Submitted:

12 March 2024

Posted:

12 March 2024

You are already at the latest version

Abstract

This study aims to explore significant present and future trends in accounting and corporate sustainability by examining publications from the Web of Science database spanning from 2010 to 2023. With a particular focus on research related to the digital business environment, the study employs bibliometric analysis grounded in the resource-based view theory to investigate the evolution of auditing and digital accounting research. Utilizing the VOSviewer tool, the study analyzes keyword relationships and their geographical distribution based on a comprehensive examination of 700 publications from the Web of Science. The findings highlight the transformative impact of auditing and digital accounting on business operations in response to rapid digitization. Key clusters identified shed light on digital transformation and the intersection between information technology and corporate management, revealing the evolving research landscape. The study discusses both practical and theoretical implications arising from these findings.

Keywords:

Digital Accounting

; Auditing

; Digital Business Environment

; Accounting

; Bibliometric.

1. Introduction

In the ever-evolving landscape of modern business, the dynamic interplay between auditing, digital accounting, and the digital business environment has undergone profound transformations driven by rapid technological advancements (Turban et al., 2021). Ushering in substantial shifts in accounting practices, processes, and methods, including the adoption of digital reports, modern technological innovations facilitate swift and accurate operations (Allioui & Mourdi, 2023). Given their diverse capabilities, these emerging technologies are poised to reshape the utilization of data and information, fostering greater efficiency for companies (Brunetti et al., 2020; Lynn et al., 2017). Consequently, the digital revolution is significantly impacting the realms of accounting and auditing, highlighting the significance of professionals possessing the requisite knowledge to develop advanced accounting information systems (Zhu et al., 2023).

This paper undertakes a comprehensive examination to chart the progression of research at the intersection of auditing and digital accounting within the framework of the digital business environment. Through rigorous bibliometric analysis, we traverse the academic landscape, unraveling trends, patterns, and key figures who have shaped the discourse in this critical domain. The effectiveness of accounting and audit procedures becomes particularly evident when digitalization is utilized to monitor, analyze, and evaluate financial data. This enhances productivity significantly while simultaneously reducing costs and streamlining management processes (Kokina & Blanchette, 2019).Operating in a digital environment necessitates the generation of digital records. In accounting, a demonstration of accountability for resource use, including public funds, underscores the vital role of records (Mosweu, 2018). Underscoring the automation of auditing and accounting procedures through the adoption of business systems (Moffitt et al., 2018), the significance of digital accounting emerges from the challenges businesses face in promptly delivering accurate digital services (Bhimani & Willcocks, 2014). The recent introduction of XBRL (Extensible Business Reporting Language) has emerged as a pivotal technology supporting financial reporting for digital companies. XBRL technology facilitates the digitization of accounting information by converting diverse data formats, thereby enhancing the monitoring and reporting of accounts (Mosteanu & Faccia, 2020).

The digitalization of organizations necessitates enhanced competence and education for the audit profession, as a natural consequence of the major shift in tools and working methods (Otia & Bracci, 2022). Digital technologies have introduced novel elements into the audit process, enhancing audit quality through the analysis of larger datasets. This augmentation elevates the probability of identifying anomalies or inconsistencies in companies' transactions (Singh et al., 2019). The digital revolution has not only impacted business practices but has also redefined the paradigms of auditing and accounting. As organizations embrace digital technologies to optimize their operations, the complexities and opportunities within these domains have expanded exponentially (Gonçalves et al., 2022). This paper seeks to unveil the intellectual progression of research in auditing and digital accounting, offering a nuanced understanding of how these disciplines have addressed and adapted to the challenges and opportunities arising from the digital business environment.

We employ bibliometric analysis as our methodological foundation to navigate the vast expanse of academic literature, identifying seminal contributions, pinpointing influential authors, and uncovering thematic trends. Our exploration encompasses the early stages of digital transformation, traversing to the current landscape, and yields insights into the future trajectory of auditing and digital accounting research. This investigation strives to enhance scholarly discourse by elucidating collaboration patterns, unraveling citation networks, and highlighting emerging themes. In doing so, it aims to provide guidance for future research initiatives and cultivate a deeper understanding of the intricate interplay between technology, auditing, and digital accounting in the contemporary business environment.

This document is organized as follows: The following section delineates the research methodology and the data employed in this study. The subsequent section presents the findings of the bibliometric analysis, with an emphasis on key discussions. Ultimately, the fourth section encapsulates the main findings and draws conclusions.

2. Methodological Framework

To unravel the intricate evolution of auditing and digital accounting research in the digital business environment, our study meticulously applies a robust bibliometric analysis methodology. This quantitative approach delves into publication patterns, citation dynamics, and collaborations among authors, journals, and countries (Abu Huson et al., 2023). By leveraging bibliometric techniques, we identify influential authors and reputable journals that shape the discourse (Mukherjee et al., 2022).

A distinguishing feature of our research lies in the integration of the science mapping approach, domain analysis, and visualization techniques (Zou et al., 2018). This method, particularly effective for handling a large volume of scientific documents, visually portrays the intellectual structure of auditing and digital accounting research. It serves as a compass, revealing research trends, pinpointing gaps, and highlighting influential contributors (Goyal & Kumar, 2021; De Bellis, 2009).

The integration of bibliometric analysis and the science mapping approach forms a powerful methodology, providing researchers with valuable quantitative insights. This synergistic approach enhances their ability to make informed decisions, identify research gaps, and actively contribute to scholarly discourse. (Kastrin & Hristovski, 2021). The following paragraphs outline our research strategy across three interconnected sections.

2.1. Data Compilation

In the realm of academia, the crucial task of identifying research gaps and trends plays a pivotal role in advancing knowledge (Aboelmaged et al., 2023). In spite of the multitude of studies on auditing and digital accounting within the digital business domain, there exists a notable deficiency in comprehensive and focused research that could provide guidance for future investigations (Pizzi et al., 2021). This study addresses this gap through meticulous scientometric analysis, aiming to uncover key research topics and illuminate literature gaps in the interplay between digital audit, digital accounting, and digital business, particularly in the context of the rapid shift toward the digital economy.

Our investigation focuses on research papers from the Web of Science (WoS) core collection. Employing carefully crafted keyword-based search queries, we sifted through article titles and keywords from 2010 to 2023, ensuring our analysis encompasses the latest research advancements in auditing and digital accounting within the digital business sphere. The deliberate selection of this timeframe guarantees the contemporary, accessible, and reliable nature of the literature, enhancing the scholarly rigor of our study.

During data collection, we applied a discerning filtration process, concentrating on specialized publications in accounting, economics, and management. This methodical filtering resulted in the meticulous selection of 700 research papers, each subjected to thorough scrutiny of titles and keywords using a hybrid of theoretical and experimental methodologies. This rigorous approach ensures the precision and relevance of the chosen literature, contributing to the robustness of our study and enriching the scholarly discourse.

2.2. Selection of Research Database

In the vast realm of bibliographic data mapping, numerous databases, such as Dimensions Database, Google Scholar, Web of Science, and Scopus, provide avenues for exploration (Rojas-Lamorena et al., 2022). Within the context of our study scrutinizing digital accounting and e-business, we strategically selected the Web of Science Database to conduct the scientometric analysis. The selection was predominantly motivated by the database's extensive inclusion of scientific publications, encompassing a diverse range of pertinent literature within our analytical scope. More specifically, our attention was directed towards the bibliometric analysis of journals using the Web of Science (WoS) Core Collection database, with a notable emphasis on the Science Citation Index Expanded (SCIE) and the Social Sciences Citation Index (SSCI).

The decision to utilize the WoS database stemmed from its distinguished reputation as a premier index, housing an extensive repository of peer-reviewed articles and supplying reliable bibliographic data. Its selection was motivated not only by its renowned standing but also by its widespread adoption among researchers. The WoS database, serving as our search engine, stands as a prevalent choice for the meticulous analysis of scientific publications (Gusenbauer, 2022). Within the WoS database, each publication unfolds as a trove of information, providing details such as the year of publication, title, abstract, authors, author affiliations, source journal, subject categories, and references (Abu Huson et al., 2023; Birkle et al., 2020). This wealth of data aligns seamlessly with the demands of our comprehensive bibliometric analysis, ensuring a robust foundation for our exploration into the evolution of auditing and digital accounting research in the digital business environment.

2.3. Choice of Science Mapping Tool: Navigating the Scientific Landscape

Effectively exploring any scientific field requires adept use of a suitable science mapping method (Gahegan, 1999). Various tools, such as VOSviewer, Gephi, CiteSpace, Sci2, and HistCite, serve this purpose. Gephi, an open-source program, visualizes graphs and networks, while CiteSpace analyzes trends in academic literature (Kehinde et al., 2023).

In our research, we utilized VOSviewer to create maps from data extracted from the Web of Science (WOS) Database. VOSviewer is versatile, constructing networks across scientific publications, journals, researchers, institutions, countries, and keywords (Chawla & Goyal, 2022). It employs various links, including co-authorship, co-occurrence, citation, bibliographic coupling, and co-citation. The tool offers three-fold visualization capabilities: network, density, and overlay visualization, enhancing map exploration (Ahmad et al., 2022). Its features, such as scrolling and zooming, are advantageous for navigating expansive maps.

We employed VOSviewer to identify current trends, literature gaps, potential research areas, significant countries, sources, and authors within the study's keywords. Scientometric techniques, including bibliographic data studies, were applied. Co-occurrence analysis scrutinized recurrent words in titles, keywords, and abstracts, while bibliographic coupling pinpointed contributing authors and countries (Sustacha et al., 2022).

Scientometrics, which involves the quantitative examination of scientific communication, impact, and policy, holds a pivotal role in assessing the field-specific impacts of academic research. (Hassan & Loebbecke, 2017). It provides insights into influential research studies in Auditing and Digital Accounting Research in the Digital Business Environment. Through the application of reproducible statistical techniques, researchers have the capability to measure research output, citation rates, influential journals, scientists, as well as the countries and regions that propel advancements in the field (Liu et al., 2023). This methodology also discerns areas that necessitate heightened or diminished research activity by mapping evolving trends (Kaur, 2024).

3. Findings and Discussions

3.1. Output Analysis and Growth Trends

Evaluating scholarly output relies on calculating publication activity within a specific timeframe and from specific entities like journals, institutions, or nations. Metrics related to publication activity offer a quantitative overview of a field, facilitating the identification of influential journals, organizations, and countries (Sugimoto & Larivière, 2018). Additionally, these metrics help pinpoint key themes addressed during the study period. This research, utilizing Microsoft Excel® spreadsheets, focused on qualitative attributes such as sector of activity, study dimension, and research methodologies.

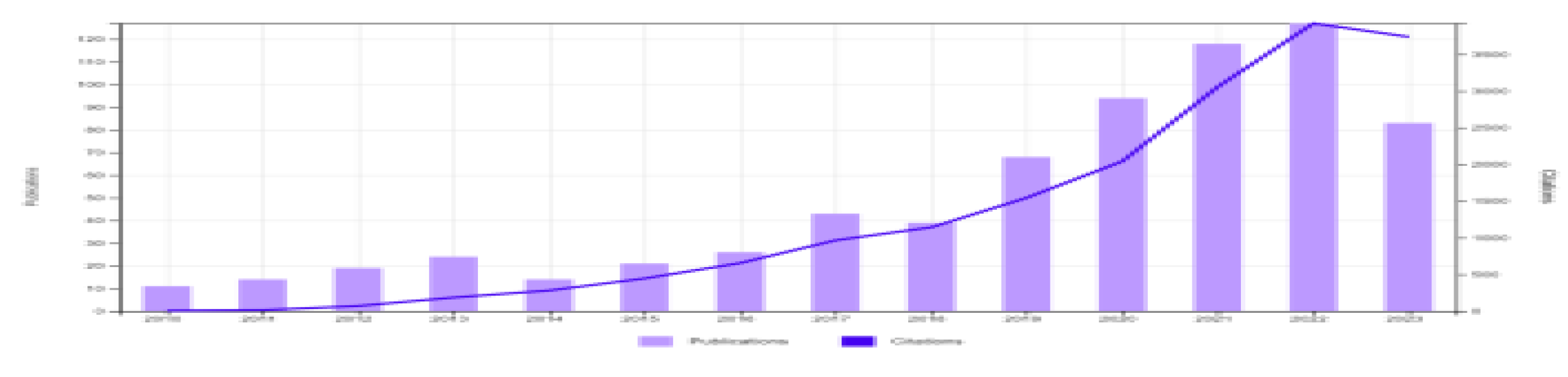

The bibliometric analysis examined the evolution of literature on auditing and digital accounting research in the digital business environment from 2010 to 2023. The study investigated significant institutions, countries, and authors, revealing substantial growth in literature on this subject in recent years. Figure 1 shows the increase in publication activity, with a significant jump in 2022 (127 publications). By 2023, there was a slight decrease with 84 publications, but the year is ongoing, and the total is expected to be higher. The 700 publications have garnered 18,112 citations, averaging 25.87 citations per publication.

Figure 1 illustrates the exponential growth in citations alongside the increasing number of published papers. Given the extensive history and evolution of these subjects, pinpointing the exact year of their conceptual introduction remains challenging.

The transformation of auditing and digital accounting research in the digital business environment signifies a shift from traditional financial scrutiny to a complex landscape driven by digital technologies (Sahut et al., 2021). In this digital context, auditing goes beyond verifying financial records to understanding the dynamics of digital processes and systems (Manita et al., 2020). Digital accounting research in the digital business environment aims to leverage technological advancements in accounting practices, recognizing the interplay between auditing, digital technologies, and the broader digital business landscape. This transformative approach underscores the need for innovative methodologies and tools to ensure the integrity and reliability of financial information in the digital age. The concept evolves in response to the challenges and opportunities posed by the ongoing digitization of business operations, emphasizing the necessity for continuous adaptation in accounting and auditing.

3.2. Key Contributions from Top Publications, Journals, and Publishers

In this section, we highlight the noteworthy contributions made by publications, journals, and publishers related to the subject under consideration.

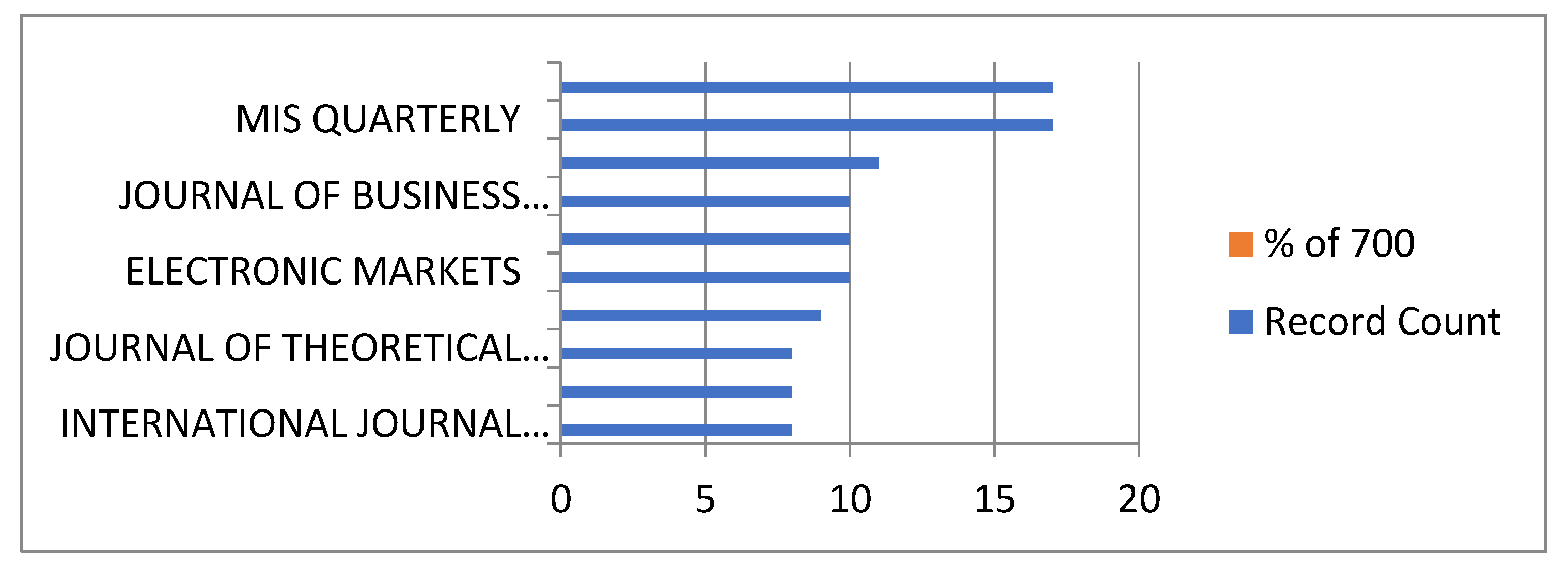

Figure 2 shows a list of journals with a high number of publications in the fields of auditing, digital accounting, and digital business. Topping the list are "MIS QUARTERLY" and "TECHNOLOGICAL FORECASTING AND SOCIAL CHANGE," both securing the first position with 17 publications each. Following closely is "MIT SLOAN MANAGEMENT REVIEW" in the second position with 11 publications, trailed by "ELECTRONIC MARKETS," "EUROPEAN JOURNAL OF INFORMATION SYSTEMS," and "JOURNAL OF BUSINESS RESEARCH," all sharing the third position with 10 publications each. These six journals collectively contribute to 9.254% of all papers published in the 397 journals.

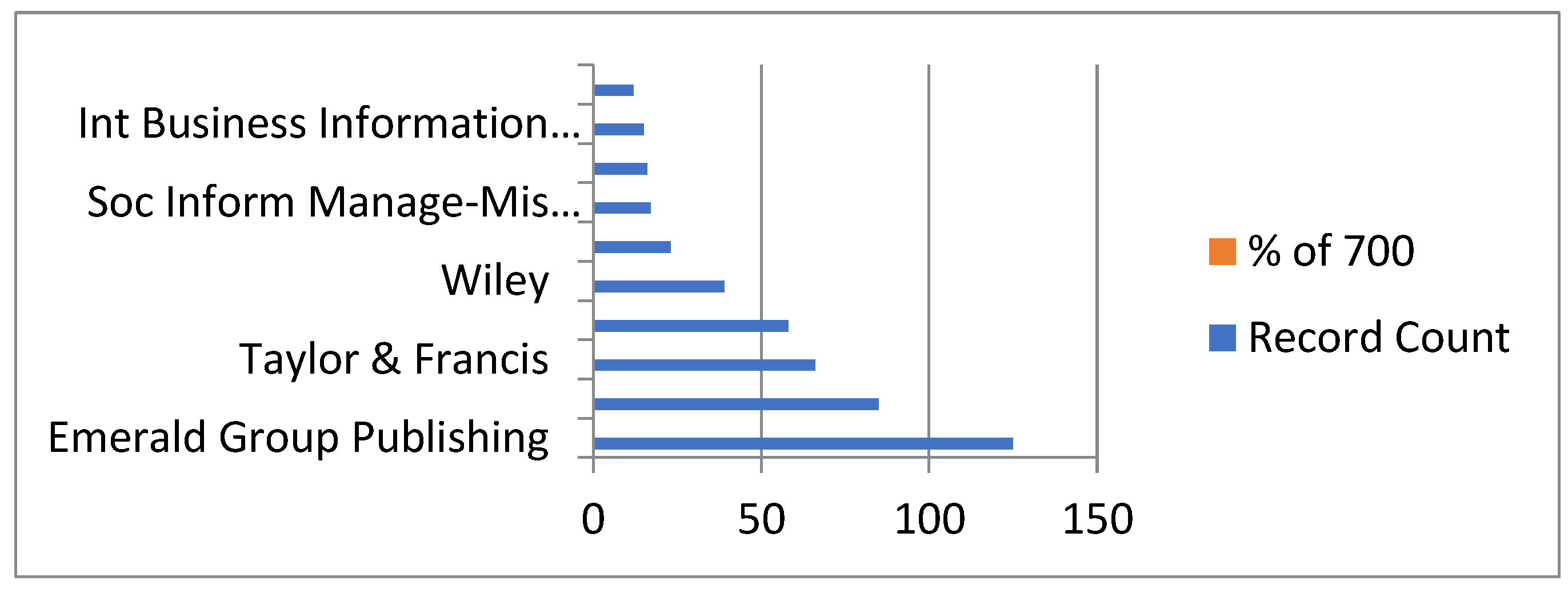

Figure 3 provides a compilation of publishers exhibiting the highest record counts in the realms of auditing, digital accounting, and digital business. Leading the list is "Emerald Group Publishing" with a noteworthy 125 record counts, representing 17.806% of the total 700 publications. In close pursuit is "Elsevier" with 85 record counts, and "Taylor & Francis" holds the third position with 66 record counts. Collectively, these three prominent publishers contribute significantly, encompassing 39.32% of the total record counts documented across all publishers, according to the WoS database.

3.3. Bibliometric Mapping: Unveiling Patterns and Trends

The subsequent sections delve into the diverse maps generated by VOSviewer, initiating with a meticulous examination of keyword co-occurrence and progressing to a comprehensive bibliographic coupling of countries and authors.

3.3.1. Keyword Co-Occurrence Analysis

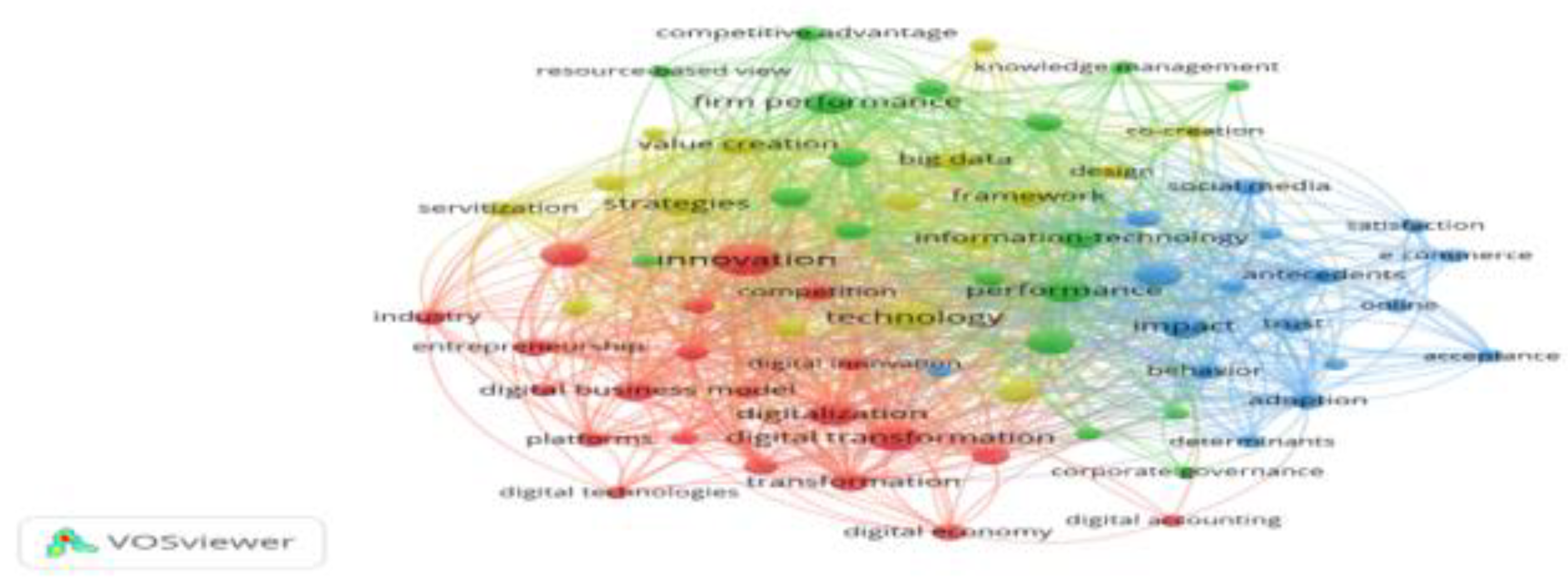

A powerful method for identifying patterns and emerging research domains in a particular field is co-occurrence analysis. This technique involves examining the concurrent occurrences of two terms in text, thereby revealing the conceptual and thematic structure of a scientific topic. An essential element of this method is co-word analysis, which investigates the occurrences of keywords in titles, abstracts, and keywords, providing insights into their prevalence in scholarly articles. Employing VOSviewer for keyword co-occurrence analysis in this study yielded a network representation that illustrates the strength and quantity of connections. The size of each circle, linked to an item, signifies the relevance of associated terms. Cluster analysis revealed established areas in auditing, digital accounting, and digital business research, offering insights into potential future trends. Figure 4 visually depicts keyword co-occurrences and network relationships within the semantic structure of Accounting and Corporate Sustainability. This visualization tool aids in assessing keyword frequency and the robustness of relationships. Circles represent keyword clusters, and connecting lines signify relationships, with shorter distances indicating stronger connections.

Cluster analysis, rooted in the co-occurrence of phrases, unveiled four principal clusters indicative of noteworthy research trends. These clusters were categorized based on their quantity and strength, resulting in the identification of four distinct clusters, encompassing 1517 links with a total link strength of 4255.

The red cluster comprises key terms like "digital transformation," "digital business model," and "digital accounting," signifying their high frequency and significance. This cluster explores digital transformation broadly, emphasizing the impact of the digital economy on professions like digital accounting and auditing during the technological revolution. It is closely connected to the Yellow cluster, collectively focusing on studies that delve into future services enabled by modern technologies in the context of business digitization, including the examination of big data and its analytical strategies.

Furthermore, the blue cluster investigates the impact of social media on e-commerce and customer behavior, with a particular emphasis on the post-COVID-19 era, during which digital strategies gained global prominence. Figure 4 depicts the emergence of the green cluster at the top of the map, featuring keywords such as "firm performance," "management," "information technology," and "digital business transformation." This cluster primarily explores the relationship between information technology and corporate management, aiming to enhance performance within the framework of business digital transformation.

3.3.2. Investigating Trends in Auditing and Digital Accounting Research within the Digital Business Environment

The researchers employed WoS data and the VOSviewer program (accessible at www.vosviewer.com; van Eck and Waltman 2010) to create four co-occurrence networks. These networks were established using all keywords identified in the titles and abstracts of papers, as well as in citation contexts associated with auditing and digital accounting research in the digital business environment. The text-mining feature of VOSviewer was utilized to extract keywords from titles, abstracts, and citation contexts, producing a comprehensive map of keyword co-occurrence. Keywords that appeared together in titles, abstracts, or citation contexts were considered to co-occur, and the proximity between keywords indicated their level of similarity in terms of co-occurrence. Terms with a higher co-occurrence frequency were more likely to be found together. Additionally, VOSviewer provided a clustering tool that grouped keywords based on their co-occurrence patterns (Van Eck and Waltman 2017).

Table 1.

Network parameters with the highest reliance on the study's keywords.

| Keywords | Links | Total Links Strength | Occurrences | Cluster Color |

|---|---|---|---|---|

| Innovation | 66 | 524 | 122 | Red |

| Technology | 64 | 372 | 78 | Yellow |

| Digital Transformation | 60 | 263 | 69 | Red |

| Firm Performance | 58 | 259 | 61 | Green |

| Digitalization | 63 | 225 | 59 | Red |

| Strategies | 60 | 277 | 58 | Yellow |

| Management | 62 | 240 | 57 | Green |

| Model | 60 | 226 | 57 | Blue |

| Information-Technology | 45 | 180 | 42 | Green |

| Digital Business | 47 | 132 | 41 | Yellow |

Table 7 displays network parameters with the highest reliance on the study's keywords. To pinpoint the distinctive theme of each cluster, the study conducted an in-depth analysis of the keywords within each cluster. This involved scrutinizing the specific topics represented by the keywords in each cluster.

Cluster 1 (Red) emerges as highly significant and deserving of comprehensive investigation in the future. It prominently occupies the left side and bottom of the map, extending from the central point. Notably, it establishes direct connections with other clusters, including the green and yellow clusters. These findings emphasize the imperative for comprehensive research on this specific cluster, aiming to attain a more profound understanding of its implications and repercussions. In the digital economy, characterized by the widespread integration of digital technologies, traditional business models are being rapidly supplanted by more agile and tech-savvy approaches (Sibanda et al., 2020). Digital accounting, as an integral component of this transformation, witnesses a fundamental evolution. Automation, artificial intelligence, and advanced data analytics are becoming pivotal elements in financial processes. Routine transactions , such as data entry and reconciliation, are increasingly automated, freeing up professionals to focus on higher-value strategic activities. Real-time data access and analysis enable more accurate and timely financial reporting, enhancing decision-making capabilities for businesses operating in the digital sphere (Ahmed et al., 2022).

Concurrently, the realm of auditing is undergoing a significant transformation. The rise of digital systems necessitates auditors to develop expertise in assessing complex technological infrastructures and data security measures (Otia, & Bracci, 2022). Auditing methodologies are evolving to assess not only financial statements but also the resilience of digital systems and the integrity of data flows. The integration of machine learning algorithms and predictive analytics into auditing processes improves the detection of anomalies and potential risks. (Roszkowska, 2021). However, these advancements also bring forth challenges. Professionals in digital accounting and auditing must grapple with issues related to data privacy, cybersecurity, and the ethical use of emerging technologies. The need for continuous learning and upskilling becomes imperative as these fields evolve at an unprecedented pace (Busulwa, & Evans, 2021).

Cluster 2 (Yellow) is a pivotal area for future in-depth exploration. The digitization of business is driving a wave of future services powered by modern technologies, ushering in a transformative era with far-reaching implications (Lang, & Lang, 2021). At the core of this evolution is the substantial impact of big data and its analytical strategies, shaping the course of business operations (Grover et al., 2018). A significant consequence is the enhanced capability for informed decision-making. As businesses undergo heightened digitization, they generate extensive data, and big data analytics allows organizations to extract meaningful insights. Consequently, this facilitates a nuanced understanding of customer behavior, market trends, and operational efficiency, empowering businesses to make accurate and forward-thinking strategic decisions. (Awan et al., 2021).

Future services in the realm of business digitization emphasize personalized customer experiences. Big data analytics enables businesses to customize services based on individual preferences, purchasing history, and behavior, enhancing satisfaction and fostering loyalty in the competitive digital landscape (Sestino et al., 2020). However, these advancements prompt considerations about data privacy and security. The collection and use of vast datasets require robust measures to protect sensitive information. Balancing the benefits of big data analytics with ensuring data protection poses a critical challenge in the pursuit of future services in business digitization (Ogbuke et al., 2022). The consequences of this shift extend beyond individual businesses, impacting broader economic landscapes. Industries adept at harnessing big data analytics gain a competitive advantage, contributing to economic growth and innovation. Conversely, businesses slow to adopt these technologies may face a disadvantage in an increasingly digitized global marketplace (Morabito, 2015).

Cluster 3 (blue) highlighted in blue on the map, comprises a complex ensemble of ideas that merit further investigation. The synergy of social media, e-commerce, and evolving consumer behavior has become a pivotal force, accentuated by the profound changes catalyzed by the COVID-19 crisis. This pandemic not only expedited the adoption of digital strategies but also fundamentally transformed the e-commerce landscape and consumer interactions, notably through the amplified role of social media (Nanda et al., 2021; Al-Qudah et al., 2022).

The immediate consequence of the crisis was a surge in online activities, driven by lockdowns and social distancing measures, compelling businesses and consumers to shift towards digital platforms (Amankwah-Amoah et al., 2021). Social media platforms emerged as central hubs for e-commerce transactions, offering innovative avenues for businesses to engage with customers. The traditional customer journey underwent a significant transformation, with social media serving as a primary touchpoint for discovery, research, and purchasing decisions (Varadarajan et al., 2022).

The implications are diverse. Firstly, social media functions as a potent tool for brand promotion and product visibility, allowing businesses to strategically reach a global audience and foster brand awareness. Secondly, The interactive character of social media facilitates instantaneous communication, empowering businesses to promptly respond to customer concerns and customize offerings based on immediate feedback. (Dwivedi et al., 2021). However, this shift also presents challenges. The vast reach of social media necessitates effective navigation of online reputation management and customer feedback complexities. Negative reviews or viral incidents can substantially impact a brand's image. Additionally, the data-driven nature of e-commerce on social media raises privacy concerns, demanding a delicate balance between personalized marketing and respecting customer privacy (Rauschnabel et al., 2022).

Cluster 4 (green) emerges as significant and deserving of comprehensive investigation in the future. The relationship between information technology and corporate management has profound implications for business performance, particularly within the framework of digital transformation. As organizations increasingly integrate advanced technologies into their operations, the impact on corporate management becomes a critical determinant of overall success (Hanelt et al., 2021).

One significant implication is the potential for streamlined operations and increased efficiency. Information technology provides tools and systems that automate routine tasks, facilitate data analysis, and enhance communication within the organizational structure (Al Hbabi et al., 2012). This automation empowers corporate management to allocate resources more strategically, emphasizing high-value tasks and strategic decision-making (Dewett & Jones, 2001). Consequently, operational efficiency frequently improves, costs diminish, and the business environment becomes more agile. Additionally, integrating information technology into corporate management practices facilitates data-driven decision-making (Brynjolfsson & Hitt, 2000). Management teams can gain comprehensive insights into various facets of the business utilizing sophisticated analytics tools and real-time reporting capabilities (Saggi & Jain, 2018). This data-driven approach enables more informed and timely decision-making, fostering proactive rather than reactive management. As a result, businesses can swiftly adapt to evolving market conditions, customer preferences, and industry trends (Tseng et al., 2022).

However, the growing dependence on information technology in corporate management presents certain challenges. The introduction of new technologies often requires substantial investment, both financially and in employee training. Additionally, there are concerns about data security, privacy, and the potential for technological disruptions. Managing these challenges effectively becomes crucial for organizations aiming to optimize the advantages of digital transformation (Saarikko et al., 2020).

3.3.3. Bibliographic Coupling of Authors

The concept of author bibliographic coupling expands upon the idea of bibliographic coupling, which pertains to the scenario in which two authors cite the same articles in their respective published papers. Author bibliographic coupling operates on the premise that the more references shared by two authors in their collective body of work, the greater the similarity in their research. The effectiveness of utilizing document bibliographic coupling for mining research frontiers and creating science maps has been thoroughly investigated.

In Figure 5, preeminent authors are ranked based on the number of papers they have cited. Specifically, Erik Brynjolfsson emerges as the most frequently cited author in the field of auditing and digital accounting research within the digital business environment during the study period from 2010 to 2023, with 7 documents and an impressive 3306 citations to his name. Following closely is Theo Lynn, with 9 documents and 60 citations to his credit.

3.3.4. Bibliographic Coupling of Nations

Figure 6 illustrates the collaborative network among various countries and territories within this specific context. The data is generated by implementing a threshold that necessitates at least one document for inclusion, revealing up to sixty of the most notable bibliographic connections. Each element is designated and typically depicted as a default circle. The size of both the label and circle reflects the element's significance, with the largest label and circle signifying the most relevant element. Lines connecting these elements denote their connections, and the distance between them indicates the degree of relatedness among countries in this specific research field. A notable advantage of this map is its capacity to emphasize countries or territories with similar characteristics, often resulting in the clustering of countries from the same continent.

Figure 6.

As depicted in Figure 6, the largest circle in the visualization represents the United States, closely linked to other nations like Singapore and Canada. The USA has 124 publications with 9805 citations, and Germany, in comparison, has 81 publications with 2259 citations.

4. Conclusion

This bibliometric analysis has yielded valuable insights into the progression of research in auditing and digital accounting within the dynamic context of the digital business environment. By systematically examining publication patterns, citation dynamics, and collaborative efforts among authors, journals, and countries, the study has uncovered significant trends and themes shaping these research domains.

4.1. Theoretical Consequences

The findings highlight the transformative nature of auditing and digital accounting in response to the rapid digitization of business operations. The emergence of key clusters, such as the red cluster focusing on digital transformation and the green cluster exploring the relationship between information technology and corporate management, indicates the evolving dimensions of research in these fields. Theoretical implications extend to understanding the profound influence of the digital economy on traditional financial practices and the need for innovative methodologies to ensure the reliability of financial information in the digital age.

4.2. Practical Implications

Practically, the study offers actionable insights for researchers, policymakers, and industry practitioners. The identification of influential authors, journals, and countries provides a roadmap for collaboration and knowledge dissemination. The clusters elucidate emerging research trends, guiding future investigations and resource allocation. Moreover, the emphasis on the impact of social media on e-commerce and customer behavior, as seen in the blue cluster, suggests practical considerations for businesses navigating the post-COVID-19 digital landscape.

4.3. Future Directions

The research has set the stage for future inquiries, prompting exploration into areas such as the integration of digital technologies in auditing practices, the implications of social media on business strategies, and the ongoing evolution of digital accounting in response to technological advancements. As the digital business environment continues to evolve, there is a need for ongoing research to adapt methodologies and address emerging challenges.

References

- 1. Aboelmaged, M., Alhashmi, S. M., Hashem, G., Battour, M., Ahmad, I., & Ali, I. (2023). Unveiling the path to sustainability: two decades of knowledge management in sustainable supply chain – a scientometric analysis and visualization journey. Benchmarking: Int. J. 2023. 2023. [CrossRef]

- Abu Huson, Y.; Sierra-García, L.; Garcia-Benau, M.A. A bibliometric review of information technology, artificial intelligence, and blockchain on auditing. Total. Qual. Manag. Bus. Excel. 2023, 35, 91–113,. [CrossRef]

- Ahmad, T.; Haroon, H.; Ornos, E.D.B.; Malibary, H.; Hussain, A.; Baig, M.; Santali, E.Y.; Alestad, J.H.; Muzaheed, M.; Rabaan, A.A.; et al. Bibliometric analysis and network visualization mapping of global research in Q fever vaccine. F1000Research 2022, 11, 364,. [CrossRef]

- Ahmed, A.S.A.; Albaz, M.M.; Metwaly, A.Z. The Role of Artificial Intelligence Technologies in Improving the Performance of the Management Accountant considering the Egyptian State’s Trend Toward Digital Transformation. World Res. Bus. Adm. J. 2022, 2, 167–182. [CrossRef]

- al Hbabi, K.N.; Alomari, Z.S. The Impact of Knowledge Management Processes on Organizational Innovation. Int. J. Acad. Res. Bus. Soc. Sci. 2020, 10, 949–967,. [CrossRef]

- Allioui, H.; Mourdi, Y. Exploring the Full Potentials of IoT for Better Financial Growth and Stability: A Comprehensive Survey. Sensors 2023, 23, 8015,. [CrossRef]

- Al-Qudah, L.A.; Qudah, H.A.; Abu Hamour, A.M.; Abu Huson, Y.; Al Qudah, M.Z. The effects of COVID-19 on conditional accounting conservatism in developing countries: evidence from Jordan. Cogent Bus. Manag. 2022, 9, 2152156. [CrossRef]

- Amankwah-Amoah, J.; Khan, Z.; Wood, G.; Knight, G. COVID-19 and digitalization: The great acceleration. J. Bus. Res. 2021, 136, 602–611,. [CrossRef]

- Awan, U.; Shamim, S.; Khan, Z.; Zia, N.U.; Shariq, S.M.; Khan, M.N. Big data analytics capability and decision-making: The role of data-driven insight on circular economy performance. Technol. Forecast. Soc. Chang. 2021, 168, 120766,. [CrossRef]

- Bhimani, A.; Willcocks, L. 10. Bhimani, A.; Willcocks, L. Digitisation,‘Big Data’and the transformation of accounting information. Accounting and business research 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Birkle, C.; Pendlebury, D.A.; Schnell, J.; Adams, J. Web of Science as a data source for research on scientific and scholarly activity. Quant. Sci. Stud. 2020, 1, 363–376,. [CrossRef]

- Brunetti, F.; Matt, D.T.; Bonfanti, A.; De Longhi, A.; Pedrini, G.; Orzes, G. Digital transformation challenges: strategies emerging from a multi-stakeholder approach. TQM J. 2020, 32, 697–724,. [CrossRef]

- Brynjolfsson, E.; Hitt, L.M. Beyond Computation: Information Technology, Organizational Transformation and Business Performance. J. Econ. Perspect. 2000, 14, 23–48,. [CrossRef]

- Busulwa, R.; Evans, N. Digital transformation in accounting; Routledge.

- Chawla, R.N.; Goyal, P. Emerging trends in digital transformation: a bibliometric analysis. Benchmarking: Int. J. 2021, 29, 1069–1112,. [CrossRef]

- De Bellis, N. Bibliometrics and citation analysis: from the science citation index to cybermetrics; scarecrow press.

- Dewett, T.; Jones, G.R. The role of information technology in the organization: a review, model, and assessment. Journal of management 2001, 27, 313–346. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Ismagilova, E.; Hughes, D.L.; Carlson, J.; Filieri, R.; Jacobson, J.; Jain, V.; Karjaluoto, H.; Kefi, H.; Krishen, A.S.; et al. Setting the future of digital and social media marketing research: Perspectives and research propositions. Int. J. Inf. Manag. 2021, 59, 102168,. [CrossRef]

- Gahegan, M. Four barriers to the development of effective exploratory visualisation tools for the geosciences. Int. J. Geogr. Inf. Sci. 1999, 13, 289–309,. [CrossRef]

- Gonçalves, M.J.A.; da Silva, A.C.F.; Ferreira, C.G. The Future of Accounting: How Will Digital Transformation Impact the Sector? Informatics 2022, 9, 19,. [CrossRef]

- Goyal, K.; Kumar, S. Financial literacy: A systematic review and bibliometric analysis. Int. J. Consum. Stud. 2021, 45, 80–105,. [CrossRef]

- Grover, V.; Chiang, R.H.; Liang, T.P.; Zhang, D. Creating Strategic Business Value from Big Data Analytics: A Research Framework. J. Manag. Inf. Syst. 2018, 35, 388–423,. [CrossRef]

- Gusenbauer, M. Search where you will find most: Comparing the disciplinary coverage of 56 bibliographic databases. Scientometrics 2022, 127, 2683–2745,. [CrossRef]

- Hanelt, A.; Bohnsack, R.; Marz, D.; Marante, C.A. A Systematic review of the literature on digital transformation: insights and implications for strategy and organizational change. J. Manag. Stud. 2021, 58, 1159–1197,. [CrossRef]

- Hassan, N.R.; Loebbecke, C. Engaging scientometrics in information systems. J. Inf. Technol. 2017, 32, 85–109,. [CrossRef]

- Kastrin, A.; Hristovski, D. Scientometric analysis and knowledge mapping of literature-based discovery (1986–2020). Scientometrics 2021, 126, 1415–1451,. [CrossRef]

- Huson, Y.A.; Almousa, M.; Alqudah, M. Exploring Corporate Tax Avoidance: Effects on Comprehensive Budget Income–a Practical Analys. Effects on Comprehensive Budget Income–a Practical Analysis: Alqudah, M., 2024. Exploring Corporate Tax Avoidance, 2024. [Google Scholar]

- Kaur, V. Neurostrategy: A scientometric analysis of marriage between neuroscience and strategic management. J. Bus. Res. 2024, 170,. [CrossRef]

- Kehinde, T.; Chan, F.T.; Chung, S. Scientometric review and analysis of recent approaches to stock market forecasting: Two decades survey. Expert Syst. Appl. 2023, 213,. [CrossRef]

- Kokina, J.; Blanchette, S. Early evidence of digital labor in accounting: Innovation with Robotic Process Automation. Int. J. Account. Inf. Syst. 2019, 35, 100431,. [CrossRef]

- Lang, V.; Lang, V. Lang, V.; Lang, V. Digitalization and digital transformation. Digital Fluency: Understanding the Basics of Artificial Intelligence, Blockchain Technology, Quantum Computing, and Their Applications for Digital Transformation. 2021, 1-50.

- Liu, L.; Jones, B.F.; Uzzi, B.; Wang, D. Data, measurement and empirical methods in the science of science. Nat. Hum. Behav. 2023, 7, 1046–1058,. [CrossRef]

- Lynn, T.; Rosati, P.; Lejeune, A.; Emeakaroha, V. Lynn, T.; Rosati, P.; Lejeune, A.; Emeakaroha, V. (2017, December). A preliminary review of enterprise serverless cloud computing (function-as-a-service) platforms. In 2017 IEEE International Conference on Cloud Computing Technology and Science (CloudCom) (pp. 162-169). IEEE.

- Manita, R.; Elommal, N.; Baudier, P.; Hikkerova, L. The digital transformation of external audit and its impact on corporate governance. Technol. Forecast. Soc. Chang. 2019, 150, 119751,. [CrossRef]

- Moffitt, K.C.; Rozario, A.M.; Vasarhelyi, M.A. Moffitt, K.C.; Rozario, A.M.; Vasarhelyi, M.A. Robotic process automation for auditing. Journal of emerging technologies in accounting 2018, 15, 1–10. [Google Scholar] [CrossRef]

- Morabito, V. Big data and analytics. Strategic and organisational impacts. 2015. [Google Scholar]

- Mosteanu, N.R.; Faccia, A. Digital systems and new challenges of financial management–FinTech, XBRL, blockchain and cryptocurrencies. Quality–Access to Success 2020, 21, 159–166. [Google Scholar]

- Mosweu, O. A framework to authenticate records in a government accounting system in Botswana to support the auditing process; Pretoria: University of South Africa, 2018. [Google Scholar]

- Mukherjee, D.; Kumar, S.; Mukherjee, D.; Goyal, K. Mapping five decades of international business and management research on India: A bibliometric analysis and future directions. Journal of Business Research 2022, 145, 864–891. [Google Scholar] [CrossRef]

- Nanda, A.; Xu, Y.; Zhang, F. How would the COVID-19 pandemic reshape retail real estate and high streets through acceleration of E-commerce and digitalization? J. Urban Manag. 2021, 10, 110–124,. [CrossRef]

- Ogbuke, N.J.; Yusuf, Y.Y.; Dharma, K.; Mercangoz, B.A. Big data supply chain analytics: ethical, privacy and security challenges posed to business, industries and society. Prod. Plan. Control. 2022, 33, 123–137,. [CrossRef]

- Otia, J.E; The SAI's perspective: Bracci, E. Digital transformation and the public sector auditing.

- Pizzi, S.; Venturelli, A.; Variale, M.; Macario, G.P. Assessing the impacts of digital transformation on internal auditing: A bibliometric analysis. Technol. Soc. 2021, 67, 101738,. [CrossRef]

- Rauschnabel, P.A.; Babin, B.J.; Dieck, M.C.T.; Krey, N.; Jung, T. What is augmented reality marketing? Its definition, complexity, and future. J. Bus. Res. 2022, 142, 1140–1150,. [CrossRef]

- Rojas-Lamorena,.J.; Del Barrio-García, S.; Alcántara-Pilar, J.M. A review of three decades of academic research on brand equity: A bibliometric approach using co-word analysis and bibliographic coupling. J. Bus. Res. 2022, 139, 1067–1083,. [CrossRef]

- Roszkowska, P. Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. J. Account. Organ. Chang. 2021, 17, 164–196,. [CrossRef]

- Saarikko, T.; Westergren, U.H.; Blomquist, T. Digital transformation: Five recommendations for the digitally conscious firm. Bus. Horizons 2020, 63, 825–839,. [CrossRef]

- Saggi, M.K.; Jain, S. A survey towards an integration of big data analytics to big insights for value-creation. Inf. Process. Manag. 2018, 54, 758–790,. [CrossRef]

- Sahut, J.-M.; Iandoli, L.; Teulon, F. The age of digital entrepreneurship. Small Bus. Econ. 2021, 56, 1159–1169. [Google Scholar] [CrossRef]

- Sestino, A.; Prete, M.I.; Piper, L.; Guido, G. Internet of Things and Big Data as enablers for business digitalization strategies. Technovation 2020, 98, 102173–102173. [Google Scholar] [CrossRef]

- Sibanda, W.; Ndiweni, E.; Boulkeroua, M.; Echchabi, A.; Ndlovu, T. Digital technology disruption on bank business models. International Journal of Business Performance Management 2020, 21, 184–213. [Google Scholar] [CrossRef]

- Singh, N.; Lai, K.; Vejvar, M.; Cheng, T.C.E. Data-driven auditing: A predictive modeling approach to fraud detection and classification. J. Corp. Account. Finance 2019, 30, 64–82,. [CrossRef]

- Sugimoto, C.R.; Larivière, V. Measuring research: What everyone needs to know. Oxford University Press. 2018. [Google Scholar]

- Sustacha, I.; Baños-Pino, J.F.; del Valle, E. Research trends in technology in the context of smart destinations: a bibliometric analysis and network visualization. Cuadernos de Gestión 2022, 22, 161–173. [Google Scholar] [CrossRef]

- Tseng, M.-L.; Bui, T.-D.; Lim, M.K.; Fujii, M.; Mishra, U. Assessing data-driven sustainable supply chain management indicators for the textile industry under industrial disruption and ambidexterity. Int. J. Prod. Econ. 2022, 245. [Google Scholar] [CrossRef]

- Turban, E.; Pollard, C.; Wood, G. Information Technology for Management: Driving Digital Transformation to Increase Local and Global Performance, Growth and Sustainability; John Wiley & Sons, 2021. [Google Scholar]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538,. [CrossRef]

- van Eck, N.J.; Waltman, L. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 2017, 111, 1053–1070,. [CrossRef]

- Varadarajan, R.; Welden, R.B.; Arunachalam, S.; Haenlein, M.; Gupta, S. Digital product innovations for the greater good and digital marketing innovations in communications and channels: Evolution, emerging issues, and future research directions. Int. J. Res. Mark. 2022, 39, 482–501,. [CrossRef]

- Zhu, Z.; Zhao, M.; Wu, X.; Shi, S.; Leung, W.K. The dualistic view of challenge-hindrance technostress in accounting information systems: Technological antecedents and coping responses. Int. J. Inf. Manag. 2023, 73,. [CrossRef]

- Zou, X.; Yue, W.L.; Le Vu, H. Visualization and analysis of mapping knowledge domain of road safety studies. Accid. Anal. Prev. 2018, 118, 131–145,. [CrossRef] [PubMed]

- Abu Orabi, T.; Al-Hyari, H.S.A.M.; Almomani, H.M.; Ababne, A.; Abu Huson, Y.; Ahmed, E.; Albanna, H. A bibliometric review of job satisfaction and organizational commitment in businesses area literatures. Hum. Syst. Manag. 2023, Preprint, 1–23,. [CrossRef]

- Huson YA, A.; Sierra-García, L.; Garcia-Benau, M.A.; Aljawarneh, N.M. EMPIRICAL INVESTIGATION INTO THE INTEGRATION OF CLOUD-BASED ARTIFICIAL INTELLIGENCE IN AUDITING. PressAcademia Procedia 2024, 18, 113–114. [Google Scholar]

- Albalawee, N.; Huson, Y.; Budair, Q.; Alqmool, T.; Arasheedi, N. Connecting legal compliance and financial integrity: A bibliometric survey of accounting practices in the corporate supply chain. Uncertain Supply Chain Manag. 2024, 12, 893–906,. [CrossRef]

Figure 1.

Publication Years from 2010 to 2023.

Figure 2.

The Most Contributed Journals.

Figure 3.

The Most Contributed publishers.

Figure 4.

Keyword Co-occurrence Analysis.

Figure 5.

Bibliographic coupling of authors.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.