Submitted:

03 February 2026

Posted:

05 February 2026

You are already at the latest version

Abstract

This study investigates Thai investors’ intentions to invest in financially innovative digital assets by extending the Theory of Planned Behavior (TPB) with financial literacy and trust to better reflect the context of emerging digital asset ecosystems. Using a quantitative survey design, data were collected from 360 mutual fund investors who were transitioning from traditional investment instruments to digital assets, and the hypothesized relationships among latent constructs were analyzed using structural equation modeling to assess both measurement properties and structural paths. The results indicate that attitude toward behavior, subjective norms, and perceived behav-ioral control all exert significant positive effects on investment intention, consistent with TPB. In addition, financial literacy and trust are identified as important contextual determinants: higher financial literacy is associated with greater perceived capability to evaluate risk and return, while trust in platforms, technologies, and regulatory safe-guards is linked to lower psychological barriers to participation. Among the examined factors, financial literacy and subjective norms show the strongest combined influence on investment intention. These findings suggest that, in the Thai digital asset market, intention formation is shaped not only by classical behavioral antecedents but also by investors’ knowledge levels and the social and institutional environment supporting digital financial innovations.

Keywords:

digital asset investment

; theory of planned behavior

; financial literacy

; trust

; investment intention

; Thai investors

; structural equation modeling

1. Introduction

In recent years, technology has become an inseparable component of everyday life, to the extent that contemporary society is virtually unimaginable without it (Banna et al., 2021). Information and communications technology has played a pivotal role in transforming the economic and social landscape of many developing countries, while financial technology has been central to reshaping the architecture of global finance (Abbasi et al., 2021). Within this evolving environment, digital financial ecosystems are rapidly redefining how individuals manage money, credit, and investments, thereby reconfiguring traditional financial intermediation and access to financial services (Lal et al., 2025). Financial innovation, as emphasized by Błach (2011), manifests in multiple forms, among which the creation of new investment instruments is particularly salient. These innovations have the potential not only to enhance the safety and resilience of financial systems but also to expand the spectrum of tradable asset classes and improve overall market liquidity through mechanisms such as asset fractionalization (Bank of England, 2024).

A central outcome of this technological and financial evolution is the emergence of financial digital assets, whose development is fundamentally underpinned by blockchain technology. Blockchain enables key processes such as tokenization, decentralized asset management, and digital currency transactions, thereby transforming how financial services are designed, delivered, and consumed (Javaid et al., 2022). By embedding trust and security through smart contracts, blockchain also contributes to improved sustainability performance and more transparent governance structures in financial and non-financial applications (Faozi et al., 2025). Technically, a blockchain is a distributed ledger in which transactions are replicated and stored across multiple nodes; these transactions are grouped into blocks that function as immutable records, ensuring the integrity of historical data (Di Pierro, 2017). The implementation of blockchain technology thus reduces intermediation costs, enhances transparency in the handling of user funds, and mitigates the risk of mismanagement or opportunistic behavior (Ammous, 2016).

Within this infrastructure, digital assets have been formalized and classified in more precise regulatory terms. The Thailand’s Securities and Exchange Commission (SEC, 2025) categorizes digital assets into two principal groups: digital tokens and cryptocurrencies. Digital tokens are further divided into investment tokens—electronic data units that confer rights to participate in an investment project or business, such as those issued via Initial Coin Offerings (ICOs)—and utility tokens, which grant rights to access or acquire specific goods and services, for example, non-fungible tokens (NFTs). Cryptocurrencies, by contrast, are electronic data units created primarily as a medium of exchange, with prominent examples including Bitcoin, Ethereum, and Tether (SEC, 2025). This regulatory classification underscores the diversity within the digital asset space and provides a conceptual foundation for analyzing their economic and financial roles.

The rise of digital assets, particularly cryptocurrencies, has led to their growing recognition as a novel class of financial investment instruments. Cryptocurrencies have emerged as a transformative force in global finance, offering alternative investment opportunities to both retail and institutional investors (Lua et al., 2025). Owing to their specific characteristics as digital exchange commodities—such as the ability to store value in tokenized form—cryptocurrencies have become a significant topic in finance, serving as alternative assets for portfolio diversification and hedging purposes (Brière et al., 2015; Subramaniam and Chakraborty, 2020). Investors increasingly regard cryptocurrencies as an investable asset class alongside traditional instruments like stocks, bonds, and real estate (Zhao and Zhang, 2021). Although they remain a relatively new investment vehicle, the aggregate market value of cryptocurrencies has reached approximately one-ninth of gold’s market capitalization, suggesting that while they may not fully replace gold, they possess the potential to challenge both gold and major fiat currencies such as the Euro and the US dollar as stores of value and investment assets (Bland et al., 2024). Moreover, empirical evidence indicates that cryptocurrencies can function as hedging tools, providing diversification benefits to investors seeking to reduce portfolio risk (Kyriazis et al., 2023).

Against this backdrop, digital assets have experienced a marked increase in popularity worldwide. The global digital asset management market was valued at 3.96 billion US dollars in 2023 and is projected to expand to 16.18 billion US dollars by 2032, reflecting a compound annual growth rate of 17% between 2024 and 2032 (Fortune Business Insights, 2024). Furthermore, the World Economic Forum estimates that digital assets could account for as much as 10% of global gross domestic product, or more than 86 trillion US dollars, by 2030, underscoring their anticipated long-term significance as investment assets. In developing economies, such as India, cryptocurrencies are increasingly used as instruments for saving, investing, and cross-border remittances (Kashyap et al., 2021). Similarly, in Indonesia, the number of crypto investors grew by 280% between 2020 and 2022, rising from 1.5 million to 4.2 million individuals, with a daily trading volume of approximately 117.4 million US dollars (Blockchain Association of Indonesia, 2022). Notably, by 2022 the number of Indonesian individuals investing in cryptocurrencies exceeded those investing in stocks (Tjondro, 2023). In advanced economies, such as the United States, the capitalization of digital assets has reached around 3 trillion US dollars, and approximately 16% of Americans have purchased cryptocurrencies, indicating substantial room for further development in terms of reliability, stability, and real-world transactional usage (White House Fact Sheet, 2022).

The financing dimension of digital assets has also evolved rapidly, particularly through ICOs as a novel fundraising mechanism. During the most active ICO period, projects raised more than 20 billion US dollars via ICO whitepapers, signaling strong market interest and speculative capital inflows (Gomaa and Li, 2022). ICOs represent a new paradigm of capital raising, enabling firms to secure substantial funds from global investors outside traditional capital markets (Winotoatmojo et al., 2022). These offerings have collectively raised tens of billions of dollars, prompting investors, entrepreneurs, and policymakers to scrutinize ICOs as a serious funding channel (Fisch, 2019). However, institutional investors, economists, and researchers hold divergent views regarding both ICOs and cryptocurrencies, reflecting ongoing debates over valuation, regulation, and long-term viability (Halaburda, 2018; Zheng et al., 2018).

Thailand closely mirrors these global trends in digital asset development. According to the Securities and Exchange Commission of Thailand (2022), as of May 2022 there were approximately 500,000 active digital asset investor accounts, compared with about 600,000 stock market investor accounts over the same period. The number of digital asset investors in Thailand has increased rapidly, driven by several factors, including the appeal of decentralized ownership, the prospect of higher short-term returns relative to traditional investments, and the influence of innovative financial products (Bank of Thailand, 2022). The SEC reports that the number of trading accounts on digital asset exchanges surged from around 170,000 in 2020 to more than 2.5 million by February 2022, with the majority belonging to individual retail investors (Securities and Exchange Commission, 2022). This rapid expansion highlights both the depth of retail participation and the systemic relevance of digital assets in the Thai financial system.

Reflecting this momentum, financial digital assets have become a focal point for policy and strategic development in Thailand. In February 2025, the Thai Cabinet approved the draft Financial Business Hub Act, which is undergoing further legislative review and comprises nine chapters and 96 sections. Within this framework, “Digital Asset” is identified as one of eight targeted business sectors under the proposed Financial Hub regime (Kasikorn Research, 2025). The swift growth of Thailand’s digital asset market underscores the increasing importance of effective policy design, robust regulatory oversight, and strategic planning for digital asset brokerage firms and related intermediaries. In this context, understanding the investment intentions of Thai investors is crucial for shaping sound supervisory frameworks, ensuring market stability, and promoting sustainable sectoral development.

Given these dynamics, digital assets—as a prominent form of financial innovation—constitute a compelling subject of academic inquiry. Investment decisions in this domain are typically grounded in trust and security which enable consumers to act rationally and feel empowered in their financial choices (Sharma et al., 2025). Behavioral finance theory further suggests that investors’ decision-making processes are shaped not only by classical economic considerations such as risk and return but also by a broader set of behavioral, psychological, and contextual influences (Treerotchananon et al., 2024). Empirical evidence shows that the largest share of crypto-assets is held by households, which motivates household finance scholars to examine the prevalence of crypto investors as well as the socio-economic, demographic, financial, and environmental determinants of cryptocurrency exposure in individual portfolios (Manaa et al., 2019).

These challenges indicate a clear research gap, particularly in the Thai context, where there is a need to investigate digital asset investment intention by integrating behavioral, psychological, social, and financial factors in order to better explain investor participation and guide policy and practice.

Therefore, this study seeks to examine the behavioral, financial, psychological, and social determinants that shape Thai investors’ investment intentions toward innovative digital assets. Specifically, it focuses on key constructs including attitude toward behavior, subjective norms, perceived behavioral control, financial literacy, and trust. Furthermore, the study aims to develop and empirically validate a comprehensive research framework using structural equation modeling to integrate these constructs and elucidate their collective influence on investor intention in the emerging digital asset market. By analyzing the interrelationships among these behavioral, psychological, social, and financial factors, the research offers empirically grounded insights that contribute to a deeper understanding of investment intention within Thailand’s evolving digital asset landscape. The findings are anticipated to advance evidence-based policymaking, inform strategic market development, and enrich the academic discourse in this rapidly transforming field.

Building on this, the study’s comprehensive framework underpins both academic rigor and practical applicability, generating insights that are highly relevant for scholars, policymakers, and financial practitioners operating within Thailand’s dynamic investment environment with risk mitigation. Its results carry significant implications for designing more effective investor education initiatives and regulatory strategies that are specifically calibrated to the distinctive features of financial digital asset markets in emerging economies.

2. Theoretical Framework

2.1. Theory of Planned behavior (TPB)

The Theory of Planned Behavior (TPB) is a prominent and widely adopted framework in behavioral research across multiple disciplines and is regarded as an efficient model for explaining and predicting intentions to use various technologies (Shaw and Shiu, 2013; Hu et al., 2019). According to TPB, behavioral intention is determined by three core components: attitude toward the behavior, subjective norms, and perceived behavioral control (Ajzen, 1985). Attitude toward the behavior reflects an individual’s positive or negative evaluation of performing a specific action, subjective norms refer to perceived social pressure to engage or not engage in the behavior, and perceived behavioral control denotes the perceived ease or difficulty of performing the behavior, shaped by available resources and opportunities (Ajzen, 1985).

In financial contexts, these three components—attitude toward the behavior, subjective norms, and perceived behavioral control—serve as key predictors of investment intention. Investment decisions are inherently voluntary, making the intention to invest a central element of the decision-making process, and a nuanced understanding of investor behavior and the dynamics of the investment sector therefore requires close examination of investment intentions (Dash et al., 2021). The study of intentions among consumers, investors, and other decision-makers has long been recognized as a significant area of inquiry, particularly given the complexity of investment choices and the need to identify the factors that shape investors’ intentions (Meng and Choi, 2018).

Investment intention is rooted in the broader construct of behavioral intention, which is widely acknowledged as the immediate antecedent of actual behavior (Ajzen, 2002). Behavioral intention captures an individual’s motivation or willingness to undertake a specific action (Yadav and Pathak, 2017). In the context of investment, this implies that the stronger an individual’s intention to invest, the higher the likelihood that the investment behavior will materialize (Xiao et al., 2011). Consequently, assessing the strength of investment intention offers valuable insights into the probability of actual investment activity.

Within financial research, TPB is frequently employed to examine and interpret behavioral finance phenomena, especially in relation to investment intentions. The model has been extensively applied to analyze how individuals form intentions to invest in a range of financial instruments, including stocks and mutual funds, as demonstrated in the studies by Akhtar and Das (2019) and Adil et al. (2023).

2.1.1. Subjective Norms

Subjective norms, or prescriptive social influences, play a critical role in financial decision-making, particularly in shaping individuals’ evaluations of whether a behavior is socially accepted or disapproved (Khaw et al., 2023). Subjective norm is defined as the perceived social pressure exerted by significant individuals or groups that influences a person’s intentions and actions (Ajzen and Driver, 1992). This construct is rooted in an individual’s beliefs about the expectations of key referents and their motivation to comply with those expectations, thereby capturing the extent to which social influences—such as those from family and friends—affect personal decisions and behaviors (Hapsari, 2021). Reflecting its importance, numerous studies have examined the effect of subjective norms on investment intention. For example, Adam and Shauki (2014) and Khan et al. (2022) provide evidence of a positive relationship between subjective norms and investment intention, which informs the development of hypothesis H2b in this research. In addition, prior work applying the full set of Theory of Planned Behavior constructs in technology-related contexts has demonstrated interrelationships between subjective norms and other variables: Liang (2016) and Kumari et al. (2022) identify a link between subjective norms and attitude toward behavior, supporting hypothesis H2a, while Gumasing and Niro (2023) show an association between subjective norms and perceived behavioral control, underpinning hypothesis H2c.

Building on a synthesis of prior literature, subjective norms can be conceptualized as comprising three primary components: normative belief, social influence, and social media. This tripartite structure is supported by empirical studies such as Adam and Shauki (2014), Pop et al. (2020), and Misra et al. (2021). Normative belief refers to an individual’s perception of the expectations held by reference groups and their motivation to conform to these expectations (Misra et al., 2021; Pilatin and Dilek, 2024). Social influence reflects the extent to which individuals perceive a technology or behavior as important or necessary, a perception that is increasingly shaped by peer and influencer endorsements (Dwivedi et al., 2017; Kilani et al., 2023). In contemporary settings, social media functions as a dynamic platform that amplifies these influences through continuous information exchange and interaction, thereby reinforcing social conformity in the digital era.

2.1.2. Attitude Towards Behavior

Attitudes and intentions are central to understanding the internal factors that influence investment intention, particularly within the framework of the Theory of Planned Behavior (TPB) (Garg et al., 2022). Eagly and Chaiken (1993) define attitude toward behavior in a manner consistent with Ajzen (1985), as an individual’s psychological and cognitive evaluation that reflects varying degrees of favor or disfavor toward a specific action. Generally, the more positively an individual evaluates a behavior, the greater the perceived social approval and the perceived ease of performing that behavior, thereby strengthening behavioral intention (Ajzen, 1991). This positive relationship between attitude and behavioral intention has been repeatedly hypothesized and empirically supported across multiple disciplines, including finance. For example, Nugraha and Rahadi (2021) report that, among young investors, attitude toward behavior is the only significant determinant of stock investment intention, while Rahadjeng and Fiandari (2020) similarly find that attitude significantly affects share investment intention in Indonesia. These findings underscore the pivotal role of attitude in shaping investment intentions and reinforce the view that TPB constructs are robust predictors of financial investment intention and decision-making.

Ajzen (1988) explains that attitude reflects the degree to which a person evaluates performing a particular behavior positively or negatively, shaped by both the value attached to the behavior and the expected satisfaction derived from it. In line with this, Armitage and Conner (2001) argue that stronger positive attitudes toward a behavior generally correspond to stronger intentions to perform it. Given this importance, attitude toward behavior clearly plays a crucial role in shaping investment intention, as highlighted by Nugraha and Rahadi (2021), and it therefore forms the basis for hypothesis H5 in this research. A review and synthesis of the relevant literature indicate that attitude toward behavior can be understood through three key components: behavioral belief, innovativeness, and past behavior. Behavioral belief concerns the anticipated outcomes of engaging in a specific behavior (Adam and Shauki, 2014); innovativeness captures an individual’s openness to and readiness for adopting new technologies (Colby and Parasuraman, 2001; Lim and Fakhrorazi, 2020; Shahzad et al. 2024); and past behavior reflects accumulated experiences that shape and inform future actions (Raut, 2020; Pilatin and Dilek, 2024). Drawing on Ajzen (1991), a robust positive correlation is observed between attitudes and intentions, which, in turn, influence behavior, and this relationship has been widely validated in diverse contexts (Abbasi et al., 2021;; Warsame and Ireri, 2016). In the Thai context, Treerotchananon et al. (2024) highlight the importance of personality in shaping investment behavior through its influence on attitudes, while Akhtar and Das (2019) apply an adapted TPB model to examine investment intentions among individual investors in India, further illustrating the relevance and applicability of attitude-focused analyses in financial decision-making.

2.1.3. Perceived Behavioral Control

Perceived behavioral control refers to an individual’s assessment of how easy or difficult it is to perform a specific behavior, taking into account prior experiences and anticipated obstacles (Ajzen, 1991). When individuals believe they possess sufficient resources and confidence, their intention to engage in the behavior is strengthened (Ajzen, 1985). In line with this conceptualization, perceived behavioral control has been widely examined for its influence on investment intention, as demonstrated by Ejigu and Filatie (2020), which forms the basis for hypothesis H4b in this research. Furthermore, other studies have identified a relationship between perceived behavioral control and attitude, including the findings of Awn and Azam (2020), which underpin hypothesis H4a.

A synthesis of prior research identifies three primary elements of perceived behavioral control: facilitating conditions, control belief, and self-efficacy. Facilitating conditions refer to environmental factors that support the performance of a behavior (Oliveira et al., 2016; Sebayang et al., 2024). Control belief involves an individual’s perception of factors that enable or constrain the behavior (Adam and Shauki, 2014). Self-efficacy concerns an individual’s confidence in their capability to carry out specific actions (Ajzen, 2002; Sharahiley, 2020; Sebayang et al., 2024).

2.2. Extended Variables

2.2.1. Financial Literacy

Financial literacy, broadly defined as the ability to understand and effectively apply financial knowledge and skills such as personal financial management, budgeting, and investing, is fundamental to sound financial decision-making (Shaikh and Khan, 2025). Many prior studies demonstrate that financial literacy promotes more rational decision-making across a range of financial contexts (Homma et al., 2025; Bawalle et al., 2025; Lusardi and Mitchell, 2014;). In a similar vein, Ahmad and Shah (2022) suggest that financial literacy enhances the quality of investment decisions and overall performance, while evidence from the Pakistani equity market highlights the importance of financial literacy—alongside market anomalies—in shaping investors’ decision-making processes (Abideen et al., 2023). Consequently, financial literacy has become a pressing concern for governments, educators, and individuals, as people are increasingly required to assume greater responsibility for their own financial well-being (Campbell et al., 2011).

Financial literacy can also be described as a process of acquiring the knowledge and skills necessary to manage personal finances effectively. Access to financial and investment services, when combined with higher levels of financial literacy, has been shown to yield positive macroeconomic effects, including higher savings rates and reductions in crime (World Bank, 2023). Empirical research indicates that more financially literate individuals are more likely to save and invest, leading to greater participation in financial markets and a lower probability of bankruptcy (Cole et al., 2012), outcomes that contribute to enhanced economic stability and financial security (Matewos et al., 2016). Reflecting this importance, numerous studies have investigated the impact of financial literacy on financial behaviors such as investment intention. For example, Akhtar and Das (2017) find a positive and significant effect of financial literacy on investment intention in the Indian stock market, a result echoed by Herawati and Dewi (2019), which forms the basis for hypothesis H1b. Moreover, financial literacy has been found to influence two key constructs of the Theory of Planned Behavior: attitude toward behavior and perceived behavioral control. Syarkani and Tristanto (2022) report a positive relationship between financial literacy and attitude toward behavior, supporting hypothesis H1a, while Raut (2020) provides evidence that financial literacy positively affects perceived behavioral control, supporting hypothesis H1c. A synthesis of academic studies and institutional reports indicates that financial literacy comprises three core components—financial knowledge, financial behavior, and financial attitude—as recognized by OECD (2016), Morgan and Trinh (2019), the Bank of Thailand (2020), and Potrich et al. (2020). Financial knowledge entails understanding key concepts such as interest, inflation, and investment risk; financial behavior encompasses actions like saving and budgeting; and financial attitude reflects beliefs and values about money management. Together, these elements offer a comprehensive basis for assessing and promoting financial literacy.

2.2.2. Trust

Research on consumer behavior has traditionally been guided by theoretical models grounded in economic, rational assumptions, particularly in the financial sector, where decision-making is widely understood to rest on the pillars of trust, privacy, and security (Alexander and Cumming, 2020; Keneley, 2020). Trust, in particular, has been identified as a critical determinant of users’ attitudes and behaviors toward financial technologies, including FinTech services and digital assets (Zarifis and Cheng, 2022). For instance, Steinmetz et al. (2021) emphasize that trust is a key driver of investment decisions in cryptocurrencies, while Catalini and Gans (2016) note that trust in cryptocurrency platforms becomes especially salient in environments characterized by high distrust in traditional financial institutions, where such platforms provide a credible alternative for individuals seeking greater control over their finances. Empirical studies further show that users who believe their financial data will be protected and their privacy respected are more likely to intend to use FinTech platforms (Bongomin and Ntayi, 2020), and that trust in security to adopt digital financial services (Setiawan et al., 2023). Recent work also supports an interaction between trust and financial literacy in shaping behavioral intentions toward central bank digital currencies (CBDC), underscoring the joint importance of these constructs in the adoption of innovative financial instruments (Palanisamy et al., 2025).

Trust is commonly defined as the personal belief that another party will act with honesty and integrity (Bottazzi et al., 2016). Its significance in financial decision-making is underscored by Guiso et al. (2009), who find that individuals with higher levels of trust are more likely to invest in stocks and other risky assets. Trust has also been shown to play a crucial role in shaping investment intentions, as evidenced by Maziriri et al. (2019), which provides the basis for hypothesis H3b in this research, while prior studies such as Amro et al. (2018) establish a positive relationship between trust and attitude toward behavior, supporting hypothesis H3a. A review of international literature identifies three key components of trust in the digital era: source credibility, privacy, and security (Ryu et al., 2018; Tran and Nguyen, 2022). Source credibility concerns the perceived trustworthiness, competence, and goodwill of individuals or institutions; privacy refers to the degree of control individuals have over the disclosure of their personal or transactional information; and security relates to the protection of personal data against unauthorized access. Collectively, these dimensions form the core structure of trust and are essential for understanding trust-based decision-making in contemporary digital financial environments.

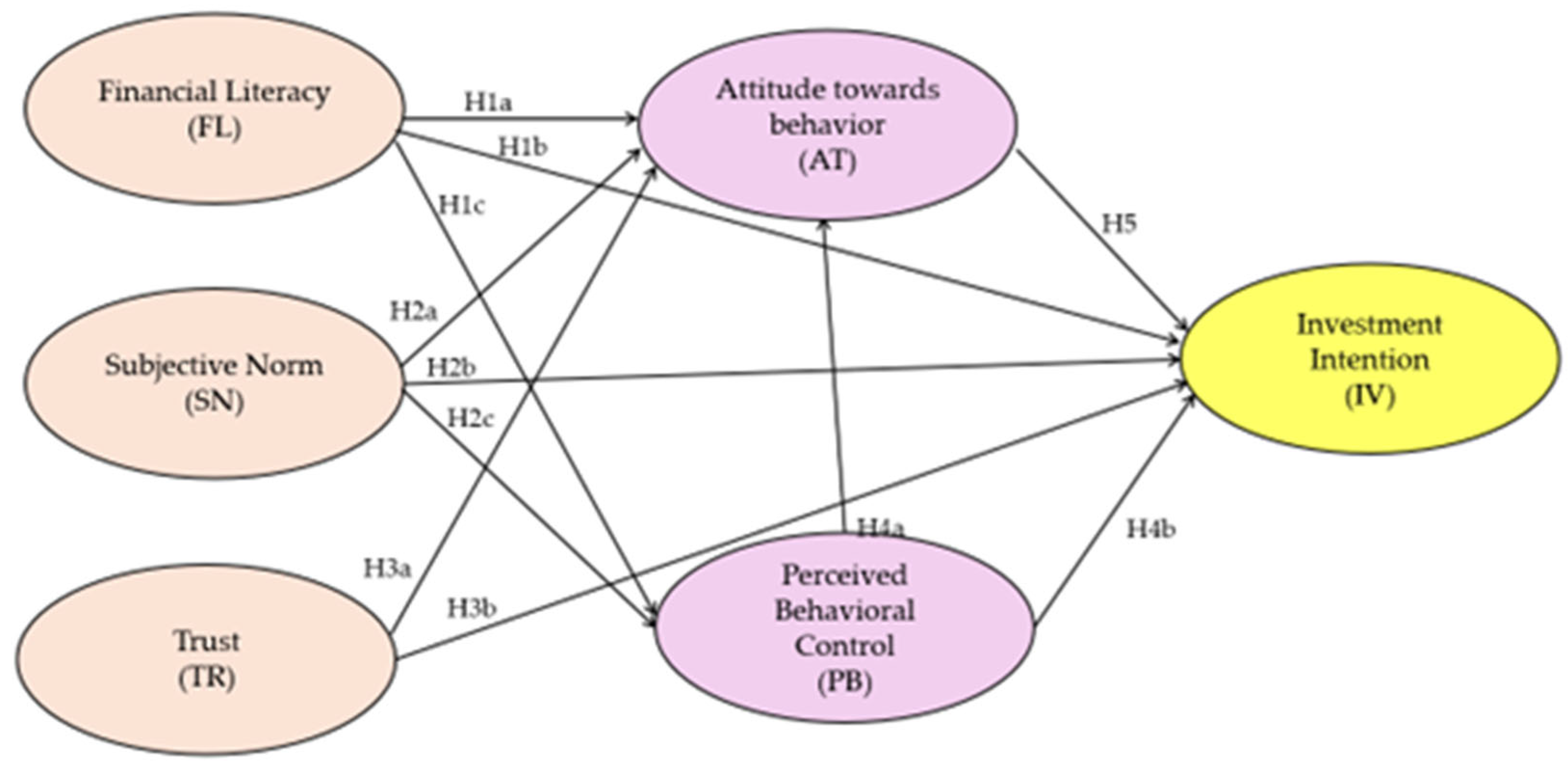

3. Hypothesis Development and Conceptual Framework

A comprehensive review of international academic literature indicates that five key factors significantly influence investment intentions in innovative digital assets: financial literacy, subjective norms, trust, perceived behavioral control, and attitude toward behavior. Evidence from prior studies provides a robust basis for understanding the interrelationships among these variables and supports the development of a conceptual framework and associated hypotheses to examine their effects on investment intentions in financially innovative digital assets within the Thai context. The research hypotheses derived from this review are articulated. Drawing on the aforementioned hypothesis development, the proposed conceptual framework is presented below.

Figure 1.

Conceptual framework.

4. Research Methodology

4.1. Research Design

The research employed a targeted sample and structured design to investigate investment intentions in digital financial assets. The population comprised investors in various asset classes, with particular emphasis on mutual fund investors, as mutual funds in Thailand span low- to high-risk categories, whereas digital assets are classified as the highest-risk category (Securities and Exchange Commission, 2024; Securities and Exchange Commission, n.d.). Purposeful sampling was used to select 360 investors with medium to high risk acceptance in mutual fund investment, reflecting the risk tolerance required for digital asset investment and enabling the examination of investment intention irrespective of risk acceptance level. The sample size was determined in accordance with criteria for structural equation modelling proposed by Hair et al. (2010), ensuring adequacy for subsequent model estimation.

4.2. Data Collection

Data were collected using a structured questionnaire with 54 items based on demographic, investment behaviors and variables a five-point Likert scale, where 5 represented the highest level and 1 the lowest, as in Table A1. Questionnaires were distributed to current mutual fund holders through Thai asset management companies, and all responses were checked for completeness and accuracy prior to analysis. The instrument was designed to capture patterns of investment intention in digital financial assets, as well as respondents’ perceptions, attitudes, demographic characteristics, investment objectives, and investment experience, alongside the key variables hypothesized to influence their intention to invest in digital assets.

4.3. Validity, Reliability and Data Analysis

The validity and reliability of the research instrument were rigorously assessed. Content validity was evaluated using the Index of Item–Objective Congruence (IOC), based on reviews by five experts in the field, including management-level positions at the Thai Securities and Exchange Commission. After revisions informed by IOC feedback, the questionnaire was pilot-tested with 30 respondents similar to, but distinct from, the main sample, and the pilot data were used to calculate Cronbach’s alpha coefficients for reliability. Items with alpha values of 0.70 or higher were deemed to have satisfactory reliability and to be suitable for data collection (Cronbach, 1951; Tenenhaus et al., 2005).

5. Research Results

5.1. Descriptive Data

The majority were female, totaling 211 individuals (58.6%), while 149 were male (41.4%). Most respondents were between 31 and 40 years of age (50.6%). The largest group held a bachelor’s degree, accounting for 198 individuals (55.0%). Most respondents were single, totaling 260 individuals (72.2%), and the majority were employed as full-time staff, totaling 246 individuals (68.3%). In terms of income, the largest proportion reported a monthly income in the range of 30,001–50,000 baht, totaling 104 individuals (28.9%) as in Table B1.

The investment-related characteristics of the respondents can be summarized as follows. Most had 5–10 years of investment experience, totaling 123 respondents (34.2%), and most reported investing with a frequency of 2–3 times per year, totaling 160 respondents (44.4%). A large proportion indicated that their financial situation was unstable, totaling 152 individuals (42.2%). The main investment objectives were to generate additional income, increase asset value, and seek opportunities from new asset classes, reported by all 360 respondents (24.16%). Regarding information sources, all respondents (360 individuals; 33.96%) relied on social media platforms (e.g., Facebook, Twitter, YouTube) as well as friends, family, or close acquaintances for financial and investment information. Most respondents reported a medium risk tolerance (seeking good returns), totaling 170 individuals (47.22%). The most important factor influencing their decision to invest in digital assets was the future growth potential of the assets. All respondents reported having at least a basic level of knowledge and understanding of digital asset investment, totaling 360 individuals as in Table B2.

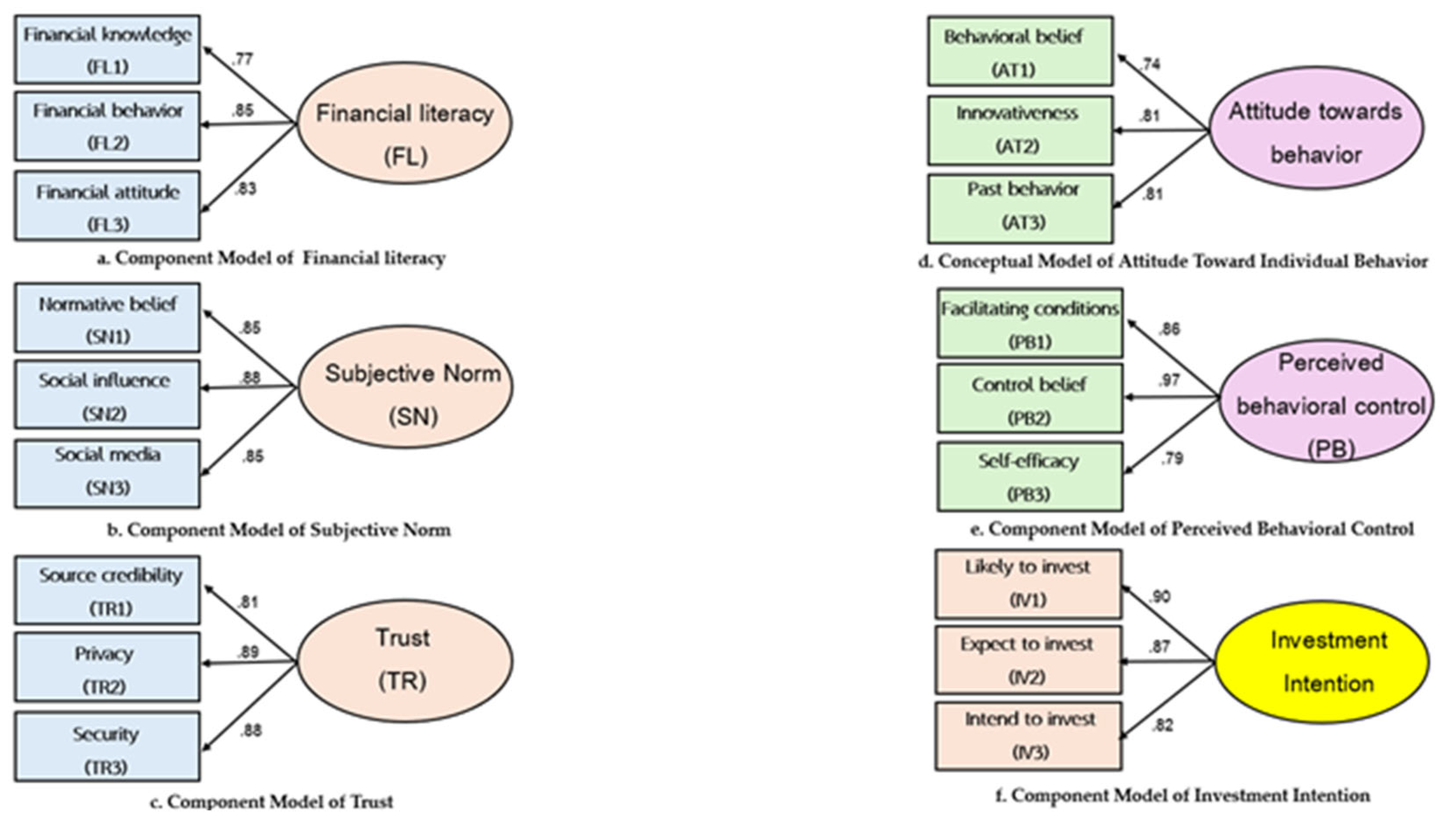

5.2. Confirmatory Factor Analysis

The Confirmatory Factor Analysis (CFA) results shown in Figure 2 were derived using the maximum likelihood estimation procedure to obtain standardized factor loadings (λ) linking the observed indicators to their corresponding latent constructs. The model fit indices, including the CFI and RMSEA, demonstrated that the specified measurement model exhibited a satisfactory correspondence with the empirical data.

The analysis demonstrated satisfactory reliability and validity, with Composite Reliability (CR) coefficients between 0.83 and 0.91 and Average Variance Extracted (AVE) values between 0.62 and 0.77, all above commonly accepted benchmarks. All factor loadings, reported in Table 1, were high (≥ 0.70) and exceeded the 0.50 threshold, providing strong evidence in support of the proposed measurement model and confirming the robustness of the latent constructs.

5.3. Correlations Among the Latent Variables in the Structural Equation Model

The correlations among the six latent variables in the structural equation model of factors influencing Thai investors’ intention to invest in financially innovative digital assets indicate that all 15 pairs of variables are positively related. The correlation coefficients range from 0.71 to 0.79 and are statistically significant at the 0.01 level, demonstrating that the constructs move in the same direction. Bartlett’s Test of Sphericity yielded a chi-square value of 8,688.495 with 153 degrees of freedom and a p-value of 0.000, which is statistically significant at the 0.01 level. Consistent with this result, the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy was 0.884, exceeding the threshold value of 0.50. These findings indicate that the correlation matrix of the observed variables is not an identity matrix and that the intercorrelations are sufficient to justify factor analysis for assessing construct validity or for estimating the structural equation model, as shown in Table 2.

5.4. Structural Model Fit and Hypothesis Testing

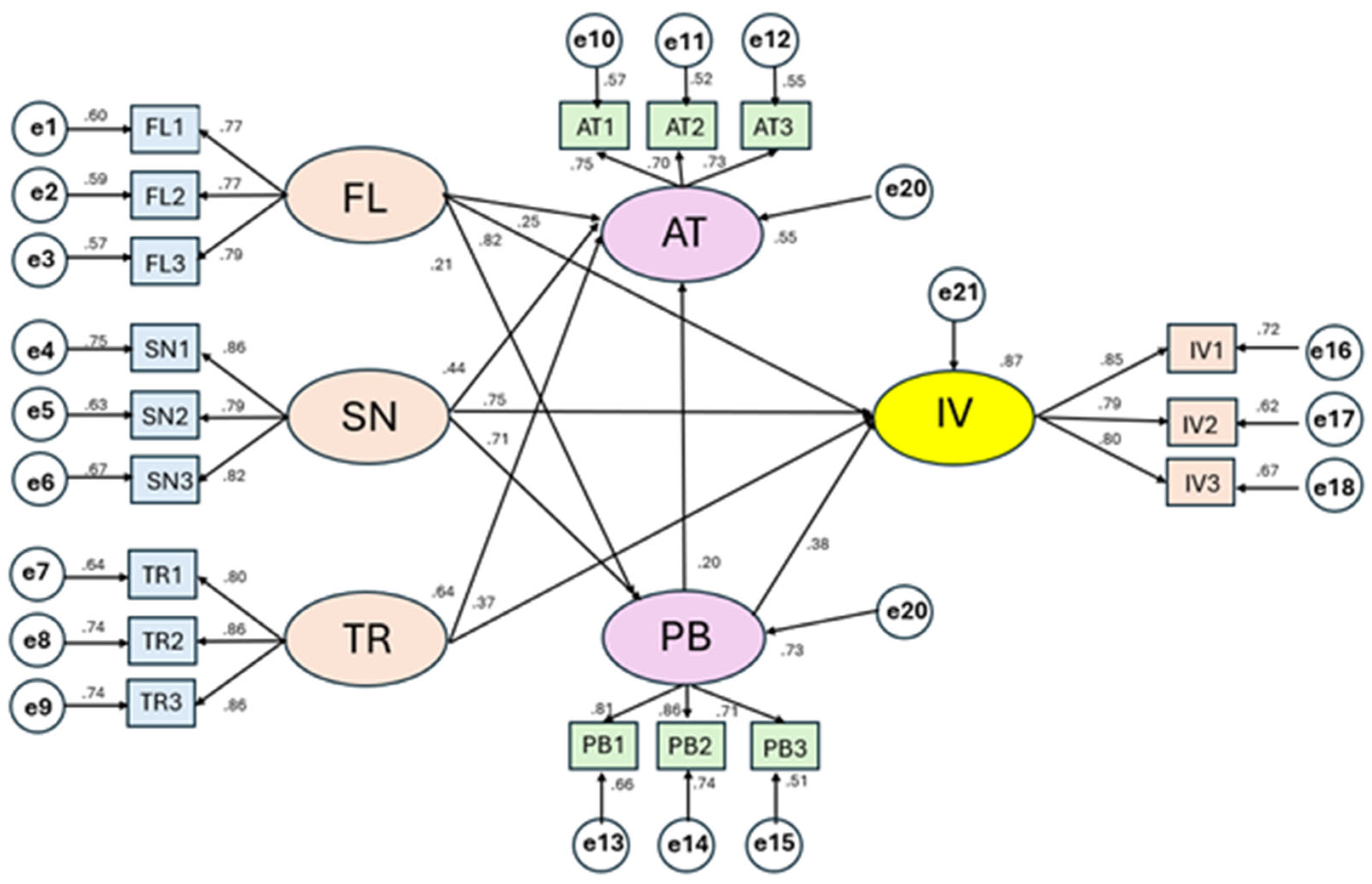

AMOS version 24 was employed for the analysis. In the final model, the validity of the structural equation model of factors influencing Thai investors’ intention to invest in financially innovative digital assets, as well as the effects among variables in the model, was evaluated using latent variable path analysis. Model fit was assessed using goodness-of-fit statistics in accordance with the criteria proposed by Wiratchai (1995) and Angsuchoti et al. (2011), namely: χ²/df < 2.00, RMSEA < 0.05, RMR < 0.05, GFI > 0.90, and AGFI > 0.90. All indices met these recommended thresholds, indicating a statistically significant and well-fitting mode

5.5. Path Coefficients and R2 Results

All exogenous variables in the model exert a positive influence on Thai investors’ intention to invest in financially innovative digital assets. Together, these variables explain 87% of the variance in investment intention (R² = 0.87). Considering the total effects on investment intention, financial literacy (FL) exhibits the largest overall impact, with a coefficient of 0.86, followed by subjective norms (SN) with a coefficient of 0.85. Trust shows a total effect of 0.46, attitude toward behavior has a total effect of 0.42, and perceived behavioral control has a total effect of 0.41. These results indicate that each causal variable is linked through a causal relationship to investment intention, with their total effects ordered from highest to lowest as financial literacy, subjective norms, trust, attitude toward behavior, and perceived behavioral control, as shown in Table 3.

All explanatory variables in the model exert significant positive effects on Thai investors’ intention to invest in financially innovative digital assets. Financial literacy (FL) has the strongest total effect (TE = 0.86), comprising a direct effect (DE) of 0.82 and an indirect effect (IE) of 0.04 (p < .01). Subjective norms (SN) are the second most in-fluential factor (TE = 0.85), with a DE of 0.75 and an IE of 0.10 (p < .01). Trust (TR) yields a TE of 0.46 (DE = 0.37; IE = 0.09; p < .01), attitude toward behavior (AT) shows a purely direct effect of 0.42 (TE = 0.42; p < .01), and perceived behavioral control (PB) has a TE of 0.41 (DE = 0.38; IE = 0.03; p < .01).

In addition, AT is positively influenced by FL (DE = 0.25; IE = 0.04; TE = 0.29) and by SN (DE = 0.44; IE = 0.14; TE = 0.58), and also receives significant direct effects from TR and PB (DE = 0.64 and 0.20, respectively; p < .01/.05). PB is directly affected by FL (DE = 0.21; IE = 0.08; TE = 0.29) and by SN (DE = 0.71; IE = 0.11; TE = 0.82; p < .01). Overall, the structural equation model indicates that FL is the most influential determinant of investment intention in financially innovative digital assets among Thai investors, followed in descending order by SN, TR, AT, and PB, as depicted in Figure 3

5.6. Hypothesis Testing Results

Based on the structural equation analysis of factors influencing Thai investors’ intention to invest in financially innovative digital assets, the researcher identified the levels of statistical significance associated with each variable in the conceptual framework. Accordingly, the results of the hypothesis testing are summarized in Table 4.

5.7. Interpretation and Theoretical Integration

The analytical results indicate that the Theory of Planned Behavior (TPB) constructs—subjective norms, attitude toward behavior, and perceived behavioral control—when integrated with financial literacy and trust, serve as key predictors of investment intention in innovative financial digital assets in Thailand. All proposed hypotheses are supported, and the findings reveal that financial literacy and subjective norms are the most influential variables in shaping Thai investors’ intentions. In line with Haq et al. (2021), investors tend to be risk-averse and loss-averse, actively seeking to reduce uncertainty in their investment decisions, while empirical evidence shows that investors do not always behave rationally, including in cryptocurrency markets (Ahmad and Wu, 2022). Within this context, Thai individual investors appear to seek confirmatory information and guidance from social media (for example, financial influencers on digital platforms) as well as from influential people in their immediate environment, such as friends and family, while also pursuing opportunities to enhance their financial literacy—particularly financial knowledge—before engaging in digital asset investment.

These results parallel those observed in Indonesia. Elisa Tjondro et al. (2023) identify salient factors influencing Indonesian cryptocurrency owners’ investment decisions and show that subjective norms play a critical role, with influential others often advising against investment when cryptocurrency prices decline sharply. Their findings contribute to dual-systems perspectives and social contagion theory, enriching empirical work on investment behavior, and align with Bonaparte’s (2022) argument that crypto owners tend to be relatively sophisticated investors with high levels of financial literacy. Related literature has also begun to examine the relationship between investor sentiment and cryptocurrency returns and volatility (Kyriazis et al., 2022), as well as herding behavior (Rubbaniy et al., 2022; Zhao et al., 2022) and bubble formation (Ghosh et al., 2022). Taken together, this body of work suggests that subjective norms can meaningfully shape trends in the digital asset investment market by influencing collective sentiment and herd-like responses among investors.

6. Discussion and Conclusions

6.1. Practical Implications and Recommendation

The findings of this research yield several important practical implications for key stakeholder groups in the digital asset ecosystem, particularly within the Thai context. The empirical evidence that financial literacy and subjective norms are the strongest determinants of investment intention indicates the need to move beyond purely structural regulation toward a more behaviorally informed policy approach. This includes designing and institutionalizing targeted investor education programs that systematically build financial knowledge, correct misconceptions about risk and return, and strengthen investors’ ability to independently evaluate digital asset products. In parallel, the documented role of trust implies that regulatory initiatives should emphasize transparency, clear disclosure standards, robust governance of digital asset service providers, and visible enforcement against misconduct, thereby reinforcing confidence in both market infrastructure and supervisory institutions. In this regard, regulatory practices such as monitoring investor forums to disseminate vetted insights and requiring real-time social sentiment indicators on trading platforms could help counter social influence risks while remaining consistent with Thailand’s collectivist decision-making patterns. The use of regulatory sandboxes for controlled experimentation with emerging digital asset products can further enhance perceived behavioral control among market participants.

For financial institutions and digital asset intermediaries, the results highlight the strategic importance of integrating investor-centered design principles into platform development and service delivery. Simplified interfaces, clear and unbiased educational content, and tools that help investors understand product risks, volatility, and fees can directly address the financial literacy and perceived behavioral control dimensions identified in the model. Platform-level innovations—such as nudge mechanisms that foreground expert analysis rather than purely trending signals, and gamified risk simulators that build user competency—can further support informed and sustainable participation. At the same time, the centrality of subjective norms and trust underscores the need for responsible use of social media and “finfluencer” channels: institutions should adopt transparent communication, avoid overly promotional narratives, and ensure that collaborations with influencers are compliant, clearly disclosed, and aligned with investor protection objectives. For individual investors, the proposed framework functions as a structured lens for self-assessment, encouraging reflection on whether their decisions are grounded in sufficient financial knowledge, an accurate understanding of risks, and well-founded trust in platforms and intermediaries, rather than being driven primarily by peer pressure or social media trends. Complementary mechanisms such as anonymous peer benchmarking of successful strategies and greater transparency regarding market volatility can help mitigate social influence biases while creating a constructive feedback loop between investor education and platform accountability. Taken together, these interventions provide a coherent, action-oriented roadmap for fostering a more stable, informed, and confident digital asset investment environment in Thailand, in which behavioral, psychological, and social factors are explicitly integrated into policy design, market practices, and personal financial decision-making.

6.2. Limitation and Future Research

This study is subject to several limitations that point to fruitful directions for future research. First, the proposed framework—integrating the core constructs of the Theory of Planned Behavior (TPB) with financial literacy and trust—was developed and tested solely within the Thai market. As a result, its generalizability to other emerging or developing economies remains uncertain, particularly in contexts with different regulatory regimes, cultural norms, and levels of digital asset adoption. Future studies should therefore extend this framework to other countries and conduct cross-market comparisons to assess whether the relative influence of financial literacy, subjective norms, trust, attitude, and perceived behavioral control is stable across different institutional and cultural environments.

Second, the present study relies on a single-method, single-period research design, which limits the ability to capture dynamic changes in investor behavior and market conditions. Subsequent research should employ longitudinal designs to observe how investment intentions in digital assets evolve over time, especially in response to regulatory changes, macroeconomic shocks, or major market events. Experimental or quasi-experimental approaches could also be used to test causal mechanisms more rigorously—for instance, by manipulating information quality, social influence cues, or trust signals and observing their impact on investment intention. Additionally, incorporating further variables such as risk tolerance, digital literacy, technology readiness, or perceived risk dimensions (e.g., performance, privacy, financial, psychological, and time risk) would allow for a more nuanced explanation of investor decision-making.

Third, from a theoretical standpoint, the study is anchored primarily in TPB, supplemented by financial literacy and trust, which, while robust, does not exhaust the range of potentially relevant behavioral and technological theories. Future research could enrich the analysis by drawing on alternative or complementary frameworks, such as the Value-based Adoption Model (VAM), Innovation Diffusion Theory, prospect theory, Expected Utility Theory, Information Cascade Theory, self-determination theory, the Technology Acceptance Model (TAM), Technology Readiness Index (TRI) and Technology Readiness Acceptance Model (TRAM), behavioral portfolio theory, goal-setting theory, the theory of reasoned action, or decomposed TPB variants that include more granular risk and trust constructs. Integrating these perspectives would deepen the theoretical foundation of digital asset research and help disentangle the complex interplay between intrinsic motivation, perceived value, social contagion, risk perception, and technology readiness in shaping investment intentions.

Author Contributions

Conceptualization, W.J., A.S. and S.V.; Methodology, A.S. and S.V.; Software, W.J. and K.P.; Validation, W.J. and A.S.; Formal analysis, W.J., A.S., S.V. and K.P.; Data curation, W.J. and A.S.; Writing—original draft, W.J., A.S., S.V. and K.P.; Writing—review & editing, W.J., A.S. and S.V. All authors have read and agreed to the published version of the manuscript.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available upon reasonable request from the corresponding author.

Acknowledgments

The authors would like to express their sincere gratitude to Collage of Innovation and Industrial Management, King Mongkut’s Institute of Technology Ladkrabang (KMITL) for providing the research facilities for this study.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Measurement Items

Table A1.

Measurement items of constructs.

| Constructs | Items | Statements | Source |

| Financial Skills | Financial Literacy | I have sufficient knowledge about digital asset investing. | Raut et al. (2021) Yoopetch and Chaithanapat (2021) Vijayalakshmi et al. (2022) Wang et al. (2022) Aliedan et al. (2023) |

| I can calculate returns from digital asset investments. | |||

| I understand the risks of digital asset investments. | |||

| Financial Behavior | I set clear financial goals for my investments. | ||

| I allocate funds to cover monthly expenses. | |||

| I regularly monitor my monthly spending. | |||

| Financial Attitudes | I find digital asset investing enjoyable. | ||

| I feel proud to invest in digital assets. | |||

| Digital asset investing keeps me up to date with technology. | |||

| Subjective Norm | Normative Beliefs | Important people expect me to invest in digital assets. | Raut et al. (2021) Yoopetch and Chaithanapat (2021) Schmidt et al. (2022) Widyastuti et al. (2022) Pilatin and Dilek (2023) |

| Expert recommendations influence my digital asset investment. | |||

| Well-known investors influence my decision to invest. | |||

| Social Influence | Investing in digital assets affects my personal image. | ||

| People I respect evaluate me based on digital asset investing. | |||

| People around me expect me to invest in digital assets. | |||

| Social Media | Social media influencers encourage me to invest in digital assets. | ||

| Social media news influences my investment decisions. | |||

| Investor networks provide useful digital asset information. | |||

| Trust Construct | Source Credibility | I trust digital assets as an investment. | Li and Wu (2016) Joo and Han (2021) Nadeem et al. (2021) Neupane et al. (2021) |

| Digital assets are reliable and stable investments. | |||

| Digital asset investments are technologically secure. | |||

| Privacy | Investor personal data is well protected. | ||

| Privacy systems effectively prevent data breaches. | |||

| Investment platforms provide sufficient privacy protection. | |||

| Security | Investor information is strongly protected. | ||

| Digital assets prevent loss of data or assets. | |||

| Digital assets are difficult to hack or steal. | |||

| Attitude Toward Individual Behavior | Behavioral Beliefs | Digital assets are a good investment alternative. | Boonroungrut and Huang (2021) Raut et al. (2021) Schmidt et al. (2022) Ma and Niro (2023) |

| Digital asset investing is easy to learn. | |||

| Digital assets help achieve my financial goals. | |||

| Innovative Capability | I am confident to start investing in digital assets. | ||

| I can understand how digital asset investing works. | |||

| I am willing to use new investment technologies. | |||

| Past Behavior | My past investment experience affects my intention to invest. | ||

| Experience in various assets influences my digital asset investment. | |||

| My past investment frequency affects future digital asset investing. | |||

| Perceived Behavioral Control | Facilitating Conditions | Digital asset systems provide sufficient facilitating conditions. | Hong (2018) Handoko et al. (2020) Neupane et al. (2021) Widyasari and Aruan (2022) Gumasing and Niro (2023) |

| Digital asset systems offer support comparable to other investments. | |||

| Support is available for digital asset investment issues. | |||

| Control Beliefs | I can manage my finances when investing in digital assets. | ||

| I can manage my investments effectively in digital assets. | |||

| I can control my financial decisions in digital asset investing. | |||

| Perceived Self-Efficacy | I am confident in my ability to invest in digital assets. | ||

| I can handle unexpected situations in digital asset investing. | |||

| Digital asset investing helps achieve my financial goals. | |||

| Investment Intention | Likelihood of Invest | I have a positive view of digital asset in | Raut et al. (2021) Yoopetch and Chaithanapat (2021) Widyasari and Aruan (2022) Widyastuti et al. (2022) Pilatin and Dilek (2024) |

| I am likely to invest in digital assets in the future. | |||

| I plan to invest in digital assets in the near future. | |||

| Expected Investment | If an opportunity arises, I will invest in digital assets. | ||

| I expect to invest in digital assets soon. | |||

| I believe I will invest in digital assets in the future. | |||

| Intention to Invest | I intend to invest in digital assets. | ||

| I have prepared myself to invest in digital assets. | |||

| I am willing to invest in digital assets without hesitation. |

Appendix B

Table B1.

Demographic data.

| Demographic profiles | Amount | Percent |

| Gender | ||

| Male | 149 | 41.40 |

| Female | 211 | 58.60 |

| Age | ||

| 30 years old and below | 150 | 41.70 |

| 31-40 years old | 182 | 50.60 |

| 41-50 years old | 28 | 7.80 |

| Education level | ||

| Bachelor degree | 198 | 55.00 |

| Master degree | 155 | 43.10 |

| Dotoral degree | 7 | 1.90 |

| Marital status | ||

| Single | 260 | 72.20 |

| Married | 100 | 27.80 |

| Employment | ||

| Full time employees | 246 | 68.30 |

| Self-employed | 100 | 27.80 |

| Freelancer | 14 | 3.90 |

| Income level | ||

| 30,000 Thai Baht and below | 1 | 0.30 |

| 30,001-50,000 Thai Baht | 104 | 28.90 |

| 50,001-70,000 Thai Baht | 58 | 16.10 |

| 70,001-90,000 Thai Baht | 45 | 12.50 |

| 90,0001-110,000 Thai Baht | 72 | 20.00 |

| 110,001 Thai Baht and above | 80 | 22.20 |

Table B2.

Investment related.

| Investment related | Amount | Percent |

| Type of assets you have investment experience | ||

| Stocks | 329 | 32.07 |

| Government bonds | 157 | 15.30 |

| Real estate | 180 | 17.54 |

| Mutual funds | 360 | 35.09 |

| Investment experience | ||

| 1-3 years | 113 | 31.40 |

| 3-5 years | 47 | 13.10 |

| 5-10 years | 123 | 34.20 |

| More than 10 years | 77 | 21.30 |

| Investment frequency | ||

| Invest regularly (every month) | 134 | 37.20 |

| Invest occasionally (2–3 times per year) | 160 | 44.40 |

| Invest very rarely (once in a long while) | 66 | 18.30 |

| Current financial situation | ||

| Financially stable with well-managed finances | 123 | 34.20 |

| Financially stable but without good financial management | 85 | 23.60 |

| Financially unstable | 152 | 42.20 |

| Main investment objectives (you may select more than one) | ||

| To generate additional income | 360 | 24.16 |

| For long-term savings | 205 | 13.76 |

| For retirement preparation | 205 | 13.76 |

| To increase the value of assets | 360 | 24.16 |

| To seek opportunities from investing in new asset classes | 360 | 24.16 |

| Sources of financial and investment information | ||

| Financial/investment news websites | 64 | 6.04 |

| Social media (e.g., Facebook, Twitter, YouTube) | 360 | 33.96 |

| Specialized websites or applications (e.g., CoinMarketCap, TradingView | 172 | 16.23 |

| Online investment groups or forums (e.g., Pantip, Telegram, Line) | 41 | 3.87 |

| Financial newspapers or journals | 8 | 0.76 |

| Financial advisors or experts | 55 | 5.18 |

| Friends, family, or close acquaintances | 360 | 33.96 |

| Risk tolerance for investing in digital assets | ||

| Very high risk tolerance (expecting high returns) | 164 | 45.56 |

| Moderate risk tolerance (expecting good returns) | 170 | 47.22 |

| Low risk tolerance (prioritizing capital safety) | 21 | 5.83 |

| Do not accept risk in digital asset investment | 5 | 1.39 |

| Key factors influencing your decision to invest in digital assets | ||

| Short-term profit opportunities | 331 | 18.89 |

| Future growth potential of the asset | 359 | 20.49 |

| Recommendations from experts or professionals | 201 | 11.47 |

| Information from media and news | 201 | 11.47 |

| Support from friends or family | 330 | 18.84 |

| Use cases or underlying technology of digital assets | 330 | 18.84 |

References

- Abideen, Z. U.; Ahmed, Z.; Qiu, H.; Zhao, Y. Do behavioral biases affect investors’ investment decision making? Evidence from the Pakistani equity market. Risks 2023, 11, 109. [Google Scholar] [CrossRef]

- Adam, A. A.; Shauki, E. R. Socially responsible investment in Malaysia: Behavioral framework in evaluating investors’ decision making process. Journal of Cleaner Production 2014, 80, 224–240. [Google Scholar] [CrossRef]

- Adil, M.; Singh, Y.; Subhan, M.; Al-Faryan, M. A. S.; Ansari, M. S. Do trust in financial institution and financial literacy enhances intention to participate in stock market among Indian investors during COVID-19 pandemic? Cogent Economics & Finance 11(1) 2023, Article 2169998. [Google Scholar] [CrossRef]

- Ahmad, M.; Shah, S. Z. A. Overconfidence heuristic-driven bias in investment decision-making and performance: Mediating effects of risk perception and moderating effects of financial literacy. Journal of Economic and Administrative Sciences 38(1) 2022, 60–90. [Google Scholar] [CrossRef]

- Ajzen, I. From intentions to actions: A theory of planned behaviour. In Action control: From cognition to behavior; Kuhl, J., Beckmann, J., Eds.; Springer, 1985; pp. 11–39. [Google Scholar] [CrossRef]

- Ajzen, I. Attitudes, personality, and behavior; Dorsey Press, 1988. [Google Scholar]

- Ajzen, I. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50(2) 1991, 179–211. [Google Scholar] [CrossRef]

- Ajzen, I. Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior. Journal of Applied Social Psychology 32(4) 2002, 665–683. [Google Scholar] [CrossRef]

- Ajzen, I.; Driver, B. L. Application of the theory of planned behavior to leisure choice. Journal of Leisure Research 24(3) 1992, 207–224. [Google Scholar] [CrossRef]

- Akhtar, F.; Das, N. Impact of financial literacy on investment intentions: Evidence from India. International Journal of Economic Perspectives 2017, 11(1), 429–436. [Google Scholar]

- Akhtar, F.; Das, N. Predictors of investment intention in Indian stock markets: Extending the theory of planned behaviour. International Journal of Bank Marketing 2019, 37(1), 97–119. [Google Scholar] [CrossRef]

- Aldean, M. M.; Alyahya, M. A.; Elshaer, I. A.; Sobaih, A. E. E. Who is going green? Determinants of green investment intention in the Saudi food industry. Agriculture 2023, 13(5), 1047. [Google Scholar] [CrossRef]

- Alexander, C.; Cumming, D. Corruption and fraud in financial markets: Malpractice, misconduct and manipulation.; John Wiley & Sons, 2020. [Google Scholar]

- Aliedan, M. M.; Alyahya, M. A.; Elshaer, I. A.; Sobaih, A. E. E. Who is going green? Determinants of green investment intention in the Saudi food industry. Agriculture 13(5) 2023, 1047. [Google Scholar] [CrossRef]

- Almaqtari, F. A.; Yahya, A. T.; Al-Maskari, N.; Farhan, N. H. S.; Al-Aamri, A.-M. Y. Y. Assessing the integrated role of IT governance, fintech, and blockchain in enhancing sustainability performance and mitigating organizational risk. Risks 2025, 13(6), 105. [Google Scholar] [CrossRef]

- Ammo us, S. Blockchain technology: What is it good for? SSRN Electronic Journal 2016. [Google Scholar] [CrossRef]

- Amro, A. M.; Ariffin, A. M.; Norsiah, A. H. The relationship between perceived security, perceived privacy and social commerce intention among university students in Saudi Arabia. International Journal of Advanced Research in Science, Engineering and Technology 2018, 5(9), 6707–6718. [Google Scholar]

- Armitage, C. J.; Conner, M. Efficacy of the theory of planned behaviour: A meta-analytic review. British Journal of Social Psychology 40(4) 2001, 471–499. [Google Scholar] [CrossRef] [PubMed]

- Awn, A. M.; Azam, S. M. F. Libyan investors’ intention to invest in Islamic Sukuk: Theory of planned behaviour approach. European Journal of Economic and Financial Research 2020, 4(1), 77–92. [Google Scholar] [CrossRef]

- Banna, H.; Mia, M. A.; Nourani, M.; Yarovaya, L. Fintech-based financial inclusion and risk-taking of microfinance institutions (MFIs): Evidence from Sub-Saharan Africa. Finance Research Letters 45 2021, 102149. [Google Scholar] [CrossRef]

- Bank of England. Innovation in digital assets in the financial system and the Bank – Speech by Sasha Mills . October 2024. Available online: https://www.bankofengland.co.uk/speech/2024/october/sasha-mills-keynote-speech-at-the-digital-assets-week.

- Bank of Thailand. Thailand’s financial literacy survey . 2020. Available online: https://www.bot.or.th/th/research-and-publications/fl-survey-report.html.

- Bawalle, A. A.; Khan, M. S. R.; Kadoya, Y. Overconfidence, financial literacy, and panic selling: Evidence from Japan. PLOS ONE 20(1) 2025, e0315622. [Google Scholar] [CrossRef]

- Bland, E.; Changchit, C.; Cutshall, R.; Pham, L. Behavioral and psychological determinants of cryptocurrency investment: Expanding UTAUT with perceived enjoyment and risk factors. Journal of Risk and Financial Management 2024, 17(10), 447. [Google Scholar] [CrossRef]

- Blockchain Association of Indonesia. Indonesia crypto outlook report 2021 . 2022. Available online: https://asosiasiblockchain.co.id.

- Błach, J. Financial innovations and their role in the modern financial system. Financial Internet Quarterly 2011, 7(3), 13–26. [Google Scholar]

- Bongomin, G. O. C.; Ntayi, J. M. Mobile money adoption and usage and financial inclusion: Mediating effect of digital consumer protection. Digital Policy, Regulation and Governance 2020, 22(3), 157–176. [Google Scholar] [CrossRef]

- Boonroungrut, C.; Huang, F. Reforming theory of planned behavior to measure money management intention: A validation study among student debtors. RAUSP Management Journal 2021, 56(1), 24–37. [Google Scholar] [CrossRef]

- Bottazzi, L.; Da Rin, M.; Hellmann, T. The importance of trust for investment: Evidence from venture capital. Review of Financial Studies 2016, 29(9), 2283–2318. [Google Scholar] [CrossRef]

- Brière, M.; Oosterlinck, K.; Szafarz, A. Virtual currency, tangible return: Portfolio diversification with Bitcoin. Journal of Asset Management 16 2015, 365–373. [Google Scholar] [CrossRef]

- Campbell, J. Y.; Jackson, H. E.; Madrian, B. C.; Tufano, P. Consumer financial protection. Journal of Economic Perspectives 2011, 25(1), 91–114. [Google Scholar] [CrossRef]

- Catalini, C.; Gans, J. S. NBER Working Paper No. 24418; Initial coin offerings and the value of crypto tokens. National Bureau of Economic Research, 2018. [CrossRef]

- Cole, S.; Sampson, T.; Zia, B. Prices or knowledge? What drives demand for financial services in emerging markets? Journal of Finance 2012, 67(6), 1933–1967. [Google Scholar] [CrossRef]

- Colby, C. L.; Parasuraman, A. Techno-ready marketing: How and why customers adopt technology; Simon & Schuster, 2001. [Google Scholar]

- Cronbach, L. J. Coefficient alpha and the internal structure of tests. Psychometrika 16(3) 1951, 297–334. [Google Scholar] [CrossRef]

- Dash, G.; Kiefer, K.; Paul, J. Marketing-to-millennials: Marketing 4.0, customer satisfaction and purchase intention. Journal of Business Research 122 2021, 608–620. [Google Scholar] [CrossRef]

- Di Pierro, M. What is the blockchain? Computing in Science & Engineering 2017, 19(5), 92–95. [Google Scholar] [CrossRef]

- Dwivedi, Y. K.; Rana, N. P.; Jeyaraj, A.; Clement, M.; Williams, M. D. Re-examining the Unified Theory of Acceptance and Use of Technology (UTAUT): Towards a revised theoretical model. Information Systems Frontiers 21(3) 2017, 719–734. [Google Scholar] [CrossRef]

- Eagly, A. H.; Chaiken, S. The psychology of attitude; Harcourt Brace Jovanovich, 1993. [Google Scholar]

- Ejigu, S. N.; Filatie, Y. S. Determinants of investment intention in micro and small enterprises among business college students in East Gojjam Zone. Research Journal of Finance and Accounting 2020, 11(3), 24–36. [Google Scholar]

- Fisch, C. Initial coin offerings (ICOs) to finance new ventures: An exploratory study. Journal of Business Venturing 2019, 34(1), 1–22. [Google Scholar] [CrossRef]

- Fortune Business Insights. Digital asset management (DAM) market size, share & industry analysisand regional forecast, 2024–2032 . 2024. Available online: https://www.fortunebusinessinsights.com/digital-asset-management-dam-market-104914.

- Garg, N.; Singh, S. Financial literacy among youth. International Journal of Social Economics 2018, 45(1), 173–186. [Google Scholar] [CrossRef]

- Gomaa, A.; Li, Y. An entrepreneurial definition of the blockchain technology and a stacked layer model of the ICO marketplace using the text mining approach. Journal of Risk and Financial Management 2022, 15(12), 557. [Google Scholar] [CrossRef]

- Guiso, L.; Sapienza, P.; Zingales, L. Cultural biases in economic exchange? The Quarterly Journal of Economics 2009, 124(3), 1095–1131. [Google Scholar] [CrossRef]

- Gumasing, M. J. J.; Niro, R. H. A. Antecedents of real estate investment intention among Filipino millennials and Gen Z: An extended theory of planned behavior. Sustainability 2023, 15(18), 13714. [Google Scholar] [CrossRef]

- Hair, J. F.; Black, W. C.; Babin, B. J.; Anderson, R. E. Multivariate data analysis: A global perspective; Pearson, 2010. [Google Scholar]

- Halaburda, H. Blockchain revolution without the blockchain? Communications of the ACM 2018, 61(7), 27–29. [Google Scholar] [CrossRef]

- Handoko, L.; Sihombing, S. O.; Saputra, T. F. The effect of electronic word of mouth on purchase intention towards healthy dessert. In Proceedings of the 4th International Conference on Time Series and Forecasting (ICITSF 2019); SciTePress, 2019; pp. 297–303. [Google Scholar] [CrossRef]

- Hapsari, S. A. The theory of planned behavior and financial literacy to analyze intention in mutual fund product investment. In Proceedings of the 5th Global Conference on Business, Management and Entrepreneurship (GCBME 2020); Atlantis Press, 2021; pp. 136–141. [Google Scholar] [CrossRef]

- Herawati, N.; Dewi, R. K. The influence of financial literacy, financial behavior, and income on investment decisions. Jurnal Manajemen dan Bisnis Indonesia 2019, 5(1), 48–56. [Google Scholar]

- Hong, I. B. Social and personal dimensions as predictors of sustainable intention to use Facebook in Korea: An empirical analysis. Sustainability 10(8) 2018, 2856. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 11(3) 2019, 340. [Google Scholar] [CrossRef]

- Javaid, M.; Haleem, A.; Singh, R. P.; Suman, R.; Khan, S. A review of blockchain technology applications for financial services. BenchCouncil Transactions on Benchmarks, Standards and Evaluations 2022, 2(3), 100073. [Google Scholar] [CrossRef]

- Joo, J.; Han, Y. An evidence of distributed trust in blockchain-based sustainable food supply chain. Sustainability 13(19) 2021, 10980. [Google Scholar] [CrossRef]

- Kasikorn Research Center. Draft Financial Business Hub Act – A milestone for elevating Thailand to the global stage (Current Issue No. 3559) . 2025. Available online: https://www.kasikornresearch.com/en/analysis/k-econ/economy/Pages/FinancialHub-CIS3559-KR-13-02-24.aspx.

- Kashyap, A. K.; Tripathi, K.; Rathore, P. S. Integrating cryptocurrencies to legal and financial framework of India. Journal of Global Policy and Governance 2021, 10(1), 121–137. [Google Scholar]

- Keneley, M. J. The shifting corporate culture in the financial services industry: Explaining the emergence of the “culture of greed” in an Australian financial services company. Business History 2020, 65(4), 583–605. [Google Scholar] [CrossRef]

- Khan, M. S.; Sari, D. P.; Dewi, N. P. R. The role of risk tolerance, financial literacy, and subjective norms in driving students toward stock investing. Asian Journal of Economics, Business and Accounting 2022, 22(3), 1–15. [Google Scholar]

- Khaw, K. W.; Alnoor, A.; AL-Abrrow, H.; Tiberius, V.; Ganesan, Y.; Atshan, N. A. Reactions towards organizational change: A systematic literature review. Current Psychology 2023, 42(22), 19137–19160. [Google Scholar] [CrossRef]

- Kilani, A. A.-H. Z.; Kakeesh, D.; Al-Weshah, G. A.; Al-Debei, M. M. Consumer post-adoption of e-wallet: An extended UTAUT2 perspective with trust. Journal of Open Innovation: Technology, Market, and Complexity 2023, 9(3), Article 100113. [Google Scholar] [CrossRef]

- Kryiazis, N.; Papadamou, S.; Tzeremes, P.; Corbet, S. Can cryptocurrencies provide a viable hedging mechanism for benchmark index investors? Research in International Business and Finance 2023, 64, Article 101832. [Google Scholar] [CrossRef]

- Kumari, J. S.; Senani, K. G. P.; Ajward, R. Predicting investors’ intention to invest in the stock market during COVID-19: Can we use an extended theory of planned behavior? Journal of Asia Business Studies 2022, 17(4), 681–700. [Google Scholar] [CrossRef]

- Lal, S.; Bawalle, A. A.; Khan, M. S. R.; Kadoya, Y. What determines digital financial literacy? Evidence from a large-scale investor study in Japan. Risks 13(8) 2025, 149. [Google Scholar] [CrossRef]

- Li, J.; Zheng, H.; Kang, M.; Wang, T.; Chen, S. Understanding investment intention towards P2P lending: An empirical study. In Proceedings of the Pacific Asia Conference on Information Systems (PACIS 2016) (Paper 86), 2016, June; AIS eLibrary. [Google Scholar]

- Liang, C.-C. Subjective norms and customer adoption of mobile banking. In Proceedings of the 49th Hawaii International Conference on System Sciences (HICSS), 2016; IEEE; pp. 1576–1585. [Google Scholar] [CrossRef]

- Lim, F.-W.; Fakhrorazi, A. The role of personal innovativeness and facilitating conditions in shaping the attitudes of mobile internet banking (MIB) adoption among Generation Y in Malaysia. Preprints 2020, Article 2020030407. [Google Scholar] [CrossRef]

- Lu, B.; Wang, Z. What makes consumers trust and adopt fintech? An empirical investigation in China. Electronic Commerce Research 2022, 22(3), 755–784. [Google Scholar] [CrossRef]

- Lu, Z. Z.; Seow, C. K.; Chan, R. C. B.; Cai, Y.; Cao, Q. Automated Bitcoin trading dApp using price prediction from a deep learning model. Applied Sciences 2024, 14(11), 4421. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O. S. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 2014, 52(1), 5–44. [Google Scholar] [CrossRef] [PubMed]

- Manaa, M.; Chimienti, M. T.; Adachi, M.; Athanassiou, P.; Balteanu, I.; Calza, A.; Devaney, C.; Fernandez, E. D.; Eser, F.; Ganoulis, I.; et al. Crypto-assets: Implications for financial stability, monetary policy, and payments and market infrastructures; (Occasional Paper Series No. 223); European Central Bank, 2019. [Google Scholar]

- Maziriri, E. T.; Mapuranga, M.; Madinga, N. W. Navigating selected perceived risk elements on investor trust and intention to invest in online trading platforms. Journal of Economic and Financial Sciences 2019, 12(1), Article a435. [Google Scholar] [CrossRef]

- Meng, B.; Choi, K. An investigation on customer revisit intention to theme restaurants: The role of servicescape and authentic perception. International Journal of Contemporary Hospitality Management 2018, 30(3), 1646–1662. [Google Scholar] [CrossRef]

- Misra, S.; Singh, S.; Kaur, I. Social influence and subjective norms in technology adoption: A meta-analysis. International Journal of Information Management 2021, 57, 102282. [Google Scholar] [CrossRef]

- Morgan, P. J.; Trinh, L. Q. Determinants and impacts of financial literacy in Cambodia and Viet Nam; (ADBI Working Paper No. 754); Asian Development Bank Institute, 2017. [Google Scholar]

- Nadeem, M. A.; Liu, Z.; Hayat, M. A.; Younis, A.; Xu, Y. The adoption of cryptocurrency in Pakistan: An extended theory of planned behavior. Frontiers in Psychology 12 2021, 744432. [Google Scholar] [CrossRef]

- Nadeem, M. A.; Liu, Z.; Pitafi, A. H.; Younis, A.; Xu, Y.; Jebran, K. Investigating the adoption factors of cryptocurrencies—A case of Bitcoin: Empirical evidence from China. SAGE Open 2021, 11(2), 1–15. [Google Scholar] [CrossRef]

- Neupane, C.; Wibowo, S.; Grandhi, S.; Deng, H. A trust-based model for the adoption of smart city technologies in Australia. Sustainability 2021, 13(16), 9316. [Google Scholar] [CrossRef]

- Nugraha, B. A.; Rahadi, R. A. Analysis of young generations toward stock investment intention. Journal of Accounting and Investment 2021, 22(1), 80–97. [Google Scholar] [CrossRef]

- OECD. OECD/INFE international survey of adult financial literacy competencies; Organisation for Economic Co-operation and Development, 2016. [Google Scholar]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Palanisamy, M.; Paul Vincent, M. T.; Hossain, M. B. Financial literacy and behavioral intention to use central banks’ digital currency: Moderating role of trust. Journal of Risk and Financial Management 2025, 18(3), 165. [Google Scholar] [CrossRef]

- Pilatin, A.; Dilek, Ö. Investor intention, investor behavior and crypto assets in the framework of decomposed theory of planned behavior. In Current Psychology; Advance online publication; 2023. [Google Scholar] [CrossRef]

- Pop, R.; Săplăcan, Z.; Alt, M. A.; Dabija, D. C. Influence of social media on consumer behavior: The case of sustainable purchasing. Frontiers in Psychology 2020, 11, 02181. [Google Scholar] [CrossRef]

- Potrich, A. C. G.; Vieira, K. M.; Mendes-Da-Silva, W. Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças 2020, 31(82), 216–232. [Google Scholar] [CrossRef]

- Rahadjeng, E. R.; Fiandari, Y. R. The effect of attitude, subjective norms and control of behavior towards intention in share investment. Manajemen Bisnis 2020, 10(2), 17–26. [Google Scholar] [CrossRef]

- Raut, R. K. Past behaviour, financial literacy and investment decision-making process of individual investors. International Journal of Emerging Markets 2020, 15(6), 1243–1263. [Google Scholar] [CrossRef]

- Raut, R. K.; Kumar, R.; Das, N. Individual investors’ intention towards SRI in India: An implementation of the theory of reasoned action. Social Responsibility Journal 2021, 17(7), 877–896. [Google Scholar] [CrossRef]

- Ryu, Y.; Kim, S.; Kim, S. Does trust matter? Analyzing the impact of trust on the perceived risk and acceptance of nuclear power energy. Sustainability 2018, 10(3), 758. [Google Scholar] [CrossRef]

- Sebayang, T. E.; Hakim, D. B.; Bakhtiar, T.; Indrawan, D. The investigation of preference attributes of Indonesian mobile banking users to develop a strategy for mobile banking adoption. Journal of Risk and Financial Management 2024, 17(3), Article 109. [Google Scholar] [CrossRef]

- Securities and Exchange Commission. Digital asset investment . n.d. Available online: https://www.sec.or.th/TH/Documents/DigitalAsset/DigitalAssetInvestment-Guide.pdf.

- Securities and Exchange Commission. Digital asset trading statistics . 2022. Available online: https://www.sec.or.th.

- Securities and Exchange Commission. Mutual fund investment . 31 July 2024. Available online: https://www.sec.or.th/TH/Template3/Articles/2567/310767.pdf.

- Securities and Exchange Commission. Digital asset classification and regulatory framework . 2025. Available online: https://www.sec.or.th.

- Shahzad, S. J. H.; Bouri, E.; Roubaud, D.; Kristoufek, L. Safe haven, hedge and diversification for G7 stock markets: Gold versus Bitcoin. Economic Modelling 87 2020, 212–224. [Google Scholar] [CrossRef]

- Sharahiley, S. M. Examining entrepreneurial intention of the Saudi Arabia’s university students: Analyzing alternative integrated research model of TPB and EEM. Global Journal of Flexible Systems Management 2020, 21(1), 67–84. [Google Scholar] [CrossRef]

- Sharma, A.; Hewege, C.; Perera, C. Enhancing consumer empowerment: Insights into the role of rationality when making financial investment decisions. Journal of Risk and Financial Management 2025, 18(2), 106. [Google Scholar] [CrossRef]

- Shaw, D.; Shiu, E. The contribution of ethical obligation and self-identity to the theory of planned behaviour: An exploration of ethical consumers—A reflective comment. Social Business 2013, 3(1), 47–65. [Google Scholar] [CrossRef]