Submitted:

07 November 2025

Posted:

12 November 2025

You are already at the latest version

Abstract

This article critically examines the role of financial education as a catalyst for financial freedom, understood not only as economic autonomy, but also as the real capacity for agency and deliberation about material life. Based on a qualitative, descriptive, and documentary study, a thematic content analysis was applied to academic literature, institutional reports, and classic and contemporary works on personal finance.The results show that financial literacy, although necessary, is insufficient if it is not articulated with psychological, socio-emotional, and cultural dimensions, such as financial mindset, discipline, emotions, and beliefs about money. From a transdisciplinary approach, the interrelationships between financial education, self-education, the psychology of money, and decision-making are explored, proposing a comprehensive model that links knowledge, action, and being.It is argued that financial education must transcend the mere transmission of technical content to become a process of ethical and political empowerment, oriented toward the development of sustainable habits, critical thinking, and socio-emotional skills that allow for conscious control over the economy and thoughtful participation in the structures that shape collective life.It concludes that, in order to be transformative, financial education must be multidimensional, situated, and adaptive, capable of responding to the challenges of a global environment characterized by inequality and technological acceleration. It proposes moving toward evidence-based programs that strengthen civic agency and deliberative participation as constitutive dimensions of contemporary political subjectivity.

Keywords:

financial education

; financial freedom

; psychology of money

; economic empowerment

; transdisciplinary approach

1. Introduction

In Recent Decades, Access To Financial Information Has Expanded Significantly, Driven By Digitization, The Proliferation Of Online Educational Resources, And The Diversification Of Banking Products. However, This Increased Availability Of Information Has Not Translated Into Substantive Transformations In The Economic Behavior Patterns Of The Population. On A Global Scale, And Particularly In Latin America, Structural Phenomena Such As Chronic Indebtedness, Excessive Consumerism, Low Savings Rates, And A Lack Of Strategic Financial Planning Persist. All Of This Highlights The Gap Between The Knowledge Available And Actual Economic Behavior (OECD, 2017; Meier & Sprenger, 2013; Mungaray Et Al., 2021). This Paradox Reveals A Structural Problem: Financial Knowledge Alone Does Not Guarantee Sound Decisions Or Sustainable Economic Well-Being.

Understanding This Phenomenon Is Critically Important In The Contemporary Debate, As The Consequences Of Financial Illiteracy Impact Not Only Individual Economic Stability But Also Social Cohesion And Equity. The Specialized Literature Agrees That The Level Of Financial Education Is A Key Determinant Of Individuals' Ability To Plan For Their Future, Manage Risks, Accumulate Savings, And Invest In An Informed And Responsible Manner (Lusardi & Mitchell, 2014; OECD, 2014; Rani, 2023). In This Context, Financial Well-Being, Conceived As The Ability To Meet Present Obligations, Project Oneself Securely Into The Future, And Make Decisions Consistent With One's Own Life Goals, Has Become A Priority Objective For Both Education Systems And Public Policies Aimed At Human Development (Brüggen Et Al., 2017).

Contemporary Financial Education Must Be Understood As More Than The Mere Acquisition Of Technical Knowledge. Its Educational Value Lies In Strengthening Individuals' Autonomy And Freedom To Exercise Economic Agency In Contexts Characterized By Market Inequality And Complexity. From A Philosophical Perspective, Autonomy Implies Not Only Independence, But Also The Capacity For Self-Regulation And Ethical Decision-Making That Reflects Distributive Justice And Social Recognition (Sen, 1999; Nussbaum, 2011). Thus, Financial Literacy Can Be Interpreted As A Form Of Social Justice, In That It Contributes To The Development Of Human Capacities That Enable People To Act Freely Within Often Restrictive Economic Structures (Fraser, 2005). On A Psychological Level, These Principles Correspond To Constructs Such As Self-Efficacy, Resilience, And Financial Socialization, Which Act As Mediators Between Financial Knowledge And Effective Economic Behavior. Financial Self-Efficacy, Understood As The Perception Of Control And Competence Over One's Own Economic Decisions, Has Been Shown To Be A Significant Predictor Of Financial Well-Being And Responsible Use Of Credit (Gulati & Singh, 2024; Hernández-Pérez & Cruz Rambaud, 2025). Complementarily, Financial Resilience Allows Individuals To Cope With Adversity And Adapt To Critical Economic Events, Strengthening Their Capacity For Agency In Uncertain Scenarios (Moazezi Khah Tehran Et Al., 2025; Masten, 2021). For Its Part, Financial Socialization Is The Process By Which Individuals Internalize Economic Norms, Values, And Habits Through Interaction With Family, Peers, And Educational Institutions (Kaur, 2024). This Process Plays A Central Formative Role In The Construction Of Political Subjectivity, Shaping Ways Of Thinking, Feeling, And Acting In Relation To Money That Transcend The Economic Sphere And Enter The Realm Of Citizenship. In This Vein, Financial Education Can Be Understood As A Device For Ethical And Political Training, Which Articulates Personal Autonomy With Social Justice And Material Freedom (Mouffe, 2000; Sen, 1999).

However, The Strategies Implemented To Date Have Proven Insufficient To Generate Sustained Changes In Financial Behavior. Most Institutional Programs Have Favored One-Dimensional Approaches, Focusing Almost Exclusively On The Transmission Of Technical Content, Neglecting Emotional, Cultural, And Psychological Factors That Have A Decisive Influence On Economic Decisions (Netemeyer Et Al., 2024; López-Lapo Et Al., 2022). Furthermore, These Programs Have Lacked Continuity, Flexibility, And Sociocultural Relevance, Which Has Limited Their Impact, Especially Among Young People, Women, And Groups Historically Marginalized From The Financial System (Desfrancois, 2024; Bado Et Al., 2023; Garg & Singh, 2018). In Light Of These Limitations, This Article Proposes An Integrative And Transformative Approach To Financial Education That Combines Technical Knowledge With Emotional, Behavioral, And Cognitive Skills. Unlike Traditional Models, It Argues That Financial Freedom Cannot Be Achieved Solely Through The Accumulation Of Information, But Rather Through The Development Of A Healthy Financial Mindset, The Reprogramming Of Limiting Beliefs, The Strengthening Of Economic Self-Concept, And The Constant Practice Of Self-Education (Duhigg, 2012; Tang & Baker, 2016; Kobsch Et Al., 2023).

This Analysis Is Structured Around Five Key Components:

- Financial Education As A Transformative Asset, Enabling Individuals To Adapt To Complex Economic Environments And Make Informed Decisions.

- The Mindset And Psychology Of Money, With An Emphasis On The Power Of Beliefs, Financial Self-Esteem, And Family Socialization.

- Savings And Smart Investing, As Practical Expressions Of Personal Economic Empowerment.

- Debt Management And The Redefinition Of Financial Freedom, Overcoming The Logic Of Survival To Build Well-Being.

- New Scenarios For Financial Education In The Face Of Digitalization, Technological Innovation, And Demands For Equity And Inclusion.

The Methodology Used Is Qualitative, Documentary, And Descriptive, With An Emphasis On Recent Studies And Empirical Evidence In Latin America And Other Regions. A Critical And Reflective Review Of Academic Literature, Institutional Reports, And Training Proposals Is Carried Out. The Results Indicate That Only A Comprehensive, Emotionally Intelligent, And Culturally Relevant Approach Can Generate Real Transformations In Financial Behavior And Facilitate The Path To Financial Freedom (Sconti Et Al., 2024; Abdul & Akhtar, 2024; Rani, 2023).

Within This Framework, The Objective Of This Study Is To Analyze, From A Qualitative And Documentary Perspective, How Financial Education Can Be Configured As A Comprehensive Path To Financial Freedom, Incorporating Technical, Emotional, Cognitive, And Sociocultural Dimensions. The Main Contribution Lies In Offering A Critical And Transdisciplinary Reinterpretation Of Financial Education That Transcends Traditional Approaches Focused On Content Transmission, Proposing It Instead As A Process Of Personal And Social Empowerment Oriented Toward Comprehensive Well-Being, Economic Justice, And Sustainability.

2. Theoretical Framework

2.1. Financial Education as a Transformative Asset

Financial Education Has Traditionally Been Conceived As The Transmission Of Basic Technical Knowledge, Budgeting, Saving, And Credit, But This Limited View Has Proven Insufficient To Sustainably Transform Economic Behavior (Atkinson & Messy, 2012; Atkinson & Messy, 2013; OECD, 2014). Today, It Is Seen As A Transformative Asset, Capable Of Empowering Individuals And Promoting Comprehensive Well-Being In Contexts Of Inequality And Exclusion (Aydin & Selcuk, 2019; Zhu & Xiao, 2022). In Latin America, Low Levels Of Financial Literacy Particularly Affect Young People And Women (De Beckker Et Al., 2019), Limiting Inclusion And Perpetuating Poverty (Mungaray Et Al., 2021). Furthermore, The Disconnect Between Educational Content And Sociocultural Realities Reduces The Effectiveness Of Programs (Asiah Et Al., 2024). In Response To This, A Situated, Critical, And Emotionally Intelligent Financial Education Is Proposed (Pulungan Et Al., 2024; Barua Et Al., 2018; Quibra, 2024).

2.2. Mindset and Psychology of Money

Financial Behavior Is Deeply Influenced By Psychological And Emotional Factors, Beyond Formal Knowledge (Khan Et Al., 2023; Noh, 2022). Behavioral Economics Has Shown How Biases Such As Procrastination Or Risk Aversion Affect Savings And Investment Decisions (Bai, 2023; Asiah Et Al., 2024; Pandey & Utkarsh, 2024). Financial Mindset Is Shaped By A Set Of Beliefs And Attitudes Molded By Experiences, Family, And Culture (Quibra, 2024; Gutiérrez-Andrade & Delgadillo-Sánchez, 2018). Financial Self-Efficacy Is Associated With Resilience And Autonomy (Abdul & Akhtar, 2024), While Early Socialization Influences Attitudes Toward Money In Adulthood (Pandey & Utkarsh, 2024). Recent Studies Highlight The Importance Of Reprogramming Limiting Beliefs (Duhigg, 2012; Vieira Et Al., 2021), Strengthening Economic Self-Concept (Lusardi & Tufano, 2015; Kharel Et Al., 2024; Bustamante & Cabrera, 2017; Mahendru Et Al., 2022), And Promoting Financial Self-Education In Digital Environments (Espino-Barranco, 2021; Desfrancois, 2024; López-Lapo Et Al., 2022).

2.3. Smart Saving and Investing

Savings Are The Foundation Of Financial Stability, But Rates Remain Low In Latin America Due To A Lack Of Planning And Disordered Consumption Habits (Ramon-Arteaga & Malla-Alvarado, 2022; Zhang & Chatterjee, 2023). Saving Should Be Understood As Behavior Influenced By Beliefs And Emotions (Pulungan Et Al., 2024). Smart Investing, On The Other Hand, Requires Risk Analysis, Time Horizons, And An Understanding Of The Economic Environment (Zelenova Et Al., 2023), With Financial Literacy Being Key, Especially When Dealing With Complex Instruments Such As Cryptocurrencies, Index Funds, Or Decentralized Finance (Leong, 2026; Mihalcova Et Al., 2020). Lack Of Knowledge And Overexposure To Social Media Generate Risks Of Speculation (Asiah Et Al., 2024; Pulungan Et Al., 2024). In Addition, Investment Must Incorporate Ethical And Sustainable Criteria (Zelenova Et Al., 2023), Linking Profitability With Social Responsibility.

2.4. Debt and Financial Freedom

When Managed Without Planning, Debt Becomes An Obstacle To Well-Being (Ramon-Arteaga & Malla-Alvarado, 2022; Cao-Alvira Et Al., 2021; Zhang & Chatterjee, 2023). Emotional Consumption And Immediacy Bias Exacerbate The Problem (Asiah Et Al., 2024). However, Debt Can Be An Instrument Of Mobility If Accompanied By Comprehensive Financial Education (Pulungan Et Al., 2024). Financial Freedom Is Conceived As An Evolutionary Process That Integrates Technical Skills, Self-Knowledge, And Social Justice (Brüggen Et Al., 2017; Álvarez-Avad Et Al., 2022; Tang & Baker, 2016; Vieira Et Al., 2021; Sangeeta Et Al., 2022). It Is Conditioned By Structural Inequalities (Bustamante & Cabrera, 2017) And Varies According To Age, Gender, And Educational Level (López-Medina Et Al., 2022). It Is Also Linked To Psychological Well-Being (Herrero Et Al., 2025; Zhang & Chatterjee 2023) And Financial Capabilities (Nussbaum, 2011; Nourallah Et Al., 2025). In Addition To The Above, The Notion Of Financial Citizenship Reinforces Economic Literacy As A Citizen's Right (Vieira Et Al., 2021).

2.5. New Scenarios: Financial Education for the Future

Digitalization, The Emergence Of Fintech, And Growing Inequality Pose New Challenges For Financial Education (Zhu, 2024; Mihalcova Et Al., 2020; Zelenova Et Al., 2023). Traditional, Decontextualized, And Prescriptive Programs Have Proven To Be Ineffective (Ramon-Arteaga & Malla-Alvarado, 2022). A Transdisciplinary Approach That Integrates Sustainability, Innovation, Entrepreneurship, And Consumer Ethics Is Required (Gallo & Sconti, 2024). Financial Literacy Should Be Considered A Citizen's Right And Incorporated Into Public Policy (Vieira Et Al., 2025; World Bank, 2013), With Strategies Such As Teacher Training, Adapted Content, And Accessible Digital Resources (Espino-Barranco, 2021). Digital Platforms And Collaborative Networks Can Enhance Self-Education, Although They Require Emotional Support And Critical Thinking. In A World Of Uncertainty, Economic Resilience And Mental Discipline Become Essential (López-Lapo Et Al., 2022).

In Order To Synthesize The Internal Logic Of The Theoretical Framework And Show The Conceptual Progression Of Its Sections, An Evolutionary Map Was Developed That Organizes The Content In A Coherent Sequence. Table 1 Presents This Structure, Highlighting How The Reflection Starts From Financial Education Understood As A Transformative Asset, Moves Towards The Incorporation Of The Mindset And Psychology Of Money, Takes Shape In Savings And Investment Practices, Expands Into The Discussion On Debt And Financial Freedom, And Finally Projects Itself Towards New Educational And Social Scenarios. This Outline Allows Us To Visualize The Articulation Between The Different Thematic Axes, The Theorical References That Support Them, And The Transitions That Connect Each Dimension, Offering A Comprehensive And Dynamic View Of The Phenomenon Studied.

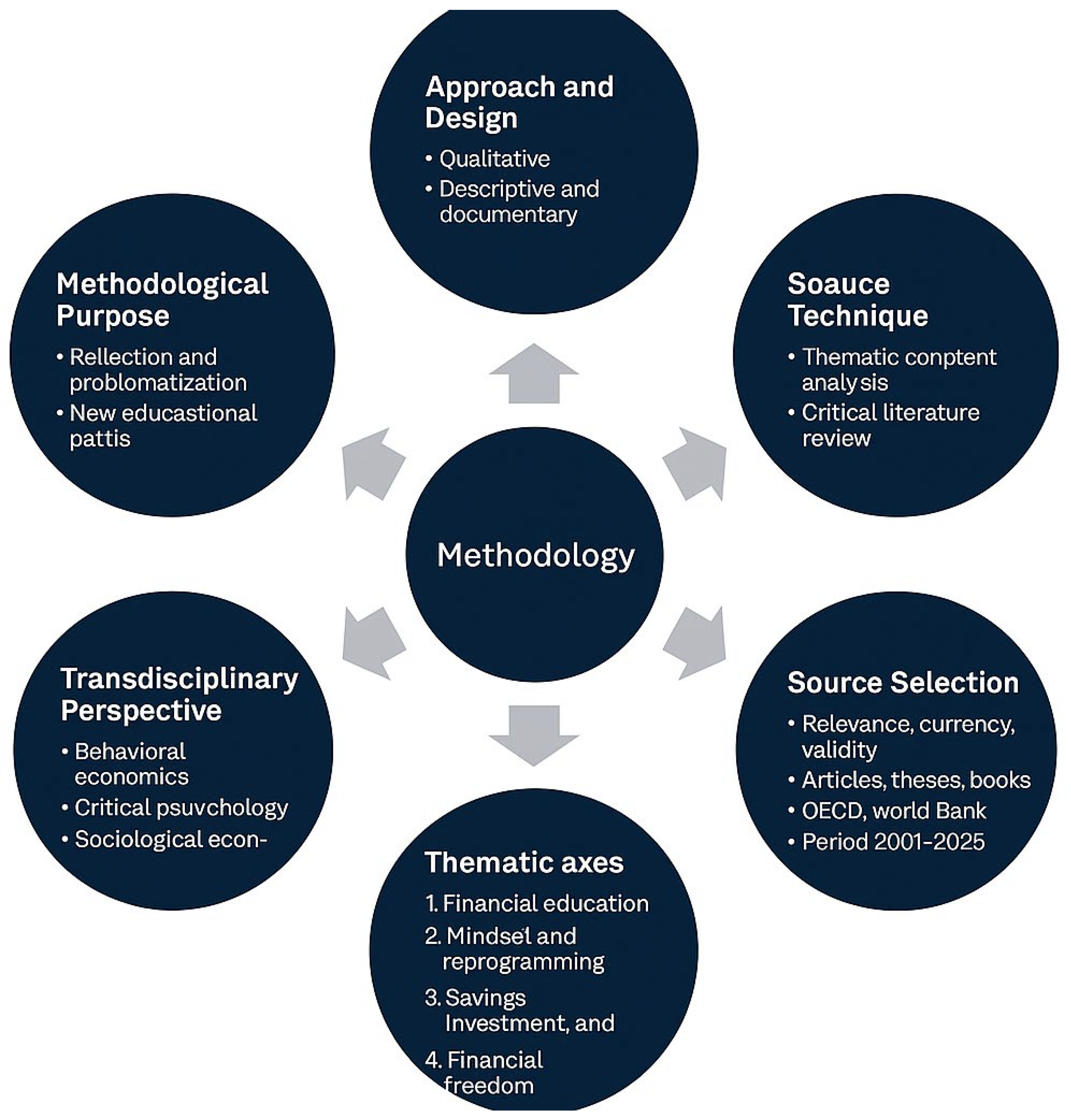

3. Methodology

This Study Was Developed Using A Qualitative, Descriptive, And Documentary Approach, With The Purpose Of Analyzing How Financial Education Can Become An Effective Path To Financial Freedom From A Comprehensive Perspective Of Personal Finance. The Methodological Design Was Based On The Review And Critical Analysis Of Academic Literature, Institutional Reports, And Specialized Publications, Which Allowed For The Construction Of A Robust Theoretical Framework And An Argumentative Interpretation Of The Findings In Relation To The Phenomenon Studied (Flick, 2014).

The Main Technique Used Was Thematic Content Analysis, Which Made It Possible To Identify Conceptual Patterns, Establish Connections Between Analytical Categories, And Construct A Narrative Consistent With The Study's Objectives. This Technique Is Particularly Suitable For A Deep Understanding Of Complex Phenomena In Real Contexts, A Central Feature Of Qualitative Research Focused On Social, Behavioral, And Educational Aspects (Álvarez-Gayou, 2003).

The Sources Consulted Were Selected Based On Criteria Of Thematic Relevance, Timeliness, Academic Validity, And Geographic Diversity, Incorporating Studies From Latin America, Europe, And Asia. Priority Was Given To Publications Issued Between 2001 And 2025, Including Indexed Scientific Articles And Reports From Multilateral Organizations Such As The OECD And The World Bank, As Well As Recent Research On Financial Education, Financial Behavior, The Psychology Of Money, And Economic Empowerment Strategies.

The Analysis Was Structured Around Five Thematic Areas:

- Financial Education As A Transformative Asset.

- Financial Mindset And Reprogramming.

- Key Behaviors Related To Saving, Investing, And Debt Management.

- Financial Freedom As An Evolutionary And Multidimensional Dimension.

- New Educational Scenarios In The Face Of Emerging Technological, Social, And Economic Challenges.

A Transdisciplinary Perspective Was Also Integrated, Connecting Theories From Behavioral Economics, Financial Psychology, Critical Education, And Economic Sociology. This Approach Made It Possible To Examine Not Only The Technical Factors Of Financial Management, But Also The Emotional, Cognitive, Cultural, And Structural Elements That Determine The Economic Decisions Of Individuals And Households (Rodríguez Et Al., 2024; Tan Et Al., 2025; Abdallah Et Al., 2025).

In Line With The Critical Perspective Of The Study, A Methodology Was Chosen That Not Only Gathered Information But Also Encouraged Reflection, Problematization, And The Proposal Of New Approaches To Teaching And Practicing Financial Education. Thus, This Analysis Constitutes Both A Theoretical And Applied Contribution Aimed At Strengthening The Design Of Educational Programs, Public Policies, And Autonomous Training Strategies In Financial Matters (See Figure 1).

Figure 1 Represents The Methodology Used In The Research, Organized Into Six Interrelated Components: (1) Approach And Design, (2) Analysis Technique, (3) Selection Of Sources, (4) Thematic Axes, (5) Transdisciplinary Perspective, And (6) Methodological Purpose. The Radial Layout Reflects The Integrative And Reflective Nature Of The Process, In Which Each Dimension Is Linked To The Others To Promote A Critical And Holistic Understanding Of Financial Education.

Based On This Methodology, The Following Section Presents A Discussion Of The Findings, Contrasting The Main Theoretical And Empirical Approaches Reviewed, As Well As Their Implications For Educational Practice And The Design Of Policies Aimed At Economic Well-Being And Financial Freedom.

4. Discussion

Based On The Documentary Analysis Carried Out, It Is Concluded That Financial Education Is A Transformative And Strategic Tool For Achieving Financial Freedom, Provided That It Is Conceived From A Comprehensive, Contextualized Approach Oriented Toward The Development Of Practical, Emotional, And Critical Skills. Unlike Traditional Approaches That Reduce Financial Education To The Technical Mastery Of Budgeting Tools Or Spending Control, This Study Argues That It Should Be Understood As A Formative Process Of Economic Empowerment, Autonomy, And The Construction Of Sustained Well-Being (Ahmed Et Al., 2021; Collins & Urban, 2020).

One Of The Central Findings Is That Persistent Financial Failures, Even In Contexts With Increasing Access To Information, Are Directly Related To Deficiencies In The Emotional And Cognitive Dimensions Of Financial Education, As Well As The Absence Of Pedagogical Strategies Focused On Experience And Critical Reflection. Recent Studies Confirm That Financial Literacy, While Necessary, Is Insufficient If It Is Not Linked To Attitudes, Self-Concept, And Risk Tolerance (Ahmed Et Al., 2021; Tiananta & Anwar, 2025). This Situation Has Limited The Scope Of Many Institutional Programs, Especially In Regions Characterized By High Inequality And Low Financial Inclusion (Rubio & León, 2025; Khan Et Al., 2022).

Likewise, Gaps Were Identified In The Attention Given To Elements Such As Financial Mindset, Limiting Beliefs, Economic Self-Concept, And Continuous Self-Education, Which Are Fundamental Dimensions For Achieving Sustainable And Conscious Financial Management. Research Shows That Family Communication And Early Financial Socialization Have A Decisive Influence On The Formation Of Habits And Attitudes Toward Money (Hanson & Olson, 2018), While Peer Pressure And Lifestyle Mediate Consumption And Economic Self-Perception In Young People (Murniawaty Et Al., 2024; Tiananta & Anwar, 2025). Effective Financial Education, Therefore, Should Not Only Teach How To Save Or Invest, But Also How To Think, Feel, And Decide In Relation To Money (She Et Al., 2024).

The Study Also Concludes That Financial Freedom Is Not Equivalent To The Accumulation Of Wealth, But Rather The Ability To Make Autonomous, Informed Economic Decisions That Are Aligned With One's Own Values And Life Goals. This Concept Implies Balance, Holistic Well-Being, A Long-Term Vision, And An Ethical Understanding Of The Role Of Money In Personal And Community Life (Riitsalu Et Al., 2024; Fan & Henager, 2022). Therefore, Promoting Critical And Proactive Financial Literacy Is Key To Transcending The Logic Of Survival And Moving Toward More Equitable And Sustainable Forms Of Economic Inclusion (Huang Et Al., 2022; Prakash & Hawaldar, 2024).

From A Public Policy Perspective, It Is Concluded That Financial Education Should Be Recognized As A Citizen’s Right, Formally Incorporated Into Education Systems From An Early Age, And Adapted To Different Sociocultural Contexts. To This End, It Is Essential To Strengthen Teacher Training, Develop Innovative Teaching Resources, And Promote Partnerships Between Public, Private, And Community Actors (Barua Et Al., 2018b; Spivak Et Al., 2024). Likewise, The Need To Include Digital Skills, Critical Thinking, And Emotional Self-Management Tools In Financial Education Programs Is Highlighted, Taking Advantage Of The Potential Of Technology-Mediated Education In Developing Countries (Menberu, 2024).

Among The Main Limitations Of This Study Is Its Documentary And Descriptive Nature, Which Restricts The Possibility Of Generalizing The Findings To Broader Empirical Contexts. Being Based On Secondary Sources, The Analysis Depends On The Quality, Timeliness, And Relevance Of The Literature Reviewed, Which May Leave Out Local Experiences Or Emerging Practices That Have Not Yet Been Systematized. Furthermore, The Absence Of Fieldwork Prevents The Direct Comparison Of Theoretical Proposals With The Actual Perceptions And Behaviors Of Individuals, Which Opens Up The Need For Future Empirical Studies To Validate And Deepen The Conclusions Presented Here (Collins & Urban, 2020; She Et Al., 2024).

Finally, This Study Opens Up Multiple Possibilities For Future Research. It Is Recommended To Advance Studies That Examine The Relationship Between Financial Education, Subjective Well-Being, And Economic Decision-Making, With An Emphasis On Variables Such As Gender, Age, Educational Level, Occupation, And Place Of Residence (Riitsalu Et Al., 2024; Prakash & Hawaldar, 2024). In Addition, It Is Pertinent To Design And Implement Experimental Programs That Integrate Emotions, Life Purpose, Sustainability, And Personal Leadership As Pillars Of Truly Transformative Financial Education (Huang Et Al., 2022; Khan Et Al., 2022).

In Short, Financial Education, Understood As A Process Of Comprehensive Human Development, Can Become A Realistic And Powerful Path To Financial Freedom, Provided That It Is Based On Respect For The Diversity Of Contexts, Recognition Of Each Person's Potential, And The Ethical Articulation Between Knowledge, Behavior, And Purpose (Rubio & León, 2025; Spivak Et Al., 2024).

5. Conclusions

Based On The Documentary Analysis Conducted, It Is Concluded That Financial Education Constitutes A Transformative And Strategic Tool For Achieving Financial Freedom, As Long As It Is Conceived From A Comprehensive, Contextualized Approach Oriented Toward The Development Of Practical, Emotional, And Critical Competencies. Unlike Traditional Approaches That Reduce Financial Education To The Technical Mastery Of Budgeting Tools Or Spending Control, This Study Argues That It Should Be Understood As A Formative Process Of Economic Empowerment, Autonomy, And The Construction Of Sustained Well-Being.

One Of The Central Findings Is That Persistent Financial Failures, Even In Contexts With Increasing Access To Information, Are Directly Related To Deficiencies In The Emotional And Cognitive Dimensions Of Financial Education, As Well As The Absence Of Pedagogical Strategies Centered On Experience And Critical Reflection (Zhang & Chatterjee, 2023; Mancone Et Al., 2024). This Situation Has Limited The Scope Of Many Institutional Programs, Especially In Regions Characterized By High Inequality And Low Financial Inclusion.

Likewise, Gaps Were Identified In The Attention Given To Elements Such As Financial Mindset, Limiting Beliefs, Economic Self-Concept, And Continuous Self-Education, Which Are Fundamental Dimensions For Achieving Sustainable And Conscious Financial Management. Effective Financial Education Should Not Only Teach How To Save Or Invest But Also How To Think, Feel, And Decide In Relation To Money. The Evidence Analyzed Shows That These Components Have Been Scarcely Considered In Previous Educational Solutions, Which Explains Their Limited Impact On The Actual Financial Behavior Of Individuals (Tiananta & Anwar, 2025; Murniawaty Et Al., 2024).

The Study Also Concludes That Financial Freedom Is Not Equivalent To The Accumulation Of Wealth, But Rather To The Ability To Make Autonomous And Informed Economic Decisions That Are Aligned With One’s Own Values And Life Goals. This Concept Implies Balance, Integral Well-Being, A Long-Term Vision, And An Ethical Understanding Of The Role Of Money In Personal And Community Life. Therefore, Promoting Critical And Proactive Financial Literacy Is Key To Transcending The Logic Of Survival And Moving Toward Fairer And More Sustainable Forms Of Economic Inclusion.

From A Public Policy Perspective, It Is Concluded That Financial Education Should Be Recognized As A Citizen’s Right, Formally Incorporated Into Educational Systems From Early Stages, And Adapted To Different Sociocultural Contexts. To This End, It Is Essential To Strengthen Teacher Training, Develop Innovative Didactic Resources, And Promote Partnerships Between Public, Private, And Community Actors (Spivak Et Al., 2024). Likewise, The Need To Include Digital Competencies, Critical Thinking, And Emotional Self-Management Tools In Financial Education Programs Is Emphasized.

Among The Main Limitations Of This Study, Its Documentary And Descriptive Nature Is Recognized, Which Restricts The Possibility Of Generalizing The Findings To Broader Empirical Contexts. Being Based On Secondary Sources, The Analysis Depends On The Quality, Timeliness, And Relevance Of The Literature Reviewed, Which May Exclude Local Experiences Or Emerging Practices That Have Not Yet Been Systematized. Similarly, The Absence Of Fieldwork Prevents The Direct Comparison Of Theoretical Proposals With Real Perceptions And Behaviors, Opening The Need For Future Empirical Studies That Validate And Deepen The Conclusions Presented Here.

Finally, This Study Opens Up Multiple Possibilities For Future Research. It Is Recommended To Advance Studies That Examine The Relationship Between Financial Education, Subjective Well-Being, And Economic Decision-Making, With An Emphasis On Variables Such As Gender, Age, Educational Level, Occupation, And Place Of Residence. Furthermore, It Is Pertinent To Design And Implement Experimental Programs That Integrate Emotions, Life Purpose, Sustainability, And Personal Leadership As Pillars Of Truly Transformative Financial Education.

In Short, Financial Education, Understood As A Process Of Integral Human Development, Can Become A Realistic And Powerful Pathway Toward Financial Freedom, Provided It Is Based On Respect For The Diversity Of Contexts, The Recognition Of Each Person’s Potential, And The Ethical Articulation Between Knowledge, Behavior, And Purpose.

References

- Abdallah, W. , Tfaily, F., Harraf. A. The Impact Of Digital Financial Literacy On Financial Behavior: Customers’ Perspective. Competitiveness Review 2025, 35, 347–370. [Google Scholar] [CrossRef]

- Abdul Ghafoor, K. , & Akhtar, M. Parents’ Financial Socialization Or Socioeconomic Characteristics: Which Has More Influence On Gen-Z’s Financial Wellbeing? Humanities And Social Sciences Communications 2024, 11, 522. [Google Scholar] [CrossRef]

- Ahmed, Z. , Noreen, U., Ramakrishnan, S. A., & Abdullah, D. F. B. What Explains The Investment Decision-Making Behaviour? The Role Of Financial Literacy And Financial Risk Tolerance. Afro-Asian Journal Of Finance And Accounting 2021, 11, 1–19. [Google Scholar] [CrossRef]

- Álvarez-Avad, N. , Braiz-Panduro, C., Pizzán-Tomanguillo, S.L., & Villafuerte De La Cruz, A.S. Financial Literacy And Credit Card Indebtedness Of Credit Card Customers Of Plaza Vea – Peru. Sapienza: International Journal Of Interdisciplinary Studies 2022, 3, 830–842. [Google Scholar] [CrossRef]

- Álvarez-Gayou Jurgenson, J. L. (2003). Cómo Hacer Investigación Cualitativa: Fundamentos Y Metodología.

- Asiah, A.N. , Haryono, A., & Churiyah, M. Financial Wellness Of Students In East Java: The Role Of Parental Financial Education, Financial Status, Financial Literacy, And Financial Behavior. Jurnal Ekonomi Pendidikan Dan Kewirausahaan 2024, 12, 297–326. [Google Scholar] [CrossRef]

- Atkinson, A. , & Messy, F. (2012). Measuring Financial Literacy: Results Of The OECD / International Network On Financial Education (INFE) Pilot Study, 15. [CrossRef]

- Atkinson, A. , & Messy, F. (2013). Promoting Financial Inclusion Through Financial Education: OECD/INFE Evidence, Policies And Practice. [CrossRef]

- Aydin, A.E. & Selcuk, E.A. An Investigation Of Financial Literacy, Money Ethics And Time Preferences Among College Students: A Structural Equation Model. International Journal Of Bank Marketing 2019, 37, 880–900. [Google Scholar] [CrossRef]

- Bado, B. , Hasan, M. , Tahir, T., & Hasbiah, S. How Do Financial Literacy, Financial Management Learning, Financial Attitudes And Financial Education In Families Affect Personal Financial Management In Generation Z? International Journal Of Professional Business Review 2023, 8, E02001. [Google Scholar] [CrossRef]

- Bai, R. Impact Of Financial Literacy, Mental Budgeting And Self Control On Financial Wellbeing: Mediating Impact Of Investment Decision Making. PLOS ONE 2023, 18, E0294466. [Google Scholar] [CrossRef]

- Barua, R. , Koh, B., & Mitchell, O. S. Does Financial Education Enhance Financial Preparedness? Evidence From A Natural Experiment In Singapore. Journal Of Pension Economics And Finance 2018, 17, 254–277. [Google Scholar] [CrossRef]

- Barua, R. , Shastry, G. K., & Yang, D. Financial Education For Female Foreign Domestic Workers In Singapore. Economics Of Education Review 2018, 78, 101920. [Google Scholar] [CrossRef]

- Brüggen, EC. , Hogreve, J., Holmlund, M., Kabadayi, S., & Löfgren, M. Financial Well-Being: A Conceptualization And Research Agenda. Journal Of Business Research 2017, 79, 228–237. [Google Scholar] [CrossRef]

- Bustamante, K.P. , & Cabrera, K.S. Microcrédito, Microempresa Y Educación En Ecuador. Caso De Estudio: Cantón Zamora. Revista Espacios, 1738. [Google Scholar]

- Cao-Alvira, J.J. , Novoa-Hoyos, A., & Núñez-Torres, A. On The Financial Literacy, Indebtedness, And Wealth Of Colombian Households. Review Of Development Economics 2021, 25, 978–993. [Google Scholar] [CrossRef]

- Collins, J.M. , & Urban, C. Measuring Financial Well-Being Over The Lifecourse. European Journal Of Finance 2020, 26, 341–359. [Google Scholar] [CrossRef]

- De Beckker, K.; De Witte, K.; Van Campenhout, G. Identifying Financially Illiterate Groups: An International Comparison. International Journal Of Consumer Studies 2019, 43, 490–501. [Google Scholar] [CrossRef]

- Desfrancois Fernand, P.G. La Educación Financiera Como Herramienta Para El Desarrollo De Hábitos Financieros Sostenibles En América Latina: La Educación Financiera Para El Desarrollo Financiero Sostenible. Mikarimin. Revista Científica Multidisciplinaria 2024, 10, 45–63. [Google Scholar] [CrossRef]

- Duhigg, C. (2012). The Power Of Habit: Why We Do What We Do In Life And Business. Random House, New York.

- Espino-Barranco, L.E. , Hernández-Calzada, M.A., & Pérez-Hernández, C.C. Educación Financiera En El Ecosistema Emprendedor. Investigación Administrativa 2021, 50, 12802. [Google Scholar] [CrossRef]

- Fan, L. , & Henager, R. A Structural Determinants Framework For Financial Well-Being. Journal Of Family And Economic Issues 2022, 43, 415–428. [Google Scholar] [CrossRef]

- Flick, U. (2014). An Introduction To Qualitative Research.

- Fraser, N. Reframing Justice In A Globalizing World. New Left Review 2005, 36, 69–88. [Google Scholar] [CrossRef]

- Gallo, G. , & Sconti, A. Could Financial Education Be A Universal Social Policy? A Simulation Of Potential Influences On Inequality Levels. Journal Of Accounting And Public Policy 2024, 46, 107231. [Google Scholar] [CrossRef]

- Garg, N. , & Singh, S. Financial Literacy Among Youth. International Journal Of Social Economics 2018, 45, 173–186. [Google Scholar] [CrossRef]

- Gulati, A. , & Singh, S. Financial Self-Efficacy Of Consumers: A Review And Research Agenda. International Journal Of Consumer Studies 2024, 48, E13024. [Google Scholar] [CrossRef]

- Gutiérrez-Andrade, O.W. , & Delgadillo-Sánchez, J.A. La Educación Financiera En Jóvenes Universitarios Del Primer Ciclo De Pregrado De La Universidad Católica Boliviana "San Pablo", Unidad Académica Regional De Cochabamba. Revista Perspectivas, /: 33-72. Recuperado De: Http, 1994. [Google Scholar]

- Hanson, T.A.; Olson, P.M. Financial Literacy And Family Communication Patterns. Journal Of Behavioral And Experimental Finance 2018, 19, 64–71. [Google Scholar] [CrossRef]

- Hernández-Pérez, J. , & Cruz-Rambaud, S. Uncovering The Factors Of Financial Well-Being: The Role Of Self-Control, Self-Efficacy, And Financial Hardship. Future Business Journal 2025, 11, 70. [Google Scholar] [CrossRef]

- Herrero, S. , Rubio, J., & León, M. Loans To Family And Friends And The Formal Financial System In Latin America. International Journal Of Financial Studies 2025, 13, 116. [Google Scholar] [CrossRef]

- Kaur, R. , & Singh, M. The Dynamics Of Family Financial Socialization: Impact On Financial Self-Efficacy And Financial Behavior. NMIMS Management Review 2024, 32, 106–117. [Google Scholar] [CrossRef]

- Khan, F. , Siddiqui, M. A., & Imtiaz, S. Role Of Financial Literacy In Achieving Financial Inclusion: A Review, Synthesis And Research Agenda. Cogent Business & Management 2022, 9, 2034236. [Google Scholar] [CrossRef]

- Khan, M.A. , Li, X., Lebaron-Black, A. B., & Serido, J. Socialización Financiera De Los Padres, Comportamientos Financieros Y Bienestar Entre Los Adultos Jóvenes De Hong Kong En Medio De La COVID-19. Relaciones Familiares 2023, 72, 2279–2296. [Google Scholar] [CrossRef]

- Kharel, K. R, Upadhyaya, Y.M., Acharya, B., Budhathoki, D.K., & Gyawali, A. Financial Literacy Among Management Students: Insights From Universities In Nepal. Knowledge And Performance Management 2024, 8, 63–73. [Google Scholar] [CrossRef]

- Kobsch, H. , Conrad, R., Goetze, M., Stricker, S. (2023). Digital Communication Strategies: The Impact Of Framing In Debt Collection Messages. In: Schmidt, C.M., Heinemann, S., Banholzer, V.M., Nielsen, M., Siems, F.U. (Eds) Soziale Themen In Unternehmens- Und Wirtschaftskommunikation. Europäische Kulturen In Der Wirtschaftskommunikation, Vol 35. Springer VS, Wiesbaden. [CrossRef]

- Leong, C. (2026). Navigating Sustainability In Digital Financial Services: Transforming The Future. In M. Ali, S. Raza, & C. Puah (Eds.), Emerging Trends And Innovations In Financial Services: A Futurology Perspective (Pp. 103-122). IGI Global Scientific Publishing. [CrossRef]

- López-Lapo, J.L. , Hernández Ocampo, S.E., Peláez Moreno, L.E., Sarmiento Castillo, G. Del P., Peña Vélez, M.J., Cueva Jiménez, N.C., & Sánchez Loor, J.P. Educación Financiera En América Latina. Ciencia Latina Revista Científica Multidisciplinar 2022, 6, 3810–3826. [Google Scholar] [CrossRef]

- López-Medina, T. , Mendoza-Ávila, I., Contreras-Barraza, N., Salazar-Sepúlveda, G., & Vega-Muñoz, A. (2022). Bibliometric Mapping Of Research Trends On Financial Behavior For Sustainability. Sustainability. [CrossRef]

- Lusardi, A. , & Mitchell, O. S. The Economic Importance Of Financial Literacy: Theory And Evidence. Journal Of Economic Literature 2014, 52, 5–44. [Google Scholar] [CrossRef]

- Lusardi, A. , & Tufano, P. Debt Literacy, Financial Experiences, And Overindebtedness. Journal Of Pension Economics & Finance 2015, 14, 332–368. [Google Scholar] [CrossRef]

- Mahendru, M. , Sharma, G.D., Hawkins, M. Toward A New Conceptualization Of Financial Well-Being. Journal Of Public Affairs 2022, 22, E2505. [Google Scholar] [CrossRef]

- Mancone, S. , Tosti, B., Corrado, S., Spica, G., Zanon, A., & Diotaiuti, P. Youth, Money, And Behavior: The Impact Of Financial Literacy Programs. Frontiers In Education 2024, 9, 1397060. [Google Scholar] [CrossRef]

- Masten, A.S. , Lucke, C.M., Nelson, K.M., & Stallworthy, I.C. Resilience In Development And Psychopathology: Multisystem Perspectives. Annual Review Of Clinical Psychology 2021, 17, 521–549. [Google Scholar] [CrossRef] [PubMed]

- Meier, S. , & Sprenger, C.D. Discounting Financial Literacy: Time Preferences And Participation In Financial Education Programs. Journal Of Economic Behavior & Organization 2013, 95, 159–174. [Google Scholar] [CrossRef]

- Menberu, A.W. Technology-Mediated Financial Education In Developing Countries: A Systematic Literature Review. Cogent Business & Management 2024, 11, 2294879. [Google Scholar] [CrossRef]

- Mihalcova, B. , Gallo, P., & Lukac, J. Management Of Innovations In Finance Education: Cluster Analysis For OECD Countries. Marketing And Management Of Innovations 2020, 1, 235–244. [Google Scholar] [CrossRef]

- Moazezi Khah Tehran, A. , Hassani, A. , Mohajer, S., Darvishan, S., Shafiesabet, A., & Tashakkori, A. The Impact Of Financial Literacy On Financial Behavior And Financial Resilience With The Mediating Role Of Financial Self-Efficacy. International Journal Of Industrial Engineering And Operational Research 2025, 7, 38–55. [Google Scholar] [CrossRef]

- Mouffe, C. Deliberative Democracy Or Agonistic Pluralism? Social Research 2000, 66, 745–758. [Google Scholar]

- Mungaray, A. , Gonzalez, N., & Osorio, G. Educación Financiera Y Su Efecto En El Ingreso En México. Problemas Del Desarrollo. Revista Latinoamericana De Economía 2021, 52, 55–78. [Google Scholar] [CrossRef]

- Murniawaty, I. , Sangadah, N., Pujiati, A., Prasetyo, P. E., & Suryanto, E. Does Peer Conformity Have Moderating Effects On University Students’ Consumptive Behavior? A Focus On Self-Concept, Economic Literacy, And E-Money Adoption. Innovative Marketing 2024, 20, 25–40. [Google Scholar] [CrossRef]

- Netemeyer, R.G. , Lynch, J.G., Lichtenstein, D.R., & Dobolyi, D. Financial Education Effects On Financial Behavior And Well-Being: The Mediating Roles Of Improved Objective And Subjective Financial Knowledge And Parallels In Physical Health. Journal Of Public Policy & Marketing 2024, 43, 254–275. [Google Scholar] [CrossRef]

- Noh, M. Effect Of Parental Financial Teaching On College Students’ Financial Attitude And Behavior: The Mediating Role Of Self-Esteem. Journal Of Business Research 2022, 143, 298–304. [Google Scholar] [CrossRef]

- Nourallah, M. , Chan, H.R., Chien, C.-L., & Öhman, P. Financial Capability, Behavior, Well-Being, And Stress Among Financial Advisors. Financial Planning Review 2025, 8, E70002. [Google Scholar] [CrossRef]

- Nussbaum, M. C. (2011). Creating Capabilities: The Human Development Approach.

- OECD. (2014). PISA 2012 Results: Financial Literacy Skills For The 21st Century.

- OECD. (2017). G20/OECD INFE Report On Adult Financial Literacy In G20 Countries.

- Pandey, A. , & Utkarsh. Determinants Of Positive Financial Behavior: A Parallel Mediation Model. International Journal Of Emerging Markets 2024, 19, 4073–4093. [Google Scholar] [CrossRef]

- Prakash, N. , & Hawaldar, A. Investigating The Determinants Of Financial Well-Being: A SEM Approach. Business Perspectives And Research 2024, 12, 11–25. [Google Scholar] [CrossRef]

- Pulungan, A.H. , Abdurrahman, D.A., Canara, B., & Ramadhan, R. The Impact Of Parental Financial Teaching On University Students’ Financial Attitudes: The Mediating Role Of Self-Control. Jurnal Pendidikan Bisnis Dan Manajemen 2024, 10, 43–57. [Google Scholar] [CrossRef]

- Quibra, R.K. Financial Knowledge, Behavior, And Attitude On The Financial Well-Being Of The Sustainable Livelihood Program Associations. Revista De Gestão - RGSA 2024, 18, E06225. [Google Scholar] [CrossRef]

- Ramon-Arteaga, B. D. , & Malla-Alvarado, F. Y. Incidencia De La Educación Financiera En Los Comerciantes Del Centro De Transferencia Comercial Mayorista Puerto Seco. Ciencia Latina Revista Científica Multidisciplinar 2022, 6, 4178–4200. [Google Scholar] [CrossRef]

- Rani, R. , (2023). The Impact Of Financial Literacy On Financial Well-Being: The Meditational Role Of Personal Finance Management, 6th International Conference On Contemporary Computing And Informatics (IC3I), Gautam Buddha Nagar, India, 2023, Pp. 2350-2355. [CrossRef]

- Riitsalu, L. , Sulg, R., Lindal, H., Remmik, M., & Vain, K. From Security To Freedom— The Meaning Of Financial Well-Being Changes With Age. Journal Of Family And Economic Issues. [CrossRef]

- Rodríguez, V. , Vílchez, P.A., Oscanoa, B.F., & Barrantes, A.M. Educación Financiera Con Enfoque Conductual Y Mitigación De Sesgos En Decisiones Crediticias. Revista Venezolana De Gerencia 2024, 29, 1560–1578. [Google Scholar] [CrossRef]

- Rubio, J. , & León, M. Financial Inclusion As A Pathway To Poverty Alleviation And Equality In Latin America: An Empirical Analysis. Journal Of Risk And Financial Management 2025, 18, 392. [Google Scholar] [CrossRef]

- Sangeeta, Aggarwal P. K., Sangal A. Determinants Of Financial Literacy And Its Influence On Financial Wellbeing — A Study Of The Young Population In Haryana, India. Finance: Theory And Practice 2022, 26, 121–131. [Google Scholar] [CrossRef]

- Sconti, A. , Caserta, M., & Ferrante, L. Gen Z And Financial Education: Evidence From A Randomized Control Trial In The South Of Italy. Journal Of Behavioral And Experimental Economics 2024, 112, 102256. [Google Scholar] [CrossRef]

- Sen, A. (1999). Development As Freedom.

- She, L. , Ma, L., Pahlevan Sharif, S., & Karim, S. Millennials’ Financial Behaviour And Financial Well-Being: The Moderating Role Of Future Orientation. Journal Of Financial Services Marketing 2024, 29, 1207–1224. [Google Scholar] [CrossRef]

- Spivak, I. , Mihus, I., & Greben, S. Financial Literacy And Government Policies: An International Study. Public Administration And Law Review 2024, 2, 21–33. [Google Scholar] [CrossRef]

- Tan, X. , Xiao, J.J., Meng, K., Xu, J. Financial Education And Budgeting Behavior Among College Students: Extending The Theory Of Planned Behavior. International Journal Of Bank Marketing 2025, 43, 506–521. [Google Scholar] [CrossRef]

- Tang, N. , & Baker, A. Self-Esteem, Financial Knowledge And Financial Behavior. Journal Of Economic Psychology 2016, 54, 164–176. [Google Scholar] [CrossRef]

- Tiananta, S. A. M. L. , & Anwar, M. Lifestyle Mediates Financial Attitudes And Self-Concept In Student Consumption. Academia Open 2025, 10, 11237. [Google Scholar] [CrossRef]

- Vieira, K.M. , Delanoy, M.M., Potrich, A.C.G., & Bressan, A.A. Financial Citizenship Perception (FCP) Scale: Proposition And Validation Of A Measure. International Journal Of Bank Marketing 2021, 39, 127–146. [Google Scholar] [CrossRef]

- Vieira, K.M. , Potrich, A.C.G., Matheis, T.K., & De Carvalho Puhle, M. Perception Of Financial Freedom: Is Financial Literacy A Relevant Background? International Review Of Economics 2025, 72, 13. [Google Scholar] [CrossRef]

- World Bank Group. (2013). Global Financial Development Report 2014: Financial Inclusion (Vol. 2). Washington, DC: World Bank Publications.

- Zelenova, K. , Raine, B., Chen, R., Williams, R.E., Davis, A.E., Loree, T., Burke, M., Nagai, M., & Frey, J. Twelve Steps To Financial Freedom For Plastic Surgeons. Plastic And Reconstructive Surgery. Global Open 2023, 11, E4990. [Google Scholar] [CrossRef]

- Zhang, Y. , & Chatterjee, S. Financial Well-Being In The United States: The Roles Of Financial Literacy And Financial Stress. Sustainability 2023, 15, 4505. [Google Scholar] [CrossRef]

- Zhu, A.Y.F. Upgrading Financial Education By Adding Python-Based Personalized Financial Projection: A Randomized Control Trial. British Journal Of Educational Technology 2024, 55, 731–750. [Google Scholar] [CrossRef]

- Zhu, T. , & Xiao, J. J. Consumer Financial Education And Risky Financial Asset Holding In China. International Journal Of Consumer Studies 2022, 46, 56–74. [Google Scholar] [CrossRef]

Figure 1.

Methodological Outline Of The Study (Radial Model).

Table 1.

Evolutionary Map Of The Theoretical Framework.

| Apartado | Ideas Clave | Referencias Principales | Transición Evolutiva |

| 2.1 Financial Education As A Transformative Asset | From A Technical Vision To A Comprehensive Vision. Competencies: Knowledge, Skills, Attitudes, And Behaviors. Gaps In Latin America: Low Literacy Levels, Inequality, And Exclusion. Financial Education As Inclusion And Social Justice. |

Atkinson & Messy (2012, 2013); OECD (2014); Aydin & Selcuk (2019); Zhu & Xiao (2022); De Beckker Et Al. (2019); Mungaray Et Al. (2021); Asiah Et Al. (2024); Pulungan Et Al. (2024); Barua Et Al. (2018); Quibra, (2024). | It Paves The Way For Understanding That Technical Knowledge Is Not Enough: Psychological And Emotional Factors Must Also Be Integrated. |

| 2.2 Mindset And Psychology Of Money | Psychological, Emotional, And Social Factors Influence Decisions. Cognitive Biases And Limiting Beliefs. Dimensions: Reprogramming Beliefs, Economic Self-Concept, Financial Self-Education. Impact On Young People And Generational Differences. |

Khan Et Al. (2023); Noh (2022); Bai (2023); Asiah Et Al. (2024); Pandey & Utkarsh (2024); Quibra, (2024); Gutiérrez-Andrade & Delgadillo-Sánchez (2018); Abdul & Akhtar (2024); (Pandey & Utkarsh, (2024); Duhigg (2012); Vieira Et Al. (2021); Lusardi & Tufano (2015); Kharel Et Al. (2024); Pulungan Et Al. (2024). |

Leads To Concrete Practices: How These Beliefs And Attitudes Are Reflected In Saving, Investing, And Resource Management. |

| 2.3 Smart Saving And Investing | Systematic Saving As The Basis For Stability. Investment As Financial Maturity: Risk, Knowledge, And Opportunity. Principle Of The “Circle Of Competence.” Digital Risks: Speculation, Fraud, Overexposure To Networks. Sustainable And Ethical Finance. |

Ramon-Arteaga & Malla-Alvarado (2022); Zhang, & Chatterjee (2023); Pulungan Et Al. (2024); Zelenova Et Al. (2023); Leong (2026); Mihalcova Et Al. (2020); Asiah Et Al. (2024); Zelenova Et Al. (2023). | Opens Up The Discussion On How Resource Management Is Conditioned By Debt And How This Can Be An Obstacle Or Lever Toward Financial Freedom. |

| 2.4 Debt And Financial Freedom | Debt As An Obstacle When Managed Without Planning. Debt As A Leverage Tool If Used Strategically. Financial Freedom As A Comprehensive And Evolving Process. Psychological Well-Being And Social Justice. Financial Citizenship As A Right. |

Ramon-Arteaga & Malla-Alvarado (2022); Cao-Alvira Et Al. (2021); Zhang & Chatterjee (2023); Herrero Et Al. (2025); Asiah Et Al. (2024); Pulungan Et Al. (2024); Brüggen Et Al. (2017); Álvarez-Avad Et Al. (2022); Tang & Baker (2016); Vieira Et Al. (2021); Sangeeta Et Al. (2022); Bustamante & Cabrera (2017); López-Medina Et Al. (2022); (Herrero Et Al. (2025); Zhang & Chatterjee (2023); Nussbaum (2011); Nourallah Et Al. (2025). |

Looks Ahead To Future Scenarios: How Financial Education Must Adapt To Digitalization, Inequality, And Sustainability. |

| 2.5 New Scenarios: Financial Education For The Future | Challenges Of Digitalization, Fintech, And Inequality. Limitations Of Traditional Programs. Transdisciplinary Approach: Sustainability, Innovation, Consumer Ethics. Financial Education As A Citizen's Right And Public Policy. Digital Self-Education And Economic Resilience. |

Zhu (2024); Mihalcova Et Al. (2020); Zelenova Et Al. (2023); Ramon-Arteaga & Malla-Alvarado (2022); Gallo & Sconti (2024); Vieira Et Al. (2025); World Bank Group (2013); Espino-Barranco (2021); López-Lapo Et Al. (2022). | Close The Flow By Showing The Need To Reinvent Financial Education As A Tool For Personal Transformation, Economic Justice, And Social Sustainability. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.