Submitted:

02 February 2026

Posted:

03 February 2026

You are already at the latest version

Abstract

Water-related resources are increasingly critical to corporate sustainability, yet many businesses struggle to account for their marine impacts effectively. Blue accounting has emerged as a tool to improve corporate transparency and responsible water stewardship, especially concerning marine ecosystems. This study conducts a scoping review to identify factors influencing corporations' adoption of blue accounting disclosures. Following Arksey and O’Malley’s framework, 109 studies were initially screened, with 18 peer-reviewed articles selected for final analysis. Results reveal that stakeholder pressure, climate action, competitive positioning, and alignment with sustainability goals, especially SDG 14, are key enablers of adoption. However, major barriers include the lack of a standardised reporting framework, limited regulatory mandates, and institutional and technical capacity constraints. The review highlights the strategic use of blue accounting as a signalling mechanism, while also cautioning against superficial “blue-washing.” It concludes that targeted policy interventions, capacity building, and globally harmonised standards are essential for improving disclosure quality and corporate accountability in marine sustainability. This review contributes to the literature by mapping current evidence, identifying adoption drivers and barriers, and proposing directions for empirical research and policy development.

Keywords:

blue accounting

; marine accounting

; ocean accounting

; corporate disclosure

; marine sustainability

; SDG 14

; sustainability reporting

; environmental governance

1. Introduction

The sustainable management of marine ecosystems is gaining critical attention in both policy and business domains, driven by increasing environmental pressures on oceans, which cover approximately 72% of the Earth’s surface (Rahmayanti & Sari, 2023; Struwig et al., 2024). Oceans support essential ecological and economic functions, yet they are threatened by over-exploitation, pollution, and habitat degradation, exacerbated by climate change and insufficient governance (Herbert-Read et al., 2022; Landrigan et al., 2020; Stafford et al., 2022). As the ocean economy expands, so does the need for robust accounting mechanisms that reflect environmental impacts and guide sustainable practices (Abreu et al., 2019; Kirkman et al., 2021).

In response, blue accounting has emerged as a promising but underdeveloped framework for integrating marine sustainability into organisational decision-making. It seeks to provide organisations and stakeholders with meaningful data on their marine-related activities, enabling them to evaluate opportunities, risks, and sustainability impacts (Abreu et al., 2019). A key component is blue accounting disclosures, which refer to systematic reporting of an organisation’s impact and actions in relation to marine and coastal ecosystems (Rahmayanti & Sari, 2023). Despite parallel advances in sustainability reporting, such as Environmental, Social, and Governance (ESG) frameworks and Integrated Reporting (IR), blue accounting remains underexplored (de Villiers et al., 2020; Syah et al., 2020). By contrast, green accounting has garnered considerable academic and policy interest since the 1970s (Pattinaja et al., 2023; Syah et al., 2020). One key limitation hindering the uptake of blue accounting is the lack of a standardised, globally recognised reporting framework, which makes it difficult for investors, regulators, and other stakeholders to assess performance consistently (Winarsih et al., 2020).

Traditional financial accounting continues to dominate corporate reporting but fails to capture the social and ecological impacts of resource extraction, especially in marine contexts (Agyemang et al., 2021; Khan et al., 2020). This underlines the urgent need to incorporate natural capital accounting approaches that consider the value, degradation, and use of marine assets (Perkiss et al., 2022; Udo, 2019). Moreover, international frameworks such as the United Nations' Sustainable Development Goals (SDGs), specifically SDG 14: Life Below Water, have reinforced the importance of integrating ocean sustainability into business practices (Lubchenco & Haugan, 2023; Souza-Piao et al., 2022).

However, blue accounting has yet to gain traction in mainstream environmental accounting scholarship, with limited empirical studies and geographic representation, particularly from Africa (Failler et al., 2023; Perkiss et al., 2022). While global dialogues like Ocean 2030 and the UN Law of the Sea emphasise the need for ocean stewardship, many businesses remain disengaged from marine reporting efforts (Castro-Cadenas et al., 2022; Failler & Seisay, 2021).

This study addresses this gap by conducting a scoping review of the literature on factors influencing corporate adoption of blue accounting disclosures. It offers four key contributions: (1) mapping the theoretical and empirical development of blue accounting; (2) identifying drivers and barriers to adoption; (3) providing insights for marine-sensitive industries; and (4) proposing policy and practice recommendations to align corporate practices with SDG 14. Ultimately, the study aims to support the institutionalisation of blue accounting as a credible mechanism for improving ocean governance and marine sustainability reporting.

2. Materials and Methods

This scoping review is grounded using principles that are designed not to test hypotheses but rather to map the breadth and depth of existing literature and identify research gaps (Arksey & O'malley, 2005). In doing so, it applies established theoretical lenses not only to interpret the literature but also to guide the categorisation of variables and the identification of drivers and barriers to the adoption of blue accounting by marine-sensitive companies.

Stakeholder theory explains how corporations respond to external pressures from investors, regulators, civil society, and the public (Freeman, 2010). Studies reviewed emphasised stakeholder pressure as a primary driver of blue accounting adoption (Abreu et al., 2019; Rahmayanti & Sari, 2023). This theory informed the coding of factors related to stakeholder influence and accountability mechanisms during data extraction.

Legitimacy theory emphasises the importance of organisations demonstrating alignment with societal norms to maintain social licence (Hora & Subramanian, 2019; Manes-Rossi et al., 2018). Disclosure practices, especially in the absence of regulation, are often used to signal legitimacy (Elshabasy, 2018; Gallardo-Vazquez et al., 2019). In this review, legitimacy theory guided the analysis of voluntary disclosure practices, particularly in contexts where regulatory enforcement is weak or fragmented.

Signalling Theory addresses the ways organisations use disclosures to communicate quality, commitment, and leadership in sustainability to reduce information asymmetry (Benjamin et al., 2023; Yasar et al., 2020). Consequently, organisations that demonstrate better sustainability performance tend to offer more comprehensive disclosures regarding their sustainability efforts than those that are less successful in this area (Benjamin et al., 2023; Datt et al., 2019). Accordingly, signalling theory shaped the classification of disclosure quality variables, distinguishing between those that served as credible signals of performance and those that were symbolic gestures.

Together, these theories were not treated in isolation but integrated into the analytical framework. They collectively informed the conceptual model, which categorises factors influencing blue accounting as either drivers (e.g., stakeholder influence, regulatory frameworks, and sustainability benefits) or barriers (e.g., weak institutional capacity and high reporting costs). This theoretical scaffolding provided coherence to the scoping review, ensuring that evidence from diverse contexts could be systematically synthesised rather than descriptively summarised.

The integration of theory with evidence enhances the analytical depth of the scoping review and provides a foundation for future studies to test propositions empirically. Specifically, the model suggests that stakeholder and legitimacy pressures act as primary drivers of disclosure, while signalling theory explains variations in disclosure quality, and institutional gaps serve as barriers to adoption. Future research can empirically test these propositions and extend the theory in the field of blue accounting.

2.1. Methodology

This study used a scoping review methodological framework presented by Arksey and O’Malley (2005) to achieve the study’s objective of identifying factors that influence the organisations’ adoption of blue accounting disclosures (Arksey & O'malley, 2005). A scoping review, also known as a scoping exercise or scoping study, is a research method which evaluates the literature on a particular discipline and identifies research gaps and forms and sources of evidence to appraise policy-making, research and practice (Lockwood et al., 2019; Matenda et al., 2021; Yuriev et al., 2020). This method provides a comprehensive overview of the existing literature, addressing a broader review question than a systematic review, and thus offers an opportunity to identify the main areas of a research topic (Munn et al., 2018; Peters et al., 2020; Rasoolimanesh et al., 2023).

A scoping review was considered appropriate as it would allow the examination of literature and other information sources, and incorporate findings from various study methods and research designs (Arksey & O'malley, 2005; Matenda et al., 2021; Peters et al., 2020; Pollock et al., 2021). It is recommended for sophisticated and diverse research areas or areas that have not been extensively covered or researched before (Munn et al., 2018; Peters et al., 2020; Rasoolimanesh et al., 2023). Furthermore, a scoping review is appropriate when responding to extensive questions and summarising findings in a particular area (Arksey & O'malley, 2005; Lockwood et al., 2019; Matenda et al., 2021). Since investigating blue accounting is a fairly new research area with limited literature, a systematic literature review would not have yielded the best results, as there is no wealth of knowledge in this area. Thus, a scoping review was more appropriate for this study, providing sound and dependable knowledge with minimal bias (Matenda et al., 2021). Further, even though a scoping review is not widely used in sustainability studies, it has been noted that it is appropriate in this research area (Yuriev et al., 2020). To strengthen transparency and replicability, the scoping review was conducted using this model (Arksey and O’Malley, 2005) below:

- i.

- Phase 1: Research question identification

- ii.

- Phase 2: Relevant articles identification

- iii.

- Phase 3: Study selection

- iv.

- Phase 4: Data charting

- v.

- Phase 5: Compiling, summarising and writing the research results.

Phase 1: Research question identification

Phase 1 identifies the research question. It involved the generation of the research question that the study sought to respond to, and thus, it directed the manner in which the search plan was designed (Arksey & O'malley, 2005; Matenda et al., 2021; Munn et al., 2018; Mvunabandi, 2024; Yuriev et al., 2020). The question dealt with in this objective is: What are the determinants of Blue Accounting Disclosure Adoption Among Corporations?

Phase 2: Relevant studies identification

Phase 2 focuses on identifying the relevant studies necessary to address the research question. This entailed covering as much ground as possible and accessing a wide range of primary sources, including published articles, that could be valuable in seeking to respond to the research question (Matenda et al., 2021; Munn et al., 2018). The articles were sourced from the following databases: ScienceDirect, Google Scholar, ResearchGate, Google, Scopus, Wiley, and a snowball approach was also employed (Matenda et al., 2021; Munn et al., 2018; Pollock et al., 2018). These databases were considered because they contain several articles in the Scopus database and are thus likely to provide relevant articles for the study (Matenda et al., 2021; Pollock et al., 2018; Rasoolimanesh et al., 2023). Although Web of Science is considered one of the largest databases of academic literature, we could not use it because the aforementioned databases were deemed better suited for the study, and it overlaps significantly with Scopus content. (Adam et al., 2019; Pranckutė, 2021). To ensure high degrees of replicability, consistency, reliability and quality and to eradicate source bias, only studies extracted from the abovementioned sources are analysed (Arksey & O'malley, 2005; Matenda et al., 2021; Munn et al., 2018). Since the examined articles were authored by researchers from diverse parts of the world, geographical biases were minimised, as relevant articles were available for selection and review (Matenda et al., 2021). Studies published at any time were considered to capture the broadest possible range of research on this emerging concept. However, the search was restricted to publications available up to October 2025, which served as the cut-off date for inclusion in this scoping review. All the articles assessed were written in English. Any articles in other languages were excluded from the search, which may pose a limitation in that those non-English articles may have been relevant but have been excluded. While translation applications are available, to the authors’ knowledge, developers have not provided information on the suitability of these applications for academic use, and the time and financial resources required for translation might be significant (Maramba et al., 2019; Matenda et al., 2021). Furthermore, incorrect translations or interpretations might have distorted the study results. To perform a preliminary search, the following search terms were used to identify literature relevant to blue accounting and its disclosure within the corporate or policy context. These terms are “blue accounting,” “ocean accounting,” “marine ecosystem accounting,” “water accounting”, and “natural capital accounting”, with corporate disclosure-related terms such as “sustainability reporting,” “ESG disclosure,” and “environmental disclosure”. This was limited to sources in business, economics, and environmental sciences, and was restricted to open-access articles. This yielded several articles that were assessed to answer the research question of interest. The search enquiries were conducted between August 2024 to October 2025 on all the above-mentioned databases.

From the searches conducted; 93 articles were identified as relevant to the study. The snowball approach was applied, and citations within the specified period identified in the selected articles were evaluated until no further relevant information was found. 16 publications were identified as relevant to the study through the snowball approach. Therefore, a total of 109 publications relevant to the research question at hand were identified for this scoping review.

Phase 3: Study selection

In phase 3, the selected articles were analysed in depth to ensure only relevant articles were included in the study. This was essential since the search strategy pulled a number of irrelevant articles for the review. All articles that were not relevant to the study and all duplicates were eliminated from the study (Arksey & O'malley, 2005; Maramba et al., 2019; Matenda et al., 2021; Matz et al., 2019).

The selection of the studies was based on the inclusion and exclusion criteria, which were set by the authors to allow objective comparison and warrant ample quality (Matenda et al., 2021; Matz et al., 2019; Peters et al., 2020). The inclusion and exclusion criteria were based on the research question to warrant reliability in decision-making (Arksey & O'malley, 2005). Only peer-reviewed articles were considered, as they are recognised for their high quality and their contributions are deemed credible, thereby enhancing the validity of the research (Baxter et al., 2008; Pita et al., 2011). To avoid biases and publication discrimination, all publications were considered, provided they were in English and appropriate to the study, to provide as comprehensive a picture as possible, thus providing a better map of the whole range of literature in this area (Maramba et al., 2019; Pollock et al., 2018; Xiao & Watson, 2019). Articles falling outside the parameters set in the study were excluded from the study (Matenda et al., 2021; Yuriev et al., 2020).

Article Suitability Assessment

For this assessment, an initial suitability assessment was made based on the titles and abstracts of the publications. This is essential, as it prevents the unnecessary use of resources to obtain research articles that do not meet the minimum inclusion criteria (Pham et al., 2014). A form for evaluating the suitability of titles and abstracts is developed, pretested, and refined as needed before implementation. Where that initial assessment was not adequate to determine the suitability of an article for the review, an additional assessment was made, where the title, abstract, introduction, and conclusion were reviewed to assess suitability, so as to enhance the efficiency with which articles were evaluated for further review (Matenda et al., 2021; Matz et al., 2019; Munn et al., 2018; Pollock et al., 2018). However, if the above assessment was not satisfactory, then the entire article was reviewed to assess its eligibility for the scoping review (Matenda et al., 2021). This indicates that the complete texts of these research papers, written in English, were available.

3. Results

3.1. Data Collection

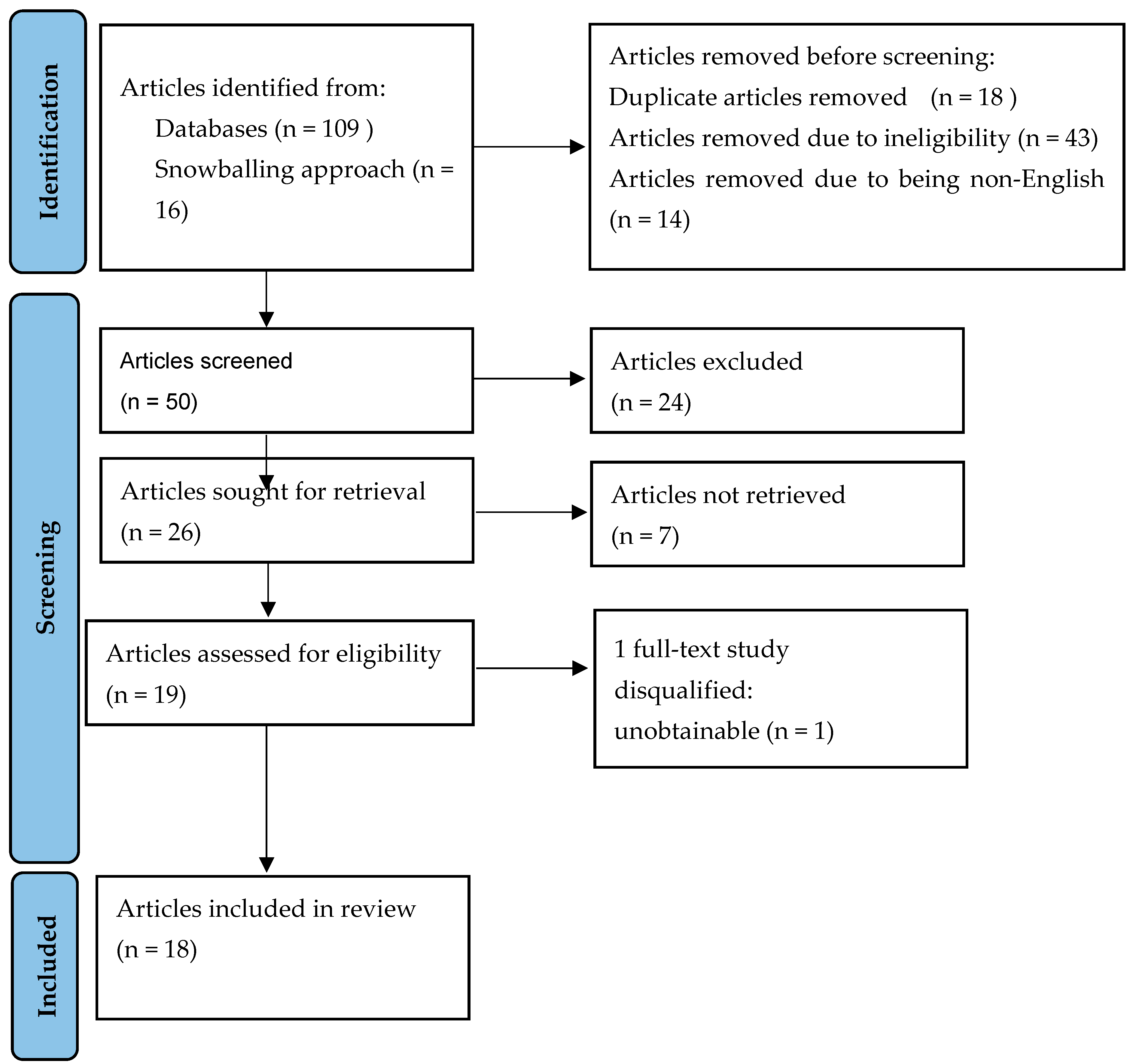

All the articles identified as relevant to the study had their full contents reviewed, and the following details were extracted: author(s), year of publication, title of the study, objective of the study, variable(s), population, composition of the sample, data source(s), technique(s)/method(s) applied, and the results (an integrated template, which was pretested and revised as required, was developed to collect these details) (Matenda et al., 2021; Peters et al., 2020; Xiao & Watson, 2019). For research papers not obtained through the authors’ affiliated institutions, attempts were made to contact the authors and journals for assistance in obtaining access to the articles. In this phase, all articles were reviewed in detail to identify relevant information for the research question, and any unsuitable articles were excluded from the study (Matenda et al., 2021). It should be noted that blue accounting is a fairly new concept, and thus, limited studies are available. The following 18 studies were ultimately selected for review in this study: (Abreu et al., 2017, 2019; Alqudhayeb, 2025; Colgan, 2016; Failler et al., 2023; Failler & Seisay, 2021; Lai et al., 2018; Larasasti et al., 2025; Loureiro et al., 2022; Moozanah et al., 2024; Nwachukwu et al., 2025; Pattinaja et al., 2023; Perkiss et al., 2022; Rahmayanti & Sari, 2023; Stefannie & Irwansyah, 2025; Syah et al., 2020; Warkula & Damayanti, 2025; Winarsih et al., 2020). Figure 1 displays the progression of articles from initial identification to final selection. Overall, 18 articles were identified and included in the study. After relevance checking and a deduplication exercise, which were included based on their titles, abstracts, introductions, and full test evaluations. One article could not be obtained and was therefore excluded from the review. Thus, only 18 studies were included in the review.

Following the tradition of narrative reviews, this study adopted the 'descriptive-analytical' approach, which involves applying a consistent analytical framework across all selected articles and systematically collecting general information from each source (Arksey & O’Malley, 2005). The data gathered were then presented in the data charting form, where the following information was captured: author(s), year of publication, title of the study, objective of the study, variable(s), population, sample, data source(s), technique(s)/method(s) applied, and results (Arksey & O'malley, 2005; Dinh et al., 2023; Matenda et al., 2021; Yuriev et al., 2020).

Phase 5: Collating, summarising and reporting results

In this phase, the results from the 18 reviewed articles were collated, summarised, and reported on. The results from the scoping review were limited to the amount of information that was examined from the scoped sources that were relevant to the research question at hand (Arksey & O'malley, 2005; Matenda et al., 2021; Peters et al., 2020). This scoping review focused on the content discovered, and quantitative analysis was limited to tallying the number of sources that mention a particular suggestion or topic (Sucharew and Macaluso, 2019). Once the data from the articles have been organised and the chosen studies reviewed, the findings are described through a narrative approach, in which insights are explained, and discussions are framed with support from the broader existing literature.

3.2. Review of Chosen Studies

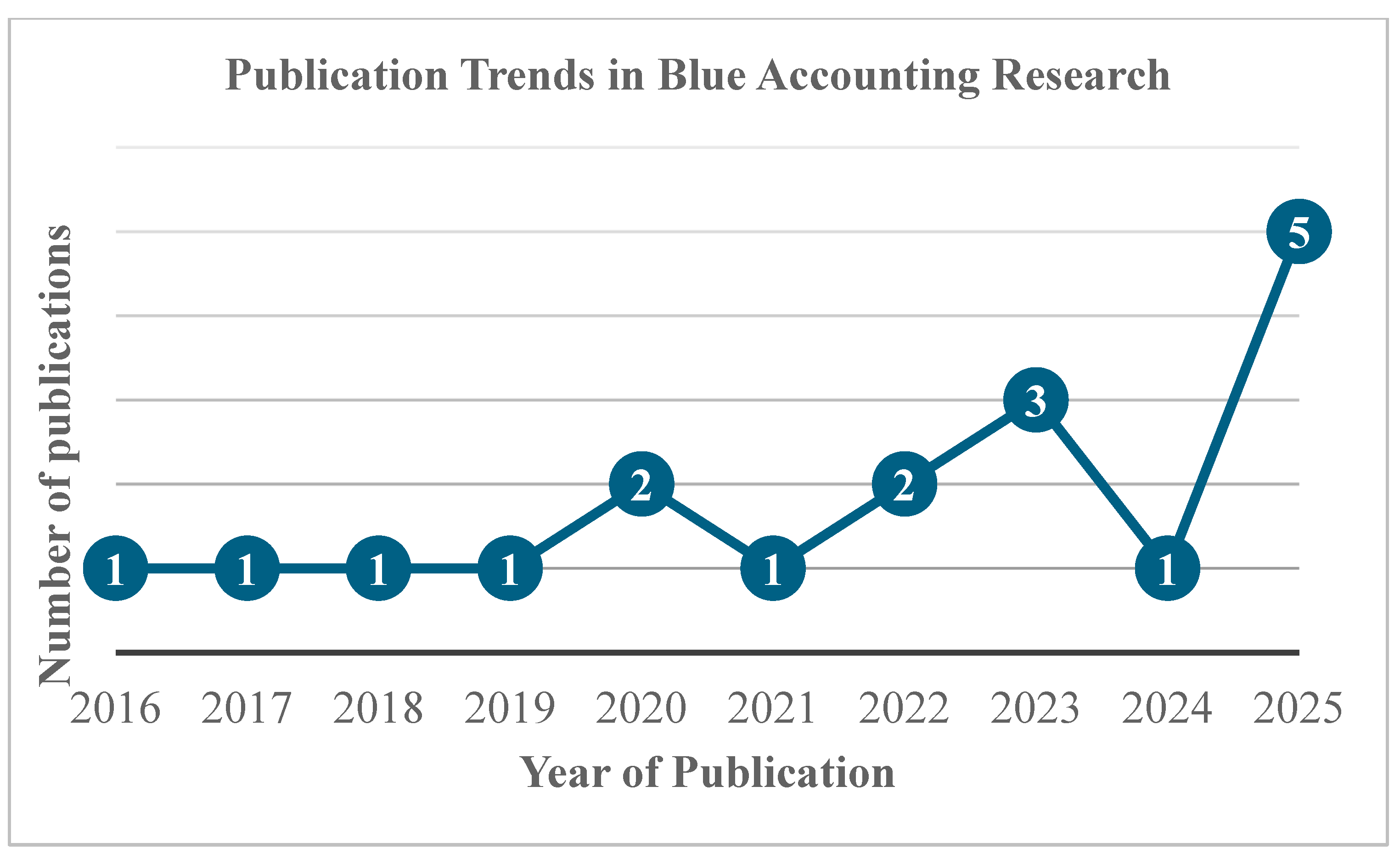

The studies reviewed were not limited to any geographical location and were published between 2016 and 2025. The figure below includes the frequency of only the years in which relevant studies were identified. Figure 2 shows the number of publications identified each year from 2016 to 2025.

Using the scoped articles, a review was conducted to identify the years in which the content was published, spanning from 2016 to 2025. From the above, 2025 (5 articles) and 2023 (3 articles) were the years when more articles appeared. The other years produced fewer articles (2016: 1; 2017: 1; 2018: 1; 2019: 1; 2020: 2; 2021: 1; 2022: 2, and 2024: 1). Having identified the period, an assessment was made of the locations where all the reviewed publications were found. This will assist in identifying the demographics of where studies on blue accounting were conducted, thereby identifying gaps, i.e., areas where there is limited or no research work on the phenomenon of blue accounting. The literature exhibits a strong empirical concentration in Indonesia, limited representation of Africa and Europe, and a reliance on non-region-specific studies, indicating that blue accounting research remains geographically uneven and constrained in its generalisability.

After identifying the years and regions covered by the articles, the findings were assessed to determine which recur across the articles and which are introduced for the first time, to identify the broad factors influencing the adoption of blue accounting.

The following provides a concise overview of all the articles scoped. The studies reflect varying conceptual developments in blue accounting and offer foundational insights into its drivers, barriers, and future potential. The studies demonstrate different considerations regarding the determinants of blue accounting disclosure adoption. A descriptive-analytical method was used to extract and synthesise the findings. The results are categorised thematically into conceptual drivers, institutional enablers, and implementation challenges, as revealed across the studies.

Several studies converge on the idea that traditional financial accounting systems, such as the System of National Accounts (SNA), are inadequate for capturing marine-related environmental degradation (Colgan, 2016; Lai et al., 2018; Winarsih et al., 2020). The adoption of Blue Accounting is therefore primarily motivated by the need to align economic data with ecological realities, especially in contexts where marine ecosystems are under pressure from unsustainable practices. The pursuit of full-spectrum sustainability is a recurring determinant. This includes social, cultural, economic, and environmental pillars, which conventional accounting often ignores (Perkiss et al., 2022; Stefannie & Irwansyah, 2025). The integration of sustainability into profit logic is especially evident in resource-dependent sectors like fishing and aquaculture (Moozanah et al., 2024; Warkula & Damayanti, 2025).

The Stakeholder Theory and Legitimacy Theory frame many of the adoption decisions. Corporations adopt Blue Accounting disclosures to meet stakeholder expectations and maintain social legitimacy (Larasasti et al., 2025; Syah et al., 2020; Warkula & Damayanti, 2025). Furthermore, another study underscores the importance of digital infrastructure, such as online dashboards, for improving data transparency and meeting the SDGs, particularly SDG 14 (Life Below Water) and SDG 17 (Partnerships for the Goals) (Rahmayanti & Sari, 2023).

Blue accounting Adoption is also heavily influenced by the presence or absence of supportive frameworks and governmental or international mandates. Several studies cite the Ocean Accounts Framework (OAF) and the Blue Economy Valuation Toolkit (BEVTK) as essential tools that guide data standardisation and facilitate investment decision-making (Failler et al., 2023; Loureiro et al., 2022). At the national level, Africa’s Blue Economy Strategy (ABES) has emerged as a critical determinant in aligning marine governance with blue accounting frameworks (Failler, 2022). Likewise, in Indonesia, models such as INABET for tuna fisheries demonstrate how localised, community-driven models can internalise blue economy principles into financial and environmental reporting (Pattinaja et al., 2023).

In fragile states, institutional determinants include the need for intersectoral coordination, especially where environmental degradation intersects with public health challenges like waterborne diseases (Alqudhayeb, 2025). These contexts require Blue Accounting to support both environmental and governance reform. While the drivers are compelling, several implementation challenges hinder widespread adoption of blue accounting. The most cited barrier is the lack of a standardised international accounting framework for marine ecosystems, which hampers comparability and decision-usefulness (Failler et al., 2023; Lai et al., 2018; Winarsih et al., 2020).

In many cases, companies and governments face resource constraints, including insufficient budgets, a lack of skilled human capital, and inadequate technical infrastructure (Moozanah et al., 2024; Stefannie & Irwansyah, 2025). Moreover, valuation difficulties for non-market ecosystem services, such as biodiversity or cultural values, challenge the integration of these variables into traditional accounting structures (Colgan, 2016; Perkiss et al., 2022). Data fragmentation across ecological, social, and economic indicators is another recurring issue. This not only weakens reporting quality but also limits the potential for evidence-based policymaking (Failler et al., 2023; Loureiro et al., 2022).

Table 1 below displays the scoping review of the literature on blue accounting. Column 1 of Table 1 displays the author(s) and (year) of publication, and Column 2 of Table 1 displays the findings. Column 3 of Table 1 displays the journal/book/series/chapter; Column 4 of Table 1 displays the title of the paper/article, and Column 5 of Table 1 displays the location.

4. Discussion

The findings of this scoping review provide important insights into the current state of Blue Accounting disclosure adoption, revealing a field that remains nascent, uneven in uptake, and constrained by significant structural and institutional barriers. This section presents the core findings, drawing on stakeholder theory, legitimacy theory, and signalling theory, and engages with existing literature while outlining implications for research, practice, and policy.

Across multiple studies, stakeholder expectations were a recurring and powerful driver of blue accounting disclosures (Abreu et al., 2019; Larasasti et al., 2025; Syah et al., 2020; Winarsih et al., 2020). This supports stakeholder theory, which posits that corporate responsiveness to environmental and social concerns is shaped by the salience of stakeholder demands (Freeman, 2010). The reviewed studies reveal that stakeholders are increasingly viewing ocean-related risks, such as overfishing, pollution, and biodiversity loss, as material sustainability concerns. In response, companies in marine-sensitive sectors seek to legitimise their operations by disclosing marine-related sustainability data, particularly under pressure from investors, regulators, consumers, and civil society.

Yet, this stakeholder response appears to be context-dependent and often limited to regions or sectors where environmental literacy and regulation are more advanced (e.g., Indonesia, certain coastal communities). Where stakeholder expectations are weak or fragmented, corporate engagement in blue accounting remains low, suggesting that stakeholder pressure alone is necessary but insufficient for widespread adoption.

Findings from several studies underscore the absence of clear legal and policy frameworks as a significant barrier (Abreu et al., 2017; Failler et al., 2023; Failler & Seisay, 2021; Loureiro et al., 2022). This directly supports legitimacy theory, which asserts that organisations use disclosure not only to meet stakeholder expectations but also to maintain a "social licence to operate" in line with prevailing institutional norms (Hora & Subramanian, 2019).

Where national or regional strategies exist, such as Africa’s Blue Economy Strategy (ABES) or Indonesia’s INABET fisheries model, corporate participation in blue accounting disclosures is higher. These cases illustrate how policy infrastructure, including toolkits such as BEVTK or OAF, can provide the scaffolding needed for disclosure systems to emerge. In contrast, jurisdictions lacking such instruments display low engagement with blue accounting, suggesting that institutional voids are a primary inhibitor.

Moreover, international standards such as IFRS S1 and GRI 304 were found to be insufficiently marine-specific, leading to a misalignment between corporate reporting frameworks and marine ecosystem priorities (Nwachukwu et al., 2025). This underscores the urgent need for a globally recognised Blue Accounting standard, which could bridge the gap between financial, environmental, and ocean governance metrics.

The literature also reflects the strategic use of blue accounting disclosures as signalling mechanisms to convey commitment to sustainability (Benjamin et al., 2023; Syah et al., 2020). Companies engaging in comprehensive blue accounting are often those that perceive sustainability leadership as a competitive differentiator, particularly in sectors reliant on high visibility, such as fisheries and aquaculture (Moozanah et al., 2024; Warkula & Damayanti, 2025). This supports signalling theory, which explains how disclosures reduce information asymmetry and help firms signal superior environmental performance.

However, the quality of disclosure is often inconsistent. In many cases, disclosures are limited to symbolic gestures or high-level commitments, rather than auditable, data-driven reporting. The risk of “blue-washing”, where companies use ocean-themed rhetoric without substantive change, was noted in several studies, echoing concerns from the critical accounting literature about the performativity of sustainability disclosures (Nwachukwu et al., 2025; Perkiss et al., 2022).

Operational challenges were also identified across the reviewed studies. These include the lack of technical expertise in marine ecosystem valuation, fragmented ecological, social, and economic data, inconsistent monitoring systems and reporting frequencies and low institutional capacity in developing economies (Alqudhayeb, 2025; Lai et al., 2018; Stefannie & Irwansyah, 2025).

These findings suggest that even when stakeholder and regulatory drivers are present, technical and infrastructural limitations may prevent meaningful disclosure. Without investments in education, training, and interdisciplinary collaboration, blue accounting risks becoming an elite or symbolic practice.

The review revealed a significant geographic concentration of studies in Indonesia and other parts of Southeast Asia. While this reflects the region’s policy leadership in blue economy governance, it also exposes a lack of empirical research from Africa, Latin America, the Caribbean, and South Asia, regions with extensive marine dependencies and significant blue economy potential. This bias limits the generalisability of the findings and suggests that regional adaptation of blue accounting frameworks may be necessary to account for cultural, ecological, and institutional diversity. Furthermore, there is an over-reliance on conceptual or qualitative studies. Very few studies offered empirical testing of disclosure models, limiting the ability to assess causality and impact.

Together, the findings reinforce a conceptual model in which stakeholder and legitimacy pressures drive voluntary disclosures, regulatory and institutional infrastructures condition the enabling environment, signalling mechanisms support strategic disclosure decisions, and Technical and knowledge-related constraints suppress or distort disclosure quality.

This integrated framework enables future studies to empirically assess the relative weight of each factor, potentially employing a mixed-methods design that combines content analysis of sustainability reports with interviews or surveys across various sectors and regions.

This scoping review identifies four key domains, namely, policy, practice/implementation, research, and theory, where blue accounting disclosure can make meaningful advancements. With regards to policy, it is evident that the lack of a globally standardised blue accounting framework is a significant barrier to adoption. International organisations, such as the United Nations, the IFRS Foundation, and GRI, are encouraged to develop marine-specific disclosure standards. This will enhance comparability, regulatory coherence, and the integration of marine impacts into corporate reporting.

Also, although stakeholder demands and alignment with the Sustainable Development Goals (particularly SDG 14) are driving adoption, many organisations lack the technical capacity and reporting infrastructure to implement blue accounting effectively. There is an urgent need for capacity-building, sector-specific guidance, and clearer implementation frameworks. Furthermore, the existing literature is largely conceptual or focused on specific regions, with limited empirical and cross-national studies, especially from the Global South. Future research should prioritise comparative, empirical, and interdisciplinary designs to improve generalizability and inform context-specific applications.

Lastly, this review supports a hybrid theoretical model that draws on stakeholder theory, legitimacy theory, and signalling theory. This integrated perspective provides a robust explanation for both the motivations for adopting blue accounting and the quality differentials in its disclosures. It should also inform future theoretical development and empirical testing.

5. Conclusions

This scoping review has mapped the emerging field of blue accounting disclosure, offering an integrative understanding of the factors influencing its adoption across corporate contexts. The review reveals that although blue accounting holds significant potential to advance marine sustainability and corporate accountability, its implementation remains limited due to the absence of standardised frameworks, data fragmentation, and capacity constraints, particularly in developing regions.

Key drivers of adoption include stakeholder pressures, climate change imperatives, SDG alignment, particularly SDG 14 and the desire to strengthen organisational legitimacy and transparency. However, substantial barriers persist, including limited technical capacity, weak institutional support, and a lack of harmonised reporting tools tailored to marine ecosystems.

The findings suggest that blue accounting is not merely a technical innovation, but a governance tool with implications for corporate strategy, policy development, and environmental stewardship. The integration of Stakeholder, Legitimacy, and Signalling Theories offers a comprehensive lens to interpret the motivations and constraints behind disclosure practices, providing a foundation for future empirical validation.

This study makes several contributions: it systematically synthesises fragmented literature on blue accounting, identifies a typology of drivers and barriers, and highlights the urgent need for regionally inclusive, empirically grounded research, especially from underrepresented Global South contexts. It also calls for coordinated global efforts to develop marine-specific accounting standards and enhance disclosure quality through policy incentives and capacity-building.

As blue economy activities expand, the role of transparent, accountable, and scientifically informed reporting becomes increasingly critical. Blue accounting, when effectively implemented, can support the sustainable governance of marine ecosystems, bridge information gaps for investors and regulators, and reinforce corporate commitments to long-term ocean health.

This review identifies several promising avenues for future research. First, empirical studies are needed to validate the conceptual propositions and theoretical insights presented in the literature. Quantitative investigations could test the impact of stakeholder pressures, regulatory environments, or ESG integration on the extent and quality of blue accounting disclosures. Second, cross-regional and cross-sectoral comparisons are largely missing; future studies should examine how institutional, ecological, and industry contexts shape disclosure practices. Third, methodological innovation, such as integrating geospatial data, digital dashboards, or natural capital valuation, could enhance the precision and decision-usefulness of blue accounting metrics. Finally, longitudinal studies would be valuable in tracking the evolution of corporate practices over time and in assessing the influence of emerging frameworks, such as the Ocean Accounts Framework and GRI’s evolving ESG standards.

As a scoping review, this study is inherently limited in its ability to assess the quality or statistical strength of the included evidence. While efforts were made to include a broad range of sources, the exclusion of non-English literature may have introduced language bias. Additionally, reliance on open-access databases may limit access to some subscription-based journals, potentially narrowing the pool of high-impact empirical studies. Furthermore, the emergent nature of blue accounting meant that most of the reviewed literature was conceptual or context-specific, thereby limiting its generalisability. These limitations underscore the need for future empirical research to expand and deepen the evidence base in this area.

Author Contributions

Conceptualization, J.D.M., F.R.M., N.M. and B.C.N.; methodology, J.D.M., F.R.M., N.M. and B.C.N.; data curation, N.M.; formal analysis, J.D.M., F.R.M., N.M. and B.C.N.; investigation, N.M.; resources, J.D.M. and B.C.N.; writing—original draft preparation, J.D.M., N.M. and F.R.M.; writing—review and editing, J.D.M., N.M., F.R.M. and B.C.N.; supervision, J.D.M. and B.C.N.; project administration, J.D.M., F.R.M., N.M. and B.C.N. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Abreu, R., David, F., Santos, L. L., Segura, L., & Formigoni, H. (2017). Blue accounting: First insights. 16th International Conference on Corporate Social Responsibility and 7th Organisational Governance Conference, Buxton, United Kingdom, August 30th-Sept. 1st, 2017,.

- Abreu, R.; David, F.; Santos, L.L.; Segura, L.; Formigoni, H. (2019). Blue Accounting: Looking for a New Standard. Responsibility and Governance: The Twin Pillars of Sustainability, 27-43.

- Adam, I.H.D.; Jusoh, A.; Mardani, A.; Streimikiene, D.; Nor, K.M. Scoping research on sustainability performance from manufacturing industry sector. Probl. Perspect. Manag. 2019, 17, 134–146. [CrossRef]

- Agyemang, A.O.; Yusheng, K.; Twum, A.K.; Ayamba, E.C.; Kongkuah, M.; Musah, M. Trend and relationship between environmental accounting disclosure and environmental performance for mining companies listed in China. Environ. Dev. Sustain. 2021, 23, 12192–12216. [CrossRef]

- Alqudhayeb, N. J. A. (2025). Synthesising prior research on blue accounting, MFCA, ABC, and public health: toward an integrated water governance framework for fragile states. Proceeding of International Students Conference of Economics and Business Excellence,.

- Arksey, H.; O’Malley, L. Scoping studies: Towards a methodological framework. Int. J. Soc. Res. Methodol. 2005, 8, 19–32. [CrossRef]

- Baxter, K.; Glendinning, C.; Clarke, S. Making informed choices in social care: the importance of accessible information. Heal. Soc. Care Community 2007, 16, 197–207. [CrossRef]

- Benjamin, S.J.; Biswas, P.K.; Wellalage, N.H.; Man, Y. Environmental disclosure and its relation to waste performance. Meditari Account. Res. 2022, 31, 1545–1577. [CrossRef]

- Castro-Cadenas, M.D.; Loiseau, C.; Reimer, J.M.; Claudet, J. Tracking changes in social-ecological systems along environmental disturbances with the ocean health index. Sci. Total. Environ. 2022, 841, 156423. [CrossRef]

- Colgan, C.S. Measurement of the Ocean Economy From National Income Accounts to the Sustainable Blue Economy. J. Ocean Coast. Econ. 2016, 2, 12. [CrossRef]

- Datt, R.R.; Luo, L.; Tang, Q. Corporate voluntary carbon disclosure strategy and carbon performance in the USA. Account. Res. J. 2019, 32, 417–435. [CrossRef]

- de Villiers, C., Hsiao, P.-C. K., & Maroun, W. (2020). Introduction to the Routledge Handbook of Integrated Reporting: An overview of integrated reporting and this book, which entails different perspectives on a maturing field and a framework for future research. The Routledge handbook of integrated reporting, 1-14.

- Dinh, T.; Husmann, A.; Melloni, G. Corporate Sustainability Reporting in Europe: A Scoping Review. Account. Eur. 2022, 20, 1–29. [CrossRef]

- Elshabasy, Y.N. The impact of corporate characteristics on environmental information disclosure: an empirical study on the listed firms in Egypt. 2018, 12. [CrossRef]

- Failler, P.; Liu, J.; Lallemand, P.; March, A. Blue Accounting Approaches in the Emerging African Blue Economy Context. J. Sustain. Res. 2023, 5. [CrossRef]

- Failler, P., & Seisay, M. (2021). Information Note on Blue Accounting in the Context of African Union Blue Economy Strategy.

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman.

- Gallardo-Vázquez, D.; Barroso-Méndez, M.J.; Pajuelo-Moreno, M.L.; Sánchez-Meca, J. Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach. Sustainability 2019, 11, 1115. [CrossRef]

- Herbert-Read, J.E.; Thornton, A.; Amon, D.J.; Birchenough, S.N.R.; Côté, I.M.; Dias, M.P.; Godley, B.J.; Keith, S.A.; McKinley, E.; Peck, L.S.; et al. A global horizon scan of issues impacting marine and coastal biodiversity conservation. Nat. Ecol. Evol. 2022, 6, 1262–1270. [CrossRef]

- Hora, M.; Subramanian, R. Relationship between Positive Environmental Disclosures and Environmental Performance: An Empirical Investigation of the Greenwashing Sin of the Hidden Trade-off. J. Ind. Ecol. 2018, 23, 855–868. [CrossRef]

- Khan, S.A.R.; Zhang, Y.; Kumar, A.; Zavadskas, E.; Streimikiene, D. Measuring the impact of renewable energy, public health expenditure, logistics, and environmental performance on sustainable economic growth. Sustain. Dev. 2020, 28, 833–843. [CrossRef]

- Kirkman, S.; Mann, B.; Sink, K.; Adams, R.; Livingstone, T.-C.; Mann-Lang, J.; Pfaff, M.; Samaai, T.; van der Bank, M.; Williams, L.; et al. Evaluating the evidence for ecological effectiveness of South Africa’s marine protected areas. Afr. J. Mar. Sci. 2021, 43, 389–412. [CrossRef]

- Lai, T.-Y.; Salminen, J.; Jäppinen, J.-P.; Koljonen, S.; Mononen, L.; Nieminen, E.; Vihervaara, P.; Oinonen, S. Bridging the gap between ecosystem service indicators and ecosystem accounting in Finland. Ecol. Model. 2018, 377, 51–65. [CrossRef]

- Landrigan, P.J.; Stegeman, J.J.; Fleming, L.E.; Allemand, D.; Anderson, D.M.; Backer, L.C.; Brucker-Davis, F.; Chevalier, N.; Corra, L.; Czerucka, D.; et al. Human Health and Ocean Pollution. Ann. Glob. Heal. 2020, 86, 151. [CrossRef]

- Larasasti, S.; Amalia, P.N.; Santika, I.; Putri, A.; Crisanta, F.; Arnita, V. The Relationship Between Blue Accounting, Marine Policy and Climate Change To The Sustainability Of Marine Ecosystems. J. Environ. Econ. Sustain. 2024, 2. [CrossRef]

- Lockwood, C.; dos Santos, K.B.; Pap, R. Practical Guidance for Knowledge Synthesis: Scoping Review Methods. Asian Nurs. Res. 2019, 13, 287–294. [CrossRef]

- Loureiro, T.G.; Du Plessis, N.; Findlay, K. Into the blue – The blue economy model in Operation Phakisa ‘Unlocking the Ocean Economy’ Programme. South Afr. J. Sci. 2022, 118. [CrossRef]

- Lubchenco, J., & Haugan, P. M. (2023). National Accounting for the Ocean and Ocean Economy. In The Blue Compendium: From Knowledge to Action for a Sustainable Ocean Economy (pp. 279-307). Springer.

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring More Sustainable Reporting in Europe Using Non-Financial Disclosure—De Facto and De Jure Evidence. Sustainability 2018, 10, 1162. [CrossRef]

- Maramba, I.; Chatterjee, A.; Newman, C. Methods of usability testing in the development of eHealth applications: A scoping review. Int. J. Med Informatics 2019, 126, 95–104. [CrossRef]

- Matenda, F.R.; Sibanda, M.; Chikodza, E.; Gumbo, V. Bankruptcy prediction for private firms in developing economies: a scoping review and guidance for future research. Manag. Rev. Q. 2021, 72, 927–966. [CrossRef]

- Matz, C.J.; Egyed, M.; Hocking, R.; Seenundun, S.; Charman, N.; Edmonds, N. Human health effects of traffic-related air pollution (TRAP): a scoping review protocol. Syst. Rev. 2019, 8, 1–5. [CrossRef]

- Moozanah, S.; Rusdiansyah, N.; Rosyidah, D.M.; Riany, M. Profit and Sustainability Perceptions Related to the Implementation of Blue Accounting in the Fishing Industry in Palabuhanratu. J. Account. Audit. Bus. 2024, 7, 36–43. [CrossRef]

- Munn, Z., Peters, M. D., Stern, C., Tufanaru, C., McArthur, A., & Aromataris, E. (2018). Systematic review or scoping review? Guidance for authors when choosing between a systematic or scoping review approach. BMC medical research methodology, 18, 1-7.

- Mvunabandi, J.D. Scholarly Discourse of Remote Forensic Auditing and Fraud Schemes in Remote Workforce: A Scoping Review. Int. J. Appl. Res. Bus. Manag. 2024, 5. [CrossRef]

- Nwachukwu, K. K., Andeb, J. O., & Ogenyi, P. D. M. A. (2025). An Integrated Reporting Approach to Blue Accounting. Journal of Accounting and Financial Management, 11(6), 20.

- Pattinaja, E. M., Abrahamsz, J., & Loppies, L. R. (2023). Blue economy accounting model for tuna fisher groups in Maluku Province, Indonesia. Aquaculture, Aquarium, Conservation & Legislation, 16(4), 2060-2071.

- Perkiss, S.; McIlgorm, A.; Nichols, R.; Lewis, A.R.; Lal, K.K.; Voyer, M. Can critical accounting perspectives contribute to the development of ocean accounting and ocean governance?. Mar. Policy 2022, 136. [CrossRef]

- Peters, M.D.J.; Marnie, C.; Tricco, A.C.; Pollock, D.; Munn, Z.; Alexander, L.; McInerney, P.; Godfrey, C.M.; Khalil, H. Updated methodological guidance for the conduct of scoping reviews. JBI Évid. Synth. 2020, 18, 2119–2126. [CrossRef]

- Pita, C.; Pierce, G.J.; Theodossiou, I.; Macpherson, K. An overview of commercial fishers’ attitudes towards marine protected areas. Hydrobiologia 2011, 670, 289–306. [CrossRef]

- Pollock, A.; Campbell, P.; Struthers, C.; Synnot, A.; Nunn, J.; Hill, S.; Goodare, H.; Morris, J.; Watts, C.; Morley, R. Stakeholder involvement in systematic reviews: a scoping review. Syst. Rev. 2018, 7, 1–26. [CrossRef]

- Pollock, D.; Davies, E.L.; Peters, M.D.J.; Tricco, A.C.; Alexander, L.; McInerney, P.; Godfrey, C.M.; Khalil, H.; Munn, Z. Undertaking a scoping review: A practical guide for nursing and midwifery students, clinicians, researchers, and academics. J. Adv. Nurs. 2021, 77, 2102–2113. [CrossRef]

- Pranckutė, R. Web of Science (WoS) and Scopus: The Titans of Bibliographic Information in Today’s Academic World. Publications 2021, 9, 12. [CrossRef]

- Rahmayanti, A.Y.; Sari, D.K. Blue Accounting to Enhance the Quality of Sustainability Report. International Conference on Vocational Education Applied Science and Technology. p. 69.

- Rasoolimanesh, S.M.; Ramakrishna, S.; Hall, C.M.; Esfandiar, K.; Seyfi, S. A systematic scoping review of sustainable tourism indicators in relation to the sustainable development goals. J. Sustain. Tour. 2020, 31, 1497–1517. [CrossRef]

- Piao, R.S.; Scalco, A.R.; Vazquez-Brust, D.; Plaza-Ubeda, J.A.; Cortés, M.E.T. Guest editorial: The UN sustainable development goals and management theory and practice. RAUSP Manag. J. 2022, 57, 358–361. [CrossRef]

- Stafford, W., Russo, V., Oelofse, S., Godfrey, L., & Pretorius, A. (2022). Reducing Plastic Pollution: A comprehensive evidence-based strategy for South Africa.

- Stefannie, D., & Irwansyah, F. N. K. (2025). Blue Accounting Practices for Marine Economic Sustainability: A Descriptive Analysis of the Implementation of Blue Accounting in the Fisheries Sector in West Kutai Regency. American Journal of Humanities and Social Sciences Research (AJHSSR), 9(6), 218-225.

- Struwig, M.; Berg, A.V.D.; Hadi, N. Challenges in the ocean economy of South Africa. Dev. South. Afr. 2023, 41, 1–15. [CrossRef]

- Syah, S., Saraswati, E., & Sukoharsono, E. G. (2020). Blue Accounting and Sustainability. 23rd Asian Forum of Business Education (AFBE 2019),.

- Udo, E. J. (2019). ENVIRONMENTAL ACCOUNTING DISCLOSURE PRACTICES IN ANNUAL REPORTS OF LISTED OIL AND GAS COMPANIES IN NIGERIA. International Journal of Accounting & Finance (IJAF), 8(1).

- Warkula, Y.Z.; Mediaty; Damayanti, R.A. Application of Blue Accounting and Sustainability Accounting in Pearl Cultivation Company Commanditaire Vennootschap (CV) Mairang Jabulenga Village, Aru Islands. J. Lifestyle SDGs Rev. 2024, 5, e02099–e02099. [CrossRef]

- Winarsih; Fuad, K.; Setyawan, H. Blue Accounting of the Marine Knowledge and Sustainable Seas: A Conceptual Model. Conference on Complex, Intelligent, and Software Intensive Systems. Australia; pp. 954–958.

- Xiao, Y.; Watson, M. Guidance on Conducting a Systematic Literature Review. J. Plan. Educ. Res. 2017, 39, 93–112. [CrossRef]

- Yasar, B.; Martin, T.; Kiessling, T. An empirical test of signalling theory. Manag. Res. Rev. 2020, 43, 1309–1335. [CrossRef]

- Yuriev, A.; Dahmen, M.; Paillé, P.; Boiral, O.; Guillaumie, L. Pro-environmental behaviors through the lens of the theory of planned behavior: A scoping review. Resour. Conserv. Recycl. 2020, 155. [CrossRef]

Figure 1.

Study selection process flowchart. Source: own compilation.

Figure 2.

Publication trends in blue accounting research (2016-2025). Source: Author's own compilation (2025).

Figure 2.

Publication trends in blue accounting research (2016-2025). Source: Author's own compilation (2025).

Table 1.

Presentation of Scoping review.

| Author(s) and (year) of publication | Findings |

Journal/Book/Series/ Chapter |

Title of the paper/article | Location |

| Failler et al. (2023) | Blue accounting provides an assessment of actions against climate change. There is no uniform accounting framework for blue accounting. The data necessary for blue accounting are scattered. Blue accounting can enhance the sustainability of the operations (conservation and sustainable consumption). Blue accounting reflects value for measuring the cost of degradation and destruction. Producing accurate data for blue accounting is difficult, especially in integrating social, economic, and ecological aspects. The legal framework/laws and regulations governing the marine space affect the adoption /non-adoption of blue accounting. |

Journal of Sustainability Research | Blue accounting approaches in the emerging African blue economy context. | Africa |

| Rahmayanti & Sari (2023) | The availability/adequacy of data for blue accounting disclosures determines whether they are adopted. The urgent need for ocean sustainability (to meet the needs of current and future generations) could accelerate the adoption of blue accounting disclosures. The achievement of SDG Goal 14 (Life Below Water) could encourage the adoption of blue accounting disclosure. The lack of a clear framework for blue accounting may hinder the adoption of blue accounting disclosure. |

Conference Proceedings (The 5th International Conference on Vocational Education, Applied Science and Technology: 2022). | Blue accounting to enhance the quality of the sustainability report. | Indonesia |

| Syah et al. (2020) | Blue accounting adoption enhances the consideration of the sustainable use of marine resources in the present and future generations. Stakeholders interested in marine ecosystems put pressure on information relating to the organisation's marine practices and their sustainability. Blue accounting adoption improves the organisation’s environmental accounting. |

Conference Proceedings: 23rd Asian Forum of Business Education | Blue accounting and sustainability | Indonesia |

| Failler & Seisay (2021) | Blue accounting can serve as a tool to assess the effectiveness of climate change actions. Government incentives, such as grants or ocean-based financing (e.g., blue bonds), could encourage marine sustainability. There is no uniform international/national framework for blue accounting, resulting in the necessary disclosure information being unavailable or incomplete. |

African Union Inter-African Bureau for Animal Resources (AU-IBAR) Information note | Information Note on Blue Accounting in the Context of African Union Blue Economy Strategy | Africa |

| Abreu et al. (2017) | Blue accounting may assist in meeting stakeholders' information needs regarding the marine ecosystem and the effects of the organisation’s operations. There is a lack of accounting and marine knowledge. A regulatory framework that enforces blue accounting might accelerate blue accounting disclosure adoption. |

Proceedings of the 16th International Conference on Corporate Social Responsibility and 7th Organisational Governance Conference | Blue accounting: First insights | Broad, including Europe |

| Abreu et al. (2019) | Blue accounting disclosures could satisfy stakeholders' information needs regarding the marine ecosystem and the effects of the organisation’s operations. The adoption might provide more knowledge about the marine ecosystem and how it interfaces with the entity’s operations. A regulatory framework that enforces blue accounting might accelerate blue accounting disclosure adoption. |

Responsibility and Governance: The Twin Pillars of Sustainability | Blue accounting: Looking for a new standard. | Europe |

| Winarsih et al. (2020) | The stakeholders' information needs regarding the marine ecosystem and its impact on the organisation’s operations may influence the organisation’s adoption of blue accounting. The organisation might legitimise its operations through blue accounting disclosures. Blue accounting adoption may be valuable to stakeholders and organisations seeking a deeper understanding of the marine ecosystem. The lack of a specific international accounting standard for blue accounting weakens the reliability and comparability of its data. The complexity of marine and maritime resources, as well as the ability to properly decipher which data is relevant for blue accounting, may pose a limitation to the adoption of blue accounting. |

Complex, Intelligent, and Software Intensive Systems: Proceedings of the 13th International Conference on Complex, Intelligent, and Software Intensive Systems (CISIS-2019). | Blue accounting of the marine knowledge and sustainable seas: A conceptual model. | The research was not conducted in a specific marine region. |

| Pattinaja et al. (2023) | The organisation's desire to identify the positive and negative environmental effects of its operations in the marine space might influence its adoption of blue accounting disclosures. | Aquaculture, Aquarium, Conservation & Legislation | Blue economy accounting model for tuna fisher groups in Maluku Province, Indonesia | Indonesia |

| Perkiss et al. (2022). | Perceiving ocean accounting as a means to measure the organisation’s progress towards attaining the SDGs might influence the adoption of blue accounting disclosure. Initiatives to develop an accounting system grounded in accounting principles and processes focused on measuring marine facets might influence the adoption of blue accounting disclosures. Pursuing effective ocean governance based on the results/information from ocean accounting might influence the adoption of blue accounting disclosure. |

Marine Policy | Can critical accounting perspectives contribute to the development of ocean accounting and ocean governance? | The research was not conducted in a specific marine region. |

| Lai et al. (2018) | There is a lack of an accounting framework that comprehensively accounts for the various factors of the marine ecosystem. There is a lack of availability of relevant, up-to-date data, thus limiting methodological consistency and accuracy when evaluating and accounting for marine ecosystem sustainability. |

Ecological Modelling | Bridging the gap between ecosystem service indicators and ecosystem accounting in Finland |

Finland |

| Loureiro et al. (2022) | The adoption would involve a multidisciplinary collaboration, as it requires integrating information from various sources to account for environmental, economic, and social factors, and utilising several established and tested accounting systems, which may lead to reluctance to adopt. Blue accounting information output provides the necessary information for sustainable development. The adoption would provide the information necessary to facilitate effective decision-making, ocean governance, and policy development. Adoption would enable ocean monitoring and assessment. Blue accounting adoption would fast-track the creation of a consistent, standardised, and holistic framework that integrates social, environmental, and economic data. The adoption would facilitate the tracking and reporting on the achievement of SDGs. |

Journal of Marine Science | Every account counts for sustainable development: lessons from the African CoP to implement ocean accounts in the Western Indian Ocean region |

Western Indian Ocean |

| Colgan (2016) | This would provide small islands, which are mainly composed of ocean, with valuable information for decision-making about their economies and livelihoods. The required capacity to undertake the necessary measurements for blue accounting may affect its adoption. |

Journal of Ocean and Coastal Economics | Measurement of the ocean economy from national income accounts to the sustainable blue economy | Not applicable |

| Warkula & Damayanti (2025) | This would provide organisations with a means to align their operations with societal norms and expectations. This would also enable sustainable maintenance of the marine ecosystem. This would enable the effective protection and preservation of this valuable economic asset, the sea. This would provide valuable marine-related information to organisations and the public, enabling them to identify, measure, evaluate, and report on blue economic growth. This would support and enable the assessment of progress toward SDG 14. |

Journal of Lifestyle and SDGs Review | Application of Blue Accounting and Sustainability Accounting in Pearl Cultivation Company Commanditaire Vennootschap (CV) Mairang Jabulenga Village, Aru Islands | Aru Islands |

| Moozanah et al. (2024) | The adoption would facilitate the tracking and reporting on the achievement of SDG 14. The adoption would ensure sustainable fishing practices that prevent over-exploitation. The adoption would create a balance between economic profit and environmental sustainability. This would also enable an effective shift from financial-focused accounting to an accounting framework that encompasses social and environmental impacts when using marine resources. This would facilitate the availability of information, increasing public and organisational awareness of marine ecosystem management. The lack of knowledge or education on blue accounting hinders its effective implementation. |

Journal of Accounting Auditing and Business | Profit and Sustainability Perceptions Related to the Implementation of Blue Accounting in the Fishing Industry in Palabuhanratu | Palabuhanratu |

| Larasasti, et al. (2025) | This would enhance the measurement of the economic, social and environmental value of marine ecosystems. This would encourage environmentally sound business practices and increase transparency in marine resource management. Adoption would encourage organisations to gain societal acceptance, thereby legitimising their stance. This promotes a competitive advantage for organisations by improving their productivity and customer preference. This would provide evidence-based data to support enhanced decision-making. This would help reduce environmental problems and contribute to reporting on environmental sustainability. The adoption is hindered by weak law enforcement and poorly designed policies. The lack of a standardised reporting framework to guide calculations, presentations, and disclosures of blue accounting under financial standards limits its widespread and consistent adoption. |

Journal of Environmental Economics and Sustainability | The Relationship Between Blue Accounting, Marine Policy and Climate Change to the Sustainability of Marine Ecosystems | Not applicable |

| Alqudhayeb (2025) | This would enable evidence-based policy making and improve intersectoral coordination. Improves national environmental accountability and sustainable development goals. Adoption would encourage organisations to gain societal acceptance, thereby legitimising their stance. Blue accounting would enable consistent monitoring and compliance with marine-related regulations. The scattered data and inconsistent reporting hinder the effective implementation of blue accounting disclosures. |

Proceeding of International Students Conference of Economics and Business Excellence | Synthesizing prior research on blue accounting, MFCA, ABC, and public health: toward an integrated water governance framework for fragile states | Not Applicable |

| Nwachukwu et al. (2025) | The adoption would improve corporate governance and sustainable performance. This would serve as a catalyst for a worldwide blue economy. Adoption would encourage organisations to gain societal acceptance, thereby legitimising their stance. The lack of a clear, transparent accounting disclosure framework leads to bluewashing and undermines market confidence. Inadequate blue accounting corporate reporting fails to capture the complex relationships between business activities and ecosystem health. The jurisdictional and regulatory challenges faced by multinational companies require adherence to diverse national and regional regulations while also meeting international standards, which poses a significant challenge. The current financial and sustainability reporting standards, such as IFRS S1 and GRI 304, lack specific guidance on ocean-related topics. The cost and complexity of establishing comprehensive blue accounting disclosure may pose barriers for smaller companies. Blue accounting measurement challenges due to the relativity of ocean-related sustainability metrics, which vary significantly by region/ecosystem type, pose a challenge to organisations providing these disclosures. The complexity of marine ecosystem interactions makes it challenging to isolate corporate-specific impacts, leading to reluctance in blue accounting disclosures. |

Journal of Accounting and Financial Management | An Integrated Reporting Approach to Blue Accounting | Not Applicable |

| Stefannie, et al. (2025) | This would help reduce environmental problems and contribute to reporting on environmental sustainability. Limited monitoring frequency and data availability hinder comprehensive time series data collection, which would enable effective blue accounting. The lack of knowledge or education on blue accounting hinders its effective implementation. The lack of capacity or human resources hinders the effective implementation of blue accounting. The adoption would facilitate the tracking and reporting on the achievement of SDG 14. |

American Journal of Humanities and Social Sciences Research (AJHSSR) | Blue Accounting Practices for Marine Economic Sustainability: A Descriptive Analysis of the Implementation of Blue Accounting in the Fisheries Sector in West Kutai Regency |

West Kutai Regency (Indonesia) |

Source: Author's own compilation (2025).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.