Submitted:

31 October 2024

Posted:

31 October 2024

You are already at the latest version

Abstract

Insurance companies have a risk of bankruptcy if the funds disbursed exceed the reserves owned, or the surplus is negative. The risk of bankruptcy can be predicted using a mathematical model to anticipate the possibility of bankruptcy early on, so the surplus process needs to be observed in its evolution over time, assumed to be discrete time because it refers to the budget year period. The surplus process model is generally determined by three components, namely company capital, total premiums, and total claims. The sharia insurance scheme separates the management of the company's capital account from the premium and claim fund accounts, making it easier to monitor the evolution of its surplus process. This study systematically reviews the surplus process model for the sharia insurance scheme. The systematic review method is carried out by collecting scientific papers published in the Scopus, ScienceDirect, Dimensions, and Google Scholar databases. The PRISMA flowchart selects and then produces three scientific papers that are relevant to the topic. The results of this study provide insight into the form of the surplus process model and four sharia insurance schemes, namely mudharabah, wakalah, hybrid, and waqf. However, the scheme introduced is still a general description, there is no scheme based on needs or social problems in society such as the integration of productive waqf with welfare benefits for groups in need such as fishermen. This research was conducted towards the transition towards sustainable development of sharia insurance.

Keywords:

bankruptcy risk

; sharia insurance

; productive waqf

; surplus process

; systematic review

MSC: 62P05; 91B05; 91G05

1. Introduction

Insurance according to the Financial Services Authority (OJK, Otoritas Jasa Keuangan) in Indonesia is an agreement between an insurance company (insurer) and a policyholder (insured) where the insured pays a premium to obtain coverage for the risk of damage, legal liability to third parties that may be suffered by the insured, receives payments based on the death or life of the insured with benefits that have been determined and/or based on the results of fund management. Insurance can be distinguished by type, namely life and general, operational objectives, namely commercial and social, and fund management, namely conventional and sharia.

Life insurance is a company that provides risk management services that provide payments to policyholders (insured) or other entitled parties in the event that the insured dies or remains alive, or other payments to policyholders (insured) or other entitled parties at a certain time stipulated in the agreement, the amount of which has been determined and/or is based on the results of fund management. General insurance is a company that provides risk coverage and compensation services due to loss or damage to valuable assets owned such as houses, shops, warehouses, motor vehicles, agricultural land, merchandise, and various other assets. Commercial insurance is a company that provides protection in the financial sector for policyholders (insured) by implementing the principle of buying and selling and investing shareholders, thus providing benefits to policyholders (insured) and insurance companies. Social insurance is a company that provides social security for members of society formed by the government based on regulations governing the relationship between insurance parties and all groups in society. Conventional insurance is a company that applies the principle of buying and selling risks (transfer risk). This means that the premium paid by the policyholder (insured) aims to transfer financial risk to the insurance company. Sharia insurance is a collection of agreements between policyholders (insured) and sharia insurance companies, and agreements between policyholders (insured), in the context of managing contributions based on sharia principles with the aim of mutual protection and assistance.

The number of insurance companies in Indonesia registered with the Financial Services Authority (OJK) over the past seven years, namely 2018 to the first quarter of 2024, is summarized in Table 1.

The number of general insurance companies in Indonesia in 2018 was recorded at 78 companies, then decreased by three companies in 2019, again decreasing by one company each in the following two consecutive years. In 2022, one company was added so that the number became 72 companies and was stable until the first quarter of 2024. Life insurance experienced more or less the same thing as general insurance, there was a large decrease in the number of companies in 2018 and 2019, and a slight increase in the number of companies in 2020 and 2021. Reinsurance is a company that provides services in re-insurance against risks faced by general insurance companies, life insurance companies and/or other reinsurance companies. The number of reinsurance companies increased by one company so that in the first quarter of 2024 there were 7 companies. The social security program is a government program consisting of national health insurance, work accident insurance, death insurance, old age insurance, pension insurance, and job loss insurance. The social security program for the past 7 years has been recorded as stable in number, namely two companies. Social insurance for civil servants, police and soldiers is social insurance formed by the government with the aim of improving the welfare of employees and retirees recorded two companies in the first quarter of 2024.

The decline in the number of insurance companies in Indonesia is generally caused by the failure of insurance companies to fulfill their obligations to policyholders (insured) or known as insurance risk, so that the Financial Services Authority (OJK, Otoritas Jasa Keuangan) carries out mergers for strategic interests or revocation of business licenses. Insurance risk is the risk of failure of insurance companies to fulfill their obligations to policyholders (insured) as a result of the inadequacy of the risk selection process, premium or contribution determination, use of reinsurance, and/or claim handling. Insurance risk control can be carried out by anticipating early on the possibility of bankruptcy through bankruptcy prediction or known as financial distress prediction. Bankruptcy prediction is obtained through mathematical modeling by observing the evolution of the surplus process over time, assumed to be discrete time because it refers to the budget year period so that the amount of funds disbursed does not exceed the company's reserve funds, or the surplus is negative. The surplus process model is generally determined by three components, namely company capital, total premiums, and total claims. The sharia insurance scheme separates the management of the company's capital account from the premium and claim fund accounts, making it easier to monitor the evolution of the surplus process. In addition, the sharia insurance company as the fund manager has an obligation to loan (Qardh-Hasan) when the surplus process experiences a decline and deficit. This kind of fund management distinguishes sharia insurance from conventional insurance, where in conventional insurance the company's capital account is combined with premiums and claims, and conventional insurance companies have no obligation to loan if there is a deficit in the underwriting process.

The Financial Services Authority (OJK, Otoritas Jasa Keuangan) released several insurance companies in Indonesia that were given sanctions in the form of restrictions on business activities, special supervision status and revocation of business licenses. The reasons for imposing sanctions vary, including: lack of capital owned by the insurance company to cover the financial deficit, failure of the insurance company to pay claim obligations to policyholders (insured), the insurance company cannot meet the requirements of risk-based capital, minimum solvency level and minimum equity amount that have been set in the Financial Services Authority (OJK, Otoritas Jasa Keuangan) regulations on the financial health of insurance companies in Indonesia.

Table 2.

Insurance companies sanctioned by the Financial Services Authority (OJK, Otoritas Jasa Keuangan) .

Table 2.

Insurance companies sanctioned by the Financial Services Authority (OJK, Otoritas Jasa Keuangan) .

| Company name | Types of Insurance | Types of Sanctions |

|---|---|---|

| PT Asuransi Syariah Mubarakah | Life insurance | Revocation of business license |

| PT Asuransi Jiwa Nusantara | Life insurance | Revocation of business license |

| PT Asuransi Jiwa Bumi Asih Jaya | Life insurance | Revocation of business license |

| PT Asuransi Tokio Marine Indonesia | General Insurance (Sharia) | Revocation of business license |

| PT Asuransi Jiwa Bakrie | Life insurance | Revocation of business license |

| PT AXA Life Indonesia | Life insurance | Revocation of business license due to the merger of PT AXA Life Indonesia into PT AXA Financial Indonesia |

| PT Asuransi Himalaya Pelindung | General Insurance | Revocation of business license |

| PT Asuransi Recapital | General Insurance | Revocation of business license |

| PT Asuransi Parolamas | General Insurance | Revocation of business license |

| PT Asuransi Jiwasraya (Persero) | Life insurance | Restructuring and establishing a new company called IFG Life |

| PT Asuransi Jiwa Syariah Bumiputera | Life Insurance (Sharia) | Restrictions on business activities for some business activities |

| PT Asuransi Jiwa Adisarana Wanaartha | Life insurance | Revocation of business license |

| PT Asuransi Cigna | Life insurance | Revocation of business license due to merger between PT Asuransi Cigna and PT Chubb Life Insurance Indonesia |

| PT Asuransi Jiwa Kresna | Life insurance | Revocation of business license |

| PT Asuransi Jiwa Bersama Bumiputera | Life insurance | Special supervision status for the implementation of the company's financial recovery plan |

| PT Asuransi Jiwa Prolife Indonesia | Life insurance | Revocation of business license |

| PT Asuransi Purna Artanugraha | General Insurance | Revocation of business license |

The imposition of sanctions by the Financial Services Authority (OJK, Otoritas Jasa Keuangan) on insurance companies in Indonesia directly harms policyholders (insured) and results in low public trust in insurance companies. Strategic steps including preparing a financial recovery plan are needed so that bankruptcy in insurance companies can be minimized. One way to measure financial health in insurance companies can be seen from the evolution of the surplus process over time, assumed to be discrete time because it refers to the budget year period, so that insurance companies can monitor capital adequacy, income and profitability, and liquidity.

The Cramer-Lundberg model is a mathematical model introduced by Harald Cramer and Filip Lundberg. This model in insurance mathematics is used to calculate a company's surplus at a certain time or the company's capital balance at a certain time known as the risk process (or surplus process), predict the time of bankruptcy, and calculate the probability of bankruptcy. The Cramer-Lundberg model describes an insurance company experiencing two opposing cash flows, namely incoming premiums and outgoing claims, written in equation 1.

with is the initial capital, is the constant premium paid by the policyholder (insured) in time period t, is the claim frequency, and is the claim severity [1,2]. The Cramer-Lundberg model was introduced in 1903 by Lundberg [3] and republished by Cramer in 1930 [4] and 1955 by assuming total claim payments as a compound Poisson process [5]. This model is discussed in introductory books on risk theory, such as Buhlmann in 1970 [6], Gerber in 1979 [7], Bowers et al. in 1997 [8], and Dickson in 2005 [9]. Dufresne and Gerber in 1991 developed the Cramer-Lundberg model by adding a diffusion process to the original model [10], and Huzak et al. in 2004 involving the Lévy process [11]. Andersen in 1957 generalized that the claim frequency process is a renewal process known as the Sparre Andersen model [12], then this model was discussed again by Dickson and Hipp in 2001 [13], Gerber and Shiu in 2005 [14], Willmot in 1999 [15], Li and Garrido in 2004 [16] and in 2005 [17].

The probability of bankruptcy as a function of the surplus process is discussed and developed by Gerber et al. in 1987 [18], then one year later Gerber proposed the compound binomial model as a discrete analogy for the compound Poisson process in risk theory [19]. Shiu in 1989 produced bankruptcy probabilities for discrete-time models [20], assuming the claim frequency process is binomial and the values of the initial capital, premiums, and claim frequencies are integers. Willmot in 1993 determined an explicit formula for the finite-time bankruptcy probabilities in the compound binomial model [21]. Gerber and Shiu in 1998 introduced the discounted penalty function as a generalization of the probability of bankruptcy over an infinite period of time [22]. This Gerber-Shiu function is a function of variables such as initial capital, dividend limits, and reinsurance parameters. In 1957, De Finetti argued that a company can maximize its surplus value [23], not only focusing on efforts to minimize the probability of bankruptcy over an infinite period of time, so an alternative formulation was proposed to avoid unlimited surplus growth by paying part of the surplus to shareholders known as dividends. Dividend strategies are also discussed by Gerber and Shiu in 2004 [24], Gerber et al. in 2006 [25], Dickson and Drekic in 2006 [26], Gerber et al. in 2008 [27] and Avanzi in 2009 [28]. Dividends were paid from part of the insurance company's surplus obtained from the difference between premium receipts and claim payments and investment returns, so that Kim and Drekic in 2016 proposed the development of the Sparre Andersen model by including external fund activities and dividends in its model because a more complex model is needed in a modern industrial environment [29]. External funds are external accounts owned by insurance companies for investment activities and lending activities when the surplus process experiences a deficit, so that management of reserve funds becomes better.

The characteristics of the Kim-Drekic model involve investment activities, loan funds and dividend payments according to the needs of the sharia insurance company. Investment results are one of the incomes for the sharia insurance company as the manager of the policyholder's funds, and the sharia insurance company has an obligation to lend funds without interest through loan (Qardh-Hasan) when the guarantee surplus process experiences a deficit. The Kim-Drekic model is a threshold-based risk model and has four threshold levels, namely the minimum surplus amount received, the trigger point for investment activities, the trigger point for dividend payments, and the loan limit from the sharia insurance company as the fund manager if the guarantee surplus process experiences a deficit. Achlak in 2016 introduced a modification of the Kim-Drekic model by adding one threshold level, namely the trigger point for dividend payments from investment results, then also introduced the general form of Islamic insurance schemes consisting of mudharabah, wakalah, hybrid, and waqf along with a study of their risk models including the surplus process model and bankruptcy opportunities [30]. El Hachlaufi and El Msiyah in 2017 developed a surplus process model for the wakalah scheme and showed that the surplus process modeling used in conventional insurance can be applied to sharia insurance while still paying attention to sharia principles [31]. Puspita et al. in 2020 developed a risk model for a hybrid scheme through a surplus process model with discrete time bankruptcy opportunities involving investment and Qard-Hasan activities [32].

Based on the introduction, it can be seen that the study of the surplus process model for the sharia insurance scheme has not been done much compared to the study of the surplus process model for conventional insurance, so that there is an opportunity to develop a surplus process model as has been done by Achlak [30], El Hachlaufi and El Msiyah [31], and Puspita et al [32]. The development of the form of the sharia insurance scheme and its surplus process model can be done starting with the existence of social needs or problems in society, and this has not been done in previous studies. Therefore, this study conducted a systematic literature review on the surplus process model for the sharia insurance scheme so that a picture of the gap between studies was obtained, as a reference for developing a scheme based on needs or social problems in society. This study consists of several stages, including:

- (a)

- Search for scientific works through databases, using specific keywords.

- (b)

- Manual selection of scientific papers, using the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) flow diagram.

- (c)

- Bibliometric analysis of scientific works selected in point (b), using VOSviewer software.

- (d)

- Gap analysis of scientific works selected in point (b).

- (e)

- The discussion is based on the results of the gap analysis in point (d) and the following proposals for developing a scheme based on needs or social problems in the community.

This research is expected to contribute to the growing literature on the surplus process model for sharia insurance schemes so that prudent risk-based capital arrangements can be implemented because it will increase the efficiency and competitiveness of the company, so that insurance companies that go bankrupt can be minimized. Furthermore, the proposed development of a needs-based scheme is expected to be an alternative solution to social problems in society and lead to a transition towards sustainable sharia insurance development. Several research questions (RQ) that will be examined in this study include:

- RQ1: What are the sharia insurance schemes used in the surplus process modeling?

- RQ2: What are the variables in the surplus process model?

- RQ3: What are the advantages and limitations in modeling the surplus process of each selected scientific work?

- RQ4: What is the form of the proposed development of a scheme based on needs or social problems in the community and a description of the surplus process?

2. Materials and Methods

2.1Search for Scientific Works

Scientific works were searched using four databases, namely Scopus, ScienceDirect, Dimensions, and Google Scholar. The scientific works searched were articles and books that discussed insurance risks, especially sharia insurance, so the keywords used in the search were (“Risk” OR “Surplus” OR “Reserve”) AND (“Islamic” OR “Sharia” OR “Takaful”) AND “Insurance”. Searching using the Scopus database by entering the keywords in the search documents section and selecting article title, abstract, keywords in the search within section, obtained 173 documents. The year of publication was not limited, so that it was known the first year the research on the surplus process model for the sharia insurance scheme began. Furthermore, the document type was limited to English-language articles and books, open access with the publication stage being final, so that after being limited by several filters, 113 documents were obtained. Searching using the ScienceDirect database through advanced search by entering keywords in the title, abstract, author-specified keywords section, obtained 12 documents. The year of publication was not limited, the article type was limited to research articles and books, open access and open archive, so that after using filters, 2 documents were obtained. Search using Dimensions database by entering keywords in the search in title and abstract section, obtained 477 documents. Publication year is not limited, publication type is limited to articles and open access books, obtained 304 documents after using several filters. Google Scholar search through the Publish or Perish (PoP) application by entering keywords in the keywords section with an unlimited publication year, obtained 420 documents.

Table 3.

Results of searching for scientific papers in four databases.

| Database | Scopus | Science Direct | Dimensions | Google Scholar |

|---|---|---|---|---|

| Amount | 113 | 2 | 304 | 420 |

2.2. Manual Selection of Scientific Papers Using PRISMA Flowcharts

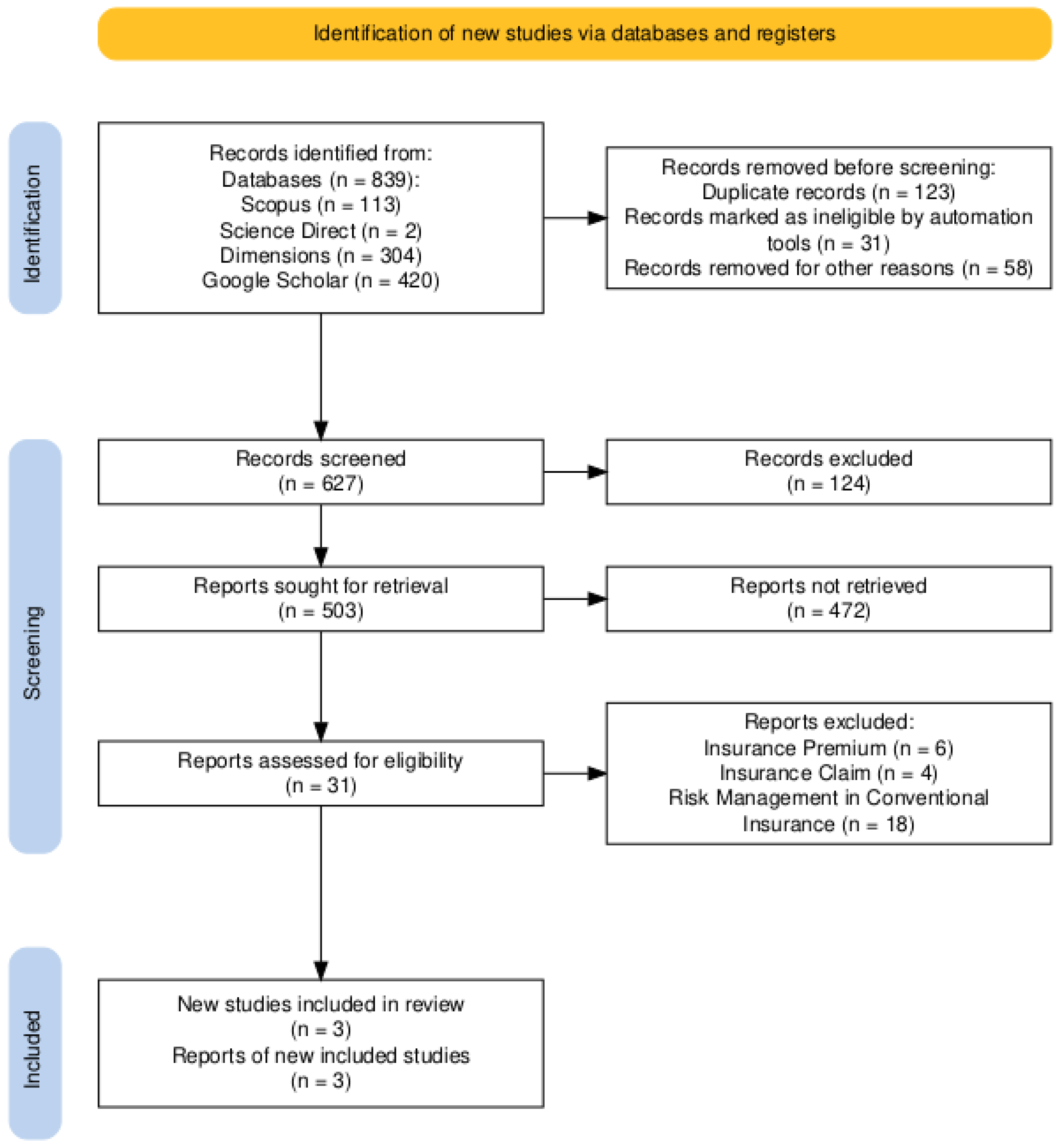

The number of scientific works obtained from the search results is presented in Table 3, then these scientific works were manually re-selected using the PRISMA flow diagram with stages as in Figure 1,

Identification stage, the total number of scientific works obtained from four databases is 839 documents. Manually selected and deleted due to duplication of as many as 123 documents, originating from the Scopus database 1 document, Dimensions 59 documents, and Google Scholar 63 documents. 31 documents were deleted because the language used is not English, originating from the Dimensions database 14 documents and Google Scholar 17 documents. 58 documents were deleted because the research topic is about Islamic banking financial institutions, originating from the Scopus database 17 documents, Dimensions 20 documents and Google Scholar 21 documents. Screening stage, deletion was carried out because the research topic is about Islamic law as many as 124 documents, originating from the Scopus database 14 documents, Dimensions 94 documents and Google Scholar 16 documents. 472 documents were deleted because the research topic is about Islamic insurance and reinsurance in general, originating from the Scopus database 73 documents, ScienceDirect 2 documents, Dimensions 111 documents and Google Scholar 286 documents. 28 documents were removed because the research topic is about actuarial on sharia insurance and risk management in conventional insurance, originating from the Scopus database 2 documents, Dimensions 10 documents and Google Scholar 16 documents. The included stage obtained 3 documents that are very relevant to the surplus process modeling for sharia insurance schemes.

Table 4.

Results of selection and deletion in the PRISMA flowchart.

| Reason for Deletion | Scopus | ScienceDirect | Dimensions | Google Scholar |

|---|---|---|---|---|

| Duplication | 1 | 0 | 59 | 63 |

| Language (other than English ) | 0 | 0 | 14 | 17 |

| Islamic law topics | 14 | 0 | 94 | 16 |

| Topic of Islamic banking financial institutions | 17 | 0 | 20 | 21 |

| General topics of sharia insurance and reinsurance | 73 | 2 | 111 | 286 |

| Actuarial in sharia insurance and risk management in conventional insurance | 2 | 0 | 10 | 16 |

2.2. Bibliometric Analysis of Selected Scientific Works

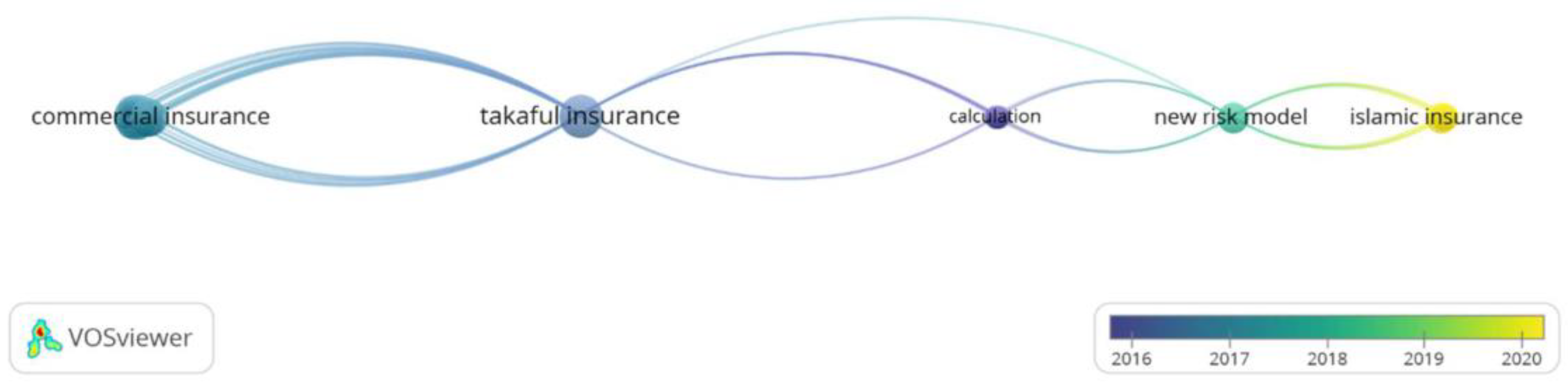

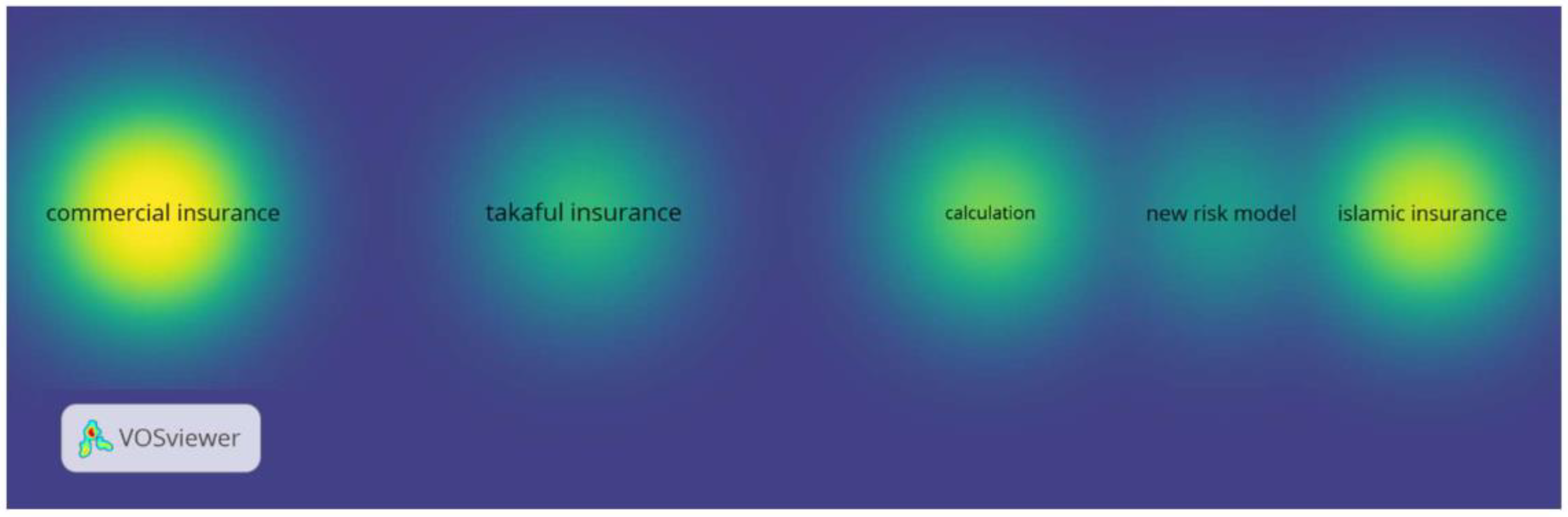

Three scientific works that are very relevant to the modeling of the surplus process for the sharia insurance scheme are presented in Table 5, then the dataset is saved in RIS file format, then the bibliometric network visualization is made using VOSviewer software. The first step, select create a map based on text data, then in choose data source select read data from reference manager files and select the files that have been saved previously. In the choose fields section, select title and abstract fields with full counting in the choose counting method. The threshold selected is one because the number of datasets is small, and the number of terms selected is 39. The next step, select finish in the verifying selected terms section and three different visualization displays will appear in network visualization, overlay visualization and density visualization. The network visualization map is used to see the relationship and cluster of research themes using keywords. Overlay visualization is used to show developments over time. Density visualization provides an overview of research that is rarely done or has been done a lot.

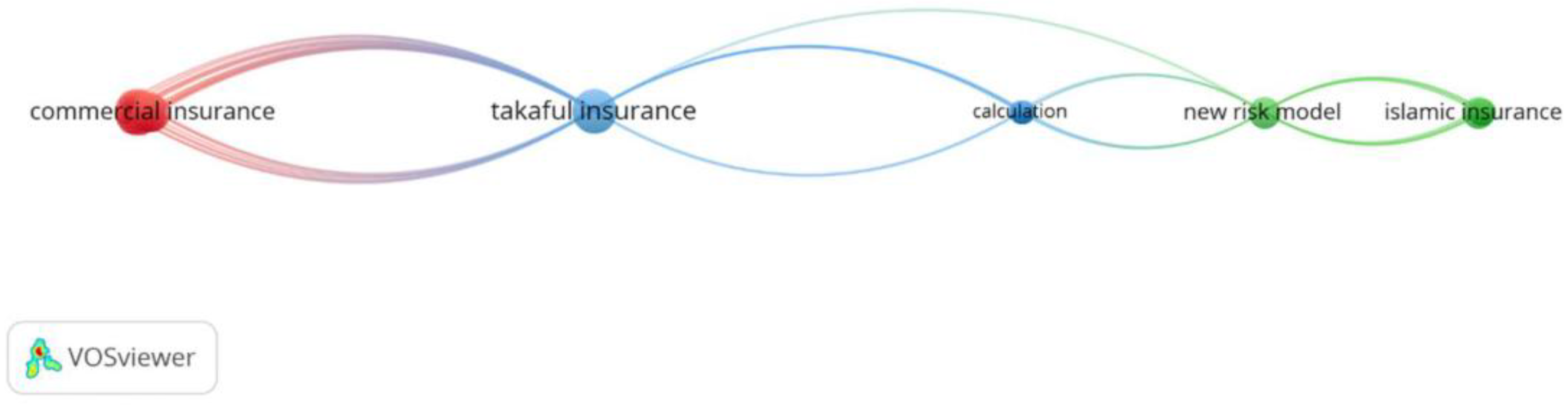

Figure 2 and Figure 3 show the relationship between research themes and their development over time. Before 2016, research on the surplus process model was mostly focused on commercial insurance that applied the principle of buying and selling like conventional insurance and the research flow was written in the introduction section. In 2016, research on the surplus process model of takaful insurance along with illustrations of its calculations was introduced by Achlak [30]. The forms of takaful insurance schemes introduced consisted of mudharabah, wakalah, hybrid and waqf accompanied by equations to calculate compensation received by the company and additional benefits received by policyholders. The term takaful refers to an insurance system based on Islamic sharia principles, so that takaful insurance in Indonesia is better known as sharia insurance. El Hachlaufi and El Msiyah in 2017 discussed the surplus process model for the wakalah scheme [31]. The substance of this study is how the surplus process modeling technique for conventional insurance can be applied to sharia insurance while still paying attention to and fulfilling the principles of Islamic sharia. This study also discusses the importance of surplus process modeling as an effort to support fair and sustainable financial decision-making in order to achieve a balance of interests between policyholders and companies. From 2017 to 2020, research on the surplus process model for sharia insurance focused on creating a new surplus process model by adding several variables to the model, such as research conducted by Puspita et al. [32]. In this study, a new surplus process model was developed for the hybrid scheme and a computational procedure for calculating the probability of bankruptcy. This hybrid scheme is a combination of wakalah and mudharabah. The wakalah scheme is applied to underwriting activities while the mudharabah scheme is applied to investment activities.

Density visualization can show which research has been widely conducted and which research is still rarely conducted. Figure 4 shows that research for commercial insurance including conventional insurance has been widely conducted, while research for takaful insurance or sharia insurance is still rarely conducted. This means that there is still an opportunity to develop a sharia insurance scheme and a new surplus process model that is adjusted to the needs of the sharia insurance industry in Indonesia as well as the needs or social problems in society. The surplus process modeling technique for conventional insurance that has been developed earlier can be used as a reference for sharia insurance on the condition that it continues to pay attention to and fulfill the principles of Islamic law. Several principles that distinguish between the two are concepts, contracts, sources of law, ownership of funds, sources of claim payments, investments, profits, and sharia supervisory boards. The differences in principle between the two are presented in Table 6. In addition to the differences in principle, several terms used in sharia insurance are also different from the terms in conventional insurance, so that these differences become characteristics for each insurance scheme. The difference in the use of the terms in question is: the term premium in conventional insurance is contribution in sharia insurance, the term claim in conventional insurance is compensation in sharia insurance, the term policyholder in conventional insurance is participant in sharia insurance, the term insurance company in conventional insurance is operator in sharia insurance, the term insurance fund in conventional insurance is tabbaru fund in sharia insurance, the term policy in conventional insurance is akad or agreement in sharia insurance, the term bridging fund in conventional insurance is Qardh in sharia insurance, the term pension fund in conventional insurance is tanahud fund in sharia insurance, the term policy validity period in conventional insurance is the agreement period in sharia insurance, the term agent fee in conventional insurance is ujrah in sharia insurance. This difference in terms has not been fully used, because there are still many conventional insurance terms that are also used in sharia insurance, so the most fundamental difference between the two is the difference in principle [33].

2.3. Gap Analysis between Selected Scientific Works

The gap analysis of the three scientific works presented in Table 5 refers to three research questions, namely what schemes are used in modeling the surplus process for sharia insurance, what variables are in the surplus process model, and the advantages and limitations in modeling the surplus process of each research written in the three scientific works. The fourth research question is presented in the discussion section.

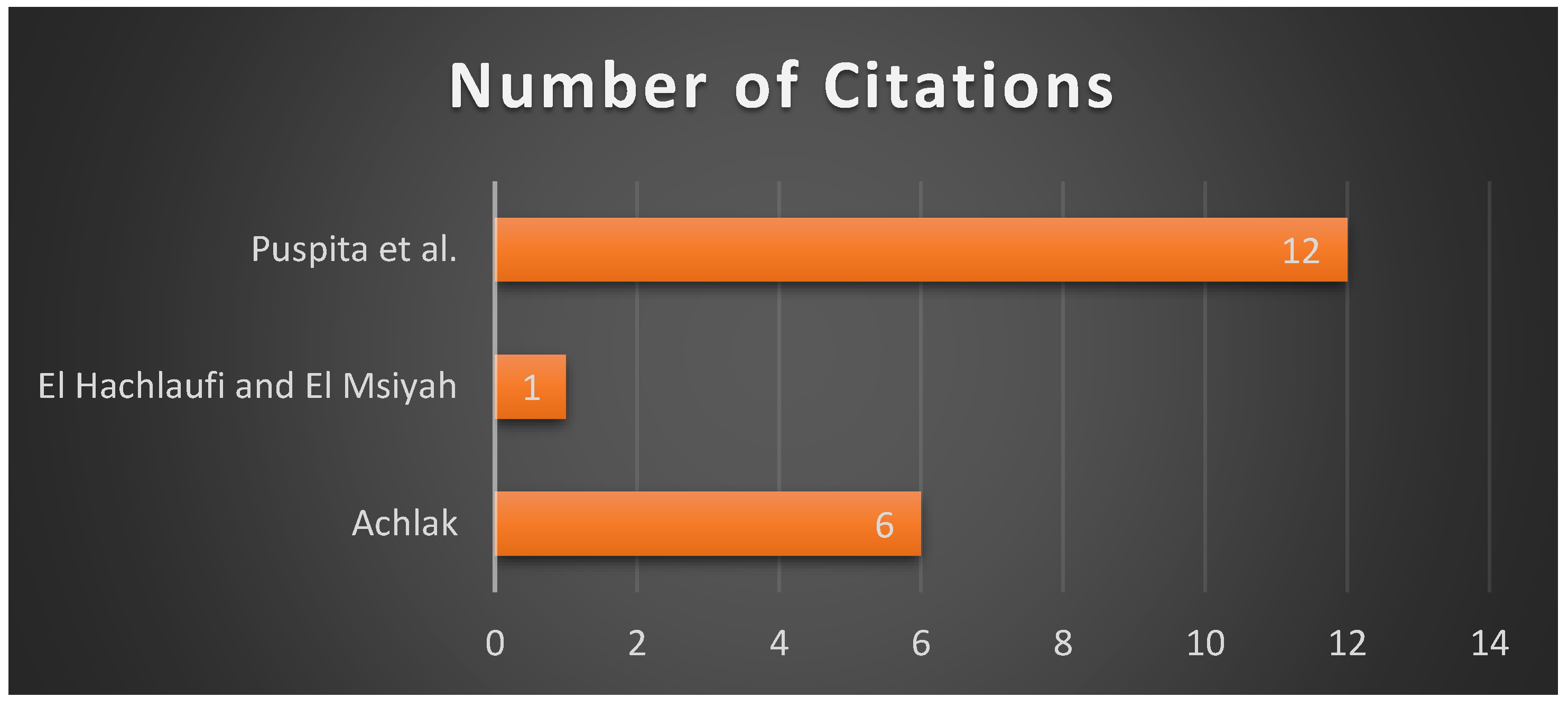

Figure 5 shows that the number of citations from each scientific work is still small, because there are not many studies that focus on modeling the surplus process for sharia insurance schemes. Thus, there is an opportunity to develop the form of the scheme and create a new surplus process model. Achlak [30] introduced the form of sharia insurance schemes in general, namely mudharabah, wakalah, hybrid, and waqf. El Hachlaufi and El Msiyah [31] developed the form of the wakalah scheme, and Puspita et.al [32] developed a hybrid scheme form that is tailored to the needs of takaful insurance or sharia insurance.

Table 7.

Sharia insurance scheme for each selected scientific work.

| Authors | Sharia insurance scheme |

|---|---|

| Achlak [30] |

Mudharabah scheme

|

| Achlak [30] |

Wakalah Scheme

|

| Achlak [30] | Hybrid Scheme

|

| Achlak [30] |

Waqf Scheme

|

| El Hachlaufi and El Msiyah [31] |

Wakalah Scheme

|

| Puspita et al. [32] | Hybrid Scheme

|

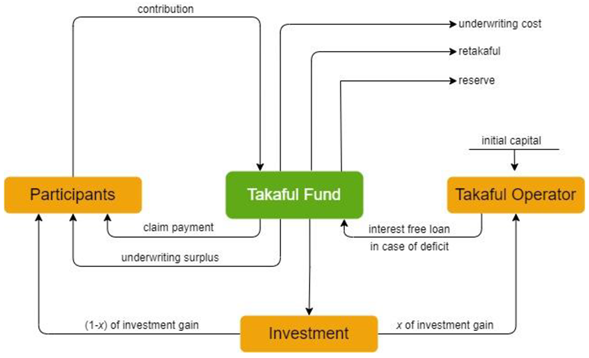

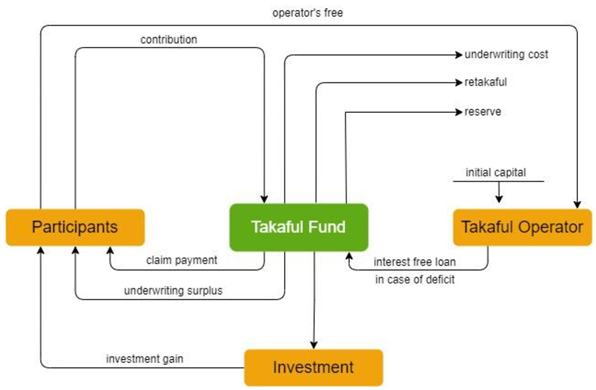

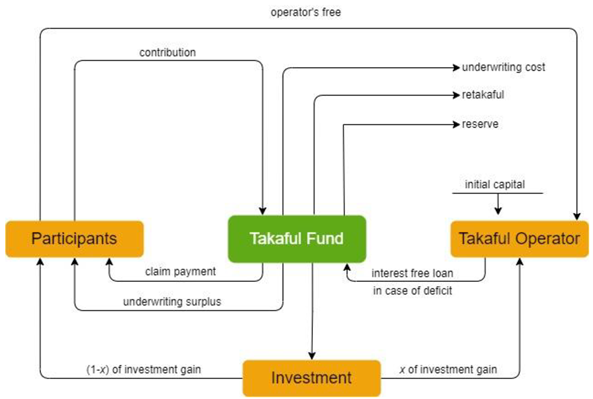

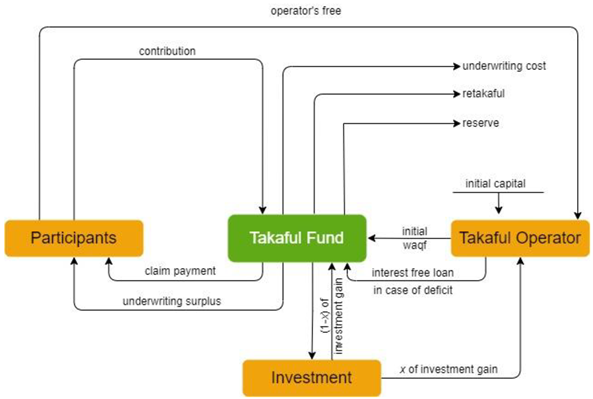

The mudhabarah, wakalah, hybrid and waqf schemes introduced by Achlak [30] at first glance have the same form, however the four schemes have similarities and differences which are written in Table 8 [30,33],

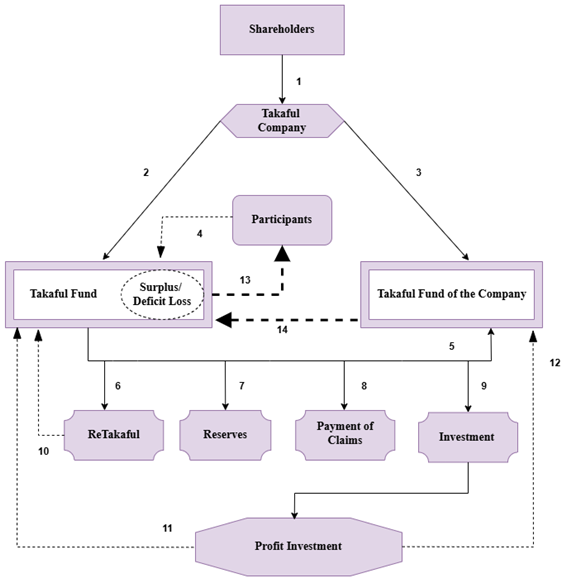

The wakalah scheme introduced by El Hachlaufi and El Msiyah [31] divides funds into two parts, namely takaful funds and company funds. Premiums received from participants are put into takaful funds while compensation for the company as the manager is put into the company funds. Takaful funds are used for claim payments, reinsurance, reserves, and investments. Part of the investment results are returned to the takaful funds and the other part is put into the company funds. If the takaful funds experience a deficit, the company lends its funds and if the takaful funds generate an underwriting surplus, part of the surplus is distributed to participants and the other part remains in the takaful funds.

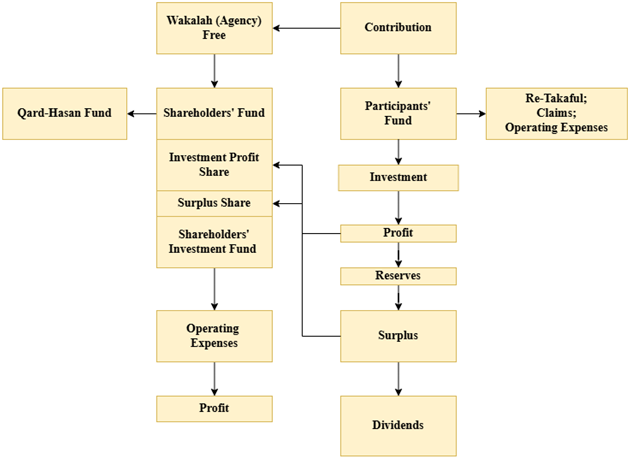

The hybrid scheme introduced by Puspita et.al [32] is similar to the hybrid scheme introduced by Achlak [30]. This scheme divides the premium into two parts, namely participant funds and wakalah fees. Participant funds are used for claim payments, reinsurance, operational costs, and investments. While the wakalah fee goes into the company's funds including loan funds (Qard-Hasan). Participant funds and company funds are both invested to generate profits. The investment profit of the company's funds goes back into the company's funds, while the investment profit of the participant's funds is partly entered into the reserve fund and the rest is distributed to the company's funds. If the guarantee results in a surplus, some are distributed to the company's funds and some are for dividend payments. Conversely, if there is a deficit, the company is required to loan (Qard-Hasan) so that the company's finances remain stable and the obligation to pay participant claims is still carried out.

The variables included in the surplus process model generally refer to equation (1) of the Cramer-Lundberg model, namely company capital, total premiums received and total claims paid. The surplus process models introduced by Achlak [30], El Hachlaufi and El Msiyah [31], and Puspita et al. [32] each have model names, equation forms, and variables as written in Table 9 and Table 10,

The surplus process model introduced by Achlak [30] consists of three models, namely the Kim-Drekic risk model, a modification of the Kim-Drekic risk model and a non-recursive function of the non-stochastic form of the surplus process. The Kim-Drekic risk model introduces the notation as the amount of surplus at time t and the notation as external funds owned by the company that manages reserve funds better through investment and loan activities (Qard-Hasan). Financial activities on external funds require the risk model to include four threshold levels, namely the minimum amount of surplus that must be achieved is denoted by , the trigger point for investment activities is denoted by , the trigger point for dividend payments to shareholders is denoted by , and the maximum loan limit (Qard-Hasan) is denoted by . The threshold level and are included in the surplus process while are included in external funds, by meeting the requirements . The relationship between the surplus process and external funds is stated by deposit (deposit) and loan (withdrawal) activities. Deposit activity refers to cash outflow activities from the surplus process into external funds and is categorized into two types, namely left-boundary deposits denoted by and right-boundary deposits denoted by . Left-boundary deposits are made at the beginning of the period when there are sufficient funds in the surplus process that can be invested while right-boundary deposits are made at the end of the period when external funds are in deficit due to loan (Qard-Hasan). Loan activities are denoted by referring to cash inflow activities from external funds into the surplus process which are carried out at the end of the period when the amount of surplus is in deficit and external funds are in sufficient condition to cover the deficit in the surplus process. Dividend payments to shareholders are denoted by being made at the beginning of the period when there is a large enough surplus and claim payments have been completed at the end of the previous period.

The amount of surplus describes the final amount of surplus at the interval when premium receipts, claim payments, deposit activities, lending activities, and dividend payments have been completed. Furthermore, it describes the final external funds at the interval when deposit activities, lending (Qard-Hasan) or other loan and investment activities have been completed with the assumption that the company has settled debts before continuing investment activities and the company has utilized its assets to adjust the amount of surplus before loan. The notation in the Kim-Drekic risk model states the end point at the interval when claims have been paid but before loan or right-boundary deposits have been made. The notation states the starting point at the interval when premiums have been received, dividends have been distributed and left-boundary deposits have been made. If the initial amount of surplus at time is , the amount of premium received at the beginning of each period with a constant rate is , the claim frequency is , and the claim severity is , then the amount of company surplus based on the Kim-Drekic risk model is written with equation (2)

with,

The evolution of external funds is expressed recursively with the assumption of the rate of return on investment and the interest rate ,

so that,

The Kim-Drekic risk model modification is a development of the model in equation (2) by changing the notation to the notation and adding one threshold level, namely . In this modification, the threshold level is the minimum surplus amount that must be achieved, is the trigger point for investment activities, is the trigger point for dividend payments from underwriting surplus by meeting the requirements . The threshold levels and are respectively the maximum loan limit (Qard-Hasan) and the trigger point for dividend payments from investment profits. Furthermore, the notation states the amount of deposit which means the same as the left limit deposit in the previous model, the notation states the amount of dividend payments from underwriting surplus and the notation states the amount of loan which means the same as loan in the previous model. The Kim-Drekic risk modification model is written with equation (8),

with,

The evolution of external funds is expressed recursively with the assumption of the rate of return on investment . If external funds reach a position or above it, then dividends resulting from investment profits are paid, denoted by ,

so that,

The third surplus process model introduced by Achlak [30] is a non-recursive function of the non-stochastic form of the surplus process. This model only involves cash inflow variables in the form of premium receipts and cash outflows in the form of deposits from the surplus process into external funds for investment activities, and is stated in equation (16),

with,

If is the notation of the initial external funds then the external funds equation is,

The surplus process model introduced by El Hachloufi and El Msiyah [31] is an annual surplus for the wakalah scheme which is determined by the company's income and expenses during the current year, stated in equation (21).

where is the annual surplus, is the amount of premium received during time t, is the amount of claims paid at time t, is the amount of technical provisions at time t, is expenditure during time t, is the market value of the company's assets at time t, is the capital (shares) at time t, and is the dividend paid at time t. Equation (21) separates the participant's funds (takaful) and the company's funds into three parts, namely the technical results of the participant's funds in part I, the financial income from assets in part II, and capital management in part III.

The surplus process model introduced by Puspita et al. [32] is a surplus process model for a hybrid scheme, applying the wakalah contract to the guarantee activity and the mudharabah contract to the investment activity. This model involves investment and lending activities (Qard-Hasan) by the company to the surplus process when the amount of its surplus decreases or even experiences a deficit. The return of the loan (Qard-Hasan) is carried out when the business generates profits in the future. If the notation is the initial surplus, the notation is the amount of premium received at time t, the notation is the amount of dividends paid by the company at time t, the notation is the deposit at interval , the notation is the return of the loan (Qard-Hasan) at interval , the notation is the withdrawal of funds from the investment fund into the surplus process at interval , the notation is the withdrawal of funds from the loan (Qard-Hasan) into the surplus process at interval , the notation is the frequency of claims, the notation is the severity of claims, then the surplus process model for the hybrid scheme is stated in equation (22),

This model divides the fund account into four parts and is managed separately, namely surplus funds denoted by , investment funds denoted by , loan funds (Qard-Hasan) denoted by and reserve funds denoted by , with three threshold levels as in the Kim-Drekic model, namely the minimum requirement for takaful surplus is denoted by , trigger point for investment activities is denoted by , trigger point for dividend payments is denoted by by fulfilling the requirements . Surplus funds and investment funds are participant funds, loan funds (Qard-Hasan) are part of the company's funds while reserve funds are introduced so that the remaining company funds that are not loaned are easier to observe. Investment funds describe financial activities carried out by the company while surplus funds describe underwriting activities where if there is a deficit then loan (Qard-Hasan) is carried out, and all are managed separately for better financial management. Surplus funds, investment funds, loan funds (Qard-Hasan) and reserve funds at time intervals are respectively denoted by , , , and .

The surplus process model for this hybrid scheme assumes a constant premium amount denoted received at time with the claim amount paid at time . Furthermore, the notations , , , and respectively denote the surplus fund, investment fund, loan fund (Qard-Hasan) and reserve fund at the time after the claim payment but before the loan (Qard-Hasan) or its return. The dividend payment scenario is determined by the threshold level denoted by . If then the amount of dividend from the underwriting surplus with the notation to be paid to the participants and the company. Furthermore, this model also proposes two dividend payment options, namely constant dividend with the notation and dividend difference from the surplus amount with the threshold level with the notation . If the premium received at time t is denoted by and the total dividend payment at time t is denoted by , then

With , and .

Threshold level is for investment activity. If then a constant amount is distributed into the investment fund at time . It is also assumed that investment activity is carried out when all debts and claims have been paid so that deposits at the time interval with the notation are stated in equation (25),

where both deposits and dividend payments are paid when the surplus amount exceeds the dividend payment threshold level, i.e. .

The hybrid scheme applies the wakalah contract to the guarantee activity and the mudharabah contract to the investment activity. The company as the manager is allowed to invest the participant's funds in sharia assets, both risky and non-risky assets, so that the company is entitled to compensation in the form of a wakalah fee (ujroh) from the management and profit sharing of the investment profit. The minimum requirement for the takaful surplus received is denoted by , if it decreases and the value is below then the investment funds are withdrawn first or a withdrawal is made from the loan (Qard-Hasan) when the investment funds cannot increase the amount of surplus to the level of . The maximum loan (Qard-Hasan) is the minimum between the shortfall to reach the level and the maximum of . This process continues so that the value does not fall below the threshold level . The withdrawal of investment funds and loans (Qard-Hasan) in each time interval is denoted and , and is stated in equations (26) and (27),

Withdrawals from loans (Qard-Hasan) must be returned in the future when the claim payment obligation has been completed and the value has exceeded the threshold level . Loan repayments (Qard-Hasan) must not contain interest, so this is what differentiates management in sharia insurance from conventional. The return on loan (Qard-Hasan) at a time interval is denoted by , expressed in equation (28),

Table 10.

Variables in each surplus process model.

| Variables | Kim-Drekic risk model |

Modified Kim-Drekic risk model |

A non-recursive function of the non-stochastic form of the surplus process | Annual surplus for Wakala models | Surplus process for Hybrid-Takaful |

|---|---|---|---|---|---|

| Surplus process | |||||

| Initial surplus (capital) | And ( | ||||

| Premium | |||||

| Deposit | And | - | |||

| Withdrawal from Qard-Hasan | - | - | |||

| Return to Qard-Hasan | - | - | - | - | |

| Withdrawal from investment funds | - | - | - | - | |

| Claim frequency | - | - | |||

| Severity of claim | - | ||||

| Dividend payment | And | - | |||

| Costs | - | - | - | And | - |

| External funds | - | And | |||

| Investment Fund | - | - | - | - |

The three studies on the surplus process model each have their own advantages and limitations. Therefore, there is still an opportunity to develop a sharia insurance scheme or create a new surplus process model with the hope of encouraging innovation in sharia insurance products and minimizing the risk of bankruptcy experienced by the company. The advantages and limitations of each study are presented in Table 11.

Based on the advantages and limitations of each study, all three focus on the surplus process model for sharia insurance schemes that comply with sharia principles and prioritize risk management in accordance with Islamic law. The Qard-Hasan facility as a company's obligation to loan funds without interest when the surplus experiences a deficit, makes management in sharia insurance different from conventional insurance.

The surplus process model for sharia insurance schemes can be used to find bankruptcy opportunities or in actuarial science it is known as ruin probability. The bankruptcy opportunity is used to measure the solvency level of a sharia insurance product, where this solvency level is related to the company's ability to carry out its obligations both in the short and long term. The computational procedure for calculating bankruptcy opportunities has been introduced by Puspita et al. [32].

3. Discussion

The surplus process model for Islamic insurance schemes introduced by Achlak [30], El Hachloufi and El Msiyah [31], and Puspita et al. [32] all focus on managing insurance risks in accordance with Islamic law, prioritizing transparency, minimizing conflict, and facilitating the supervision process by separating participant funds from company funds (external). Qard-Hasan as an interest-free loan facility plays an important role in increasing financial stability and reducing the risk of bankruptcy of Islamic insurance companies. However, in the future, it is necessary to discuss how to implement a loan (Qard-Hasan), especially when facing limited company capital or shareholder funds. Furthermore, the portion of the loan funds (Qard-Hasan) that is not withdrawn remains invested so that funding capacity increases by considering investment risk when placed in risky instruments.

Based on the availability of company capital, the waqf scheme has a lower potential for bankruptcy. Company capital consists of initial capital and initial waqf funds that can be productively utilized to generate waqf profits and benefits. However, the selection of the sharia insurance scheme used by the company is adjusted to the conditions of each, taking into account applicable regulations and the level of public interest [35-37]. The challenge facing the future is how to apply the stochastic process in investment activities while still considering the technical and operational challenges faced and establishing assumptions that are more in line with reality.

The distribution of surplus in the mudharabah scheme can cause problems from the perspective of balance between participants and companies, so that future discussions can also be focused on the optimal arrangement of surplus distribution for participants and companies. Furthermore, case studies and empirical data are needed in simulations to validate the model and determine the accuracy of the research results. However, the challenge faced is the difficulty of obtaining empirical data because the data in the company is generally not freely open. Empirical data is used by companies for decision-making, as a planning guideline, as a reference for implementing activities, as material for evaluating activities, and as organizational memory.

Based on the gap analysis between the studies that have been conducted, the consideration that the availability of company capital is one of the determining factors that can minimize the chances of bankruptcy, and efforts to transition towards the development of sustainable sharia insurance and benefits for the community, this study proposes a sharia insurance scheme based on community needs, which is named the productive waqf integration scheme with fishermen's welfare benefits, and this has not been done in previous studies. This scheme answers the fourth research question.

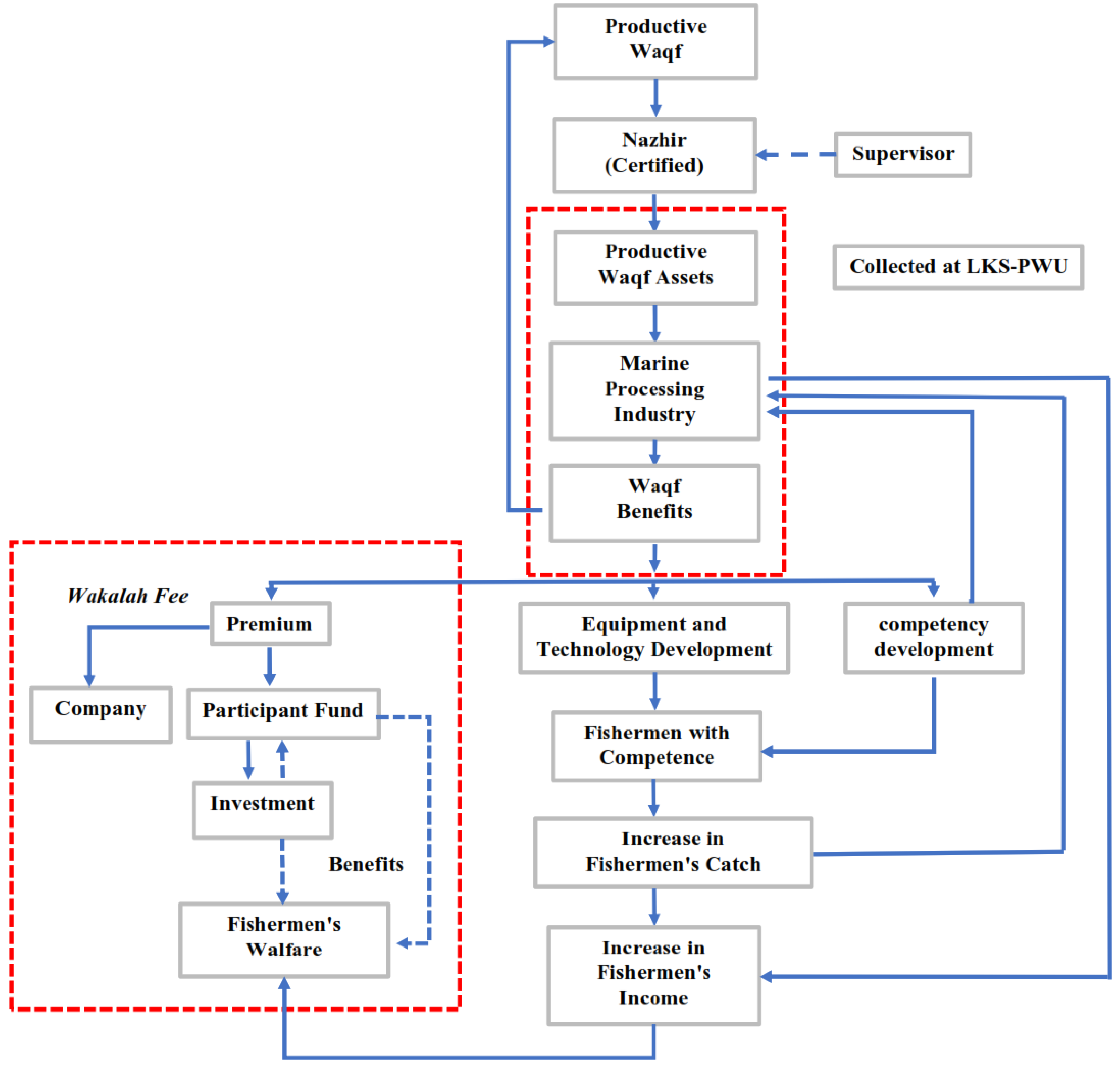

The productive waqf integration scheme with fishermen's welfare benefits is a sharia insurance scheme where the source of premium income comes from the benefits of productive waqf. This innovation will greatly help the fishing community in Indonesia who still needs attention, especially in the context of welfare. The benefits of productive waqf in addition to premium payments are also used for activities that can improve fishermen's welfare, such as the development of tools and technology and competency development [38]. The proposed design of the productive waqf integration scheme with fishermen's welfare benefits is presented in Figure 6,

This scheme starts with the existence of productive waqf, namely fixed assets or principal that are donated to be used in production activities, and the benefits of the waqf are distributed for the welfare of the community. This productive waqf is maintained and managed by Nazhir and supervised by the Indonesian Waqf Board (BWI¸ Badan Wakaf Indonesia). Land, buildings, and cash as productive waqf assets can be used to finance marine processing industry activities, so as to produce processed products with high economic value that can be sold to a wider target market to gain as much profit as possible. This profit will then be divided as waqf benefits and additional waqf assets so that the principal is maintained and/or increased. Therefore, the sustainability of the marine processing industry must be maintained so that it is stable and even increases in gaining profit.

The benefits of waqf are then distributed for the welfare of fishermen in the form of sharia insurance premium payments, equipment and technology development activities, and competency development activities. The development of equipment, technology, and competency is expected to produce reliable fishermen so as to encourage an increase in catches at sea which will have an impact on increasing income and welfare. Competency development is also given to fishermen's families, with the hope of producing reliable human resources who can support and encourage the progress of the marine product processing industry, and this will also have an impact on increasing welfare. Furthermore, the provision of sharia insurance for fishermen also has an impact on increasing welfare and minimizing financial risks for fishermen.

The improvement of fishermen's welfare can be realized when productive waqf through the marine product processing industry makes a profit or surplus and risk management activities through the sharia insurance scheme also make a profit or surplus. Therefore, in the future, it is necessary to discuss how to create a surplus process model for this scheme so that productive waqf and risk management do not go bankrupt. Referring to the surplus process model introduced by Achlak [30], El Hachloufi and El Msiyah [31], and Puspita et al. [32], the surplus process model for productive waqf integration scheme with fishermen's welfare benefits will produces two models, namely the surplus process model for waqf productive and surplus process models for scheme sharia insurance.

The surplus process model for waqf productive is analogous such as the surplus process model for scheme sharia insurance, so that consists of four variables, namely waqf productive assets, industry income, industry expenditure, and activities investment, with multiple threshold levels such as the amount maximum purchase results catch fisherman customized with capacity asset waqf and amount maximum investment in nor risk investment. Next, the surplus process model for scheme sharia insurance, namely scheme wakalah, will be made in two separate models, namely the surplus process model for corporate funds with multiple threshold levels and the surplus process model for participant funds with multiple threshold levels. This separation of the surplus models is an innovation that has not been conducted in research previously. Separation offers more transparency, makes it easier to look for reasons for bankruptcy, whether is it from corporate fund management or from the management of participant funds, and facilitates the monitoring process Because overall management must in accordance with sharia principles.

The productive waqf integration scheme with fishermen's welfare benefits open opportunity collaboration between the Indonesian government through State-Owned Enterprises (BUMN, Badan Usaha Milik Negara) based on holding companies, the Indonesian Waqf Board (BWI), and the community fisherman in frame support the program for reach target Vision of Golden Indonesia 2045, especially in the field of economy.

4. Conclusions

This study systematically reviews the surplus process model for Islamic insurance schemes. The systematic review method has been demonstrated, starting with the collection of scientific works in the form of articles or books published in the Scopus, ScienceDirect, Dimensions, and Google Scholar databases using the keywords (“Risk” OR “Surplus” OR “Reserve”) AND (“Islamic” OR “Sharia” OR Takaful) AND “Insurance”. Furthermore, a selection was carried out through the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) flow diagram presented in Figure 2 with several reasons for deletion presented in Table 4, resulting in three very relevant scientific works presented in Table 5. The three scientific works are entitled: 1) Discrete-Time Surplus Model for Takaful Insurance with Multiple Threshold Levels, 2) Surplus Modeling for Wakala Model of Insurance Takaful, and 3) Discrete Time Ruin Probability for Takaful (Islamic Insurance) with Investment and Qard-Hasan (Benevolent Loan) Activities.

The gap analysis of the three scientific works begins with the form of the sharia insurance scheme used to build the surplus process model, presented in Table 7. The name of the surplus process model and its equation form are presented in Table 9 with its explanation. The variables contained in each surplus process model are presented in Table 10, and the advantages and limitations of each study in the three scientific works are presented in Table 11. These three scientific works are studies that focus on managing insurance risks in accordance with sharia principles, prioritizing transparency, minimizing conflict, and facilitating supervision by separating company funds and participant funds. These three scientific works provide practical insights for the risk management of sharia insurance companies in maintaining solvency levels in order to minimize bankruptcy.

The productive waqf integration scheme with fishermen's welfare benefits proposed in this study can be an alternative scheme based on benefits and needs in the community, the implementation of which requires support and cooperation from the government, institutions, and the community, so that the phenomenon of market monopoly from fish traders and ship owners that causes social inequality can be reduced.

Research on sharia insurance schemes and surplus process models is expected to continue to develop in the future, because the evolution of the surplus process is very important for several company needs, including: 1) solvency risk management, namely checking whether the company has sufficient liquidity and capital reserves to pay future claims, 2) determining capital reserves, namely calculating how much reserve must be prepared to face unexpected claims in the future, and 3) bankruptcy risk testing, where the risk of bankruptcy can be calculated when the surplus is negative.

Author Contributions

Conceptualization, R.C. and S.; methodology, R.C., S. and R; software, R.C. and N.Z.; validation, S., R. and N.Z.; formal analysis, R.C.; investigation, S., R. and N.Z.; resources, S.; data curation, N.Z.; writing—original draft preparation, R.C.; writing—review and editing, S., R. and N.Z.; visualization, R.C.; supervision, S., R. and N.Z.; project administration, S.; funding acquisition, S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Universitas Padjadjaran, via Hibah Penelitian Kementarian Pendidikan, Kebudayaan, Riset dan Teknologi Skema Penelitian Disertasi Doktor, with a contract number: 074/E5/PG.02.00.PL/2 024.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Acknowledgments

The author would like to thank the Dean of the Faculty of Mathematics and Natural Sciences, Universitas Padjadjaran and the Directorate of Research and Community Service (DRPM), who have provided funding via the Universitas Padjadjaran.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Shiraishi, H. Review of statistical actuarial risk modelling. Cogent Mathematics 2016, 3(1), pp. 1123945. [CrossRef]

- Li, S.; Lu, Y.; Garrido, J. A review of discrete-time risk models. Rev. R. Acad. Cien. Serie A. Mat 2009, 103, pp. 321–337. [CrossRef]

- Lundberg, F. 1. Approximerad framställning af sannolikhetsfunktionen: 2. Återförsäkring af kollektivrisker.; Almqvist &Wiksells, 1903.

- Cramér, H. On the mathematical theory of risk.; Centraltryckeriet, 1930.

- Cramér, H. Collective risk theory: A survey of the theory from the point of view of the theory of stochastic processes.; Nordiska bokhandeln, 1955.

- Bühlmann, H. Mathematical methods in risk theory.; Springer-Verlag: Berlin, Heidelberg, New York, 1970.

- Gerber, H.U. An introduction to mathematical risk theory.; S. S. Huebner Foundation for Insurance Education: Wharton School, University of Pennsylvania, 1979.

- Bowers, N.L.; Gerber, H.U.; Hickman, J.C.; Jones, D.A.; Nesbitt, C.J. Actuarial mathematics, 2nd ed.; Society of Actuaries, 1997.

- Dickson, D.C.M. Insurance risk and ruin, 2nd ed.; Cambridge University Press, 2016. [CrossRef]

- Dufresne, F.; Gerber, H.U. Risk theory for the compound Poisson process that is perturbed by diffusion.; Elsevier, Insurance: Mathematics and Economics 1991, 10(1), pp. 51-59. [CrossRef]

- Huzak, M.; Perman, M.; Šikić, H.; Vondraček, Z. Ruin probabilities for competing claim processes. Journal of Applied Probability 2004, 41(3), pp. 679-690. [CrossRef]

- Andersen, E.S. On the collective theory of risk in case of contagion between claims. Bulletin of the Institute of Mathematics and Its Applications 1957, 12(2), pp. 275-279.

- Dickson, D.C.M.; Hipp, C. On the time to ruin for Erlang(2) risk process. Insurance: Mathematics and Economics 2001, 29(3), pp. 333-344. [CrossRef]

- Gerber, H.U.; Shiu, E.S.W. The time value of ruin in a Sparre Andersen model. North American Actuarial Journal 2005, 9(2), pp. 49-84.

- Willmot, G.E. A Laplace transform representation in a class of renewal queueing and risk processes. Journal of Applied Probability 1999, 36(2), pp. 570–584. [CrossRef]

- Li, S.; Garrido, J. On ruin for the Erlang(n) risk process. Insurance: Mathematics and Economics 2004, 34(3), pp. 391-408. [CrossRef]

- Li, S.; Garrido, J. On a general class of renewal risk process: analysis of the Gerber-Shiu function. Advances in Applied Probability 2005, 37(3), pp. 836-856. [CrossRef]

- Gerber, H.U.; Goovaerts, M.J.; Kaas, R. On the probability and severity of ruin. ASTIN Bulletin: Cambridge University Press, 1987, 17(2), pp. 151-163. [CrossRef]

- Gerber, H.U. Mathematical fun with the compound binomial process. ASTIN Bulletin 1988, 18(2), pp. 161-168. [CrossRef]

- Shiu, E.S.W. The probability of eventual ruin in the compound binomial model. ASTIN Bulletin 1989, 19(2), pp. 179-190. [CrossRef]

- Willmot, G.E. Ruin probabilities in the compound binomial model. Insurance: Mathematics and Economics 1993, 12(2), pp. 133-142. [CrossRef]

- Gerber, H.U.; Shiu, E.S.W. On the time value of ruin. North American Actuarial Journal 1998, 2(1), pp. 48–72. [CrossRef]

- Finetti, B.D. Su un’Impostazione alternativa della teoria collettiva del rischio. Proceedings of the Transactions of the XV International Congress of Actuaries, New York, 1957.

- Gerber, H.U.; Shiu, E.S.W. Optimal dividends: analysis with brownian motion. North American Actuarial Journal 2004, 8(1), pp. 1-20. [CrossRef]

- Gerber, H.U.; Shiu, E.S.W.; Smith, N. Maximizing dividends without bankruptcy. ASTIN Bulletin 2006, 36(1), pp. 5-23. [CrossRef]

- Dickson, D.C.M.; Drekic, S. Optimal dividends under a ruin probability constraint. Annals of Actuarial Science 2006, 1(2), pp. 291-306. [CrossRef]

- Gerber, H.U.; Shiu, E.S.W.; Smith, N. Methods for estimating the optimal dividend barrier and the probability of ruin. Insurance: Mathematics and Economics 2007, 42, pp. 243-254. [CrossRef]

- Avanzi, B. Strategies for dividend distribution: A review. North American Actuarial Journal 2009, 13(2), pp. 217–251. [CrossRef]

- Kim, S.S.; Drekic, S. Ruin analysis of a discrete-time dependent Sparre Andersen model with external financial activities and randomized dividends. Risks 2016, 4(1), pp. 1-15. [CrossRef]

- Achlak, A. Discrete-time surplus process for takaful insurance with multiple threshold levels. Master of Science, Middle East Technical University, 2016.

- El Hachloufi, M.; El Msiyah. Surplus modeling for model wakala of insurance takaful. International Journal of Statistics and Economics 2017, 18(1), pp. 16-26.

- Puspita, D.; Kolkiewicz, A.; Tan, K.S. Discrete time ruin probability for takaful (islamic insurance) with investment and Qard-Hasan (benevolent loan) activities. Journal of Risk and Financial Management 2020, 13(9), pp. 1-24. [CrossRef]

- Cahyandari, R.; Kalfin.; Sukono.; Purwani, S.; Ratnasari, D.; Herawati, T.; Mahdi, S. The development of sharia insurance and its future sustainability in risk management: A systematic literature review. Sustainability 2023, 15(10), pp. 1-23. [CrossRef]

- Delbaen, F.; Haezendonck, J. Classical risk theory in an economic environment. Insurance: Mathematics and Economics 1987, 6(2), pp. 85-116. [CrossRef]

- Cahyandari, R.; Mayaningsih, D.; Sukono. A design of mathematical modelling for the mudharabah scheme in shariah insurance. International Conference on Operations Research, Bogor, Indonesia, 27 August 2016. [CrossRef]

- Cahyandari, R.; Ariany, R.L.; Sukono.; Perkasa, Y.S. The hybrid model algorithm on sharia insurance. International conference on computation in science and engineering, Bandung, Indonesia, 10-12 July 2017. [CrossRef]

- Cahyandari, R.; Awalluddin, A.S.; Wulani, I.; Ariany, R.L.; Rachmawati, T.K.; Setiadji, S.; Sukono. Integration Model Table as an Alternative Presentation of Summary of Illustration Sharia Insurance. The 1st International Conference on Computer, Science, Engineering and Technology, Tasikmalaya, Indonesia, 27-28 November 2018. [CrossRef]

- Cahyandari, R.; Sukono.; Riaman.; Zamri, N. Rancangan inovasi bisnis integrasi wakaf produktif: BUMN holding asuransi. Antologi: transformasi BUMN berbasis holding, seri 1. Unpad Press: Sumedang Jawa Barat, Indonesia, 2024; pp. 207-223.

- Bulinskaya, E.V. New research directions in modern actuarial sciences. International Conference on Modern Problems of Stochastic Analysis and Statistics, Moscow, Rusia, 29 May - 2 June 2016. [CrossRef]

- Bulinskaya, E.V. Discrete time insurance models. Moscow University Mathematics Bulletin 2023, 78, pp. 298-308. [CrossRef]

Figure 1.

PRISMA flowchart stages.

Figure 2.

Network visualization for three selected scientific works.

Figure 3.

Overlay visualization for three selected scientific works.

Figure 4.

Density visualization for three selected scientific works .

Figure 5.

Number of citations in three selected scientific works.

Figure 6.

The productive waqf integration scheme with fishermen's welfare benefits.

Table 1.

Number of insurance companies in Indonesia over the last 7 years .

| Company Insurance | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Quarter-1 2024 |

|---|---|---|---|---|---|---|---|

| General Insurance | 76 | 73 | 72 | 71 | 72 | 72 | 72 |

| Life insurance | 59 | 53 | 52 | 53 | 53 | 49 | 49 |

| Reinsurance | 6 | 6 | 6 | 6 | 7 | 7 | 7 |

| Social Security Program | 2 | 2 | 2 | 2 | 2 | 2 | 2 |

| Social Insurance for Civil Servants, Police and Military | 3 | 3 | 3 | 3 | 3 | 2 | 2 |

Table 5.

Scientific works for bibliometric analysis.

| Authors | Scientific works | Title | Year |

|---|---|---|---|

| Achlak [30] | Book | Discrete-Time Surplus Process for Takaful Insurance with Multiple Threshold Levels | 2016 |

| El Hachlaufi and El Msiyah [31] |

Article | Surplus Modeling for Model Wakala of Insurance Takaful | 2017 |

| Puspita et al. [32] | Article | Discrete-Time Ruin Probability for Takaful (Islamic Insurance) with Investment and Qard-Hasan (Benevolent Loan) Activities | 2020 |

Table 6.

Differences in principles between conventional insurance and sharia insurance.

| Principle | Conventional Insurance | Sharia Insurance |

|---|---|---|

| Concept | Risk transfer: an agreement between two or more parties, where the insurer binds itself to the insured by accepting an insurance premium to provide compensation to the insured. |

Risk sharing: a group of people who help each other, guarantee each other and work together by each issuing tabbaru funds for loss insurance, while for life insurance they issue tabbaru funds and savings funds. |

| Contract | Sale and purchase agreement (contract of agreement) |

Tabbaru contract (grant) and tijarah contract (mudharabah, wakalah bil ujroh, mudharabah-musytarakah) |

| Source of Law | Based on human thought and culture. Based on positive law, natural law, and previous examples. | Based on the Word of Allah, Al-Hadith and Ijma Ulama |

| Fund Ownership | The premium funds belong entirely to the company, so the company is free to use and invest them. | Funds from participants, some will belong to the participants, some will be managed by the company as a trustee. |

| Claim Payment Source | Company Account as a consequence of the guarantor towards the insured | Tabbaru accounts are funds belonging to participants |

| Investment | Make investments within the limits of statutory provisions and are not limited to the halal and haram nature of the investments used. | Make investments in accordance with the provisions of the law as long as they do not conflict with Islamic sharia principles. Free from usury and various prohibited investment places |

| Profit | Company owned | Can be shared between the Company and participants in the form of prizes |

| Accounting System | Accrual basis: an accounting process that recognizes events (revenue, increases in assets, liabilities, expenses) that will be received in the future. | Cash basis: recognizing what really exists |

| Sharia Supervisory Board (DPS, Dewan Pengawas Syariah) |

No DPS | There is a DPS to ensure that the business runs in accordance with Islamic sharia principles. |

Table 8.

Similarities and differences in the sharia insurance schemes introduced by Achlak in 2016.

| Mudharabah | Wakalah | Hybrid | Waqf | |

|---|---|---|---|---|

| Contribution (premium) | ||||

| Operator's fee | ||||

| Underwriting costs | ||||

| Retakaful | ||||

| Reserve | ||||

| Claim payment | ||||

| Underwriting surplus (for participants) |

||||

| Underwriting surplus (for companies) |

||||

| Investment returns: takaful fund (for participants) | ||||

| Investment returns: takaful fund (for companies) | ||||

| Interest-free loan (if deficit) | ||||

| Waqf fund (initial) | ||||

| Initial capital |

Table 9.

Name of surplus process model in selected scientific works.

| Authors | Model Name | Equation Number |

|---|---|---|

| Achlak [30] | Kim-Drekic risk model | (2) |

| Modified Kim-Drekic risk model | (8) | |

| A non-recursive function of the non-stochastic form of the surplus process | (16) | |

| El Hachloufi dan El Msiyah [31] |

Annual surplus for Wakala model | (21) |

| Puspita et al. [32] | Surplus process for Hybrid-Takaful | (22) |

Table 11.

Advantages and limitations of the research.

| Authors | Advantages | Limitations |

|---|---|---|

| Achlak [30] | This research can help companies choose the right business scheme, such as the mudharabah model in the long term produces higher profits along with the increasing amount of external funds. The wakalah model offers stable income for the company. The hybrid model is a combination of mudharabah and wakalah, while the waqf model offers a lower chance of bankruptcy because of the initial waqf capital provided by shareholders through the company. | The model variables still depend on certain assumptions such as claim distribution and management costs are still considered fixed, while in reality they are influenced by many factors, one of which is inflation [34]. The investment level in this study is also still assumed to be fixed, so it does not fully describe the realistic uncertainty in the investment market. |

| El Hachloufi dan El Msiyah [31] |

This study offers better transparency, by separating company funds from participant funds. Company funds are then divided into three parts, namely technical results, financial income and capital management. In addition to transparency, this separation of funds can also reduce the potential for conflict and facilitate the supervision of risk management in accordance with sharia principles. | This research has not used empirical data and case studies, so model validation cannot be carried out and the reliability and accuracy of the research results cannot be known. |

| Puspita et al. [32] | This study offers a hybrid scheme with important innovations in Islamic insurance, namely Qard-Hasan facilities and investment activities. Qard-Hasan facilities can improve financial stability and reduce the risk of corporate bankruptcy in a certain period. Furthermore, the numerical simulations carried out can provide practical insights for corporate risk management in maintaining solvency during a certain period. Furthermore, this study also compares it with conventional schemes so that it can show that the offered Islamic insurance surplus process model has a lower chance of bankruptcy than conventional, especially when the Qard-Hasan lending capacity is high. | This research has not used empirical data from insurance companies. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.