in Cyprus. Journal of Management and Economics Research, 16(1), 347-357.

- Jenkins, H., Hesami, S., & Yesiltepe, F. (2022). Factors Affecting Internet Banking Adoption: An Application of Adaptive LASSO. Computers, Materials & Continua, 72(3), 6167-6184. [CrossRef]

- Chauhan, S., Akhtar, A., & Gupta, A. (2022). Customer experience in digital banking: A review and future research directions. International Journal of Quality and Service Sciences, 14(2), 311-348. [CrossRef]

- Wasan, P. (2018). “Predicting customer experience and discretionary behaviors of bank customers in India”. International Journal of Bank Marketing, 36(4), 701-725. [CrossRef]

- Carbone, L. P., & Haeckel, S. H. (1994). Engineering Customer Experiences. Journal of Marketing Management, 3(3), 8-19.

- Hussadintorn Na Ayutthaya, D., & Koomsap, P. (2019). Improving Experience Clues on a Journey for Better Customer Perceived Value. In Transdisciplinary Engineering for Complex Socio-technical Systems (pp. 53-62). IOS Press.

- Lemon, K. N., & Verhoef, P. C. (2016). Understanding customer experience throughout the customer journey. Journal of marketing, 80(6), 69-96. [CrossRef]

- Godovykh, M., & Tasci, A.D.A. (2020). Customer experience in tourism: A review of definitions, components, and measurements. Tourism Management Perspectives, 35, 1-10. [CrossRef]

- Chepur, J., & Bellamkonda, R. (2019). Examining the conceptualizations of customer experience as a construct. Academy of Marketing Studies Journal, 23(1), 1-9.

- Heinonen, K., & Lipkin, M. (2023). Ordinary customer experience: Conceptualization, characterization, and implications. Psychology & Marketing, 40(9), 1720-1736. [CrossRef]

- Rais, N. M., Musa, R., & Muda, M. (2016). Reconceptualisation of customer experience quality (CXQ) measurement scale. Procedia Economics and Finance, 37, 299-303. [CrossRef]

- Bhatnagr, P., Rajesh, A., & Misra, R. (2024). A study on driving factors for enhancing financial performance and customer-centricity through digital banking. International Journal of Quality and Service Sciences, 16(2), 218-250. [CrossRef]

- Amenuvor, F. E., Owusu-Antwi, K., Basilisco, R., & Bae, S. C. (2019). Customer Experience and Behavioral Intentions: The Mediation Role of Customer Perceived Value. International Journal of Scientific Research and Management, 7(10), 1359-1374. [CrossRef]

- Gahler, M., Klein, J. F., & Paul, M. (2023). Customer Experience: Conceptualization, Measurement, and Application in Omnichannel Environments. Journal of Service Research, 26(2), 191-211. [CrossRef]

- Lin, W. R., Wang, Y. H., & Hung, Y. M. (2020). Analyzing the factors influencing adoption intention of internet banking: Applying DEMATEL-ANP-SEM approach. PloS one, 15(2), e0227852. [CrossRef]

- De Keyser, A., Verleye, K., Lemon, K. N., Keiningham, T. L., & Klaus, P. (2020). Moving the Customer Experience Field Forward: Introducing the Touchpoints, Context, Qualities (TCQ) Nomenclature. Journal of Service Research, 23(4), 433-455. [CrossRef]

- Flacandji, M., & Krey, N. (2020). Remembering shopping experiences: the shopping experience memory scale. Journal of Business Research, 107, 279-289. [CrossRef]

- Arici, H. E., Köseoglu, M. A., & Sökmen, A. (2022). The intellectual structure of customer experience research in service scholarship: A bibliometric analysis. The Service Industries Journal, 42(7-8), 514-550. [CrossRef]

- Ban, H. J., & Jun, J. K. (2019). A study on the semantic network analysis of luxury hotel and business hotel through the big data. Culinary Science & Hospitality Research, 25(1), 18–28.

- Almansour, B., & Elkrghli, S. (2023). Factors influencing customer satisfaction on e-banking services: a study of Libyan banks. International Journal of Technology, Innovation and Management (IJTIM), 3(1), 34-42. [CrossRef]

- Gronroos, C. (1984). A service quality model and its marketing implications. European Journal of Marketing, 18(4), 36–44. [CrossRef]

- Nkwede, M. F. C., Ogba, I. E., & Nkwede, F. E. (2022). Determinants of customer satisfaction in a high-contact service environment: a study of selected hotels in Abakaliki metropolis, Nigeria. Research in Hospitality management, 12(2), 183-190. [CrossRef]

- Taherdoost, H. (2018). A review of technology acceptance and adoption models and theories. Procedia manufacturing, 22, 960-967. [CrossRef]

- Sathar, M. B. A., Rajagopalan, M., Naina, S. M., & Parayitam, S. (2022). A moderated-mediation model of perceived enjoyment, security and trust on customer satisfaction: evidence from banking industry in India. Journal of Asia Business Studies, 17(3), 656-679. [CrossRef]

- Bleier, A., Harmeling, C. M., & Palmatier, R. W. (2019). Creating effective online customer experiences. Journal of marketing, 83(2), 98-119. [CrossRef]

- Ma, Y. (2021). Elucidating determinants of customer satisfaction with live-stream shopping: An extension of the information systems success model. Telematics and Informatics, 65, 101707. [CrossRef]

- Cele, N. N., & Kwenda, S. (2024). Do cybersecurity threats and risks have an impact on the adoption of digital banking? A systematic literature review. Journal of Financial Crime.

- Shaikh, I. M., & Amin, H. (2024). Influence of innovation diffusion factors on non-users’ adoption of digital banking services in the banking 4.0 era. Information Discovery and Delivery (ahead-of-print).

- Park, J., Yoo, J. W., Cho, Y., & Park, H. (2024). Understanding switching intentions between traditional banks and Internet-only banks among Generation X and Generation Z. International Journal of Bank Marketing, 42(5), 1114-1141. [CrossRef]

- Raza, S. A., Umer, A., Qureshi, M. A., & Dahri, A. S. (2020). Internet banking service quality, e-customer satisfaction and loyalty: the modified e-SERVQUAL model. The TQM Journal, 32(6), 1443-1466. [CrossRef]

- Zia, A. (2022). Discovering the linear relationship of service quality, satisfaction, attitude and loyalty for banks in Albaha, Saudi Arabia. PSU Research Review, 6(2), 90-104. [CrossRef]

- Supriyanto, A., Wiyono, B. B., Burhanuddin, B., & Olan, F. (2021). Effects of service quality and customer satisfaction on loyalty of bank customers. Cogent Business & Management, 8(1), 1937847. [CrossRef]

- Lei, Z., Duan, H., Zhang, L., Ergu, D., & Liu, F. (2022). The main influencing factors of customer satisfaction and loyalty in city express delivery. Frontiers in Psychology, 13, 1044032. [CrossRef]

- Mazhar, M., Hooi Ting, D., Zaib Abbasi, A., Nadeem, M. A., & Abbasi, H. A. (2022). Gauging customers’ negative disconfirmation in online post-purchase behaviour: The moderating role of service recovery. Cogent Business & Management, 9(1), 2072186. [CrossRef]

- Siddique, J., Shamim, A., Nawaz, M., Faye, I., & Rehman, M. (2021). Co-creation or co-destruction: a perspective of online customer engagement valence. Frontiers in Psychology, 11, 591753. [CrossRef]

- Islam, R., Ahmed, S., Rahman, M., & Al Asheq, A. (2021), "Determinants of service quality and its effect on customer satisfaction and loyalty: an empirical study of private banking sector", The TQM Journal, 33(6), 1163-1182. [CrossRef]

- Yüksel, A., & Yüksel, F. (2008). Consumer satisfaction theories: a critical review. Tourist satisfaction and complaining behavior: Measurement and management issues in the tourism and hospitality industry, 65-88.

- Rust, R. T., & Oliver, R. L. (1994). Service quality: Insights and managerial implications from the frontier. Service Quality: New Directions in Theory and Practice, 7(12), 1–19.

- Zhang, J., Chen, W., Petrovsky, N., & Walker, R. M. (2022). The expectancy-disconfirmation model and citizen satisfaction with public services: A meta-analysis and an agenda for best practice. Public Administration Review, 82(1), 147-159. [CrossRef]

- Zamani, E. D., & Pouloudi, N. (2021). Generative mechanisms of workarounds, discontinuance and reframing: a study of negative disconfirmation with consumerised IT. Information systems journal, 31(3), 384-428. [CrossRef]

- Sreelakshmi, CC., & Prathap, S. K. (2020). Continuance adoption of mobile-based payments in Covid-19 context: an integrated framework of health belief model and expectation confirmation model. International Journal of Pervasive Computing and Communications, 16(4), 351-369. [CrossRef]

- Gautam, D. K., & Sah, G. K. (2023). Online Banking Service Practices and Its Impact on E-Customer Satisfaction and E-Customer Loyalty in Developing Country of South Asia-Nepal. Sage Open, 13(3), 1-14. [CrossRef]

- Ayinaddis, S. G., Taye, B. A., & Yirsaw, B. G. (2023). Examining the effect of electronic banking service quality on customer satisfaction and loyalty: an implication for technological innovation. Journal of Innovation and Entrepreneurship, 12(1), 22. [CrossRef]

- Khan, F. N., Arshad, M. U., & Munir, M. (2023). Impact of e-service quality on e-loyalty of online banking customers in Pakistan during the Covid-19 pandemic: mediating role of e-satisfaction. Future Business Journal, 9(1), 23. [CrossRef]

- Anouze, A.L.M. and Alamro, A.S. (2020), "Factors affecting intention to use e-banking in Jordan", International Journal of Bank Marketing, 38(1), 86-112. [CrossRef]

- Park, S., & Han, J. J. (2023). The Effects of Service Clues on Likelihoods of Additional Purchase. Journal of Student Research, 12(4). [CrossRef]

- Quiber, N., D., B. (2023). Impact of online banking in customer’s behavior in San Pablo City, Laguna. Journal Of Third World Economics (JTWE), 1(1), 14-17.

- Berry, L. L., Wall, E. A., & Carbone, L. P. (2006). Service clues and customer assessment of the service experience: Lessons from marketing. Academy of management perspectives, 20(2), 43-57. [CrossRef]

- Borishade, T. T. (2017). Customer experience management and loyalty in healthcare sector: a study of selected private hospitals in Lagos State, Nigeria. Doctoral dissertation, Covenant University, Ota, Nigeria.

- Liu, F., Lai, K. H., Wu, J., & Duan, W. (2021). Listening to online reviews: A mixed-methods investigation of customer experience in the sharing economy. Decision Support Systems, 149, 113609. [CrossRef]

- Prentice, C., & Nguyen, M. (2020). Engaging and retaining customers with AI and employee service. Journal of Retailing and Consumer Services, 56, 102186. [CrossRef]

- Zaid, S., & Patwayati, P. (2021). Impact of customer experience and customer engagement on satisfaction and loyalty: A case study in Indonesia. The Journal of Asian Finance, Economics and Business, 8(4), 983-992.

- Ha, M. T. (2021). The impact of customer experience on customer satisfaction and customer loyalty. Turkish Journal of Computer and Mathematics Education, 12(14), 1027-1038.

- Tjahjaningsih, E., Widyasari, S., Maskur, A., & Kusuma, L. (2021). The Effect of Customer Experience and Service Quality on Satisfaction in Increasing Loyalty. In The 3rd International Conference On Banking, Accounting, Management And Economics (Icobame 2020) (pp. 395-399). Atlantis Press.

- Verhoef, P. C., Lemon, K. N., Parasuraman, A., Roggeveen, A., Tsiros, M., & Schlesinger, L. A. (2009). Customer experience creation: Determinants, dynamics and management strategies. Journal of retailing, 85(1), 31-41. [CrossRef]

- Kamath, P.R., Pai, Y.P., & Prabhu, N.K.P. (2019). Building customer loyalty in retail banking: a serial-mediation approach. International Journal of Bank Marketing, 38(2), 456-484. [CrossRef]

- Kamboj, N., & Singh, G. (2018). Customer satisfaction with digital banking in India: Exploring the mediating role of demographic factors. Indian Journal of Computer Science, 3(2), 9–32.

- Bhatt, A., & Bhatt, S. (2016). Factors affecting customer adoption of mobile banking services. The Journal of Internet Banking and Commerce, 21(1), 1.

- Sambaombe, J. K., & Phiri, J. (2021). An analysis of the impact of online banking on customer satisfaction in commercial banks based on the TRA model (a case study of stanbic bank Lusaka main branch). Open Journal of Business and Management, 10(1), 369-386. [CrossRef]

- Wang, S. H., & Pang, Y. L. (2021). Demographics and customer satisfaction. EPRA International Journal of Environmental Economics, Commerce and Educational Management, 8(9), 1-6.

- Hair, J.F., Black, W.C., Babin, B.J., & Anderson, R.E. (2010). Multivariate Data Analysis. London:Pearson.

- Rahi, S. (2017). Research design and methods: A systematic review of research paradigms, sampling issues and instruments development. International Journal of Economics & Management Sciences, 6(2), 1-5.

- Turner, D. P. (2020). Sampling Methods in Research Design. Headache: The Journal of Head & Face Pain, 60(1).

- Bouafi, S. (2020). The Effects of Digital Banking on Customer Experience, Customer Satisfaction, and Customer Loyalty in Morocco. Master's thesis, Eastern Mediterranean University.

- Altobishi, T., Erboz, G., & Podruzsik, S. J. I. J. O. M. S. (2018). E-Banking effects on customer satisfaction: The survey on clients in Jordan Banking Sector. International Journal of Marketing Studies, 10(2), 151-161. [CrossRef]

- Wolfinbarger, M., & Gilly, M. C. (2003). eTailQ: dimensionalizing, measuring and predicting etail quality. Journal of retailing, 79(3), 183-198. [CrossRef]

- Flavián, C., Guinalíu, M., & Gurrea, R. (2006). The role played by perceived usability, satisfaction and consumer trust on website loyalty. Information & management, 43(1), 1-14. [CrossRef]

- Christine Roy, M., Dewit, O., & Aubert, B. A. (2001). The impact of interface usability on trust in web retailers. Internet research, 11(5), 388-398. [CrossRef]

- Kirakowski, J., & Cierlik, B. (1998, October). Measuring the usability of web sites. In Proceedings of the Human Factors and Ergonomics Society annual meeting (Vol. 42, No. 4, pp. 424-428). Sage CA: Los Angeles, CA: SAGE Publications.

- Chahal, H., & Dutta, K. (2015). Measurement and impact of customer experience in banking sector. Decision, 42, 57-70. [CrossRef]

- Garg, R., Rahman, Z., & Kumar, I. (2010). Evaluating a model for analyzing methods used for measuring customer experience. Journal of Database Marketing and Customer Strategy Management, 17(2), 78-90. [CrossRef]

- Klaus, P. P., & Maklan, S. (2013). Towards a better measure of customer experience. International journal of market research. 55(2, 227-246. [CrossRef]

- Liang, C. J., Wang, W. H., & Farquhar, J. D. (2009). The influence of customer perceptions on financial performance in financial services. Marketing, 27(2), 129-149. [CrossRef]