Submitted:

03 December 2024

Posted:

04 December 2024

You are already at the latest version

Preprints on COVID-19 and SARS-CoV-2

Abstract

In the wake of numerous banking panics plaguing the nation’s economic stability, a strengthened structure was implemented to replace the country’s largely fragile and fragmented banking system. This came in the form of the United States Federal Reserve, an independent body tasked with ensuring economic stability. Since its implementation by Congress in 1913, the Federal Reserve has served as the United States’ primary decentralized centralized banking system. What began as a small and divisive banking system, has today become the largest and most powerful economic institution, not only in the U.S., but the world. The purpose of this paper is to provide data-driven, objective insights into the various tools employed by the Fed, their effectiveness, limitations, criticisms, and an outlook for the future of the central banking system in a growing digital world.

Keywords:

monetary policy

; federal reserve

; economic stability

; banking system

; price stability

; maximum employment

; inflation control

; deflation avoidance

; long-term interest rates

; financial system stability

; macroeconomic goals

; open market operations

; OMOs

; treasury bills

; government bonds

; expansionary monetary policy

; contractionary monetary policy

; discount rate

; reserve requirement

; liquidity control

; Quantitative Easing

; QE

; monetary tools

; short-term interest rates

; asset purchases

; GDP growth

; economic growth

; Japan

; Asian Financial Crisis

; U.S. financial crisis

; COVID-19 pandemic

; RRR

; reserve requirement ratio

; People’s Bank of China

; 2008 financial crisis

; Volcker Era

; interest rate

; inflation rate

; free market

; laissez-faire

; stagflation

; Japan’s lost decade

; decentralized currencies

; blockchain technology

; Bitcoin

; Ethereum

; digital assets

; central bank digital currencies

; CBDCs

; financial innovation

; systemic risks

; wealth

1. Introduction

Monetary Policy is primarily aimed at achieving key macroeconomic goals, with the Federal Reserve focusing on maintaining price stability and maximum employment. Price stability refers to controlling inflation, typically targeted at 2-3% annually. By keeping inflation stable, the Fed helps protect purchasing power, encourage savings, and foster investment, while also avoiding deflation, which can harm economic growth. On the other hand, maximum employment reduces unemployment to its natural level at around 4-5%, where the economy is growing efficiently without triggering inflation. High employment boosts productivity and strengthens consumer spending, which drives economic growth. Another important goal is to maintain moderate long-term interest rates, which supports sustainable economic growth by encouraging investment and consumption. Low rates make borrowing cheaper for businesses and consumers, driving spending and stimulating demand. Lastly, the financial system’s stability is crucial for preventing financial crises. The Fed works to ensure the health of financial institutions and markets, managing risks that could disrupt the economy. By achieving these objectives, the Federal Reserve helps create a stable environment conducive to long-term growth and prosperity.

2. Monetary Policy Tools

The first of the three major tools utilized by the Federal Reserve is Open Market Operations. Simply put, OMOs are the Fed’s purchasing and selling of treasury bills and government bonds to and from banks. Expansionary monetary policy entails the central bank purchasing treasury bills, thereby injecting cash into banks, filling their reserves far above the reserve requirement. This boosts the supply of cash in the economy and encourages banks to lend more, lowering the federal funds rate, and making loans cheaper for businesses and consumers. On the contrary, in contractionary monetary policy, the Fed sells treasury bills and bonds to banks, leading to less money for the banks to loan out and a higher interest rate in markets.

The 2nd policy that the Fed uses that directly reflects its stance on monetary policy is the discount rate. This is the most basic form of monetary policy which is closest to general public sentiment of the Fed’s power coming from its ability to control the interest rate. Through shifting the discount rate, the interest rate banks are charged for loans, the price of money is shifted, and its effects are tricked down, eventually reaching businesses and consumers. This strategy is frequently exercised by the Fed to control liquidity throughout the banking system.

The final primary tool in controlling the money supply and stabilizing the economy is the reserve requirement. The central bank sets a legal minimum percentage of funds which the bank must keep in reserves, and not lend to customers. During a highly expansionary phase in the economy, the Fed might adopt a contractionary monetary policy by increasing the reserve requirement and cutting the money supply, thus increasing the interest rate and lowering spending throughout. Although mostly effective, this strategy is used sparingly as sudden changes can often cripple individual banks’ operations.

Other policies are used in specific economic times, for example Quantitative Easing. This strategy is used during a recession where short-term interest rates are near zero and the Fed wants to bolster economic growth through a larger money supply and lower long-term interest rates. Large-scale purchases of assets like government bonds are made by the Fed, thereby boosting the money that banks have available to lend as well as making bonds more expensive and inversely lowering their yield, contributing to a lower long-term interest rate. This motivates businesses and consumers to invest in major long-term projects and make more expensive purchases like homes.

3. Effectiveness and Limitations of Monetary Policy Tools

Monetary policies are implemented after thorough consideration of their direct effects and however positive the short-term effects may be, the long-term effects are difficult to predict; the devil is in the details.

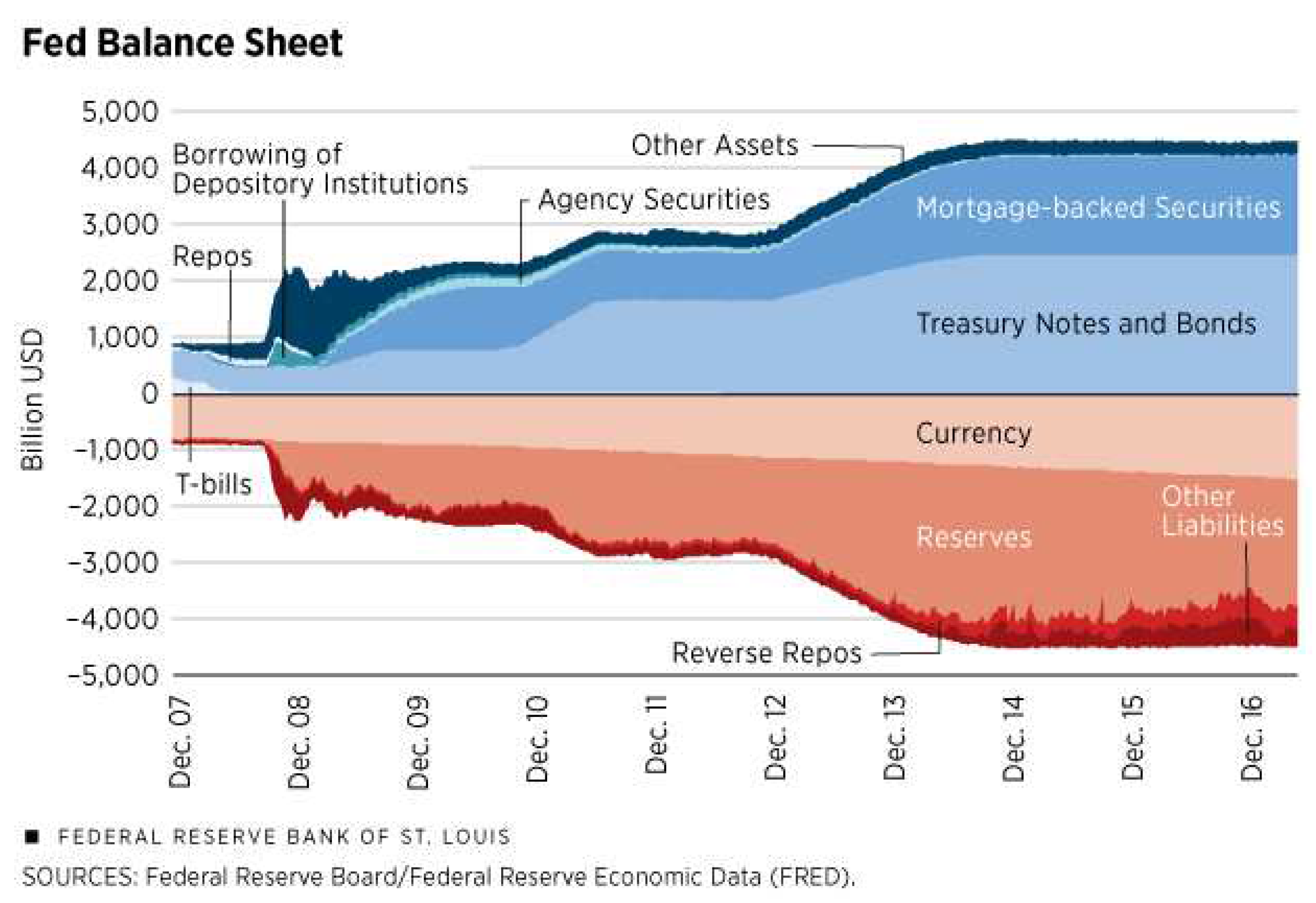

For example, after the 1997 Asian Financial Crisis, Japan began an extensive quantitative easing effort, investing heavily in private debt and stocks. The effect was beneficial initially, as Japan’s GDP rose from $4.1 trillion in 1998 to $6.27 trillion in 2012. However, this short-lived gain soon retracted back to $4.44 trillion by 2015. Similar policies have also been implemented in the United States, with the Fed launching QE1, QE2, and QE3, purchasing $4.5 trillion in assets. This slowly reduced long-term treasury yields and interest rates by 1% and lowered unemployment by 5% over 6 years. Some inevitable adverse effects of QE exist, though, including disproportionately benefiting wealthy individuals who have a higher portion of their net worth in assets like stocks, owning 87% of stocks.

Reserve requirements can also significantly impact market dynamics, with a small change having mammoth impacts on liquidity. In 2008, the People’s Bank of China brought down the reserve requirement ratio from 17.5% to 15.5% in response to the 2008 financial crisis. This spurred a $1.3 trillion increase in lending in the nation, bolstering economic growth by 9.4%. The United States adopted more aggressive RRR changes during the COVID-19 pandemic, dropping it to 0%. This boosted bank lending and contributed to aiding small businesses and individuals hurt during the period. Some pitfalls arise as even incremental changes in reserve requirements can have adverse effects on the functioning of smaller banks and can greatly destabilize them.

Figure 1.

Effects of Quantitative Easing on Fed’s Assets.

Additionally, discount rates can help provide funds as a last resort during liquidity crises. This has been proven to be highly effective in keeping the economy from collapsing. For example, the Global Financial Crisis of 2008 was the most severe worldwide economic crisis after the 1929 Wall Street Crash. To combat this, the Federal Reserve lowered discount rates from 6.25% to 0.5% to quickly inject money supply into the economy. This helped U.S. banks stabilize preventing the collapse of the financial system. One of its drawbacks is the stigma of borrowing; banks are reluctant to borrow money from the central bank due to the perception of them seeming weak, diminishing the effectiveness of the discount rate. Additionally, there is a moral hazard associated with this policy, where banks may overly rely on the central bank to bail them out, resulting in risky behavior. Finally, there is the problem of the limited impact of this tool. It only affects banking liquidity, with very limited impact on business and consumer loans.

Finally, Open Market Operations (OMO) can significantly increase the amount of money in circulation, helping banks with their target interest rate and supporting the economy. For example, during the Volcker Era (early 80s), the Fed aggressively sold government bonds to combat inflation as credit became more expensive for households and businesses. The result of this action was monumental, lowering the staggering inflation rate of 13.5% in 1980 to a low of 3.2% by 1983, although at the cost of a recession. However, an adverse effect of the OMO is that it primarily influences short-term rates and liquidity but can’t help with long-term economic stability. Another main problem is dependence on market dynamics. It is necessary for financial institutions to comply with the central bank’s goals, but they don’t always align with central banks, which may result in OMOs being ineffective.

4. Criticisms of Central Bank Policies

Although there may be many positive attributes to monetary policy, there are also many negative attributes and criticisms against it as well. First of all, it goes against the idea of free market and laissez-faire principles since it involves direct government control. Many critics point out that monetary policy tools allow the government to have more influence on the economy. Additionally, there are many instances where this policy has failed, undermining its true potential of having overall positive effects. Some notable instances are stagflation in the 1970s and Japan’s lost decade of the 1990s.

During the 1970s, the Federal Reserve and other central banks struggled to combat the combination of high inflation and high unemployment. Due to concerns about job losses, policymakers did nothing to combat it, resulting in prolonged economic instability. This shows how monetary failed to do its job, illustrating a severe criticism utilized by adversaries of monetary policy. Another example, Japan’s lost decade (1990s), illustrates how monetary policy failed to keep the economy stable, diminishing the power of the policy. The Bank of Japan decided to tighten monetary policy due to the bursting of a massive asset bubble in the late 1980s. However, when they shifted to quantitative easing, it was too late, sending the economy into a downward spiral. This would cause Japan to suffer a prolonged period of stagnant growth and deflation. Critics often use these examples to criticize monetary policy, especially since these were failures that could have been avoided.

Besides affecting the economy, monetary policy also increases the gap between income. People who own massive amounts of financial assets can make much more money, increasing the gap between socioeconomic classes. Also on a grander scale, monetary easing resulting in competitive devaluations can cause arguments between countries, destabilizing global trade and financial systems. All these different reasons help illustrate the criticisms of central bank policies, revealing its fair share of pitfalls.

5. The Future for Central Banks (Challenges and Opportunities)

The rise of decentralized currencies, such as Bitcoin and Ethereum, presents unique challenges and opportunities for central banks like the Federal Reserve. Unlike traditional fiat currencies, decentralized currencies operate without a central authority, relying on blockchain technology to manage and verify transactions. This growing use of decentralized currencies reduces the Federal Reserve’s direct influence over the money supply and financial stability. Decentralized currencies challenge the Fed’s ability to control inflation and growth. The U.S. government and the Federal Reserve are exploring regulatory frameworks to address these concerns. Efforts include developing regulations that increase transparency and oversight for digital asset transactions and integrating central bank digital currencies (CBDCs) to provide a government-backed digital alternative. Measures also focus on limiting risks like financial crimes, fraud, and system vulnerabilities that could destabilize broader financial markets.

The tension between promoting financial innovation and ensuring stability continues to challenge central banks worldwide. Policymakers are engaged in ongoing research and discussions to strike a balance between fostering technological advancements and maintaining control over the financial system.

6. Conclusion

In large, monetary economic policies have had beneficial outcomes for individuals and businesses and have aided in significant economic relapses post-financial crises. These tools, including reserve requirements, the discount rate, open market operations, and quantitative easing, are crucial to guiding our economy in the right direction, curbing inflation, and promoting long-term growth. Each tool must be exercised prudently, and the possible adverse effects should be deliberated upon before taking highly consequential measures. Each tool carries risks, such as fractured lending, long-term externalities, or increased wealth inequality—consequences that must be weighed against the potential short-term and long-term benefits. Central banks must remain flexible, adjusting their strategies and using data-driven approaches to decision-making, especially in the new digital age, thereby ensuring seamless coordination of tools used to maintain economic stability and promote sustainable growth.

References

- Antoni, E. J. “Time to End the Fed and Its Mismanagement of Our Economy.” The Heritage Foundation, 2 Oct. 2023, www.heritage.org/monetary-policy/commentary/time-end-the-fed-and-its-mismanagement-our-economy.

- Board of Governors of the Federal Reserve System. “Monetary Policy: What Are Its Goals? How Does It Work?” Board of Governors of the Federal Reserve System, 29 July 2021, www.federalreserve.gov/monetarypolicy/monetary-policy-what-are-its-goals-how-does-it-work.htm.

- Borio, Claudio, and Claudio Borio. “Toughest Challenges for Monetary Policy Are Probably Still to Come - OMFIF.” OMFIF, 15 Nov. 2024, www.omfif.org/2024/11/toughest-challenges-for-monetary-policy-are-probably-still-to-come/. Accessed 17 Nov. 2024.

- Brock, Thomas. “Monetary Policy Meaning, Types, and Tools.” Investopedia, 2024, www.investopedia.com/terms/m/monetarypolicy.asp.

- Brock, Thomas. “Quantitative Easing Definition.” Investopedia, 2021, www.investopedia.com/terms/q/quantitative-easing.asp.

- Callen, Tim, and Jonathan Ostry. “Japan’s Lost Decade --- Policies for Economic Revival.” Www.imf.org, 13 Feb. 2003, www.imf.org/external/pubs/nft/2003/japan/index.htm.

- Eisinger, Jesse. “The Fed Keeps Getting More Powerful. Is It Bad for America?” ProPublica, 5 Aug. 2022, www.propublica.org/article/lev-menand-fed-unbound-interview.

- “Federal Reserve Board - Central Bank Digital Currency (CBDC).” Www.federalreserve.gov, 2 Aug. 2024, www.federalreserve.gov/central-bank-digital-currency.htm.

- Federal Reserve Bank of, St. Louis. “Federal Reserve System History and Purpose | in Plain English | St. Louis Fed.” Stlouisfed.org, 2019, www.stlouisfed.org/in-plain-english/history-and-purpose-of-the-fed.

- “Remarks on Monetary Policy and the, U.S. Economic Outlook.” Stlouisfed.org, 2024, www.stlouisfed.org/from-the-president/remarks/2024/remarks-monetary-policy-and-u-s-economic-outlook. Accessed 17 Nov. 2024.

- “Reserve Requirement - an Overview | ScienceDirect Topics.” Www.sciencedirect.com, www.sciencedirect.com/topics/economics-econometrics-and-finance/reserve-requirement.

- Sanchez, Joaquina. “Discount Rate—Explanation, Definition and Examples.” Valutico, 12 Mar. 2024, www.valutico.com/understanding-the-discount-rate/.

- Williamson, Stephen. “Quantitative Easing: How Well Does This Tool Work?” Stlouisfed.org, Federal Reserve Bank of St. Louis, 18 Aug. 2017, www.stlouisfed.org/publications/regional-economist/third-quarter-2017/quantitative-easing-how-well-does-this-tool-work.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.