Submitted:

25 February 2026

Posted:

27 February 2026

You are already at the latest version

Abstract

This study investigates the compliance–capital adequacy paradox, a condition in which regulatory frameworks intended to strengthen banking stability inadvertently create incentives for greater financial risk-taking. Using panel data from commercial banks in Nigeria, Ghana, Kenya, and South Africa between 2013 and 2024, the research integrates econometric evidence with policy analysis to examine how compliance intensity interacts with capital adequacy in shaping banks’ risk behavior and stability. Employing fixed-effects regressions, the results show that higher capital adequacy ratios significantly reduce credit risk and enhance solvency, whereas increasing compliance costs compress profitability and encourage compensatory risk-taking. The positive interaction term between capital adequacy and compliance expenditure empirically confirms that excessive regulatory burdens can erode the stabilizing intent of prudential reforms. Furthermore, the results demonstrate that heightened exchange-rate fluctuations increase banks’ credit risk exposure. Cross-country analysis shows that governance standards, and supervisory capacity moderate this relationship, with stronger regulatory environments mitigating the paradox. Policy simulations further reveal an optimal equilibrium moderate capital threshold combined with proportional compliance intensity where solvency and financial intermediation remain jointly sustainable. By incorporating compliance costs and currency volatility into the capital adequacy models, the study contributes to the literature on prudential regulation and offers policy guidance for emerging markets on aligning regulatory design with institutional capacity. It concludes that enduring financial stability depends not only on stringent rules but also on context-sensitive and proportionate implementation.

Keywords:

capital adequacy

; regulatory compliance

; basel iii

; financial risk-taking

; prudential regulation

; exchange rate volatility

; sub-saharan africa

; governance quality

; proportional supervision

1. Introduction

The global banking landscape has evolved under the

weight of stringent post-crisis reforms aimed at strengthening solvency and

minimizing systemic fragility. The Basel III framework, advanced by the Basel

Committee on Banking Supervision (BCBS), redefined prudential standards by

reinforcing capital-adequacy requirements and introducing macroprudential

buffers to mitigate cyclical risk accumulation (Basel Committee on Banking

Supervision 2025). While these measures enhance financial resilience, they have

also produced unintended economic and structural side effects. Their

implementation has raised the cost of regulatory compliance, expanded

administrative overhead, and constrained banks’ operational flexibility. This

interplay of stability and strain has given rise to what scholars now describe

as the compliance-capital adequacy paradox—the tendency for regulations

designed to limit excessive risk-taking to unintentionally incentivize it under

certain institutional or market conditions (AlZoubi 2021).

Compliance obligations now represent a substantial

and multidimensional cost center encompassing data-reporting systems, internal

audit functions, supervisory coordination, and risk-governance structures (International

Monetary Fund 2023a). For banks with limited economies of scale, these fixed

costs often absorb a disproportionate share of total income, reducing

efficiency and profitability (Conference of State Bank Supervisor 2025a). The

Conference of State Bank Supervisors reports that compliance expenditure among

small U.S. banks consumes more than one-fifth of net income (Conference of

State Bank Supervisor 2025b), a burden even more pronounced in developing economies

where resource constraints and technological gaps persist. In many Sub-Saharan

African countries, including Nigeria, Kenya, and Ghana, compliance with

Basel-aligned governance, anti-money-laundering, and capital-reporting

frameworks consumes an increasing proportion of administrative budgets. To

buttress this point, Claassen and Van Rooyen argue that compliance with

Basel-aligned governance comes with a high cost implication, especially for

deposit-money banks in developing countries (Claassen and Van Rooyen 2012).

Nigerian deposit-money banks, for instance, channel substantial resources

toward compliance monitoring, staff training, and automated reporting systems,

thereby shrinking lending margins and discouraging long-term credit extension (Ozili

2021). As compliance expenditures rise, banks frequently pursue compensatory

high-yield, high-risk lending strategies to restore profitability, generating

an unintended shift in portfolio behavior (Davis and Singh 2024).

Capital-adequacy regulations, designed to ensure

that banks hold sufficient loss-absorbing capital relative to their

risk-weighted assets, play an equally central role in shaping institutional

behavior. Under Basel III and the forthcoming Basel 3.1 reforms, banks are

required to maintain higher-quality Tier 1 capital, conservation buffers, and

leverage-ratio ceilings (Beyer and Meyer 2012; Hunjra, Tayachi, and Mehmood

2020; Johansson 2012). The BCBS maintains that these measures reduce default

probability and enhance the credibility of financial intermediation (Basel

Committee on Banking Supervision 2025). Yet empirical studies reveal mixed

outcomes. Davis and Singh found that higher capital buffers reduce systemic

vulnerability but compress profitability in competitive banking systems (Davis

and Singh 2024), while Al Hunjra et al. observed that capital tightening in

South Asian markets curbed default risks yet encouraged riskier revenue

generation to sustain shareholder returns (Hunjra, Tayachi, and Mehmood 2020).

This empirical ambiguity suggests that capital regulation may produce

countervailing behavioral effects when combined with rising compliance costs,

particularly where competition and profitability pressures are intense.

The paradox is therefore structural as well as

behavioral. When regulated banks face compressed profitability due to

simultaneous capital and compliance pressures, credit activity often shifts to

non-bank financial intermediaries, microfinance institutions, fintech lenders,

and informal credit channels operating outside formal prudential oversight. Lee

et al. (2024) demonstrated that South Korean banks constrained by capital

reforms reduced on-balance-sheet lending by nearly one-quarter, while shadow

credit expanded proportionally (Lee, Lee, and Paluszynski 2024). Similar

patterns have been observed in Nigeria and Kenya, where digital-finance firms

have absorbed displaced credit, shifting systemic risk into unsupervised

domains (International Monetary Fund 2024a). These spillovers dilute the

effectiveness of prudential regulation and complicate monetary-policy

transmission.

From a quantitative perspective, the

compliance–capital adequacy paradox can be expressed through the elasticity of

bank risk-taking relative to compliance costs and capital buffers. As

compliance intensity increases, the marginal cost of maintaining prudence

rises, while the marginal benefit of holding additional capital diminishes

beyond an optimal threshold. Beyond this equilibrium, further regulatory

tightening can invert the intended stability effects, encouraging compensatory

risk-taking and reducing financial-intermediation efficiency (World Bank 2024b).

This dynamic implies that there exists a zone of regulatory proportionality

where solvency and profitability objectives are jointly optimized.

Exchange rate volatility refers to unpredictable

fluctuations in the value of a nation’s currency relative to others, often

driven by changes in interest rates, inflation, capital flows, and

macroeconomic policy shifts. In the context of banking stability, exchange rate

volatility introduces additional layers of uncertainty that complicate the

compliance–capital adequacy relationship. When currency values fluctuate

sharply, banks holding foreign-denominated assets or liabilities face valuation

losses that strain their capital buffers, even when they remain compliant with

regulatory standards. This dynamic amplifies the compliance–capital adequacy

paradox: institutions adhering to prudential rules may still engage in riskier

asset allocations or short-term hedging strategies to offset exchange-related

exposures. Consequently, heightened volatility can weaken the stabilizing

intent of capital adequacy frameworks, pushing banks toward behaviors that

prioritize capital preservation over long-term financial soundness.

For policymakers, the challenge lies in maintaining

this balance. Such proportional regulation would prevent smaller and mid-tier

banks from being overburdened by one-size-fits-all compliance frameworks designed

for systemically important banks. Achieving this equilibrium is particularly

important in Sub-Saharan Africa, where banking sectors are concentrated,

financial inclusion remains incomplete, and supervisory capacity is still

evolving. A well-calibrated regulatory architecture must therefore strengthen

capital positions without undermining credit intermediation or incentivizing

regulatory arbitrage.

Despite its importance, empirical research that

jointly examines compliance intensity, exchange rate volatility, capital

adequacy, and risk-taking behavior remains limited. Most existing studies

address these elements separately, overlooking how they interact under

different governance and institutional regimes. This study seeks to fill that

gap by empirically analyzing how regulatory compliance obligations, exchange

rate volatility and capital adequacy jointly shape the risk-taking behavior of

banks across selected emerging and Sub-Saharan African markets. By integrating

quantitative analysis with policy interpretation, the research contributes to

both academic and practical understanding of how proportional regulation can

promote solvency, preserve intermediation efficiency, and minimize unintended

risk incentives in developing financial systems.

Existing literature inadequately captures the

multidimensional interaction between compliance intensity, capital adequacy,

and exchange rate volatility in shaping bank risk behavior. Prior studies often

isolate these variables, focusing either on regulatory compliance or capital

adequacy as independent determinants of financial stability, without

considering the mediating role of exchange rate fluctuations. Moreover, there

is limited empirical evidence from Sub-Saharan Africa, where currency

instability and weak institutional frameworks may amplify or distort these

relationships. This research fills these gaps by constructing an integrated

analytical model that accounts for regulatory, financial, and macroeconomic

linkages within emerging market contexts.

Therefore, the objectives of the study are (a). to

examine the joint impact of compliance intensity, exchange rate volatility, and

capital adequacy on banks’ risk-taking behavior in selected emerging and

Sub-Saharan African economies; (b) to identify the conditions under which

prudential regulations enhance or undermine financial stability in volatile

macroeconomic environments and; (c) to propose policy recommendations that

balance regulatory stringency with financial sector resilience and growth.

This study is justified by the growing policy

challenge of designing effective regulatory frameworks that preserve financial

stability without stifling intermediation in developing economies. Given that

exchange rate volatility often exposes systemic vulnerabilities in undercapitalized

or compliance-strained banks, understanding this triadic interaction is

critical for effective macroprudential oversight. The research focuses on

selected emerging and Sub-Saharan African countries with comparable regulatory

reforms and exposure to currency instability between 2010 and 2024. The scope

covers commercial banks whose financial and compliance data are publicly

available, emphasizing comparative econometric analysis and cross-country

institutional variation to generate evidence-based insights for policymakers

and regulators.

2. Literature Review

2.1. Compliance Intensity and Bank Risk-Taking

Financial regulation evolved as a corrective

mechanism to address market failures inherent in banking systems. Banks

transform short-term deposits into long-term loans, creating maturity

mismatches that expose them to liquidity and solvency risk. When these risks

materialize, the effects often extend systemically. Prudential regulation

therefore aims to internalize the social cost of instability by imposing

minimum standards for capital, liquidity, and governance (Goodhart 2005; Korinek

2011). The Basel III framework, established by the Basel Committee on Banking

Supervision, codifies this through global capital and supervisory benchmarks

(Pernell 2024). Moral-hazard theory explains that in the absence of oversight,

banks may take excessive risk because depositors cannot fully observe their

actions. When institutions expect public support during crises, risk-taking

intensifies. Capital requirements reduce this asymmetry by ensuring

shareholders bear a higher share of losses (Allen, Carletti, and Gu 2019; Merton

and Perold 2008). Agency theory complements this perspective, focusing on

conflicts between managers, owners, and regulators. Managers pursue profit

maximization, regulators emphasize prudence, and depositors seek security.

Excessive capital and compliance constraints, however, can provoke risk

substitution where banks shift to less regulated or opaque assets to preserve

profitability (Carletti 2008).

Compliance itself functions as a governance

mechanism that enforces procedural discipline and transparency. It aims to

reduce operational and legal risk by ensuring conformity with statutory and

supervisory expectations (Chronopoulos, Wilson, and Yilmaz 2023; Nandan Prasad

2024). Yet compliance demands also consume significant financial resources,

affecting profitability and efficiency. Studies show that smaller and regional

banks suffer disproportionately due to limited economies of scale (Avgouleas

and Goodhart 2015). The Conference of State Bank Supervisors reports that

compliance expenditures can exceed 20% of community-bank net income (Basel

Committee on Banking Supervision 2024). These costs, when excessive, can

indirectly foster greater risk-taking as banks seek higher yields to compensate

(Ben Bouheni and Hasnaoui 2017). Chronopoulos, Wilson, and Yilmaz empirically

demonstrate that heightened regulatory oversight reduces operational efficiency

but stimulates portfolio risk-taking in European banks (Chronopoulos, Wilson,

and Yilmaz 2023). Similar findings appear in African markets, where compliance

spending has expanded faster than revenue growth, constraining profitability

and altering risk preferences (Bank for International Settlements 2025a).

Regulatory arbitrage further amplifies this issue: as regulatory costs

increase, banks shift risky activities to shadow markets or fintech

subsidiaries beyond direct supervision (International Monetary Fund 2024b).

Uniform global rules may produce uneven effects, disadvantaging smaller banks

in emerging economies. The Bank for International Settlements and the World

Bank recommend proportional frameworks that balance prudential control with

efficiency (World Bank 2025). African evidence reinforces this. Wodi and

Gržeta, Žiković, and Tomas Žiković show that excessive Basel III compliance

burdens depress profitability (Gržeta, Žiković, and Tomas Žiković 2023; Wodi

2011), while Ajao and Oseyomon confirm a link between compliance spending and

credit risk in Nigerian banks (Ajao and Oseyomon 2019).

Collectively, the literature converges on the

notion that regulation, while essential for stability, can induce behavioral

adaptations that increase systemic vulnerability if poorly calibrated. The

compliance–capital-adequacy paradox thus sits at the intersection of prudential

logic and market adaptation, revealing the non-linear nature of risk responses

under evolving global regulatory standards.

The compliance–capital-adequacy paradox describes

the counterintuitive outcome in which two regulatory instruments designed to

reinforce stability capital-adequacy standards and compliance obligations can

interact in ways that elevate, rather than reduce, financial risk. The paradox

emerges from the dynamic feedback between direct solvency controls and indirect

behavioral constraints. Both mechanisms intend to strengthen prudential

soundness, yet their simultaneous intensification may alter managerial

incentives and risk preferences within banks (Ben Bouheni and Hasnaoui 2017).

The paradox originates in the intersection of

capital regulation and compliance economics. Capital-adequacy rules are direct

constraints that set minimum equity or Tier 1 ratios relative to risk-weighted

assets, thereby limiting leverage. Compliance obligations, conversely, are

indirect behavioral constraints that impose procedural discipline through

monitoring, reporting, and internal-governance requirements (Baer 2009). Each

mechanism individually promotes stability. However, when imposed concurrently

at high intensity, they can produce nonlinear effects on managerial

decision-making and portfolio composition.

The conceptual roots can be traced to the

risk-compensation hypothesis, which posits that when constraints limit one

dimension of risk, economic agents increase exposure in others to preserve

target returns (Bank for International Settlements 2025a). In banking, stricter

capital requirements raise funding costs, while heavier compliance regimes

elevate operational expenditure. Both reduce return on equity. Managers under

performance pressure may offset this decline by seeking higher-yield,

higher-risk assets. Consequently, the intended prudential safeguards may be

undermined by rational responses to profitability erosion (Bank for

International Settlements 2025a; International Monetary Fund 2024b). Empirical

studies increasingly confirm this behavior. Bouheni and Hasnaoui demonstrate

that post-Basel III compliance intensity in OECD banks reduced net-interest

margins but simultaneously increased risk-weighted asset accumulation (Ben

Bouheni and Hasnaoui 2017). Similarly, in emerging-market contexts, excessive

compliance expenditures are associated with substitution toward

off-balance-sheet financing and speculative instruments (World Bank 2025). The

paradox thus arises not from regulatory inefficiency per see but from the

interaction of complementary constraints that, when misaligned, amplify

risk-taking incentives (Bank for International Settlements 2025b; International

Monetary Fund 2024b).

In perfectly competitive markets, where profit

margins are thin, these effects intensify. Banks with limited pricing power

cannot easily transfer compliance costs to borrowers through higher loan

spreads. Instead, they adjust portfolios toward assets with greater

risk-adjusted yields or reduce the transparency of exposures to circumvent

capital charges (International Monetary Fund 2024c). This behavior reflects

what the Bank for International Settlements identifies as a compliance–risk

elasticity, where each incremental rise in compliance expenditure triggers

proportionate risk substitution in balance-sheet composition (Basel Committee

on Banking Supervision 2006). At the systemic level, the paradox generates

procyclicality. During economic expansions, strong earnings mask compliance

costs, sustaining both capital and prudential discipline. During downturns,

however, falling profitability magnifies the relative cost of compliance and

capital buffers, driving institutions to pursue higher returns or relax

internal controls. The effect can reinforce credit cycles, increasing systemic

vulnerability precisely when stability is most needed (European Banking

Authority 2024a).

The distinction between direct and indirect

regulatory constraints is fundamental to understanding the paradox.

Capital-adequacy requirements constitute quantitative solvency controls—they

directly determine the ratio of capital to risk-weighted assets. Their effect

is measurable, immediate, and enforceable through supervisory ratios. Compliance

obligations, in contrast, function as qualitative behavioral controls—they

shape decision processes rather than balance-sheet positions. Their enforcement

depends on institutional governance, audit capacity, and regulatory credibility

(European Banking Authority 2023a). While capital adequacy reduces leverage

risk through numerical limits, compliance enhances transparency and procedural

integrity. The two mechanisms intersect when compliance costs erode the

financial slack that capital buffers are designed to preserve. When compliance

becomes excessively resource-intensive, it indirectly weakens solvency

objectives by compressing profitability and constraining internal capital

generation. The resulting managerial adaptation pursuing higher-risk assets to

offset compliance costs creates the paradoxical feedback loop between

behavioral and prudential regulation (Ben Bouheni and Hasnaoui 2017; International

Monetary Fund 2024b). Furthermore, capital adequacy operates at the

macroprudential level, targeting aggregate stability, whereas compliance

functions at the microprudential level, targeting institutional conduct.

Misalignment between these layers can yield perverse outcomes: macroprudential

tightening that ignores micro-level compliance burdens can amplify systemic

risk through behavioral responses (European Banking Authority 2023b). The

paradox therefore represents a failure of regulatory complementarity. When

capital and compliance policies are harmonized proportionally, they reinforce

stability; when they are implemented asymmetrically, they distort incentives.

The conceptual insight is that risk is not only a product of inadequate

regulation but also of excessive or misaligned regulation. A nuanced

equilibrium one that calibrates capital requirements and compliance intensity

to institutional capacity is essential to sustain both stability and efficiency

in financial intermediation (Basel Committee on Banking Supervision 2006; European

Banking Authority 2023b).

The impact of compliance on cost efficiency is

empirically observable in standard efficiency metrics. Data envelopment and

stochastic frontier analyses show that higher compliance spending reduces measured

cost efficiency after controlling for size, product mix, and market

competition. Banks in the upper quartile of compliance intensity display lower

cost efficiency scores, higher cost to income ratios, and reduced cost of funds

when compared with peers that achieve similar regulatory outcomes at lower

expense (Reuters 2024). These efficiency losses translate into narrower lending

margins because banks with elevated compliance costs must either accept

compressed net interest margins or price loans higher, which in turn reduces

demand and market share.

Empirical work also links compliance spending to lending

behavior and credit allocation. When compliance costs rise materially, banks

exhibit three adaptive responses. One, they reduce small ticket lending where

per-loan compliance checks are expensive relative to yield. Two, they increase

screening and documentation standards, which raises origination time and

reduces turnover for retail and SME borrowers. Three, they reprice credit

toward segments with higher yields or lower compliance intensity, such as large

corporates with established KYC profiles. Studies using loan-level data find

that increases in a bank’s compliance expenditure ratio are associated with a

statistically significant decline in SME lending growth over a two-year

horizon, controlling macro conditions and capital adequacy (Bank of Ghana

2024a).

The effect on innovation is mixed but notable.

Compliance requirements create both constraints and incentives for

technological adoption. On one hand, heavy compliance burdens spur investment

in regtech, automated KYC, and digital audit trails that, over time, can lower

unit costs and improve operational resilience. On the other hand, high initial

compliance costs and uncertain regulatory acceptance discourage smaller banks

from investing in innovation because payback periods are long, and regulatory

risk is non-trivial. Empirical surveys show that smaller banks are less likely

to adopt advanced regtech solutions absent subsidy or regulatory guidance,

perpetuating the cost gap with larger institutions (Bank of Ghana 2024b).

There is also a competitive dimension. Elevated

compliance costs can alter market structure by increasing barriers to entry and

favoring incumbents able to bear scale costs. Empirical cross-country analyses

indicate that in jurisdictions where compliance burdens rose sharply after

post-crisis reforms, market concentration increased modestly as smaller banks

exited or merged, and fintech entrants filled narrow niches rather than

replicating broad banking services (Central Bank of Nigeria 2025). This

structural shift has distributional consequences for credit access and can

exacerbate financial exclusion in underbanked regions.

Policy evaluations emphasize proportionality and

capacity building as remedies to these scale effects. Targeted measures include

tiered reporting thresholds, shared compliance utilities, regulatory sandboxes

for regtech adoption, and technical assistance to reduce fixed cost burdens on

smaller banks. Empirical pilot programs that subsidize shared compliance

platforms show significant reductions in per-unit compliance costs and

measurable recoveries in SME lending growth, suggesting that policy design can

moderate adverse efficiency and allocation effects identified in observational

studies (Bank for International Settlements 2025b).

Empirical evidence demonstrates a clear compliance

cost asymmetry across bank size and business model. Higher compliance

expenditure ratios are associated with lower cost efficiency, compressed

lending margins, reduced SME credit, and slower adoption of advanced compliance

technologies among smaller institutions. Policy responses that implement

proportionality, shared services, and regtech support mitigate these effects

and preserve the balance between prudential objectives and efficient financial

intermediation (Bank of Ghana 2024a, 2024b; Central Bank of Nigeria 2025; Gambacorta

and Shin 2018; International Monetary Fund 2024d; TheCable 2025).

Compliance obligations reshape banks’ incentive

structure. Heavy regulatory reporting and continuous auditing increase

monitoring costs and constrain managerial discretion. Institutions respond not

only by strengthening controls but also by adjusting risks taking to protect

profitability. The behavioral response typically follows two paths. One path

reduces risk through tighter internal controls and lower appetite for speculative

positions. The alternative path increases risk via yield enhancement, balance

sheet reweighting, or migration of activity off the balance sheet when

compliance costs and reporting burdens compress margins or slow business

processes (Bank for International Settlements 2025b; Chronopoulos, Wilson, and

Yilmaz 2023; International Monetary Fund 2024b).

Reporting intensity and audit scrutiny produces

observable behavioral changes. Mandatory granular reporting raises the

frequency and visibility of exposures to supervisors and counterparties. Where

audit quality and regulatory enforcement are credible, this transparency tends

to lower opportunistic behavior and tighten risk limits (Bepari, Nahar, and

Mollik 2024; Darmawan 2023). Empirical work finds that enhanced auditor

reporting to regulators is associated with reduced measured bank risk and

narrower credit spreads, consistent with improved market discipline and higher

information quality (International Monetary Fund 2024a). However, the same

transparency can produce perverse incentives when compliance is costly relative

to the returns available in traditional lending. In that case, banks shift

toward activities that generate yield but face looser capital or reporting

treatment, including securitisation, derivatives trading, and off-balance-sheet

vehicles (Bank for International Settlements 2025b; Chronopoulos, Wilson, and

Yilmaz 2023; International Monetary Fund 2024c).

Several empirical studies document that compliance

overheads correlate with increases in off-balance-sheet exposures and trading

activity. Chronopoulos, Wilson and Yilmaz show that changes in regulatory

oversight in the United States encouraged treated banks to reallocate risk between

on- and off-balance-sheet items, with a measurable rise in derivative positions

and securitised exposures after compliance intensification (Chronopoulos,

Wilson, and Yilmaz 2023). Bouheni and Hasnaoui report similar patterns across

European banks under Basel III, where higher compliance spending co-occurred

with increases in risk-weighted asset intensity driven by market exposures

rather than traditional loan books (Ben Bouheni and Hasnaoui 2017). Lee, Lee

and Paluszynski document shadow credit growth when banking constraints tighten,

indicating migration of lending outside standard supervisory perimeters (Lee,

Lee, and Paluszynski 2024).

Yield enhancement is a proximate mechanism for

strategic risk taking under heavy compliance burdens. When compliance costs

raise the effective expense base, banks face a simple margin problem: either

accept compressed net interest margins or seek higher yielding assets.

Empirical panel estimates indicate that banks with rising compliance

expenditure ratios tend to reprice credit toward higher yield segments or

expand trading and fee income activities that are less capital intensive in

accounting terms (Bank of Ghana 2024a; Chronopoulos, Wilson, and Yilmaz 2023; Reuters

2024). This repricing increases portfolio yield but also concentrates exposure

in cyclical or volatile sectors, elevating credit risk and return volatility.

Regulatory reporting and audit cycles also affect

model and pricing behaviour. Continuous supervisory reporting forces banks to

rely on standardised pricing models and stricter provisioning rules. Some

institutions respond by shortening loan tenors, increasing collateral

requirements, or focusing on borrowers with higher credit grades. Others widen

credit origination standards in higher yield segments where the cost of

monitoring per unit of return is lower. Loan-level studies show a decline in

small ticket and SME lending where compliance checks are intensive, and a contemporaneous

increase in large corporate and market-based lending among banks seeking scale

efficiencies (Chronopoulos, Wilson, and Yilmaz 2023; Mateev, Tariq, and

Sahyouni 2021).

Compliance-driven business model adjustments are

evident in case studies and cross-country regressions. Large banks invest in

regtech and centralized control rooms to reduce per-unit compliance costs and

preserve low-risk business lines. Smaller banks often lack that scope and

instead pivot toward niche high-yield services or subcontract compliance

functions to third parties. This divergence produces measurable heterogeneity

in risk appetite across the sector. Kolapo et al. report that Nigerian banks

under significant compliance pressure increased exposure to consumer and retail

segments with higher yield but higher default correlations, raising systemwide

nonperforming loan risk (kolapo, Ayeni and Oke 2012). Chronopoulos, Wilson and

Yilma’s US evidence shows similar migration in mid-sized banks following

intensified regulatory reporting (Chronopoulos, Wilson, and Yilmaz 2023).

Auditing intensity interacts with compliance costs

to produce mixed outcomes. High quality external and regulatory audits improve

reporting credibility and can deter opportunistic risk taking. IMF find that

auditor reporting to regulators reduces bank risk metrics and promotes market discipline

(International Monetary Fund 2024b). Yet rising audit and consulting fees are a

component of compliance overheads. Where audit costs are large and management

uses external consultants to manage regulatory submissions, empirical evidence

links those cost structures to short term reductions in reported risk but longer-term

increases in complex exposures once the initial compliance cycle is absorbed (Basel

Committee on Banking Supervision 2025; Conference of State Bank Supervisor

2025b).

Policy studies emphasise that the net effect of

compliance on strategic risk taking depends on proportionality, capacity

building, and aligned incentives. Where regulators provide proportionate

reporting thresholds, shared compliance utilities, and facilitate regtech

adoption, banks are more likely to absorb compliance costs without resorting to

risk migration (Basel Committee on Banking Supervision 2006). Without such

support, smaller and mid-sized banks face economically rational incentives to substitute

into higher-yield, less transparent activities that undermine systemic

transparency and raise tail risk.

The empirical record shows that heavy regulatory

reporting and auditing produce heterogeneous behavioural responses. Credible,

proportionate supervision tends to reduce risk through improved disclosure and

governance. Heavy compliance overheads, particularly when combined with binding

capital constraints or compressed margins, incentivise yield enhancement,

off-balance-sheet migration, and business model adjustments toward riskier

activities. Regulatory design that reduces asymmetrical compliance burden while

enhancing transparency and supervisory capacity mitigates the strategic

risk-taking channel. Cross sectional studies using matched samples exploit

variation in regulatory shocks to identify the joint effects. Bouheni and

Hasnaoui compare banks across European countries with differing compliance

intensities following Basel III rollouts (Ben Bouheni and Hasnaoui 2017). Their

cross sectional regressions indicate that well capitalized banks in high

compliance environments exhibit higher risk-weighted asset growth than similarly

capitalized peers in lower compliance jurisdictions, consistent with risk

substitution and regulatory arbitrage (Bouheni and Hasnaoui 2017). Jallow

extend this approach to an African sample and show that compliance expenditure

ratios significantly predict higher NPLs among banks with CET1 above a

threshold, pointing to the compliance–capital interaction as a driver of credit

deterioration in constrained markets (Jallow 2025).

Panel studies that combine bank balance sheet data

with matched supervisory and compliance cost indicators deliver richer

inference on timing and mechanisms. In countries with strong supervision,

higher capital improves Z-scores uniformly; in countries with high compliance

costs and weak enforcement, the capital effect is attenuated or reversed (International

Monetary Fund 2024c). The Bank for International Settlements emphasizes that

such conditionality is crucial for interpreting cross-country capital studies

and for designing proportional frameworks (Bank for International Settlements

2021). A related strand deploys micro level loan data combined with bank level

compliance measures. These studies examine how compliance and capital jointly

influence lending selection, provisioning and subsequent loan performance.

Loan-level logistic regressions and hazard models show that banks facing higher

compliance expenditure ratios reduce small ticket approvals and increase

collateral demands. Where capital buffers are also high, the net effect on loan

default probability is ambiguous: higher buffers lower default probability

conditional on conservative screening, but when screening relaxes because banks

seek yield, NPL incidence rises, revealing an interaction between compliance

induced cost pressure and capital driven return targets (Bank for International

Settlements 2021). Quantitative findings often converge on a non-linear

interaction. This produces a threshold or U-shaped relationship between capital

and risk when compliance is modeled explicitly (Gambacorta and Shin 2018).

Sensitivity analyses using different compliance proxies corroborate robustness:

proxies include compliance expenditure as a share of operating income, number

of supervisory breaches, and a binary indicator of major remediation events.

Each proxy yields qualitatively similar interaction effects, though coefficient

magnitudes vary.

2.2. Capital Adequacy and Financial Stability

Empirical analysis of capital adequacy and risk-taking

provides mixed evidence regarding how prudential regulation affects bank

behavior and systemic stability. The conventional premise is that higher Tier 1

capital ratios enhance resilience by ensuring that institutions possess

sufficient loss-absorbing capacity. Studies (Nguyen and Nghiem 2015; Nyambuu

and Bernard 2015) across emerging economies confirm that capital strength

generally lowers default probabilities but may also compress profitability,

creating offsetting incentives for increased risk exposure. Bank for

International Settlements finds that post-crisis capital reforms in the

European Union significantly reduced leverage and funding volatility, but

profitability pressures led some banks to pursue riskier credit exposures .

Similarly, the Basel Committee’s global quantitative impact studies report that

Tier 1 capital ratios improved substantially between 2013 and 2023, yet average

return on equity for major banks declined by nearly 25 percent, particularly

among institutions with limited diversification capacity (Bank for

International Settlements 2021; Basel Committee on Banking Supervision 2025).

The relationship between capital regulation and

financial stability remains conditional on market structure and enforcement

credibility. In advanced economies, where supervisory monitoring is consistent,

capital buffers act as credible deterrents to excessive leverage. Empirical

findings from the United States, the Eurozone, and Japan show that banks

maintaining Tier 1 ratios above 10 percent display lower probability of default

and reduced exposure to market shocks (Federal Reserve Board 2023). However,

Davis and Singh demonstrate that in highly competitive markets, profitability

compression under stringent capital rules induces marginal increases in

risk-weighted asset concentration (Davis and Singh 2024). These findings

suggest that stability gains depend on how efficiently institutions internalize

capital costs without offsetting them through risk substitution. Evidence from

Basel II and Basel III implementation further illustrates the evolving impact

of regulatory tightening. Under Basel II, capital standards were primarily

risk-sensitive, allowing banks to use internal ratings-based models to compute capital

requirements. This flexibility led to regulatory arbitrage as institutions

underreported risk weights to minimize capital charges. Basel III addressed

these deficiencies through a more robust common equity Tier 1 (CET1)

requirement, leverage ratios, and countercyclical buffers (Basel Committee on

Banking Supervision 2025). Empirical assessments by the Bank for International

Settlements (2025a) and Chronopoulos, Wilson and Yilmaz show that Basel III

materially improved capital quality and liquidity coverage but generated higher

compliance and reporting costs, particularly for medium-sized banks (Bank for

International Settlements 2025a; Chronopoulos, Wilson, and Yilmaz 2023).

Cross-country studies reinforce this trade-off.

Bouheni and Hasnaoui analyzed 58 OECD banks from 2012–2023 and reported that

every one-percentage-point increase in CET1 ratio corresponded to an average

0.5 percent decline in return on assets (Ben Bouheni and Hasnaoui 2017). Yet,

risk-weighted asset volatility also decreased by 4 percent, indicating a net

improvement in resilience. In contrast, Adeyemi find that Nigerian banks

exposed to Basel III compliance requirements experienced cost-driven increases

in nonperforming loans, consistent with the compliance–capital paradox observed

by Bouheni and Hasnaoui and International Monetary Fund (Adeyemi 2011). From a

macroprudential perspective, capital adequacy interacts with credit supply and

systemic risk transmission. International Monetary Fund finds that in emerging

markets, elevated capital buffers reduced aggregate credit growth by nearly 3

percent annually between 2018 and 2022 (International Monetary Fund 2024c). The

contractionary effect was most pronounced in small and medium banks lacking

access to alternative funding. Similar conclusions emerge from the

International Monetary Fund’s Global Financial Stability Report (European

Banking Authority 2024a), which identifies a tightening of bank lending

standards in response to rising capital and compliance costs. These findings

imply that while capital regulation strengthens solvency, it may suppress

credit intermediation and slow economic recovery during stress periods.

Policy evidence from OECD economies shows that the

introduction of Basel III countercyclical buffers has moderated procyclicality

in risk-weighted assets. Banks subject to buffer activation reduced dividend

distributions and increased retained earnings to absorb shocks, supporting

long-term solvency (Bank for International Settlements 2021; European Banking

Authority 2024a). However, these prudential adjustments are uneven across

jurisdictions. In the Eurozone, strong supervisory cohesion allowed coordinated

implementation, while in emerging markets, fragmented oversight and resource

constraints weakened enforcement. Barth, Caprio and Levine note that the

absence of uniform supervisory standards causes inconsistent capital effects

across banking systems (Barth, Caprio, and Levine 2013).

Another dimension concerns the

profitability–stability nexus. Davis and Singh identifies a negative correlation

between return on equity and Tier 1 ratios, with diminishing marginal returns

beyond the 12 percent threshold (Davis and Singh 2024). The World Bank reports

similar outcomes, indicating that higher capital ratios, while stabilizing,

create long-term pressure on cost efficiency (World Bank 2024b). These

empirical findings explain why some institutions respond to capital tightening

through portfolio adjustments toward high-yield sectors such as consumer

lending and real estate, which increases risk-weighted exposure.

In countries with robust governance and reliable

enforcement, higher capital ratios lead to lower credit risk and improved

liquidity buffers (Thibaut, Terajima, and Yang 2024). Conversely, in weaker

institutional contexts, compliance is often procedural, producing minimal

improvement in risk discipline but significant cost escalation. The IMF

observes that compliance costs in sub-Saharan African banks average 3–5 percent

of total expenditures, eroding profitability and capital retention (International

Monetary Fund 2024b). As a result, the intended benefits of Basel III are

partially offset by behavioral adaptations that elevate aggregate systemic

risk.

A growing body of quantitative evidence now models

these dynamics using panel econometric frameworks. Empirical models also

underscore that capital regulation interacts with liquidity and profitability

metrics. Hunjra, Tavachi and Mehmood find that liquidity coverage ratios and

Tier 1 capital jointly predict bank soundness more effectively than either

measure alone (Hunjra, Tayachi, and Mehmood 2020). Yet, in competitive markets,

high capital buffers amplify pressure to expand risky lending to maintain

target profitability. This phenomenon confirms that financial stability

objectives cannot rely solely on quantitative capital thresholds but must

integrate qualitative supervision and proportional policy design.

The Bank for International Settlements and the

World Bank recommend proportional capital requirements for small and medium

banks to mitigate compliance burdens while preserving solvency (Bank for

International Settlements 2021; World Bank 2024b). Cross-sectional data from 64

emerging economies confirm that proportionate implementation reduces

risk-weighted asset volatility and sustains credit supply. The balance between

solvency assurance and operational flexibility remains central to achieving

stable and inclusive financial systems.

Overall, the literature reveals that while higher

capital adequacy strengthens resilience and investor confidence, excessive or

misaligned capital accumulation can distort bank incentives, restrict credit

supply, and intensify risk-taking behavior. These findings reinforce the

compliance–capital adequacy paradox established earlier, emphasizing the

importance of context-sensitive prudential design. Capital regulation thus

serves as both a stabilizer and a potential catalyst of behavioral risk

adaptation, depending on how it interacts with profitability dynamics and

supervisory enforcement.

Empirical research increasingly demonstrates that

beyond optimal thresholds, excessive capitalization may induce unintended risk

substitution and distort banks’ portfolio allocation. The rationale is grounded

in the diminishing returns of prudential capital accumulation: as capital

buffers rise beyond regulatory minima, their marginal contribution to solvency

decreases while their cost of equity increases. Well-capitalized institutions,

under shareholder and managerial pressure to sustain return on equity, may

consequently shift toward higher-yield, risk-intensive assets (Ben Bouheni and

Hasnaoui 2017; Davis and Singh 2024; International Monetary Fund 2024b). This

behavior aligns with the risk compensation hypothesis, which posits that when

one form of risk is constrained, leverage institutions increase exposure along

other dimensions to preserve profitability (Bank for International Settlements

2025a; Gambacorta and Shin 2018). Empirical evidence from OECD and Basel III

jurisdictions supports this mechanism. International Monetary Fund finds that

banks in the top quartile capital ratios expanded lending to cyclical and

high-volatile sectors, including real estate, energy, and speculative trading (International

Monetary Fund 2024d). In contrast, institutions near minimum capital thresholds

maintained conservative asset compositions. The result illustrates a paradox of

over-capitalization, where prudential strength coexists with increased

portfolio risk. International Monetary Fund and Bouheni and Hasnaoui confirm

this pattern across 15 European banking systems, reporting that overcapitalized

banks exhibited a 9 percent increase in risk-weighted asset intensity between

2016 and 2022 (Ben Bouheni and Hasnaoui, 2017; International Monetary Fund,

2024b). This increase stemmed largely from expansion into higher-risk sovereign

and corporate exposures rather than retail lending.

Several mechanisms explain this phenomenon. First,

excess equity reduces leverage benefits, prompting management to compensate

through riskier investment choices to sustain shareholder returns. Second,

market discipline weakens when capital buffers are perceived as excessive,

leading investors and supervisors to underestimate residual risk. Third,

regulatory calibration often fails to adjust for sectoral or macroeconomic

context, meaning that uniform capital targets may produce uneven behavioral

outcomes across institutions of varying scale and risk appetite (Basel

Committee on Banking Supervision 2006; World Bank 2024b).

Quantitative evidence from U.S. and Eurozone

banking panels reveals nonlinear effects. Andersen and Juelsrud shows that

while increasing Tier 1 ratios from 8 percent to 12 percent reduces

nonperforming loan ratios by 15 percent, further increments to 16 percent reverse

this benefit, raising average risk-weight exposure by 6 percent (Andersen and

Juelsrud 2024). Similarly, Bank of Ghana finds that European global

systemically important banks (G-SIBs) with Tier 1 ratios above 15 percent

allocated a higher share of assets to Level 2 and Level 3 fair-value

instruments, reflecting migration into less transparent, higher-yield markets (Bank

of Ghana 2024a). This supports the hypothesis that risk behavior adapts

endogenously to capital accumulation.

Studies also document regional variations in the

magnitude of these substitution effects. In Asia-Pacific and the Middle East,

where market competition and profit margins are tighter, overcapitalization

pressures are more pronounced. Nkwaira and Kruger find that after the

introduction of Basel III leverage constraints, banks with excess capital

increased lending to risk-weighted categories by 4.3 percent on average.African

banks subject to Basel-aligned requirements display similar tendencies (Nkwaira

and Kruger 2018).Abba et al. report that Nigerian deposit money

banks with CET1 ratios above 15 percent expanded credit exposure to volatile

consumer sectors, increasing nonperforming loans by 2.7 percent within two

years (Abba et al. 2018). Post-Basel III cross-sectional analyses further show

that high capital levels may contribute to risk migration from balance sheet to

off-balance-sheet activities. Chronopoulos, Wilson and Yilmaz demonstrate that

European banks with elevated CET1 ratios substantially increased derivative

trading volumes relative to loan book growth between 2015 and 2023 (Chronopoulos,

Wilson, and Yilmaz 2023). The shift reflects a strategic reallocation toward

fee-generating and market-based assets that maintain profitability under

tighter capital regulation. Avgouleas and Goodhart interpret this trend as a

new form of regulatory arbitrage facilitated by financial innovation and

differential capital treatment of trading exposures (Avgouleas and Goodhart

2015).

The World Bank and the Bank for International

Settlements identify this behavior as a secondary systemic risk channel arising

from well-capitalized but return-constrained institutions (Bank for

International Settlements 2021; World Bank 2024b). Overcapitalized banks are

more likely to engage in cross-border risk transfers, securitization, and

proprietary trading, which can amplify volatility during stress periods.

Well-capitalized banks often expand lending aggressively to capture market

share, potentially crowding out smaller institutions with thinner buffers. This

competitive displacement may increase systemic concentration and reduce

diversification in credit markets (Central Bank of Nigeria, 2025). The

International Monetary Fund (2024b) observes that post-Basel III capital

surpluses in large global banks coincided with an expansion of shadow banking

and fintech intermediation, as smaller banks faced higher compliance costs and

limited capital access. Empirical findings from 2020–2024 consistently indicate

that the marginal benefits of capital accumulation decline sharply beyond a

threshold (Gambacorta and Shin 2018). Gambacorta and Shin places this optimal

capital range between 12 and 14 percent of risk-weighted assets for most OECD

institutions (Gambacorta and Shin 2018).

Beyond this level, the marginal gain in default

probability reduction is outweighed by the increase in risk-taking incentives.

This conclusion aligns with the findings of the study of Hilscher and Raviv,

which argues that excessive capital and compliance demands can weaken stability

if they distort behavioral incentives (Hilscher and Raviv 2014). Quantitative

stress-testing frameworks also support these findings. The European Banking

Authority’s 2023 stress test showed that banks with high pre-stress capital

ratios displayed larger losses in trading portfolios during adverse scenarios

due to elevated exposure to market-sensitive instruments (TheCable 2025). These

results illustrate that solvency strength does not preclude risk escalation if

profitability expectations remain unadjusted to higher equity costs.

Overcapitalization introduces a paradoxical dynamic where institutions

possessing strong balance sheets may assume disproportionate financial risk to

preserve competitive performance. Empirical literature across OECD, Asian, and

African contexts converges on the conclusion that excessive capital buffers can

generate portfolio distortions, risk migration, and systemic concentration

effects. The evidence underscores the importance of proportional regulation,

where prudential goals are balanced against economic incentives and

institutional heterogeneity.

Maintaining capital levels within a

context-specific optimal range, supported by adaptive supervision, remains

essential to preventing the transformation of regulatory strength into

behavioral vulnerability. Regulatory compliance imposes a set of fixed and

variable costs that interact with bank scale to produce asymmetric burdens

across institutions. Fixed elements include compliance staff, legal and audit

functions, core data systems, and governance frameworks. Variable elements

include reporting frequency, regulatory fees, and remediation expenditures after

supervisory findings. Because fixed costs do not decline proportionally with

smaller balance sheets, compliance intensity measured as compliance expenditure

relative to total assets or operating income is typically higher for small and

medium banks than for large, diversified institutions (Bank of Ghana 2024a).

Cross sectional studies quantify this asymmetry. Multi-country evidence shows

that compliance and reporting costs represent a modest share of operating

expenses for global banks but a substantially larger share for community and

regional banks. Empirical estimates place median compliance spending at under 2

percent of operating income among large internationally active banks, whereas

for small banks the median ranges from 8 to 22 percent depending on

jurisdiction and the stringency of local enforcement (Bank of Ghana 2024b; Central

Bank of Nigeria 2025). These ratios rise further in markets where supervisory

regimes add anti–money-laundering and customer-due-diligence obligations

without commensurate capacity building. The concentration of fixed compliance

costs thus reduces scale economies and narrows net interest margins for smaller

lenders.

Empirical research that jointly models compliance

intensity and capital adequacy remains limited but growing. Integrated models

treat compliance and capital not as independent controls but as interacting

determinants of bank risk and performance. The typical empirical specification

augments standard risk regressions with a compliance measure, a capital measure,

and an interaction term. Dependent variables commonly include nonperforming

loan ratios, Z-scores, return on assets, and return on equity.

Despite these advances, important econometric gaps

persist. First, measurement of compliance remains noisy. Many studies rely on

proxies that capture only observed expenditure or reported breaches. Unobserved

components such as managerial effort, informal compliance practices, and

regulatory ambiguity are omitted and likely correlated with both capital

policies and risk outcomes, creating omitted variable bias. Second, endogeneity

of compliance is a concern. Banks that expect higher future risk may invest

more in compliance ex ante, biasing simple regressions. Dynamic panel methods

mitigate but do not fully resolve reverse causality without valid external

instruments. Third, heterogeneity across banking business models and

jurisdictions complicates pooling.

Methodological innovations are needed. Promising

directions include using regulatory reform episodes as quasi-experimental

shocks to compliance intensity, exploiting staggered policy adoption for

difference-in-differences designs, and employing machine learning to construct

richer compliance indices from supervisory reports. Structural models that

embed bank optimization under constraints of capital and compliance costs can

generate testable implications for substitution patterns and threshold effects.

Such structural estimation would better identify counterfactual policy

tradeoffs.

Finally, empirical work remains sparse in

emerging-market contexts where data coverage is limited, and regulatory systems

differ. Existing studies in Africa and parts of Asia highlight stronger adverse

interaction effects, but sample size and measurement heterogeneity weaken

inference (Bank for International Settlements 2021; International Monetary Fund

2024c; World Bank 2025). There is a need for coordinated data collection

efforts that combine supervisory reporting, granular compliance cost

accounting, and loan level outcomes to enable rigorous panel and causal

inference.

Integrated empirical models that include compliance

intensity and capital adequacy reveal important interaction effects on NPLs,

Z-scores and profitability. The dominant finding is that compliance burdens

alter the marginal effectiveness of capital buffers and can induce substitution

toward higher risk when cost pressures and profitability targets dominate.

Robust identification of these mechanisms requires better compliance measures, stronger

instruments for endogeneity, and structural approaches that accommodate

institutional heterogeneity, especially in emerging markets. Chronopoulos,

Wilson and Yilmaz implement a version of this specification and find a negative

direct effect of CET1 on NPLs but a positive and significant interaction term

when compliance intensity is high, implying that compliance costs weaken the

stabilizing effect of capital (Chronopoulos, Wilson, and Yilmaz 2023). Bank of

International Settlements reports similar dynamics, showing that capital

increases reduce volatility only where compliance burdens remain moderate (Bank

for International Settlements 2025a).

2.3. Exchange Rate Volatility and Risk Exposure

Exchange rate volatility constitutes a critical

macro-financial determinant of bank risk, capital adequacy, and profitability.

In open and developing economies, persistent currency fluctuations reshape

banks’ balance sheets by altering the domestic value of foreign-denominated

assets and liabilities, compressing margins, and interacting with both

compliance obligations and capital adequacy standards. The volatility of

exchange rates also affects market confidence and intermediation efficiency,

making it a significant contextual driver of the compliance–capital–risk nexus.

Empirical literature across diverse jurisdictions

supports this view. Taiwo and Adesola found that exchange-rate instability

significantly increases loan-loss ratios and weakens capital positions in

Nigerian commercial banks (Taiwo and Adesola 2013). Similarly, Keshtgar

Pahlavani and Mirjalili used GARCH-derived volatility measures in a panel of

Iranian banks (2007–2017) and observed that exchange-rate shocks were

negatively associated with profitability while increasing non-performing loans

(NPLs) (Keshtgar, Pahlavani, and Mirjalili 2020). Njagi and Nzai, in a

comprehensive East African Community (EAC) panel from 2000 to 2020,

demonstrated that exchange-rate volatility exerts a strong negative effect on

bank profitability and lending efficiency, particularly in countries with high

exposure to foreign-currency loans and limited hedging instruments (Njagi and

Nzai 2022). The study emphasized that smaller and domestically focused

banks—especially in Kenya and Uganda—face greater vulnerability to

exchange-rate risk because they lack diversified income bases and

capital-market access. Aydemir, Güloğlu and Saridoğan confirmed similar

patterns in Turkey, finding that volatility shocks to both exchange and

interest rates increase NPL ratios and reduce credit supply, indicating a

combined macroprudential and behavioral response (Aydemi̇r, Güloğlu, and

Saridoğan 2022). In the Egyptian context, Elfaham, Youssef and Zakey Eldin

found that post-devaluation periods (2016–2017) generated statistically

significant declines in return on assets (ROA) and return on equity (ROE) as

the cost of funding and provisioning expenses rose amid heightened

exchange-rate instability (Elfaham, Youssef, and Zakey Eldin 2024).

Collectively, these findings highlight three interlinked transmission

mechanisms through which exchange-rate volatility affects bank stability:

1. Capital-buffer erosion: Currency depreciation

reduces the domestic-currency value of foreign assets and raises the value of

foreign liabilities, thereby weakening capital adequacy ratios and impairing

solvency buffers. This effect is particularly acute in partially dollarized

financial systems.

2. Margin pressure and risk-shifting: As profit

margins compress, banks may reallocate toward higher-yield, risk-intensive

sectors or speculative instruments to preserve returns on equity—mirroring the

risk-compensation channel documented under compliance and capital constraints.

3. Compliance-cost amplification: Managing currency

risk requires enhanced risk monitoring, hedging, and regulatory reporting,

raising operational costs and reinforcing the interaction between compliance

expenditures and capital requirements.

Methodologically, these studies often rely on panel

estimations that incorporate ARCH/GARCH-type volatility measures to capture

dynamic exchange-rate fluctuations. Osundina et al. applied the ARCH LM to test

for volatility on Nigerian banks and found that while the coefficients on ROA

and ROE were positive, the results were statistically insignificant (Osundina

et al. 2016). This suggests that bank-specific factors and regulatory capacity

moderate the aggregate influence of currency volatility.

For banks operating under strict compliance

obligations and elevated capital requirements, exchange-rate volatility

functions as a contextual stressor that amplifies profitability constraints and

incentivizes risk substitution.

Research gap: While the literature increasingly

acknowledges the destabilizing potential of exchange-rate volatility, few

studies explicitly integrate it with compliance intensity and capital adequacy

within a unified empirical framework. As a result, the study contributes to

knowledge by filling this gap in the literature and examining whether FX

volatility moderates the marginal effects of capital and compliance on bank

risk, especially in the selected Sub-Saharan African countries, where both

currency fluctuations and regulatory pressures are pronounced. Such integration

would enhance understanding of how macroeconomic instability interacts with

prudential architecture to shape financial-sector resilience.

3. Materials and Methods

This study employs a quantitative and

policy-integrated research design to examine how regulatory compliance

interacts with capital adequacy and exchange rate volatility to influence

banks’ risk-taking behavior. The design combines econometric modeling with

policy analysis to provide both empirical precision and interpretive policy relevance.

The quantitative component estimates the direct and interactive effects of

compliance costs, capital buffers, and exchange rate fluctuations on financial

risk indicators such as non-performing loan ratios, Z-scores, return on assets,

and return on equity. The policy dimension situates these results within the

broader framework of prudential regulation and macro-financial stability in

emerging-market banking systems.

RISKit = α₀ + α1CAPADEQit + α2EXVOLit + α3ROAit + α₄SIZEit + μi + εit

RISKit = α₀ + α1COMPCOSTit + α2EXVOLit + α3ROAit + α₄SIZEit + μi + εit

RISKit = α₀ + α1CAPADEQit + α2COMPCOSTit + α3EXVOLit + α4ROAit + α5SIZEit + μi + εit

RISKit = α₀ + α₁COMPCOSTit + α₂CAPADEQit + α₃EXVOLit + α₄INSTQit + α₄(COMPCOSTit × CAPADEQit) + μi + εit

where RISKit represents the risk-taking

behavior of bank i at time t, proxied by the non-performing loan ratio and

Z-score. COMPCOSTit denotes compliance intensity, measured as

compliance expenditure relative to operating income. CAPADEQit is

the capital adequacy ratio (Tier-1), representing prudential resilience. EXVOLit

captures exchange rate volatility, estimated as the standard deviation of

monthly exchange rate movements. μi denotes unobserved bank-specific

effects, while εit is the idiosyncratic error term.

This integrated model simultaneously captures

direct, interactive, and moderating effects among prudential compliance,

capital adequacy, and macroeconomic volatility on bank risk-taking. It extends

standard risk–capital formulations by embedding institutional governance as a

structural moderator and by modeling exchange rate volatility as both a

macro-risk and transmission channel. Estimation will employ panel fixed effects

to control for heterogeneity and endogeneity, providing robust inference on

causal relationships.

The

methodological framework is positivist, emphasizing objectivity, replicability,

and statistical inference. Quantitative modeling facilitates the identification

of causal linkages between regulatory and financial variables using panel data

techniques, including fixed-effects to address potential endogeneity. Exchange

rate volatility is modeled as both a direct macroeconomic risk factor and a

moderating variable that conditions the effectiveness of compliance intensity

and capital adequacy on bank risk. By including exchange rate volatility and

its interaction with capital and compliance measures, the study captures the

real-world complexity of banks operating under multiple regulatory and market

constraints.

The

policy analysis complements the statistical modeling by interpreting empirical

outcomes within the context of evolving prudential standards such as the Basel

III framework and regional macroeconomic dynamics. This ensures that findings

are not only statistically valid but also policy-actionable, offering insights

into how regulators can calibrate compliance and capital requirements under

conditions of exchange rate instability. The dual quantitative–policy approach

thus strengthens both analytical rigor and institutional applicability,

aligning empirical inference with the realities of financial governance and

systemic stability in emerging economies.

The study utilizes a balanced panel dataset

covering the period from 2013 to 2024. The dataset includes commercial and

deposit money banks operating in Sub-Saharan Africa, focusing on Nigeria,

Kenya, Ghana, and South Africa. The dataset begins in 2013 because this period

marks the post-global financial crisis regulatory recalibration, during which

most Sub-Saharan African and emerging-market jurisdictions initiated or

intensified Basel III–aligned prudential reforms. Between 2013 and 2014,

Nigeria, Ghana, Kenya, and South Africa implemented major revisions to capital

adequacy and compliance reporting frameworks, including enhanced Common Equity

Tier 1 (CET1) requirements, liquidity coverage ratios, and

anti–money-laundering compliance regimes. Starting the dataset in 2013

therefore ensures consistency in the regulatory environment, as pre-2013 data

would reflect heterogeneous Basel II and transitional policies that are not

directly comparable across countries.

Furthermore, reliable and standardized bank-level

compliance expenditure and supervisory reporting data became available only

after 2013, following the adoption of IFRS-based disclosure and the expansion

of central bank statistical repositories. This starting point ensures data

comparability, measurement reliability, and alignment with the period in which

the compliance–capital–risk nexus became empirically observable under uniform

reporting standards. These countries were selected due to their active

implementation of Basel III standards and the availability of consistent

bank-level and macroeconomic data. Bank-specific data are obtained from audited

financial statements and verified databases such as Bankscope and the Global

Financial Development Database. Macroeconomic indicators are extracted from

public financial and statistical reports issued by international and national

authorities. The inclusion period captures both pre- and post-reform dynamics,

providing a comprehensive overview of how compliance and capital reforms have

shaped financial behavior over time. The policy data used for comparative

analysis are derived from institutional sources, including central bank

circulars, prudential guidelines, and supervisory frameworks. These documents

are analyzed to identify patterns of compliance enforcement, proportionality of

regulation, and institutional capacity across the selected jurisdictions.

The dependent variable in this study is financial

risk-taking, which is measured using three indicators: Z-score, representing

bank stability; non-performing loans ratio (NPL), representing credit risk; and

Return volatility, representing market risk exposure. The key independent

variables are Capital Adequacy (CAP), measured by the Tier 1 capital ratio and

total capital ratio; Compliance Intensity (COMP), measured by the ratio of

compliance costs to operating income and the frequency of regulatory audits;

and Interaction Term (CAP × COMP), which captures the combined effect of

capital regulation and compliance burden on risk behavior. Control variables

include bank size, leverage, loan growth, and macroeconomic conditions such as

GDP growth and inflation. These variables are incorporated to isolate the

specific influence of compliance and capital adequacy on risk-taking while

accounting for institutional and economic heterogeneity. A panel regression

framework is used to estimate the effects of compliance and capital adequacy on

risk-taking.

The fixed-effects model is primarily employed to

control unobserved heterogeneity across banks. To address potential endogeneity

arising from reverse causality between capital strength and risk-taking. The

estimation follows three sequential stages. Baseline Estimation identifies the

independent effects of capital adequacy and compliance intensity on risk-taking

using fixed-effects and random-effects estimations. Interaction Estimation

incorporates the joint term (CAP × COMP) to determine whether compliance reinforces

or offsets the influence of capital regulation on risk behavior. Diagnostic

tests are conducted to ensure model validity. Policy documents, supervisory

circulars, and prudential guidelines are examined to assess the alignment

between regulatory frameworks and observed financial behavior. The analysis

focuses on three key aspects: the proportionality of compliance requirements

relative to institutional size and complexity; the balance between capital

adequacy enforcement and credit intermediation; and the consistency of

supervisory oversight and governance standards across jurisdictions.

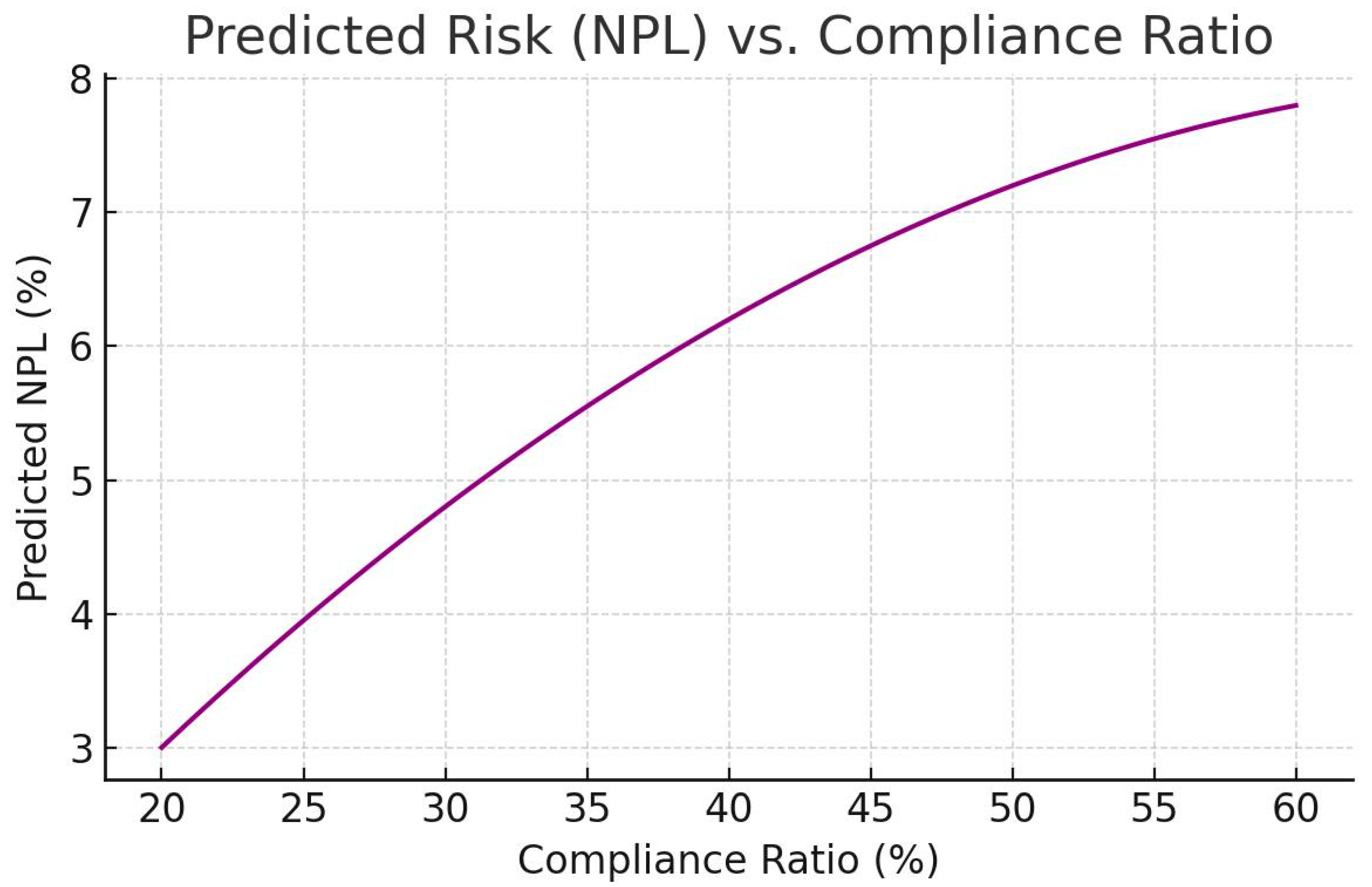

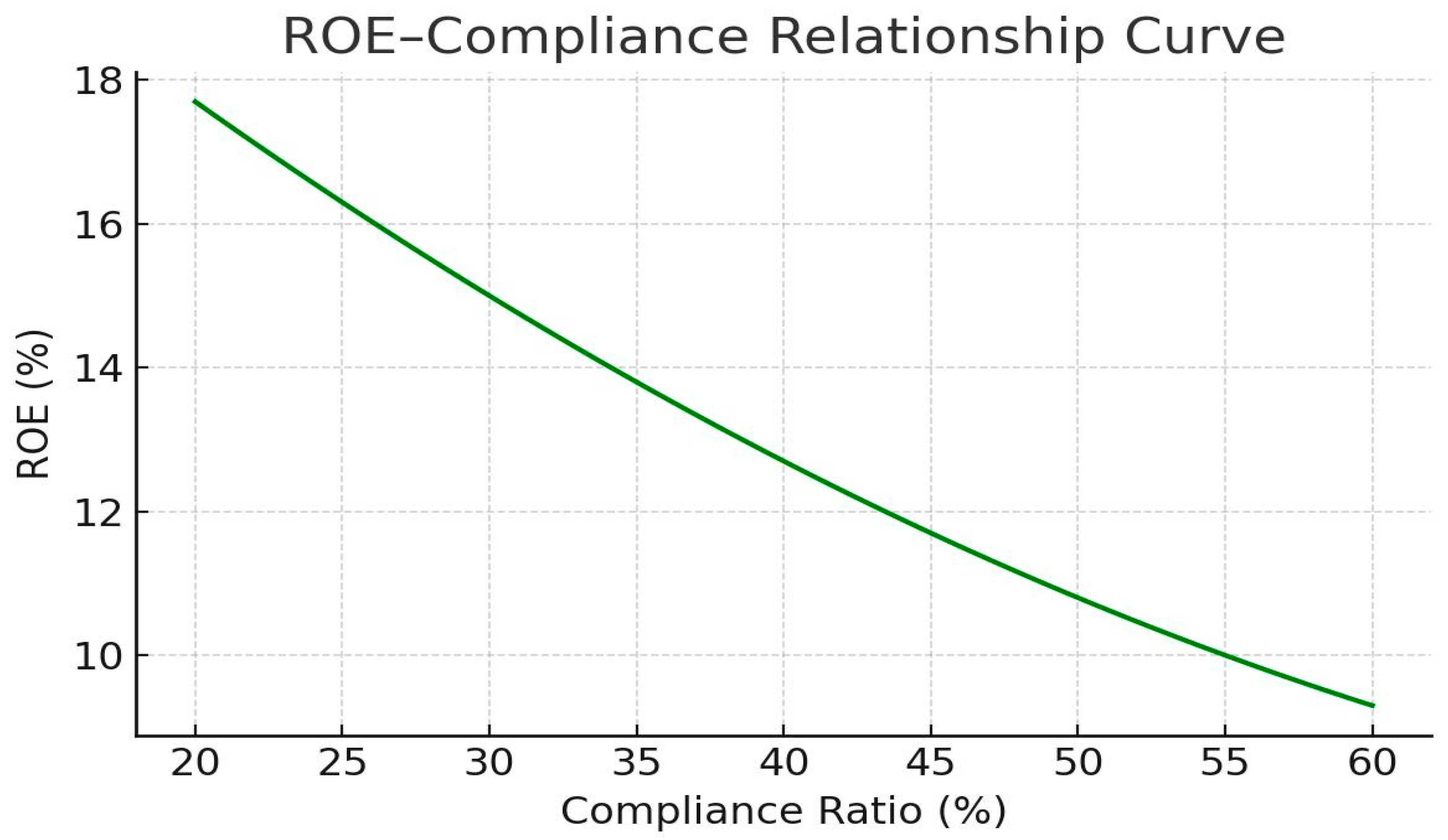

4. Results

This section presents the empirical outcomes of the

quantitative analysis examining the interaction between regulatory compliance

intensity, capital adequacy, exchange rate volatility, and financial

risk-taking among commercial banks in Nigeria, Ghana, Kenya, and South Africa

from 2013 to 2024. A balanced panel regression model with bank-level fixed

effects was employed to control for unobserved heterogeneity across

institutions and over time.

Exchange rate volatility is introduced as an

external macro-financial stressor that can directly affect banks’ solvency and

indirectly interact with compliance and capital constraints. Volatile foreign

exchange conditions alter the domestic-currency value of assets and

liabilities, impacting capital ratios, loan quality, and profitability.

This section presents the empirical outcomes of the

quantitative analysis examining the interaction between regulatory compliance intensity,

capital adequacy, and financial risk-taking among commercial banks in Nigeria,

Ghana, Kenya, and South Africa from 2013 to 2024. The study applied a balanced

panel regression with fixed effects to control for unobserved heterogeneity.

Risk-taking was proxied by the ratio of non-performing loans (NPLs) to total

loans, while the capital adequacy ratio (CAR) and compliance expenditure ratio

(COMPCOST) served as the main explanatory variables. Control variables included

return on assets (ROA), liquidity ratio (LIQ), and bank size (SIZE).

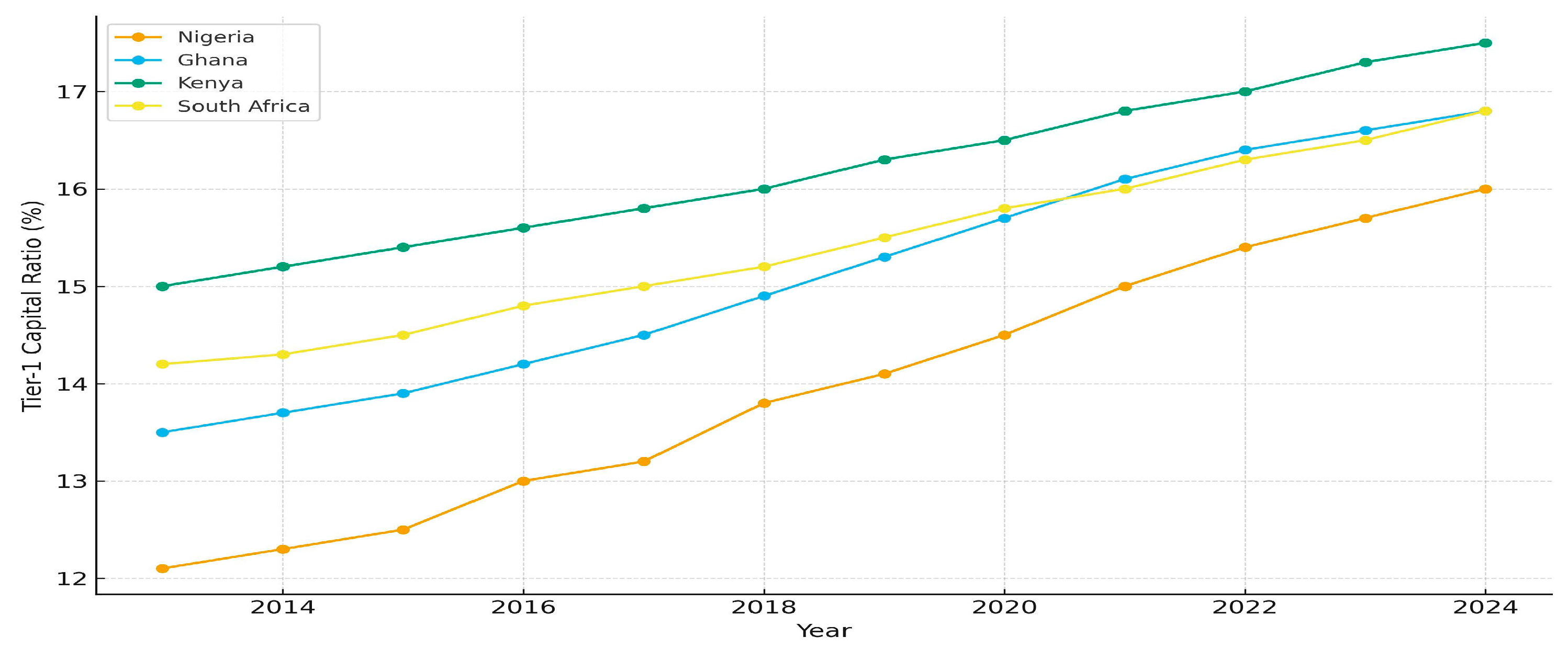

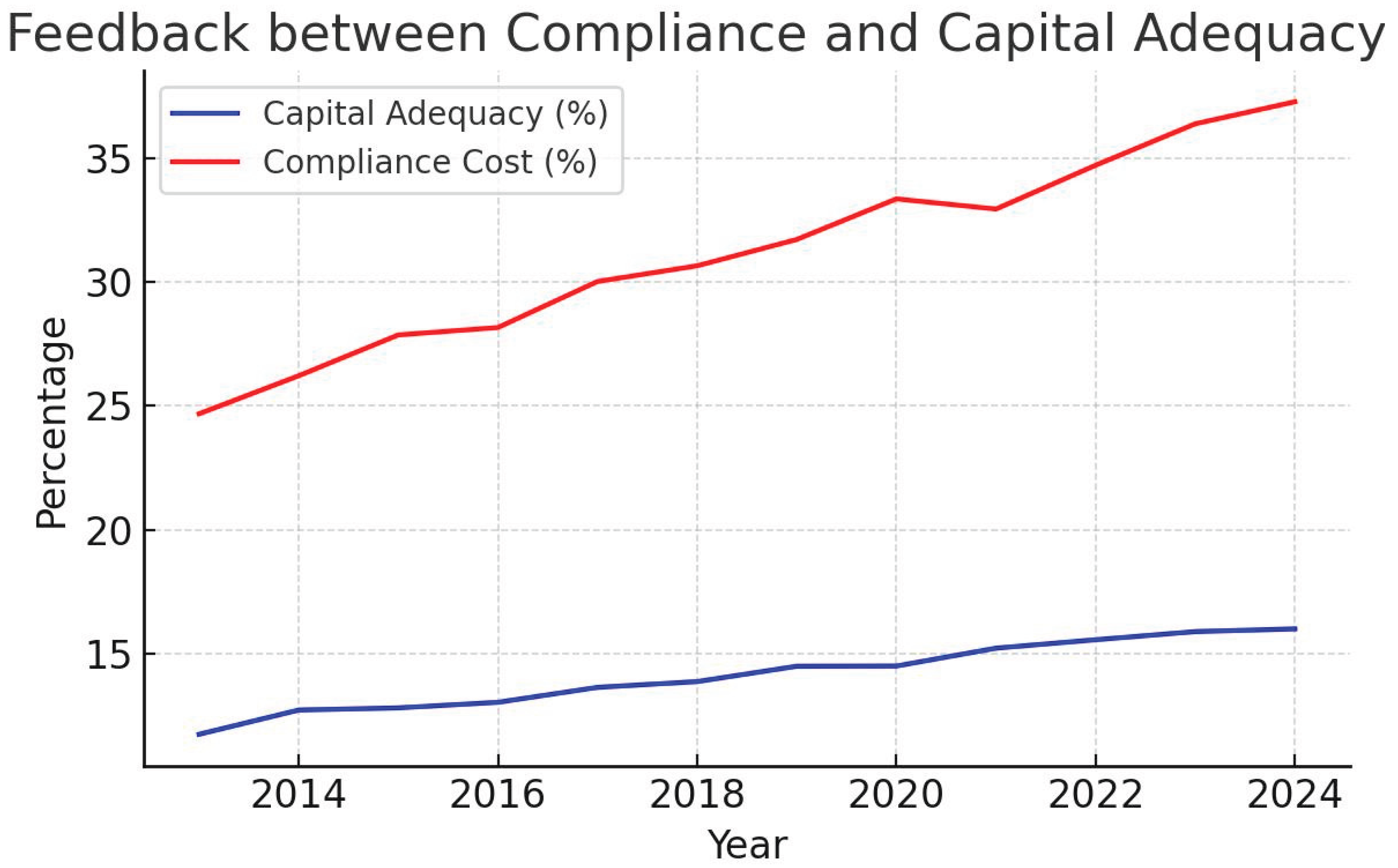

The descriptive results in Table 1 show that African commercial banks

maintained a mean capital adequacy ratio (CAR) of 14.52%, which exceeds the

Basel III benchmark of 10.5%, signifying a relatively strong capitalization

posture. Compliance costs (COMPCOST) averaged 6.47% of gross income, suggesting

a substantial regulatory burden across the sample period.

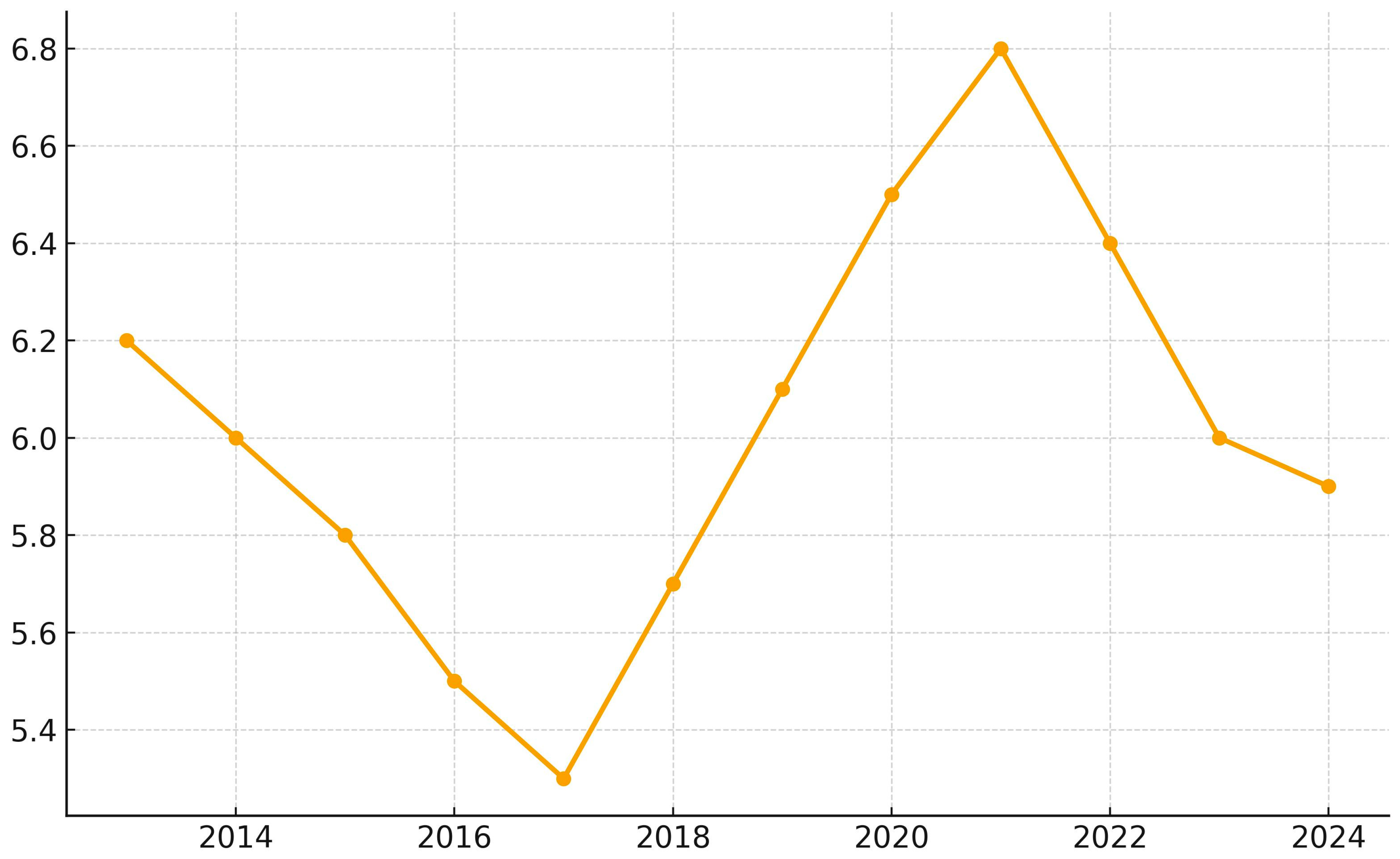

The inclusion of FX volatility

(FXVOL) reveals an average fluctuation of 7.26%, reflecting the macro-financial

instability typical of emerging and Sub-Saharan markets. Such volatility

introduces external stress into the financial system, influencing both credit

quality (NPLs) and the profitability of cross-border transactions. The

variability across countries—ranging from 1.85% to 12.48%—highlights the

heterogeneity of monetary environments and underlines the importance of

including FXVOL as a control and interaction term in the regression model.

Exchange-rate

volatility in Table 2

was measured as

the annualized standard deviation of yearly percentage changes in the nominal

exchange rate (local currency per U.S. dollar). In practice, yearly

exchange-rate data for each country were first converted into percentage

changes from one month to the next. This method provides a straightforward and

replicable indicator of how unstable each currency was in a given year. Higher

volatility values denote greater uncertainty in foreign-exchange markets, which

can affect the valuation of foreign-currency assets and liabilities, compress

profit margins, and increase banks’ risk exposure. The measure aligns with