Submitted:

08 February 2026

Posted:

09 February 2026

You are already at the latest version

Abstract

Corporate social responsibility (CSR) training plays a crucial role in deepening employees’ understanding of the ethical, social, and environmental expectations associated with their work. Such training helps build the attitudes and competencies that strengthen organisational CSR performance and contribute to long-term trust and value creation for stakeholders. Drawing on the Resource-based view (RBV), this study examines how employees’ CSR training influences CSR performance and further explores how firm size and CSR expenditures shape this relationship. The study employed purposive sampling, guided by clear inclusion and exclusion criteria, to identify 488 non-financial firms listed on the Tokyo Stock Exchange (TSE) between 2010 and 2024. Data were sourced from the Bloomberg database. To ensure robust and reliable estimates, the analysis utilised Feasible Generalized Least Squares (FGLS), the Augmented Mean Group (AMG) estimator, and the two-step System Generalized Method of Moments (GMM). The findings indicate that employees’ CSR training, captured by the number of training sessions provided annually, has a significant and positive effect on CSR performance. Moreover, both firm size and CSR expenditures were found to strengthen the influence of CSR training on CSR outcomes. These results suggest that managers and policymakers should give sustained attention to CSR-related capacity-building efforts. Regular, well-designed CSR training can enhance employees’ awareness and ethical conduct, foster stronger engagement, and ultimately support more effective and sustainable corporate practices.

Keywords:

corporate social responsibility performance

; corporate social responsibility expenditures

; corporate social responsibility

; Corporate social responsibility employees’ training

; corporate strategy

1. Introduction

Corporate social responsibility (CSR) performance has increasingly become a central indicator of a firm’s competitiveness and long-term sustainability [1]. CSR involves more than compliance with regulations or adherence to ethical standards; it plays a strategic role in building stakeholder trust, attracting socially responsible investors, and strengthening corporate reputation. In today’s business environment, where social and environmental accountability significantly shapes firm valuation, companies that demonstrate a strong commitment to CSR often benefit from enhanced access to capital, better risk management, and stronger long-term value creation [2,3]. These developments underscore an important question: to what extent does CSR performance translate into tangible financial and strategic benefits for firms striving to balance profit-making with their social and environmental responsibilities?

Employees remain at the heart of translating CSR commitments into practical actions within organisations [4]. Their decisions, behaviours, and engagement directly influence whether CSR policies are implemented in the workplace. CSR training equips employees with the knowledge, skills, and orientation necessary to integrate sustainability principles into their daily tasks and organisational decision-making processes [5]. Such training also helps cultivate a culture of accountability, responsibility, and ethical conduct. Organisations that prioritise CSR-focused training often report improved CSR performance, stronger employee engagement, and deeper trust-based relationships with stakeholders [6].

Yet, despite the recognised value of CSR, many companies still struggle with its effective implementation [7]. In many cases, CSR initiatives are introduced through top-down directives, leaving employees with limited involvement and understanding. This approach often results in compliance at a superficial level, rather than genuine behavioural and cultural transformation. Without structured training that strengthens employees’ competence, confidence, and motivation, firms risk falling short of their sustainability goals and may be unable to convert CSR commitments into meaningful organisational and societal benefits [8].

Although research on CSR has expanded, empirical work specifically examining the influence of employees’ CSR training on overall CSR performance remains sparse. Much of the existing scholarship examines these areas separately, focusing either on how CSR training shapes employee attitudes and engagement [9,10] or on how CSR performance contributes to corporate reputation and financial outcomes [11,12]. Little attention has been given to whether training employees in CSR directly strengthens corporate-level CSR performance. Understanding this connection is crucial for assessing the true contribution of employee-centred CSR initiatives to organisational sustainability.

Firm-specific characteristics may further influence the effectiveness of CSR training. Larger firms, for instance, often possess more resources, established systems, and managerial capacity to implement CSR-related activities. Likewise, CSR expenditures may enhance the impact of training by improving program design, delivery, and assessment. However, the interaction between firm size, CSR expenditures, and employees’ CSR training in shaping CSR performance has received limited research attention.

This study addresses these gaps by examining how employees’ CSR training affects corporate CSR performance and exploring whether firm size and CSR expenditures moderate this relationship. The analysis is guided by the following research questions: What is the effect of employees’ CSR training on CSR performance? How do firm size and CSR expenditures influence this relationship? Using purposive sampling guided by clear inclusion and exclusion criteria, 488 non-financial firms listed on the Tokyo Stock Exchange (TSE) between 2010 and 2024 were identified from the Bloomberg database. To ensure robust and reliable estimates, the analysis utilised Feasible Generalized Least Squares (FGLS), the Augmented Mean Group (AMG) estimator, and the two-step System Generalized Method of Moments (GMM). The findings indicate that employees’ CSR training has a significant positive effect on CSR performance.

The study contributes to the literature in several ways. First, it offers empirical evidence on how employees’ CSR training influences corporate CSR performance, highlighting the practical value of employee development in achieving sustainability outcomes. This sheds light on how strengthening employees’ CSR competencies can enhance corporate sustainability performance and improve the overall effectiveness of CSR strategies. Second, the study shows how firm size shapes the impact of CSR training, recognising that larger firms may be better positioned to support training initiatives and translate them into meaningful CSR outcomes. Finally, the study demonstrates the moderating role of CSR expenditures, emphasising that financial investment is essential for ensuring that CSR training results in measurable performance improvements.

This study is driven by the growing need for firms to move beyond symbolic CSR commitments and focus on actions that yield measurable results. Understanding how CSR training contributes to corporate success can support the development of more effective sustainability strategies. The study is significant because it links human resource development with long-term strategic and sustainability goals, offering insights that can guide managers and policymakers in building socially responsible and resilient organisations.

2. Literature Review

2.1. Theoretical Background of the Study

The resource-based view (RBV) provides a strong foundation for this study, positing that firms gain sustainable competitive advantage by developing internal resources and capabilities that are valuable, rare, inimitable, and non-substitutable [13]. Employees’ CSR training aligns with this perspective by strengthening human capital and equipping employees with enduring skills that support organisational sustainability. Such training enhances ethical awareness, problem-solving abilities, and operational competencies, which contribute to improved CSR performance—capabilities that competitors cannot easily replicate. Firm size further reinforces these advantages, as larger firms often have greater financial resources, organisational structures, and managerial systems to institutionalise training programmes and integrate CSR competencies into strategic processes [14]. Adequate CSR expenditures also enhance training effectiveness by supporting advanced programmes, tools, and monitoring systems [15].

To complement the RBV, signalling theory explains how these internal investments communicate a firm’s commitment to CSR to external stakeholders [16]. By visibly investing in employees’ CSR training, larger CSR budgets, and structured programmes, firms send credible signals of ethical commitment, social responsibility, and long-term sustainability orientation. These signals can strengthen stakeholder trust, attract socially conscious investors, and enhance corporate reputation, thereby reinforcing the competitive advantage highlighted by the RBV.

Overall, combining the RBV and signalling theory provides a comprehensive theoretical framework: the RBV explains how internal resources—human capital, firm size, and CSR expenditures—enable superior CSR performance, while Signalling theory illustrates how these investments convey credibility and commitment to external stakeholders, creating both internal and external mechanisms for sustaining competitive advantage.

2.2. Hypothesis Development

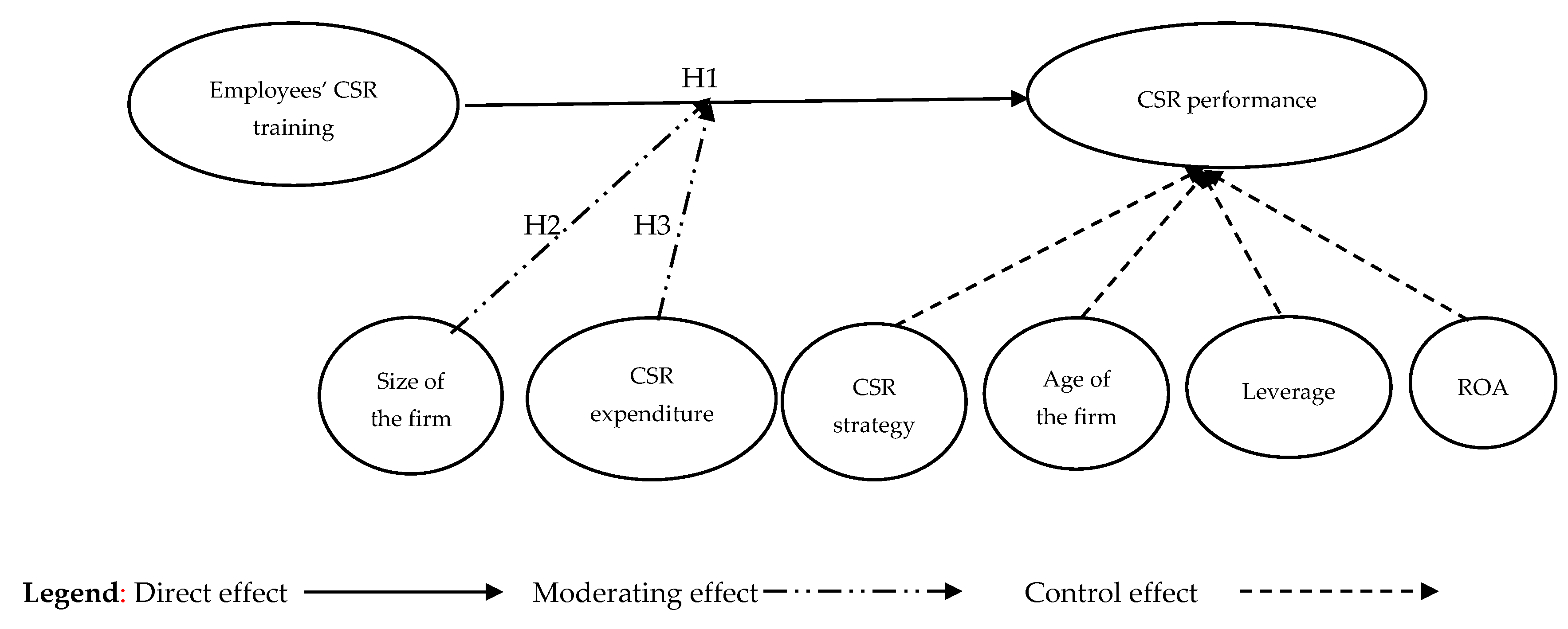

The conceptual framework of this study is presented in Figure 1, which shows the relationships among the dependent, independent, control, and moderating variables. It also shows the hypothesis number assigned to each relationship that is consistent with the hypothesis relationship presented in this section.

2.2.1. The Influence of Employees’ CSR Training on CSR Performance

Corporate social responsibility training equips employees with the knowledge, principles, and skills needed to embed sustainability considerations into their daily work [17]. In doing so, it strengthens the organisation’s overall CSR performance. Structured CSR education helps employees understand how their decisions affect environmental, social, and governance (ESG) outcomes, enabling them to make choices that support the organisation’s sustainability goals. Ayub et al. [10] report that CSR training enhances employees’ ethical awareness and socially responsible behaviour, while Lee [18] found that such training deepens internal CSR engagement and commitment. From the RBV standpoint, these improvements in human capital represent valuable internal resources that can contribute to a firm’s sustained competitive advantage by promoting responsible organisational conduct.

CSR training also fosters innovation and encourages employees to participate in activities that advance social and environmental wellbeing, thereby improving corporate CSR performance [9]. When employees grasp the principles underpinning CSR, they are more likely to act as proactive agents of change, promoting sustainable practices that are environmentally sound, operationally efficient, and ethically robust. Kim and Kim [6] argue that employee participation in CSR initiatives significantly enhances corporate sustainability outcomes and strengthens stakeholder relationships. Consistent with the RBV, this process transforms employees’ knowledge, values, and behaviours into organisational competencies—intangible assets that are difficult for competitors to imitate. CSR training, therefore, builds accountability and expertise across the workforce, enabling organisations to deliver consistent and credible CSR outcomes [8].

Moreover, CSR training helps align organisational policies and practices with stakeholder expectations [19]. This alignment contributes to stronger CSR reporting, an improved corporate reputation, and enhanced overall performance. Yan et al. [20] found that firms that prioritise sustainability-oriented training achieve higher CSR ratings and foster greater investor trust. These developments are consistent with signalling theory, which suggests that CSR-trained employees serve as credible signals of a firm’s commitment to sustainability by communicating ethical integrity and accountability to external stakeholders. Taken together, the RBV and signalling theory illustrate how CSR training strengthens internal capabilities while simultaneously enhancing organisational legitimacy and market appeal, ultimately improving CSR performance. Based on these discussions, this research hypothesized that:

Hypothesis (H1).

CSR employees’ training positively and significantly influences CSR performance.

2.2.2. The Moderating Effect of Firm Size in the Relationship Between Employee CSR Training and CSR Performance

Firm size significantly influences employees’ learning about CSR and shapes overall organizational performance. Larger firms typically possess greater financial, human, and material resources, enabling them to design and implement more comprehensive CSR training programmes [21]. They also tend to have established structures for monitoring and evaluating the outcomes of such training, ensuring that CSR initiatives translate into measurable performance improvements. According to Liakh [22], large firms attract greater stakeholder attention and scrutiny, which compels them to align their CSR efforts with long-term sustainability objectives. From the perspective of the RBV, firm size supports the development of valuable internal capabilities, such as specialised departments and highly skilled personnel, that enhances the effectiveness of CSR training in improving firm performance.

In contrast, smaller firms often struggle to implement CSR training programmes effectively due to limited financial capacity, inadequate staffing, and insufficient long-term funding [23]. These constraints affect their ability to sustain training initiatives or track their long-term outcomes. Nonetheless, smaller organizations may be more agile and maintain closer relationships with stakeholders, which can facilitate behavioural change through CSR training, although on a more modest scale. Hiss [24] notes that large firms tend to adopt formal and explicit CSR policies, whereas smaller firms often rely on the personal values and commitments of their managers. Consequently, firm size shapes both the consistency and the strength of the relationship between CSR training and organizational performance, with larger firms generally demonstrating more systematic and substantial outcomes.

Signaling theory further explains how firm size shapes the external perception of CSR efforts. Large firms often use CSR training as a signal of their commitment to sustainability, employing diverse communication channels to reinforce their reputation and credibility among stakeholders. Such external signaling amplifies the benefits of internal CSR training, as stakeholders are more likely to view the firm’s initiatives as credible and strategically grounded [25]. Smaller firms, despite delivering effective internal training, may not achieve comparable reputational gains because their signals carry less weight in the broader market. Thus, firm size influences not only an organisation’s ability to deliver CSR training but also the recognition and legitimacy it receives for these efforts, ultimately shaping CSR-related performance outcomes [26]. Based on these discussions, this study hypothesized that:

Hypothesis (H2).

The size of a firm positively and significantly moderates the relationship between CSR employees’ training and CSR performance

2.2.3. The Moderating Role of CSR Expenditures in the Relationship Between Employee CSR Training and CSR Performance

CSR expenditures indicate a company’s commitment to achieving its social and environmental objectives [12]. This can enhance the efficacy of employee CSR training in augmenting overall CSR performance. The RBV posits that financial resources enable firms to transform the knowledge and skills acquired via training into substantial and enduring CSR outcomes [27]. Organizations that invest significantly in CSR can provide enhanced training programs, superior sustainability tools, and incentives that motivate employees to effectively implement CSR initiatives. This transform learning into quantifiable enhancements in performance.

This perspective is supported by empirical studies showing that increased CSR expenditures lead to improved sustainability outcomes and stronger stakeholder relationships [12,28]. Increased CSR expenditure facilitates the implementation of employee-led initiatives, thereby aligning training objectives with workplace practices. When employees possess adequate financial resources and support from their supervisors, their CSR initiatives significantly influence both social and financial results [29].

Conversely, organizations that invest minimally in CSR may struggle to maximize staff training due to insufficient funds to implement, manage, and sustain sustainability initiatives over time [15]. In this scenario, CSR expenditure serves as a moderating variable, either amplifying or attenuating the effect of staff training on CSR performance. This moderation exemplifies the RBV emphasis on resource sufficiency and capability deployment, with financial investment serving as a crucial enabler that shapes the extent to which training generates lasting organizational value. Based on these discussions, this study proposes that:

Hypothesis (H3).

CSR expenditures positively and significantly moderate the relationship between CSR employees’ training and CSR performance.

3. Materials and Methods

3.1. Sample and Data

This study focuses on Japan, a country hypothesizes for its strong institutional and regulatory commitment to CSR and sustainable business practices [30]. Bodies such as the Japan Business Federation (Keidanren) and the Ministry of the Environment have jointly advanced the integration of CSR through initiatives including the Keidanren Charter of Corporate Behavior and the SDGs Implementation Guiding Principles. Japanese firms continue to perform strongly in areas such as social responsibility, employee engagement, and environmental innovation. Importantly, Japan’s emphasis on long-term stakeholder value and corporate ethics aligns closely with the study’s focus on employee-driven CSR performance [31]. These national frameworks and cultural traditions make Japan an appropriate and relevant context for the research.

The study concentrates on non-financial firms listed on the Tokyo Stock Exchange (TSE) because these firms play a substantial role in advancing Japan’s sustainability agenda outside the banking sector [32]. Non-financial enterprises contribute significantly to environmental, social, and governance (ESG) outcomes through industrial innovation, responsible production systems, and employee-led CSR initiatives. The TSE enforces rigorous standards of transparency and governance, which enhances data credibility and allows for meaningful comparisons across firms. Focusing on non-financial firms also avoids sector-specific regulatory complexities associated with financial institutions, enabling a clearer assessment of how CSR training influences organizational performance.

A purposive sampling strategy was employed to select 488 non-financial companies listed on the TSE from 2010 to 2024, based on explicit inclusion and exclusion criteria. Data were obtained from the Bloomberg database, which provides consistent and reliable firm-level information. To be included, companies needed to meet three conditions: (1) availability of complete CSR and financial data for the entire study period; (2) continuous listing on the TSE between 2010 and 2024; and (3) documented involvement in employee-centred CSR activities such as training programmes. Firms were excluded if they were (1) financial institutions, due to distinct regulatory and reporting frameworks; (2) firms with missing or inconsistent data; or (3) firms listed after 2010.

The period from 2010 to 2024 was deliberately selected to capture major shifts in Japan’s corporate sustainability landscape following key institutional reforms that encouraged CSR and ESG integration. During this period, the government introduced influential policies such as the Revitalization Strategy (2013) and the Stewardship Code (2014), which promoted responsible investment and enhanced stakeholder engagement. The Corporate Governance Code (2015; revised 2021) further strengthened CSR reporting requirements and encouraged deeper employee involvement in sustainability practices. Japan’s commitment to the UN Sustainable Development Goals and its 2050 Carbon Neutrality target has also shaped corporate behaviour throughout these years, making this timeframe especially pertinent for analysing the dynamics between CSR training and organizational performance.

3.2. Dependent, Independent, Control and Moderating Variables

This study presented a summary of the variables in Table 1, including their computation formulae and abbreviations used in the regression model.

3.2.1. Dependent Variable

The dependent variable in this study is CSR performance, conceptualised as a firm’s ability to meet its environmental, social, and governance obligations to stakeholders [33]. CSR performance was assessed using the ESG score obtained from the Bloomberg database, which ranges from 0 to 100. Higher ESG scores reflect stronger sustainability practices, ethical conduct, and more robust stakeholder engagement [34], while lower scores signal weaker CSR integration and limited responsibility fulfilment. The ESG score is widely used as a comprehensive indicator of CSR outcomes across the three core dimensions of corporate responsibility [35]. Its adoption in this study allows for reliable comparisons across firms and years, consistent with global sustainability assessment practices and established empirical research.

3.2.2. Independent Variable

The independent variable for this study was employees’ CSR training, defined as structured programmes designed to educate and involve employees in the principles and practices of corporate social responsibility [36]. This variable was operationalised as the annual number of CSR-related training sessions provided to employees, based on information reported in firms’ sustainability disclosures and compiled in the Bloomberg database. These training sessions were accompanied by internal evaluation or assessment procedures designed to verify employees’ comprehension of the training content and to ensure alignment with the firms’ CSR objectives [37]. A higher number of sessions reflects a stronger organisational commitment to embedding CSR values and practices across the workforce [38], whereas fewer sessions suggest limited integration of CSR within the firm. This measure is appropriate because it captures firms’ deliberate efforts to build human capital in support of CSR implementation, consistent with earlier studies that identify employee training as a critical driver of CSR effectiveness and long-term organisational performance [39].

3.2.3. Control Variables

A company’s CSR strategy reflects the extent to which sustainability objectives are embedded in its vision, operations, and stakeholder engagements [40]. This study used Bloomberg’s CSR Strategy Score, ranging from 0 to 100, to measure this construct. Higher scores indicate stronger alignment between the firm’s strategic orientation and its CSR objectives. Including this variable as a control allowed the study to account for the influence of firm-level strategic commitment on CSR performance.

Firm age was measured as the number of years a company had been in operation [41]. Older firms generally possess accumulated experience, institutional knowledge, and hypothesized stability that support the effective implementation of CSR initiatives, whereas newer firms may still be developing systems for integrating sustainability. Controlling for firm age therefore helps to isolate differences in CSR performance attributable to hypothesized maturity.

Leverage was assessed using the total-debt-to-total-assets ratio, which reflects a firm’s financial risk and capital structure [42,43]. Firms with high debt levels may prioritise repayment obligations over investments in sustainability, limiting their ability to finance CSR activities. By contrast, moderate leverage can strengthen operational efficiency and enhance stakeholder confidence. This control variable ensures that variations in CSR performance account for differences in firms’ financial constraints.

Return on Assets (ROA), calculated as net income divided by total assets, was used to capture firm profitability and operational efficiency [44]. More profitable firms are generally better positioned to allocate resources to CSR training and related initiatives. Controlling for ROA helps ensure that observed differences in CSR performance are not simply a reflection of disparities in financial capacity.

3.2.4. Moderating Variables

Firm size was measured using the natural logarithm of total assets, an approach commonly used to capture a company’s scale and resource capacity [45]. Larger firms generally have greater financial, human, and infrastructural resources to support CSR initiatives and to provide structured employee training. Firm size was treated as a moderating variable to examine how the availability of these resources influences the effectiveness of employee CSR training in improving CSR performance. Large firms also tend to have more sophisticated mechanisms for integrating, monitoring, and reporting sustainability activities.

CSR expenditures were assessed using CSR intensity, calculated as total CSR spending divided by total assets [46]. This measure reflects the proportion of a firm’s resources devoted to CSR activities. As a moderating variable, CSR intensity captures how investment levels shape the effectiveness of employee training; higher CSR expenditure is likely to strengthen implementation, amplify impact, and improve stakeholder-related outcomes.

3.3. Diagnostic Tests

To ensure the robustness, validity, and accuracy of the empirical findings, this study conducted three diagnostic tests to guide the selection of appropriate regression estimators. The first test assessed cross-sectional dependence, a condition that arises when unobserved shocks or industry-wide influences simultaneously affect multiple firms [47]. This is common in multi-firm, multi-period datasets, and ignoring it may result in biased standard errors and misleading inferences. Accordingly, the Pesaran, Friedman, and Frees tests were applied, using the null hypothesis of independence across cross-sections and alternative hypothesis of dependence.

The second diagnostic test, the Pesaran–Yamagata slope heterogeneity test, examined whether the explanatory variables, CSR training, firm size, and CSR expenditures, exerted uniform or varying effects across companies. The null hypothesis assumes slope homogeneity, while the alternative indicates heterogeneous firm-specific responses.

The third diagnostic procedure, the Durbin–Wu–Hausman (DWH) test, was used to detect endogeneity. Endogeneity may occur through omitted variables, simultaneity, or reverse causality, ultimately biasing parameter estimates and weakening the credibility of causal interpretations [48,49]. The null hypothesis of this study assumes exogeneity while alternative indicates endogeneity.

3.4. Pre-Estimation Tests

Second-generation unit root tests were applied to examine the time-series properties of the panel data, addressing the possibility of non-stationarity while accounting for cross-sectional dependence among firms. The study employed the Cross-sectionally Augmented Dickey–Fuller (CADF) and Cross-sectionally Augmented IPS (CIPS) tests, both of which incorporate cross-sectional averages to reduce the influence of common shocks that may affect all firms simultaneously [50]. These tests are based on the null hypothesis of a unit root, indicating non-stationarity, against the alternative hypothesis of stationarity.

The study employed the Westerlund cointegration test to determine whether a long-term equilibrium relationship exists between employees’ CSR training and CSR performance, particularly within a panel structure characterized by cross-sectional dependence. This approach incorporates bootstrapping and error-correction mechanisms, enabling it to account effectively for inter-firm correlations and shared long-run dynamics [51]. The test evaluates the null hypothesis of no cointegration against the alternative hypothesis that a stable long-term relationship is present.

3.5. The Choice of Regression Model

The study employed the Feasible Generalized Least Squares (FGLS) estimator for the primary analysis, given the presence of cross-sectional dependence, slope heterogeneity, and persistent correlations among the variables. FGLS is well suited to these conditions because it corrects for heteroskedasticity and cross-sectional correlation while accommodating firm-specific responses to common shocks [52]. In contexts where disturbances are correlated across units, FGLS yields more precise, unbiased, and consistent estimates than conventional methods such as Pooled Ordinary Least Squares (OLS) or Fixed Effects, which assume independent units and constant error variance [53]. These advantages make FGLS particularly appropriate for multi-firm panel data, ensuring a credible assessment of the effect of employees’ CSR training on CSR performance across diverse hypothesized settings.

To verify the robustness of the findings, the Augmented Mean Group (AMG) estimator was applied. AMG effectively handles cross-sectional dependence and heterogeneity by incorporating common dynamic processes and allowing slope coefficients to vary across firms [54]. Unlike traditional panel estimators that assume uniform model specifications for all firms, AMG estimates firm-level long-run coefficients, providing a clearer understanding of heterogeneous effects. The alignment of AMG results with those obtained from FGLS confirmed the stability and reliability of the estimated relationship between employees’ CSR training and CSR performance.

To address potential endogeneity arising from simultaneity, omitted variables, or reverse causality, the study employed the two-step Generalized Method of Moments (GMM) estimator. This approach uses lagged explanatory variables as internal instruments, thereby mitigating endogeneity bias and improving the consistency of parameter estimates [55]. The two-step GMM estimator also reduces finite-sample bias and yields asymptotically efficient results, making it highly suitable for dynamic panel analysis. The GMM findings reinforced the credibility of the causal interpretation by demonstrating that the positive effect of employees’ CSR training on CSR performance reflects substantive hypothesized processes rather than statistical artefacts [56].

3.6. Model Presentations

The study examined the effect of employees’ CSR training on CSR performance, as well as the moderating roles of firm size and CSR expenditures, using three estimation models. Model 1 assessed the direct relationship between employees’ CSR training and CSR performance. Model 2 introduced firm size as a moderating variable to determine whether organisational scale strengthens or weakens this relationship. Model 3 incorporated CSR expenditures to evaluate their moderating effect. Together, these models provide a structured and systematic analysis of both the direct influence of CSR training and the conditions under which this influence becomes pronounced. These models are presented below:

Model 1:

Model 2:

Model 3:

NB: Table 1 defines the abbreviations used in the equation models. Additionally, “c” stands for the chosen companies, “t” for the chosen study years, and “u” for the error term.

4. Data Analysis, Results and Interpretations

4.1. Cross-Sectional, Heterogeneity and Endoegenity Tests

As shown in Table 2, all three tests rejected the null hypothesis, indicating significant cross-sectional dependence among the sampled firms and underscoring the need for estimators that adequately account for inter-firm interdependencies.

Table 2 shows that slope homogeneity was rejected, implying substantial variations in how CSR training influences CSR performance. These differences likely arise from hypothesized factors such as management structures, cultural orientations, and varying levels of sustainability commitment. The presence of slope heterogeneity therefore warrants the use of econometric methods capable of capturing firm-specific dynamics.

The DWH results, presented in Table 2, confirmed the presence of endogeneity, indicating the need for advanced estimation approaches. Consequently, the study employed the two-step GMM estimator to generate consistent and unbiased estimates of the relationship between CSR training and CSR performance.

4.2. Unit Root Assessment

The results presented in Table 3 show that all variables are stationary in both levels and first differences. This outcome confirms that the dataset is appropriate for long-term panel estimation, reduces the likelihood of spurious regression, and strengthens confidence in the reliability of the estimated relationships between employees’ CSR training and corporate CSR performance.

4.3. Unit Root Assessment

As reported in Table 4, the null hypothesis was rejected, indicating a statistically significant long-term association between employees’ CSR training and corporate CSR performance. This outcome provides a robust empirical basis for the subsequent estimation procedures, confirming that CSR training initiatives are consistently linked to sustained improvements in CSR performance over time.

4.4. Descriptive and Variance Inflation Analysis

The descriptive statistics for the study variables are presented in Table 5. The average CSR performance score shows that corporations are actively engaged in CSR activities, reflecting a consistent commitment to social and environmental responsibilities. In contrast, the relatively low mean value for employees’ CSR training suggests limited participation in CSR-related capacity-building initiatives, indicating a substantial opportunity for firms to strengthen training efforts. The average CSR strategy score further shows that CSR objectives are only partially integrated into core business operations, underscoring the need for stronger strategic alignment.

The mean age of firms indicates that most are well established, a characteristic that may facilitate the adoption, implementation, and reporting of CSR initiatives. The average leverage level reflects moderate debt exposure, suggesting balanced financial risk management, which may influence firms’ willingness to invest in CSR. Similarly, the average ROA demonstrates that firms are generally profitable, implying they possess the financial capacity to sustain long-term CSR commitments without undermining operational efficiency or shareholder interests.

Firm size is, on average, large, implying greater resource availability, heightened public visibility, and stronger stakeholder expectations—factors that typically heighten pressure for meaningful CSR engagement. However, the average CSR expenditure remains low, suggesting that despite participating in CSR activities, firms allocate relatively limited financial resources to such initiatives compared to their overall operating costs.

Multicollinearity was assessed using the Variance Inflation Factor (VIF). All VIF values were below the accepted threshold of [57], confirming the absence of multicollinearity. This indicates that the explanatory variables do not overlap significantly and that the relationships identified in the regression models are valid, reliable, and statistically robust.

4.5. Matrix Correlation Analysis

The study employed the correlation matrix presented in Table 6 to evaluate the possibility of multicollinearity among the explanatory variables. According to Arhinful et al. [58], correlation coefficients exceeding 0.70 between any two predictors signal potential multicollinearity. In this analysis, all correlation coefficients fell below the 0.70 threshold, indicating minimal interdependence among the variables. These results align with the VIF findings reported in Table 5 and confirm that the explanatory variables are sufficiently distinct. This strengthens the reliability, validity, and overall robustness of the regression estimates.

4.6. Testing of Hypothesis

The FGLS results, presented in Table 7, summarise the empirical evidence on the influence of CSR employees’ training on CSR performance. These findings formed the basis for evaluating all the hypothesized relationships. The analysis shows that the number of CSR training activities undertaken by employees has a positive and statistically significant effect on CSR performance, thereby supporting Hypothesis H1 and confirming its acceptance.

Additionally, the interaction effects involving firm size and CSR expenditures with CSR employees’ training also demonstrated positive and significant impacts on CSR performance. These results provide empirical support for Hypotheses H2 and H3, affirming the moderating roles of firm size and CSR expenditures in strengthening the relationship between employees’ CSR training and CSR performance.

4.7. Robustness Testing

Validating the empirical results with an alternative model was essential in this study. Accordingly, the FGLS findings were subjected to robustness testing using the AMG estimator. Both models produced results that pointed in the same direction, demonstrating consistent significant positive or negative effects of the explanatory, control, and moderating variables on CSR performance.

The primary differences between the two models relate to their coefficient estimates and standard errors, which arise from the distinct ways each estimator addresses cross-sectional dependence and heterogeneity to produce unbiased and reliable outcomes. Despite these variations, the AMG results presented in Table 8 align with the empirical patterns reported in Table 7, thereby confirming the robustness and stability of the study’s findings.

4.8. Dealing with Endogeneity and Evaluation of GMM Model Fitness

The two-step difference GMM estimator was applied to address endogeneity arising from omitted variables, simultaneity, and reverse causality. This estimator incorporates both internal and external instruments to produce consistent and unbiased results. In the first step, the dependent variable, CSR performance, was lagged by one year and included as a dynamic independent variable. Introducing the lagged dependent variable mitigates dynamic feedback effects, preventing past CSR performance from distorting current estimates.

In the second step, all endogenous independent variables were also lagged, using periods ranging from one to five, depending on the variable, until they became exogenous. This procedure represents the use of internal instrumental variables to resolve endogeneity concerns.

In the third step, external instruments such as staff social security expenses, wages and salaries, total assets, and total liabilities were incorporated to strengthen instrument validity and identification. Combining internal and external instruments enhances the model’s ability to isolate external influences on employees’ CSR training, ensuring an impartial estimation of its causal effect on CSR performance.

The validity of the GMM model was assessed using the Arellano–Bond, Sargan, and Hansen J-tests. First, the statistical significance of the AR(1) and the insignificance of the AR(2) confirmed the appropriateness of the GMM estimator by indicating the absence of second-order serial correlation [59]. Second, the statistically insignificant Sargan test results demonstrated the exogeneity of both internal and external instruments. Finally, the Hansen J-test, with insignificant values between 0.10 and 0.30, confirmed that the instruments were uncorrelated with the error terms.

Overall, the GMM estimator was validated, confirming that endogeneity was effectively addressed and that previously endogenous variables became exogenous within the model. All diagnostic tests, AR(1), AR(2), Sargan, and Hansen, reported in Table 9 were satisfied. The GMM findings also aligned with the FGLS and AMG results, consistently demonstrating significant positive or negative effects. This convergence further reinforces the robustness and credibility of the study’s empirical results.

5. Discussion of the Findings

The study found that employees’ CSR training had a positive and significant effect on CSR performance. This result aligns with the RBV, which argues that firms gain competitive advantage by developing internal resources that are valuable, rare, and difficult to imitate. Training employees in sustainability creates an intangible strategic asset that strengthens the firm’s capacity to implement CSR initiatives effectively [39]. Such training enhances creativity, ethical awareness, and stakeholder trust, reinforcing RBV assumptions that improved internal capabilities drive superior performance. In Japan, long-standing corporate culture, characterized by kaizen (continuous improvement), investment in human capital, and social cohesion [60], further supports these outcomes. Government frameworks, including the Corporate Governance Code (2015) and the SDGs Action Plan, have encouraged firms to integrate CSR into employee development [61], producing a workforce increasingly skilled in sustainable management and stakeholder engagement.

The findings further show that CSR-focused training improves operational efficiency, reduces legal and reputational risks, and increases firms’ appeal to socially responsible investors. Management should therefore regard CSR training as a long-term investment rather than a cost. Firms that build employees’ CSR competencies tend to experience more stable growth and lower investor-related risks.

CSR strategy also had a positive and significant effect on CSR performance. This supports the RBV view that aligning CSR with corporate strategy enhances internal capabilities and strengthens long-term competitiveness. In Japan, the SDGs Implementation Guiding Principles require firms to embed sustainability within governance and national development frameworks [62], prompting businesses to adopt more deliberate CSR approaches. These structured strategies facilitate stakeholder collaboration, regulatory compliance, and innovation. As a result, firms with clearly defined CSR strategies enjoy stronger reputations, lower borrowing costs, and higher investor confidence [63,64], underscoring the importance of strategic CSR alignment for sustained corporate success.

Firm age was also found to have a positive and significant effect on CSR performance. From an RBV perspective, organizational experience, routines, and accumulated knowledge function as distinct, non-replicable assets. Older firms in Japan have had more time to develop formal CSR processes, embed sustainability within their corporate culture, and align with national policies such as the Corporate Governance Code and the SDG frameworks [30]. This organizational maturity enhances CSR implementation and fosters responsible innovation. Established firms often possess stronger reputations and better risk management capabilities, which increase investor confidence [65]. The results therefore suggest that long-standing companies generally exhibit superior CSR performance.

Leverage exhibits a negative and significant effect on CSR performance, reflecting several interconnected mechanisms. Increased leverage elevates the cost of debt repayment, hence constraining managerial options and complicating the acquisition of additional funds for discretionary CSR initiatives such as employee training and stakeholder engagement. From the RBV, substantial debt impedes the development and maintenance of crucial intangible assets, such as human capital, corporate reputation, and stakeholder trust, which are essential for effective CSR performance.

In Japan, heavily indebted enterprises may prioritize their obligations to creditors over long-term strategies that benefit partnerships and stakeholders [30]. Furthermore, substantial debt may result in increased operational and reputational challenges, hence diminishing organizations’ willingness to engage in CSR initiatives. This may adversely affect the company’s market valuation and diminish shareholder confidence. These processes demonstrate that an imbalanced capital structure complicates the acquisition of financial and strategic resources essential for effective CSR [66]. This illustrates the significance of maintaining a balanced leverage ratio to sustain CSR performance and competitive advantage.

ROA had a positive and significant effect on CSR performance. Profitable firms possess the financial flexibility to invest in training, sustainability programs, and stakeholder engagement, consistent with the RBV [67]. Strong financial performance fosters innovation, ethical practices, and long-term value creation. Firms with higher ROA typically enhance their market reputation, mitigate risks, and attract socially responsible investors [68]. This confirms that financial stability is essential for maintaining effective CSR activities.

The interaction between firm size and employees’ CSR training had a positive and significant effect on CSR performance. According to the RBV, larger firms possess more extensive tangible and intangible resources, enabling them to implement broader and more sophisticated CSR training programs. In Japan, larger firms often have formalized CSR structures, dedicated sustainability departments, and established governance mechanisms [30,69], which enhance the effectiveness of CSR training. These firms also gain reputational benefits, improved stakeholder trust, and reduced operational risks [63]. The results show that scaling CSR training within large organizations strengthens CSR outcomes.

Finally, the interaction between CSR expenditures and employees’ CSR training had a positive and significant effect on CSR performance. This demonstrates that combining financial investment with human capital development produces a synergistic effect. The RBV suggests that CSR expenditure enhances the effectiveness of training by providing necessary tools and incentives. Japanese firms that allocate more resources to CSR can support comprehensive training programs that translate employee knowledge into tangible sustainability outcomes [31,70]. This combination strengthens organizational resilience, improves stakeholder engagement, and fosters innovation. The findings indicate that coordinated investment in financial and human resources yields the strongest CSR outcomes and enhances firms’ attractiveness to socially responsible investors.

6. Conclusions, Theoretical, Policy, and Practical Implications

This study examined the effect of employees’ CSR training on CSR performance and assessed how firm size and CSR expenditures moderate this relationship. The association between CSR training and CSR outcomes remains insufficiently explored in the existing literature, making this investigation particularly relevant. Using purposive sampling based on explicit inclusion and exclusion criteria, the study selected 488 non-financial firms listed on the TSE from 2010 to 2024, drawing data from the Bloomberg database.

The analysis employed advanced econometric techniques, FGLS, AMG, and the two-step GMM, to validate the hypothesized relationships and address cross-sectional dependence, heterogeneity, and endogeneity concerns. The results consistently showed that employees’ CSR training has had a significant positive effect on CSR performance. In addition, the moderating effects of firm size and CSR expenditures strengthened the relationship between CSR training and CSR performance, indicating that firms with greater resources and higher CSR investments derive greater benefits from training initiatives.

The findings highlight the relevance of the RBV for firms listed on the TSE, showing that internal capabilities, particularly staff CSR training and institutional knowledge, play a decisive role in shaping CSR performance. When companies adopt structured training programmes that focus on sustainability, ethical behaviour, and stakeholder engagement, they build a workforce capable of implementing CSR initiatives with greater precision and impact. Such investments allow firms to convert employee competence into a sustained competitive advantage, enabling them to respond more effectively to shifting market expectations and regulatory requirements.

The results further show that firm size and CSR expenditure significantly strengthen the impact of employee training on CSR outcomes. Larger firms, often equipped with broader financial and operational resources, are better positioned to integrate employee development with strategic CSR spending. By aligning training with budgeted CSR activities, such as environmental interventions, community projects, and stakeholder-focused campaigns, these organizations are able to maximize the returns on their social investments. Ensuring coherence between CSR budgets and employee development efforts enhances the likelihood that these initiatives will translate into measurable improvements in both corporate reputation and sustainability performance.

In addition, the study points to a strong link between CSR achievements and financial performance. Companies with higher profitability and robust ROA appear better equipped to design and execute effective CSR programmes. For firms listed on the TSE, this suggests the importance of embedding CSR priorities within broader financial and strategic planning. Allocating a portion of earnings to long-term sustainability initiatives, and tracking progress through clearly defined indicators, helps firms maintain a balance between ethical obligations, stakeholder expectations, and financial targets. Such integration not only strengthens investor confidence but also enhances the firm’s overall competitiveness in the long term.

The findings have significant practical implications for policymakers and regulatory bodies overseeing firms listed on the TSE. In line with Japan’s Corporate Governance Code, which emphasizes sustainable value creation and stakeholder engagement, regulators could provide targeted incentives, such as tax benefits or recognition schemes, to encourage firms to implement structured CSR training programs. Embedding CSR principles within corporate governance practices, as promoted by the Code, can help develop employees’ skills and institutional knowledge, enabling effective implementation of social and environmental initiatives.

Regulators can further guide firms by aligning CSR expenditures with employee development and sustainability objectives, supported by clear reporting standards and performance benchmarks. Mandatory disclosure of CSR activities and ESG performance, consistent with Japanese governance guidelines, would enhance transparency, strengthen investor confidence, and encourage integration of CSR into long-term corporate strategy, ultimately improving corporate reputation and supporting sustainable economic growth.

The findings have significant policy implications for government and regulatory bodies overseeing firms listed on the TSE. Tax incentives or recognition programmes that support structured CSR training can strengthen employees’ capacity to implement sustainable initiatives effectively. Embedding CSR principles into corporate governance frameworks would further cultivate the skills and knowledge needed to achieve social and environmental goals.

Regulators should also ensure that CSR expenditures align with employee development initiatives. Setting clear performance benchmarks and reporting standards for CSR activities would promote efficient resource use and ensure that financial commitments yield measurable improvements in CSR outcomes.

Moreover, transparency and accountability measures, such as mandatory disclosure of CSR and ESG performance, can strengthen the link between corporate sustainability and financial performance. Such policies encourage the integration of CSR into long-term strategic planning, thereby enhancing corporate reputation, mitigating risk, building investor confidence, and fostering sustained economic growth.

7. Limitations and Future Directional Study

Focusing solely on Japan presents a limitation, as the findings may not apply to countries with different institutional, cultural, or regulatory environments. Future research could conduct cross-national comparisons to assess whether the relationship between employees’ CSR training and CSR performance holds in economies with varying CSR norms and governance structures.

Restricting the sample to non-financial firms listed on the TSE also limits generalizability. Subsequent studies could include financial institutions, small- and medium-sized enterprises (SMEs), or privately owned firms to determine whether organizational types shape the effectiveness of CSR training. Factors such as budget constraints, ownership structure, and board diversity may serve as relevant moderators.

Excluding firms with incomplete data introduces the possibility of sample bias. Future studies may mitigate this by drawing from alternative databases or applying imputation techniques to enhance data coverage. Additionally, the study’s focus on CSR training, firm size, and CSR expenditure omits other important determinants. Future research may explore how corporate culture, employee engagement, technological capability, and environmental regulations influence CSR effectiveness, thereby offering a more comprehensive understanding of strategic sustainability initiatives.

Employees’ training is a multidimensional construct that extends beyond the frequency of training sessions to include aspects such as training quality, duration, and participant engagement. However, when relying on secondary data sources, these qualitative dimensions cannot be directly observed or consistently measured. As a result, the present study captures employees’ training primarily through observable quantitative indicators. Future studies are encouraged to employ primary or qualitative data collection methods to examine the depth, effectiveness, and experiential aspects of employees’ training more comprehensively.

Author Contributions

AAAE: Conceptualization, writing – review & editing, Writing – original draft, Visualization, Validation, Software, Resources, Project administration. AC: Writing – original draft, Investigation, Data curation, Conceptualization, Methodology, Supervision. All authors have read and agreed to the published version of the manuscript.

Funding

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Institutional Review Board Statement

Not Applicable.

Informed Consent Statement

Not applicable for secondary data.

Data Availability Statement

Data will be made available on reasonable request through correspondent author.

Conflicts of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

References

- Famiyeh, S. Corporate social responsibility and firm’s performance: empirical evidence. Social Responsibility Journal 2017, 13(2), 390–406. [Google Scholar] [CrossRef]

- Obeng, H. A.; Arhinful, R.; Mensah, L.; Mensah, C. C. The mediating role of service quality in the relationship between corporate social responsibility and sustainable competitive advantages in an emerging economy. Business Strategy & Development 2025, 8(1), e70099. [Google Scholar]

- Arhinful, R.; Mensah, L.; Amin, H. I. M. Does corporate governance influence corporate social responsibility in developing African countries? Evidence from manufacturing companies listed in Ghana and Nigeria’s Stock Exchange. International Journal of Corporate Governance 2024, 14(3), 247–271. [Google Scholar] [CrossRef]

- Adu-Gyamfi, M.; He, Z.; Nyame, G.; Boahen, S.; Frempong, M. F. Effects of internal CSR activities on social performance: The employee perspective. Sustainability 2021, 13(11), 6235. [Google Scholar] [CrossRef]

- Kong, L.; Sial, M. S.; Ahmad, N.; Sehleanu, M.; Li, Z.; Zia-Ud-Din, M.; Badulescu, D. CSR as a potential motivator to shape employees’ view towards nature for a sustainable workplace environment. Sustainability 2021, 13(3), 1499. [Google Scholar] [CrossRef]

- Kim, M.; Kim, J. Corporate social responsibility, employee engagement, well-being and the task performance of frontline employees. Management Decision 2021, 59(8), 2040–2056. [Google Scholar] [CrossRef]

- Nave, A.; Ferreira, J. Corporate social responsibility strategies: Past research and future challenges. Corporate Social Responsibility and Environmental Management 2019, 26(4), 885–901. [Google Scholar] [CrossRef]

- Miller, K. E.; Akdere, M. Advancing organizational corporate social responsibility (CSR) agenda: Implications for training and development. European Journal of Training and Development 2019, 43(9), 860–872. [Google Scholar] [CrossRef]

- Supanti, D.; Butcher, K.; Fredline, L. Enhancing the employer-employee relationship through corporate social responsibility (CSR) engagement. International Journal of Contemporary Hospitality Management 2015, 27(7), 1479–1498. [Google Scholar] [CrossRef]

- Ayub, A.; Iftekhar, H.; Aslam, M. S.; Razzaq, A. A conceptual framework on examining the influence of behavioral training & development on CSR: an employees’ perspective approach. European Journal of Business and Social Sciences 2013, 2(1), 33–42. [Google Scholar]

- Fourati, Y. M.; Dammak, M. Corporate social responsibility and financial performance: International evidence of the mediating role of reputation. Corporate Social Responsibility and Environmental Management 2021, 28(6), 1749–1759. [Google Scholar] [CrossRef]

- Arhinful, R.; Mensah, L.; Obeng, H. A. Corporate social responsibility’s role in shaping environmental innovation and reputation: Evidence from London’s non-financial sector. Corporate Social Responsibility and Environmental Management 2025. [Google Scholar] [CrossRef]

- Zvarimwa, C.; Zimuto, J. Valuable, rare, inimitable, non-substitutable and exploitable (VRINE) resources on competitive advantage. International Journal of Business & Management Sciences 2022, 8(1), 9–22. [Google Scholar]

- Alshukri, T.; Seun Ojekemi, O.; Öz, T.; Alzubi, A. The interplay of corporate social responsibility, innovation capability, organizational learning, and sustainable value creation: does stakeholder engagement matter? Sustainability 2024, 16(13), 5511. [Google Scholar] [CrossRef]

- Fallah Shayan, N.; Mohabbati-Kalejahi, N.; Alavi, S.; Zahed, M. A. Sustainable development goals (SDGs) as a framework for corporate social responsibility (CSR). Sustainability 2022, 14(3), 1222. [Google Scholar] [CrossRef]

- Mensah, L.; Arhinful, R.; Obeng, H. A.; Gyamfi, B. A. The impact of capital structure on product responsibility and corporate reputation: Evidence from non-financial institutions listed on the London stock exchange. European Research on Management and Business Economics 2025, 31(3), 100287. [Google Scholar] [CrossRef]

- Ketschau, T. J. A conceptual framework for the integration of corporate social responsibility and human resource development based on lifelong learning. Sustainability 2017, 9(9), 1545. [Google Scholar] [CrossRef]

- Lee, Y. Linking internal CSR with the positive communicative behaviors of employees: the role of social exchange relationships and employee engagement. Social Responsibility Journal 2022, 18(2), 348–367. [Google Scholar] [CrossRef]

- Onyekwelu, N. P.; Ezeafulukwe, C.; Owolabi, O. R.; Asuzu, O. F.; Bello, B. G.; Onyekwelu, S. C. Ethics and corporate social responsibility in HR: A comprehensive review of policies and practices. International Journal of Science and Research Archive 2024, 11(1), 1294–1303. [Google Scholar] [CrossRef]

- Yan, X.; Espinosa-Cristia, J. F.; Kumari, K.; Cioca, L. I. Relationship between corporate social responsibility, organizational trust, and corporate reputation for sustainable performance. Sustainability 2022, 14(14), 8737. [Google Scholar] [CrossRef]

- Inyang, B. J. Defining the role engagement of small and medium-sized enterprises (SMEs) in corporate social responsibility (CSR). International business research 2013, 6(5), 123. [Google Scholar] [CrossRef]

- Liakh, O.; Spigarelli, F. Managing corporate sustainability and responsibility efficiently: A review of existing literature on business groups and networks. Sustainability 2020, 12(18), 7722. [Google Scholar] [CrossRef]

- Hadi, N.; Udin, U. Testing the effectiveness of CSR dimensions for small business entrepreneurs. Journal of Open Innovation: Technology, Market, and Complexity 2020, 7(1), 6. [Google Scholar] [CrossRef]

- Hiss, S. From implicit to explicit corporate social responsibility: Institutional change as a fight for myths. Business Ethics Quarterly 2009, 19(3), 433–451. [Google Scholar] [CrossRef]

- Carlini, J.; Grace, D. The corporate social responsibility (CSR) internal branding model: Aligning employees’ CSR awareness, knowledge, and experience to deliver positive employee performance outcomes. Journal of Marketing Management 2021, 37(7-8), 732–760. [Google Scholar] [CrossRef]

- Park, B. I.; Ghauri, P. N. Determinants influencing CSR practices in small and medium sized MNE subsidiaries: A stakeholder perspective. Journal of World Business 2015, 50(1), 192–204. [Google Scholar] [CrossRef]

- Ying, Q.; Hassan, H.; Ahmad, H. The role of a manager’s intangible capabilities in resource acquisition and sustainable competitive performance. Sustainability 2019, 11(2), 527. [Google Scholar] [CrossRef]

- Cho, S. J.; Chung, C. Y.; Young, J. Study on the Relationship between CSR and Financial Performance. Sustainability 2019, 11(2), 343. [Google Scholar] [CrossRef]

- Shen, J.; Zhang, H. Socially responsible human resource management and employee support for external CSR: roles of organizational CSR climate and perceived CSR directed toward employees. Journal of Business Ethics 2019, 156(3), 875–888. [Google Scholar] [CrossRef]

- Suto, M.; Takehara, H. Corporate social responsibility and corporate finance in Japan; Springer Singapore, 2018. [Google Scholar]

- Chen, X.; Dong, X.; Ma, C. Investing with purpose: the role of CSR in enhancing Chinese firms’ performance in Japan. Journal of the Knowledge Economy 2024, 15(4), 20135–20171. [Google Scholar] [CrossRef]

- Arhinful, R.; Radmehr, M. The effect of financial leverage on financial performance: evidence from non-financial institutions listed on the Tokyo stock market. Journal of Capital Markets Studies 2023, 7(1), 53–71. [Google Scholar] [CrossRef]

- Barauskaite, G.; Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corporate Social Responsibility and Environmental Management 2021, 28(1), 278–287. [Google Scholar] [CrossRef]

- Arhinful, R.; Obeng, H. A.; Mensah, L.; Mensah, C. C. Signaling Sustainability: The Impact of Sustainable Finance on Dividend Policy Among Firms Listed on the London Stock Exchange. In Business Strategy and the Environment; 2025. [Google Scholar]

- Diez-Cañamero, B.; Bishara, T.; Otegi-Olaso, J. R.; Minguez, R.; Fernández, J. M. Measurement of corporate social responsibility: A review of corporate sustainability indexes, rankings and ratings. Sustainability 2020, 12(5), 2153. [Google Scholar] [CrossRef]

- Fenwick, T.; Bierema, L. Corporate social responsibility: issues for human resource development professionals. International Journal of training and Development 2008, 12(1), 24–35. [Google Scholar] [CrossRef]

- Basarab, D. J., Sr.; Root, D. K. The training evaluation process: A practical approach to evaluating corporate training programs; Springer Science & Business Media, 2012; Vol. 33. [Google Scholar]

- Pless, N. M.; Maak, T.; Stahl, G. K. Promoting corporate social responsibility and sustainable development through management development: What can be learned from international service learning programs? Human resource management 2012, 51(6), 873–903. [Google Scholar] [CrossRef]

- López-Pérez, M. E.; Melero, I.; & Javier Sesé, F. Does specific CSR training for managers impact shareholder value? Implications for education in sustainable development. Corporate Social Responsibility and Environmental Management 2017, 24(5), 435–448. [Google Scholar] [CrossRef]

- Lim, J. S.; Greenwood, C. A. Communicating corporate social responsibility (CSR): Stakeholder responsiveness and engagement strategy to achieve CSR goals. Public relations review 2017, 43(4), 768–776. [Google Scholar] [CrossRef]

- Arhinful, R.; Mensah, L.; Amin, H. I. M. Does corporate governance influence corporate social responsibility in developing African countries? Evidence from manufacturing companies listed in Ghana and Nigeria’s Stock Exchange. International Journal of Corporate Governance 2024, 14(3), 247–271. [Google Scholar] [CrossRef]

- Arhinful, R.; Amin, H. I. M.; Mensah, L.; Gyamfi, B. A.; Obeng, H. A. Determining an optimal capital structure and its impact on financial performance. Insight from the firms listed on the New York Stock Exchange. Cogent Economics & Finance 2025, 13(1), 2571401. [Google Scholar] [CrossRef]

- Arhinful, R.; Mensah, L.; Obeng, H. A.; Gyamfi, B. A. Corporate Social Responsibility Governance Systems: Catalysts for Sustainable Performance in London Stock Exchange Firms. In Sustainable Development; 2025. [Google Scholar]

- Arhinful, R.; Mensah, L.; Gyamfi, B. A.; Obeng, H. A. The impact of non-performing loans on bank growth: The moderating roles of bank size and capital adequacy ratio—Evidence from US banks. International Journal of Financial Studies 2025, 13(3), 165. [Google Scholar] [CrossRef]

- Mensah, L.; Arhinful, R.; Obeng, H. A.; Gyamfi, B. A. Analyzing the impact of operating leverage on sustainable performance in Japanese firms using contingency theory. Sustainable Development 2025. [Google Scholar]

- Bhattacharyya, A.; Rahman, M. L. Mandatory CSR expenditure and firm performance. Journal of Contemporary Accounting & Economics 2019, 15(3), 100163. [Google Scholar] [CrossRef]

- Bailey, N.; Kapetanios, G.; Pesaran, M. H. Exponent of cross-sectional dependence: Estimation and inference. Journal of Applied Econometrics 2016, 31(6), 929–960. [Google Scholar] [CrossRef]

- Abdallah, W.; Goergen, M.; O’Sullivan, N. Endogeneity: How failure to correct for it can cause wrong inferences and some remedies. British Journal of Management 2015, 26(4), 791–804. [Google Scholar] [CrossRef]

- Mensah, L.; Arhinful, R.; Obeng, H. A.; Gyamfi, B. A. Corporate Social Responsibility (CSR) Governance Systems in Shaping Firms’ Environmental Innovation on the London Stock Exchange. In Corporate Social Responsibility and Environmental Management; 2025. [Google Scholar]

- Pesaran, M. H. A simple panel unit root test in the presence of cross-section dependence. Journal of applied econometrics 2007, 22(2), 265–312. [Google Scholar] [CrossRef]

- Westerlund, J. New simple tests for panel cointegration. Econometric Reviews 2005, 24(3), 297–316. [Google Scholar] [CrossRef]

- Wooldridge, J. M. Econometric analysis of cross section and panel data; MIT press, 2010. [Google Scholar]

- Musau, V. M.; Waititu, A. G.; Wanjoya, A. K. Modeling panel data: Comparison of GLS estimation and robust covariance matrix estimation. American Journal of Theoretical and Applied Statistics 2015, 4(3), 185–191. [Google Scholar] [CrossRef]

- Holly, S.; Petrella, I.; Santoro, E. Aggregate fluctuations and the cross-sectional dynamics of firm growth. Journal of the Royal Statistical Society Series A: Statistics in Society 2013, 176(2), 459–479. [Google Scholar] [CrossRef]

- Ullah, S.; Akhtar, P.; Zaefarian, G. Dealing with endogeneity bias: The generalized method of moments (GMM) for panel data. Industrial Marketing Management 2018, 71, 69–78. [Google Scholar] [CrossRef]

- Arhinful, R.; Gyamfi, B. A.; Mensah, L.; Obeng, H. A. Non-performing loans and their impact on investor confidence: A Signaling Theory perspective—Evidence from US Banks. Journal of Risk and Financial Management 2025, 18(7), 383. [Google Scholar] [CrossRef]

- Mensah, L.; Arhinful, R.; Bein, M. A. The Impact of Corporate Governance on Financial Decision-making: Evidence from Non-financial Institutions in the Australian Securities Exchange. Asian Academy of Management Journal of Accounting and Finance 2024, 20(1), 41–95. [Google Scholar] [CrossRef]

- Arhinful, R.; Mensah, L.; Owusu-Sarfo, J. S. Board governance and ESG performance in Tokyo stock exchange-listed automobile companies: An empirical analysis. Asia Pacific Management Review 2024, 29(4), 397–414. [Google Scholar] [CrossRef]

- Mensah, L.; Bein, M. A. Sound corporate governance and financial performance: Is there a link? Evidence from manufacturing companies in South Africa, Nigeria, and Ghana. Sustainability 2023, 15(12), 9263. [Google Scholar] [CrossRef]

- Macpherson, W. G.; Lockhart, J. C.; Kavan, H.; Iaquinto, A. L. Kaizen: a Japanese philosophy and system for business excellence. Journal of Business Strategy 2015, 36(5), 3–9. [Google Scholar] [CrossRef]

- Walker, J.; Pekmezovic, A.; Walker, G. Sustainable development goals: Harnessing business to achieve the SDGs through finance, technology and law reform; John Wiley & Sons, 2019. [Google Scholar]

- Carneiro, L. S.; Henry, M. Integrating the Sustainable Development Goals into Corporate Governance: A Cross-Sectoral Analysis of Japanese Companies. Sustainability 2024, 16(15), 6636. [Google Scholar] [CrossRef]

- Obeng, H. A.; Atan, T. Understanding Turnover Intentions: The Interplay of Organizational Politics, Employee Resilience, and Person-Job Fit in Ghana’s Healthcare Sector. Sustainability (2071-1050) 2024, 16(22). [Google Scholar] [CrossRef]

- Urip, S. CSR strategies: Corporate social responsibility for a competitive edge in emerging markets; John Wiley & Sons, 2010. [Google Scholar]

- Gatzert, N.; Schmit, J. Supporting strategic success through enterprise-wide reputation risk management. The Journal of Risk Finance 2016, 17(1), 26–45. [Google Scholar] [CrossRef]

- Birinci, H.; Esenyel, I.; Obeng, H. A. Sustainable destination management in luxury tourism: Balancing economic development and environmental responsibility. Sustainability 2025, 17(15), 6815. [Google Scholar] [CrossRef]

- Villarón-Peramato, O.; García-Sánchez, I. M.; Martínez-Ferrero, J. Capital structure as a control mechanism of a CSR entrenchment strategy. European Business Review 2018, 30(3), 340–371. [Google Scholar] [CrossRef]

- Suto, M.; Takehara, H. Stakeholder Engagement and Innovation in Japan; Springer, 2025. [Google Scholar]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. Journal of banking & finance 2008, 32(9), 1723–1742. [Google Scholar]

- Asare Obeng, H.; Atan, T. The public hospital exodus: Unraveling the interplay of turnover intentions and organizational politics. SAGE Open 2025, 15(3), 21582440251337902. [Google Scholar] [CrossRef]

Figure 1.

Conceptual framework.

Table 1.

Dependent, independent, and control variables.

| Index | Variable | Acronym | Formulae |

|---|---|---|---|

| Dependent variable: | |||

| 1 | CSR performance | CSRPFM | ESG Score (0 to 100) |

| Independent variable: | |||

| 1 | Employees’ CSR training | ECSRTN | Number of CSR trainings organized by the companies in a year. |

| Control variables | |||

| 1 | CSR strategy | CRSSTG | CSR strategy score (0-100) |

| 2 | Age of the firm | AGOTF | It was determined by subtracting the year of incorporation by the companies from the observation year. |

| 3 | Leverage | LEVER | |

| 4 | Return on assets (ROA) | ROA | |

| Moderating variables | |||

| 1 | Size of the firm | SZOTFM | Log (total assets) |

| 2 | CSR expenditures (intensity) | CSEEXPEN |

Table 2.

Heterogeneity, Cross-sectional and endogeneity tests.

| Types tests | CSR performance |

| Cross-sectional tests | |

| Pesaran’s test | 10.322 *** |

| Friedman’s test | 127.332 *** |

| Frees’ test | 32.531 *** |

| Heterogeneity test (Peseran-Yamagata test) | |

| Δ-tilde stat. | 13.061 *** |

| Δadj-tilde stat. | 28.222 *** |

| Endogeneity test | |

| Durbin-Wu-Hausman (DWH) Test | 6.584 *** |

|

*** p<.01, ** p<.05, * p<.1. | |

Table 3.

Stationary assessment.

| Variable | Cross-Sectional Augmented Dickey-Fuller (CADF) | Cross-sectional Augmented IPS (CIPS) | ||

| Levels | 1st Difference | Levels | 1st Difference | |

| CSR performance | -5.843 *** | -13.537 *** | -5.034 *** | -13.032 *** |

| Employees’ CSR training | -15.047 *** | -35.242 *** | -16.098 *** | -38.362 *** |

| CSR strategy | -20.032 *** | -48.800 *** | -21.032 *** | -45.044 *** |

| Age of the firm | -8.135 *** | -19.203 *** | -8.521 *** | -20.642 *** |

| Leverage | -6.388 *** | -27.145 *** | -8.405 *** | -23.135 *** |

| ROA | -11.242 *** | -22.003 *** | -10.993 *** | -21.077 *** |

| Size of the firm | -4.003 *** | -13.072 *** | -4.088 *** | -14.743 *** |

| CSR expenditures | -37.036 *** | -73.342 *** | -38.563 *** | -72.441 *** |

| *** p<.01, ** p<.05, * p<.1. | ||||

Table 4.

Westerlund test for cointegration.

| Test | CSR performance |

| Westerlund test | -9.036 *** |

| *** p<.01, ** p<.05, * p<.1. | |

Table 5.

Descriptive statistics.

| Variable | Obs | Mean | Std. Dev. | Min | Max | VIF | 1/VIF |

| CSR performance | 7,320 | 64.09 | 43.832 | 11.031 | 96.37 | - | - |

| Employees’ CSR training | 7,320 | 6 | 2.344 | 2 | 14 | 1.373 | 0.728 |

| CSR strategy | 7,320 | 50.32 | 39.362 | 5.04 | 96.34 | 1.422 | 0.703 |

| Age of the firm | 7,320 | 58 | 40.463 | 3 | 189 | 1.993 | 0.502 |

| Leverage | 7,320 | 2.284 | .973 | 0.122 | 14.362 | 1.382 | 0.724 |

| ROA | 7,320 | 6.142 | 2.402 | -27.871 | 20.027 | 1.075 | 0.930 |

| Size of the firm | 7,320 | 7.883 | 1.029 | 1.009 | 13.462 | 1.332 | 0.751 |

| CSR expenditures | 7,320 | 2.052 | 0.862 | 0.162 | 8.225 | 1.455 | 0.687 |

Table 6.

Matrix correlation analysis.

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| (1) CSR performance | 1.000 | |||||||

| (2) Employees’ CSR training | 0.026 | 1.000 | ||||||

| (3) CSR strategy | 0.032 | 0.163 | 1.000 | |||||

| (4) Age of the firm | 0.142 | 0.033 | 0.483 | 1.000 | ||||

| (5) Leverage | 0.188 | 0.026 | 0.305 | 0.087 | 1.000 | |||

| (6) ROA | 0.292 | 0.172 | 0.203 | 0.343 | 0.027 | 1.000 | ||

| (7) Size of the firm | 0.223 | 0.499 | 0.213 | 0.472 | 0.038 | 0.423 | 1.000 | |

| (8) CSR expenditures | 0.142 | 0.222 | 0.171 | 0.108 | 0.378 | 0.406 | 0.311 | 1.000 |

Table 7.

Feasible generalized least squares.

| Variables | CSR performance | ||

| Model 1 | Model 2 | Model 3 | |

| Employees’ CSR training | 0.389 *** (0.022) |

0.405 *** (0.021) |

0.412 *** (0.023) |

| CSR strategy | 0.755 *** (0.311) |

0.762 *** (0.303) |

0.766 *** (0.309) |

| Age of the firm | 0.068 *** (0.019) |

0.071 *** (0.019) |

0.072 *** (0.018) |

| Leverage | -0.173 *** (0.017) |

-0.182 *** (0.018) |

-0.186 *** (0.019) |

| ROA | 0.435 *** (0.091) |

0.452 *** (0.088) |

0.467 *** (0.090) |

| Size of the firm | 0.288 *** (0.016) |

0.253 *** (0.015) |

0.263 *** (0.014) |

| CSR expenditures | 0.596 *** (0.186) |

0.602 *** (0.184) |

0.616 *** (0.191) |

| Employees’ CSR training × firm size | 0.308 *** (0.061) |

||

| Employees’ CSR training × CSR expenditures | 0.043 *** (0.011) |

||

| Constant | 1.473 *** (0.066) |

1.483 *** (0.061) |

1.488 *** (0.065) |

| Number of observations | 7,320 | 7,320 | 7,320 |

| Chi-square | 3.943 *** | 3.964 *** | 3.994 *** |

| * ** p<.01, ** p<.05, * p<.1. | |||

Table 8.

Augmented Mean Group (AMG) estimator.

| Variables | CSR performance | ||

| Model 1 | Model 2 | Model 3 | |

| Employees’ CSR training | 0.597 *** (0.204) |

0.604 *** (0.204) |

0.618 *** (0.211) |

| CSR strategy | 0.843 *** (0.330) |

0.848 *** (0.329) |

0.851 *** (0.332) |

| Age of the firm | 0.070 *** (0.014) |

0.072 *** (0.014) |

0.077 *** (0.013) |

| Leverage | -0.104 *** (0.012) |

-0.108 *** (0.012) |

-0.119 *** (0.014) |

| ROA | 0.209 *** (0.052) |

0.228 *** (0.050) |

0.248 *** (0.049) |

| Size of the firm | 0.387 *** (0.101) |

0.396 *** (0.103) |

0.403 *** (0.102) |

| CSR expenditures | 0.513 *** (0.222) |

0.533 *** (0.228) |

0.585 *** (0.226) |

| Employees’ CSR training × firm size | 0.388 *** (0.094) |

||

| Employees’ CSR training × CSR expenditures | 0.188 *** (0.028) |

||

| CD-statistic | 0.436 *** (0.042) |

0.584 *** (0.038) |

0.592 *** (0.040) |

| Constant | 1.833 *** (0.028) |

1.830 *** (0.027) |

1.855 *** (0.031) |

| Observation | 7,320 | 7,320 | 7,320 |

| Wald tests | 3.948 *** | 3.953 *** | 3.983 *** |

| RMSE | 0.031 | 0.037 | 0.035 |

| *** p<.01, ** p<.05, * p<.1. | |||

Table 9.

Two-step GMM (Difference method).

| Variables | CSR performance | ||

| Model 1 | Model 2 | Model 3 | |

| CSR performance (-1) | 0.386 *** (0.017) |

0.388 *** (0.017) |

0.395 *** (0.016) |

| Employees’ CSR training | 0.463 *** (0.188) |

0.478 *** (0.185) |

0.482 *** (0.187) |

| CSR strategy | 0.193 *** (0.041) |