Submitted:

11 April 2024

Posted:

11 April 2024

You are already at the latest version

Abstract

Financing frameworks for Public Private Partnerships (PPPs) are lacking in developing countries. This study develops and recommends a financing framework for water and sanitation PPP infrastructure projects in Zimbabwe. The framework model integrates the Public Private Partnership models, sources of finance for water and sanitation PPPs, and the drivers of water and sanitation PPP finance. Both the public and private sources of finance are instrumental for financing water and sanitation PPP projects. Tobit econometric models are applied on data collected from both international and domestic data banks. The time frame for the analysis is a 25-year period running from 1996 ending 2021. Capital market variables, bank market development and economic affluence drive the financing of water and sanitation Public Private Partnership infrastructure projects in Zimbabwe. The study recommends the application of the developed framework in the water and sanitation Public Private Partnership infrastructure financing policy, for developing countries.

Keywords:

Water and Sanitation

; Public private partnerships

; Infrastructure finance

; Zimbabwe

1. Introduction

After decades of economic turmoil and political turbulence, the deterioration of infrastructure in Zimbabwe is evident [1]. Fiscal misalignment, corruption and the haphazardness with which the land redistribution programme was executed piloted the deepest peace-time economic contraction the country has ever seen [2,3]. Western governments, responding to human rights abuses and the disregard for the rule of law imposed political and economic sanctions [4]. Consequentially, the country failed to service its debts and payment arrears accumulated with International Development Partners (IDP) and bilateral creditors. Zimbabwe’s debt overhang currently stands at over US$17.7 billion and it’s making it difficult for the country to obtain long-term infrastructure financing [5]. The result has been the depletion of the productive capacity of existing infrastructure facilities including those under the water and sanitation sector.

In Zimbabwe, water and sanitation services provision is unreliable [6]. Securing capital investment hasn’t been easy for the country resulting in a sustained deterioration in the quality of operations. Frequently, sewage networks experience disruptive blockages, and the scarceness of wastewater treatment chemicals is resulting in unprocessed sewage being disposed in freshwater bodies that supplies Zimbabwe`s urban populace [7]. Water treatment plants are malfunctioning fundamentally because the machinery has long outlived its productive life. Water and sanitation sector challenges are further compounded by the structural bottlenecks in the generation and distribution of electricity [8]. Water and sewage systems requires dependable electricity supply without which they cannot be efficiently operated. Often, maintenance of water and sanitation plants is deferred and the lack of financing for plant expansion and rehabilitation has made water services delivery sporadic thus creating a constant threat to public health [9]

Others support the view that Public Private Partnerships (PPP), if well structured, can remedy financing bottlenecks in the water and sanitation infrastructure sector [10]. PPPs can crowd in private sector experience, operational efficiencies and most importantly needed capital for water and sanitation infrastructure development. The government of Zimbabwe is conscious of this. Under its Agenda for Sustainable Socio-Economic Transformation (Zim-ASSET) and the Transitional Stabilisation Programme (TSP), the government has opened the water and sanitation sector to private sector investments [11]. However, comparative to China where the demand for water and sanitation PPP transactions continue to strengthen, the uptake of PPP ventures is currently very low [12]. Several factors explain the positive trend in the number of Infrastructure PPPs that have reached financial closure in China. The Chinese government shifted from a centrally planned economic system where water supply was viewed as an indispensable task for the government to satisfy the elementary public needs with urban water and sanitation services being provided by the State free of charge [13,14]. Foreign investors are permitted to pursue a competitive bidding process for urban water infrastructure contracts. Market oriented reforms which entailed liberalisation of water tariffs if a project finance structure has a foreign component in it were instituted [13,14]. Through the reforms, international investors received attractive risk-adjusted net returns from Chinese water and sanitation infrastructure projects. Moreover, besides the tariff reforms, instead of relying solely on foreign banks for financing, China encouraged domestic banks to invest in water and sanitation PPPs [14].

In contrast to PPP market developments in China, [15] reports that since 1994, notwithstanding the socio-economic importance of the water for sustainable development and the infrastructure inadequacy in Zimbabwe`s, there hasn`t been any mega water or sanitation sector PPP transaction that has successfully been executed. Where the water and sanitation PPPs are implemented, projects have stalled [16]. The Matabeleland Zambezi Water Project (MZWP) whose conception was in 1912, during the colonial era is a classic example of one such project. Although several factors can be cited for the delays, according to [16], the key constraint is inadequate finance. Given this background, in this paper, the research seeks to propose a framework to finance water and sanitation PPPs in Zimbabwe. [17] notes that infrastructure development, in part, is constrained by the lack of comprehensive frameworks to guide policy. Studies that seek to cover the gap in [17] in Zimbabwe are scant. Where reseachers have attempted to fill this gap, either the methodology has been largely qualitative [18] or a broad categorisation of infrastructure sectors has been adopted [18,19]. The current study, quantitative in nature, recognises that risk and return profiles differ across infrastructure sectors hence the focus on the water and sanitation sector.

The remainder of the paper is structured as follows: section 2 reviews the literature with a specific focus on the sources and drivers of PPP finance, the methodology is presented under section 3 with 4 discussing the findings. The framework for financing water and sanitation PPPs is presented under section 5. Section 6 concludes the paper.

2. Review of Literature: Sources and Drivers of PPP Finance

Government, in the greater interest of society, provide public goods. [20] noted that, in Europe, public financing of water and sanitation infrastructure is institutionalised at the continental level through the European Union (EU) Cohesion Funds. Infrastructure development in Central and Eastern European countries benefited immensely from the EU Cohesion Funds [20]. Equality and sustainable access to water and sanitation services is achievable subject to public investment [21]. Taxes and tariffs revenue can finance water and sanitation infrastructure either in competition or in collaboration with private investors. With proper administrative capacity, taxation and tariffs can be a stable source of viability gap finance in water and sanitation PPPs [22]. The size of the tax base is a fundamental determinant of the amount of revenue that can mobilised. The informal structure of the economy as well as profit-shifting activities by multinational companies predominantly through transfer pricing manipulation has eroded the tax base in Zimbabwe [23]. Hence the need to integrate other innovative sources to finance PPPs.

Official development finance (ODF) consists of various forms of international developmental financial flows mainly towards emerging and developing countries [24]. The key components of ODF are Official development assistance (ODA), other official Flows (OOF), other transactions from development finance institutions (DFIs) and contributions towards peacekeeping operations among other forms of financial flows [24]. Official development assistance (ODA) refers to financial flows issued from publicly controlled bilateral or multilateral development agencies [25]. ODF loans and grants are issued either on concessional or non-concessional terms [26]. Concessional loans have favourable loan servicing structures that suit the peculiar socio-economic conditions of the recipient country [27]. For most developing countries, ODF still constitutes a small proportion of water infrastructure finance. [28] stated that ODF for water and sanitation is increasing at slower rates compared to the health and education sectors. Regardless, given the water and sanitation infrastructure financing gap, ODA has been noted to be insufficient to address the scope of investment requirements as many donor countries have failed to reach the 0.7% of Gross Domestic Product (GDP) aid target [29].

Foreign direct investment in Infrastructure (FDII) is important in providing financial resources, know-how and technology for water and sanitation infrastructure development [30,31]. Privatisation policies of the 1990s immensely promoted FDII. Private FDII investments have taken many forms that vary depending on the level of investment risk [32]. Investment structures such as joint ventures and divestitures have been used in FDII. With greenfield infrastructure projects, for instance, a foreign enterprise can jointly finance, construct and operate a water and sanitation facility [33]. Ownership of the facility can either remain joint or can transfer to either the private or public enterprise at the end of the contract. With a divesture structure, foreign companies purchase an equity stake in a state-owned (SOE) enterprise through an asset sale, privatisation or public offering [34]. The government of Zimbabwe view FDII as important to meet the SDGs targets. Accordingly, the Zimbabwe Investment Development Agency (ZIDA) bill was promulgated in 2019 to outline safeguards and opportunities available to international investors. The ZIDA bill is complemented by the National Development Strategy 1 (NDS 1), a blueprint directing economic decisions between 2021 and 2025.

Optimising bank sources of finance reduces financial pressure on the governments seeking to develop infrastructure facilities. Banks, as financial intermediaries, provide loanable funds [35,36]. This functionality that banks provide under project finance structures is very important and complex at the same time. Banks can issue securities to mobilise loanable resources. With developments in financial engineering, banks can underwrite infrastructure loans with the intention of selling the entire asset or a part of it on the bank loan secondary market [37]. The global financial crisis of 2007 and the Euro-zone sovereign crisis, as well as the regulatory changes that followed, have not made bank lending to PPP infrastructure projects any easier [38]. The policy induced changes in the way banks conduct business impact negatively on the large-scale construction industry that relies on long-term loans to bring projects to financial and operational completion. [39] noted that the size of commercial banks in Africa is small. This is compounded by the lack of meaningful domestic savings in developing economies.

Listed Infrastructure companies raise equity capital to finance investments in PPP projects through issuing shares. Shares are perpetuities that confer ownership to the holders and are ideal for long-term investments. In emerging markets, public equity markets are dominated by infrastructure companies [40]. Their participation is traced back to the era of privatisation policies [41]. Like infrastructure companies, infrastructure funds are active in the PPP market. [42] highlighted that infrastructure funds invest heavily in PPP/PFI projects hence they are an attractive source of project finance. The funds are largely popular in Australia having been promoted through the partnership that Macquarie Group entered with state-controlled entities [43]. Financing PPP through the stock market requires the market to be developed to a stage where it’s feasible to mobilise the huge amounts required to develop economy-transforming infrastructure projects. Stock market crashes typified by the global financial meltdown of 2007 can potentially result in massive capital losses to investors in PPP projects [36].

The universe of bonds is very wide [44]. Nonetheless, project bonds are an instrument of choice for PPP financing. The SPV can issue project bonds to a catchment of investors to whom commitment is made to periodically make coupon payments and to reimburse the capital when the bond matures or according to a predetermined amortisation schedule [45]. Obligations to bondholders are settled exclusively from the cash flows generated by the project without the possibility of recourse from other cash flow sources. The financial performance of the underlying project is integral to debt servicing. The SPV can issue bonds denominated in domestic currency with a preference for holding the security being given to domestic institutional and retail investors. Such bonds are defined as domestic instruments. Domestic bonds are ideal when financing is being sought for small-scale projects whose geographical concentration is well defined with a large constituent of raw materials being locally sourced. Financing large-scale infrastructure projects using domestic bonds is challenging for most developing countries. Bond markets are underdeveloped and as such, they cannot supply the requisite financial resources [46,47]. Contra to domestic bonds are foreign project bonds, an instrument of choice for large-scale capital-intensive projects. Foreign bonds are issued in foreign markets in the currency of the placement market. Bonds have been used to finance public infrastructure in Zimbabwe with the medium of issue being private placement [19]. However, the use of infrastructure bonds is constrained by the absence of a developed bond market.

In most developing countries, [48] confirmed that PPP financing is driven by the nature of the economic environment. The same study further postulated that indebted governments have a higher likelihood of signing PPP contracts. The indebtedness of the government of Zimbabwe has substantially curtailed international capital inflows hence the policy inclination towards private investment for water and sanitation infrastructure development. [49], further confirmed that inflation, import cover, market size and purchasing power drive PPP investments in developing countries. However plausible the findings are, they cannot be superimposed to the Zimbabwean scenario in view of the socio-economic transformation the country underwent over the recent past. [50] concluded that the level of inflation negatively relates with PPP financing. The finding is congruent to economic theory that emphasises the corrosive effect of high inflation on return on investment. Nonetheless, the study is premised on the supposition that, in developing countries, the impact of macro-economic factors is symmetric across infrastructure sectors, which is not the case. In the current study, the examination is water and sanitation sector specific.

Financial market access is a pre-requisite for infrastructure project companies to borrow long-term. [51] established that, in PPP energy markets, the extent of financial market advancement significantly impacts financing. Nonetheless, and relative with the bank loan market, the capital market predominantly drives PPP energy investment. Extending [51] analysis to Zimbabwe`s infrastructure sectors and compare the results adds value to discussions on PPP financing in emerging and developing countries. Contra to [51,52], empirically identified the bank loan market as the main driver relative to the capital market. The finding suggests that the bank market is central to intermediating PPP infrastructure investments in developing countries.

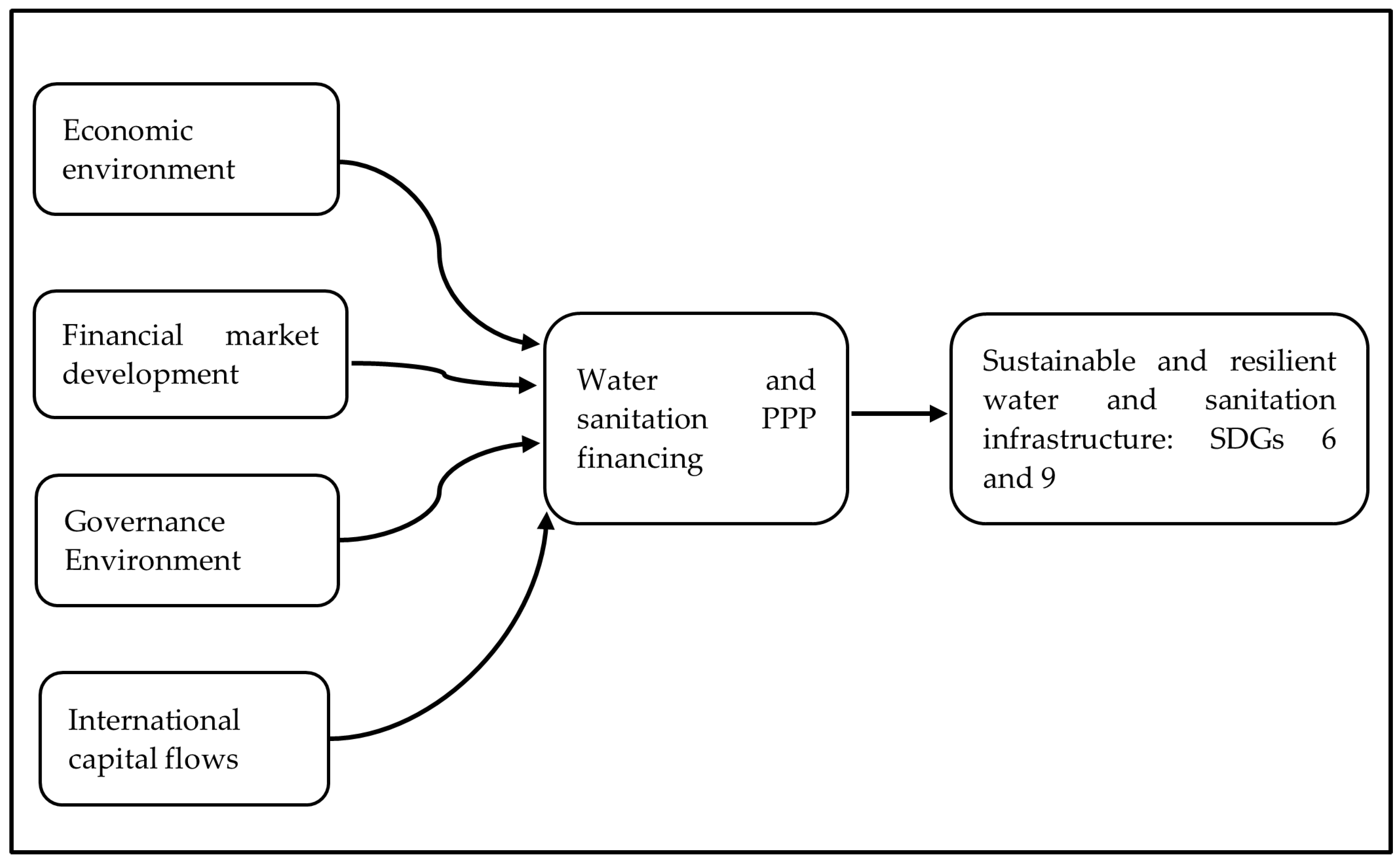

Other than economic and financial development variables, the governance environment influences the sustainable financing of water and sanitation PPPs. Either collectively or individually, governance elements of rule of law, control of corruption, among others, exert influence PPP finance. However, reseachers at times report contrasting results with regard to the relationship between the element of the governance environment and the financing of PPP infrastructure projects. For instance, contrary to [53,54] reported that, in selected developing countries, the more corrupt the economic environment is, the higher the level of PPP infrastructure investments. The researchers argued that, at times project sponsors cannot entirely circumvent corruption. Similarly, [55], counter intuitively reported the finding that a higher likelihood of political instability results increases PPP infrastructure investments. This is contrary to [56] who postulated an inverse relationship between infrastructure investment and political instability. [55] argued that citizen demand for better services expressed through political uprising may compel public authorities to use PPPs to increase investments in infrastructure. Conceptually, the relationship between determinants of PPP investment and elements of the economic environment, financial market development and the governance environment and water and sanitation PPP financing is presented under Figure 1.

3. Materials and Methods

In line with [50] and [57] the study uses secondary data for empirical analysis. Data on PPPs investment is obtained from the World Bank`s Private Participation in Infrastructure database (PPI). Even though the PPI databank provides good reporting of internationally published PPP projects. According to [48], the data bank falls short regarding the reporting of small projects that involve domestic sponsors. As such, domestic databases: the Central Statistics Office (CSO) Zimbabwe and the Reserve Bank of Zimbabwe (RBZ) data bank will supplement the World Bank databases. The sample frame is from 1996 to 2021. The choice of time frame is rationalised on the grounds that, Zimbabwe, being an infant PPP market, it was in the late 1990s that the pioneering PPP contract was signed. The sample frame provides 25 data points that the researchers consider reasonable, given that this is a single country analysis. In sync with [52] and [58] the dependent variable (PPPUSD) is the investment value of PPPs that reached financial closure. Table 1 summaries explanatory variables.

The objective of the analysis is to present a proposed framework for financing water and sanitation PPP projects in Zimbabwe. Achieving the objective requires firstly, the identification of finance sources for PPP projects (section 2), and secondly, empirical determination of the variables that drives PPP financing in Zimbabwe. To achieve the later, and since the dependent variable (PPPUSD) is a non-negative and continuous variable, the Tobit regression model is used [55,58]. Moreso, Tobit regression model accounts for censoring in the dependent variable that can potentially create biases if Ordinary Least Squares (OLS) was to be used. Parameters are estimated using the maximum likelihood estimation. The dependent variable is judged to left censored, being characterised by a clustering pattern around zero. Zimbabwe`s PPP market is in its formative stages and for this reason, over the sample period, some years have recorded zero PPPs that were finalised. Literature confirms governance variables to be highly correlated [67,68]. To manage the adverse consequences of multicollinearity and the loss of explanatory power, governance variables are examined separately, and hence seven models are estimated.

Where is the natural logarithm of the USD investment value differenced once. and is the natural logarithm of the one period lag of GDP per capita and Inflation differenced once. Whereas represents a one period lag of the ratio of international reserves to imports differenced once. Whilst , , and are financial market measures of stock market capitalisation to GDP, domestic bank credit to private sector, the ratio of bank credit to bank deposits and non-performing loans respectively. The metrics are in first difference. , , , , and represents the first difference of the percentile ranking of the governance variables namely the control of corruption, regulatory quality, rule of law, voice and accountability, political stability and government effectiveness, respectively. : is the error term. Multicollinearity is controlled by estimating models using variables with a variance inflation factor (VIF) under 10 [62]. Unit root testing is performed using the Augmented-Dick-Fuller test [69]. ADF and VIF diagnostics are reported under Appendix A. As recommended by [69,70,71], to control heteroskedasticity, robust standard errors are used.

4. Results and Discussion of Findings

Seven models are estimated, and the results are summarised in Table 2. Mixed influence of GDP per capita on PPP financing is reported across the models. Models 1, 2 and 6 confirms that GDP per capita, at 10% and 5% level of significance impact water and sanitation PPP investment. Contrary to Sharma [50]) and [58], the relationship between GDP per capita and PPP financing in Zimbabwe is negative. The inverse variation between GDP per capita and water and sanitation PPPs, consistent across the 7 models, can be explained by the World Bank observation that low-income economies have greater need to invest in infrastructure including through PPP to transform economies and enhance the standards of leaving. As countries prosper, the demand for PPP declines since public finances can adequately finance water infrastructure. Nevertheless, models 3, 4, 5 and 7 report that GDP per capita does not significantly influence the financing of water PPPs in Zimbabwe. China is the main source of infrastructure finance in Zimbabwe, and primarily, investments are rationalised on political solidarity rather than economic metrics.

The ratio of international reserves to imports (IRIMP) does not influence water and sanitation PPPs. [72] argues that the level of import cover is an important determinant of infrastructure investments on the observation that developing economies characterised by low import cover are prone to currency crashes. In Zimbabwe, IRIMP has largely been low [73]. [74] assert that the closure of water and sanitation PPPs is explained by the prevalence of the stable rate of inflation in China. However, despite high inflation volatility [20], the bearing of inflation on water and sanitation infrastructure financing is insignificant. Perhaps, the finding can be explained by the fact that precious minerals have been used to guarantee returns for investors. On the other hand, we determine that the relationship between FDI and PPP financing is negative and significant. The negative relationship implies that subject to dwindling international capital inflows, the government of Zimbabwe values PPPs for water infrastructure development. In fact, [75] states that it is only when public finances are under pressure that the government of Zimbabwe seek to attract private partners.

The ratio of stock market capitalisation positively relates with water and sanitation finance and the relationship is significant at 1%. Earlier, [51] confirmed that PPP investments are mainly driven by capital market development. Characteristically, infrastructure investments are long-term in nature and thus require liquid markets for financing. Other than the capital market, bank market development influences water and sanitation PPP financing. The bank credit to bank deposits (BCD) ratio influence significantly PPP financing at 1%. The finding is synchronous to [35] and [64] who in their studies established that commercial banks with large balance sheet are better positioned to finance infrastructure projects. The ratio of domestic bank credit to private sector (DBC) significantly influences water PPP finance. During the early construction phases, [35,52] reiterated the centrality of commercial bank loans as source of debt finance.

Non-performing loans (NPL) significantly and negatively bears on financing PPP investment. The finding supports the proposition that the propensity to avail project finance is high for institution with high asset quality [35]. According to [76], since 2015, the proportion of non-performing loans in the banking sector has been improving. Contrary to [18,55,56,65,75,77] who reiterated the importance of governance indicators in project finance, the current study, concludes that, in Zimbabwe, the governance environment has insignificant bearing on PPP financing. Perhaps, the observation can be explained by the fact that the Chinese, with little regard for institutional quality, are the main sponsors of water and sanitation PPPs in Zimbabwe.

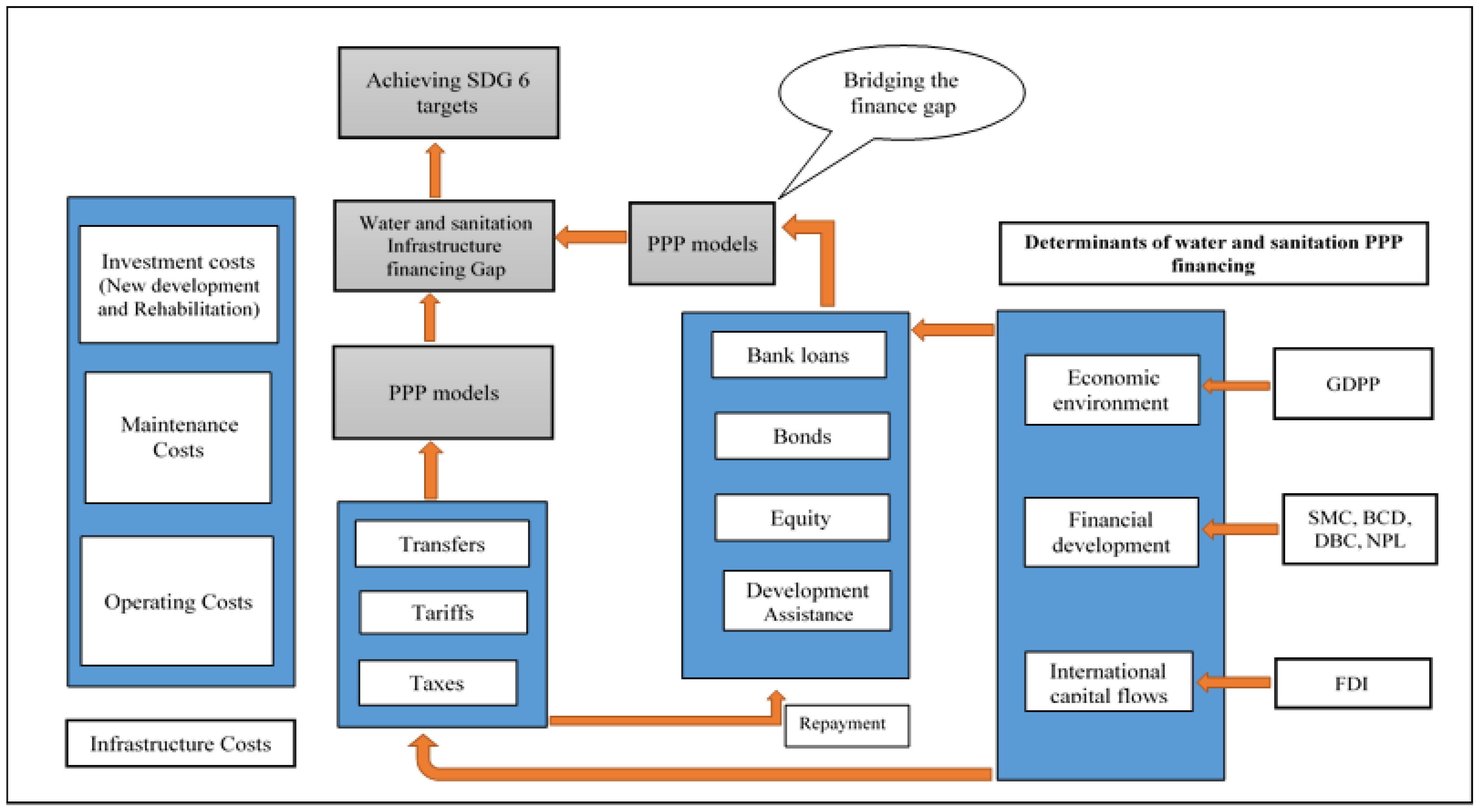

5. Framework for Financing Water and Sanitation PPPs.

Figure 2 summarises the framework to finance water and sanitation infrastructure PPPs in Zimbabwe. The provision of water and sanitation can be conceptualised as constituting of three cost components namely capital investment, maintenance, and operating costs [78]. Capital investment is expenditure on hardware and software on water and sanitation infrastructure systems. Expenditure on upgrading or expanding water and sanitation services to additional consumers is classified as capital in nature. Software capital expenditure includes the costs of assessment studies that precede the water and sanitation project implementation along with any other costs for capacity building. Once construction is completed, a phase comes in the lifecycle of the project when the infrastructure asset becomes operational. [82] noted that, even though operating expenditure receives limited attention in the water and infrastructure financing discourse, over the life-time of the asset, operating expenditure are substantial. Moreover, in some developing countries, despite international support to build infrastructure assets, domestic resource could not suffice to operate the asset. Operating costs are recurrent in nature and include expenditure on labour and materials needed to keep water and sanitation systems functional. Operating costs are expected to constitute a significant share of infrastructure cost if sustainable development targets on water are to be achieved [79]. Overtime, some components of the water and sanitation systems may stop working and would require maintenance. [80] reiterated that water and sanitation finance plan in Zimbabwe, for the decade ahead, must prioritise maintenance expenditures. Approximately 50% of the treated water produced in Zimbabwe cannot be accounted for due to network distribution losses. Inadequate expenditure on maintenance, besides reducing the useful life of investment assets, increases asset replacement cost by 60%. [79]. To meet SDG target 6.1 and 6.1 is estimated to cost developing countries between 1.1% and 1.4% of GDP.

The water and sanitation financing gap in Zimbabwe is huge. For instance, according to the greater Harare master plan, the city requires, between 2021 and 2030, USD1.4 billion to finance water and sanitation infrastructure. When investment requirements for other cities such as Gweru, Bulawayo and Mutare are factored in, the investment need is even high. The need for capital investments has come during a phase of severe economic underperformance. Given the acceptance of PPPs for infrastructure development in Zimbabwe, Figure 2 shows that private and public sources complement to finance PPPs [81]. Commercial bank loans can be used to channel capital, operational and maintenance resources for water and sanitation PPP projects. Zimbabwe has 19 functional banking institutions which, given a conducive environment can be a rich source of loanable funds. Bank source can be supplemented with bonds. On average bonds offer long maturity hence the suitability to finance infrastructure. The types of bonds that can be issued may include sovereign bonds, corporate bonds, diaspora bonds, project bonds among other bond classes. Furthermore, domestic and international equity markets can be used to mobilise finance. The equity market is an attractive source for long-term investments since there is no specific deadline for capital repayment. Moreso, equity investors are often interested in holding a stake in PPPs for a longer period to maximise on both the capital gains and the holding period return. Harnessing the sources of financing is dependent on the economic, financial development and international capital flow variables econometrically confirmed significant determinants. PPP financing policy in Zimbabwe should target these variables to enhance investment inflows into the water and sanitation sector.

6. Conclusions

The study sought to develop a financing framework for water and sanitation PPPs in Zimbabwe. This follows the observation by [17] that even in developed OECD countries, there are no readily available comprehensive frameworks for financing public infrastructure. [19] further recommends that logical frameworks be developed to guide public infrastructure policies a gap the study contributed to. The study concludes that water and sanitation financing frameworks, in line with SDG 17, must integrate both state and non-state sources of finance to sustainably bridge the water and sanitation financing gap in Zimbabwe. The government of Zimbabwe should seek to optimize internal public revenue sources of taxes, tariffs and transfers. Collectively and independently, public sources of PPP financing provide viability gap funding critical to enhance the risk profile of water and sanitation infrastructure projects. To crowd in private investors, the study concludes that the level of financial market development is key. For that reason, enhancing private sources of PPP finance requires that economic policies in Zimbabwe stimulates both capital market and bank market development [61]. Developed financial markets are efficient in intermediating infrastructure investments. The prosperity of a nation measured through GDP per capita is an important determinant of water and sanitation PPP financing in Zimbabwe. Unlocking investment in the water sector thus depends on prudent macro-polices that enhances the standard of living in Zimbabwe given that services consumption is dependent on income levels. The government of Zimbabwe should thus institute effective growth oriented macro-economic policies. Other than contributing to the scant literature on financing frameworks for water and sanitation PPPs in Zimbabwe, the study is a basis for future research. Instead of censored regression, future research can consider count models instead to build the framework. Moreso a similar study can be replicated in other jurisdictions and compare the findings.

Author Contributions

Conceptualization, J.M. and P.M.; methodology, J.M. and P.L.M.; formal analysis, J.M. and P.L.M.; writing—original draft preparation, J.M.; review and editing, P.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding. The APC was paid by the University of South Africa (UNISA).

Data Availability Statement

Data used in the study was sourced from publicly accessible repositories of: World Bank PPI database, Reserve Bank of Zimbabwe, Central Statistics Office Zimbabwe.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A.

Table 3.

Variance inflation factor analysis.

| Variable | Acronym | VIF |

|---|---|---|

| Stock market capitalisation to GDP | SMC | 5,43 |

| Foreign direct investment | logFDI | 4,9 |

| Non-performing loans | NPL | 3,68 |

| Domestic bank credit to GDP | DBC | 3,32 |

| Bank credit to bank deposits | BCD | 3,15 |

| Gross domestic product per capita | logGDPP | 2,82 |

| Political stability | PS | 2,72 |

| Inflation | logIFN | 2,4 |

| Government effectiveness | GE | 2,01 |

| Regulatory quality | RQ | 1,98 |

| Control of corruption | CC | 1,86 |

| Rule of law | RL | 1,85 |

| Voice and accountability | VA | 1,84 |

| International reserves to imports | IRIMP | 1,76 |

| Mean VIF | 2,837 |

Table 4.

ADF unit root test.

| Variable | ADF Statistic | Critical value (1%) | Critical value (5%) | Critical value (10%) |

|---|---|---|---|---|

| ΔlogPPPUSD | -6.207*** | -4.380 | -3.600 | -3.240 |

| ΔlogGDPP | -2.796** | -2.528 | -1.725 | -1.325 |

| ΔIRIMP | -6.362*** | -4.380 | -3.600 | -3.240 |

| ΔlogIFN | -3.673*** | -2.528 | -1.725 | -1.325 |

| ΔlogFDI | -4.163** | -4.380 | -3.600 | -3.240 |

| ΔSMC | -4.338** | -4.380 | -3.600 | -3.240 |

| ΔDBC | -5.529*** | -4.380 | -3.600 | -3.240 |

| ΔBCD | -4.616*** | -4.380 | -3.600 | -3.240 |

| ΔNPL | -2.320** | -2.528 | -1.725 | -1.325 |

| ΔFDX | -5.529*** | -4.380 | -3.600 | -3.240 |

| ΔGIX | -4.891*** | -4.380 | -3.600 | -3.240 |

| ΔCC | -1.728** | -2.528 | -1.725 | -1.325 |

| ΔRQ | -4.348*** | -4.380 | -3.600 | -3.240 |

| ΔRL | -5.807*** | -4.380 | -3.600 | -3.240 |

| ΔVA | -1.834** | -2.528 | -1.725 | -1.325 |

| ΔPS | -3.219*** | -2.528 | -1.725 | -1.325 |

| ΔGE | -4.891** | -4.380 | -3.600 | -3.240 |

Note: Δ denotes the first difference operator and test are conducted at first difference. ***; **; * indicate that the null hypothesis of unit root tests is rejected at 1%, 5% and 10%, respectively.

References

- Bandauko, E., Bobo, T., and Mandisvika, G., 2018, Towards Smart Urban Transportation System in Harare, Zimbabwe. In Intelligent Transportation and Planning: Breakthroughs in Research and Practice, pp. 962-978. [CrossRef]

- Drabo, D., 2018, From Land Reform to Hyperinflation: The Zimbabwean Experience of 1997-2008 . Available at: https://econpapers.repec.org/paper/haljournl/hal-02141818.htm [Accessed: 20 August 2020].

- Adeleke, F., 2019, Illicit financial flows and inequality in Africa: How to reverse the tide in Zimbabwe. South African Journal of International Affairs, vol. 26, no. 3. pp. 367-393. [CrossRef]

- Marevesa, T., 2019, The government of national unity and national healing in Zimbabwe. In National Healing, Integration and Reconciliation in Zimbabwe. 1st edition. Routledge, pp. 55-68. [CrossRef]

- Saungweme, T. and Odhiambo, N. M., 2019, Government debt, government debt service and economic growth nexus in Zambia: a multivariate analysis. Cogent Economics and Finance, vol. 7, no. 1. pp. 1-17. [CrossRef]

- Nhapi, I., 2015, Challenges for water supply and sanitation in developing countries: case studies from Zimbabwe. In Understanding and managing urban water in transition, pp. 91-119. Springer, Dordrecht. [CrossRef]

- Tendaupenyu, P., Magadza, C.H.D. and Murwira, A., 2017, Changes in landuse/landcover patterns and human population growth in the Lake Chivero catchment, Zimbabwe, Geocarto International, vol. 32, no. 7, pp.797-811. [CrossRef]

- Homerai, F., Mayo, A.W. and Hoko, Z., 2019; Sustainability of Chiredzi town water supply and wastewater management in Zimbabwe. African Journal of Environmental Science and Technology, vol. 13, no. 1, pp.22-35. [CrossRef]

- Cole, A., Mudhuviwa, S., Maja, T. and Cronin, A., 2021, Lessons Learnt from financing WASH rehabilitation works in small towns in Zimbabwe. Development in Practice, vol. 31, pp.533-547. [CrossRef]

- Fall, M., Marin, P., Locussol, A., and Verspyck, R., 2009, Reforming Urban Water Utilities in Western and Central Africa: Experiences with Public-Private Partnerships Case studies. Available at: http://www.ifc.org/wps/wcm/connect/31d1eb804ba99afa8df8ef1be6561834/WaterPPPvol2.pdf?MOD=AJ PERES (accessed 28 March 2021).

- Ministry of Finance and Economic Development 2019, 2019 national budget statement. Harare, Zimbabwe. Available at: http://www.zimtreasury.gov.zw/?page_id=731 (Accessed 25 September 2022).

- Zhao, Z.J., Su, G., and Li, D., 2018, The rise of public-private partnerships in China, Journal of Chinese Governance, vol. 3, no. 2, pp. 158. [CrossRef]

- Wu, X., Schuyler House, R., and Peri, R., 2016, Public-private partnerships (PPPs) in water and sanitation in India: lessons from China. Water Policy, vol. 18, no. 1, pp. 153-176. [CrossRef]

- Qian, N., House, S., Wu, A.M. and Wu, X., 2020, Public–private partnerships in the water sector in China: A comparative analysis. International Journal of Water Resources Development, vol. 36, no. 4, pp. 631-650. [CrossRef]

- Private participation in infrastructure database. Available at: https://ppi.worldbank.org/en/ppi (Accessed 10 May 2023).

- Chilunjika, A., 2023. Public Private Partnerships (PPPs), road tolling and highway infrastructure investment in Zimbabwe. International Journal of Research in Business and Social Science , vol. 12, no. 3, 575-584. https://orcid.org/0000-0001-9801-4803.

- Henn, L., Sloan, K., Charles, M.B. and Douglas, N., 2016, An appraisal framework for evaluating financing approaches for public infrastructure. Public Money & Management, vol. 3, no. 36, pp. 273-280. [CrossRef]

- Tshehla M. F., Mukudu E., 2020. Addressing Constraints for Effective Project Finance for Infrastructure Projects in Emerging Economies–the Case of Zimbabwe. Journal of Construction Business and Management, vol. 4, no. 1. Pp. 48-59. [CrossRef]

- Kapesa, T., Mugano, G. and Fourie, H., 2021, A framework for financing public economic infrastructure in Zimbabwe. Southern African Journal of Accountability and Auditing Research, vol. 23, no. 1, pp. 65-76. [CrossRef]

- Frone, S. and Frone, D.F., 2018, issues of efficiency for public-private partnerships in the water sector. Studies and scientific researches. economics edition, vol. 27, Available at: pdfs.semanticscholar.org (accessed 20 Jan 2022).

- World Bank. 2017, Reducing inequalities in water supply, sanitation, and hygiene in the era of the sustainable development goals: Synthesis report of the WASH poverty diagnostic initiative. World Bank Group: Washington, DC. https://openknowledge.worldbank.org/bitstream/handle/10986/27831/w17075.pdf?sequence=5&isallowed=y (accessed 19 May 2020).

- Möykkynen, H. and Pantelias, A., 2021, Viability gap funding for promoting private infrastructure investment in Africa: Views from stakeholders. Journal of Economic Policy Reform, vol. 24, no. 2, pp. 253-269. [CrossRef]

- Sebele-Mpofu, F.Y., Mashiri, E. and Korera, P., 2021. Transfer Pricing Audit Challenges and Dispute Resolution Effectiveness in Developing Countries with Specific Focus on Zimbabwe. Accounting, Economics, and Law: A Convivium. [CrossRef]

- Miyamoto, K. and Chiofalo, E., 2016, Official development finance for infrastructure: with a special focus on multilateral development banks. [CrossRef]

- Patel, P., Dahab, M., Tanabe, M., Murphy, A., Ettema, L., Guy, S. and Roberts, B., 2016. Tracking official development assistance for reproductive health in conflict-affected countries: 2002—2011. BJOG: An International Journal of Obstetrics & Gynaecology, vol. 123, no. 10, pp. 1693-1704. [CrossRef]

- Kolker, J.E., Trémolet, S., Winpenny, J. and Cardone, R. 2016. Financing options for the 2030 water agenda. https://hdl.handle.net/10986/25495 (accessed 19 May 2021).

- Kitano, N. and Harada, Y., 2016, Estimating China’s foreign aid 2001–2013, Journal of International Development, vol. 28, no. 7, pp.1050-1074. [CrossRef]

- Alaerts, G.J. 2018. Financing for water – Water for financing: A global review of policy and practice. Sustainability, vol. 11, no. 3, pp.821-846. [CrossRef]

- Yaya, S., Udenigwe, O. and Yeboah, H., 2019, Development aid and access to water and sanitation in sub-Saharan Africa. In Better Spending for Localizing Global Sustainable Development Goals, pp. 167-185. [CrossRef]

- Osano, H.M. and Koine, P.W., 2016, Role of foreign direct investment on technology transfer and economic growth in Kenya: a case of the energy sector, Innovation and Entrepreneurship, vol. 5, no. 1, pp. 1-25. [CrossRef]

- Ghebrihiwet, N. and Motchenkova, E., 2017, Relationship between FDI, foreign ownership restrictions, and technology transfer in the resources sector: A derivation approach. Resources Policy, vol. 52, no. 1. pp. 320-326. [CrossRef]

- Kirkpatrick, C., Parker, D. and Zhang, Y.F., 2006, An empirical analysis of state and private-sector provision of water services in Africa. The World Bank Economic Review, vol. 20, no. 1, pp. 143-163. [CrossRef]

- Nag, T., Kettunen, J. and Sorsa, K., Exploring Private Participation in Indian Water Sector: Issues and Options. Sustainable Engagement in the Indian and Finnish Business, no. 119. Available at: isbn9789522167040.pdf (theseus.fi) (accessed 20 May 2021).

- Jackline, A., 2021, Public water and waste management in Uganda: the legal framework, obstacles and challenges. KAS African Law Study Library, vol. 7, no. 4, 642-652; Available at: 2363-6262-2020-4-642.pdf (nomos-elibrary.de) (accessed 15 Jan 2021).

- Rao V., 2018, An Empirical Analysis of the Factors that Influence Infrastructure Project Financing by Banks in Select Asian Economies. ADBI No 554. Available from: https://www.think-asia.org/bitstream/handle/11540/8651/ewp-554-project-financing-infrastructure-ppp-projects.pdf?sequence=1 (Accessed: 11 August 2021).

- Linh, N. N., Wan, X. and Thuy, H. T., 2018, Financing a PPP Project: Sources and Financial Instruments—Case Study from China. International Journal of Business and Management, vol. 13, no. 10, pp. 240-248. [CrossRef]

- Lu, Z., Peña-Mora, F., Wang, S.Q., Liu, T. and Wu, D., 2019, Assessment framework for financing public–private partnership infrastructure projects through asset-backed securitization. Journal of Management in Engineering, vol. 35, no. 6. [CrossRef]

- Vassallo, J.M., Rangel, T., de los Ángeles BAEZA, M., and Bueno, P.C., 2018, The Europe 2020 Project Bond Initiative: an alternative to finance infrastructure in Europe. Technological and Economic Development of Economy, vol. 4, no. 1, pp. 229-252. [CrossRef]

- WB (World Bank). 2011, Zimbabwe`s Infrastructure a continental perspective. Available at: https://openknowledge.worldbank.org/bitstream/handle/10986/27258/647390WP0P12420e0country0report0Web.pdf?sequence=1&isAllowed=y [Accessed: 02 February 2021].

- Srivastava, V., 2017, Project finance bank loans and PPP funding in India: A risk management perspective. Journal of Banking Regulation, vol. 18, no. 1, pp. 14-27. [CrossRef]

- Inderst, G., 2016. Infrastructure investment, private finance, and institutional investors: Asia from a global perspective.

- OECD (Organisation for Economic Cooperation and Development). 2015. Infrastructure financing instruments and incentives. Available at: https://www.oecd.org/finance/private-pensions/Infrastructure-Financing-Instruments-and-Incentives.pdf [Accessed 15 October 2022].

- Lara-Galera, A., Sánchez-Soliño, A. and Gómez-Linacero, M., 2017. Analysis of infrastructure funds as an alternative tool for the financing of public-private partnerships. Revista de la Construcción. Journal of Construction, vol 16, no. 3, pp.403-411. [CrossRef]

- Oji, C.K., 2015. Bonds: A Viable Alternative for Financing Africa’s Development. Available at: https://africaportal.org/publication/bonds-a-viable-alternative-for-financing-africas-development/ (Accessed 20 June 2023).

- Vecchi, V., Casalini, F., Cusumano, N., Leone, V.M. 2021. Private Investments for Infrastructure. In: Public Private Partnerships. Palgrave Macmillan, Cham. [CrossRef]

- Musah, A., Badu-Acquah, B. and Adjei, E., 2019, Factors that influence bond markets development in Ghana. Jurnal Perspektif Pembiayaan dan Pembangunan Daerah, vol. 6, no. 4, pp. 461-476. [CrossRef]

- Hyun, S., Park, D., and Tian, G., 2018. Determinants of Public–Private Partnerships in Infrastructure in Asia: Implications for Capital Market Development. Asian Development Bank Economics Working Paper Series, 552. [CrossRef]

- Jensen O., Blanc-Brude F., 2006, The handshake: why do governments and firms sign private sector participation deals? Evidence from the water and sanitation sector in developing countries. World Bank Policy Research Working Paper, (3937). Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=923244#:~:text=Jensen%2C%20Olivia%20and,com/abstract%3D923244 (Accessed 15 Aug 2022).

- IMF (International Monetary Fund) 2006, Determinants of public-private partnerships in infrastructure. Available at: https://www.elibrary.imf.org/view/journals/001/2006/099/001.2006.issue-099-en.xml (Accessed: 20 October 2022).

- Sharma C., 2011), Determinants of PPP in infrastructure in developing economies. Transforming government: people, process and policy, vol. 6, no. 2, 149-166. [CrossRef]

- Ba, L., Gasmi, F. and Noumba, P., 2010, Is the level of financial sector development a key determinant of private investment in the power sector?. World Bank Policy Research Working Paper, (5373). https://ssrn.com/abstract=1647517.

- Ba, L., Gasmi, F. and Um, P.N., 2017, The relationship between financial development and private investment commitments in energy projects. Journal of Economic Development, vol. 42, no.3, pp. 17-40. [CrossRef]

- Jensen, O. and Blanc-Brude, F., 2005, October. The institutional determinants of private sector participation in the water and sanitation sector in developing countries. In 4th Conference on Applied Infrastructure Research. https://www.researchgate.net/publication/228775879_The_Institutional_Determinants_of_Private_Sector_Participation_in_the_Water_and_Sanitation_Sector_in_Developing_Countries.

- Banerjee, S.G., Oetzel, J.M. and Ranganathan, R., 2006, Private provision of infrastructure in emerging markets: do institutions matter?. Development Policy Review, vol.24, no.2, pp.175-202. [CrossRef]

- Fleta-Asín, J. and Muñoz, F., 2021; Renewable energy public–private partnerships in developing countries: Determinants of private investment. Sustainable Development, vol. 29, no.4; pp.653-670. [CrossRef]

- Taguchi, H. and Sunouchi, Y., 2019, The role of institutions in private participation in infrastructure in low-and middle-income countries: Greenfield versus brownfield projects, Economics Bulletin, vol. 39, no. 3, pp.2027-2039; Available at: MPRA_paper_93555.pdf (uni-muenchen.de) (accessed 20 Aug 2022).

- Panayides, P.M., Parola, F. and Lam, J.S.L., 2015. The effect of institutional factors on public–private partnership success in ports. Transportation research part A: policy and practice, vol. 71, pp.110-127. [CrossRef]

- Pan, D., Chen, H., Zhou, G. and Kong, F., 2020, Determinants of public-private partnership adoption in solid waste management in rural China, International Journal of Environmental Research and Public Health, vol. 17, no. 15, pp. 1-14. [CrossRef]

- Kumar, N., 2019, Determinants of Public Private Partnerships in Infrastructure: A Study of Developing Countries. Journal of Commerce and Accounting Research, vol. 8, no. 2, pp. 79-85.

- Kasri, R. A., and Wibowo, F. A., 2015, Determinants of Public Private Partnerships in Infrastructure provision: Evidence from Muslim developing countries. Journal of Economic Cooperation and Development, vol. 36, no. 2, pp. 1-34.

- Marozva, G. and Makoni, P.L., 2018, Foreign direct investment, infrastructure development and economic growth in African economies, Acta Universitatis Danubius. Œconomica, vol.14, no. 6.

- Chikaza, Z. and Simatele, M., 2021, Private financing for infrastructural development: a search for determinants in public–private partnerships in SSA. Acta Universitatis Danubius. Œconomica, vol. 17, no. 6, pp. 170-188.

- Telang, V. and Prakash, S., 2015, Financing of public private partnerships in India (sources, problems and challenges). Research front, vol. 3, no. 1, 49-62.

- Kamau P., 2016, Commercial Banks and Economic Infrastructure PPP Projects in Kenya: Experience and Prospects. KBA Centre for Research on Financial Markets and Policy Working Papers Series WPS/01, 16. Available from https://www.kba.co.ke/downloads/Working%20Paper%20WPS-01-16.pdf (Accessed: 11 August 2021).

- Banerjee, S. G., Rondinelli, D. A. and Koo, J. 2003. Decentralisation’s Impact on Private Participation in Infrastructure in Developing Countries. Working Paper. Chapel Hill, NC: University of North Carolina. [CrossRef]

- Sahni, H., Nsiah, C. and Fayissa, B., 2021. Institutional quality, infrastructure, and economic growth in Africa. Journal of African Development, vol. 22, no. 1, pp.7-37. [CrossRef]

- Nxumalo I. S., 2020. International capital inflows in emerging markets: the role of institutions. (Masters’ dissertation). University of South Africa. Available at: dissertation_nxumalo_is.pdf (unisa.ac.za).

- Nxumalo, I.S., and Makoni, P.L., 2021, Analysis of International Capital Inflows and Institutional Quality in Emerging Markets. Economies, vol. 9, no. 4, pp.179. [CrossRef]

- Brooks, C., 2008. Introductory Econometrics for finance, Cambridge University.

- Mundonde, J. and Makoni, P.L., 2023. Public private partnerships and water and sanitation infrastructure development in Zimbabwe: what determines financing?. Environmental Systems Research, vol. no.1, pp. 14. [CrossRef]

- Wooldridge, J.M., 1989. A computationally simple heteroskedasticity and serial correlation robust standard error for the linear regression model. Economics letters, vol. 31. No. 33, pp.239-243. [CrossRef]

- Nakatani R., 2017, Structural vulnerability and resilience to currency crisis: Foreign currency debt versus export, The North American Journal of Economics and Finance, vol. 42, no. 1, pp. 132-143. [CrossRef]

- Kavila, W. and Le Roux, P., 2016, Inflation dynamics in a dollarised economy, The case of Zimbabwe, Southern African Business Review, vol. 20, no. 1, pp.94-117.

- Chan, A.P., Lam, P.T., Wen, Y., Ameyaw, E.E., Wang, S. and Ke, Y., 2015, Cross-sectional analysis of critical risk factors for PPP water projects in China. Journal of Infrastructure Systems. vol.24, no.1, pp. 401-403. [CrossRef]

- Maposa, L. and Munanga, Y., 2021, Public-private partnerships development finance model in Zimbabwe infrastructure projects, Open Access Library Journal, vol. 8, no. 4, pp.1-24. [CrossRef]

- RBZ (Reserve Bank of Zimbabwe) 2020, Monetary policy statement. Available at: https://www.rbz.co.zw/index.php/monetary-policy/monetary-policy-statements (Accessed: 18 November 2022).

- Chitongo L., 2017, Public private partnerships and housing provision in Zimbabwe: The case of Runyararo South West housing scheme (Mbudzi) Masvingo. European Journal of Research in Social Sciences , vol. 5, pp. 17-29. http://localhost:8080/xmlui/handle/123456789/295.

- Goksu, A., Trémolet, S., Kolker, J.E., 2017. Easing the transition to commercial financing for sustainable water and sanitation. Available at: Easing the Transition to Commercial Finance for Sustainable Water and Sanitation (oecd.org) (accessed 04 April 2023).

- Rozenberg, J. and Fay, M. eds., 2019, Beyond the gap: How countries can afford the infrastructure they need while protecting the planet. World Bank Publications. Available at: http://documents.worldbank.org/curated/en/189471550755819133/Beyond-the-Gap-How-Countries-Can-Afford-the-Infrastructure-They-Need-while-Protecting-the-Planet (Accessed 18 November 2022).

- AfDB (African development bank). 2019, Zimbabwe Infrastructure report. Available at: https://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-and Operations/Zimbabwe_Infrastructure_Report_2019_-_AfDB.pdf.

- Humphreys, E., van der Kerk, A. and Fonseca, C., 2018. Public finance for water infrastructure development and its practical challenges for small towns. Water Policy, vol. 20, no. 1, pp. 100-111. [CrossRef]

Figure 1.

Conceptual framework.

Figure 2.

Framework model for financing water and sanitation infrastructure in Zimbabw.

Table 1.

Explanatory variables.

| Variable | Indicator | Data source | Reference |

|---|---|---|---|

| GDPP | GDP per capita | World Bank WDI database | [35,48,49] |

| IRIMP | International reserves to imports ratio | World Bank WDI database | [49,50,59] |

| INF | Consumer price index | World Bank WDI database, Reserve Bank of Zimbabwe | [35,49,50,60] |

| FDI | Net FDI to GDP (%) | World Bank WDI database | [61,62] |

| SMC | Stock market capitalisation to GDP (%) | World Bank WDI database | [51,52] |

| DBC | Domestic bank credit to GDP (%) | World Bank WDI database | [51,52] |

| BCD | Bank credit to bank deposits (%) | Reserve Bank of Zimbabwe | [58] |

| NPL | Non-performing loans to bank assets (%) | Reserve Bank of Zimbabwe | [35,63,64] |

| CC | Control of corruption percentile rank | World Bank WGI database | [48,53,65,67] |

| RQ | Regulatory quality percentile rank | World Bank WGI database | [56,65,66,67] |

| RL | Rule of law percentile rank | World Bank WGI database | [48,53,67,68] |

| VA | Voice and accountability percentile rank | World Bank WGI database | [55,56,65,67,68] |

| PS | Political stability percentile rank | World Bank WGI database | [48,65,66,68] |

| GE | Government effectiveness percentile rank | World Bank WGI database | [48,56,65,67,68] |

Source: Authors’ own conceptualisation.

Table 2.

Tobit regression estimates.

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 |

|---|---|---|---|---|---|---|---|

| ΔlogGDPP | -2.0335* | -2.3409* | -0.9765 | -0.4760 | -1.5471 | -2.1273** | -0.7663 |

| (1.1927) | (-1.866) | (1.573) | (2.2012) | (1.2456) | (1.0908) | (1.6072) | |

| ΔIRIMP | -0.0181 | -0.0043 | -0.1268 | -0.1890 | -0.0222 | -0.0194 | -0.1302 |

| (0.1200) | (-0.0422) | (0.162) | (0.2255) | (0.1180) | (0.1217) | (0.1617) | |

| ΔlogIFN | -0.0368 | -0.0266 | -0.061 | -0.0456 | -0.0795 | -0.0152 | -0.0746 |

| (0.1039) | (-0.2514) | (0.110) | (0.1006) | (0.1273) | (0.1109) | (0.1187) | |

| ΔlogFDI | -0.391*** | -0.389*** | -0.395** | -0.3037** | -0.433*** | -0.3579** | -0.363*** |

| (0.1351) | (-2.7217) | (0.122) | (0.1523) | (0.1260) | (0.1587) | (0.1291) | |

| ΔSMC | 0.0083*** | 0.0087*** | 0.0071** | 0.0071*** | 0.0076*** | 0.0083*** | 0.0069*** |

| (0.0018) | (3.7934) | (0.002) | (0.00239) | (0.0020) | (0.0018) | (0.0022) | |

| ΔDBC | -0.020*** | -0.019*** | -0.02*** | -0.022*** | -0.019*** | -0.020*** | -0.0181** |

| (0.0066) | (-3.2793) | (0.006) | (0.0066) | (0.0064) | (0.0076) | (0.0073) | |

| ΔBCD | 0.0234*** | 0.0238*** | 0.023*** | 0.0231*** | 0.0246*** | 0.0218*** | 0.0244*** |

| (0.0073) | (3.0830) | (0.006) | (.006071) | (0.0074) | (0.0069) | (0.0071) | |

| ΔNPL | -0.068*** | -0.061*** | -0.09*** | -0.087*** | -0.084*** | -0.064*** | -0.076*** |

| (0.0158) | (-3.0704) | (0.023) | (0.0241) | (0.0253) | (0.0193) | (0.0180) | |

| ΔCC | 0.0178 | ||||||

| (0.5068) | |||||||

| ΔRQ | -0.068 | ||||||

| (0.049) | |||||||

| ΔRL | -0.06097 | ||||||

| (0.0586) | |||||||

| ΔVA | -0.0539 | ||||||

| (0.0595) | |||||||

| ΔPS | 0.0127 | ||||||

| (0.0366) | |||||||

| ΔGE | -0.04758 | ||||||

| (0.0344) |

1%, 5%, 10% significance level is represented by ***, ** and * respectively. Source: authors’ own computations.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.