Submitted:

25 August 2025

Posted:

26 August 2025

You are already at the latest version

Abstract

Effective budgeting is a critical determinant of project success, ensuring optimal resource allocation, financial control, and timely delivery. While multiple factors influence project management outcomes, inadequate budgeting remains one of the primary causes of project failure. This systematic review evaluates the application, advantages, and limitations of three widely used budgeting techniques in project management—Top-Down, Bottom-Up, and Activity-Based Budgeting (ABB)—to assess their impact on cost estimation accuracy, resource allocation, and project outcomes. A systematic search of Scopus, Web of Science, and Google Scholar was conducted for peer-reviewed literature published between 2014 and 2024. Forty eligible studies were identified, screened, and synthesized using established inclusion criteria. Data extraction focused on budgeting methodology, project type, industry context, and reported performance outcomes. The findings indicate that budgeting effectiveness varies by project size, complexity, and organizational context. Bottom-Up budgeting demonstrated the highest cost estimation accuracy, achieving 15–30% improvement over Top-Down approaches. ABB provided significant cost efficiency gains (20–40%) in projects with well-defined activities, though it required extensive data and analytical infrastructure. Top-Down budgeting was most effective for ensuring strategic alignment but frequently lacked precision. Across studies, the choice of technique was strongly influenced by organizational goals, project scale, and stakeholder involvement. Budgeting techniques exert a measurable influence on project outcomes by enhancing cost control, transparency, and resource efficiency. While no single method is universally superior, aligning budgeting strategies with project complexity, industry requirements, and organizational objectives is essential. This review provides evidence-based recommendations to support project managers in selecting context-appropriate budgeting methods and leveraging technological tools to strengthen financial planning and decision-making in project management.

Keywords:

project management

; budgeting techniques

; top-down

; bottom-up

; activity-based budgeting

; cost estimation

; financial planning

1. Introduction

Effective project management depends heavily on cost planning, activity planning, and accurate budgeting practices. Budgeting is not only a financial tool but also a strategic mechanism that ensures optimal resource allocation, cost control, and timely project delivery. When implemented effectively, budgeting provides the financial discipline needed for successful project execution and long-term organizational sustainability [1,2]. Organizations develop budgets to monitor progress toward goals, manage expenditures, and predict both cash flow and profitability. Several budgeting methods are commonly applied, including Traditional Budgeting, Better Budgeting (such as Zero-Based, Value-Based, and Rolling Forecasts), Advanced Budgeting, and Beyond Budgeting. Each of these approaches plays a central role in management control systems by supporting planning, coordination, and performance monitoring [1,17]. Budgeting has long been recognized as one of the most important and effective managerial accounting tools [17]. In sectors such as construction, accurate cost estimation is critical, as total project costs comprise not only construction-related expenses but also engineering and consulting costs [51]. For this reason, precise recordkeeping of labor hours and resource utilization is a core aspect of cost control and profitability assurance [51].

Budgeting and financial oversight are not isolated functions limited to finance departments. Instead, they are embedded across organizational units, including regional offices, product lines, and operational teams. Effective planning, budgeting, accounting, and performance appraisal should operate in a closed-loop system in which planning guides budget allocation, and accounting evaluates execution [2,18,19]. Within this system, business plans become the central driver of financial allocation and flexible resource distribution, particularly when supported by rolling forecasts [19]. The increasing adoption of agile project management has further emphasized the importance of flexible and adaptive budgeting. Technological advancements have introduced greater efficiency, transparency, and accuracy in cost planning and monitoring. Agile environments in particular require frequent re-estimation, dynamic cost tracking, and collaborative financial planning, where effective budgeting supports project adaptability and timely delivery [34]. Strong project teams, when supported by advanced budgeting tools, enhance project performance and increase the likelihood of on-time and on-budget completion [34]. Budget managers also categorize expenditures into components such as personnel, travel, training, supplies, research, capital expenditures, and overhead to ensure structured allocation of resources [2].

Cost estimation remains a fundamental dimension of project budgeting, as it provides approximations of the resources required for task completion. Higher-level budget reviewers must balance organizational constraints with local-level needs to allocate resources effectively. Advanced models of cost allocation increasingly recommend scheduling resources to minimize idle time, thereby maximizing project benefits [30]. Among the most widely studied methodologies are Top-Down, Bottom-Up, and Activity-Based Budgeting (ABB). Each offers unique strengths depending on project complexity, industry requirements, and organizational structures. Top-Down approaches support strategic alignment, Bottom-Up methods increase accuracy and stakeholder involvement, while ABB provides detailed cost attribution but requires significant data and analytical resources [30,49]. In summary, planning provides the foundation for effective budgeting, and robust budgeting systems remain central to achieving project success [41].

1.1. Research Questions

Despite extensive scholarship on budgeting in project management, there remains a need for systematic evaluation of how different techniques perform across project types and contexts. This review is guided by the following research questions:

- What are the documented advantages and applications of Top-Down, Bottom-Up, and Activity-Based Budgeting in project management?

- How do these techniques compare in terms of cost estimation accuracy, efficiency, and applicability across industries and project sizes?

- In what ways do budgeting techniques contribute to reducing project failure through improved cost control, risk management, and resource allocation?

- How do budgeting strategies influence project outcomes, including financial performance, stakeholder satisfaction, and alignment with organizational objectives?

- Which actors (e.g., project managers, financial officers, stakeholders) are responsible for ensuring the effective implementation of budgeting practices?

- How have technological tools—such as ERP systems, predictive analytics, and automation—shaped the application and effectiveness of budgeting techniques in project management?

- What overall impacts on project success are consistently attributed to effective budgeting practices?

1.2. Rationale

The rationale for this review is to consolidate and evaluate empirical evidence on budgeting techniques in project management, focusing on their applications, comparative effectiveness, and contextual suitability. Budgeting remains a decisive factor in project performance, influencing cost accuracy, financial transparency, and strategic alignment. Given the wide variation in project contexts—from construction and IT to healthcare and public sector projects—the effectiveness of specific budgeting techniques often depends on project complexity, industry norms, and organizational goals. By synthesizing studies published between 2014 and 2024, this review addresses a gap in the literature by providing a comprehensive and evidence-based understanding of how budgeting methods contribute to project success.

1.3. Objectives

The primary objective of this review is to systematically identify, evaluate, and analyze the most widely applied budgeting techniques in project management, with particular focus on Top-Down, Bottom-Up, and Activity-Based Budgeting. The review aims to:

- Examine the documented strengths and limitations of each method in diverse project settings.

- Assess their impact on cost control, resource allocation, and financial decision-making.

- Identify the role of advanced technologies (e.g., ERP systems, AI-driven tools) in improving budgeting efficiency and accuracy.

- Provide evidence-based insights to support project managers in selecting context-appropriate budgeting strategies.

1.4. Research Contributions

This review contributes to the field of project management by:

- Providing a systematic comparison of Top-Down, Bottom-Up, and Activity-Based Budgeting, highlighting their advantages, limitations, and performance outcomes.

- Demonstrating how the integration of software tools, predictive analytics, and automation enhances budgeting effectiveness in practice.

- Clarifying the extent to which effective budgeting mitigates financial risks, reduces project failure, and improves overall project delivery.

1.5. Research Novelty

The novelty of this review lies in its structured comparison of budgeting techniques across industries and project scales, offering both theoretical and practical insights. Specifically:

- It highlights the interaction between budgeting methods and contextual factors such as organizational structure, project complexity, and stakeholder involvement.

- It demonstrates how traditional methods are being adapted or supplemented by data-driven and hybrid approaches, reflecting evolving project management needs.

- It provides an updated synthesis of budgeting research over the last decade, bridging the gap between established practices and emerging technological solutions.

2. Materials and Methods

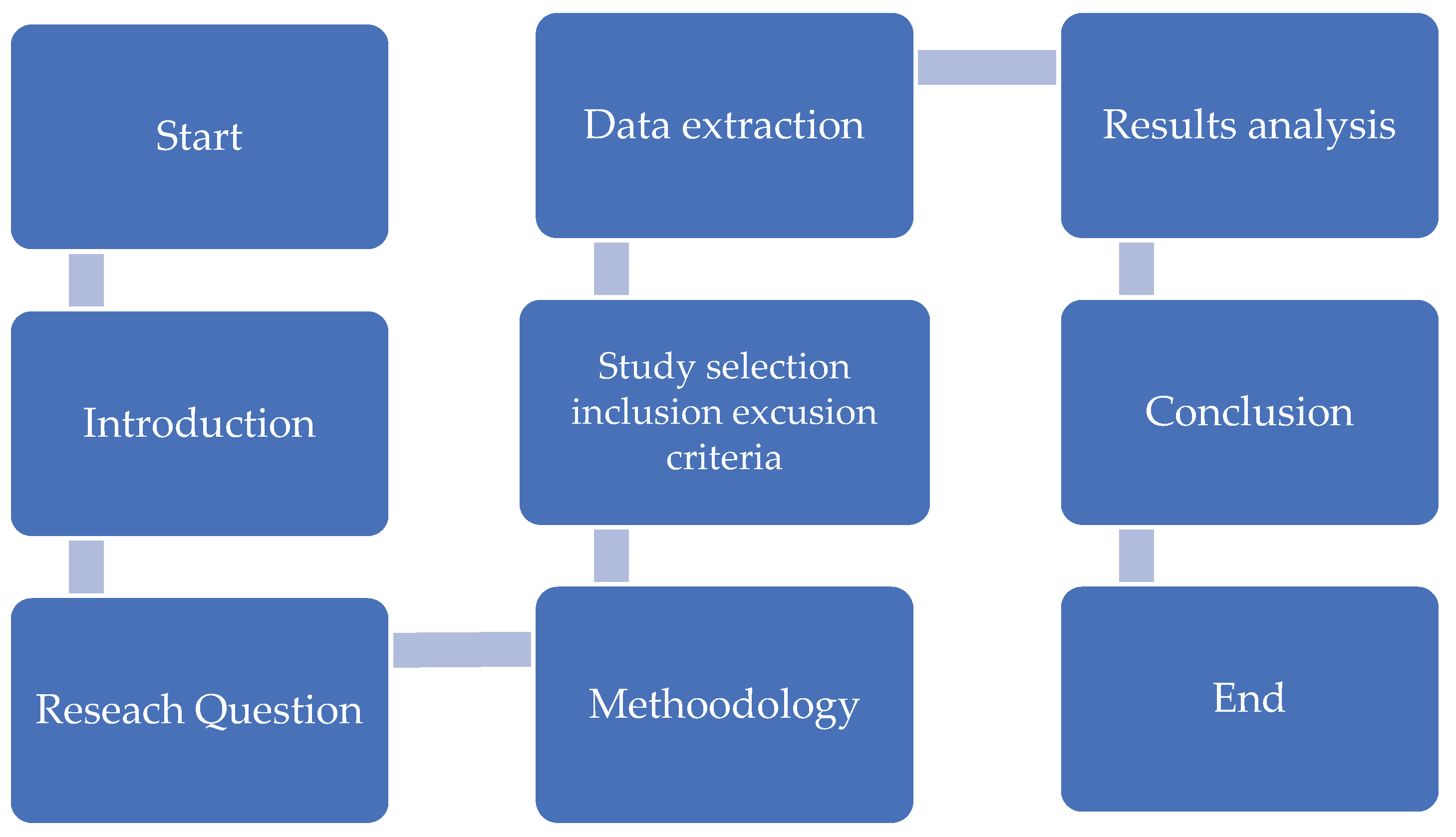

In this section of our research, the methodology used to establish a systematic review of Budgeting Techniques of the following “Top-Down, Bottom-Up, and Activity-Based Budgeting” in Project Management. The research is only focused on an 11-year review from 2014 to 2025. The research methodology includes the careful selection of relevant peer-reviewed articles from key online databases, namely Scopus, Google Scholar, and Web of Science, ensuring a thorough examination of the subject matter. The methodology used lays the groundwork for a thorough analysis of each component in the sections that follow by providing guidelines for choosing studies, data sources, and the approach used to review the gathered literature. The following flow diagram, shown in Figure 2, shows the proposed structure of SLR to be followed whilst writing and compiling this study. (Kgakatsi, et al., 2024)

Figure 1.

SLR Flow diagram.

2.1. Eligibility Criteria

A systematic examination of peer-reviewed literature on budgeting techniques in project management was undertaken to identify studies relevant to top-down, bottom-up, and activity-based budgeting. Research papers published between the year 2014 and 2025 were considered. All the papers that were considered are written in English only. A method was that ensured that only the relevant research papers were found was used, so that only the publications dealing with one or all the three budgeting methods was used and papers focused on other information not regarding or related to our research were not included. The inclusion and exclusion criteria for this study is used to help select research papers that concern top-down, bottom-up, or activity-based budgeting techniques involved in project management. The inclusion and exclusion criteria for this study is tabulated as in Table 2 [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45].

2.2. Information Sources

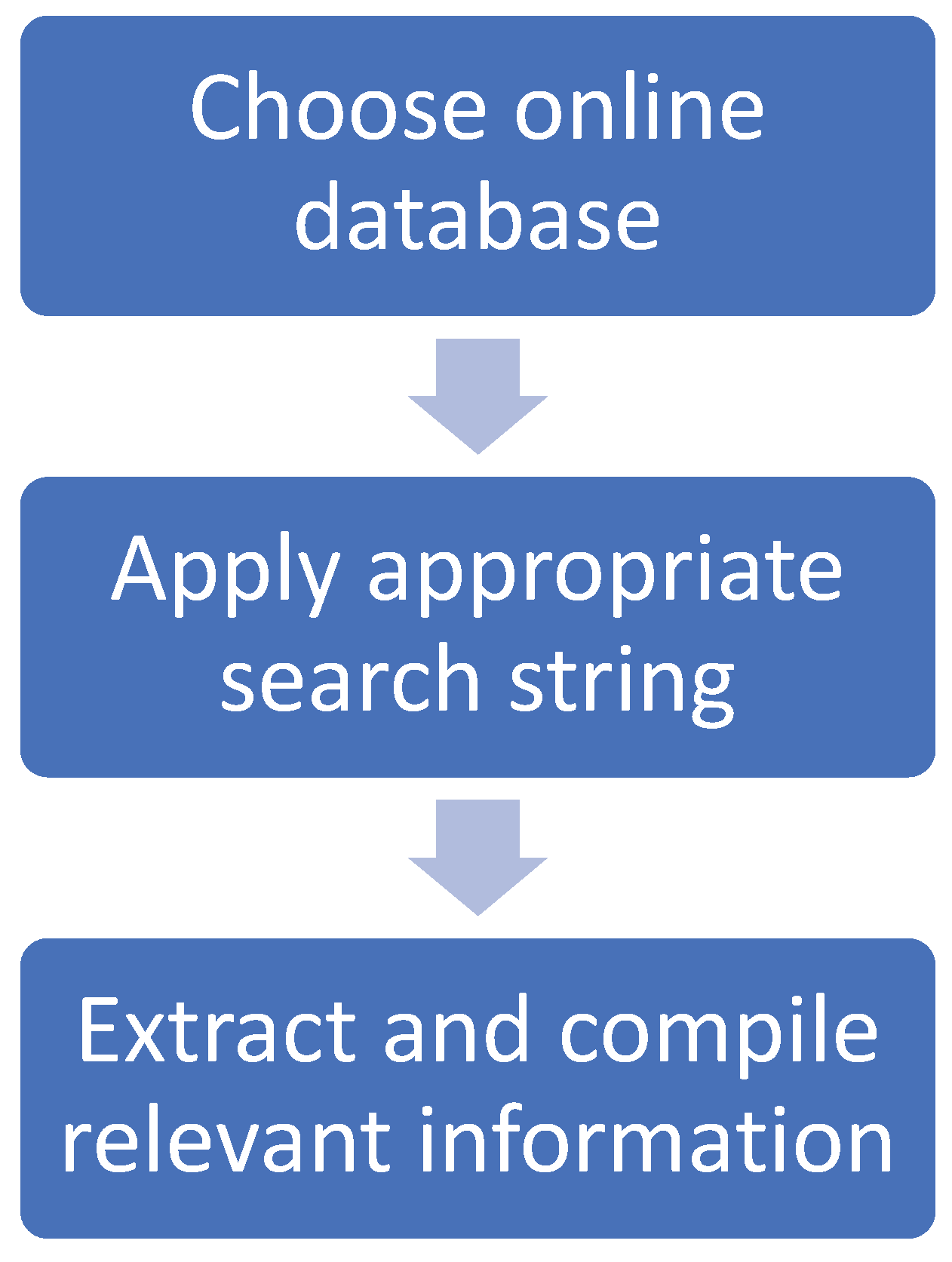

A systematic search conducted across the following online database, SCOPUS, Google Scholar and Web of Science to identify relevant studies for this review. Google Scholar is an online database that provides a simple way to broadly search for scholarly literature across many disciplines and sources, you can search articles, theses, books, abstracts and court opinions, from academic publishers, professional societies, online repositories, universities and other web sites and helps you find the work most relevant to you. SCOPUS is a large, multidisciplinary database of peer-reviewed literature: scientific journals, books, and conference proceedings, it delivers a comprehensive overview of the world's research output in the fields of science, technology, medicine, social science, and arts and humanities [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45]. Web of Science is a collection of databases that index the world’s leading scholarly literature in the sciences, social sciences, arts, and humanities, as published in journals, conference proceedings, symposia, seminars, colloquia, workshops, and conventions across the globe. These three databases, SCOPUS, Google Scholar, and Web of Science, were utilized due to their reputation in the research field and abundance of peer-reviewed literature, empirical research, and quantitative research papers, even in the field of Project Management. Each database was searched using different kinds of search strings catered to the specific online database, to get the most relevant results, to help us compile a proper systematic review research paper.

Figure 2.

The method use to search for publications.

2.3. Search Strategy

The literature that was used in this research was compiled from very reputable online research databases, using search strings that are focused on the different budgeting techniques namely Top-down, bottom-up, and activity-based budgeting techniques in Project Management. The inclusion of the budget techniques in the search strings when we were searching in Google Scholar, Web of Science and SCOPUS ensured that the results we got from the online databases above was of only of the research papers related to the information we needed, which is only relevant to the budget techniques. The search strings that were used to find the most relevant studies, were the following, on SCOPUS ("top-down budgeting" OR "bottom-up budgeting" OR "activity-based budgeting")

AND ("project management" OR "project budgeting") was used which resulted with 2 paper, on Google Scholar ("top-down budgeting" OR "bottom-up budgeting" OR "activity-based budgeting") AND ("project budgeting") was used and the results had 841 papers and lastly on Web of Science which resulted with 2 papers used this search string TS=("top-down budgeting" OR "bottom-up budgeting" OR "activity-based budgeting") AND TS=("project budgeting"), thus helping us to find the relevant papers that were published between the year 2014 and 2025. (Khanyi, et al., 2024) This process helped to decrease and limit the literature to the most relevant, useful, updated and high-quality sources for this study. Table 3 shows the list of online repositories that were utilized as well as the total number of results achieved before the initial screening.

2.4. Selection Process

Forty papers were researched and selected independently by Mr. Cossa R and Mr. Zwane SM. A discussion on how and which papers to select and use for the research was had by the parties involved in compiling the research. All the opinions and disagreements where discussed, as there were different approaches were brought forth by the different parties and third parties were also consulted to get a different perspective and ideas, to help reach a conclusion. Then the papers collected were properly reviewed to see if they have the information that can help us in our research the paper, after an agreement and a conclusion. Figure 2, shown below, shows the methods of the inclusion and exclusion criteria [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45].

Figure 3.

Procedures and Stages of the Review.

2.5. Data Collection Process

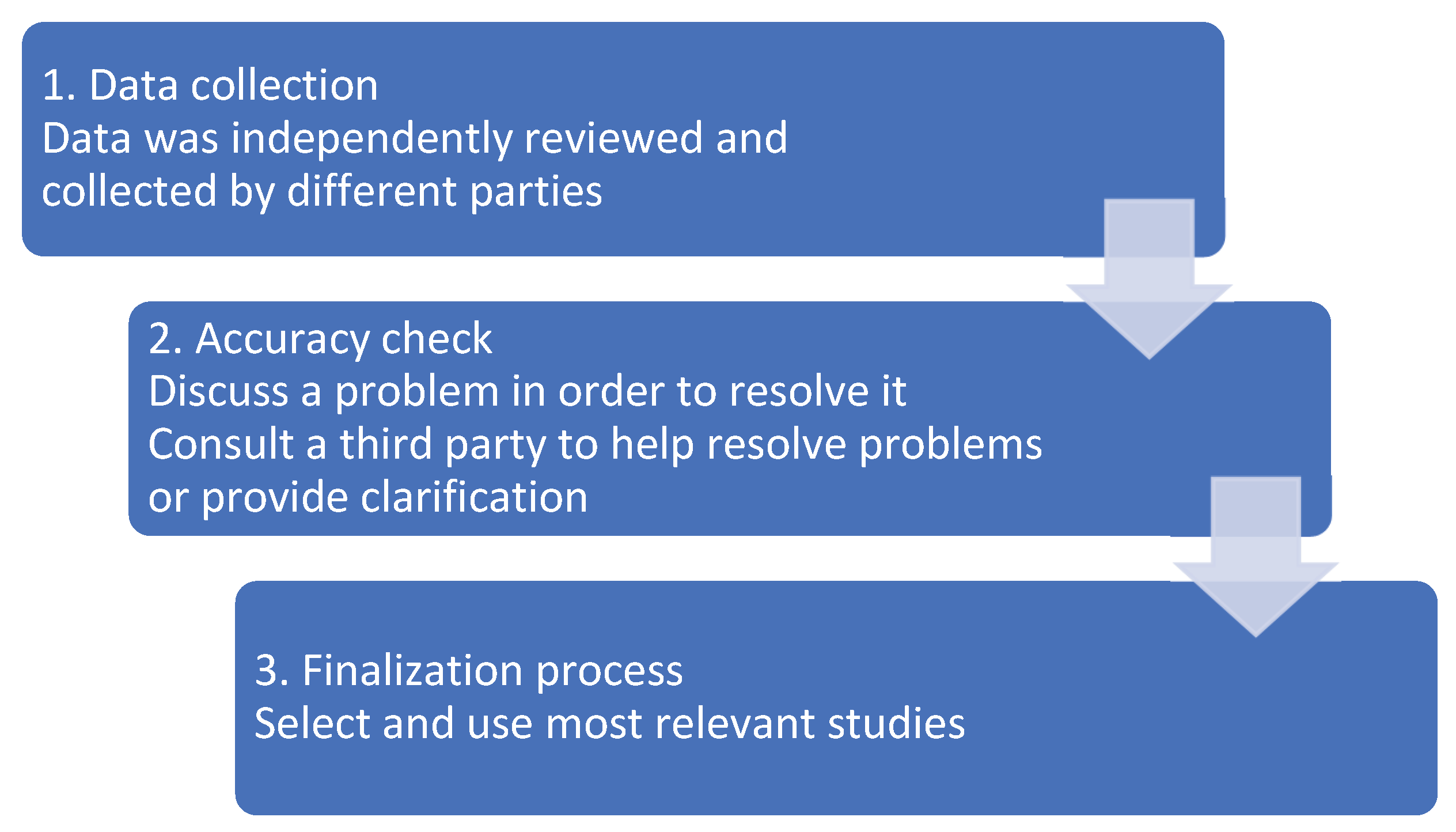

To ensure that the data we collected from the studies was the data needed, we followed a structured approach to ensure data collected was accurate, and we only used relevant papers from 2014 to 2025 that were written only in English, to minimize errors. Two reviewers independently collected the data from different studies, then reviewed each other’s work through a discussion to critique and resolve each other’s mistakes. Any differences in the extracted data were discussed until an agreement was reached on how to fix errors. The data selected was carefully entered and double-checked for accuracy, and consistency through the entered data was used to avoid errors in the data collection stage on Excel, so that it will be easier to summarize, tabulate, and make graphs of the data and results found. In the times where we were struggling or did not understand on how to go about a process or stage, a third party was consulted to help us clear the confusion. No automation tools were used; all the irrelevant or missing data was found the clarification of a third party or the times we were double checking. The data collection method is shown in Figure 3 [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45].

Figure 4.

Flow of Data Selection process.

2.6. Data Items

This section highlights the selection criteria method used to collect and comprehensively assess the impact and applicability of top-down, bottom-up, and activity-based budgeting used in project management.

2.6.1. Data Collection Method

Data was compiled and collected by two reviewers independently, from three different online databases, SCOPUS, Google Scholar, and Web of Science. The papers that were selected were those related to top-down, bottom-up, and activity-based budgeting in Project Management. The relevant years between 2014 to 2025 were used to limit and decrease the number of paper results, thus only showing the most relevant results, and all papers outside this limit were immediately discarded. The language of all the papers collected was English to avoid misinterpretation and errors. The collected data was entered carefully one by one onto the Excel data sheet and was then double-checked to look for inconsistencies and errors, or mistakes. All this research gave the researchers more knowledge on the types of budgeting techniques available, when and how to apply the different techniques on different projects, to ensure be best and most efficient budgeting method for that type of project. This gave us insight into how effective accurate cost management techniques are developed, planned, and managed throughout the project. Studies with effective budgeting techniques were specifically looked at, and the results were compiled on which budgeting technique is the best for which kind of project or situation [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45].

2.7. Study Risk of Bias Assessment

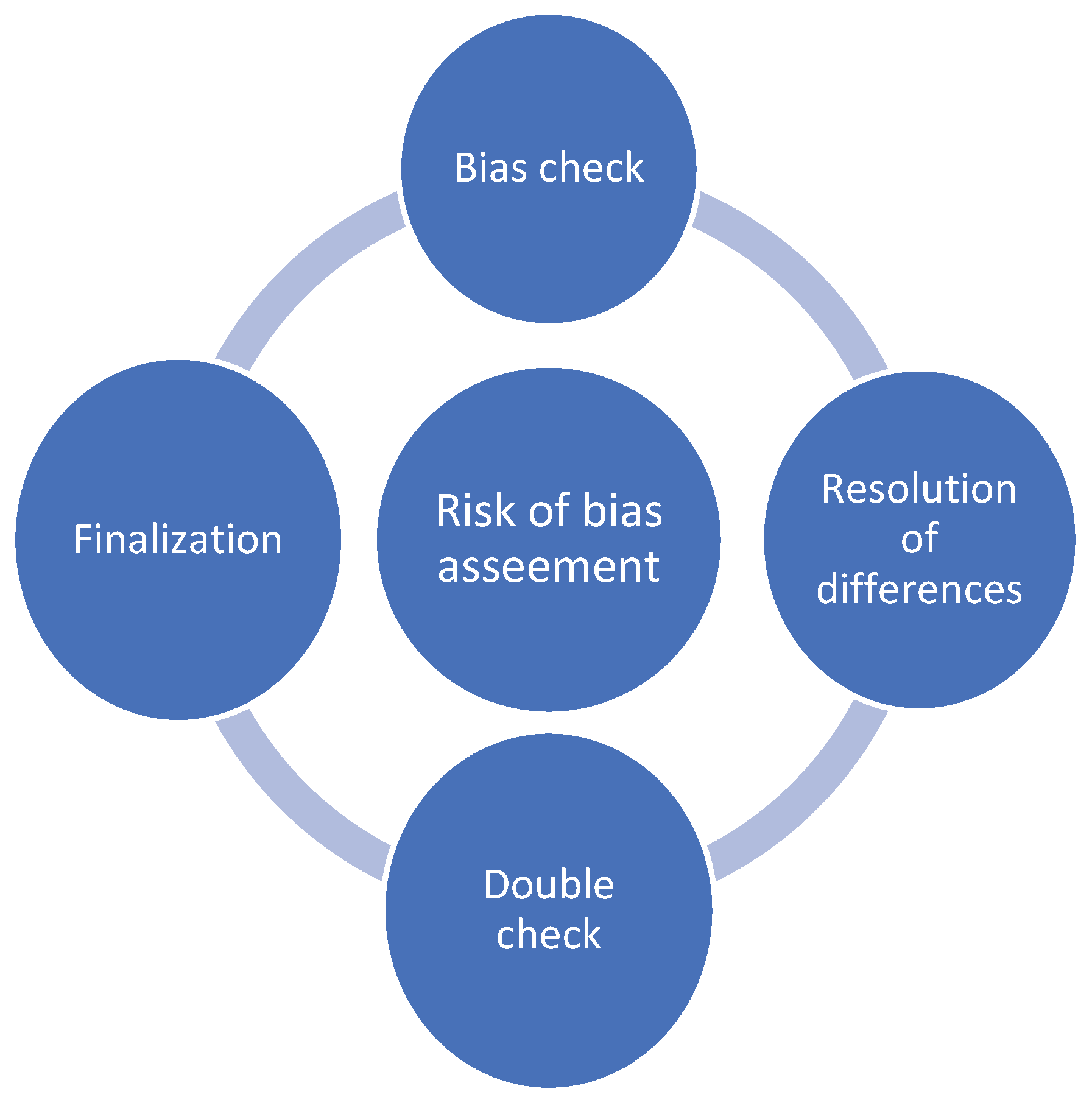

In the studies, particularly those examining different budgeting techniques in Project Management, it was essential to critically evaluate the risk of bias to ensure the reliability and validity of the findings. To ensure that there’s no bias in the data we compiled, we made sure to be diverse and not to reuse the same papers we have already used or papers coming from the same organisation or writers. The different parties involved reviewed each other's work to check whether the other party might have been biased in the process of compiling the research separately. A discussion was then had, an agreement was reached, and mistakes and errors were corrected. A third party was also consulted to advise us on how to avoid being biased when researching and on how to avoid using the same research, and they also check our document to see whether there’s bias in the compiled research and compiled papers. Papers without enough relevant information were removed and replaced with papers found to have more information about the different budgeting techniques, from the online databases of SCOPUS, Google Scholar, and Web of Science. In some studies, we found and identified key drivers that push for the use of a certain budgeting technique. We also looked at the factors that determine which methods to choose. The factors can either be internal or external. The internal factors include working hours, machine runtime, or material usage, and the external factors can include economy, market volatility, regulatory constraints, environment, taxes, or inflation [29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45].

Figure 5.

Risk of Bias Assessment Process.

2.8. Synthesis Methods

It's crucial to have a well-defined and structured approach to selecting scholarly papers for synthesis. This process starts by establishing clear inclusion and exclusion criteria to ensure that only relevant, high-quality studies are considered. The synthesis process aimed to integrate findings across diverse contexts, study designs, and industries to evaluate the application, effectiveness, and comparative advantages of Top-Down, Bottom-Up, and Activity-Based Budgeting (ABB). This section outlines the methods used for consolidating and analyzing data about budgeting techniques in various project management. In implementing structured criteria, the review aims to synthesize relevant findings effectively while providing a comprehensive understanding of the role of budgeting strategies in promoting effectiveness in project management. Moreover, once the scholarly papers are identified, their characteristics are systematically extracted and tabulated in a Microsoft Excel file. This includes key elements as demonstrated in Table 5.

2.8.1. Eligibility for Synthesis

In this systematic review, only studies that provided empirical, theoretical, or case-based evidence relating to at least one of the three targeted budgeting techniques (Top-Down, Bottom-Up, or ABB) were deemed eligible for synthesis. Inclusion was limited to studies published between 2014 and 2025, written in English, and accessible in full text through databases such as Google Scholar, Scopus, and Web of Science. Peer-reviewed articles, industry reports, and academic research were prioritized, excluding non-peer-reviewed sources or anecdotal evidence. Studies without a clear methodological framework or those lacking descriptive or comparative data on budgeting practices were excluded. A final set of 40 studies met these criteria and were subjected to full synthesis.

2.8.2. Data Preparation for Synthesis

Data from the eligible studies were systematically extracted and entered into a standardized Excel spreadsheet before the synthesis. Handling missing data was a critical aspect of the analysis. We clean the data by identifying and removing duplicate or redundant entries from various sources. The whole dataset was pre-processed to ensure consistency and comparability. The spreadsheet captured key characteristics shown in Table 5, such as publication year, budgeting technique(s) analysed, industry or sector of application, outcomes assessed (e.g., accuracy, resource allocation, stakeholder engagement), study design, and reported limitations. This approach ensured that the dataset was comprehensive and robust, allowing for a more accurate and reliable analysis.

2.8.3. Tabulation and Visual Display of Results

To enhance clarity and comprehension, the synthesized findings were presented in tabular formats and visual illustrations such as graphs and charts. A well-assembled complete table was created capturing the essential features of each study, including Paper Title, Citations, Year Published, Research Type (e.g., Journal Paper, Conference Paper), Online Repository (e.g., Google Scholar, Scopus), Journal Name, and Country of Authors. Tabulated results included comparative matrices of technique characteristics (advantages, disadvantages, and suitability), frequency of use across industries, and performance metrics (e.g., cost control, time efficiency, strategic alignment). RAWGraphs software was employed to generate visual representations. Showcasing effects, estimates, and confidence intervals for each study alongside a summary estimate.

2.8.4. Synthesis of Results

As part of our manual search on online repositories like Google Scholar, Scopus, and Web of Science, we carefully examined and combined findings from relevant studies. The way we synthesized the data depended on its nature and how much variation existed among the studies. This ensured that our analysis remained thorough, accurate, and reflective of the patterns observed across different sources. The results revealed that each budgeting technique exhibits unique strengths, top-down budgeting excels in strategic alignment and frequently applied in highly regulated industries such as pharmaceuticals and oil and gas., bottom-up budgeting promotes accuracy and proved effective in construction and engineering fields where detailed cost estimations are needed, and ABB supports detailed resource tracking and showed strong applicability in IT and communication sectors, optimizing resource allocation based on operational needs.

2.8.5. Exploring Causes of Heterogeneity

Heterogeneity among study results was explored by examining contextual variables. The systematic review identified various sources of budgeting technique effectiveness, such as the industry sector, where regulatory compliance requirements influence cost allocation strategies. Economic sectors such as market fluctuations and inflation, impact budgeting stability across different project management environments. Organizational structures and project complexity. The differences in study objectives, measurement tools, and outcome definitions also contributed to result variability.

2.8.6. Sensitivity Analyses

Sensitivity analysis was conducted to evaluate how variations in research methodologies and external influences affected the synthesized results. Identifying whether the removal of certain studies significantly alters conclusions drawn from the synthesis. Assessing how minor changes in financial parameters impact overall budgeting efficiency. Ensuring that findings remain valid across different analytical methods and assessment frameworks. The review established a comprehensive understanding of budgeting techniques in project management, ensuring its findings are applicable across diverse industrial sectors.

2.9. Reporting Bias Assessment

In conducting our systematic review on the application and advantages of effective budgeting techniques in project management, it was crucial to assess the risk of bias due to potentially missing results, particularly those arising from reporting biases such as selective publication or selective reporting of outcomes. These forms of bias can affect the reliability and generalizability of synthesized results, particularly when studies selectively report positive findings or unfavourable results. Studies with statistically significant or positive results are more likely to be published, while negative or inconclusive findings may remain unpublished. We recognized that these biases could significantly impact the validity and reliability of our synthesis, and thus, we employed a thorough and methodical approach to address this concern. A wide range of scholarly databases (Google Scholar, Scopus, Web of Science) was used to minimize publication bias. We opted for the use of contour-enhanced funnel plots, a powerful visual tool that allowed us to detect asymmetries in the data. These plots were carefully inspected to identify any potential publication bias by highlighting areas where studies might be missing due to bias versus those missing due to chance. Explicit criteria for study selection ensured unbiased representation of budgeting techniques. The inclusion of statistical significance contours provided us with a clear and intuitive way to differentiate between these two scenarios, offering a robust visual representation of potential biases. Only English-language studies were included. Although necessary for consistency, this criterion may have excluded valuable research conducted and published in other languages, particularly in non-Western contexts, potentially skewing the geographical representativeness of the results. We intentionally did not use automation tools for assessing reporting bias in this review. Instead, we opted for a manual approach, utilizing tools such as Excel for creating charts and plots. This hands-on method allowed us to carefully analyze and visualize the data, ensuring a detailed and thorough examination. By manually inspecting the data, we ensured that no subtle patterns or potential biases were overlooked. We also applied explicit and consistent selection criteria during the screening process, ensuring a fair and representative inclusion of studies across all three budgeting techniques: Top-Down, Bottom-Up, and Activity-Based Budgeting (ABB). This also helped prevent the overrepresentation of one method over the others due to selective inclusion.

3. Results

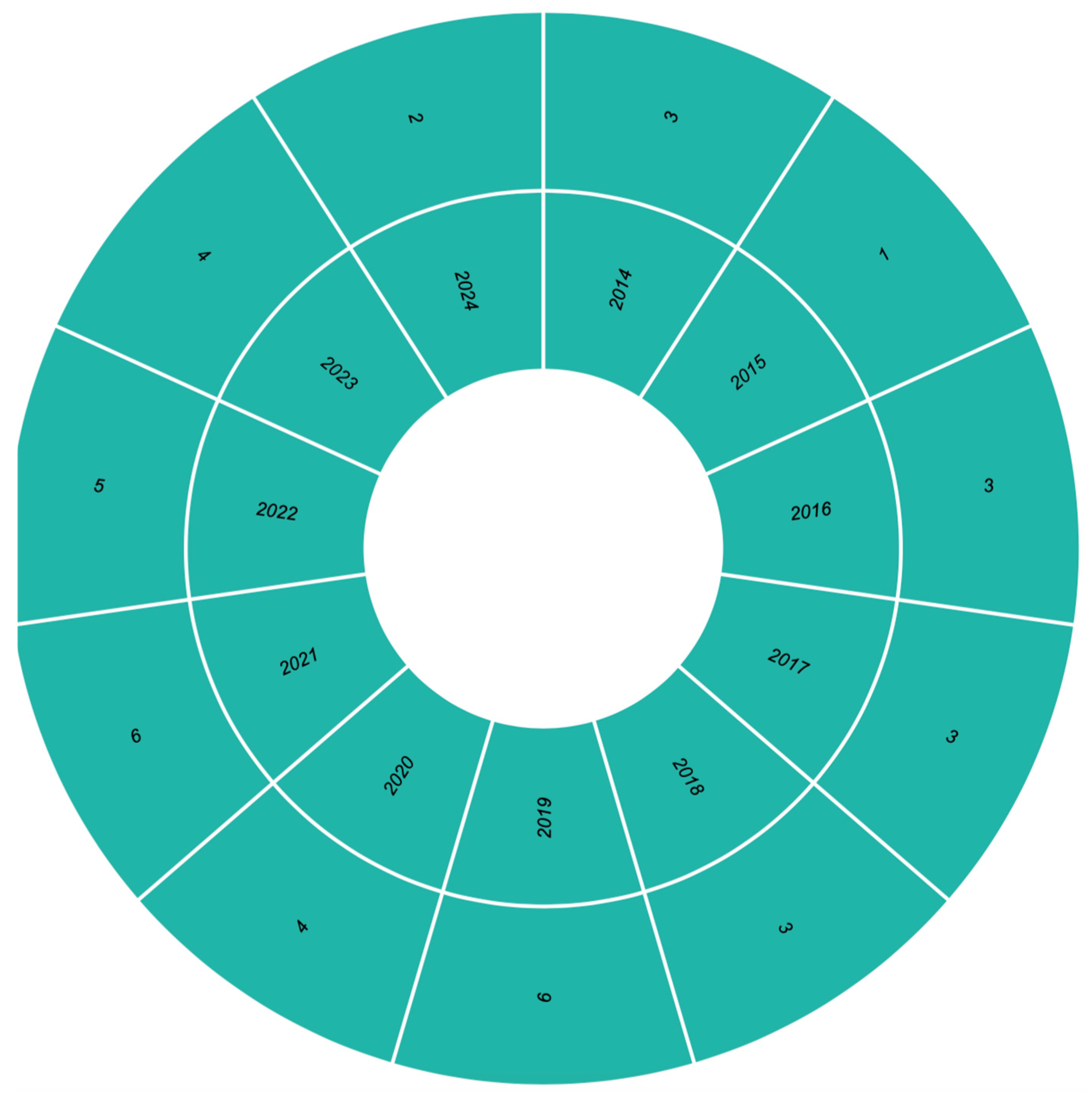

3.1. Publication Trends over Time

The temporal distribution of reviewed studies illustrates how research interest in budgeting techniques within project management has evolved between 2014 and 2023. Figure 6 presents a sunburst visualization of annual publication frequencies. The earliest contributions appeared in 2014 and 2015, reflecting initial efforts to frame budgeting techniques in project management discourse. From 2016 to 2018, publication frequency increased modestly, suggesting a steady but still limited academic focus on budgeting methodologies. A marked growth can be observed from 2019 onward, with 2020–2022 showing the highest activity. Specifically, 2020 and 2021 together accounted for 12 studies (30%), highlighting a surge of interest, likely linked to the rising complexity of projects in the digital transformation era and the disruptions caused by COVID-19, which emphasized the importance of accurate budgeting and financial control.

In 2023, the number of publications decreased slightly, but the overall trend indicates a consolidation of budgeting research in recent years. This trajectory suggests that budgeting techniques have gained recognition as a critical factor for project success, with the literature becoming more rigorous and methodologically diverse during the last five years.

Figure 6.

Publication Trends Over Time.

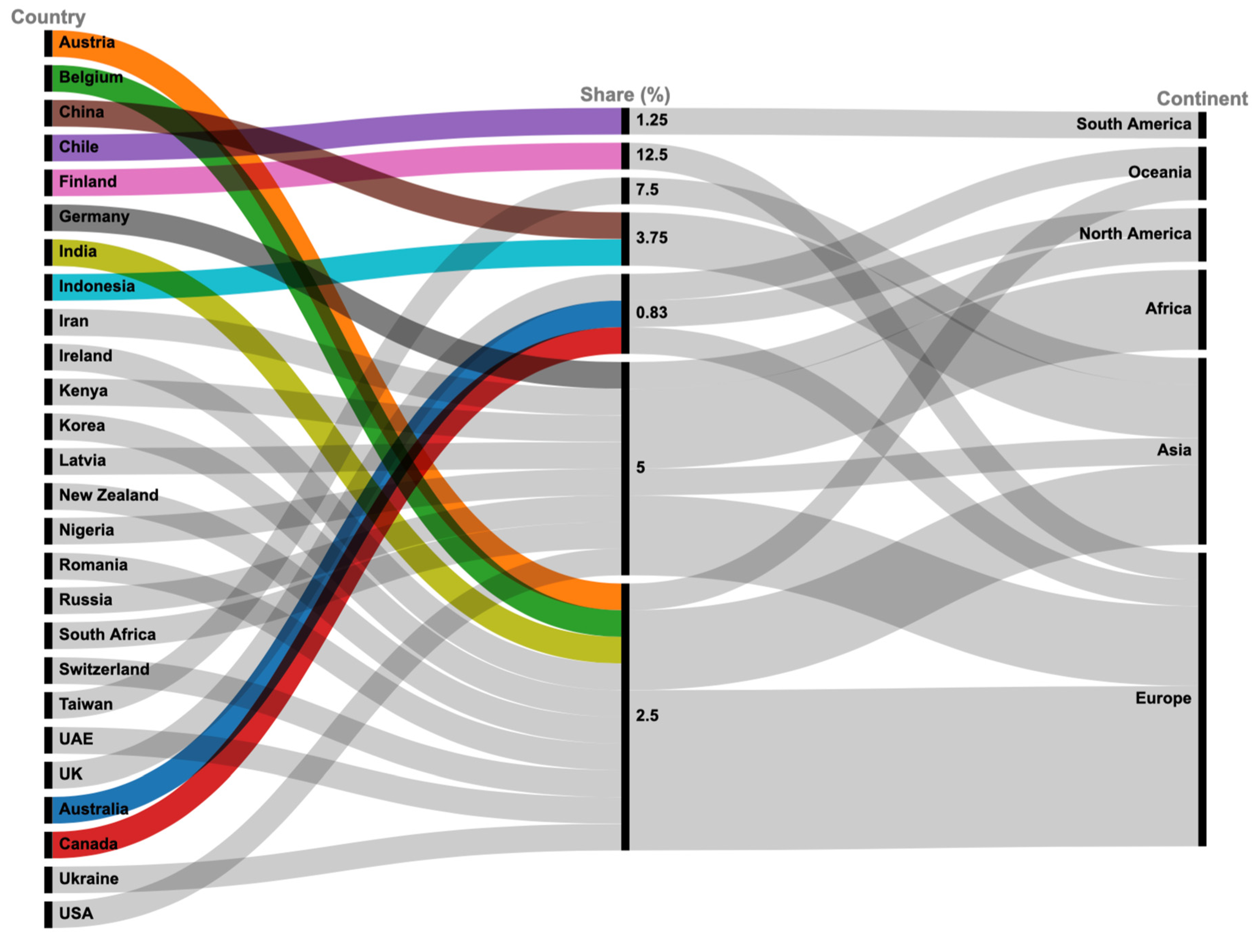

3.2. Geographic Distribution of Studies

The systematic review shows a wide global spread of publications, with the strongest representation from Europe (42.5%) and Asia (32.5%), followed by Africa (10%), North America (7.5%), Oceania (5%), and South America (2.5%). Within Europe, Finland (12.5%) leads, while Taiwan (7.5%) dominates the Asian contributions. Africa’s 10% share demonstrates increasing engagement from emerging economies such as Kenya, Nigeria, and South Africa. North America is represented by the USA and Canada, while Oceania contributes through Australia and New Zealand. South America is present via Chile.

This distribution confirms Europe as the central hub of scholarly output, with Asia showing dynamic growth. Meanwhile, Africa’s emerging presence highlights expanding interest in project budgeting research in developing regions.

Figure 7.

Geographic distribution of reviewed studies.

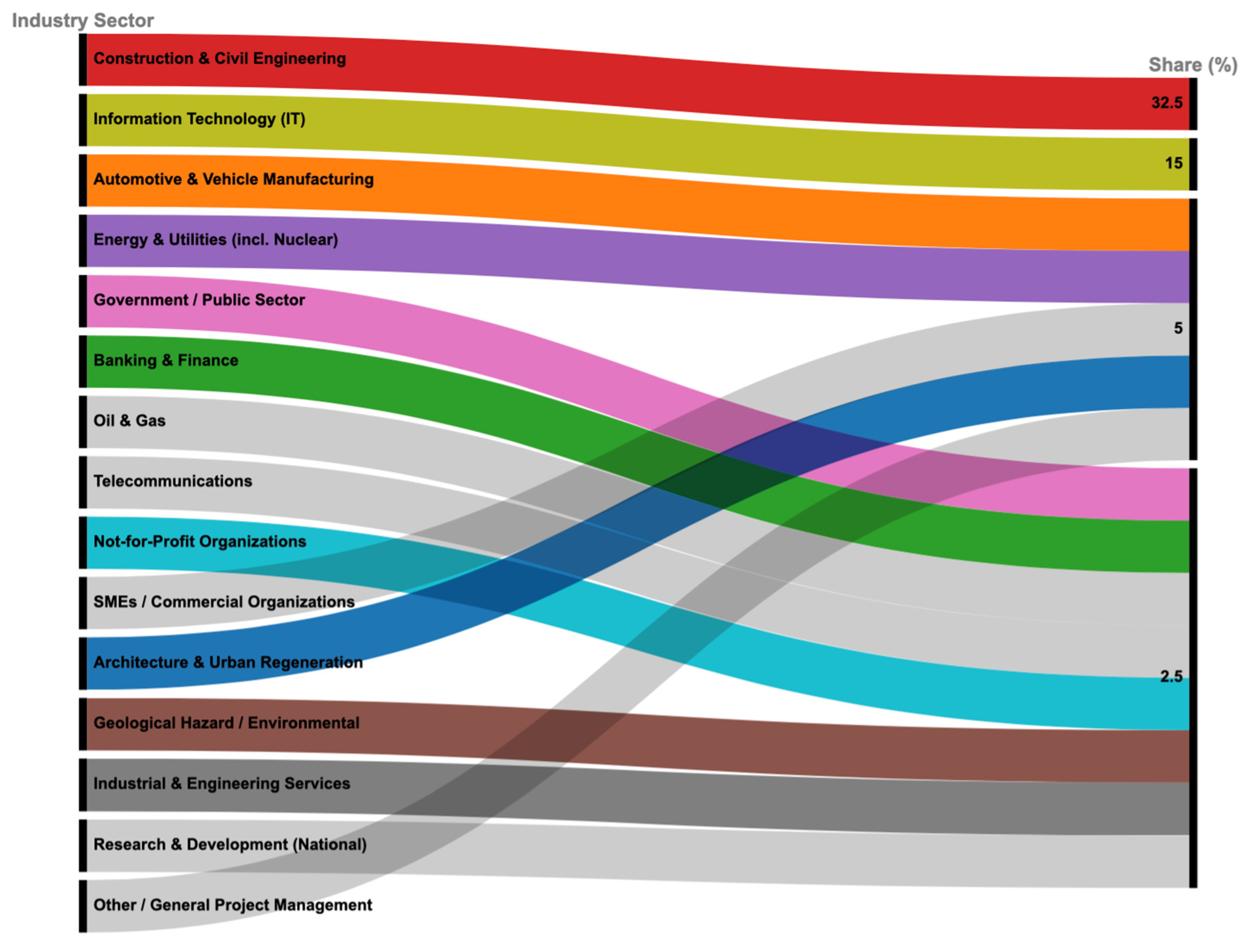

3.3. Industry Distribution of Reviewed Studies

The reviewed studies span a wide array of sectors, but contributions are concentrated in Construction & Civil Engineering (32.5%) and Information Technology (15%), which together account for nearly half of all studies. This reflects the critical role of budgeting and scope management in industries where cost overruns, delays, and complexity are common. Other notable contributions come from Manufacturing/Automotive (5%), Energy & Utilities (5%), and Public Sector/Government (2.5%). The remaining studies are dispersed across specialized fields such as Telecommunications, Banking, Oil & Gas, Urban Regeneration, and Not-for-Profit organizations, each contributing 2.5%.

This distribution demonstrates that while budgeting practices are universally relevant, industries with complex, resource-intensive, and high-risk projects dominate the academic and practical focus.

Figure 8.

Industry Distribution of Studies.

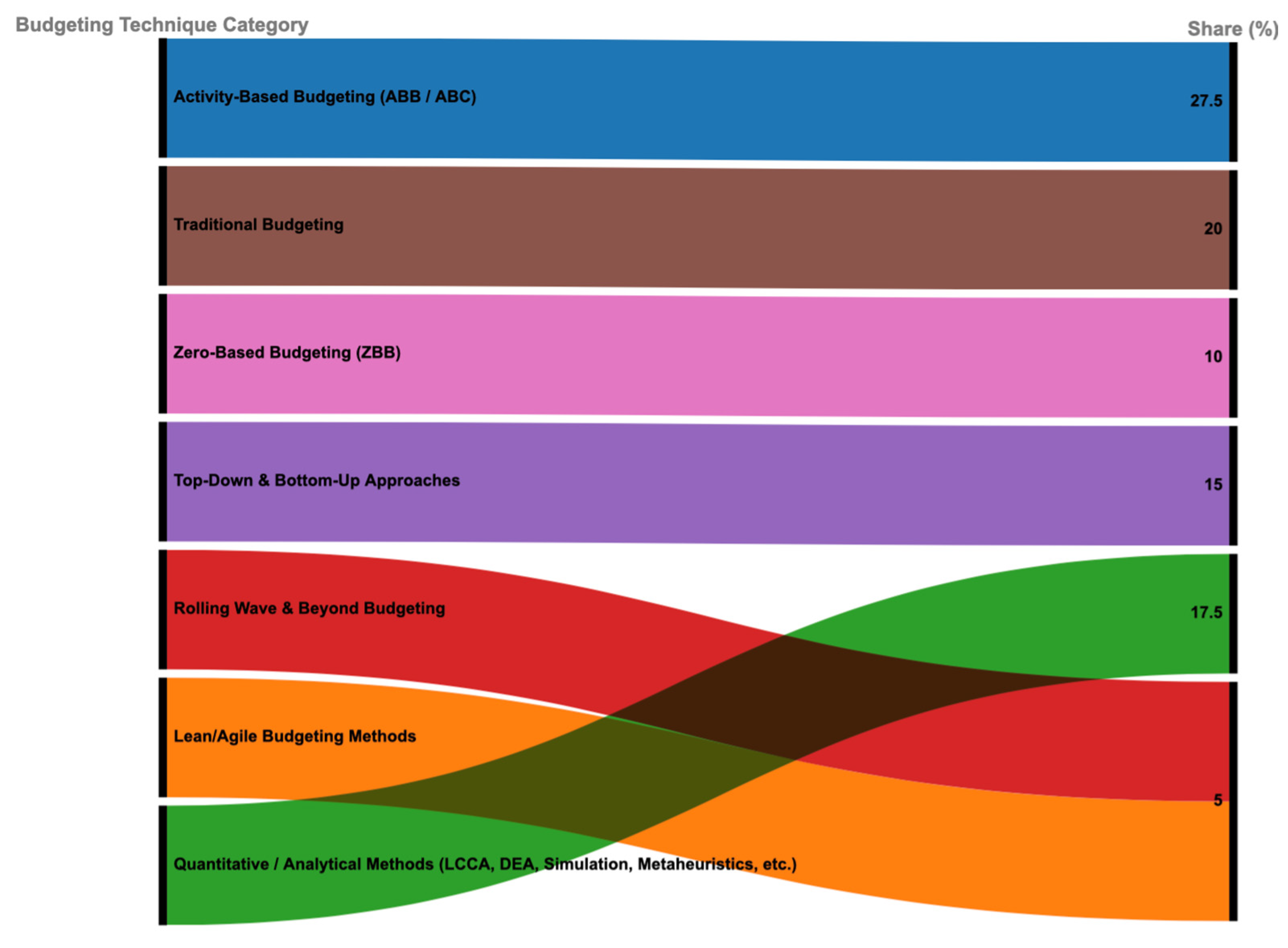

3.4. Budgeting Techniques Distribution in Reviewed Studies

The reviewed studies revealed a strong emphasis on Activity-Based Budgeting (27.5%), followed by Traditional Budgeting approaches (20%) and Zero-Based Budgeting (10%). Together, these three methods dominate the academic discussion, accounting for nearly 60% of the literature. Top-Down and Bottom-Up approaches (15%) also feature prominently, reflecting their widespread use in cost estimation and resource allocation for complex projects. More advanced or hybrid methods, such as Rolling Wave and Beyond Budgeting (5%), Lean/Agile-oriented budgeting (5%), and Other quantitative techniques (e.g., predictive analytics, life-cycle costing, metaheuristics) (17.5%), are less common but provide innovative perspectives in specialized contexts.

This distribution highlights that while Activity-Based and Traditional approaches remain dominant, there is a gradual shift toward data-driven, hybrid, and agile-oriented methods, reflecting the increasing complexity of projects and the need for dynamic financial planning.

Figure 9.

Categorization of Budgeting Techniques.

3.5. Comparative and Performance Focus in Budgeting Studies

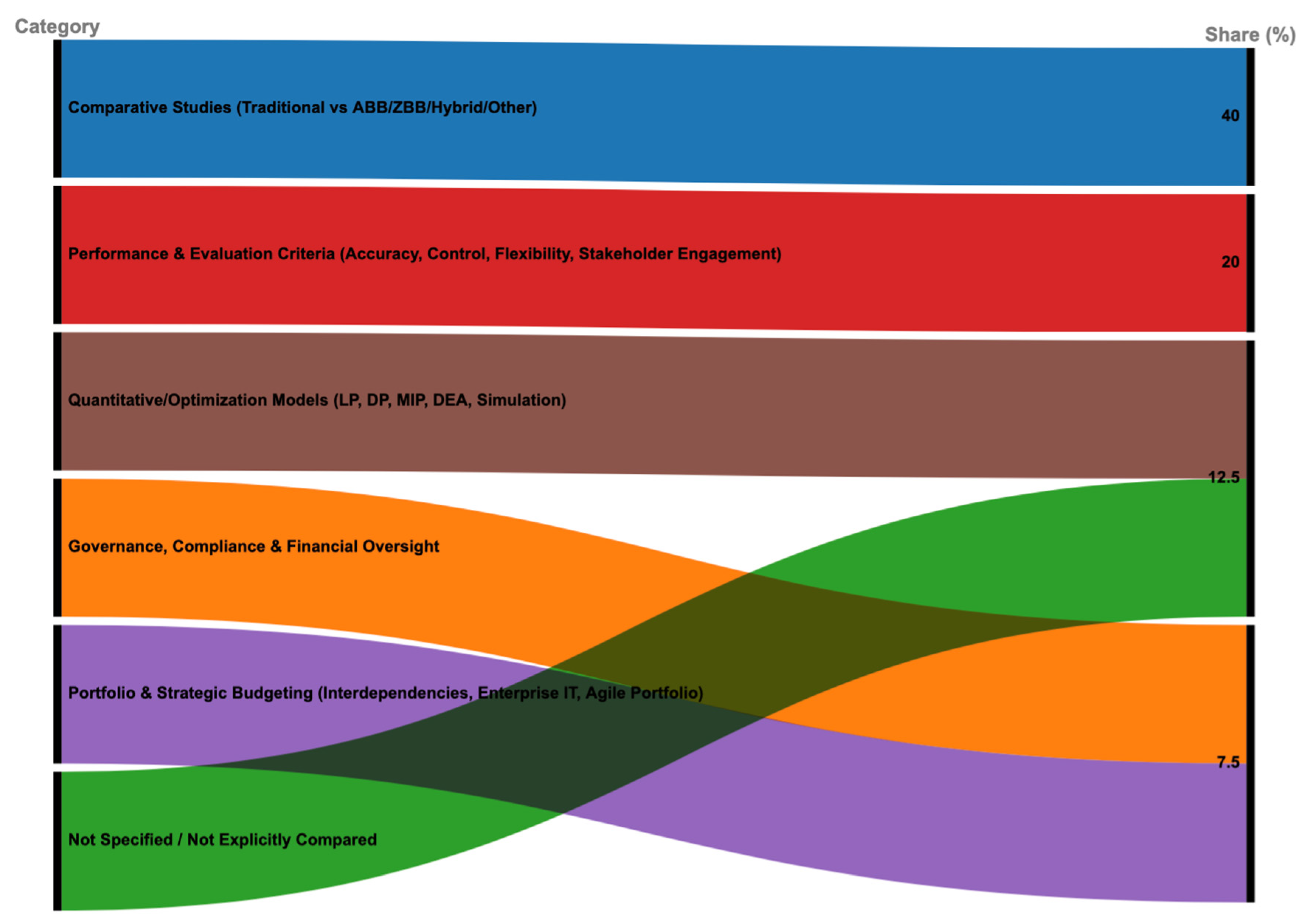

The extracted dataset shows that a substantial portion of studies emphasize comparisons between budgeting techniques (40%), particularly between traditional approaches and more modern methods such as Activity-Based Budgeting (ABB), Zero-Based Budgeting (ZBB), and simulation-based tools. Another group of studies (20%) centers on performance and evaluation metrics, such as accuracy, control, flexibility, cost-efficiency, and stakeholder engagement. Meanwhile, quantitative and optimization models (12.5%)—including linear programming, dynamic programming, and DEA—reflect a niche but growing interest in mathematical approaches to financial planning. A smaller segment (7.5%) focused on governance and compliance frameworks in budgeting, while “Not specified/Not explicitly compared” entries (12.5%) highlight incomplete methodological transparency.

The evidence reveals that the majority of the literature focuses on direct comparative analysis between budgeting techniques, often contrasting traditional models against more adaptive or analytical approaches. This trend underscores the ongoing shift from rigid, legacy frameworks toward data-driven and flexible budgeting strategies in project management.

Figure 10.

Categorization of Comparative/Performance Themes.

3.6. Reported Impacts of Budgeting Techniques

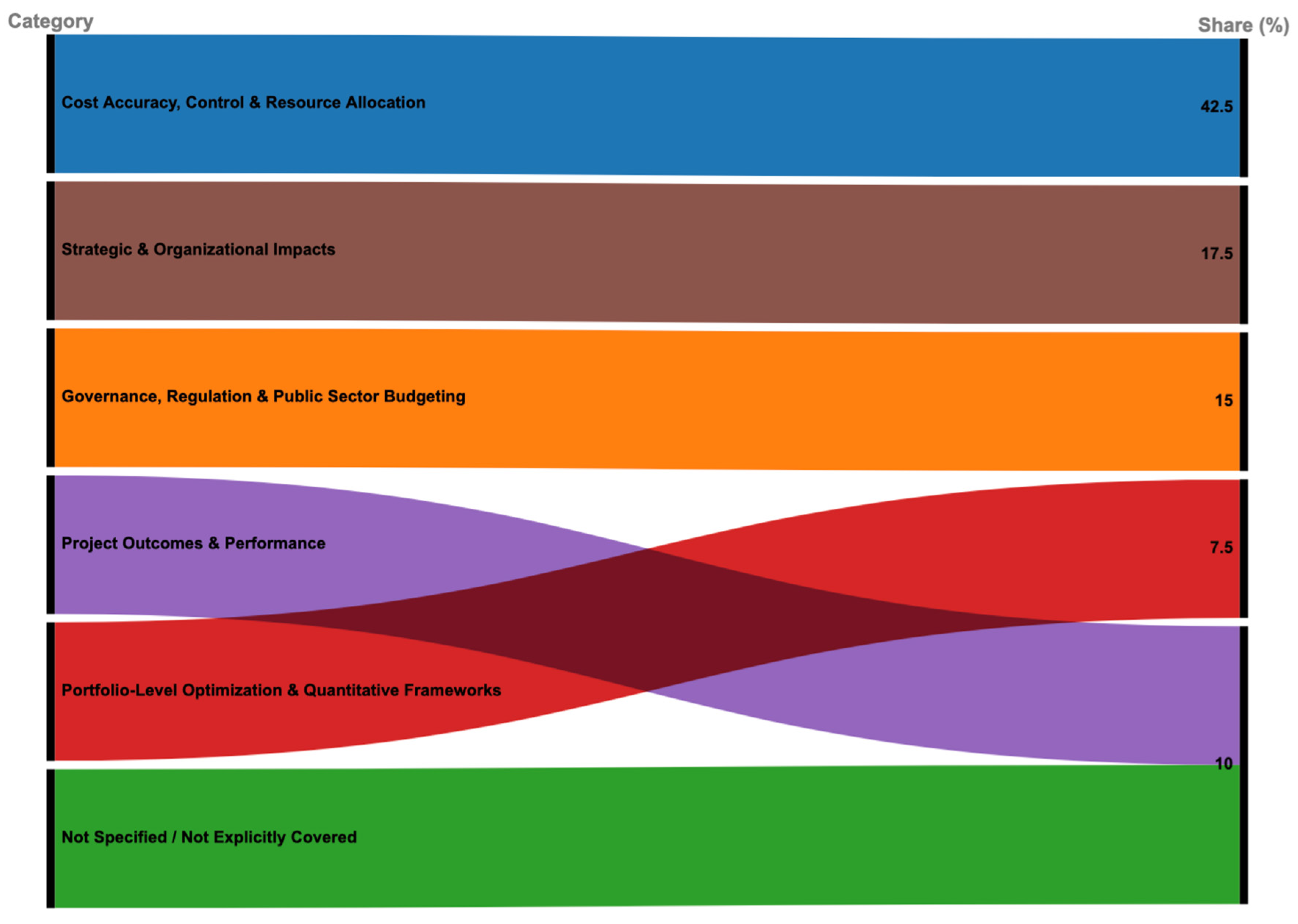

The reviewed studies consistently highlight that budgeting practices in project management have a direct influence on cost control, financial transparency, and resource allocation efficiency. A large proportion of studies (42.5%) focused on improved cost accuracy, control, and visibility, emphasizing how structured budgeting frameworks mitigate cost overruns, enhance estimation reliability, and support optimized resource utilization. A second cluster of findings (17.5%) addressed strategic and organizational outcomes, where flexible and lean budgeting approaches were linked to profitability, sustainability, and adaptability to market trends.

Another important share of the literature (15%) focused on public governance and regulatory impacts, including government budget allocation, compliance frameworks, and infrastructure planning. Meanwhile, 10% of studies analyzed performance and project outcomes, highlighting reduced time-cost overruns, better quality, and client satisfaction. Smaller proportions examined portfolio-level optimization and mathematical decision frameworks (7.5%), reflecting an emerging shift toward quantitative financial modeling in project contexts.

Finally, not specified or vaguely reported outcomes (10%) point to methodological gaps in transparency that limit broader synthesis. Overall, the evidence indicates that budgeting techniques play a multi-dimensional role, with cost-related impacts dominating, but also with clear extensions into governance, sustainability, and strategic adaptability.

Figure 11.

Categorization of Reported Outcomes.

3.7. Reported Challenges in Budgeting Techniques

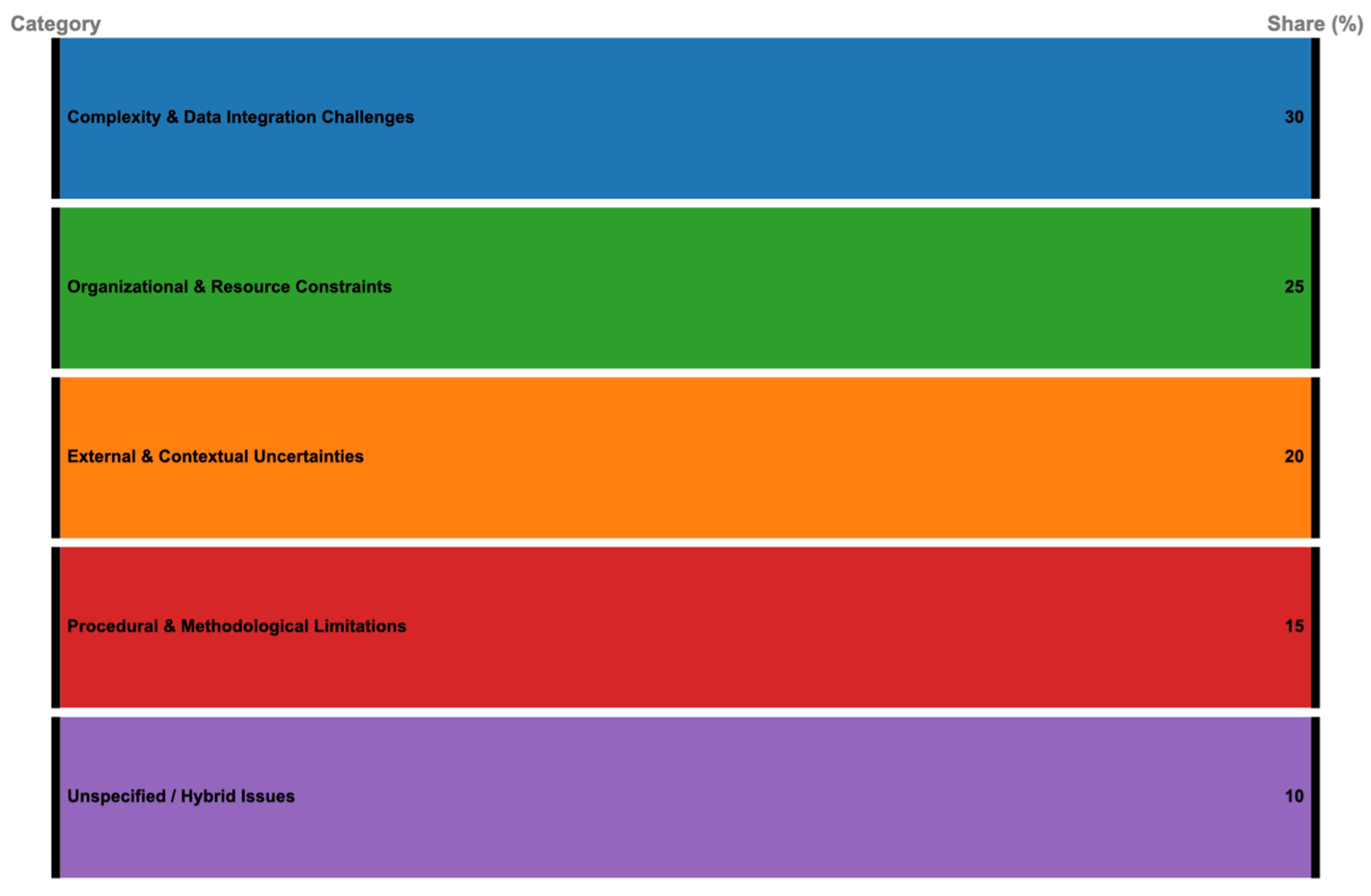

The reviewed studies reveal that budgeting in project management, while essential for financial control and strategic alignment, is often hindered by complexity, organizational resistance, and external uncertainties. A dominant theme (30%) concerns implementation complexity and data-related issues, including the need for real-time data, integration with existing management systems, and inconsistencies across sources. These challenges underscore the difficulty of operationalizing sophisticated budgeting methods without significant infrastructural and cultural shifts. Another major group of limitations (25%) relates to resource and organizational constraints, such as stakeholder resistance, lack of expertise, insufficient collaboration, and reliance on outdated IT systems. These issues reflect the socio-technical nature of budgeting practices, where organizational culture and human factors significantly shape success. A third cluster (20%) highlights external and contextual uncertainties, including economic volatility, inflation, political interference, and regulatory compliance. These external forces limit the stability and predictability of budgeting outcomes, particularly in large infrastructure and government-led projects. Methodological and procedural concerns accounted for 15% of the reported challenges. These include time-consuming processes, managerial conflicts of interest, non-uniqueness of modeling results, and insufficient guidelines, all of which affect the reliability and scalability of budgeting frameworks.

Figure 12.

Categorization of Reported Challenges in Budgeting.

Finally, a residual category (10%) covered unspecified or hybrid issues, where challenges were either vaguely reported or tied to technical proposals such as hybrid algorithms without clear applicability.

3.8. Technological Tools Supporting Budgeting Practices

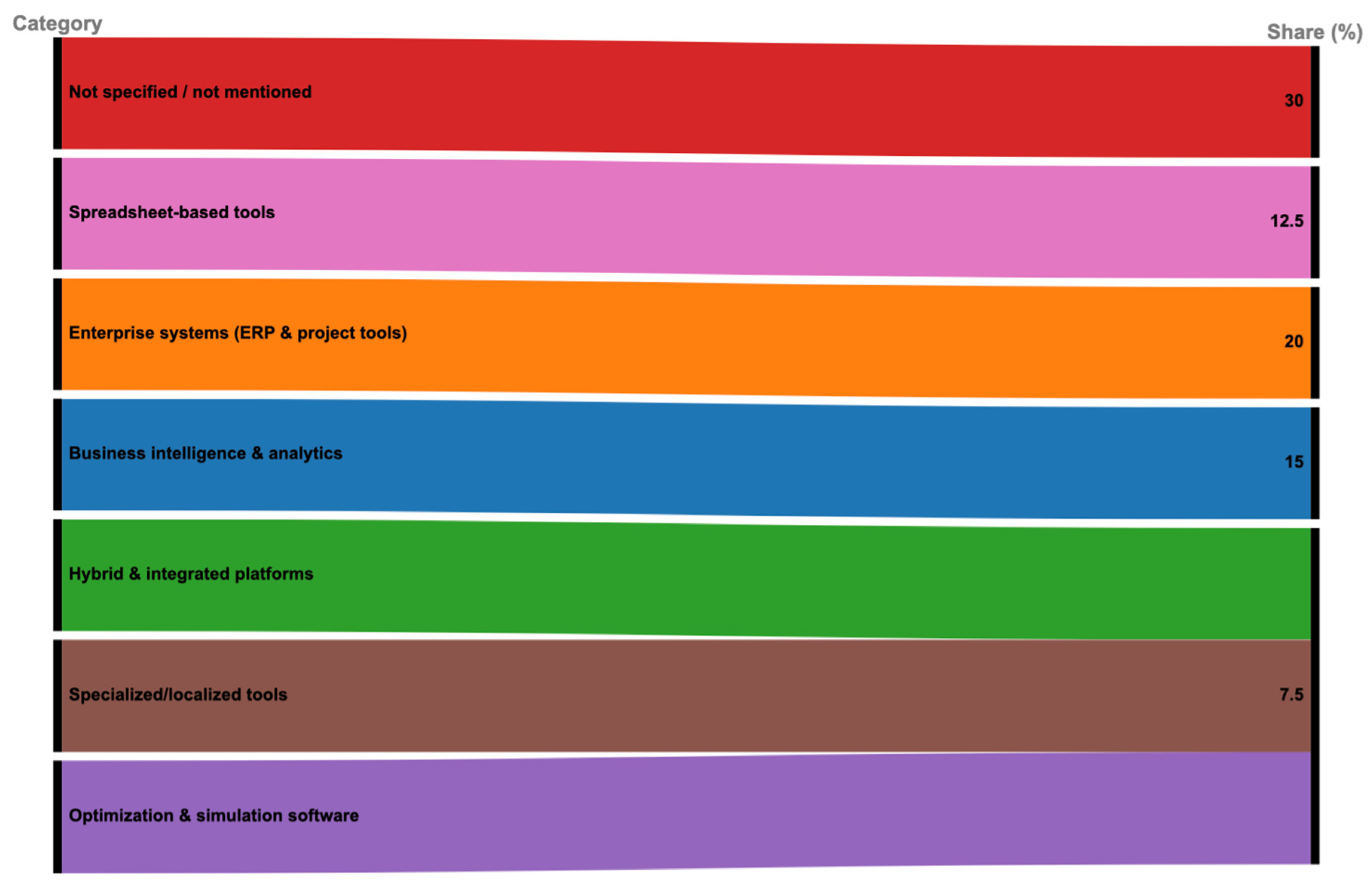

The evidence reveals that budgeting in project management is strongly shaped by the availability and integration of technological tools, ranging from basic spreadsheet software to advanced enterprise systems and predictive analytics. A significant portion of studies (30%) did not explicitly specify the tools used, reflecting either a focus on conceptual frameworks or limitations in reporting. Among those that did, Microsoft Excel emerged as the most dominant platform (12.5%), underscoring its continued relevance due to accessibility, flexibility, and ease of use in project budgeting across industries. Beyond spreadsheets, enterprise resource planning (ERP) systems and specialized cost management platforms were widely applied (20%), including SAP, Oracle P6, Primavera, and Microsoft Project. These systems facilitated large-scale integration, real-time cost tracking, and multi-stakeholder alignment, particularly in construction, IT, and government-led projects. A growing cluster of studies (15%) incorporated business intelligence (BI) and predictive analytics tools, including AI, machine learning, Monte Carlo simulations, SPSS, Power BI, and optimization software (e.g., IBM ILOG CPLEX). These approaches reflect the trend toward data-driven financial forecasting and scenario modeling, supporting proactive risk management and strategic decision-making.

A smaller group of studies (7.5%) referenced specialized sectoral or local government tools, such as NetMiner, DEA optimization software, or localized ERP systems tailored for specific national or organizational contexts.

Figure 13.

Categorization of Tools and Software in Budgeting Practices.

5. Conclusion

This systematic review synthesized findings from 40 scholarly studies published between 2014 and 2024, providing a comprehensive overview of budgeting techniques in project management. The evidence confirms that budgeting remains a decisive factor for project success, influencing cost accuracy, transparency, resource allocation, and organizational outcomes. The temporal analysis revealed growing scholarly attention to budgeting methodologies after 2019, reflecting the increasing complexity of projects and disruptions such as digital transformation and the COVID-19 pandemic. Geographically, research output is concentrated in Europe and Asia, with emerging contributions from Africa, signaling expanding interest in developing economies. In terms of industries, construction and information technology dominate, underlining the centrality of budgeting in high-cost, high-risk, and complex project environments. Across budgeting methodologies, Activity-Based Budgeting (ABB) emerged as the most frequently studied, followed by traditional and zero-based approaches. While Top-Down and Bottom-Up methods remain foundational for strategic alignment and detailed estimation, ABB demonstrates stronger contributions to cost efficiency in projects with well-defined activities. More advanced and hybrid approaches, including rolling forecasts, beyond budgeting, and data-driven methods, are gaining prominence, reflecting the shift toward adaptive and analytical financial planning.

Comparative studies highlighted the limitations of rigid traditional approaches when contrasted with flexible and technology-enhanced methods. Most notably, structured budgeting practices were consistently linked to improved cost control, reduced overruns, and enhanced organizational adaptability. However, the review also identified persistent challenges, including implementation complexity, stakeholder resistance, and external uncertainties such as inflation and regulatory constraints. These findings emphasize the socio-technical nature of budgeting, where both organizational culture and contextual factors determine success. Finally, the review underscores the growing role of technological tools in budgeting. While Microsoft Excel continues to dominate due to accessibility, advanced ERP systems and predictive analytics platforms are increasingly applied, enabling real-time data integration, scenario modeling, and improved decision-making. This trend reflects the broader movement toward data-driven project management and financial forecasting.

References

- Aalto, O., & Varis, K, 2020. Controller as Strategic Partner in Project-Based Business. Turku amk, 20(2), p. 23.

- Aaltonen, A., 2023. Defining a Budgeting Tool for Projects. [Online] Available at: https://ijietap.journals.publicknowledgeproject.org/index.php/ijie/article/download/8421/1329.

- Adafin, J., Rotimi, OB, J. & Wilkinson, S., 2021. An evaluation of risk factors impacting project budget performance in New Zealand. Emerald Insight, 19(1).

- Alu, A. J., Frank, A. & Ogedengbe, F. A., 2023. Evaluating the Effect of Cost Management Practices on Profitability and Financial Stability in Nigerian Construction Firms: A Theoretical and Conceptual Perspective. Research Article, 29(4).

- Anon., 2017. RESOURCE SCHEDULING AND PROJECT PERFORMANCE OF INTERNATIONAL NOT-FOR PROFIT ORGANIZATIONS IN NAIROBI CITY COUNTY,KENYA. International Academic Journal of Information Sciences and Project Management, 2(2), pp. 199-217 .

- Anon., 2021. STELLENBOSCH UNIVERSITY. [Online] Available at: https://libguides.sun.ac.za/c.php?g=742949&p=5315983.

- Anon., 2024. LIbGUides. [Online] Available at: https://belmont.libguides.com/Scopus [Accessed 23 04 2025].

- Anon., 2025. Harvard Library. [Online] Available at: https://library.harvard.edu/services-tools/web-science [Accessed 23 04 2025].

- Aziz, M. Y., 2014. Business Intelligence Trends and Challenges. BUSTECH 2014 : The Fourth International Conference on Business Intelligence and Technology.

- Chakko, J. P., Huygh, T. & Haes, S. D., 2015. Achieving Agility in IT Project Portfolios – A Systematic Literature Review. Springer Nature, p. 71–90.

- Cleary, P., Quinn, M., Rikhardsson, P. & Batt, C., 2022. Exploring the Links Between IT Tools, Management Accounting Practices and SME Performance: Perceptions of CFOs in Ireland. Accounting, Finance & Governance Review, Volume 28.

- Dadpour, M., Shakeri, E. & Nazari, A., 2019. Analysis of Stakeholder Concerns at Different Times of Construction Projects Using Social Network Analysis (SNA). s.l., SPRINGER NATURE .

- Dilger, h., Ploder, C. & Wolfgang Haas, P. S. R. B., 2020. Continuous Planning and Forecasting Framework (CPFF) for Agile Project Management: Overcoming the. SIGITE, pp. 371 - 377.

- Dvulit, Z., Peredalo, K., Tylipska, R. & Terno, R., 2019. THE PROJECT ESTIMATION TECHNIQUES’ APPROACHES. s.l., Research Gate.

- Elghaish, F., Abrishami, S., Hosseini, M. R. & Abu-Samra, S., 2012. Revolutionising cost structure for integrated project delivery: a BIM-based solution. s.l., Engineering, Construction and Architectural Management.

- Guinan, B., 2024. bright work. [Online] Available at: https://www.brightwork.com/blog/external-and-internal-factors-to-include-in-project-planning [Accessed 23 04 2025].

- Hitz, C., Krey, M. & Marius Albath, R. W. a. P. T., 2019. IT-Budgeting Processes in Swiss Banks and How They Are Influenced by Rapidly Changing Regulatory Requirements. EU Research in Business, 2018(2018), p. 10.

- Huang, W., 2018. Developing a Better Planning, Budgeting,, s.l.: Springer Nature Link.

- Huang, W., 2019. Developing a Better Planning, Budgeting,. China: Check for Updates.

- Huke, J. & Siegfried, P., 2021. Finance Methods in the Automotive Sector - Business Agility in the Age of Digital Disruption. International Journal of Automotive Science And Technology, 5(3), pp. 281 - 288.

- Ishmuradova, I. I., Karamyshev, A., Lysanov, D. & Isavnin, A. G., 2019. Persectives of Application of Project Budgeting in Commercial Organizations. s.l., 12th International Conference on Developments in eSystems Engineering (DeSE).

- Jowah, L. & Mkuhlana, X., 2021. BUDGETING SYSTEMS AND PROJECT EXECUTION AT A SELECTED GOVERN. Journal of Public Administration and Development Alternatives , 6(2), p. 16.

- Kalle, S., 2020. Financial Planning & Analysis Tool for Commissioning. s.l.:s.n.

- Kalle, S., 2020. FP&A Tool for Architectural Design Projects, Haaga Helia: Haaga Helia University of Applied Science.

- Khanyi, M. B. et al., 2024. A Roadmap to Systematic Review: Evaluating the Role of Data Networks and Application Programming Interfaces in Enhancing Operational Efficiency in Small and Medium Enterprises. MDIP, 16(23).

- Koroļova, A. & Treija, S., 2019. Participatory Budgeting in Urban Regeneration: Defining the Gap Between Formal and Informal Citizen Activism, Riga, Latvia: Riga Technical University.

- Kurakova & Oksana, 2017. Use of budget- and process-based planning in. Moscow, Web of Conference.

- Liang, Y.-C. & Chuang, C.-Y., 2014. Variable neighborhood search for multi-objective resource allocation problems. Science Direct, 29(3), pp. 73-78.

- Mtjilibe, Tshepang and Rameetse, Emmanuel and Mgwenya, Nkosinathi and Thango, Bonginkosi, Exploring the Challenges and Opportunities of Social Media for Organizational Engagement in SMEs: A Comprehensive Systematic Review (July 06, 2024). Available at SSRN: https://ssrn.com/abstract=4998542 or http://dx.doi.org/10.2139/ssrn.4998542.

- LIU, S.-S., ARIFIN, M. & CHEN, A. W. T., 2022. An Integrated Optimization Model for Life Cycle Pavement Maintenance Budgeting Problems. IEEE Access, p. 17.

- Lou, A. K. B. & Alireza Parvishi, E. J., 2016. COST MANAGEMENT IN CONSTRUCTION PROJECTS WITH THE APPROACH. The iioab Journal.

- Luo, G. et al., 2024. Cost Estimation for the Operation and Maintenance of Automated Monitoring and Early-Warning Equipment for Geological Hazards. MDIP, 16(23).

- Melese, F., Richter, A. & Solomon, B., 2015. Military Cost–benefit. London: Routledge.

- Naidoo, V. & Verma, R., 2023. Contemporary Challenges for Agile Project Management. USA: IGI Global.

- Okorie, V. N., Okoro, C. S. & Musonda, a. I., 2016. Leadership influence on construction site workers’ health and safety behaviour. SA, s.n.

- Thango, B. A., & Obokoh, L. (2024). Techno-Economic Analysis of Hybrid Renewable Energy Systems for Power Interruptions: A Systematic Review. Eng, 5(3), 2108-2156. [CrossRef]

- Oliveira, A. B. d., 2018. Budgeting Tool for Private Residential Construction , s.l.: Bachelor’s Thesis Plan Degree Programme in International Business .

- Park, K., Sim, H. & Cha, S., 2022. A Study on the Improvement of National R&D. Asian Journal of Innovation and Policy, 11(3), p. 21.

- Pendharkar, P. C., 2014. A decision-making framework for justifying a portfolio of IT projects. ScienceDirect, 32(4), pp. 625-639.

- Nethanani, Ronewa and matlombe, luzuko and Vuko, Siphethuxolo N. and Thango, Bonginkosi, Customer Relationship Management (CRM) Systems and their Impact on SMEs Performance: A Systematic Review (October 21, 2024). Available at SSRN: https://ssrn.com/abstract=4996185 or. [CrossRef]

- Pingilili, A. et al., 2025. Guiding IT Growth and Sustaining Performance in SMEs Through Enterprise Architecture and Information Management: A Systematic Review. MDIP, 5(2).

- Rajan, D., Barroy, H. & Stenberg, K., 2016. Chapter 8 Budgeting for health. s.l.:ResearchGate.

- Rani, P. & Dharyan, S., 2023. Implication of Budgeting on Contemporary Project Management. EBSCOhost.

- Simon, K., Morrisson, M. & Paul., S., 2024. Financial resource scheduling and road construction projects performance in Nairobi Metropolitan, KenyaInternational Journal of Research in Business and Social Science. International Journal of Research in Business and Social Science, 13(4), pp. 223-229.

- Ngcobo, Kwanele and Bhengu, Sandiswa and Mudau, Ambani and Thango, Bonginkosi and Lerato, Matshaka, Enterprise Data Management: Types, Sources, and Real-Time Applications to Enhance Business Performance - A Systematic Review (September 26, 2024). Systematic Review | September 2024 |. https://doi.org/10.20944/preprints202409.1913.v1, Available at SSRN: https://ssrn.com/abstract=4968451. [CrossRef]

Table 2.

Proposed Inclusion and Exclusion Criteria.

| Criteria | Inclusion | Exclusion |

|---|---|---|

| Topic | Studies focused on examining top-down, bottom-up, or activity-based budgeting in project management | Studies not focusing on the three budgeting techniques of Project Management (top-down, bottom-up, or activity-based budgeting) |

| Research Framework | The researched papers must include research methodology for top-down, bottom-up, or activity-based budgeting in project management | Articles must exclude research framework or methodology that are not related to top-down, bottom-up, or activity-based budgeting in project management |

| Language | Publications must be written in English only | Publications not written in English |

| Period | Articles between 2014 to 2025 | Articles outside 2014 and 2025 |

Table 3.

Results Achieved from Literature Search.

| No. | Online Repository | Number of results |

|---|---|---|

| 1 | Google Scholar | 841 |

| 2 | Web of Science | 2 |

| 3 | Scopus | 2 |

| Total | 845 |

Table 5.

The proposed characteristics of scholarly papers.

| Characteristics |

| Title Year of Publication Research Data Source Research Type Country of Authors Industry/Application (IT, Construction, Healthcare, etc.) Types of Budgeting Techniques Reviewed (Top-Down Budgeting, Bottom-Up Budgeting, Activity-Based Budgeting, Rolling Wave Budgeting, Zero-Based Budgeting) Comparison of Budgeting Methods (Control, Flexibility, Accuracy, Stakeholder Engagement) Impact of Budgeting Techniques on Project Success (Cost Control, Transparency, Efficiency in Resource Allocation) Challenges in Selecting and Implementing Budgeting Approaches (Complexity, Resistance from Stakeholders, Time-Intensive Analysis) Best Practices for Effective Project Budgeting (Hybrid Budgeting Approaches, Regular Budget Reviews, Integrating Risk Analysis in Budgeting) Case Studies on Budgeting Techniques (Government Infrastructure Spending, Agile Software Development, Healthcare Project Financing) Software and Tools for Budgeting in Project Management (Microsoft Project, Primavera, SAP, Oracle P6) Future Research Recommendations |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.