Submitted:

06 February 2026

Posted:

09 February 2026

You are already at the latest version

Abstract

This study constitutes the second part of a comprehensive investigation of the persistence of weighted average cost of capital (WACC) rates despite declining risk-free interest rates. While theory suggests that WACC should reflect lower risk-free interest rates and decline as well with falling government bond yields, empirical evidence reveals minimal adjustment in reported WACC figures. Disclosed WACC of DAX40 companies remain between 7% and 8% as yield of a ten-year German government bond fell from 4.1% to –0.2%. After the quantitative risk analysis (part I) systematically lacks market-based and fundamental explanations – demonstrating that neither systematic risk, overall market risk, earnings risk nor leverage increased sufficiently to justify this stability – this article addresses the resulting explanatory gap through qualitative inquiry. Employing grounded theory methodology, we investigate causes and consequences of persistent WACC through systematic analysis of 18 problem-centered semi-structured expert interviews (22 respondents comprising corporate finance executives, investment bankers, strategy consultants, auditors). The investigation reveals that behavioral economics (risk aversion, opportunism, subjectivity), organizational constraints (strategic path dependency, implementation complexity, financial criterion rigidity), and model-theoretic discretion (parameter averaging, analyst influence, supplementary risk adjustments) substantially shape practical WACC determination – factors that quantitative risk analysis cannot capture. Practitioners employ disclosed WACC strategically to reconcile investor return requirements with long-term operational stability, avoid audit friction, and hedge geopolitical-monetary risks – consequences that generate capital opportunity costs offsetting traditional value-maximization objectives. Combined quantitative and qualitative evidence yields actionable insights for value-based capital cost methodologies aligned with organizational and market realities.

Keywords:

WACC

; portfolio theory

; investment appraisal

; risk perception

; grounded theory

; behavioral finance

; interest rate environment

; value-based management

; managerial finance

; risk aversion

1. Introduction

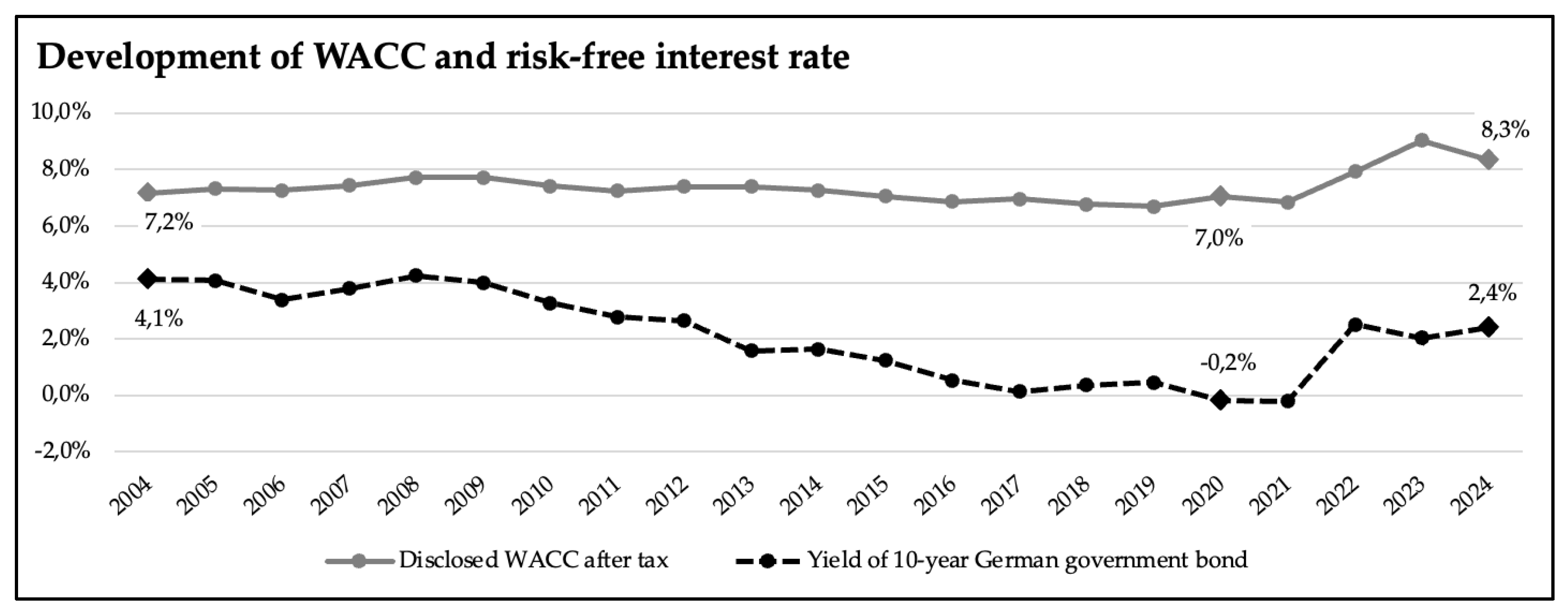

Current corporate practice presents a fundamental empirical anomaly: the persistent stability of weighted average cost of capital (WACC) reported by German DAX40 companies between 2004 and 2021, despite substantial declines in risk-free interest rates from 4.1% to -0.2%, represents a fundamental empirical puzzle with significant implications for value-based management and capital allocation efficiency (see Figure 1).

This research comprises two complementary components designed to identify root causes and implications of persistent WACC levels in a declining interest rate environment. In part I of this investigation (Frey/Heilmann, 2026e), the phenomenon of persistent WACC was addressed through a comprehensive quantitative risk analysis. Using capital market data and fundamental data from 2000 to 2023, the authors tested whether systematic increases in risk exposure – specifically beta factors, market volatility, market price of risk, earnings volatility, or financial structure risks – could justify stable WACC levels. Collectively, findings systematically demonstrate that conventional quantitative risk parameters measured through capital market data and fundamental financial metrics cannot explain the observed WACC persistence confirming that standard financial-mathematical models and external capital market data reach their explanatory limits in accounting for the observed WACC persistence.

The article provides empirically grounded explanation of the theory-practice divergence in WACC estimation, moving beyond theoretical speculation to systematic investigation of practitioner motivations and organizational contexts. It demonstrates that behavioral economics, organizational factors, and strategic considerations are equally consequential as financial-mathematical risk parameters in explaining corporate WACC determination – findings that challenge the conventional assumption that WACC is determined primarily through technical financial models. Additionally, it illuminates the trade-offs and organizational benefits of stable WACC practices, suggesting that divergences from theoretical optima may reflect rational responses to competing organizational objectives (operational stability, strategic flexibility, risk hedging) rather than pure estimation error.

The remainder of this article proceeds as follows. Section 2 presents the problem statement and research methodology, situating the investigation within prior quantitative analysis. Section 3 details the research design, grounded theory methodology, expert interview protocol, and data analysis procedures. Section 4 presents the four core categories of findings, with causal mechanisms and consequences for investment decision-making. Section 5 concludes with synthesis of key findings, theoretical implications, and directions for future research integrating quantitative and qualitative approaches to capital cost determination in contemporary corporate finance practice.

2. Problem Statement and Research Design

2.1. Problem Statement

The research endeavor necessitates a methodological shift from quantitative observation to qualitative inquiry. Since market and firm data cannot explain the anomaly, the causes must lie within internal decision-making processes, behavioral dynamics, organizational constraints and methodological choices employed in WACC estimation. Therefore, this second part of the study adopts a qualitative approach to overcome the limitations of the quantitative analysis. By employing grounded theory methodology and analyzing 18 problem-centered semi-structured expert interviews with corporate finance practitioners, financial analysts, and senior managers directly involved in capital cost determination and investment appraisal decisions. Together, these investigations provide a comprehensive examination of the divergence between theoretically correct WACC computations and observed WACC computation in practice.

2.2. Research Questions

The quantitative falsification of risk-based explanations in part I isolates the central research problem of this study: (1) What causal mechanisms explain observed deviations between WACC figures employed in corporate investment decision-making and theoretically consistent estimates derived from capital market data? (2) How do these mechanisms influence (strengthening/weakening) corporate investment decisions and value creation capabilities? This focus shifts the analytical perspective from the what (observable risk parameters) to the why and how, requiring an exploratory design capable of capturing the complexity of expert knowledge.

2.3. Research Design

To explore these unobservable internal factors, this study adopts an interactive research design based on Maxwell (2008). Unlike linear quantitative designs, Maxwell’s framework allows for the continuous interaction between research questions, methods, and validity checks – a necessary flexibility when investigating complex organizational phenomena. The design explicitly integrates contextual factors, specifically the institutional environment of capital market-oriented companies and the researchers’ prior quantitative findings, into the data collection strategy. By prioritizing “theoretical transferability” over statistical generalizability, the design aims to uncover deep structural explanations for WACC persistence that are applicable across comparable corporate finance contexts.

3. Materials and Methods

3.1. Methodological Approach

This study employs grounded theory methodology as a rigorous qualitative research approach, which enables systematic theory development directly from empirical data. Through iterative coding, constant comparison, and theoretical sampling, this methodology facilitates the discovery of underlying patterns, behavioral dynamics, and institutional factors that quantitative methods cannot capture. The problem-centered semi-structured interview technique permits in-depth exploration of practitioners’ estimation methodologies, decision-making rationales, and the organizational contexts influencing WACC applications, while maintaining sufficient structure to ensure comparability across respondents. Through systematic coding and analysis of interview transcripts, this qualitative phase aims to develop theoretical propositions explaining why practitioners maintain relatively stable WACC estimates despite substantial changes in risk-free interest rate environments, thereby addressing the second and third research questions initially posed: what causes explain observed deviations between WACC figures employed in corporate investment decision-making and theoretically consistent estimates, and what implications do these theory-practice deviations have for corporate investment decisions and value creation capabilities. This mixed-methods research design, integrating quantitative risk analysis with qualitative grounded theory investigation, exemplifies methodological triangulation and enables comprehensive examination of complex financial phenomena that neither quantitative nor qualitative approaches alone can adequately address. The complementary nature of these methodological strands – with quantitative analysis systematically excluding conventional explanations and qualitative inquiry illuminating practitioner perspectives and organizational contexts – provides robust empirical foundation for understanding the persistent WACC phenomenon and it’s implications for capital allocation efficiency in contemporary corporate finance practice.

3.2. Methodological and Evaluation-Relevant Factors

Since measurable risk parameters systematically fail to explain observed capital cost stability within declining interest rate environments, alternative theoretical perspectives capable of illuminating factors beyond conventional financial-economic models are required. Accordingly, Table 1 delineates the core elements, foundational assumptions and hypothesized relationships constituting this research design.

3.3. Data Collection Through Expert Interviews

Qualitative interviews are employed to systematically explore the explanatory mechanisms underlying observable deviations in capital cost estimation and their consequential impacts on corporate decision-making. Expert interviews are particularly suited for investigating organizational decision-making processes, as respondent seniority and direct involvement in relevant decisions substantially enhance the reliability and relevance of qualitative data. As Littig (2008) emphasizes, experts function not merely as external knowledge providers but as informants who possess knowledge inaccessible through alternative sources, particularly senior executives bearing responsibility for strategic decisions and exercising substantive decision-making authority. The respondent selection strategy is structured around five core design principles: (1) Focused problem-centered questioning: Respondents are queried specifically and exclusively regarding the tension between capital cost estimation, investment decision-making, and corporate objective formulation. (2) Practitioner-embedded expertise: Rather than relying exclusively on external experts (analysts, valuation specialists, economists), respondents are themselves embedded within the organizational decision-making context, ensuring familiarity with both capital cost estimation methodology and the strategic importance of cost-of-capital determinations in investment appraisal and objective-setting processes. (3) Heterogenous expert sample: Qualitative analysis of DAX40 company annual reports revealed two distinct populations: firms that dynamically adjust capital costs to reflect evolving environmental and strategic conditions, and firms maintaining stable, constant capital cost estimates. Respondent selection deliberately balances representation across both populations and intermediary roles (investment bankers, management consultants) with knowledge of both approaches. (4) Requisite investment and organizational expertise: Respondents possess demonstrable knowledge of organizational structures, processes, and decision-making mechanisms, coupled with substantive decision-making authority and capacity to influence investment appraisal outcomes (Meuser/Nagel, 1991). This encompasses executive leadership and external consultants with access to internal firm knowledge and direct involvement in capital allocation decisions (Welch et al., 2002). (5) Sample adequacy through theoretical saturation: Sample size varies contextually based on research questions and analytical progression toward theoretical saturation – the point at which additional interviews generate no new conceptual insights. Accordingly, this study encompasses 15 to 20 German expert interviews, a range calibrated to anticipated saturation dynamics given the specified research domain (Saunders et al., 2012).

Semi-structured interviews are administered within a flexible thematic framework comprising predefined topic domains and associated investigative questions. The interview protocol permits dynamic adaptation: supplementary questions emerge in response to respondent elaborations, conversely, prespecified questions may be omitted when redundant or contextually inappropriate, and the sequence of inquiry may be reordered based on conversational flow. The interview incorporates a diverse repertoire of question types, including process-oriented questions that systematically interrogate the causal mechanisms (‘how’) and rationales (‘why’) underlying practitioner decisions and organizational phenomena.

3.4. Data Preparation Through MAXQDA

The analysis of expert interviews is conducted using MAXQDA software. As explained in the context of grounded theory, coding of interviews involves a multi-stage, iterative process to give meaning to individual text segments, thereby transforming raw qualitative data into theoretically meaningful categories.

3.5. Data Analysis Through Grounded Theory

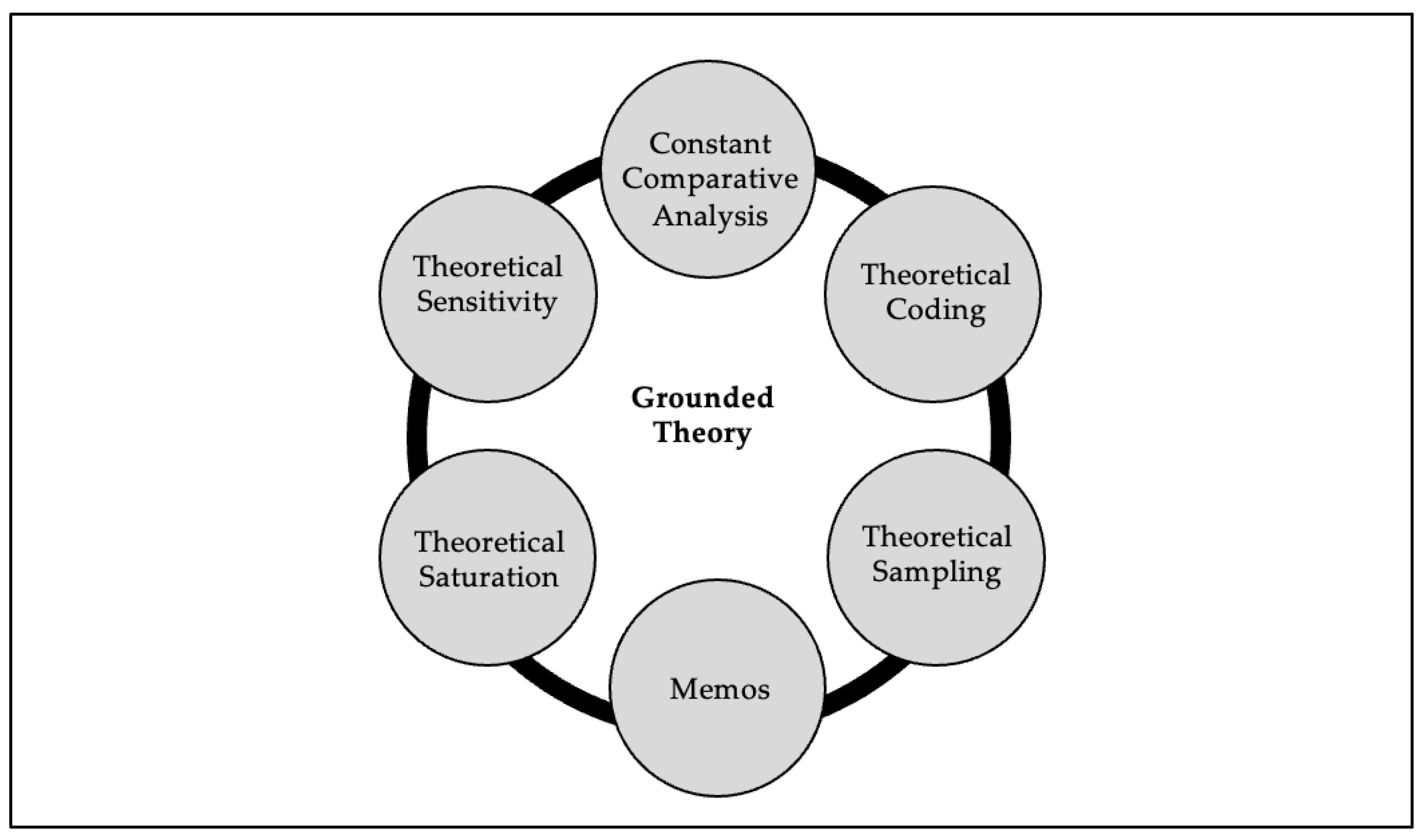

Grounded theory “seeks not only to uncover relevant conditions but also to determine how actors under investigation actively respond to those conditions, and to the consequences of their actions […].” (Corbin/Strauss, 1990; Locke 2001). It aims to construct empirically grounded theory through systematic analysis of qualitative data. Central to this approach, Corbin/Strauss (1990) design the research process as iterative and concurrent, characterized by simultaneous rather than sequential execution of data collection, analytical coding, and theorical conceptualization. Rather than proceeding through predetermined, linear stages, the researcher engages in abductive movement among data generation, interpretive analysis, and conceptual refinement, enabling continuous refinement of emerging propositions based on empirical evidence. Thus, grounded theory methodology is anchored in six foundational principles:

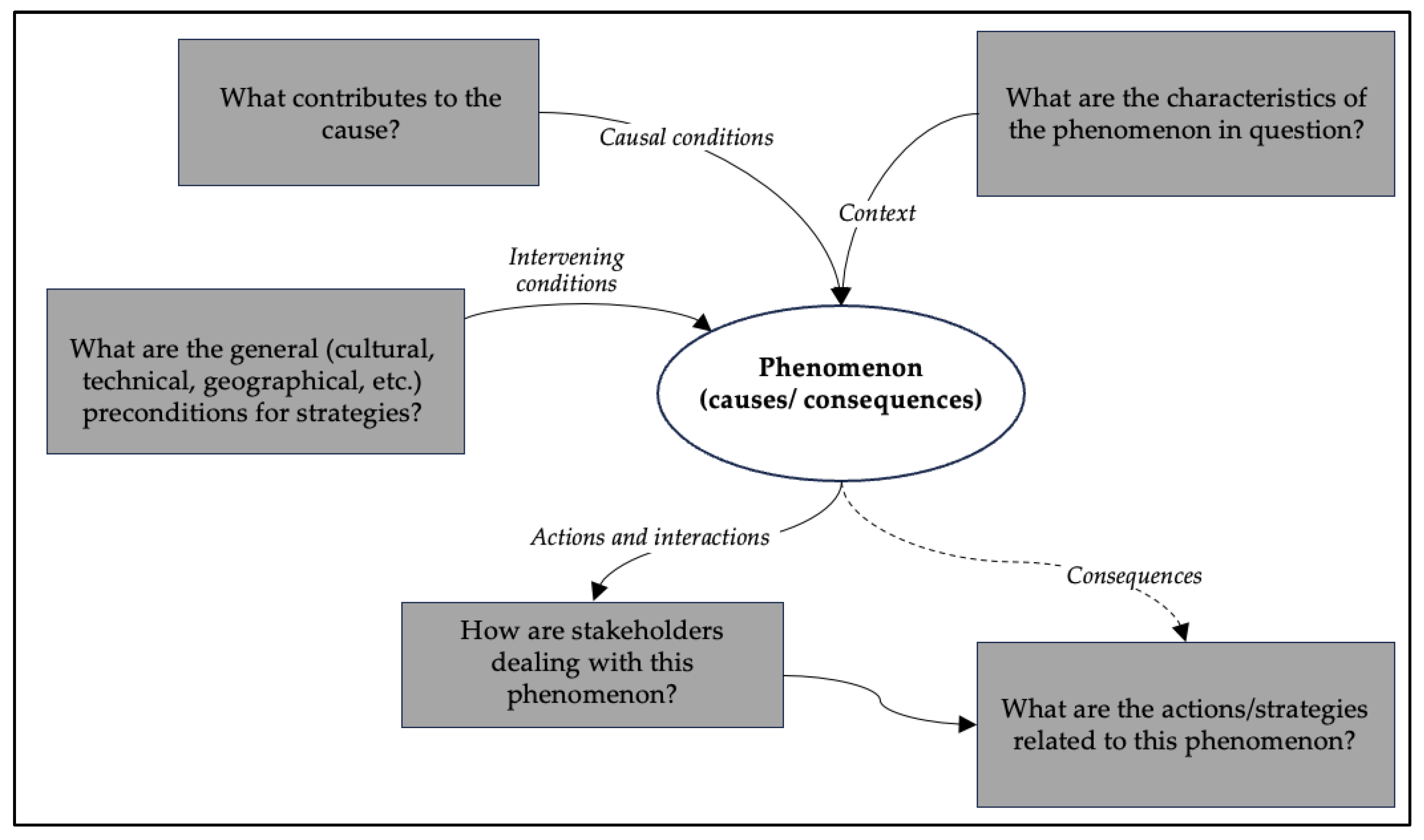

Constant comparative analysis is a core analytical principle that pervades the entirety of grounded theory research, operationalized through concurrent, iterative cycles of open coding, axial coding, and selective coding applied to qualitative data (Locke, 2001). This iterative analytical procedure encompasses four sequential yet overlapping operations: (1) comparing incidents applicable to each emerging category; (2) integrating categories and properties through relational analysis; (3) delimiting the theory by reducing theoretical scope to the most parsimonious set of categories and relationships; and (4) articulating the integrated theory through formal written exposition (Glaser/Strauss, 1967). Theoretical coding is operationalized through two interdependent yet analytically distinct phases—open coding, axial coding – that collectively transform raw qualitative data into conceptually integrated categories and emergent theoretical explanations. As Charmaz (2006) explains, coding constitutes “the pivotal link between collecting data and developing an emergent theory to explain these data.” Open coding initiates analysis by permitting inductive, data-driven assignment of conceptual labels to interview segments, thereby maintaining epistemological openness to emergent categories and novel theoretical constructs grounded directly in text segments. Axial coding constitutes the second analytical phase, reorienting analytical focus from category definition toward the relational architecture linking codes within categories and across the categorical system. This phase operationalizes the Strauss-Corbin coding paradigm, which systematically examines causal conditions, contextual factors, actions and interactions, intervening conditions, and consequences:

Figure 2.

Principles of Grounded Theory approach (O’Reilly et al., 2012; Rynes/Gephart, 2004).

Figure 3.

Coding paradigm (Strauss/Corbin, 1998).

This inductive approach is complemented through concurrent memoing. Memo writing emerges as analytical notes documenting conceptual relationships and provisional interpretations as coding progresses (Charmaz, 2006). Theoretical sampling describes “the process of data collection for generating theory whereby the analyst jointly collects, codes, and analyzes his data and decides what data to collect next and where to find them, in order to develop his theory as it emerges.” (Charmaz, 2006). Thus, theoretical sampling comprises the ongoing data collection process, which is guided by analyses already conducted on existing data material. The sampling process is not plannable in advance because at the beginning of a research project, no data-based categories and no theoretical concepts yet exist (Strübing, 2021). Theoretical sampling continues until theoretical saturation is achieved – the point at which additional data collection yields no new insights. Theoretical sensitivity denotes the researcher’s capacity to interpret data meaningfully and to discern which empirical patterns or data segments are substantively significant for advancing the emerging theoretical framework (Glaser, 1978).

4. Results

The results of the qualitative expert interviews unfold in two complementary stages: Stage one documents the iterative-cyclical theoretical sampling process, including pertinent contextual variables and respondent characteristics that shaped data collection dynamics (section 4.1.). Phase two (sections 4.2. to 4.5) describes the key explanatory findings: the multidimensional causes of the observed WACC deviations and their resulting impact on investment decisions and the achievement of corporate goals, obtained through grounded theory analysis. According to Pentzold et al. (2018), findings are systematically organized around four analytically derived core categories that emerged from the coding process: ‘Capital Market-Related Factors’, ‘Subjective Factors’, ‘Model-Theoretic Factors’, and ‘Organizational Factors’ – each addressing distinct dimensions of cost of capital practices.

4.1. Sample Characteristics

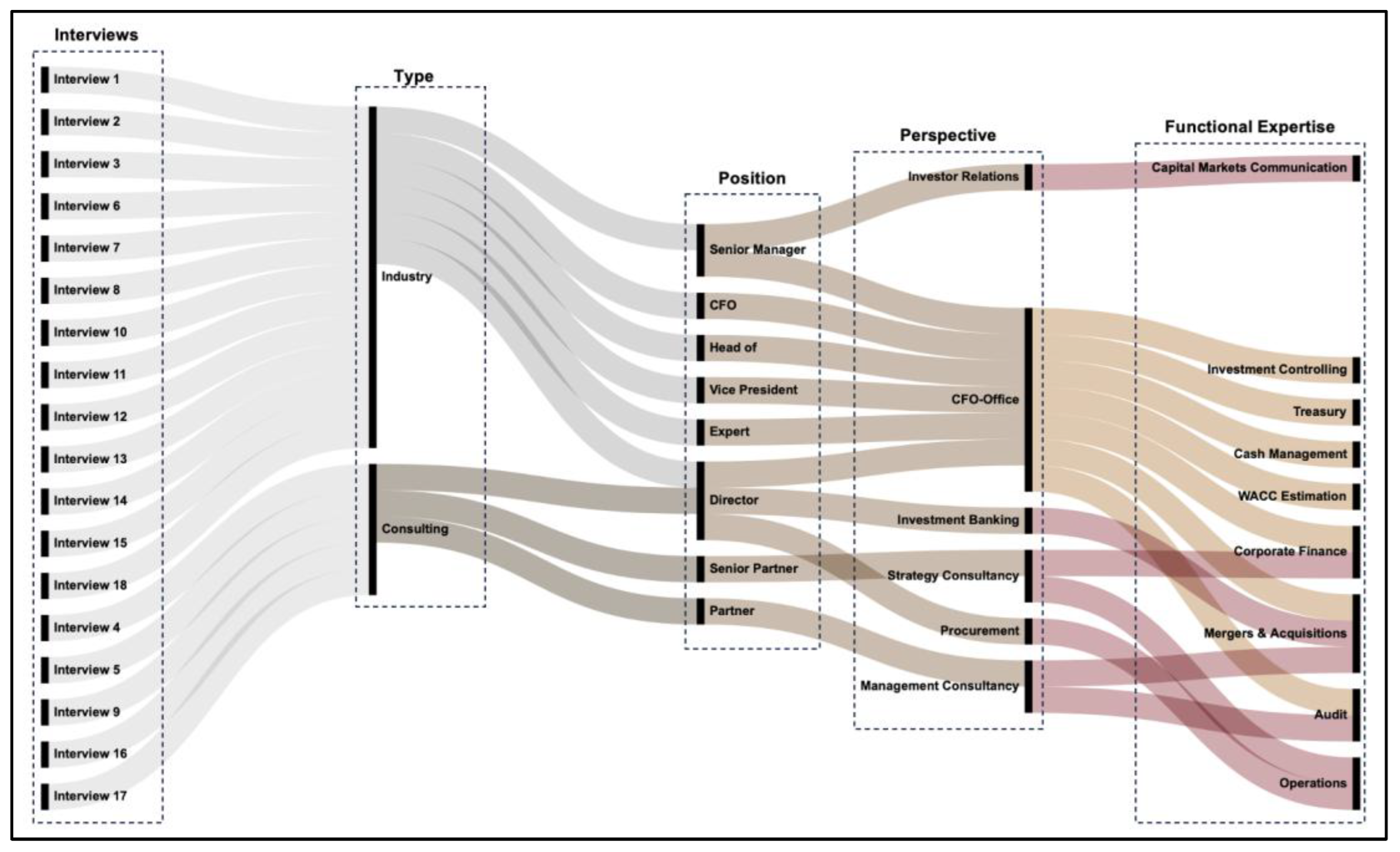

Contacts to experts emerged through personal professional networks, investor relations correspondence, and LinkedIn initiative outreach, whereby the selection of suitable respondents was conducted according to the theoretical sampling approach. Between June 18, 2024, and December 16, 2024, 18 semi-structured interviews were conducted with 22 expert participants representing diverse organizational roles across corporate finance, strategic investment management, and external advisory services comprising strategy consultants and investment bankers. Figure 4 summarizes respondent characteristics, including organizational affiliation, functional responsibilities, and relevant domain expertise:

Thirteen of 18 interviews involved corporate finance practitioners from listed and private companies (DAX40, MDAX, and mid-market firms), including one Chief Financial Officer (CFO) from a large mid-market enterprise (revenues exceeding €500 million). This CFO interview was strategically added following Interview 3, conducted with a DAX40 investor relations executive whose account highlighted capital market influences on WACC determination and objective-setting. The subsequent CFO interview proved analytically valuable for triangulating and contextualizing capital market-related claims against the experience of non-listed company practitioners. Five interviews involved external consultants: senior partners and managing directors from strategy and management consulting firms, plus a former investment banking director, ensuring representation of third-party practitioner perspectives on capital cost practice. Complementing the practitioner-focused interviews, two dedicated interviews engaged financial and quantitative methodology experts to provide technical validation of respondent claims. Additionally, four interviews included methodology experts as co-participants.

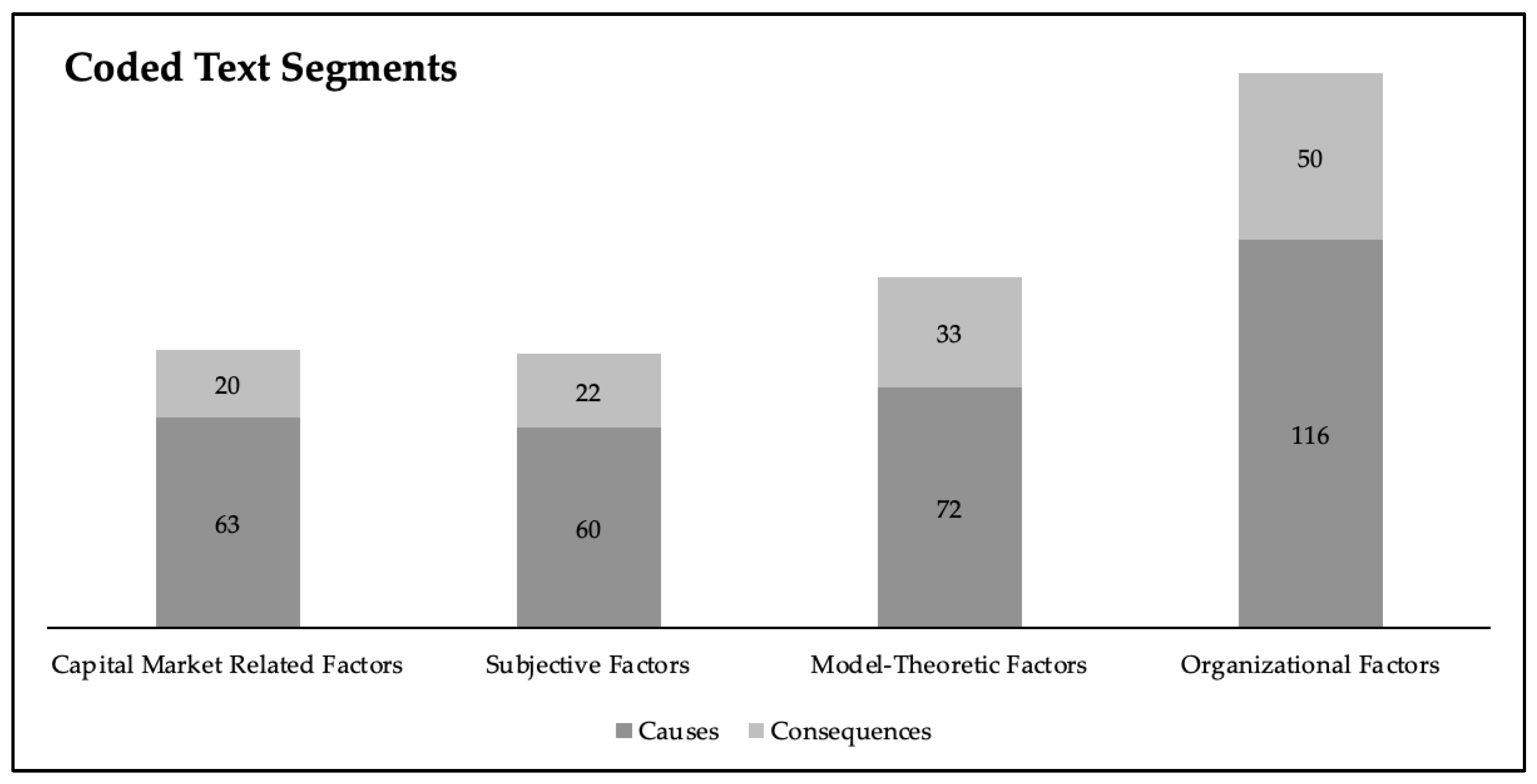

Figure 4 documents that eleven interviews engaged CFO-level executives and finance professionals whose functional expertise spans investment controlling, treasury, cash management, capital cost determination, corporate finance, mergers and acquisitions, and auditing. Analysis of the 18 expert interviews systematically reveals multiple dimensions that practitioners operationalize as constraints within capital cost estimation processes. Through inductive clustering of coded interview data, four core categories emerged that collectively explain systematic deviations between theoretically prescribed WACC-CAPM calculations and practitioner-disclosed capital cost estimates: ‘Capital Market Related Factors’, ‘Subjective Factors’, ‘Model-Theoretic Factors’, and ‘Organizational Structural Factors’. These analytically derived categories function as explanatory frameworks illuminating how financial-economic realities and organizational contingencies necessitate pragmatic divergence from idealized WACC methodologies. Figure 5 presents the thematic distribution of 436 coded text segments systematically categorized as causal mechanisms and consequential implications of observed WACC divergences.

The following sections present a category-based analysis of the empirically identified factors underlying observed WACC divergences and their implications for investment decision-making and corporate objective attainment. Each category is examined along two analytical dimensions: the causal mechanisms explaining why practitioners maintain divergent capital cost estimates, and the consequential effects—both enabling and constraining—that such divergence produces for financial decision-makers and organizational value creation

4.2. Capital Market Related Factors

Observed divergences between theoretically consistent WACC calculations and corporate-disclosed capital cost estimates are substantially attributable to the preponderant influence of capital market dynamics and stakeholder expectations. Consequently, practitioners align investment and capital allocation decisions with capital market imperatives, even when such market-responsive practices diverge systematically from idealized theoretical prescriptions derived from WACC/CAPM models.

4.2.1. Causes

Company executives and decision-makers base strategic decisions on investor expectations, which are primarily measured using shareholder value indicators. Capital market factors that influence WACC deviations include analyst influence, share buybacks, and capital market obligations. Listed companies must meet investors’ return requirements, which reflect expected future value creation and risk perception rather than theoretically derived risk parameters. According to interview partner 11 – Treasury Director of a DAX40 company – an equity investor ultimately trades your earnings expectations, and these expectations don’t necessarily align with model-calculated risk. Interview 3 (Senior Investor Relations Manager, 25+ years capital markets experience) attributed stable disclosed WACC amid declining risk-free rates to constant price-earnings multiples, revealing two insights: Investor return requirements are implicitly measurable through P/E ratios, and these requirements remain invariant to interest rate changes – Shareholders say: ‘I want my 8–9%. I don’t care what the risk-free rate is’ (Interview 3, Senior Investor Relations Manager, DAX40). Share buybacks constitute an alternative investment benchmark against which project profitability is evaluated. The CFO of a mid-sized company states, that one alternative is always returning cash to shareholders. Thus, companies must measure against this possibility. Consequently, firms face three capital deployment options: internal growth, external growth (M&A), or share repurchases. Analyst estimates significantly influence capital cost determinations. A Senior Partner at a global strategy consultancy observed that analysts and investors often impose excessive return requirements: ‘Some investors—the KKRs and Goldmans—never fully disclose their models. It’s their holy grail. I sometimes sense they build in higher return requirements because they’ve calculated an additional buffer’ (Interview 5, Senior Partner, Strategy Consultancy).

4.2.2. Consequences

Advantages. Capital market-oriented WACC determination enables CFOs to avoid contentious discussions with auditors and investors: “Nobody wants a debate with the auditor or supervisory board” (Interview 3). Under shareholder-oriented objectives, WACC divergences can generate excess returns and enhance shareholder value creation. Interview 14 clarified that elevated return requirements need not disadvantage firms: “Institutional investor return demands are typically higher, which isn’t disadvantageous if we earn more than our WACC” (Interview 14, Senior Controlling Manager, DAX40). Moreover, firms generate liquidity under high return thresholds that can be directly distributed to shareholders (Interview 11).

Disadvantages. Interviews reveal negative consequences of capital market-driven WACC practices. Firms cannot always verify investor calculation methodologies due to information asymmetry (Interview 14). Blind reliance on analyst estimates creates misallocation risk: erroneous analyst projections can trigger flawed investment decisions and destroy value. Without transparency regarding analysts’ minimum return expectations, firms may reverse-engineer WACC from P/E multiples and manipulate WACC-CAPM models accordingly (Interview 3).

4.3. Subjective Factors

The core category ‘subjective factors’ encompasses causes and consequences attributable to individual behavioral patterns and risk preferences of corporate decision-makers. Expert interviews reveal that subjective risk perception, security demands (expressed as additional risk buffers), experiential judgement, and intuition systematically contribute to WACC divergences.

4.3.1. Causes

Beyond investor return demands (Section 4.2.1), firms impose internal profitability thresholds through hurdle rates that is not based on a theoretical conception (i.e. subjective profitability requirements): ‘WACC calculations can be highly detailed and model-theoretic, but the extra markup doesn’t really fit. By the minimum value contribution stage, it’s clearly just an excess return expectation.’ (Interview 14, Senior Controlling Manager, DAX40).

Capital costs establish minimum return thresholds, frequently adjusted by subjective risk premiums satisfying managerial risk aversion and satisfying the individual subjective security demand: “There’s the scientifically grounded approach, and then there’s saying: ‘No, I’m adding a safety markup—that’s sufficient’“ (Interview 3, Senior Investor Relations Manager, DAX40). Risk-averse managers create organizational tension by demanding ambitious returns. ‘Cash is king, and security is king. Risk aversion can definitely explain WACC divergences’ (Director, Operations, DAX40).

WACC divergences may reflect heightened (subjective) risk perception justifying latent risk increases that counteract declining risk-free rates: ‘You’ve empirically proven that the volatility of the various markets has not increased significantly in this decade. I believe that the perception is different. And if you are an entrepreneur, even if these are only short-term volatilities, but if you want to make a transaction and there is a market distortion at that moment, then that is extremely unpleasant [...]. Depending on how exposed you are. I can’t prove this empirically, but my feeling is that this has happened more often in the last few years, that there have been such short-term, very volatile phases in which two, three, four visible things went wrong [...].” (Interview 5, Senior Partner, Strategy Consultancy). This perception prompts managers to elevate minimum returns defensively.

WACC determination in practice incorporates subjective factors beyond theoretical models (i.e. relying on experience-based cost of capital estimation): ‘When carrying out a DCF calculation, I first need a valid basis on which to base my medium-term planning. This involves a lot of subjective assessment. For example: How will the business develop in the future? (Interview 12, Head of Consolidation, DAX40). Interview partner 13 states: ‘It’s appropriate to trust top management, who have business intuition, to assess risks well. WACC is a hard business case driver, but subjective adjustments occur through experience and different business perspectives.’ (Interview 13, Head of Free Cash Management, DAX40).

4.3.2. Consequences

Advantages. Upward WACC adjustments through subjective premiums enable efficient investment project screening (Interview 1, Head of Controlling, MDAX). Minimum returns exceeding actual financing costs ensure higher project quality—both entry probability and return magnitude—preventing return dilution: ‘[...] it (the investment decision) dilutes the minimum return requirement, which we don’t want. Precisely because we say that we currently have a minimum return requirement of 6% to 7% on the capital market, [...] and we have to generate that. In this respect, we can only undertake projects that ultimately achieve this at the end of the day.’ (Interview 10, Vice President Corporate Development, DAX40). Additionally, the hurdle rate serves as protection against unexpected market distortions: ‘We still target EBIT margins of 8% to 9%, and if it’s more than that, we’ll be happy. (Interview 2, Director Corporate Investments, DAX40). The subjective need for security allows companies and managers to protect themselves against risks. In the context of low or zero interest rates for investments with a term of ten to 20 years, business decisions regarding financing changes still make economic sense: “I want to be safe when interest rates come back: ‘So let’s calculate with a 3.0% cost of debt instead of 1.0%.’” (Interview 5, Senior Partner, Strategy Consultancy).

Disadvantages. Subjectively driven decisions and capital cost formation create misallocation risks. Varying consideration of the human component, coupled with the lack of transparency in the model-based approaches used to derive investment and corporate goals, can be difficult for stakeholders due to the low traceability of the WACC calculation (Interview 14, Senior Manager Controlling, DAX40). Heightened risk perception (e.g., elevated short-term volatility) can preclude value-creating opportunities: ‘If I work with a client and two or three acquisitions take place in their industry in which they were not involved, it may be that they have calculated too conservatively, for example.’ (Interview 5, Senior Partner, Strategy Consultancy).

4.4. Model-Theoretic Factors

The third dimension covers model-theoretic factors that contribute to WACC persistence despite fluctuating risk-free interest rates. Corporate practitioners enrich the WACC and/or CAPM with firm-specific parameters, exploiting methodological options in parameter selection and data sourcing.

4.4.1. Causes

Methodological causes for persistent WACC comprise differing data sources, assumptions and computation techniques, a practitioner distortion by multiples, and discrepancy between WACC/CAPM assumptions and corporate realism.

Practitioners exercise substantial discretion in determining WACC parameters (i.e. WACC-/CAPM parameter calculation methodology). Market risk premium estimation is inherently contested—proxy selection for the market portfolio is discretionary, and external recommendations (e.g., Damodaran) vary considerably: ‘I believe that market risk premium is the factor that is most open to debate. There are several well-known sources, such as Damodaran, who is the best known. However, I find that it fluctuates significantly from year to year because, in my view, the market risk premium is more of a fictitious construct that tells me what an equity investor wants as an excess return on a safe investment.’ (Interview 1, Head of Controlling Financial Risks, MDAX). Similarly, beta calculation permits analogous discretion regarding benchmark index selection. Additionally, firms incorporate credit spreads reflecting firm-specific default risk; the risk-free rate from government bonds cannot serve directly as debt cost. Given financing uncertainty from volatile risk-free rates, firms employ average calculations rather than spot market rates—a practice both industry and consultants endorse (Interview 5, Senior Partner, Strategy Consultancy).

Temporal dynamics contribute as another methodically-driven cause. WACC and CAPM are theoretically static models. Yet long-term investments face evolving capital costs inadequately captured by modern portfolio theory: ‘I think the problem lies more in the sequence of events, or the timeline, compared to theory. Companies don’t have the visibility to know whether something better is coming in the future. That means we could perhaps use our money much more wisely. Instead, we always have a point-in-time view [...].’ (Interview 1; Head of Controlling Financial Risks; MDAX).

Firms apply supplementary risk adjustments for country, construction, or market price risks absent from single-factor CAPM (Interview 10, Vice President Corporate Development, DAX40). This is reminiscent of the core category ‘Subjective Factors’.

Lastly, practitioners rely on multiple-based valuation methods in addition to DCF-analyses incorporating WACC and CAPM. Some firms calculate business cases requiring internal rates of return exceeding WACC (Interview 13, Head of Free Cash Management, DAX40). Capital costs function as important but non-exclusive investment criteria; firms combine multiple valuation approaches rather than relying solely on WACC.

4.4.2. Consequences

Advantages. The correlation between the long-term orientation of investment decisions and the long-term outlook for interest rates is one reason for calculating averages of capital market interest rates in the WACC model. This allows companies to hedge against interest rate increases and secure stable long-term project financing: ‘[...] what they (companies) then say is: we take the corresponding average to adjust for possible distortions and outliers [...].’ (Interview 3; Senior Manager Investor Relations; DAX40). Inflated hurdle rates protect against unbudgeted cost overruns: ‘A buffer is particularly effective when you have to estimate CapEx after exceeding your budget. But who decides on the size of the buffer? Anyone who has experience in construction knows that if I hire individual tradespeople to build a house, the final bill will always be higher than the individual invoices.’ (Interview 14; Senior Manager Controlling; DAX40). or firm valuations, model-theoretic deviations yield market-acceptable valuations: applying strict CAPM-WACC produces non-market multiples avoidable through comparable approaches (Interview 9, Director, Investment Banking).

Disadvantages. Multiple-based approaches constrain methodologically sound WACC application since multiples derive from comparable transactions. Firms may possess capacity for accurate WACC calculations but remain dependent on multiple methodologies, preventing implementation (Interview 7, CFO, mid-market firm).

4.5. Organizational Factors

The fourth core category, Organizational Factors, encompasses WACC divergences arising from internal organizational elements (management, strategy, operations, financing, processes) and external environmental conditions.

4.5.1. Causes

Management behaves predominantly conservative, favoring projects with upside potential while minimizing downside risk: ‘[…] you always have security and only upside. That’s basically good management. So I would do the same thing. If I were CFO, I would manage in such a way that I had 80% upside and 20% downside. And not fifty-fifty.’ (Interview 4, Senior Partner, Strategy Consultancy). As interview 17 reveals, the ownership structure is an important factor in investment decisions and corporate objectives. For example, in the case of private equity-managed companies, investment decisions tend to be more risk-tolerant (Interview 17, Partner, Management Consultancy).

Strategic imperatives constrain capital deployment: firms invest available capital in core business projects even with suboptimal financial metrics: ‘We had profitable business cases on paper, but they didn’t align with core operations, so they couldn’t proceed’ (Interview 1, Head of Controlling, MDAX). Additionally, strategic communication with capital markets commits firms to stated investment trajectories, potentially precluding profitable opportunities in adjacent or new business segments (Interview 14, Senior Controlling Manager, DAX40).

Operational interconnections influence WACC through supplier financing arrangements. ‘We don’t see that supplier-granted pre-financing reflects lower risk-free rates. Financing costs should have declined with low interest rates, but suppliers haven’t passed through savings’ (Interview 8, Director Procurement, DAX40). Moreover, firms hesitate to communicate WACC changes to line operations and investors (Interview 2, Director Corporate Investments, DAX40).

Implementation of WACC parameters lag current market values, creating time-lagging distortions: ‘In practice, you experience time-lagging. It’s currently painful because interest rates rose sharply. We couldn’t pass increases to customers quickly enough, pressuring financing margins’ (Interview 11, Director Treasury, DAX40). Implementing WACC adjustments organization-wide is complex. Investment decisions rely on historical assumptions, and major projects require central approval, complicating implementation: ‘Organizationally, it’s complex. Recalculating is a half-day task but cascading through the organization and sensitizing everyone is substantially more complex’ (Interview 1, Head of Controlling, MDAX).

The financing and interest rate perspective shows, that firms are inherently long-term financed, hence they are less sensitive to short-term rate changes. Long-duration investments require averaging rates over extended horizons to estimate robust returns resilient to market fluctuations (Interview 9, Director, Investment Banking). A frequently discussed factor concerns interest rate level treatment. Many firms adopt long-term interest perspectives rather than spot rates, enabling disclosed WACC to exceed methodologically current WACC—insulating decisions from temporary distortions (Interview 13, Head of Free Cash Management, DAX40). Managers increasingly question market interest rate mechanisms, viewing central bank-determined rates as artificial and unsustainable: “We know rates are artificially low. Central banks created money outside all conventional constraints” (Interview 5, Senior Partner, Strategy Consultancy). Lastly, geopolitical risks – US-China trade tensions, Ukraine-Russia military conflict, unstable supply chains – have increased volatility and capital costs.

4.5.2. Consequences

From a management perspective, avoiding operational expenses, hedging against geopolitical and monetary policy shifts, and ensuring operational stability and robust refinancing capabilities are of paramount importance.

Advantages. Managers’ adherence to stable return thresholds generates two complementary operational benefits. First, conservative hurdle rate maintenance enables enhanced project selection discipline—enabling firms to maintain or increase required returns despite budget constraints, thereby improving project quality. Second, consistent return criteria facilitate longitudinal performance assessment across multi-year investment horizons and mitigate organizational disruption from frequent parameter revisions, allowing operational managers to focus on execution rather than continuously adjusting financial criteria. This stability simultaneously provides strategic value: constant return requirements anchor investor communications and reduce capital market uncertainty regarding investment discipline, while protecting operational continuity from volatile market-driven parameter fluctuations.

Disadvantages. Organizational constraints generate three distinct adverse consequences. Strategic path dependency constrains investment opportunity options: firms publicly committed to stated strategic trajectories systematically forgo profitable opportunities in adjacent or nascent business segments when such investments diverge from market-communicated strategy (Interview 14, Senior Controlling Manager, DAX40). This reflects the strategic signaling literature’s recognition that capital allocation signals investor expectations regarding firm positioning. Financial criterion rigidity further restricts project selection: adherence to constant minimum return requirements and invariant WACC parameters mechanically excludes projects that may create shareholder value but fall below organizationally defined thresholds (Interview 9, Director, Investment Banking). This dynamic reflects the tension between theoretically flexible capital allocation and the organizational convenience of static financial criteria. Foregone M&A value creation represents a third adverse consequence: rigid return requirements and strategic constraints preclude acquisitions that would generate value through synergy realization or portfolio diversification (Interview 2, Director Corporate Investments, DAX40). Collectively, these organizational rigidities impose material opportunity costs – quantifiable in terms of foregone net present value and unrealized strategic optionality – that offset the operational and communicative benefits of stable return criteria.

5. Conclusions

This study explains causes and consequences of observed divergences between disclosed and theoretically consistent WACC computation. Unlike previous capital cost research, this investigation integrates capital cost determination with interest rate dynamics and investment decision-making processes. Through interdisciplinary methodology, the study identifies a theory-practice contradiction in capital cost application that qualitative analysis reveals – not quantitatively – to reflect multifaceted behavioral and organizational determinants within managerial corporate finance. Qualitative expert interviews were systematically examined to identify and synthesize causal mechanisms and consequential outcomes into seven empirically grounded propositions regarding capital cost practice.

Whereas prior empirical research emphasizes model-theoretic CAPM/WACC refinement for precise estimation, this investigation reveals that behavioral economics (risk aversion, opportunism, subjectivity), procedural complexity in implementing capital cost adjustments, and systematic rejection of risk-free rate approximation via government bond yields substantially shape practical capital cost determination. Additionally, behavioral economics considerations, organizational structures, accounting regulation, and disclosure requirements are equally consequential as financial-mathematical risk parameters in explaining corporate capital cost divergences.

Another core insight addresses that investment decisions and corporate objective derivation cannot be governed exclusively through WACC/CAPM frameworks as financial theory prescribes. Both quantitative analysis and qualitative investigation establish that WACC/CAPM tools are only partially effective for real-world capital allocation and corporate goal-setting. Instead, financial market dynamics, behavioral factors, and organizational constraints decisively influence long-term value governance in publicly listed firms. The study demonstrates that practitioners frequently equate WACC with equity return demands, systematically distort capital costs through subjective adjustments, and violate value-maximization principles – consequences that potentially generate capital misallocation and negative value effects.

Despite suboptimal economic value effects, disclosed capital costs provide multiple organizational benefits: (1) increase decision-maker confidence in investment safety; (2) enable pursuit of excess returns and opportunistic gains; (3) preempt discussions with auditors and investors; (4) strengthen individual organizational positioning; and (5) hedge against market disruptions and rate changes. The final benefit reflects practitioners’ calculated rejection of low-rate incorporation – recognizing that historical rate assumptions protect long-term project return stability. Despite theoretical capital cost prescriptions, practical implementation systematically diverges from scientific recommendations. Combined quantitative and qualitative evidence yields actionable insights for optimizing capital cost methodologies aligned with organizational requirements.

Abbreviations

The following abbreviations are used in this manuscript:

| CAPM | Capital Asset Pricing Model |

| CapEx | Capital Expenditure |

| CFO | Chief Financial Officer |

| EBIT | Earnings Before Interests and Taxes |

| KKR | Kohlberg Kravis Roberts & Co |

| M&A | Mergers & Acquisitions |

| WACC | Weighted Average Cost of Capital |

References

- Charmaz, K. Constructing Grounded Theory: A Practical Guide through Qualitative Analysis; SAGE Publications, 2006. [Google Scholar]

- Corbin, J.; Strauss, A.L. Grounded Theory Research: Procedures, Canons and Evaluative Criteria. Zeitschrift für Soziologie 1990, 19(6), 418–427. [Google Scholar] [CrossRef]

- Glaser, B. G. Theoretical Sensitivity: Advances in the methodology of grounded theory; The Sociology Press, 1978. [Google Scholar]

- Glaser, B. G.; Strauss, A. L. The Discovery of Grounded Theory: Strategies for Qualitative Research; Routledge, 1967. [Google Scholar]

- Gleißner, W. Unternehmenswert, Ertragsrisiko, Kapitalkosten und fundamentales Beta - Studie zu DAX und MDAX. In BewertungsPraktiker; 2016; Volume 2, pp. 60–70. [Google Scholar]

- Littig, B. Interviews mit Eliten – Interviews mit ExpertInnen: Gibt es Unterschiede? Forum: Qualitative Sozialforschung 2008, 9(3), 1–17. [Google Scholar]

- Locke, K. Grounded Theory in Management Research; Sage Publications, 2001. [Google Scholar]

- Maxwell, J. A. Designing a Qualitative Study. In The SAGE Handbook of Applied Social Research Methods, 2nd ed.; Bickman, L., Rob, D. J., Eds.; 2008; pp. 214–253. [Google Scholar]

- Meuser, M.; Nagel, U. ExpertInneninterviews – vielfach erprobt, wenig bedacht: ein Beitrag zur qualitativen Methodendiskussion. In Qualitativ-empirische Sozialforschung: Konzepte, Methoden, Analysen; Garz, D., Kraimer, K., Eds.; Westdt. Verlag, 1991; pp. 441–471. [Google Scholar]

- O’Reilly, K.; Paper, D.; Marx, S. Demystifying Grounded Theory for Business Research. Organizational Research Methods 2012, 15(2), 247–262. [Google Scholar] [CrossRef]

- Pentzold, C.; Bischof, A.; Heise, N. Praxis Grounded Theory: Theoriegenerierendes empirisches Forschen in medienbezogenen Lebenswelten. Ein Lehr- und Arbeitsbuch; Springer VS, 2018. [Google Scholar]

- Rynes, S.; Gephart, R. P. From the Editors: Qualitative Research and the “Academy of Management Journal”. The Academy of Management Journal. 2004, 47(4), 454–462. [Google Scholar]

- Saunders, M. N. K.; Lewis, P.; Thornhill, A. Research methods for business Students, 2nd ed.; Pearson, 2012. [Google Scholar]

- Strübing, J. Grounded Theory: Zur sozialtheoretischen und epistemologischen Fundierung eines pragmatistischen Forschungsstils, 4th ed.; Springer, 2021. [Google Scholar]

- Strauss, A. L.; Corbin, J. M. Basics of Qualitative Research. In Techniques and Procedures for Developing Grounded Theory, 2nd ed.; Thousand Oaks, 1998. [Google Scholar]

- Vettiger, T.; Volkart, R. Kapitalkosten und Unternehmenswert. Zentrale Bedeutung der Kapitalkosten. Der Schweizer Treuhänder 2002, 2(5), 751–758. [Google Scholar]

- Welch, C.; Marschan-Piekkari, R.; Penttinen, H.; Tahvanainen, M. Corporate elites as informants in qualitative international business research. International Business Review 2002, 11(5), 611–628. [Google Scholar] [CrossRef]

Figure 1.

Development of WACC and risk-free interest rate.

Figure 4.

Sankey diagram displaying interview characteristics.

Figure 5.

Coded Text Segments.

Table 1.

Foundational elements of the research design.

| Element | Explanation |

|---|---|

| Concept |

|

| Relevant methods |

|

| Assumptions for research approach |

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.