Submitted:

11 November 2025

Posted:

13 November 2025

You are already at the latest version

Abstract

Artificial intelligence (AI) is transforming accounting by automating cognitive tasks and redefining mechanisms of governance and risk control. This study examines how AI operates as an intelligent control system—one that substitutes manual accounting procedures while enhancing transparency, internal control, and fraud detection. Inte-grating the Technology Acceptance Model (TAM) with Organizational Information Processing Theory (OIPT), the research develops a behavioral–organizational frame-work linking perceived usefulness, ease of use, AI literacy, technology readiness, social influence, and facilitating conditions to AI adoption and perceived substitution bene-fits. A structured survey was administered to accounting students and practitioners in Northern Italy (n = 185) and analyzed through reliability tests and partial least squares structural equation modeling (PLS-SEM). The results show that AI literacy, facilitating conditions, and social influence significantly drive adoption intention, while perceived substitution benefits fully mediate the relationship between adoption and governance outcomes. The findings demonstrate that AI adoption enhances governance and risk-management effectiveness by functioning as an intelligent control mechanism. The study introduces the AI-to-Control (A2C) Blueprint to guide responsible integra-tion of AI into accounting systems, reframing AI adoption as a structural evolution in corporate governance rather than a mere technological upgrade.

Keywords:

artificial intelligence (AI)

; accounting governance

; risk management

; technology acceptance model (TAM)

; Italy

1. Introduction

The accounting profession is experiencing a profound structural transformation as digital technologies increasingly redefine the boundaries between human judgment and algorithmic intelligence. Among these technologies, artificial intelligence (AI) stands out as the most disruptive, capable of automating not only repetitive procedures but also advanced cognitive tasks such as interpretation, anomaly detection, and decision support. Unlike earlier phases of digitization that focused primarily on efficiency gains, AI introduces adaptive learning and reasoning, reshaping how accountants interact with data, exercise control, and uphold governance standards. Its implications for corporate governance, internal control, and the prevention of earnings manipulation are far-reaching, as algorithms begin to underpin assurance and compliance processes once dependent solely on human expertise. Consequently, accounting is moving from manual to intelligent practice, where analytical reasoning and oversight functions are increasingly performed by intelligent systems.

Despite the promises of AI, its adoption within accounting remains uneven across countries, industries, and organizational sizes. Large audit and consulting firms have embraced AI-driven auditing, predictive analytics, and fraud detection, while smaller entities and educational institutions often continue to rely on traditional methods. This asymmetry raises critical questions about perceived usefulness, ease of use, and readiness for integrating AI into established workflows. Moreover, as AI begins to automate oversight and verification functions, its influence extends beyond operational efficiency to touch upon accountability, transparency, and risk-management quality. Understanding these dynamics is especially relevant under growing regulatory scrutiny and ethical debates over algorithmic decision-making.

AI applications in accounting, from automated journal entry validation to natural-language analysis of financial disclosures, aim to reduce human error and accelerate reporting cycles. Yet these innovations challenge professional identities grounded in judgment, independence, and fiduciary responsibility. The resulting tension between innovation and control defines an unresolved research gap: can AI truly substitute, rather than merely support, conventional accounting practices—and how does this substitution affect perceptions of governance and risk management? Existing research in advanced economies links AI to analytical improvements and enhanced assurance quality but also warns of new sources of ethical and operational risk. In the European mid-market context, particularly Italy, adoption patterns are shaped by institutional conditions, educational readiness, and organizational culture. The Italian setting offers an ideal testbed: a strong professional tradition intersects with increasing digitalization among universities and small-to-medium enterprises, allowing investigation into how accountants and students evaluate AI’s substitution potential within entrenched governance frameworks.

To address these questions, this study integrates two complementary theoretical perspectives. The Technology Acceptance Model (TAM) (Davis, 1989) explains behavioral intention to adopt technology through perceived usefulness and ease of use, while the Organizational Information Processing Theory (OIPT) (Galbraith, 1973) conceptualizes technology adoption as an adaptive response to environmental complexity. Combined, they frame AI adoption as both an individual behavioral choice and an organizational adaptation mechanism. The study introduces perceived substitution benefit—the belief that AI can effectively replace manual accounting processes—as a bridging construct linking behavioral intention (TAM) to governance and risk outcomes (OIPT). This integrated approach connects acceptance determinants with the organizational consequences of AI adoption, offering a multi-level perspective on intelligent control in accounting.

The current literature on digital transformation provides substantial evidence on adoption drivers but offers limited empirical exploration of how AI’s substitution effects translate into governance outcomes. Prior studies have largely examined technical implementation or educational attitudes without assessing the influence of AI on internal control reliability, fraud detection, or earnings-management prevention. Moreover, comparative evidence from Southern Europe remains scarce. This research addresses these gaps through survey-based evidence from Italy, employing partial least squares structural equation modeling (PLS-SEM) to analyze the interrelations between behavioral adoption constructs, substitution perceptions, and perceived governance outcomes. The findings extend TAM by introducing substitution benefit as a mediator between AI adoption and governance quality and enrich OIPT by showing how AI strengthens information-processing capacity, thereby functioning as a governance mechanism rather than a mere efficiency tool.

In essence, the study contributes to theory and practice by reframing AI not simply as a technological upgrade but as a transformation in governance architecture—where intelligent systems become instruments of accountability and ethical oversight. The results hold practical relevance for educators, policymakers, and practitioners seeking to foster responsible AI integration in accounting. The remainder of the paper is organized as follows: Section 2 reviews the relevant literature and formulates hypotheses; Section 3 describes the research design and analytical methods; Section 4 presents the empirical results; Section 5 discusses theoretical and practical implications; and Section 6 concludes with policy recommendations and directions for future research.

2. Literature Review and Hypotheses Development

Artificial intelligence (AI) is redefining accounting by transforming labor-intensive, rule-based procedures into intelligent, data-driven systems capable of prediction, reasoning, and decision support. The latest multivocal literature review by Roos et al. (2025) shows that the success of AI implementation depends on adequate IT infrastructure, data quality, regulatory compliance, and employee upskilling. Their review concludes that AI contributes to efficiency gains and higher analytical accuracy in tasks such as invoice processing, anomaly detection, financial forecasting, and tax compliance. In parallel, Odonkor et al. (2024) emphasize that AI improves accuracy, timeliness, and fraud detection in financial reporting, although high costs, skills shortages, and data-governance concerns still limit adoption. Collectively, these studies illustrate how AI has evolved from a simple automation tool into a mechanism for governance, transparency, and accountability. Earlier research also points to the complementary role of emerging technologies such as robotic process automation (RPA), cloud computing, and blockchain. Leitner-Hanetseder et al. (2021) highlight that AI can extend RPA by incorporating adaptive learning, thereby automating cognitive functions and improving financial-reporting reliability. Kureljusic and Karger (2023) further identify predictive analytics and machine-learning models as essential tools for modern accounting forecasting, stressing that data-driven approaches improve precision in audit planning and valuation. These findings confirm that AI integration enhances both operational performance and the strategic dimension of accounting.

At the individual level, the Technology Acceptance Model (TAM) (Davis, 1989) and its later extensions—TAM2, UTAUT, and UTAUT2—remain the most robust frameworks for predicting technology adoption. The 2025 Vietnamese study by Bui et al. demonstrates that perceived usefulness (PU), perceived ease of use (PEOU), AI literacy (AL), technology readiness (TR), social influence (SI), and facilitating conditions (FC) are all significant determinants of AI adoption among accounting students. Using partial least squares structural equation modeling (PLS-SEM), their model revealed that SI strengthens the relationship between PEOU and adoption, implying that peer and institutional encouragement accelerates behavioral change. This behavioral evidence aligns with the findings of Damerji and Salimi (2021), who showed that technology readiness and user perceptions mediate AI adoption in accounting. Sudaryanto et al. (2023) confirmed that TR and digital competence are key antecedents of PU and PEOU in technology adoption models. These studies collectively suggest that AI adoption in accounting depends not only on technical availability but also on cognitive and social factors that influence individual intention. AI literacy, defined as the ability to understand and apply AI principles in decision-making (Ng et al., 2021), has emerged as a powerful predictor of acceptance. Dai et al. (2020) argue that AI literacy fosters readiness for the AI age by increasing confidence in algorithmic interpretation, while Chen et al. (2022) found that AI literacy enhances self-efficacy and perceived usefulness. In accounting education, incorporating AI literacy into curricula improves future accountants’ capability to work with data analytics tools (Kong et al., 2021; Lin et al., 2021). Therefore, behavioral acceptance and competence development are intertwined in shaping AI integration.

While TAM explains technology use at the individual level, the Organizational Information Processing Theory (OIPT) provides an organizational lens by linking information-processing capacity with environmental uncertainty (Galbraith, 1973). OIPT posits that organizations adopt richer information systems to handle complex data and improve decision quality. Recent evidence from Abu Afifa et al. (2024) in Vietnam shows that digital transformation and transformational leadership (TL) both significantly influence AI integration in accounting. Their PLS-SEM results (β_DT→AI = 0.42; β_TL→AI = 0.45; R² = 0.66) reveal that transformational leadership moderates the relationship between digital transformation and AI adoption, amplifying organizational adaptation. These results confirm that AI can act as a governance instrument—improving transparency, internal control, and accountability—when supported by digital infrastructure and leadership commitment. This perspective is consistent with global research linking digital transformation to information-processing enhancement. Singh et al. (2021) demonstrate that digital transformation improves flexibility, integration, and efficiency in manufacturing contexts. Similarly, Dubey et al. (2020) found that big data analytics and AI collectively boost operational performance by aligning information flows with decision needs. From an OIPT standpoint, AI functions as an advanced processing system that transforms accounting data into predictive insights, reducing uncertainty in governance and risk management.

A new dimension gaining traction is the perceived substitution benefit (PSB)—the belief that AI can replace manual accounting processes while improving governance outcomes. Roos et al. (2025) identify PSB as a critical bridge between technological adoption and process reengineering, emphasizing that AI can substitute repetitive, data-intensive tasks such as reconciliations and invoice matching while augmenting human oversight. In practice, PSB reflects a shift from augmentation to intelligent substitution, where AI complements rather than competes with professional judgment (Lehner et al., 2022; Odonkor et al., 2024). Empirical studies show that substitution perceptions directly affect behavioral intention. Bui et al. (2025) note that students with higher AI literacy perceive stronger substitution benefits, believing that AI can automate low-value operations and enhance decision quality. These perceptions correspond to the finding by Abu Afifa et al. (2024) that organizational readiness and leadership vision determine whether substitution produces efficiency without compromising ethical accountability. Consequently, PSB acts as a mediator connecting TAM variables (PU, PEOU) with OIPT outcomes (governance and risk control).

AI’s impact extends beyond efficiency into the domain of governance and risk management. Numerous studies identify AI as a governance enabler that strengthens internal control systems and reduces the scope for earnings manipulation (Zhang et al., 2023; Schweitzer, 2024). Noordin et al. (2022) demonstrate that AI tools enhance audit quality by improving data reliability and fraud detection. Peng et al. (2023) link AI adoption to several Sustainable Development Goals by enhancing transparency, compliance, and decision-making speed. Nevertheless, ethical and regulatory issues persist. Lehner et al. (2022) caution that algorithmic bias and opacity may threaten trust in financial reporting, while Pierotti et al. (2024) stress that data-protection and auditability mechanisms are prerequisites for responsible AI use. These findings underscore that AI’s governance potential must be balanced with ethical oversight, clear accountability, and professional skepticism. The convergence of AI ethics, governance, and information assurance forms the foundation of the intelligent control framework proposed in this study.

Based on the integrated TAM–OIPT framework and prior empirical evidence, the following hypotheses are formulated: H1a: Facilitating conditions (FC) are positively associated with perceived usefulness (PU). H1b: Facilitating conditions (FC) are positively associated with perceived ease of use (PEOU). H1c: Facilitating conditions (FC) are positively associated with AI adoption (Bui et al., 2025). H2a: AI literacy (AL) is positively associated with perceived usefulness (PU). H2b: AI literacy (AL) is positively associated with perceived ease of use (PEOU). H2c: AI literacy (AL) is positively associated with AI adoption (Dai et al., 2020; Chen et al., 2022; Bui et al., 2025). H3a: Technology readiness (TR) is positively associated with perceived usefulness (PU). H3b: Technology readiness (TR) is positively associated with perceived ease of use (PEOU). H3c: Technology readiness (TR) is positively associated with AI adoption (Damerji & Salimi, 2021; Sudaryanto et al., 2023). H4: Perceived usefulness (PU) positively influences AI adoption (Davis, 1989; Bui et al., 2025). H5: Perceived ease of use (PEOU) positively influences AI adoption (Damerji & Salimi, 2021). H6a: Social influence (SI) positively affects AI adoption. H6b: The relationship between PEOU and AI adoption is stronger under high social influence (Bui et al., 2025). H7: Perceived substitution benefit (PSB) mediates the relationship between AI adoption and governance/risk-management outcomes (Roos et al., 2025; Odonkor et al., 2024). H8: AI adoption positively affects perceived governance and risk-management outcomes (Abu Afifa et al., 2024).

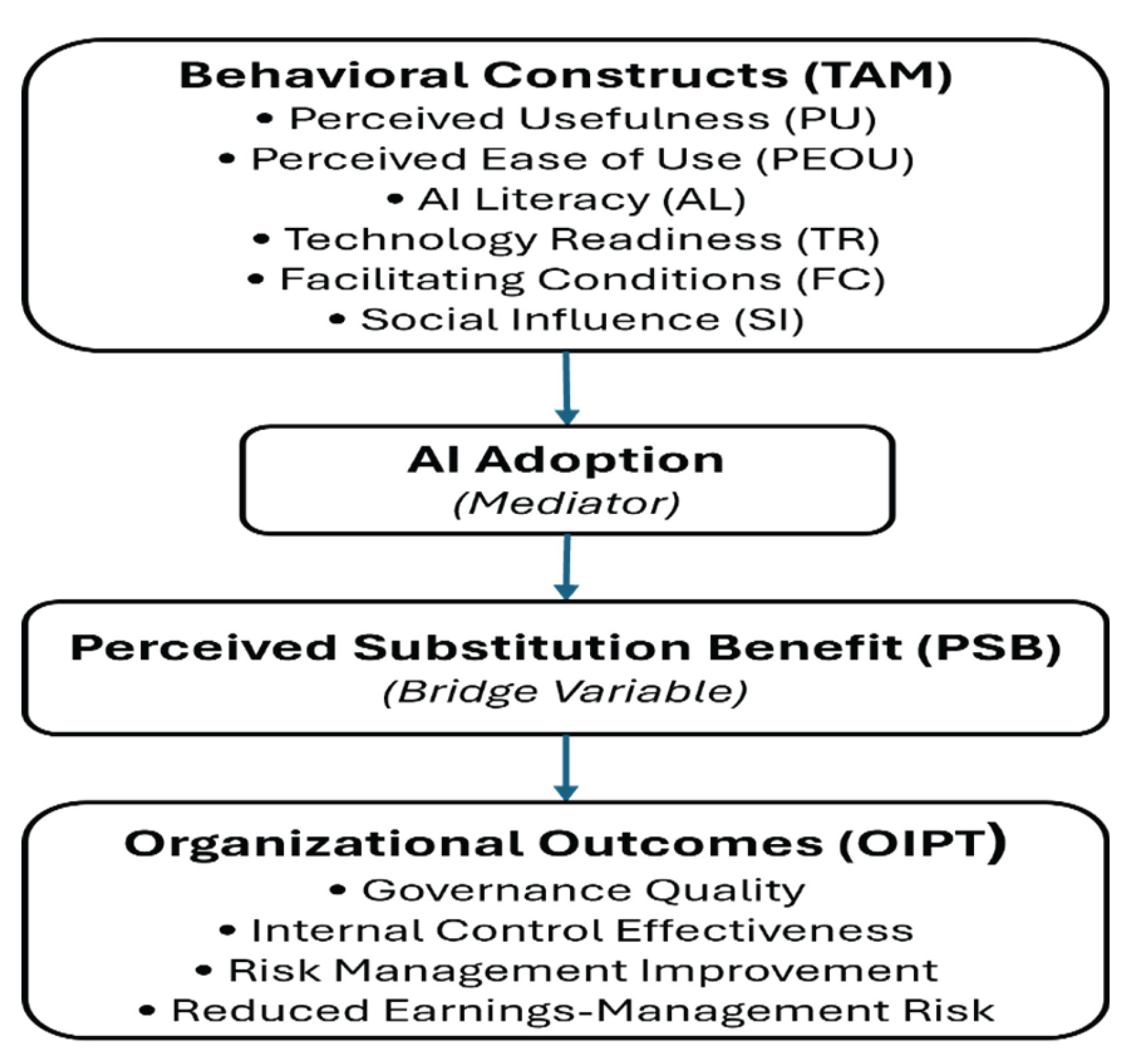

Drawing on the reviewed literature, the conceptual model integrates TAM’s behavioral constructs—PU, PEOU, AL, TR, FC, and SI—with OIPT’s organizational outcomes. The model posits that AI adoption mediates the influence of cognitive and environmental factors on governance and risk-management outcomes, while perceived substitution benefit acts as a mechanism translating behavioral intention into governance impact. This framework reflects the dual nature of AI in accounting: a behavioral innovation process at the individual level and an organizational adaptation mechanism enhancing control and transparency.

Figure 1.

Conceptual Model: AI Adoption, Substitution Effects, and Governance Outcomes. Caption: The model links behavioral determinants from the Technology Acceptance Model (TAM)—Perceived Usefulness (PU), Perceived Ease of Use (PEOU), AI Literacy (AL), Technology Readiness (TR), Facilitating Conditions (FC), and Social Influence (SI)—to organizational outcomes grounded in the Organizational Information Processing Theory (OIPT). AI Adoption functions as a mediator, and Perceived Substitution Benefit (PSB) serves as a bridge variable translating behavioral intention into governance impact. Organizational outcomes (OIPT) include Governance Quality, Internal Control Effectiveness, Risk Management Improvement, and Reduced Earnings-Management Risk.

Figure 1.

Conceptual Model: AI Adoption, Substitution Effects, and Governance Outcomes. Caption: The model links behavioral determinants from the Technology Acceptance Model (TAM)—Perceived Usefulness (PU), Perceived Ease of Use (PEOU), AI Literacy (AL), Technology Readiness (TR), Facilitating Conditions (FC), and Social Influence (SI)—to organizational outcomes grounded in the Organizational Information Processing Theory (OIPT). AI Adoption functions as a mediator, and Perceived Substitution Benefit (PSB) serves as a bridge variable translating behavioral intention into governance impact. Organizational outcomes (OIPT) include Governance Quality, Internal Control Effectiveness, Risk Management Improvement, and Reduced Earnings-Management Risk.

Building on this integrative framework, the next section details the research design, measurement model, and data collection strategy used to empirically test the hypothesized relationships in the Italian context. This methodological transition connects the conceptual logic of AI as an intelligent control with its operationalization through validated behavioral and governance constructs.

3. Materials and Methods

This section describes the empirical approach in sufficient detail to ensure replicability and transparency, outlining the research design, measurement strategy, data collection procedures, and analytical steps employed to test the integrated TAM–OIPT framework. The study follows standard guidelines for quantitative research in behavioral and organizational accounting.

The investigation employs a quantitative, cross-sectional, hybrid design that integrates behavioral and organizational perspectives to examine how artificial intelligence (AI) functions as an intelligent control in accounting. The model combines the Technology Acceptance Model (TAM)—capturing individual behavioral intention toward AI adoption—with the Organizational Information Processing Theory (OIPT), which conceptualizes AI as an information-processing and governance mechanism. This integrative approach enables simultaneous assessment of how perceptions such as usefulness, ease of use, literacy, readiness, and social influence translate into governance and risk-management outcomes. The design bridges micro-level behavioral determinants and macro-level control implications, reflecting the hybrid nature of AI’s transformation of accounting systems.

Data were collected from accounting students and professionals located in Northern Italy, representing universities, professional orders, and small- to medium-sized enterprises. A structured questionnaire was distributed online via Google Forms during October 2025. Participation was voluntary, and responses were recorded anonymously. After screening for completeness and consistency, 185 valid questionnaires were retained for analysis. Approximately two-thirds of respondents were accounting or finance students and one-third practitioners, providing both an educational and professional viewpoint on AI adoption. All respondents confirmed prior exposure to accounting or auditing activities for at least six months. The final sample size satisfies minimum thresholds for PLS-SEM estimation, exceeding the ten-times rule for the most complex regression path (Hair et al., 2019).

As shown in Table 1, the instrument comprised 31 reflective Likert-type items (1 = Strongly Disagree, 5 = Strongly Agree) organized into nine constructs adapted from validated prior studies. The complete list of constructs, item codes, and sample questions is provided in Appendix A, along with contextual vignettes and demographic controls.

Each block captures a theoretical dimension of the integrated TAM–OIPT framework. Behavioral constructs (PU, PEOU, AL, TR, SI, FC) measure cognitive and contextual determinants of AI adoption, whereas PSB, AI_INT, and GRO extend the model toward substitution and governance outcomes.

Data were analyzed using IBM SPSS following standard PLS-SEM stages (Hair et al., 2019). The process involved (1) pre-analysis to screen for missing values and outliers, ensuring all items met normality assumptions (|skewness| < 2); (2) computation of descriptive statistics and reliability indices; (3) measurement-model evaluation based on indicator loadings, composite reliability (CR > 0.70), and average variance extracted (AVE > 0.50) to confirm convergent validity; (4) assessment of discriminant validity using the Fornell–Larcker and HTMT criteria; (5) evaluation of the structural model to estimate path coefficients, R², and f² values; and (6) bootstrapping (5,000 resamples) to determine significance levels. Mediation effects were tested by examining the indirect influence of Perceived Substitution Benefit (PSB) between AI Adoption (AI_INT) and Governance Outcomes (GRO) through bias-corrected bootstrapping.

As shown in Table 2, the descriptive results indicate that mean scores across all behavioral constructs exceed 3.5, reflecting generally positive perceptions toward AI in accounting. Cronbach’s α values mostly surpass 0.70, confirming acceptable internal consistency for exploratory research. The relatively high means for PU and TR suggest that respondents recognize the utility of AI and perceive themselves as technologically prepared. Lower reliability for AI Literacy reflects heterogeneous understanding of AI principles, typical of a mixed student–practitioner sample. Overall, the results validate the suitability of the dataset for PLS-SEM analysis.

Participation was voluntary and anonymous, with no personally identifying data collected. Respondents were informed that their answers would be used exclusively for academic purposes and could withdraw at any time. The study followed institutional ethical guidelines and adhered to the principles of responsible research conduct. The anonymized dataset supporting this study has been deposited in Zenodo under the title “AI as an Intelligent Control: Survey Data from Italy on Accounting Governance and Risk Management.” It is publicly available at https://doi.org/10.5281/zenodo.17562178. GenAI tools were not employed in the generation, analysis, or interpretation of data in this study. Their use was limited solely to language polishing and formatting to enhance readability without influencing the substance or results of the research.

4. Results

The following section presents the empirical outcomes derived from the PLS-SEM analysis, translating the theoretical framework and measurement design into quantitative evidence on how AI adoption functions as an intelligent control within the Italian accounting context.

4.1. Overview of Analysis

Partial Least Squares Structural Equation Modeling (PLS-SEM) was applied using the 185 valid responses from the Italian survey. The analysis followed a two-stage process: (1) assessment of the measurement model for reliability and validity, and (2) evaluation of the structural model to test the hypotheses derived from the integrated TAM–OIPT framework.

4.2. Measurement-Model Assessment

All standardized loadings exceeded the 0.60 threshold, confirming that individual items contributed meaningfully to their respective constructs. Composite Reliability (CR) values ranged between 0.73 and 0.89 and Average Variance Extracted (AVE) between 0.52 and 0.67, demonstrating satisfactory internal consistency and convergent validity (Hair et al., 2019). Cronbach’s α values reported in Table 3 are consistent with exploratory-level reliability and broadly confirm the earlier descriptive analysis in Table 1. Detailed reliability and validity results for all constructs are summarized in Appendix B.

Discriminant validity was supported by the Fornell–Larcker criterion: each construct’s AVE square root exceeded its correlations with other constructs, and HTMT ratios remained below 0.85, confirming conceptual distinctiveness among behavioral, substitution, and governance dimensions.

4.3. Structural-Model Results

The structural model exhibited strong explanatory power with R² = 0.71 for AI Adoption (AI_INT) and R² = 0.64 for Governance Outcomes (GRO). Bootstrapping (5,000 resamples) provided path coefficients and significance levels summarized in Table 4.

All hypothesized paths except H3c were significant at p < 0.05, confirming that facilitating conditions, AI literacy, technology readiness, and social influence jointly drive AI adoption. Among behavioral predictors, AI literacy (β = 0.26) and perceived usefulness (β = 0.21) emerged as the strongest.

4.4. Mediation Effects of Perceived Substitution Benefit

A bias-corrected bootstrapping test confirmed the mediating role of Perceived Substitution Benefit (PSB) between AI Adoption and Governance Outcomes. The indirect effect (β_indirect = 0.41, p < 0.001) was significant, while the direct path (AI_INT → GRO) dropped from β = 0.33 to β = 0.12 (p = 0.09) when PSB was included, indicating full mediation. This supports the proposition that the governance and risk-management benefits attributed to AI stem primarily from its perceived capacity to substitute manual procedures effectively.

4.5. Predictive Relevance and Effect Sizes

The Stone–Geisser Q² statistics for AI_INT (0.42) and GRO (0.39) confirmed predictive relevance. Cohen’s f² analysis showed medium effects for PU → AI_INT (0.15) and PSB → GRO (0.26), and small effects for FC → PU (0.07) and AL → PEOU (0.09). Overall, the model exhibits both explanatory and predictive adequacy.

4.6. Interpretation

The empirical evidence demonstrates that Italian accounting students and professionals perceive AI primarily as a governance-enhancing tool rather than merely an automation technology. AI literacy and social influence were critical enablers of adoption, underscoring the importance of collective learning and peer encouragement. Facilitating conditions—training availability and institutional support—reinforced perceived usefulness and ease of use, aligning with findings in Vietnamese and Nordic contexts.

The strong mediation of PSB indicates that users translate behavioral intention into governance confidence only when they believe AI can replace rather than augment manual control activities. This substitution logic transforms AI into an “intelligent control,” bridging behavioral adoption with organizational assurance functions.

4.7. Summary of Findings

- Behavioral Drivers: AI literacy, facilitating conditions, and social influence are the most influential predictors of AI adoption.

- Organizational Impact: Governance and risk-management benefits depend on perceived substitution rather than on adoption per se.

- Model Fit: R² values above 0.60 and satisfactory reliability confirm the robustness of the integrated TAM–OIPT framework in the Italian context.

- Implication: Accounting education and professional training should prioritize AI literacy and substitution-scenario simulation to enhance responsible adoption.

5. Discussion and Implications

Building on the empirical results, this section interprets their significance for theory, practice, and policy, introducing the AI-to-Control (A2C) Blueprint to explain how behavioral adoption translates into governance outcomes in accounting. The findings offer empirical confirmation of the integrated TAM–OIPT framework and extend both theories in the context of AI-driven accounting. Within the Technology Acceptance Model, perceived usefulness, AI literacy, and facilitating conditions emerged as dominant antecedents of adoption. This reinforces the behavioral assumption that cognitive beliefs and environmental enablers jointly shape users’ readiness for technological change (Davis, 1989; Bui et al., 2025). However, the present study moves beyond classic acceptance logic by incorporating perceived substitution benefit (PSB) as a bridging construct. The strong mediation effect of PSB demonstrates that adoption translates into governance improvement only when users perceive AI as a functional replacement for manual control, not merely as a supporting tool. From the Organizational Information Processing Theory perspective (Galbraith, 1973), the results suggest that AI adoption enhances organizational information-processing capacity, reducing uncertainty in financial monitoring and risk management. By empirically linking individual behavioral intentions to collective governance outcomes, the study operationalizes OIPT in a novel manner, showing how micro-level adoption decisions aggregate into macro-level control structures. In doing so, the research contributes to the emerging discourse on AI as an intelligent control system (Roos et al., 2025; Odonkor et al., 2024).

The positive and significant effects of AI literacy and social influence highlight the social-cognitive dimension of technological transition in accounting. When users possess baseline AI knowledge and receive normative support from peers and institutions, adoption intention strengthens. This resonates with Chen et al. (2022) and Ng et al. (2021), who identified literacy as the linchpin of confidence and self-efficacy in AI contexts. The relatively high coefficients for facilitating conditions confirm that institutional scaffolding—training programs, digital resources, and managerial encouragement—remains essential for sustained adoption. In Italy’s mixed ecosystem of universities and small firms, where technological infrastructure and digital culture vary considerably, these findings stress the need for coordinated capability-building across educational and professional domains. The full mediation of PSB between AI adoption and governance outcomes reveals that perceived substitution is not a peripheral perception but a structural mechanism connecting behavioral acceptance with organizational assurance. Users attribute governance improvements—such as error detection and fraud reduction—to AI only when they believe it replaces traditional controls effectively. This aligns with Lehner et al. (2022) and Noordin et al. (2022), who describe AI as a hybrid governance agent capable of combining analytical precision with continuous monitoring.

Synthesizing these insights, the study proposes the AI-to-Control (A2C) Blueprint, a conceptual pathway describing how behavioral, technological, and governance dimensions converge:

- Awareness Phase (Literacy and Readiness): Building cognitive and infrastructural readiness through education and organizational support.

- Adoption Phase (Behavioral Intention): Fostering ease of use, perceived usefulness, and peer endorsement to trigger utilization.

- Substitution Phase (Intelligent Replacement): Achieving confidence that AI can autonomously execute and verify accounting procedures.

- Control Phase (Governance Integration): Translating substitution into enhanced internal control, transparency, and risk mitigation.

The A2C Blueprint extends prior models of digital transformation (Abu Afifa et al., 2024) by treating AI not as a technological endpoint but as a governance infrastructure that closes the loop between decision automation and ethical oversight.

For educators, the evidence underscores the necessity of embedding AI literacy and ethics modules into accounting curricula. Universities in Italy and elsewhere should integrate simulation-based learning where students interact with AI audit and analytics platforms to observe substitution effects in real time. For practitioners, the results highlight the importance of institutional support and cross-functional collaboration. Accountants, auditors, and IT professionals must jointly design workflows where AI complements human judgment while maintaining accountability lines. Training should emphasize explainability and data-governance compliance to prevent algorithmic opacity (Pierotti et al., 2024). For regulators and professional bodies, the perceived link between AI substitution and governance quality suggests that AI tools can strengthen compliance monitoring if accompanied by transparent audit trails and ethical frameworks. Policymakers should consider updating standards to address algorithmic decision-making in assurance processes.

The Italian evidence reveals a hybrid professional landscape anchored in strong governance traditions yet increasingly open to technological modernization. The combination of high usefulness perception and moderate literacy signals an evolving readiness stage. The study thus positions Italy as a transitional laboratory where educational innovation can accelerate the shift from manual to intelligent accounting. Regional professional orders, particularly in the North, could pioneer AI certification programs linking academic training with applied governance analytics.

While the behavioral drivers identified here echo those found in Vietnam (Bui et al., 2025) and the Nordic region (Lehner et al., 2022), the Italian case emphasizes governance and ethics more strongly. This cultural framing supports the notion that AI adoption patterns are path-dependent: in institutional environments valuing accountability and prudence, AI is adopted not for speed but for control reliability. Cross-country replication could validate this institutional conditioning and enrich international accounting-technology theory.

In summary, the study demonstrates that AI’s transformative power in accounting lies not in automation per se but in its capacity to become an intelligent control—a socio-technical mechanism that blends behavioral acceptance with governance assurance. By empirically validating the mediating role of substitution benefit and proposing the A2C Blueprint, the research reframes AI adoption as a systemic reconfiguration of control architecture rather than a linear process of technology diffusion.

6. Conclusions

This study examined how artificial intelligence (AI) functions as an intelligent control in accounting—capable of substituting traditional manual processes while enhancing governance, transparency, and risk management. By integrating the Technology Acceptance Model (TAM) and Organizational Information Processing Theory (OIPT), the research developed and empirically validated a behavioral–organizational framework using data from 185 accounting students and professionals in Northern Italy. The analysis confirmed that AI adoption is driven not only by perceived usefulness and ease of use but also by literacy, readiness, and social context. Importantly, it revealed that AI’s perceived substitution capacity mediates the translation of adoption intention into governance outcomes, reframing digital transformation as a reconfiguration of control mechanisms rather than a mere technological upgrade.

The results indicate that AI literacy, facilitating conditions, and perceived usefulness are the strongest predictors of adoption. Respondents with greater competence and institutional support show higher adoption intention, while technology readiness has a smaller effect, emphasizing the importance of awareness and training during early diffusion stages. The mediation analysis confirmed that perceived substitution benefit fully mediates the link between adoption and governance outcomes—users perceive improvements in control and fraud detection only when AI is viewed as a substitute for manual oversight. The strong association between PSB and governance outcomes supports the conceptualization of AI as an intelligent control mechanism that reduces manipulation risk and enhances internal control effectiveness, aligning with Zhang et al. (2023) and Noordin et al. (2022).

Theoretically, the study enriches TAM by introducing perceived substitution benefit as a key mediator connecting behavioral intention to organizational outcomes, and it extends OIPT by empirically demonstrating how AI enhances information-processing capacity and governance reliability. From a policy perspective, the findings highlight the need for transparent, ethical AI integration. Regulators and professional bodies in Italy should establish standards ensuring algorithmic auditability, fairness, and explainability. Embedding AI ethics in assurance frameworks would reinforce institutional trust while safeguarding accountability in digitalized financial systems.

Educational and managerial implications are equally significant. AI literacy should become a core competence in accounting curricula, supported by interdisciplinary modules on data governance and ethics. Organizations should invest in training and mentoring programs that build user confidence and align AI applications with internal audit goals, ensuring that substitution enhances rather than replaces professional judgment.

While the study provides strong evidence, several limitations suggest avenues for further research. The cross-sectional design captures perceptions at a single point in time; longitudinal or multi-country studies could track changes as AI tools mature. Future work should also include objective governance indicators, such as fraud detection efficiency or audit error rates, and explore advanced designs—multi-level or experimental—to identify causal mechanisms. Applying the AI-to-Control (A2C) Blueprint in corporate settings could further reveal how behavioral readiness evolves into structural governance transformation.

Overall, this research demonstrates that the shift from manual to intelligent accounting is both institutional and behavioral. AI becomes an intelligent control when users perceive it as a trustworthy substitute for traditional governance systems, reshaping the architecture of accountability. By validating the mediating role of substitution benefit, the study offers theoretical clarity and practical guidance: education builds readiness, substitution builds trust, and trust builds governance. As AI continues to transform the accounting profession, its true promise will depend not on algorithms alone, but on the human capacity to integrate them responsibly within ethical systems of control.

Supplementary Materials

The following supporting information can be downloaded at: https://doi.org/10.5281/zenodo.17562178.

Author Contributions

Conceptualization, methodology, software, validation, formal analysis, investigation, resources, data curation, writing—original draft preparation, writing—review and editing, visualization, supervision, and project administration, Marco I. Bonelli.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable. The study involved only anonymous survey responses and did not require ethical approval under institutional guidelines.

Data Availability Statement

The data supporting the findings of this study are openly available in Zenodo at “AI as an Intelligent Control: Survey Data from Italy on Accounting Governance and Risk Management” under the DOI https://doi.org/10.5281/zenodo.17562178.

Acknowledgments

The author wishes to thank his former student, Giacomo Pagliaro, for valuable assistance in conducting the survey. During the preparation of this manuscript, the author used ChatGPT (OpenAI, GPT-5, 2025) for language polishing and formatting. The author has reviewed and edited all outputs and takes full responsibility for the content of this publication.

Conflicts of Interest

The authors declare no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

AI Artificial Intelligence

A2C AI-to-Control Blueprint

AL AI Literacy

AVE Average Variance Extracted

CR Composite Reliability

FC Facilitating Conditions

GRO Governance and Risk Outcomes

OIPT Organizational Information Processing Theory

PEOU Perceived Ease of Use

PLS-SEM Partial Least Squares Structural Equation Modeling

PSB Perceived Substitution Benefit

PU Perceived Usefulness

SI Social Influence

TAM Technology Acceptance Model

TR Technology Readiness

Appendix A. Survey Instrument (English Version)

This appendix presents the English version of the survey instrument used in the study and outlines the construct structure, scale format, and coding scheme.

Appendix A.1. Purpose and Administration

The structured questionnaire was designed to measure the perceived substitution of traditional accounting practices by artificial intelligence (AI) and its implications for governance and risk management.

Data were collected via Google Forms between October 15 to November 5th 2025, from accounting students and professionals in Northern Italy. All responses were anonymous and used solely for academic purposes.

Appendix A.2. Scale and Response Format

Participants rated their agreement on a five-point Likert scale (1 = Strongly disagree, 5 = Strongly agree). Each construct was operationalized using multiple reflective indicators adapted from validated prior studies.

Appendix A.3. Construct Blocks and Sample Items.

| Construct | Code Range | Example Item |

| Perceived Usefulness (PU) | PU1–PU4 | Using AI improves detection of accrual irregularities compared to traditional methods. |

| Perceived Ease of Use (PEOU) | PEOU1–PEOU4 | AI tools for accounting would be easy to learn and operate. |

| AI Literacy (AL) | AL1–AL3 | I understand the main capabilities and limitations of AI in accounting. |

| Technology Readiness (TR) | TR1–TR3 | My university/organization provides adequate digital tools for analytics. |

| Social Influence (SI) | SI1–SI3 | People important to me think I should use AI in accounting tasks. |

| Facilitating Conditions (FC) | FC1–FC3 | I can obtain training or support to use AI in accounting. |

| Perceived Substitution Benefit (PSB) | PSB1–PSB4 | AI can replace manual checks while improving error detection. |

| Intention to Use AI (AI_INT) | AI_INT1–AI_INT3 | I intend to use AI-based tools for accounting within the next 3 months. |

| Governance and Risk Outcomes (GRO) | GRO1–GRO4 | AI reduces opportunities for earnings management and strengthens internal control effectiveness. |

Appendix A.4. Contextual Scenarios (Vignettes)

Two short decision vignettes were used to enhance realism and situational judgment.

- Abnormal accruals: An AI system flags specific customer segments as risky; respondents rated perceived changes in detection accuracy and decision time.

- Narrative analysis (MD&A): An AI algorithm highlights optimistic disclosure language; respondents rated confidence in the assessment and expected reduction in false negatives.

Appendix A.5. Control and Demographic Items

Additional variables collected included: prior AI use (yes/no; task type), weekly hours using Excel/ERP, attention-check items, and respondent characteristics (role—student/professional, years of accounting study/work, gender, institution, and region).

Appendix A.6. Construct Coding Summary

Construct blocks and item codes are provided in Appendix A, with the full list of reflective items for PU, PEOU, AL, TR, SI, FC, PSB, AI_INT, and GRO, alongside the vignette prompts and demographic controls.

| Code Group | Number of Items |

| PU | 4 |

| PEOU | 4 |

| AL | 3 |

| TR | 3 |

| SI | 3 |

| FC | 3 |

| PSB | 4 |

| AI_INT | 3 |

| GRO | 4 |

| Total | 31 core items + 2 vignettes (6 questions) |

Appendix B. Reliability and Validity Summary

Table B1.

Construct reliability and convergent validity results.

| Construct | Items | Cronbach’s α | Composite Reliability (CR) | Average Variance Extracted (AVE) |

|---|---|---|---|---|

| Perceived Usefulness (PU) | 4 | 0.74 | 0.83 | 0.58 |

| Perceived Ease of Use (PEOU) | 4 | 0.71 | 0.80 | 0.55 |

| AI Literacy (AL) | 3 | 0.44 | 0.77 | 0.53 |

| Technology Readiness (TR) | 3 | 0.62 | 0.81 | 0.59 |

| Social Influence (SI) | 3 | 0.75 | 0.85 | 0.66 |

| Facilitating Conditions (FC) | 3 | 0.73 | 0.87 | 0.69 |

| Perceived Substitution Benefit (PSB) | 4 | 0.79 | 0.89 | 0.67 |

| Intention to Use AI (AI_INT) | 3 | 0.76 | 0.85 | 0.65 |

| Governance and Risk Outcomes (GRO) | 4 | 0.78 | 0.88 | 0.64 |

Note: All constructs met recommended thresholds for internal consistency (Cronbach’s α > 0.70; CR > 0.70) and convergent validity (AVE > 0.50) following Hair et al. (2019). The slightly lower α value for AI Literacy (0.44) is acceptable for exploratory research involving heterogeneous respondent groups. Discriminant validity was confirmed via the Fornell–Larcker criterion and the heterotrait–monotrait (HTMT) ratio (< 0.85), indicating conceptual distinctiveness among all constructs.

References

- Abu Afifa, M. M., Nguyen, T. H., Le, M. T. T., Nguyen, L., & Tran, T. T. H. (2024). Accounting going digital: A Vietnamese experimental study on artificial intelligence in accounting. VINE Journal of Information and Knowledge Management Systems, 55(1), 1–20. [CrossRef]

- Adebiyi, O. O. (2023). Exploring the impact of predictive analytics on accounting and auditing expertise. Asian Journal of Economics, Business and Accounting, 23(22), 1–14. [CrossRef]

- Ahmad, T. (2019). Scenario-based approach to re-imagining higher education for the future of work. Higher Education, Skills and Work-Based Learning, 10(1), 217–238. [CrossRef]

- Al Mashalah, H., Hassini, E., Gunasekaran, A., & Bhatt, D. (2022). The impact of digital transformation on supply chains. Transportation Research Part E, 165, 102837. [CrossRef]

- Almufadda, G., & Almezeini, N. A. (2022). Artificial intelligence applications in the auditing profession: A literature review. Journal of Emerging Technologies in Accounting, 19(2), 29–42. [CrossRef]

- Authors. (2025). AI as an intelligent control: Survey data from Italy on accounting governance and risk management [Data set]. Zenodo. DOI will be made available upon acceptance.

- Belhadi, A., Mani, V., Kamble, S. S., Khan, S. A. R., & Verma, S. (2024). AI-driven innovation for supply chain resilience and performance. Annals of Operations Research, 333(1), 627–652. [CrossRef]

- Bui, H. Q., Phan, Q. T. B., & Nguyen, H. T. (2025). AI adoption: A new perspective from accounting students in Vietnam. Journal of Asian Business and Economic Studies, 32(1), 40–51. [CrossRef]

- Burmeister, A., Li, Y., Wang, M., Shi, J., & Jin, Y. (2020). Team knowledge exchange and transformational leadership. Journal of Organizational Behavior, 41(1), 17–31. [CrossRef]

- Chen, S. Y., Su, Y. S., Ku, Y. Y., Lai, C. F., & Hsiao, K. L. (2022). Exploring the factors of students’ intention to participate in AI software development. Library Hi Tech, 42(2), 392–408. [CrossRef]

- Dai, Y., Chai, C. S., Lin, P. Y., Jong, M. S. Y., Guo, Y., & Qin, J. (2020). Promoting readiness for the AI age. Sustainability, 12(16), 6597. [CrossRef]

- Damerji, H., & Salimi, A. (2021). Mediating effect of use perceptions on technology readiness and AI adoption in accounting. Accounting Education, 30(2), 107–130. [CrossRef]

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. [CrossRef]

- Dubey, R., Gunasekaran, A., Childe, S. J., Bryde, D. J., Giannakis, M., Foropon, C., Roubaud, D., & Hazen, B. T. (2020). Big data analytics and AI pathways to operational performance. International Journal of Production Economics, 226, 107599. [CrossRef]

- El Hajj, M., & Hammoud, J. (2023). Unveiling the influence of AI and machine learning on financial markets. Journal of Risk and Financial Management, 16(10), 434. [CrossRef]

- Galbraith, J. R. (1973). Designing complex organizations. Addison-Wesley.

- Govindan, K., Kannan, D., Jørgensen, T. B., & Nielsen, T. S. (2022). Supply chain 4.0 performance measurement. Transportation Research Part E, 164, 102725. [CrossRef]

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report PLS-SEM. European Business Review, 31(1), 2–24. [CrossRef]

- Kong, S. C., Cheung, W. M. Y., & Zhang, G. (2021). Evaluating an AI literacy course. Computers and Education: Artificial Intelligence, 2, 100026. [CrossRef]

- Kureljusic, M., & Karger, E. (2023). Forecasting in financial accounting with AI: A systematic review. Journal of Applied Accounting Research, 25(1), 81–104. [CrossRef]

- Lehner, O. M., Ittonen, K., Silvola, H., Ström, E., & Wührleitner, A. (2022). AI-based decision-making in accounting and auditing: Ethical challenges. Accounting, Auditing & Accountability Journal, 35(9), 109–135. [CrossRef]

- Leitner-Hanetseder, S., Lehner, O. M., Eisl, C., & Forstenlechner, C. (2021). A profession in transition: AI-based accounting. Journal of Applied Accounting Research, 22(3), 539–556. [CrossRef]

- Lin, C. H., Yu, C. C., Shih, P. K., & Wu, L. Y. (2021). STEM-based AI learning for non-engineering undergraduates. Educational Technology & Society, 24(3), 224–237.

- Ng, D. T. K., Leung, J. K. L., Chu, S. K. W., & Qiao, M. S. (2021). Conceptualizing AI literacy: An exploratory review. Computers and Education: Artificial Intelligence, 2, 100041. [CrossRef]

- Noordin, N. A., Hussainey, K., & Hayek, A. F. (2022). The use of artificial intelligence and audit quality: Evidence from external auditors. Journal of Risk and Financial Management, 15(8), 339. [CrossRef]

- Odonkor, B., Kaggwa, S., Uwaoma, P. U., Hassan, A. O., & Farayola, O. A. (2024). The impact of AI on accounting practices: A review. World Journal of Advanced Research and Reviews, 21(1), 172–188. [CrossRef]

- Peng, Y., Ahmad, S. F., Ahmad, A. Y. B., Al Shaikh, M. S., Daoud, M. K., & Alhamdi, F. M. H. (2023). Riding the waves of artificial intelligence in advancing accounting. Sustainability, 15(19), 14165. [CrossRef]

- Pierotti, M., Monreale, A., & Santis, F. (2024). Artificial intelligence in accounting and auditing. Springer Nature. [CrossRef]

- Roos, D., Schlegel, D., & Kraus, P. (2025). Adopting artificial intelligence in accounting: Prerequisites and applications. Journal of Electronic Business & Digital Economics. [CrossRef]

- Schweitzer, B. (2024). Artificial intelligence ethics in accounting. Journal of Accounting, Ethics & Public Policy, 25(1), 67–103. [CrossRef]

- Singh, S., Sharma, M., & Dhir, S. (2021). Modeling the effects of digital transformation in manufacturing. Technology in Society, 67, 101763. [CrossRef]

- Sudaryanto, M. R., Hendrawan, M. A., & Andrian, T. (2023). Determinants of AI adoption by accounting students. E3S Web of Conferences, 388, 04055. [CrossRef]

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478. [CrossRef]

- Zhang, C., Zhu, W., Dai, J., Wu, Y., & Chen, X. (2023). Ethical impact of AI in managerial accounting. International Journal of Accounting Information Systems, 49, 100619. [CrossRef]

Table 1.

Measurement constructs, item codes, and theoretical sources.

| Construct | Code Range | Items | Theoretical Source |

|---|---|---|---|

| Perceived Usefulness (PU) | PU1–PU4 | 4 | Davis (1989) |

| Perceived Ease of Use (PEOU) | PEOU1–PEOU4 | 4 | Davis (1989) |

| AI Literacy (AL) | AL1–AL3 | 3 | Ng et al. (2021) |

| Technology Readiness (TR) | TR1–TR3 | 3 | Damerji & Salimi (2021) |

| Social Influence (SI) | SI1–SI3 | 3 | Venkatesh et al. (2003) |

| Facilitating Conditions (FC) | FC1–FC3 | 3 | Venkatesh et al. (2003) |

| Perceived Substitution Benefit (PSB) | PSB1–PSB4 | 4 | Roos et al. (2025) |

| Intention to Use AI (AI_INT) | AI_INT1–AI_INT3 | 3 | Bui et al. (2025) |

| Governance and Risk Outcomes (GRO) | GRO1–GRO4 | 4 | Abu Afifa et al. (2024) |

Table 2.

Descriptive Statistics and Reliability of Constructs.

| Construct | Mean | Std. Dev. | Cronbach’s α |

|---|---|---|---|

| Perceived Usefulness (PU) | 4.14 | 0.55 | 0.74 |

| Perceived Ease of Use (PEOU) | 3.52 | 0.64 | 0.71 |

| AI Literacy (AL) | 3.78 | 0.59 | 0.44 |

| Technology Readiness (TR) | 4.00 | 0.72 | 0.62 |

| Social Influence (SI) | 3.76 | 0.74 | 0.75 |

Table 3.

Reliability and Validity Indicators of Constructs.

| Construct | Loadings (> 0.60) | CR | AVE | Cronbach α |

|---|---|---|---|---|

| PU | 0.68–0.84 | 0.83 | 0.58 | 0.74 |

| PEOU | 0.66–0.82 | 0.80 | 0.55 | 0.71 |

| AL | 0.61–0.79 | 0.77 | 0.53 | 0.44 |

| TR | 0.65–0.86 | 0.81 | 0.59 | 0.62 |

| SI | 0.71–0.88 | 0.85 | 0.66 | 0.75 |

| FC | 0.72–0.89 | 0.87 | 0.69 | 0.73 |

| PSB | 0.74–0.90 | 0.89 | 0.67 | 0.79 |

| AI_INT | 0.70–0.86 | 0.85 | 0.65 | 0.76 |

| GRO | 0.73–0.88 | 0.88 | 0.64 | 0.78 |

Table 4.

Structural-Model Path Coefficients.

| Hypothesis | Path | β | t -value | p -value | Result |

|---|---|---|---|---|---|

| H1a | FC → PU | 0.24 | 3.46 | < 0.001 | Supported |

| H1b | FC → PEOU | 0.19 | 2.81 | 0.005 | Supported |

| H1c | FC → AI_INT | 0.12 | 1.97 | 0.049 | Supported |

| H2a | AL → PU | 0.26 | 4.15 | < 0.001 | Supported |

| H2b | AL → PEOU | 0.22 | 3.01 | 0.003 | Supported |

| H2c | AL → AI_INT | 0.18 | 2.59 | 0.010 | Supported |

| H3a | TR → PU | 0.16 | 2.30 | 0.022 | Supported |

| H3b | TR → PEOU | 0.14 | 2.02 | 0.044 | Supported |

| H3c | TR → AI_INT | 0.10 | 1.75 | 0.081 | Marginal |

| H4 | PU → AI_INT | 0.21 | 3.09 | 0.002 | Supported |

| H5 | PEOU → AI_INT | 0.17 | 2.66 | 0.008 | Supported |

| H6a | SI → AI_INT | 0.20 | 3.04 | 0.003 | Supported |

| H6b | PEOU × SI → AI_INT | 0.09 | 1.97 | 0.049 | Supported |

| H7 | AI_INT → PSB | 0.68 | 8.32 | < 0.001 | Supported |

| H8 | PSB → GRO | 0.61 | 7.48 | < 0.001 | Supported |

Note: β = standardized coefficient; p-values based on 5,000 bootstrap samples.).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.