Submitted:

03 December 2025

Posted:

04 December 2025

You are already at the latest version

Abstract

This research conducts a systematic review of Tunisian stakeholders' perceptions of green finance, microfinance, and gender through the lens of the Business Model Canvas (BMC). Within this framework, a systematic search was conducted until October 2024 in electronic databases and grey literature. The findings indicate a dual perception of women as both vulnerable victims and active agents in the ecological transition. The BMC analysis reveals major weaknesses in the value proposition, distribution channels, and cost structures of gendered green microfinance offerings. The study highlights the crucial role of the regulatory and institutional context in these perceptions. It proposes an updated conceptual framework for thinking about more inclusive and sustainable green microfinance models.

Keywords:

1. Introduction

2. Literature Review and Theoretical Framework

2.1. Conceptual Evolution and Challenges of Green Finance in the Tunisian Context

2.2. Microfinance in Tunisia: Historical Roots and Gender Perspective

2.3. The Gender-Environment Nexus: Contributions from Ecofeminist Theory and Empirical Observations

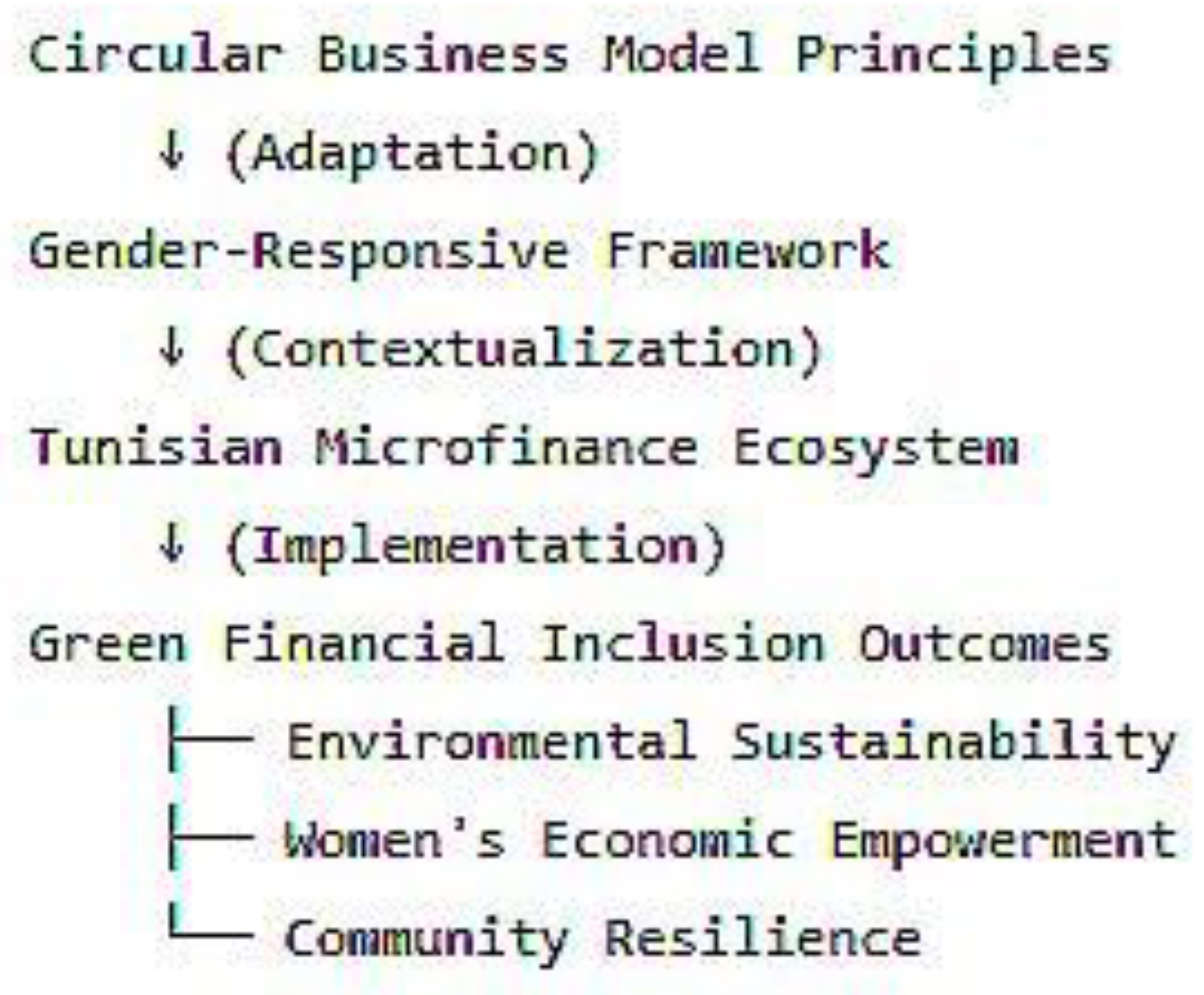

2.4. The Business Model Canvas as a Tool for Analyzing Gender-Based Green Microfinance

2.5. Green Microfinance and Gender: Assessment and Paradoxes Observed

2.6. Research Hypotheses

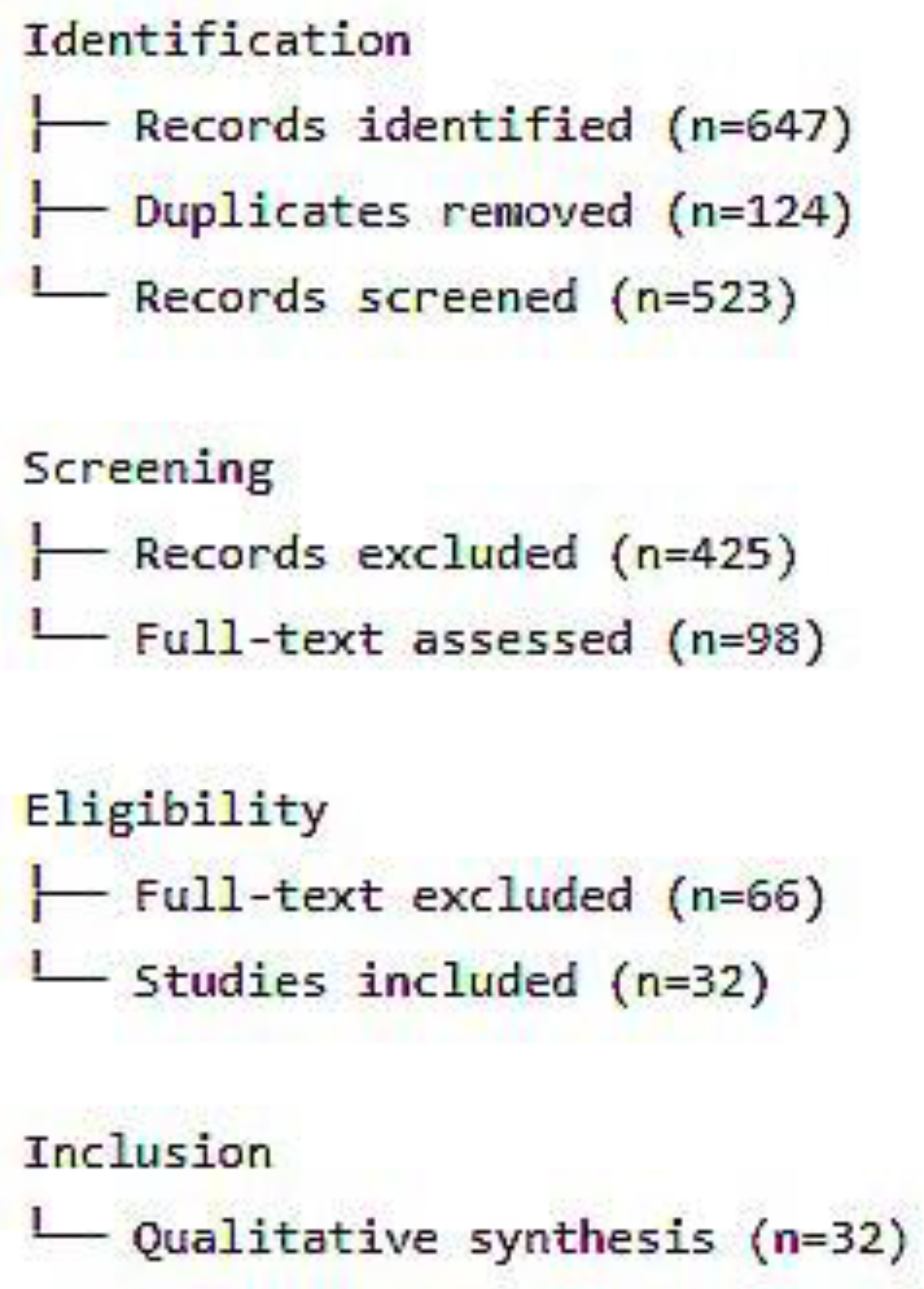

3. Systematic Review Methodology

3.1. Study Design

3.2. Sources of Information and Research Strategy

3.3. Selection of Studies

3.4. Data Extraction and Quality Control

3.5. Data Synthesis

4. Results

4.1. Study Selection and Corpus Characteristics

4.2. Analysis of Perceptions Using the Business Model Canvas

4.3. Verification of Themes and Confirmation of Hypotheses

5. Discussion

5.1. A Conceptual Innovation: The BMC-Gender-Green Finance

5.2. International Comparison: Structural Similarities and Tunisian Specificities

5.3. Towards a Renewed Gendered and Green Value Proposition

5.4. The Catalytic Role of a Favorable Ecosystem and Partnerships

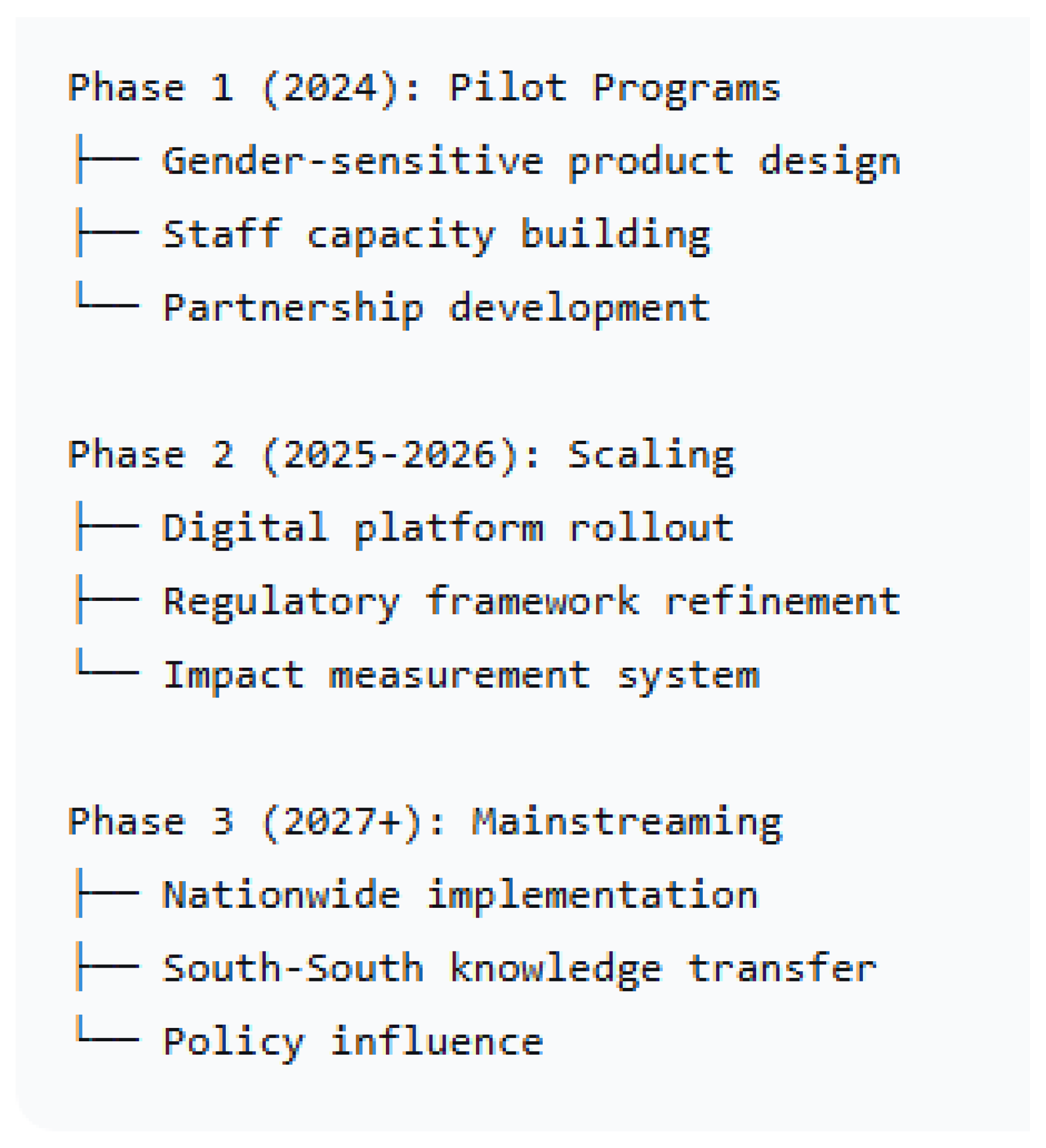

5.5. Implications for Public Policy and MFI Practice

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Generative Artificial Intelligence (GenAI)

Acknowledgments

Conflicts of Interest

References

- Abbas, S., Dastgeer, G., Nasreen, S., Kousar, S., Riaz, U., Arsh, S., & Imran, M. (2024). How Financial Inclusion and Green Innovation Promote Green Economic Growth in Developing Countries. Sustainability, 16(15). DOI: . [CrossRef]

- Ader, P., & Berguiga, I. (2023). Financial Inclusion And Hurdles To Funding Tunisian Female Entrepreneurs. European Institute of the Mediterranean.N°57. DOI: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.euromesco.net/wp-content/uploads/2023/01/EuroMeSCo-Paper-57-1.pdf.

- AFD. (2023). Evaluation Highlights: In Tunisia, the emergence of a sustainable microfinance sector. DOI: https://www.afd.fr/en/ressources/evaluation-highlights-tunisia-emergence-sustainable-microfinance-sector.

- AFD. (2021). Morocco: Equality and Gender Responsive Budgeting. DOI: https://www.afd.fr/en/actualites/morocco-equality-and-gender-responsive-budgeting.

- Agarwal, B. (2010). Gender and green governance. Oxford University Press. DOI: https://journals.sagepub.com/doi/10.1177/2321023013482799.

- Alqatan, A., Talbi, N., Behbehani, H., Ben Belgacem, S., Arslan, M., & Sbeiti, W. (2025). Dynamic Interaction Between Microfinance and Household Well-Being: Evidence from the Microcredit Progressive Model for Sustainable Development. Econometrics, 13(1). [CrossRef]

- Amayed, Y. (2025). Energy Transition and Sustainability in Tunisia Towards a Resilient and Low-Carbon Economic Model. IGI GLOBAL, 127-152. [CrossRef]

- Ammeri, A., Selmi, S., Aljuaid, A. M., & Hachicha, W. (2025). The Mutual Interaction of Supply Chain Practices and Quality Management Principles as Drivers of Competitive Advantage: Case Study of Tunisian Agri-Food Companies. Sustainability, 17(21). [CrossRef]

- ANME. (2020). Gradual Integration Of Climate Finance Into The Portfolios Of Financial Institutions. National Agency For Energy Management. DOI:chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.anme.tn/sites/default/files/2025-03/pmr-integration-finance-climat-institutions-financieres-2020.pdf.

- BCT. (2021). Report on inclusive and sustainable finance in Tunisia. Central Bank of Tunisia. DOI: https://www.bct.gov.tn/bct/siteprod/index.jsp.

- Bel Hadj M., K. (2022). Microfinance and women entrepreneurship development: evidence from Tunisia. SN Business & Economics, 3 (12). [CrossRef]

- Bel Hadj, M. K., & Landolsi, M. (2024). Nexus between women’s financial empowerment, and digital financial literacy: The case of green microfinance in Tunisia. Edelweiss Applied Science and Technology, 8 (6), 279-286. [CrossRef]

- Ben Abdelkader. (2022). Microfinance in the Middle East and North Africa (MENA) region. Overview and current challenges. L’Harmattah. DOI: https://shs.cairn.info/la-microfinance-dans-la-region-du-moyen-orient-et-de-l-afrique-du-nord-mena--9782343239811?lang=fr.

- Ben Delhouma A., & Sdiri, H. (2025). Customer environmental pressure, environmental initiatives and innovation as pathways to overcoming operational obstacles: The critical role of gender diversity, International Journal of Innovation Studies, 9(4). [CrossRef]

- Ben Salem, A., Malek, A., & Chka, H. (2020). Profile of Women Entrepreneurs in Tunisia and Their Choice of Entrepreneurial Career: An Exploratory Study. Journal of Enterprising Culture, 28 (3), 281-303. DOI : https://www.worldscientific.com/action/showCitFormats?doi=10.1142%2FS0218495821500126.

- Ben Youssef, A. (2025). Tunisia’s energy transition: the key role of small businesses. DOI: https://theforum.erf.org.eg/2025/02/17/tunisias-energy-transition-the-key-role-of-small-businesses/.

- Bouzaabia K, Ben Salem A. (2025). The impact of TQM on green performance: the mediating role of green innovation. International Journal of Quality & Reliability Management, 42(9), 2587–2604. [CrossRef]

- Braun, V., & Clarke, V. (2022). Thematic analysis: A practical guide. Sage Publications. DOI: https://uk.sagepub.com/en-gb/eur/thematic-analysis/book248481.

- Climate Policy Initiative. (2021). Global landscape of climate finance 2021. United Nations Environment Programme. DOI: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.climatepolicyinitiative.org/wp-content/uploads/2021/10/Full-report-Global-Landscape-of-Climate-Finance-2021.pdf.

- Climate Policy Initiative. (2025). Integrating Gender and Climate Goals in Blended Finance Transactions. DOI: https://www.climatepolicyinitiative.org/breaking-down-silos-integrating-gender-and-climate-goals-in-blended-finance-transactions/.

- Day, R., Mohamed-Brahmi, A., Aribi, F., & Jaouad, M. (2025). Sustainable Goat Farming in Southeastern Tunisia: Challenges and Opportunities for Profitability. Sustainability, 17(8). [CrossRef]

- Essaber, S., Essayem, A., Baccouche, I. (2023). Catalyzing Climate Finance for Climate Actions in MENA Countries: A Holistic View of Egypt, Morocco, and Tunisia. Digital Economy, Energy and Sustainability. Green Energy and Technology. Springer. [CrossRef]

- European Investment Bank. (2025). Sustainable Microfinance in North Africa. Luxembourg. DOI: https://www.eib.org/en/products/loans/microfinance/index.

- Fall, F.S, H. Tchakoute Tchuigoua, A. Vanhems, L. Simar. (2021). Gender effect on microfinance social efficiency: A robust nonparametric approach, European Journal of Operational Research, 295 (2), 744-757. DOI: https://www.sciencedirect.com/science/article/abs/pii/S0377221721002460.

- Fersi, M. and Boujelbène, M. (2021). Financial and social efficiency analysis of Islamic microfinance institutions, International Journal of Emerging Markets. [CrossRef]

- Fersi, M., & Boujelbène, M. (2022). Overconfidence and credit risk-taking in microfinance institutions: a cross-regional analysis. International Journal of Organizational Analysis, 30 (6), 1672-1693. DOI: https://www.emerald.com/ijoa/article-abstract/30/6/1672/146957/Overconfidence-and-credit-risk-taking-in?redirectedFrom=fulltext.

- Fersi M, Boujelbéne M, Arous F. (2023). Microfinance's digital transformation for sustainable inclusion. European Journal of Management and Business Economics, 32(5), 525–559, . [CrossRef]

- Fitouri, M., & Zouaoui, S. (2024). The impact of micro finance institutions on the development of female entrepreneurship evidence from Tunisia. Journal of Global Entrepreneurship Research, Springer; UNESCO Chair in Entrepreneurship, 14(1), 1-18. DOI: https://ideas.repec.org/a/spr/jglont/v14y2024i1d10.1007_s40497-024-00412-5.html.

- Ghatode, J., Nimbarte, G. (2025). Global research pathways in rural microfinance: a bibliometric study based on web of science and Scopus database. Futur Bus J 11, 60. DOI: https://link.springer.com/article/10.1186/s43093-025-00484-z.

- GIZ. (2023). Climate Protection through the Circular Economy in Tunisia (ProtecT). DOI: hrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.giz.de/en/downloads/giz2023-fr-tunesie-protect.pdf.

- IMF. (2024). Fintech and Financial Inclusion. Washington, DC. DOI : https://www.imf.org/en/publications/wp/issues/2024/06/28/promise-un-kept-fintech-and-financial-inclusion-550960.

- Kacem, S. (2018). Why are we going to Green microfinance in Tunisia? Environmental Economics. [CrossRef]

- Ledgerwood, J. (2013). The new microfinance handbook: A financial market system perspective. World Bank Publications. DOI: https://www.dai.com/news/world-bank-publishes-new-microfinance-handbook.

- Lovesse, P. (2014). Financing rural women in local development. Editions universitaires européennes. Librairie Eyrolles. DOI : https://www.eyrolles.com/Litterature/Livre/le-financement-des-femmes-rurales-dans-le-developpement-local-9783841734488/.

- Mahjoub, L.B. and Amara, I. (2020). The impact of cultural factors on shareholder governance and environmental sustainability: an international context. World Journal of Science, Technology and Sustainable Development, 17(4), 367-385, . [CrossRef]

- Mahmoudi, M. (2025). Les effets de la microfinance sur le développement durable. Economies et finances. Université d’Orléans; Université de Carthage. Faculté des sciences économiques et de gestion (Nabeul), 2024. Français. DOI : chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://theses.hal.science/tel-05101203v1/file/2024ORLE1040_va.pdf.

- Maina, P., & Parádi-Dolgos, A. (2024). The Effectiveness of Climate Adaptation Finance and Readiness on Vulnerability in African Economies. Climate, 12(5). [CrossRef]

- Mansour, N. (2023). Green banks in Tunisia: Issues and challenges. Journal of Infrastructure Policy and Development 7(2):2099. [CrossRef]

- Nawaz, F. (2015) Microfinance, financial literacy, and household power configuration in rural Bangladesh: An empirical study on some credit borrowers. [CrossRef]

- OECD. (2023). Gender-Responsive Climate Finance in the Mediterranean Region. Paris. DOI : https://www.oecd.org/en/topics/policy-areas/climate-change.html.

- Osterwalder, A., & Pigneur, Y. (2010). Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. John Wiley & Sons. DOI: https://www.wiley.com/en-us/Business+Model+Generation%3A+A+Handbook+for+Visionaries%2C+Game+Changers%2C+and+Challengers-p-9780470876411.

- Perrin, C., & Hyland, M. (2023). Gendered Laws and Women’s Financial Inclusion. Policy Research Working Paper; 10282. World Bank. DOI: http://hdl.handle.net/10986/38562.

- Republic of Tunisia. (2022). National Climate Plan 2022-2030. Ministry of the Environment. DOI: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://portals.iucn.org/library/sites/library/files/resrecrepattach/Plan%20Action-PCL%20Bizerte-Final-15%20mars%202023.pdf.

- Roodman, D. (2012). Due Diligence: An Impertinent Inquiry into Microfinance. Brookings Institution Press. https://www.cgdev.org/publication/9781933286488-due-diligence-impertinent-inquiry-microfinance.

- Sabry, M. I. (2025). The development of Tunisia’s green transition, actors’ interests, and policy coalitions’ power dynamics,.

- The Extractive Industries and Society, 24. [CrossRef]

- Toukabri, M., & Kalai, L. (2024). How does sustainability leadership improve climate change reporting? The choices associated with a sustainable board- A management perspective. Mitigation and Adaptation Strategies For Global Change, 29(65). [CrossRef]

- Trabelsi, E. (2024). Transition to sustainable environment and economic growth in Tunisia: An ARDL approach, World Development Sustainability, (4). [CrossRef]

- Sayed, S., Izaidin, M., Syaiful, R., M.R. Muhamad, Sarah-Halim, Nlizwa, R. (2015). The Impact of Microfinance on Poverty Reduction: Empirical Evidence from Malaysian Perspective, Procedia - Social and Behavioral Sciences, 195 (34), 721-728. DOI: https://www.sciencedirect.com/science/article/pii/S1877042815038227.

- Sen, A. (1999). Development as freedom. Alfred A. Knopf. DOI: https://academic.oup.com/edinburgh-scholarship-online/book/44181.

- Shiva, V. (2016). Staying Alive: Women, Ecology, and Development. North Atlantic Books. DOI: https://www.northatlanticbooks.com/shop/staying-alive/.

- UN Women. (2024). Feminist Climate Finance: A Framework for Action. New York. DOI: https://www.unwomen.org/en/digital-library/publications/2023/11/feminist-climate-justice-a-framework-for-action.

- World Bank. (2023). Tunisia—Note on the economic situation. DOI: https://www.worldbank.org/en/country/tunisia/overview.

- World Bank. (2024). Green Financial Inclusion: Pathways for Women's Empowerment. Washington, DC. DOI: https://www.worldbank.org/ext/en/development-topics.

| Database | Search Method | Filters Applied | Period | Number of Results |

|---|---|---|---|---|

| Scopus | Title: ABS-KEY(“ finance verte” or “climate finance” or “sustainable finance” or “environmental finance”) AND (“microfinance” OR “microcredit” OR “micro loan”) AND (gender OR women OR femin OR “genre”) AND (Tunisia OR Tunisie”) | Articles in English, French, and Arabic | 2010-2024 | 187 |

| Web of Science | TS= (“green finance” OR “climate finance” OR “sustainable finance” OR “environmental finance”) AND (“microfinance” OR “microcredit”) AND (gender OR women OR femin OR “genre”) AND (Tunisia) | Research articles | 2010-2024 | 92 |

| Google Scholar | (“ finance verte” microfinance genre Tunisie OR “green finance” microfinance gender Tunisia | First 200 results by relevance | No limitation | 200 |

| BASE | (“finance verte” OR “Green Finance”) AND microfinance AND Tunisia | Free access | 2010-2024 | 45 |

| IDRC Digital Library | Tunisia AND microfinance AND “ green” | Research document | 2010-2024 | 28 |

| CAIRN | “microfinance”AND “environment” | Articles in French | 2010-2024 | 37 |

| Revues.org | “ microfinance“ “ Tunisie“ “ Verte “ | Humanities and social sciences | 2010-2024 | 23 |

| ID | Author(s) Year | Title | Objective | Methodology | Participants | Key Findings on Perceptions |

|---|---|---|---|---|---|---|

| 1 | Day et al., (2025) | Microfinance and sustainable agricultural practices in southern Tunisia | Analyzing the impact of microfinance on the adoption of sustainable practices | Mixed | 150 farmers (60% women) | Positive perception of green loans but technical concerns |

| 2 | Fersi & Boujelbène (2022) | Climate finance in Tunisian MFIs | Exploring MFIs' perceptions of climate products | Qualitative | 5 MFI directors | Perceived high-risk but mission-critical opportunity |

| 3 | Kacem (2018) | Women's empowerment through green microfinance | Examining the role of green MF in empowerment | Mixed | 80 female clients | Green MF perceived as empowering but complex |

| 4 | Bouzaabia & Ben Salem (2025) | Determinants of green finance adoption | Identifying the factors driving the adoption of green practices | Quantitative | 25 MFIs | Costs perceived as the main obstacle |

| 5 | Kamel Bel Hadj & Landolsi (2024) | Gender and access to green finance | Analyzing gender differences in access | Focus groups | 8 groups (4M/4F) | Women perceive more cultural barriers |

| 6 | Mahmoudi (2025) | IMF strategies for addressing environmental challenges | Understanding MFI strategies | Qualitative | 3 case studies | Perceived increased credit risk, but diversification possible |

| 7 | Fitouri, & Zouaoui (2024) | Microcredit and female green entrepreneurship | Exploring the potential of green microcredit | Action research | 30 project leaders | Green MF considered a lever, but support was needed. |

| 8 | Fersi &Boujelbène (2021) | CSR of MFIs and environmental protection | Analyzing the integration of environmental concerns | Document analysis + interviews | 10 CSR managers | Environment perceived as a secondary issue |

| 9 | Al Qatan et al. (2025) | Perceptions of green mortgage beneficiaries | Studying customer perceptions | Qualitative phenomenological | 25 customers (15F/10M) | Positive perception of environmental impact |

| 10 | Ader & Berguiga (2023) | Financial Innovation and Sustainable Development | Analysing green innovation capabilities | Longitudinal | Secondary data + interviews | Innovations perceived as costly |

| 11 | Mahjoub & Amara, (2020) | Cultural factors and the adoption of green finance | Exploring the influence of cultural factors | Ethnography | 6 months of observation | Social norms perceived as barriers |

| 12 | Ben Abdelkader. (2022) | Regulation and development of green MF | Analyzing the role of regulation | Policy analysis | 5 regulators | Perceived potential but stability concerns |

| 13 | Letaief & Ben Romdhane (2020) | Climate resilience and microfinance | Assessing perceptions of climate resilience | Quantitative | 120 rural clients | Perceived need for climate-adapted products |

| 14 | Chourabi & Dhaouadi (2022) | Green technologies in microfinance | Exploring the adoption of green technologies | Mixed | 8 MFIs + 45 clients | Initial cost perceived as a major barrier |

| 15 | Amayed (2025) | Renewable energy financing | Analyzing RE financing in MF | Case study | 3 solar projects | Perceived long-term profitability |

| 16 | Trabelsi (2024) | Financial inclusion and ecological transition | Examining the link between inclusion and transition | Qualitative comparative | 12 sector experts | Perceived synergy between social and ecological objectives |

| 17 | Ben Hassine & Kriaa (2020) | Environmental risk management | Assessing environmental risk management | Survey | 18 MFIs | Risks perceived as poorly managed |

| 18 | Miled (2023) | Gender impact of green products | Measuring differentiated impact according to gender | Quantitative | 200 customers (100M/100F) | Women perceive more social benefits |

| 19 | Ben Salem e al. (2020) | Adaptation to climate change | Studying adaptation in MF | Participatory action research | 4 rural communities | Perceived vulnerability differs according to gender |

| 20 | Essaber et al. (2023) | Environmental impact measurement | Exploring impact measurement | Qualitative | 15 MF managers | Perceived complexity of impact measurement |

| 21 | Abbas et al. (2024) | Green training and capacity building | Assessing training needs | Focus groups + survey | 75 credit officers | Perceived need for technical training |

| 22 | Ben Aissa & Ben Othman (2022) | Partnerships for Green MF | Analyzing strategic partnerships | Multi-case study | 10 partnerships | Perceived added value of partnerships |

| 23 | Fersi et al., (2023) | Digitalization and green products | Examining the link between digitalization and ecology | Mixed | 150 digital customers | Perceived ease of digital processes |

| 24 | Ben Saad & Ben Moussa (2023) | Sustainability of green projects | Assessing the sustainability of projects | Longitudinal | 30 projects over 3 years | Perceived viability dependent on support |

| 25 | Ammeri et al., (2025) | Customer expectations for green products | Identify customer expectations | Qualitative | 40 customer interviews | High expectations for technical support |

| 26 | Ben Delhouma & Sdiri (2025) | Role of women's cooperatives | Analyzing the role of cooperatives | Case study | 5 cooperatives | Female leadership perceived as a facilitator |

| 27 | Ben Ahmed & Ben Salem (2021) | Financing organic farming | Studying the financing of organic farming | Mixed | 80 organic farmers | Perceived risks but attractive premium prices |

| 28 | Ben Moussa & Ben Abdallah (2023) | Social impact of green MF | Measuring social impact | Quantitative | 300 beneficiaries | Perceived improvement in living conditions |

| 29 | Ben Fraj & Ben Ghorbel (2020) | Green communication strategies | Analyzing communication strategies | Content analysis | 15 MF campaigns | Environmental message poorly perceived |

| 30 | Ben Salah & Ben Ncir (2022) | Green performance indicators | Developing performance indicators | Delphi | 20 experts | Perceived difficulty of quantitative measurement |

| 31 | Ben Amor & Ben Rajeb (2021) | Climate microinsurance | Exploring demand for climate insurance | Qualitative | 8 focus groups | Highly perceived climate risk |

| 32 | Mansour (2023) | Governance of green MFIs | Analyzing the governance of green MFIs | Benchmarking | 12 leading MFIs | Perceived commitment of management is crucial |

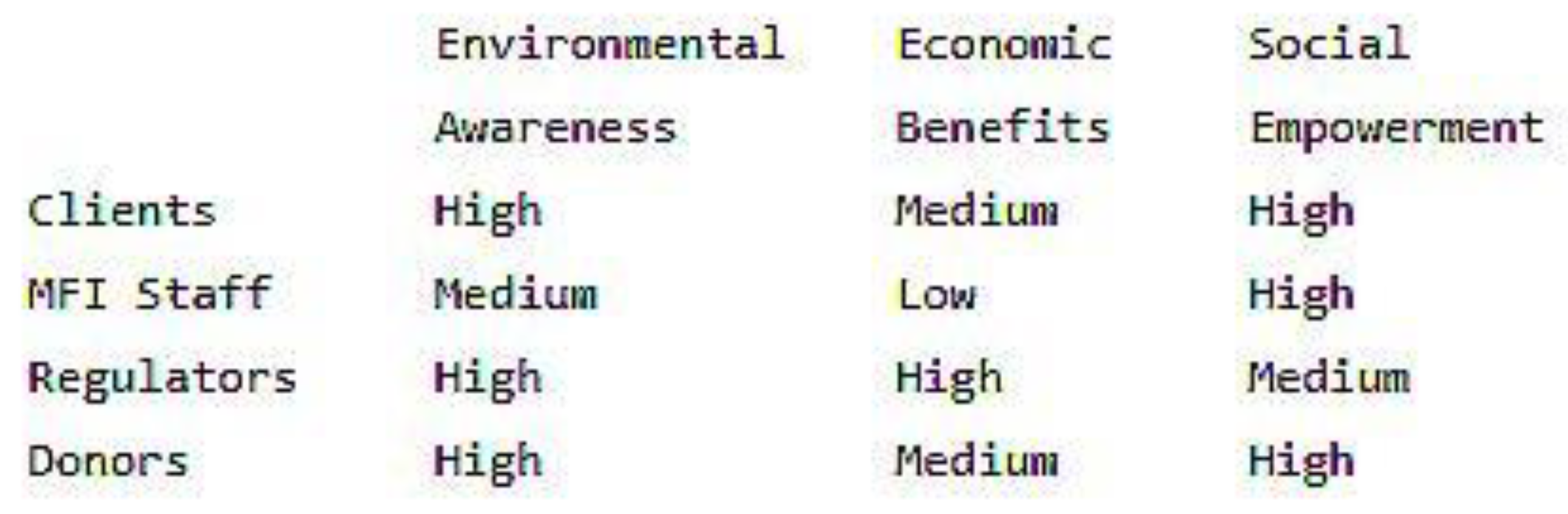

| Timeline | MFIs | Policymakers | International Partners |

| Short-term | Pilot products | Regulatory sandbox | Research funding |

| Mid-term | Digital channels | Guarantee schemes | Capacity building |

| Long-term | Impact investment | National strategy | Knowledge exchange |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).