Submitted:

01 August 2024

Posted:

06 August 2024

You are already at the latest version

Abstract

This study examines the integration of Environmental, Social, and Governance (ESG) factors into global banking practices and their impact on financial stability, measured by the Bank to Capital Asset Ratio. Through a comprehensive literature review and data analysis, the paper highlights the dual role of banks as catalysts for ESG investment and risk managers. It discusses the challenges and opportunities in transitioning to ESG-aligned business models, emphasizing the importance of regulatory frameworks and risk management approaches. The findings suggest that ESG integration enhances bank stability and competitiveness, contributing to sustainable economic development. The paper concludes with policy implications and recommendations for further integration of ESG factors into banking governance.

Keywords:

ESG factors

; Banking Stability

; Financial Performance

; Bank to Capital Asset Ratio

; Sustainable Finance

; Risk Management

1. Introduction

To be achieved, the objective of a complete ecological transition requires the transfer of a huge amount of financial resources and in this context the banking sector can play a crucial role.

This paper intends to satisfy two objectives:

- propose a theoretical reflection on the possible impacts of ESG factors on the management of banking institutions through a systematic analysis of the most recent literature;

- measure the impact of ESG factors on banking stability assessed as Bank to Capital Asset Ratio % at a global level.

The role that can be taken on by banks consists of catalysing if they manage to direct private and public capital to finance ESG investments. The success of this objective would produce important returns, both reputational (i.e., greater customer trust in those banks that take a more active role for the growth of their territories, financing initiatives with environmental and social impact) but also economic for the banks. The path to completing the ESG transition by banking institutions is not yet concluded as highlighted by La Torre (2021) who states: “to date, the sustainable transition of banks seems motivated more by branding issues and compliance obligations, rather which gives performance and financial sustainability objectives”. In one of his studies which will be illustrated in detail in a subsequent section of this paper, he highlights some of the possible motivations that push banks to implement strategies with an environmental and social impact. According to these authors, the transition from financial sustainability to ESG (Environmental, Society, Governance) sustainability requires the implementation of changes in three directions: 1) the implementation of integrated accounting that links accounting metrics and market-based ones with ESG metrics; 2) from the point of view of the regulatory authorities, the challenge to be faced is the construction of a harmonized ESG rating framework and giving incentives to financial institutions to acquire impact-oriented business models; 3) from the point of view of individual banking institutions it is necessary to move from a credit risk management approach to sustainability risk management approaches. These new risk management approaches aim to reduce the volatility that threatens the financial stability of banking institutions (and not only) by integrating financial risk with ESG risks. In particular, these risk management models focus on sustainability risk, i.e., the set of environmental, social and governance factors that can negatively impact the assets of banking institutions, investment funds and companies as well as their overall performance.

This paper starts from the belief that has emerged in recent years in the debate between academics, managers and finance experts that sustainability has become a crucial strategic driver for the competitiveness of banking companies and can play an important role in the transformation of banking business models. In this regard, a research group from the Polytechnic University of Milan conducted a survey in 2021 on a sample of banks representing 71% of the total assets of the Italian banking system to give a snapshot of the state of the art of the integration of ESG factors in the credit sector and identify some possible lines of development. According to this survey, 92% of the banks interviewed are aware of the long-term financial relevance of ESG factors. Only 9% of them consider the financial impacts of ESG in their risk appetite statement. To confirm this, with reference to the policies adopted, for 91% of banks the percentage of credit flows destined for businesses and projects with a high environmental impact is below 25%. Among the ESG factors, it is the environmental one that is capturing the attention of banks the most; in fact, more than half of them have already activated sustainable credit lines from an environmental point of view and the other half plan to do so in the short term. The integration of ESG factors has made further progress in investment activity: for 25% of banks, up to 75% of investment flows are influenced by sustainability policies. 33% of banks adopt ESG risk assessment and screening processes in building their investment portfolio. With reference to ESG risks, despite pressure from regulators, climate risk assessment is poorly developed. This is because there is a lack of dedicated risk management, there is little use of stress testing techniques and analysis of climate scenarios and there is particular divergence regarding the most appropriate time horizon in which physical and transition climate risk manifests itself. From an organizational point of view, 37% have not yet developed governance dedicated to sustainability or do not follow a structured approach. Almost 50% of them do not systematically consider ESG factors as part of their business strategy and if they do, they go beyond corporate social responsibility principles and place sustainability at the heart of the business. A critical issue that most of the banks interviewed have in common and which is one of the impacts attributable to the inclusion of ESG factors in banking businesses according to many of the studies that will be illustrated below, is the poor integration of ESG factors in the associated risk management techniques to lending and investment activities (almost 67% of banks report a significant delay in this regard). This criticality highlights that ESG profile evaluations are almost completely absent both in loan pricing decisions and in the evaluation of guarantees. The banks interviewed denounce as the cause of these delays in the adoption of ESG factors the presence of unclear regulatory requirements, the lack of data which hinders the integration of ESG factors, the persistence of high uncertainty regarding the economic benefits deriving from from their inclusion.

In light of the previous considerations, the future of any financial institution can no longer ignore a new approach to finance, namely that of sustainable finance. For these reasons, the topic of sustainable finance or social impact finance has become the focus of the regulation of the main national and international supervisory institutions in the credit sector. This last consideration should not lead one to think that the application of ESG (Environmental, Society, Governance) factors is an obligation rather a real opportunity for change in banking businesses in all their facets from the configuration of the strategies to be adopted, from the type of product and services to offer, from the management of relationships with customers and the assessment of the risks affecting them. In this regard, Simsek and Cankaya (2021) examine the link between ESG scores and financial performance in banks in G8 countries. They find a positive correlation, suggesting that higher ESG scores are associated with better financial outcomes. The introduction of risks linked to ESG issues expands the taxonomy of banking risks and in particular by managing in a more conscious way the interconnections between environmental risks and financial risks, primarily credit risk, allows a reduction in the incidence of non-performing loans in balance sheets of financial institutions. Therefore, the ability of banks to grow in the near future must be commensurate with the creation of an increasingly complete introduction of ESG factors into their businesses supported by regulatory evolution. To confirm what has just been said, the supervisory institutions have introduced “ambitious” packages of measures/regulations aimed at sustainability. Above all, it was environmental problems (therefore relating to the first ESG pillar) that attracted the majority of global initiatives. When we talk about sustainability we are referring to environmental, social and governance-related sustainability. In the first case, reference is made mainly to climate changes to be reduced and adapted to, ecological behaviours, environmental risks, primarily natural disasters. Social sustainability is interconnected with environmental sustainability because climate shocks can generate inequalities and increases in poverty.

The sustainability of governance concerns, for example, relations with employees and their remuneration and that of managers. In particular, the European Commission has developed a community action plan “the Action Plan” for sustainable finance which intends to achieve a compensation between the financial needs of the world and European economy and the protection of the quality of the environment and of our society. To meet this macro objective, this action plan sets three micro objectives: 1) reorient capital flows towards a more sustainable economy, 2) integrate sustainability into risk management, 3) promote transparency and long-term perspective term. The European Union has invested at least 20% of its budget in the fight against climate change. Another supervisory institution, the European Banking Association (EBA) has designed an Action Plan structured in three mandates: the first mandate provides for the inclusion of ESG factors in the supervisory review and evaluation process (SREP), the second mandate concerns the inclusion of ESG factors in the third pillar, the third mandate explains how a prudential treatment of ESG exposures is to be achieved in the first pillar. The EBA has also published three important documents with a view to the ESG transition in the credit sector: the guidelines on the granting and monitoring of loans and the discussion document on the management and supervision of ESG risks and finally a guide on climate and environmental risks . The first document is aimed at encouraging greater inclusion of considerations relating to ESG issues in the credit management process. In particular, this inclusion requires banks to implement ten-year long-term plans. The second document represents a first attempt to propose the inclusion of ESG factors in the regulatory and supervisory framework. In particular, the objective is to achieve climate neutrality by 2050. Among environmental risks, climate risks generated by physical and meteorological events and transition risks that derive from rapid changes in the values of assets occupy a prominent place. The management of risks that integrate with financial risks requires banks to adopt a “holistic” approach since ESG risks cannot be configured as “stand alone” risks whose effects can only be seen in financial terms. In light of these considerations which define the theoretical framework within which this paper is inserted, banks must adopt a new credit culture and at the same time will guide companies towards building a more resilient and sustainable bank-business relationship. The governance of credit institutions must be able to approach the risks associated with lending in a context of sustainability, must have in-depth knowledge of the social context of the person requesting the loan and finally guarantee sustainability conditions in the medium-long term.

These challenges for banking governance will translate into a change in the approach of the European regulator from a reactive nature which proposes an ex post management of non-performing loans to a proactive ex ante approach which is characterized by a precautionary vision of credit management. Another important consideration that explains the important role that banking institutions can assume in this process of transition towards sustainable finance is that they play the role of both suppliers and users of information relating to environmental factors, primarily changes climate. In this sense, banks can exacerbate the risks if, through their investments, they finance the economic activities that represent the originating causes of climate shocks and natural events or at the same time they can promote the creation of a low-carbon economy, focusing their strategies of future investments on the reduction of climate impacts. The implementation of ESG factors in the credit sector concerns not only risk management processes but also internal control systems and the compliance function. In fact, banks will have to tend to be increasingly ESG compliant, guaranteeing greater information transparency on environmental and social risks, starting from compliance with environmental and safety regulations. The ESG Compliance function can help the bank assess the materiality of the impacts of ESG factors on financial performance from a long-term management perspective. The compliance function may require a refocus towards internal regulations (rather than being structured looking exclusively at external supervisory requirements) i.e., greater integration of ESG risks into the governance structures of banking institutions.

The paper presents a structure divided into five sections. After the introductory part, the second section contains a literature review focusing mainly on the impacts of ESG factors on the financial performance of banks. The third section contains an analysis of the trends at a global level in terms of the value of banking stability. The fourth section contains an analysis conducted through the application of the k-Means machine learning algorithm optimized with the Silhouette coefficient and the Elbow Method. The fifth section presents the policy implication. The sixth section concludes.

2. ESG Factors and the Financial Performance of Banking Intermediaries: A Review

This section has the main objective of illustrating how issues relating to ESG aspects have entered into the construction of strategies, business models and the assessments and management of the main risks inherent in the bank-business relationship. To do this, we propose a systematic analysis of recent studies that have fueled the scientific debate on these aspects, highlighting how ESG factors represent a fundamental driver for greater competitiveness of banking intermediaries in a context that is becoming increasingly uncertain and in which the ability creating value can no longer be measured by looking exclusively at the achievement of financial sustainability objectives. In order to strengthen its ability to influence territorial development processes, any company, and therefore also banking companies, must be able to plan operational choices that produce significant impacts at an environmental and social level and on the related internal governance (i.e., on the three dimensions ESG). Therefore, it is necessary for banking companies to also be able to seize all the opportunities coming both from the external environment in which they operate and within themselves, which can facilitate the transition from financial sustainability to ESG sustainability.

The contributions reported in this section have analyzed the ESG challenge for banks, favouring as a point of view the impacts of ESG factors on the economic-financial profile of banks.

Within this analytical perspective we find Batae (2021) which takes into consideration a sub-sample of 38 banks (initially the banks considered were 104) operating in Europe in the period immediately following the international financial crisis of 2008. In his study, based on the Thomson Reuters Refnitiv database) financial performance is measured using some profitability indicators (Return on assets, Return on equity, Stock market returns, Tobin’s q) while ESG issues are monitored using ten pillars (resource use efficiency; emission and waste reduction; workforce rights; Among the interesting results emerges a greater impact of the variables relating to the Governance pillar on financial performance compared to the other two pillars. With reference to the governance pillar, there are three governance-related variables that impact financial performance. In particular, a first result is a negative correlation between the variable relating to the bank’s ability to include social and environmental aspects in its decision-making process and stock market returns. A second result is a negative correlation between the variable measuring the quality of corporate governance and stock market returns. A third result is a negative correlation between the variable that captures the commitment and effectiveness of the banking intermediary in ensuring compliance with corporate governance principles and the return on assets. These results point in the direction that the presence of more powerful governance does not seem to produce improvements in terms of profitability. With reference to the social pillar, a negative correlation emerges between a single social variable represented by the ability of banks to offer high quality products and services to customers (and the related rate of change) and the Return on equity.

The weak impact of social factors on the financial performance of banks can be motivated in light of the little weight that the main stakeholders of banks attribute to the intermediary’s ability to create a solid and peaceful working environment with its employees, to attention towards human rights or the involvement of citizens in its modus operandi. Therefore, in light of these reasons, corporate social responsibility is not considered a strategic lever for the creation of value in the credit market. With reference to the environmental pillar, the existence of a positive correlation emerges between a single variable represented by the reduction of carbon dioxide emissions and waste production in carrying out its operational activities and the return on assets. The importance of aspects relating to the social pillar is instead highlighted by Houston and Shan (2022) who delve into the interaction between corporate ESG profiles and banking relationships. Their research indicates that banks with strong ESG profiles tend to have better relationships with their stakeholders, which in turn improves their financial performance. This study highlights the strategic advantage that banks gain by integrating ESG factors into their core operations and relationship management. La Torre et al. (2021), always taking the European territory as the territorial scope, propose empirical work on a larger sample than the previous one, made up of 44 banks and which are listed on the STOXX Europe 600 market. In particular, the objective of this work is to propose a reflection on what the market can stimulate the adoption of sustainable behavior from an ESG perspective by bank management. In addition to the sample size and the exclusion of unlisted European banks, another important difference compared to previous work is the reference period investigated.

In this case; in fact, the effects of the international financial crisis are also considered given that the period is 2008-2019. Regarding the metrics used to monitor financial performance, a value-based metric, namely the EVA spread, is added to those used in the previous work which are predominantly market-based and account-based in nature. Substantially, the authors estimate five models that differ depending on the dependent variable considered (the EVA spread in model 1, Tobin’s q in models 2 and 3, the Return on Asset and the Return on equity in models 4 and 5). The independent variables are: the ESGP i.e., the score calculated by Thomson Reuters (which can take values in the range 0-100 and which measures the level of transparency of a company), the TIER 1 Ratio (TIR) i.e., a capital buffer at disposition of the banks to manage unexpected losses, Net revenues from interest rates compared to the intermediation margin (expression of the degree of diversification of the banking business model), Loans to deposit (LTD) as a proxy of banks’ liquidity. In all five estimated models, the size of the bank expressed by the logarithm of total assets and the growth rate of Gross Domestic Product were used as control variables. A first result found is the existence of a positive and statistically significant correlation between the voluntary inclusion of ESG (dependent variable) aspects in its modus operandi by bank management and value-based metrics (VBM) while no relationship links the dependent variable with account-based metrics. Surprisingly, the study found a negative and very weak relationship with both dependent variables chosen to express a bank’s market performance and ESGP.

These results therefore appear not to incentivize, in terms of profitability, banks to direct banking management towards the inclusion of ESG factors, at least in a short-term management perspective. This explains why banking authorities focus on ESG risks rather than opportunities. The banking authorities will therefore have to take action to provide stimuli for changing banking business models in a long-term management perspective aimed at encouraging the pursuit of sustainable growth objectives. In this way, banks would be able to embrace the ESG philosophy comprehensively and not just for marketing strategies aimed at reducing the risk of green-washing in the short term. DASZYŃSKA-ŻYGADŁO et al. (2021), take into consideration, unlike previous works, a sample of banks geographically not only in Europe but also in America, the Middle East, Africa and Asia Pacific. The period investigated is also the post-crisis period (2009-2016). The authors intend to demonstrate empirically that the ability of banks to create value is strongly influenced by the availability of a portfolio of activities aimed at highly performing companies from a social point of view. In particular, within the credit sector, they take into consideration banking services and investment banking services and investment services. In this way the authors try to estimate the intensity of the relationship between the social performance and the financial performance of companies. Also in this case the database used is Refinitiv by Thomson Reuters.

With reference to the dependent variable, the financial performance metric based on the market is also in this case Tobin’s Q while the financial performance using metrics based on accounting data is expressed by the Return on asset. The two types of metrics are complementary since the former reflect the banks’ ability to create added value in a long-term perspective while the latter allow monitoring the short-term effects (maximum of one year) of the social performance of companies on the financial sector. The independent variables are ESG from the Refinitiv database and some control variables that served as proxies for bank size and sales growth (such as the logarithm of market capitalization and one-year revenue growth). In addition to these control variables in the model where accounting performance is considered, the lag of the dependent variable was also considered as an independent variable since the accounting profitability of the previous period influences the profitability of the current one. the results highlight the existence of a positive correlation between environmental and social factors that have a negative impact on the performance of banks, whereas factors relating to the governance pillar do not. Considering banking services, social factors reduce the performance of investment banks (measured by Tobin’s q) and have no impact on the Return on assets. Considering the investment banking sector, social factors reduce the return on assets and do not produce any long-term impact. Furthermore, the relationship between the social performance of banks and financial performance takes on different connotations depending on the type of banking operation and the way of conceiving the role of the bank in the territory.

This explains the greater attention of investors to acquiring stakes in the most sustainable banks in terms of ESG and also the banks’ commitment to achieving higher income results thanks to social initiatives. Similar to the findings of Batae (2021), the authors find that it is the governance pillar that produces the greatest impacts on the performance of banks in both types of services offered (banking and investment banking). Gangi et al. (2019) propose an empirical analysis on the impacts of banking corporate social responsibility on financial performance. The ESG metrics are those provided by the data provider Thomson Reuters. In particular, taking into consideration a sample of 142 banks located in 35 countries in the post-financial crisis period (2011-2015), they try to identify, as a first step, which factors most consistently stimulate banks’ commitment to assuming an identity of an environmentally friendly bank and as a second step they investigate the relationship between a bank’s environmental commitment and its risk. With reference to the first reflection, significant factors are those inherent to the composition of the board of directors and its functioning. The authors demonstrate that the specific characteristics of banks and governance allow effective monitoring of banking risk and consequently its reduction. Esteban-Sanchez et al. (2017) analyze how four variables relating to the social and governance pillars (corporate governance, employee relations, relationship with the company, responsibility for the product offered) impact financial performance. The dependent variable relating to performance is expressed by accounting indicators of return on assets and return on equity.

The variables relating to governance relate to the quality of the board and its structure, remuneration policies adopted, integration of strategies that focus on the principles of corporate social responsibility, protection of shareholder rights. The variables relating to social aspects are employee skills, well-being and safety at work, respect for diversity and guarantees of equal professional opportunities. The variables relating to relations with the community are corporate philanthropy, business ethics, respect for human rights. The variables relating to product liability are the quality and safety of the product or services, information transparency. Their survey sample consists of 154 banks operating in 22 countries. The period investigated takes into account the effects of the financial crisis on the credit sector (2005-2010); in fact, they are considered the countries most affected by this exogenous economic-financial shock. The findings suggest that banks did not derive economic benefits from their social responsibility performance across all dimensions. The presence of good governance and the establishment of good relationships with employees have a clear positive effect on company financial results. This result means that relationships with shareholders and employees can constitute fundamental strategic levers for improving the performance of the banking sector. An interesting result is that the financial crisis has significantly reduced the impact of governance on the financial performance of banks, highlighting that the Board of Directors has probably not fulfilled its risk control and risk assessment function in the best possible way. This may be due to a lack of incomplete and adequate information or a partial vision of corporate governance. Furthermore, the insignificant impact of product responsibility on financial performance which highlights a lack of commitment by banks on product/service construction policies, may have caused a weakening of relationships with customers who are increasingly dissatisfied with the banking offer. Nizam et al. (2019) seek to identify and understand the impact of banks’ social and environmental performance on their financial performance. The database used is MSCI ESG Research which contains information on the total social and environmental sustainability of over 11,306 companies from various sectors.

The authors exclusively selected banking companies as the first step, reducing the dataset to 2891 institutions from over 99 countries. They then further reduced the sample to 713 institutions operating in 99 countries by considering those banks for which they were available for both social and environmental issues. The dependent variable is monitored using accounting indicators (return on equity) as sustainability performance issues are generally evaluated by shareholders and investors. The explanatory variables are access to financing, especially for the financially weakest people and SMEs (providing a measure of the social role of banks) and the environmental impact generated by banks when they grant liquidity advances and carry out effective due diligence on green initiatives. In addition to these variables, the level of capitalization of the banks (which denotes their ability to manage any shocks on their balance sheets), the quality of the assets, the liquidity (includes sources of financing and maturity misalignments), the management efficiency and the type of business model (depending on whether the primary source of profitability is the interest margin or the intermediation margin), the size of the bank, the growth of loans and deposits, intangible assets (which measure the effect of corporate social responsibility on brand equity). The rate of change in gross domestic product, the inflation rate and the degree of concentration of the banking sector were inserted as control variables. As a first result, the return on equity improves if banks allow better access to financing. Similar results if banks grant greater financial support to green initiatives. This means that the bank’s financial performance will improve if the bank focuses on improving access to financing practices. Likewise, if banks were to expand their financing for green projects with low environmental impact. Furthermore, significant differences emerge regarding the positive impact of access to financing on the performance of banks linked to the different banking size.

This impact is stronger for smaller banks (i.e., banks with total assets below the $2.07 threshold). Andrieș and Sprincean (2023), Agnese and Giacomini (2023) and Shin (2021) also insist on the impacts of ESG factors on the costs of loans disbursed. The first authors explore the relationship between ESG performance and banks’ funding costs. They find that higher ESG performance is associated with reduced financing costs for banks, indicating that investors and creditors increasingly value ESG credentials. This suggests that banks with better ESG practices can access capital at lower costs, providing a financial incentive for banks to improve their ESG performance. The second authors find that banks with higher ESG ratings tend to benefit from lower financing costs. This correlation is attributed to the increased trust and reduced risk perceived by investors and creditors in banks that prioritize sustainable and responsible practices. The findings suggest that integrating ESG considerations into banking operations can lead to significant financial benefits by reducing the cost of capital. Shin (2021) reveals that banks that lend to companies with a high ESG profile tend to incur lower borrowing costs. This cost reduction is attributed to the lower risk associated with companies that adhere to strong ESG practices, which can lead to more favorable lending conditions and reduced default rates. The study suggests that aligning bank loan portfolios with ESG principles can be financially beneficial for both banks and their customers. Shen et al. (2016) intend to verify whether or not banks that adopt practices focused on corporate social responsibility manage to generate greater profits and improve the quality of their loans on their balance sheets. The survey sample is made up of banks that apply the principles of corporate social responsibility in 18 countries identified by the FTSE4Good index constructed by FTSEGOOD Group in July 2001.

The authors, using a score matching model, construct a dependent variable that takes the form of a one-dimensional probability. The value of these probabilities is conditioned by a benchmark vector of five explanatory variables characteristic of the banking business (total assets, total deposits, total credits, financial leverage, the lag of the return on assets) of each bank from 2000 to 2009. Therefore in this case is considered the impact of the global financial crisis. Their conclusion is that the best performing banks in terms of corporate social responsibility obtain better results in terms of profitability on their investments and equity capital. Placing the principles of corporate social responsibility at the center of one’s strategies constitutes a fundamental condition for guaranteeing the bank’s survival in a long-term perspective. Shakil et al. (2019) consider the ESG performance of 93 banks in emerging markets from 2015 to 2018, using two databases. For ESG metrics the data is extrapolated from Refinitiv’s ESG Asset4 database while for accounting and financial data the Refinitiv Datastream Database is used. Performance is understood in this case as both operational and financial. For operational performance, return on assets is used, while for financial performance, return on equity is used. Bank size, financial leverage and dividend yield are used as control variables. Their conclusion is that banks that are more committed to environmental and social performance achieve better financial results. Gutiérrez-Ponce and Wibowo (2024) also arrive at similar results when analyzing the contribution of sustainability practices to the financial performance of banks in South-East Asia. Unlike previous works, in this study the variables relating to the governance pillar do not significantly affect the financial performance of banks. The low impact of governance, according to the authors, may be attributable to the weak corporate governance practices of emerging market banks and the lack of regulatory pressure from regulatory bodies such as the Securities Commission and other environmental and social agencies.

Again with reference to developing economies, other studies (Azmi et al. 2021, Arun et al. 2022) highlight the potential of ESG activities in contributing to financial stability and growth in developing markets, where conditions economic and regulatory policies can differ significantly from those of more developed regions. Unlike previous contributions that look exclusively at the impacts of ESG factors on bank performance measured by accounting metrics, Toth et al. (2021) focus on the contribution of ESG information to the stability of European banks in their target markets. These authors argue that ESG disclosures improve transparency, leading to greater stability and resilience in the banking sector. This study highlights the positive impact of sound ESG practices on financial stability, underlining the importance of comprehensive ESG reporting in European banks. Similarly Chiaramonte et al. (2022) investigate whether ESG strategies improve banking stability during periods of financial turbulence in Europe. Their findings suggest that banks with strong ESG strategies are better equipped to withstand financial instability, thus improving overall stability. Yuen et al. (2022) analyze the impact of ESG activities on profitability in the global banking sector during the COVID-19 pandemic. Their study reveals that banks with strong ESG practices were better able to maintain profitability despite disruptions from the pandemic. This finding highlights the resilience conferred by robust ESG frameworks, suggesting that such practices are vital for addressing crises and ensuring financial stability in adverse conditions.

Citterio and King (2023) examine the role of ESG factors in predicting bank financial distress. They find that banks with higher ESG scores are less likely to experience financial distress. The study highlights the predictive power of ESG parameters in assessing the financial health and resilience of banks, supporting the integration of ESG considerations into financial risk assessments. Lupu et al. (2022) explore how ESG factors are reflected in European financial stability. They find that higher ESG scores contribute positively to the financial stability of European banks. Research indicates that banks with strong ESG commitments are better positioned to manage risks and support long-term financial health, thereby supporting the overall stability of the financial system.

3. Trend in the Bank to Capital Asset Ratio value globally between 2010 and 2022

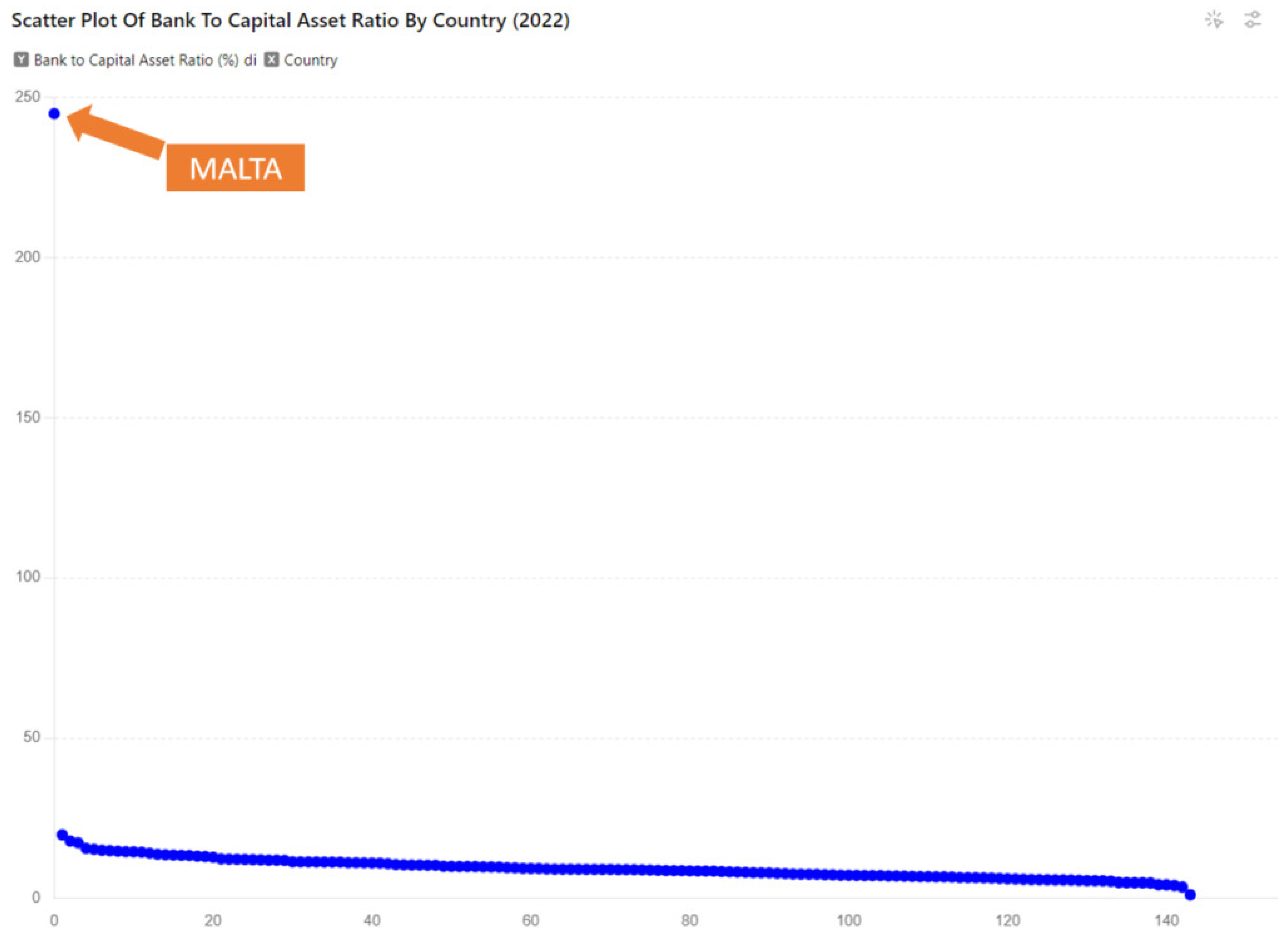

Trend of the bank to capital asset ratio in 2022. The 2022 data on “Bank to Capital Asset %” from the World Bank reveals significant disparities among countries, highlighting the financial stability and risk management strategies of their banking sectors. Malta stands out with an exceptionally high ratio of 244.91%, indicating a robust capital cushion relative to its assets, reflecting a conservative banking approach that enhances resilience against potential financial shocks. In stark contrast, Equatorial Guinea shows a low ratio of 1.15%, suggesting limited capital buffers, which could indicate higher vulnerability in turbulent economic times. Other countries such as Tajikistan (19.77%), Maldives (17.8%), and Tonga (17.27%) demonstrate moderately high ratios, which may point to a balance between risk and stability. Meanwhile, nations like Lithuania (15.5%), Cambodia (14.92%), and Uganda (14.8%) maintain similar levels, suggesting a cautious yet effective capital management. Middle-income countries, including Argentina (14.64%), Rwanda (14.46%), and Saudi Arabia (13.68%), fall within the average range, indicating standard banking practices in line with global norms. Major economies like the United States (8.58%), Germany (5.61%), and France (4.78%) display lower percentages, potentially reflecting larger asset bases and diversified portfolios that mitigate risk through other financial instruments. This data underscores the diverse approaches to banking stability across the globe, shaped by economic, regulatory, and cultural factors. As countries navigate economic challenges, maintaining an optimal balance in their “Bank to Capital Asset %” ratios will be critical in ensuring financial resilience and growth.

Trend of the bank to capital asset ratio between 2010 and 2022. The “Bank to Capital Asset Ratio %” data reveals varied trends across countries. Notably, Malta experienced a dramatic increase of over 4000%, indicating a significant strengthening of its capital reserves, suggesting a conservative approach to financial risk management. Countries like Lesotho and Argentina also saw substantial growth, suggesting improved financial stability and enhanced resilience against economic shocks. Moderate gains in nations such as Uganda, Peru, and Thailand reflect improved risk management practices and a balanced approach to maintaining capital buffers. However, declines in countries like Iceland, Croatia, and Ukraine highlight potential economic challenges and vulnerabilities in their banking sectors. These reductions may signal issues such as economic instability or inadequate capital management strategies. In contrast, countries like the Maldives and Samoa remained stable, showing minimal changes, which could indicate steady economic conditions and effective capital management practices. Conversely, Lithuania and Equatorial Guinea faced notable reductions in their ratios, raising concerns about their financial resilience and ability to withstand potential economic downturns. These decreases may reflect increased financial risks or deteriorating economic conditions. Overall, while many countries have improved their capital positions, enhancing their financial stability, others continue to face significant challenges that may impact their long-term economic health. This data underscores the importance of robust capital management in ensuring the stability and resilience of banking systems worldwide.

Countries for which banking stability increased between 2010 and 2022. The “Bank to Capital Asset Ratio %” serves as a critical indicator of financial stability and resilience in the banking sectors of various countries. It measures the proportion of a bank’s capital to its assets, reflecting its ability to absorb losses and manage financial risks. An increase in this ratio typically indicates stronger capital reserves and improved financial health.

Malta experienced an extraordinary increase from 5.80% in 2010 to 244.91% in 2022, marking an absolute variation of 239.11% and a staggering percentage increase of 4122.59%. This dramatic rise suggests a strategic shift towards conservative banking practices, enhancing the country’s financial resilience against potential shocks. The substantial increase in capital reserves points to a robust regulatory framework and prudent risk management. Nigeria also saw a significant increase in its ratio, rising from 1.49% to 5.69%. Although the absolute variation is only 4.20%, the percentage change of 281.88% indicates considerable strengthening of its banking sector. This increase could be attributed to improved regulatory oversight and efforts to bolster financial stability. Lesotho experienced a notable rise from 5.20% to 12.14%, reflecting an absolute increase of 6.94% and a percentage increase of 133.46%. This suggests enhanced risk management and increased capital buffers, indicating a move towards greater financial stability. Argentina and Bhutan also reported substantial growth in their ratios, with increases of 102.21% and 88.26% respectively. Argentina’s increase from 7.24% to 14.64% highlights a more than doubling of its capital reserves, which is crucial for a country often facing economic volatility. Bhutan’s rise from 8.09% to 15.23% indicates a similar trend towards improving financial health. Countries like Uganda, Peru, and Tajikistan showed moderate but significant increases in their ratios. Uganda’s increase from 11.26% to 14.80% (31.44%) reflects improved capital management, possibly due to regulatory enhancements. Peru and Tajikistan’s increases of 33.42% and 31.10%, respectively, signify better risk management practices and increased resilience in their banking sectors. Mauritius, Indonesia, and Luxembourg also demonstrated noteworthy improvements. The rise in Mauritius from 5.51% to 9.00% (63.34%) and in Indonesia from 8.19% to 13.29% (62.27%) reflects strengthened financial stability. Luxembourg’s increase of 55.45% indicates a focus on bolstering capital reserves in a well-developed banking environment. Cameroon and Paraguay both showed substantial growth, with percentage increases of 54.61% and 53.97%, respectively. Their improved ratios reflect efforts to enhance banking sector stability through increased capital reserves. The United Kingdom and Netherlands also recorded significant gains, with increases of 44.07% and 35.59%. These improvements suggest enhanced risk management strategies and an emphasis on financial stability, which are critical for these major economies. Several countries, including Portugal (29.57%), Australia (26.84%), and France (22.88%), showed moderate gains. These improvements indicate a stable approach to risk management and capital adequacy in the face of global economic uncertainties. Germany, Greece, and Switzerland also saw increases of around 30%, demonstrating efforts to strengthen their banking sectors amidst ongoing economic challenges in Europe. Countries like Dominica (3.70%), China (3.32%), and Israel (3.28%) experienced minimal increases in their ratios. While these increases suggest some improvements, they may reflect a stable banking environment with minimal changes needed in capital reserves. Lebanon and Bangladesh showed almost no change, indicating a steady banking sector with existing capital levels deemed adequate. Hong Kong SAR, China and Sri Lanka recorded no change in their ratios over the period, reflecting stability in their banking sectors. This could indicate a well-managed capital position that meets regulatory requirements without the need for significant adjustments (Figure 1).

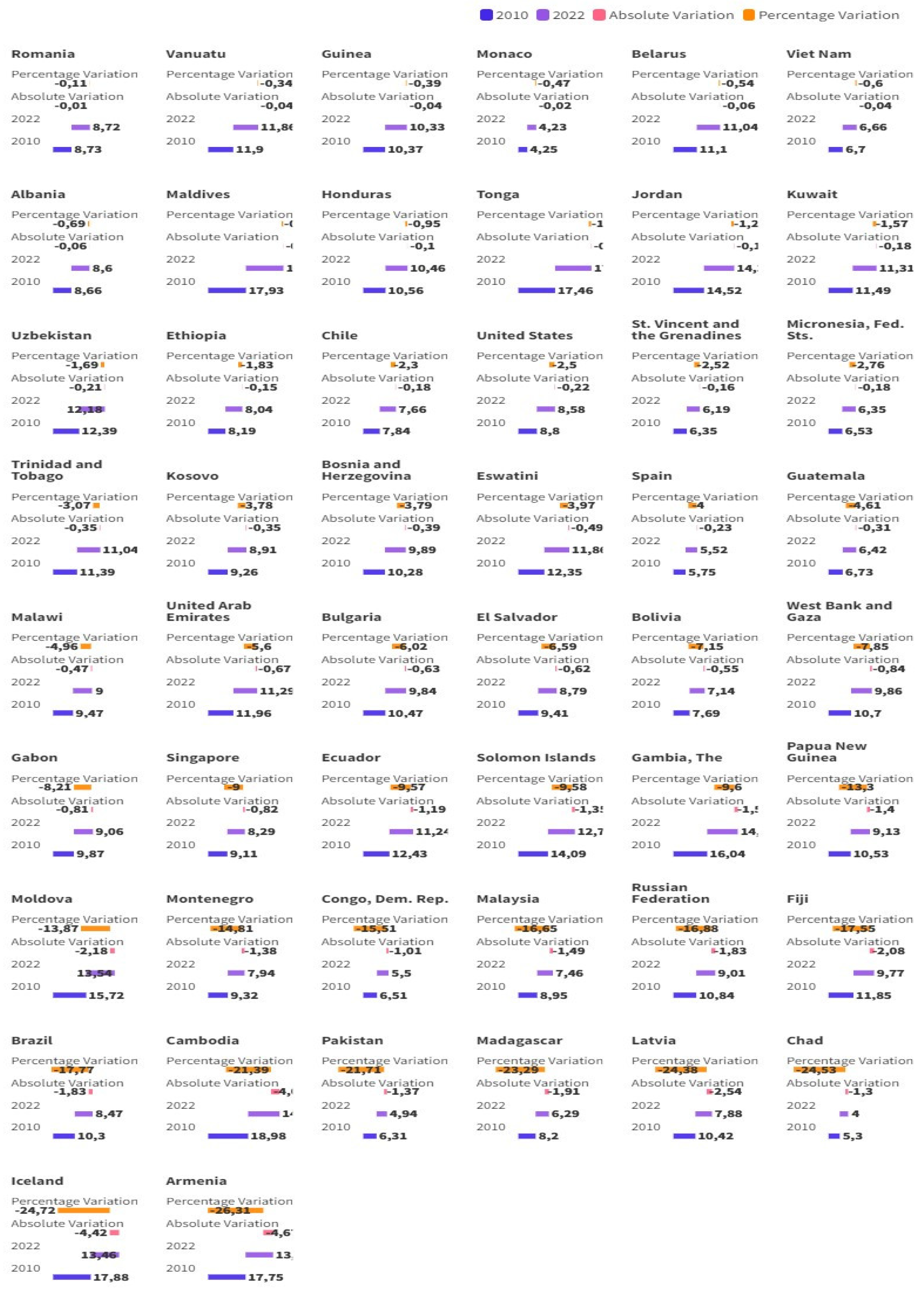

Countries for which banking stability decreased between 2010 and 2022. Countries like Romania, Vanuatu, and Guinea experienced minor decreases in their bank to capital asset ratios, indicating stable banking environments with slight adjustments in capital reserves. These minimal changes, ranging from -0.11% to -0.39%, suggest that these countries have maintained a consistent approach to financial risk management, reflecting resilience in their banking sectors. In contrast, countries such as Albania, Maldives, and Honduras faced moderate declines in their ratios, around -0.7% to -1.1%. These reductions may indicate slight shifts in financial strategies or adjustments in asset composition. Despite these decreases, overall stability remains intact, suggesting that these banking sectors are adapting to evolving economic conditions without major disruptions. Countries like Kuwait, Uzbekistan, and Ethiopia experienced more notable reductions, with declines of -1.5% to -1.8%. This indicates potential challenges in maintaining adequate capital buffers, possibly due to economic fluctuations, increased lending activities, or regulatory changes. These declines may require more focused strategies to ensure sufficient capital reserves in the face of potential risks. Several countries, such as the United States and Spain, saw significant decreases in their ratios, ranging from -2.5% to -4%. These reductions likely reflect increased economic pressures or shifts in banking regulations, necessitating more strategic management of capital reserves. The need to balance risk and capital adequacy in these economies highlights the importance of adaptive financial policies. Nations like Brazil, Russia, and Malaysia faced major declines of around -16% to -17%, suggesting considerable economic challenges or changes in regulatory environments that impacted their banking sectors’ capital adequacy. These substantial decreases may indicate increased vulnerability to external economic shocks or shifts in market conditions. Countries like Turkey, Ghana, and Ukraine experienced severe declines, with reductions exceeding -30%. These sharp drops highlight significant financial instability or economic crises, necessitating substantial changes in capital management strategies. Such drastic measures indicate the profound impact of economic turmoil on these banking sectors. Croatia and Lithuania faced extreme declines of over -50%, while Equatorial Guinea saw a staggering -86.06% drop. These drastic reductions indicate severe economic or financial challenges, reflecting profound vulnerabilities in their banking sectors. The significant decrease in capital ratios in these countries underscores the need for comprehensive reforms and strengthened financial oversight to address underlying economic issues and bolster banking sector resilience. Figure 2

4. Clusterization with k-Means Algorithm: Silhouette Coefficient Vs Elbow Method

Below we present a clustering with the k-Means algorithm to identify groupings between the countries considered in terms of bank capital to asset ratio. The k-Means algorithm is an unsupervised clustering method that partitions data into k clusters. It works iteratively by minimizing the variance within each cluster. The process involves assigning data points to the nearest centroids and updating the centroids based on the mean of the assigned points. k-Means is simple and efficient but sensitive to the initial choice of k and the initial centroid positions. It’s particularly effective for well-separated data but less suitable for clusters with complex shapes.

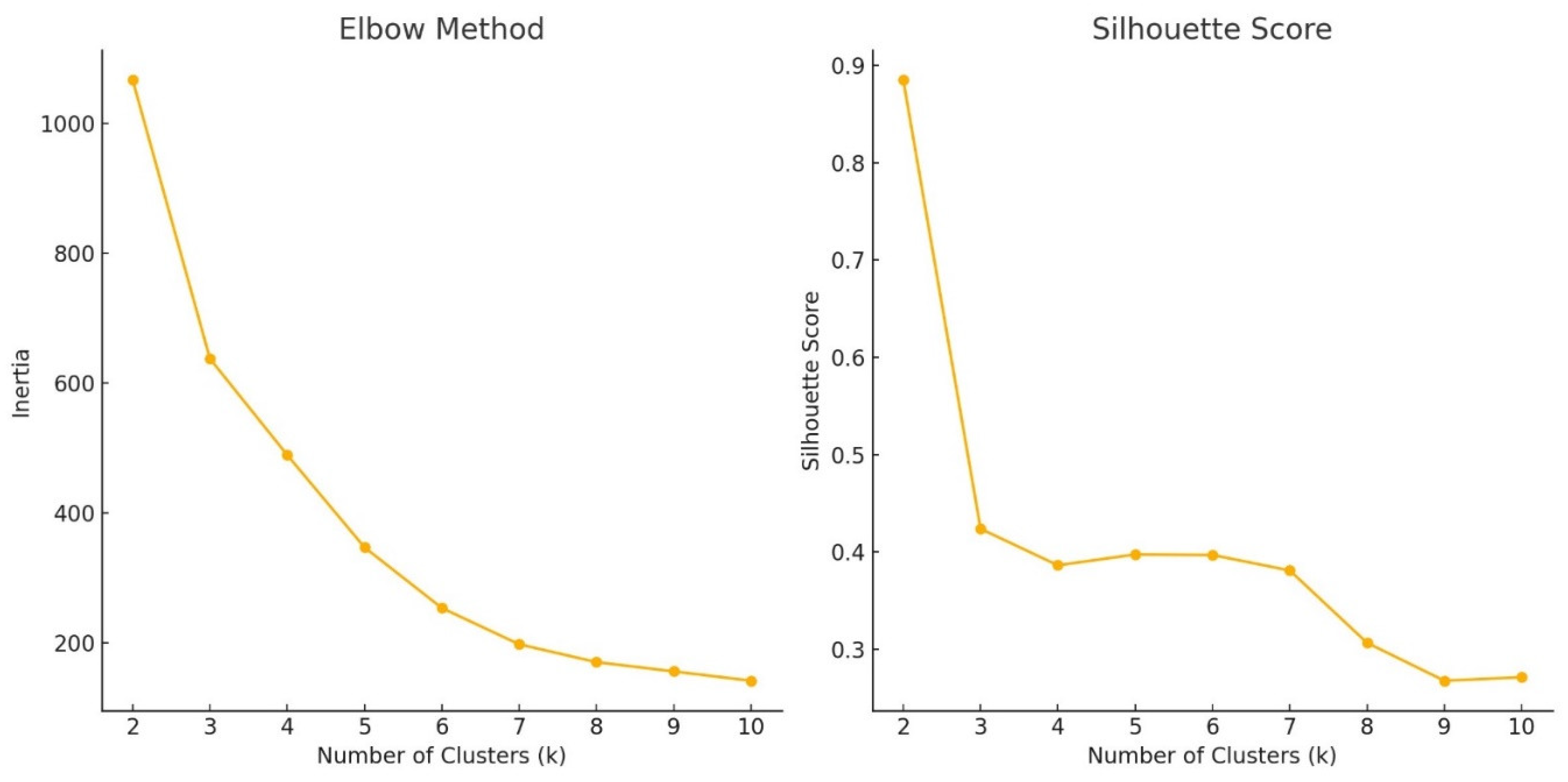

Utilizing multiple methods, such as the Elbow Method and the Silhouette Coefficient, is essential for optimizing k-Means clustering because each method offers unique insights into the data’s structure. The Elbow Method helps determine the optimal number of clusters by plotting the explained variance as a function of the number of clusters. It identifies the point where adding more clusters results in marginal gains, providing a clear visual cue, but it can sometimes be subjective, as the “elbow” may not be well-defined. On the other hand, the Silhouette Coefficient evaluates the quality of clustering by measuring how similar an object is to its own cluster compared to other clusters. This metric provides a more quantitative assessment of how well the data points are clustered, taking into account both cohesion and separation. A higher silhouette score indicates well-separated and well-formed clusters. By combining these two methods, analysts can cross-validate their results, ensuring that the chosen number of clusters is both theoretically justified and practically effective. This multi-method approach enhances the robustness of the clustering solution, allowing for more reliable interpretations and more actionable insights from the data. It ensures that the clusters identified are not only statistically valid but also meaningful in the context of the specific analysis, leading to better decision-making and strategic planning. Below we present the results of the clustering with the k-Means algorithm both with the Elbow method and with the Silhouette coefficient (Figure 3).

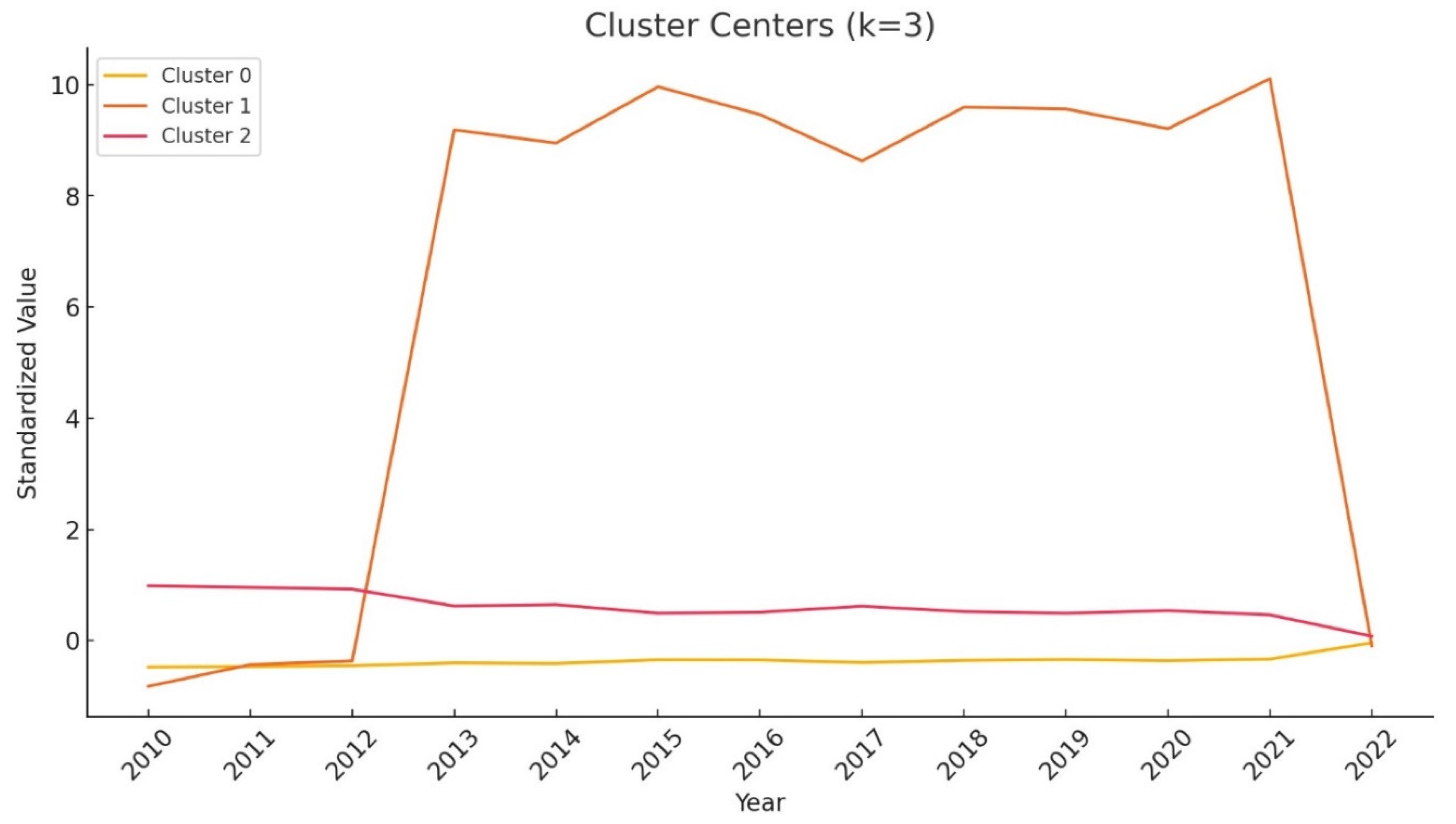

However, we must consider that the Elbow method suggests an optimal number of clusters in relation to k=3, while the Silhouette coefficient suggests a value of k=2. Since the overall sample is made up of 144 countries, it follows that a clustering carried out with a value of k=2 could be largely insufficient in its ability to identify the presence of groupings between the countries considered in terms of bank capital to asset ratio. For this reason, being able to choose one of the two methods, we prefer to choose the Elbow method as with a k=3 we believe we can capture a greater complexity of groupings present within the analyzed data. To verify the hierarchy of the three identified clusters, i.e., which of the three clusters presents the highest level of centroids during the period considered, we analyze Figure 4. The results show that cluster 1 tends to have a dominance in terms of value of bank capital to asset ratio higher than the other two clusters.

The composition of the three clusters is analyzed as follows:

- Cluster 0: Comprises countries with lower, stable values over time. These countries show moderate growth without significant spikes. Countries are: Malta, Argentina, Lesotho, Barbados, Colombia, Thailand, Peru, Mexico, Brunei Darussalam, Costa Rica, Slovenia, Gabon, Mauritius, Malawi, Botswana, Kosovo, El Salvador, Albania, United States, Brazil, Hungary, Luxembourg, Montenegro, Nicaragua, Latvia, Malaysia, Nepal, Slovak Republic, Greece, Cyprus, Czechia, Cameroon, Sweden, United Kingdom, Guatemala, Madagascar, Netherlands, Australia, Ukraine, Finland, Nigeria, Spain, Congo, Pakistan, Denmark, Canada, Chad , Macao SAR, Equatorial Guinea, Afghanistan, Angola, Antigua and Barbuda, Austria, Belgium, Bangladesh, Bolivia, Switzerland, Chile, China, Congo, Germany, Djibouti, Dominica, Dominican Republic, Algeria, Ethiopia, Fiji, France, Micronesia Fed Sts, Grenada, Hong Kong SAR, India, Ireland, Israel, Italy, Korea Rep, Lebanon, St. Lucia, Sri Lanka, Monaco, Mozambique, Namibia, Philippines, Poland, Portugal, West Bank and Gaza, Romania, Russian Federation, Singapore, San Marino, Seychelles, Uruguay, St. Vincent and the Grenadines, Vietnam, South Africa. This cluster comprises countries like Malta, Argentina, and the United States. These nations generally exhibit a stable bank to capital asset ratio, indicating solid financial health and resilience. The ratio suggests that banks in these countries maintain a balanced approach to capital management, ensuring stability even in fluctuating economic conditions. This stability is crucial for attracting investments and supporting economic growth. Countries in Cluster 0 exhibit economic stability through consistent and moderate growth in their bank to capital asset ratios. This stability is attributed to robust financial systems, which prioritize effective risk management and regulatory compliance. These nations often benefit from diverse economies, reducing dependency on any single sector and mitigating potential risks. Sound governance and strong regulatory frameworks further support financial health, fostering investor confidence. Additionally, moderate leverage within the banking sector allows these countries to withstand economic fluctuations without significant distress. Prudent fiscal and monetary policies enhance resilience, balancing growth with financial security. Overall, Cluster 0’s combination of sound financial management, diverse economic structures, and effective governance contributes to their sustained economic stability, making them attractive environments for investment and development. Countries in Cluster 0 demonstrate significant economic stability, driven by several key factors. First, these nations typically have well-established financial systems with stringent regulatory frameworks that ensure effective risk management and compliance. This helps maintain a healthy balance between assets and liabilities in their banking sectors. Additionally, the diversity of their economies reduces reliance on any single industry, thereby mitigating risks associated with economic downturns in specific sectors. The presence of sound governance further enhances stability, promoting investor confidence through transparency and accountability. Moderate leverage within the banking systems allows these countries to withstand external economic shocks, ensuring resilience during periods of global financial uncertainty. Lastly, prudent fiscal and monetary policies support sustainable economic growth, balancing the need for expansion with the importance of financial security. Together, these factors make Cluster 0 countries attractive for investment and development, as they provide a stable and secure environment conducive to long-term economic growth.

- Cluster 1: has intermediate values, showing slight growth or variations over time. The trend is upward but without extreme fluctuations. The only country in this cluster is Paraguay. This cluster has higher bank to capital asset ratios, which may indicate a more aggressive capital structure or a response to higher perceived risks. Such ratios reflect a focus on leveraging assets for growth, although this can lead to increased vulnerability during economic downturns. Paraguay needs to balance growth aspirations with prudent risk management. This country face moderate economic risks characterized by intermediate bank to capital asset ratios. Paraguay often strive for growth, resulting in higher leverage and potential exposure to financial instability. The focus on leveraging assets can lead to increased vulnerability during economic downturns, as higher debt levels may strain financial systems. Additionally, Paraguay may experience fluctuating market conditions due to reliance on specific industries, which can impact economic resilience. While they benefit from gradual growth, the balance between expansion and risk management remains crucial. Effective regulatory frameworks and diversified economic policies are essential to mitigate potential risks, ensuring sustainable development while safeguarding financial stability.

- Cluster 2: Contains countries with higher or more unstable values, characterized by significant variations across the years. These countries exhibit a more pronounced growth trend or considerable fluctuations. Maldives, Cambodia, Uganda, Central African Republic, Saudi Arabia, Moldova, Iceland, Indonesia, Georgia, Samoa, Uzbekistan, Kenya, Panama, Kyrgyz Republic, United Arab Emirates, North Macedonia, Ecuador, Croatia, Bosnia and Herzegovina, Bulgaria, Estonia, Papua New Guinea, Belize, Turkey, Ghana, Armenia, Burundi, Belarus, Bhutan, Comoros, Guinea, Gambia, The, Honduras, Iraq, Jordan, Kazakhstan, Kuwait, Lithuania, Rwanda, Solomon Islands, Eswatini, Tajikistan, Tonga, Trinidad and Tobago, Tanzania, Vanuatu, Zambia. They show varying bank to capital asset ratios, often reflecting dynamic economic environments. High ratios may indicate rapid economic growth or higher financial risk exposure, while lower ratios suggest more stability. These countries must navigate potential volatility carefully, ensuring that their banking sectors remain robust and adaptable to changing conditions. Countries in Cluster 2 exhibit notable economic volatility, characterized by fluctuating bank to capital asset ratios. These nations often experience rapid growth periods, driven by aggressive investment and development strategies. However, this growth can be accompanied by increased financial risk, as higher leverage ratios may expose them to instability during economic downturns. The economies in this cluster often rely on specific industries or resources, making them susceptible to market fluctuations and global economic conditions. While the potential for high returns exists, these countries must navigate the challenges of maintaining stability amidst dynamic changes. Effective governance and diversified economic policies are crucial in mitigating risks, ensuring that growth is sustainable and resilient in the face of economic shocks. Overall, Cluster 2 reflects a balance of opportunities and risks, requiring strategic management to foster long-term development. Countries in Cluster 2 often experience significant impacts on growth due to their high volatility and fluctuating bank to capital asset ratios. These nations pursue aggressive growth strategies, leveraging assets to stimulate rapid economic expansion. However, this approach can lead to increased financial risk and susceptibility to market fluctuations. While the potential for high returns exists, these economies may face instability during downturns, affecting long-term growth prospects. The reliance on specific industries or resources further amplifies this risk, making diversification crucial. Despite the challenges, effective governance and strategic economic policies can mitigate these risks, promoting sustainable growth and resilience. Overall, Cluster 2 countries embody a balance of high growth potential and inherent economic risks, requiring careful management to harness opportunities while maintaining stability.

The cluster analysis highlights the diversity in banking and capital asset management across countries. Cluster 0 emphasizes stability and resilience, Cluster 1 focuses on growth with higher leverage, and Cluster 2 showcases a mix of high growth potential and associated risks. This understanding helps tailor financial policies and strategies to foster sustainable economic development while managing financial risks effectively. Each cluster represents distinct economic characteristics and growth patterns. Cluster 0 comprises countries with stable, moderate growth, supported by strong financial systems and effective governance. These nations maintain balance in their bank to capital asset ratios, ensuring resilience during economic fluctuations. Cluster 1 includes countries with intermediate values and a focus on growth, often leveraging assets for expansion. While they show potential for development, they also face risks from higher debt levels and economic vulnerability. Cluster 2, on the other hand, consists of countries with higher volatility and rapid growth, driven by aggressive investment strategies. These nations experience significant fluctuations, making them susceptible to market instability. Overall, the clusters illustrate a spectrum of economic stability and growth potential, with Cluster 0 prioritizing resilience, Cluster 1 balancing growth and risk, and Cluster 2 showcasing high growth potential amid greater economic uncertainty. Effective management and policy frameworks are crucial across all clusters to ensure sustainable development.

5. Policy Implications

The integration of Environmental, Social, and Governance (ESG) factors into banking practices carries significant policy implications that are essential for fostering global financial stability. As the world increasingly recognizes the interconnectedness of financial systems and sustainability, policymakers must develop robust regulatory frameworks that mandate the incorporation of ESG considerations into banks’ risk assessment and management processes. By systematically addressing potential environmental and social risks, such frameworks can mitigate vulnerabilities within the banking sector, ensuring resilience in the face of global challenges. To encourage the adoption of ESG principles, governments can implement incentives such as tax benefits or reduced borrowing costs for banks that actively engage in sustainable practices. These financial incentives align the banks’ profitability goals with broader societal and environmental objectives, reinforcing the idea that sustainable finance is not only beneficial for the planet but also advantageous for long-term financial health. This alignment creates a positive feedback loop, where financial stability and sustainability mutually reinforce each other. Mandatory ESG reporting standards are crucial for enhancing transparency within the banking sector. By requiring detailed disclosures on ESG-related activities and risks, stakeholders, including investors and customers, can more accurately evaluate a bank’s commitment to sustainable practices. This transparency fosters greater accountability, building trust among stakeholders and promoting informed decision-making. Furthermore, standardized reporting can help create a consistent benchmark for assessing ESG performance, driving competition among banks to improve their sustainability credentials. Capacity-building initiatives play a vital role in supporting banks’ efforts to integrate ESG factors effectively. Extensive training programs for bank staff on ESG issues equip employees with the necessary skills and knowledge to identify and mitigate ESG-related risks. These programs enhance the overall risk management capabilities of financial institutions, ensuring that they are well-prepared to address emerging challenges in a rapidly evolving landscape. By investing in human capital, banks can foster a culture of sustainability that permeates all levels of their operations. Public-private partnerships are another critical element in advancing the integration of ESG factors in banking. By collaborating with governments, banks can leverage resources and expertise to finance sustainable projects that balance profitability with positive social and environmental impact. Such partnerships can drive significant progress in areas such as renewable energy, infrastructure development, and community initiatives, contributing to broader societal goals while ensuring financial returns. Global cooperation is imperative for the success of these initiatives. Cross-border regulatory alignment on ESG criteria ensures that sustainability efforts are consistent and effective worldwide. A coordinated approach to ESG integration creates a level playing field for banks operating in different regions, reducing the risk of regulatory arbitrage and enhancing overall banking stability. This global collaboration fosters resilience not only within individual financial institutions but also across the entire financial system, contributing to sustainable economic development on a larger scale. In conclusion, the policy implications of integrating ESG factors into banking are profound and multifaceted. By establishing comprehensive regulatory frameworks, offering financial incentives, enhancing transparency, investing in capacity-building, fostering public-private partnerships, and promoting global cooperation, policymakers can create an environment where banks are better equipped to navigate the complexities of modern finance. This approach not only supports financial stability but also advances broader societal and environmental objectives, paving the way for a more sustainable and resilient future for the global economy (Figure 5).

6. Conclusions

The integration of Environmental, Social, and Governance (ESG) factors into the banking sector has evolved from being a peripheral consideration to becoming a central pillar in financial strategy. This shift reflects a broader recognition that sustainable finance not only contributes to social and environmental well-being but also enhances financial performance and resilience. As banks increasingly adopt ESG principles, they are better positioned to navigate the complexities of modern financial markets, mitigating risks and seizing new opportunities. The banking sector’s transition towards sustainability is driven by the growing awareness that ESG factors are integral to long-term profitability and risk management. Traditionally, banks focused primarily on financial metrics to assess performance. However, this approach often overlooked critical risks associated with environmental degradation, social inequality, and poor governance. By integrating ESG considerations, banks can adopt a more holistic view of risk, encompassing factors that might otherwise lead to financial instability. Research indicates that banks with higher ESG scores tend to experience better financial outcomes. This positive correlation underscores the potential of ESG integration as a driver of growth. For instance, by financing projects that promote renewable energy, resource efficiency, and social development, banks not only enhance their reputational standing but also contribute to the creation of sustainable markets. These investments can lead to increased customer trust and loyalty, fostering long-term relationships that benefit both the banks and their stakeholders.

Despite the clear benefits, the path to full ESG integration is fraught with challenges. One of the most significant obstacles is the lack of clear regulatory frameworks. Banks often face ambiguity regarding the specific requirements for ESG compliance, which can hinder their ability to implement effective strategies. This uncertainty is particularly pronounced in emerging markets, where regulatory bodies may not have established comprehensive guidelines for ESG practices. Moreover, the availability of high-quality, standardized ESG data remains a critical issue. Banks require reliable data to assess the ESG impact of their investments accurately. However, inconsistencies in data collection and reporting methodologies can lead to difficulties in evaluating ESG performance. This lack of transparency can also contribute to skepticism among stakeholders regarding the actual impact of ESG initiatives on financial performance. Another challenge lies in the perception of ESG factors as being secondary to traditional financial considerations. In many cases, banks have been slow to fully integrate ESG into their core risk management frameworks. This reluctance is often rooted in uncertainty about the long-term financial benefits of ESG practices, as well as a focus on short-term profitability. However, this perspective is gradually shifting as more evidence emerges demonstrating the positive impact of ESG factors on financial stability and performance.

Banks play a pivotal role in promoting economic stability through their ESG initiatives. By financing environmentally and socially responsible projects, they contribute to broader efforts to address climate change, social inequality, and governance issues. This not only mitigates risks associated with environmental degradation and social unrest but also fosters a more sustainable economy. For example, banks that prioritize lending to green projects help reduce the carbon footprint of their investment portfolios. This not only aligns with global sustainability goals but also reduces the potential for asset stranding as economies transition to low-carbon models. Additionally, banks that support social initiatives, such as financial inclusion and community development, contribute to social stability by promoting economic equity and reducing poverty. The positive impact of ESG practices on economic stability is particularly evident during periods of crisis. Research has shown that banks with robust ESG frameworks were better equipped to withstand the financial disruptions caused by events such as the COVID-19 pandemic. These banks demonstrated resilience by maintaining profitability and continuing to support their communities, highlighting the importance of ESG considerations in crisis management.

As global regulatory focus on sustainability intensifies, banks must adapt to the evolving landscape by rethinking their traditional risk management models. This requires a shift from viewing ESG factors as merely compliance obligations to recognizing them as integral components of financial strategy. Banks that successfully integrate ESG considerations into their operations will not only enhance their competitive advantage but also contribute to the broader goal of sustainable economic development. To achieve this, banks must adopt innovative strategies that balance profitability with sustainability. This includes developing new financial products and services that cater to the growing demand for sustainable investments. For instance, green bonds and social impact bonds are gaining traction as instruments that finance projects with positive environmental and social outcomes. By offering such products, banks can attract socially conscious investors and expand their customer base. Furthermore, banks need to invest in capacity-building initiatives that enhance their ability to assess and manage ESG risks. This includes training programs for staff, as well as the development of advanced analytical tools that integrate ESG data into risk assessment models. By building internal expertise in ESG, banks can better identify opportunities for sustainable investments and mitigate potential risks. Collaboration among banks, regulators, and other stakeholders is essential for the successful integration of ESG factors into the financial sector. Regulatory bodies play a crucial role in establishing clear guidelines and standards for ESG practices, providing the framework within which banks can operate. By working together, banks and regulators can develop consistent reporting standards that enhance transparency and facilitate the evaluation of ESG performance. Engaging with stakeholders, including investors, customers, and civil society, is also critical. By communicating their ESG strategies and achievements, banks can build trust and demonstrate their commitment to sustainable finance. This engagement fosters a culture of accountability and encourages banks to continuously improve their ESG practices.

In conclusion, the integration of ESG factors into the banking sector is not just a trend but a necessary evolution in response to the challenges and opportunities of the modern financial landscape. Banks that embrace ESG considerations as core components of their strategy are better equipped to navigate risks, enhance their financial performance, and contribute to sustainable economic development. Despite challenges such as regulatory ambiguity and data limitations, the potential benefits of ESG integration far outweigh the obstacles. By adopting innovative strategies, investing in capacity-building, and engaging with stakeholders, banks can position themselves as key drivers of sustainable finance, fostering resilience and stability in an increasingly complex world. As we move forward, it is clear that ESG integration will continue to play a pivotal role in shaping the future of the banking sector. Banks that prioritize sustainability, transparency, and collaboration will not only thrive in the evolving financial landscape but also contribute significantly to building a more sustainable and equitable global economy.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare that there is no conflict of interests regarding the publication of this manuscript. In addition, the ethical issues, including plagiarism, informed consent, misconduct, data fabrication and/or falsification, double publication.

References

- Agnese, P.; Giacomini, E. (2023), Bank’s funding costs: Do ESG factors really matter? Finance Research Letters, 51, 103437.

- Andrieș, A.M.; Sprincean, N. (2023). ESG performance and banks’ funding costs. Finance research letters, 54, 103811.

- Arun, T.; Girardone, C.; Piserà, S. (2022)., ESG issues in emerging markets and the role of banks. Handbook of Banking and Finance in Emerging Markets, 321.

- Azmi, W.; Hassan, M.K.; Houston, R.; Karim, M.S. (2021), ESG activities and banking performance: International evidence from emerging economies. Journal of International Financial Markets, Institutions and Money, 70, 101277.

- Batae, O.M. (2021), The relationship between environmental, social and financial performance in the banking sector A European study”, Journal of Cleaner Production, Volume 290, 25 March 2021, 125791.

- Chiaramonte, L.; Dreassi, A.; Girardone, C.; Piserà, S. (2022). Do ESG strategies enhance bank stability during financial turmoil? Evidence from Europe. The European Journal of Finance, 28(12), 1173-1211.

- Citterio, A.; King, T. (2023), The role of Environmental, Social, and Governance (ESG) in predicting bank financial distress. Finance Research Letters, 51, 103411.

- Daszyńska-Żygadło, K.; Słoński, T.; Dziadkowiec, A. (2021, Corporate Social Performance and Financial Performance Relationship in Banks: Sub-Industry and Cross-Cultural Perspective’, Journal of Business Economics & Management, 22(2), pp.

- Esteban-Sanchez, P.; Gonzalez, M.; Gazquez, J. I: Corporate social performance and its relation with corporate financial performance: International evidence in the banking industry, 2017; 162, 1102–1110.

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. (2019), Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky?, Corporate Social Responsibility and Environmental Management, 2019, vol. 26, issue 3, 529-547.

- Giorgino, M. (2021), ESG, finanza sostenibile e banche in Italia: stato dell’arte e prospettive, 25 Maggio.

- Gutiérrez-Ponce, H.; Wibowo, S.A. (2024), Do sustainability practices contribute to the financial performance of banks? An analysis of banks in Southeast Asia. Corporate Social Responsibility and Environmental Management, 31(2), 1418-1432.

- Houston, J.F.; Shan, H. (2022). Corporate ESG profiles and banking relationships. The Review of Financial Studies, 35(7), 3373-3417.

- La Torre, M. (2021), Banche e sostenibilità: più dell’amor può la compliance. L’anima ESG delle banche europee: chi vince tra autorità e mercato?, Il Sole 24Ore, 7 Aprile.

- La Torre, M.; Leo, S.; Panetta, I.C. (2021), Banks and environmental, social and governance drivers: Follow the market or the authorities? Corp Soc Responsib Environ Manag. 2021;1–15.

- Lupu, I.; Hurduzeu, G.; & Lupu, R. (2022). How is the ESG reflected in European financial stability?. Sustainability, 14(16), 10287.

- Nizam, E.; Ng, A.; Dewandaru, G.; Nagayev, R.; Nkoba, M.A. (2019), Theimpact of social and environmental sustainability on financial performance: a global analysis of the banking sector. J. Multinatl. Financ. Manag. 49, 35-53.

- Shakil, M.H.; Mahmood, N.; Tasnia, M.; Munim, Z.H. (2019). Do environmental, social and governance performance affect the financial performance of banks? A cross-country study of emerging market banks, Manag. Environ. Qual. Int. J. 30, 1331-1344.

- Shen, C.H.; Wu, M.W.; Chen, T.H.; Fang, H. (2016). To engage or not to engage incorporate social responsibility: empirical evidence from global banking sector.Econ. Modell. 55, 207e225.

- Shin, D. (2021), Corporate esg profiles, matching, and the cost of bank loans. University of Washington.

- Simsek, O.; Cankaya, S. (2021). Examining the relationship between ESG scores and financial performance in banks: Evidence from G8 countries. Press Acad. Procedia, 14, 169-170.

- Tóth, B.; Lippai-Makra, E.; Szládek, D.; Kiss, G.D. (2021), The contribution of ESG information to the financial stability of European banks. PÉNZÜGYI SZEMLE/PUBLIC FINANCE QUARTERLY, 66(3), 429-450.

- Yuen, M.K.; Ngo, T.; Le, T.D.; Ho, T.H. (2022), The environment, social and governance (ESG) activities and profitability under COVID-19: evidence from the global banking sector. Journal of Economics and Development, 24(4), 345-364.

Figure 1.

Representation of countries that have experienced an increase in the level of banking stability. Elaboration by the authors using Flourish chart with World Bank data. Malta is excludes since it is an outlier.

Figure 1.

Representation of countries that have experienced an increase in the level of banking stability. Elaboration by the authors using Flourish chart with World Bank data. Malta is excludes since it is an outlier.

Figure 2.

Representation of countries that have experienced a reduction in the level of banking stability. Elaboration by the authors using flourish chart with World Bank data.

Figure 2.

Representation of countries that have experienced a reduction in the level of banking stability. Elaboration by the authors using flourish chart with World Bank data.

Figure 3.

Results of clustering with k-Means algorithm both with the Elbow method and with the Silhouette coefficient.

Figure 3.

Results of clustering with k-Means algorithm both with the Elbow method and with the Silhouette coefficient.

Figure 4.

Representation of the centers of the clusters in a dynamic dimension with identification of the hierarchical trend.

Figure 4.

Representation of the centers of the clusters in a dynamic dimension with identification of the hierarchical trend.

Figure 5.

A map of the policy implications of the integration of ESG factors in the governance of banking stability.

Figure 5.