Submitted:

29 August 2024

Posted:

30 August 2024

You are already at the latest version

Abstract

Modern advances in technology have increased the demand for traditional accounting systems to be upgraded for real-time data processing, security, and standardized reports. Thus, this paper proposes a new accounting information system that integrates IoT, blockchain, and XBRL. The proposed system aims to automate the accounting process by using IoT to collect data and send it automatically to a blockchain, which acts as a database that will generate journal entries automatically through smart contracts. XBRL will then be used as an output method for standardized financial reports based on the data transferred from the blockchain. This paper uses a qualitative research design based on semi-structured interviews with 13 industry experts from IT engineering, academia, and financial systems analysis. NVivo software was used to conduct a thematic analysis of interview transcripts. The findings revealed the technical feasibility, challenges, and benefits of the proposed integration and identified the most efficient mechanism for data transmission across the three technologies. The paper concluded that while integration complexity and user adoption are challenging, this integrated system can revolutionize accounting by enabling real-time data capture, automation of essential operations, data security, and integrity improvements. To our knowledge, this is the first paper to develop a comprehensive accounting information system framework using IoT, blockchain, and XBRL to automate data collection, improve data security, and streamline financial reporting. The study's potential to impact accounting systems and financial reporting research and practice emphasizes its importance.

Keywords:

blockchain

; Internet of Things (IoT)

; eXtensible Business Reporting Language (XBRL)

; smart contract

; accounting system

; automation

1. Introduction

The rapid advancement of technology in the modern business environment has significantly transformed fundamental accounting and financial reporting processes (Savić & Pavlović, 2023). The development of accounting information technology has been crucial in changing how firms operate, control, and disclose financial information (Kraus et al., 2022; Ojha et al., 2023). Advanced technology can enhance the recording and communicating of all business activities, from purchasing materials to paying final dividends to shareholders (Vial, 2019). In the rapidly evolving financial technology landscape, traditional accounting systems struggle to keep pace with the demands for real-time data processing, security, and standardized reporting (Murinde et al., 2022; Ojha et al., 2023). The integration of IoT, blockchain, and XBRL offers a promising solution to these challenges (Nofel et al. 2024). However, there is a lack of comprehensive frameworks that effectively combine these technologies to create a robust, efficient, and transparent accounting system. This research aims to fill this gap by proposing a new accounting system based on the integration of three advanced technologies: IoT, blockchain, and XBRL.

To begin with, IoT is an expanded network built on the Internet (Zhu & Qin, 2024). Its main goal is to allow things, machines, and people to interact in real-time using a variety of cutting-edge technologies (Wang et al., 2021). The expression "Internet of Things" was first introduced in 1999 by Kevin Ashton (Valentinetti & Flores Muñoz, 2021). The concept was initially centred on the ability of computers to efficiently manage distinct objects using radio-frequency identification technology (Ashton, 2009). However, there has been an increase in other technologies in recent times. For instance, according to Lee and Lee (2015), the following five technologies are frequently used to deploy successful Internet-of-Things-based products and services: radio frequency identification (RFID), which uses radio waves to enable automatic detection and data collection; wireless sensor networks (WSN), which are made up of geographically distributed separate sensor-equipped devices to monitor physical or environmental conditions of things; middleware, a software layer that sits between software applications to facilitate communication and input/output for software developers; cloud computing, a model for immediate access to a shared pool of configurable resources; and IoT application software, which facilitates reliable and robust device-to-device and human-to-device interactions.

IoT is an open and comprehensive network of intelligent objects that can self-organize, share information, data, and resources, and react to changes in the environment (Madakam et al., 2015). IoT can be used to automate accounting activities, thus reducing human error and enhancing performance (Desyatnyuk et al., 2022), and can be utilized for tracking and overseeing accounting procedures (Song, 2022). Moreover, IoT can offer data input for the accounting system. IoT enables the collection of data in real time, reducing the need for manual data entry and lowering the incidence of errors (Cao & Zhu, 2012).

Despite the advantages of using IoT in accounting, the literature highlights two significant limitations of traditional IoT centralized architecture (Christidis & Devetsikiotis, 2016; Dorri et al., 2017; Khan & Salah, 2018; Mistry et al., 2020; Reyna et al., 2018; Zheng et al., 2017): (i) the risk of a single point of failure that can compromise the entire system's integrity, and (ii) the lack of trust among entities in the system. Integrating IoT with blockchain addresses these issues. Before blockchain became widely accepted, security and privacy concerns hindered the mainstream adoption and future application of IoT. These concerns included ensuring data authenticity, preventing tampering during data transfer, and protecting data from unauthorized access or theft. Blockchain technology effectively resolves these security and privacy issues associated with IoT data (Fernández-Caramés & Fraga-Lamas, 2018; Novo, 2018; Wu et al., 2019). Smart contracts, based on blockchain technology, enhance IoT by incorporating social features, enabling interactions between various entities, and creating new economic transaction models (Zghaibeh, 2023). This integration enables the seamless and secure sharing of data, allowing the IoT to overcome its initial limitations.

Blockchain is described as one of the most important and innovative technologies developed in recent years (Peters & Panayi, 2016). Blockchain technology, also known as distributed ledger technology, is a system in which transaction records stored in blocks are maintained across multiple computers linked to a peer-to-peer network that uses consensus algorithms to verify transactions (Dai & Vasarhelyi, 2017). Blockchain is a decentralized database that stores complete information on every transaction that has occurred throughout its history (Trozze et al., 2022). Thus, blockchain is a digital ledger designed to capture transactions conducted among multiple parties in a network. It is a peer-to-peer, Internet-based distributed ledger that includes all transactions since its inception (Baiod & Hussain, 2024). All participants using the shared database are “nodes” connected to the blockchain, each maintaining an identical copy of the ledger (Autore et al., 2024). Every entry into the blockchain is a transaction representing an exchange of value between participants (Bible et al., 2017).

While blockchain architecture provides an immutable and transparent ledger for recording transactions, it is important to note that it does not guarantee the accuracy of the data itself (Nofel et al., 2024). Blockchain's strength lies in its capacity to confirm data integrity after recording, rather than verifying its initial accuracy. In simple terms, if incorrect data enters the chain, it remains permanently. To address this risk, the authors of this research suggest that integrating IoT devices could be a potential solution. Blockchain systems can use IoT technology as an automatic, real-time data input mechanism, significantly reducing the risk of human error or intentional manipulation during data entry (Nofel et al., 2024). Organizations can use a network of IoT sensors and devices to collect and transmit transactional data directly to the blockchain ledger, eliminating the need for manual input processes. This interaction between IoT and blockchain has the potential to create a stronger and more trustworthy accounting ecosystem.

Moreover, when it comes to digitizing corporate reporting, XBRL plays a crucial role (Hoffman & Rodríguez, 2013). XBRL is a significant development in accounting that profoundly impacts the financial reporting process (Hao et al., 2014). It is a digital format for financial reporting that can potentially replace traditional reports published in PDF or HTML formats (Martinis et al., 2020). XBRL simplifies the process of obtaining, transmitting, and using financial information to facilitate decision-making (Hsieh et al., 2019). XBRL allows companies to submit a single set of information instead of submitting it multiple times in various formats to different professional bodies and government authorities for different objectives (Kim et al., 2012). Moreover, it enables corporate entities to present and communicate their financial and non-financial information in a customized format (Scarlata et al., 2019).

Traditional forms of financial reports, such as Word, Excel, PDF, and HTML, are static and need to be reformatted to meet the needs of different users (Sarwar et al., 2021). This reformatting requires additional time, effort, and resources (Vasarhelyi et al., 2012). Consequently, there was a need to use a customized format for reports. XBRL's ability to prepare customized business reports is a unique feature that enables firms to report and disclose business and financial information according to the diverse requirements of various stakeholders (Gunn, 2007; Roohani et al., 2009). XBRL facilitates the standardization of financial reporting worldwide because it is based on accounting rules, methods, and Generally Accepted Accounting Principles (GAAP) (Saragih & Ali, 2023).

Nofel et al. (2024) argue that although blockchain, IoT, and XBRL are three different technologies designed for specific processes, they offer complementary advantages when integrated into AIS. The IoT serves as the input mechanism, relying on sensors to collect real-time data on physical assets, inventory levels, resource consumption, and environmental conditions. In the processing stage, blockchain provides a distributed, tamper-proof ledger that enhances the transparency, security, and traceability of financial transactions. XBRL represents the third stage, the output phase. It is a standardized, machine-readable format for the electronic transmission of business and financial data, enabling institutions and regulators to exchange relevant financial information smoothly and with high precision. To the best of our knowledge, no previous study has provided a framework for integrating these three technologies, so this paper seeks to address the following question: How can IoT, blockchain, and XBRL be effectively integrated to create a more efficient and transparent accounting system?

The motivations for this research arise from the growing demand for real-time, precise accounting information in decision-making processes, increasing concerns about data security and integrity in accounting systems, and emerging technologies with the potential to transform traditional accounting methods. This research is important because it proposes an innovative approach to utilizing cutting-edge technologies in accounting. Additionally, the research proposes a system that could improve the efficiency, accuracy, and reliability of financial reporting and auditing. Moreover, this research contributes to the ongoing digital transformation of the accounting profession. Furthermore, this paper adds to the academic literature on the relationship between emerging technologies and accounting practices.

This paper proposes a detailed plan for transforming accounting systems through the integration of IoT, blockchain, and XBRL. This paper offers several contributions. Firstly, this research is unique in its integration of IoT, blockchain, and XBRL into an accounting system. The adoption of these technologies in accounting combines their strengths to create a more robust and efficient system, representing a novel approach. To the best of our knowledge, this is the first paper to provide a framework for integrating these three technologies into a unique accounting system. Additionally, the proposed system uses IoT devices to automate the real-time collection and transfer of accounting data. This not only guarantees greater data accuracy by reducing errors in manual data entry but also provides stakeholders with rapid access to financial insights. Furthermore, blockchain technology significantly improves the security and integrity of accounting data. The immutable ledger of blockchain ensures the secure recording of all financial transactions, preventing any chance of manipulation. This feature is crucial for protecting the reliability of accounting data and providing an accessible audit trail necessary for regulatory compliance and fraud prevention. Moreover, XBRL ensures consistency in financial reporting, making it easier to exchange and analyze financial information across different platforms and stakeholders. Furthermore, the proposed system enhances efficiency and automates various accounting processes, including transaction recording, reconciliation, and reporting. This automation leads to significant time and cost savings by reducing the need for manual intervention and minimizing human errors. Finally, this research presents a foundational framework that can be used for future research and development in integrating IoT, blockchain, and XBRL in accounting and other business applications.

The subsequent sections of this paper are organized as follows: Section 2: Literature Review provides an analysis of previous studies on IoT, blockchain, and XBRL, and their relation to accounting. Section 3: Methodology provides a comprehensive explanation of the research methodology and methods used in this study. Section 4: Results and Discussion explains the proposed framework for the suggested accounting system. Section 5: Conclusion.

2. Literature Review

2.1. The Internet of Things (IoT)

Most IoT literature focuses on the corporate benefits and drawbacks of IoT. Haddud et al. (2017) suggested that adopting IoT could improve transparency, visibility of information and material flows, product tracking, inventory control and management, internal business process integration, and operational efficiency. According to Van Niekerk and Rudman (2019), integrating IoT into company activities can generate value through integration and increased information quality by providing real-time data. Furthermore, Karmańska (2021) suggests adopting IoT as an input tool in the accounting system of a road transport company and examining its impact on the accounting profession. Karmańska found that adopting IoT enables advanced report analysis using sensor data, cloud computing, and automated accounting processes. Wu et al. (2019) further noted that IoT could improve accounting data quality by adding transactional data sources to accounting information systems. Sensors are replacing manual data entry, allowing real-time accounting data collection and processing without human intervention. They added that IoT may gather audio, location, and physical data like length, weight, and volume. As a result, financial reports would include more than just monetary values, enabling users to incorporate critical data and make informed estimates.

Additionally, Roszkowska (2021) claimed that IoT sensors can timely update financial data such as inventories, production, equipment usage, and depreciation. This capability provides real-time data, minimizes human costs, and prevents data tampering. In an empirical investigation of Chinese stock exchange-listed enterprises, Wang et al. (2021) revealed that IoT reduced financial earnings manipulation. This decrease is observed in both accrual-based and real earnings manipulation. According to Wang et al. (2021), IoT technology enhances asset monitoring and information flow, reduces agency problem costs, and improves internal control. Also, Elmaasrawy and Tawfik (2024) found that employing IoT as an accounting information system input tool reduces human data entry errors. Large amounts of data are quickly entered into the accounting system. Furthermore, Maharani et al. (2024) emphasized IoT's ability to collect and process enormous amounts of data, as well as the real-time monitoring and tracking of data across IoT-enabled devices. Additionally, Zhen and Zhen (2024) highlighted the possibility of using IoT as an input method in accounting information systems.

2.2. Blockchain Technology and Accounting Systems

While various fields have highlighted blockchain technology's benefits, there is a lack of studies investigating its use in accounting, particularly as an accounting information system or within accounting processes. Several researchers (Thies et al., 2023; Peters & Panayi, 2016; Schmitz & Leoni, 2019) suggest that blockchain technology could develop a triple-entry accounting system, transforming the accounting ledger. Moreover, Dai & Vasarhelyi (2017) introduced a blockchain-based triple-entry accounting system, where automated verification reduces the risk of financial record concentration and manipulation. Blockchain, serving as a company's ledger, stores financial transactions and accounting data streams, enabling timely reporting and financial visibility. In the same vein, Inghirami's (2020) research clarified the concept of blockchain as a service helping accounting departments integrate TEA.

Similarly, Maiti et al. (2021) proposed a blockchain-based triple-entry accounting (TEA) framework. They discussed three accounting techniques: sophisticated double-entry accounting software, blockchain and triple-entry accounting, and disruptive technologies related to blockchain and triple-entry accounting. In the same context, Cai (2021) compared TEA to double-entry in a blockchain ecosystem. Cai argues that the decentralized and permanent ledger nature of blockchain reduces the need for external auditors. Thus, traditional audits may take less time, reduce costs, and eliminate fraud and errors. In support of blockchain in TEA, Carlin (2019) conducted a conceptual and theoretical analysis to move beyond double-entry accounting. Carlin suggested that blockchain technology for TEA might increase precision and transparency in record-keeping and transaction processing while lowering costs. Faccia et al. (2020) proposed replacing double-entry accounting with triple-entry accounting using blockchain technology. They introduced a third axis of transaction hashes to enhance the auditing architecture.

Desplebin et al. (2021) investigated how blockchain technology could revolutionize accounting. They suggested that blockchain technology in accounting could initiate an evolutionary process like the transition from paper to digital databases. They argued that blockchain technology enhances TEA by providing a secure, immutable ledger. Furthermore, Ibañez et al. (2023) analyzed the history of shared ledger systems, focusing on the development of TEA and the Resource-Event-Agent (REA) accounting paradigm. Their study showed that shared ledger systems evolved from concepts in three research streams that converged but matured independently. Ibañez et al.'s research suggests that shared ledger systems like blockchain are a product of convergence. These systems are decentralized and trustless, adhering to triple-entry accounting principles.

Other literature has suggested using blockchain as an independent accounting system. O'Leary's (2017) study examined the use of blockchain technology in accounting and supply chain transaction processing. O'Leary focused on cloud-based and private blockchain accounting solutions in firms. Faccia and Petratos (2021) employed an e-procurement case study to test the viability and benefits of blockchain technology in AIS and ERP systems. According to O'Leary (2017) and Faccia and Petratos (2021), blockchain accounting systems improve transparency and security through accountability, immutable record-keeping, and consensus-based updates. Faccia and Petratos also noted that smart contracts offer several blockchain accounting applications. Self-executing contracts automate complex accounting operations, reducing the need for intermediaries and minimizing human error. The immutability of blockchain records addresses accounting issues related to data reliability, transaction tracking, and verification (Baiod & Hussain, 2024).

Empirical evidence supports blockchain-powered accounting information systems. Saraiva and Vieira (2023) used blockchain technology to improve the Portuguese accounting system, creating two proofs of concept (PoCs). Their study demonstrated how blockchain can streamline accounting and create a more transparent and trustworthy financial environment by conducting accounting directly on the blockchain platform. Additionally, a case study by Gomaa et al. (2019) examined the practicalities and impacts of blockchain technology in AIS. Furthermore, Tan and Low (2019) claimed that blockchain technology can digitize validation, thereby enhancing the accuracy and integrity of financial records. Moreover, Benedetti et al. (2020) reinforced this viewpoint by describing blockchain technology's multi-level structure, which makes it suitable for minimizing corporate fraud. Also, Wang and Kogan (2018) proposed a prototype blockchain-based transaction processing system incorporating zero-knowledge proof and homomorphic encryption. This system was designed to demonstrate real-time accounting, monitoring, and fraud protection.

2.3. eXtensible Business Reporting Language (XBRL)

As a global business reporting standard, XBRL allows all types of enterprises to easily record and exchange information about their operations (Plumlee & Plumlee, 2008). As a widely recognized accounting technology, XBRL has been extensively studied. It is a standardized markup language for financial reporting (Bergeron, 2004; Z. Wang & Gao, 2012). Companies organize financial data in XBRL for analysis and comparison. XBRL also allows businesses to customize their financial and non-financial reporting (Scarlata et al., 2019). As Alathamneh (2020) notes, it enhances the efficiency and accuracy of an organization's accounting information system. Advances in corporate reporting technologies can minimize the risks and challenges of real-time communication with stakeholders (Trigo et al., 2014).

Yoon et al. (2011) found that XBRL reduces stock market information asymmetry. In the same context, in 2017, Liu et al. explored how XBRL reduces information asymmetry in the European finance industry. The study examined market liquidity and information asymmetry in Belgian non-financial firms before and after XBRL implementation. Additionally, Liu et al. (2017) found that XBRL adoption boosts market liquidity and minimizes information asymmetry, particularly benefiting larger and non-tech companies. Also, Palas & Baranes (2019) noted that XBRL provides easily accessible, up-to-date financial information for financial analysis and decision-making. Borgi & Tawiah (2022) also found that XBRL improves financial reporting, especially in developing countries.

The adoption of XBRL for corporate reporting has enhanced accounting and financial reporting. Companies benefit from cost-effective reporting, faster communication, and more efficient financial analysis for performance management (Uyob et al., 2019). Additionally, Arora & Chauhan (2023) pointed out that mandating the adoption of technologies like XBRL to enhance financial disclosure efficiency, precision, user-friendliness, and clarity should drive innovation. XBRL technology enhances the precision and comparability of financial and non-financial data, making firms more competitive. This enables stakeholders to assess a company's financial strengths and weaknesses (Yang et al., 2018). Moreover, Huang et al. (2021) noted that XBRL adoption impacts stock prices, market perception, and firm competitiveness. Technology-driven business reporting enables companies to compare their performance with competitors by creating standardized reports. It also helps identify competitive strengths and weaknesses in the market (Sassi et al., 2024).

Kim et al. (2019) found that XBRL reduced discretionary accruals, thus limiting earnings manipulation. The impact was more pronounced with standardized XBRL elements. Kim et al. (2019) noted that standardized XBRL features improve financial reporting transparency and reduce managers' capacity to alter financial accounts. This highlights XBRL's role in corporate governance and financial reporting. In the same vein, Mayapada et al. (2020) examined the impact of XBRL implementation on earnings management in Indonesian manufacturing firms. They found significant differences in earnings manipulation before and after XBRL deployment, demonstrating that XBRL reduces managerial manipulation and improves financial reporting.

2.4. The Integration of IoT, Blockchain, and XBRL

There is a lack of studies examining the integration of these technologies (Nofel et al., 2024). A few studies have explored the integration of IoT and blockchain, while even fewer have investigated the integration of blockchain and XBRL.

IoT-blockchain integration is considered innovative (Atzori, 2018; Christidis & Devetsikiotis, 2016; Zhang & Wen, 2017). Similarly, Wu et al. (2019) proposed a blockchain-IoT transaction model for accounting. IoT connects the digital and physical worlds by collecting data from sensors. Wu et al. (2019) argued that a strong IoT infrastructure facilitates the easy deployment of smart contracts. IoT securely collects and records data, ensuring fast and accurate transmission to the blockchain. Sherif and Mohsin (2021) supported blockchain-IoT integration. They studied the combined effect of these technologies, which upload IoT data via a decentralized blockchain infrastructure. This method successfully addressed a single point of failure. This integration reduces knowledge asymmetry between accountants and regulators by offering greater transparency. It prevents information manipulation and financial misrepresentation.

Together, smart contracts and IoT can track and manage the state and actions of physical products (Dai & Vasarhelyi, 2017). Using IoT location data, smart contracts can automatically record sales transactions on the blockchain ledger when inventory items leave the organization. Electronic devices should also be equipped with sensors, powerful processors, and connectivity (Dai & Vasarhelyi, 2017). As a result, these devices can automatically notify of inventory damage, non-delivery, and delays. These notifications can prompt smart contracts to immediately update accounting records. The IoT system is composed of three layers: sensor, network, and application (Xiao, 2017). Blockchain technology can provide a solid foundation for IoT's customized application layer.

On the other hand, Faccia et al. (2019) developed a cloud-based solution using cloud computing, AI, blockchain, and XBRL to optimize the financial accounting cycle. Blockchain technology ensured data immutability, transparency, and security, enabling a triple-entry accounting system that reduces errors and fraud. Financial reporting was standardized using XBRL, improving comparison and analysis across enterprises and countries. Another theoretical study by Beerbaum (2018) found that integrating blockchain technology with XBRL in accounting improves the reliability and accuracy of financial records, validates financial and non-financial data, and enables real-time reporting and accounting, thereby speeding up financial processes.

Wahab's (2019) study examined whether XBRL and blockchain could improve Malaysian company reporting. The study investigated transparency, data integrity, and data availability. Wahab (2019) argued that strategic planning and technological advancements could make this integration realistic and beneficial for Malaysian corporations. Additionally, Serag (2022) proposed using blockchain's decentralized peer-to-peer network to distribute XBRL information while maintaining government data management. The study highlighted transparency, data integrity and quality, security, auditing efficiency, and real-time data availability.

Boixo et al. (2019) reviewed an XBRL chain demo employing blockchain technology to verify the integrity and non-repudiation of business reports, leveraging blockchain's immutability and transparency. Le et al. (2019) also developed a blockchain-based financial reports ledger prototype to improve trust and transparency in published financial reports, influencing inter-organizational transactions. They claimed that XBRL reports could be stored on the Ethereum blockchain to restore credibility in financial reporting.

3. Methodology

Qualitative research was employed to build a framework for integrating IoT, blockchain, and XBRL into an accounting system. A qualitative study reveals participants' interpretations of variables and how they understand the topic (Cooper & Schindler, 2014). In qualitative research, like in interviews, researchers interact with participants during data gathering. The flexible nature of qualitative research design allows for considerable creation and reconstruction (Maxwell, 2005). The qualitative approach in this study facilitated understanding and analyzing how to integrate IoT, blockchain, and XBRL into a novel accounting system.

The paper collected data on the integration of IoT, blockchain, and XBRL into accounting systems using semi-structured interviews with open-ended questions. This facilitated the discussion of both predetermined and emerging issues (Flick, 2009; Kvale, 2011). Semi-structured interviews yielded more comparable responses while allowing flexibility in identifying important issues (Collis & Hussey, 2013).

This paper used purposive sampling, a technique that selects participants who have a strong understanding of the topic. It is a non-probabilistic technique (Kothari, 2004). Purposive sampling is recommended for studies that require interviewees to have in-depth knowledge of the topic (Creswell, 2016). This sampling method allows researchers to carefully select interviewees (King et al., 2019; Qu & Dumay, 2011). Our sampling strategies included criterion sampling and snowball sampling. Criterion sampling involves selecting study participants based on specific criteria related to the study subject. Snowball sampling involves asking pre-selected participants to recommend others who understand the research issue (Bloomberg & Volpe, 2012; Moser & Korstjens, 2018). To fulfil the study's objectives, a purposive sample of participants was selected based on their understanding of the topic and willingness to share their experiences with blockchain, IoT, and XBRL.

Qualitative research often uses the "saturation point" to determine the number of participants. Data saturation occurs when additional interviews are unlikely to provide new information (Flick, 2009; Kvale, 2011; Turner, 2010). Guest et al. (2020) observed that 6–7 interviews typically yield the majority of themes, while 11–12 interviews generally achieve greater saturation. A sample size of five to twenty-five is considered sufficient for semi-structured interview research using non-probability sampling, according to Saunders et al. (2019). In this study, thirteen interviews were conducted with experts from different backgrounds, as shown in Appendix A. Theoretical saturation was reached after eight interviews, with no new knowledge or patterns emerging. The first eight interviews produced similar insights on integrating IoT, blockchain, and XBRL in accounting. Five additional interviews were conducted to ensure all research findings were covered.

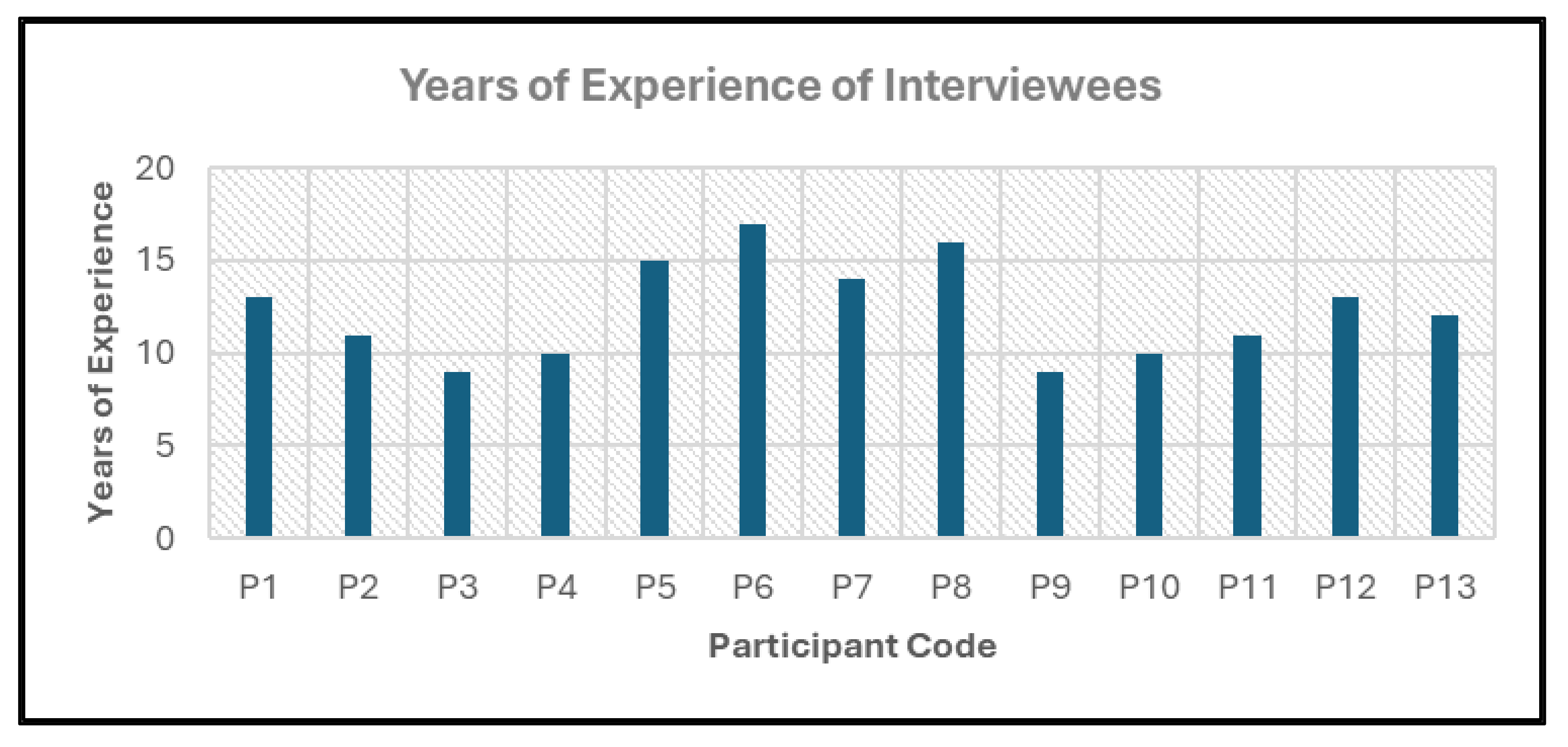

Figure 1 illustrates the participants' extensive professional backgrounds. Participants had 9–17 years of experience, averaging 12 years. This distribution demonstrates the participants' considerable knowledge of IoT, blockchain, and XBRL accounting systems. Most interviewees have over 10 years of experience in their respective fields, ensuring that the knowledge is based on professional practice.

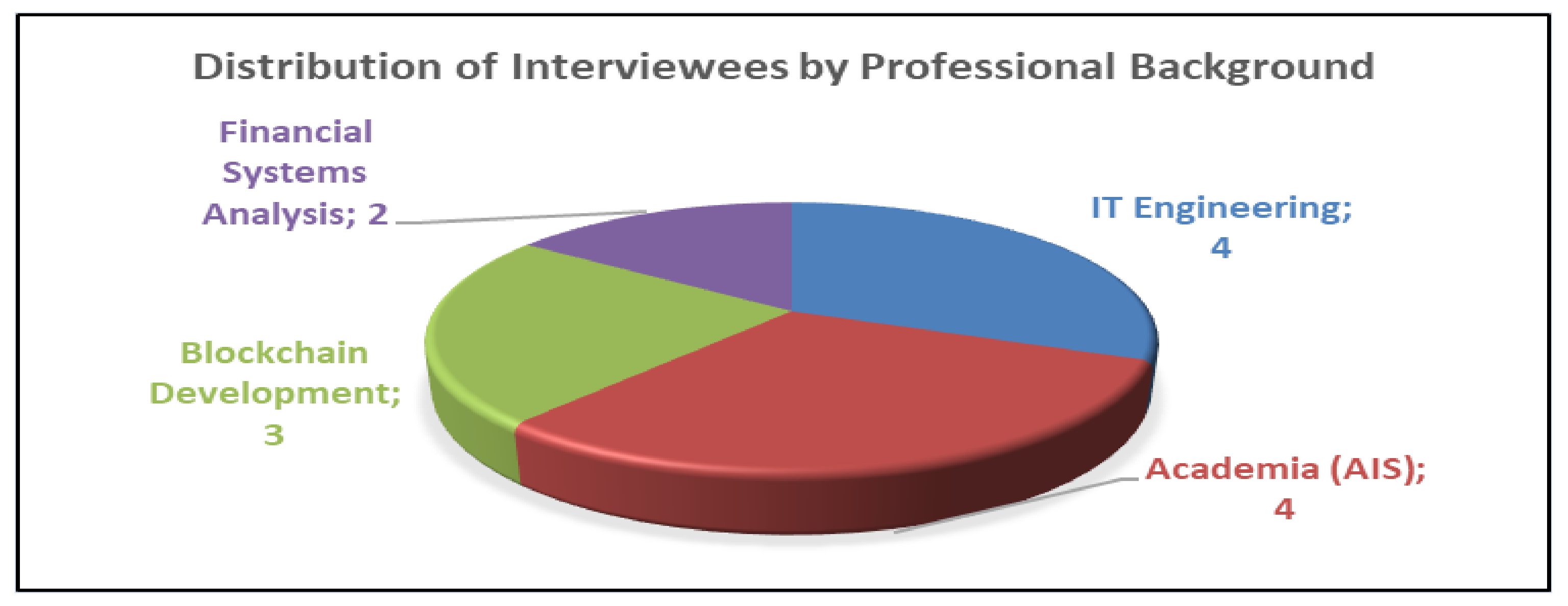

Figure 2 illustrates the wide range of study-related knowledge among participants. Figure 2 displays the interviewees' professions, including IT engineering, academia (particularly accounting information systems), blockchain development, and financial systems analysis. Participants with diverse professional backgrounds enhance the study's diversity, providing in-depth insights into how to integrate these technologies into a single accounting information system, as well as the challenges and potential benefits of integrating innovative technology into modern accounting systems.

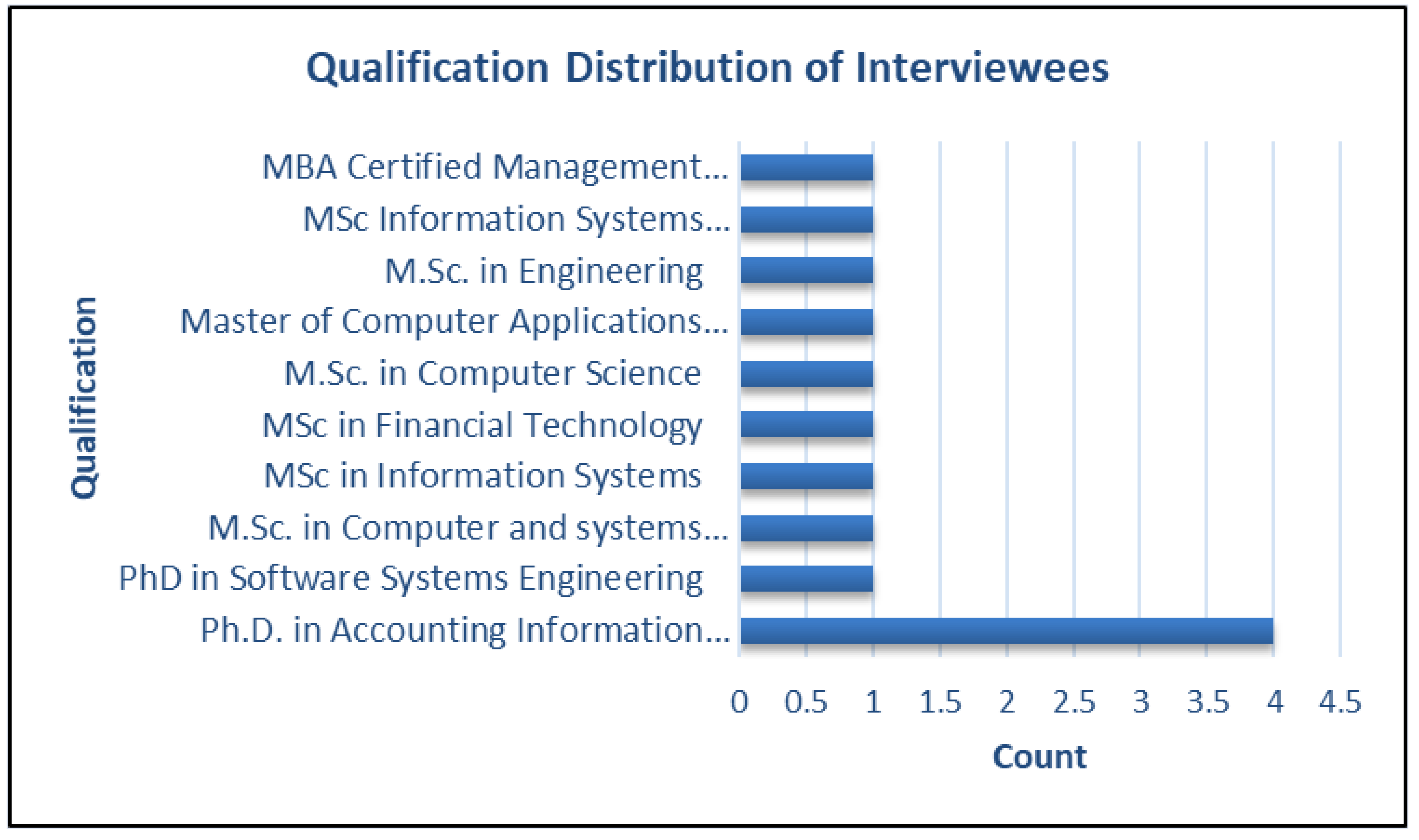

Figure 3 presents the qualifications of the interviewees, highlighting a strong academic foundation among all participants. The highest and most predominant qualification is a master's degree in information systems engineering and financial technology. This is followed by PhDs in Accounting Information Systems, ensuring a broad perspective on how best to integrate emerging technologies into accounting.

The data collection procedure commenced with the development of an interview protocol to provide a guide to conducting the interviews. Based on the related literature on IoT, blockchain, and XBRL, several interview questions were developed, as shown in Appendix B. The study used LinkedIn, a social networking service, as the primary platform for searching and reaching out to the targeted participants. Initially, a total of 20 potential participants were identified, and each was sent an email invitation along with a copy of the consent form and participant information sheet. After the potential participants consented to participate, the interview time and location were arranged according to their preferences. The majority of the interviews were conducted online via Microsoft Teams, with the exception of one interview that took place in person within the city of Leicester. Before each interview, the researcher obtained a signed consent form from the participants and sent them a Microsoft Teams meeting invitation link at the appointed time.

This paper adopted thematic analysis to analyze the qualitative data. According to Braun & Clarke (2006), thematic analysis is a technique used to identify, analyze, and interpret patterns of meaning (themes) in qualitative data. Using thematic analysis offers several important benefits, such as the ability to provide comprehensive and high-quality analysis of large qualitative datasets; simplicity and clarity; and the ability to effectively extract and analyze important themes from datasets (Braun & Clarke, 2006; Castleberry & Nolen, 2018; Finlay, 2021; Lochmiller, 2021; Naeem et al., 2023; Nowell et al., 2017). Additionally, Braun and Clarke (2006) assert that thematic analysis provides a flexible and user-friendly method for assessing qualitative data, which can be applied to any relevant theory and research methodology. These benefits are why the thematic analysis approach was chosen for this study. After transcription, the interviews were uploaded to NVIVO and coded using a mixed thematic analysis technique. This hybrid approach uses inductive coding to find patterns in the data and deductive coding to apply predefined themes from literature and theories. This allows for a comprehensive analysis of emergent ideas and theoretical constructs (Kiger & Varpio, 2020; Nowell et al., 2017; Thomas & Harden, 2008).

4. Results and Discussion

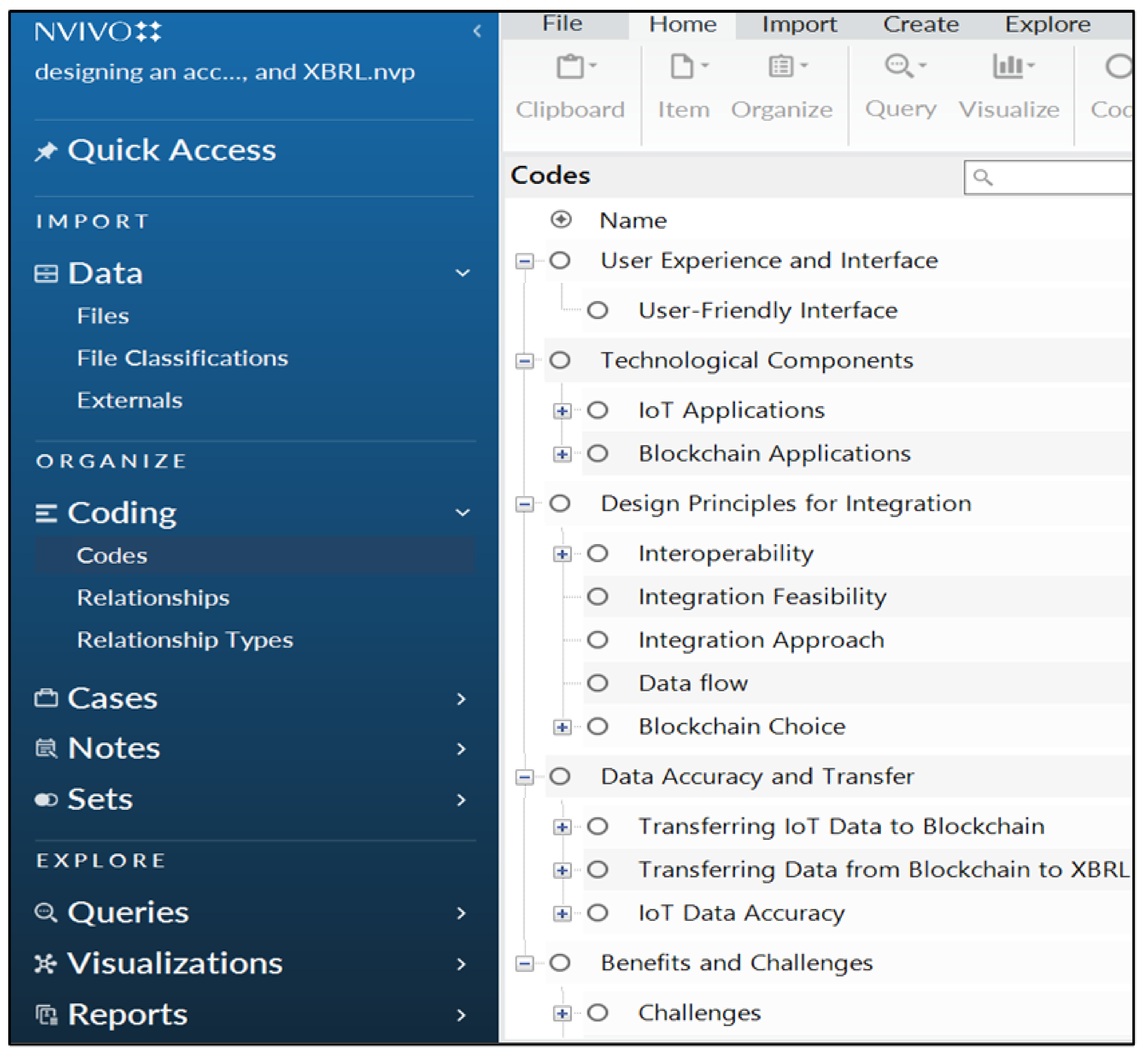

The thematic analysis of the interview transcripts identified key areas of focus for understanding the integration of IoT, blockchain, and XBRL technologies into accounting systems. The main themes include technological components, integrated design concepts, data accuracy and transmission, benefits and challenges, and user experience and interface. Subthemes include IoT applications, blockchain applications, interoperability, integration feasibility, data flow, and others. Figure 4 illustrates the primary themes and subthemes, offering a detailed overview of the interview topics.

4.1. Integration Feasibility

All interviewees agreed on the technical feasibility and high potential of integrating IoT, blockchain, and XBRL into a single accounting system. It was argued that these technologies would complement each other perfectly by enhancing specific components of financial operations. P1, blockchain engineer, asserted:

“It's totally doable, and it's a great idea from my perspective. You could have your IoT devices capturing data, then have it stored safely by the blockchain, and then—boom—come the automatic formatting of that data for financial reports with XBRL. To sum it up in a word: automation. So many of the accounting functions involved in this whole stream can be handled with such a system. Inventory management, invoice processing, and even financial reporting—all may occur on a preprogrammed basis.”

Participants explained how each technology fits into the planned system. The company uses IoT sensors and devices to collect real-time data from all sources, including inventory levels, machine status, and sales transactions, eliminating manual data entry and minimizing errors (Sharma et al., 2024). The blockchain network securely receives real-time data from these IoT devices (Košt’ál et al., 2019; Xu et al., 2021). Blockchain technology stores data in an immutable, transparent ledger that cannot be altered without authorization, ensuring data integrity (Grigg, 2024). Blockchain smart contracts automatically update accounting records based on predefined rules (Chou et al., 2021). They can automatically update journal entries, inventories, and process transactions within the accounting system. This further reduces manual intervention, ensuring the maintenance and updating of accounting records. After smart contracts process the data, XBRL is used. Financial reporting in XBRL is machine-readable and facilitates easy comparison (Sanad, 2024).

The method involves mapping blockchain data to XBRL taxonomies and validating it to ensure regulatory compliance (Mosteanu & Faccia, 2020). XBRL data is utilized in standardized financial reports. Accurate, transparent, and regulatory-compliant reports ensure that auditors, regulators, and investors can easily understand them. For example, P13, senior blockchain developer, highlighted:

“Yeah, it's definitely possible. Tricky, but possible. Here's how I see it playing out: With all your IoT devices out there doing their thing—collecting data—your information flows into the blockchain, where it sits as your safe, unchangeable database. The blockchain's smart contracts process that data to develop those automatic journal entries we were talking about. Here is where XBRL comes in. You could easily program your system to have the blockchain automatically produce those same financial reports but with XBRL tagging. But let me tell you, getting all these pieces to play nice together will not be a walk in the park. Serious integration work will be required.”

Even though combining IoT, blockchain, and XBRL holds significant promise, the interviewees pointed out a few issues that need to be addressed before this system can be implemented.

4.2. The Challenges of the Proposed System

This section discusses the main challenges of integrating IoT, blockchain, and XBRL, as highlighted by the participants, and explores possible solutions to overcome these challenges to ensure the system's success.

Firstly, one significant challenge of the proposed system is the complexity of integrating diverse technologies. The participants argued that integrating some technological tools that "speak different languages," as they expressed, could be challenging. P1, blockchain engineer, illustrated:

“The considerable challenge of course would be the integration. IoT devices, blockchain technology, XBRL software some would liken it to getting different languages to talk with one another. It's sometimes hard to get those to speak well with each other.”

P6, blockchain engineer, agreed with the previous statement, elaborating:

“The guiding, bringing it all together is a significant challenge. IoT devices, blockchain systems, and XBRL tools can be very disparate technologies to integrate and work smoothly together.”

To overcome this challenge, the interviewees suggested using specialized middleware or integration platforms (e.g., Apache Camel, Apache Kafka) to facilitate communication between different components (IoT, blockchain, and XBRL). Apache Camel is an open-source rule-based routing and mediation engine (Emmersberger & Springer, 2013). It is designed to provide API implementation, abstracting various systems in a way that allows different applications to use the same API, thus making it easier and simpler to use without the hassle of writing custom complex integration code. Apache Kafka is an open-source, distributed event streaming platform (Peddireddy, 2023). It was designed to provide efficient data processing and low latency, but it is most commonly used to build real-time pipelines for moving extracted information for real-time indexing (Sanjana et al., 2023). For example, P11, professor of accounting information systems clarified:

“I would strongly urge the implementation of any middleware platform, like Apache Camel, to make all these systems just talk to each other seamlessly”

Additionally, P12, software engineer, illustrated:

“This requires solid integration tools and middleware, like Apache Kafka, to process streams of data and ensure systems communicate efficiently.”

Additionally, ensuring data accuracy and validation is another challenge of the proposed integration. The interviewees expressed their worries about the quality of data in the proposed system. They emphasized the importance of ensuring data accuracy, as inaccurate input data can compromise the entire system. For instance, P2, professor of accounting information systems, mentioned:

“You know the saying, Garbage in, garbage out. If your sensors give you insufficient data or somebody makes a human error when the data is entered manually, it all gets messed up. You have to be very, very careful about making sure all of your data is accurate.”

To overcome this challenge, the interviewees recommended implementing multi-level validation processes at different stages of data processing, from IoT devices to XBRL reports. For example, P13, senior blockchain developer, explained:

“My advice would be to put in place multi-level validation—at the IoT devices themselves, then again when data hits the blockchain, and finally when you're creating the XBRL report. It's kind of like having three layers of quality control.”

Another challenge mentioned by the interviewees is the scalability of the system, specifically the ability of the proposed system to handle increased scale. When users, data, or the complexity of operations increase, this system should continue to be effective without significant degradation in performance. They were concerned that the system might face limitations in handling a continuous increase in the number of IoT data inputs. Additionally, they were concerned that blockchain networks might encounter scalability issues, leading to long transaction processing times (Akter et al., 2024). For instance, P8, professor of accounting information systems, argued:

“While it can handle a vast amount of information, it is not limitless. If numerous IoT devices are sending a tremendous amount of information, then you are most likely to face problems. Besides this, calls to the blockchain can end up being rather expensive if many transactions have to go through. You need to make sure in both cases that the system is within budget and can be scaled according to your business expansion.”

To address scalability issues, participants suggested implementing scalable blockchain platforms such as Hyperledger Fabric (Pajooh et al., 2021). Hyperledger Fabric is a modular enterprise-grade permissioned blockchain technology that can optimize performance and handle large transaction volumes (Melo et al., 2022). In addition, Layer 2 solutions process transactions off-chain, reducing the load on the main blockchain, particularly for base-layer blockchain systems (Hang & Kim, 2021). For example, P9, financial systems analyst, claimed that:

“Another way is to use the permissioned blockchain like Hyperledger Fabric. A business-class blockchain is capable of enduring burdens prompted by information and transaction loads. It also performs very well compared to public blockchains, which for this purpose can become very costly.”

Furthermore, the cost of implementing the suggested system was another issue raised in the interviews. Participants acknowledged that an integrated IoT, blockchain, and XBRL system is expensive to set up and maintain. IoT integration requires a large number of devices with reliable connectivity, significant hardware and network infrastructure investments, and substantial maintenance costs (Lee & Lee, 2015). Setting up and maintaining a secure, scalable blockchain network involves a significant initial cost (Akter et al., 2024). XBRL integration requires additional spending because existing systems and procedures must be updated to accommodate the financial reporting standard (Sassi et al., 2024). This includes software updates, employee retraining, and system reconfiguration to meet XBRL standards. For example, P3, professor of accounting information systems, explained:

“Setting up and then maintaining such an integrated system can be highly expensive upfront. Integrating blockchain, IoT, and XBRL is labour- and cost-intensive. Therefore, do a complete cost-benefit study to ensure that the benefits derived will be of greater importance than the costs incurred”

To address cost issues, participants suggested several options. Cloud-based solutions could reduce infrastructure costs and scale at a price that is manageable for the organization (Bonsón & Bednárová, 2019). Additionally, using open-source blockchain and IoT platforms like Hyperledger Fabric and ThingsBoard can reduce software licensing costs. Also, using open-source XBRL tools can help standardize reporting without significant costs (O'Riain et al., 2012). Participants also recommended conducting regular cost-benefit analyses that would justify the investment in the integrated system and ensure business-aligned returns. They also advised a phased implementation of the proposed system. This is supported by the discussion of P5, senior financial systems analyst, elaborating:

“Therefore, do a complete cost-benefit study to ensure that the benefits derived will be of greater importance than the costs incurred. Again, consider cloud-based options that can help cut down infrastructural expenses and make a system more able to scale for additional users”.

Moreover, the interviewees explained that user adoption and training are essential for the successful implementation of the proposed system. When integrating IoT, blockchain, and XBRL into an accounting system, interviewees raised user adoption as a major challenge. They suggested that such modern and complex technologies could be problematic for users, especially those accustomed to traditional accounting methods. They highlighted that employees may resist new systems and processes during this technological transition. This integrated system design relies on users being willing to accept changes, adapt to new workflows, and use the system efficiently. They argued that without user acceptance, the accuracy, security, and efficiency gains from integration may remain unrealized, reducing the system's overall efficacy. P6, blockchain engineer, expressed:

“What good is it to develop the best system in the world if nobody would like to work with it? Your accountants and other users must be on board and understand how the system runs”

To address this challenge, participants suggested implementing comprehensive training programs and involving users from the outset. They pointed out that early employee involvement will ease concerns, increase trust, and ensure that the technology aligns with user needs. Early user involvement allows organizations to gather valuable insights into the system's design and operation, making it more user-friendly and easier to use. This inclusive approach would help identify potential resistance and allow the organization to prepare accordingly. Finally, extensive training and follow-up should instill confidence and competence in staff using the new integrated accounting system (Fresner & Engelhardt, 2004). For instance, P7, blockchain engineer, stated:

“The success of the method is very much dependent on the level of training and familiarization needed in using it. Some resistance to this more integrated technique can come from persons trained using older accounting methods. To get around this, give end-users sufficient training and involve them during the early planning stages. This will make them understand the benefits and ease their dislike of the change.”

Also, another challenge raised by the interviewees is the difficulty of ensuring cross-jurisdictional compliance in the proposed system. Diverse regulatory landscapes across different regions pose significant challenges due to varying compliance requirements (Younis et al., 2024). For example, IoT involves varied data privacy and security regulations that differ from one region to another. Additionally, despite its inherent properties of transparency and immutability, blockchain technology still faces legal and regulatory review (Akter et al., 2024). This specifically pertains to data protection laws, financial regulations, and contractual enforceability across various countries. Failure to meet compliance requirements can result in legal implications, financial penalties, and a loss of stakeholder confidence. Thus, cross-jurisdictional compliance is one of the most important and challenging aspects of implementing this integrated accounting information system. For example, P9, blockchain developer, commented:

“Compliance with regulations is challenging because new technologies, like blockchain and IoT, vary continuously. It can become very exhaustive to stay in compliance as guidelines keep changing”

Interviewees suggested several cross-jurisdictional compliance strategies. First, consulting legal and regulatory professionals to understand compliance needs in each jurisdiction. This would ensure that legal compliance measures are incorporated into the system design from the outset. Second, the system should have a flexible compliance structure. Adaptable configuration settings and modular updates would enable the framework to adapt to changing regulations. P1, blockchain engineer, remarked:

“Tracking the changes and due info on new rules will support maintaining pace. Also, make your system flexible so that you might adapt to any new needs quickly. Another way to make sure your system meets the required standards is by working in cooperation with compliance experts and regulatory groups”

Although the proposed system may face some challenges, interviewees indicated that minimizing these challenges could yield significant benefits. It can improve operational efficiency, data accuracy, and security. The benefits of the proposed system justify the investment and help create a more robust and future-proof accounting infrastructure.

4.3. The Benefits of the Proposed System

The following paragraphs discuss the potential benefits of the proposed system based on analyzing the interviewees' responses.

Firstly, interviews revealed that the proposed system could improve accounting data accuracy and timeliness. Because IoT sensors and blockchain technology require little to no manual entry, they could eliminate the error-prone and delayed processes associated with manual data entry (Louis & Dunston, 2018). This would allow data to be automatically captured at its source, reducing discrepancies in financial records (Desyatnyuk et al., 2022). The real-time data flows from IoT sensors transition enterprises from periodic reporting to continuous availability of financial information. Real-time insights improve decision-making efficiency and enable businesses to respond quickly to changes with reliable data (Karmańska, 2021). Smart contracts on the blockchain would automatically update accounts using IoT real-time data (Chang et al., 2019). As P1, blockchain engineer, highlighted:

“This would provide access to accurate and timely data. Imagine a situation where your inventory is changing continuously. IoT sensors avoid manual counting and, hence, are much more efficient and precise. We get the data in real-time, and we have introduced a blockchain system that will create a perfect record of it”

Also, P5, senior financial systems analyst, supported this by elaborating:

“This can even extend to data collection more accurately and in real-time. IoT devices automate data collection—for instance, inventory amount and utilization of assets—without leaving a window of error by people. The real-time data helps ensure that your financial data remains accurate and fresh. Higher integrity and security for data are major benefits. Data once recorded on blockchain cannot be deleted. This makes the records of all financial transactions very secure and reliable.”

Additionally, interviewees identified the system's potential to automate and enhance accounting operations as its greatest benefit. They emphasized the integrated system's ability to simplify or eliminate manual, labour-intensive procedures. IoT, blockchain, and XBRL automate data collection, recording, and reporting, thereby improving workflow (Faccia et al., 2019). This would reduce the burden on accounting professionals and minimize errors associated with manual processes. For example, P2, professor of accounting information systems, remarked:

“To sum it up in a word: automation. So many of the accounting functions involved in this whole stream can be handled with such a system. Inventory management, invoice processing, and even financial reporting—all may occur on a preprogrammed basis, thus reducing errors and releasing accountants for far more strategic work”

Furthermore, the interview data analysis suggested that this proposed solution could improve accounting data integrity and security. Blockchain technology was highlighted as the primary driver of this potential benefit. Interviewees noted that an immutable, tamper-proof blockchain would greatly enhance the reliability of financial records (Alkafaji et al., 2023; Dai & Vasarhelyi, 2017). IoT data collection reduces human error and manipulation, thereby improving data integrity (Nofel et al., 2024). Standardizing financial data with XBRL enhances data integrity and accessibility (Al-Okaily et al., 2024). From data acquisition to structured representation, this approach strengthens the reliability and auditability of financial information. Supporting this, P6, blockchain engineer, indicated:

“A significant advantage is better integrity and protection for data. Data recorded on blockchain cannot be deleted. This makes your records of all financial transactions much more secure and reliable”

Moreover, interviews indicated that integrated IoT, blockchain, and XBRL systems can reduce costs. Participants acknowledged that while implementation costs are significant, this system offers long-term financial benefits by automating manual tasks and reducing errors, thereby decreasing labor expenses. It enhances data quality and reduces the need for manual data entry and verification, thereby lowering administrative costs. The blockchain component simplifies fraud investigation, further reducing costs. Interviewees also noted that streamlined regulatory reporting saves money through increased XBRL compliance. P4, blockchain developer, pointed out:

“By doing that, you can save much in administrative costs. With all the manual work, fewer mistakes, and higher data quality, it cuts down all the administrative costs. Blockchain also reduces the possibility of fraud and additional work in investigating it. In addition, XBRL facilitates compliance with regulations and hence reduces fines and penalties. Everyone benefits in this value chain”

In addition, participants suggested that the proposed system could increase accounting transparency and trust. The open and immutable ledger qualities of blockchain contribute to this benefit (Jena, 2024; Rijanto, 2024). Participants emphasized the need to trace and verify blockchain transactions to enhance financial data accuracy and reliability. Additionally, transparency, combined with real-time IoT data, can produce credible financial reports. Moreover, standardized financial information facilitated by XBRL enhances stakeholder confidence by improving reporting clarity and accuracy (Al-Okaily et al., 2024). The interviewees argued that this system can improve accounting transparency and confidence by incorporating all three technologies. P2, professor of accounting information systems, highlighted:

“Doesn't it make things pretty transparent? You will with blockchain be able to consider it an open book of sorts where anybody can see what is going on and completely immutable. This engenders trust with the investors, the auditors anyone who needs to have confidence in your information. You can also apply XBRL, so you're not just firing out numbers, it's structured, so everyone can compare your data quickly and see what is going on.”

After establishing the significant potential benefits of integrating IoT, blockchain, and XBRL into a unified accounting system and acknowledging the challenges involved, the next section of this paper focuses on the practical aspects of system design.

4.4. Specific Design Considerations

The participants discussed several considerations that must be taken into account during the design of the proposed system, which are explained in the following section.

4.4.1. Integration Approach

Interview data analysis strongly supported a centralized integration approach, with a single blockchain serving as the key data repository, a secure database and a processing engine (Akter et al., 2024; Bonsón & Bednárová, 2019). Regarding the suitable blockchain platform, participants suggested using Hyperledger Fabric. The analysis also indicated that the implementation of the proposed accounting system requires a layered approach to integrate IoT, blockchain, and XBRL. Participants recommended starting with IoT sensors at inventory and production lines to collect real-time data. Many participants suggested a multi-step process involving edge data filtering and blockchain smart contracts for cross-verification to validate data. Then, validated data is transmitted to a permissioned blockchain network using high-grade encryption and access controls to ensure data integrity and immutability. Sequentially, blockchain smart contracts automate journal entries and transaction validation. Finally, the system converts blockchain data into XBRL format using a translator module or by configuring the blockchain to automatically generate tagged reports. P11, professor of accounting information systems, pointed out:

“Combining IoT, blockchain, and XBRL is best achieved by creating a multi-layered system. The first step is deploying the IoT sensors to collect real-time data. This could be inventory levels, status of equipment, or sales transactions. Then, the collected data is securely transferred to a blockchain network, ensuring its immutability and resistance to tampering. Smart contracts would, therefore, generate journal entries on the blockchain automatically with this available information. Finally, the data sourced from the blockchain shall be extracted and transformed in the form of XBRL-formatted data so that consistent financial reporting can be achieved”

Several experts recommended a modular and incremental implementation approach, where strategically chosen accounting processes would be implemented first, followed by a gradual expansion of the system's scope. This would enable phased implementation, allowing organizations to test the system before fully implementing it (Pérez Estébanez, 2024).

4.4.2. Interoperability

The participants asserted that the seamless communication and data exchange between the integrated components—IoT devices, blockchain, and XBRL—are therefore paramount. The interviewees emphasized interoperability as a key factor in creating a unified and functional accounting system. P1, blockchain engineer, elaborated:

“Take, for instance, individuals who speak different languages. Definitely, if they are going to discuss something with each other, then some kind of translation in the middle is necessary. In the same way, in these technologies, a layer has to be interposed in order for them to be able to talk to one another”

Participants recommended adopting standardized APIs, middleware for data processing and routing, and well-defined data formats like JSON or XML to achieve interoperability. Middleware for data transformation and interoperability emerged as a key theme. Middleware facilitates connectivity between IoT devices, blockchain networks, and XBRL systems (Alles & Grey, 2020). Additionally, APIs (Application Programming Interfaces) were frequently cited as essential for system communication. APIs enable different technologies to communicate effectively (Efuntade & Efuntade, 2023). Most interviewees emphasized the importance of well-defined APIs that bridge systems to facilitate seamless information flow.

4.4.3. Blockchain Choice for the Proposed System

Many interviewees preferred Hyperledger Fabric as a permissioned or private blockchain to use in the proposed system. The main advantages of this choice are improved privacy and security of sensitive financial data, access rights control, scalability, and regulatory compliance (Antwi et al., 2021). Participants also highlighted customization and blockchain adaptability for corporate needs. Moreover, the ability to efficiently handle large amounts of IoT data was another important factor. Some participants cited R3 Corda and Quorum, but all recognized Hyperledger Fabric as enterprise-grade, supporting smart contracts with seamless integration in most systems (Kim et al., 2021). P8, professor of accounting information systems, commented:

“Looking at the requirements of your system, I would propose private blockchains like Hyperledger Fabric, and Corda would be suitable for your system. Hyperledger Fabric provides a reliable and flexible platform with many advanced features to handle vast amounts of automated IoT data together with manual data entries in a reliable and failsafe way. This allows one to automate different processes with its strong support for smart contracts, confirming the integrity and safety of data and compliance with regulations”

4.4.4. IoT Data Accuracy

Based on the interviewees' knowledge, the accuracy of an accounting information system depends on its inputs; therefore, they emphasized that IoT data must be examined and verified before being recorded on the blockchain in the proposed system. IoT challenges may include sensor errors, transmission issues, and malicious manipulations. Interview data suggests several methods to validate and verify IoT data before recording it in accounting systems. Participants emphasized that edge computing is essential for source-level real-time data validation (Yu et al., 2017). These checks filter out noise from malfunctioning sensors to ensure data falls within expected ranges. Furthermore, smart contracts implemented on the blockchain could automatically flag or reject data that does not meet preset criteria for data quality rule compliance. To prevent data collection problems, participants suggested monthly calibration and maintenance testing for IoT devices. Also, cross-validation of critical data points by multiple sensors improved data accuracy (Garrido-Labrador et al., 2020). Most importantly, human evaluation through regular reviews and audits was also deemed important to detect errors and ensure data integrity (Zhou et al., 2018). P4, blockchain developer, expressed:

“A good starting point is edge computing, as one of the activities for ensuring that data from the IoT is accurate before being recorded in the accounting systems. These include data validation and preprocessing at the data source: the scrubbing of information that may not be necessary, and the correction of any abnormalities. Use threshold checks to discard data that falls outside the expected ranges. Making sure your data is clean from the beginning is critical”

4.4.5. Transferring IoT Data to Blockchain

Blockchain technology is ideal for secure and transparent data storage; however, most interviewees agreed that moving raw IoT data directly to the blockchain is not recommended. According to the participants, directly transmitting IoT data to the blockchain raises concerns about data quality and volume. Data analysis also indicated that IoT data needs to be processed and prepared by middleware before being recorded on the blockchain. As P9, blockchain developer, mentioned:

“This would probably not be the best approach, considering that potential data quality issues may create problems. There has to be an intermediate step within this process to clean and validate the data properly. Instruments like Apache NiFi for data transformation and AWS IoT Core for ease of integration help in making sure that the data recorded on your blockchain is clean and accurate, maintaining its integrity”

4.4.6. Transferring Data from Blockchain to XBRL

Interview data revealed a multi-step method for automatically converting blockchain transactions into XBRL financial statements. First, the Hyperledger Fabric REST API should be used to extract blockchain transaction data. Most participants favoured middleware like Apache NiFi for cleaning and validating the extracted data. The next crucial step is translating blockchain data into financial statements and XBRL tags. To do so, participants suggested using Python transformation scripts or mapping tools like Altova MapForce. The interviewees stressed the necessity of choosing the right XBRL taxonomy for the business and region. Finally, tools such as Arelle, Altova MapForce, and XBRL Composer can be used to create XBRL documents. Participants proposed automating blockchain-to-XBRL data transmission using ETL tools like Talend or Apache Airflow. Additionally, participants suggested using the XBRL Validation Suite to check technical and business rules during validation. Additionally, Participants recommended using cryptographic methods like hashing and digital signatures to protect data transferred from the blockchain to the XBRL software. Data should be hashed to create a unique fingerprint that helps detect any changes. On the other hand, digital signatures verify the integrity of the data source. The interviewees also suggested implementing role-based access control to restrict data access to authorized entities.

4.4.7. User-Friendly Interface

Interviewees stressed the need for a simple human data input interface because IoT devices cannot capture all data. Accountants will use the interface as a bridge to easily interact with the secure blockchain-based system. Participants emphasized the need for a user-friendly design that facilitates data entry and reduces errors. They suggested using web applications due to their ease of use and accessibility. Additionally, participants recommended using APIs to seamlessly connect the user interface with the blockchain for secure data transfer and smart contract recording. For instance, P1, blockchain engineer, stated that:

“There must be a simple interface to enable accountants to enter data into the blockchain simply. This can be realized with Web or mobile app logins, followed by the completion and submission of forms with data obtained. Ensure that the forms have inbuilt checking to avoid errors before the information is finally dispatched. Use multi-factor login and encrypt data while sending it over to protect it. Information, upon being sent, is dealt with by an API and stored on the blockchain by smart contracts”

4.5. The Proposed System

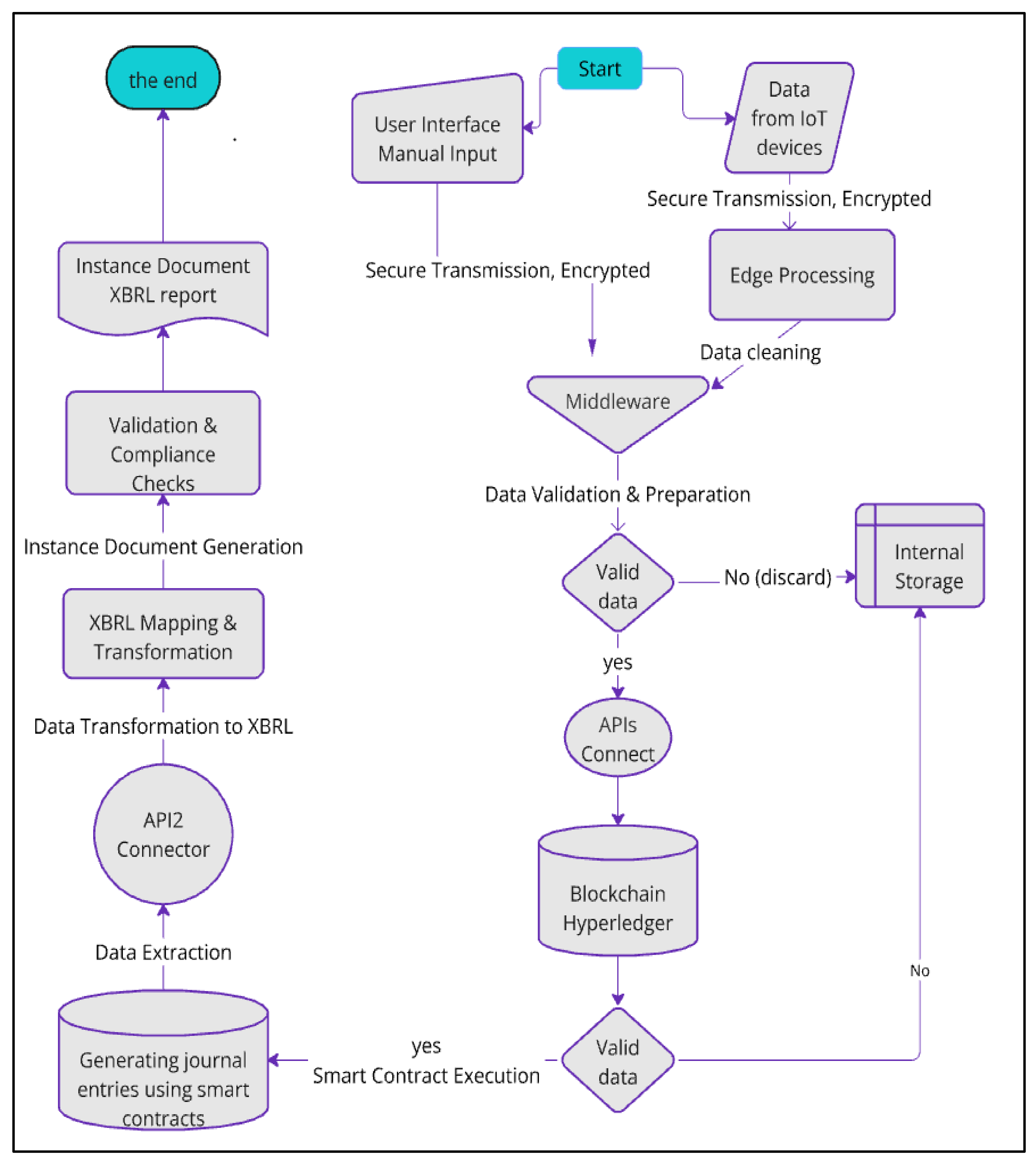

The proposed integrated accounting system relies on a robust and secure data flow, utilizing the interaction among IoT, blockchain, and XBRL technologies to automate processes and achieve financial transparency. Figure 5 presents a flowchart of the data flow, starting from data capture and ending with the production of validated XBRL reports.

As seen in Figure 5, the proposed system begins with data collection, which serves as the system's input. The data flow within the proposed system begins with receiving data from two primary sources: IoT devices and manual input. The first step involves incorporating IoT sensors into various business operations to collect data. The IoT devices monitor real-time data related to multiple aspects, such as inventory levels, equipment status, and sales transactions. Next, edge computing devices process raw data from these IoT devices through preliminary validation and filtering. This edge computing layer is the first step toward ensuring high-quality data and minimizing the data volumes to be transmitted to the blockchain at a later stage of the system. Based on the analysis of interviewees' responses, edge processing offers several benefits: it reduces the amount of data sent to a central server by filtering out unnecessary information; it improves data quality by eliminating inconsistencies or errors at their source; and it enables real-time responses to critical events.

Simultaneously, data that cannot be automatically collected by IoT devices is recorded by authorized accountants using a simple user interface accessed through web browsers or mobile applications, as suggested by the interviewees. This manually entered data is transmitted to a server using secure, encrypted protocols. Then, both IoT collected and manually entered data flow into a middleware layer powered by robust data processing tools such as Apache Kafka, as suggested by the interviewees. This layer will further clean, validate, and aggregate all incoming data. It acts as a buffer between the high-volume, real-time data collection of IoT devices, the more structured manually handled data, and the transaction-based nature of the blockchain. Additionally, this intermediate layer will standardize data formats, resolve discrepancies across information sources, and securely prepare the consolidated data for transmission to a blockchain network. At the middleware level, data undergoes comprehensive validation. This step essentially checks data for accuracy and relevance against predefined business rules, normalizes the data, and ensures that all incoming information meets the system's standards. This stage ensures data consistency and prepares it for integration with the blockchain and financial reporting. Any data that does not meet these criteria is rejected, ensuring that only accurate and reliable data is stored.

In the next phase, the validated data will be transmitted to the blockchain network within the system via APIs. APIs facilitate the connection between the middleware and the blockchain network. Based on the interviewees' recommendations, Hyperledger Fabric is the most suitable blockchain for the proposed system due to its previously discussed benefits. The blockchain contains smart contracts that self-execute to automate various accounting functions. These contracts can be used to create journal entries, validate transactions, and execute predefined actions based on both the incoming IoT data and manually entered data. These smart contracts are pre-programmed with specific accounting rules and triggers. When valid data enters the blockchain, the relevant smart contracts automatically execute, generating appropriate journal entries. This automation significantly reduces manual intervention, minimizes errors, and ensures the consistent application of accounting principles across all transactions. For example, a smart contract could automatically calculate depreciation based on IoT-reported equipment usage while allowing manual adjustments through the user interface.

As the system approaches its final stage, the financial data recorded on the blockchain will be extracted using secure APIs and transmitted to a tool designed for mapping financial data for reporting in XBRL format. This step prepares the comprehensive dataset for its final conversion into XBRL format. The interviewees recommended using specialized tools like Altova MapForce to map blockchain data to relevant financial accounts and XBRL tags, ensuring accurate translation into standardized financial reporting formats.

The final step in the data processing workflow is generating XBRL instance documents. According to the interviewees, after the mapping and transformation of blockchain data are completed, XBRL documents can be generated using tools such as Arelle or XBRL Composer. Afterward, the instance document must undergo a final validation process using the XBRL Validator Suite or similar tools to ensure compliance with regulatory requirements or reporting standards, resulting in an accurate and standardized financial report ready for submission or analysis. According to the interviewees, the entire process, from collecting IoT data and manual input to generating XBRL reports, can be managed by automated workflow tools such as Apache Airflow or Talend. These tools ensure that each stage of the data flow is executed in the correct sequence and at the appropriate times.

5. Conclusions

This paper aims to propose a new framework for integrating IoT with blockchain and XBRL into a modern accounting system. This proposed framework seeks to enhance the efficiency, accuracy, and transparency of accounting systems. By leveraging the capabilities of these emerging technologies, the proposed framework can address the growing demands for real-time data processing, secure transactions, and standardized financial reporting.

This paper employed a qualitative research design using semi-structured interviews with 13 participants from various professional backgrounds, including IT engineering, academia (specifically in accounting information systems), blockchain development, and financial systems analysis, all with a minimum of 9 years of experience. The main contribution of this paper is an extensive framework for designing an innovative accounting system that integrates IoT, blockchain, and XBRL, based on insights from the interviewees. The analysis of interviews yielded valuable insights into the technical feasibility, benefits, and challenges of such integration. According to the interviewees, the proposed framework can bring significant improvements in data accuracy, automation, enhanced security, and, ultimately, cost efficiency. However, it also presents challenges related to integration complexity, scalability issues, and cross-jurisdictional compliance concerns.

Despite providing extensive insights into the best way to integrate IoT, blockchain, and XBRL into a single accounting system, this paper has some limitations that must be acknowledged and can be addressed in future research. First, it relies on qualitative data derived from semi-structured interviews with a relatively small sample of 13 industry experts. Although these participants were selected based on their expertise and diverse professional backgrounds, the number of interviews conducted might not fully capture the range of perspectives and potential challenges that exist for such integration in different sectors or geographical regions, which may limit the generalizability of the findings. Additionally, this paper is a conceptual framework and did not undergo empirical testing in the real world. Following this conceptual foundation, the proposed system design in this paper needs to be tested through practical implementation to gain adequate legitimacy. Furthermore, the rapid evolution of the involved technologies—IoT, blockchain, and XBRL—can be a limitation of this study. Advancements in the technologies may render some features of the framework irrelevant or require significant changes to the framework to accommodate them. Moreover, the study did not discuss how these technologies can be adapted to different regulatory environments and organizational cultures, which could impact the application of the proposed framework.

Future research can address some of the limitations of the current study by considering a larger sample size and greater participant diversity to increase the generalizability of the findings. Future research may also employ a quantitative approach to complement qualitative studies in determining the feasibility and scalability of integrating IoT, blockchain, and XBRL with modern accounting systems. Additionally, future research can use case studies to test the proposed system practically. Furthermore, the impact of the proposed system in this paper can be empirically examined on important accounting variables, such as earnings management. Since these are dynamic technologies, longitudinal studies may be necessary to assess the ongoing impact of technological advancements on the proposed framework. Future research can also investigate context-specific challenges and regulatory implications for implementing such technologies within different industries and regions.

In summary, while this study makes significant contributions to the academic discourse on accounting innovation and establishes a foundational framework for integrating advanced technologies into accounting systems, it also calls for further research to address challenges and limitations related to this integration. The combination of IoT, blockchain, and XBRL has the potential to drive significant transformation towards enhanced efficiency, transparency, reliability, and trust in published financial reports. However, additional investigation is required to fully validate this transformative potential.

Author Contributions