Submitted:

04 May 2023

Posted:

05 May 2023

You are already at the latest version

Abstract

Development of Halal Tourism in Indonesia is the focus of the Indonesian government and MSMEs have an important role in supporting the development of halal tourism in Indonesia. This study aims to examine the relationship between marketing communication and Islamic financial literacy on Islamic financial inclusion and MSMEs performance in the halal tourism sector. A covariance-based SEM technique utilizing LISREL software was used to analyze the data from this investigation. Non-probability sampling was employed to collect the data, and the sample consists of 152 halal tourism entrepreneurs. We find that positive and significant association between Islamic financial inclusion and business performance. We also find that there are a positive and significant association between Islamic Financial Literacy and Islamic Financial Inclusion. Marketing communication and Islamic financial inlcuon a positive relationship but insignificant. This studi implies that to establish a halal tourist ecosystem for long-term development in Indonesia, commercial actors must lend their full support. This study demonstrates that they can thrive when MSMEs in the halal tourist ecosystem are backed by Islamic banking and Islamic rural banks. As a result, a more accommodating approach from Islamic banking is required to provide access to halal finance for business actors in Indonesia’s halal tourism ecosystem.

Keywords:

Marketing Communication

; Islamic Financial Literacy

; Islamic Financial Inclusion

; MSMEs Performance

1. Introduction

Tourism is one of the leading wheels of a country’s economy; several countries rely only on tourism to fuel their economy. Andora is one of the few countries where tourism is the principal source of state revenue, accounting for 80 percent of the country’s GDP (Gross Domestic Product). Not only do countries like Andora lack superior resources except in the tourist industry, but tourism has also become a trend of economic development of countries around the world because it has a significant impact on a nation’s life. According to a World Travel and Tourism Council (WTTC) assessment on the global economic effects of traveling and tourism activities, the tourism and travel sector generated 3% of total global GDP in 2015. In 2019, this contribution increased to 10.3 percent of the total global GDP. The absorption of labor is the direct influence of tourism and traveling activities on GDP. In 2015, the number of workers directly absorbed (direct contribution) by the tourism and travel sector was 107.8 million (3.6 percent of the total workforce). In the meantime, the actual contribution (indirect impact) on employment reached 283.6 million (9.5 percent of the entire workforce). While the amount of labor absorbed in 2019 gained 330 million workers, or 10.4 percent of total employment [1]. During the Covid-19 pandemic, employment from the tour and travel sector increased from 271.3 million in 2020 to 289.5 million in 2021 [2].

The development of GDP and employment impacts the survival of the tourist and travel business. This GDP generation is due to a rise in the number of investments, with total investment in this industry reaching USD 774.6 billion in 2015, accounting for 4.3 percent of total global investment. It climbed by 4.5 percent in 2016, with a total investment value of USD 1.3 trillion. According to the survey, it is likewise dominated by vacationers (tourism). According to the report, overseas tourists account for 76.6 percent of all visitors. The remaining 23.4 percent, on the other hand, was due to official travel or business matters. Meanwhile, overall investment in 2019 totaled USD 948 billion, accounting for 4.8 percent of total global investment [1]. Indonesia ranks fourth in terms of the number of international tourists visiting the ASEAN area. The Ministry of Tourism said that 10.87 million foreign tourists visited Indonesia in 2016, exceeding the target of 12 million foreign tourists set for 2016. As a result, Thailand ranked first with 27 million international tourists, followed by Malaysia with 17.6 million. On the other hand, Singapore ranked third, with 12 million foreign visitors in that month. Meanwhile, foreign tourist arrivals in 2019 totaled 16.11 million, a 1.88 percent raise over the previous year [3].

They perceive the attractive function of tourism in boosting a country’s economy and the competitiveness of Indonesian tourism, which is still inferior to neighboring countries as a foreign tourist destination. As a result, through the Ministry of Tourism and Creative Industries, the Indonesian government conducts numerous efforts to enhance national tourism to expect many foreign tourists to visit. In addition, domestic tourists may also call, boosting the economy of the selected tourist destination. This national tourist development comprises enhancing facilities, increasing the promotion budget, and building infrastructure to host international events. Furthermore, in addition to expanding existing tourism, the government prioritizes halal or sharia tourism. The goal is to attract more tourists from Muslim-majority countries.

According to Mardianto et al. [4], Halal tourism has recently received a lot of attention. Halal tourism is defined as tourism that complies with all criteria of Islamic law drawn from the Al-Qur’an and As-Sunah as guidelines. Halal tourism is a tourist location that has been well-planned and chosen following Sharia principles, as the atmosphere in this tourism environment is free of any banned contamination. Meanwhile, a halal tourist destination is a geographical area within one or more administrative regions that contains tourist attractions, religious and public facilities, tourism facilities, accessibility, and communities that are interconnected and complement the realization of a statement by the Sharia principle. According to Zaki et al. [5], Sharia tourism is separated into numerous components, including Islamic hotels, Islamic travel agents, halal restaurants, and Islamic tourism artifacts. Tourism growth has a substantial influence in terms of increased Original Local Government Revenue and investment in regional development. An increase in money from the tourism sector provides locals more power in their lives since it opens them to more work alternatives. This strategy benefits investors because the government has made it easier to open new business opportunities in the tourism sector [5].

Halal tourism becomes a distinct trend for a country since the amount of foreign exchange it can bring in for the country is significant. This is attributable to an increase in the number of Muslim tourists worldwide. According to the Global Muslim Travel Index (GMTI), the number of Muslim travelers increased to 121 million in 2016 and is expected to expand to 156 million in 2020 (assuming no Covid-19 epidemic), with a total expenditure of USD 220 billion and expected to reach USD 300 billion in 2026 [6]. To capture the hearts of potential visitors and persuade them to visit a place, a systematic and measurable effort is required, with the support of all stakeholders. The Indonesian government is working hard to compete worldwide in attracting foreign tourists by developing a sustainable halal tourism ecosystem.

The development of the Halal tourist ecosystem in Indonesia employs a Penta helix strategy, with five factors intended to promote the growth and development of halal tourism in Indonesia. In Halal tourism, the five elements are the government, media, academics, communities, and commercial actors. The Global Muslim Travel Index (GMTI) recognized Indonesia with the “World Best Halal Travel Destination” award in 2019 for the hard work of all these factors in the growth of halal tourism in Indonesia [7]. Tourist object managers, transport or ticketing businesses, hotels, restaurants, gift stores, or goods are essential components of the halal tourism development ecosystem. However, despite its importance in absorbing labor and investment, the tourism industry, a sub-sector of the creative economy, has gotten less attention from the banking industry, particularly Islamic banking. In 2017, only 6% of tourism sector actors used financial institutions, while 94% of tourism sector company actors continued to rely on private finance [8].

Camara and Tuesta [9] say that financial inclusion is very important in creating a country's economic growth because every individual has the opportunity to access financial institutions. Abubakar [10] adds that MSME development without the support of financial institutions will be difficult to realize. Badulescu et al. [11] have studied the potential of banking financing to boost rural tourism. Because of a drop in agricultural real income, a lack of genuine economic alternatives, and demographic difficulties Small local companies that valorize natural, cultural, and anthropological resources could contribute to rural sustainable development. However, the majority of them require financial assistance from private creditors (banks).

With the engagement of Islamic banking in the tourism industry, halal business is predicted to promote growth in the sector and boost its market share and Islamic banking market share in Indonesia. To date, Islamic banking has only had a 6.1 percent market share. It is hoped that the penetration of this industry will boost the market share of Islamic banking and the incorporation of Islamic financing in the tourism sector. The performance of MSMEs in the tourism sector is arguably still low if the guidelines for their contribution to GDP have only reached 4.80 percent in 2019. However, there is a positive trend, namely an increase from the previous year, although in previous years the contribution was lower than in 2019. In 2015 the contribution of the tourism sector to Indonesia's GDP reached 4.25 percent, then in 2016 it decreased to 4.13 percent and in 2017 it decreased again to 4.11 pecent. Although in 2018 it increased to 5.25 percent. Kemudian pada tahun kontribusi terhadap PDB mencapai 4.7 persen pada tahun 2019, kemudian pada tahun 2020 turun menjadi 4.05 persen [12]. Employment of MSMEs in halal tourism is also low when compared to other sectors. In 2018, the tourism sector was only able to absorb a workforce of 12.7 million workers.The Covid-19 pandemic in 2020 made the tourism sector suffer the biggest losses compared to other sectors in Indonesia. In a difficult situation like this, the financial sector has a crucial role in helping to restore the tourism sector in Indonesia, including Islamic banking. Therefore it is important for both individuals and MSMEs to increase financial inclusion.

Several studies highlight that the determinants of Islamic financial inclusion are financial literacy [13,14,15]. Selain financial literasi, marketing communication juga menjadi elemen penting dalam mempromosikan produk-produk keuangan Islam kepada calon nasabah potensial [15,16]. Ignorance of potential customers about the existence of Islamic financial products has resulted in little access to Islamic finance by entrepreneurs in the tourism sector in Indonesia. This study aims to investigate the role of marketing communication and Islamic financial literacy in creating financial inclusion for entrepreneurs in the halal tourism sector in Indonesia. This research will also investigate the role of Islamic banking in boosting MSMEs in the halal tourism sector in Indonesia.

This research is an initial effort to explore the development of halal tourism from the supply side. Investigating the role of Islamic financial institutions in developing MSMEs in the tourism sector has never been carried out by previous researchers and this is the novelty of this research. The author finds that studies on halal tourism are still dominated by the demand side, as was done by [17] and [18]. Several additional scholars, like [19,20,21,22,23,24], focus on the notion of halal tourism and the key difficulties associated with its development.

The findings of this study are likely to contribute to the growth of halal tourism in Indonesia and development of MSMEs in the Indonesian halal tourism ecosystem. Furthermore, this research is expected to be able to help achieve the master plan of the Indonesian Islamic economy by examining the factors that influence the acceptance of Islamic Banks in halal tourism SMEs.

2. Literature Review

2.1. Halal Tourism Concept

Halal tourism is a novel approach to meeting the travel needs of Muslim travelers . Most Indonesians, however, misunderstand the concept of halal tourism because it is confused with religious tourism, even though the two are distinct [25]. According to Muhammad Munir Chaudry, head of the Islamic Nutrition Council of America, halal tourism is a novel concept. This is not religious tourism in the same way that Umrah and Hajj are. Instead, halal tourism is tourism that provides vacations and vacation styles that are tailored to the needs and desires of Muslim guests. In this scenario, the hotel can assist the Muslim guest with Islamic compliance, such as no alcohol at the hotel [26]. There are numerous words used to describe halal tourism, such as Islamic tourism [24,27,28], Halal tourism [21,22,23,27]. Halal tourism refers to the traveling activities of Muslims who are migrating from one location to another or who are residing in a location other than their regular residence for less than a year and engaging in activities with Islamic objectives. It should be mentioned that Islamic activities must adhere to universally accepted Islamic norms, i.e., halal [18]. Halal tourism refers to any activities related to tourism that must suit the needs of a Muslim traveler, such as the availability of places of worship, kosher food, or food that is classified as Muslim friendly [19,20,29]. Nonetheless, academics’ use of halal tourism or Muslim-friendly terminology is still contested and contradictory. As a result, standardization is required to use the same terms [30]. The Indonesian government defines halal tourism as an activity supported by a wide range of facilities and services supplied by communities, businesses, the government, and local governments that adhere to Sharia law [19].

The Ministry of Tourism and the Creative Economy uses the Penta helix concept as a halal tourism ecosystem in establishing the notion of halal tourism. This halal tourism ecosystem is predicted to hasten national tourism development, as seen by increasing the number of tourists visiting Indonesia. The Penta Helix concept evolved from the Triple Helix concept proposed by Etzkowitz and Leydesdorff [31] , including government, academia, and businesses. Their essay stressed the importance of collaboration among government, academic, and corporate actors in creating and developing innovations on a national and regional scale.

Arif Yahya, Indonesia’s Minister of Tourism, announced the Penta Helix plan for tourism growth. The Republic of Indonesia’s Minister of Tourism Regulation (Permen) No. 14 of 2016 on Guidelines for Sustainable Tourism Destinations. The regulation aims to develop orchestrations to ensure the quality of activities, facilities, and services and generate experiences and value for tourism benefits. The law also aims to give advantages and benefits to society and the environment. As a result, it is critical to promote the tourist system by maximizing business, government, community, academic, and media ( BGCAM ). Arif Yahya underlined that promoting Indonesian tourism is the responsibility of all stakeholders in the tourism ecosystem, not only the government [32].

According to the Penta Helix concept, the government is responsible for tourism infrastructure such as developing roads and airports as access to a tourism location via a GI rating. Furthermore, the government serves as a regulator and a facilitator for all stakeholders. Universities serve as drafters, putting together the findings of field studies and applied research to help accelerate the development of halal tourism. The research university will be given to the government in order for it to design policies and offer business persons opportunities to grow their businesses. Business actors, as the third component of the halal tourist ecosystem, are at the heart of tourism activities. They provide tourist facilities by constructing a tourist-friendly region with Muslim passengers as a halal package, halal accommodation, halal food and beverage, and halal financial airport service [20]. Many people work in the halal tourism industry, including providers of tourist attractions, hotels, restaurants, travel, transportation, and other supporting businesses like gift shops and products. Meanwhile, community is the fourth component of the Penta helix. The community acts as a catalyst for the growth of halal tourism. They can mobilize their community to travel, resulting in a congested tourist area, which is critical in the development of halal tourism [18]. The final Penta helix is mass media, which accelerates the development of halal tourism in Indonesia.

2.2. Financial Literacy and Marketing Communication

Increasing the Islamic financial Literacy of business actors is one strategy to improve financial inclusion in the MSMEs sector. Financial Literacy is defined as the awareness, information, skills, attitude, and behavior required to make wise financial decisions and attain individual financial well-being [33]. The Indonesian Financial Services Authority (OJK) has developed an Islamic financial literacy strategy that focuses on target groups such as students, college students, communities, and business actors [34]. The goal of enhancing financial Literacy is to understand Islamic finance and, of course, to be able to handle finances. Someone who is well-versed in financial Literacy is more likely to successfully manage their funds [35] and to make sensible financial judgments [36,37]. According to Abubakar [10], business actors that understand financial Literacy are more likely to successfully run their enterprises. Furthermore, multiple research have found a favorable and significant association between financial Literacy and financial inclusion [13,38,39,40].

In addition to financial Literacy, Islamic financial inclusion in business actors can be caused by Islamic banking marketing communication. Marketing communication in Islamic banking can be defined by researchers as how Islamic banks communicate with their customers and potential customers to convey their corporate values, update information about the bank and products, and share their advantages or objectives through various communication channels [16]. The goal of marketing communication is to persuade potential customers to make financial purchases. They will create financial inclusion through financial transactions [15]. Advertising through various media such as billboards, television, banners, and social media is one form of marketing communication that Islamic banking can engage in. Advertisement in the financial services industry delivers essential information about products and services [16]. Relationship marketing is another type of marketing communication that Islamic banking might use.

Relationship marketing in the banking industry is defined as operations carried out by the bank to interact, communicate with, and retain more profitable or high net-worth customers [41]. It is envisaged that through implementing relationship marketing, marketing services will be able to persuade potential clients to undertake transactions with Islamic banks by delivering superior personal services [42,43]. Eldeep et al. [44] add that marketing communications focused on four components: first, developing a comprehensive advertising campaign to promote bank credibility, reputation, and image to MSMEs; second, developing a comprehensive advertising campaign to promote bank credibility, reputation, and image to MSMEs; and third, developing a comprehensive advertising campaign to promote bank credibility, reputation, and image to MSMEs. Second, encourage the introduction of new items and the modification of existing ones. The third entails ongoing public relations, regular interviews, and media events to keep MSMEs informed about bank activity. Employee skills and organizational knowledge were finally being scaled up.

2.3. Islamic Financial Inclusion and Business Performance

Islamic Banking and Islamic rural banking, as halal finance, play an important part in the development of the Islamic economy. The presence of Islamic banking and Islamic rural banks is intended to make the greatest possible contribution to the real sector. Islamic banking and Islamic rural banks can play this function by providing finance to business players as well as other services such as deposits, transfers, online banking, and mobile banking to help enterprises in the real sector. As a result, the incorporation of Islamic finance for business actors in the halal tourist ecosystem is a must. Financial inclusion is defined as “the process of ensuring vulnerable groups, such as weaker parts and low-income groups, access to financial services and timely and enough credit where needed at an affordable cost” [45]. The researcher can assess financial inclusion by examining access and impediments [9]. Access to Islamic banking for businesses is still being actively pursued by all stakeholders. However, due to the lack of accessibility in Indonesia, the Islamic banking and regulatory industries remain underdeveloped. The provinces of Jakarta have the highest level of inclusion, while the provinces of East Nusa Tenggara have the lowest [46]. In general, public access to banking is limited, with Indonesia ranking 75th out of 137 countries [9].

Because it is difficult to develop without financial inclusion, business actors’ access to formal financial institutions is likely to have an impact on their business development [10]. Financial inclusion can also increase the performance of businesses, according to empirical evidence [39,40,47,48]. The World Bank also urges every nation with a low degree of accessibility to develop financial inclusion for low-income people and Micro, Small, and Medium Enterprises (MSME) under the program Financial Inclusion Support Framework (FISF) (MSMEs). Through Minister of Finance Regulation No.22/2010 on access to finance for micro and small enterprises, the Indonesian government has also made different measures to ensure that business players, particularly MSMEs, can formally access financial institutions. This policy’s goal is to help business actors improve their business performance. One indicator of their success is the expansion of their firm, an increase in the number of employees, and an increase in financial and non-financial capability [49,50].

2.4. Previous Studies and Hypothesis Development

The authors were unable to locate any research on the function of Islamic banking in fostering business growth in the tourism sector, but numerous academics have undertaken similar studies. Bongomin et al. [38], for example, evaluated the association between Uganda’s financial Literacy and financial inclusion. There is a positive and substantial association between financial Literacy and financial inclusion, according to a study including 400 samples and evaluated with ModGrap. Bongomin et al., [39] conducted a study involving 5000 respondents in Uganda. This study aims to examine the role of microfinance in increasing financial inclusion for the poor. The study was analyzed using SEM AMOS, where financial literacy in the poor has a positive impact on increasing financial inclusion in Uganda. Bongomin et al., [40] also investigate the relationship between financial literacy with financial inclusion of the poor in the rural area in Uganda. With the 400 respondent, they are found that there are a positif relationship. In the context of MSMEs, Trianto et al., [15] investigate 198 entrepreneurs in Indonesia using the SEM Bootstrap approach found the empirical fact that Islamic financial literacy have a positif relationship with Islamic financial inclusion but insignificant. Trianto et al. [51] also conducted an investigation in the creative economy sector where there is a positive and significant relationship between Islamic financial literacy and Islamic financial inclusion. This study involved 62 business owners in the creative economy sector and analyzed using SEM GSCA. Sanistasya et al., [52] investigate the relationship between financial literacy and financial inclusion in Kalimantan, Indonesia. Involvep 100 MSMEs and analyze using SEM-PLS they found that there are positive and significant relationship for both. Thus following our hypothesis :

H1: Islamic financial literacy positive impact on Islamic financial inclusion

Marketing communication has a very vital role in promoting a product. The purpose of marketing communications is to motivate potential customers [15]. Prospective potential customers can be influenced through various appropriate promotional activities [53,54]. Hoque et al., [10] added that Islamic banking must increase the intensity of its marketing communications so that potential customers can become customers. Empirical facts also show that it will influence someone in making decisions ( Laverin and Liljander; 2006). Companies that do relationship marketing in the long term will be able to attract customers and retain customers [55]. Wahyuni [56] interviewed 198 people in Surakarta, Indonesia about purchasing Islamic banking products, and the most important aspects were product knowledge and social context. Meanwhile, Trianto et al. [15] discovered that marketing communication influences the inclusivity of Islamic finance for business actors. Based on the above explanation, following is our next hypothesis :

H2: Marketing communication positive impact on Islamic financial inclusion

Company performance can be influenced by several factors, including financial literacy and access to financial institutions. Trianto et al. [51] have explored the influence of Islamic banking in promoting business actors in the creative economy sector. The study’s findings indicate that the varied incorporation of Islamic finance has a favorable and significant impact on the growth of enterprises in the creative economy sector. According to the findings of the preceding study, financial inclusion is critical to business development. What variables impact business players ready to buy products from formal financial institutions such as Islamic banking is no less essential. The study also found that entrepreneurs who have good financial literacy are able to develop their businesses well. More precisely, Riwayati [ (2017) discovered that business actors that have access to financial institutions are more likely to succeed in their endeavors. The study included 90 business actors in Malang, Indonesia’s MSMEs sector, and was analyzed using Partial Least Squares (PLS). Sanistasya et al. (2019) discovered the same thing in Kalimantan, Indonesia where financial inclusion plays a critical role in the development of enterprises in the MSMEs sector. Purnomo (2018) investigate 375 small creative business in Yogjakarta, Indonesia the relationship between financial literacy and business performance. He found that there are positive relationship for boths. Based on the aforementioned description, the authors offer the following study hypotheses :

H3: Islamic financial literacy positive impact on business performance

H4: Islamic financial inclusion positive impact on business performance

3. Method

3.1. Information

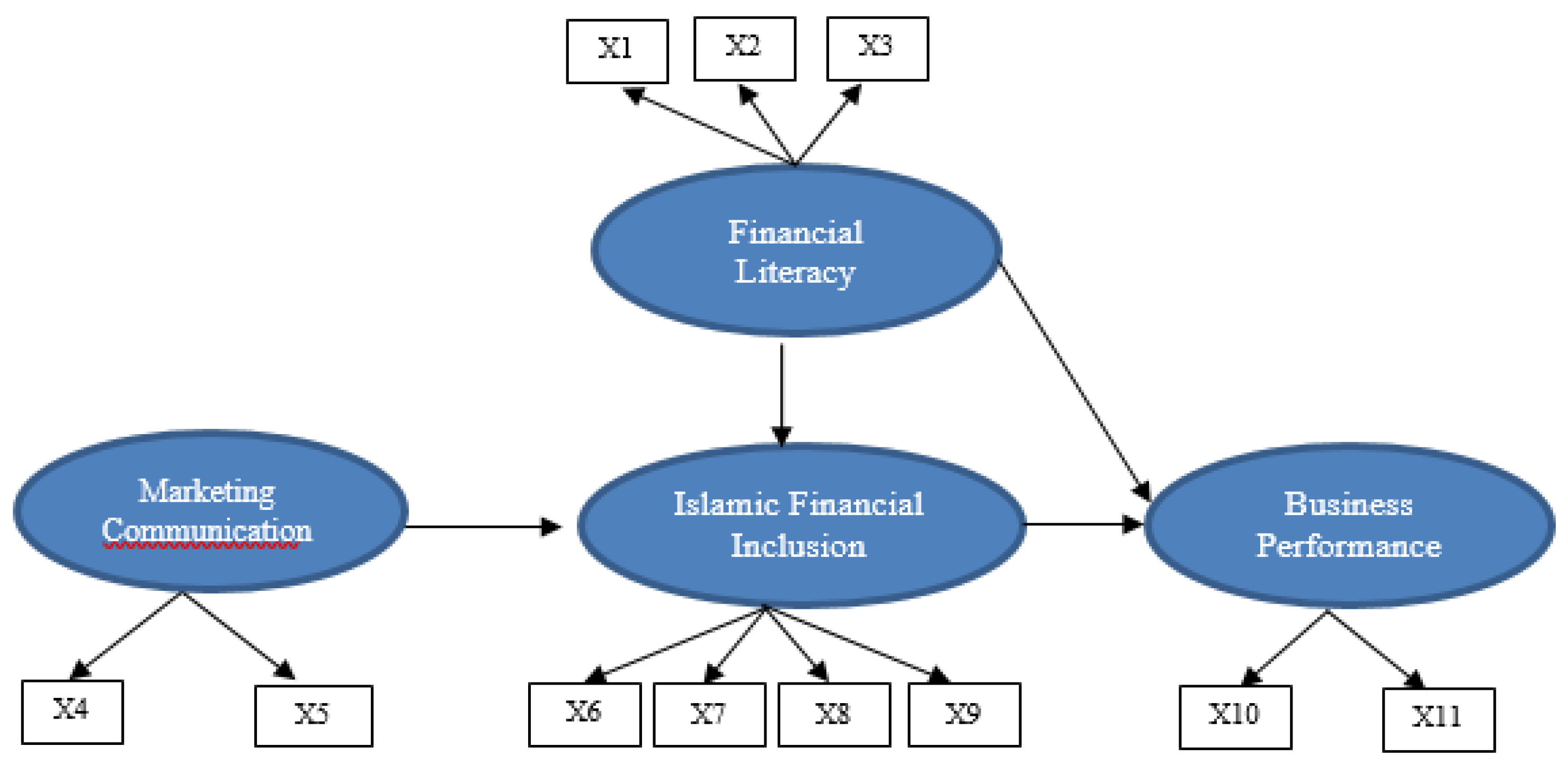

This study employs peer data, including information gathered from respondents using an online questionnaire. The Indonesian Hotel and Restaurant Association (IHRA), the Association Tourism Halal Indonesia (PPHI), the Consortium Halal We, Risen Muslim Entrepreneurs (BPM), and the Generation of Productive Muslim Entrepreneurs (BPM) have all sent out online questionnaires to the business community (Genpro). Therefore, this study’s sample consists of Indonesian entrepreneurs who support halal tourism, such as hotels and homestays, restaurants, tours and travel, transportation, and souvenirs. We obtained feedback from 274 respondents who completed the online questionnaires that we sent. After screening, there were only 152 responders who satisfied the study’s criteria hence the sample size was 152 MSMEs. We employed four variable delay variables and twelve indicator variables in this investigation. Financial Literacy, marketing communication, financial inclusion, and company performance are the four latent variables. There are three indicator variables for financial Literacy: awareness (X1), knowledge (X2), and skill (X3) (X3). Relationship marketing (X4) and advertising are two indicator variables in marketing communication (X5). Access (X 6), utilization (X 7), obstacles (X 8), and quality are the four indicator variables for financial inclusion (X 9 ). Finally, there are two indicator variables for business performance: sales growth (X1 0 ) and profit growth (X1 1 ).

3.2. Empirical Model

This research aims to examine the role of Islamic banking on the development of MSMEs in Indonesia’s halal tourist ecosystem. This contribution is visible in the level of Islamic financial inclusion for MSMEs, which is projected to improve their business performance. Therefore, this study will investigate the relationship between financial inclusion and MSME business performance in Indonesia’s halal tourism environment. In addition, this study will examine the causality of the relationship between exogenous variables, such as financial Literacy, marketing communication, and financial inclusion, and endogenous variables, such as business performance. The empirical model used in this study is as follows :

Figure 1.

3.3. Information

This research conduct SEM for analysis method. SEM is a powerful method for estimating multiple and concurrent relationships involving several dependent and explanatory factors, and it allows for the inclusion of latent variables that cannot be measured directly but may be described as a function of other measurable variables. This brief definition of SEM does not do credit to the intricacy of the processes needed in building a structural equation model, but it does highlight SEM's distinction from statistical methodologies (Mazzocci, 2011). Hair et al., (2006) state that an appropriate method to examine the latent variables is use SEM Method. A single dependent variable is related to one or more independent (explanatory) factors in linear regression, with the premise that these explanatory variables are fixed, independent of each other, and exogenous (which means that they are determined outside the relationship).

This study was evaluated with LISREL 8.7 software and a covariance-based Structural Equation Model (SEM) technique (CB-SEM). Several researchers [57,58] indicate that research undertaken to test theory should utilize CB-SEM, whereas research conducted to forecast a construct should use PLS-SEM. This study employs CB-SEM with LISREL software to evaluate and corroborate assumptions concerning financial inclusion, financial Literacy, marketing communication, and business success. The analyst is CB-SEM, and among the evaluations are the loading factor values for each construct and the Goodness of Fit (GOF) models. According to Hair et al. [58] the loading factor for each relationship between the latent variable and an indicator variable is 0.5, while the loading factor for the Goodness of Fit Model is as follows :

Table 1.

Goodness of Fit Model Criteria.

| No | The goodness of Fit Model Category | Criteria |

| 1 | Chi-Square | Small is better |

| 2 | Probability | > 0.05 |

| 3 | Goodness of Fit Index (GFI) | > 0.90 |

| 4 | Average of Goodness of Fit Index (AGFI) | Usually below of GFI |

| 5 | Root Mean Square Errors of Approximation (RSMEA) | < 0.08 |

Source: Hair et al., (2006).

4. Results

4.1. Respondent Profile

Respondents in this study were dominated by men with a total of 87 or 57.24 percent and the level of education was dominated by college graduates who reached 81 or 53.29 percent with an average of very productive or mature age of 53 people or 34.87 percent. Hotels and homestays are essential components that must exist to accommodate guests on vacation. Respondents who tried on the field hotel & homestay reached 29 or 19:08 percent in this survey. Meanwhile, respondents with a restaurant company accounted for 85 people or 55.92 percent of the total. This is the highest amount among other firms. One of the key elements encouraging halal tourism is 12 or 07.89 percent of transportation, tour, and travel companies. In this analysis, companies involved in souvenirs accounted for 20 percent or 13.16 percent. Souvenirs are one of the key auxiliary goods in tourism that travellers can use as souvenirs. In Table 4, information on the number of workers is also shown, with the entire workforce successfully absorbed in the halal tourist ecosystem reaching 713 persons, with six enterprises employing more than 20 people. Meanwhile, the number of enterprises employing 6-20 employees reached 19 (or 12.50). Table 2 further demonstrates that micro-scale organizations dominate this research’s respondents, accounting for 104 companies or 68.42 percent.

4.2. SEM Evaluation

4.2.1. Descriptive Statistic

Table 3 shows the data from this study where the mean value of all variables is greater than three and the standard deviation is more significant than 0.5. In the meantime, the minimum value is 0.912, and the maximum value is 5,204. Table 5 also displays the P-value for each indicator variable’s skewness and kurtosis. These values are greater than 0.05, indicating that the data is regularly distributed. The data must be periodically distributed, which is one of the most important conditions in the CB-SEM analysis. In contrast to PLS-SEM, where data are not required to be regularly distributed [58.59].

Table 2.

Respindent Profile.

| No | Descriptions | Total | Percentage |

| 1 | Gender | ||

|

87 65 |

57.24 42.76 |

|

| 2 | Education | ||

|

27 44 81 |

17.76 28.95 53.29 |

|

| 3 | Age | ||

|

51 44 53 4 |

33.55 28.95 34.87 02.63 |

|

| 4 | Business Type | ||

|

29 85 12 6 20 |

19.08 55.92 07.89 03.95 13.16 |

|

| 5 | Business Sales Per Years | ||

|

104 35 13 |

68.42 23.03 08.55 |

|

| 6 | Number of Employees | ||

|

127 19 6 |

83.55 12.50 03.95 |

Source : Authors Calculation, 2023.

Table 3.

Descriptive Statistic.

| Variabel | Mean | St.Dev | Min | Max | Skewness & Curtosis | |

| Chi-Square | P-Value | |||||

| X1 | 3.339 | 0.709 | 1.340 | 5.074 | 0.662 | 0.718 |

| X2 | 3.289 | 0.657 | 20001 | 5.169 | 0.081 | 0.961 |

| X3 | 3.250 | 0.702 | 1983 | 5.034 | 0.086 | 0.958 |

| X4 | 2,947 | 0.744 | 0.994 | 5.018 | 0.360 | 0.835 |

| X5 | 3.151 | 0.735 | 0.912 | 5.204 | 0.117 | 0.943 |

| X6 | 3.645 | 0.694 | 1.476 | 5.185 | 2,797 | 0.247 |

| X7 | 3.566 | 0.851 | 1.012 | 4.977 | 0.284 | 0.868 |

| X8 | 3.395 | 0.862 | 1.399 | 5.154 | 0.085 | 0.958 |

| X9 | 3.395 | 0.870 | 1.252 | 5.118 | 0.181 | 0.914 |

| X10 | 3,599 | 0.730 | 1.366 | 5.083 | 0.534 | 0.766 |

| X11 | 3.447 | 0.717 | 1.414 | 5.022 | 0.584 | 0.747 |

Source : Authors Calculation, 2023.

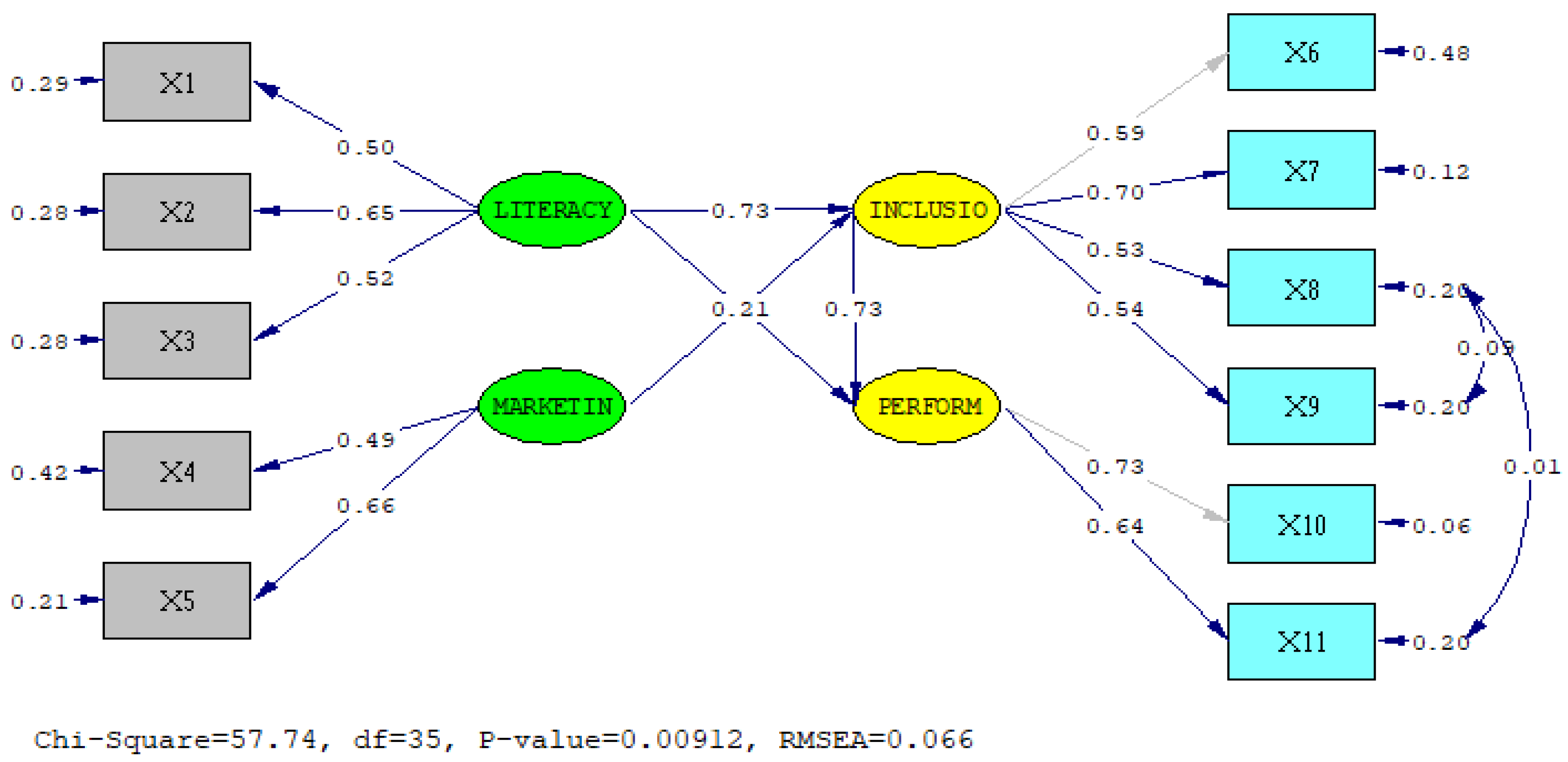

Table 4 shows the covariance matrix for each latent variable, wherein the matrix shows a positive value for the whole relationship. Meanwhile the loading factor values are shown in Table 5, which all have a loading factor value greater than 0.5. Table 6 also shows the Cronbach alpha value’s reliability, with a composite Cronbach alpha value of 9.26, indicating that it is dependable with an explained variance of 41,197 – 46,912. Whereas, the goodness of fit models can be seen in Table 7. In the first evaluation, not all criteria were met, so it was necessary to modify the model. After adjusting the model, Table 7 shows that all the requirements for the goodness of fit model have met the model’s feasibility test standard.

Table 4.

Covariance Matrix Among Laten Variables.

| Variables | Financial Inclusion | Business Performan | Financial Literacy | Marketing Comm |

| Financial Inclusion | 1.00 | |||

| Business Perform | 0.90 | 1.00 | ||

| Financial Literacy | 0.78 | 0.78 | 1.00 | |

| Marketing Comm | 0.64 | 0.63 | 0.79 | 1.00 |

Source : Authors Calculation, 2023.

Table 5.

Loading Factor and Cronbach Alpha.

| Variables | Loading Factor | Cronbach Alpha | Composite Alpha | Variance Explained |

| X1 | 0.50 | 0.926 | 46.430 | |

| X2 | 0.66 | 0.919 | 44.906 | |

| X3 | 0.52 | 0.921 | 45.070 | |

| X4 | 0.50 | 0.927 | 46.912 | |

| X5 | 0.65 | 0.922 | 9.26 | 45.127 |

| X6 | 0.60 | 0.928 | 47.209 | |

| X7 | 0.70 | 0.917 | 42.490 | |

| X8 | 0.53 | 0.924 | 44.197 | |

| X9 | 0.54 | 0.915 | 41.992 | |

| X10 | 0.73 | 0.917 | 43.834 | |

| X11 | 0.64 | 0.921 | 44.877 |

Source : Authors Calculation, 2023.

Table 6.

Goodness of Fit Statistic Evaluation.

| Categoty | Criteria | Result | Remarks |

| Chi-Square | Small is better | 56.42 | FIT |

| Profitabiliy | >0.05 | 0.01 | Marginal FIT |

| GFI | >0.90 | 0.94 | FIT |

| AGFI | Below GFI | 0.88 | FIT |

| RSMEA | <0.08 | 0.06 | FIT |

Source : Authors Calculation, 2023.

4.2.2. Correlation Matrix of Laten Variables

Table 8 depicts the association between latent factors, with all latent variables having a positive relationship and a correlation value of 0.7 8 for the relationship between financial literacy and marketing communication. While the association between financial literacy variables and financial inclusion is 0.78, the relationship between financial literacy variables and company performance is 0.77. The association between marketing communication and financial inclusion is 0.62, and the link between marketing communication and business performance is 0.70. Financial inclusion and business performance have a 0.90 link.

4.2.3. Structural Model evaluation

Table 9 displays the structural model findings so that you can see the effect of each variable. Table 9 demonstrates a positive and substantial link between financial literacy and financial inclusion variables. As a result, we accept H1. Meanwhile, marketing communication has a beneficial but non-significant impact on financial inclusion. According to estimate 0.06, and hence on the beginning of H2. With a coefficient of 0. 21, variable financial Literacy has a positive but non-significant effect on variable business success, and we reject H3. The following relationship is a positive and significant between financial inclusion and business performance. H4 was also acceptable.

Figure 2.

Structural Model Evaluation.

5. Discussions

Halal finance is one of the locomotives propelling Islamic finance’s genuine industry. The structural model results reveal that Islamic banking, has a positive and significant association with the performance of MSME in the halal tourism ecosystem. This study’s findings are consistent with Trianto et al. [15,51], Sanistasya et al. [52]. Badulescu et al. [14] also outlined the steps these enterprises must take to obtain financial resources from banks, namely the diversification of income sources, the association and adherence to recognized brands, and the maintenance of a sustainable leverage ratio. In addition, it was discovered that the size of the bank is unimportant, but the kind of the bank’s capital is: private domestic banks are more ready to finance such firms.

This finding shows that MSMEs in Indonesia’s halal tourism ecosystem requires access to Islamic finance institutions to improve and expand their operations. Furthermore, MSMEs must be educated on the importance of company development through financial institutions. On the other side, Islamic banking must expand its operations as halal finance by focusing on the MSME market, particularly MSMEs in the halal tourist ecosystem. Furthermore, due to the merging of three state banks, Bank Syariah Indonesia must become a locomotive committed to the development of halal tourism in Indonesia. This study also demonstrates a favorable and statistically significant association between financial literacy and financial inclusion. The outcomes of this study support earlier researchers’ conclusions [13,38,39,40]. As a result, both parties must increase their Islamic financial Literacy. Sharia banking can work with the entrepreneur community in the halal tourist ecosystem to teach Islamic Financial Literacy, increasing the prospects for sharia financial inclusion.

The structural model also discovered a positive but insignificant association between financial Literacy and business success. This finding contradicts the findings with [40, 15, 13, 39, 47 and 48]. Although not considerable, this association has had a favorable impact on incorporating Islamic finance and improving MSME business performance in Indonesia’s halal tourist ecosystem. As a result, initiatives to improve Islamic financial Literacy must be pursued indefinitely in order to have a greater impact. Improving Islamic financial Literacy can be accomplished by honing Islamic financial skills. Such as the notion of syirkah in building their business and enhancing their knowledge of halal financial products to have a stronger impact on the development of MSMEs in the Indonesian halal tourism ecosystem.

This study also provides information that there is a positive but not significant relationship between marketing communication and financial inclusion. The results of this study are not in line with [43,51,59]. However, although not significant, the relationship is positive. This means that marketing communications run by Islamic banking as halal finance has attracted interest for MSMEs. For this reason, Islamic banking needs to improve marketing communication to the entrepreneur community in the halal tourism ecosystem because marketing communication is a pivotal strategy for banking industries. Customers are not only interested in the products offered but also in how they are offered, which is the most important thing in marketing communication [60]. Furthermore, [61] said that banks must carry out integrated marketing communication so that prospective customers can buy the products offered. Scholars such as [53,54] said that potential customers are as important as existing customers so an intense approach is needed. In Islamic banking, they must carry out integrated marketing communication through various programs and inform the media channels they have. Meanwhile, [62] recommends that marketing communication carried out by banks emphasizes more on adopting personal selling.

Therefore, to improve the performance of SMEs in halal tourism, it is necessary to pay attention to the above variables. The marketing communication variable is a variable that needs attention from Islamic banking. Islamic banking needs to improve its marketing communication through promotion to MSMEs on halal tourism by taking a more intensive approach, so that they are interested and decide to use Islamic banking services. The decision of MSMEs to use services in Islamic banking will certainly make it easier for them to conduct business transactions, such as the use of financing, the use of e-banking, mobile banking and internet banking. MSMEs in halal tourism also need to improve Islamic financial literacy in order to be able to manage finances well. Thus, their business performance can also improve well. Financial knowledge and financial skills which are part of financial literacy seem to need special attention for them. Financial knowledge such as knowledge about Islamic financial products will help entrepreneurs in halal tourism to develop their business portfolios. Meanwhile, financial skills such as the ability to manage debt, the ability in budgeting will help them in maintaining the company and in developing their business.

6. Conclusion and Recommendations

6.1. Conclusion

Sustainable halal tourism necessitates concerted efforts and commitment from all stakeholders, including business actors and the financial industry, particularly halal finance. This study demonstrates that Islamic banking, as halal financing, has a meaningful contribution to the development of halal tourism in Indonesia. However, it is not optimal in terms of providing access to business actors involved in tourism for a variety of reasons. MSMEs have a significant duty to promote halal tourism in Indonesia as one of the components in the halal tourism ecosystem in Indonesia thus they should have the bravery to build their business, even more, using various financing schemes supplied by Islamic banking. Halal finance, on the other hand, such as Islamic banking, Islamic rural banks, and Islamic microfinance, must be made available to MSMEs in the halal tourist ecosystem. As a result, the role of Islamic finance in the development of MSMEs in the halal tourist ecosystem maybe even more critical. This study has limitations that this study has not included conventional financial institution variables as control variables. The results of this study may be different if the existence of conventional financial institutions is included in the model. We recommend further researchers to include conventional financial institution variables for more comprehensive research results.

6.2. Recommendations

We recommend MSME development policies in the halal tourism sector in Indonesia. First, for Government or Regulator. The government can encourage Islamic financial institutions to penetrate the Halal Tourism MSME actors market in Indonesia. In this case, the government needs to provide rewards for Islamic financial institutions that focus on halal MSME actors. For example, a liquidity policy is more specific for Islamic banks with consumers who are SMEs. Second, for Islamic bankers. Islamic bankers should think about and implement strategies explicitly made for halal MSMEs because they have different socioeconomic conditions from other consumers and have their characteristics.

Author Contributions

Conceptualization, B.T. and S.M.; methodology, B.T. and E.F.C; software, B.T.; validation, B.T., E.F.C. and R..; formal analysis, All Authors.; investigation, All Authrs.; resources, S.M.; data curation, B.T. and R; writing—original draft preparation, B.T., S.M. and E.F.C; writing—review and editing, R.; Project administration, S.M. and R.; funding acquisition, S.M. and R. All authors have read and agreed to the published version of the manuscript.

Funding

This study ws fully funded from LPPM Universitas Muhammadiyah Sumatera Utara, Medan, Indonesia.

Acknowledgments

We would like to thank LPPM Muhammadiyah University of North Sumatra, reviewers, respondents and all parties involved in this research.

Conflicts of Interest

The authors declare that this study no conflict of interest.

References

- Global Economic Impact & Trend 2020. World Travel and Tourism Council. 2020. Retrived from : Global Economic Impact Trends 2020.pdf (wttc.org).

- Travel and Tourism Economic Impact on 2022. World Travel and Tourism Council. 2022. Retrived from : EIR2022-Global Trends.pdf (wttc.org).

- BPS. (2020). The Number of Tourist Visits to Indonesia in December 2019 Reached 1.38 Visits. Retrived from: https://www.bps.go.id/pressrelease/2020/02/03/1711/sum-kunjungan-wisman-ke-indonesia-desember-2019-menreach-1-38-juta-kunjungan-.html. 20 December.

- Mardianto, M. F. F., Cahyono, E. F., Syarifah, L., & Andriani, P. (2019). Prediction of the Number of Foreign Tourist Arrival in Indonesia Halal Tourism Entrance using Simultaneously Fourier Series Estimator. KnE Social Sciences, 1093–1104-1093–1104.

- Zaki, I., Hamida, G., & Cahyono, E. F. (2020). POTENTIALS OF IMPLEMENTATION OF SHARIA PRINCIPLES IN THE TOURISM SECTOR OF BATU CITY, EAST JAVA. Amwaluna: Jurnal Ekonomi dan Keuangan Syariah, 4(1), 96-111.

- Global Muslim Travel Index. (2019). Mastercard-Crescentating (GMTI). Bukit Merah Central : Crescentrating Company. C: Central.

- Antara. Indoesian Named as the Wolrd’s Best Halal Tourist Destination. 2019. Retrived from Indonesia named as the world's best halal tourist destination - ANTARA News.

- Pikiran Rakyat. (2017). Ekonomi Kreatif Intangible Sulit Akses Perbankan. https://www.pikiran-rakyat.com/ekonomi/pr-01286464/ekonomi-kreatif-intangible-sulit-akses-perbankan-410021. Access date : th, 2020. 11 August.

- Camara, N. and Tuesta, D. (2017). Measuring Financial Inclusion: A Multidimensional Index . Bank of Morocco – CEMLA –IFC Satellite Seminar of The ISI World Statistics Congress on Financial Inclusion. Morocco : Marrakech.

- Abubakar, H.A. (2015), "Entrepreneurship development and financial literacy in Africa", World Journal of Entrepreneurship, Management and Sustainable Development, Vol. 11 No. 4, pp. 281-294. [CrossRef]

- BADULESCU D, GIURGIU A, ISTUDOR N, BADULESCU A. Rural tourism development and financing in Romania: A supply-side analysis. Agric. Econ. - Czech. 2015, 61, 72-8. [CrossRef]

- Alinea. Kontribusi Sektor Pariwisata Terhadap PDB Tahun 2017 – 2021. 2022. Retrived from Kontribusi sektor pariwisata terhadap PDB 2017-2021 - Grafik Alinea ID.

- Ali, M.M., Devi, A., Furqani, H. and Hamzah, H. (2020), "Islamic financial inclusion determinants in Indonesia: an ANP approach", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 13 No. 4, pp. 727-747. [CrossRef]

- JANAH, M. (2021). MINAT USAHA MIKRO KECIL MENENGAH PASAR BAWAH UNTUK MELAKUKAN PEMBIAYAAN BERBASIS KONVENSIONAL DAN BERBASIS SYARIAH (Doctoral dissertation, Universitas Islam Negeri Sultan Syarif Kasim Riau).

- Trianto, B., Rahmayati, R., Yuliaty, T., & Sabiu, T. T. (2021). Determinant factor of Islamic financial inclusiveness at MSMEs: Evidence from Pekanbaru, Indonesia. Jurnal Ekonomi & Keuangan Islam, 7(2), 105–122. [CrossRef]

- Hoque, M.E., Nik Hashim, N.M.H. and Azmi, M.H.B. (2018), "Moderating effects of marketing communication and financial consideration on customer attitude and intention to purchase Islamic banking products: A conceptual framework", Journal of Islamic Marketing, Vol. 9 No. 4, pp. 799-822. [CrossRef]

- Devi, A., & Firmansyah, I. (2019). DEVELOPING HALAL TRAVEL AND HALAL TOURISM TO PROMOTE ECONOMIC GROWTH: A CONFIRMATORY ANALYSIS. Journal of Islamic Monetary Economics and Finance, 5(1), 193-214. [CrossRef]

- Zamani-Farahani, H. and Henderson, JC (20 10 ). Islamic Tourism and Managing Tourism Development in Islamic Societies: The Case of Iran and Saudi Arabia. International Journal of Tourism Research, 12, 79-89. [CrossRef]

- Jaelani, A. (2017). Halal Tourism Industry in Indonesia: Pontential and Prospects. Munich Personal RePEc , 76235.

- Chianeh, R.H., Kian, B. and Azgoomi, S.K.R. (2019), "Islamic and Halal Tourism in Iran", Experiencing Persian Heritage (Bridging Tourism Theory and Practice, Vol. 10), Emerald Publishing Limited, Bingley, pp. 295-307. [CrossRef]

- Mohsin, A., Ramli, N., & Alkhulayfi, B. A. (2016). Halal tourism: Emerging opportunities. Tourism Management Perspectives, 19, 137–143. [CrossRef]

- Battour, M., & Ismail, M. N. (2016). Halal tourism: Concepts, practises, challenges and future. Tourism Management Perspectives, 19, 150–154. https://doi.org/10.1016/j.tmp.2015.12.008Rahman, R. F. (2021). PENGARUH BRAND IMAGE BANK SYARIAH TERHADAP MINAT PINJAMAN MODAL UMKM (Studi Kasus Pada Bank Kal-Sel Syariah Kota Banjarmasin) (Doctoral dissertation, Universitas Islam Kalimantan MAB). [CrossRef]

- El-Gohary, H. (2016). Halal tourism, is it really Halal? Tourism Management Perspectives, 19, 124–130. [CrossRef]

- Din, K. H. (1989). Islam and tourism. Annals of Tourism Research, 16(4), 542–563. [CrossRef]

- Republika. (2019). People Still Misunderstand the Definition of Halal Tourism. Retrieved https://www.republika.co.id/berita/gaya-Life/travelling/19/03/25/pox1lw459- Masyarakat-masih-salah-paham-pengertian-wisata-halal.

- Wuryasti. F. (2013). Halal Tourism, a New Concept of Tourism Activities in Indonesia. Retrieved from https://travel.detik.com/travel-news/d-2399509/wisata-halal-concept-baru-activity-wisata-di-indonesia.

- Jafari, J.Y., & Scott, N. (2014). Muslim world and its tourisms. Annals of Tourism Research, 44, 1-19. [CrossRef]

- Carboni, M., Parelli, C . and Sistu, G. (2014). Is Islamic Tourism a Viable Option for Tunisian Tourism ? Insight from Djerba. Tourism Management Perspectives, Vol.11, pp.1-9. 1–9.

- Bogan, E. and Sarusik, M. (2018). Halal Tourism : Conceptual and Practical Challenges. Journal of Islamic Marketing.

- Khan, F. and Callanan, M. (2017). The “Halilification” of Tourism. Journal of Islamic Marketing, Vol.8, No.4, pp.558 0 577. .4.

- Etzkowitz, H. and Leydesdorff, L . (1995). Triple Helix - University Industry Government Relations: A Laboratory for Knowledge Based Economy . Development. EASST Review 14 .

- Bisnis. (2016). Minister of Tourism Emphasizes Penta Helix Collaboration. Here’s the explanation. https://ekonomi.bisnis.com/read/20160725/12/568877/menteri-pariwisata-tekankan-kolaborasi-penta-helix.-begini-pencepatan . Access Date: 1 st November 2020. 20 November.

- OECD INFE. ( 2011 ). Measuring Financial Literacy: Questionaire and Guidance Notes For Conducting an Internationally Comparable Survey of Financial Literacy. International Network on Financial Education, Paris.

- OJK. (2017). Indonesian Financial Literacy National Strategy (Revisit). Available at : https://www.ojk.go.id/id/berita-dan-activities/publikasi/Documents/Pages/Strategi-Nasional-Literasi-Keuangan-Indonesia-(Revisit-2017)-/SNLKI%20( Revisit%202017)-new.pdf. Access date, 28 June 2020.

- Pond, C. (2008 ). Financial Capability Strategy. OECD-US Treasury International Conference on Financial Education. Taking Financial Literacy to the Next Level : Important Challenges and Promising Solutions . Volume I. US Treasury Department and OECD.

- Van Rooij, M., Lusardi, A. and Alessie, R. (2007). Financial Literacy and Stock Market Participation. Available at : https://www.dartmouth.edu/~alusardi/Papers/Literacy_StockMarket.pdf . Access date : 29 June 2020. 29 June.

- Lusardi, A. and Mitchell, OS (2014). The Economic Importance of Financial Literacy: Theory and Evidence. Journal of Economic Literature , 52(1), 5-44.

- Bongomin, GOC, Munene, JC, Ntayi, JM and Malinga, CA (2018). Nexus between financial Literacy and financial inclusion . Examining the moderating role of cognition from a developing country perspective. International journal of bank marketing.

- Bongomin, GOC, Ntayi, JM and Malinga, CA (2020). Analyzing the relationship between financial Literacy and financial inclusion by microfinance in developing countries: social network theoretical approach. International Journal of Sociology and Social Policy.

- Bongomin, GOC, Ntayi, JM, Munene, JC and Malinga, CA (2017). The Relationship Between Access to Finance and Growth of SMEs in Developing Economies : Financial Literacy as a Moderator. Review of International Business and Strategy, Vol. 27, No.4, pp.520 – 538.

- Walsh, S., Gilmore, A. and Carson, D. (2004). Managing and Implementing Simultaneous Transaction and Relationship Marketing. International Journal of Bank Marketing , Vol. 22 , No. 7, pp. 468-83. 7.

- Eisingerich, AB and Bell, SJ (2006). Relationship Marketing in the Financial Services Industry: The Importance of Customer Education, Participation and Problem Management for Customer Loyalty. Journal of Financial Services Marketing , Vol. 10 No. 4, pp. 86-97.

- Laverin, A. and Liljander, V. (2006). Does Relationship Marketing Improve Customer Relationship Satisfaction and Loyalty?. International Journal of Bank Marketing , Vol.24, No.4, pp. 232 – 251. .4.

- El-Deeb, MS, Halim, YT and Kamel, EM (2021). The pillars determining financial inclusion of SMEs in Egypt: Service awareness , access and usage metrics and macroeconomic policies. Future Business Journal, 7(32).

- Rangarajan, C. (2008). Report of The Committee on Financial Inclusion.

- Puspitasasi, S., Mahri, AJW and Utami, SA (2020). Sharia Financial Inclusion Index in Indonesia 2015 – 2018. Amwaluna : Journal of Islamic Economics and Finance, Vol.4, No.1.

- Kalunda, E. (2013). Financial Inclusion Impact on Small-Scale Tea Farmers in Pain County, Kenya. Proceedings of the 6th International Business and Social Sciences Research Conference , 3 – 4 January. Dubai: UAE. U: Dubai.

- Ajide, FM (2019). Financial Inclusion in Africa : Does it Promote Entrepreneurship ?. Journal of Financial Economic Policy.

- Neely, A. , Gregory, MJ and Platts, K. (1995). Performance measurement system design: a literature review and research agenda . International Journal of Operations & Production Management , Vol. 15 No. 4, pp. 80-116. 4.

- Kaplan , RS and Norton, DP (1996). Linking the balanced scorecard to strategy (reprinted from the balanced scorecard). California Management Review , Vol. 39 No. 1, pp. 53-79.

- Trianto, B., Barus, E.E. and Sabiu, T.T. (2021). Relationship between Islamic financial Literacy, Islamic financial inlusion and business performance : Evidence from culinary cluster of creative economy.

- Sanistasya, P.A, Rahardjo, K. and Iqbal, M. (2019). The Effect of Financial Literacy and Financial Inclusion on Small Entreprises Performance in Kaliimantan. Jurnal Economia, Vol15, No.1, 48 – 59.

- Sherril,. GW, Kennedy, H., Cheese, J. And Rushton, A. (1990). Maximizing Marketing Effectiveness. Management Decisions, Vol.8, Iss 2. Emerald Backfiles 2007.

- Cheese, J., Day, A. and Wills, G. (1988). Handbook of Marketing and Selling Bank Services. International Journal of Bank Marketing, Vol.6, Iss 3, pp.3 – 186. Emerald Backfiles 2007. 2007; 3.

- Payne, A. and Frow, P. (2017). Relationship Marketing : Looking Backwards Towards Future. Journal of Services Marketing , 31/1, 11 – 15.

- Wahyuni, S. (2012). Moslem Community Behavior in The Conduct of Islamic Bank: The Moderation Role of Knowledge and Pricing. International Conference on Asia Pacific Business Innovation and Technology Management. Procedia : Social and Behavioral Science 59 : 290-298. [CrossRef]

- Hair, J. F., Hult, G. T. M., Ringle, C. M., and Sarstedt, M. (2014). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Ed. Thousand Oaks, CA: Sage.

- Hair, J.F., Black, W., Babin, B., Anderson, R., & Tatham, R. (2006). Multivariate Data Analysis (6th ed.). Upper Saddle River, NJ : Pearson Prentice Hall.

- Raji, RA, Rashid, S. and Ihhak, S. (2019). The Mediating Effect of Brand Image on The Relationship between Social Media Advertisemnet, Sales Promotion Content and Behavioral Intention. Journal of Research in Interactive Marketing , Vol. 13, No. 3, pp.302 – 330.

- Manisha. (2017). Marketing Communication as a pivotal strategy for banking sector – A study literarute. International journal of Engineering Research & Technology.

- Tantisaowaphap, K. (2001). Measuring effectivenees of integrated marketing communications program in services business. Thesis, Mass communication industrial techno,ogy : consumer behaviour. Bangkok : Chulalongkorn University.

- Mehta, S. (2001). Personal selling – a strategy for promoting banking marketing. State Bank of Indian, Monthly review.

Table 8.

Correaltions Matrix Among Laten Variables

| Variables | Financial Inclusion | Business Performan | Financial Literacy | Marketing Comm |

| Financial Inclusion | 1.00 | |||

| Business Perform | 0.90 | 1.00 | ||

| Financial Literacy | 0.78 | 0.78 | 1.00 | |

| Marketing Comm | 0.64 | 0.63 | 0.79 | 1.00 |

Source : Authors Calculation, 2023.

Table 9.

Structural Model.

| Relationships | Path Coefficients | ||

| Estimate | SE | CR | |

| Marketing Communication on Financial Inclusion | 0.06 | 0.18 | 0.36 |

| Financial Literacy on Financial Inclusion | 0.73 | 0.19 | 3.83* |

| Financial Literacy on Business Performance | 0.21 | 0.11 | 1.90 |

| Financial Inclusion on Business Performance | 0.73 | 0.13 | 5.67* |

CR* = Significant at 0.5 level.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.