Submitted:

25 January 2026

Posted:

26 January 2026

You are already at the latest version

Abstract

In the context of economic integration and the global trend of sustainable development, sustainability information disclosure is increasingly becoming an essential requirement for businesses. For the listed wine, beer, and soft drink industry in Vietnam (Listed Wine, Beer, Soft Drink Companies: WBDCs), a sector with a significant impact on the environment and society, the Sustainability Report (SR) is not only a communication tool but also a representation of the company’s long-term development strategy. This study aims to identify and measure the extent of influence of internal and external factors on the decision to adopt SR in companies belonging to the WBDCs.

Through quantitative survey and data analysis using the SEM model, the results show that the group of factors related to Enterprise Size plays a decisive role. Additionally, the managerial perspective is also identified as a crucial driver in promoting the transparency of sustainability information. From the research findings, the author team proposes several policy recommendations and orientations to support businesses in enhancing their capacity for sustainability information disclosure, aiming to improve competitiveness and long-term development of the industry in the context of deep integration.

Keywords:

sustainability report

; listed wine

; beer and soft drink companies

; Vietnam

1. Introduction

In recent years, sustainable development is no longer an unfamiliar concept but has become a strategic orientation in the operations of many businesses. Faced with increasing demands from consumers, investors, and regulatory agencies, companies not only need to achieve financial efficiency but also must demonstrate their social and environmental responsibility. In this context, the SR is increasingly seen as an effective tool to help businesses convey information transparently, build a positive image, and create a long-term competitive advantage.

For WBDCs, a sector closely related to public health and subject to strict supervision regarding the environment and business ethics, the requirement for transparent operations through SR becomes even more urgent. Sustainable development is an approach that integrates social, economic, and environmental impacts into a solid and comprehensive business strategy. The development and disclosure of this report not only reflect the company’s commitment to the principles of sustainable development but also contribute to building trust with customers, partners, and society as a whole. However, reality shows that the prevalence and quality of SR in the industry still have many limitations, mainly due to factors such as insufficient awareness, lack of implementation resources, and the absence of a suitable framework for the specific nature of the industry’s operations.

Therefore, studying the factors influencing the ability and extent of SR adoption in WBDCs is necessary to clearly identify the barriers and favorable conditions in the implementation process. Concurrently, proposing a report template suitable for the industry’s reality will not only support businesses in enhancing their governance capacity but also help adjust their operational strategies towards transparency, responsibility, and sustainability.

2. Literature Review

2.1. Studies on the Adoption of Sustainability Reporting Abroad

Kilic, M., Uyar, A., & Ataman, B. (2017) surveyed the SR practices of non-financial companies listed on Borsa Istanbul during the 2004–2015 period. The results showed a significant increase in the number of standalone reports, reflecting a growing awareness among Turkish businesses about sustainable development. However, the disclosure rate remained low and primarily followed the Global Reporting Initiative (GRI) framework. Factors such as being listed on the Corporate Governance Index (CGI), Enterprise Size, industry, Return on Assets, and the existence of a sustainability committee significantly influenced the decision to disclose the report. The study further affirmed the roles of the CGI, company size, and the sustainability committee in promoting report disclosure during the 2013–2015 period. However, the percentage of companies conducting report audits was very low due to the lack of mandatory regulations and clear standards. The study suggests that factors related to the level of disclosure and external pressures have a major impact on the behavior of disclosing sustainability information.

Tauringana, V. (2020) emphasized the role of managerial perception in identifying factors that promote sustainability reporting in developing countries. The results show that factors such as legislation, training, guidance, awareness communication, and pressure from the market, stakeholders, and the public significantly influence the decision to disclose sustainability information. However, the efforts of the GRI during the 2014–2019 period were assessed as having a limited impact. The author recommends adopting an evidence-based approach from managerial perception to improve the effectiveness of SR implementation in a context of weak institutions. The study also calls for expanding surveys on factors promoting SR in many other countries, as well as evaluating the effectiveness of current policies.

Iranmanesh, M., Foroughi, B., & Hyun, S. S. (2019) examined the institutional, cultural, and corporate characteristic factors affecting the quality of SR of financial institutions in both developed and developing countries. The results show that factors such as country of origin, religion, ownership, and mission statement have a significant impact on SR. Particularly, the religion factor (Islam/non-Islam) is negatively moderated by environmental performance. The study contributes to the literature on Corporate Social Responsibility (CSR) by emphasizing the role of cultural-institutional factors in the financial sector – a field less researched previously. However, the study is limited to the financial sector and does not clearly explain the differences in self-reported questionnaire responses between the private and public sectors, suggesting that future research should expand the scope of industries and further explore intermediate factors.

Alicia, G., Amirreza, K., & Antonella, F.C. (2020) analyzed the factors influencing the adoption of SR and external assurance in large corporations in Asia and Africa. Based on data from GRI and Orbis, the results show that operating in the manufacturing sector and the proportion of women on the board of directors have a positive relationship with both SR disclosure and financial performance. Conversely, the age of the board of directors did not have a significant impact on reporting practices. The study contributes to the literature on emerging economies, while also supporting the shaping of policies that encourage transparency and independence in SR.

Sebrina, N., Salma, T., Mayar, A., & Dovi, S. (2022) surveyed the prevalence and quality of standalone SR at listed companies in Indonesia – an emerging market without mandatory SR regulations. Analyzing 240 reports from 2016–2019, the study found that the prevalence of reporting was still low, and the quality of disclosure was limited, especially in terms of reliability. Among the three pillars of the GRI report, economic content was disclosed the most, while environmental content was given less attention. The results show that current SR practices do not yet reflect the role of the report as a tool for building corporate image, raising questions about the suitability of legitimacy theory in the Indonesian context. The study continues to clarify the limitations on the quality of SR in Indonesia by pointing out that the reliability of the report is still low due to the absence of independent third-party verification. Although the factors of “timeliness” and “stakeholder engagement” reached a satisfactory level – reinforcing the arguments of stakeholder theory – the indicators of clarity and accuracy only met acceptable levels, while reliability did not yet meet requirements.

The study by Adams, D., Hines, F., & Munday, M. (2022), based on 21 semi-structured interviews with 16 large food and beverage companies in Australia (including 11 multinational corporations), aimed to identify the drivers and barriers to implementing sustainable development strategies in the food and beverage supply chain. Using institutional theory and the extended resource-based view (ERBV), the study indicates that commitment from senior leadership is the primary internal driver, while the lack of a legal framework and government environment is the biggest external barrier. Corporate culture factors, costs, and the lack of technical solutions were also identified as significant barriers. Notably, the study shows that materiality assessment plays an important role in identifying priority environmental–social issues, thereby building a strategy consistent with stakeholder expectations and local as well as international conditions. However, the results are contextual, limited to large companies operating in Australia, and have not yet analyzed the relative influence among the factors. Nevertheless, this study expands the theoretical framework of sustainable supply chain management (SSCM) and provides a foundation for both managers and policymakers to enhance the effective implementation of sustainable development initiatives in this high-impact environmental–social industry.

The study by Jihan, S., & Niken, K. (2024) assessed the relationship between SR disclosure and Enterprise Size with ROA of companies in the telecommunications, basic chemicals, and other industries on the Indonesia Stock Exchange for the period 2018-2022. With data from 15 companies over 5 years, multiple linear regression analysis showed that Enterprise Size has a significant positive impact on Return on Assets (ROA), reflecting the advantage of scale in Return on Assets. Conversely, SR disclosure had no significant impact, which is explained by limited environmental awareness and weak enforcement of waste management laws in Indonesia.

2.2. Studies on the Adoption of Sustainability Reporting in Vietnam

Tuan, L. A., et al. (2019) conducted a survey of 265 managers from the department head level and above at 60 companies under the Vietnam National Petroleum Group (Petrolimex) to assess the factors influencing SR disclosure. Using descriptive statistics, EFA, CFA, and SEM analysis methods, the results showed that factors such as Enterprise Size, business sector, Return on Assets, growth opportunities, and legal basis all have a positive impact on report disclosure. Conversely, the managerial perspective had no significant impact. The disclosure of sustainability information is seen as a tool to help businesses enhance their reputation, improve information transparency, and create favorable conditions in relationships with investors and regulatory agencies. However, in Vietnam, disclosure is still perfunctory due to the lack of detailed guidance and supervision from the State. The study is limited in scope to Petrolimex and does not fully reflect the entire industry, thus requiring an expanded sample and survey scope in future research for more comprehensive conclusions.

Luc, T. H. et al. (2019) surveyed 143 companies in the VNR500 group listed on the Vietnamese stock exchange in 2017 to analyze the factors influencing SR disclosure. The results showed that factors such as Enterprise Size, field of operation, and development opportunities have a positive impact on report disclosure, while ROA has no significant impact. Additionally, state-owned enterprises tend to disclose SR more than private enterprises. Disclosing the report not only helps to enhance reputation and information transparency but also supports businesses in internal control and brand strategy. However, the study is limited in terms of sample size and the number of research variables, so future research should expand the scope and use qualitative methods to better understand the drivers and barriers in SR disclosure at Vietnamese companies.

Phuong, B. M. (2021) conducted a study focusing on analyzing the factors influencing the disclosure of sustainability information of chemical companies listed on the Vietnamese stock exchange for the period 2017-2019. The results showed that four factors have a positive and statistically significant impact on the level of information disclosure: Enterprise Size, foreign ownership ratio, ROCE, and state ownership ratio. The study affirms the applicability of theories such as stakeholder theory, agency theory, ownership cost, and signaling theory. From there, the study makes recommendations to raise awareness and promote the disclosure of sustainability information, contributing to supporting investment decisions and the development of the stock market towards transparency and sustainability.

Nga, N. H. (2022) analyzed the quality of SR of 120 listed companies in Vietnam in 2020, through the role of third-party assurance and the GRI framework. The results showed that assurance from an independent service provider helps improve the reliability and effectiveness of the internal reporting system. The motivation comes from perceived benefits, proactivity from large companies, and pressure from stakeholders. The author also emphasized and proposed an 8-step model for implementing sustainable development according to Veleva & Ellenbecker (2001), while also recommending that businesses choose appropriate criteria to gradually build a quality and substantive report.

Nguyet, N. T. T. et al. (2023), based on legitimacy theory and stakeholder theory, analyzed the impact of pressure from stakeholders on the level of sustainability information disclosure of 142 large listed companies in Vietnam in 2020. Using content analysis techniques according to Circular 96/2020/TT-BTC, the results showed that the level of information disclosure is significantly influenced by consumers, employees, and parties interested in the environment. The study contributes to clarifying the role of corporate social responsibility and GRI standards in the Vietnamese context.

2.3. Foundational Theories for Building the Research Model

2.3.1. Stakeholder Theory

Stakeholder Theory was proposed by Freeman, R. E. (1984), emphasizing that a business does not exist solely to create value for shareholders, but must also consider the interests of other groups affected by its business operations – including employees, customers, the government, local communities, non-governmental organizations, suppliers, and other social organizations. According to this theory, SR disclosure is a form of response from the business to the pressures, expectations, or demands of stakeholders. Businesses have a responsibility to be transparent and provide information not only about finance but also about environmental, social, and governance (ESG) issues to maintain trust, support, and sustainability in their relationships with stakeholders.

In the wine-beer-soft drink industry, especially in Vietnam, businesses face increasing pressure from consumers who are conscious of protecting their health, medical organizations, the environment, and affected local communities. These stakeholders push businesses to be more transparent about social responsibility and environmental impacts. According to Deegan, C., & Blomquist, C. (2006), businesses heavily impacted by stakeholders will tend to be more proactive in disclosing SR as a way to maintain harmony with these interest groups.

2.3.2. Legitimacy Theory

Legitimacy Theory originates from the research of Dowling & Pfeffer (1975) and was further developed by Deegan, C. (2002). This theory suggests that businesses exist within a “social contract” – in which the behaviors and activities of the business need to be accepted by society. When there is a discrepancy between actual behavior and social expectations, the business may lose its “legitimacy.” To avoid this, they use information disclosure as a strategy to adjust public perception, maintain a positive image, and affirm their social standing. SR disclosure plays the role of an image management tool, helping the business respond to criticisms from society, alleviate concerns about ethics, the environment, and health. Particularly, in industries considered “harmful” or “sensitive,” information disclosure is a means for the business to reinforce its legitimacy. Wine, beer, and soft drink manufacturing businesses are often criticized by the public for issues related to public health, environmental pollution, consumption of water resources, and packaging waste. Faced with these pressures, businesses in this industry use SR as a “legitimization mechanism” to rebuild their image and affirm that they still operate responsibly. Cho, C. H., & Patten, D. M. (2007) also found that companies in socially sensitive industries tend to disclose more ESG information to protect their legitimate standing.

2.3.3. Signalling Theory

Signalling Theory was initiated by Spence, M. (1973) to explain the behavior of communicating information in the context of information asymmetry between parties (e.g., between a business and an investor). Accordingly, the party holding the information (the business) will send out reliable “signals” to reduce suspicion and build trust with the information-receiving party (investors, the public, regulatory agencies). A business’s proactive disclosure of SR is seen as a signal that they have good governance capacity, high ethical commitment, a long-term strategy, and are willing to be transparent. This not only helps enhance reputation but also creates a competitive advantage in attracting investment, retaining customers, and accessing preferential capital sources. In the wine-beer-soft drink industry, where brand competition is fierce and corporate image plays a vital role – SR becomes an important signal to demonstrate differentiation and affirm value. Businesses with high-quality disclosure, as noted by Michelon, G., Pilonato, S., & Ricceri, F. (2015), often leverage the report as a strategic communication tool to strengthen trust from shareholders and relevant financial stakeholders.

2.3.4. Institutional Theory

Institutional Theory, developed by DiMaggio, P. J., & Powell, W. W. (1983), posits that a business’s behavior is influenced by institutional factors in its operating environment, including: Coercive pressure: from laws, policies, regulations; Mimetic pressure: from imitating successful competitors; Normative pressure: from professional ethics, industry standards, and social expectations. Under institutional pressure, businesses tend to comply with behaviors considered appropriate by society and the market, including ESG information disclosure. Disclosure is not only for compliance but also helps the business maintain stability and position within the industry. In Vietnam, although SR is not yet a mandatory requirement, regulations such as Circular 96/2020/TT-BTC, guidance from the State Securities Commission, and global trends from international investors are creating increasing institutional pressure on listed companies, especially in the wine-beer industry – which is highly scrutinized by medical and environmental organizations. Therefore, a business may implement SR disclosure as an adaptive behavior to institutional requirements to maintain competitiveness and avoid legal and reputational risks (Bansal, P., 2005; Campbell, J. L., 2007).

2.3.5. Resource-Based Theory (RBV)

Resource-based theory (RBV), developed by Barney JB. (1991), suggests that a firm’s sustainable competitive advantage comes from possessing and effectively exploiting internal resources that are valuable, rare, inimitable, and non-substitutable. In the context of increasing pressure from stakeholders such as investors, customers, regulatory bodies, and society, the adoption of SR is not just a communication tool but also a manifestation of a firm’s internal capabilities and long-term strategic orientation. For firms in the wine, beer, and soft drink industry—a sector with a high level of environmental and social impact—the implementation of SR can reflect sustainable governance capabilities, the ability to integrate social responsibility into business operations, as well as the level of investment in resources like green technology, clean production processes, and the capacity of the team managing social responsibility of a firm (Corporate Social Responsibility).

According to RBV, internal factors such as Enterprise Size, financial capacity, quality of management, level of awareness of sustainable development, and the accounting information system are key resources that determine the level and quality of SR adoption. Large firms with strong financial potential often have more resources to invest in non-financial reporting activities, hire experts, and build ESG data collection systems.

WBDCs also face the demand for information transparency and improving their corporate image before the public. Therefore, adopting SR is not only a response to external pressure but also a strategy to effectively use internal resources to create a sustainable competitive advantage.

3. Methodology

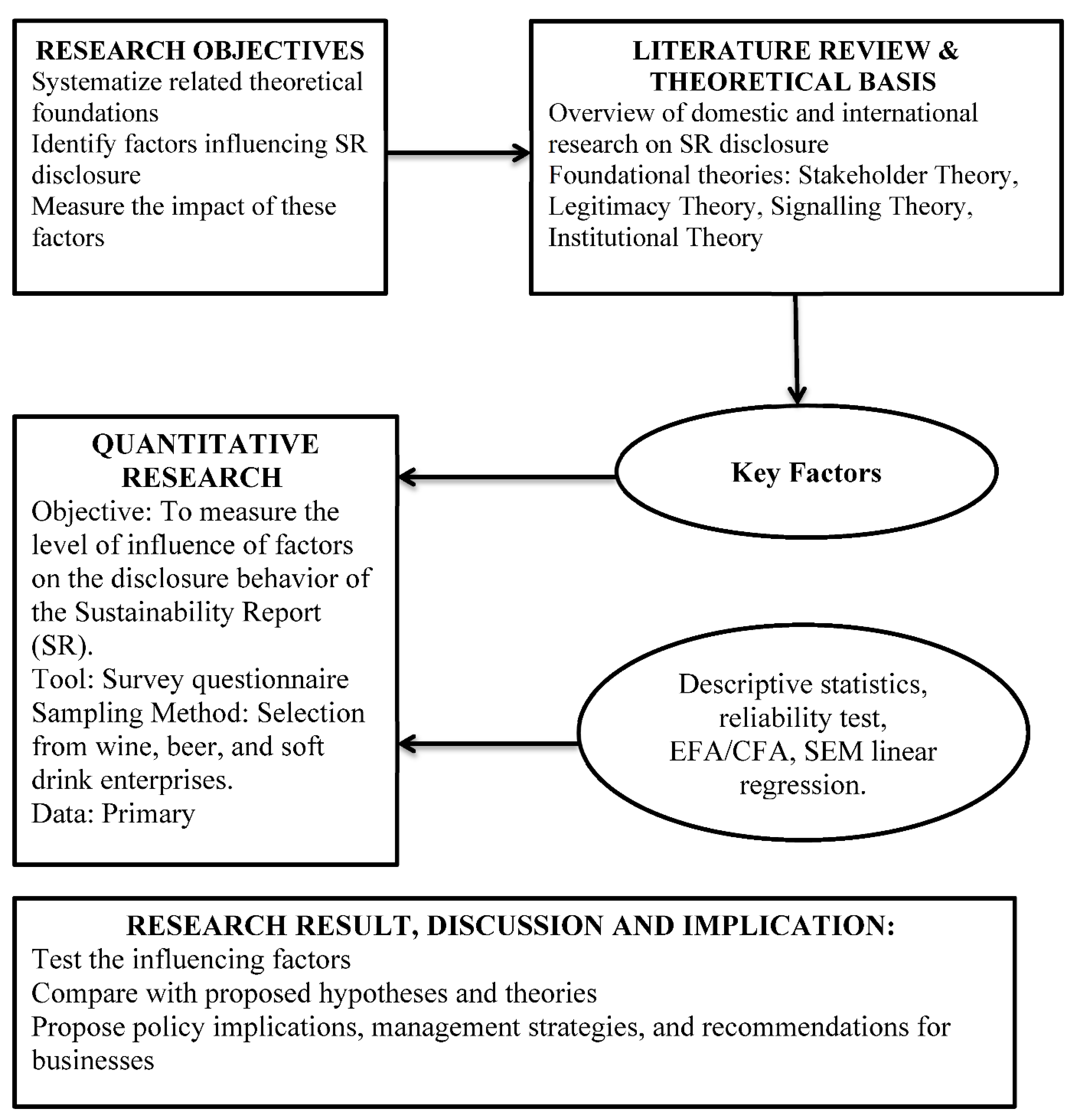

3.1. Research Process

The research process is depicted in Figure 1.

3.2. Questionnaire Design

3.2.1. Research Hypotheses

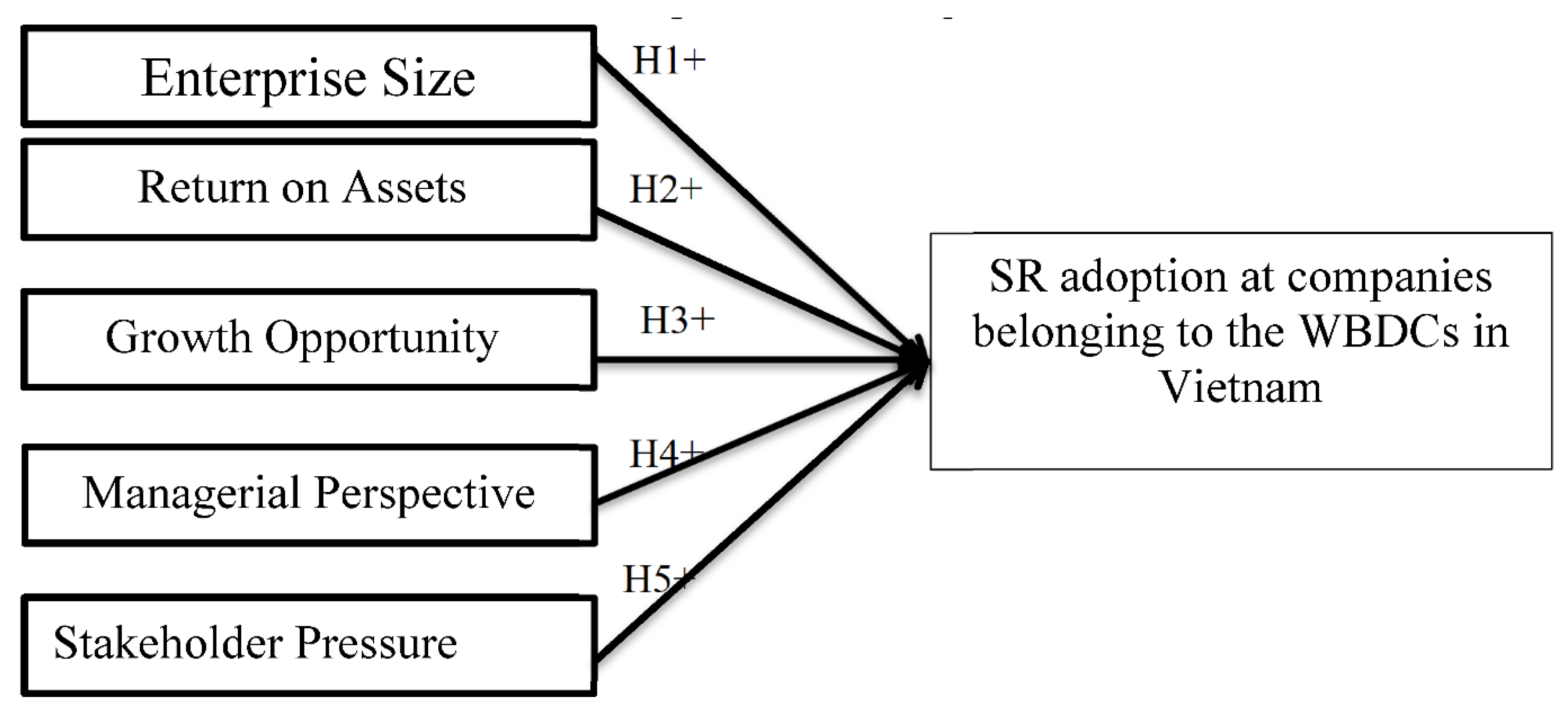

Based on Stakeholder Theory, Legitimacy Theory, Signalling Theory, and Institutional Theory, RBV, along with a review of empirical research both domestically and internationally, this study proposes a model to test the factors influencing the adoption of SR at WBDCs in Vietnam. The hypotheses are built around five main factors: Enterprise Size, Return on Assets, growth opportunities, managerial perspective, and pressure from stakeholders.

H1⁺: Enterprise Size has a positive influence on the adoption of SR.

According to RBV, a firm with a large size often possesses strong financial, human, and technological resources to meet the requirements of preparing an SR, which is a process that demands significant investment (Jaggi, B., & Low, P. Y., 2000). Additionally, large firms also face higher pressure from the public and stakeholders regarding transparency and social responsibility (Amran, A. et al, 2008). Therefore, hypothesis H1+ is set to test the positive relationship between Enterprise Size and the level of SR adoption.

H2+: Return on Assets has a positive influence on the adoption of SR.

Research by Cormier, D., & Magnan, M. (2003) shows that highly profitable firms often have stronger motivation to disclose non-financial information like SR, aiming to enhance brand image and affirm social responsibility. Return on Assets also reflects governance efficiency and the willingness to invest in non-financial activities. Therefore, H2+ hypothesizes that the higher the Return on Assets, the higher the likelihood of adopting SR.

H3+: Growth opportunities have a positive influence on the adoption of SR.

Firms with good growth prospects often aim to build a sustainable corporate image, attract investment capital, and maintain a competitive position. Kent, P., & Monem, R. (2008) and Hahn, R., & Kühnen, M. (2013) both emphasize that during expansion phases, firms often view SR disclosure as a strategy to enhance brand value and credibility with stakeholders. Therefore, H3+ is constructed to determine the role of growth opportunities in the decision to disclose SR.

H4+: Managerial perspective has a positive influence on the adoption of SR.

The perspective and strategic orientation of the leadership team are internal factors that decisively influence the implementation of sustainable development policies. Herremans, I. M. et al. (1993) point out that the awareness and commitment of managers have a direct impact on the level and quality of sustainability information disclosure. Similarly, Michelon, G. (2011) affirms the role of the executive in integrating social responsibility into the corporate culture. Therefore, H4+ assumes that a positive managerial perspective will promote the adoption of SR.

H5⁺: Pressure from stakeholders has a positive influence on the adoption of SR.

Stakeholder Theory suggests that a firm must respond to the expectations and pressures of interest groups such as investors, customers, regulatory agencies, and the community (Freeman, R. E., 1984). In the wine, beer, and soft drink industry – which is under high social scrutiny due to its impact on public health and the environment – pressure from stakeholders becomes even more pronounced. Deegan, C. (2002) emphasizes that stakeholders play a crucial role in shaping the behavior of disclosing sustainability information of a firm. Therefore, hypothesis H5+ is proposed to test the role of external pressure in promoting SR practices.

3.2.2. Research Model

The official research model is presented in Figure 2.

3.2.3. Official Measurement Scale

The official measurement scale is presented in Table 1.

3.2.4. Data Collection Method

To test the research hypotheses, the author team conducted a quantitative survey through a structured questionnaire, designed based on foundational theories and previous studies. The survey subjects were managers from the department level upwards at companies operating in the wine, beer, and soft drink sector.

The sample size was determined by the ratio between the number of observed variables and the number of survey samples, with a minimum ratio of 5:1 as proposed by Bollen (1989). With a research model consisting of 23 observed variables across 6 latent variables, the minimum required sample size was 115. However, the research team distributed 300 questionnaires at more than 60 companies in the industry, receiving 275 responses, of which 250 were valid and included in the analysis. Ensuring a larger sample size than required helps increase the reliability and generalizability of the results.

The measurement scale used in the questionnaire is a 5-point Likert scale (1: Strongly disagree; 5: Strongly agree). The content of the questionnaire was developed and adjusted through three stages: (1) consulting previous research, (2) interviewing 10 experts in the fields of accounting, corporate governance, and sustainable development, and (3) pilot testing the questionnaire at some companies in the industry to adjust the wording and structure to fit the Vietnamese context.

3.2.5. Data Analysis Method

The collected data was processed using SPSS 26 and AMOS 24 software. The analysis steps include:

1. Descriptive statistics to identify sample characteristics and check the preliminary distribution of the data.

2. Assessing the reliability of the measurement scale through Cronbach’s Alpha, with an acceptance threshold of ≥ 0.7 according to Hair et al. (2010). Variables with a low corrected item-total correlation (< 0.3) will be removed.

3. Exploratory Factor Analysis (EFA) using the Principal Axis Factoring method with Varimax rotation to determine the structure of the latent factors, ensuring a factor loading value ≥ 0.5 and a total explained variance ≥ 50%.

4. Confirmatory Factor Analysis (CFA) to test the goodness of fit of the measurement model, through indicators such as: Chi-square/df < 3, CFI > 0.90, TLI > 0.90, RMSEA < 0.08.

5. Finally, the research model is tested using Structural Equation Modeling (SEM) to determine the relationships between variables and test the proposed hypotheses.

The use of SEM with empirical data from the wine, beer, and soft drink industry – a sector subject to much debate in the context of sustainable development – helps provide valuable empirical evidence, contributing to both the theory and practice of the SR field in Vietnam.

4. Results and Discussions

4.1. Quantitative Research Results

4.1.1. Descriptive Statistics

The descriptive statistics are presented in Table 2.

From the table above, it can be seen that the mean values of the observed variables are all within the range of (3.37; 3.90). This demonstrates that the research sample is representative of the population.

4.1.2. Cronbach’s Alpha Reliability Test

The item-total correlation and Cronbach’s Alpha are presented in Table 3.

According to Table 3, all scales have a Cronbach’s Alpha Coefficient > 0.7. The item-total correlation coefficients are all greater than 0.3 and are suitable for these scales. Thus, it can be assessed that these are good measurement scales, suitable for conducting exploratory factor analysis (EFA).

4.1.3. Exploratory Factor Analysis (EFA)

Exploratory Factor Analysis (EFA) for independent variables

The KMO and Bartlett’s test for the independent variables are shown in Table 4.

The test results in Table 4 show that the Kaiser-Meyer-Olkin (KMO) index reaches a value of 0.879, higher than the recommended minimum of 0.5, indicating that the data sample is suitable for performing exploratory factor analysis (EFA). According to Kaiser’s (1974) standard, a KMO level from 0.8 to 0.9 is considered “very good,” reflecting that the correlation level among the observed variables is sufficiently high to extract latent factors.

Furthermore, Bartlett’s Test of Sphericity has a Chi-Square value (Approx. Chi-Square) = 1471.190, with degrees of freedom (df) = 171 and Sig. < 0.001, proving that the correlation matrix among the variables is significantly different from an identity matrix. This confirms that the observed variables have a sufficiently strong linear relationship to proceed with factor analysis.

During the exploratory factor analysis (EFA) process, the independent variable “Growth Opportunity” did not meet the necessary criteria to be retained in the model. Specifically, this variable had a factor loading lower than the permissible threshold (0.5) and did not converge clearly with any factor group, affecting the convergence and discrimination of the scale. Therefore, this variable was removed from the analysis process to ensure the appropriateness and reliability of the model.

The total variance explained is presented in Table 5.

According to Table 5, the EFA results show that 4 factor groups were extracted with 16 observed variables. The total variance explained by these 4 groups is 58.896%, indicating that the extracted factors explain 58.896% of the data’s variance.

We have the rotated factor matrix in Table 6 as follows:

The results of the rotated factor analysis show that the observed variables have converged into 4 factor groups, corresponding to the independent variables in the research model.

Exploratory Factor Analysis (EFA) for the dependent variable

The KMO and Bartlett’s test for the dependent variable are presented in Table 7.

Through analysis using SPSS, the KMO test result = 0.830 > 0.5 meets the requirement for conducting EFA and factor analysis suitable for the research data. The Bartlett’s test result: Sig < 0.001 < 0.05 shows that the variables are correlated with each other in the overall population, so EFA can be performed.

The EFA results show that there is 1 factor group extracted with 4 observed variables. We have the component matrix in Table 8 as follows:

Based on the component matrix results, the dependent factor “Adoption of SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam (AD)” is measured by 4 observed variables (AD1, AD2, AD3, AD4). These observed variables all have high factor loadings, ranging from 0.853 to 0.879, ensuring the necessary convergent validity according to the standard (factor loading ≥ 0.5).

The component matrix results confirm that the scale designed to measure the dependent factor “Adoption of SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam (AD)” has high reliability and is suitable for the empirical data.

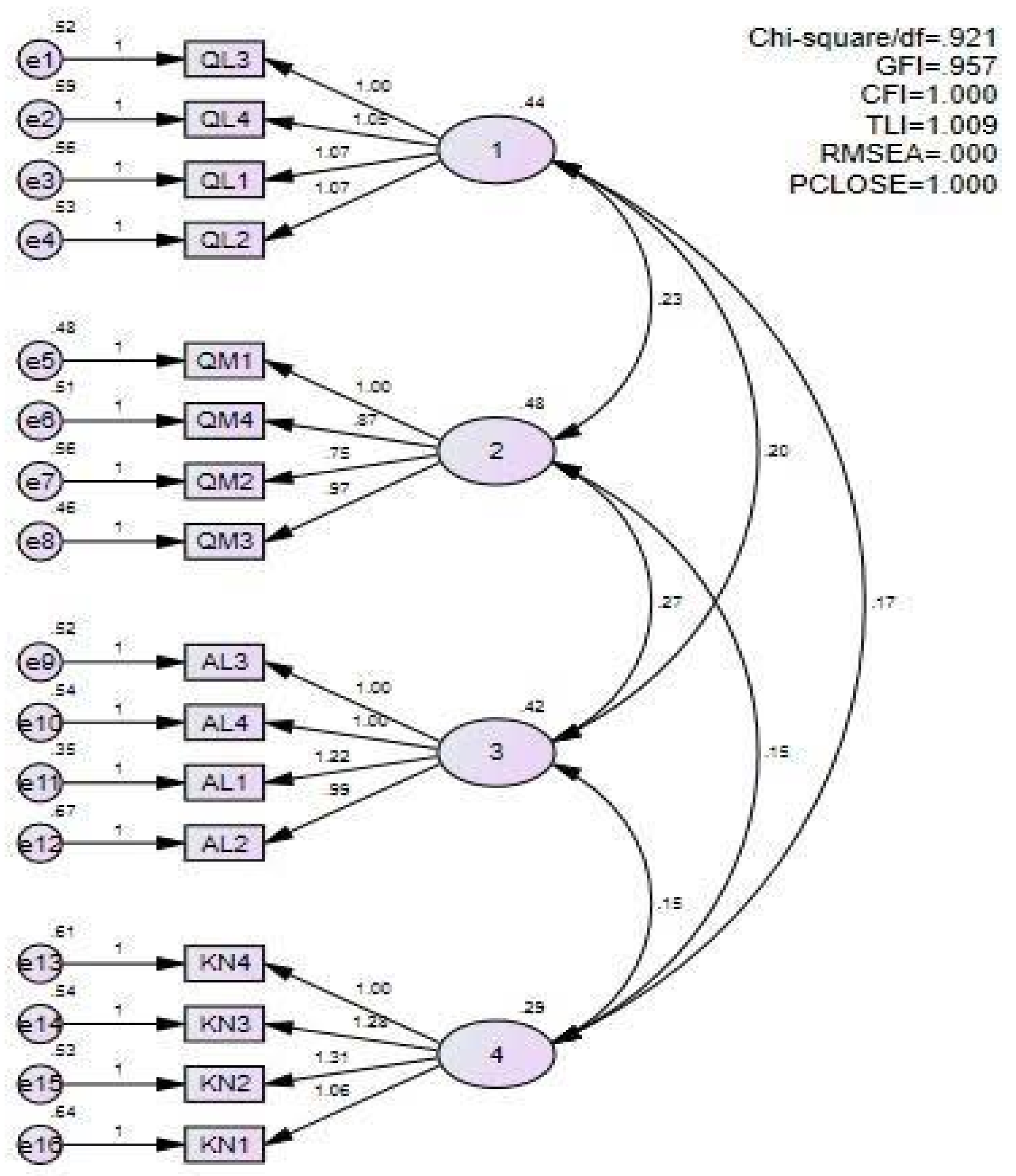

4.1.4. Confirmatory Factor Analysis (CFA)

*Overall goodness-of-fit assessment of the data. The CFA diagram is shown in

Figure 3.

Common criteria used to evaluate Model Fit include:

+ CMIN/df = 1.145 ≤ 3

+ CFI = 0.934 ≥ 0,9

+ GFI = 0.987 ≥ 0,8

+ TLI = 0.985 ≥ 0,9

+ RMSEA = 0.024 ≤ 0.06

+ PCLOSE = 0.999 ≥ 0.05

All the above indicators meet the permissible conditions, showing that the model has a good fit with the market data.

*Assessment of convergent validity and discriminant validity is presented in Table 9:

Convergent validity: The CR index of the factors are all greater than 0.7, the AVE index are all greater than 0.5, both indicators meet the assessment threshold, the convergent validity meets the condition very strongly.

+ Discriminant validity: All factors have an MSV index that is smaller than AVE, if it is guaranteed to be smaller, then discriminant validity is ensured. The square root of AVE of a variable (the bolded value at the beginning of each column following the arrow in the Fornell and Larcker table) is greater than the correlation between that variable and other variables in the model, thus discriminant validity will be ensured.

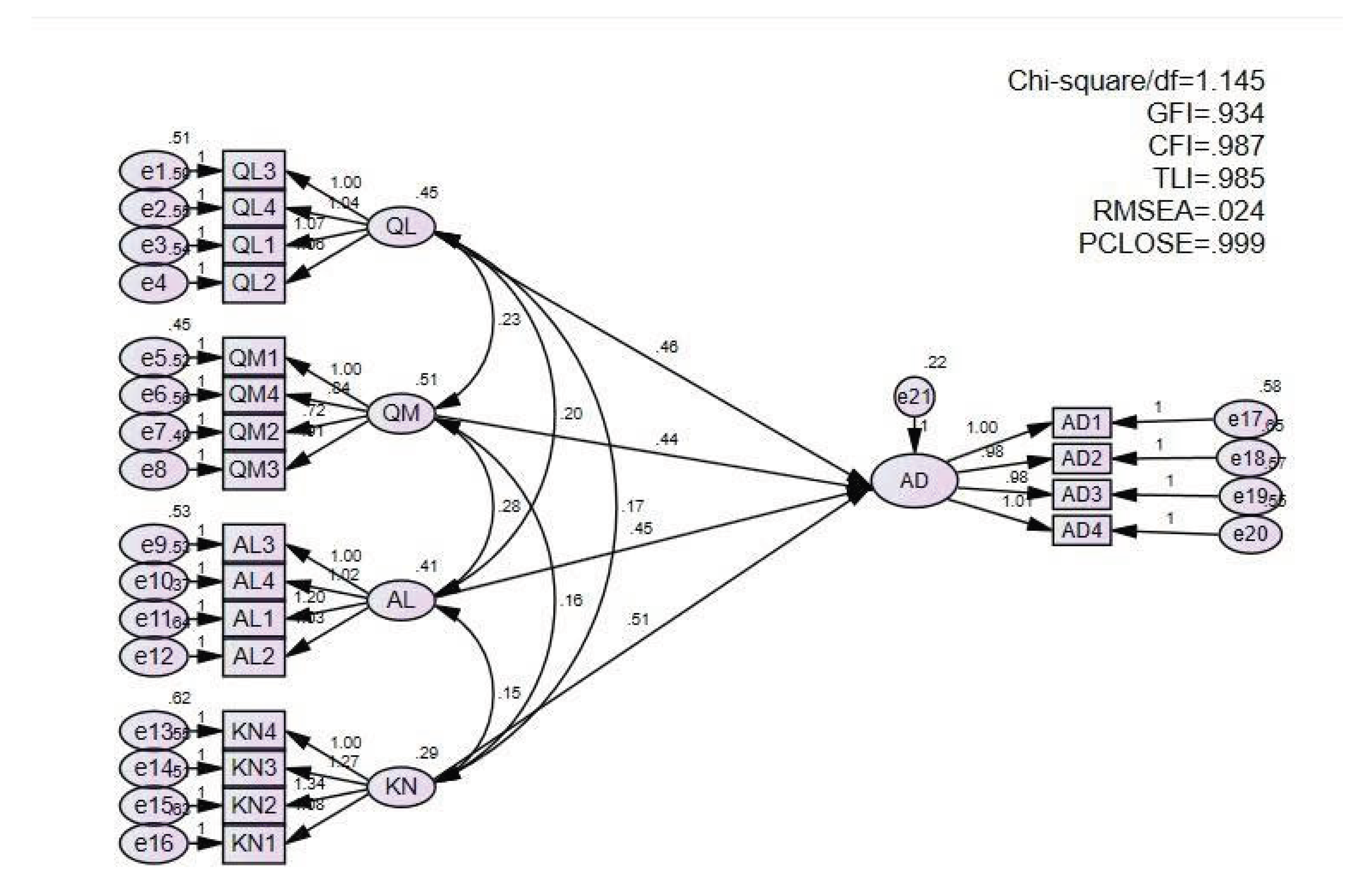

4.1.5. SEM Analysis

The research model of factors affecting the adoption of SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam yields the results as shown in Figure 4.

The commonly used indicators to assess the overall goodness of fit of the model include:

+ CMIN/df = 1.145 ≤ 3

+ CFI = 0.987 ≥ 0.9

+ GFI = 0.934 ≥ 0.8

+ TLI = 0.985 ≥ 0.9

+ RMSEA = 0.024 ≤ 0.06

+ PCLOSE = 0.999 ≥ 0.05

All the above indicators meet the permissible conditions, showing that the model has a good fit with the market data.

The results obtained are shown in Table 10.

In Table 10, with a 95% confidence level, the P-value of the 4 factors “Enterprise Size”, “Return on Assets”, “Stakeholder pressure”, “Managerial perspective” are all less than 0.05, so all 4 factors affect the adoption of SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam.

The variables QM, KN, AL, QL have a Beta coefficient > 0, proving that these 4 independent variables in the model have a positive impact on the dependent variable, i.e., the factors “Enterprise Size”, “Growth opportunity”, “Industry characteristics”, “Benefits of adopting the sustainability report”, “Stakeholder pressure”, “Managerial perspective” all have a positive impact on the ability to adopt the SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam. Thus, the research model proposed by the author is appropriate and meaningful.

Standardized regression weights – Sem are presented in Table 11.

Table 11 shows the standardized regression coefficients, indicating the level of impact of the factors on the adoption of SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam. The level of influence of the factors on the ability to adopt the SR at listed Wine, Beer, and Soft Drink Enterprises in Vietnam: the QM factor has the strongest impact on AD (Beta = 0.301), the next strongest impact is QL (Beta = 0.297), followed by the AL factor (Beta = 0.274), and the KN factor has the weakest impact among the 4 factors (Beta = 0.263).

The coefficient of determination – SEM is presented in Table 12.

The R² of the dependent variable is 0.800, meaning the 4 factors “Enterprise Size”, “Stakeholder pressure”, “Managerial perspective” explain 80% of the variance.

5. Discussion and Implications

5.1. Discussion

The results of the structural equation modeling (SEM) analysis show that the research model has a high degree of fit with the collected data. The factors included in the model are: “Enterprise Size” (QM), “Managerial perspective” (QL), “Stakeholder pressure” (AL), and “Return on Assets” (KN), all of which have a positive and statistically significant influence on the adoption of SR at listed enterprises in the wine, beer, and soft drink industry in Vietnam.

Among the factors, “Enterprise Size” (QM) is the factor with the strongest influence on the level of SR adoption, with an estimate coefficient of 0.301. This reflects that large-scale enterprises often have better financial and human resources, making it easier to invest in the SR system. A large size also means a higher level of attention from the market and stakeholders, requiring the enterprise to be more transparent and responsible in its reporting activities.

Next is the “Managerial perspective” (QL) factor, with an estimate coefficient of 0.297, showing the central role of the leadership in promoting the sustainable development strategy. Managers with a high awareness of the importance of SR will be willing to allocate resources and guide the organization to seriously implement the reporting content, thereby enhancing transparency, reliability, and the enterprise’s image before investors, customers, and society.

The “Stakeholder pressure” (AL) factor also shows a positive influence with a coefficient of 0.279. Under pressure from shareholders, regulatory agencies, customers, and the community, enterprises are forced to seriously consider disclosing information about their environmental, social, and governance (ESG) activities to meet the expectations of stakeholders, maintain reputation, and ensure competitive advantage.

Finally, “Return on Assets” (KN) also affects the adoption of SR with a coefficient of 0.263. A profitable enterprise will have the conditions to invest more in the reporting system and activities related to sustainable development. At the same time, stable financial performance is also the basis for the enterprise to show a long-term commitment to social and environmental responsibility.

Thus, the model not only shows a close relationship between internal factors and the adoption of SR but also suggests a direction for enterprises in prioritizing the development of scale and strengthening the role of management as key drivers to promote sustainability in business operations.

5.2. Implications

5.2.1. For the Enterprise Size Factor

The research results show that Enterprise Size is the factor with the strongest influence on the adoption of SR in the wine, beer, and soft drink industry. Large-scale enterprises often possess more abundant financial and human resources, helping them easily build and maintain a systematic sustainability reporting system. At the same time, a large size also comes with closer scrutiny from investors, regulatory agencies, and the public, making information disclosure an mandatory requirement to maintain reputation and enhance brand value. Therefore, large enterprises in the industry should leverage their leading role by investing in technology, training specialized human resources, and applying international reporting standards to enhance transparency and the effectiveness of information disclosure. Conversely, small and medium-sized enterprises also need to proactively approach the SR model with a suitable scale, gradually integrating it into their long-term development strategy to increase their competitive value in the market.

5.2.2. For the Managerial Perspective Factor

The managerial perspective plays a central role in shaping and promoting sustainable development policies within an enterprise. Especially in the wine, beer, and soft drink industry – which often faces high social scrutiny due to issues related to public health and the environment – the guiding role of leadership becomes even more important. When senior management has full awareness and a clear commitment to sustainable development goals, they will lead the entire operating system in a responsible direction. Therefore, enterprises need to implement in-depth training programs, integrating sustainable development goals into performance evaluation criteria for management, thereby turning the sustainable development strategy into an inseparable part of the long-term growth orientation.

5.2.3. For the Return on Assets Factor

Return on Assets is a key factor influencing the ability to implement activities related to sustainable development. Enterprises with high business efficiency often have the conditions to invest in reporting systems, technology, and training personnel to serve the disclosure of sustainability information. In the wine, beer, and soft drink industry – which is a highly competitive sector and under great pressure regarding social responsibility – good Return on Assets helps the enterprise consolidate its position and enhance its dialogue capacity with stakeholders. When it is recognized that sustainable development is not just a cost but also an opportunity to create long-term value, enterprises will proactively integrate financial and non-financial information to affirm an effective and responsible growth strategy.

5.2.4. For the Stakeholder Pressure Factor

Although it is not the factor with the strongest influence, pressure from stakeholders such as shareholders, customers, regulatory agencies, and the community still plays a role that cannot be underestimated in promoting enterprises to adopt SR. Especially in the wine, beer, and soft drink industry – where products have a direct impact on health and society – the demand for transparency and responsibility is becoming increasingly clear. Enterprises need to proactively build a two-way interaction mechanism with stakeholders, through effective communication channels, timely information disclosure, and receiving transparent feedback. This not only helps the enterprise strengthen trust from the market but also creates conditions for stakeholders to become partners in the journey of sustainable development.

6. Conclusions

This study has shed light on the factors influencing the adoption of SR in the wine, beer, and soft drink industry in Vietnam through a quantitative method. The results show that, except for the Growth Opportunity factor, 4 factors: Enterprise Size, managerial perspective, Return on Assets, and stakeholder pressure all have a positive and statistically significant influence on the level of SR adoption.

In particular, Enterprise Size is identified as the factor with the strongest influence, showing the key role of resources and the level of transparency that an enterprise must meet in the context of increasing scrutiny. The managerial perspective plays a central role in promoting the sustainable development strategy, reflecting the decisive role of awareness and internal commitment. Return on Assets and pressure from stakeholders, although having a lower level of impact, still contribute significantly to shaping the information disclosure behavior of the enterprise.

The research model achieves a good fit with the empirical data, explaining 80% of the variance in the behavior of adopting SR, indicating high value and applicability. On that basis, the study not only provides empirical evidence to serve public policy and corporate governance planning but also contributes to supplementing the theoretical basis for theories of sustainable development, in the specific context of an industry and a developing country like Vietnam.

From the research results, the author team recommends that enterprises in the industry should proactively integrate sustainable development into their core business strategy, with a special emphasis on the role of leadership, financial capacity, and the mechanism for dialogue with stakeholders. At the same time, policymakers should improve the legal framework, issue specific guidance on the content and standards of SR, and create conditions to promote the legitimacy, transparency, and efficiency of this activity throughout the industry.

References

- Ministry of Finance. Circular No. 96/2020/TT-BTC dated November 16, 2020, guiding information disclosure on the stock market . 2020. Available online: https://thuvienphapluat.vn/van-ban/chung-khoan/Thong-tu-96-2020-TT-BTC-cong-bo-thong-tin-tren-thi-truong-chung-khoan-457442.aspx.

- Hung, D. N.; Diep, P. T. H.; Dung, T. T.; Cuong, D. V. Factors affecting the level of disclosure of social responsibility and sustainable development information of listed enterprises in Vietnam. In Workshop on Research and Training in Accounting and Auditing; (In Vietnamese). 2018. [Google Scholar]

- Nga, N. H. The quality of sustainability reports of listed enterprises in Vietnam. Journal of Science & Banking Training (In Vietnamese). 2022. [Google Scholar]

- Nguyet, N. T. T.; Hai, T. T. T. The influence of stakeholder pressure on the level of sustainability information disclosure. Journal of Accounting & Auditing (In Vietnamese). 2023. [Google Scholar]

- Luc, T. H.; Phuoc, T. T. Factors affecting the sustainability information disclosure of listed enterprises in Vietnam. In Ho Chi Minh City Open University Journal of Science; (In Vietnamese). 2019. [Google Scholar]

- Phuong, B. M. Factors affecting the sustainability information disclosure of listed chemical enterprises in Vietnam. Journal of Accounting & Auditing (In Vietnamese). 2021. [Google Scholar]

- Quyen, P. T. T.; Huyen, T. T. M.; Nhi, T. T. P. The quality of sustainability reports of Vietnamese enterprises. Dong A University Journal of Science (In Vietnamese). 2019, 3. [Google Scholar]

- Tuan, L. A.; Tuyen, N. V.; Huong, P. T. T. A study of factors affecting the sustainability report disclosure at enterprises belonging to Petrolimex. In Economics and Forecast Review; (In Vietnamese). 2019. [Google Scholar]

- Adams, D.; Hines, F.; Munday, M. Sustainability in large food and beverage companies and their supply chains: An investigation into key drivers and barriers affecting sustainability strategies. Journal of Business Strategy and the Environmeny 2022, 8(2), 123–145. [Google Scholar] [CrossRef]

- Alicia, G.; Amirreza, K.; Antonella, F.C. Sustainability Reporting and Firms’ Economic Performance: Evidence from Asia and Africa. Journal of the knowledge economy (2021) 2020, 12, 1741–1759. [Google Scholar] [CrossRef]

- Amran, A.; Susela, S.D. The impact of goverrnment and foreign affiliate influence on corporate social reporting: The case of Malaysia. Managerial Auditing Journal 2008, 386–404. [Google Scholar] [CrossRef]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strategic Management Journal 2005, 26(3), 197–218. [Google Scholar] [CrossRef]

- Barney, JB. Resources and Sustained Competitive Advantage. Journal of Management 1991, P 99–120. [Google Scholar] [CrossRef]

- Campbell, J. L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Academy of Management Review 2007, 32(3), 946–967. [Google Scholar] [CrossRef]

- Cho, C. H.; Patten, D. M. The role of environmental disclosures as tools of legitimacy: A research note. Accounting, Organizations and Society 2007, 32(7–8), 639–647. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. Environmental reporting management: A continental European perspective. Journal of Accounting and Public Policy 2003, 22(1), 43–62. [Google Scholar] [CrossRef]

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures – a theoretical foundation. Accounting, Auditing & Accountability Journal 2002, 15(3), 282–311. [Google Scholar] [CrossRef]

- Deegan, C.; Blomquist, C. Stakeholder influence on corporate reporting: An exploration of the interaction between WWF-Australia and the Australian minerals industry. Accounting, Organizations and Society 2006, 31(4–5), 343–372. [Google Scholar] [CrossRef]

- DiMaggio, P. J.; Powell, W. W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review 1983, 48(2), 147–160. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational legitimacy: Social values and organizational behavior. Pacific Sociological Review 1975, 18(1), 122–136. [Google Scholar] [CrossRef]

- Fathi, W. Corporate social responsibility disclosure and firm performance: The role of corporate governance. International Journal of Accounting and Financial Reporting 2013, 3(2), 221–241. [Google Scholar]

- Fernandez – Feijoo, B.; Silvia., R.; Silvia, R.B. Effect of Stakeholders’ Pressure on Transparency of Sustainability Reports within the GRI Framework. Journal of Business Ethics 2013, 122. [Google Scholar] [CrossRef]

- Freeman, R. E. Strategic management: A stakeholder approach; Pitman: Boston, 1984. [Google Scholar]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production 59 2013, 5–21. [Google Scholar] [CrossRef]

- Herremans, I. M.; Akathaporn, P.; McInnes, M. An investigation of corporate social responsibility reputation and economic performance. Accounting, Organizations and Society 1993, 18(7–8), 587–604. [Google Scholar] [CrossRef]

- Iranmanesh, M.; Foroughi, B.; Hyun, S. S. Determinants of sustainable reporting quality: Evidence from the financial sector. Sustainability 2019, 11(9), 2464. [Google Scholar] [CrossRef]

- Jaggi, B.; Low, P. Y. Impact of culture, market forces, and legal system on financial disclosures. International Journal of Accounting 2000, 35(4), 495–519. [Google Scholar] [CrossRef]

- Jihan, S.; Niken, K. Effect of Sustainability Report Disclosure and Company Size on Company Performance. Journal of Business Management and Economic Development 2024, Volume 2(Issue 03), Pp. 1354–1362. [Google Scholar] [CrossRef]

- Kent, P.; Monem, R. What drives TBL reporting: Good governance or threat to legitimacy? Australian Accounting Review 2008, 18(4), 297–309. [Google Scholar] [CrossRef]

- Kilic, M.; Uyar, A.; Ataman, B. Preparedness of companies for sustainability reporting: An analysis of Turkish firms. Sustainability 2017, 9(10), 1839. [Google Scholar] [CrossRef]

- Michelon, G. Sustainability disclosure and reputation: A comparative study. Corporate Reputation Review 2011, 14(2), 79–96. [Google Scholar] [CrossRef]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Critical Perspectives on Accounting 33 2015, 59–78. [Google Scholar] [CrossRef]

- Sebrina, N.; Salma, T.; Mayar, A.; Dovi, S. Analysis of sustaninability reporting quality and corporate social responbility on companies listed on the Indonesia stock exchange. Cogent business & management (2023) 2022, 10, 2157975. [Google Scholar] [CrossRef]

- Spence, M. Job market signaling. Quarterly Journal of Economics 1973, 87(3), 355–374. [Google Scholar] [CrossRef]

- Tauringana, V. Exploring the determinants of sustainability reporting in developing countries: The role of managerial perception. Journal of Accounting in Emerging Economies 2020, 10(2), 193–215. [Google Scholar]

Figure 1.

Research Process

(Source: Compiled by the author).

Figure 2.

Official Research Model.

Figure 3.

CFA Diagram.

(Source: Calculation results from AMOS software).

Figure 4.

SEM Model

(Source: Calculation results from AMOS software).

Table 1.

Official Measurement Scale.

| Scale | Measurement Item | Code | Source |

|---|---|---|---|

| Enterprise Size | Large labor force influences SR adoption | QM1 | Tuan, L. A., et al. (2019) |

| Market capitalization influences SR adoption | QM2 | Tuan, L. A., et al. (2019) | |

| Natural logarithm of total assets influences SR adoption | QM3 | Phuong, B. M. (2021) | |

| A large firm needs to disclose more information | QM4 | Fathi, W. (2013) | |

| Return on Assets | Return on Equity (ROE) helps the firm invest in SD activities | KN1 | Tuan, L. A., et al. (2019), Dang Ngoc X et al. (2018) |

| An efficiently operating firm will proactively disclose more information | KN2 | Alicia, G., Amirreza, K., Antonella, F.C,. (2020), Kilic, M., Uyar, A., & Ataman, B.(2017) | |

| A firm proactively adopts SR to enhance brand reputation in the future | KN3 | Tuan, L. A., et al. (2019) | |

| Increase in total assets when disclosing SR | KN4 | ||

| Growth Opportunity | The firm has a long-term strategy and SD orientation | CH1 | Hung, D. N., et al (2018) |

| Adopting SR helps the firm find new opportunities in the market | CH2 | Luc, T. H. et al. (2019) | |

| Adopting SR enhances transparency, helping to improve image in the eyes of investors and consumers | CH3 | Tuan, L. A., et al. (2019) | |

| Managerial Perspective | The manager avoids conflicts of interest with investors | QL1 | Tuan, L. A., et al. (2019) |

| The manager voluntarily discloses transparent information | QL2 | ||

| The manager has knowledge about SR | QL3 | ||

| Not subject to influence from superiors | QL4 | ||

| Stakeholder Pressure | Firms in environmentally sensitive industries disclose more SD information than those not in sensitive industries | AL1 | Nguyet, N. T. T. et al. (2023) |

| The firm is known by consumers for disclosing more SD information | AL2 | Femandez-Feijoo et al, 2014 |

|

| The firm faces high pressure from investors to disclose more SD information | AL3 | Nguyet, N. T. T. et al. (2023) | |

| The firm has foreign investment and discloses more SD information | AL4 | Phuong, B. M. (2021), Nguyet, N. T. T. et al. (2023) | |

| Adoption of SR at WBDCs in Vietnam (AD) | Method of disclosing report information | AD1 | Quyen, P. T. T., et al. (2024), Chang et al. (2019) |

| Application of GRI standards when preparing the report | AD2 | Quyen, P. T. T., et al. (2019), Sebrina, N., et al. (2022) | |

| Information in the report is reliable, presented truthfully (audited by an independent auditor) | AD3 | Nga, N. H. (2022) | |

| Timely issuance of SR | AD4 | Quyen, P. T. T., et al. (2019) |

(Source: Compiled by the author).

Table 2.

Descriptive Statistics of the Research Sample.

| Analysis Variable | Component | Indicator | Mean |

|---|---|---|---|

| Factors influencing the adoption of the SR at listed wine-beer-soft drink enterprises in Vietnam | Enterprise Size (QM) | QM1 | 3.77 |

| QM2 | 3.72 | ||

| QM3 | 3.81 | ||

| QM4 | 3.76 | ||

| Return on Assets (KN) | KN1 | 3.64 | |

| KN2 | 3.62 | ||

| KN3 | 3.52 | ||

| KN4 | 3.68 | ||

| Growth Opportunity (CH) | CH1 | 3.70 | |

| CH2 | 3.54 | ||

| CH3 | 3.77 | ||

| Managerial Perspective (QL) | QL1 | 3.47 | |

| QL2 | 3.44 | ||

| QL3 | 3.59 | ||

| QL4 | 3.37 | ||

| Stakeholder Pressure (AL) | AL1 | 3.81 | |

| AL2 | 3.74 | ||

| AL3 | 3.90 | ||

| AL4 | 3.70 | ||

| Adoption Capability | Adoption of SR at WBDCs in Vietnam (AD) | AD1 | 3.55 |

| AD2 | 3.59 | ||

| AD3 | 3.62 | ||

| AD4 | 3.68 |

(Source: Calculation results from SPSS software).

Table 3.

Item-Total Correlation and Cronbach’s Alpha.

| Item-Total Correlation | Cronbach’s Alpha if Item Deleted | Item-Total Correlation | Cronbach’s Alpha | ||

|---|---|---|---|---|---|

| Cronbach’s Alpha: 0.749 | Cronbach’s Alpha: 0.775 | ||||

| QM1 | 0.597 | 0.660 | AL1 | 0.667 | 0.674 |

| QM2 | 0.473 | 0.728 | AL2 | 0.498 | 0.765 |

| QM3 | 0.567 | 0.678 | AL3 | 0.583 | 0.719 |

| QM4 | 0.539 | 0.694 | AL4 | 0.574 | 0.724 |

| Cronbach’s Alpha: 0.729 | Cronbach’s Alpha: 0.725 | ||||

| KN1 | 0.480 | 0.690 | CH1 | 0.615 | 0.551 |

| KN2 | 0.557 | 0.645 | CH2 | 0.518 | 0.674 |

| KN3 | 0.554 | 0.647 | CH3 | 0.511 | 0.679 |

| KN4 | 0.484 | 0.688 | |||

| Cronbach’s Alpha: 0.781 | Cronbach’s Alpha: 0.879 | ||||

| QL1 | 0.580 | 0.730 | AD1 | 0.735 | 0.846 |

| QL2 | 0.593 | 0.723 | AD2 | 0.707 | 0.857 |

| QL3 | 0.588 | 0.727 | AD3 | 0.738 | 0.845 |

| QL4 | 0.581 | 0.730 | AD4 | 0.773 | 0.831 |

(Source: Calculation results from SPSS software).

Table 4.

KMO and Bartlett’s Test for independent variables.

| KMO Coefficient | 0.879 | |

|---|---|---|

| Bartlett’s Test Chi-Square | Chi-Square | 1471.190 |

| df | 171 | |

| Sig. | < .001 | |

(Source: Calculation results from SPSS software).

Table 5.

Total Variance Explained.

| Factor | Initial Eigenvalues | Sums of Squared Loadings | ||||

|---|---|---|---|---|---|---|

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

| 1 | 4.958 | 30.985 | 30.985 | 4.958 | 30.985 | 30.985 |

| 2 | 1.729 | 10.804 | 41.789 | 1.729 | 10.804 | 41.789 |

| 3 | 1.476 | 9.225 | 51.014 | 1.476 | 9.225 | 51.014 |

| 4 | 1.261 | 7.882 | 58.896 | 1.261 | 7.882 | 58.896 |

| 5 | 0.755 | 4.719 | 63.615 | |||

| 6 | 0.743 | 4.645 | 68.26 | |||

| 7 | 0.67 | 4.186 | 72.446 | |||

| 8 | 0.63 | 3.935 | 76.381 | |||

| 9 | 0.605 | 3.781 | 80.163 | |||

| 10 | 0.531 | 3.316 | 83.479 | |||

| 11 | 0.512 | 3.202 | 86.681 | |||

| 12 | 0.473 | 2.957 | 89.638 | |||

| 13 | 0.469 | 2.939 | 92.578 | |||

| 14 | 0.432 | 2.698 | 95.276 | |||

| 15 | 0.39 | 2.438 | 97.704 | |||

| 16 | 0.367 | 2.296 | 100 | |||

(Source: Calculation results from SPSS software).

Table 6.

Rotated Component Matrix.

| Factor | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| QL3 | .757 | |||

| QL4 | .754 | |||

| QL2 | .727 | |||

| QL1 | .726 | |||

| QM1 | .778 | |||

| QM4 | .723 | |||

| QM3 | .690 | |||

| QM2 | .671 | |||

| AL3 | .781 | |||

| AL1 | .781 | |||

| AL4 | .766 | |||

| AL2 | .568 | |||

| KN3 | .734 | |||

| KN2 | .725 | |||

| KN4 | .725 | |||

| KN1 | .684 |

(Source: Calculation results from SPSS software).

Table 7.

KMO and Bartlett’s Test for the dependent variable.

| KMO Coefficient | 0.830 | |

|---|---|---|

| Bartlett’s Test | Chi-Square | 509.496 |

| df | 6 | |

| Sig. | <0.001 | |

(Source: Calculation results from SPSS software).

Table 8.

Component Matrix.

| Factor | |

|---|---|

| 1 | |

| AD1 | .855 |

| AD2 | .835 |

| AD3 | .856 |

| AD4 | .879 |

(Source: Calculation results from SPSS software).

Table 9.

Assessment of convergent and discriminant validity of the scale.

| CR | AVE | MSV | MaxR(H) | QM | KN | QL | AL | |

|---|---|---|---|---|---|---|---|---|

| QM | 0.781 | 0.561 | 0.245 | 0.781 | 0.749 | |||

| KN | 0.751 | 0.538 | 0.372 | 0.759 | 0.495*** | 0.733 | ||

| QL | 0.782 | 0.577 | 0.372 | 0.798 | 0.464*** | 0.610*** | 0.760 | |

| AL | 0.729 | 0.541 | 0.236 | 0.738 | 0.485*** | 0.412*** | 0.443*** | 0.732 |

(Source: Calculation results from AMOS software).

Table 10.

Regression Weights - SEM.

| Relationship | Estimate | S.E. | C.R. | P |

|---|---|---|---|---|

| AD ⟵ QL | 0.464 | 0.108 | 4.300 | *** |

| AD ⟵ QM | 0.442 | 0.112 | 3.944 | *** |

| AD ⟵ AL | 0.455 | 0.122 | 3.721 | *** |

| AD ⟵ KN | 0.513 | 0.136 | 3.781 | *** |

(Source: Calculation results from AMOS software).

Table 11.

Standardized Regression Weights - SEM.

| Relationship | Estimate | |

|---|---|---|

| AD ⟵ QL AD ⟵ QM AD ⟵ AL AD ← KN |

0.297 0.301 0.279 0.263 |

(Source: Calculation results from AMOS software).

Table 12.

Coefficient of Determination - SEM.

| Estimate | |

|---|---|

| AD | 0.800 |

(Source: Calculation results from AMOS software).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.