Submitted:

21 June 2023

Posted:

21 June 2023

You are already at the latest version

Abstract

Current and dynamic developments in green technologies have led to several innovation practices in the manufacturing sector only to become the top approaches used for achieving and accelerating sustainable development (SD) in the current business markets. In addition, manufacturing firms is in need of green innovation to be able to monitor and control their operations and enhance their environmental performance. However, regardless of its many benefits, the level of green innovation adoption and implementation is still lower than expected among manufacturing industries. Thus, this study aimed to minimize the gap by developing and validating a study model underpinned by Resource based view and Institutional theories, along with the Technology-Organization-Environment (TOE) framework in combination to convince firms to adopt green innovation. The study gathered data from 179 respondents using a survey distributed to manufacturing firms, after which data was exposed to Structural Equation Modeling (PLS-SEM) approach, for analysis. Based on the approach deliverables, all the integrated constructs of the model, namely perceived benefits, top management support, coercive pressure, normative pressure and mimetic pressure all predicted green management accounting practices. Moreover, green management accounting practices were found to directly and significantly affect green environmental performance. The developed integrated model provides a clear implication to decision-makers, indicating the importance of adopting and using green practices and innovative technologies for enhancing environmental performance. Based on the results from the reviewed advanced green technologies studies, there is considerable connection between green management accounting practices and environmental performance in the context of developing economies.

Keywords:

Environmental management accounting

; Environmental Sustainability

; green practices

; institutional pressure

; Resource-Based View

; Technology

; Organization-Environment Framework

1. Introduction

The dynamic evolution and growth of the industrial and corporate sectors in countries has led to environmental issues including augmented waste and toxins disposal, shortage of natural resource and mass amount of carbon and gas emissions that all poses as reasons behind the adverse climate changes albeit the organizations are only out to achieve their sustainability [1]. Such challenges can be addressed by the pursuant of green practices and innovative technologies in compliance with the organization’s social responsibilities. The observation around the globe evidences the establishment of regulatory policies that promote economic activity that is aligned with the sustainability of the environment, particularly among major manufacturing firms [2]. However, in the current times, focus has been laid on small and medium-sized enterprises (SMEs) and their promotion of businesses that are environmentally friendly. Current corporate stakeholders have intensified their awareness of environmental issues and corresponding solutions, leading to emphasis on environmental performance analysis and assessment among such establishments [3]. Firms’ threats to environmental sustainability has resulted in the development of processes that identify their effects on the environment and the increasing inclination towards sustainable products and services among customers along with the environmental legislation development has made firms turn to eco-friendly organizational policies practices to ensure that they remain competitive in the global marketplace [3,4].

In effect, green innovation is valuable to firms, particularly SMEs, and such value is attributed to such innovations ability to enhance their green environmental performance [5]. The use of green innovations properly ensures resource saving and mitigation of environmental pollution, and maintains balanced profitability and environmental responsibility [6,7]. Owing to the significant contribution of SMEs to national economies, their survival remains of great concern and because of their role as major economic pillars in majority of nations, SMEs need to be pro-active in enhancing their productivity and competitiveness (Lutfi et al., 2023). In this regard, what distinguishes successful SMEs from their unsuccessful counterparts is the former’s use of green practices and innovative technologies [8].

Therefore, enhancing global sustainability among SMEs and communities calls for the introduction of policies and the development of methodologies [9], among which is the adoption of green environmental management accounting system (EMAS) [10]. EMAS is basically referred to as instrument that facilitates the environmental performance management in firms and environmental information reporting to the entire stakeholders (internal and external) [3] It assists the corporate sector in identifying, gathering, and analyzing financial and non-financial environmental information towards enhancing the company’s achievement of financial and environmental performance. EMAS was conceptualized owing to the environmental challenges that traditional management accounting was not able to address. EMAS enables the implementation of different practices, including Energy Accounting (EA), Water Management Accounting (WMA), material flow accounting, biodiversity accounting and Carbon Management Accounting (CMA) towards enhanced financial and environmental performance [11]. It also enables companies to enhance their efficiency and manage environment via the control of energy consumption, natural resources, and costs of materials and their use, as well as, pollution, to formulate environmentally friendly decisions, enhanced quality, and competitiveness [12].

In fact, the adoption of EMAS is viewed as core component of the environmental management control system of the firm, involving the gathering of physical or financial data from the historical or future actions of the firm to present time-series trends for pursuing strategic operational and growth initiatives and objectives [13]. According to Asiaei et al., [1] the decision of a firm to manage its environment would involve the integration of accounting data and the environmental data and strategies and to this end, EMAS has been known to realize high corporate environmental performance. The objective of the firms is competitive advantage sustainability through the adoption of the environmental approach; for instance, the efficiency of firms can be enhanced through the elimination of contamination from the manufacturing processes (via minimal required input, short processes and compliant-related expenses and accountabilities control) [9]. To this end, literature has documented the increasing momentum of environmental accounting among firms in search of sustainability [14,15,16]. This may be attributed to the stakeholders demand that managers focus on evaluating their environmental issues and performance [3,9]. Optimum corporate environmental management and environmental strategies implementation, along with environmental management accounting (EMA) use has been viewed as the top competitive advantages among firms [17]. EMAS can support these strategies in that it grants a capability to businesses promoting green technologies [18,19]. A literature review highlights the key role of EMAS through integrating environmental considerations into their decision-making processes, leading to improved environmental performance and financial results [20,21,22]. However, little is known about the role of EMAS adoption in SMEs context. Further, regardless of the industry, the relationship between EMAS adoption and its impact on environmental performance remains poorly justified empirically. Kung et al. [23] found a direct influence of EMAS on environmental performance.

Nevertheless, although the benefits and significant importance of EMAS is widespread, its adoption level and implementation remain low among SMEs of emerging economies [24], and this holds true for Jordan. This explains the lack of empirical testing of the relationships of relevant factors, with literature urging for additional studies to shed light on the Jordanian situation in light of concepts and practices relating to sustainability [25]. Such lack of studies is related to the lack of knowledge and training, low awareness of the environmental issues and the ineffectiveness of professional bodies, lack of stakeholder pressure, ineffective environmental legislation, and the difficulties of firms in defining, categorizing, distinguishing, controlling and gauging environmental protection costs [3]. Hence, considering the low level of adoption and awareness of EMAS among SMEs, there is a need to determine the influencing factors on the system’s implementation and adoption among industry decision-makers. Literature reviewed concerning the topic have been conducted in industrial nations but remains lacking in developing ones, like Jordan. There have been past studies on the understanding and implementation of the concept, but none have so far addressed the environmental management practices adoption in Jordanian SMEs for environmental performance sustainability.

Therefore, this study is conducted under the motivation of the lack of empirical studies that are available concerning EMAS implementation and its role in enhancing environmental performance of firms [7], as majority of studies that related accounting to sustainability have mainly focused on corporate social disclosure [9,11] and the effects of eco-efficiency on the performance of firms [26,27], the relationship between environmental disclosure and firm performance [28,29], the extent of environmental disclosure [30] or the extend of financial performance of firms [10,31]. Reviews of literature from [3] indicated literature gaps that need addressing, which includes the managerial aspect of environmental accounting adoption and the role of EMAS, top management support and other factors in enhancing corporate greening practices. To the best of the author’s knowledge, intention to adopt EMAS among decision-makers has remained untouched in accounting literature and thus, the study aims to address this gap by developing and proposing a holistic EMAS adoption framework and assessing its implications based on the perspective of the organization. The study objectives are thus as follows;

- To determine the drivers of adopting EMAS and;

- To determine the effect of EMAS adoption on green environmental performance.

This study aims to answer the following questions: Do TOE factors influence the adoption of EMAS? And Does EMAS adoption influencing the green environmental performance? In this study, we developed a theoretical model based on integration of technology-organization-environment (TOE) framework, institutional theory, and resource-based view (RBV) theory; we also applied a Structural Equation Modelling (SEM) approach to evaluate the research questions. Thus, to achieve the aims and objectives of this study, earlier available knowledge is assessed in literature review for developing the hypothesis of the current research. After that, the rigorous methodology procedures are developed for conclusion the findings of this study. Findings were drawn later via applying advanced statistical technique, which is mentioned in the analysis section.

The contributions of this study to the existing literature are threefold. First, it extends the previous literature and interested researcher in green practices and innovative technologies context by validating the conceptual model in SMEs, in a country like Jordan. Notably, while earlier works tends to disregard the investigation the antecedents and impact of EMAS adoption [25,32], this research considers these relationships. This in turn would enrich and improve the theoretical understanding of such relationships and impact in the context of EMAS and green innovation. Secondly, the current research evaluates of the importance of the framework concerning EMAS practices in the context of manufacturing SMEs, in Jordan, an emerging nation. The findings of the study are expected to validate the environmental performance of businesses upon undertaking green innovation, which plays a key role in their effective and efficient running of daily processes and activities. Finally, the study has implications for developing economies, like Jordan, owing to the need to counter its vulnerability to the changes in the global environment and the lack of studies in literature that demonstrates the relevance of EMAS in day-to-day activities of businesses to enhance their green environmental performance.

The organization of the paper takes the following direction: in the next section, literature on the topic is reviewed based on which the hypotheses are formulated. This is followed by the presentation of the research method and the relevant techniques. The empirical results are then presented and discussed, after which their academic and practical implications are presented in detail.

2. Literature review

EMAS is a tool that can help businesses manage their environmental impacts while improving their financial performance. EMA involves identifying and quantifying the environmental costs and benefits associated with a company's operations and products and using this information to make more informed decisions. EMAS encapsulates the environmental and economic performance of firms via the development and implementation of proper and suitable environmental related accounting systems and practices [9]. The distinction between EMAS and conventional accounting approaches lies in the former’s ability to identify environmental information, measure environmental data, and interpret environmental information in financial statements, bringing forward the consideration of environmental aspects. Thus, EMAS adoption can lead to mitigated costs and better overall performance (financial and environmental) [10] and decrease the pressure of environmental regulations, while enhancing the reputation of the firm based on its environmental performance. Basically, EMAS entails the dealing with environmental information that affects the environment and improves the company’s performance, environmental and otherwise and the system can be categorized into two main areas, the monetary aspect, and the physical aspect [2,33]. The former has its basis on the firm’s environmental related activities expressed in monetary units, which present useful information to decision-making, whereas the latter has its basis on the natural environmental information, indicated in physical units [2]. Both information systems make sure that informed decisions are made by top management when it comes to enhancing the firm’s performance (environmental and economic).

More importantly, EMAS has been introduced as an extension of conventional management accounting, considering that accountants have been under pressure to adopt better environmental management and accounting practices. Thus, viewed as a part of environmental accounting, EMAS assists in identifying, classifying, allocating and controlling environmental costs, which results in informed decisions and environmental management, making it more effective than traditional management accounting systems [34]. Added to this, EMAS was originally developed to assist decision-making of managers when it comes to enhancing corporate environmental performance [10] and it is extensively utilized by firms to reap different types of benefits, including identifying cost savings opportunities, enhancing product pricing, and pricing decisions, enhancing environmental performance, more informed decision-making process and improved innovation [3,14]. Other benefits also include enhanced corporate reputation and better stakeholders’ decisions [9,27], staff retention, mitigated regulatory attention, and enhanced competitive advantage [35].

Notwithstanding the many benefits that can be obtained from EMAS adoption, empirical findings [15] indicated several barriers to such adoption. Most of these empirical findings stemmed from studies focused on emerging developing nations like Malaysia leaving others behind like Jordan, wherein which the topic remains unexplored in its entirety. Owing to the significant cultural, social, economic, and political differences among the countries which more often than not influence their accounting practices, it is safe to say that the findings from the developed or newly industrialized countries may not be suitable for their emerging developing counterparts [7]. Hence, more studies in developing nations could present a deeper insight of the adoption of EMAS in the current times. Lack of studies examining the EMAS practices and barriers level among firms in developing nations highlights a gap in accounting literature and to mitigate such a gap, this study examines the adoption level and the barriers that are EMAS related in the context of Jordanian firms.

3. Theoretical Understanding and Foundation

This study carries out an analysis of the EMAS adoption and value based on the organizational perspective. Past studies of this caliber have explored the subject based on two distinct approaches: first, focusing on the variables impacting innovation adoption decisions and second, focusing on the drivers and effects of innovation adoption.

To begin with, a literature review of the past relevant studies showed that TOE framework presents a valuable point from which the examination of innovation adoption can be initiated [36]. More specifically, the TOE framework is useful in identifying three categories of factors influencing the adoption via which the technologies are used by the firm, the first of which is the technological category. This category is described as the perceived attributes of the innovation to be adopted and according to Tornatizky and Fleischer [34], its top relevant, positive, and significant feature is perceived benefits, which this study examines. The organizational context is the second category, within which important variables constitute the quantity of internally available slack resources, with top management support found as the top determinant of innovation adoption. Moreover, the third category is the environmental context and for its in-depth understanding, scholars have integrated the TOE framework with other theories (e.g., institutional theory) to examine the relationship, with the latter theory providing factors of institutional environments that shape the structure, norms, and actions of the organization, like the adoption of innovation. Studies in this line made use of the theory and TOE framework to examine the environmental context [37].

A branch of study has also extended the TOE framework by including the influence of technology adoption on the basis of the RBV rationale which states that the creation of value by the firm is affected by its joining resources that are difficult for another firm to imitate owing to limited economical resources [38]. Added to this, the effect of resources lies more in the firm’s ability to use innovation rather than the innovation to be leveraged. In other words, the effect of the innovation depends on the level to which it is used in the firm’s principal value chain activities, in that the higher the level of use, the higher will be the probability of strong impact [39]. This notion has branched out to a stream of research that focuses on the antecedents and outcomes of the use of innovation [8,32].

On the whole, TOE has been the general framework used in past studies to shed light on the EMAS adoption drivers, whereas those that focused on the effects of EMAS adoption on environmental performance adopted the RBV theory.

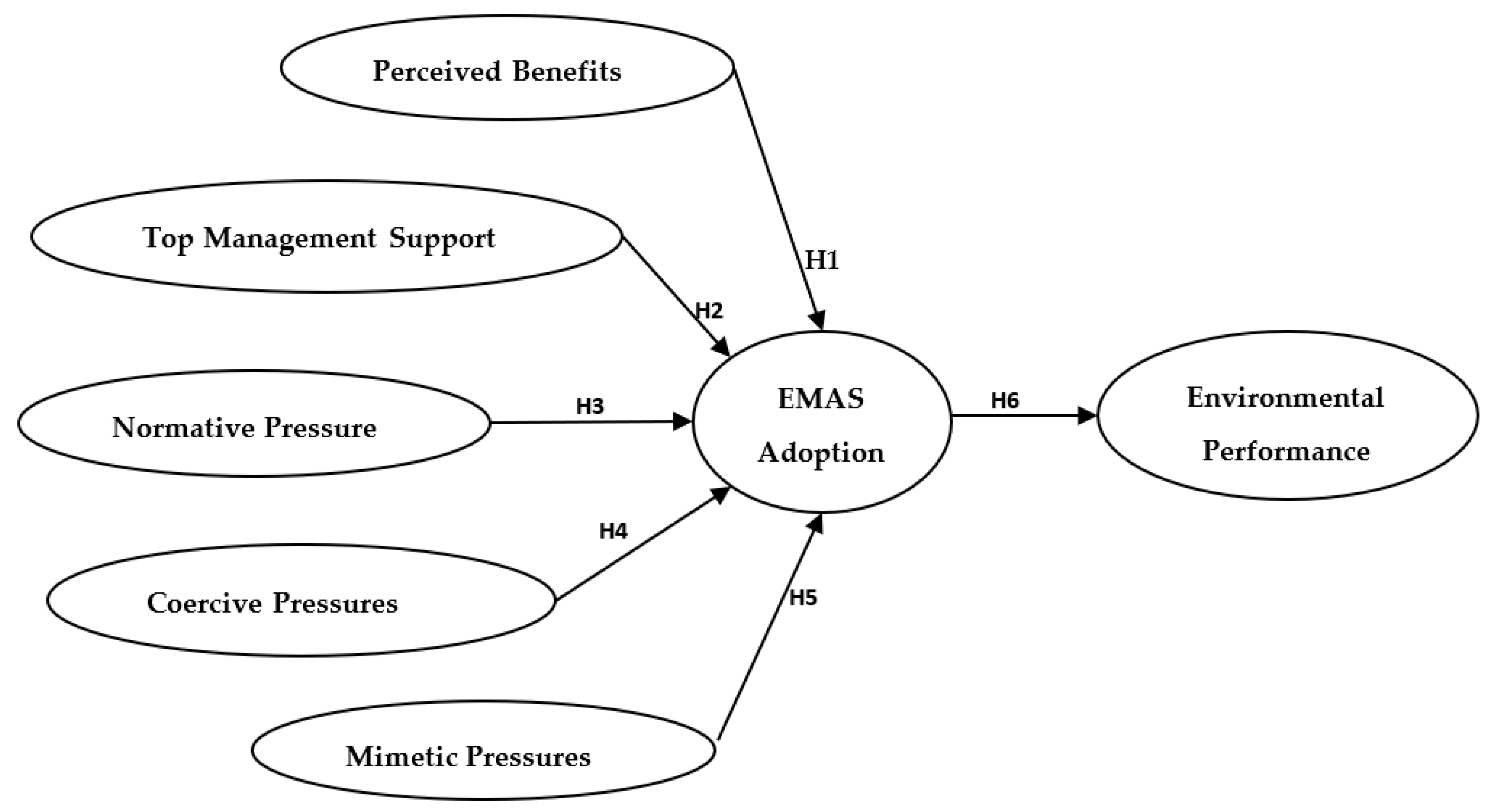

4. Research Model and Hypotheses

The proposed model is underpinned by the TOE framework and the RBV theory, which have been extensively used in the past innovation technologies adoption literature [5,8]. Moreover, the paper used the theories to view and assess EMAS adoption effects on SMEs in Jordan, and in so doing, the factors affecting such adoption in different contexts and the differences it makes on environmental performance can be discerned. Following a review of the relevant variables in literature, the study developed a model to be used as its guide (refer to Figure 1), which includes the following factor categories, technological factors, organizational factors, and environmental factors. All the contexts are examined in the coming sections based on which the hypotheses are formulated.

4.1. Perceived Benefits

One of the top innovation characteristics is perceived benefits and based on Brammer et al., [40] it is regarding the encapsulated benefits, particularly, the level of agreement with claimed benefits. Similarly, Kong et al., [23] described perceived benefits/usefulness as the level to which the firm or the individuals perceive that the system benefits them or is useful to them in enhancing their performance. Perceived benefits have a significant influence over the individual’s behavioral intention towards adopting and using a new system or technology [40]. Empirical findings indicate that perceived benefits significantly affect innovation adoption [23].

Stakeholders’ understanding of the benefits they can leverage from EMAS is crucial for their practical application and development of the system [3]. This reflects the relationship between the firm interests and social benefits, as well as the participation in the application of EMAS. Also, EMAS adoption assists firms through the provision of a more complete, accurate and inclusive data and information for performance measurement and for enhancement of the firm reputation, heightening of interactions with the other stakeholders and community, steering clear of possible fines, adhering with environmental law, obtaining compensation benefits, and addressing and resolving issues in the environment [3]. A firm ensures that its activities are aligned with societal requirements and with its social responsibility through the disclosure of its environmental information and its activities relating to its adaptation to the environment. In so doing, the company can receive several benefits and advantages in their operating process like building a strong business-societal trust, enhancing status and image, and achieving competitiveness.

As a result, if the firm is convinced that its adopted EMAS practices will benefit its enhancement of economic and environmental performance, then managers will focus more on EMAS adoption, which would result in heightened and optimum environmental performance and as such, this study proposes that:

H1:

Perceived benefit has a significant and positive relationship with EMAS adoption.

4.2. Top Management Support

This support translates to the level of active engagement, commitment and support from management when planning and using technological systems to ensure that they are used by the workers [32,41,42]. In this regard, decision-making is the role of the managers in SMEs and thus, they must be committed to its implementation through the use of available and proper resources so that the system use is successful and the barriers of natural resistance to use are tackled and resolved [43]. In a company that environmentally friendly, the dependence lies on management support and interest for ultimate enhanced productivity and competitiveness [3,9]. Achieving excellent environmental performance calls for involving the resources of the company with the inclusion of top management support, which is a planning process that integrates corporate strategy with environmental issues and EMAS implementation and use.

Furthermore, social community pressure, legal authorities monitoring, and environmental groups’ demands have forced organizations to carry out their environmental responsibility using standard environmental management and the transformation of the accounting system to suitable environmental information disclosure. Hence, the response and reception to new technology use and the changes that come with it are dependent on the perceived management needs. Prior literature revealed that the commitment and support of top management are both significant to environmental management practice success [9]. EMAS success/failure among firms hinges on the ability of management and administrators to support implementation.

In fact, the perception of management is considered as one of the top factors in EMA practice as highlighted in literature [3] owing to the influence of management on the policy choices and environmental strategies to be adopted in business activities. Therefore, the awareness of managers of the benefits and usefulness of EMAS practices would make a proactive and smooth implementation of an environmental strategy to furnish environmental information, mitigate operational costs and waste, and explore new markets and attract potential customers via green practices and products [3,44]. On the other hand, lack of environmental responsibility and active support from management for EMAS can be a barrier to its implementation and adoption [45]. According to past studies, innovation adoption and implementation depends on top management support in order so that technology use will be successful within SMEs. Such dependence makes the factor a major element in adopting EMAS [3,46]. Hence, this study proposes that:

H2:

Top management support has a significant and positive relationship with EMAS adoption.

4.3. Normative Pressure

Normative pressure is described as the influence stemming from firms running in the same industry (professionalism) or individuals in the same group [47] and is related with the trade associations, media, suppliers, clients, and other social actors for legitimate behavior. Additionally, trade associations as well as other unions are often viewed as the main sources of normative pressure, while customers and suppliers’ demands are viewed to influence the firm’s decision to act in a particular way. In connection to this, firms are often interested in the technologies and techniques that are viewed as effective in the communities within which they operate [48] as social players force business to make use of a specific technology/innovation because they are adopted by the businesses in the same industry.

Also, knowledge sharing of the usefulness of adopting a specific technology urges firms towards adoption intention and such sharing is possible through customer, supplier, trading agencies and firms’ networks [49]. More importantly, normative pressure makes sure that supplier and customer circles within the same exterior environment and organizations adhere to the social activities, which boosts the adoption of EMAS. Firms’ implementation of EMAS enables their management of public perception using practices of control and communication and as such, firms who fail to manage public perception and steer clear of trade unions, end up adversely affecting their image and reputation [2]. With damaged reputations, firms can lose their competitive advantage and incur losses [50]. In other words, the adoption of EMAS could affect the image, reputation, and competitive advantage of firms and thus, normative pressure is a significant predictor of technology adoption [37]. This study proposes the following hypothesis for testing:

H3:

Normative pressure has a positive and significant relationship with EMAS adoption.

4.4. Coercive Pressure

According to Di Maggio and Powell [51], coercive pressure is a regulatory compliance to the current regulations, main branches, and resource dominant firms. It is the pressure that powerful stakeholders exert, and this includes the government with their regulations and the non-government institutions like customers, competitors and suppliers – all of them pressure the firms to adhere to and adopt environmental standards and regulations [2]. Based on the institutional theory, coercive pressure can form the legislative mandates and environmental protection among firms, and based on [50] empirical study, regulatory forces and competitors significantly influence the adoption of innovation. Also, in their investigation of the cloud-based accounting system adoption, [37] revealed that coercive pressure (CP) has a significant influence on the decision-making of management. In the same way, majority of government authorities establish conditions to motivate firms towards EMAS adoption via coercive pressure and when this happens, EMAS is adopted to enhance the firms’ environmental performance and obtain government support and economic paybacks, while the social reputation of the firm is enhanced. In the Jordanian context, government pollution standards and laws concerning pollution incidents have been established in a way that manufacturing companies are motivated towards EMAS practices adoption.

Also, on the basis of the INS theory and innovation adoption literature on SMEs, governmental policies incentivize SMEs decisions towards adoption through environmental pressure/driving force that has a positive and significant relationship with such decision – this is the same way as CP in INT theory. Added to this, the government-established policies concerning different promotional initiatives/rules are pursuant to EMAS adoption, and ultimately its institutionalized adoption [9]. Hence, it is indicated that CP multiplicity from many sources can have a significant influence over the adoption of EMAS and the opposite way holds true. On the basis of the above discussion, this study proposes that:

H4:

Coercive pressure has a positive and significant relationship with EMAS adoption.

4.5. Mimetic Pressure

According to Di Maggio and Powell [51], mimetic pressure is an institutional factor that refers to the ambiguous goals and misunderstood technologies that direct firms’ capitalization on external experience via modeling after rivals who are successful. More specifically, firms often relate their rivals’ successes to their strategic choices, which would lead to imitating their behaviors and actions when it comes to practices and conduct in the hopes of preserving shares in the market and continuing their survival [50]. Hence, despite the lack of justification of such imitation in light of efficiency, a firm may still be driven by mimetic forces to steer clear of perceived risks and to mitigating trialing costs that early adopters carry [14,52].

The above logic can be juxtaposed to SMEs adoption decisions when it comes to EMAS. In other words, upon learning of their rivals leveraging EMAS benefits, they feel mimetic pressure and may imitate the former. Also, considering the risks surrounding the adoption of EMAS, direct exploration of the values and outcomes of the system may be costly or impossible for firms and thus, to cut costs or mitigate experimentation costs, they may rather be driven by mimetic pressure towards adopting the innovation [37]. Literature evidenced that higher pressure is felt by organizations when they see others like them in the industry and environment who employ innovation are successful and thus, they feel the need to be like them to ensure their competitive sustainability [2].

Past literature and INT show that mimetic pressure stemming from competitor firms has a significant influence over innovation adoption; for instance, [2] revealed that mimetic pressure from rival firms has a significant relationship with intention towards adopting environmental information systems. Additionally, mimetic pressure was gauged by the perceived success of rival adopters and the level of adoption among competing firms [49]. Even though past works on EMAS adoption have not applied INT, some of them showed that adopting EMAS in SMEs had been highly driven by competitive pressure (i.e., mimetic pressure). This is exemplified by [8] and their study on using AIS – their findings showed that SMEs realization that others in the same chain use innovation in their operations urges them to do the same. Hence, based on the INT theory and past studies on adopting innovation, EMAS may be subject to rival mimetic pressure and therefore, this study proposes that:

H5:

Mimetic pressure has a positive and significant relationship with EMAS adoption.

4.6. EMAS and Environmental Performance

Environmental performance refers to the result that reflects the commitment of the firm to maintain the natural environment [53]. It is evaluated through pollution control, waste reduction, lower environmental emissions, and recycling activities [54]. EMAS use and implementation effectiveness allow managers and decision-makers in SMEs to limit the level of environmental issues and problems by addressing and resolving them through current information culled from sources (both external and internal) [55]. Through EMAS provision of supporting data at the opportune time managers can mitigate external anomalies occurrences and their effect on management knowledge of environmental dynamics, only to reap the environmental benefits and understand what their responsibilities to the environment are [19,41,56]. EMAS also brings about decision-making as it gathers relevant information about the reliance of the firm on energy and its role in intensifying harmful carbon emissions that result from the consumption of energy [1,19,24]. As a result, the environmental management strategies and financial control come into play in environmental management control system and therefore, the integration of EMAS can assist firms in achieving environmental quality and performance. Such IT may also bring in profitability for the firm through the increasing ecological demands and opportunities to improve environmental practices using accounting information processes that are effective.

Furthermore, EMA facilitates the measurement, control, and disclosure of business environmental performance [54]. This paper aims to test a conceptual framework that describes the relationship between environmental strategy, environmental management accounting and environmental performance. In this paper, the authors argue that environmental strategy can directly influence environmental performance through environmental management Accounting, Management and Policy [10,54], with its environmentally friendly practices and tools, which is why it has a significant impact on the performance of businesses [57]. The higher the level of EMAS adoption, the higher will be the level of control and decision-making effectiveness generated from reliable, updated, actual and integrated information that are useful for enhanced environmental performance [41,54]. Empirical findings evidenced the positive influence of adopting EMAS on environmental performance Erauskin-Tolosa et al., [20]. EMAS studies however only examined the relationship in Western nations leaving the developing nations like Jordan far behind in terms of research. This study proposes that:

H6:

EMAS adoption has a positive and significant relationship with environmental performance.

5. Methodology

5.1. Instruments

A thorough review of literature supports this study’s adoption of a structured, closed-ended questionnaire with 8 sections – in the first section, the respondents’ demographical information is obtained, while the second section up to the eighth one are dedicated to measuring the items of the constructs (perceived benefits, top management support, mimetic pressure, coercive pressure, normative pressure, EMAS adoption, and environmental performance). The validity of the questionnaire was tested by piloting the study on 40 individuals, after which a large-scale survey was carried out. The items measuring the constructs were measured through a 5-point Likert scale ranging from strongly disagree (1) to strongly agree (5).

5.2. Sample and Data Collection Method

This study’s objective was achieved by adopting a quantitative approach, using questionnaire survey to gather primary data from manufacturing SMEs in Jordanian cities of Amman, Zarqa and Irbid, as they have the highest proportion of SMEs of all sectors. Manufacturing enterprises in Jordan are categorized based on their employees’ number and the annual revenue they bring in. Based on the Amman Chamber Industry, enterprises that employ 1-9 full-time employees are called micro enterprises and the majority of them are cottage and handicraft type industries with low effect on the environment. This study excluded this category of enterprises. The next enterprise category is small enterprises which employ between 10 and 49 full-time employees, and then the medium-sized enterprises which employ between 50 and 249 full-time employees [58]. SMEs contribute 35% to the GDP and employ approximately 28% of the labor force in Jordan [37,50,59,60]. This makes them have a key role in the region’s broader economic policy. The study drew samples of SMEs from various manufacturing sectors using a simple random sampling method. A total of 8000 manufacturing SMEs exist out of which 941 match the definition of SMEs considered in this study.

The process of collecting data for a research study entails several steps, including the identification of the target audience, selection of sampling method, determination of sample size, and selection of sample factors. The appropriate size of the sample depends on various factors, such as the chosen regression model processing method and required reliability. For exploratory factor analysis (EFA), the recommended sample size is typically four to five times the number of variables in the analysis [61]. However, practical research applications often require a larger sample size of more than 150 units [62]. In multiple regression analysis, a commonly used formula for determining the minimum sample size (n) is that it should be higher than 50+8p, where p is the number of independent variables included in the model [63].

In this study, a sample of 500 questionnaires was distributed using online means (email and Google-form URL) to different small and medium-sized enterprises (SMEs). A larger sample size was chosen to avoid potential issues during data collection, such as low response rates, non-engagement of participants, and missing values. Prior to the survey, participants were informed about the nature and objectives of the research and given the option to drop out at any time. Of the 500 questionnaires distributed, 196 were returned, and data were examined for outliers and non-engaged responses. This involved calculating and recording the standard deviation value of each respondent's answers. Respondents who consistently answered all or most questions with the same answer or pattern were considered non-engaged. Based on this examination, 17 responses were dropped as they had a standard deviation lower than 1 (SD≤1), leaving 179 valid responses, reflecting a response rate of 35.8%.

5.3. Constructs Measures

This quantitative research method used a closed-ended questionnaire survey for collection of data, with the variables measured using multiple-item scales. There were 30 items in the questionnaire that are constructs related. Perceived benefits was measured by four items adopted from [23], TMS was measured by four items adopted from [23], while mimetic, coercive and normative pressure were measured by four items adopted from [2]. Moreover, six item scale was used to measure EMAS adoption and they were taken from [2] and lastly, environmental performance measurement items were four in number, and they were adopted from [64].

The questionnaire survey was the main tool for data collection while the metrics were obtained from prior literature and interviews with 8 professionals from the enterprises. The measures were originally in English but were translated into Arabic and back translated into English to minimize measures validity issues. Based on the interviews with the professionals, the phrasing of the items was modified to make sure that the items matched the business environment in Jordan. The questionnaire items are tabulated in Table 1.

6. Data Analysis

The PLS-SEM approach, which is a multivariate statistical method that allows for the evaluation of multiple variables in one model at the same time, was used for analysis of data. The approach efficiently works even with complex models that involve many latent variables, with moderating variables and with lower-sized samples [65]. On the basis of the above, this study preferred PLS over other methods for data analysis. The proposed model involves moderating variable, which added to its complexity and the size of the sample is relatively small (179) – it is less than the threshold values required for other techniques. Lastly, this explorative study is underpinned by the TOE, INST and RBV theories. A combination that calls for a path modeling approach as several studies indicated that if a study is oriented towards prediction or if it is an extension of an existing theory, then the appropriate approach to be used is PLS-SEM [65].

7. Results

7.1. Assessment of the Measurement Model

According to the recommendation forwarded by [65], the measurement model/outer model’s measurement is a major step in the PLS-SEM as it determines the reliability or lack thereof of the indicator constructs. Unreliable constructs could prevent the evaluation of the structural model/inner model. The measurement model evaluation therefore entails determining the construct item’s reliability and validity.

The relevant indicators representing the measurement model are tabulated in Table 2, and from the table, data supports the reliability and validity of the values that are did not breach any threshold for Cronbach’s alpha, composite reliability, and average variance extracted, which are 0.70, 0.70 and 0.5 respectively [65]. The entire items showed had good convergent and discriminant validities as the loadings of the factors on their respective constructs exceeded 0.40 – a condition explained by [65]. Also, the study used Fornell-Larcker criterion to establish the constructs discriminant validity by comparing the squared AVEs with the construct’s correlation coefficients.

Based on the data displayed in Table 3, the squared AVEs on the diagonal space exceeded the values of the correlation coefficients between the constructs, indicating the constructs discriminant validity. Upon taking into account all the indicators, it can be concluded that the measurement model achieved the requirements for convergent validity, discriminant validity and reliability at two levels, namely item and construct. Hence, the study proceeded with the hypotheses testing in the structural model assessment.

5.2. Assessment of the Structural Model

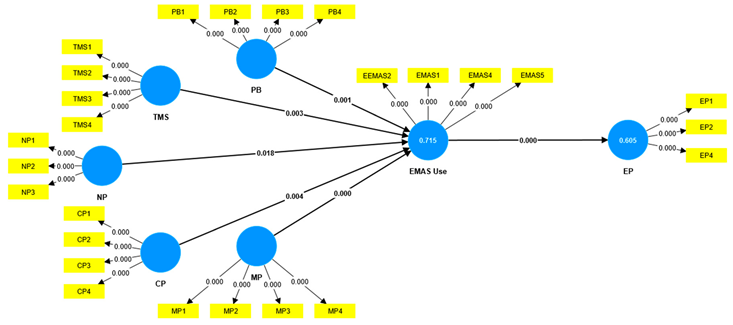

The study applied the PLS algorithm and bootstrapping test using 5000 resamples to determine the path coefficients level and significance for the formulated hypotheses. The standardized path coefficients (β-values), critical ratios (t-values) and p-values (with supported hypotheses) of every hypothesized relationship are presented in Table 4. Of the six developed hypotheses, all were supported at 90-95% confidence levels.

Table 4.

Result of Hypotheses Testing of the Direct Relationship Model.

| Hypothesis No. | Relationship | Path coefficient | STDEV | T –Value | P - Value | Supported |

|---|---|---|---|---|---|---|

| H1 | PB → EMAS U | 0.153 | 0.046 | 3.350 | 0.001*** | Yes |

| H2 | TMS → EMAS U | 0.184 | 0.061 | 2.992 | 0.003** | Yes |

| H3 | NP → EMAS U | 0.105 | 0.045 | 2.359 | 0.018* | Yes |

| H4 | CP → EMAS U | 0.161 | 0.055 | 2.917 | 0.004** | Yes |

| H5 | MP → EMAS U | 0.509 | 0.054 | 9.343 | 0.000*** | Yes |

| H6 | EMAS U → EP | 0.778 | 0.037 | 21.218 | 0.000*** | Yes |

Note: Significant at * p < 0.05, ** p < 0.01, and *** p < 0.001.

8. Discussion and conclusion

The primary aim of this study is to explore the operational dimensions of Technology-Organization-Environment (TOE) framework that can enhance the implementation of Eco-Management and Audit Scheme (EMAS), and its impact on environmental performance. The research employs the TOE, institutional, and resource-based view (RBV) theories to analyze the manufacturing SMEs operating amidst a constantly changing business environment while striving to remain competitive. The study reveals that the adoption of EMAS has a significant and positive influence on environmental performance. However, the moderating effect of green innovation is negative and significant in the relationship between EMAS implementation and environmental performance. Moreover, the study shows that TOE dimensions such as perceived benefits, top management support, coercive pressure, normative pressure, and mimetic pressure have a positive and significant impact on EMAS adoption. The integrated theories applied in this study provide insight into the factors affecting EMAS adoption among manufacturing SMEs. The positive influence of TOE factors on EMAS adoption emphasizes the necessity for SMEs to adopt EMAS for achieving environmental goals.

In the context of TOE constructs, Phan et al. [66] highlight the crucial role of perceived benefits as a tool for fostering collaboration among employees and enhancing departmental performance within organizations. The adoption of EMAS is more likely to occur when managers perceive its benefits. From an accounting perspective, the benefits that the accounting department derives from implementing EMAS can extend to other departments within the business. By facilitating environmental responsibilities and meeting societal requirements, EMAS can engender community trust in the business, improve its image, and bolster its competitive position. These findings are consistent with those of previous studies [67,68,69].

Furthermore, this study confirms the positive influence of top management support on EMAS adoption, which has been documented in prior research [23,59,67]. Top management support empowers companies to adopt green innovative technologies and generate green products by leveraging digital manufacturing tools and technologies [57]. Managers and business operators, who are at the forefront of the decision-making process concerning technology adoption, develop strategies and make decisions for achieving sustainable development goals. Thus, their recognition of the benefits of EMAS can accelerate its adoption throughout the organization. Management and business operators should leverage the benefits of EMAS, such as proactive environmental strategy, provision of accurate information, reduced operational costs, new market exploitation, and attraction of potential consumers via green products.

In addition, the three components of institutional pressure, namely coercive pressure, normative pressure, and mimetic pressure had a positive and significant relationship with EMAS adoption, as per the findings. This implies that firms experiencing higher levels of pressure from all three components are more likely to adopt EMA in order to establish a legitimate and solid relationship with their stakeholders [2,14]. Government-enforced regulatory policies, standards, and regulations on firms are primarily focused on companies that neglect the natural environment. As a result, the government's significant role in environmental protection has a substantial influence on the behavior and decision-making processes of firms. Similarly, parent firms set policies and rules for data management, resources management, and environmental management. The commitment to such policies and rules would penalize unyielding firms, negatively impacting their reputation and overall performance. These findings correspond with earlier research that signify the importance of coercive pressure in the adoption processes of EMAS and other technologies among Small and Medium-sized Enterprises (SMEs) [9,37,52].

More specifically, mimetic pressure, according to the results, has a positive significant effect over EMAS adoption, which means that if the rival firm adopts new technologies, focal firms would be pressurized to do the same to remain in competition. The finding receives considerable support in former research which reported critical association between mimetic pressure and EMAS adoption [14,49,52]. This mimicking of the rival technology adoption mitigates the risks of failure and more accurately, in today’s technological advancement era, it is advantageous to maintain a competitive edge over rival entities. Prior research has demonstrated the significant influence exerted by mimetic pressure on behavioral dynamics, particularly those implicated in intricate and comprehensible adoption processes [23]. Conversely, when a firm's adoption of EMAS has already attained a high level, the impact of mimetic pressure tends to diminish.

In the context of small and medium-sized manufacturing enterprises (SMEs), normative pressure has been identified as a significant driver for the adoption of the EMAS. A primary objective of such firms is to satisfy customer demand, and the adoption of technological innovations is a means of achieving this aim. The present study finds that normative pressure has a positive impact on the adoption of EMAS among SMEs in the manufacturing sector. These findings are consistent with prior research, which has established a positive relationship between institutional isomorphism and technology adoption [2,23,35,49].

The present study has demonstrated a statistically significant positive relationship between the adoption of EMA and a firm's environmental performance. This finding is consistent with prior research that has reported a substantial link between environmentally friendly practices and environmental performance [1,10]. The results suggest that effective use of EMA can facilitate firm control and informed decision-making, leading to positive outcomes and improved environmental performance [54]. In particular, engagement with EMAS enables managers to make informed decisions about environmental matters, enhancing their efficiency and accuracy while minimizing resource wastage and preventing environmental pollution [70]. Therefore, firms that prioritize environmental practices are more likely to concentrate on green resources to achieve better overall performance, including environmental performance [71]. This aligns with the Resource-Based View theory and earlier studies' assertions that specific strategies or resources can enhance a firm's environmental performance [72,73], thus making EMA adoption an attractive option. Overall, this study highlights the efficacy of EMA as a tool for quantifying environmental-related issues and facilitating decision-making. It also emphasizes the potential benefits of adopting EMAS, such as gaining a competitive advantage, reducing costs, improving operational efficiency, increasing revenues, and enhancing corporate environmental performance.

9. Implications

9.1. Theoretical Implications:

This study has several implications for literature. Firstly, the development of an innovation adoption model based on the integration of TOE framework, INS and RBV theory, which is validated and provides new correlations to examine in the green practices, EMAS and management accounting fields. To the best of the author’s knowledge, this is a pioneering study when it comes to examining EMAS adoption using decision-making factors in Jordan, an emerging nation. Secondly, the study also extends past studies concerning the exploration of the adoption of green innovation practices, which has been until now limited to adoption rather than the overall effect of such adoption. The integration of TOE, institutional theory and RBV in one model to examine the phenomenon under study also increases the explanatory and predictive powers of both models and generates findings that have implications to practitioner and academic circles.

9.2. Practical Implications:

The results of this study also are expected to have implications on managers, industry leaders, government agencies, policymakers and other relevant stakeholders who are concerned with the lagging behind of SMEs in Jordan when it comes to EMAS implementation. Firstly, the significant role of the examined factors could urge the awareness of businesses to the current regulatory rules, policies, and regulations regarding the adoption of EMAS. Secondly, in a similar manner, training institutions and professional entities can introduce campaigns to promote the awareness of EMAS benefits and advantages in congruence with the firm’s corporate responsibilities. Also, seminars can be held to discuss environmental issues, provide short-term training courses in accounting and auditing as well as to conduct program visits for the introduction of EMAS adoption and for the promotion of awareness among firms concerning the connection between green innovation and environmental performance. Thirdly, viewed from the government perspective, policymakers can play a key role in the formulation and design of legal documents that regulate the implementation of EMAS and other innovative technologies among firms. Regulations on how to disclose or encourage business to disclose information of their green practices, taxes, and environmental violations penalties should be made clear. Firms need to coordinate and collaborate with innovation consultants and advisers from SMEs to organize training courses on environmental protection and environmental accounting for support and guidance towards long-term business orientations and adopted strategies to support environmental regulations and standards. Finally, the proposed and validated model could be useful for SME managers to identify the drivers of EMAS adoption and the influence of such adoption on the firms’ environmental performance. Finally, the model assists in focusing on the distinct effects of such adoption on previously ignored green environmental performance.

10. Limitations and Recommendations for Future Studies

This study possesses certain limitations and offers potential avenues for future research. Firstly, the cross-sectional data collected in the Jordanian context, while illuminating causal relationships between variables, may not fully represent the proposed model and may therefore be inadequate for a comprehensive assessment of causal relationships. To mitigate this limitation and avoid bias, future studies may incorporate longitudinal designs to enhance the validation and accuracy of findings. Consequently, it would be constructive to validate the present study's findings with data from other countries such as Saudi Arabia, Kuwait, and Qatar. Additionally, the sample size and regions involved in this study were limited; future studies may broaden the range of regions and increase the sample size to improve the generalizability of the findings.

Secondly, while the study focuses on manufacturing SMEs, it would be beneficial to include non-manufacturing and services SMEs in future research. This is because such businesses also interact with the natural environment, albeit indirectly. Including them would provide a more comprehensive understanding of how different types of SMEs implement EMAS. Furthermore, the study's sample size is limited to a specific industry and location. To gain a broader perspective and compare results, it may be advantageous to extend the sample to include other industries and nations. This would enable researchers to identify any patterns or trends in EMAS implementation across various contexts and assess the effectiveness of the program in different settings. Overall, by including non-manufacturing and services SMEs in future research and expanding the sample to encompass other industries and nations, researchers can gain a more nuanced understanding of EMAS implementation and its impact.

Thirdly, this study examined the impact of selected TOE variables on the adoption of EMAS and its influence on environmental performance. While this study provides a valuable insight into the relationship between these variables, there may be other factors that can also impact these outcomes. Future studies could consider other internal and external TOE variables in addition to those already analyzed in the current study. These variables may include aspects like organizational culture, leadership style, market competition, and regulatory frameworks. By considering a broader range of variables, researchers can obtain a more comprehensive understanding of the factors that influence SMEs' adoption of EMAS and its impact on their financial, social, and environmental sustainability. Moreover, future research studies may explore combining the TOE model with other theories or models like diffusion of innovation theory, Unified Theory of Acceptance and Use of Technology (UTAUT), or Delone & McLean model for more nuanced implications. For instance, the diffusion of innovation theory examines how innovations are adopted and diffused over time, and it may provide insights into the stages of adoption of EMAS by SMEs. The UTAUT model looks at the factors that influence individuals to use technology, and it could provide insights into why SMEs adopt EMAS. The Delone & McLean model focuses on the impact of information systems on organizations, and it could provide insights into how EMAS impacts SMEs' overall operational efficiency and effectiveness. Incorporating these additional theories or models would enable researchers to gain a more sophisticated understanding of the complex relationship between the adoption of EMAS, its impact on an SME's environmental performance, and the broader implications for its financial and social sustainability.

The authors of the study conducted quantitative research by analyzing survey responses and using SEM-PLS analysis. This approach helped them gain a better understanding of the phenomenon under investigation. However, to delve deeper into the topic, future research could include qualitative methods such as conducting semi structured interviews with owners or managers. These interviews could provide valuable insights into the drivers and antecedents of EMAS, including technological and managerial capabilities. Furthermore, the authors only discussed the direct effects of variables in their study. Other variables may have different effects or act as mediators in the relationship between the variables studied. Therefore, future studies should investigate these effects to provide comprehensive and enriching research. Such research would be crucial in providing a more detailed understanding of the phenomenon and its impact on various stakeholders. Ultimately, it could help policymakers and business owners make informed decisions that align with environmental sustainability goals.

Funding

This research was funded by the Deanship of Scientific Research at King Faisal University, grant no. GRANT3202.

Acknowledgments

The author acknowledges the Deanship of Scientific Research at King Faisal University for their financial support under grant no. (GRANT3202).

Conflicts of Interest

The author declares no conflict of interest.

References

- Asiaei, K.; Bontis, N.; Alizadeh, R.; Yaghoubi, M. Green Intellectual Capital and Environmental Management Accounting: Natural Resource Orchestration in Favor of Environmental Performance. Bus. Strategy Environ. 2022, 31, 76–93. [Google Scholar] [CrossRef]

- Latif, B.; Mahmood, Z.; Tze San, O.; Mohd Said, R.; Bakhsh, A. Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability 2020, 12, 4506. [Google Scholar] [CrossRef]

- Nguyen, T.H. Factors Affecting the Implementation of Environmental Management Accounting: A Case Study of Pulp and Paper Manufacturing Enterprises in Vietnam. Cogent Bus. Manag. 2022, 9, 2141089. [Google Scholar] [CrossRef]

- Iqbal, Q.; Ahmad, N.H.; Li, Z. Frugal-Based Innovation Model for Sustainable Development: Technological and Market Turbulence. Leadersh. Organ. Dev. J. 2021. [Google Scholar] [CrossRef]

- Idris, K.M.; Mohamad, R. The Influence of Technological, Organizational and Environmental Factors on Accounting Information System Usage among Jordanian Small and Medium-Sized Enterprises. Int. J. Econ. Financ. Issues 2016, 6, 240–248. [Google Scholar]

- Normal, I.N.; Setini, M. Absorption Capacity and Development of Photocatalyst Green Ceramic Products with Moderation of Green Environment for Sustainability Performance of Developing Industries. Sustainability 2022, 14, 10457. [Google Scholar] [CrossRef]

- Wasiq, M.; Kamal, M.; Ali, N. Factors Influencing Green Innovation Adoption and Its Impact on the Sustainability Performance of Small- and Medium-Sized Enterprises in Saudi Arabia. Sustainability 2023, 15, 2447. [Google Scholar] [CrossRef]

- Idris, K.M.; Mohamad, R. AIS Usage Factors and Impact among Jordanian SMEs: The Moderating Effect of Environmental Uncertainty. J. Adv. Res. Bus. Manag. Stud. 2017, 6, 24–38. [Google Scholar]

- Chen, X.; Weerathunga, P.R.; Nurunnabi, M.; Kulathunga, K.M.M.C.B.; Samarathunga, W.H.M.S. Influences of Behavioral Intention to Engage in Environmental Accounting Practices for Corporate Sustainability: Managerial Perspectives from a Developing Country. Sustainability 2020, 12, 5266. [Google Scholar] [CrossRef]

- Deb, B.C.; Rahman, Md.M.; Rahman, M.S. The Impact of Environmental Management Accounting on Environmental and Financial Performance: Empirical Evidence from Bangladesh. J. Account. Organ. Change 2022. [CrossRef]

- Dissanayake, K.; Rajapakse, B. Environmental Management Accounting for Corporate Sustainability: A Case from a Sri Lankan Automobile Company. Int. J. Audit. Account. Stud. 2020, 2, 41–65. [Google Scholar]

- Shahzad, M.; Qu, Y.; Rehman, S.U.; Zafar, A.U. Adoption of Green Innovation Technology to Accelerate Sustainable Development among Manufacturing Industry. J. Innov. Knowl. 2022, 7, 100231. [Google Scholar] [CrossRef]

- Mukwarami, S.; Nkwaira, C.; van der Poll, H.M. Environmental Management Accounting Implementation Challenges and Supply Chain Management in Emerging Economies’ Manufacturing Sector. Sustainability 2023, 15, 1061. [Google Scholar] [CrossRef]

- Al-Tamimi, S.A. Towards Integrated Management Accounting System for Measuring Environmental Performance. 2022.

- Javed, F.; Yusheng, K.; Iqbal, N.; Fareed, Z.; Shahzad, F. A Systematic Review of Barriers in Adoption of Environmental Management Accounting in Chinese SMEs for Sustainable Performance. Front. Public Health 2022, 10, 832711. [Google Scholar] [CrossRef]

- Mohd Fuzi, N.; Habidin, N.F.; Janudin, S.E.; Ong, S.Y.Y.; Ku Bahador, K.M. Environmental Management Accounting Practices and Organizational Performance: The Mediating Effect of Information System. Meas. Bus. Excell. 2019, 23, 411–425. [Google Scholar] [CrossRef]

- Ha, V.T. Factors Affecting The Implementation Of Environmental Management Accounting In Manufacturing Enterprises: Evidence From Vietnam. J. Posit. Sch. Psychol. 2022, 6, 1–17. [Google Scholar]

- Iqbal, Q. The Era of Environmental Sustainability: Ensuring That Sustainability Stands on Human Resource Management. Glob. Bus. Rev. 2020, 21, 377–391. [Google Scholar] [CrossRef]

- Iqbal, Q.; Ahmad, N.H.; Li, Z.; Li, Y. To Walk in Beauty: Sustainable Leadership, Frugal Innovation and Environmental Performance. Manag. Decis. Econ. 2022, 43, 738–750. [Google Scholar] [CrossRef]

- Erauskin-Tolosa, A.; Zubeltzu-Jaka, E.; Heras-Saizarbitoria, I.; Boiral, O. ISO 14001, EMAS and Environmental Performance: A Meta-Analysis. Bus. Strategy Environ. 2020, 29, 1145–1159. [Google Scholar] [CrossRef]

- Kong, Y.; Javed, F.; Sultan, J.; Hanif, M.S.; Khan, N. EMA Implementation and Corporate Environmental Firm Performance: A Comparison of Institutional Pressures and Environmental Uncertainty. Sustainability 2022, 14, 5662. [Google Scholar] [CrossRef]

- Ema, 2022.Pdf.

- Kong, Y.; Javed, F.; Sultan, J.; Hanif, M.S.; Khan, N. EMA Implementation and Corporate Environmental Firm Performance: A Comparison of Institutional Pressures and Environmental Uncertainty. Sustainability 2022, 14, 5662. [Google Scholar] [CrossRef]

- Daddi, T.; Todaro, N.M.; Marrucci, L.; Iraldo, F. Determinants and Relevance of Internalisation of Environmental Management Systems. J. Clean. Prod. 2022, 374, 134064. [Google Scholar] [CrossRef]

- Saleh, M.M.A.; Jawabreh, O.A.A. ROLE OF ENVIRONMENTAL AWARENESS IN THE APPLICATION OF ENVIRONMENTAL ACCOUNTING DISCLOSURE IN TOURISM AND HOTEL COMPANIES AND ITS IMPACT ON INVESTOR’S DECISIONS IN AMMAN STOCK EXCHANGE. Int. J. Energy Econ. Policy 2020, 10, 417–426. [Google Scholar] [CrossRef]

- Khan, M.A. ESG Disclosure and Firm Performance: A Bibliometric and Meta Analysis. Res. Int. Bus. Finance 2022, 61, 101668. [Google Scholar] [CrossRef]

- Puertas, R.; Guaita-Martinez, J.M.; Carracedo, P.; Ribeiro-Soriano, D. Analysis of European Environmental Policies: Improving Decision Making through Eco-Efficiency. Technol. Soc. 2022, 70, 102053. [Google Scholar] [CrossRef]

- Carnini Pulino, S.; Ciaburri, M.; Magnanelli, B.S.; Nasta, L. Does ESG Disclosure Influence Firm Performance? Sustainability 2022, 14, 7595. [Google Scholar] [CrossRef]

- Chouaibi, S.; Rossi, M.; Siggia, D.; Chouaibi, J. Exploring the Moderating Role of Social and Ethical Practices in the Relationship between Environmental Disclosure and Financial Performance: Evidence from ESG Companies. Sustainability 2021, 14, 209. [Google Scholar] [CrossRef]

- Wu, S.; Li, Y. A Study on the Impact of Digital Transformation on Corporate ESG Performance: The Mediating Role of Green Innovation. Sustainability 2023, 15, 6568. [Google Scholar] [CrossRef]

- Naranjo Tuesta, Y.; Crespo Soler, C.; Ripoll Feliu, V. Carbon Management Accounting and Financial Performance: Evidence from the European Union Emission Trading System. Bus. Strategy Environ. 2021, 30, 1270–1282. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 2022, 14, 5362. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Othman, M.S.H.; Saeidi, P.; Saeidi, S.P. The Moderating Role of Environmental Management Accounting between Environmental Innovation and Firm Financial Performance. Int. J. Bus. Perform. Manag. 2018, 326–348. [Google Scholar] [CrossRef]

- Ismail, M.S.; Ramli, A.; Darus, F. Environmental Management Accounting Practices and Islamic Corporate Social Responsibility Compliance: Evidence from ISO14001 Companies. Procedia - Soc. Behav. Sci. 2014, 145, 343–351. [Google Scholar] [CrossRef]

- Xu, N.; Fan, X.; Hu, R. Adoption of Green Industrial Internet of Things to Improve Organizational Performance: The Role of Institutional Isomorphism and Green Innovation Practices. Front. Psychol. 2022, 13, 917533. [Google Scholar] [CrossRef]

- Tornatzky, L.; Fleischer, M. The Process of Technology Innovation, Lexington, MA 1990.

- Alshirah, M.; Lutfi, A.; Alshirah, A.; Saad, M.; Ibrahim, N.; Mohammed, F. Influences of the Environmental Factors on the Intention to Adopt Cloud Based Accounting Information System among SMEs in Jordan. Accounting 2021, 7, 645–654. [Google Scholar] [CrossRef]

- Lutfi, A.; Alsyouf, A.; Almaiah, M.A.; Alrawad, M.; Abdo, A.A.K.; Al-Khasawneh, A.L.; Ibrahim, N.; Saad, M. Factors Influencing the Adoption of Big Data Analytics in the Digital Transformation Era: Case Study of Jordanian SMEs. Sustainability 2022, 14, 1802. [Google Scholar] [CrossRef]

- Zhu, K.; Kraemer, K.L.; Xu, S. The Process of Innovation Assimilation by Firms in Different Countries: A Technology Diffusion Perspective on e-Business. Manag. Sci. 2006, 52, 1557–1576. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental Management in SMEs in the UK: Practices, Pressures and Perceived Benefits: Environmental Management in SMEs. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Piwowar-Sulej, K.; Iqbal, Q. Leadership Styles and Sustainable Performance: A Systematic Literature Review. J. Clean. Prod. 2023, 382, 134600. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Multi-Group Analysis of the Role of Firm Size. Glob. Bus. Rev. 2020, 0972150920965079. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alshira’h, A.F.; Alshirah, M.H.; Alsyouf, A.; Alrawad, M.; Al-Khasawneh, A.; Saad, M.; Ali, R.A. Antecedents of Big Data Analytic Adoption and Impacts on Performance: Contingent Effect. Sustainability 2022, 14, 15516. [Google Scholar] [CrossRef]

- Organizational Citizenship Behavior for the Environment Decoded: Sustainable Leaders, Green Organizational Climate and Person-Organization Fit | Emerald Insight. Available online: https://www.emerald.com/insight/content/doi/10.1108/BJM-09-2021-0347/full/html (accessed on 6 June 2023).

- Jamil, C.Z.M.; Mohamed, R.; Muhammad, F.; Ali, A. Environmental Management Accounting Practices in Small Medium Manufacturing Firms. Procedia - Soc. Behav. Sci. 2015, 172, 619–626. [Google Scholar] [CrossRef]

- Latan, H.; Chiappetta Jabbour, C.J.; Lopes de Sousa Jabbour, A.B.; Wamba, S.F.; Shahbaz, M. Effects of Environmental Strategy, Environmental Uncertainty and Top Management’s Commitment on Corporate Environmental Performance: The Role of Environmental Management Accounting. J. Clean. Prod. 2018, 180, 297–306. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding the Intention to Adopt Cloud-Based Accounting Information System in Jordanian SMEs. Int. J. Digit. Account. Res. 2022, 22, 47–70. [Google Scholar] [CrossRef] [PubMed]

- Xu, M.; Zou, X.; Su, Z.; Zhang, S.; Ge, W. How Do Complementary Technological Linkages Affect Carbon Emissions Efficiency? J. Innov. Knowl. 2023, 8, 100309. [Google Scholar] [CrossRef]

- Adjei, J.K.; Adams, S.; Mamattah, L. Cloud Computing Adoption in Ghana; Accounting for Institutional Factors. Technol. Soc. 2021, 65, 101583. [Google Scholar] [CrossRef]

- Lutfi, A. Investigating the Moderating Role of Environmental Uncertainty between Institutional Pressures and ERP Adoption in Jordanian SMEs. J. Open Innov. Technol. Mark. Complex. 2020, 6, 91. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 147–160. [Google Scholar] [CrossRef]

- Latif, B.; Mahmood, Z.; Tze San, O.; Mohd Said, R.; Bakhsh, A. Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability 2020, 12, 4506. [Google Scholar] [CrossRef]

- Ong, T.S.; Lee, A.S.; Latif, B.; Sroufe, R.; Sharif, A.; Heng Teh, B. Enabling Green Shared Vision: Linking Environmental Strategic Focus and Environmental Performance through ISO 14001 and Technological Capabilities. Environ. Sci. Pollut. Res. 2023, 30, 31711–31726. [Google Scholar] [CrossRef]

- Solovida, G.T.; Latan, H. Linking Environmental Strategy to Environmental Performance: Mediation Role of Environmental Management Accounting. Sustain. Account. Manag. Policy J. 2017, 8, 595–619. [Google Scholar] [CrossRef]

- Do Dynamic Capabilities Matter? A Study on Environmental Performance and the Circular Economy in European Certified Organisations - Marrucci - 2022 - Business Strategy and the Environment - Wiley Online Library. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/bse.2997 (accessed on 6 June 2023).

- Burritt, R.L.; Herzig, C.; Schaltegger, S.; Viere, T. Diffusion of Environmental Management Accounting for Cleaner Production: Evidence from Some Case Studies. J. Clean. Prod. 2019, 224, 479–491. [Google Scholar] [CrossRef]

- The Contribution of the Eco-Management and Audit Scheme to the Environmental Performance of Manufacturing Organisations - Marrucci - 2022 - Business Strategy and the Environment - Wiley Online Library. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/bse.2958 (accessed on 6 June 2023).

- Alshira’h, A.F.; Alsqour, M.; Lutfi, A.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding Cloud Based Enterprise Resource Planning Adoption among SMEs in Jordan. J. Theor. Appl. Inf. Technol. 2021, 99, 5944–5953. [Google Scholar] [CrossRef]

- Hoang, N.-L.; Landolfi, A.; Kravchuk, A.; Girard, E.; Peate, J.; Hernandez, J.M.; Gaborieau, M.; Kravchuk, O.; Gilbert, R.G.; Guillaneuf, Y.; et al. Toward a Full Characterization of Native Starch: Separation and Detection by Size-Exclusion Chromatography. J. Chromatogr. A 2008, 1205, 60–70. [Google Scholar] [CrossRef]

- Gerbing, D.W.; Anderson, J.C. An Updated Paradigm for Scale Development Incorporating Unidimensionality and Its Assessment. J. Mark. Res. 1988.

- Tabachnick, B.G.; Fidell, L.S. Computer-Assisted Research Design and Analysis; Allyn and Bacon: Boston, 2001; ISBN 978-0-205-32178-0. [Google Scholar]

- Lisi, I.E. Translating Environmental Motivations into Performance: The Role of Environmental Performance Measurement Systems. Manag. Account. Res. 2015, 29, 27–44. [Google Scholar] [CrossRef]

- Hair, J.F.; Sarstedt, M.; Ringle, C.M. Rethinking Some of the Rethinking of Partial Least Squares. Eur. J. Mark. 2019, 53, 566–584. [Google Scholar] [CrossRef]

- Phan, T.N.; Baird, K.; Su, S. Environmental Activity Management: Its Use and Impact on Environmental Performance. Account. Audit. Account. J. 2018, 31, 651–673. [Google Scholar] [CrossRef]

- Wang, S.; Wang, H.; Wang, J. Exploring the Effects of Institutional Pressures on the Implementation of Environmental Management Accounting: Do Top Management Support and Perceived Benefit Work? Bus. Strategy Environ. 2019, 28, 233–243. [Google Scholar] [CrossRef]

- Malik, S.; Chadhar, M.; Vatanasakdakul, S.; Chetty, M. Factors Affecting the Organizational Adoption of Blockchain Technology: Extending the Technology–Organization–Environment (TOE) Framework in the Australian Context. Sustainability 2021, 13, 9404. [Google Scholar] [CrossRef]

- Phan, T.N.; Baird, K. The Comprehensiveness of Environmental Management Systems: The Influence of Institutional Pressures and the Impact on Environmental Performance. J. Environ. Manage. 2015, 160, 45–56. [Google Scholar] [CrossRef]

- Tashakor, S.; Appuhami, R.; Munir, R. Environmental Management Accounting Practices in Australian Cotton Farming: The Use of the Theory of Planned Behaviour. Account. Audit. Account. J. 2019, 32, 1175–1202. [Google Scholar] [CrossRef]

- Marrucci, L.; Daddi, T.; Iraldo, F. The Circular Economy, Environmental Performance and Environmental Management Systems: The Role of Absorptive Capacity. J. Knowl. Manag. 2022, 26, 2107–2132. [Google Scholar] [CrossRef]

- Lutfi, A.; Alshira’h, A.F.; Alshirah, M.H.; Al-Okaily, M.; Alqudah, H.; Saad, M.; Ibrahim, N.; Abdelmaksoud, O. Antecedents and Impacts of Enterprise Resource Planning System Adoption among Jordanian SMEs. Sustainability 2022, 14, 3508. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Group Analysis of the Role of Firm Size. Glob. Bus. Rev. 2020, 21, 1–19. [Google Scholar] [CrossRef]

Figure 1.

Figure 1. Research Model.

Table 1.

Measurements of Constructs.

| Construct | Items | Adopted From |

|---|---|---|

| Perceived benefits | 4 | [23] |

| TMS | 4 | [23] |

| Mimetic pressure | 4 | [2] |

| Coercive pressure | 4 | [2] |

| Normative pressure | 4 | [2] |

| EMAS adoption | 6 | [2] |

| Environmental performance | 4 | [64] |

Table 2.

Relevant Indicators of the Measurement Model.

| Latent Construct | Cronbach’s alpha | Composite Reliability (rho_c) | AVE |

|---|---|---|---|

| > 0.7 | > 0.7 | > 0.5 | |

| Environmental Performance (EP) | 0.720 | 0.775 | 0.543 |

| EMAS Use (EMAS U) | 0.755 | 0.844 | 0.576 |

| Perceive Benefits (PB) | 0.775 | 0.856 | 0.598 |

| Top Management Support (TMS) | 0.704 | 0.815 | 0.527 |

| Coercive Pressure (CP) | 0.860 | 0.908 | 0.715 |

| Normative Pressure (NP) | 0.897 | 0.935 | 0.827 |

| Memetic Pressure (MP) | 0.713 | 0.812 | 0.522 |

Table 3.

AVE Square Root (Correlations among Latent Constructs).

| CP | EMAS Use | EP | MP | NP | PB | TMS | |

|---|---|---|---|---|---|---|---|

| CP | 0.845 | ||||||

| EMAS Use | 0.525 | 0.759 | |||||

| EP | 0.449 | 0.728 | 0.737 | ||||

| MP | 0.426 | 0.717 | 0.701 | 0.722 | |||

| NP | 0.588 | 0.449 | 0.372 | 0.335 | 0.909 | ||

| PB | 0.034 | 0.425 | 0.327 | 0.414 | 0.071 | 0.773 | |

| TMS | 0.439 | 0.640 | 0.543 | 0.602 | 0.371 | 0.263 | 0.726 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.