Submitted:

30 November 2024

Posted:

03 December 2024

You are already at the latest version

Abstract

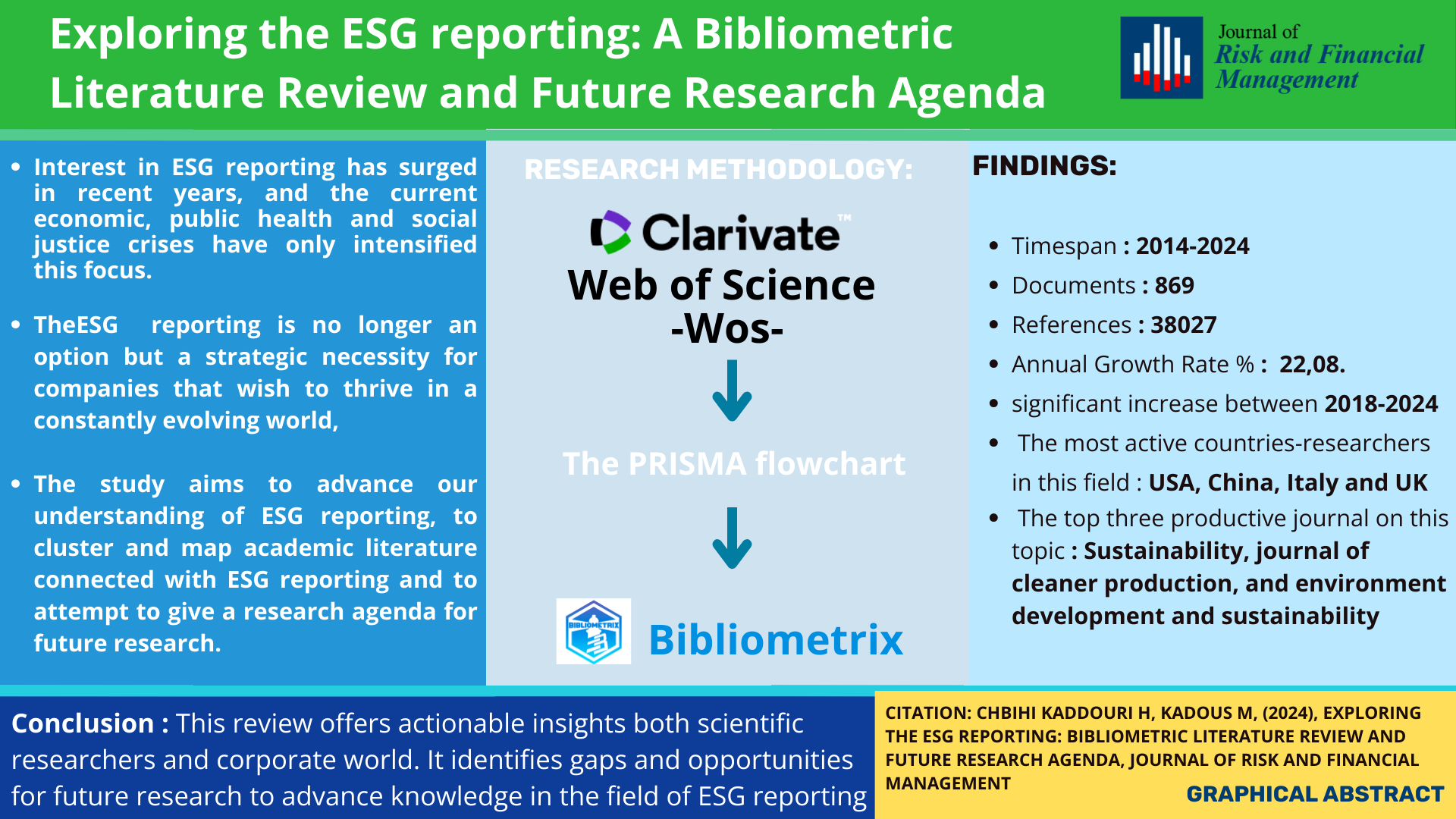

ESG reporting has attracted a lot of attention during the past several decades. However, bibliometric analysis on this topic remains limited. This paper aims to advance our understanding of ESG reporting, to cluster and map academic literature connected with ESG reporting and to attempt to give a research agenda for future research. We undertake a bibliometric analysis review of the current literature to discover present and future research directions of ESG reporting. In this study, the authors used datasets from the Web of Science (WoS) database, covering 869 research papers from 2014 to 2024 and using the Bibliometrix package also known as “Bibliometrix 3.0” or “Biblioshiny”. Bibliometric analysis offers a comprehensive overview of a certain field, such as authorship trends, geographical spread, research importance, influential authors and publications, new concepts, and emerging ideas. This research has implications for both scientific researchers and corporate world.

Keywords:

1. Introduction

- RQ1. What are the current trends in the ESG reporting field regarding publications, citations, journals, authors, and affiliated countries?

- RQ2. What are the current developments in this area of study?

- RQ3. What are the main gaps and research questions that require future research in the ESG reporting field?

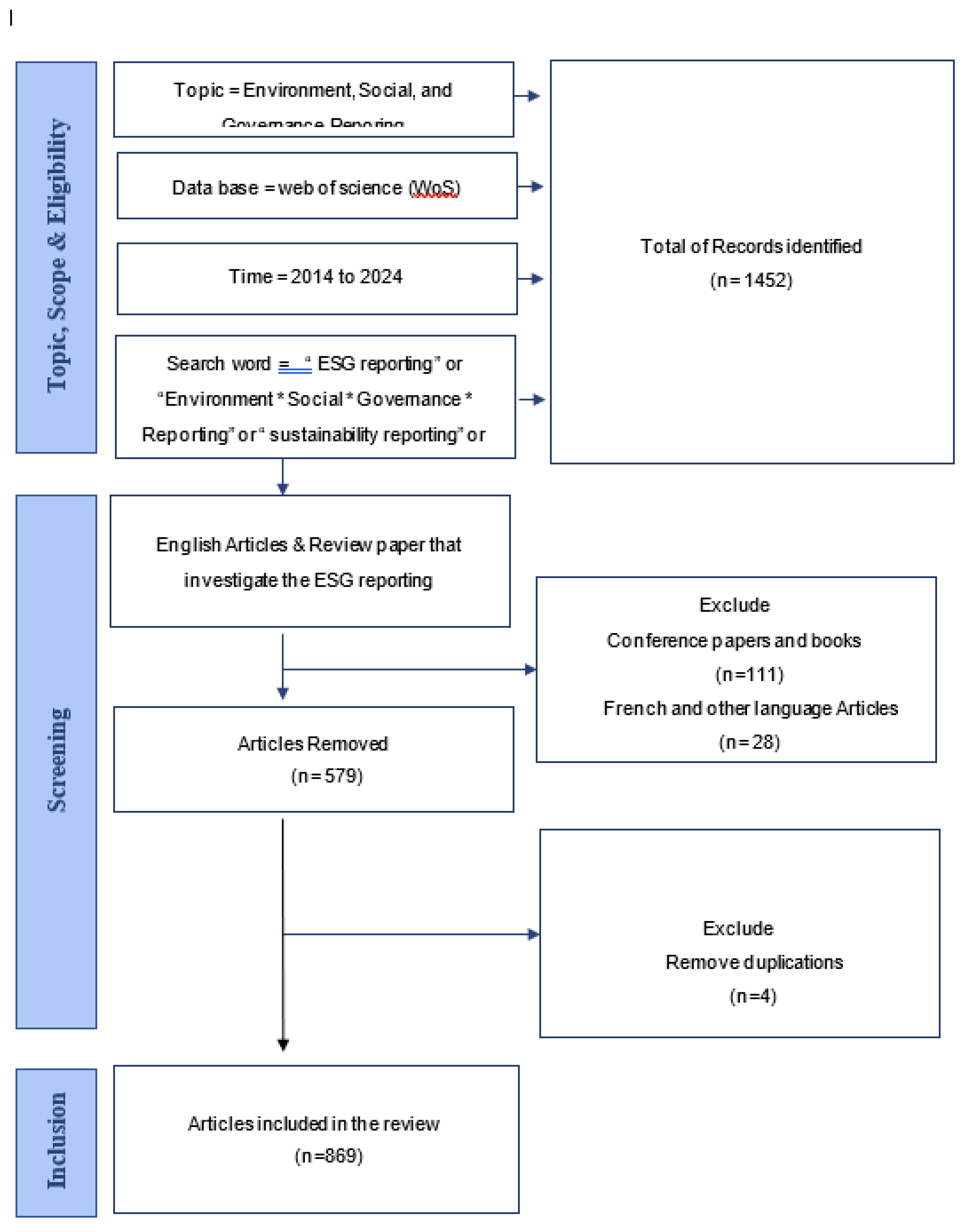

2. Research Methodology: Procedure and Strategies

3. Findings and Discussion: Bibliometrics and Trends

3.1. List of Top Cited Articles and Most Productive Journals on “ESG Reporting”

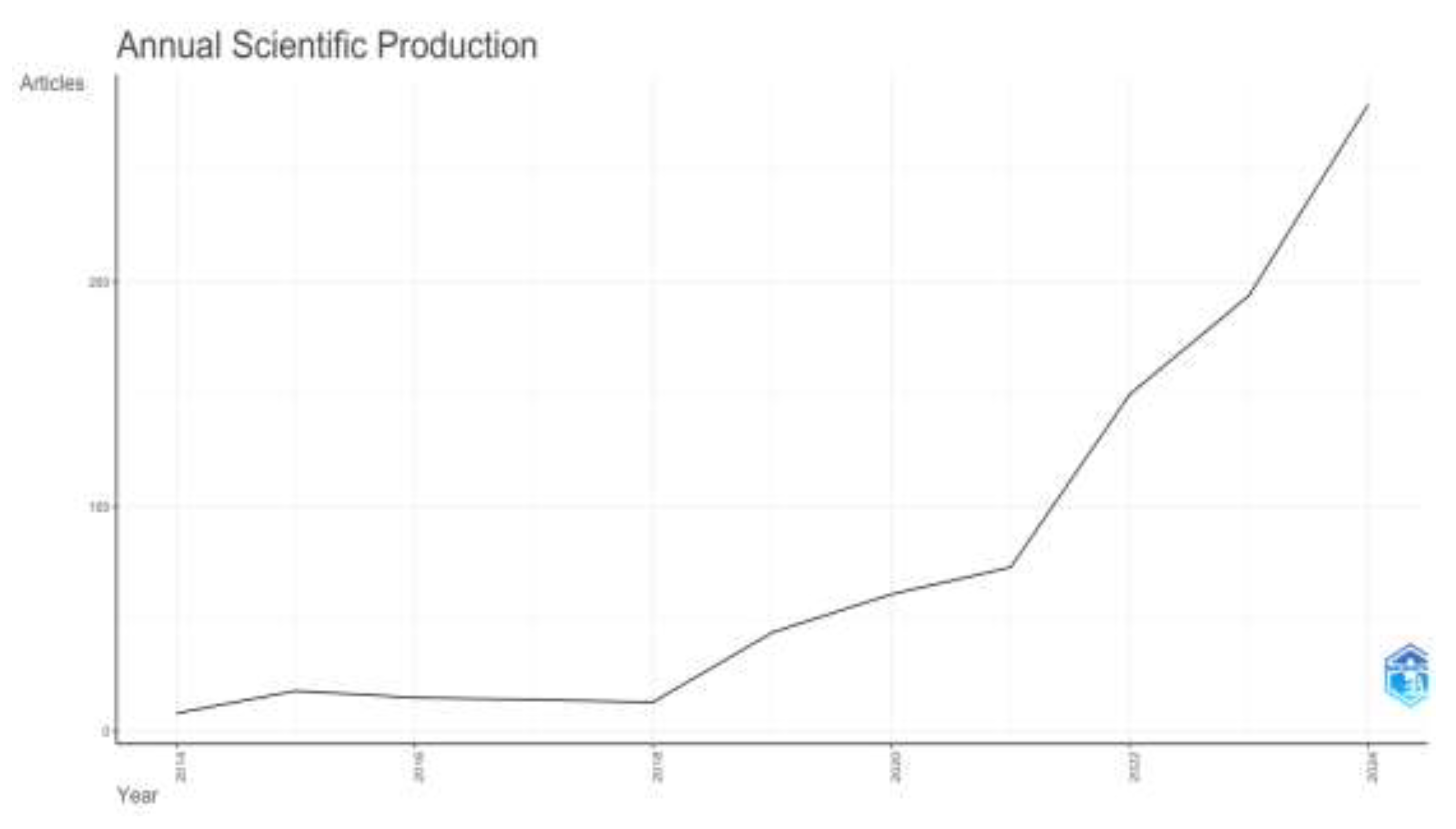

3.2. Research Production Over Years

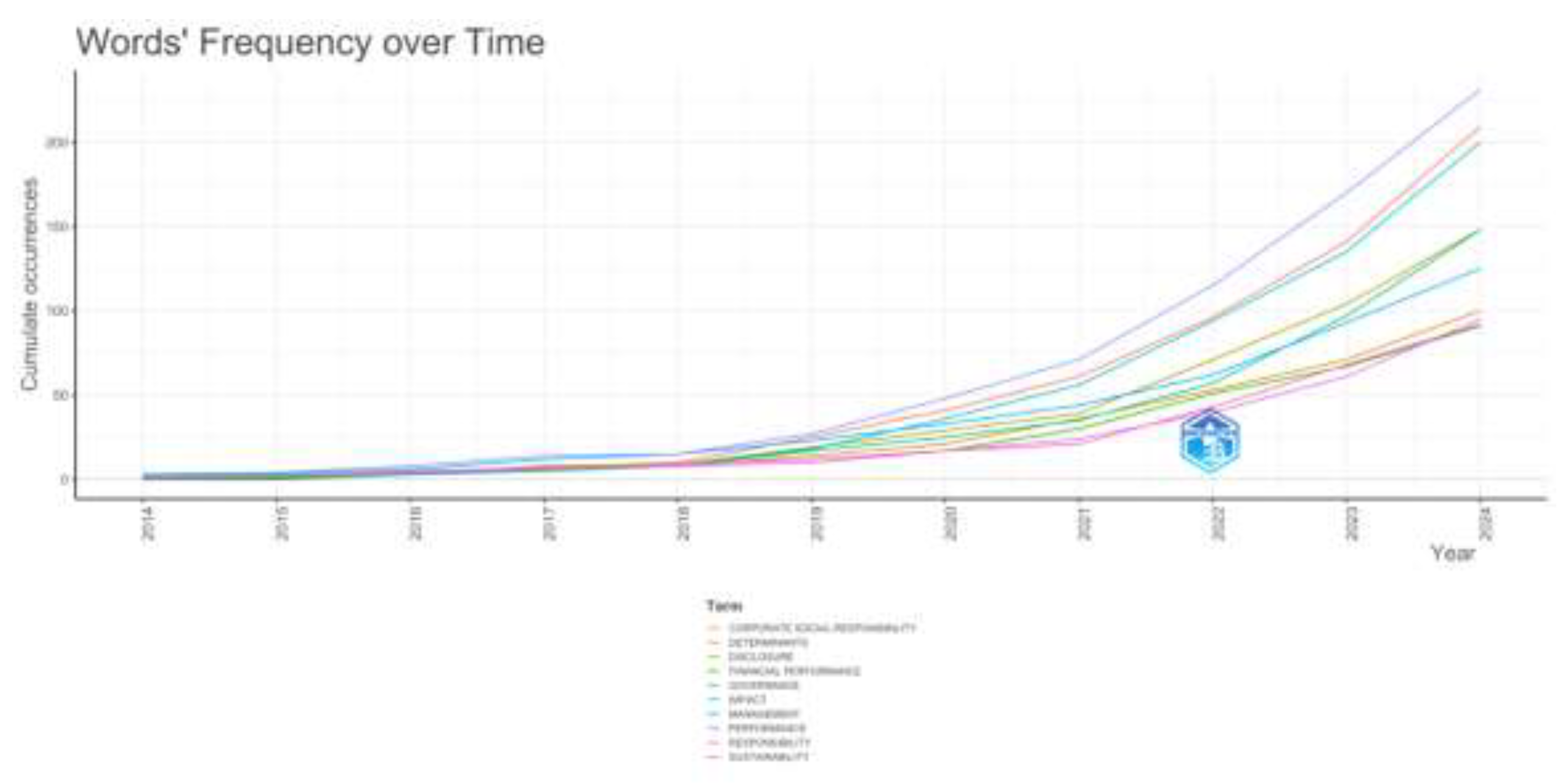

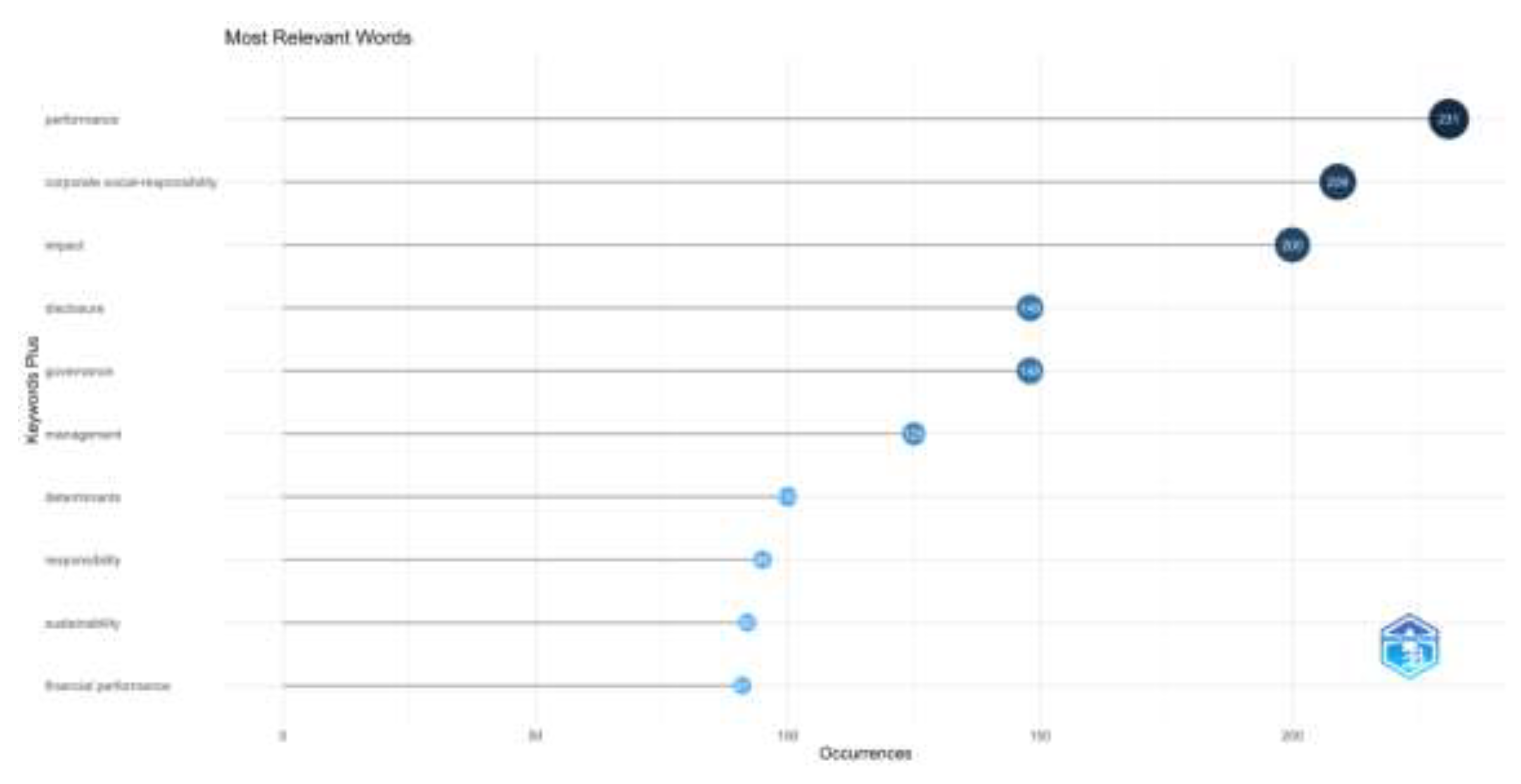

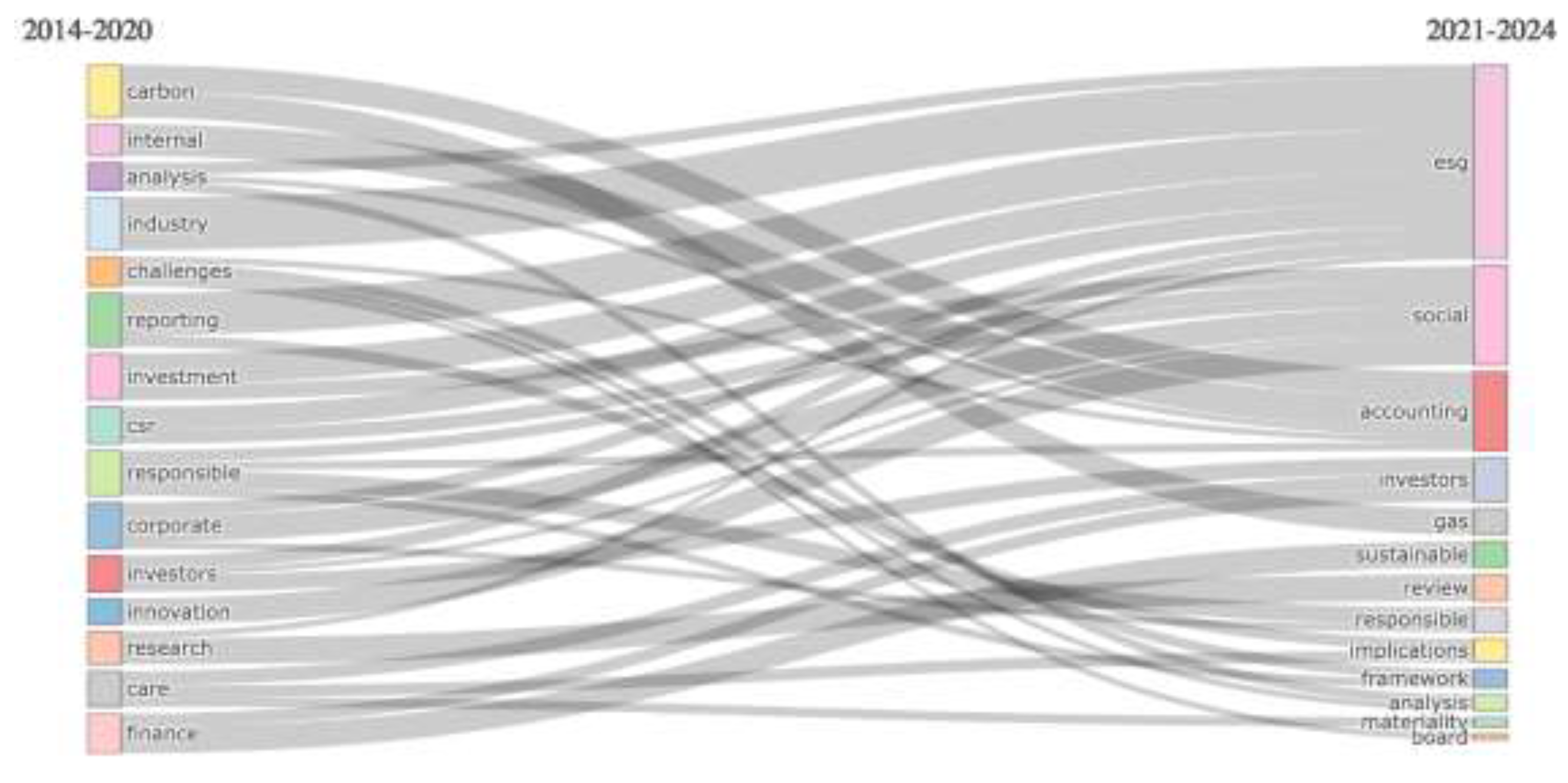

3.3. Trends Topic Over Time

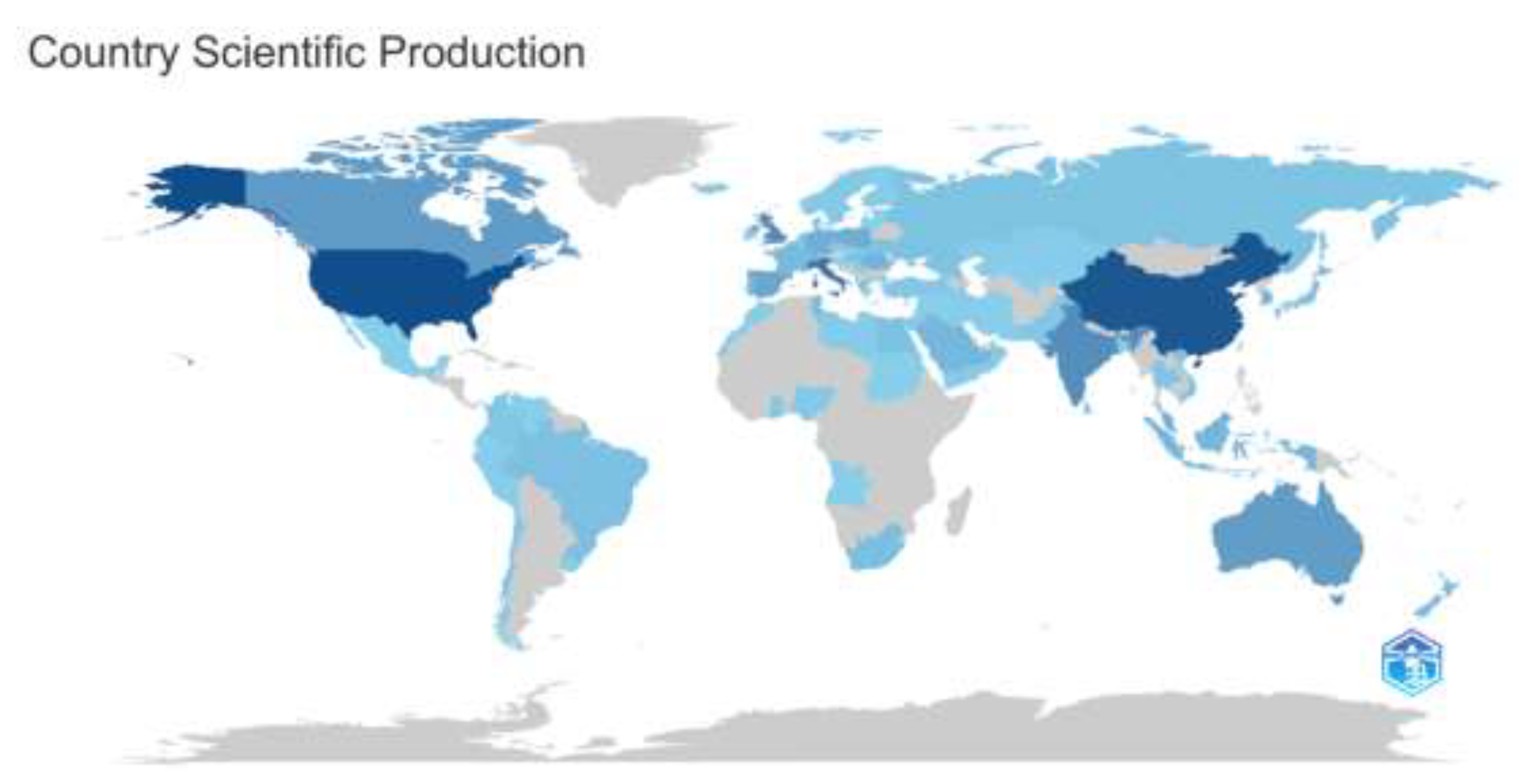

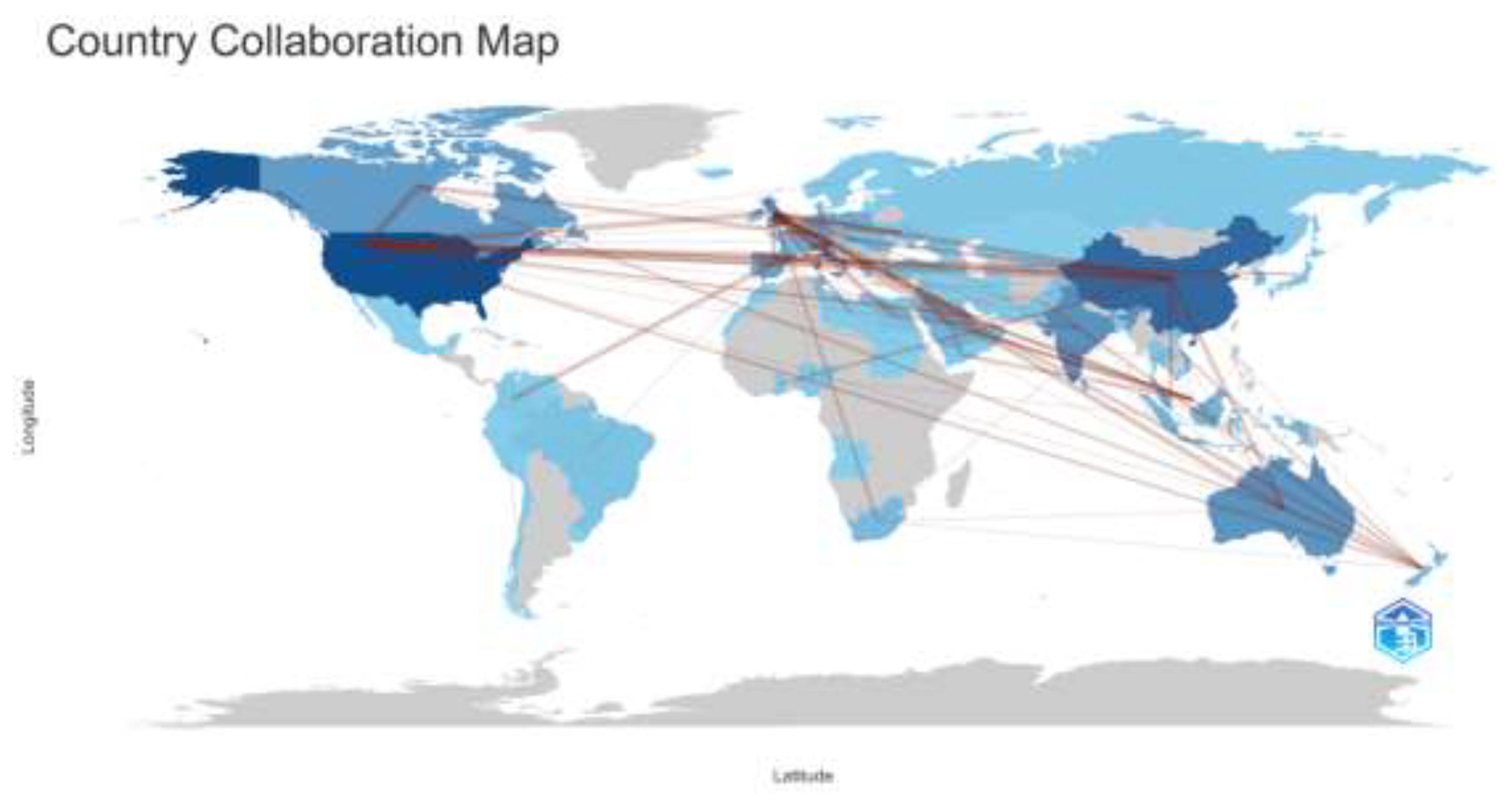

3.4. Top 10 Contributing Countries

| Rank | Country | No. of articles and % (N = 1727) | Total citation | Average articles citation |

|---|---|---|---|---|

| 1 | USA | 340 (19) | 2535 | 25.40 |

| 2 | CHINA | 315 (18) | 723 | 8.80 |

| 3 | ITALY | 227 (13) | 1838 | 25.90 |

| 4 | UK | 172 (9,9) | 3700 | 77.10 |

| 5 | INDIA | 163 (9,43) | 760 | 14.60 |

| 6 | CANADA | 130 (7,52) | 551 | 15.30 |

| 7 | AUSTRALIA | 124 (7,18) | 1141 | 27.20 |

| 8 | SPAIN | 96 (5,55) | 280 | 26.20 |

| 9 | POLAND | 83 (4,80) | 787 | 9.70 |

| 10 | GERMANY | 77 (4,45) | 1283 | 44.20 |

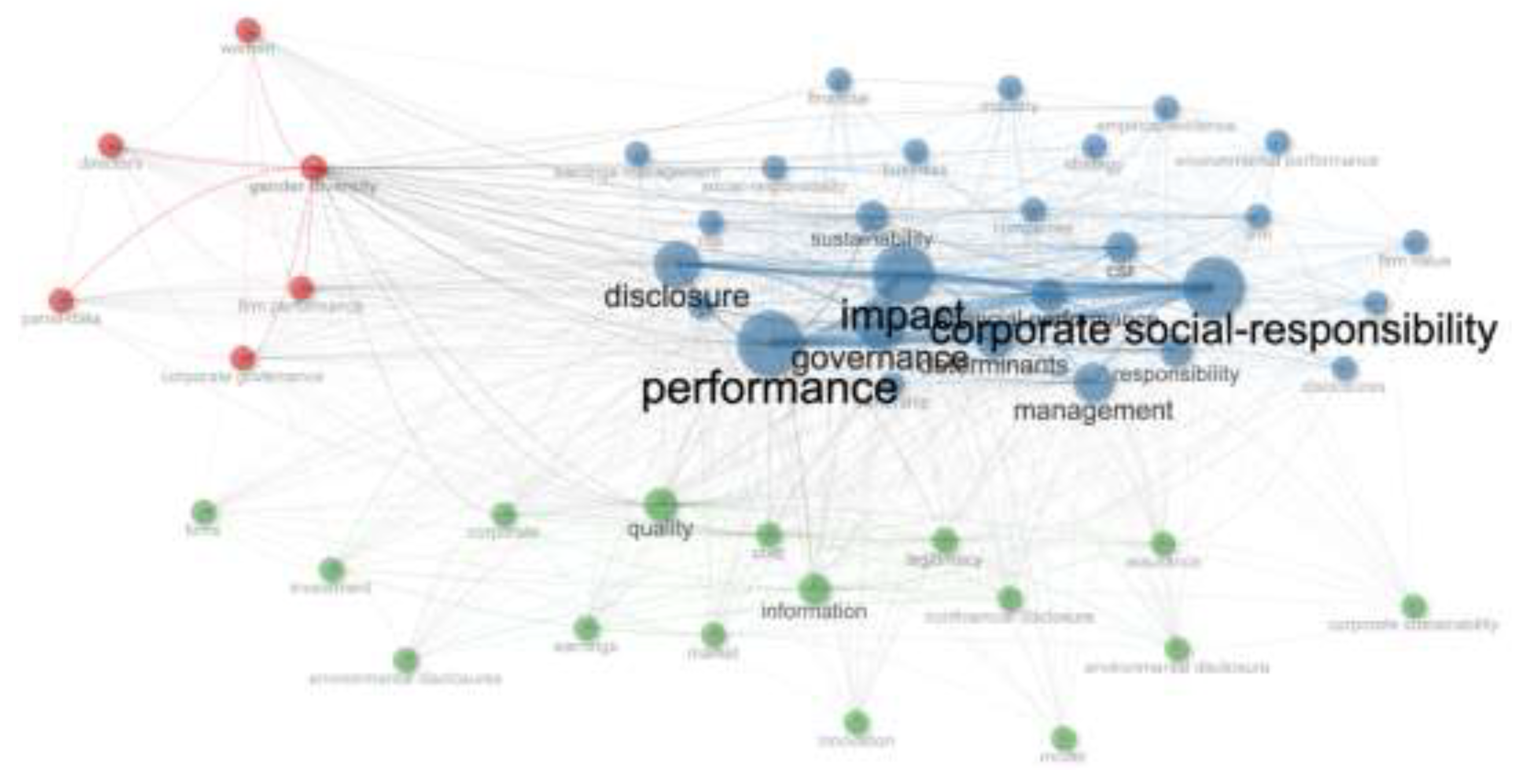

3.5. Thematic evolution and trends linking

3.5.1. Co-Occurrence Analysis

3.5.2. Thematic Evolution

4. Conclusions and Future Research Directions

Author Contributions

Conflicts of Interest

Funding

Data Availability

Acknowledgments

References

- Adriaanse, L.; Rensleigh, C. (2013), Web of science, scopus and google scholar: A content comprehensiveness comparison. Electron Libr. Emerald group publishing Limited, Leeds, Vol.31No.6, PP.727–744. [CrossRef]

- Ahmed, F.; Hussainey, K. (2023). A bibliometric analysis of political connections literature. Review of Accounting and Finance, Emerald group publishing Limited, Leeds, Vol.22 No.2, PP.206–226. [CrossRef]

- Alareeni, B.A. Alareeni, B.A. and Hamdan, A. (2020), "ESG impact on performance of US S&P 500-listed firms", Corporate Governance, Vol. 20 No. 7, pp. 1409-1428. [CrossRef]

- Almici, A, (2024), Does sustainability in executive remuneration matter? The moderating effect of Italian firms' corporate governance characteristics, Meditari accountancy research, Emerald group publishing Limited, Leeds, Vol. 31 No.7, PP.49-87. [CrossRef]

- Arduino, Francesca Romana, Bruno Buchetti, and Murad Harasheh. 2024. The veil of secrecy: Family firms’ approach to ESG transparency and the role of institutional investors. Finance Research Letters, Elsevier SCI LTD, London, Vol.62. [CrossRef]

- Aria, M., & Cuccurullo, C. (2017). bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of informetrics, Elsevier SCI LTD, London, Vol. 11 No.4, PP. 959-975. [CrossRef]

- Balatbat M, Siew R, Carmichael D, (2012), ESG scores and its influence on firm performance: Australian evidence Australian School of Business School of Accounting, pp. 1-30.

- Bergman, Mark S., Ariel J. Deckelbaum, and Brad S. Karp. 2020. Introduction to ESG. The Harvard Law School Forum on Corporate Governance. Available online: https://corpgov.law.harvard.edu/2020/08/01/introduction-to-esg/ (accessed on 30 August 2024).

- Boffo, R., Patalano R. (2020) ESG Investing: Practices, Progress and Challenges. Open Access Library Journal, OECD Paris, Vol.11 No.1. [CrossRef]

- Briner, R.B.; Denyer, D.; Rousseau, D.M. (2009). Evidence-Based Management: Concept Cleanup Time? Academy of Management Perspectives, Vol.23, No 4, PP. 19-32. [CrossRef]

- Cao, June; Huang, Zijie; Kristanto, Ari Budi; Scott, Tom, (2024), Pacific accounting review in 2013-2023: A bibliometric analysis, Pacific accounting review, Emerald group publishing Limited, Leeds, Vol. 36 No.3/4, PP.297-347. [CrossRef]

- Chahed, Y, (2021), Words and Numbers: Financialization and Accounting Standard Setting in the United Kingdom, Contemporary accounting research, Wiley, Hoboken, Vol. 38 No.1, PP.302-337. [CrossRef]

- Christensen, HB; Hail, L; Leuz, C, (2021). Mandatory CSR and sustainability reporting: Economic analysis and literature review, Review of accounting studies, Springer, Dordrecht, Vol. 26 No.3. PP. 1176-1248. [CrossRef]

- Dilling, PFA; Harris, P; Caykoylu, S, (2024), The Impact of Corporate Characteristics on Climate Governance Disclosure, Sustainability, MDPI, Basel, Vol. 16 No.5. [CrossRef]

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N. and Lim, W.M. (2021), “How to conduct a bibliometric analysis: An overview and guidelines”, Journal of Business Research, Elsevier SCI LTD, London, Vol. 133, pp. 285-296. [CrossRef]

- El-Jourbagy, J; Gura, PP, (2022). In Space, No One Can Hear You're Green: Standardization of Environmental Reporting, the SEC's Proposed Climate Change Disclosure Rules, and Remote Sensing Technology, American business law journal, Wiley, Hoboken, Vol. 59 No.4, PP.333-820. [CrossRef]

- Elkington, J. (1998), "Accounting for the triple bottom line", Measuring Business Excellence, Emerald group publishing Limited, Leeds, Vol. 2 No. 3, pp. 18-22. [CrossRef]

- Gundlach, G.T., Achrol, R.S. (1993). Governance in exchange: Contract law and its alternatives. Journal of Public Policy & Marketing, JSTOR, New York, Vol.12, No.2, PP. 141-155.

- Jain, M.; Sharma, G.D.; Srivastava, M. (2019), Can Sustainable Investment Yield Better Financial Returns: A Comparative Study of ESG Indices and MSCI Indices. Risks, MDPI, Basel, Vo. l7, No.15. [CrossRef]

- Jebe, R, (2019). The Convergence of Financial and ESG Materiality: Taking Sustainability Mainstream, American business law journal, Wiley, Hoboken, Vol. 56 No.3, PP.645-702. [CrossRef]

- Krishnamoorthy, R. (2021) Environmental, Social, and Governance (ESG) Investing: Doing Good to Do Well. Open Journal of Social Sciences, Vol. 9, PP. 189-197, Scientific research, Chicago. [CrossRef]

- Landi G, Sciarelli M, (2018). "Towards a more ethical market: The impact of ESG rating on corporate financial performance," Social Responsibility Journal, Emerald Group Publishing Limited, vol. 15, No.1. [CrossRef]

- Persakis, A, (2024). The impact of climate policy uncertainty on ESG performance, carbon emission intensity and firm performance: Evidence from Fortune 1000 firms, Environment development and sustainability, Springer, Dordrecht, Vol. 26 No.9. PP.24031-2408. [CrossRef]

- Marzuki, Ainulashikin, Fauzias Mat Nor, Nur Ainna Ramli, Mohamad Yazis Ali Basah, and Muhammad Ridhwan Ab Aziz. 2023. The Influence of ESG, SRI, Ethical, and Impact Investing Activities on Portfolio and Financial Performance—Bibliometric Analysis/Mapping and Clustering Analysis. Journal of Risk and Financial Management Vol.16, 321. [CrossRef]

- Mengist W, Soromessa T, Legese G. (2020), Method for conducting systematic literature review and meta-analysis for environmental science research. Methods X, Elsevier SCI LTD, London, Vol.7. [CrossRef]

- Moussa, A S. (2023). The Cost Implications of ESG Reporting: An Examination of Audit Fees in the UK. International Journal of Accounting, Auditing and Performance Evaluation. Preprint, Vol.20, No.(3/4), pages 399-420. [CrossRef]

- Sulkowski, A; Jebe, R, (2022). Evolving ESG Reporting Governance, Regime Theory, and Proactive Law: Predictions and Strategies, American business law journal Wiley, Hoboken, Vol. 59 No.3, PP.449-503. [CrossRef]

- Wang, Haijun, Shuaipeng Jiao, and Chao Ma. 2024. The impact of ESG responsibility performance on corporate resilience. International Review of Economics & Finance Vol.93, PP.1115–1129. [CrossRef]

- Wen, Q; Shao, SP; Wang, YP; Hong, JK; Lu, K; Zhao, QY; Zheng, HR; Ma, L, (2023). Does creation-oriented culture promote ESG activities? Evidence from the Chinese market, Global environmental change-human and policy dimensions, Elsevier SCI LTD, London, Vol. 86 No.1, PP.254-607. [CrossRef]

| Description | Results |

|---|---|

| Timespan | 2014:2024 |

| Sources (Journals, Books, etc) | 289 |

| Documents | 869 |

| Annual Growth Rate % | 42,64 |

| Document Average Age | 1,97 |

| Average citations per doc | 22,08 |

| References | 38027 |

| Keywords Plus (ID) | 1126 |

| Author's Keywords (DE) | 2410 |

| AUTHORS | |

| Authors | 2273 |

| Authors of single-authored documents | 100 |

| AUTHORS COLLABORATION | |

| Single-authored documents | 113 |

| Co-Authors per Document | 3,01 |

| International co-authorships % | 30,15 |

| Journal | Rank | No of Articles and % |

|---|---|---|

| SUSTAINABILITY | 1 | 131 (54,81) |

| JOURNAL OF CLEANER PRODUCTION | 2 | 28 (11,71) |

| ENVIRONMENT DEVELOPMENT AND SUSTAINABILITY | 3 | 14 (5,85) |

| JOURNAL OF ENVIRONMENTAL MANAGEMENT | 4 | 12 (5,02) |

| ENVIRONMENTAL SCIENCE AND POLLUTION RESEARCH | 5 | 10 (4,18) |

| FRONTIERS IN ENVIRONMENTAL SCIENCE | 6 | 7 (2,92) |

| UTILITIES POLICY | 7 | 6 (2,51) |

| CLEAN TECHNOLOGIES AND ENVIRONMENTAL POLICY | 8 | 2 (0,83) |

| ENVIRONMENTAL SCIENCE \& TECHNOLOGY | 9 | 2 (0,83) |

| MANAGEMENT SCIENCE | 10 | 2 (0,83) |

| POLISH JOURNAL OF ENVIRONMENTAL STUDIES | 11 | 2 (0,83) |

| AGRIBUSINESS | 12 | 1 (0,41) |

| ATMOSPHERIC ENVIRONMENT | 13 | 1 (0,41) |

| CARBON BALANCE AND MANAGEMENT | 14 | 1 (0,41) |

| ECOLOGICAL INDICATORS | 15 | 1 (0,41) |

| ECONOMIC COMPUTATION AND ECONOMIC CYBERNETICS STUDIES AND RESEARCH | 16 | 1 (0,41) |

| ENVIRONMENTAL DEVELOPMENT | 17 | 1 (0,41) |

| ENVIRONMENTAL ENGINEERING AND MANAGEMENT JOURNAL | 18 | 1 (0,41) |

| ENVIRONMENTAL POLLUTION | 19 | 1 (0,41) |

| ENVIRONMENTAL PROGRESS \& SUSTAINABLE ENERGY | 20 | 1 (0,41) |

| FOOD POLICY | 21 | 1 (0,41) |

| FRONTIERS IN MARINE SCIENCE | 22 | 1 (0,41) |

| GLOBAL ENVIRONMENTAL CHANGE-HUMAN AND POLICY DIMENSIONS | 23 | 1 (0,41) |

| GLOBAL NEST JOURNAL | 24 | 1 (0,41) |

| INTERNATIONAL JOURNAL OF ENVIRONMENTAL RESEARCH AND PUBLIC HEALTH | 25 | 1 (0,41) |

| INTERNATIONAL JOURNAL OF LIFE CYCLE ASSESSMENT | 26 | 1 (0,41) |

| INTERNATIONAL JOURNAL OF TECHNOLOGY MANAGEMENT | 27 | 1 (0,41) |

| JOURNAL OF CONTAMINANT HYDROLOGY | 28 | 1 (0,41) |

| JOURNAL OF MEDICAL ETHICS | 29 | 1 (0,41) |

| RESOURCES CONSERVATION AND RECYCLING | 30 | 1 (0,41) |

| SUSTAINABLE CHEMISTRY AND PHARMACY | 31 | 1 (0,41) |

| TECHNOVATION | 32 | 1 (0,41) |

| TRANSPORTATION RESEARCH PART D-TRANSPORT AND ENVIRONMENT | 33 | 1 (0,41) |

| TRANSPORTATION RESEARCH PART E-LOGISTICS AND TRANSPORTATION REVIEW | 34 | 1 (0,41) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).