Submitted:

22 January 2024

Posted:

23 January 2024

You are already at the latest version

Abstract

Different severe energy crises episodes occurred in the world in the last five decades. Energy crises lead to deterioration of international relations, economic crises, changes in monetary systems and social problems in countries. This paper aims to show the essential determinants of energy crises by developing a binary logit model which estimates the predictive ability of thirteen indicators in a sample that covers the period from January 1973 to December 2022. The empirical results show that the energy crises are mainly due to energy supply-demand imbalances (petroleum stocks, fossil energy production-consumption imbalance and changes in energy imports by country groups), energy investments (oil and natural gas drilling activities), economic and financial disruptions (inflation, dollar index, index of global real economic activity) and geopolitical risks. Additionally, the model is capable of accurately predicting the world energy crisis event months with 99% probability.

Keywords:

energy crisis

; early warning systems

; energy crisis definition

; logistic regression

1. Introduction

Promete’s stealing fire from the god Zeus and giving it to humans marked the beginning of mankind’s dependence on energy. Again, the industrial revolution began in 1763 when James Watt stole knowledge from the gods and made coal-powered steam engines available to humanity. With the industrial revolution, energy has become an indispensable element of life. With the industrial revolution, technology development, increasing urbanization, population growth and growing world trade have further increased the need for fossil energy. Increases in energy demand has accelerated the search for utilization of energy sources other than coal. In the early 20th century, having discovered that oil was a more efficient source of energy than coal, major western countries began converting coal-fired steam engines to internal combustion oil engines. Owning oil resources has now become the most important strategy of all western developed countries. This strategy led the world into the First and Second World Wars. After these wars, the countries of the world accelerated their technological search for the use of alternative energy sources in order to get rid of the huge costs (wars) of trying to have fossil-based energy. As a result of this technological search, the use of hydraulic power plants, atomic power plants and renewable energy sources has increased. However, the dangers of nuclear power plants and the disadvantages of renewable energy, such as intraday and seasonal production fluctuations, have not reduced the importance of fossil resources. According to the International Energy Agency (IEA), since the beginning of the Industrial Revolution in the 18th century, global fossil fuel use has continued to expand its share of the global economy, along with rising GDP. Fossil fuels also have the largest share in world trade. The share of fossil fuels in global energy use has remained stubbornly high at around 80% for decades. More than 50% of the world’s proven oil reserves and more than 30% of the world’s natural gas reserves are located in Middle Eastern countries [1]. The intense demand for energy resources and the transportation of energy from energy resource-rich countries to energy-poor countries, and any disruption in the supply of energy resources (Supply restrictions, speculation, war, natural disasters etc.) have led the world to face energy crises. Energy-poor countries have developed energy security strategies against possible energy crises. However, with the scarcity of energy resources and increasing energy demand, disruptions in energy supply (such as the Russia-Ukraine war in 2022) can throw countries’ energy security strategies into the trash bin.

Energy, which is seen as vital for world economies, reminds the human being how important it is with the crises that arise as a result of supply-demand mismatch. These energy crises create many negative economic, political and social consequences. The energy crises that emerged especially in the 1970s led to the elimination of the “Bretton Woods System”, also known as the “dollar-gold system” in world trade after the Second World War, and its replacement by the “petrodollar” system. In addition, China’s massive energy demand, which accompanied the 2008 Global Financial Crisis (GFC), led to the 2008 energy crisis. After the 2008 energy crisis, China started to use “petroyuan” contracts in energy trade. These new contracts are another important impact of energy crises on international trade [2]. As a result of energy crises, energy prices increase dramatically. Thus, increased energy expenditures increase production costs, which in turn lead to high inflation in economies. Rising inflation reduces consumption expenditures, leading to declines in GDP and high current account deficits in energy-poor countries. [3] (p. 204). In addition, rising energy prices damage the balance of payments in energy-poor countries, disrupting their external economic balances and triggering economic crises [4,5]. More recently, Alam et al. [6], and Prohorovs [7], argue that the energy crisis resulting from the Russia-Ukraine war has raised inflation, increased price volatility in the commodity market, caused welfare losses and worsened future economic expectations in the world.

Another important development in the energy market is the phenomenon of “financialization of the energy market”, which increased in the early 2000s. Essentially, the financialisation of the energy market implies to the increased participations of insurance companies, hedge funds and pension funds, among other financial actors, in the commodity futures markets. Impressively, in their annual World Oil Outlook report, Organization of Petroleum Exporting Countries (OPEC) made one of the most exaggerated estimates of the size of OTC (over the counter) markets, stating that speculator activity on New York Mercantile Exchange (NYMEX) rose to record levels in the first quarter of 2011. West Texas Intermediate (WTI) on NYMEX exceeded an unprecedented level of 1.5 million contracts, which is 18 times higher than the amount of physical oil traded daily [8]. It is now accepted and internalized by the market that the increases in oil prices include significant elements of financial speculation and financialization of the oil market [9]. According to Frankel and Rose [10], and Redrado et al. [11], increased oil prices have amplified the financialisation of the oil markets and, in turn, speculative trade activity in the oil market.

As mentioned above, large increases in energy prices are seen as an extremely important phenomenon due to the negative consequences they have on economies. For this reason, researchers have produced numerous studies on the economic effects of energy price volatilities, the macroeconomic consequences of energy shocks and the forecasting of energy prices (or energy price determinants). They saw energy crises as unpredictable or as a natural process of the economic cycle. However, they are also aware of the importance of anticipating and taking precautions in advance, as the consequences of energy crises can cause unemployment, poverty and social unrest around the world. Due to this importance, we have tried to make an original contribution to the literature with the study titled “Early Warning Systems for World Energy Crises”. Early Warning Systems (EWS) consist of three main components: crisis definition, analysis method and explanatory variables. In addition, the study makes a quantitative “energy crisis definition” and provides another original contribution to the literature by creating a subjective evaluation systematic for energy crises. As an EWS analysis method, Logistic Regression (LR) analysis, which is frequently used especially in the EWS modeling of financial crises, was used. The last component of the EWS, the explanatory variables, is constructed by taking into account the energy price determinants in the existing literature. The EWS model for energy crises identified 12 different monthly energy crisis events in the 600-month period from January 1973 to December 2022. Moreover, the model predicted each case (crisis or no crisis) of the 600-month period with 99% accuracy.

The rest of the paper is arranged as follows Section 2 reviews studies close to the topic of energy crises. In Section 3, the parameters of the EWS model are established within the scope of energy crisis definition, analysis method and explanatory variables. Assumptions and limitations of the study are also stated. Section 4 provides the results of the analysis of the EWS model of energy crises and the statistical test results of the model. Section 5 presents the results of the analysis, evaluations on the model’s prediction of energy crises and suggestions for future studies in relation to this study.

2. Literature Review

In this section, literature studies that can be utilized in the construction of the energy crisis model are reviewed. These studies are analyzed in three different groups. The first group of studies focus on the causes of energy price shocks and their negative economic consequences such as growth, unemployment and inflation, the second group of studies focus on the causes and macroeconomic effects of energy price fluctuations (volatility), and the last group of studies focus on energy price determinants for forecasting energy prices.

Since Hamilton’s [12], seminal work on the macroeconomic implications of oil price shocks, there have been many similar studies in the literature. It has been firmly established that oil shocks are closely related to a range of macroeconomic and financial variables, including employment, aggregate output, inflation, stock returns and exchange rates [13,14,15,16,17,18]. Oil shocks hit economies both on the supply and demand sides as well as through the trade channel [19,20,21,22]. On the supply side, oil shocks lead to input scarcity, which increases production costs and reduces output and productivity. On the demand side, it leads to higher inflation rates and lower real disposable income, leading to lower demand [23]. The trade channel effect of oil shocks is that oil importing countries allocate more resources from wealth accumulation and face deteriorating trade balances. This leads to appreciation in the exchange rates of oil exporting countries and depreciation in the exchange rates of oil importing countries [24,25,26].

In the literature, the volatility of energy prices is measured by the standard deviation of energy price data in the relevant period. Studies generally include assessments of the economic consequences of sudden fluctuations in oil prices and uncertainties in the oil market.

Elder and Serletis [27], show that oil price volatility has a negative impact on total US production, investment and consumption. Moreover, Henriques and Sadorsky [28], argue that oil price volatility has an impact on the strategic investment decisions of US firms. They conclude that increased oil price volatility affects the cost of oil inputs and creates uncertainty not only for investment decisions but also for firm valuation and firm profitability. Similarly, Diaz et al. [29], provide evidence that high oil price volatility negatively affects stock market returns in G7 economies. Finally, Bouri et al. [30], report that oil price volatility has a significant impact on the sovereign credit risk of BRICS countries.

In relation to the investigation of the determinants of oil price volatility, Van Robays [31], argues in his study that macroeconomic uncertainty triggered by economic recessions and financial crises leads to higher oil price uncertainty. More specifically, Van Robays [31], argues that during periods of heightened macroeconomic uncertainty, oil price volatility is driven by fundamental factors underpinning oil supply and demand shocks. In this case, it is largely associated with lags in the production and consumption decisions of market actors. He explains that the main reason for this is that increased macroeconomic uncertainty reduces the price elasticity of oil supply and oil demand and thus increases oil price volatility. Another interesting aspect of oil price volatility and its determinants is the analysis of speculation in the oil market and how speculation can potentially lead to high volatility. Van Robays [31], argues that changes in the price elasticity of oil supply and oil demand should not be attributed to changes in oil inventory holding levels and that speculation should not be seen as a factor that actually contributes to changes in the oil price.

Using data on global oil stocks to approximate changes in speculative oil demand, authors such as Beidas-Strom and Pescatori [32] argue that there is a link between the increase in oil inventories and the increase in the oil price. They conclude that financial speculation triggers short-term oil price fluctuations between 3 and 22 percent. Moreover, Robe and Wallen [33], investigate whether physical energy market fundamentals, financial and macroeconomic conditions lead to oil price volatility over one to six months. Robe and Wallen [33], use the term structure of oil option price volatility and report that the Chicago Board Options Exchange Volatility Index (VIX) significantly affects oil volatility, but both other macroeconomic variables and speculative activity do not appear to have a significant effect.

In parallel, Caldara et al. [34], examine the causes of oil price volatility. They conclude that oil supply shocks and global demand shocks are important in driving oil price fluctuations. Specifically, they report that oil supply shocks and global demand shocks contribute to explain 50 percent and 35 percent of oil price fluctuations, respectively.

The general consensus from this part of the literature is that oil price volatility estimating has become increasingly important in recent years mainly due to the financialization of oil markets and the fact that oil is now viewed as a financial asset by market participants such as hedge funds, insurance companies and pension funds [35].

Petroleum (oil) price forecasting literature, there are two base groups of estimation methods: qualitative methods and quantitative. Qualitative methods forecast impact of infrequent cases such as natural disasters and wars on petroleum prices; these approaches recently gained more popularity among petroleum price estimating literature [36]. Even so, between various types of qualitative estimation methods there are no many of them that are implemented to estimate petroleum prices, such as Delphi method [37], belief networks [38], fuzzy logic and expert systems [39], and web text mining method [40,41]. On the other side, Quantitative approaches show numerical and quantitative variables that effect on petroleum prices; include two groups of techniques: non-standard methods and econometrics methods. The main non-standard approaches which are the most frequently implemented in terms of petroleum price estimating are artificial neural networks [42,43] and support vector machines [44,45]. On other hand, among them, econometrics models are grouped into the three classes of models: time series models [46,47,48], financial models [49,50,51] and structural models. The structural models that are utilized to forecast petroleum prices based on five different models: OPEC behavior models [52,53,54], inventory models [55,56], combination of OPEC behavior with inventory models [57,58,59], supply and demand models [60,61,62,63,64,65,66,67] and non-oil models (models using variables such as DXY, GDP etc.) [68,69,70,71,72,73,74].

In the existing literature, there are many studies on energy shocks, price volatility and energy price determinants (or energy price forecasts). However, the absence of studies on the estimation of energy crises, which have a deeper negative impact on economies, has been considered as a gap in the literature. The reason for this lack is that energy crises until the 1990s were generally accepted as supply-driven energy crises. The causes of energy crises were considered to be only energy supply disruptions due to geopolitical risks. However, after the millennium, it has been observed that energy crises can occur in combination with different factors, including the financialization of the energy market, economy and financial markets and rapid increases in world energy demand. In addition, recently, financial crisis terms such as “speculative attack”, “herd psychology”, “self-fulfilling process” and “moral hazard” have been frequently mentioned in the energy market.

3. Model

Although no EWS model for energy crises has been studied in the literature, there are many studies in the literature where EWS models have been constructed for financial crises. The methods used in the construction of EWS models are classified into two groups: traditional approaches and other approaches. Traditional methods include the signal approach [75,76] and probit/logit models with limited dependent variables [77,78]. Other approaches such as Markovswitching approach [79,80], machine learning based analysis such as artificial neural networks and genetic algorithms [81,82], binary recursive trees [83] are used in the literature under the name of method classification for EWS model building. EWS models consist of 3 main elements: crisis index (binary dependent variable), explanatory variables and method of analysis [84]. LR method is used as the statistical method in this paper.

3.1. Logistic Regresion

The LR method is a statistical method that directly assesses the conditional probability of a crisis using a set of early warning indicators and can easily interpret the probability of a crisis. It is also amenable to standard statistical tests that assess the robustness of forecast results [85]. The estimated logit-probit model takes the following form:

, The dependent variable Energy Market Pressure Index (EMPI) with values of “1” or “0” (energy crisis or no energy crisis) is determined according to Equation (1).

In Equation (2), is the mean and is the standard deviation of the index. The probability of an energy crisis event is calculated by Equation (2).

denotes the explanatory variables and β denotes the model parameters. The odds ratio required for estimation interpretations is determined in Equation (3).

Logistic regression (LR) is a statistical analysis method that enables classification in accordance with probability theory by probabilistically calculating the estimated values of the dependent variable with the help of models created from the logistic probability distribution function. In LR LR analysis, the maximum likelihood method is used instead of the ordinary least square estimation method. In general, probit and logit models are seen as alternatives to each other. The probability distribution of probit models is based on the normal probability distribution. Probit and logit models give similar results, and the preference for one of these methods is based on its convenient package program and ease of interpretation [86], (p.145,154).

3.2. The Dependent Variable

According to Reinhart and Rogoff [87], there are two types of crisis definitions: the first is defined by exceeding a quantitative threshold, while the second is largely based on qualitative and judgmental analysis. In the first group of crisis definitions, a large increase in inflation in a certain period (e.g., 100% annual inflation) is defined as an inflation crisis, while a large increase in the exchange rate in a certain period (e.g., 30% monthly depreciation) is defined as a currency crisis based on a quantitative magnitude. The second group of crises defined by the definition method includes debt (domestic and external) and banking crises. For example; Failure to make a foreign debt payment when it is due is defined as a foreign debt crisis. Blocking and restricting accounts for domestic debt payment is also a case of domestic debt crisis. Events such as public takeover of banks against the risk of bank failure or bank shutdown are called banking crises.

In this context, in this study, a crisis is defined as a case when the EMPI, which is constructed with the help of an index formed by the energy price index and U.S. inflation, exceeds a certain threshold. In the process of estimating crises with LR analysis, each period should be converted into a binary dependent variable (crisis, 1; no crisis, 0). Yokuş and Ay [88], in their study on the systematics of defining currency crises, state that in the process of defining crises, an index is created with crisis parameters (price, quantity, inflation, etc.), and a significant deviation from the trend of this index can be defined as a crisis. Similarly, in this study, the form we call EMPI for energy crises is given in Equation (4).

Energy Cost Index (): The value of the index in period based on the World Bank Commodity Price Data [89] with 4.7% coal, 84.6% crude oil and 10.8% natural gas weighted prices. RCEI: the real energy price value of the ECI in period t (the value of the ECI trend in period t) calculated with the U.S. Consumer Price Index (CPI), : the standard deviation of the monthly changes in the ECI in the whole period, : the standard deviation of the monthly changes in the ECI trend in all periods. When calculating the RCEI, the ECI value in January 1960 and the U.S. CPI value are taken as the base period and the RCEI values for the period January 1960-December 1973 are calculated. Similarly, the base period for the remaining periods is January 1974. The reason for updating this ECI with inflation is that if Equation (4) is based only on the monthly increase of the ECI, the ECI falls and returns to a trend which would be identified as an energy crisis. For example, if the ECI, which has been moving at 60 units for a long time, falls to 15 units and then reaches a price of 40 units, it will be identified as a crisis case. In this case, it will cause the energy crisis months to be determined incorrectly. In order to eliminate this error, the EMPI equation is constructed with both the change of the ECI compared to the previous month and the deviation of the ECI from the real ECI. In the equation, these two parameters are divided by their standard deviations to prevent the EMPI from changing under the dominance of either of these two variables. As a result of these explanations, the definition of energy crisis takes the form of Equation (5).

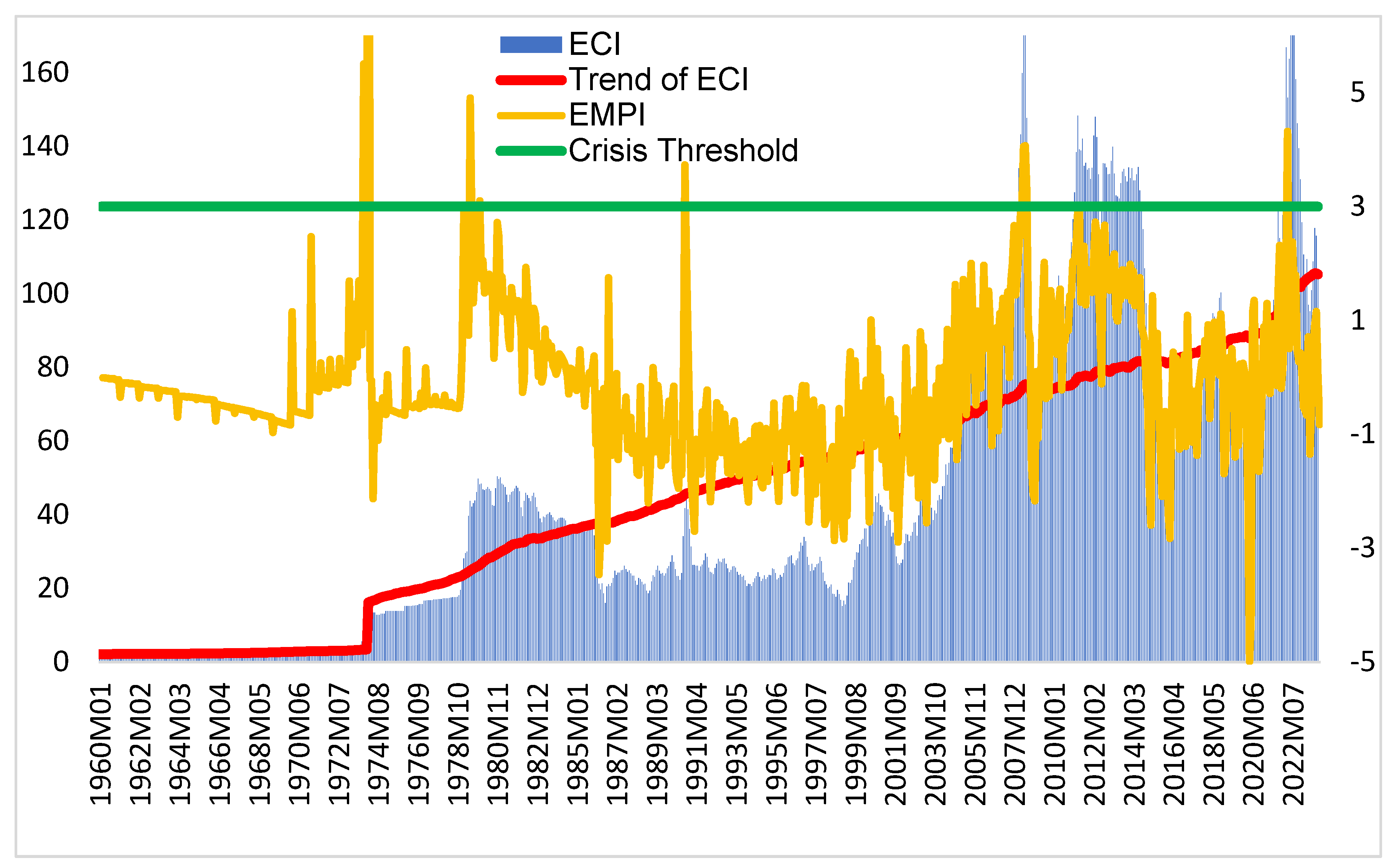

When the equation is analyzed, “b” is the magnitude coefficient of the exceedance from the average of the EMPI between 1 and 3. In the literature on the definition of financial crises, a certain (between 1-3) Standard Deviation (SD) exceedance from the index average is defined as a crisis [88]. Statistically normally distributed data fall within this threshold by 68%, 95% and 99.7% for 1 SD, 2 SD and 3 SD deviations from the mean, respectively. This value comparison shows that a 2 SD exceedance of the EMPI average is reasonable. Nevertheless, since the energy crisis definition is a new definition, the crisis cases detected in case of both 2 SD and 1.5 SD exceedances from the average are given in Table 1. According to the energy crisis definition, ECI, EMPI index, ECI trend and crisis threshold value for the period between January 1960 and November 2023 are given in Figure 1.

In order to examine the definition of energy crisis in more detail, the scope of the crisis definition is extended to 769 months between January 1960 and November 2023. According to Figure 1. the periods when the EMPI exceeds the crisis threshold are defined as crisis months (energy crisis cases). When the energy crisis definition is examined in the current Israel-Hamas conflict that started on October 7, 2023, it is not identified as an energy crisis by the definition, even though the ECI index increased. All of the crises in Table 1. are referred to as crises in different studies, but there is no explanation as to why they are referred to as crises, in which month they started or in which month they ended. These crises are automatically identified by the crisis definition.

In Table 1. 24 energy crisis cases were detected in the 769-month period as a result of 1.5 SS exceedance in the average of EMPI, and 12 crisis cases were detected in 2 SS exceedance of the average. The dependent variable in the study is set as no crisis (0) in 588 months and crisis (1) in 12 periods in the 600-month period between January 1973 and December 2022. Thus, the dependent variable is created by defining energy crises, which is the first component of EWS models.

3.3. Explanatory Variables

The set of explanatory variables of the EWS model is determined by considering the studies on energy prices in the literature. According to EIA, crude oil prices are determined by 7 main factors: the oil supply of non-OPEC countries, OPEC supply, supply and demand balance, spot prices, financial markets, consumption of non-OECD developing countries, demand of OECD countries [90]. Perifanis and Dagoumas [91], classifies indicators such as demand, supply, inventories, speculation (financialization of the crude oil market) investment, uncertainty (geopolitical risks) are classified into 6 subgroups.

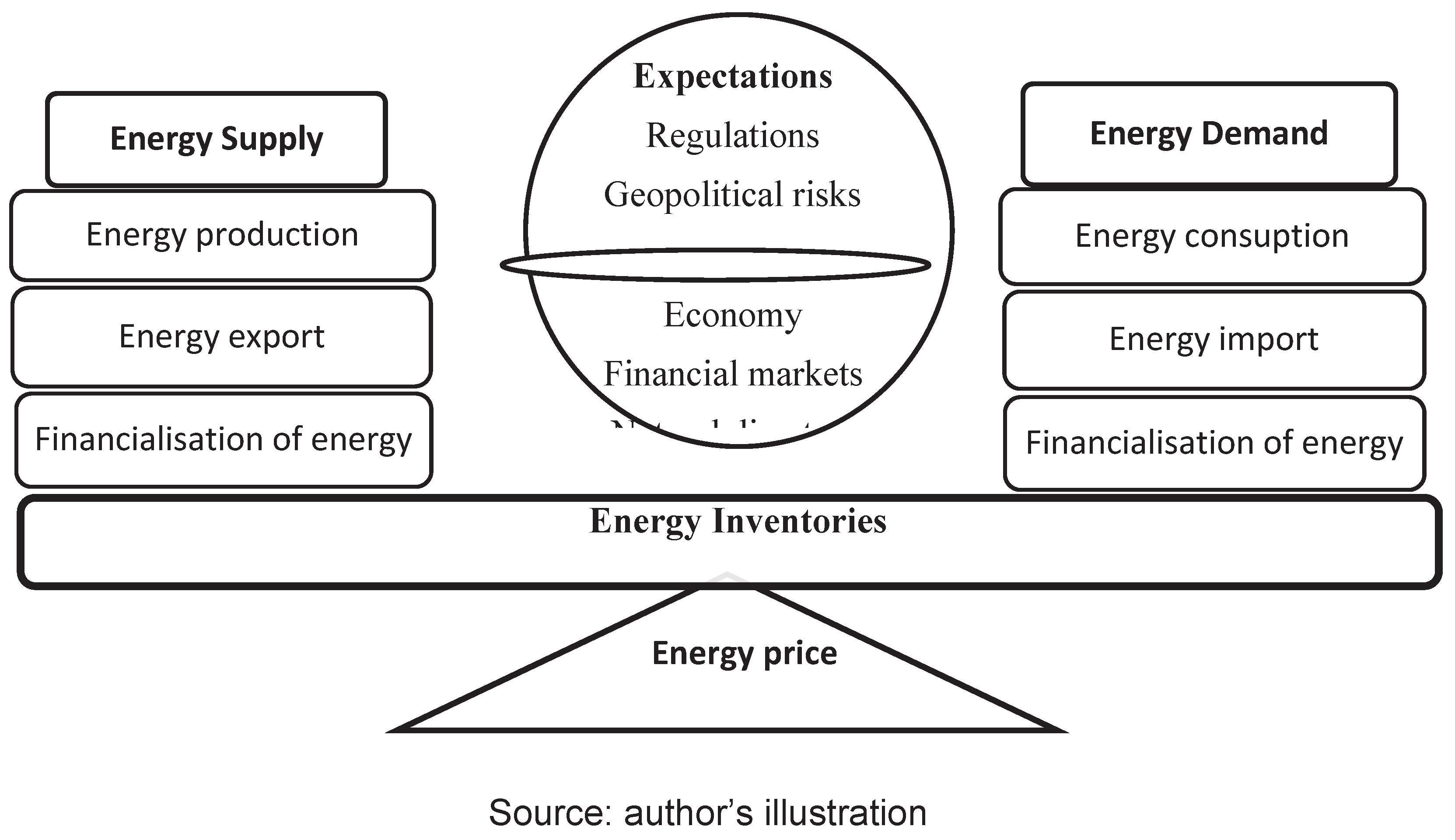

A schematic representation of how the energy price is formed in the market is given in Figure 2. Under normal conditions, the energy price is formed in the energy market according to the energy supply and demand balance as shown in Figure 2. Energy crises, on the other hand, are the cycles of increasing prices and market expectations in the energy market as a result of energy inventories, regulations, geopolitical risks, economic and financial markets and natural disasters that affect energy supply and demand. In the spot energy market, rising energy prices increase price expectations and rising price expectations increase the spot price. As a result of this cycle, exceeding the EMPI average by 2 SD is defined as an energy crisis.

Figure 2. and the existing literature, 27 indicator sets were identified as energy crisis determinants in 6 groups: supply and demand, economy financial markets, investments, geopolitical risks and expectations (see Appendix A).

3.4. Assumptions and Limitation of the Model

In the application of the EWS model for energy crises, some constraints and assumptions were made both for the LR analysis to make consistent and accurate predictions and for the start date and content of the data. For LR analysis, we tried to keep the data set as large as possible for consistent estimation [92], (p. 14). However, many indicators could not be used due to starting dates of series and lack of monthly data. In this context, indicators such as NYMEX, VIX, world oil stocks, world energy production-consumption and World energy import-export data were not included in the LR analysis. In addition, since there is no indicator data for regulations (e.g., regulations on environmental pollution or global warming and energy export sanctions from Russia due to the Russia-Ukraine war in 2022, etc.) and natural disasters, which are considered to be important for energy crises, they could not be added to the model.

For more consistent accurate estimation of LR analysis, extreme values are identified in the data set by performing extreme value analysis and these values are either removed from the data set or these data are adjusted. However, since the crisis phenomenon already occurred in the extreme values of the data, no adjustment was made for extreme values. As another issue, most of the studies in the literature are based on oil or petroleum resources. In this study, the energy cost index (ECI), which takes into account energy sources such as coal and natural gas in addition to oil, is used. Finally, although there are 27 factorial numbers of different alternative models for 27 independent variables, the assumption is made that the 13-variable model is the most consistent and the best predictor model according to the inadequacy of the data set and the selection algorithm of the SPPSS 27 package program.

3.5. Model Specification

The monthly data set for the period January 1973-December 2022 is used to estimate the Energy Crises EWS model. The dependent variable of the model is constructed as binary as there is a crisis (1) in the 12-month period and no crisis (0) in the 588-month period, as per the definition of energy crisis.

In order to determine the set of independent variables, new series up to 6 lags were created for each of the 27 independent variables. The univariate correlations of these new variables (series) with the dependent variable are analyzed. As a result of the analysis, by comparing the univariate correlations and probability values between each independent variable (including its lagged series) and the dependent variable [93] (p.93-95), it was determined which series of each of these 27 variables should be included in the model variable selection. Thus, these lagged explanatory variables provide the model with a crisis prediction capability with sufficient time intervals for policies and practices to mitigate the effects of the energy crisis before the crisis occurs. These 27 independent variables were subjected to variable selection methods in SPPSS 27 package program [94] and a final model with 13 explanatory variables was obtained.

Another aspect is that, in order to evaluate the performance of an EWS, the estimated probability of a crisis generated by the EWS model is usually compared to the actual probability of a crisis. Since the predicted probability is a continuous factor, the cut off threshold should be set as the level of the predicted probability of a crisis. This means that a crisis is expected when the probability generated by the model exceeds this threshold [95]. This raises the question of what is the “optimal” cut off threshold for the model to correctly predict the presence or absence of crises. Choosing a lower probability threshold will increase the number of correctly predicted crises, but this will increase the number of false crisis alarms (Type II errors). Conversely, choosing a higher threshold will reduce the number of false alarms, but this will result in an increased number of missed crises (Type I f errors). When setting the threshold, a balance can be struck by defining a threshold probability based on the relative importance given to Type I and Type II errors. In the EWS literature, a threshold value of 50% is generally accepted. However, as Esquivel and Larrain [96], point out, crisis cases are relatively unbalanced in the samples compared to no crisis cases. Therefore, choosing a threshold value of 50% weakens the predictive power of the EWS model. For this reason, we use both 50% and 25% threshold levels to evaluate the forecasting performance of the EWS model.

LR analysis does not require the assumptions of linear regression analysis, such as normality, continuity, equivariance and multivariate normality. However, as in all analyses where one variable is the outcome, the usual caveats about causal inference apply. Therefore, taking these general conditions into account in the studies where LR analysis will be applied will enable us to interpret the analyzes more reliably and more accurately [97] (p. 346,350). In LR analysis, it is important to test the stationarity of time series [98] (p. 12), sample size, independence of errors, linearity in the logit for continuous variables, absence of multicollinearity and lack of strongly influential outliers [99] (p. 9). Statistical tests and considerations regarding these assumptions were examined and found to be appropriate for the final model. However, in order not to lengthen the paper, these tests are not presented within its framework, but will be provided upon request.

4. Estimation results

4.1. Explanatory Variables Estimation Results

The EWS model of energy crises was constructed with 13 explanatory variables as a result of LR analysis. Variable coefficients, odds ratio, statistical significance level of the coefficients are given in Table 3. Nine predictor variables make a statistically significant (under %10 level) and unique contribution to the model: CPIG7, DXY3, FD1, GPRH, GREAICI6, FP/PEP3, PS, OPECI/NOPECI and PEP/PEC4. Independent variables with negative coefficients that contribute to the model: DXY3, PS, OPECI/NOPECI and PEP/PEC4. Declines in the monthly values of these variables with negative coefficients increase the probability of an energy crisis. In general, the variables affect the probability of energy crisis with signs in line with the economic literature.

The dollar index (DXY) is statistically shown to be negatively correlated with oil prices in Sui et al. [100]; Pal and Mitra, [101]; and is consistent with the model estimation. The other variables with negative coefficients, oil stocks (PS), oil imports from OPEC countries/imports from non-OPEC countries (OPECI/NOPECI) and primary energy production/consumption ratio with 4 lags (PEP/PEC4) are also negatively correlated with the energy crisis without any evidence from the literature. If DXY3, PS, OPECI/NOPECI ve PEP/PEC4 ratio increase by one unit of measure, chance that the energy crisis will occur decreases 0.4995, 0.5872, 0.9997 and 0.8338 times, respectively

The other statistically significant variables (CPIG7, FD1, GPRH, GREAICI6 and FP/PEP3), coefficient is positive, indicating that the rise in the value of these five variables increases the posibblity of a energy crisis. If CPIG7, FD1, GPRH, GREAICI6 and FP/PEP3 ratio rise by one unit of measure, chance that the energy crisis will occur increase 63.081, 1.1086, 1.0228, 1.0340, and 1.9636 times, respectively.

These variables are analyzed separately:

An increase in inflation in G7 countries (CPIG7: representative world inflation) is known to increase not only the costs of energy production, exploration, extraction, distribution and transportation, but also the risk perceptions of all firms involved in the energy production to consumption process. Moreover, an increase in inflation raises the expectation of an increase in energy prices, increasing the physical energy demand of individuals and firms for energy stocks, while financial actors will turn to speculative investments in the financialized energy market. These expectations of the market will increase energy prices and contribute to an energy crisis in the world.

An increase in the Crude Oil, Natural Gas, and Dry Wells, Total Footage Drilled (FD) indicator one month before the crisis increases the probability of an energy crisis. The main objective of firms is profit maximization. With the expectation that energy prices will increase, it is obvious that firms will prepare to produce more to meet the rising demand. Also in the literature, Ali et al. [102], statistically showed that the increase in oil and natural gas prices increases energy dirilling activities.

Another positive coefficient indicator of the energy crisis is the historical the geopolitical risk (GPRH) index. This index Dario Caldara and Matteo Iacoviello [34] (at the Federal Reserve Board.) compose a measure of adverse geopolitical incidents and associated risks based on a score of newspaper articles covering geopolitical stress, and examine its development and economic effects since 1900. It is generally accepted in the literature that energy prices are positively correlated with this indicator and that an rise in GPRH leads to an increase in energy prices [103,104]

The Index of global real economic activity (GREAICI) indicator was constructed by Kilian [17] using dry bulk one-way sea freight data for various industrial commodities such as grain, oilseed, coal, iron ore, fertilizer and scrap metal. He also showed that the index is positively correlated with energy prices. Again, this index was updated by Kilian [105] by eliminating the deficiencies of the index. In the model, an increase in the GREAICI indicator in the 6th month before the energy crisis increases the probability of an energy crisis.

Finally, an increase in the FP/PEP3 (Total Fossil Fuels Production/Total Primary Energy Production) ratio 3 months before an energy crisis increases the probability of an energy crisis. A relatively larger increase in total fossil energy production relative to energy production from primary energy sources (fossil, renewable and nuclear) increases the likelihood of an energy crisis. The reason for this situation is considered as more energy production from fossil sources due to the climatic production decline in renewable energy sources.

4.2. Goodness of Fit and Predictive Ability of The Model

The statistical results of the goodness of fit calculated from Eviews 13 and SPSS 27 package programs for the EWS model of energy crises constructed by LR analysis with statistically significant and insignificant independent variables are given in Table 4. According to the Eviews 13 test results given in the table: The model is quite robust as the McFadden R2 is above 60% and the LR statistical probability is below the 0.1% level.

According to the SPSS 27 test results given in the table: A model that includes all predictor variables is statistically significant, which shows that the model can differentiate cases with crisis from those with no crisis. Hosmer and Lemeshow test supports the model if the test result is not statistically significant., The whole model explains between 62,8% (Nagelkerke R2) and 11.2% (Cox and Snell R2) of variations in the dependent variable.

All these test results show that the EWS model of energy crises with 13 independent variables is a statistically significant and consistent model.

4.3. Model Prediction Accuracy

Although the EWS model of energy crises has successfully passed the statistical tests, it is extremely important that the model can accurately predict the observed dependent variables. Regarding the model’s forecasting ability, Table 5. presents the prediction accuracy data for the model’s observed dependent variables according to the probability thresholds of 0.25 and 0.5.

The model correctly classified 99% of cases (within both thresholds) for 595 months (595 months due to lagged series of independent variables) of the forecast period.

According to the Table 5., when the threshold value is set as 0.500, the model predicts that there will be no energy crisis in 582 months out of 583 months (with 99.8% accuracy) and that a crisis will occur in 1 month by giving a false crisis alarm (although no crisis is observed). Again, at the same threshold value, in the prediction of 12 months of observed crises, it predicts that a crisis will occur in 7 months (with 58.3% accuracy) and no crisis will occur in the remaining 5 months (even though a crisis is observed). When the threshold is set to 0.250, the model predicts crisis months with 75% accuracy and non-crisis months with 99.5% accuracy, while the overall prediction accuracy of 99% remains unchanged. Considering the negative consequences of crises, it is clear that Type I errors would be preferred if the model predicts the observed crisis as non-existent (Type I errors) compared to the classification of unobserved crisis as a crisis event (Type II errors).

5. Concluding Remarks

In the energy market, which has been financialized since the turn of the millennium, crisis determinants such as speculative attack, herd psychology, self-fulfilling process and expectations, which are familiar from financial crises, have started to be frequently mentioned in studies on energy price movements. In line with recent developments, the aim of this study is to build an EWS model of energy crises using LR analysis.The EWS model uses half a century of monthly data for the period from January 1973 to December 2022. Another contribution of the study to the literature is the development of a systematic definition of energy crises that has not been defined before. According to this definition, energy crisis cases were identified in different 12-month periods in the world during the analysis period. The crisis periods identified as a result of this definition are in line with the periods called energy/oil/oil crisis by researchers in the literature without qualitative or quantitative definitions.

According to model the estimation results, the energy crises are due to a combination of different energy supply-demand imbalances (Oil and natural gas drilling activities: FD1;Petroleum Stocks :PS; Fossil Fuels Production/Primary Energy Production ratio: FP/PEP3; Petroleum Imports From OPEC/Petroleum Imports From Non-OPEC Countries:OPECI/NOPECI and Primary Energy Production/Primary Energy Consumption ratio :PEP/PEC4), economic and financial disruptions (inflation: CPIG7; dollar index: DXY3,; index of global real economic activity :GREAICI6) and The geopolitical risks (GPRH).

An important criterion for the goodness of the EWS model is that it predicts crises a certain amount of time before they occur. In other words, there should be enough time for policies and measures to prevent or mitigate crises. The model takes the deterioration in global real economic activity 6 months before the crisis as the first signal, the energy production-consumption imbalance in the 4th month as the second signal, and the depreciation of the dollar index and the increase in fossil-based energy production relative to primary energy production as the third signal. In the pre-crisis month, natural gas and oil drilling activities increase, and when the crisis month arrives, energy crises may emerge as the rise in geopolitical risks and inflation increases are accompanied by declines in oil stocks.

This manuscrit could be extended for further research by including new explanatory variables like energy market financialization factors, other energy source indicators, contagion indicator and more variables that take into account private sector investments. Additionally, other methods like the signaling approach, the Markovswitching approach and machine learning approaches might be used in order to compare the models of estimation results.

Appendix A

The appendix contains explanations, abbreviations, data source and references for the explanatory variables.

Table A.

Explanatory variables of the model.

| Indicator | Abbreviation | Refernce | Data Sources |

|---|---|---|---|

| Supply and Demand | |||

| U.S. Total Fossil Fuels Consumption (Quadrillion Btu) | FC | [17,36,58,60,61,62,63,64,65,66,67] | U.S.EIA |

| U.S. Total Fossil Fuels Production (Quadrillion Btu) | FP | ||

| U.S. Total Primary Energy Consumption (Quadrillion Btu) | PEC | ||

| U.S. Total Primary Energy Production (Quadrillion BTU) | PEP | ||

| U.S.Total Petroleum Stocks (Million Barrels) | PS | ||

| U.S.Total Energy Net Imports | ENI | ||

| U.S.Petroleum Imports From Total Non-OPEC Countrie | INOPEC | ||

| U.S.Petroleum Imports From Total OPEC (Thousand Barrels per Day) | IOPEC | ||

| Petroleum Imports From Total OPEC (Thousand Barrels per Day)/Petroleum Imports From Total Non-OPEC Countries | IOPEC/ INOPEC | ||

| Total Petroleum Stocks/Petroleum Consumption (Excluding Biofuels) | PS/PC | ||

| Total Fossil Fuels Consumption/Total Fossil Fuels Production *100 | FC/FP | ||

| Total Fossil Fuels Production/Total Primary Energy Production | FP/PEP | ||

| Total Primary Energy Production/Total Primary Energy Consumption | PEP/PEC | ||

| (Total Fossil Fuels Consumption- Total Fossil Fuels Production) /Net Energy İmport | FC-FP/NEI | ||

| Total Primary Energy Comsumtion- Total Primary Energy Production)/Net Energy İmpor | PEC-PEP/NEI | ||

| Total Energy Net Imports/Total Petroleum Stocks | ENI/PS | ||

| Economy Financial Markets | |||

| G7 Industrial Production, Seasonally adjusted, Index (It is an index created by the author according to the GDP weight of countries in 2021.) | IPI | [63,106,107,108,109] | International Financial Statistics (IFS) Data |

| Federal Funds Effective Rate | FEDIN | [110,111,112,113] | Federal Reserve Bank of St. Louis (FRED) |

| Consumer price indices G7 | G7CPI | [63,114,115,116] | OECD |

| Prices, Consumer Price Index, All items | USA CPI | International Financial Statistics (IFS) | |

| U.S. Dollar Index | DXY | [63,68,69,70,71] | Bank for International Settlements (BIS) |

| Gold ONS Spot Price | GOS | [72,73,74] | FRED database of the Federal Reserve Bank of St. Louis. |

| Investments | |||

| Crude Oil, Natural Gas, and Dry Wells, Total Footage Drilled (Thousand Feet) | FD | [102] | U.S.EIA |

| Bakers Hugehes Ring Count | BHRC | [117] | https://rigcount.bakerhughes.com/ |

| Geopolitical Risks | |||

| Historical index (since 1900): The geopolitical risk (GPR) index | GPRH | [103,104] | https://www.policyuncertainty.com/ |

| Index of global real economic activity in industrial commodity markets | GREAICI | [17,63,105] | https://sites.google.com/site/lkilian2019/home |

| G20 Composite leading indicator (CLI) | G20CLI | [118] | OECD |

*Monthly changes of the indicators were used and conversions were made for different energy units in the indicator.

References

- International Energy Agency (IEA). (2022). World Energy Outlook (WEO) 2022. Paris: International Energy Agency (IEA).

- Alshareef, S. The Gulf’s shifting geoeconomy and China’s structural power: From the petrodollar to the petroyuan? Compet. Chang. 2023, 27, 340–401. [Google Scholar] [CrossRef]

- van de Ven, D.J. Historical energy price shocks and their changing effects on the economy. Energy Econ. 2017, 204–216. [Google Scholar] [CrossRef]

- Alagöz, M.; Yokuş, N.; Yokuş, T. Photovoltaic solar power plant investment optimization model for economic external balance: Model of Turkey. Energy Environ. 2019, 30, 522–541. [Google Scholar] [CrossRef]

- Saçık, S.Y.; Yokuş, N.; Alagöz, M.; Yokuş, T. Optimum Renewable Energy Investment Planning in Terms of Current Deficit: Turkey Model. Energies 2020, 13, 1509. [Google Scholar] [CrossRef]

- Alam, M.K.; Tabash, M.I.; Billah, M.; Kumar, S.; Anagreh, S. The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets. J. Risk Financ. Manag. 2022, 15, 352. [Google Scholar] [CrossRef]

- Prohorovs, A. Russia’s War in Ukraine: Consequences for European Countries’Businesses and Economies. J. Risk Financ. Manag. 2022, 15, 1–15. [Google Scholar] [CrossRef]

- Organization of Petroleum Exporting Countries (OPEC). (2011). World Oil Outlook 2011. Vienna: Organization of Petroleum Exporting Countries (OPEC).

- Khan, M.S. The 2008 Oil Price “Bubble”. Peterson Institute for International Economics. 2009, 1-9.

- Frankel, J.; Rose, A.K. (2010). Determinants of Agricultural and Mineral Commodity Prices. HKS Faculty Research Working Paper Series, RWP10-038, 1-48.

- Redrado, M.; Carrera, J.; Bastourre, D.; Ibarlucia, J. (2009). Financialization of Commodity Markets: Nonlinear Consequences from Heterogeneous. Banco Central De La República Argentina, Investigaciones Económicas., Working Paper 2009, 1-57.

- Hamilton, J.D. Oil and the Macroeconomy since World War II. J. Political Econ. 1983, 91, 228–248. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Filis, G. Oil shocks and stock markets: Dynamic connectedness under the prism of recent geopolitical and economic unrest. Int. Rev. Financ. Anal. 2017, 50, 1–26. [Google Scholar] [CrossRef]

- Chisadza, C.; Dlamini, J.; Gupta, R.; Modise, M.P. The impact of oil shocks on the South African economy. Energy Sources Part B Econ. Plan. Policy 2016, 11, 739–745. [Google Scholar] [CrossRef]

- Gkillas, K.; Gupta, R.; Wohar, M.E. Oil shocks and volatility jumps. Rev. Quant. Financ. Account. 2020, 54, 247–272. [Google Scholar] [CrossRef]

- Hollander, H.; Gupta, R.; Wohar, M.E. The Impact of Oil Shocks in a Small Open Economy New-Keynesian Dynamic Stochastic General Equilibrium Model for an Oil-Importing Country: The Case of South Africa. Emerg. Mark. Financ. Trade 2019, 55, 1593–1618. [Google Scholar] [CrossRef]

- Kilian, L. Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market. Am. Econ. Rev. 2009, 99, 1053–1069. [Google Scholar] [CrossRef]

- Kang, W.; Ratti, R.A. Oil shocks, policy uncertainty and stock returns in China. Econ. Transit. 2015, 23, 657–676. [Google Scholar] [CrossRef]

- Balli, E.; Çatık, A.N.; Nugent, J.B. Time-varying impact of oil shocks on trade balances: Evidence using the TVP-VAR model. Energy 2021, 217, 119377. [Google Scholar] [CrossRef]

- Forhad, M.; Alam, M. Impact of oil demand and supply shocks on the exchange rates of selected Southeast Asian countries. Glob. Financ. J. 2021, 54, 100637. [Google Scholar] [CrossRef]

- Schneider, M. The Impact of Oil Price Changes on Growth and Inflation. Monet. Policy Econ. 2004, 2, 27–36. [Google Scholar]

- Sill, K. (2007). The Macroeconomics of Oil Shocks. Federal Reserve Bank of Philadelphia, Business Review, 1.

- Farzanegan, M.R.; Markwardt, G. The effects of oil price shocks on the Iranian. Energy Econ. 2009, 31, 134–151. [Google Scholar] [CrossRef]

- Haug, A.A.; Basher, A.S. (tarih yok). Exchange rates of oil exporting countries and global oil price shocks: A nonlinear smooth-transition approach. Applied Economics, 51. [CrossRef]

- Khraief, N.; Shahbaz, M.; Mahalik, K.M.; Bhattacharya, M. Movements of oil prices and exchange rates in China and India: New evidence from wavelet-based, non-linear, autoregressive distributed lag estimations. Phys. A:Stat. Mech. Its Appl. 2021, 563, 125423. [Google Scholar] [CrossRef]

- Krugman, P. New theories of trade among industrial countries. Am. Econ. Rev 1983, 73, 343–347. [Google Scholar]

- Elder, J.; Serletis, A. Oil Price Uncertainty. J. Money Credit. Bank. 2010, 42, 1137–1159. [Google Scholar] [CrossRef]

- Henriques, I.; Sadorsky, P. The effect of oil price volatility on strategic investment. Energy Econ. 2011, 33, 79–87. [Google Scholar] [CrossRef]

- Diaz, E.M.; Molero, C.J.; de Gracia, F.P. Oil price volatility and stock returns in the G7 economies. Energy Econ. 2016, 54, 417–430. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.; Raza, N.; Roubaud, D. Oil volatility and sovereign risk of BRICS. Energy Econ. 2018, 70, 258–269. [Google Scholar] [CrossRef]

- Van Robays, I. Macroeconomic Uncertainty and Oil Price Volatility. Oxf. Bull. Econ. Stat. 2016, 78, 671–693. [Google Scholar] [CrossRef]

- Beidas-Strom, S.; Pescatori, A. Oil Price Volatility and the Role of Speculation. IMF Work. Pap. 2014, 14, 1. [Google Scholar] [CrossRef]

- Robe, M.A.; Wallen, J. Fundamentals, Derivatives Market Information and Oil Price Volatility. J. Futures Mark. 2015, 36, 317–344. [Google Scholar] [CrossRef]

- Caldar, D.; Cavallo, M.; Iacoviello, M. Oil price elasticities and oil price fluctuations. J. Monet. Econ. 2019, 103, 1–20. [Google Scholar] [CrossRef]

- Fattouh, B.; Kilian, L.; Mahadeva, L. The role of speculation in oil markets: What have the role of speculation in oil markets. Energy J. 2013, 34, 7–33. [Google Scholar] [CrossRef]

- Behmiri, N.B.; Manso, J.R. Crude Oil Price Forecasting Techniques: A Comprehensive Review of Literature. Altern. Investig. Anal. Rev. 2013, 2, 30–48. [Google Scholar] [CrossRef]

- Chuaykoblap, S.; Chutima, P.; Chandrachai, A.; Nupairoj, N. Expert-based text mining with Delphi method for crude oil price prediction. Int. J. Ind. Syst. Eng. 2017, 25, 545–563. [Google Scholar] [CrossRef]

- Abramson, B.; Finizza, A. Using belief networks to forecast oil prices. Int. J. Forecast. 1991, 7, 299–315. [Google Scholar] [CrossRef]

- Agbon, I.S.; Araque, J.C. (2003). Predicting Oil and Gas Spot Prices Using Chaos Time Series Analysis and Fuzzy Neural Network Model. SPE Hydrocarbon Economics and Evaluation Symposium. Dallas, Texas.

- Li, X.; Shang, W.; Wang, S. Text-based crude oil price forecasting: A deep learning approach. Int. J. Forecast. 2019, 35, 1548–1560. [Google Scholar] [CrossRef]

- Yu, L.; Wang, S.; Lai, K.K. A rough-set-refined text mining approach for crude oil market tendency forecasting. Int. J. Knowl. Syst. Sci. 2005, 2, 33–46. [Google Scholar]

- Gupta, N.; Nigam, S. (2020). Crude Oil Price Prediction using Artificial Neural Network. The 3rd International Conference on Emerging Data and Industry 4.0 (EDI40) (s. 642–647). Warsaw: Procedia Computer Science.

- Vochozka, M.; Horák, J.; Krulický, T.; Pardal, P. Predicting future Brent oil price on global markets. Acta Montan. Slovaca 2020, 25, 375–392. [Google Scholar] [CrossRef]

- Xie, W.; Yu, L.; Xu, S.; Wang, S. (2006). A New Method for Crude Oil Price Forecasting Based on Support Vector Machines. Computational Science – ICCS 2006. 3994, s. 444–451. Berlin: Springer.

- Yu, L.; Zhang, X.; Wang, S. Assessing Potentiality of Support Vector Machine Method in Crude. EURASIA J. Math. Sci. Technol. Educ. 2017, 13, 7893–7904. [Google Scholar] [CrossRef] [PubMed]

- Pindyck, R.S. The Long-Run Evolution of Energy Prices. Energy J. 1999, 20, 1–27. [Google Scholar] [CrossRef]

- Lanza, A.; Manera, M.; Giovannini, M. Modeling and forecasting cointegrated relationships among heavy. Energy Econ. 2005, 27, 831–848. [Google Scholar] [CrossRef]

- Aloui, C.; Mabrouk, S. Value-at-risk estimations of energy commodities via longmemory, asymmetry and. Energy Policy 2010, 38, 2326–2339. [Google Scholar] [CrossRef]

- Abosedra, S.; Baghestani, H. On the predictive accuracy of crude oil futures prices. Energy Policy 2004, 32, 1389–1393. [Google Scholar] [CrossRef]

- Alexander, C.; Lazar, E. Normal mixture GARCH (1, 1): Applications to exchange rate modelling. J. Appl. Econom. 2006, 21, 307–336. [Google Scholar] [CrossRef]

- Hung, J.-C.; Wang, Y.-H.; Chang, M.C.; Shih, K.-H.; Kao, H.-H. Minimum variance hedging with bivariate regime-switching model for WTI crude oil. Energy 2011, 36, 3050–3057. [Google Scholar] [CrossRef]

- Huntington, H.G. l price forecasting in the 1980s: What went wrong? Energy J. 1994, 15, 1–22. [Google Scholar] [CrossRef]

- Krugman, P.R. Target zones and exchange rate dynamics. Q. J. Econ. 1991, 106, 669–682. [Google Scholar] [CrossRef]

- Tang, L.; Hammoudeh, S.M. An empirical exploration of the world oil price under the target zone model. Energy Econ. 2002, 24, 577–596. [Google Scholar] [CrossRef]

- Merino, A.; Ortiz, Á. Explaining the So-called ‘Price Premium’ in Oil Markets. OPEC Rev. 2005, 29, 133–152. [Google Scholar] [CrossRef]

- Ye, M.; Zyren, J.; Shore, J. Forecasting Short-run Crude Oil Price Using High and Low Inventory Variables. Energy Policy 2006, 34, 2736–2743. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Dees, S.; Karadeloglou, P.; Sanchez, M. Does OPEC Matter? An Econometric Analysis of Oil Prices. Energy J. 2004, 25, 67–90. [Google Scholar] [CrossRef]

- Dées, S.; Karadeloglou, P.; Kaufmann, R.K.; Sánchez, M. Modelling the world oil market: Assessment of a quarterly econometric model. Energy Policy 2007, 35, 178–191. [Google Scholar] [CrossRef]

- Chevillon, G.; Rifflart, C. Physical market determinants of the price of crude oil and the market premium. Energy Econ. 2009, 31, 537–549. [Google Scholar] [CrossRef]

- Yang, C.W.; Hwang, M.J.; Huang, B.N. An analysis of factors affecting price volatility of the US oil market. Energy Econ. 2002, 24, 107–119. [Google Scholar] [CrossRef]

- Mirmirani, S.; Li, H.C. A comparison of VAR and neural networks with genetic algorithm in forecasting. Adv. Econom. 2004, 19, 203–223. [Google Scholar]

- Gong, X.; Chen, L.; Lin, B. Analyzing dynamic impacts of different oil shocks on oil price. Energy 2020, 198, 117306. [Google Scholar] [CrossRef]

- Drachal, K. Forecasting crude oil real prices with averaging time-varying VAR models. Resour. Policy 2021, 74, 102244. [Google Scholar] [CrossRef]

- Fueki, T.; Nakajima, J.; Ohyama, S.; Tamanyu, Y. Identifying oil price shocks and their consequences: The role of expectations in the crude oil market. Int. Financ. 2021, 24, 53–76. [Google Scholar] [CrossRef]

- Sanders, D.R.; Manfredo, M.R.; Boris, K. Evaluating information in multiple horizon forecasts: The DOE’s energy price forecasts. Energy Econ. 2009, 31, 189–196. [Google Scholar] [CrossRef]

- Hamilton, J.D. Historical Oil Shocks. NBER Work. Pap. 2011, 16790, 1–51. [Google Scholar]

- Baumeister, C.; Kilian, L. Understanding the Decline in the Price of Oil since June 2014. J. Assoc. Environ. Resour. Econ. 2016, 3, 131–158. [Google Scholar] [CrossRef]

- Beckmann, J.; Czudaj, R.L.; Arora, V. The relationship between oil prices and exchange rates: Revisiting theory and evidence. Energy Econ. 2020, 88, 104772. [Google Scholar] [CrossRef]

- Aloui, R.; Hammoudeh, S.; Nguyen, D.K. A time-varying copula approach to oil and stock market dependence: The case of transition economies. Energy Econ. 2013, 39, 208–221. [Google Scholar] [CrossRef]

- Thalassinos, E.I.; Politis, E. The Evaluation of the USD Currency and the Oil Prices: A VAR Analysis. Eur. Res. Stud. J. 2012, 15, 137–146. [Google Scholar]

- Jawadi, F.; Louhichi, W.; Ameur, H.B. On oil-US exchange rate volatility relationships: An intraday analysis. Econ. Model. 2016, 59, 329–334. [Google Scholar] [CrossRef]

- Reboredo, J.C. Is gold a hedge or safe haven against oil price movements? Resour. Policy 2013, 38, 130–137. [Google Scholar] [CrossRef]

- Mokni, K. Time-varying effect of oil price shocks on the stock market returns: Evidence from oil-importing and oil-exporting countries. Energy Rep. 2020, 6, 605–619. [Google Scholar] [CrossRef]

- Tiwari, K.A.; Aye, G.C.; Gupta, R.; Gkillas, K. Gold-oil dependence dynamics and the role of geopolitical risks: Evidence from a Markov-switching time-varying copula model. Energy Econ. 2020, 88, 104748. [Google Scholar] [CrossRef]

- Kaminsky, G.L.; Reinhart, C.M. The twin crises: The causes of banking and balance-of-payments problems. Am. Econ. Rev. 1999, 89, 473–500. [Google Scholar] [CrossRef]

- Kaminsky, L.G.; Lizondo, S.; Reinhart, C.M. Leading Indicators of Currency Crises. IMF Working Papers 1997, 1997, 1–43. [Google Scholar] [CrossRef]

- Eichengreen, B.; Rose, A.K.; Wyplosz, C. Contagious Currency Crises. Natl. Bur. Econ. Res. (NBER) Work. Pap. 1996, 5681, 1–50. [Google Scholar] [CrossRef]

- Frankel, J.A.; Rose, A.K. Currency crashes in emerging markets: An empirical treatment. J. Int. Econ. 1996, 41, 351–366. [Google Scholar] [CrossRef]

- Cerra, V.; Saxena, C.S. What Caused the 1991 Currency Crisis in India? IMF Econ Rev. 2002, 49, 395–425. [Google Scholar] [CrossRef]

- Abiad, A. Early-Warning Systems:A Survey and a Regime-Switching Approach. IMF Working Papers 2003, 2003, 160. [Google Scholar]

- Nag, A.K.; Mitra, A. (1999). Reserve Bank of India Occasional Paper, 20(2), 183-222. Oil shocks, policy uncertainty and stock returns in China. (2015). Economics of Transition, 23(4), 657-676.

- Apoteker, T.; Barthelemy, S. (2000). Genetic Algorithms and Financial Crises in emerging markets. AFFI International Conference in Finance Processing. 45. Sienne: CEFI.

- Ghosh, S.R.; Ghosh, A.R. Structural Vulnerabilities and Currency Crises. IMF Econ Rev 2003, 50, 481–506. [Google Scholar] [CrossRef]

- Ari, A. Early warning systems for currency crises: The Turkish case. Econ. Syst. 2012, 36, 391–410. [Google Scholar] [CrossRef]

- Candelon, B.; Dumitrescu, E.-I.; Hurlin, C. Currency crisis early warning systems: Why they should be dynamic. Int. J. Forecast. 2014, 30, 1016–1029. [Google Scholar] [CrossRef]

- Gujarati, D. (2011). Econometrics by Example. New York: Palgrave Macmillan.

- Reinhart, C.M.; Rogoff, K.S. (2009). This Time Is Different: Eight Centuries of Financial Folly. Princeton and Oxford: Princeton University Press.

- Yokuş, T.; Ay, A. Kur Krizleri ve Türkiye: 2006-2018 Dönemi. Yönetim Ve Ekon. Araştırmaları Derg. 2020, 18, 295–316. [Google Scholar] [CrossRef]

- World Bank (WB). Commodity Markets. Available online: https://www.worldbank.org/en/research/commodity-markets (accessed on 22 December 2023).

- USEnergy Information Administration (EIA) (2018) What drives crude oil prices: Overview Washington: U.S. Energy Information Administration (EIA).

- Perifanis, T.; Dagoumas, A. Crude oil price determinants and multi-sectoral effects: A review. Energy Sources Part B Econ. Plan. Policy 2021, 16, 787–860. [Google Scholar] [CrossRef]

- Schoonbroodt, A. (2004). Small sample bias using maximum likelihood versus moments: The case of a simple search model of the labor market. Working Paper, University of Minnesota, 1-29.

- Hosmer Jr, D.W.; Lemeshow, S. (2000). Applied logistic regression. Ohio: Wİley.

- Field, A. (2013). Discovering Statistics Using IBM SPSS Statistics. London: SAGE Publications Ltd.

- Bussière, M.; Fratzscher, M. (2002). Towards a new early warning system of financial crises. Frankfurt: European Central Bank (ECB).

- Esquivel, G.; Larrain, F. (1998). Explaining Currency Crises. John F. Kennedy Faculty Research, WP Series R98-07, 1-43.

- Tabachnick, B.G.; Fidell, L.S. (2019). Using Multivariate Statistics. New York: Pearson.

- Peltonen, T.A. (2006). Are emerging market currency crises predictable? A test. ECB Working Paper, No. 571, 1-49.

- Josephat, P.K.; Ame, A. Effect of Testing Logistic Regression Assumptions on the Improvement of the Propensity Scores. Int. J. Stat. Appl. 2018, 8, 9–17. [Google Scholar]

- Sui, B.; Chang, C.-P.; Jang, C.-L.; Gong, Q. Analyzing causality between epidemics and oil prices: Role of the stock market. Economic Analysis and Policy 2021, 70, 148–158. [Google Scholar] [CrossRef]

- Pal, D.; Mitra, S.K. Asymmetric oil price transmission to the purchasing power of the U.S. dollar: A multiple threshold NARDL modelling approach. Resour. Policy 2019, 64, 101508. [Google Scholar] [CrossRef]

- Ali, M.K.; Zahoor, M.K.; Saeed, A.; Nosheen, S.; Thanakijsombat, T. Institutional and country level determinants of vertical integration: New evidence from the oil and gas industry. Resour. Policy 2023, 84, 103777. [Google Scholar] [CrossRef]

- Wang, K.-H.; Su, C.-W.; Umar, M. Geopolitical risk and crude oil security: A Chinese perspective. Energy 2021, 219, 119555. [Google Scholar] [CrossRef]

- Liu, J.; Ma, F.; Tang, Y.; Zhang, Y. Geopolitical risk and oil volatility: A new insight. Energy Econ. 2019, 84, 104548. [Google Scholar] [CrossRef]

- Kilian, L. Measuring global real economic activity: Do recent critiques hold up to scrutiny. Econ. Lett. 2019, 178, 106–110. [Google Scholar] [CrossRef]

- Ratti, R.A.; Vespignani, J.L. Oil prices and global factor macroeconomic variables. Energy Econ. 2016, 59, 198–212. [Google Scholar] [CrossRef]

- Yıldırım, E.; Öztürk, Z. Oil price and industrial production in G7 countries: Evidence from the asymmetric and non-asymmetric causality tests. Procedia Soc. Behav. Sci. 2014, 143, 1020–1024. [Google Scholar] [CrossRef]

- Pinno, K.; Serletis, A. Oil Price Uncertainty and Industrial Production. Energy J. 2013, 34, 191–216. [Google Scholar] [CrossRef]

- Elder, J. Oil Price Volatiiıty: Industrial Production and Special Aggregates. Macroecon. Dyn. 2018, 22, 640–653. [Google Scholar] [CrossRef]

- Arora, V.; Tanner, M. Do oil prices respond to real interest rates? Energy Econ. 2013, 36, 546–555. [Google Scholar] [CrossRef]

- Kilian, L.; Zhou, X. Oil prices, exchange rates and interest rates. J. Int. Money Financ. 2022, 126, 102679. [Google Scholar] [CrossRef]

- Cologni, A.; Manera, M. Oil prices, inflation and interest rates in a structural cointegrated VAR model for the G-7 countries. Energy Econ. 2008, 30, 856–888. [Google Scholar] [CrossRef]

- Kim, J.-M.; Jung, H. Dependence Structure between Oil Prices, Exchange Rates, andInterest Rates. Energy J. 2018, 39, 259–280. [Google Scholar] [CrossRef]

- Cheng, I.-H.; Xiong, W. Financialization of Commodity Markets. Annu. Rev. Financ. Econ. 2014, 6, 419–441. [Google Scholar] [CrossRef]

- Arnold, S.; Auer, B.R. What do scientists know about inflation hedging? North-Am. J. Econ. Financ. 2015, 34, 187–214. [Google Scholar] [CrossRef]

- Wen, F.; Zhang, K.; Gong, X. The effects of oil price shocks on inflation in the G7 countries. North-Am. J. Econ. Financ. 2021, 57, 101391. [Google Scholar] [CrossRef]

- Khalifa, A.; Caporin, M.; Hammoudeh, S.M. The relationship between oil prices and rig counts: The importance of lags. Energy Econ. 2017, 63, 213–226. [Google Scholar] [CrossRef]

- Byrne, J.P.; Lorusso, M.; Xu, B. Oil Prices, Fundamentals and Expectations. Energy Econ. 2019, 79, 59–75. [Google Scholar] [CrossRef]

Figure 1.

World Energy Crises: 1960 January-2023 November. Source:author’s illustration.

Figure 2.

Figural representation of the formation of energy prices.

Table 1.

World Energ Crises: 1960 January-2022 December.

| Crises Term | EMPI | Principal factors | Crises Term | EMPI | Principal factors |

|---|---|---|---|---|---|

| 1971M01 | 2.47 | Trans-Arabian pipeline rupture | 2008M03 | 2.85 | GFC and Oil demand increases |

| 1973M10* | 5.50 | Yom Kippur war | 2008M04* | 3.04 | |

| 1974M01* | 28.65 | 2008M05* | 4.05 | ||

| 1979M01* | 3.00 | Iranian revolution | 2008M06* | 4.06 | |

| 1979M05* | 4.90 | 2008M07* | 3.26 | ||

| 1979M06 | 2.93 | 2011M03 | 2.88 | Arab Spring | |

| 1979M10 | 2.47 | 2011M04* | 3.02 | ||

| 1979M11* | 3.10 | 2012M02 | 2.72 | ||

| 1980M10 | 2.72 | The Iran-Iraq War | 2012M03 | 2.55 | |

| 1980M11 | 2.49 | 2012M08 | 2.67 | ||

| 1990M08* | 3.73 | First Gulf War | 2022M03* | 4.32 | Ukraine-Rusia War |

| 2007M11 | 2.66 | 2008 GFC and Oil demand increases | 2022M06 | 2.38 |

* There are crisis cases of excess of 2 SD from the mean and other cases of excess of 1.5 SD. Source: author’s illustration.

Table 3.

Results of the evaluated logit model with 13 independent variables.

| Variable | Coefficient | Odds ratio | z-Statistic | P. | 95% CI | |

| Low | High | |||||

| CPIG7 | 4.1444 | 63.0817 | 3.0976 | 0.0020 | 1.5166 | 6.7723 |

| DXY3 | -0.6942 | 0.4995 | -3.0793 | 0.0021 | -1.1369 | -0.2514 |

| FD1 | 0.1031 | 1.1086 | 1.6233 | 0.0945 | -0.0216 | 0.2278 |

| G20CLI6 | -0.0018 | 0.9982 | -0.6175 | 0.5369 | -0.0077 | 0.0040 |

| GOS | 0.0892 | 1.0933 | 1.4842 | 0.1378 | -0.0288 | 0.2072 |

| GPRH | 0.0226 | 1.0228 | 3.1858 | 0.0014 | 0.0087 | 0.0365 |

| GREAICI6 | 0.0334 | 1.0340 | 3.5745 | 0.0004 | 0.0151 | 0.0518 |

| FP/PEP3 | 1.2241 | 3.4012 | 1.9636 | 0.0496 | -0.0003 | 2.4486 |

| PS | -0.5324 | 0.5872 | -1.8659 | 0.0621 | -1.0929 | 0.0280 |

| NOPECI1 | 0.0594 | 1.0612 | 1.2512 | 0.2109 | -0.0338 | 0.1525 |

| OPECI/NOPECI | -0.0003 | 0.9997 | -1.8350 | 0.0665 | -0.0006 | 0.0000 |

| PECDPEP/NEI4 | -0.0005 | 0.9995 | -1.1627 | 0.2449 | -0.0015 | 0.0004 |

| PEP/PEC4 | -0.1818 | 0.8338 | -1.9603 | 0.0500 | -0.3640 | 0.0003 |

| C | -10.3061 | 0.0000 | -5.2548 | 0.0000 | -14.1582 | -6.4541 |

*The number at the end of the abbreviation of the variable indicates the month of lag. CI: Confidence interval.

Table 4.

Eviews 13 and SPSS 27 Model Goodness of Fit Test Results.

| Eviews 13 Model Goodness of Fit Test Results | |||

| McFadden R-squared | 0.603304 | ||

| LR statistic | 70.85451 | ||

| Prob (LR statistic) | 0.00001 | ||

| SPSS 27 Model Goodness of Fit Test Results | |||

| Omnibus Tests of Model Coefficients | Chi-square (χ2) | Degrees of freedom | Significance |

| 70.984 | 13 | 0.000 | |

| Hosmer and Lemeshow Test | 7.647 | 8 | 0.469 |

| Model Match Test | -2 Log likelihood | Cox & Snell R Square | Nagelkerke R Square |

| 46,460a | 0.112 | 0.628 | |

a. Estimation terminated at iteration number 10 because parameter estimates changed by less than ,001.

Table 5.

Model Prediction Accuracy.

| Predicted (The cut value is .500) | Predicted (The cut value is .250) | ||||||

| Crises | Percentage Correct | Crises | Percentage Correct | ||||

| 0 | 1 | 0 | 1 | ||||

| Observed Crises | 0 | 582 | 1 | 99.8 | 580 | 3 | 99.5 |

| 1 | 5 | 7 | 58.3 | 3 | 9 | 75 | |

| Overall Percentage | 99.0 | 99 | |||||

*Monthly changes of the indicators were used and conversions were made for different energy units in the indicator.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.